fiscal federalism jonathan rodden stanford university august 8, 2011

TRANSCRIPT

Fiscal Federalism

Jonathan RoddenStanford University

August 8, 2011

Part 1:Broad Overview

• Intellectual history• From welfare economics and public choice to

political economy

• Stylized facts and trends • Partial decentralization• Incomplete contracts

• An example: The study of intergovernmental grants

Part 2: Macroeconomic management

• State/local budgets and the business cycle• Pro-cyclical fiscal flows and borrowing

• Fiscal discipline in multi-layered systems• The end of market discipline?

Intellectual historyFrom “First Generation” to “Second Generation” fiscal

federalism

Welfare economics

• Coherent logic connecting Montesquieu, Rousseau, Tocqueville, Madison, Musgrave, Oates:• To achieve simultaneously the advantages of

large and small governmental units by solving the “assignment problem.”

• Oates: “The provision of public services should be located at the lowest level of government encompassing, in a spatial sense, the relevant benefits and costs.”

Welfare economics, cont.

• Assume that political leaders are benevolent despots who maximize the welfare of their constituents.

• Presumption in favor of decentralization because of:• stronger incentives• better information about preferences• above all, greater homogeneity of preferences

at lower levels of government

Competition and sorting

• Tiebout (1956): Key advantage of decentralization is the market analogy. • Citizen land-owners sort into communities that

offer desired levels of taxes and bundles of goods.

• Provides a powerful preference-revelation mechanism beyond voting and lobbying.

Competition as a restraint on government

• Leviathan (Hayek 1939, Brennan and Buchanan 1980)• Tax competition prevents revenue-hungry

politicians and bureaucrats from consuming too much.

• Persson and Tabellini (2000), Weingast (1995)• Decentralization with capital mobility allows

government to commit not to over-tax capital or over-regulate the economy.

Broad consensus circa 1990:

• Based on theory literature, virtual consensus about potential benefits of decentralization, especially in developing countries in late 1980s

What went wrong?

• The obvious things:• Corruption, clientelism, elite capture• Accountability problems• Challenges for safety nets and poverty

reduction• Macroeconomic management:

• Specifically, soft budget constraints and bailouts

What was the theory literature missing?

• Decentralization in practice rarely resembles the type of decentralization imagined in the theory literature.

• “Partial Decentralization” • Grants and shared taxes rather than

autonomous local taxation• Muddy division of authority• Politicized resource distribution

What do we know?Trends and stylized facts

0

0.2

0.4

0.6

0.8

1

1965 1975 1985 1995

Percent of countries with elected subnational governments (43 countries)

local

regional

00.10.20.30.40.5

1965 1975 1985 1995

Average Expenditure Decentralization, 29 countries

Source: GFS

Correlates of expenditure decentralization

• Panizza 1999, Garrett and Rodden 2005:• Country size• GDP per capita• Democracy • Federal constitution• Ethno-linguistic heterogeneity?

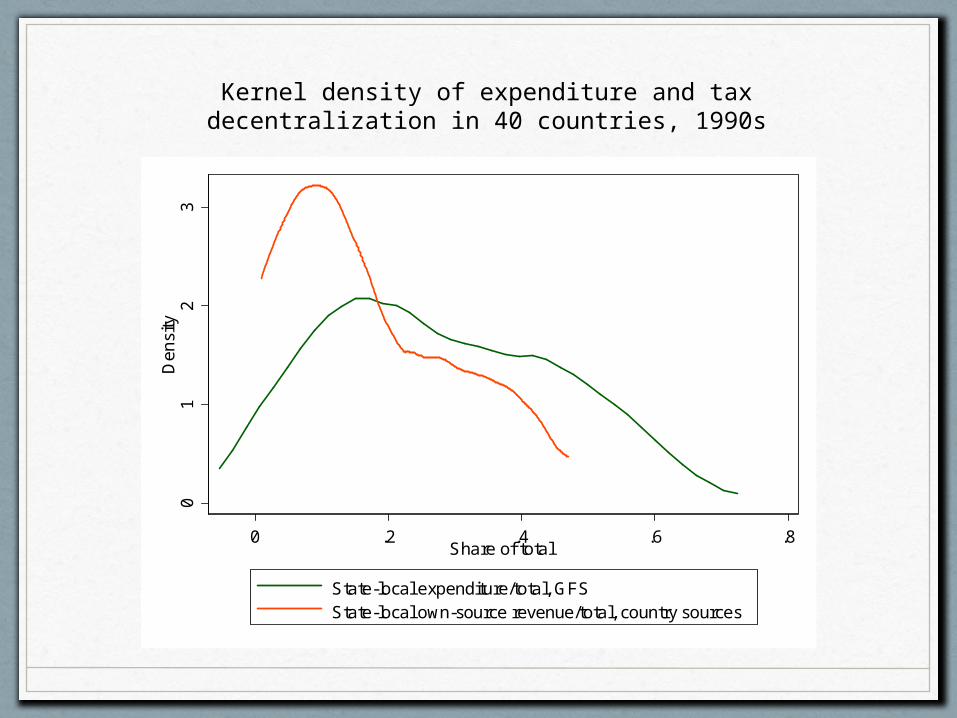

But what about the revenue side?

01

23

Den

sity

0 .2 .4 .6 .8Share of total

State-local expenditure/total, GFSState-local own-source revenue/total, country sources

