fm1 solutions

DESCRIPTION

FM practice exam solutionsTRANSCRIPT

© 2007 The Infinite Actuary, LLC 1 Joint Exam 2/FM (Sample Exam)

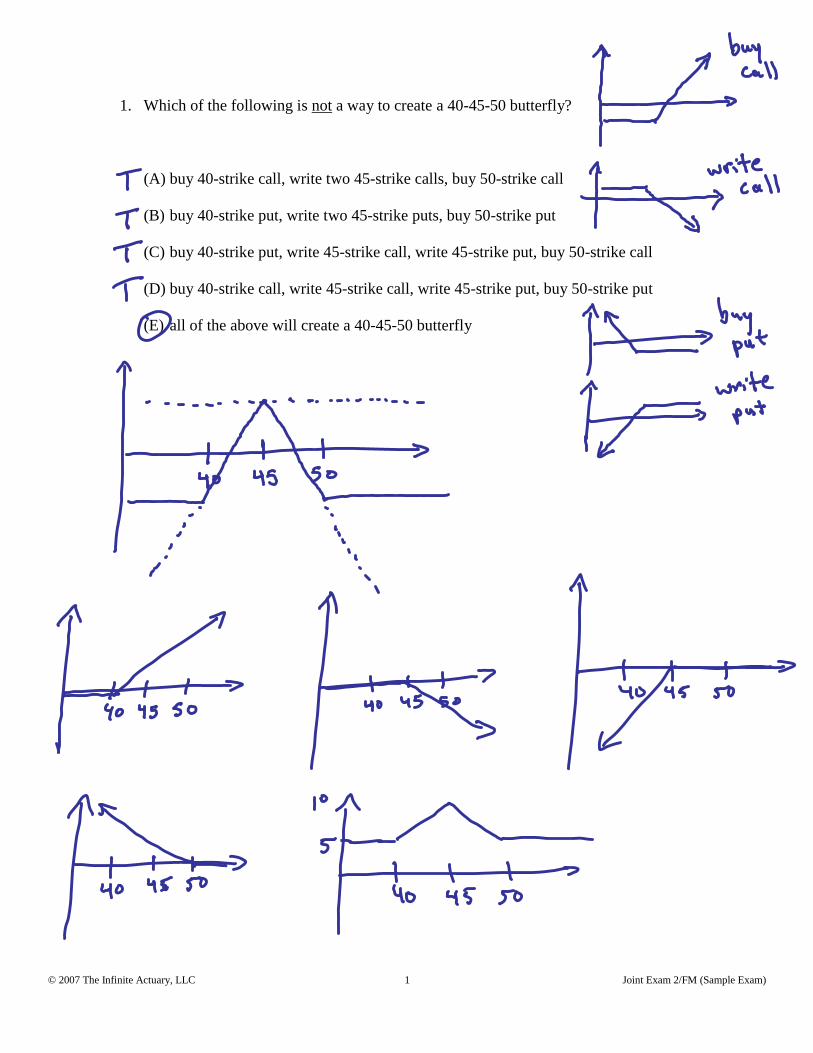

1. Which of the following is not a way to create a 40-45-50 butterfly?

(A) buy 40-strike call, write two 45-strike calls, buy 50-strike call

(B) buy 40-strike put, write two 45-strike puts, buy 50-strike put

(C) buy 40-strike put, write 45-strike call, write 45-strike put, buy 50-strike call

(D) buy 40-strike call, write 45-strike call, write 45-strike put, buy 50-strike put

(E) all of the above will create a 40-45-50 butterfly

© 2007 The Infinite Actuary, LLC 2 Joint Exam 2/FM (Sample Exam)

2. Let 1

, 0 154t t

t

What is the first year for which the effective rate of discount is less than 12.5?

(A) 3

(B) 4

(C) 5

(D) 6

(E) 7

© 2007 The Infinite Actuary, LLC 3 Joint Exam 2/FM (Sample Exam)

