first- and second-order effects of consumers ... · denzau and north (1994) note that categories...

TRANSCRIPT

First- and second-order effects of consumers’

institutional logics on firm–consumer

relationships: A cross-market

comparative analysis

Jagdip Singh1,Patrick Lentz2 andEdwin J Nijssen3

1Weatherhead School of Management, CaseWestern Reserve University, Cleveland, USA;2Department of Marketing, University of

Dortmund, Dortmund, Germany; 3Department

of Technology Management, EindhovenUniversity of Technology, Eindhoven, the

Netherlands

Correspondence: EJ Nijssen, Department ofTechnology Management, EindhovenUniversity of Technology, PO Box 513, 5600MB Eindhoven, the Netherlands.Tel: þ31 (0)40 2472170;Fax: þ31 (0)40 2468054;E-mail: [email protected]

Received: 22 August 2008Revised: 29 August 2009Accepted: 3 September 2009Online publication date: 11 February 2010

AbstractConsumers’ conceptions of a market’s institutional logic affect mechanisms

of firm–consumer relationships, but are generally neglected in comparativestudies of international marketing. This study bridges institutional and relation-

ship marketing theories to examine two questions: do consumers hold

meaningful mental models of a market’s institutional logics, and do these

mental models explain differentiated patterns of market relationships acrossinternational contexts? Building on contract-relational duality, we develop

a market-level construct for capturing consumers’ socially constructed mental

models for the institutional logics of market action. We theorize that differencesin consumers’ institutional logics will influence both their evaluation of a firm’s

capabilities (first-order effect) and the degree to which they reward a firm

through their commitment (second-order effect). These bridging predictionsare tested using data from the insurance industry across three international

markets. Our results show that the German insurance market is located in the

relatively high contracts–low relational quadrant, whereas the US and Dutch

markets are both located in the relatively low contracts – high relationalquadrant. Our results also suggest that consumer commitment conforms to a

principle of alignment such that commitment accrues to providers who align

their capabilities with consumers’ prevalent institutional logics of the market,and penalizes those who deviate from it.

Journal of International Business Studies (2010) 1–27. doi:10.1057/jibs.2009.101

Keywords: institutional theory; relationship marketing; cross-cultural analysis; compa-rative analysis

INTRODUCTIONUnderstanding similarities and differences in mechanisms offirm–consumer relationships is of fundamental interest for inter-national marketing researchers and practitioners alike. Researchersseek differentiating ‘‘patterns of exchange’’ that characterizecomparative marketing systems, while practitioners drive for‘‘discretionary decision-making’’ that exploit disparate patternsfor strategic advantages in global markets (Iyer, 1997: 552).

Two dominant, but distinct, streams of research have emerged toilluminate mechanisms of firm–consumer relationships acrossmarkets. The institutional perspective emphasizes the embedded

Journal of International Business Studies, 1–27& 2010 Academy of International Business All rights reserved 0047-2506

www.jibs.net

view of market exchanges, and theorizes the role of‘‘constitutive norms’’ of the marketplace (Grewal &Dharwadkar, 2002; Scott, 2001). In viewing institu-tional fields as social structures with isomorphicforce, this perspective acknowledges but subordi-nates the role of strategic action in individual firm–consumer relationships. By contrast, relationshipmarketing theory focuses on ongoing marketexchanges to identify firms’ capabilities critical toearning consumers’ commitment (Morgan & Hunt,1994; Sirdeshmukh, Singh, & Sabol, 2002). Con-sistent with its emphasis on managerial agency, thisapproach accepts cross-market variability, but mar-ginalizes the role of the larger context in whichexchanges develop and evolve. Both perspectivescan claim support within their literatures (Kostova& Roth, 2002; Palmatier, Dant, Grewal, & Evans,2006). However, few studies have attempted tobridge these differing perspectives. Thus the con-cerns raised over a decade ago by Iyer (1997: 553)that theories of international marketing ‘‘have y

failed to deal adequately with y the fundamentalnature of market [exchange] relations’’ and limitour understanding of ‘‘buyer behavior under gen-eralized [institutional] contexts’’ continue to persisttoday.

We aim to bridge the institutional and relation-ship marketing perspectives, and make three spe-cific contributions. First, we emphasize and developconsumers’ conception of a market’s institutionalenvironment. Thus far, research grounded in insti-tutional theory has tended to focus either onmanagerial conceptions of institutional environ-ments (Porac, Thomas, & Baden-Fuller, 1989;Prahalad & Bettis, 1986) or on inter-firm relation-ships (business-to-business, B2B) (Grewal & Dhar-wadkar, 2002; Heide & Wathne, 2006), largelyignoring the consumers’ perspective in business-to-customer (B2C) relationships (Brief & Bazerman,2003). Our study addresses this imbalance. Weutilize institutional theory ideas of contract-relational duality to conceptualize consumers’shared and socially constructed mental models forthe institutional ‘‘logics’’ of the marketplace. Wethus offer a more socialized view of ongoing firm–consumer relationships. By focusing on the con-sumer perspective, we affirm that consumers arecritical market actors who shape and sustainongoing market relationships through their com-mitment to maintain (or terminate) exchanges.

Second, we theorize how consumers’ institutionallogics impact on mechanisms of consumer com-mitment in ongoing relationships with individual

firms across international markets. We refer topredictions from our theorizing as bridging hypo-theses. We anticipate influences both on consu-mers’ evaluation of a firm’s capabilities and onthe degree to which they reward a firm throughtheir commitment, which we refer to as first- andsecond-order effects respectively. Past research hasfocused on describing rather than theorizing andexplaining variability across international markets.For instance, Wulf, Odekerken-Schroder, and Iaco-bucci (2001) examine the mechanisms of relation-ship commitment across three internationalmarkets (Belgium, the Netherlands, and the US),but posit no a priori hypotheses for the variability inmodeled relationships. In their analysis, theseauthors find significant variability for almost everypath in their model across the three markets (theirTable 4: 43). Our study addresses this gap, anddevelops a priori institutional-theory-based predic-tions to account for the variability in exchangerelationships across market contexts.

Third, we operationalize consumers’ conceptionsof institutional logics, theorized as a market-levelconstruct – consumers’ institutional logics of marketaction (CILMA) – and examine its potential tocapture variability in institutional environments ofthe insurance industry for three contrasting markets(Germany, the Netherlands, and the US). We alsoexamine the incremental contribution of the CIL-MA construct to explain variability in exchange-levelmechanisms of relationship marketing (i.e., firm–consumer relationships) while remaining sensitiveto alternative explanations rooted in cultural differ-ences. We specifically control for cultural variabilitydue to masculinity and uncertainty avoidance –dimensions most closely related to contract-rela-tional duality.

The paper is organized as follows. First, we reviewthe institutional perspective to establish that con-sumers, like managers, are also likely to developa shared mental model of a market’s institutionallogics. Thereafter, we develop and define theCILMA construct to capture consumers’ concep-tions of institutional logics, and outline its simila-rities and differences with respect to extant culturalconstructs. Next, we review the relationship mar-keting perspective on ongoing firm–consumerrelationships, and theorize the incremental con-tribution of the CILMA construct by developingbridging hypotheses of first- and second-ordereffects. Following this, we report on the empiricalstudy involving the insurance market in threenations, organized in two subsections: the first

Consumers’ institutional logics Jagdip Singh et al

2

Journal of International Business Studies

relating to CILMA’s construct validity, and thesecond to testing the bridging hypotheses. Finally,we discuss our findings, and derive the theoreticaland managerial implications.

INSTITUTIONAL PERSPECTIVE ONCONSUMERS’ LOGICS OF MARKET EXCHANGESInstitutional theory, generally viewed as one of theleading perspectives for analysis of market actionand evolution, draws on three central premises(Heugens & Lander, 2009; Lawrence & Suddaby,2006). First, institutional theorists emphasize therole of institutional fields as established andprevalent social rules and norms structuring socialinteractions among market actors with economicobjectives, thereby rejecting the atomistic and‘‘undersocialized’’ view of neoclassical economicsand rational choice theorists (Heugens & Lander,2009; Hodgson, 2006). Second, the institutionalview conceives ‘‘logics’’ as socially constructedmental models that groups of individuals hold asshared cognitions of socialized routines for action.As Scott (2001: 57) noted, ‘‘compliance occurs y

[as] routines are followed because they are taken forgranted as ‘the way we do these things’.’’ Third,institutional fields reproduce and sustain them-selves through instruments of socialization, includ-ing word of mouth, stories, and artifacts thatengage and socialize new members, and allowenvironmental changes to be incorporated intopre-existing routines and patterns (Lawrence &Suddaby, 2006).