Kernel density of expenditure and tax decentralization in 40 countries, 1990s

01

02

03

0D

ensi

ty

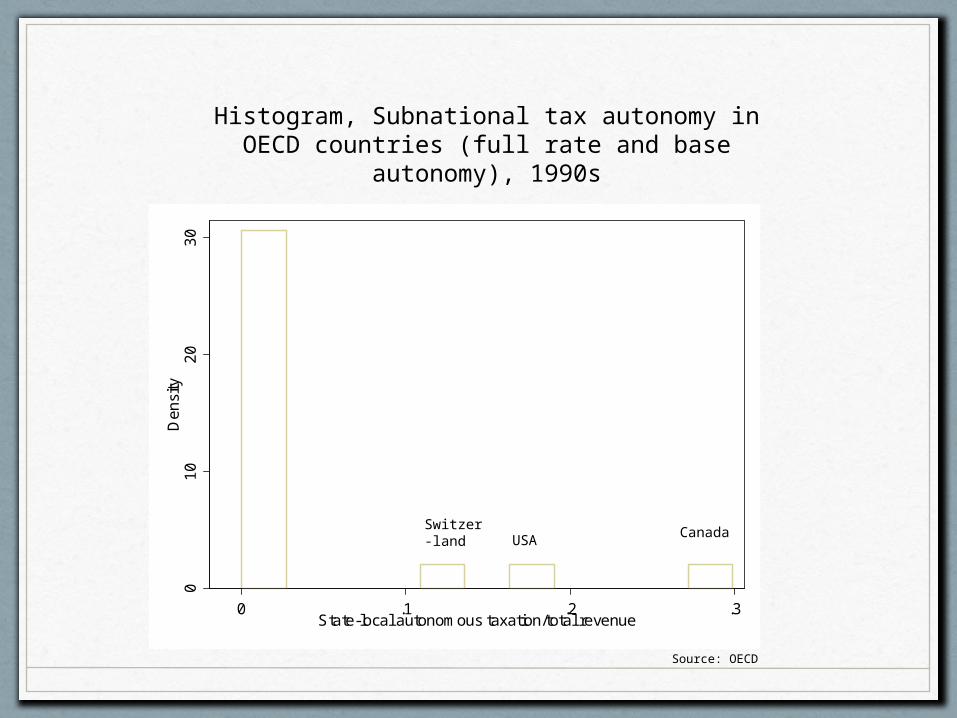

0 .1 .2 .3State-local autonomous taxation/total revenue

Switzer-land USA Canada

Histogram, Subnational tax autonomy in OECD countries (full rate and base autonomy), 1990s

Source: OECD

Federalism vs. decentralization

• Federalism has roots in a bargain or contract• Coming together vs. holding together

• To be credible, the contract usually requires institutional protections:• Unit-based rather than population-based

representation• Supermajority requirements• Courts with judicial review• Explicit delimitation of powers & responsibilities,

residual powers

The division of expenditure responsibilities

0

0.2

0.4

0.6

1965 1975 1985 1995

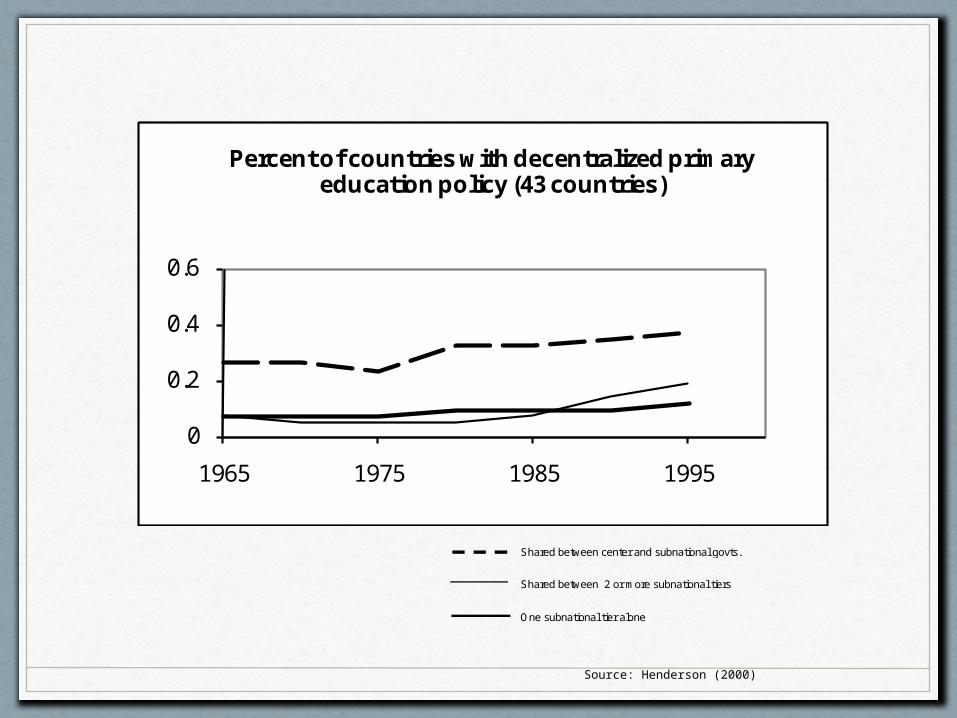

Percent of countries with decentralized primary education policy (43 countries)

Shared between center and subnational govts.

Shared between 2 or more subnational tiers

One subnational tier alone

Source: Henderson (2000)

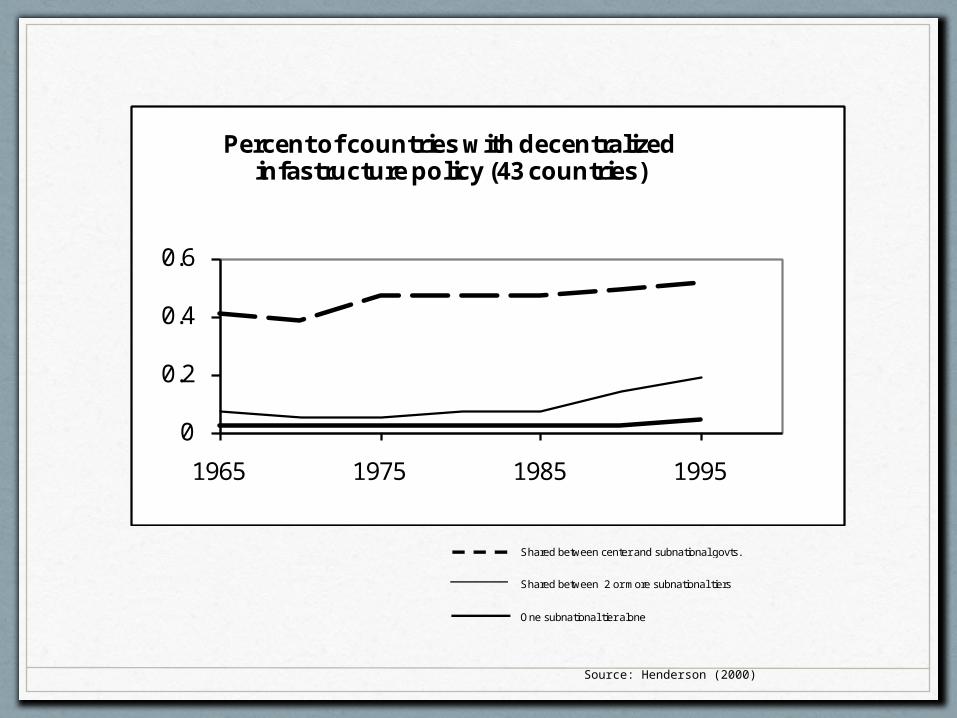

Shared between center and subnational govts.

Shared between 2 or more subnational tiers

One subnational tier alone

Source: Henderson (2000)

0

0.2

0.4

0.6

1965 1975 1985 1995

Percent of countries with decentralized infastructure policy (43 countries)

Pathologies of partial fiscal decentralization

• Limited accountability• Local governments direct resources to clients

and blame higher-level governments for poor service provision.

• Offloading and unfunded mandates• Stringent conditions for grants• Incentives for local governments to hide

information and dissemble• Politicized transfers

Rethinking fiscal federalism in the last decade

• Motivations of politicians• Electoral and other political motivations

replace benevolent despots and Leviathans.

