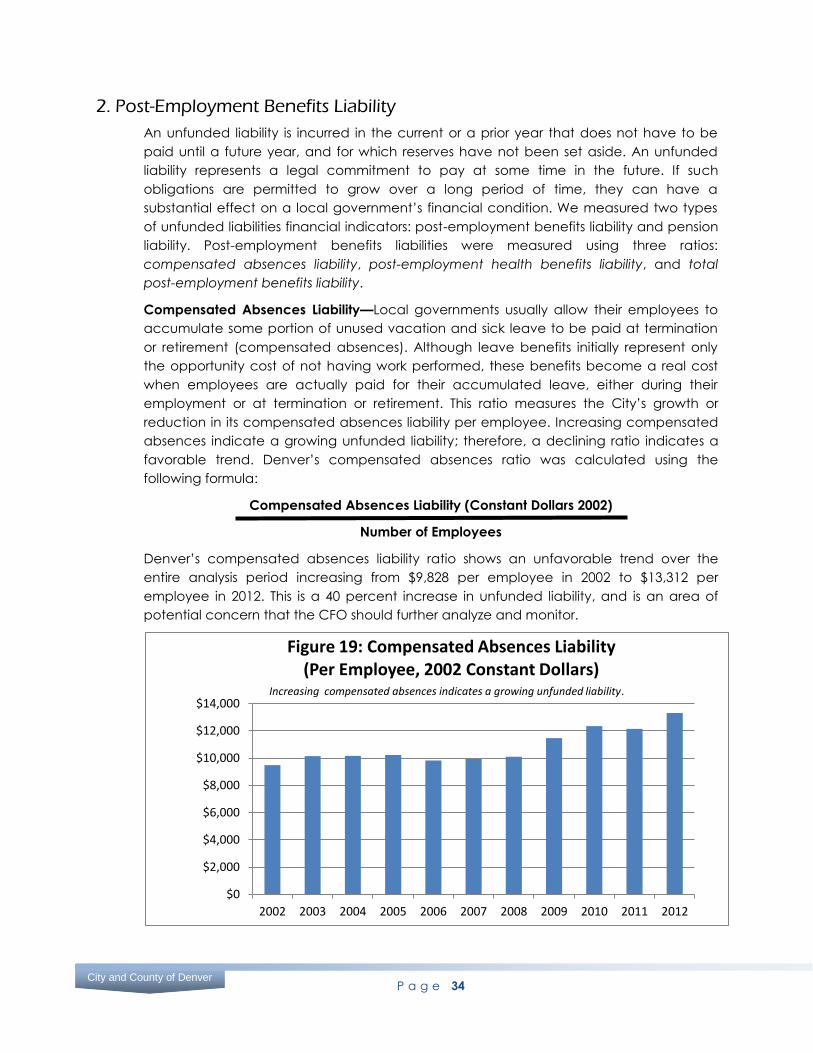

fiscal sustainability: financial condition and transparency · pdf filefiscal sustainability:...

TRANSCRIPT

Dennis J. Gallagher Auditor

Office of the Auditor

Audit Services Division

City and County of Denver

Fiscal Sustainability: Financial Condition and Transparency

Performance Audit

December 2013

The Auditor of the City and County of Denver is independently elected by the citizens of Denver.

He is responsible for examining and evaluating the operations of City agencies for the purpose

of ensuring the proper and efficient use of City resources and providing other audit services and

information to City Council, the Mayor and the public to improve all aspects of Denver’s

government. He also chairs the City’s Audit Committee.

The Audit Committee is chaired by the Auditor and consists of seven members. The Audit

Committee assists the Auditor in his oversight responsibilities of the integrity of the City’s finances

and operations, including the integrity of the City’s financial statements. The Audit Committee is

structured in a manner that ensures the independent oversight of City operations, thereby

enhancing citizen confidence and avoiding any appearance of a conflict of interest.

Audit Committee

Dennis Gallagher, Chair Robert Bishop

Maurice Goodgaine Jeffrey Hart

Leslie Mitchell Timothy O’Brien, Vice-Chair

Rudolfo Payan

Audit Staff

Audrey Donovan, Deputy Director, CIA, CRMA, CGAP

Chris Horton, Audit Supervisor, PhD, CGAP, CRMA, CCSA

Marcus Garrett, Audit Supervisor, CIA, CGAP, CRMA

Bonnie Doty, Lead Auditor, MGPS

Anna Hansen, Lead Auditor

Robyn Lamb, Lead Auditor

You can obtain copies of this report by contacting us at:

Office of the Auditor

201 West Colfax Avenue, Department 705 Denver CO, 80202

(720) 913-5000 Fax (720) 913-5247

Or download and view an electronic copy by visiting our website at:

www.denvergov.org/auditor

To promote open, accountable, efficient and effective government by performing impartial reviews and other audit services

that provide objective and useful information to improve decision making by management and the people.

We will monitor and report on recommendations and progress towards their implementation.

City and County of Denver 201 West Colfax Avenue, Department 705 Denver, Colorado 80202 720-913-5000

FAX 720-913-5247 www.denvergov.org/auditor

Dennis J. Gallagher

Auditor

December 19, 2013

Cary Kennedy, Deputy Mayor, Chief Financial Officer

Department of Finance

City and County of Denver

Dear Ms. Kennedy:

Attached is the Auditor’s Office Audit Services Division’s report of their audit of fiscal

sustainability, specifically financial condition and the transparency of financial reporting. This is

the first report covering the City’s fiscal sustainability. The purpose of the audit was to assess the

City’s financial condition using a well-regarded methodology and determine if there were any

areas that needed additional attention and investigation by your department. The Division will

report further on fiscal sustainability in early 2014.

I’m pleased to report that our assessment of the City’s financial condition had numerous positive

results, including several favorable financial condition indicators and our determination that the

City’s public financial reporting adheres to leading practices in several areas. However, we

noted some areas of concern regarding the amount of debt that the City maintains, particularly

with respect to debt at Denver International Airport. We also make recommendations regarding

areas where the City can further enhance its financial transparency as we seek to become a

world class city. I am confident that these findings will not fall on rocky soil under your leadership.

If you have any questions, please call Kip Memmott, Director of Audit Services, at 720-913-5000.

Sincerely,

Dennis J. Gallagher

Auditor

DJG/cnh

cc: Honorable Michael Hancock, Mayor

Honorable Members of City Council

Members of Audit Committee

Ms. Janice Sinden, Chief of Staff

Ms. Stephanie O’Malley, Deputy Chief of Staff

Ms. Beth Machann, Controller

Mr. Brendan Hanlon, Budget Director

To promote open, accountable, efficient and effective government by performing impartial reviews and other audit services

that provide objective and useful information to improve decision making by management and the people.

We will monitor and report on recommendations and progress towards their implementation.

Mr. Robert Gibson, Director of Cash, Risk, and Capital Funding

Mr. Doug Friednash, City Attorney

Ms. Janna Young, City Council Executive Staff Director

Mr. L. Michael Henry, Staff Director, Board of Ethics

Ms. Kim Day, Manager of the Department of Aviation

Mr. Patrick Heck, Chief Financial Officer, Department of Aviation

Mr. Steven Hutt, Executive Director, Denver Employees Retirement Plan

To promote open, accountable, efficient and effective government by performing impartial reviews and other audit services

that provide objective and useful information to improve decision making by management and the people.

We will monitor and report on recommendations and progress towards their implementation.

City and County of Denver 201 West Colfax Avenue, Department 705 Denver, Colorado 80202 720-913-5000

FAX 720-913-5247 www.denvergov.org/auditor

Dennis J. Gallagher

Auditor

AUDITOR’S REPORT

We have completed an audit assessing the fiscal sustainability of the City, specifically related to

its financial condition and the transparency of its financial reporting practices. This is the first

report reviewing the City’s fiscal sustainability. This audit had two objectives: to assess the City’s

current financial condition; and to assess the degree to which financial information is publicly

reported in comparison to leading practice.

This performance audit is authorized pursuant to the City and County of Denver Charter, Article

V, Part 2, Section 1, General Powers and Duties of Auditor, and was conducted in accordance

with generally accepted government auditing standards. Those standards require that we plan

and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis

for our findings and conclusions based on our audit objectives. We believe that the evidence

obtained provides a reasonable basis for our findings and conclusions based on our audit

objectives.

The audit found that as of December 31, 2012, Denver’s overall financial condition is promising

due to a favorable financial position and positive revenue-related financial indicators. However,

the audit identified unfavorable indicators of financial condition related to debt, capital assets,

and liabilities. Left unchecked, these unfavorable financial condition areas may diminish the

City’s ability to provide existing services on an ongoing basis. Audit work also determined that

the City has enhanced transparency and accessibility of financial information through the use of

several web pages, and could potentially become a local government transparency leader by

further improving the financial data it shares with stakeholders.

We extend our appreciation to the Chief Financial Officer, the City Controller, the City Budget

Director, the Director of Cash, Risk, and Capital Funding, and all of the other City personnel and

outside parties who assisted us during the audit.

Audit Services Division

Kip Memmott, MA, CGAP, CRMA

Director of Audit Services

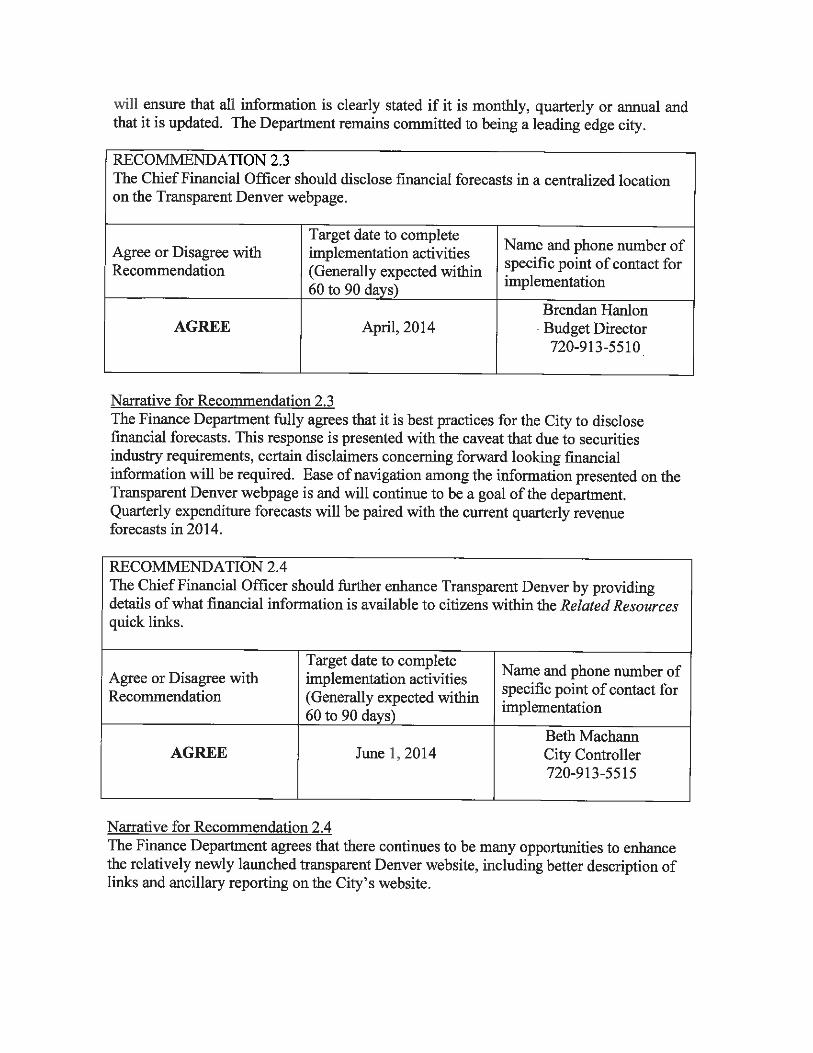

Background The Department of Finance is

responsible for the City’s financial

management, including collecting

revenues and other funds, tracking

and accounting for City funds, and

creating the City Budget. The

Department of Finance is led by the

Chief Financial Officer. Key

components of the Department

include the Treasury Division, the

Controller’s Office, and the Budget

and Management Office.

Purpose This audit report contains the results

of two audit objectives: to assess the

City’s current financial condition; and

to assess the degree to which

financial information is publicly

reported in comparison to leading

practice. The financial condition

assessment included a review of

thirteen financial condition

indicators, such as revenues,

liquidity, solvency, capital assets,

debt management, expenditures, and

post-employment benefits such as

pensions.

City and County of Denver – Office of the Auditor Audit Services Division

REPORT HIGHLIGHTS

Fiscal Sustainability: Financial Condition and Transparency

December 2013

The audit evaluated the City’s fiscal health based thirteen key financial indicators, and assessed the extent

to which the City conforms to leading practice in financial transparency.

Highlights As of December 31, 2012, Denver’s overall financial condition is

promising. For example, since 2009, the City’s ability to handle

unforeseen resource needs over the short-term has trended

upward. Moreover, since 2009, the City has reduced reliance on

general revenues (primarily taxes) and increased the self-

sufficiency of basic government services. While Denver’s current

financial outlook is promising, the audit identified several less

favorable indicators of financial condition which warrant further

analysis. These include primary government debt burden per

resident, the sufficiency of Denver’s Enterprise Funds’ resources to

repay debt, and the City’s maintenance of capital assets. These

indicators are intended to provide a snapshot of potential financial

concerns so the City’s leadership can conduct further assessment

and implement appropriate and timely responses.

The audit also found that, while the City has increased

transparency and accessibility of financial information through its

reports and website, more could be done to enhance transparency

for its various stakeholders by adopting recently articulated leading

practices in financial reporting.

