fisheries reform of the market policy of the common fishery policy eafa workshop: optimising value...

TRANSCRIPT

FISHERIES

Reform of the market policy of the Common Fishery PolicyEAFA Workshop: Optimising Value Chains in Fisheries

Market & Trade Xavier GUILLOU 2 June 2010

Fisheries 2

FISHERIES

Slide

Consultations and methodology

• Green paper on the reform of the CFP (April 2009)

• Evaluation of the Common Organisation of the Markets in Fishery and Aquaculture Products

http://ec.europa.eu/fisheries/documentation/studies/study_evaluation_market/index_en.htm

• Study on the supply and marketing of fishery and aquaculture products in the European Union

http://ec.europa.eu/fisheries/documentation/studies/study_market/index_en.htm

Fisheries 3

FISHERIES

Slide

Thematic seminars

• Price formation and marketing of fisheries and aquaculture products (December 2009)

http://ec.europa.eu/fisheries/news_and_events/events/price_seminar/index_en.htm

• Promotion of fishery and aquaculture products (April 2010)http://ec.europa.eu/fisheries/news_and_events/events/seminar_140410/index_en.htm

• Supply to the EU market (April 2010)http://ec.europa.eu/fisheries/news_and_events/events/seminar_150410/index_en.htm

Fisheries 4

FISHERIES

Slide

EU market: main trends • EU market: dynamic growth and increasing deficit

– Increased consumption (20 kg per capita)– EU supply down by 30% in 10 years– Large increase of imports– Self sufficiency rate down from 57% to less than 40%

• EU: a very attractive market– Largest, most profitable, involving large world companies– Fish market - globalised market– Dynamic development of new products sold in the EU

• Active and integrated internal market– Main MS producers export essentially within the EU– Interdependence of EU markets

Fisheries 5

FISHERIES

Slide

EU first market in the world

Source: AIPCE (2007)

Importations9,4 Mt

Captures5,4 Mt

Aquaculture1,3 Mt

Disponible16,1 Mt

Exportations2,1 Mt

Utilisationsnon alimentaires

1,9 Mt

Marché12,1 Mt

Non-food products

Exports

Available quantities

EU market

imports

• value € 55 billion, volume 12 million tonnes,

Fisheries 6

FISHERIES

Slide

Dynamic growth and trade balance deficit

0

2000

4000

6000

8000

10000

12000

14000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

100

0 t

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

60,0%

70,0%

Approvisionnement du marché Taux d'auto-approvisionnement

Fisheries 7

FISHERIES

Slide

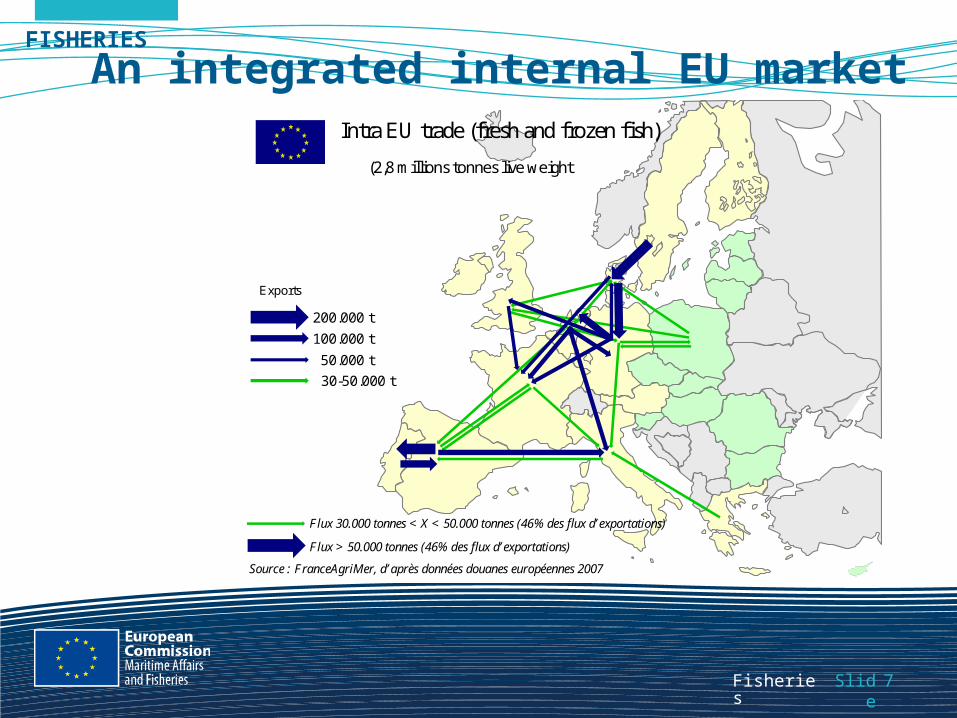

An integrated internal EU marketIntra EU trade (fresh and frozen fish)

(2,8 millions tonnes live weight

200.000 t

100.000 t

50.000 t

Exports

Flux 30.000 tonnes < X < 50.000 tonnes (46% des flux d’exportations)

