fixed income and money market instu_final

TRANSCRIPT

FIXED INCOME AND MONEY FIXED INCOME AND MONEY MARKET INSTRUMENTSMARKET INSTRUMENTS

BondsBonds

DefinitionDefinition

A A bondbond is a debt security, in which the issuer is a debt security, in which the issuer owes the holders a debt and is obliged to repay owes the holders a debt and is obliged to repay the principal and interest (the coupon).the principal and interest (the coupon).

Bonds are generally issued for a fixed term (the Bonds are generally issued for a fixed term (the

maturity) longer than one year.maturity) longer than one year.

Features of BondFeatures of Bond Issued by public authorities, credit institutions, Issued by public authorities, credit institutions,

companies and supranational institutions in the companies and supranational institutions in the primary markets.primary markets.

Issued through underwriting,auctioningIssued through underwriting,auctioning..

The return on a bond is composed of three The return on a bond is composed of three elements: elements:

Interest paid on the bond - the coupon Interest paid on the bond - the coupon Return on interest paid on the bond that is reinvested - i.e. Return on interest paid on the bond that is reinvested - i.e.

interest on interest interest on interest The capital gain or loss on the bond in terms of its price.The capital gain or loss on the bond in terms of its price.

A bond’s price and a bond’s yield are inversely A bond’s price and a bond’s yield are inversely related. related.

Features of Bond-Cont.Features of Bond-Cont.

Nominal, principal or face amountNominal, principal or face amount . .

Issue price - The price at which investors buy the bonds when Issue price - The price at which investors buy the bonds when they are first issued.they are first issued.

Maturity date - The date on which the issuer has to repay the Maturity date - The date on which the issuer has to repay the nominal amount.nominal amount.

Coupon - The interest rate that the issuer pays to the bond Coupon - The interest rate that the issuer pays to the bond holders.holders.

Optionality - A bond may contain an embedded option.Optionality - A bond may contain an embedded option.

Callability - Some bonds give the issuer the right to repay the Callability - Some bonds give the issuer the right to repay the bond before the maturity date on the call dates. This is mainly the bond before the maturity date on the call dates. This is mainly the case for high-yield bonds.case for high-yield bonds.

Puttability - Some bonds give the bond holder the right to force Puttability - Some bonds give the bond holder the right to force the issuer to repay the bond before the maturity date on the put the issuer to repay the bond before the maturity date on the put datesdates

Bond Interest CalculationsBond Interest Calculations

Purchase Interest/Sale Interest – When any bond is Purchase Interest/Sale Interest – When any bond is purchased/sold generally it is done cum interest. In purchased/sold generally it is done cum interest. In case of purchase of Bond the interest paid by buyer case of purchase of Bond the interest paid by buyer is known is Purchase Interest. In case of sale the is known is Purchase Interest. In case of sale the interest received by seller is known as sell interest. interest received by seller is known as sell interest.

It is calculated from the last day the bond paid It is calculated from the last day the bond paid interest up to but not including Settle Dateinterest up to but not including Settle Date

Interest accrual is getting started on a daily basis on Interest accrual is getting started on a daily basis on Settle DateSettle Date

It gets stopped accruing on day before Maturity DateIt gets stopped accruing on day before Maturity Date Bondholder receive Coupon and Principal on Bondholder receive Coupon and Principal on

Maturity DateMaturity Date

ExampleExample

Buy: 50,000,000 US Treasury Bond 7.25% Buy: 50,000,000 US Treasury Bond 7.25% 05/15/1005/15/10

Price: 96.3125 (par 100, price on % terms)Price: 96.3125 (par 100, price on % terms) Trade date:Trade date: 10/28/0610/28/06 Settle date:Settle date: 10/31/0610/31/06 Accrual Con.:Accrual Con.: 30/36030/360 Coupon Freq.:Coupon Freq.: Semi-AnnualSemi-AnnualCalculate purchase interest.Calculate purchase interest.

Players in Bond MarketPlayers in Bond Market

IssuersIssuers

InvestorsInvestors

RegulatorsRegulators

IssuerIssuer• The issuer base includes governments, MNCs, large local The issuer base includes governments, MNCs, large local

corporates, financial institutions.corporates, financial institutions.