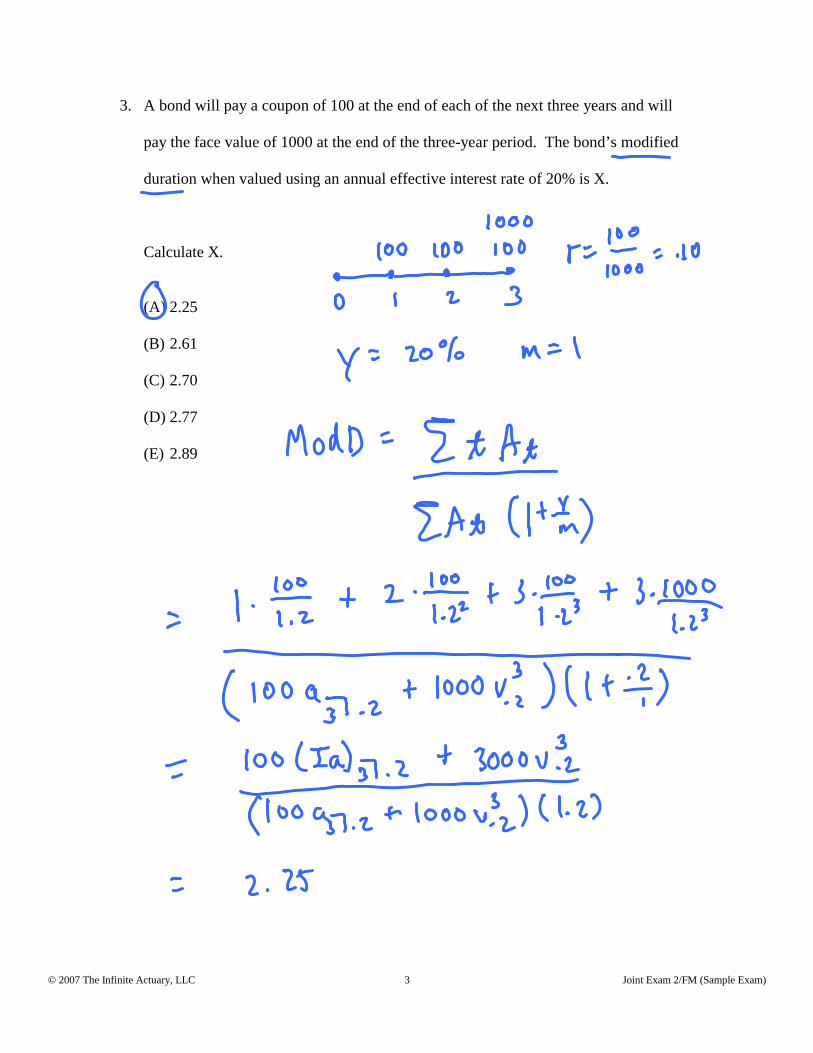

3. A bond will pay a coupon of 100 at the end of each of the next three years and will

pay the face value of 1000 at the end of the three-year period. The bond’s modified

duration when valued using an annual effective interest rate of 20% is X.

Calculate X.

(A) 2.25

(B) 2.61

(C) 2.70

(D) 2.77

(E) 2.89

© 2007 The Infinite Actuary, LLC 4 Joint Exam 2/FM (Sample Exam)

4. You are given the following table of interest rates:

Calendar Year of Original

Investment

Portfolio Rates(in %)

y

1992 8.25 8.25 8.40 8.50 8.50 8.351993 8.50 8.70 8.75 8.90 9.00 8.601994 9.00 9.00 9.10 9.10 9.20 8.851995 9.00 9.10 9.20 9.30 9.40 9.101996 9.25 9.35 9.50 9.55 9.60 9.351997 9.50 9.50 9.60 9.70 9.701998 10.00 10.00 9.90 9.801999 10.00 9.80 9.702000 9.50 9.502001 9.00

Investment Year Rates (in %)

1yi 2

yi 3yi 4

yi 5yi 5yi

A person deposits 1000 on January 1, 1997. Let the following be the accumulated

value of the 1000 on January 1, 2000.

P: under the investment year method

Q: under the portfolio yield method

Calculate P + Q.

(A) 2575

(B) 2595

(C) 2610

(D) 2655

(E) 2700

© 2007 The Infinite Actuary, LLC 5 Joint Exam 2/FM (Sample Exam)

5. A loan is repaid with 10 annual payments. The first payment occurs one year after

the loan. The first payment is 100 and each subsequent payment increases by 10.

The annual effective rate of interest is 5%. The amount of principal repaid in the 4th

payment is X.

Determine X.

(A) 71

(B) 76

(C) 80

(D) 84

(E) 91

© 2007 The Infinite Actuary, LLC 6 Joint Exam 2/FM (Sample Exam)

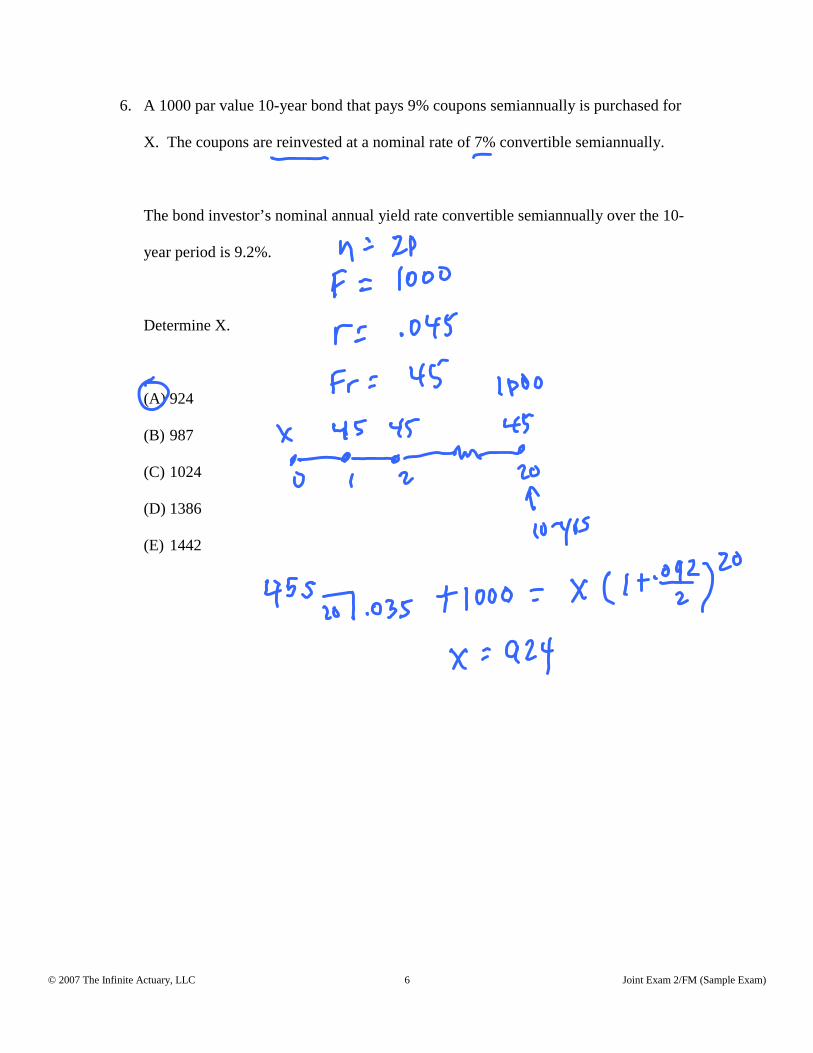

6. A 1000 par value 10-year bond that pays 9% coupons semiannually is purchased for

X. The coupons are reinvested at a nominal rate of 7% convertible semiannually.

The bond investor’s nominal annual yield rate convertible semiannually over the 10-

year period is 9.2%.

Determine X.