Source : FranceAgriMer, d’après données douanes européennes 2007

30-50.000 t

Flux > 50.000 tonnes (46% des flux d’exportations)

Fisheries 8

FISHERIES

Slide

Heterogeneous consumption habits in the EU

Fisheries 9

FISHERIES

Slide

Consumption trends

TAAM> 1% 0.5%<TAAM<1%

0<TAAM<0.5%

TAAM < 0

Fisheries 10

FISHERIES

Slide

Retails• Increased share of large retail companies• Role in consumption growth and in development of ‘new’

products• Development of labelling• Catering, restaurants and takeaways

Impact of the trade policy

• Trend towards decrease in customs duties • Increasing importance of non tariff issues

Fisheries 11

FISHERIES

Slide

Reform of the market policy

Fisheries 12

FISHERIES

Slide

LEGAL ARCHITECTURE

CFP basic Regulation

New chapter « Market Policy »

for fisheries and aquaculture productsMarketing standards

(2406/96)

CMO Regulation

(104/2000)

Information to consumers

(2065/2001)

)

Fisheries 13

FISHERIES

Slide

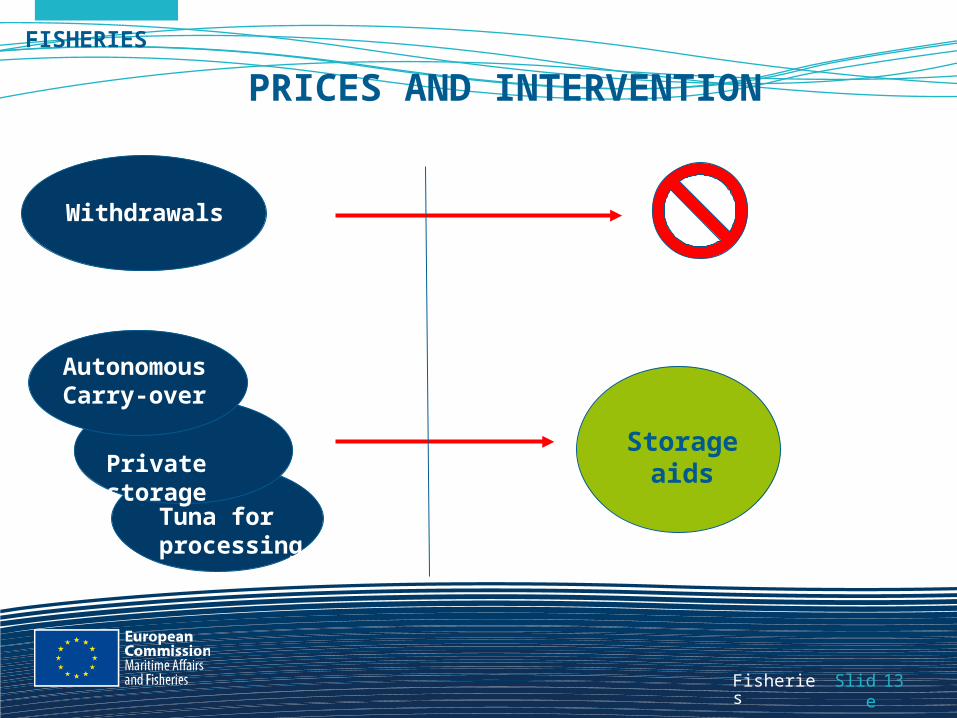

PRICES AND INTERVENTION

Storage aids

Withdrawals

Autonomous Carry-over

Private storage

Tuna for processing

Fisheries 14

FISHERIES

Slide

PRODUCER AND INTERBRANCH ORGANISATIONS

Producer organisations

- encourage production planning (catch plans)

- promote concentration of supply

- stabilise prices

- encourage sustainable fishing methods

-……………………………

Interbranch organisations

- improve transparency of production and market

- draw up contracts

- ……………………………………………

Producer organisations

Production planning

Product value at 1st

sale

Better knowledge of markets and marketing

Interbranch organisations

Contractualisation

Promotion

Storage

Aid

Fisheries 15

FISHERIES

Slide

EU MARKET OBSERVATORY

The information about market is scattered between

regions and MS, and heterogeneous along the

supply chain

The information is not shared between

stakeholders and is much better on the

processor/retailer side than on the producer/wholesaler

side

International context

Global view of the EU market

All market actors Policy makers- Better view of market prices and opportunities

- Production planning

- Knowledge of consumer’s demand (when, where, what…)

- Background for policy design

-Early warning of crises

- Survey of margins along the marketing chain

From 1st sale…

….to retailprice

Fisheries 16

FISHERIES

Slide

MARKETING STANDARDS AND INFORMATION TO CONSUMER

Species

Freshness

Size

Presentation

Information to consumer Commercial

designation

Production method

Catch area

Marketing standards

Marketing standards

Compulsory Voluntary

Information to consumer

Scientific name

More detailed catch area

Fishing method

…

Nutritional

Environmentally friendly

Fair trade and social aspects

Updating grading

Minimum marketing sizes

eBusinness

+

Fisheries 17

FISHERIES

Slide

Next steps…Options studies

Reform proposals by mid 2011