• Focus on institutions of representation• E.g., the nature of legislative bargaining:

Persson and Tabellini (1996), Inman and Rubinfeld (1997), Dixit and Londregan (1998), Besley and Coate (2003), Lockwood (2002).

Rethinking federalism, cont.

• Sharper focus on “fiscal interests”• Taxes and fees vs. grants• Types of grants, formulas

• Incomplete contracts• The ultimate locus of authority is often unclear

and contested.

• Principal-agent relationship• Focus on crafting better incentives for

subnational governments

Re-centralization?

• Central governments are seeking out new ways of structuring the principal-agent relationship• Replacing discretion with rules• Audits• Enhanced central monitoring and data

collection

• But challenges remain:• Example: difficulty of data collection in

decentralized environments

Who gets what?Empirical studies of intergovernmental transfers

Motivation

• The trend toward fiscal decentralization is funded primarily by a combination of formulaic and discretionary transfers.

• Grants and fiscal flows shape incentives of regional governments and central legislators.

• By what logic are they distributed?

Studies of intergovernmental grants

• First generation: Welfare economics and fiscal flows

• Second generation: Political economy of fiscal flows• Partisan dictators• Legislative bargaining

• Fiscal flows and inter-regional redistribution: When and where are grants progressive?

• Representation and redistribution

Welfare economics

• Central government is a benevolent dictator

• Uses inter-regional fiscal flows to:• Capitalize on economies of scale in taxation

• Internalize externalities• Facilitate inter-governmental competition• Stabilize asymmetric shocks

Partisan dictators• Cox and McCubbins (1986):

• Core support• Key assumptions: Risk-averse incumbent

• Dixit and Londregan (1996):• “Swing voters”

• These theories are not necessarily about geography or districts, but the application is natural

• Partisan alignment

Empirical literature

• Scattered evidence for all these propositions• Usually an empirical focus on one relatively small,

discretionary part of the budget (e.g. environmental grants in Sweden, infrastructure grants in Spain).

• “Core vs. swing” debate unresolved: Basic story is that incumbents favor some combination of marginal and core districts, direct resources away from the opponent’s core support districts.

• Strong support for the partisan alignment hypothesis• Formulaic transfers are not immune

• Challenges:• Measuring ideological indifference• Endogeneity: Do fiscal flows actually buy votes?

Big questions left unanswered:

• What happens when we drop fixed effects and examine long-term cross-section variation?

• Are fiscal flows progressive?• When and where?• Implications for European idea of a “transfer union.”

Empirical analysis of fiscal flows

• MacDougall Report (1977)

• Renewed interest due to optimal currency area literature, e.g. Sala-i-Martín and Sachs (1992); Bayoumi and Masson (1995)

• Broadest comparative work builds on Bayoumi and Masson (1995): Espasa (2001); Barberán, Bosch, Castells, Espasa (2000); Bosch, Espasa, Sorribas (2002)

Income elasticity of fiscal flows

im

iii

m

i eY

Yba

B

B

ln10ln

income capitaper real Y

balance fiscal capitaper real B

regions all of average torefers

region torefers

m

i

-6-4

-20

2In

com

e e

last

icity

of g

ran

ts

ARG AUS BRA CAN DEU ESP EU IND USACountry

Income elasticity of grants in 9 federations, 1990-2005

Average income and transfers (1990-2005)

To sum up:

• Considerable redistribution through intergovernmental grants in Canada, Spain, Germany, and Australia

• Very little redistribution in Argentina, Brazil, Mexico, Switzerland, the United States, and the EU.

• Why?

The representation of regions

• Some state receive far more representation per capita than others.

• There are good reasons to believe that over-represented states will do well in the game of legislative bargaining

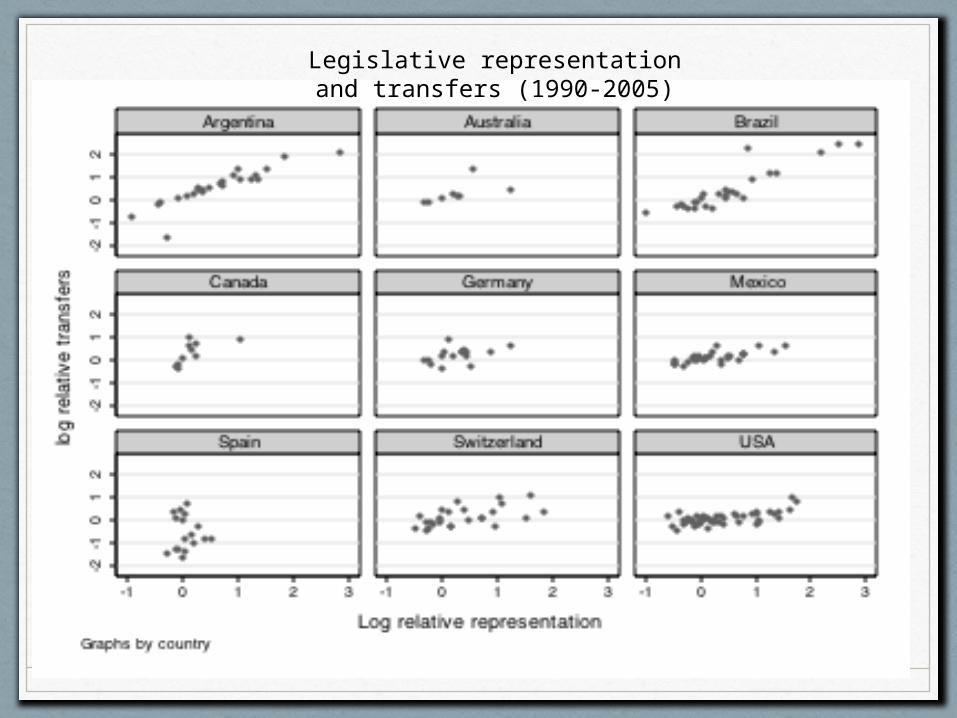

Legislative representation and transfers (1990-2005)

Average income and transfers (1990-2005)

Size of marker reflects relative per-capita representation

Another possible explanation:

• Classic political economy theory about the income distribution:• Does the skew in the inter-regional income

distribution predict redistribution? • If the policy is set by the median state, we

should expect to see large redistribution when median state is poor relative to the mean.