• PurposePurpose

Diversification of funding base and increased stability in the Diversification of funding base and increased stability in the

capital structurecapital structure

To secure intermediate maturity funding for long term To secure intermediate maturity funding for long term

projects and capital expenditureprojects and capital expenditure

Mitigation of FX riskMitigation of FX risk

Funding costs relative to maturity tends to be cheaper than Funding costs relative to maturity tends to be cheaper than

rolling over short-term bank facilitiesrolling over short-term bank facilities

Positive impact on branding through market publicityPositive impact on branding through market publicity

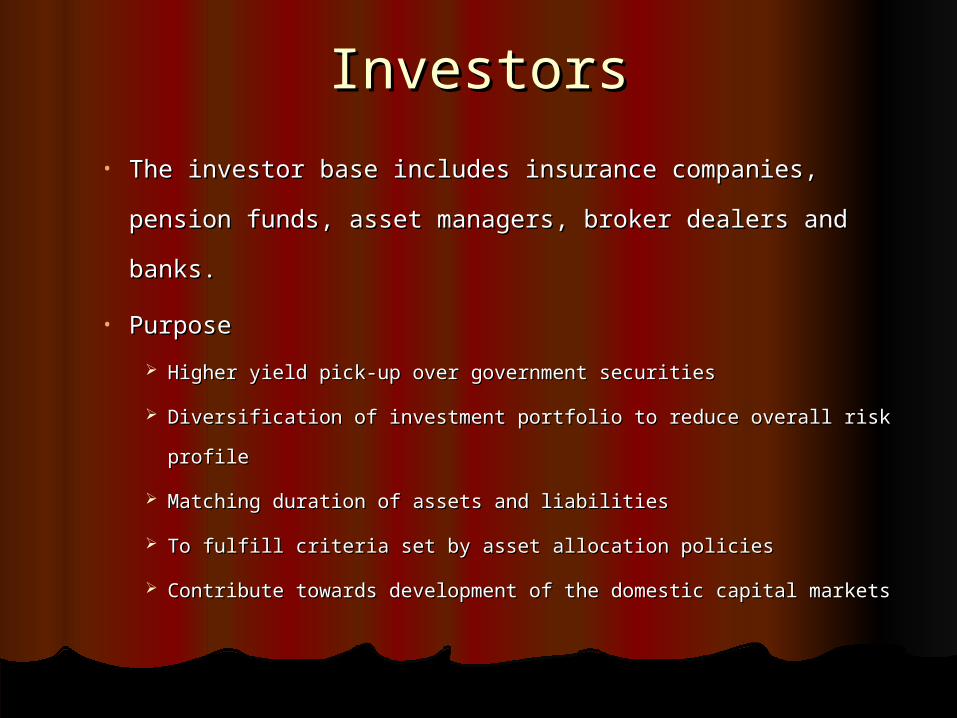

InvestorsInvestors

• The investor base includes insurance companies, The investor base includes insurance companies,

pension funds, asset managers, broker dealers and pension funds, asset managers, broker dealers and

banks.banks.

• PurposePurpose

Higher yield pick-up over government securitiesHigher yield pick-up over government securities

Diversification of investment portfolio to reduce overall risk profileDiversification of investment portfolio to reduce overall risk profile

Matching duration of assets and liabilitiesMatching duration of assets and liabilities

To fulfill criteria set by asset allocation policiesTo fulfill criteria set by asset allocation policies

Contribute towards development of the domestic capital marketsContribute towards development of the domestic capital markets

RegulatorsRegulators

• Key regulators in the are Government, CMA or Key regulators in the are Government, CMA or

equivalent body, and the Stock Exchangeequivalent body, and the Stock Exchange

• PurposePurpose

Government Government has overall responsibility to institute macro economic has overall responsibility to institute macro economic

measures and a strong legal framework that create an enabling measures and a strong legal framework that create an enabling

environmentenvironment

The Capital Markets AuthorityThe Capital Markets Authority ensures investor protection through ensures investor protection through

supervision of the securities industry.supervision of the securities industry.

The Stock ExchangeThe Stock Exchange provides a market place for secondary trading provides a market place for secondary trading

activity and approves the listing of new issues.activity and approves the listing of new issues.

Types of bondTypes of bond Fixed rate bonds Fixed rate bonds

Have a coupon that remains constant throughout the life Have a coupon that remains constant throughout the life of the bond. of the bond.