(A) 924

(B) 987

(C) 1024

(D) 1386

(E) 1442

© 2007 The Infinite Actuary, LLC 7 Joint Exam 2/FM (Sample Exam)

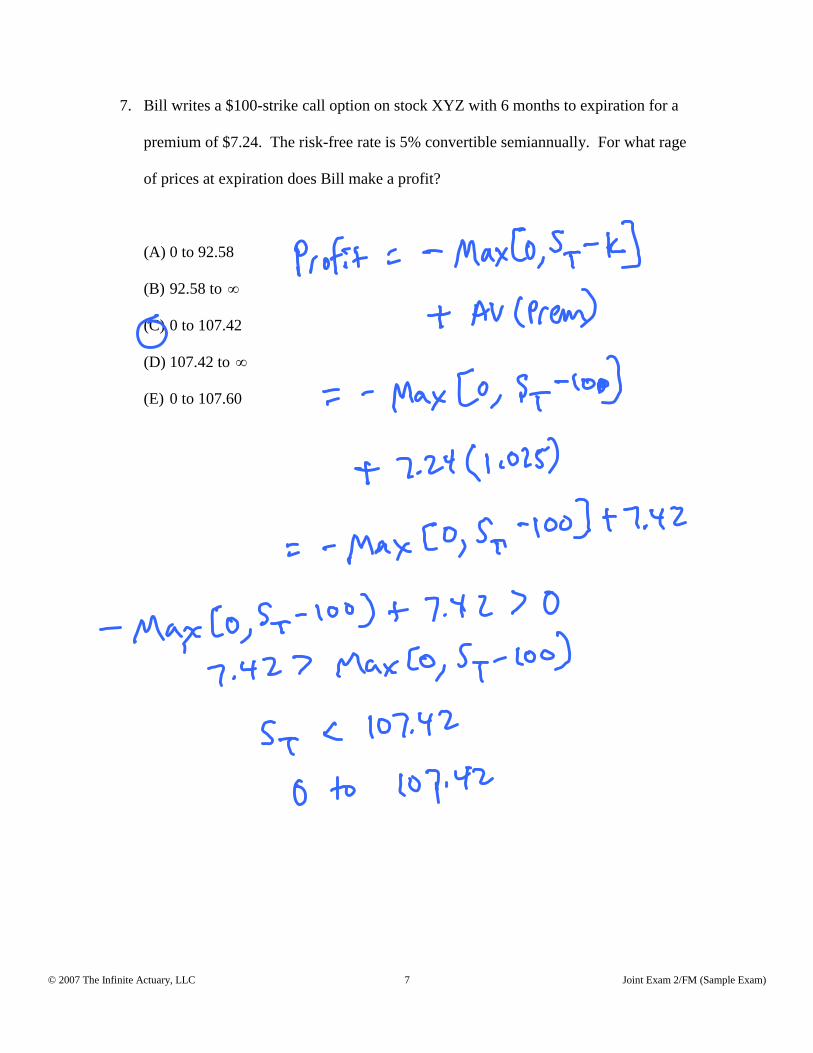

7. Bill writes a $100-strike call option on stock XYZ with 6 months to expiration for a

premium of $7.24. The risk-free rate is 5% convertible semiannually. For what rage

of prices at expiration does Bill make a profit?

(A) 0 to 92.58

(B) 92.58 to

(C) 0 to 107.42

(D) 107.42 to

(E) 0 to 107.60

© 2007 The Infinite Actuary, LLC 8 Joint Exam 2/FM (Sample Exam)

8. 10 deposits of $2000 are made every other year with the first deposit made

immediately. The resulting fund is used to buy a perpetuity with payments made

once every 3 years following the pattern X, 4X, 7X, 10X, …. The first perpetuity

payment is made 3 years after the last deposit of $2000. The annual effective rate of

interest is 6%.

Determine X.

(A) 408

(B) 458

(C) 471

(D) 512

(E) 603

© 2007 The Infinite Actuary, LLC 9 Joint Exam 2/FM (Sample Exam)

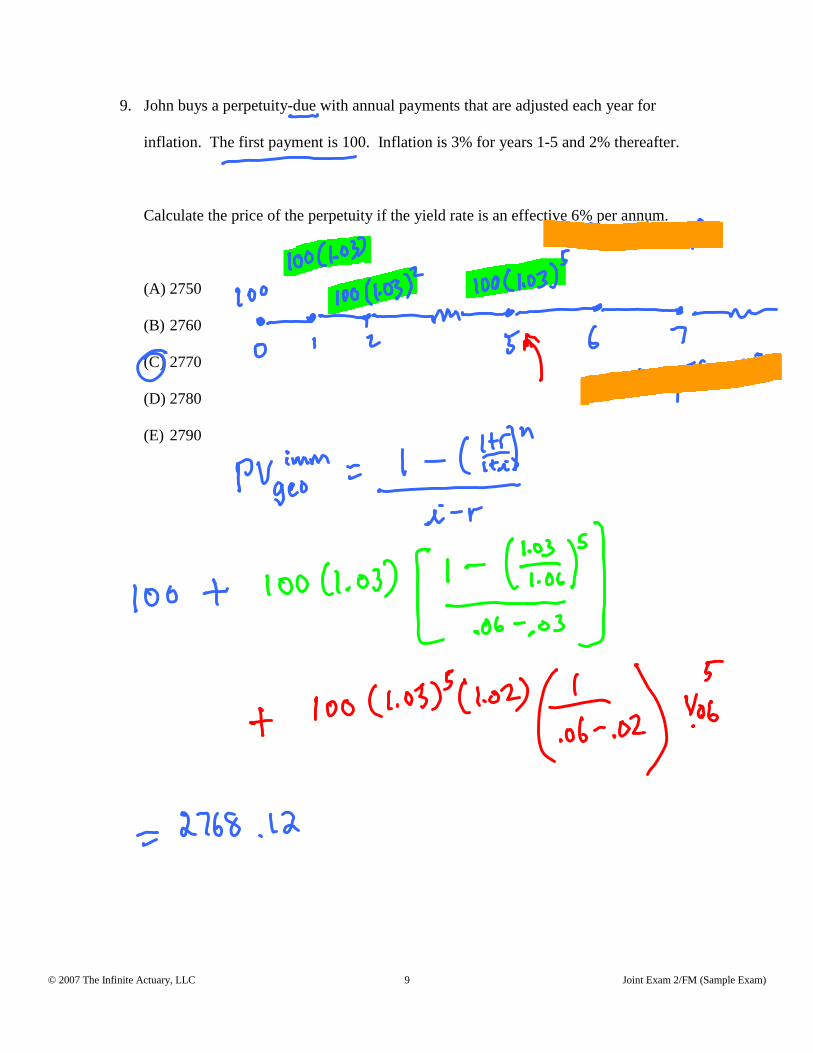

9. John buys a perpetuity-due with annual payments that are adjusted each year for

inflation. The first payment is 100. Inflation is 3% for years 1-5 and 2% thereafter.