For a complete copy of this report, visit www.denvergov.org/auditor Or Contact the Auditor’s Office at 720.913.5000

TABLE OF CONTENTS

INTRODUCTION & BACKGROUND 1

SCOPE 9

OBJECTIVE 9

METHODOLOGY 9

FINDING 1 12

Denver’s Financial Condition Is Promising but There Are Some Key

Unfavorable Financial Indicators That Warrant Additional

Attention 12

Denver’s Current and Historic Financial Condition 12

10-Point Test Financial Indicators with Favorable Results 15

1. Short-run Financial Position 16

2. Liquidity 17

3. Financial Asset Performance 18

4. Solvency 19

5. Primary Government Revenues 20

6. Governmental Activities Revenues 21

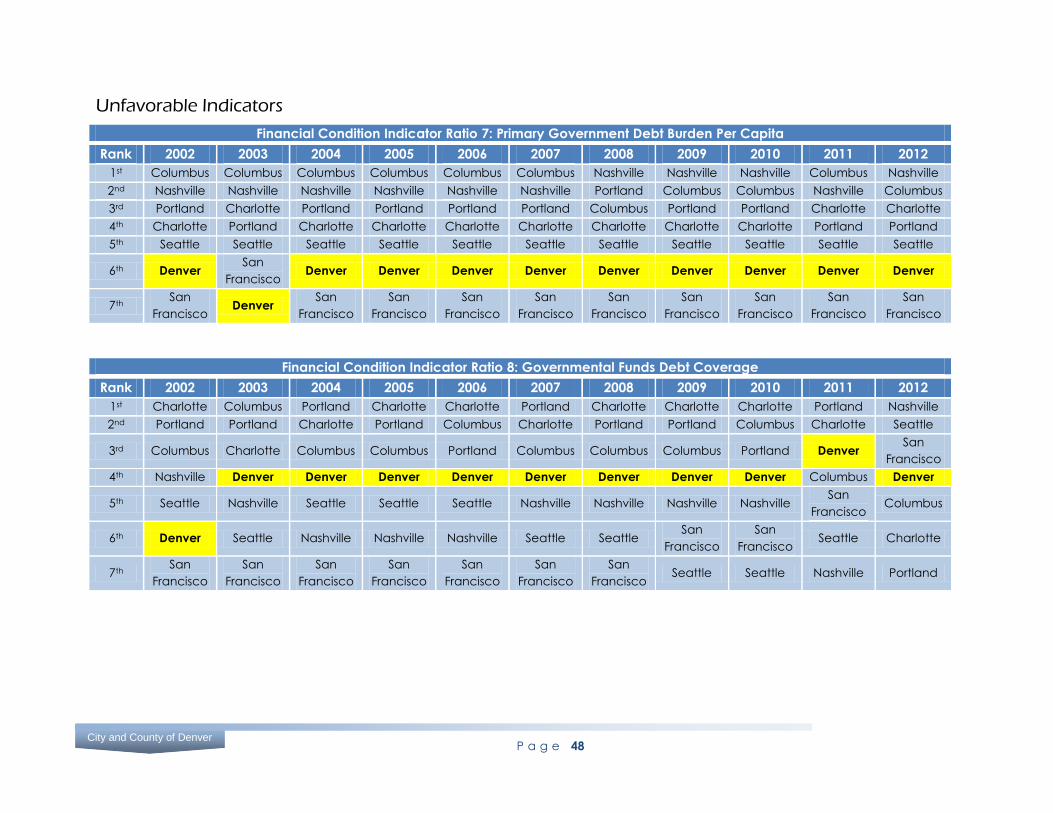

10-Point Test Financial Indicators with Unfavorable Results 23

7. Primary Government Debt Burden Per Capita 24

8. Governmental Funds Debt Coverage 26

9. Enterprise Funds Debt Coverage 27

10. Capital Assets 28

Results of Three Additional Financial Indicator Analyses 30

1. Expenditures 32

2. Post-Employment Benefits Liability 34

3. Unfunded Pension Liability 37

Importance of City Management Performing a Periodic Financial

Condition Analysis 38

TABLE OF CONTENTS (continued)

RECOMMENDATIONS 38

FINDING 2 39

Department of Finance Provides Financial Transparency and Can

Implement Additional Leading Practices 39

RECOMMENDATIONS 43

APPENDIX A 44

10-Point Test Rankings for Denver and Benchmark Cities, 2002-

2012 44

Favorable Indicators 44

Unfavorable Indicators 48

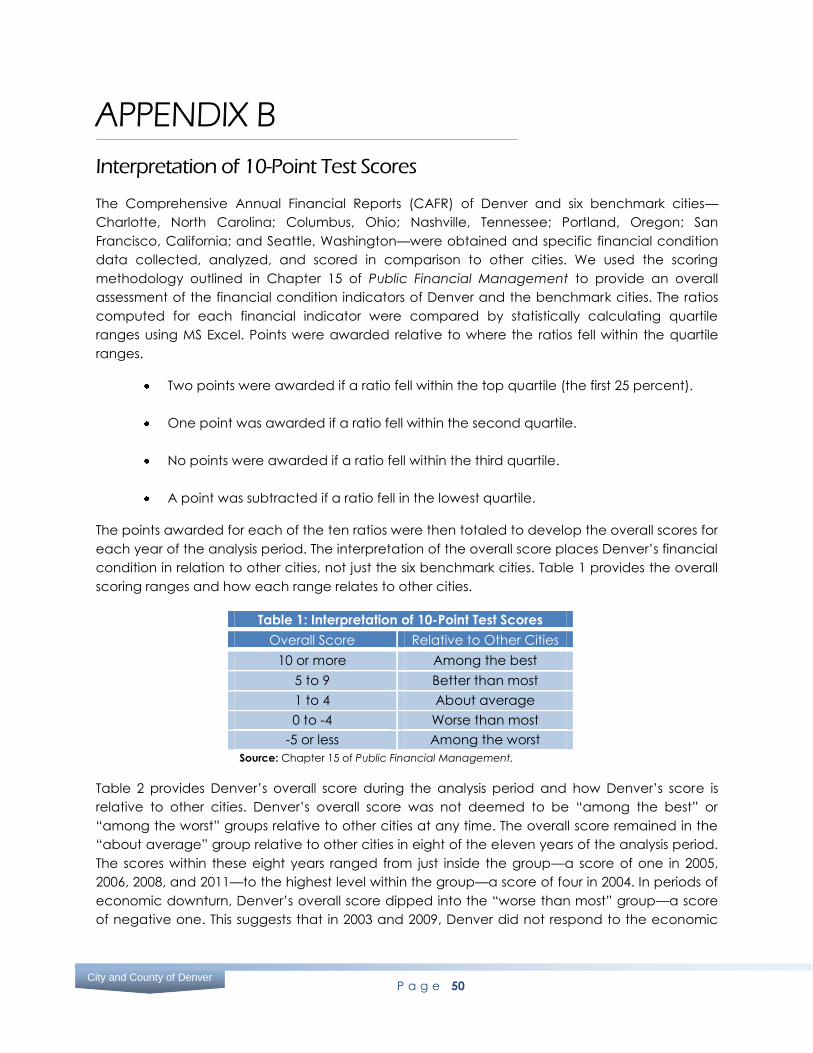

APPENDIX B 50

Interpretation of 10-Point Test Scores 50

AGENCY RESPONSE 52

P a g e 1

Office of the Auditor OOffffiiccee ooff tthhee AAuuddiittoorr

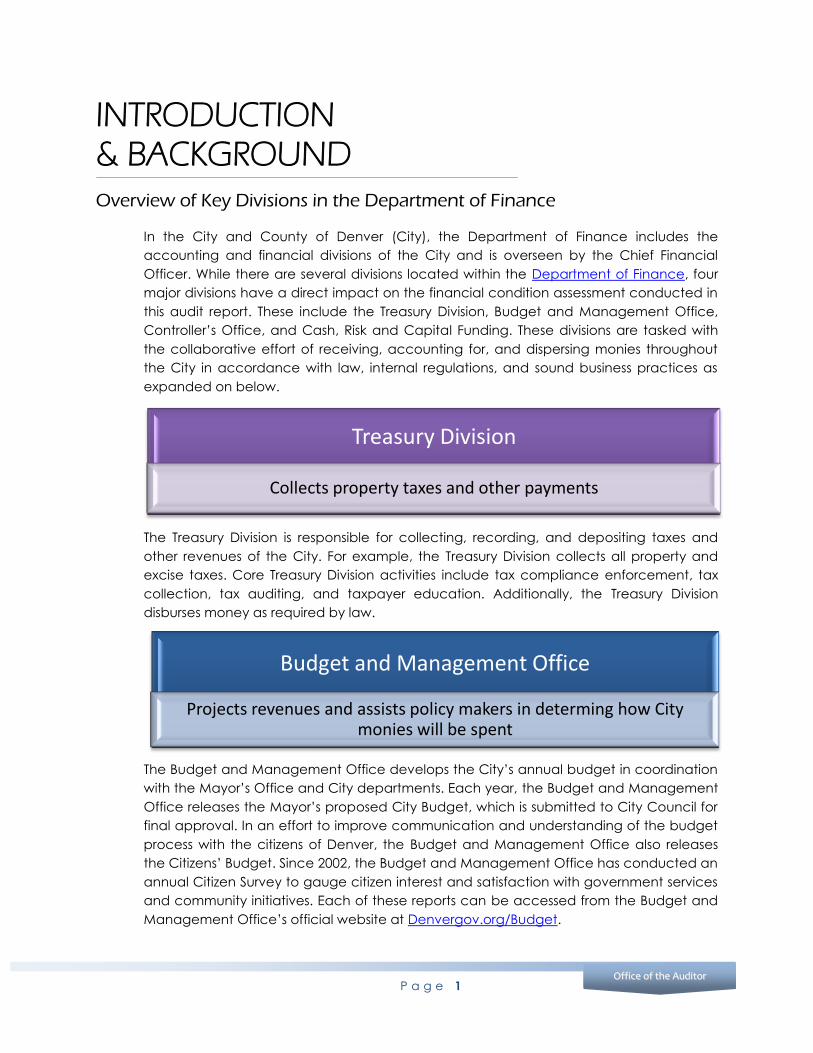

INTRODUCTION & BACKGROUND

Overview of Key Divisions in the Department of Finance

In the City and County of Denver (City), the Department of Finance includes the

accounting and financial divisions of the City and is overseen by the Chief Financial

Officer. While there are several divisions located within the Department of Finance, four

major divisions have a direct impact on the financial condition assessment conducted in

this audit report. These include the Treasury Division, Budget and Management Office,

Controller’s Office, and Cash, Risk and Capital Funding. These divisions are tasked with

the collaborative effort of receiving, accounting for, and dispersing monies throughout

the City in accordance with law, internal regulations, and sound business practices as

expanded on below.

The Treasury Division is responsible for collecting, recording, and depositing taxes and

other revenues of the City. For example, the Treasury Division collects all property and

excise taxes. Core Treasury Division activities include tax compliance enforcement, tax

collection, tax auditing, and taxpayer education. Additionally, the Treasury Division

disburses money as required by law.

The Budget and Management Office develops the City’s annual budget in coordination

with the Mayor’s Office and City departments. Each year, the Budget and Management

Office releases the Mayor’s proposed City Budget, which is submitted to City Council for

final approval. In an effort to improve communication and understanding of the budget

process with the citizens of Denver, the Budget and Management Office also releases

the Citizens’ Budget. Since 2002, the Budget and Management Office has conducted an

annual Citizen Survey to gauge citizen interest and satisfaction with government services

and community initiatives. Each of these reports can be accessed from the Budget and

Management Office’s official website at Denvergov.org/Budget.

Treasury Division

Collects property taxes and other payments

Budget and Management Office

Projects revenues and assists policy makers in determing how City monies will be spent

P a g e 2

City and County of Denver

The Controller’s Office is responsible for accounting, payroll, and financial reporting in the

City. Core activities include establishing, maintaining, and enforcing the City’s

accounting policies and procedures, which are often conveyed through the adoption of

Fiscal Accountability Rules. Further, the Controller’s Office develops the Comprehensive

Annual Financial Report (CAFR)—an annual report that contains audited financial

information on the operations of the City. The audit of CAFR data is performed by the

City’s external auditor under the oversight of the City’s Independent Audit Committee.

Moreover, the Controller’s Office issues the Popular Annual Financial Report—a citizen-

centric report focused on providing the public with a less complicated breakdown of the

City’s finances. In addition, the Controller’s Office works with the independent external

auditors to provide vital financial data for the creation of the annual Single Audit—a

federally mandated assessment of non-federal entities, such as municipal governments,

that expended more than $500,000 or more in federal awards, such as grants.

The Cash, Risk, and Capital Funding (CRCF) Division was created in 2012, by combining

the Financial Management Section of the Treasury Division with the Risk Management

Division. CRCF’s financial management roles include overseeing the City’s banking

services, cash, and investments, and managing debt issuances. CRCF’s risk

management roles include overseeing the City’s self-funded Worker’s Compensation

insurance program, and managing the City’s risk and exposure due to activities of

departments, agencies, and employees.

City Budget

For 2014 the Mayor has proposed a budget of $1.64 billion for all appropriated funds. The

budget is divided into three general groups of appropriated funds: governmental funds;

proprietary funds; and fiduciary funds.1

Governmental Funds—Governmental funds are the funds used for the City’s basic

operations. This group includes the General Fund, which is the main operating fund for

the City, composed mostly of tax revenues. The General Fund is the funding source for

1 All information in this section was derived from the Approved 2013 Budget and the Mayor’s Proposed 2014 Budget, and from

guidance provided by the Governmental Accounting Standards Board (www.gasb.org).

Controller's Office

Ensures City monies are properly collected, distributed, paid, and recorded

Cash, Risk, and Capital Funding

Manages the cash position, oversees cash handling practices, coordinates commercial banking services, and invests the City's funds

P a g e 3

Office of the Auditor OOffffiiccee ooff tthhee AAuuddiittoorr

cornerstone municipal activities such as Police, Fire, Public Works, and Parks and

Recreation. In 2014, the proposed funding level for the General Fund is $1.06 billion,

about 65 percent of the entire proposed budget for the City.

Other specific governmental funds are the Special Revenue Funds, the Capital

Improvement Funds, and the Debt Service Fund. The Special Revenue Funds consist of

monies that have dedicated purposes, such as federal or state grants. Special Revenue

Funds support varied activities, including economic development, human services, and

public safety. Capital Improvement Funds provide a means for the purchase and

maintenance of major capital assets, though such assets may also be purchased

through different funds depending on the circumstances.2 The City’s various Capital

Improvement Funds comprise monies from various sources, such as property taxes, voter-

approved general obligation bonds, state lottery proceeds, the Highway Users Trust Fund,

and royalties paid to the City from the Winter Park Ski Resort. Finally, the Debt Service

Fund exists to support ongoing long-term debt payments.

Proprietary Funds—The City’s two main types of proprietary funds support business-like

activities and operate similar to funds utilized by the private sector. Most of the City’s

proprietary funds are Enterprise Funds, while a few are Internal Service Funds. The

Enterprise Funds receive revenue primarily from user charges, where the specific users

rather than general taxpayers are responsible for the ongoing revenue stream. The City

has four different enterprise funds, in order of highest revenues to lowest: the Aviation

Enterprise Fund, which supports Denver International Airport; the Wastewater

Management Enterprise Fund, which supports the City’s wastewater and storm water

sewer operations; the Golf Enterprise Fund, which supports operations of the City’s five

municipal golf courses; and the Environmental Services Enterprise Fund, which supports

the City’s efforts to manage environmental liability. The City’s Internal Service Funds

account for goods and services provided to City departments on a cost reimbursement

basis. Fleet, Asphalt Plant, and Workers’ Compensation are examples of Internal Service

Funds.

Fiduciary Funds—The City’s fiduciary funds comprise resources held by a government but

belonging to individuals or entities other than the City government. A prime example of a

fiduciary fund is a trust fund for a public employee pension plan.