0.5

11

.52

2.5

Den

sity

0 1 2 3 4Share of national average

GDP per capita Expenditures per capita

Brazil, 1990-2001

0.5

11

.52

2.5

Den

sity

0 1 2 3 4Share of national average

GDP per capita Expenditures per capita

Argentina, 1990-2001

0.5

11

.52

2.5

Den

sity

0 1 2 3 4Share of national average

GDP per capita Expenditures per capita

USA, 1990-1997

01

23

45

Den

sity

0 1 2 3 4Share of national average

GDP per capitaExpenditures per capita

Australia, 1990-2001

Note: NT dropped

01

23

45

Den

sity

0 1 2 3 4Share of national average

GDP per capitaExpenditures per capita

Canada, 1990-1997

01

23

45

Den

sity

0 1 2 3 4Share of national average

GDP per capitaExpenditures per capita

Germany, 1990

Note: city-states dropped

But what is the politically relevant income distribution?

• Perhaps in the parliamentary federations without much inter-provincial bargaining, the relevant distribution is the (highly skewed) inter-personal one, and high levels of inter-personal and inter-regional redistribution go hand in hand.

• But an interesting thing happens when the geography is divided into winner-take-all districts or states…

0.0

000

2.0

000

4.0

000

6D

ensi

ty

20000 40000 60000 80000Households: Median household income in 1999

U.S. House District MediansU.S. State Medians

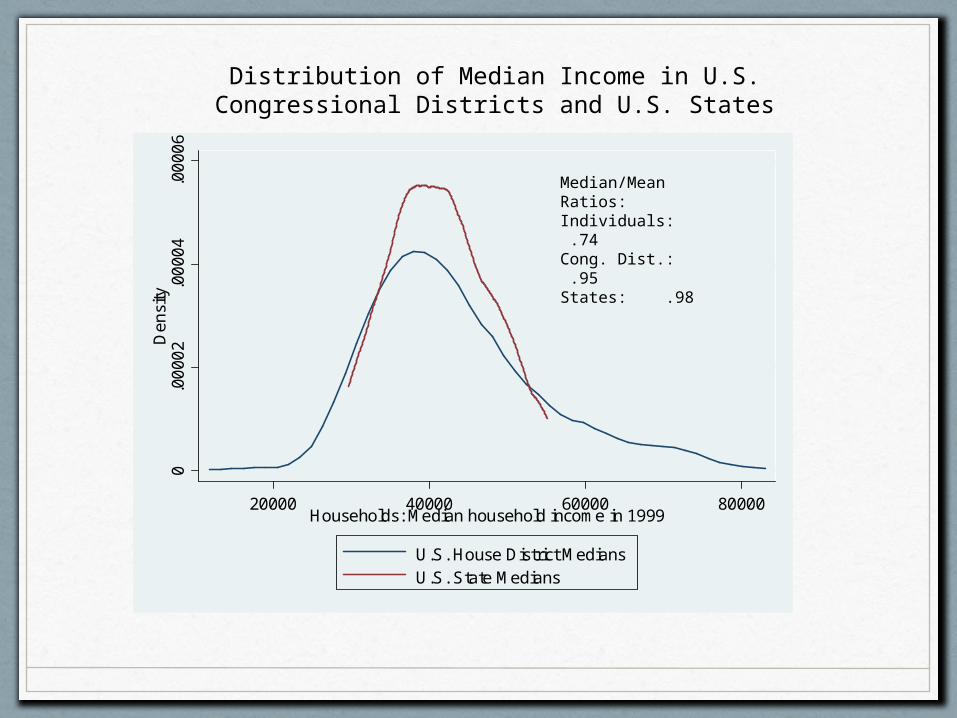

Distribution of Median Income in U.S. Congressional Districts and U.S. States

Median/Mean Ratios:Individuals: .74Cong. Dist.: .95States: .98

A different perspective on unit-based vs. population-based representation

• Perhaps this helps explain why federations, and countries with single-member districts, demonstrate lower levels of redistribution

• The politically relevant median voter (the median income in the median state) is not very poor relative to the mean

A related observation:

• All of the redistributive federations are parliamentary systems with strong and disciplined political parties.

• The non-redistributive federations are presidential systems with weaker parties and region-based coalition building in the legislature, especially the upper chamber.

• A similar story emerges from Persson and Tabellini (1996), who show that inter-regional bargaining leads to lower levels of risk-sharing than majority rule

Summing up:

• The “first generation” literature taught lessons about the optimal distribution of authority that are still relevant

• But it ignored questions related to institutional design and political economy

• After addressing these questions, we now know more about the incentives generated by fiscal and political institutions for voters, creditors, elected officials, and bureaucrats.

• This helps provide a clearer sense of the conditions under which decentralization might facilitate or undermine service delivery and macroeconomic management.

Summing up (cont.):

• Much literature now focuses on strategies to minimize the “dangers” of decentralization

• Not much focus on the impact of decentralization per se

• Instead, focus on incentives created by the intergovernmental framework

• Transition from observational to experimental empirical research

Looking ahead

• Macroeconomic management in a world of:• Partial decentralization• Incomplete contracts• Politicized transfers

Coffee Break

Overview

• Fiscal federalism and the business cycle

• Fiscal adjustment in a multi-layered system: the moral hazard problem

• Paths to fiscal discipline• Hierarchy• Markets

• Can market discipline survive?

Fiscal federalism and the business

cycle

Some important questions:

• How do local budgets respond to the business cycle?

• With what implications for macroeconomic management?

• If central government attempts to generate fiscal stimulus during recession, to what extent do credit-constrained subnational governments undermine this?

Provincial-level time series data (real local currency units per capita):

• Variables:• Total revenue

• Grants (discretionary and formulaic)• Total taxes and fees

• Total expenditures• Deficit • Provincial GDP

• Federations: • Canada, USA, Germany, Australia, Argentina,

Brazil, India

What should we expect?

• Revenues:• Highly pro-cyclical taxes• Grants?

• First generation fiscal federalism literature seems to imply counter-cyclical grants

• Literature on optimal currency unions• But second generation political economy

perspective leads to skepticism

What should we expect?

• Expenditures and borrowing• Barriers to borrowing (and saving):

• USA: Balanced budget rules and revenue restrictions

• Canada is at the opposite extreme: No centrally- or self-imposed restrictions

• Centrally-imposed and cooperative restrictions in each of the other federations• But many loopholes (e.g. German “golden rules,”

Brazilian Senate oversight)

• Voracity effect, credit crunch problem

Figure 1: Elasticity of Budget Items

Figure 1, cont.