Calculate the price of the perpetuity if the yield rate is an effective 6% per annum.

(A) 2750

(B) 2760

(C) 2770

(D) 2780

(E) 2790

© 2007 The Infinite Actuary, LLC 10 Joint Exam 2/FM (Sample Exam)

10. Given the following information about the treasury market:

Term Coupon Price1 0% 96.622 0% X3 0% 88.9

It is known that the 2-year forward rate is 4.5%.

Calculate X.

(A) 87.65

(B) 89.70

(C) 92.90

(D) 93.45

(E) 95.50

© 2007 The Infinite Actuary, LLC 11 Joint Exam 2/FM (Sample Exam)

11. A 20-year bond is priced at par and pays R% coupons semiannually. The bond’s

duration is 13.95 years.

Determine R.

(A) 2

(B) 3

(C) 4

(D) 5

(E) 6

© 2007 The Infinite Actuary, LLC 12 Joint Exam 2/FM (Sample Exam)

12. Which of the following is not true?

(A) An asset insured with a floor is equivalent to investing in a zero-coupon bond and

buying a call option on the asset.

(B) A short position insured with a cap is equivalent to writing a zero-coupon bond

and buying a put option on the asset.

(C) A covered written call is equivalent to investing in a zero-coupon bond and

writing a put option on the asset.

(D) A covered written put is equivalent to writing a zero-coupon bond and writing a

call option on the asset.

(E) All of the above are true.

© 2007 The Infinite Actuary, LLC 13 Joint Exam 2/FM (Sample Exam)

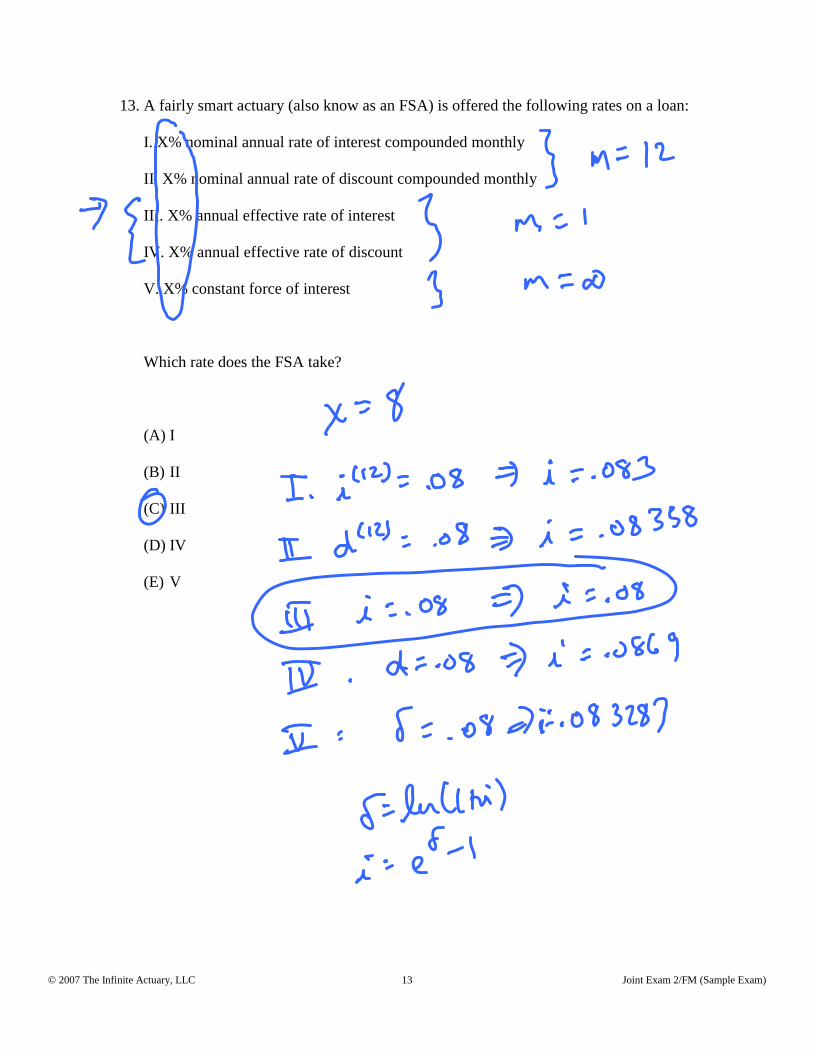

13. A fairly smart actuary (also know as an FSA) is offered the following rates on a loan:

I. X% nominal annual rate of interest compounded monthly

II. X% nominal annual rate of discount compounded monthly

III. X% annual effective rate of interest

IV. X% annual effective rate of discount

V. X% constant force of interest

Which rate does the FSA take?

(A) I

(B) II

(C) III

(D) IV

(E) V

© 2007 The Infinite Actuary, LLC 14 Joint Exam 2/FM (Sample Exam)

14. An annuity pays 1 at the beginning of each year for n years. Using an annual

effective interest rate of i, the present value of the annuity at time 0 is 8.55948. It is

also known that 1 3.172169n

i .

Find the accumulated value of the annuity immediately after the last payment.