Passage of Amendment 2A—The approved 2013 City budget improved significantly in

comparison to the last few years, in part due to the passage of Amendment 2A in

November 2012. Amendment 2A’s passage allowed the City to retain an estimated $44

million of property tax revenue that had been previously credited back to Denver

taxpayers. These funds allowed the City to enhance service levels in various areas, such

as extending the hours during which Denver’s public libraries are open, restoring child

care assistance funding, and providing free access to recreation centers and outdoor

pools for Denver students. In addition, Amendment 2A funding allowed additional

recruits for both the Denver Police Department and the Denver Fire Department. The

additional Amendment 2A funds also increased funding for the Business Incentive Fund,

2 Capital improvement funds are used for the acquisition, repair, or rehabilitation of assets that last for fifteen years or more.

Examples of major capital assets are roads, bridges, buildings, and parks.

P a g e 4

City and County of Denver

expanded the number of lane miles to be paved in the Street Paving Program,

earmarked monies for the technology infrastructure improvements, and increased the

City’s Contingency and Reserve Fund Balance.3

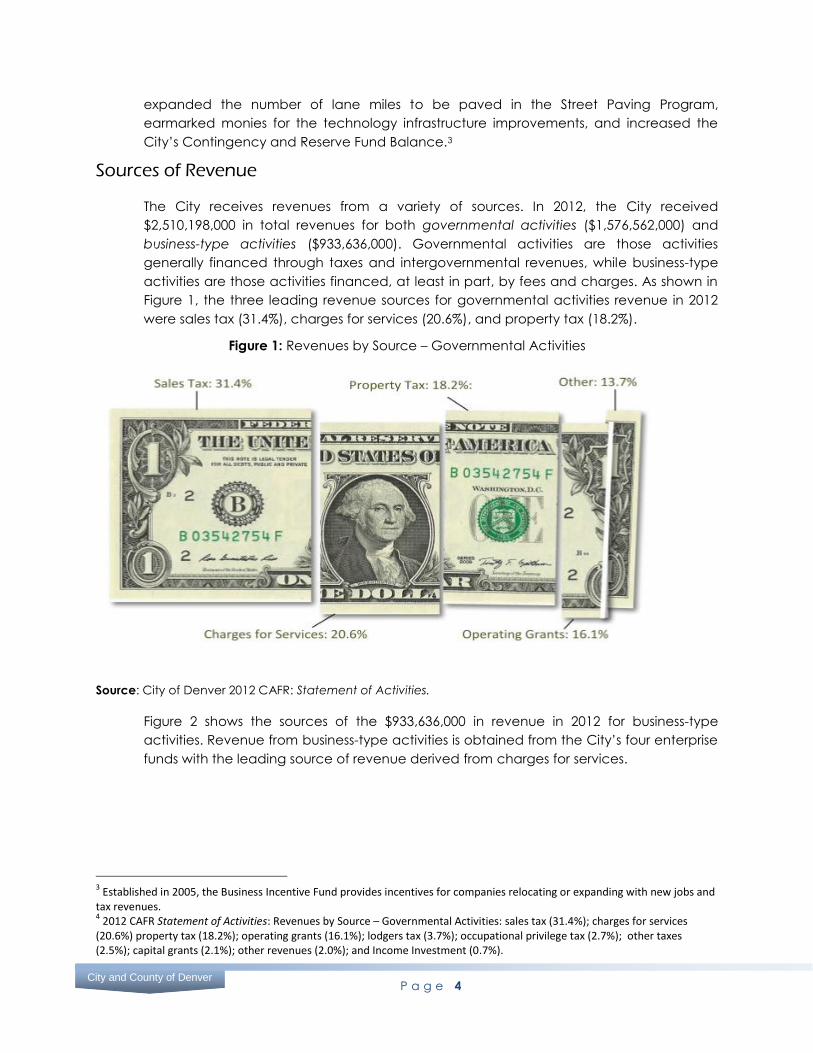

Sources of Revenue

The City receives revenues from a variety of sources. In 2012, the City received

$2,510,198,000 in total revenues for both governmental activities ($1,576,562,000) and

business-type activities ($933,636,000). Governmental activities are those activities

generally financed through taxes and intergovernmental revenues, while business-type

activities are those activities financed, at least in part, by fees and charges. As shown in

Figure 1, the three leading revenue sources for governmental activities revenue in 2012

were sales tax (31.4%), charges for services (20.6%), and property tax (18.2%).

Figure 1: Revenues by Source – Governmental Activities

Source: City of Denver 2012 CAFR: Statement of Activities.

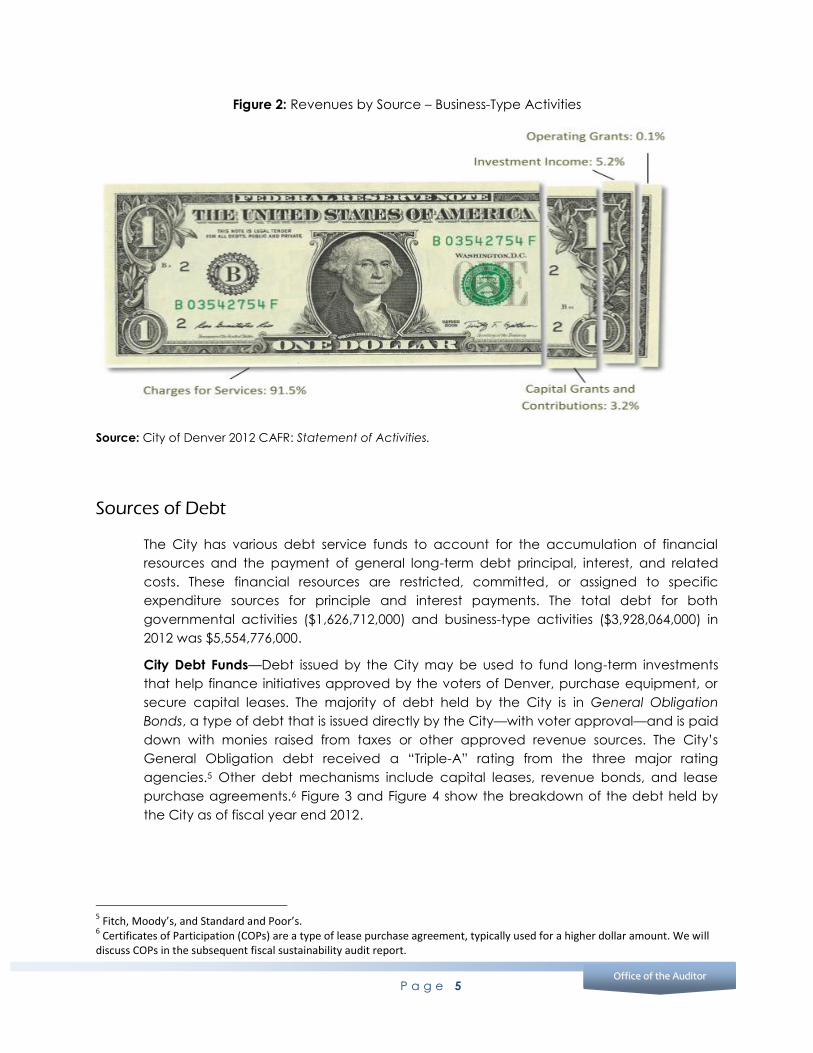

Figure 2 shows the sources of the $933,636,000 in revenue in 2012 for business-type

activities. Revenue from business-type activities is obtained from the City’s four enterprise

funds with the leading source of revenue derived from charges for services.

3 Established in 2005, the Business Incentive Fund provides incentives for companies relocating or expanding with new jobs and

tax revenues. 4 2012 CAFR Statement of Activities: Revenues by Source – Governmental Activities: sales tax (31.4%); charges for services

(20.6%) property tax (18.2%); operating grants (16.1%); lodgers tax (3.7%); occupational privilege tax (2.7%); other taxes (2.5%); capital grants (2.1%); other revenues (2.0%); and Income Investment (0.7%).

P a g e 5

Office of the Auditor OOffffiiccee ooff tthhee AAuuddiittoorr

Figure 2: Revenues by Source – Business-Type Activities

Source: City of Denver 2012 CAFR: Statement of Activities.

Sources of Debt

The City has various debt service funds to account for the accumulation of financial

resources and the payment of general long-term debt principal, interest, and related

costs. These financial resources are restricted, committed, or assigned to specific

expenditure sources for principle and interest payments. The total debt for both

governmental activities ($1,626,712,000) and business-type activities ($3,928,064,000) in

2012 was $5,554,776,000.

City Debt Funds—Debt issued by the City may be used to fund long-term investments

that help finance initiatives approved by the voters of Denver, purchase equipment, or

secure capital leases. The majority of debt held by the City is in General Obligation

Bonds, a type of debt that is issued directly by the City—with voter approval—and is paid

down with monies raised from taxes or other approved revenue sources. The City’s

General Obligation debt received a “Triple-A” rating from the three major rating

agencies.5 Other debt mechanisms include capital leases, revenue bonds, and lease

purchase agreements.6 Figure 3 and Figure 4 show the breakdown of the debt held by

the City as of fiscal year end 2012.

5 Fitch, Moody’s, and Standard and Poor’s.

6 Certificates of Participation (COPs) are a type of lease purchase agreement, typically used for a higher dollar amount. We will

discuss COPs in the subsequent fiscal sustainability audit report.

P a g e 6

City and County of Denver

Source: City of Denver 2012 CAFR: Ratios of Outstanding Debt by Type. Note: Figure shows total debt as of

December 31, 2012.

Source: City of Denver 2012 CAFR: Ratios of Outstanding Debt by Type. Note: Figure shows total debt as of

December 31, 2012.

General

Obligation bonds

55% Excise tax

revenue bonds

14%

Capital leases

27%

Unamortized

premium

3% Notes payable

1%

Figure 3: 2012 Governmental Activities $1,626,712,000

Revenue bonds 95%

Unamortized (discount)/premium

4%

Notes payable 1%

Figure 4: 2012 Business-Type Activities $3,928,064,000

P a g e 7

Office of the Auditor OOffffiiccee ooff tthhee AAuuddiittoorr

Fiscal Sustainability and Financial Condition Analysis

There is not a widely accepted standard definition for fiscal sustainability. However,

generally a city should be able to balance service demands while demonstrating it can

withstand economic downturns similar to those that occurred in 2001 and 2009. Based on

the specific needs, goals, and objectives of the municipality, fiscal sustainability can be

assessed by monitoring trends in several areas. While any number of financial indicators

may be reviewed, this audit focused on thirteen key factors, which we believe provide a

robust cross-section for determining the health, current condition, and sustainability of

the City.

Why Conduct a Financial Condition Analysis?—A fiscal sustainability analysis or financial

condition test helps determine how the City’s policy decisions impact current citizens, as

well as stakeholders such as investors. Although reviewing the financial condition of a

municipality is a complex exercise, this analysis can assist key stakeholders, such as the

Mayor’s Office, City Council, and the Department of Finance, address negative trends as

they emerge and help inform discussions involving financial and policy objectives in a

timely manner. Further, fiscal sustainability highlights whether today’s fiscal decisions

create a disproportionate impact on tomorrow’s taxpayers. Ensuring that the costs and

benefits of government services are equally borne by both present and subsequent

generations is a principle known as intergenerational equity, and is an important

component of sound fiscal policy.

While there are strengths and limitations to conducting any fiscal analysis—such as the

limited conclusions that might be drawn based on the financial indicators selected and

the fact that no assessment can account for all contributing factors, some of which are

outside of the control of the City such as population growth or stagnation—many of

these limitations can be reduced. A financial condition analysis is greatly enhanced

when combined with the monitoring of key trends over a designated period of time and

if the findings are benchmarked against municipalities with similar government structures,

funding obligations, and population size, since these entities should face similar policy

and financial decisions.

In addition to conducting benchmarking in our assessment of the City’s financial

condition, we relied heavily on CAFR data for several reasons. First, the City’s CAFR is

developed by the Controller’s Office in the Department of Finance. As noted above, the

Department of Finance plays a critical role in assessing and monitoring financial trends.

Secondly, the CAFR contains data that has been audited by a firm of certified public

accountants, under the direction of the City’s Independent Audit Committee, the

members of which attest that the financial information presented by the City is free from

material misstatement and presented in accordance with generally accepted

accounting principles (GAAP).7 This same requirement was met by each of the

benchmark cities used within this report. Therefore, rather than relying on various financial

7 The Governmental Accounting Standards Board (GASB) is the independent organization that establishes and improves

standards of accounting and financial reporting for U.S. state and local governments. GASB is recognized by governments, the accounting industry, and the capital markets as the official source of generally accepted accounting principles (GAAP) for state and local governments. GASB, accessed November 12, 2013, http://www.gasb.org/.

P a g e 8

City and County of Denver

sources, the controls surrounding the CAFR ensure that the conclusions contained within

this report are derived from audited, complete, and reliable financial data.

Transparency

Transparency is one of the cornerstones of democracy. Through greater insight into the

activities of government, citizens are better able to hold their elected officials and the

civil servants accountable for their actions. The City provides a significant amount of

financial information to citizens and other stakeholders to enhance transparency and

accountability, including the City’s Proposed and Adopted Budgets, the Comprehensive

Annual Financial Report, the Disclosure Statement to City investors, the Popular Annual

Financial Report and Citizens’ Budget, which are both intended for non-financial experts.

The City’s Transparent Denver website enhanced the City’s transparency efforts when it

came online in July 2013. The website seeks to aid citizens and other stakeholders in

understanding the City’s financial condition even better, by providing more detail on

revenues and expenditures down to the level of individual payments. Transparent Denver

further enhances the City’s efforts at a time when the City has been recognized as an

“advancing city” in the area of transparency.8

8 United States Federation of State Public Interest Research Groups. “Transparency in City Spending. Rating the Availability of

Online Government Data in America’s Largest Cities”: January 23, 2013, http://www.uspirg.org/reports/usp/tranparency-city-spending.

P a g e 9

Office of the Auditor OOffffiiccee ooff tthhee AAuuddiittoorr

SCOPE

The audit reviewed data from the City’s CAFR for the years 2002 through 2012, and also

used CAFR data from six benchmark cities—Charlotte, North Carolina; Columbus, Ohio;

Nashville, Tennessee; Portland, Oregon; San Francisco, California; and Seattle,

Washington—for the same eleven-year period. Further, audit findings reflect

transparency practices that were current as of October 23, 2013.

This report is the result of a performance audit, and was not performed as part of the

City's annual financial audit on the City's financial statements.

OBJECTIVE

The audit included four objectives, two of which will be discussed in this report and two of

which will be reported on in early 2014. This report contains the results of audit objectives

that: assessed the City’s current financial condition; and the degree to which financial

information is publicly reported in comparison to leading practice. The financial

condition analysis was not intended and should not be used as a predictive

(prospective) analysis, but rather as a broad analytical and diagnostic tool.