Summing up:

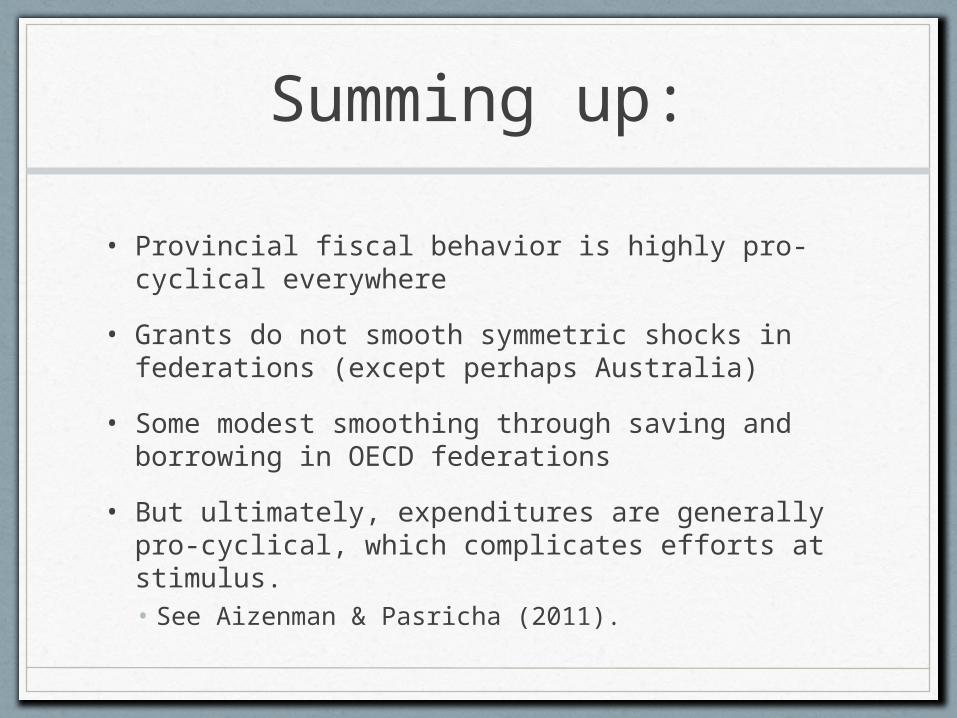

• Provincial fiscal behavior is highly pro-cyclical everywhere

• Grants do not smooth symmetric shocks in federations (except perhaps Australia)

• Some modest smoothing through saving and borrowing in OECD federations

• But ultimately, expenditures are generally pro-cyclical, which complicates efforts at stimulus. • See Aizenman & Pasricha (2011).

Fiscal federalism and fiscal discipline

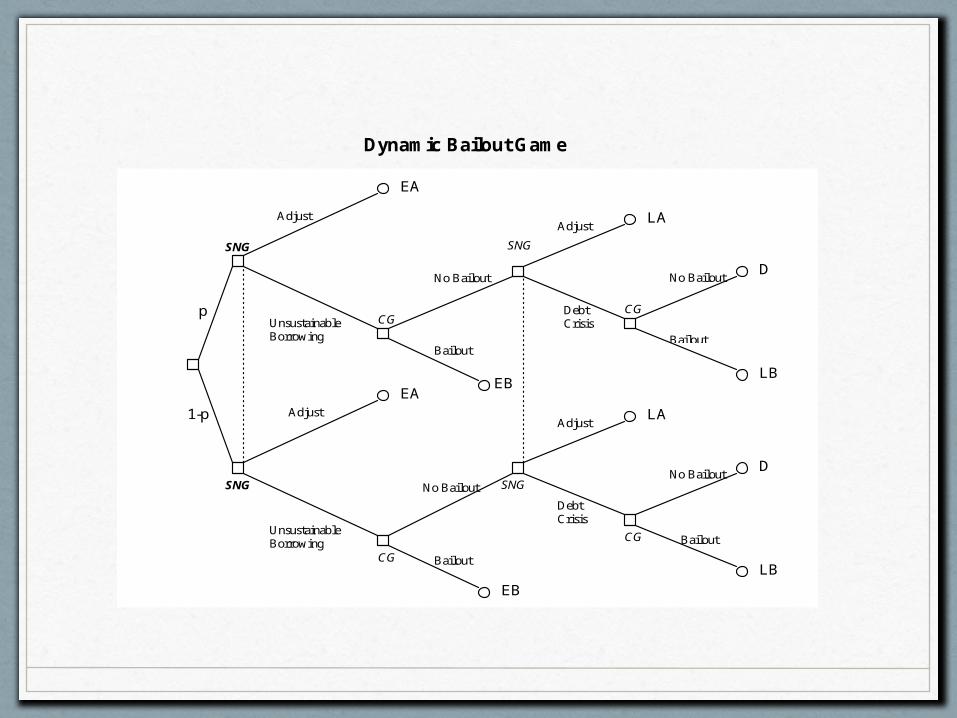

Dynamic Bailout Game

C

hanc

e

p

1-p

Adjust

Unsustainable Borrowing

Adjust

Unsustainable Borrowing

Bailout

No Bailout

Bailout

No Bailout

No Bailout

No Bailout

Bailout

Bailout

EA

EA

EB

EB

LB

D

LB

D

SNG

SNG

CG

CG

C

G

SNG

CG

CG

LA

LA

Adjust

Debt Crisis

Adjust

Debt Crisis

SNG

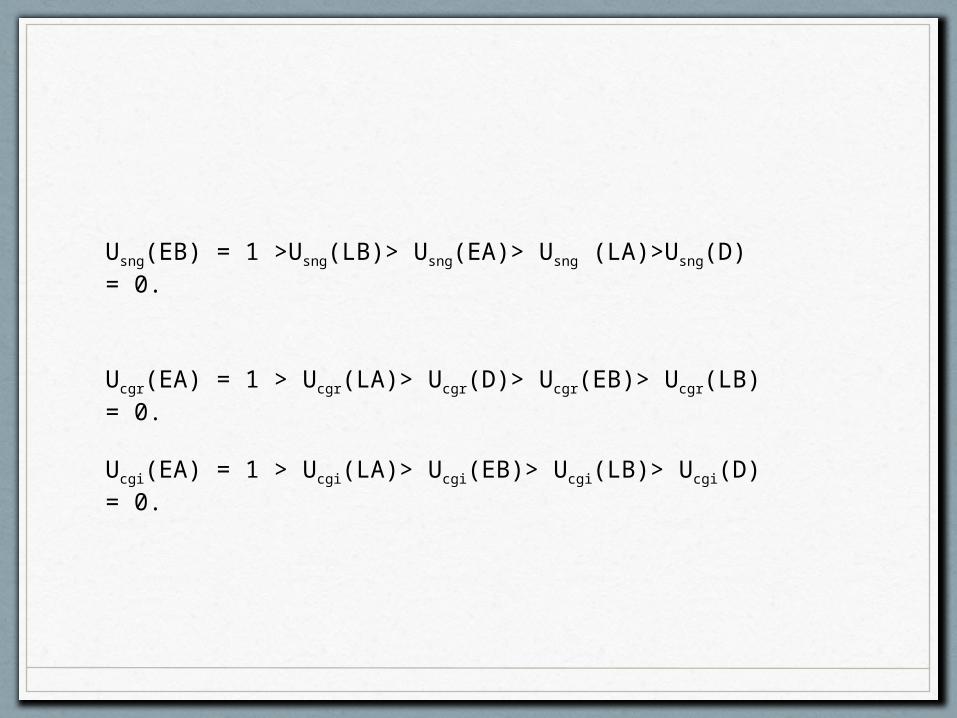

Usng(EB) = 1 >Usng(LB)> Usng(EA)> Usng (LA)>Usng(D) = 0.