(A) 27.152

(B) 28.456

(C) 29.513

(D) 30.765

(E) 31.973

© 2007 The Infinite Actuary, LLC 15 Joint Exam 2/FM (Sample Exam)

15. Deposits are made at the beginning of every month into a fund earning a nominal

annual rate of 6% convertible monthly. The first deposit is 100 and deposit increase

2% every year. In other words, deposits 1-12 are 100, deposits 13-24

are100 1.02 102 , deposits 25-36 are 2100 1.02 104.04 , and so on.

Calculate the fund balance at the end of 10 years.

(A) 16,569

(B) 16,893

(C) 17,257

(D) 17,770

(E) 17,859

© 2007 The Infinite Actuary, LLC 16 Joint Exam 2/FM (Sample Exam)

16. On January 1 a fund has a balance of $100. Sometime during the year a withdrawal

of $20 is made. Immediately before the withdrawal the fund balance is $110. At

year-end the balance is $95.

If the time weighted and dollar weighted rates for the year are equal, then in what

month was the $20 withdrawal made?

(A) June

(B) July

(C) August

(D) September

(E) October

© 2007 The Infinite Actuary, LLC 17 Joint Exam 2/FM (Sample Exam)

17. A common stock pays annual dividends at the end of each year. The earnings per

share in the year just ended were J. Earnings are assumed to grow 10% per year in

the future. The percentage of earnings paid out as a dividend will be 0% for the next

5 years and 50% thereafter.

Calculate the theoretical price of the stock to yield the investor 21%.

(A) 4

5

1.1

J

(B) 5

5

1.1

J

(C) 6

5

1.1

J

(D) 5

10

1.1

J

(E) 6

10

1.1

J

© 2007 The Infinite Actuary, LLC 18 Joint Exam 2/FM (Sample Exam)

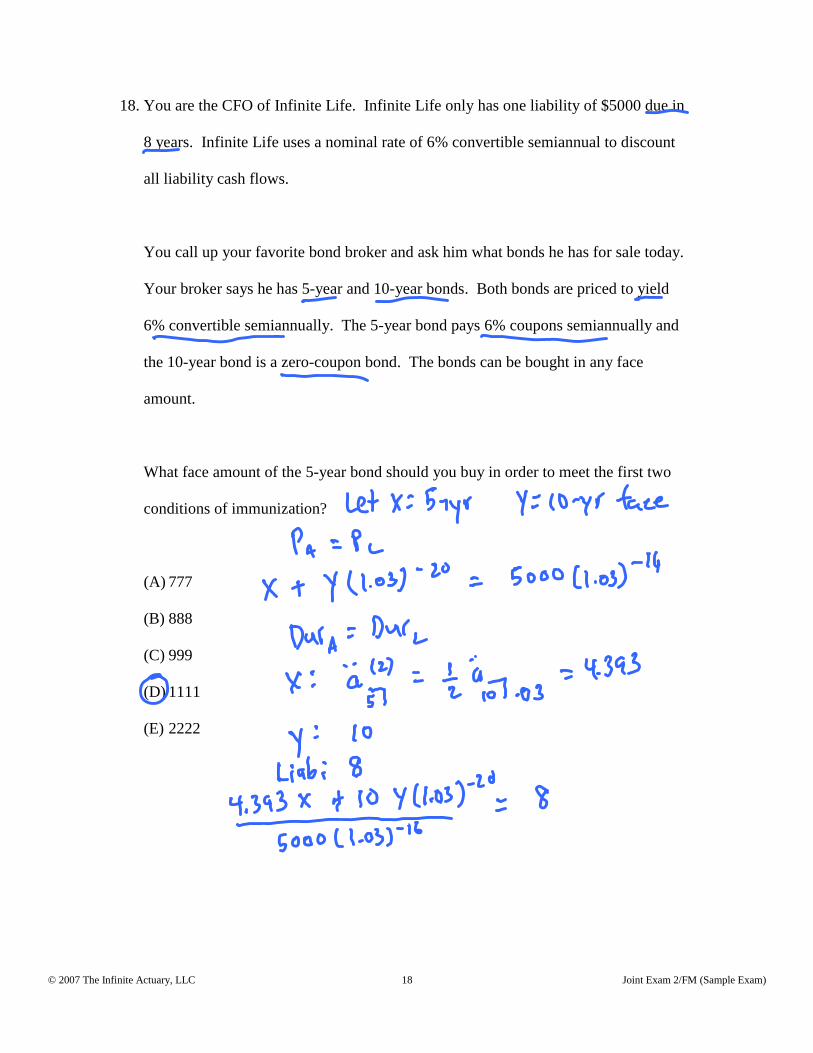

18. You are the CFO of Infinite Life. Infinite Life only has one liability of $5000 due in

8 years. Infinite Life uses a nominal rate of 6% convertible semiannual to discount

all liability cash flows.

You call up your favorite bond broker and ask him what bonds he has for sale today.

Your broker says he has 5-year and 10-year bonds. Both bonds are priced to yield

6% convertible semiannually. The 5-year bond pays 6% coupons semiannually and

the 10-year bond is a zero-coupon bond. The bonds can be bought in any face

amount.

What face amount of the 5-year bond should you buy in order to meet the first two

conditions of immunization?

(A) 777

(B) 888

(C) 999

(D) 1111

(E) 2222

© 2007 The Infinite Actuary, LLC 19 Joint Exam 2/FM (Sample Exam)

19. You are given the following prices for $100 zero-coupon bonds:

Term Price1 95.242 89.003 81.63

R is the swap rate in a 3-year swap contract.

Determine R.