In addition to this report, our objective of assessing the City’s debt management

processes and ascertaining the status of recommendations made in December 2011 by

the City’s Structural Financial Task Force will be reported on in early 2014.9

METHODOLOGY

This report utilizes various standard information-gathering techniques, as well as a

comprehensive approach to assess the City’s financial condition.

Standard Techniques for Gathering Information—In keeping with our standard information

gathering approach, the audit team interviewed various officials and employees within

the Department of Finance and reviewed numerous City finance documents to develop

information for this report. Among the documents we reviewed were the City’s 2012 and

2013 budgets, the City’s CAFRs from 2002 through 2012, the management letter issued by

the City’s external auditor in May 2013, City fiscal accountability rules, the City’s debt

policy, and City Disclosure Statements. In addition to internal documents we also

reviewed numerous external documents, including fiscal sustainability or financial

condition audits from Portland, Oregon, and Lawrence, Kansas, and the financial trend

9 In 2011, Mayor Vidal appointed a Structural Financial Task Force, comprising twenty-one community, business, and civic

leaders, to address Denver’s structural budget gap. The Task Force spent approximately one year analyzing the City’s finances and in January 2012 issued nearly thirty recommendations to eliminate the ongoing budget gap.

P a g e 10

City and County of Denver

monitoring report from Golden, Colorado. We also reviewed multiple methodologies for

evaluating municipal financial condition, including approaches presented by the

International City/County Management Association (ICMA) and by an article entitled “A

Manageable System of Economic Condition Analysis for Governments.”10, 11 Finally, we

conducted an interview with Dean Mead, who developed the financial condition

assessment methodology we used (the 10-Point Test), to clarify questions regarding

usage and interpretation.12

To better understand leading practice in municipal financial transparency, we reviewed

documents from the Securities and Exchange Commission, the National Association of

State Controllers, Auditors, and Treasurers, and the United States Federation of State

Public Interest Research Groups. Further, we reviewed and analyzed the financial

reporting contained on the City’s new Transparent Denver website.

Financial Condition Assessment—To create a picture of Denver’s financial condition, we

utilized a test of ten financial indicators—the 10-Point Test—developed by Dean Mead of

GASB and outlined in Chapter 15 of the textbook entitled Public Financial

Management.13 We augmented the 10-Point Test by assessing three indicators from

ICMA’s Financial Trend Monitoring System.

For the 10-Point Test we identified six benchmark cities—Charlotte, North Carolina;

Columbus, Ohio; Nashville, Tennessee; Portland, Oregon; San Francisco, California; and

Seattle, Washington—based on their size, geographic location, type of government, and

the presence of a large enterprise fund similar to that which funds DIA.14 Each city's

CAFRs from 2002 through 2012 were obtained and specific financial condition data

collected, analyzed, and scored in comparison to other cities. We used the scoring

methodology outlined in Chapter 15 of Public Financial Management to provide an

overall assessment of the financial condition indicators of Denver and the benchmark

cities. Quartile ranges were statistically calculated for each indicator using MS Excel. The

points awarded for each of the ten ratios were then totaled and compared among the

cities. We did not develop a 10-Point Test style score for the ICMA indicators. Therefore

the results of our analysis of the ICMA indictors are presented separately in Finding 1.

10

Dean Mead. (2006). “A Manageable System of Economic Condition Analysis for Governments” in Howard Frank, ed., Public Financial Management, 383-419, Boca Raton, FL: CRC Press. 11

ICMA. (2003). Evaluating Financial Condition: A Handbook for Local Governments, 4th

ed. Washington, DC: ICMA. 12

Dean Mead is Research Manager at the GASB, overseeing the GASB’s research agenda, managing external research, interfacing with the academic community, and coordinating constituent outreach. Mead is the author of the GASB’s User Guide Series. He has published articles in journals such as Public Budgeting & Finance, Journal of Policy Analysis and Management, State and Local Government Review, Journal of Public Health Management and Practice, and Journal of Government Financial Management. He has recently contributed chapters to The Handbook of Municipal Bonds, Handbook of Local Government Fiscal Health, Management Policies in Local Government Finance, and Public Financial Management. “GASB Update: Government and Nonprofit Section American Accounting Association March 8, 2013”, accessed November 12, 2013, http://www.gasb.org/jsp/GASB/Document_C/GASBDocumentPage&cid=1176162204587. 13

Mead refined and extended the original 10-Point Test developed by Ken Brown. We used the Mead version of the test for our analysis. For more information about the Brown version see: Ken Brown. (December 1993). The 10-Point Test of Financial Condition: Toward an Easy-to-Use Assessment Tool for Smaller Cities, Government Finance Review, 21-26. (http://gfoa.org/services/dfl/bulletin/BUDGET-10-point-test.pdf) 14

Nashville, Tennessee, and San Francisco, California, are unified city-county governments, and Charlotte, North Carolina has a governmental structure that overlaps to some degree with Mecklenberg County.

P a g e 11

Office of the Auditor OOffffiiccee ooff tthhee AAuuddiittoorr

Some Limitations to Determining Comparable Data—The thirteen financial condition

indicators we assessed used reliable data from cities’ audited financial statements

(CAFRs); however, although the CAFR document is generally presented in the same way

across different cities, in a few cases we found that not all CAFR data is presented the

same for each city in each year. There were three key limitations. First, some cities

presented data differently over time due to differences in when GASB statement

changes were implemented.15 Second, deferred revenues per the Statement of Net

Assets (or Net Position) used to calculate solvency was presented as deferred revenues in

early years, unearned revenues in later years, or even deferred credits (with explanation

in notes that deferred credits included deferred revenues). Third, we noted differences

when comparing Denver to other cities in our assessment of post employment benefits

(PEB) liability and unfunded pension liability as a percentage of pension plan assets. Both

of these calculations divided the total unfunded liability into the actuarial value of assets

of the plans. However, most cities did not begin reporting PEB data in their CAFRs until

2008.

While these differences impacted our ability to ensure that we were comparing like data,

we have made efforts to validate our comparison efforts through discussions with subject

matter experts. Further, the areas in which data were presented differently among cities

made up a small percentage of the overall data set and we believe that the potential

impact of an unreliable comparison is insignificant.

15

GASB statements set the generally accepted accounting principles (GAAP) for state and local governments.

P a g e 12

City and County of Denver

10-Point Test

Financial Indicators

Favorable

1. Short-run Financial

Position

2. Liquidity

3. Financial Asset

Performance

4. Solvency

5. Primary Government

Revenues

6. Governmental

Activities Revenues

Unfavorable

7. Primary Government

Debt Burden Per

Capita

8. Governmental Funds

Debt Coverage

9. Enterprise Funds Debt

Coverage

10. Capital Assets

FINDING 1

Denver’s Financial Condition Is Promising but There Are Some Key Unfavorable Financial Indicators That Warrant Additional Attention

As of December 31, 2012, Denver’s overall financial condition is promising due to a

favorable financial position and positive revenue-related financial indicators. However,

the City also exhibits some unfavorable indicators of financial condition related to debt,

capital assets, and liabilities. Left unchecked, these unfavorable indicators may diminish

the City’s ability to provide existing services on an ongoing

basis. Implementing a periodic financial condition analysis of

the City, including benchmarking similar cities and tracking

outcomes over time, would: enhance the City’s ability to

assess and understand its overall financial health; help to

better understand how policy decisions will impact future

taxpayers; assist City management in addressing negative

trends as they emerge; and help inform timely discussions

involving the current impact of financial and policy

objectives. Furthermore, disclosing the outcome of the City’s

financial condition analysis would provide important financial

information to key stakeholders in the City, such as Denver

citizens, City Council, and investors, and further the City’s

efforts to promote transparency and accountability.

Denver’s Current and Historic Financial Condition

When compared to benchmark cities, the City of Denver’s

current financial condition improved from 2011 to 2012. This

improvement is attributable to a combination of several

financial position and revenue financial indicators, and

resulted in an increase in the overall financial condition

ranking (See Figure 5, following page). However, historic

trends were not as favorable for the eleven-year analysis

period. City management should be optimistic, yet cautious

in assuming the 2012 spike is a trend that constitutes a new

baseline in the City’s future financial performance.

Denver’s Current Financial Condition Compared to Benchmark Cities Is Promising—The

City’s 2012 overall financial condition ranking (tied for third) is at its highest level during

the eleven-year period reviewed compared to six benchmark cities (Charlotte, North

Carolina; Columbus, Ohio; Nashville, Tennessee; Portland, Oregon; San Francisco,

California; and Seattle, Washington). Further, the quick rebound from 2011’s worst-place

position compared to these benchmark cities is promising. The City’s overall financial

condition score is based on its performance in ten financial indicators outlined in

Chapter 15 of the Public Financial Management book, as compared to select

P a g e 13

Office of the Auditor OOffffiiccee ooff tthhee AAuuddiittoorr

benchmark cities. The outcomes from each of the ten financial indicators are discussed

in detail later in the audit report.

Note: Denver’s fifth-place ranking in 2007 is a tie with San Francisco and Nashville. Denver’s

sixth-place ranking in 2008 is a tie with San Francisco. Denver’s third-place ranking in 2012 is

a tie with Charlotte and San Francisco.

The City’s improvement in several financial position and revenue related financial

indicators contributed to the increase in the overall financial condition score. Since 2009,

the City’s ability to handle unforeseen resource needs over the short-term has trended

upward. The 2012 ratio is at the highest point since 2008, ranking best among benchmark

cities. Additionally, the City’s primary government revenues have decreased

dependence on intergovernmental aid. Reliance on resources from other governments

was close to its highest point prior to the most recent national economic downturn in

2009. In 2012, Denver received 10 percent of its total primary government revenue in the

form of intergovernmental operating support, such as state and federal grants, as

opposed to 15 percent in 2008, ranking Denver third best among benchmark cities.

Furthermore, since 2009, the City has reduced reliance on general revenues (primarily

taxes) and increased the self-sufficiency of basic government services. Denver’s basic

government services were 41 percent self-funded in 2012, ranking second best among

benchmark cities

While Denver’s current financial outlook is promising based on its 2012 ranking, the City

exhibits several less favorable indicators of financial condition which warrant further

analysis and inspection. For instance, only one benchmark city (San Francisco) had a

worse primary government debt burden per resident in 2012. In addition, the sufficiency

of Denver’s Enterprise Funds’ resources to repay debt ranked worst in 2012, as did the

indicator measuring whether infrastructure was being properly maintained. The City’s

unfunded pension and post-employment benefits liabilities have also grown

exponentially, and are at their highest levels in 2012. Left unchecked, these less favorable

indicators related to debt, capital assets, and liabilities may diminish the City’s ability to

provide existing service levels on an ongoing basis.

7 7

5

7 7

5

6

7

6

7

3

1

2

3

4

5

6

7

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Figure 5: Denver's Overall Financial Condition Ranking by Year (7 Cities)

P a g e 14

City and County of Denver

Denver’s Historic Financial Condition Compared to Benchmark Cities Has Been Less

Promising—Historically, the City’s financial condition as compared to six benchmark cities

has been unfavorable. Denver’s overall financial condition ranking was worst in six of the

eleven years, or 55 percent, of the analysis period: 2002, 2003, 2005, 2006, 2009, and 2011.

While several of these years represent periods of national economic downturn, this

suggests Denver did not manage the economic stress of these periods and respond as

well as the benchmark cities. In addition, there is no clear trend that can be derived from

the City’s 2002 through 2012 overall financial condition rankings, other than showing that

the City experienced wide fluctuations from year to year. Therefore, City management

should be cautious in assuming the 2012 spike is a trend that constitutes a new baseline

in the City’s future financial performance.

As explained in the audit report Methodology section, we performed a financial

condition analysis of the City and six benchmark cities. This analysis included ten financial

condition indicators (the 10-Point Test) from Chapter 15 of Public Financial Management,

written by Dean Mead of the Governmental Accounting Standards Board, and three

financial condition indicators from the International City/County Management

Association’s (ICMA) Evaluating Financial Condition handbook.16 The first ten financial

condition indicators were compared with results from the benchmark cities and

reviewed over an eleven-year period (2002 through 2012). The three additional indicators

were also reviewed over the same eleven-year period (2002 through 2012) but not

measured against benchmark cities due to the lack of comparable information for all

three indicators. For example, post-employment health benefits (PEHB) liability data was

presented by Denver for the entire eleven-year analysis period, but for only five years by

most of the benchmark cities. In addition, PEHB plan and pension plan liabilities varied

greatly based on whether most city employees participated in a city-established plan

like Denver or in a state-established plan like Columbus. Cities whose employees

participate in a state-established plan contribute to the plan but do not incur liability.

The results of the 10-Point Test and our additional analysis are documented in the

following three sections: 10-Point Test Financial Indicators with Favorable Results; 10-Point

Test Financial Indicators with Unfavorable Results; and Results of Three Additional

Financial Indicator Analyses.

16

ICMA. (2003). Evaluating Financial Condition: A Handbook for Local Governments, 4th

ed. Washington, DC: ICMA.

P a g e 15

Office of the Auditor OOffffiiccee ooff tthhee AAuuddiittoorr

HOW TO READ THE 10-POINT TEST FINANCIAL INDICATORS RESULTS

Financial ratios were calculated for Denver and each of the benchmark cities.

The average ratio of benchmark cities was then determined. The average

benchmark and Denver’s ratios are presented as graphs throughout both this

section and the next section, entitled 10-Point Test Financial Indicators with

Unfavorable Results. Denver’s ratios are presented in column form, while the

average of benchmark cities is presented in line form. All graphs are displayed

to present a higher chart position as better. Therefore, if Denver’s column is

higher than the average benchmark line, Denver’s performance was better

than the average. In order to present chart position in this manner, the y-axis of

some graphs has been inverted.

10-Point Test Financial Indicators with Favorable Results

The financial condition analysis determined the City displayed favorable results for six

indicators. These favorable indicators contributed to Denver’s 2012 increase in overall

ranking—tied for third—compared to benchmark cities. Indicators with favorable results

included:

Financial Position—Financial position is a government’s financial standing at a

given point in time. Financial position is measured by four indicators: (1) short-run

financial position, (2) liquidity, (3) financial performance, and (4) solvency.

Revenues—Revenues determine the capacity of a city to provide services.

Revenues are measured by two indicators: (5) primary government revenues and

(6) governmental activities revenues.