Shared logics are ‘‘essential’’ to facilitate commu-nication, order interactions, and promote learningamong market actors (Denzau & North, 1994: 4–5;March & Olsen, 1998; Scott, 2001). Most marketsare too complex for an individual to independentlylearn how they work, or what routines to enact forsuccessful market exchanges (Mantzavinos, North,& Shariq, 2004). Social interactions and socializa-tion processes help individuals learn efficientlyfrom the collective knowledge of institutionallogics, and store it as a shared mental model thatguides their market actions. Mental models areneither static over time nor deterministic in shap-ing the actions of market actors. Rather, thesemodels are dynamically updated as individualslearn through feedback from market exchanges,and their normative influence waxes and wanesas they compete with other cultural, social, andeconomic forces influencing individual action.Denzau and North (1994: 5) note that under-standing shared mental models is the ‘‘single most

important step’’ for replacing the ‘‘black box ofrationality assumption used in economics andrational choice models.’’

Past research has generally neglected consumers’mental models of a market’s institutional logics.This possibly reflects a misconception that com-munication across consumers is too diffused,fragmented and infrequent to support meaningfulmental models. However, sufficient evidence existsto suggest that consumers (1) are motivatedto engage in social learning and construct suchmodels, and (2) use them to navigate their actionfor productive market exchanges (Mantzavinoset al., 2004). For example, research on lay theoriessuggests that, especially in uncertain environ-ments, consumers actively learn from self, andvicariously from others’ market experiences todevelop and share naıve theories (Molden &Dweck, 2006). Moreover, modern technologies arerapidly enabling forums for social learning. Thisincludes online communities, consumer blogs andforums, word of mouth through texting, e-mail andphone, and public sources that reflect and frameconsumers’ market experiences and expectations.Such shared experiences and learning promote andexplain the mental models that consumers collec-tively develop and share.

The CILMA Construct: Conceptualization andDimensionsWe conceptualize CILMA as consumers’ sharedmental model for the institutional field of market-place exchanges. Following Denzau and North(1994), we posit that these logics are typicallyorganized around (1) categories that classify differ-ent types of market exchanges, and (2) conceptsthat characterize distinctive features of marketexchanges. We develop each of these ideas in turn.

Denzau and North (1994) note that categories arekey architectural features of individuals’ mentalmodels. Categories define boundaries separatingentities that differ in the institutional logicsgoverning their social structure. Within a category,entities are thought to be structured with commoninstitutional logics. Across categories, the structur-ing logics are likely to be differentiated. Categoriesprovide efficiency in negotiating market exchangesby providing a common set of expectations for ahost of entities that are categorized similarly. Forinstance, insurance providers in a given culturalcontext (e.g., Germany) may be categorizedtogether, indicating that market exchanges withthem are characterized by common expectations

Consumers’ institutional logics Jagdip Singh et al

3

Journal of International Business Studies

regarding service interactions, pricing, product, andrelated features. How these common expectationsarise is probably a combination of cultural-histor-ical factors relating to the nation (e.g., regulatorygovernance in Germany) and the institutionsunique to the industry (e.g., professional govern-ance of the insurance industry). In other words,each industry is likely to be organized arounddistinct technologies and processes, governed bylargely distinct regulatory codes, and to carry ahistorical and cultural trace of negotiations amongmarketers and consumers.

It is therefore inappropriate to presume thatinstitutional logics are common across differentindustries within a nation (e.g., automobiles andinsurance in the US) or for similar industries acrossdifferent nations (e.g., insurance in the US andGermany). Several studies indicate that the varia-bility across industries within nations is substantial,and comparable to cross-national variability (Dyer& Chu, 2000; Kostova & Roth, 2002; Makhija &Stewart, 2002), suggesting industry as a reasonablebasis for categorization.

Moreover, building on Denzau and North’s (1994)notion of concepts as basic blocks of mental models,we posit that, within a category, institutional logicswill be characterized by different combinations of afew elementary concepts. While prototypical con-cepts offer theoretical clarity owing to their elemen-tary focus, in practice no market is likely to becompletely defined by a single prototypical concept.Markets are complex contexts of exchanges thatrequire a multi-conceptual space to specify theirdistinct and sometimes competing logics (Jackson &Deeg, 2008).

Within the institutional literature, two prototy-pical concepts that have received the most atten-tion relate to March’s distinction between the logicsof ‘‘instrumentalism’’ and ‘‘appropriateness’’ (Kos-tova & Roth, 2002; Makhija & Stewart, 2002),which, in turn, have their roots in the duality ofcontracts and relational forms of governance(Macaulay, 1963). These logics provide contrastingor alternative mechanisms for reducing risk anduncertainty in market exchanges, thereby promot-ing an orderly structure for the consummation ofexchanges and sustenance of ongoing relationships(Macaulay, 1963; March & Olsen, 1998).

As per the logic of instrumentalism, marketexchanges are structured by institutions thatemphasize the rule of formal contracts in dicta-ting the terms of firm–consumer relationships(Macaulay, 1963; March & Olsen, 1998). Because

the monitoring and enforcing of contracts arecritical to the instrumentality of market exchanges,the role of contracts is often vested in agencies thattranscend firms and consumers involved in marketexchanges. Typically federal, state, or regulatoryagencies fill this institutional role (Griffiths &Zammuto, 2005). For instance, in some nations,regulatory agencies provide commercial firms witha framework of mandatory contracts for differentlevels of products and services (e.g., heating oil,insurance) to consumers.

Contractually structured market exchanges areintended to ensure that consumers have access tothe products and services they need, and safeguardtheir interests from the opportunistic intentions offirms to restrict consumer welfare or renege onpromised products or services. Contracts need notalways be mandated by regulatory agencies. Firms,either individually or through collective action(e.g., associations), can offer formal contracts thatdetail terms of exchange with sufficient depth andclarity to mitigate the risk and uncertainty ofmarket exchanges. Such contracts, however, areunlikely to have pragmatic utility unless they areevaluated to be fair and enforceable by a neutralthird party with superseding power.

Few agencies can match the state and federallysupported institutions as a credible third party. Ina nation such as Germany, for instance, whereformal contracts are historically preferred, theinsurance market is governed by Bundesanstalt furFinanz-dienstleistungsaufsicht (BaFin), a federalagency for the supervision of financial services.The BaFin acts on federal laws that include detailedlegislation for insurance companies and its pro-ducts/services, and monitors firms for financialsolvency and compliance with the official guide-lines (see the Appendix for additional details).

An alternative mechanism for structuring marketexchanges is the logic of appropriateness (March &Olsen, 1998), where relational codes of conduct areinstitutionalized to emphasize trust and reciprocityamong market actors as a basis for reducing riskand uncertainty (Macaulay, 1963). The notion oftrust, central to the relational codes exemplified byappropriateness logics, is market actors’ (e.g., con-sumers’) confident expectation that other actorsinvolved in market exchanges (e.g., firms) will curbopportunism and fulfill exchange promises. Whentrust is one-sided, market exchanges may not besustainable. When trust is reciprocated, such thattrusted actors are committed to mutually satisfyingrelationships, relational codes dominate market

Consumers’ institutional logics Jagdip Singh et al

4

Journal of International Business Studies

exchanges and become institutionalized throughscripts and routines for long-term relationships.Formal institutional mechanisms of governance,including regulatory agencies and written con-tracts, are avoided recognizing that such mechan-isms may hinder the development of trust betweenmarket actors (Griffiths & Zammuto, 2005).

The relational logics have received much atten-tion as principles of relationship marketing in B2C(in addition to B2B) markets (Garbarino & Johnson,1999; Morgan & Hunt, 1994; Sirdeshmukh et al.,2002). Relationship marketing asserts that marketsbased on relational codes are self-reinforcing andefficient because they obviate the need for costlymonitoring and legal enforcement of contractualobligations. Relational codes commit market actorsto finding mutually acceptable solutions to pro-blems that permit the relationship to continue overtime (Dyer & Chu, 2000; Heide & Wathne, 2006).