Floating rate notes Floating rate notes Have a coupon that is linked to a money market index, Have a coupon that is linked to a money market index,

such as LIBORsuch as LIBOR..

High yield bonds High yield bonds Bonds that are rated below investment grade by the Bonds that are rated below investment grade by the

credit rating agencies.credit rating agencies. RRelatively risky.elatively risky. Also called Junk bonds.Also called Junk bonds.

Zero coupon bonds Zero coupon bonds Do not pay any interest.Do not pay any interest. Traded at a substantial discount from par valueTraded at a substantial discount from par value . .

Types of bond – Cont.Types of bond – Cont.

Inflation linked bonds Inflation linked bonds Principal amount is indexed to inflationPrincipal amount is indexed to inflation.. Interest rate is lower than for fixed rate bondsInterest rate is lower than for fixed rate bonds with a comparable with a comparable

maturity.maturity. Eg:Treasury Inflation-Protected Securities (TIPS) and I-bonds.Eg:Treasury Inflation-Protected Securities (TIPS) and I-bonds.

Asset-backed securities Asset-backed securities Bonds whose interest and principal payments are backed by underlying Bonds whose interest and principal payments are backed by underlying

cash flows from other assets.cash flows from other assets. Eg: MBS, CMO, CDOEg: MBS, CMO, CDO

Subordinated bonds Subordinated bonds Has a lower priority than other bonds of the issuer in case of Has a lower priority than other bonds of the issuer in case of

liquidation.liquidation. Has a lower credit rating and a higher risk.Has a lower credit rating and a higher risk.

Perpetual bonds Perpetual bonds No maturity date.No maturity date. Eg : UK ConsolsEg : UK Consols

RISKSRISKS

Credit risk or default riskCredit risk or default risk

Market or interest rate riskMarket or interest rate risk

Reinvestment riskReinvestment risk

Inflation riskInflation risk

Liquidity riskLiquidity risk

Political or legal riskPolitical or legal risk

Event riskEvent risk

REPURCHASE REPURCHASE AGREEMENT(REPO)AGREEMENT(REPO)

Repo-DefinitionRepo-Definition Transaction involving selling of securities and Transaction involving selling of securities and

simultaneously agreeing to purchase of the simultaneously agreeing to purchase of the same after specified time at a given price.same after specified time at a given price.

Repo when viewed from the perspective of Repo when viewed from the perspective of the supplier of the securities and a reverse the supplier of the securities and a reverse repo from the point of view of the supplier of repo from the point of view of the supplier of funds.funds.

Terminology depends largely on which party Terminology depends largely on which party initiated the transaction. initiated the transaction.

CharacteristicsCharacteristicsMaturitiesMaturities

CollateralCollateral Type- G-Sec, Federal Bonds ,T-bills.Type- G-Sec, Federal Bonds ,T-bills. Value-Dirty Price.Value-Dirty Price.

YieldsYields The sale and repurchase at the same price.The sale and repurchase at the same price. Provider of funds receives agreed upon Provider of funds receives agreed upon

interest.interest. Lender of security receives the coupon, if any.Lender of security receives the coupon, if any.