P a g e 16

City and County of Denver

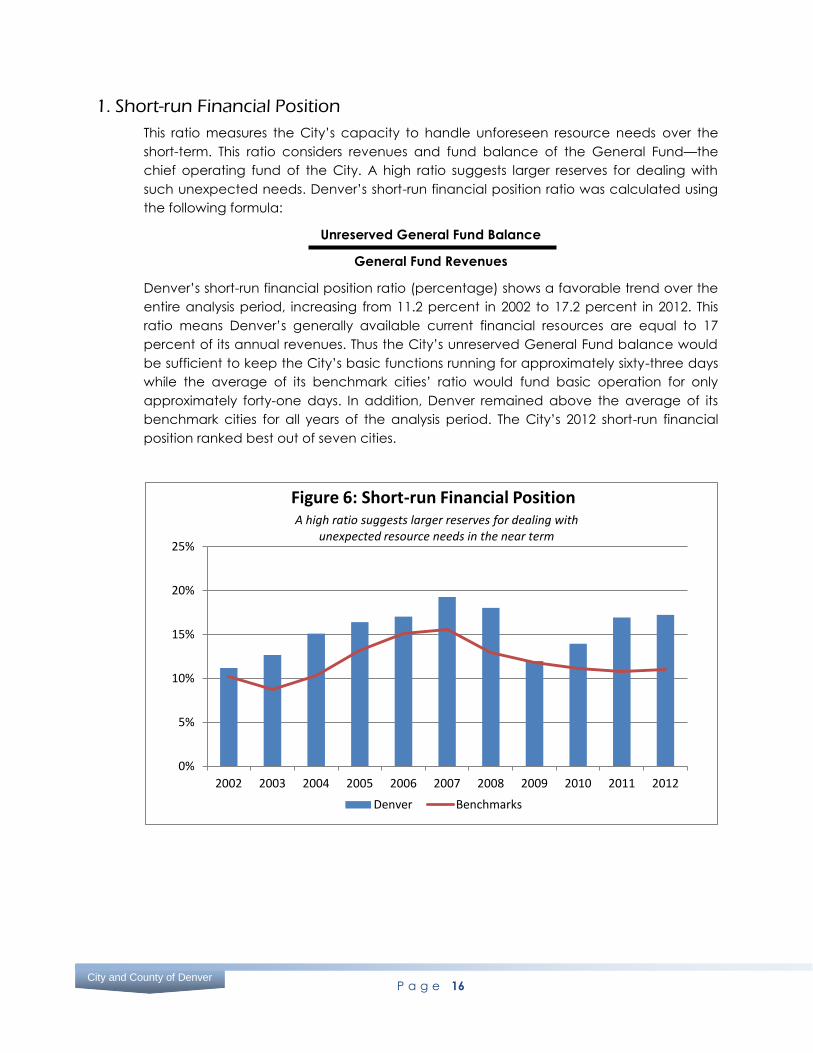

1. Short-run Financial Position

This ratio measures the City’s capacity to handle unforeseen resource needs over the

short-term. This ratio considers revenues and fund balance of the General Fund—the

chief operating fund of the City. A high ratio suggests larger reserves for dealing with

such unexpected needs. Denver’s short-run financial position ratio was calculated using

the following formula:

Unreserved General Fund Balance

General Fund Revenues

Denver’s short-run financial position ratio (percentage) shows a favorable trend over the

entire analysis period, increasing from 11.2 percent in 2002 to 17.2 percent in 2012. This

ratio means Denver’s generally available current financial resources are equal to 17

percent of its annual revenues. Thus the City’s unreserved General Fund balance would

be sufficient to keep the City’s basic functions running for approximately sixty-three days

while the average of its benchmark cities’ ratio would fund basic operation for only

approximately forty-one days. In addition, Denver remained above the average of its

benchmark cities for all years of the analysis period. The City’s 2012 short-run financial

position ranked best out of seven cities.

0%

5%

10%

15%

20%

25%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Figure 6: Short-run Financial Position

Denver Benchmarks

A high ratio suggests larger reserves for dealing with unexpected resource needs in the near term

P a g e 17

Office of the Auditor OOffffiiccee ooff tthhee AAuuddiittoorr

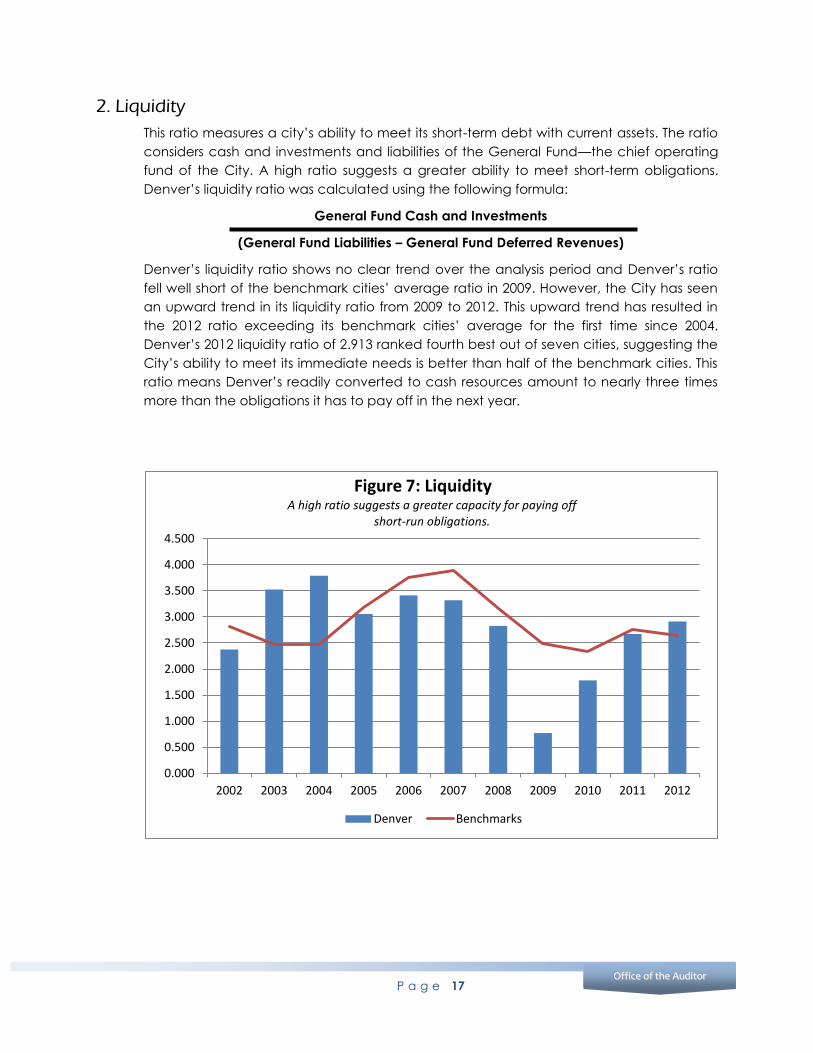

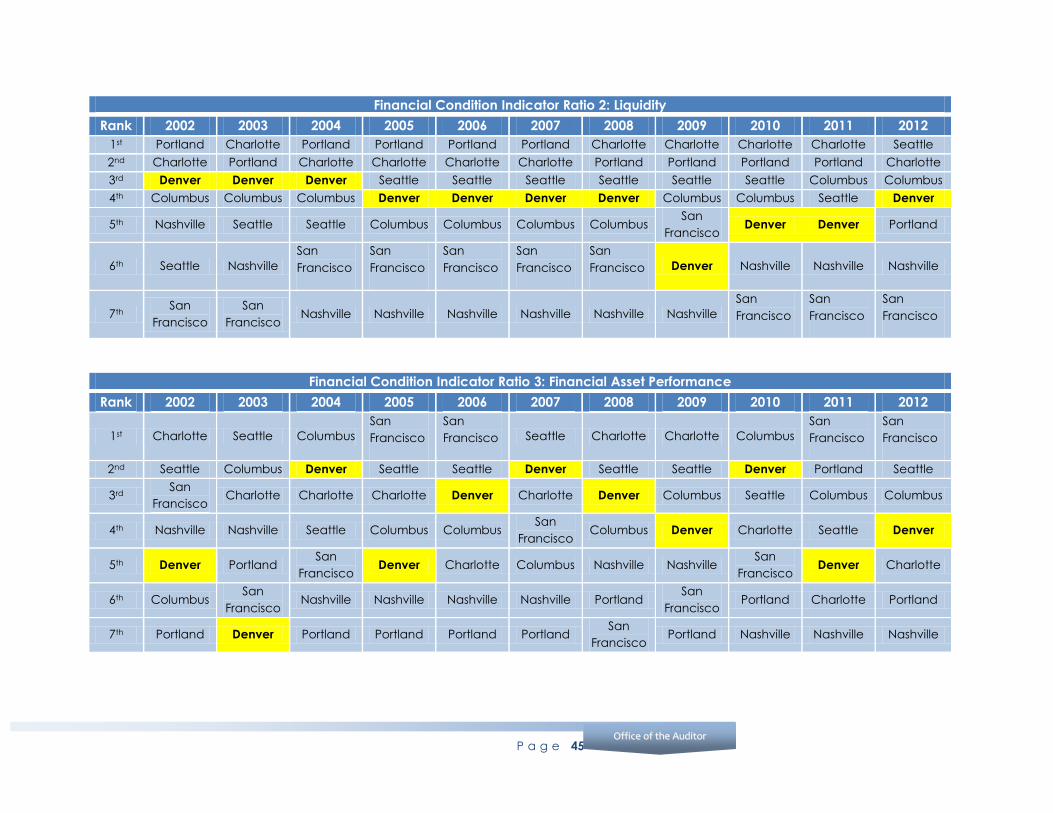

2. Liquidity

This ratio measures a city’s ability to meet its short-term debt with current assets. The ratio

considers cash and investments and liabilities of the General Fund—the chief operating

fund of the City. A high ratio suggests a greater ability to meet short-term obligations.

Denver’s liquidity ratio was calculated using the following formula:

General Fund Cash and Investments

(General Fund Liabilities – General Fund Deferred Revenues)

Denver’s liquidity ratio shows no clear trend over the analysis period and Denver’s ratio

fell well short of the benchmark cities’ average ratio in 2009. However, the City has seen

an upward trend in its liquidity ratio from 2009 to 2012. This upward trend has resulted in

the 2012 ratio exceeding its benchmark cities’ average for the first time since 2004.

Denver’s 2012 liquidity ratio of 2.913 ranked fourth best out of seven cities, suggesting the

City’s ability to meet its immediate needs is better than half of the benchmark cities. This

ratio means Denver’s readily converted to cash resources amount to nearly three times

more than the obligations it has to pay off in the next year.

0.000

0.500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Figure 7: Liquidity

Denver Benchmarks

A high ratio suggests a greater capacity for paying off short-run obligations.

P a g e 18

City and County of Denver

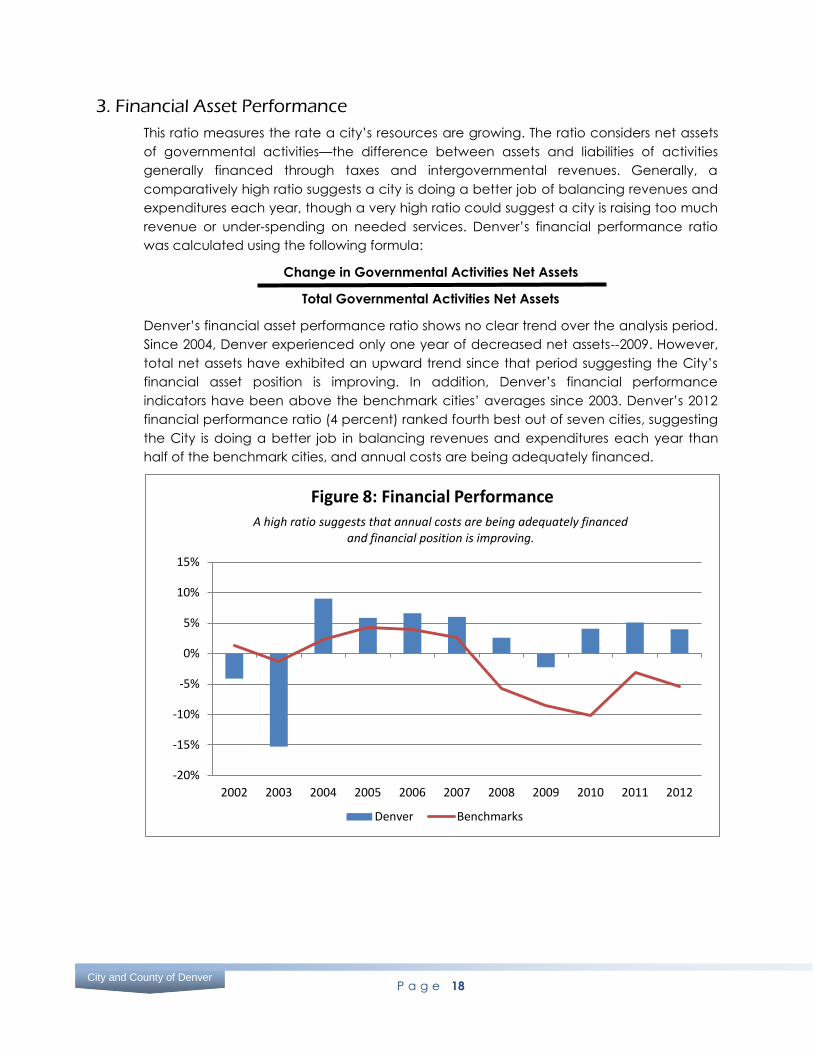

3. Financial Asset Performance

This ratio measures the rate a city’s resources are growing. The ratio considers net assets

of governmental activities—the difference between assets and liabilities of activities

generally financed through taxes and intergovernmental revenues. Generally, a

comparatively high ratio suggests a city is doing a better job of balancing revenues and

expenditures each year, though a very high ratio could suggest a city is raising too much

revenue or under-spending on needed services. Denver’s financial performance ratio

was calculated using the following formula:

Change in Governmental Activities Net Assets

Total Governmental Activities Net Assets

Denver’s financial asset performance ratio shows no clear trend over the analysis period.

Since 2004, Denver experienced only one year of decreased net assets--2009. However,

total net assets have exhibited an upward trend since that period suggesting the City’s

financial asset position is improving. In addition, Denver’s financial performance

indicators have been above the benchmark cities’ averages since 2003. Denver’s 2012

financial performance ratio (4 percent) ranked fourth best out of seven cities, suggesting

the City is doing a better job in balancing revenues and expenditures each year than

half of the benchmark cities, and annual costs are being adequately financed.

-20%

-15%

-10%

-5%

0%

5%

10%

15%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Figure 8: Financial Performance

Denver Benchmarks

A high ratio suggests that annual costs are being adequately financed and financial position is improving.