For example, in the US where relationshipmarketing has taken hold, state and federal agen-cies set only minimum thresholds for insuranceproducts and services. Service and price levels varywidely across insurance providers (www.iii.org) toreflect different levels of customer relationships.Consumer blogs emphasize the importance ofselecting a reputable company for a long-termrelationship to secure a comprehensive coverageof insurance needs (www.insurance.ca.gov). Con-sistent with this, professional associations suchas the American Council of Life Insurers (ACLI)petition for limiting regulatory oversight, relyinginstead on self-regulation to stimulate competitive-ness and emphasize relational modes of exchange(see the Appendix for additional details).

Although we used the US and German insurancemarkets as examples that evidence relational andcontractual logics respectively, we emphasize that,in practice, institutional contexts of any market,including the US and Germany, are likely to evi-dence both logics to different degrees (March &Olsen, 1998). For example, while the contractslogic is compatible with the historical evolutionof the German insurance industry, the industrywas deregulated in 1994 to promote competition,reduce regulation, and favor relational orientationbetween providers and consumers. Likewise, in theUS, where the insurance industry was deregulatedat least a decade earlier, formal regulatory mechan-isms are assuming a greater role, with growingevidence of fraudulent and opportunistic activitiesof insurance providers (see the Appendix for addi-tional details).

CILMA and Culture: Points of Distinction andSimilaritiesThe proposed CILMA construct is distinct fromcultural constructs available in the literature,although it does share some common elements.Hofstede (1993) defines culture as the collectiveprogramming of the mind that distinguishes themembers of one category of people from those ofanother. Culture is composed of certain values,which shape behavior as well as one’s perceptionof the world. Examining this definition in light ofthe proposed conceptualization of the CILMAconstruct suggests three points of distinction.

First, cultural constructs reflect higher-order (i.e.,more general) programming of mental modelsshared by all members of a cultural community,and are ostensibly relevant across all situations.For instance, uncertainty avoidance is a culturalconstruct that reflects the ‘‘degree to which peoplein a country [generally] prefer structured overunstructured situations’’ (Hofstede, 1993: 90). Bycontrast, CILMA is a lower-order (i.e., less general)logic of the mental model that is specific to marketexchanges. Our theorizing of CILMA focuses speci-fically on the logics governing the social struc-ture of exchanges among market actors. Thecontract-relational duality is therefore unlikely tobe relevant for non-exchange situations such asinterpersonal and family relationships. In thissense, CILMA is proximal to the phenomenon ofmarket exchanges, whereas cultural constructsare located distally at a higher level of generality.

Second, the programming implied by culturalconstructs is ‘‘hardwired’’ as central to the identityof its members (Hofstede, 1993). For instance,German people are reportedly higher in uncer-tainty avoidance than those residing in the US,indicating that to be an American (German) is tohave a general preference for less (more) structuredexperiences. By contrast, the CILMA construct is‘‘soft-wired’’ in the sense that mental modelsdevelop with accumulating experience of marketexchanges in a particular industry/market. Becausethe CILMA construct is not moored to eitherindividual or collective identities, it is more labileand responsive to active constructions throughsocial mechanisms by market actors.

Third, the focus on values vs norms or expecta-tions is another source of difference. The culturalconstructs tap into underlying values that defineand characterize members of a cultural group.Germans are thought to prefer structure, not simplybecause it enhances predictability and efficiency,

Consumers’ institutional logics Jagdip Singh et al

5

Journal of International Business Studies

but because formal order and organization arevalued and aspired attributes by its members.Likewise, Americans are thought to value unpre-dictability, and disdain formal structures. This isnot because they would rather be inefficient anddisorganized, but in spite of it.

By contrast, the CILMA construct’s theoreticalfocus is on norms for market exchanges and,as a result, is more closely related to expectationsthat describe market actors’ behaviors in marketexchanges. Unlike values, such norms and beha-vioral expectations are more easily observable andidentifiable across markets because they are moreclosely tied to behavior.

It is also useful, however, to recognize somesimilarities between cultural constructs and CILMA.The CILMA construct is posited to set contextualcontingencies for the behaviors of market actors.Similarly, cultural constructs are thought to boundthe behaviors of members by what Poortinga (1992:10) has noted as ‘‘constraints that limit thebehavioral repertoire available to members.’’ Giventhis similarity, it is tempting to view cultural con-structs and CILMA simply as competing mecha-nisms of influence. This would be inappropriate,since CILMA is incompletely nested within thehigher-order cultural constructs. Cultural factorsplay a role, along with a host of other category-specific factors, in shaping the institutional logicsconceptualized as CILMA. It is appropriate to ask,for instance, whether the contract-relational duali-ty of CILMA goes beyond the structured-unstruc-tured duality represented by the uncertaintyavoidance construct. Also, unlike cultural con-structs, CILMA is proximal to market exchanges,and is conceptualized with lower-order specificityto enhance its relevance for the study of institu-tional influence on relationship marketing mecha-nisms. We develop hypotheses for this influencenext.

INSTITUTIONAL LOGICS AND FIRM–CONSUMER RELATIONSHIPS: FRAMEWORK

AND HYPOTHESES

Relationship Marketing and Firm–consumerRelationshipsRelationship marketing has emerged as ‘‘one ofthe dominant mantras in business strategy circles’’for understanding consumer–firm relationships(Palmatier et al., 2006: 136), and has been success-fully used for comparative international marketinganalysis (Wulf et al., 2001). Relationship marketing

is defined as ‘‘all marketing activities directedtoward establishing and maintaining successfulrelational exchanges’’ with a firm’s customers(Morgan & Hunt, 1994: 22). It shifts the marke-ters’ frame from a transactional to a relationshipmode, and asserts a customer-centric orientation(R. L. Oliver, 1997). A customer-centric orientationbrings into focus the critical role of sensing theevolving needs and preferences of customers, andmaking strategic decisions that enhance a firm’sability to gain customer commitment (Zeithaml,Berry, & Parasuraman, 1996). Committed custo-mers are motivated to maintain an ongoingrelationship with a specific firm through futurepurchase intentions, increased share of wallet, andpositive word of mouth. A portfolio of committedconsumers ensures a revenue stream essential forthe sustainability of a firm’s capabilities. Sensingand strategizing for sustained customer commit-ment are therefore key managerial responsibilitiesfor effective management of firm–consumer rela-tionships.

A significant amount of work, in both nationaland international contexts, supports relationshipmarketing mechanisms for gaining customer com-mitment (Palmatier et al., 2006). Although severalcompeting theories exist (Wulf et al., 2001), moststudies appear to converge around three keymechanisms for securing customer commitment:

(1) transactional satisfaction;(2) social trust; and(3) economic value (to be discussed).

With a few exceptions, relationship marketingstudies that examine contextual influences, suchas in comparative international marketing ana-lysis, tend to describe rather than theorize andexplain variability across contexts (Nijssen, Singh,Sirdeshmukh, & Holzmuller, 2003). As noted, Wulfet al. (2001) examine the mechanisms of relation-ship quality and commitment across three interna-tional markets, and find significant variabilityacross almost every modeled path for the three mar-kets (see their Table 4: 43). Consequently, there issufficient evidence to suggest that exchangemechanisms of relationship marketing vary signifi-cantly across market contexts, but there is littletheorizing to predict and explain this variability.

We develop institutional-theory-based explana-tions for hypothesizing the differentiated patternsof firm–consumer exchange mechanisms acrossmarket contexts. Specifically, we use the CILMAconstruct to explicate how consumers’ conceptions

Consumers’ institutional logics Jagdip Singh et al

6

Journal of International Business Studies

of a market’s institutional logics influence mechan-isms leading to their decisions to maintain ongoingrelationships with individual firms. However, wefirst outline a model that represents the extantrelationship marketing literature, and does notconsider the role of market context (referred to asthe ‘‘baseline’’ model). We do not posit formalhypotheses for these well-established effects.

A Baseline Model of Firm–consumer RelationshipsThe central block in Figure 1 displays the baselinemodel. The independent variables represent man-agerial agency for investing in mechanisms oftransactional satisfaction, social trust (firm andfrontline employee-based trust), and economicvalue. Each mechanism is evaluated by consumersand may subsequently be reciprocated with con-sumer commitment. Because these mechanisms arewell established in the literature, we provide only abrief review.