(A) 5.7%

(B) 6.1%

(C) 6.5%

(D) 6.9%

(E) 7.2%

© 2007 The Infinite Actuary, LLC 20 Joint Exam 2/FM (Sample Exam)

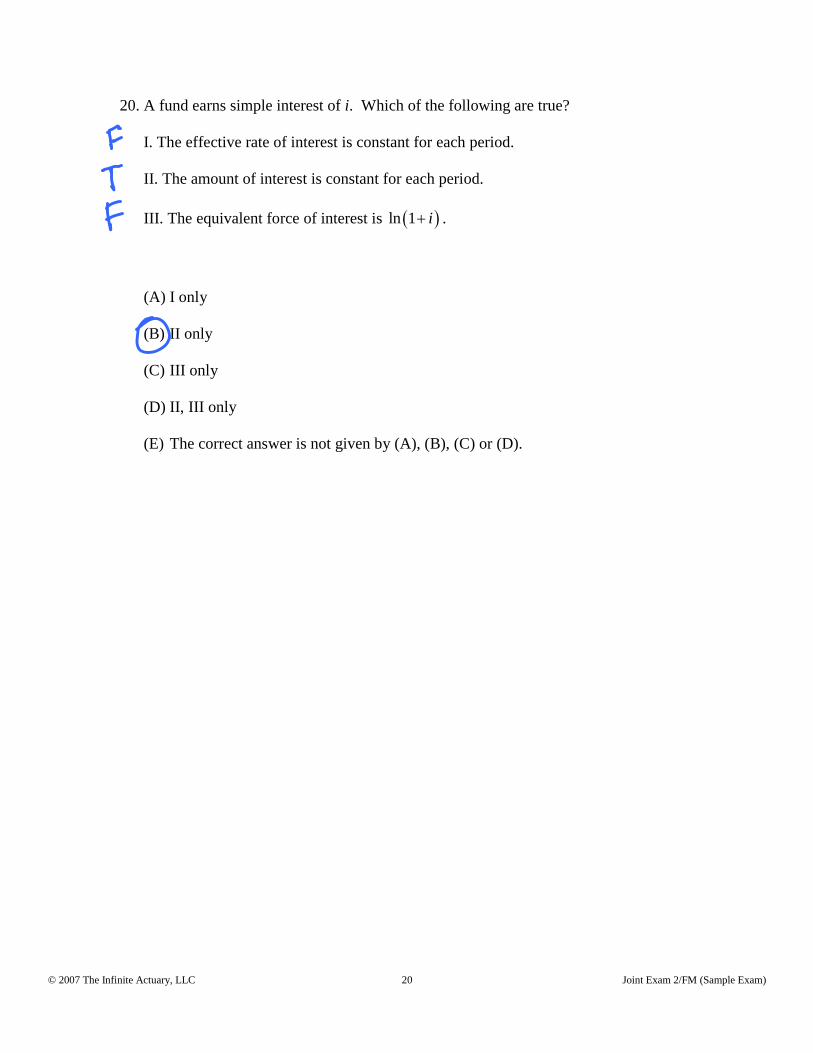

20. A fund earns simple interest of i. Which of the following are true?

I. The effective rate of interest is constant for each period.

II. The amount of interest is constant for each period.

III. The equivalent force of interest is ln 1 i .

(A) I only

(B) II only

(C) III only

(D) II, III only

(E) The correct answer is not given by (A), (B), (C) or (D).

© 2007 The Infinite Actuary, LLC 21 Joint Exam 2/FM (Sample Exam)

21. If 2, 0 and 13.03567.

1t n

tt Ia

t

Determine n.

(A) 10

(B) 11

(C) 12

(D) 13

(E) 14

© 2007 The Infinite Actuary, LLC 22 Joint Exam 2/FM (Sample Exam)

22. You are given the following information about 3 funds:

FundEffective Rate

per YearInterest Payments

A j % paid directly to investor

B 5% paid directly to investor

C 4% automatically reinvested

An investor deposits $10,000 into fund A. He reinvests fund A’s interest payments

into fund B. He reinvests fund B’s interest payments into fund C. The total value of

all three funds after 10 years is $20,000.

Determine j.

(A) 6

(B) 7

(C) 8

(D) 9

(E) 10

© 2007 The Infinite Actuary, LLC 23 Joint Exam 2/FM (Sample Exam)

23. Which of the following are true?

I. Modified duration is greater for bonds with higher par values.

II. Modified duration is greater for yields compound more frequently.

III. The modified duration of a single cash flow is the time remaining until the cash

flow.

(A) I only

(B) II only

(C) III only

(D) II, III only

(E) The correct answer is not given by (A), (B), (C) or (D).

© 2007 The Infinite Actuary, LLC 24 Joint Exam 2/FM (Sample Exam)

24. An annuity-immediate has the following payments:

10, 20, 30, 40, 50, 40, 30, 20, 10

Which of the following expressions represents the present value of the annuity?

(A) 5 5

10a a

(B) 5 5

10a a

(C) 5 4

10a a

(D) 5 4

10a a

(E) 5 410 10Ia Da

© 2007 The Infinite Actuary, LLC 25 Joint Exam 2/FM (Sample Exam)

25. You are given the following term structure of interest rates.

Term(in years) Spot Rate

1 5.00%2 5.75%3 6.25%4 6.50%

Calculate 41000 Da rounded to the nearest 100.

(A) 8700

(B) 8800

(C) 8900

(D) 9000

(E) 9100

© 2007 The Infinite Actuary, LLC 26 Joint Exam 2/FM (Sample Exam)

26. Suppose you desire to short-sale 200 shares of ABC stock, which has a bid price of

$24.82 and an ask price of $25.01. You cover the short position three months later

when the bid price is $21.45 and the ask price is $21.64.

Your broker charges a 0.3% commission to engage in the short-sale and a 0.3%

commission to close the position. He also requires a 50% haircut on the net proceeds

of the short-sale. The market rate of interest is 6% convertible continuously and the

short-rebate on the haircut is 4% convertible continuously. No dividends were paid

on the stock during the three months.

Calculate the profit on the short-sale.