P a g e 19

Office of the Auditor OOffffiiccee ooff tthhee AAuuddiittoorr

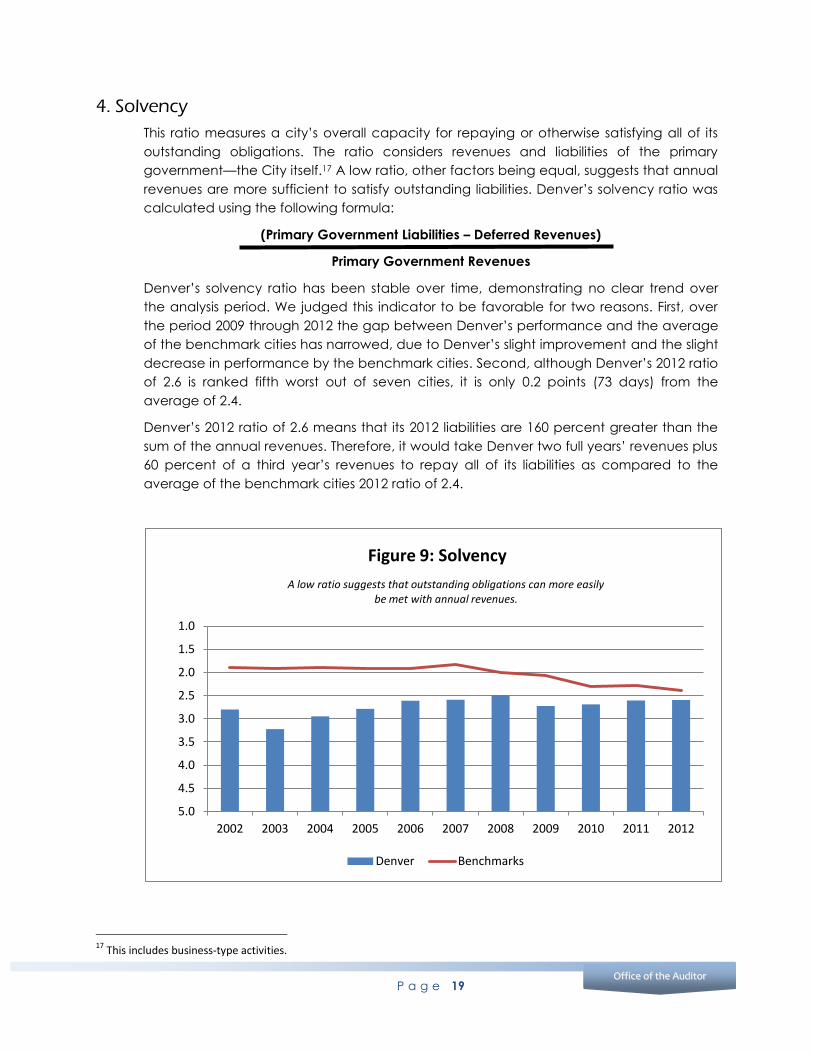

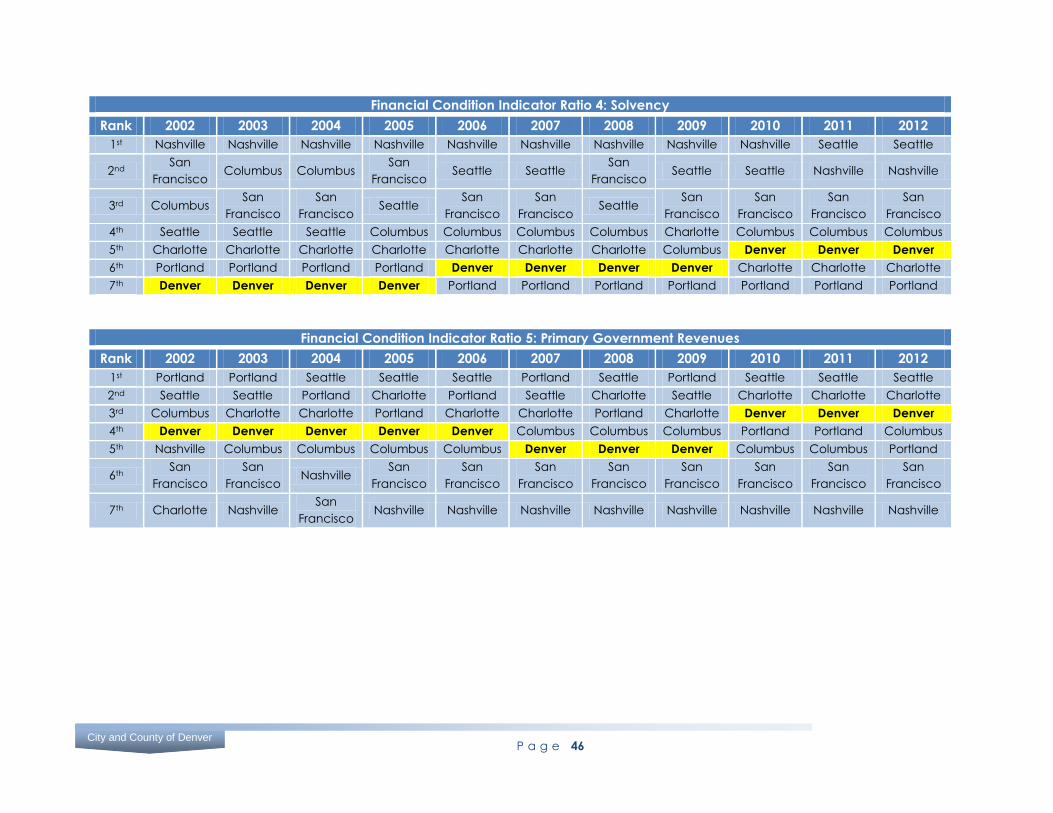

4. Solvency

This ratio measures a city’s overall capacity for repaying or otherwise satisfying all of its

outstanding obligations. The ratio considers revenues and liabilities of the primary

government—the City itself.17 A low ratio, other factors being equal, suggests that annual

revenues are more sufficient to satisfy outstanding liabilities. Denver’s solvency ratio was

calculated using the following formula:

(Primary Government Liabilities – Deferred Revenues)

Primary Government Revenues

Denver’s solvency ratio has been stable over time, demonstrating no clear trend over

the analysis period. We judged this indicator to be favorable for two reasons. First, over

the period 2009 through 2012 the gap between Denver’s performance and the average

of the benchmark cities has narrowed, due to Denver’s slight improvement and the slight

decrease in performance by the benchmark cities. Second, although Denver’s 2012 ratio

of 2.6 is ranked fifth worst out of seven cities, it is only 0.2 points (73 days) from the

average of 2.4.

Denver’s 2012 ratio of 2.6 means that its 2012 liabilities are 160 percent greater than the

sum of the annual revenues. Therefore, it would take Denver two full years’ revenues plus

60 percent of a third year’s revenues to repay all of its liabilities as compared to the

average of the benchmark cities 2012 ratio of 2.4.

17

This includes business-type activities.

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Figure 9: Solvency

Denver Benchmarks

A low ratio suggests that outstanding obligations can more easily be met with annual revenues.

P a g e 20

City and County of Denver

5. Primary Government Revenues

This ratio measures the flexibility of a city’s revenues. The ratio considers different sources

of revenues of the primary government—the City itself.18 Operating grants and

contributions include monies from other governmental agencies to be used for specific

programs or functions, while unrestricted aid is monies from other governmental

agencies that are not restricted for specific programs or functions. The ratio examines the

City’s reliance on resources from other governments which are largely outside the City’s

control. A low ratio suggests a city is not heavily reliant on intergovernmental aid.

Denver’s primary government revenues ratio was calculated using the following formula:

(Primary Government Operating Grants and Contributions + Unrestricted Aid)

Total Primary Government Revenues

Denver’s primary government revenue ratio shows a favorable trend over the analysis

period, decreasing from a percentage of 15.6 in 2002 to 10.1 in 2012. While Denver was

below the average of benchmark cities prior to 2010, it has consistently performed better

than the average since this year. This means the City is not as heavily reliant on

intergovernmental aid as the average of benchmark cities. In 2012 Denver received 10

percent of its total revenues in the form of intergovernmental operating supporting,

which ranked third best of seven cities.19

18

This includes business-type activities. 19

A November 2013 report from the Pew Charitable Trust entitled America’s Big Cities in Volatile Times: Meeting Fiscal Challenges and Preparing for the Future underscored the importance of municipal self-sufficiency. The Pew study found that cities relying more on intergovernmental aid typically suffered more severe economic declines from 2010-2012.(http://www.pewstates.org/research/reports)

6%

8%

10%

12%

14%

16%

18%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Figure 10: Primary Government Revenues

Denver Benchmarks

A low ratio suggests a government is not heavily reliant on intergovernmental aid.

P a g e 21

Office of the Auditor OOffffiiccee ooff tthhee AAuuddiittoorr

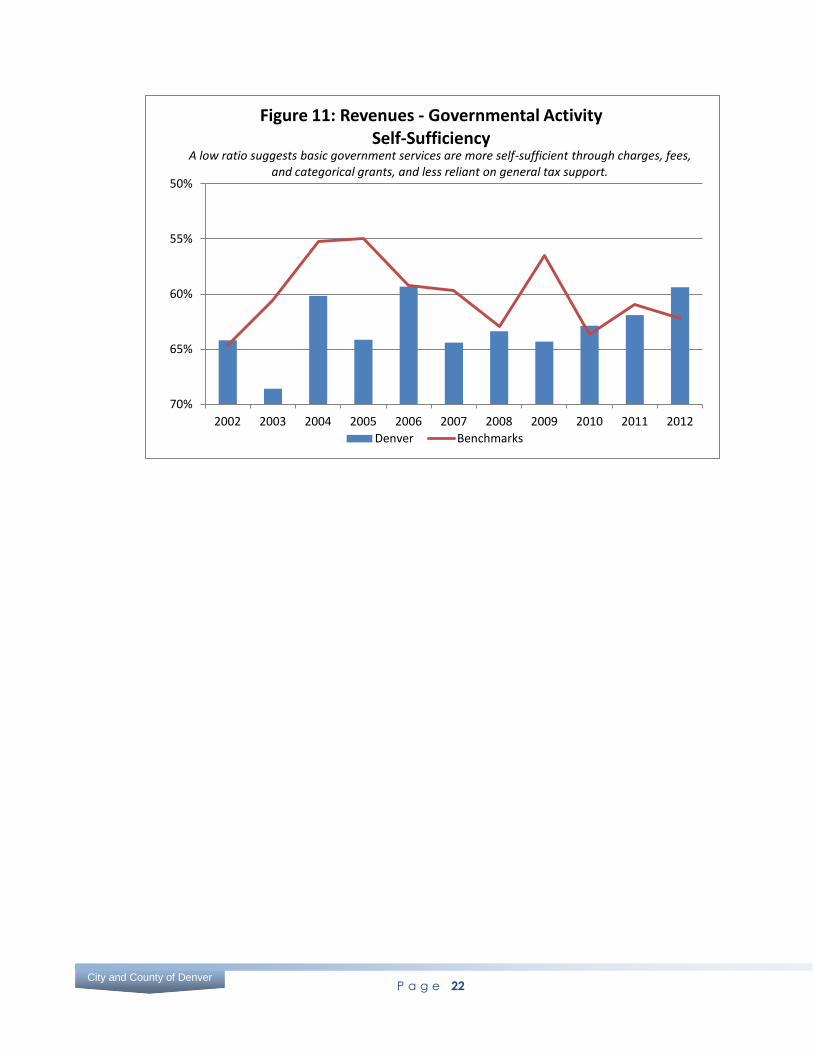

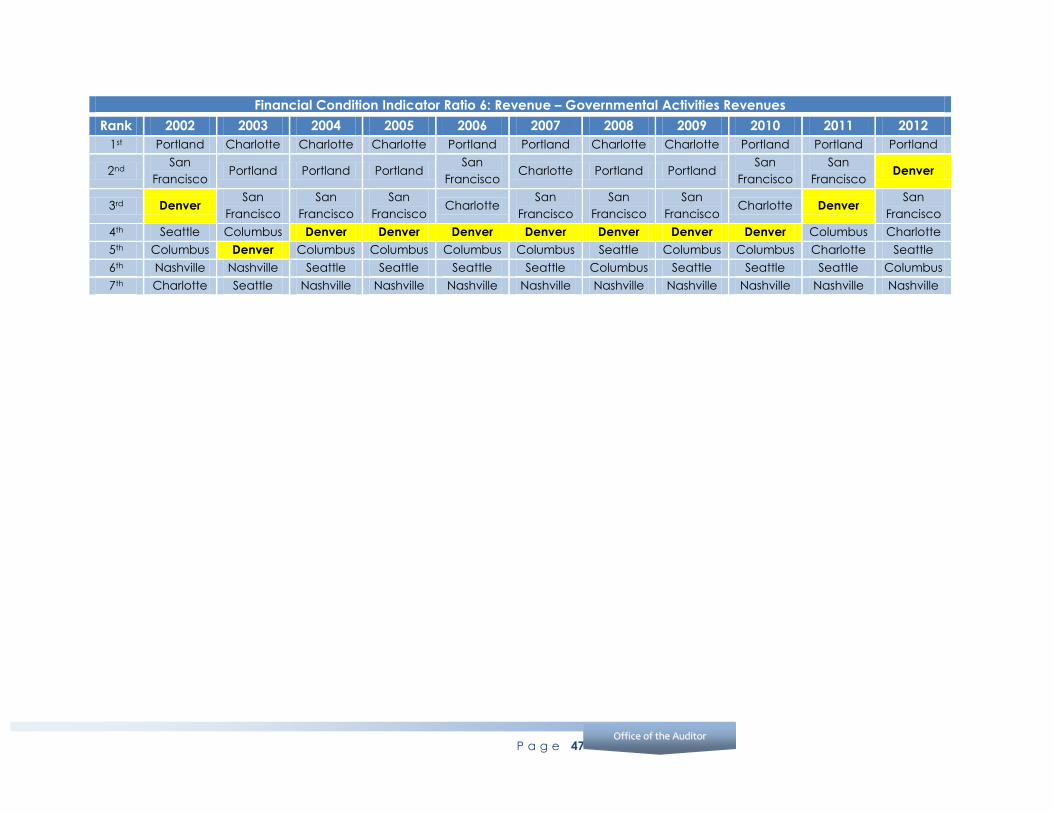

6. Governmental Activities Revenues

This ratio presents information about revenue sufficiency and the use of governmental

revenues. The ratio considers expenses and program revenues for governmental

activities—those activities generally financed through taxes and intergovernmental

revenues. When governmental activities expenses exceed revenues raised by a City

from charges, fees, and grants, the result is a net expense, and additional funding must

be provided by general revenues to support the activities. Therefore, this ratio shows the

degree to which governmental activities’ functions and programs are self-financed or

the degree to which they depend on financing from governmental revenues, primarily

taxes. A low ratio suggests services are less reliant on general revenue financing and are

more self-supporting through charges for services, grants, and contributions. Denver’s

governmental activities revenues ratio was calculated using the following formula:

Net (Expense) Revenue for Governmental Activities

Total Governmental Activities Expense

While Denver’s governmental activities revenue ratio shows no clear trend over the

analysis period, there has been an upward trend since 2009. Specifically, Denver’s

percentage of governmental activities supported by general taxes decreased from 64.3

in 2009 to 59.4 in 2012. Denver’s 2012 ratio means that 59 percent of the expenses of

Denver’s 2012 governmental activities functions and programs were financed with taxes

and other revenues while 41 percent were self-funded through charges for services,

grants, and contributions. Denver’s 2012 ratio was lower than the benchmark average,

suggesting the City’s governmental activities are more self-sufficient than the average.