Consumers’ evaluation of transactional satisfac-tion involves the degree of fulfillment of some

need, desire, goal, or other pleasurable end-statein a specific exchange encounter with the firm(R. L. Oliver, 1997). Consumers form expectationsof future market transactions based on priorexperiences and knowledge (e.g., what do I expectto get?) and, when these expectations are fulfilledor positively confirmed (did I get what I expected,or more?), consumers perceive their exchangeto be satisfactory, thereby building commitment(R. L. Oliver, 1997).

The social trust mechanism involves consumers’evaluation that a firm can be relied upon to deliveron its promises and curb opportunism in futureexchanges (Morgan & Hunt, 1994). Substantialevidence suggests that consumers reward trustedfirms with their commitment (Palmatier et al.,2006). Factors resulting in positive trust evalua-tions include initiating and building long-termconsumer relationships, making idiosyncraticinvestments that foster consumer trust and resolveconflicts, and developing frontline capabilitiesthat place consumers’ interests above the firm’s

Consumers’ Institutional Logics of Market Action (CILMA)

Ongoing firm–consumer relationships

First-order effects

Sec

ond-

orde

r ef

fect

s

Firs

t-or

der

effe

cts

First-order Effects

First-order effects

Transactionsatisfaction

Firmtrust

Frontlineemployee

trust

Economicvalue

(shared and socially constructed mental model for the social structure of marketplace exchanges)

Consumercommitment

Figure 1 First- and second-order effects of consumers’ institutional logics of market action on mechanisms of ongoing firm–

consumer relationships.

Consumers’ institutional logics Jagdip Singh et al

7

Journal of International Business Studies

short-term revenue goals (Palmatier et al., 2006;Sirdeshmukh et al., 2002). Consistent with recentwork, frontline employee and firm trust are dis-tinguished.

Finally, consumers evaluate economic value byconsidering the benefits enjoyed relative to thecosts incurred in ongoing relationships. Severalstudies stress the importance of understandingeconomic value from the consumers’ perspective(Brief & Bazerman, 2003), and firms are increas-ingly focusing their efforts toward enhancingtangible and/or intangible consumer benefits with-out concomitant increases in costs (Sirdeshmukhet al., 2002).

Overall, relationship marketing theory posits thateach of the preceding three mechanisms directlyaffects consumer commitment. However, theseeffects are not necessarily linear. Recent studiesreport curvilinear effects such that, for instance inrelational exchanges, trust has a ‘‘motivator’’ effect(increasing exponentially) whereas transactionalsatisfaction has a ‘‘hygiene’’ effect (decreasingexponentially or leveling off). Only the effect ofeconomic value is reported to be linear (Agustin &Singh, 2005). Thus, in the baseline model, weinclude curvilinear effects of satisfaction and bothtrust mechanisms.

Influence of CILMAs on Firm–consumerRelationshipsA key insight from institutional theory is the non-trivial influence of institutional logics on indivi-dual behavior (Scott, 2001). Such institutionallogics are ‘‘rules of procedures that actors employflexibly and reflexively to assure themselves andthose around them that their behavior is reason-able’’ (DiMaggio & Powell, 1991: 20).

We draw on this insight to hypothesize thatconsumers are likely to weight exchange mechan-isms more favorably if they are aligned with thedominant institutional logic prevailing in themarket (referred to as the principle of alignment).Two specific hypotheses are developed relating toCILMA’s influence on: (1) the mean levels ofconsumers’ satisfaction, trust, value, and commit-ment evaluations for the individual firm withwhom they maintain ongoing relationships (‘‘first-order effects’’ in Figure 1); and (2) moderating theeffect of satisfaction and trust evaluations onconsumers’ commitment (indicated by ‘‘second-order effects’’ in Figure 1). We discuss each in turn.

In positing first-order effects, we assert thatconsumers’ normative expectations in market

relationships (e.g., what should I expect?) areshaped by the mental model of the market’sinstitutional field. For instance, when CILMA iscontracts-dominated, consumers expect firms toinvest in transactional capabilities. Quality norms,certifications, and other product guarantees man-dated by formal bodies in this institutional fieldmitigate the need for relational trust, and shiftthe focus toward transactional satisfaction. Kollock(1994) showed that when product quality is assu-red, or where ‘‘the experimenter served as a regula-tory agency to insure the terms of the exchange,’’relational trust between exchange parties was lessvital, and transactional factors assumed greaterimportance.

By contrast, in relational-dominated CILMA,consumers are likely to expect firms to invest incapabilities that emphasize relational processes andbuild trust (Agustin & Singh, 2005). The limitedmonitoring and safeguarding against opportunisticbehavior of individual firms is likely to favorconsumers’ motivation to develop close relation-ships with their providers.

Moreover, we expect higher levels of consumercommitment in a relational CILMA. Consumercommitment is a forward-looking indicator of con-sumers’ intentions to maintain ongoing relation-ships (Dyer & Chu, 2000). In contracts-dominatedCILMA, substitutability among providers is likelyto be high because the greater emphasis on insti-tutional standards for quality norms, certifications,and product guarantees mitigates the need forconsumer commitment toward any single pro-vider. By contrast, consumers in relational CILMAare more likely to rely on close relationships topolice opportunistic firm behaviors, and to avoidcosts of locating trustworthy providers. Thus weposit:

Hypothesis 1: Compared with contracts-domi-nated CILMA, relational-dominated CILMA willbe associated with (a) lower levels of transactionalsatisfaction, and (b) higher levels of trust andconsumer commitment.

In support of second-order effects, the principleof alignment also identifies conditions underwhich consumers will reciprocate a firm’s invest-ments with their commitment. When a marketis characterized by relational-dominated CILMA,consumers are likely to weight the relationalcapabilities of exchanges more favorably (Nijssenet al., 2003). Research on how consumers process

Consumers’ institutional logics Jagdip Singh et al

8

Journal of International Business Studies

information about markets (e.g., brands) andcategorize it to cope with market decisions effec-tively (e.g., brand choice) provides support for thisassertion (Bettman & Sujan, 1987). As per categor-ization research, consumers differentiate amongbrands on key attribute(s) that are relevant andsalient for a given market. Also, once brands aredifferentiated, consumers are more sensitive tovariations along the attributes used for categoriza-tion. This increased sensitivity is found to enhancethe weighting of the categorizing attributes inconsumer decisions (Bettman & Sujan, 1987).

Building on the preceding research, we expectthat consumers in relational CILMA will be likelyto differentiate among firms based on the socialtrust mechanism. This is because a relational-dominated CILMA primes consumers to attend tothe relational aspects of market exchange, makingsocial trust both relevant and salient. As a result,consumers are expected to be more sensitive toevaluations of relational trust, and to weight itmore favorably in making commitment decisions.Also, the ‘‘motivator’’ role of trust is expectedto be amplified in relational CILMA (Agustin &Singh, 2005). Thus the influence of trust is likely tofollow an exponentially increasing pattern inrelational CILMA, consistent with the motivatorhypothesis.

Similarly, when the institutional logic emphasizescontracts, consumers are primed to attend to thetransactional qualities of market relationships,including the degree to which firms meet or exceedexpectations when making commitment judgments.As a result, transactional satisfaction assumes a moresalient and relevant role in differentiating firms,while relational considerations of trust are givenless significance. Differentiation on the basis oftransactional capabilities is therefore likely tobolster consumers’ sensitivity to evaluations ofexchange satisfaction in making commitment deci-sions. This implies that the influence of transactionsatisfaction on consumer commitment is relativelystronger and more salient in contracts-dominatedCILMA. Consistent with this, we expect that theinfluence of satisfaction in relational-dominatedcontexts is likely to follow an exponentiallydecreasing pattern to reflect its relatively weakand hygiene effect in this context. Thus:

Hypothesis 2a: Compared with contracts-dominated CILMA, relational-dominated CILMAwill be associated with a relatively stronger effectof trust on commitment.

Hypothesis 2b: Compared with relational-dominated CILMA, contracts-dominated CILMAwill be associated with a relatively strongereffect of satisfaction on commitment.