Ucgr(EA) = 1 > Ucgr(LA)> Ucgr(D)> Ucgr(EB)> Ucgr(LB) = 0. Ucgi(EA) = 1 > Ucgi(LA)> Ucgi(EB)> Ucgi(LB)> Ucgi(D) = 0.

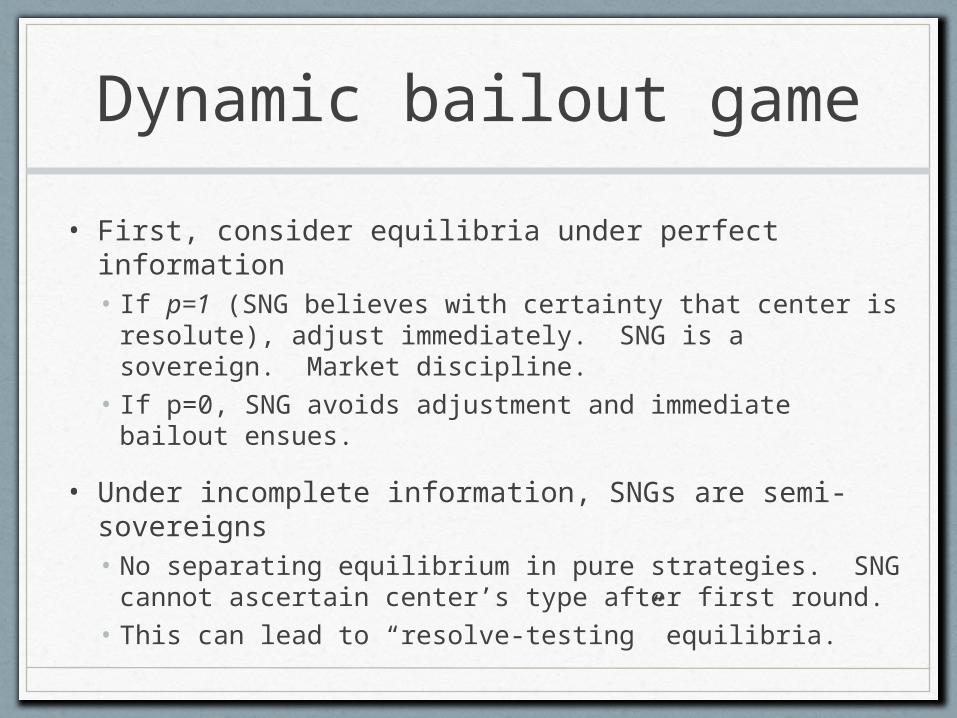

Dynamic bailout game

• First, consider equilibria under perfect information• If p=1 (SNG believes with certainty that center is

resolute), adjust immediately. SNG is a sovereign. Market discipline.

• If p=0, SNG avoids adjustment and immediate bailout ensues.

• Under incomplete information, SNGs are semi-sovereigns• No separating equilibrium in pure strategies. SNG

cannot ascertain center’s type after first round.• This can lead to “resolve-testing” equilibria.

What drives perceptions of the center’s resolve?

• Basic powers and obligations of the center

• Externalities and the structure of jurisdictions

• Identity of debt holders

• Legislative representation of solvent and insolvent states

• Court decisions

• Revenue sources and autonomy

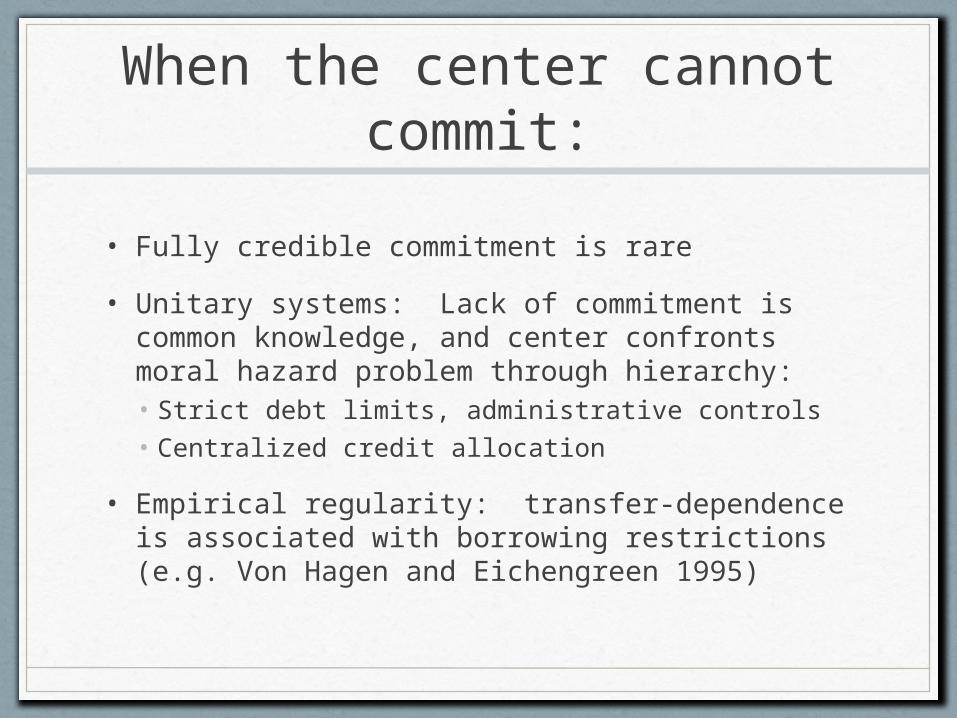

When the center cannot commit:

• Fully credible commitment is rare

• Unitary systems: Lack of commitment is common knowledge, and center confronts moral hazard problem through hierarchy:• Strict debt limits, administrative controls• Centralized credit allocation

• Empirical regularity: transfer-dependence is associated with borrowing restrictions (e.g. Von Hagen and Eichengreen 1995)

Commitment problems in federations

• Recall that federations emerged from historical bargains with institutional legacies that make hierarchical control difficult:• Brazilian Senate• EU Council of Ministers

• Dysfunctional federalism: Center can neither commit nor regulate• Argentina and Brazil early 1990s• European Union today

What went wrong in Europe?