(A) 595.60

(B) 608.13

(C) 652.33

(D) 671.50

(E) 684.12

© 2007 The Infinite Actuary, LLC 27 Joint Exam 2/FM (Sample Exam)

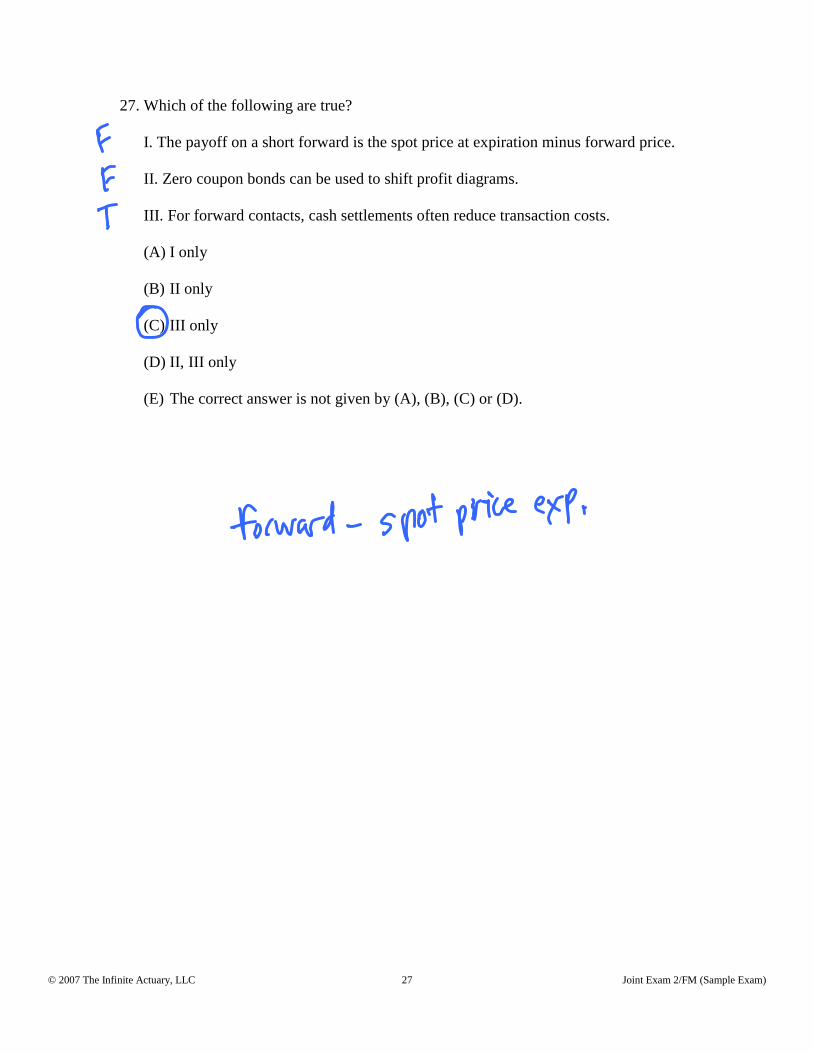

27. Which of the following are true?

I. The payoff on a short forward is the spot price at expiration minus forward price.

II. Zero coupon bonds can be used to shift profit diagrams.

III. For forward contacts, cash settlements often reduce transaction costs.

(A) I only

(B) II only

(C) III only

(D) II, III only

(E) The correct answer is not given by (A), (B), (C) or (D).

© 2007 The Infinite Actuary, LLC 28 Joint Exam 2/FM (Sample Exam)

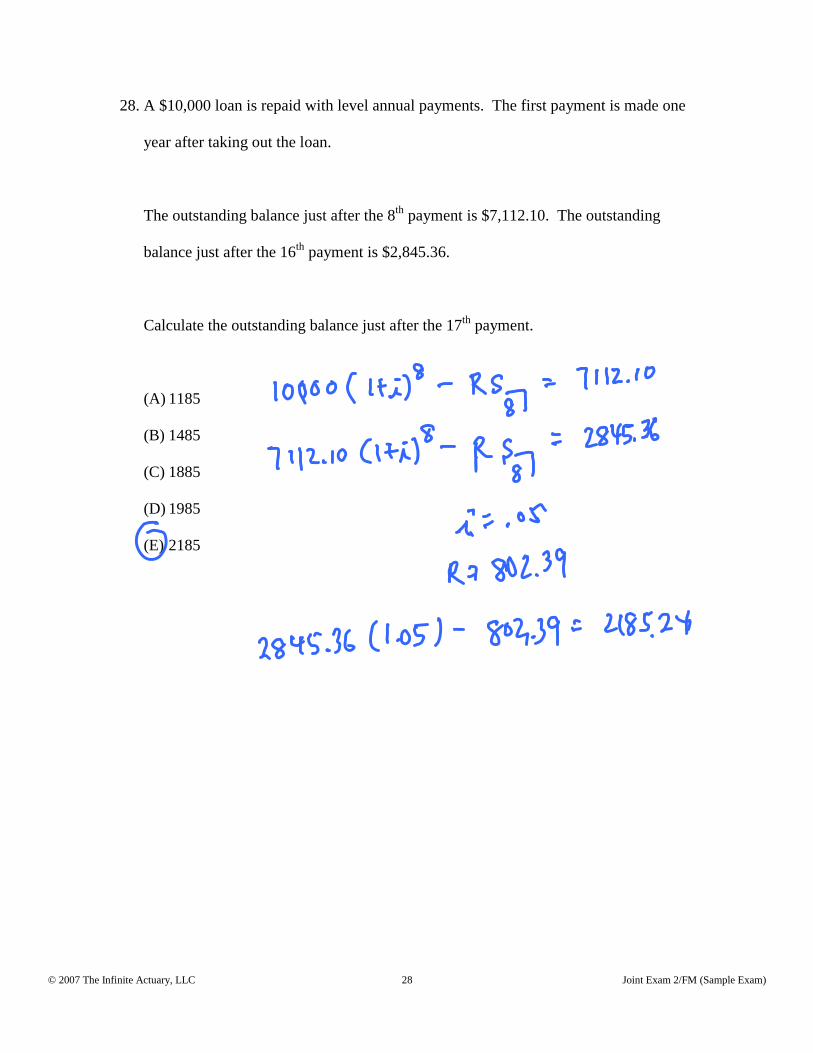

28. A $10,000 loan is repaid with level annual payments. The first payment is made one

year after taking out the loan.