Based on the universal importance of value, wedo not expect the economic mechanism to besensitive to variability in CILMA. To consumers,economic value represents a superordinate goal inmarket relationships (Sirdeshmukh et al., 2002).Firms lacking capabilities for providing consumer-perceived value will be less likely to gain consumercommitment, regardless of differences in institu-tional logics. Consequently, while we expect eco-nomic value to significantly influence consumercommitment, we do not expect consumers’ CILMAto have second-order effects on this influence.Thus:

Hypothesis 3: Consumers’ perceived economicvalue will have a significant effect on consumercommitment that is invariant to CILMA.

RESEARCH DESIGN AND METHOD

Study ContextWe selected a single industry and three contrastingnational contexts to examine empirically theCILMA construct and the posited hypotheses. Byfocusing on a single industry across markets, weaimed to provide variation in institutional fieldswhile controlling for confounding effects due tocross-industry variation. Because services are anincreasingly important aspect of leading econo-mies, we chose the insurance industry, particularlylife, home, and automobile insurance services.Health insurance was not included because theselection of a healthcare provider is often at thediscretion of an employer.

We used secondary data sources to identify theGerman, US, and Dutch markets as potentialcontexts that offered contrasting institutionallogics for the insurance industry as well as feasi-bility of collecting data in a systematic andcoordinated manner (to be discussed). Our selec-tion of these markets does not constitute an a priorispecification or predetermination of their locationin the institutional logics space. The secondarydata are intended only to ensure that we expectvariability across these markets for the institutionallogics of the insurance industry.

As stated earlier, the German insurance marketis governed by BaFin, a federal agency for the

Consumers’ institutional logics Jagdip Singh et al

9

Journal of International Business Studies

supervision of financial services. The BaFin actson federal laws that include detailed legislationfor insurance companies (VAG or Versicherungs-Aufsichts-Gesetz), products/services (VVG or Versi-cherungs-Vertrags-Gesetz), monitoring financialsolvency of firms, and imposing penalties, includ-ing voiding a firm’s license in the case of non-adherence or violations.

In the US, state and federal agencies set onlyminimum thresholds for insurance products andservices. Service and price levels vary widely acrossinsurance providers (www.iii.org), and consumerblogs emphasize the importance of selecting areputable company (www.insurance.ca.gov). Con-sistent with this, professional associations suchas the ACLI petition for limiting regulatory over-sight and promote self-regulation to stimulatecompetitiveness and emphasize relational modesof exchange.

Finally, the Dutch insurance market is rathercomplex, with two institutions sharing governanceresponsibilities, the De Nederlandsche Bank andAutoriteit Financiele Markten (AFM). While clearlydemarcated monitoring and standard-settingresponsibilities have yet to emerge, some progresshas been made, with the Dutch governmentshifting responsibility for consumer affairs to AFM(for further details see the Appendix).

Next, materials from Consumer Reports-typeagencies, as well as typical contracts for home andauto insurance in the three markets, were collected.Consistent with Faems, Janssens, Madhok, and vanLooy (2008), who examined the length of contrac-tual documents to infer the degree to which con-tracts are important in alliance governance, weused similar procedures to infer the importanceof contracts in individual insurance markets. Ouranalysis indicated that typical contracts for homeand auto insurance were relatively longer inGermany, and substantially shorter in the US(19–30% less) and the Netherlands (30–70% less)respectively (see the Appendix).

In accord with this trend, consumer organiza-tions in Germany (e.g., Stiftung Warentest) focusmore on price comparisons. By contrast, lead-ing consumer organizations in the US urge con-sumers to consider relational issues when selectingan insurance provider, noting that ‘‘it may not bewise to jump to an unknown company to savea few dollars’’ (www.ohioinsurance.gov, Shopper’sGuide, 7). Suggestions on how to select a pro-vider are also present in the Netherlands (e.g.,Consuwijzer) but the information is usually general

and not specific. In sum, the secondary data suggestthat the three countries selected offer a reasonablepossibility of obtaining variability in institutionallogics for the insurance industry.

Sampling ProceduresThe CILMA construct and the firm–consumerexchange constructs are conceptualized at thegroup and individual levels respectively. Thisallows data to be collected for each level eitherfrom two different groups of consumers or fromthe same consumer. Obtaining data from thesame consumer about the institutional logics andexchange constructs is likely to introduce same-source bias in testing hypotheses that relate thesetwo levels.

For instance, if the institutional logics constructwere measured first, it is likely that the respon-dents’ sensitivity to contractual and relationalissues would bleed into their evaluations ofexchange relationships. Likewise, if the institu-tional logics were measured subsequent toexchange relationships, respondents might havecarried their evaluative frames over to assessmentsof contractual and relational logics. Thus wepreferred data from two distinct samples, with eachfocusing on one level of data, and subsequentlyto combine them with the notion that the insti-tutional data capture contextual characteristicsthat are commonly shared across individuals thatbelong to that context.

We refer to these two data sets as: (1) institutionallogics data, that is, the data set drawn from a ran-dom sample of key informants to evaluate CILMA;and (2) firm–consumer relationships data, that is, thedata set drawn from a random sample of consumersto capture measures of their ongoing relationshipswith insurers. Sampling plans and field proceduresfor both data collections were coordinated acrosscountries to achieve equivalence in data collection,measurement, survey instrument, and data hand-ling (Easterby-Smith & Malina, 1999).

Institutional logics data. Random samples of keyinformants were selected from commercial lists ofconsumers, using selection criteria to ensureexperience with insurance products. The surveyswere administered in two waves, with an overallsurvey period covering 4–5 weeks. Customaryincentives were used to increase the response rate.In all, 1000 consumers in each of the threecountries were selected as key informants for

Consumers’ institutional logics Jagdip Singh et al

10

Journal of International Business Studies

participation. Informants were asked to self-selectfor participation if they met the following criteria:

(1) primary household responsibility for insuranceneeds;

(2) at least 35 years old; and(3) recent contact with insurance agent/company

to report problems and/or discuss changes to apolicy.

The numbers of qualified responses obtainedwere: 227 in Germany, 128 in the US, and 139 inthe Netherlands. On average, about two-thirdsof all respondents were male, with an average ageof about 50 years, and 80% married. The majorityof the respondents had a college degree, andan average yearly gross income of about $95,000in the US and $50,000 in the other two countries.

Firm–consumer relationships data. Random samplesof consumers were selected from independentcommercial lists, avoiding overlaps with thoseselected for institutional logics data. The surveyswere administered in a total of three waves spreadout over a 7–10-week survey period. Severalmeasures were taken to secure reasonable responserates (e.g., reminder cards, follow-up calls, andlottery drawing), allowing for small variations infield methods per country. In all, 4000 consumers inGermany, 3900 in the US, and 2850 in theNetherlands were selected for participation. Res-pondents were qualified to complete the survey ifthey identified an insurance company for whichthey had at least (1) one auto, home or lifeinsurance policy, and (2) one contact in the last 12months with a frontline employee regarding theirpolicy. Non-qualifying respondents were asked toreturn their surveys unfilled.

Using information from responses of non-quali-fying persons and follow up phone calls, a qualifyingrate was estimated at 47%, 55%, and 45% inGermany, the US, and the Netherlands, respec-tively. A qualifying rate indicates the percentage ofrespondents in a random sample of population whoare likely to meet the selection criteria establishedfor the study (i.e., at least one policy and inter-personal contact). Based on these qualifying ratesand the number of responses – 504 in Germany, 365in the US, and 316 in the Netherlands – theestimated response rates (corrected for qualifyingrates) were 26%, 21%, and 28% for Germany, theUS, and the Netherlands respectively.

Table 1 summarizes the demographic character-istics of the respondents, and shows that while

the Dutch and US data indicate a more evendistribution of gender groups (males¼55.6% and61.4% respectively), the German data are domi-nated by males (87.2%, po0.01). Moreover, theGerman respondent is likely to be older (mode X55years) than the Dutch or US respondents (mode¼35–44 years, po0.01). Although the householdsize in the US (mode¼4) is larger than in Germanyand the Netherlands (mode¼2, po0.01), the res-pondents’ marital status is fairly consistent acrossthe three contexts, with the majority being marr-ied (478%). Comparisons for education andincome are not straightforward, owing to thenecessity of using country-specific categories. How-ever, middle- to high-income households withhigher education dominate our sample, as maybe expected, based on the sampling design used.To account for this variability in demographiccharacteristics, gender, age, and income were inclu-ded as control variables.