• Half-hearted attempts at markets (no-bailout clause) and hierarchy (excessive deficit procedure).• The latter undermined the former

• The identity of debt holders, externalities

• Banking sector

• Uncertainty• Both about bailouts and defaults

51

01

51

0-y

ear

bo

nd

yie

ld

February 7 1992 January 1 1999

Belgium GermanyItaly France

Netherlands PortugalSpain SwedenDenmark UK

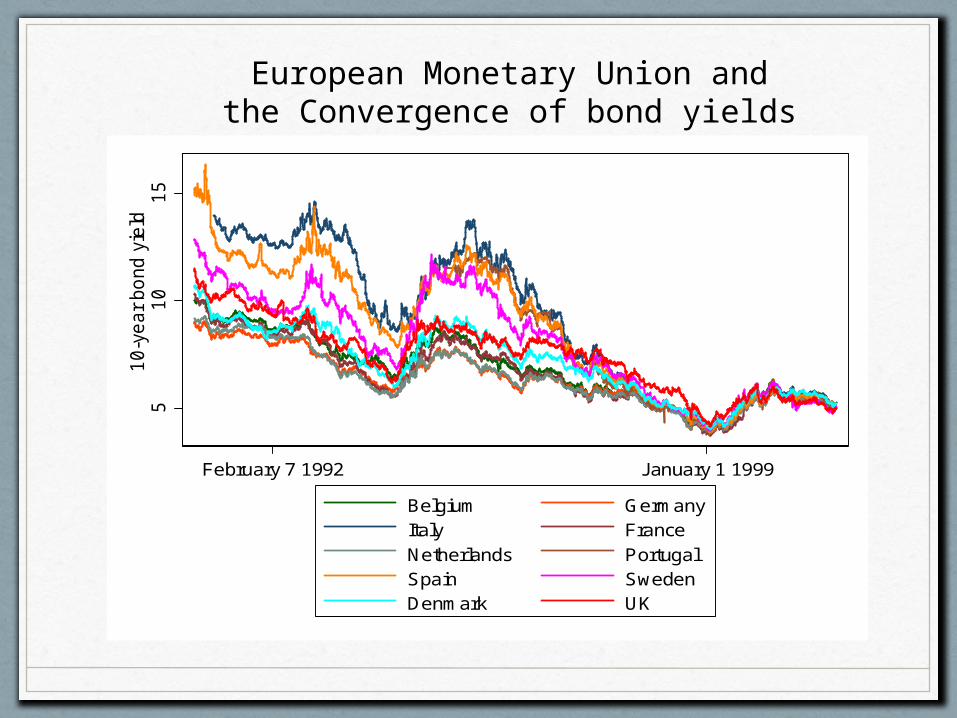

European Monetary Union and the Convergence of bond yields

Debt crisis and divergence in 2010

24

68

10

12

10-y

ear

bo

nd

yie

ld

April 2009 May 10 2010 Nov 12 2010

Belgium GermanyItaly FranceGreece Netherlands

Portugal SpainSweden UKIreland

The way forward in Europe

• A moment for centralization?

• Can market discipline function again?• Toward an orderly default procedure• European bankruptcy?

What about the United States?

• On one hand, some market analysts believe default is imminent.

• On the other hand, Roubini and Buffet tell us that in the wake of Bear Stearns and GM, federal government already provides an implicit guarantee.

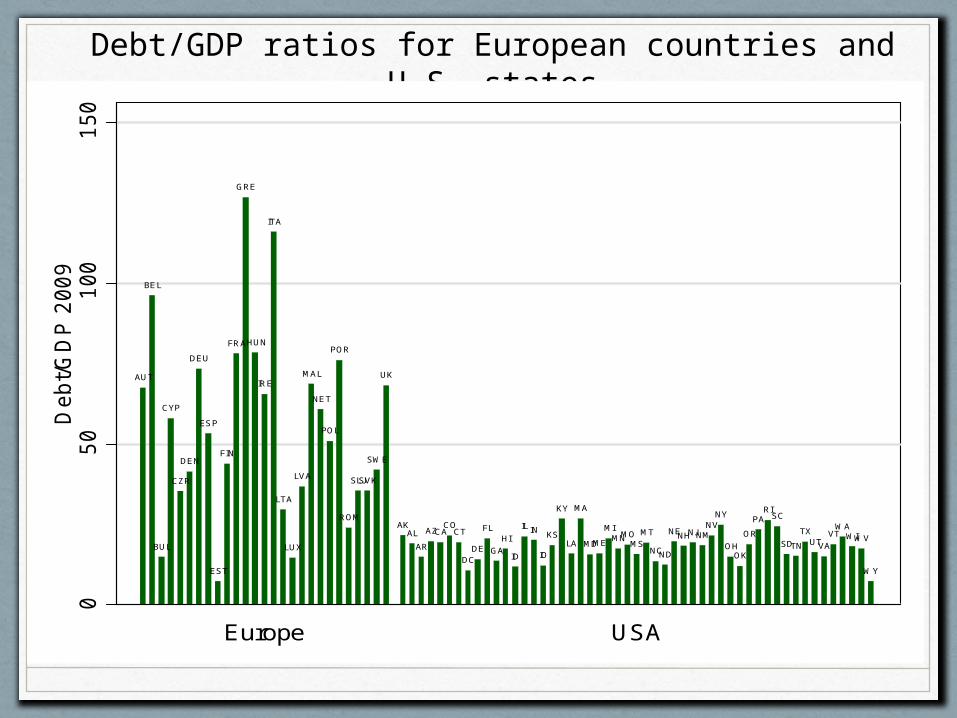

Debt/GDP ratios for European countries and U.S. states

AUT

BEL

BUL

CYP

CZR

DEN

DEU

ESP

EST

FIN

FRA

GRE

HUN

IRE

ITA

LTA

LUX

LVA

MAL

NET

POL

POR

ROM

SLJSVK

SWE

UK

AKAL

AR

AZCACO

CT

DCDE

FL

GA

HI

ID

IL IN

IO

KS

KY

LA

MA

MDME

MIMNMO

MS

MT

NCND

NENHNJNMNV

NY

OHOK

OR

PARI

SC

SDTN

TXUTVA

VTWA

WIWV

WY

05

01

00

150

Deb

t/G

DP

200

9

Europe USA

But this is deceptive

• Unfunded pension liabilities

• Implicit responsibility for municipal debt

• Insolvency is probably not imminent, but if conditions deteriorate, will states be allowed to default? Will the federal government provide a bailout?

Market discipline in U.S. federalism

• Begins with aftermath of 1840s debt crisis

• Throughout 20th century, rapid response to negative revenue shocks, especially in states with most stringent balanced budget requirements (e.g. Poterba 1995).

• Bond yields and ratings quickly very responsive to changes in debt/GSP ratio and other indicators

• Default extremely rare

• No federal debt assumptions

But much has changed

• Beginning with the New Deal, creeping centralization.