The outstanding balance just after the 8th payment is $7,112.10. The outstanding

balance just after the 16th payment is $2,845.36.

Calculate the outstanding balance just after the 17th payment.

(A) 1185

(B) 1485

(C) 1885

(D) 1985

(E) 2185

© 2007 The Infinite Actuary, LLC 29 Joint Exam 2/FM (Sample Exam)

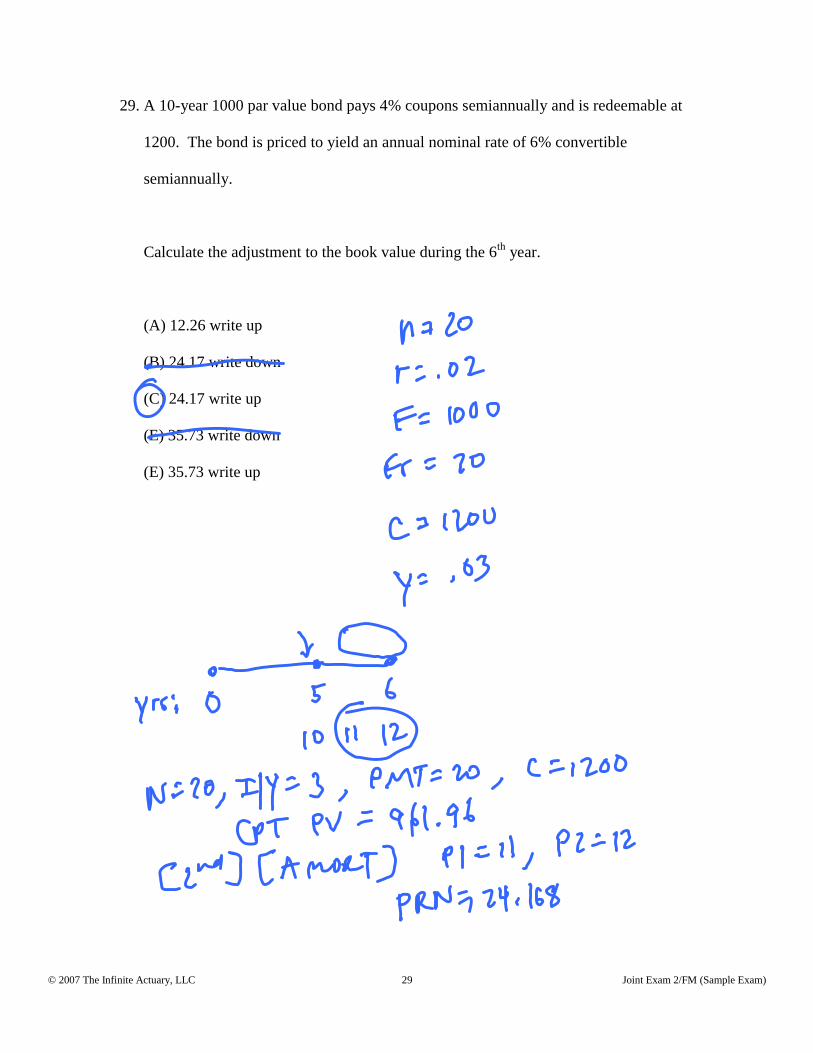

29. A 10-year 1000 par value bond pays 4% coupons semiannually and is redeemable at

1200. The bond is priced to yield an annual nominal rate of 6% convertible

semiannually.

Calculate the adjustment to the book value during the 6th year.

(A) 12.26 write up

(B) 24.17 write down

(C) 24.17 write up

(E) 35.73 write down

(E) 35.73 write up

© 2007 The Infinite Actuary, LLC 30 Joint Exam 2/FM (Sample Exam)

30. The present value of a 25-year annuity-immediate with a first payment of $2500 and

decreasing by X each year thereafter is $15,923. The annual effective rate of interest

is 10%.

Determine X.

(A) 70

(B) 80

(C) 90

(D) 100

(E) 110

© 2007 The Infinite Actuary, LLC 31 Joint Exam 2/FM (Sample Exam)

31. Which of the following expression does not represent a definition for |m na ?

(A) m

nv a

(B) m n m

a a

(C) m n

nv s

(D) 1m m m nv v v

(E) All of the above represent a definition for |m na .

FM Sample Exam #1 SolutionsLast updated December 7, 2009

32.

(1 + i)x = 5

2(1 + i)y = 8

(1 + i)y = 4

3(1 + i)z = 20

(1 + i)z =20

3

12(1 + i)3x−2y+z =12 [(1 + i)x]3 (1 + i)z

[(1 + i)y]2=

12(5)3(20

3

)(4)2 = 625

33. After the 3 years of interest only payments the balance is still 100,000 so wesolve

100,000 = 1500an 0.01

Using the calculator we get 111 payments plus the 3 years of interest only paymentsequals 111 + 3(12) = 147 payments.

34. The sinking fund payment is

Rs25 0.04 = 10,000

R = 240.12

The interest payment is10,000× 0.05 = 500

The sinking fund balance at time 11 is

240.12s11 0.04 = 3238.34

c©2008 The Infinite Actuary, LLC FM Sample Exam #1 Solutions

So the interest earned on the sinking fund during the 12th year is

3238.34× 0.04 = 129.53

And the net interest paid is

500− 129.53 = 370.47

The increment in the sinking fund for the 8th year is

240.12s8 0.04 − 240.12s7 0.04 = 315.98

Finally the sum of these two items are

370.47 + 315.98 = 686.45

35. Using Put-Call Parity

Call(K, T )− Put(K, T ) = PV(F0,T −K)

93.809− 74.201 =F0,0.5 − 1000

1.02

F0,0.5 = 1020

c©2008 The Infinite Actuary, LLC FM Sample Exam #1 Solutions