Denver ranks second best of seven cities for 2012.

X -1

P a g e 22

City and County of Denver

50%

55%

60%

65%

70%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Figure 11: Revenues - Governmental Activity Self-Sufficiency

Denver Benchmarks

A low ratio suggests basic government services are more self-sufficient through charges, fees, and categorical grants, and less reliant on general tax support.

P a g e 23

Office of the Auditor OOffffiiccee ooff tthhee AAuuddiittoorr

10-Point Test Financial Indicators with Unfavorable Results

The financial condition analysis determined that several indicators displayed unfavorable

results. These unfavorable indicators contributed to Denver’s low overall rankings most

years of the analysis period and continued to be problem indicators in 2012. The

indicators warrant further analysis and monitoring by the Chief Financial Officer (CFO) to

determine why the financial condition ratios exhibit weak financial performance and

what policy decisions can be made to mitigate the weaknesses.

There were four indicators with unfavorable results, which we grouped under debt and

capital assets.

Debt Indicators—Three debt indicators were calculated for the financial condition

analysis: (7) debt burden per capita and (8, 9) debt coverage. Debt burden per capita

was calculated separately for the primary government and governmental activities,

while debt coverage was calculated separately for governmental funds and enterprise

funds. The debt burden inputs calculated for the financial condition analysis include

general obligation bonds, revenue bonds, certificates of participation (COP), and

capital leases as long-term liabilities.

Capital Assets—One (10) capital asset indicator was calculated. Capital funding is

necessary for the ongoing maintenance and repair of the City’s current capital assets

and future infrastructure enhancements and additions. According to the City’s Six-Year

Capital Improvement Plan, Denver is committed to the ongoing maintenance and repair

of capital assets, recognizing the critical value of infrastructure to the economic,

aesthetic, and functional viability of the City. Many of the City’s capital asset projects are

funded through long-term debt mechanisms.

P a g e 24

City and County of Denver

7. Primary Government Debt Burden Per Capita

This ratio indicates the level of debt burden on a city’s residents. The ratio considers the

long-term debt of the primary government—the City itself. A low ratio suggests there is

less debt burden imposed on taxpayers and a greater potential capacity for additional

borrowing. Denver’s primary government debt burden per capita ratio was calculated

using the following formula:

Total Outstanding Primary Government Long-Term Debt

Population

Denver’s primary government debt burden ratio shows no clear trend for the analysis

period; however, as compared to the average of the benchmark cities’ primary

government debt burden, it is considered less favorable. In 2012, the total outstanding

debt per resident was $8,758, which ranked sixth worst out of seven cities, suggesting

Denver has a higher debt burden per resident and less capacity for additional

borrowing. Approximately 69 percent of Denver’s 2012 primary government long-term

debt belonged to the Denver International Airport (DIA) Aviation Enterprise Fund.20

Denver’s high debt burden ratio over the analysis period compared to benchmark cities

is an area of potential concern that the CFO should further analyze and monitor.

20

DIA’s debt represents 98 percent of all debt related to business-type activities (i.e. enterprise funds).

$0

$2,000

$4,000

$6,000

$8,000

$10,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Figure 12: Primary Government Debt Burden Per Capita

Denver Benchmarks

A low ratio suggests less burden on taxpayers and greater capacity for additional borrowing.

P a g e 25

Office of the Auditor OOffffiiccee ooff tthhee AAuuddiittoorr

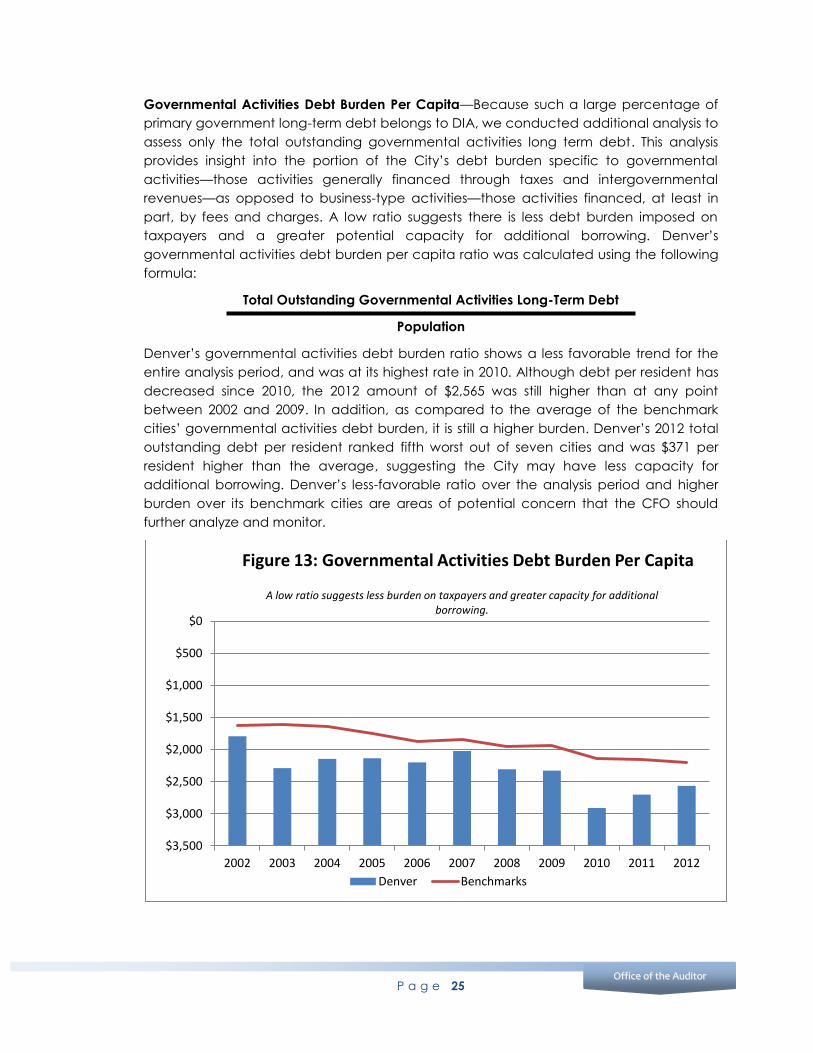

Governmental Activities Debt Burden Per Capita—Because such a large percentage of

primary government long-term debt belongs to DIA, we conducted additional analysis to

assess only the total outstanding governmental activities long term debt. This analysis

provides insight into the portion of the City’s debt burden specific to governmental

activities—those activities generally financed through taxes and intergovernmental

revenues—as opposed to business-type activities—those activities financed, at least in

part, by fees and charges. A low ratio suggests there is less debt burden imposed on

taxpayers and a greater potential capacity for additional borrowing. Denver’s

governmental activities debt burden per capita ratio was calculated using the following

formula:

Total Outstanding Governmental Activities Long-Term Debt

Population

Denver’s governmental activities debt burden ratio shows a less favorable trend for the

entire analysis period, and was at its highest rate in 2010. Although debt per resident has

decreased since 2010, the 2012 amount of $2,565 was still higher than at any point

between 2002 and 2009. In addition, as compared to the average of the benchmark

cities’ governmental activities debt burden, it is still a higher burden. Denver’s 2012 total

outstanding debt per resident ranked fifth worst out of seven cities and was $371 per

resident higher than the average, suggesting the City may have less capacity for

additional borrowing. Denver’s less-favorable ratio over the analysis period and higher

burden over its benchmark cities are areas of potential concern that the CFO should

further analyze and monitor.

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Figure 13: Governmental Activities Debt Burden Per Capita

Denver Benchmarks

A low ratio suggests less burden on taxpayers and greater capacity for additional borrowing.

P a g e 26

City and County of Denver

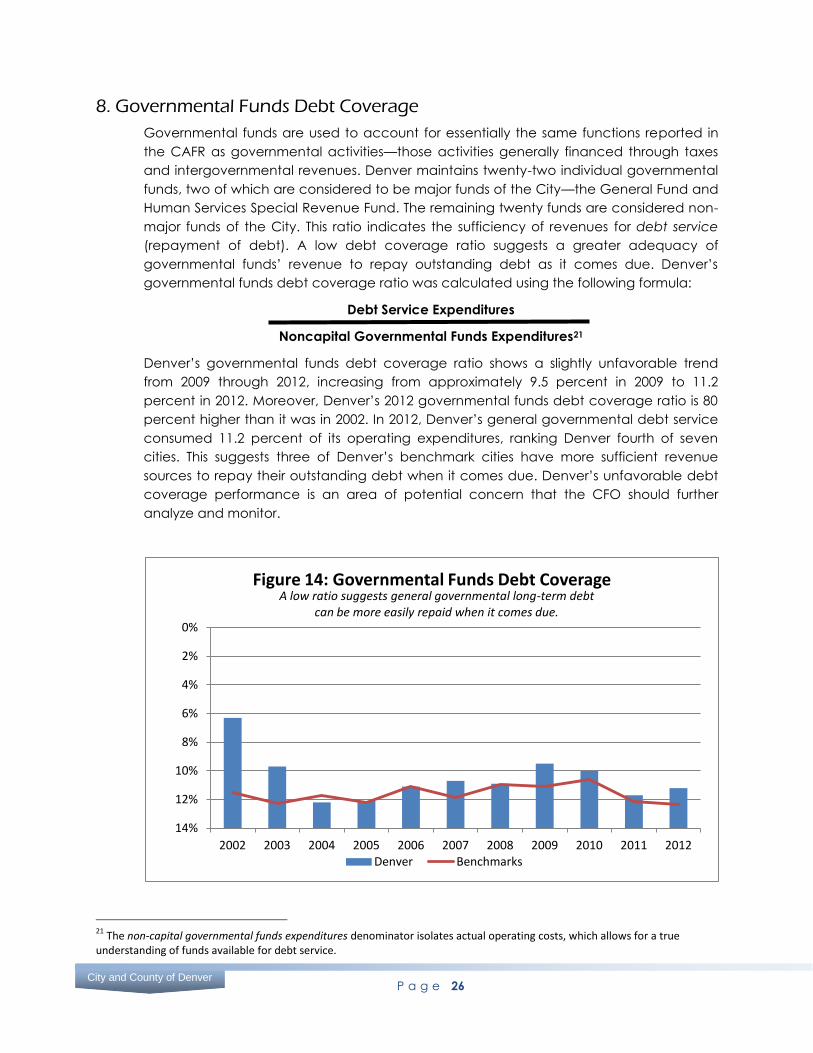

8. Governmental Funds Debt Coverage

Governmental funds are used to account for essentially the same functions reported in

the CAFR as governmental activities—those activities generally financed through taxes

and intergovernmental revenues. Denver maintains twenty-two individual governmental

funds, two of which are considered to be major funds of the City—the General Fund and

Human Services Special Revenue Fund. The remaining twenty funds are considered non-

major funds of the City. This ratio indicates the sufficiency of revenues for debt service

(repayment of debt). A low debt coverage ratio suggests a greater adequacy of

governmental funds’ revenue to repay outstanding debt as it comes due. Denver’s

governmental funds debt coverage ratio was calculated using the following formula:

Debt Service Expenditures

Noncapital Governmental Funds Expenditures21

Denver’s governmental funds debt coverage ratio shows a slightly unfavorable trend

from 2009 through 2012, increasing from approximately 9.5 percent in 2009 to 11.2

percent in 2012. Moreover, Denver’s 2012 governmental funds debt coverage ratio is 80

percent higher than it was in 2002. In 2012, Denver’s general governmental debt service

consumed 11.2 percent of its operating expenditures, ranking Denver fourth of seven

cities. This suggests three of Denver’s benchmark cities have more sufficient revenue

sources to repay their outstanding debt when it comes due. Denver’s unfavorable debt

coverage performance is an area of potential concern that the CFO should further

analyze and monitor.

21

The non-capital governmental funds expenditures denominator isolates actual operating costs, which allows for a true understanding of funds available for debt service.

0%

2%

4%

6%

8%

10%

12%

14%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Figure 14: Governmental Funds Debt Coverage

Denver Benchmarks

A low ratio suggests general governmental long-term debt can be more easily repaid when it comes due.

P a g e 27

Office of the Auditor OOffffiiccee ooff tthhee AAuuddiittoorr

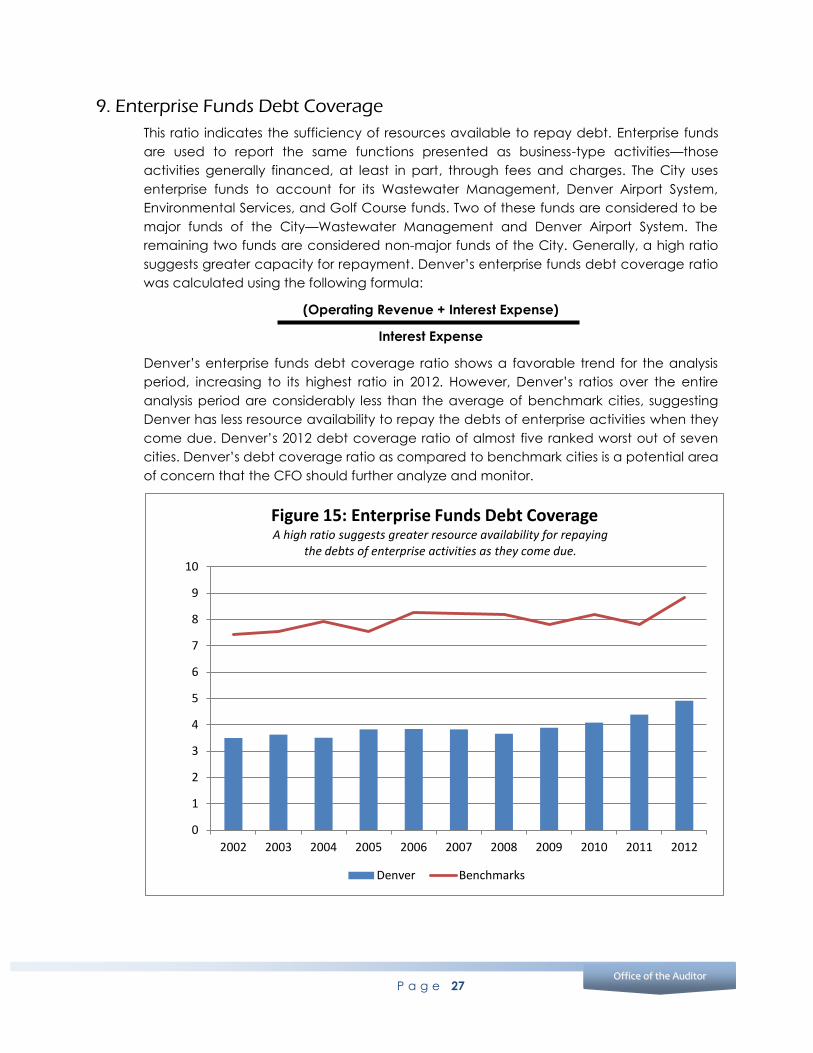

9. Enterprise Funds Debt Coverage

This ratio indicates the sufficiency of resources available to repay debt. Enterprise funds

are used to report the same functions presented as business-type activities—those

activities generally financed, at least in part, through fees and charges. The City uses

enterprise funds to account for its Wastewater Management, Denver Airport System,

Environmental Services, and Golf Course funds. Two of these funds are considered to be

major funds of the City—Wastewater Management and Denver Airport System. The

remaining two funds are considered non-major funds of the City. Generally, a high ratio

suggests greater capacity for repayment. Denver’s enterprise funds debt coverage ratio

was calculated using the following formula:

(Operating Revenue + Interest Expense)

Interest Expense

Denver’s enterprise funds debt coverage ratio shows a favorable trend for the analysis

period, increasing to its highest ratio in 2012. However, Denver’s ratios over the entire

analysis period are considerably less than the average of benchmark cities, suggesting

Denver has less resource availability to repay the debts of enterprise activities when they

come due. Denver’s 2012 debt coverage ratio of almost five ranked worst out of seven

cities. Denver’s debt coverage ratio as compared to benchmark cities is a potential area

of concern that the CFO should further analyze and monitor.