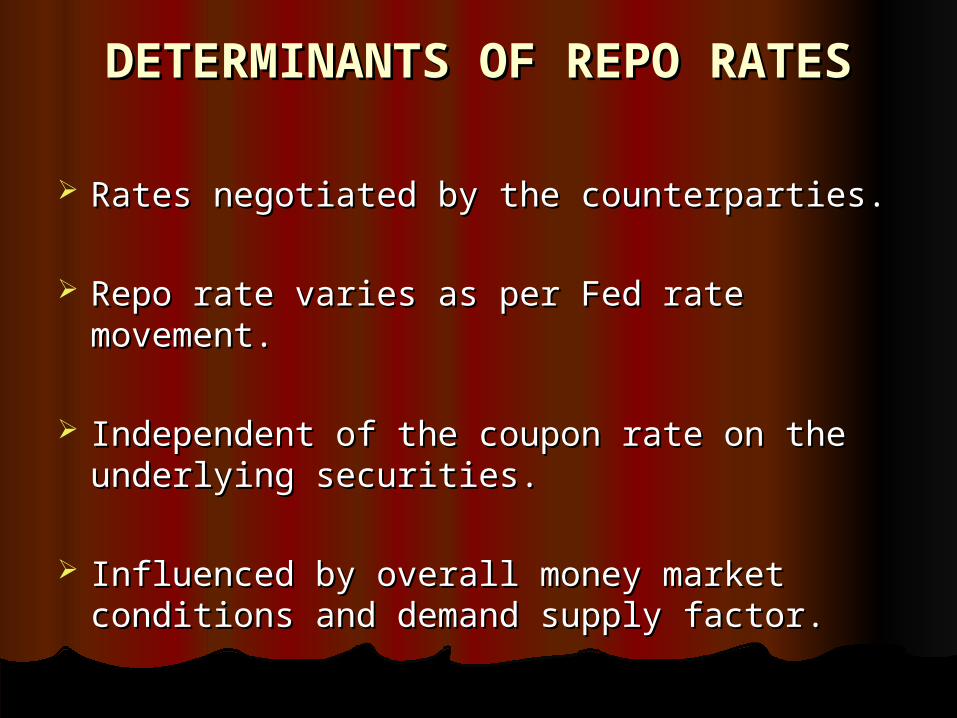

DETERMINANTS OF REPO DETERMINANTS OF REPO RATESRATES

Rates negotiated by the counterparties.Rates negotiated by the counterparties.

Repo rate varies as per Fed rate movement.Repo rate varies as per Fed rate movement.

Independent of the coupon rate on the Independent of the coupon rate on the underlying securities.underlying securities.

Influenced by overall money market Influenced by overall money market conditions and demand supply factor.conditions and demand supply factor.

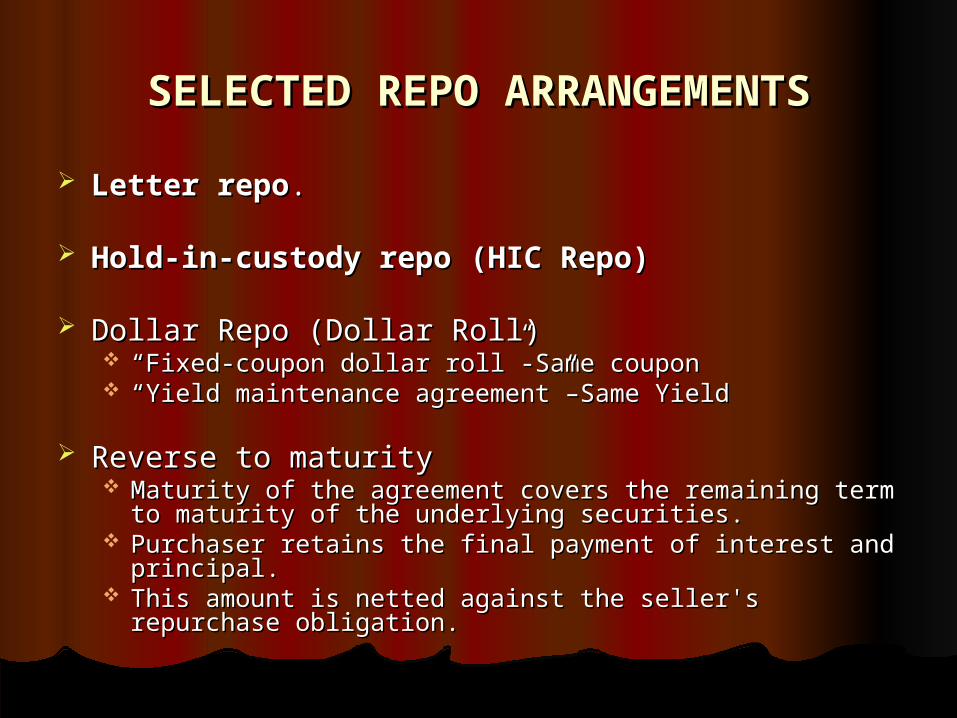

SELECTED REPO ARRANGEMENTSSELECTED REPO ARRANGEMENTS

Letter repoLetter repo. .

Hold-in-custody repoHold-in-custody repo (HIC Repo)(HIC Repo)

Dollar Repo (Dollar Roll)Dollar Repo (Dollar Roll) ““Fixed-coupon dollar roll”-Same couponFixed-coupon dollar roll”-Same coupon ““Yield maintenance agreement”–Same YieldYield maintenance agreement”–Same Yield

Reverse to maturity Reverse to maturity Maturity of the agreement covers the remaining term to Maturity of the agreement covers the remaining term to

maturity of the underlying securities.maturity of the underlying securities. Purchaser retains the final payment of interest and Purchaser retains the final payment of interest and

principal.principal. This amount is netted against the seller's repurchase This amount is netted against the seller's repurchase

obligation.obligation.