Measurements

Institutional logics data. Initially, we formulated aset of 20 items to operationalize the CILMAconstruct. Half the items pertained to the logic ofcontracts, and the remaining items referred torelational logic. The master version of the que-stionnaire was developed in English and translated–back-translated into Dutch and German, using twobilingual respondents. In addition, the Germanversion was translated into Dutch and triangulatedwith the Dutch version derived from the Englishmaster version. Discrepancies were discussed, andjointly resolved for comprehension consistencyby either revising the master version or adaptingthe translated version to accurately reflect theintended meaning. The revised items were pretes-ted using a think-aloud exercise with a sample of18–30 consumer informants in each country.Researchers met to discuss pretest results, andaimed to select items that were robust acrosscontexts and sufficiently non-overlapping to pro-vide a representative coverage of construct band-width. Based on this, a final list of 12 items wasretained (see Table 2).

Firm–consumer relationships data. To capture thefirm–consumer exchange constructs, we reliedmostly on existing scales for transactional satis-faction, firm and frontline employee trust, eco-nomic value and consumer commitment.Most measures were drawn from the marketing

Consumers’ institutional logics Jagdip Singh et al

11

Journal of International Business Studies

Table 1 Demographic profile of the respondents for the firm–consumer relationships data (all numbers are in percentages)

Gender (%) Age in years (%) Educationa

Gb US NLb G US NL G US NL

Male 87.2 55.6 61.4 p34 7.0 22.7 28.2 High school 1st level 32.7 — 14.4

Female 12.8 44.4 38.6 35–44 23.0 34.3 30.1 High school 2nd level 8.7 19.3 12.0

45–54 29.4 24.4 23.0 Professional education 28.0 — 27.8

X55 40.7 18.6 18.7 Some college — 30.5 27.3

College — 30.5 14.8

Graduate school 30.6 19.8 3.8

Marital status Household size (%) Incomec (%)

G US NL No. of people G US NL G US NL

Married 81.6 82.7 78.5 1 10.2 7.4 16.7 o h12,000 5.7 — 3.1

Single 5.8 9.1 14.4 2 46.4 25.5 41.1 h12,001–24,000 33.3 — 39.8

Divorced/sep. 10.2 6.6 4.3 3 17.8 21.0 12.0 h24,001–36,000 31.2 — 34.0

Widow/widower 2.3 1.6 2.9 4 17.5 26.7 20.6 h36,001–48,000 13.2 — 13.1

5 6.4 12.8 6.7 h48,001–60,000 6.9 — 6.8

46 1.7 6.6 2.9 h60,001–72,000 3.9 — —

h72,001–84,000 2.4 — —

4 h84,000 3.3 — 2.1

o $35,000 — 8.3 —

$35,001–54,999 — 30.7 —

$55,000–74,999 — 25.9 —

$75,000–94,999 — 17.6 —

$95,000–114,999 — 8.3 —

$115,000–134,999 — 2.7 —

4 $135,000 — 6.6 —

aThe category labels for education categories were modified for relevance in each cross-national context. For the Dutch data, the categories labels were: (1) mavo/havo/vwo; (2) lbo; (3) mbo;(4) hbo; (5) universiteit; (6) higher. For the US data, the categories labels were: (1) high school; (2) some college; (3) college; (4) graduate studies; For the German data, the categories labels were:(1) high school (1 level), (2) high school (2 level), (3) professional education, and (4) university degree.bG¼Germany, NL¼the Netherlands, US¼United States.cSimilarly, because income levels and currencies vary across nations, the category labels were adjusted for relevance for each cross-national data. For the German and Dutch data, net income is usedafter tax deduction, whereas for the US data, gross income before tax deduction is employed.

Co

nsu

mers’

institu

tion

al

log

ics

Jag

dip

Sin

gh

et

al

12

Journ

al

of

Inte

rnatio

nalBusin

ess

Stu

die

s

Table 2 Operational measures and reliabilities of study constructsa

Consumer institutional logics of market actions (CILMA) dimensions

Relational dimension, five-point scale, Strongly disagree–Strongly agree, RelG¼0.93, AVEG¼0.70, HVSG¼0.10, RelUS¼0.95, AVEUS¼0.78,

HVSUS¼0.39, RelNL¼0.92, AVENL¼0.68, HVSNL¼0.35.

Interactions between consumers and insurance companies and agents are generally based on y

Trusting relationships (REL1)

Terms of doing business that are satisfying for both, insurer and customer (REL2)

Working through problems in a mutually satisfying manner (REL3)

Developing a mutual understanding (REL4)

Open and honest relationships (REL5)

Maintaining a long-term working relationship (REL6)

Contracts dimension, five-point scale, Strongly disagree–Strongly agree, RelG¼0.97, AVEG¼0.83, HVSG¼0.07, RelUS¼0.95, AVEUS¼0.76,

HVSUS¼0.22, RelNL¼0.95, AVENL¼0.75, HVSNL¼0.35.

Interactions between consumers and insurance companies and agents are generally based on y

Meeting only the requirements of the policy contract (CON1)

Following written rules of contract even when solving problems (CON2)

Strictly following contract guidelines (CON3)

Contractual details (e.g., fine print) rather than working flexibly to meet customer needs (CON4)

Procedures and practices spelled out in formal agreements (CON5)

Formal requirements set by the rules of the contract (CON6)

Consumer–firm exchange constructs

Satisfaction (R. L. Oliver, 1997), ten-point scale, RelG¼0.96, AVEG¼0.90, HVSG¼0.62, RelUS¼0.96, AVEUS¼0.88, HVSUS¼0.28, RelNL¼0.95,

AVENL¼0.86, HVSNL¼0.64;

Your overall feelings of satisfaction involving the recent interactions with the issuing insurance company:

Highly satisfactory/Highly unsatisfactory (SAT1)

Very pleasant/Very unpleasant (SAT2)

Delightful/Terrible (SAT3)

Frontline employee trust (Morgan & Hunt, 1994), ten-point scale, RelG¼0.96, AVEG¼0.91, HVSG¼0.62, RelUS¼0.98, AVEUS¼0.94,

HVSUS¼0.44, RelNL¼0.96, AVENL¼0.90, HVSNL¼0.57;

I feel that the representatives (e.g., agents/employees) of this company are:

Very dependable/Very undependable (FLE1)

Of very high integrity/Of very low integrity (FLE2)

Very trustworthy/Not at all trustworthy (FLE3)

Firm trust (Morgan & Hunt, 1994), ten-point scale, RelG¼0.97, AVEG¼0.93, HVSG¼0.58, RelUS¼0.99, AVEUS¼0.97, HVSUS¼0.45, RelNL¼0.97,

AVENL¼0.92, HVSNL¼0.45;

I feel that this insurance company’s management practices are:

Very dependable/Very undependable (FIRM1)

Of very high integrity/of very low integrity (FIRM2)

Very trustworthy/Not at all trustworthy (FIRM3)

Economic value (Sirdeshmukh et al., 2002), ten-point scale, RelG¼0.97, AVEG¼0.91, HVSG¼0.46, RelUS¼0.99, AVEUS¼0.96, HVSUS¼0.45,

RelNL¼0.96, AVENL¼0.90, HVSNL¼0.57;

Considering all of the insurance benefits you receive in exchange for the prices (premiums) you pay, how would you rate this company relative to

its competitors?

Very good value/Extremely poor value (VAL1)

Very good deal/Very poor deal (VAL2)

Very worthwhile/Not at all worthwhile (VAL3)

Consumer commitment (Zeithaml et al., 1996), seven-point scale, Very unlikely–Very likely, RelG¼0.91, AVEG¼0.77, HVSG¼0.37, RelUS¼0.87,

AVEUS¼0.75, HVSUS¼0.32, RelNL¼0.89, AVENL¼0.75, HVSNL¼0.19;

How likely are you to:

Use this company for most of your future insurance needs (COM1)

Use this company the next time you need to buy insurance (COM2)

Use this company for other financial services that you may require (COM3)

aThe psychometric properties of constructs are indicated by composite reliability (Rel) and average variance extracted (AVE), as well as by highestvariance shared (HVS), as per Fornell and Larcker (1981).

Consumers’ institutional logics Jagdip Singh et al

13

Journal of International Business Studies

literature, and evidenced acceptable psychometricproperties (see Table 2). A translation–back-trans-lation procedure and follow-up triangulation wereused for developing a final set of context-robustoperational measures for inclusion in the surveyinstrument.