0

1

2

3

4

5

6

7

8

9

10

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Figure 15: Enterprise Funds Debt Coverage

Denver Benchmarks

A high ratio suggests greater resource availability for repaying the debts of enterprise activities as they come due.

P a g e 28

City and County of Denver

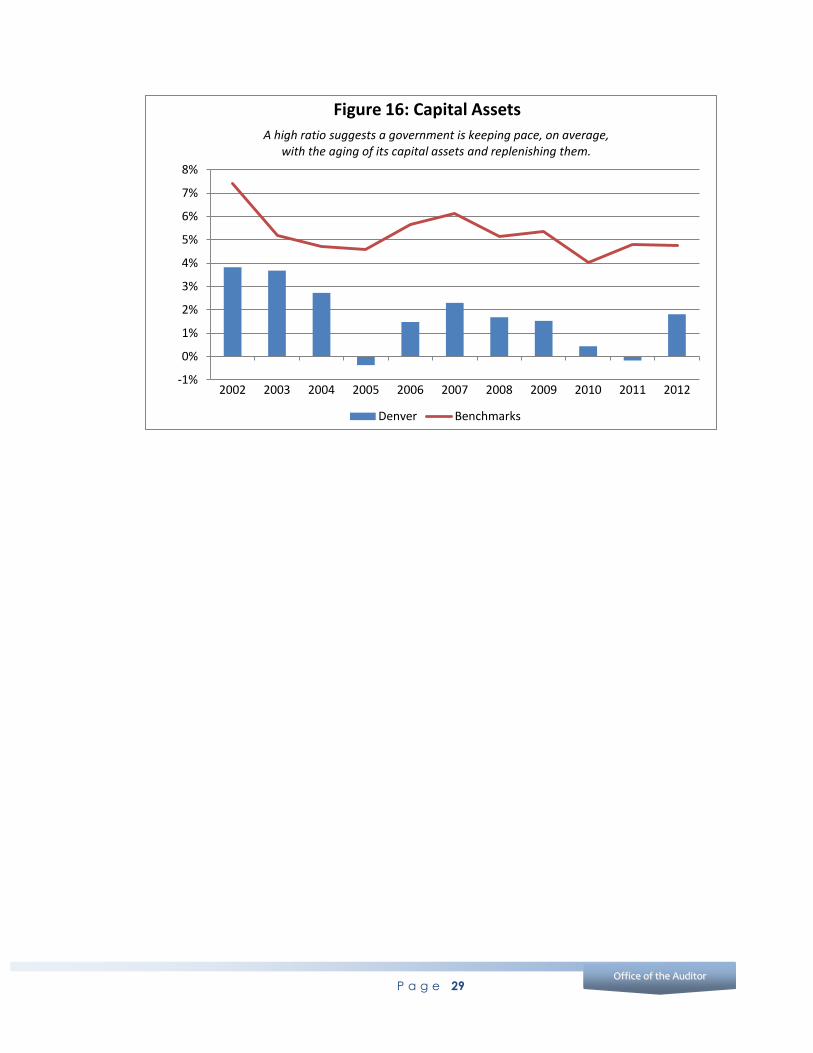

10. Capital Assets

The City’s capital assets include buildings and improvements; motor vehicles and

motorized equipment; furniture, machinery, and other equipment; collections; library

books; and infrastructure. This ratio measures whether capital assets are being properly

maintained. It is an indicator of whether a city’s investment in purchasing or constructing

new assets and refurbishing old assets is keeping pace with the rate of depreciation and

disposal of assets. A positive percentage change suggests the capital stock is being

replenished while a negative number suggests the capital stock is being depleted.

Therefore, a high ratio suggests a government is keeping pace, on average, with the

aging of its capital assets and replenishing them as necessary. Denver’s capital assets

ratio was calculated using the following formula:

(Primary Government Capital Assets Ending Net Value – Beginning Net Value)

Beginning Net Value

Denver’s capital assets ratio shows an unfavorable trend for the analysis period. In

addition, Denver’s ratios were consistently lower than the average of benchmark cities

during this time. Furthermore, in both 2005 and 2011, Denver had negative percentage

changes suggesting the City has not always kept pace with the aging of its capital assets

or replenished them as necessary. Denver’s 2012 capital assets ratio of .018 ranked worst

out of seven cities, and has continually ranked worst since 2005. While this ratio means

that the net value of the City’s capital assets increased 1.8 percent over the previous

year, the: unfavorable trend over the analysis period, lower than average ratios as

compared to benchmark cities, and the negative percentage change in 2011 are areas

of potential concern that the CFO should further analyze and monitor.

This indicator may be of particular concern given the already high debt burden imposed

on residents when considering that many of the City’s capital asset projects are funded

through long-term debt mechanisms. For example, in November 2007, Denver voters

authorized up to $550 million in “Better Denver” general obligation bonds related to 319

different capital improvement projects. In addition, the City has routinely issued COPs—

which do not require the vote of the people—to expand City buildings and property,

such as the Webb Municipal Office Building, Central Platte Campus Facility, and the

Blair-Caldwell African American Research Library, increasing the debt burden on

taxpayers.

P a g e 29

Office of the Auditor OOffffiiccee ooff tthhee AAuuddiittoorr

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Figure 16: Capital Assets

Denver Benchmarks

A high ratio suggests a government is keeping pace, on average, with the aging of its capital assets and replenishing them.

P a g e 30

City and County of Denver

Results of Three Additional Financial Indicator Analyses

Based on our research into financial condition analysis and our assessment of financial

trends for local governments, we determined that it would be appropriate to review

some indicators not included in the 10-Point Test. Therefore, we augmented the 10-Point

Test by assessing three indicators from the International City/County Management

Association’s (ICMA’s) Financial Trend Monitoring System that cover expenditures,

pension benefits liabilities, and non-pension post-employment benefit liabilities. We did

not develop a score for these indicators. Therefore the results of our analysis of the ICMA

indictors are presented separately from the results of the 10-Point Test. These three

additional indicators were reviewed over an eleven-year period (2002 through 2012) but

not measured against benchmark cities, thus the results discuss Denver’s performance

only. Please note that the three indicators have six subcomponents, and the reader will

see ratios and graphs for each of these six subcomponents. Indicators assessed included:

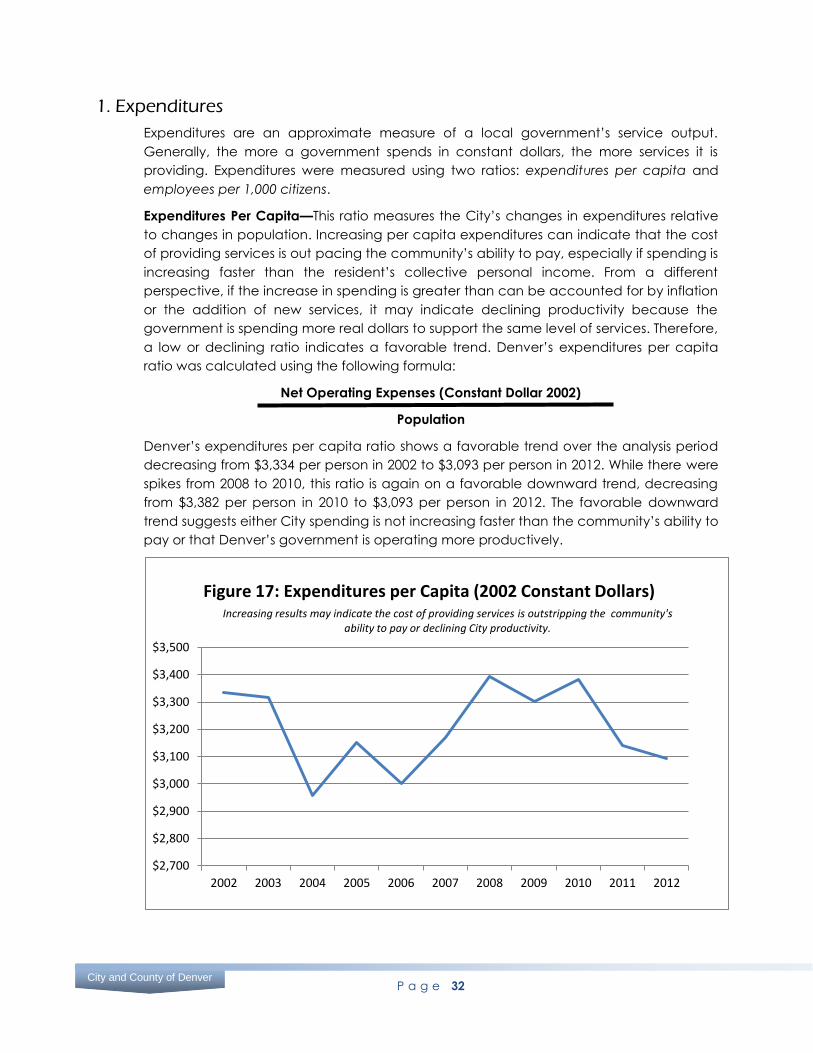

Expenditures—Expenditures are an approximate measure of a local government’s

service output. Generally, the more a government spends in constant dollars, the more

services it is providing. However, this formula does not take into account how effective

the services are or how efficiently they are delivered. Analyzing a city’s expenditure

profile aids in identifying issues related to:

Excessive expenditure growth compared to revenue or program growth that

creates future liabilities

An undesirable increase in fixed costs

Ineffective budgetary controls

A decline in personnel productivity

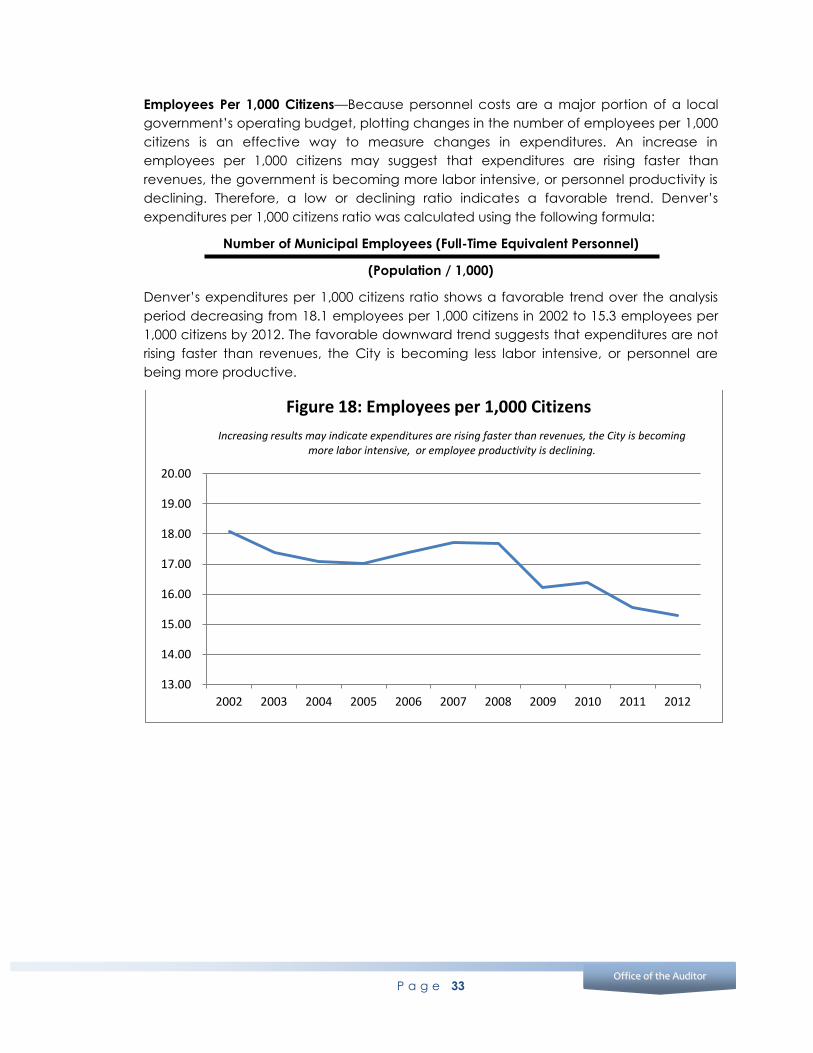

Expenditures were measured using two ratios: expenditures per capita and employees

per capita. Figures 17 and 18 display Denver’s performance related to expenditures.

Unlike the other figures in the finding, these two figures do not convey that a higher chart

position is synonymous with better performance, since these analyses are based on year-

to-year trends (horizontal) rather than a pre-determined optimal direction (vertical).

Unfunded Post-Employment Benefits Liabilities and Pension Benefits Liabilities—An

unfunded liability is incurred in the current or a prior year that does not have to be paid

until a future year, and for which reserves have not been set aside. An unfunded liability

represents a legal commitment to pay at some time in the future. If such obligations are

permitted to grow over a long period of time, they can have a substantial effect on a

local government’s financial condition.

Analyzing a city’s unfunded liabilities can answer the following questions.

Is the pension liability increasing? How fast is it growing? How much is

unfunded?

Are pension contributions, pension system assets, and investment earnings

keeping pace with the growth in benefits?