SELECTED REPO ARRANGEMENTS- Cont.SELECTED REPO ARRANGEMENTS- Cont.

Flex RepoFlex Repo Repo arrangement with a flexible term to Repo arrangement with a flexible term to

maturity.maturity. Sells some of the securities before repo matures.Sells some of the securities before repo matures. The dealer pays a lower rate to compensate The dealer pays a lower rate to compensate

early maturity.early maturity.

Index RepoIndex Repo Underlying interest rate resets periodically Underlying interest rate resets periodically

based on Fed Rate, LIBOR etc.based on Fed Rate, LIBOR etc. Resembles flex repos.Resembles flex repos. Used regularly to hedge or finance positions in Used regularly to hedge or finance positions in

securities such as floating-rate notes securities such as floating-rate notes

PARTICIPANTS IN THE REPO PARTICIPANTS IN THE REPO MARKETMARKET

InvestorsInvestors

DealersDealers

BrokersBrokers

Federal ReserveFederal Reserve

TREASURY BILLSTREASURY BILLS

TREASURY BILLSTREASURY BILLS

Short-term securities issued by the Short-term securities issued by the U.S. Treasury.U.S. Treasury.

Maturities – 1,3, 6 and 12 months.Maturities – 1,3, 6 and 12 months. Minimum denominations - $1,000.Minimum denominations - $1,000. Issuance. Issuance.

Auction-Tue, Mon, Thu.Auction-Tue, Mon, Thu. Competitive and non-competitive Competitive and non-competitive

bidding.bidding. When-issued trading.When-issued trading.

INVESTMENT INVESTMENT CHARACTERISTICSCHARACTERISTICS

Default RiskDefault Risk

Liquidity Liquidity

Taxes Taxes

Low minimum denomination Low minimum denomination

INVESTORSINVESTORS

IndividualsIndividuals commercial bankscommercial banks Money market mutual fundsMoney market mutual funds Foreign InvestorsForeign Investors Nonbank financial institutionsNonbank financial institutions Non financial corporations.Non financial corporations. State and local governments.State and local governments.

COMMERCIAL PAPERSCOMMERCIAL PAPERS

COMMERCIAL PAPERSCOMMERCIAL PAPERS An unsecured, short-term debt instrument An unsecured, short-term debt instrument

issued by a corporation for meeting short-issued by a corporation for meeting short-term liabilities.term liabilities.

Not to be registered with the SEC if Not to be registered with the SEC if matures within 9 months.matures within 9 months.

Rollover riskRollover risk..

ISSUING OF COMMERCIAL ISSUING OF COMMERCIAL PAPERPAPER

IssuersIssuers BanksBanks NBFCNBFC Manufacturing co.Manufacturing co.

Types of issueTypes of issue DirectDirect Through DealersThrough Dealers

CHARECTERISTICS OF CHARECTERISTICS OF COMMERCIAL PAPERCOMMERCIAL PAPER

Maturity – Upto 1 year.Maturity – Upto 1 year.

Large minimum denominations.Large minimum denominations.

Issued to finance "current Issued to finance "current transactions”.transactions”.

Issued at discount and matured at Issued at discount and matured at face value.face value.

CERTIFICATE OF DEPOSITCERTIFICATE OF DEPOSIT

Certificate of DepositCertificate of Deposit

Debt instruments issued by banks and Debt instruments issued by banks and other financial institutions.other financial institutions.

CD bears a maturity date, a specified CD bears a maturity date, a specified fixed interest rate and can be issued in fixed interest rate and can be issued in any denomination. any denomination.

Generally issued by commercial banks and Generally issued by commercial banks and are insured by the FDIC. are insured by the FDIC.

Tenure- one month to five years.Tenure- one month to five years. Types- Small and large CDs.Types- Small and large CDs. Minimum deposit - $1000Minimum deposit - $1000

CD RATESCD RATES

Fixed interest rate paid on CDFixed interest rate paid on CD

Factors influencing the interest rate:Factors influencing the interest rate:Principal. Principal. Term to maturity. Term to maturity. Size of the issuing bankSize of the issuing bankType of CDType of CD

FUNCTIONING OF CDFUNCTIONING OF CD

Issued in the form of book entry.Issued in the form of book entry.