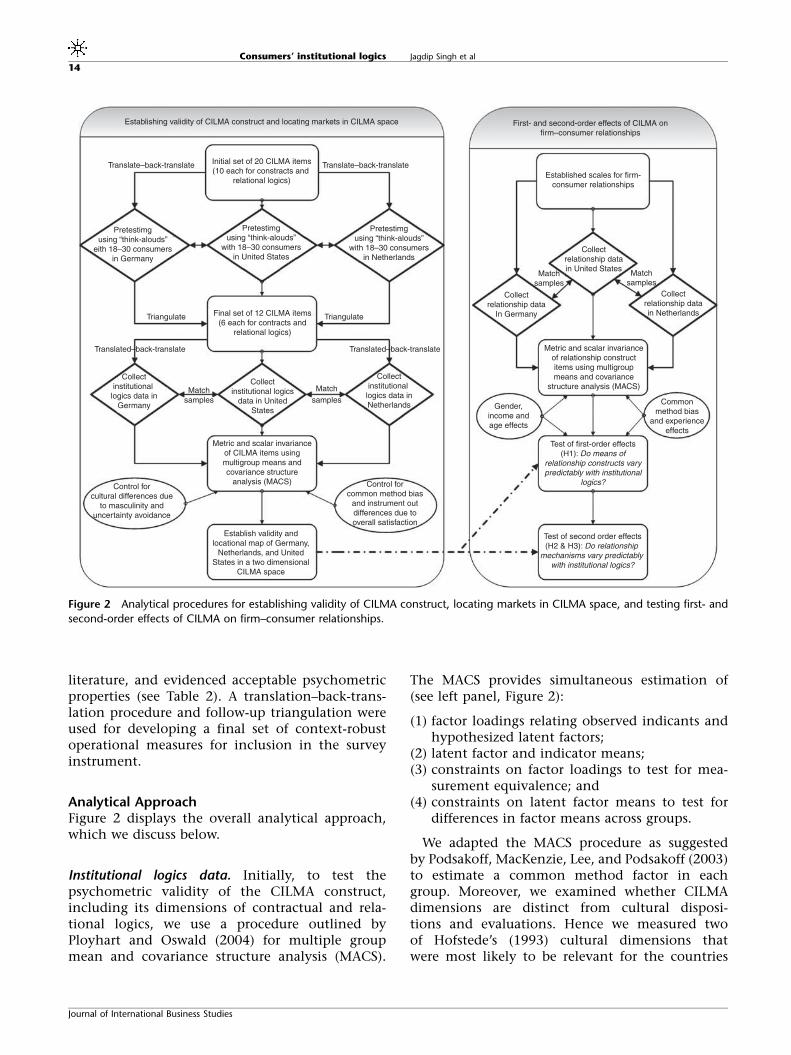

Analytical ApproachFigure 2 displays the overall analytical approach,which we discuss below.

Institutional logics data. Initially, to test thepsychometric validity of the CILMA construct,including its dimensions of contractual and rela-tional logics, we use a procedure outlined byPloyhart and Oswald (2004) for multiple groupmean and covariance structure analysis (MACS).

The MACS provides simultaneous estimation of(see left panel, Figure 2):

(1) factor loadings relating observed indicants andhypothesized latent factors;

(2) latent factor and indicator means;(3) constraints on factor loadings to test for mea-

surement equivalence; and(4) constraints on latent factor means to test for

differences in factor means across groups.

We adapted the MACS procedure as suggestedby Podsakoff, MacKenzie, Lee, and Podsakoff (2003)to estimate a common method factor in eachgroup. Moreover, we examined whether CILMAdimensions are distinct from cultural disposi-tions and evaluations. Hence we measured twoof Hofstede’s (1993) cultural dimensions thatwere most likely to be relevant for the countries

Establishing validity of CILMA construct and locating markets in CILMA space

Translate–back-translate Initial set of 20 CILMA items(10 each for constracts and

relational logics)

Translate–back-translate

Pretestimgusing “think-alouds”

eith 18–30 consumersin Germany

Triangulate Final set of 12 CILMA items(6 each for contracts and

relational logics)

Pretestimgusing “think-alouds”

with 18–30 consumersin United States

Pretestimgusing “think-alouds”

with 18–30 consumersin Netherlands

Triangulate

Translated–back-translate Translated–back-translate

Collectinstitutional logics data in

Germany

Matchsamples

Matchsamples

Collectinstitutional logics

data in UnitedStates

Collectinstitutional logics data inNetherlands

Metric and scalar invarianceof CILMA items usingmultigroup means andcovariance structure

analysis (MACS)Control for

cultural differences dueto masculinity and

uncertainty avoidance

Establish validity andlocational map of Germany,

Netherlands, and UnitedStates in a two dimensional

CILMA space

Control forcommon method bias

and instrument outdifferences due tooverall satisfaction

First- and second-order effects of CILMA onfirm–consumer relationships

Established scales for firm-consumer relationships

Collectrelationship datain United States

Collectrelationship datain Netherlands

Collectrelationship data

In Germany

Matchsamples

Matchsamples

Metric and scalar invarianceof relationship constructitems using multigroupmeans and covariance

structure analysis (MACS)

Gender,income andage effects

Commonmethod bias

and experienceeffects

Test of first-order effects(H1): Do means of

relationship constructs varypredictably with institutional

logics?

Test of second order effects(H2 & H3): Do relationship

mechanisms vary predictably with institutional logics?

Figure 2 Analytical procedures for establishing validity of CILMA construct, locating markets in CILMA space, and testing first- and

second-order effects of CILMA on firm–consumer relationships.

Consumers’ institutional logics Jagdip Singh et al

14

Journal of International Business Studies

considered – masculinity and uncertainty avoid-ance – and included these as control variables in theMACS analysis. Whereas the three countries are alllow on power distance, and similarly high onindividualism, Germany is relatively higher inuncertainty avoidance than the US, and the USand Germany are relatively more masculine thanthe Netherlands.

Finally, we recognize that, despite our best effortsto select random samples with identical researchdesigns across contexts, sampled respondentsmay differ systematically. To control for this biaswe included respondents’ overall satisfaction withinsurance providers as an instrumental variable,resulting in the following estimated equations:

Z1j ¼ l1j þ g1;1c1j þ g1;2c2j þ g1;3c3j þ y1j ð1Þ

Z2j ¼ l2j þ g2;1c2j þ g2;2c2j þ g2;3c3j þ y2j ð2Þ

Here, Z1 and Z2 correspond to latent constructs forrelational and contracts logics, respectively; lrepresents the latent factor means; c1 refers tooverall satisfaction; c2 and c3 represent the culturaldimensions of masculinity and uncertainty avoid-ance; and the subscript j indexes the marketcontext (1¼Germany, 2¼US, 3¼the Netherlands).We selected Germany as the baseline group, con-straining its latent means for both dimensions (i.e.,Z11 and Z21) to 0. Finally, the results of the analyseswere plotted in a two-dimensional space of rela-tional and contracts logics to facilitate interpreta-tion and testing of first- and second-order effects (tobe discussed).

Firm–consumer relationships data. Initially, we usedthe MACS approach to estimate the latent meansfor the exchange constructs and test for differencesin latent means across CILMAs (see right panel,Figure 2). To test for the first-order hypothesis,we employed the LM test for multiple-group com-parisons involving latent mean differences for theNetherlands and US relative to the German data.For this purpose, we used the multiple-groupstructural equation modeling (SEM) procedureoutlined by Card and Little (2006), which expli-citly addresses metric and scalar equivalence issues.To control for other confounding effects andalternative explanations, we included:

(1) common method factor, as noted above;(2) consumer experience (i.e., number of contacts

with the provider in the last 24 months); and

(3) individual consumers’ gender, age, and income,as samples differ on these demographic char-acteristics (see Figure 2).