• States are increasingly used as agents of the federal government

0.0

5.1

.15

.2.2

5F

ed

era

l gra

nts

as

sh

are

of cu

rre

nt e

xpe

nd

iture

s

1920 1940 1960 1980 2000 2020year

Source: BEA

Federal grants as share of state-local current expenditures

Response to recent recessions:

• Inefficient and painful expenditure cuts

• Requests for implicit bailouts:• Medicaid assistance• Infrastructure stimulus• Build America bonds

• These are delayed, ad hoc, and politicized.

• They send the wrong signals to market actors.

• But do they spell the end of market discipline?

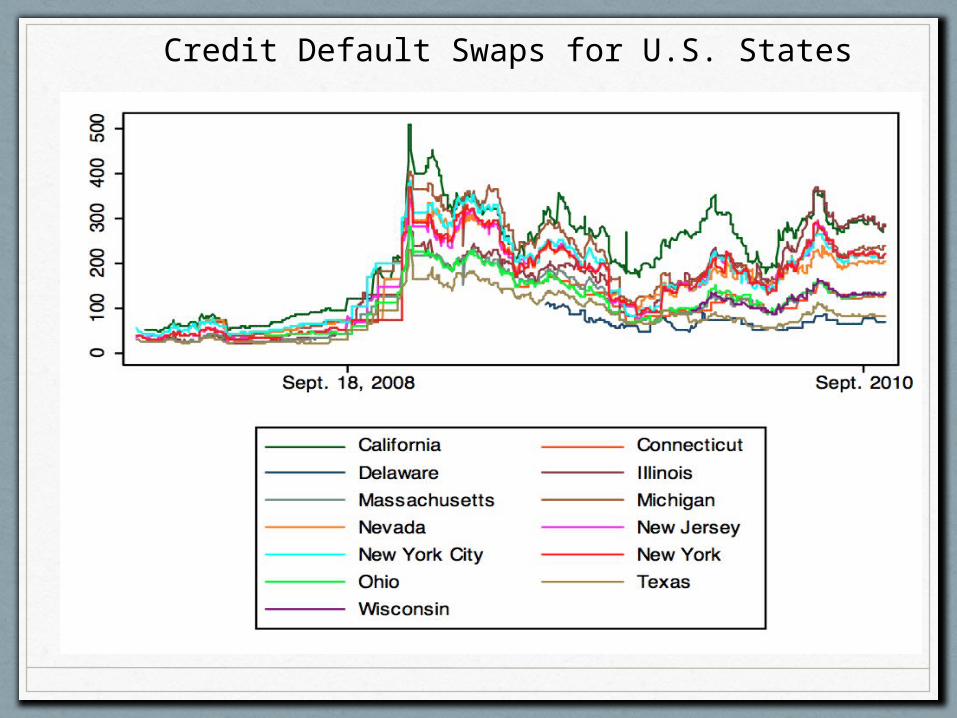

Credit Default Swaps for U.S. States

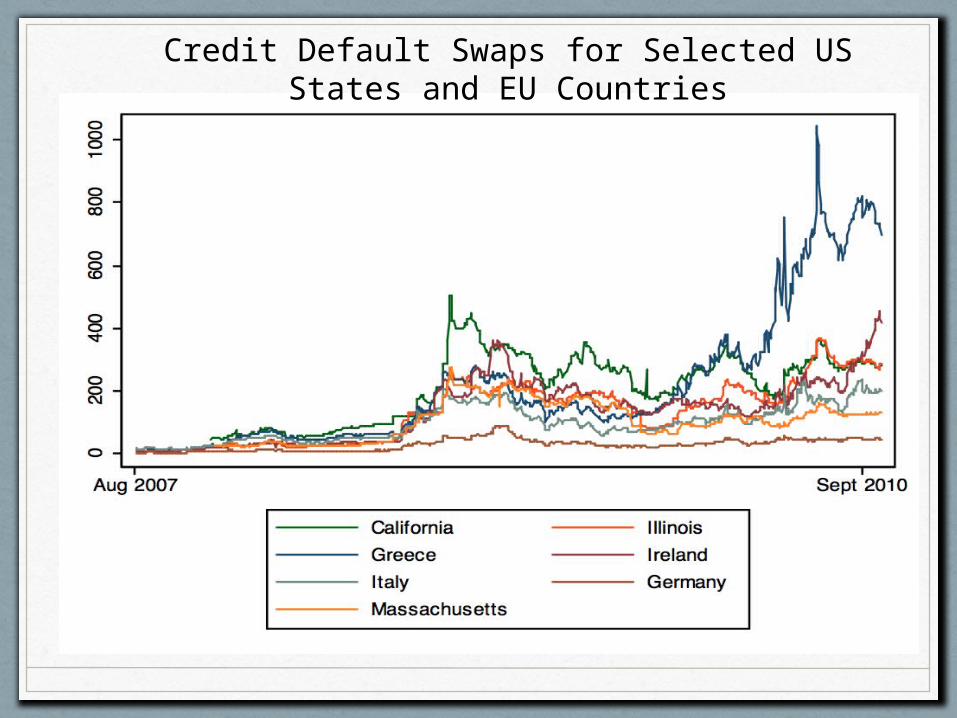

Credit Default Swaps for Selected US States and EU Countries

Can market discipline survive?

• There are good reasons for optimism. • Identity of bond-holders• Representation of (potentially) insolvent states

• The most important question is not whether bailouts are possible, but whether states and creditors are sufficiently uncertain.

• States and their creditors are not behaving as if bailouts are imminent.

• States are making better progress than the federal government

Bolstering market discipline

• Reduce unfunded mandates

• Avoid policies that make states responsible for municipalities

• Embed automatic stabilizers into transfer system

• Keep state and federal obligations as separate as possible

• Orderly default procedure

Summary

• Fiscal federalism creates serious challenges for macroeconomic management, especially in the wake of fiscal crisis

• Subnational governments are font-line service providers, often responsible for providing unemployment insurance, health services, safety net, not to mention education, police, fire protection, infrastructure.

• Own-source revenues are extremely pro-cyclical, and grants are not much better. Most subnational governments are highly credit-constrained, and cannot easily borrow to smooth shocks.

Summary (cont.)

• Subnational governments are thus largely reliant on the central government for stabilization (as prescribed in the first-generation normative literature).

• But central governments, and the intergovernmental fiscal framework, are often not up to the task.

• This is an important area for reform

• Even in unitary systems, there is an ongoing struggle to improve incentives associated with partial decentralization

• But the largest challenges appear to be in federations and quasi-federations, where institutions, along with ethnic and regional tensions, undermine both hierarchical and market-based forms of fiscal discipline.

Implications for the IMF

• Conditions, targets, monitoring must be sensitive to activities and obligations of subnational governments

• It is important to assess the basic incentives created by the intergovernmental framework. Things are often not as they appear on paper, and it is crucial to understand the political incentive structure.

• Need for further collaborative research