Option of interest withdrawl.Option of interest withdrawl.

Choice of Choice of Rolling overRolling over..

Penalty of withdrawl before the Penalty of withdrawl before the maturity date.maturity date.

CD- CharacteristicsCD- Characteristics

CD REFINANCECD REFINANCE PPenalty for early withdrawalenalty for early withdrawal to be decided at the time of issue. to be decided at the time of issue. Opt for refinance is the added interest exceeds the cost of withdrawlOpt for refinance is the added interest exceeds the cost of withdrawl..

CD LADDERSCD LADDERS Distributes the deposits over a period of several years.Distributes the deposits over a period of several years. Enjoys the benefits of the longterm rates.Enjoys the benefits of the longterm rates. Retain the option to re-invest or withdraw. Retain the option to re-invest or withdraw.

CDCD DEPOSIT INSURANCEDEPOSIT INSURANCE

Governed by complex FDIC rules.Governed by complex FDIC rules. Basic Coverage is $100,000 for a single account and $200,000 for a Basic Coverage is $100,000 for a single account and $200,000 for a

joint accountjoint account. .

Callable CDsCallable CDs Bank reserves the right to "call" the investmentBank reserves the right to "call" the investment.. pays a premium interest rate.pays a premium interest rate. Banks manage their interest rate risk by selling callable CDsBanks manage their interest rate risk by selling callable CDs

ASSET BACKED SECURITIESASSET BACKED SECURITIES

An asset-backed security (ABS) is a securitized An asset-backed security (ABS) is a securitized interest in a pool of assets. interest in a pool of assets.

The majority of these "pools" consist of:The majority of these "pools" consist of: Auto loans and leases Auto loans and leases Credit Tenant Leases Credit Tenant Leases Consumer and business installment receivables Consumer and business installment receivables Bank and Financial Assets Bank and Financial Assets Equipment leases Equipment leases Student loans Student loans Specialized Assets Specialized Assets

Characteristics Of ABSCharacteristics Of ABS

ABS bring together a pool of financial ABS bring together a pool of financial assets that otherwise could not easily assets that otherwise could not easily be traded in their existing form.be traded in their existing form.

ABSs are backed by non-mortgage ABSs are backed by non-mortgage assets.assets.

ABSs entail credit risk but tends to be ABSs entail credit risk but tends to be modest.modest.

ABSs can be structured into different ABSs can be structured into different classes or tranches based on class of classes or tranches based on class of debt, maturity etc.debt, maturity etc.

ADVANTAGES OF ABSADVANTAGES OF ABS Original lenders recover cash quickly, Original lenders recover cash quickly,

enabling them to make more loans.enabling them to make more loans.

It improves liquidity as well as balance It improves liquidity as well as balance sheet ratios while also reducing interest sheet ratios while also reducing interest expense.expense.

The originator of the receivables usually The originator of the receivables usually

continues to service the assets and collect continues to service the assets and collect the payments.the payments.

Funding can be structured to be either Funding can be structured to be either fixed or floating.fixed or floating.

Mortgage Backed SecuritiesMortgage Backed Securities

MORTGAGE BACKED SECURITIESMORTGAGE BACKED SECURITIES

Debt obligations that represent claims to the cash Debt obligations that represent claims to the cash flows from pools of mortgage loans.flows from pools of mortgage loans.

Represents pool of mortgages as collateral.Represents pool of mortgages as collateral.

Belongs to a class of ABS.Belongs to a class of ABS.

Individual investor earns interest in proportion to Individual investor earns interest in proportion to his stake in the entire pool.his stake in the entire pool.

Payments to investors usually made on a monthly Payments to investors usually made on a monthly basis. basis.

Types of MBSTypes of MBS

Ginnie Mae- MBS issued by the Government Ginnie Mae- MBS issued by the Government National Mortgage Association.National Mortgage Association.

Fannie Mae – Issued by Federal National Fannie Mae – Issued by Federal National Mortgage Association.Mortgage Association.

Freddie Mac - Federal Home Loan Mortgage Freddie Mac - Federal Home Loan Mortgage Corporation.Corporation.