For testing the second-order effects, we utilized atwo-step single-indicant approach by Ping (1995),which controls for measurement error in curvi-linear terms, and involved estimating the followingequation:

pj ¼kj þ B1x1j þ B2x2j þ B3x3j þ B4x4j þ B5x1j�x1j

þ B6x2j�x2j þ B7x3j�x3j þ B8x5j þ B9x6j

þ B10x7j þ B11x8j þ zj

ð3Þ

where p is consumer commitment construct, andthe vector n represents the exogenous variablessuch that x1 to x4 correspond to satisfaction, firmtrust, frontline employee trust, and economicvalue, respectively, and their corresponding quad-ratic terms are represented by product expressions(e.g., x1� x1). In addition, x5 refers to the level ofconsumer–firm interaction, while x6, x7 and x8

represent gender, age and income, respectively,which are included to control for individualcharacteristics.

We analyzed all three markets in a single,simultaneous analysis. For this purpose, we esti-mated factor scores for each construct, and usedmultiple group comparisons to identify patterns ofsimilarities and differences in estimated effectsacross markets. If the respective test for suchcomparison was significant, we released the con-straint, and tested for bivariate equality. Separateestimates were obtained for corresponding coeffi-cients only if all tests were significant.

RESULTS

Institutional Logics Data

Overall psychometrics and model fits. Tables 3 and 4summarize the results from the MACS analysis.Regardless of the model estimated, the CILMAitems depict sound psychometric properties (seeTable 4). All items load significantly (40.4,po0.05) on their corresponding contracts orrelational factors, which, in combination withsmall residuals (SRMR¼0.01), provide evidence ofconvergent validity. Table 4 also reports the averagevariance extracted (AVE) and highest varianceshared (HVS), based on the final model (Fornell &Larcker, 1981). The AVE are estimated at 0.70(Germany), 0.78 (US), and 0.68 (the Netherlands)

Consumers’ institutional logics Jagdip Singh et al

15

Journal of International Business Studies

for relational logics, and 0.83 (Germany), 0.76 (US),and 0.75 (the Netherlands) for contracts logics.Without exception, each construct extractssignificantly more variance from its own items

than it shares with any other construct. Thisprovides support for discriminant validity.Specifically, the estimated correlations betweenthe dimensions of contracts and relational logics

Table 3 Model fit statistics and latent mean total effects estimates from MACS analysis of CILMA data

Model estimated: Constraints used Model fit statistics

w2 df Dw2 (Ddf) p-value for Dw2 CFI NFI TLI RMSEA (90% CI)

M1: fully unconstrained 924.9*** 615 — — 0.99 0.98 0.99 0.032 (0.028; 0.036)M2: loadings fully constrained 970.0*** 647 45.1w (32) 0.06 0.99 0.98 0.99 0.032 (0.028; 0.036)M3: intercepts fully constrained 1094.2*** 693 124.2*** (46) o0.01 0.99 0.98 0.99 0.034 (0.030; 0.038)

M3a: intercepts partially constrained 976.5*** 674 6.5 (27) 0.99 0.99 0.98 0.99 0.030 (0.026; 0.034)M4: latent means fully constrained 1031.9*** 684 55.4*** (7) o0.01 0.99 0.98 0.99 0.032 (0.028; 0.036)M4a: latent means partially constraineda 954.4*** 673 29.5 (58) 0.99 0.99 0.98 0.99 0.029 (0.025; 0.033)

aSome loadings gave significant LM tests upon introduction of scalar constraints, which led to differences in degrees of freedom.wSignificant at the 10% level; ***significant at the 0.1% level.

Table 4 Fit statistics, factor loadings, measurement properties and interfactor correlations of CILMA dimensions across contexts from

partially constrained multi-group confirmatory factor analysis

Itemsa Germany (high contract,low relational)

US (intermediate contract,high relational)

The Netherlands(low contract,

high relational)

lb Int.c Rel.d AVE e HVS f lb Int.c Rel.d AVE e HVS f lb Int.c Rel.d AVE e HVS f

Relations 0.00g 0.93 0.70 0.10 0.85*** 0.95 0.78 0.39 0.77*** 0.92 0.68 0.351. REL1 1.00 �0.46*** 1.00 �0.46*** 1.00 �0.46***

2. REL2 0.92*** �0.49*** 0.92*** �0.20* 0.92*** �0.49***3. REL3 1.05*** �0.52*** 1.05*** �0.52*** 1.05*** �0.39***4. REL4 1.10*** �0.45*** 1.10*** �0.45*** 0.89*** �0.45***

5. REL5 1.06*** �0.53*** 1.27*** �0.75*** 1.06*** �0.35***6. REL6 0.86*** �0.37*** 0.86*** �0.37*** 0.73*** �0.37***

Contracts 0.00g 0.97 0.83 0.07 �0.64*** 0.95 0.76 0.22 �0.81*** 0.95 0.75 0.351. CON1 1.00 0.47*** 1.00 0.47*** 1.00 0.30***2. CON2 1.08*** 0.45*** 1.08*** 0.45*** 1.08*** 0.45***3. CON3 1.17*** 0.45*** 1.01*** 0.45*** 1.17*** 0.45***

4. CON4 1.13*** 0.38*** 0.90*** 0.38*** 1.13*** 0.57***5. CON5 1.18*** 0.49*** 1.18*** 0.49*** 1.18*** 0.49***6. CON6 1.18*** 0.44*** 1.18*** 0.62*** 1.18*** 0.44***

Masculinity 0.00g 0.80 0.67 0.07 0.92*** 0.81 0.67 0.39 0.54*** 0.80 0.67 0.061. MASC1 1.00 �0.40*** 1.00 �0.40*** 1.00 �0.40***

2. MASC3 1.06*** �0.42*** 1.06*** �0.42*** 1.06*** �0.42***

Uncertainty avoid. 0.00g 0.64 0.59 0.16 �0.31*** 0.79 0.65 0.14 �0.60*** 0.58 0.53 0.16

1. UA1 1.00 0.27** 1.00 0.27** 1.00 0.27**2. UA3 0.55*** 0.31*** 1.11*** �0.16* 0.55*** 0.31***

Model fit statistics: w2(673)¼954.5 (po0.001); CFI¼0.99; NFI¼0.98; TFI¼0.99; SRMR¼0.05; RMSEA (90% confidence interval)¼0.03 (0.025–0.033).

aComplete text of item statements is in Table 2.bLoading estimate (t-value); all significant at p¼0.01.cIntercept estimate for item level/latent mean estimate for construct level.dEstimated composite reliability (Fornell & Larcker, 1981).eAverage variance extracted (Fornell & Larcker, 1981).fHighest variance shared (Fornell & Larcker, 1981).gLatent means for Germany have been constrained to 0 (baseline group).Italic loadings non-invariant across contexts.*significant at the 5% level; **significant at the 1% level; ***significant at the 0.1% level.

Consumers’ institutional logics Jagdip Singh et al

16

Journal of International Business Studies

are estimated as �0.32 (Germany), �0.62 (US), and�0.59 (the Netherlands), suggesting less than 35%shared variance. The preceding convergent anddiscriminant validity evidence is largelyunperturbed across the different models estimatedand reported in Table 3.

Next, as reported in Table 3, we tested for metricand scalar invariance before testing differences inlatent means (Card & Little, 2006; Steenkamp &Baumgartner, 1998). The condition for metricinvariance is met, since constraining all loadingsto equal across the three market contexts yieldsa non-significant change in w2 (M2: w2

diff¼45.1,dfdiff¼32, p¼0.06). However, the scalar invariancecondition is not met, since constraining corre-sponding observed means to equal across contextsresults in a significant increase in w2 (M3: w2

diff¼124.2, dfdiff¼46, po0.01). To test for partial scalarinvariance, we released some constraints in accordwith Steenkamp and Baumgartner (1998: 81) toobtain a non-significant increase in w2 over M2(M3a: w2

diff¼6.5, dfdiff¼27, p¼0.99).To examine whether the latent means for CILMA

construct vary across market contexts, we com-pared a fully constrained model (M4) with a modelthat meets metric and scalar (partial) invari-ance condition (M3a). This comparison yields asignificant w2, indicating that the latent meansdiffer substantially (w2

diff¼55.4, dfdiff¼7, po0.01).We released constraints based on Lagrange multi-plier (LM) test to obtain a final model that isequivalent to model M3a (M4a: w2

diff¼29.5, dfdiff¼58, p¼0.99) and fits the data well (w2

df¼673¼954.4,

TLI¼0.99, CFI¼0.99, RMSEA¼0.029 (90% CI: 0.025,0.033)). We use this final model for latent meanscomparisons of CILMA dimensions.

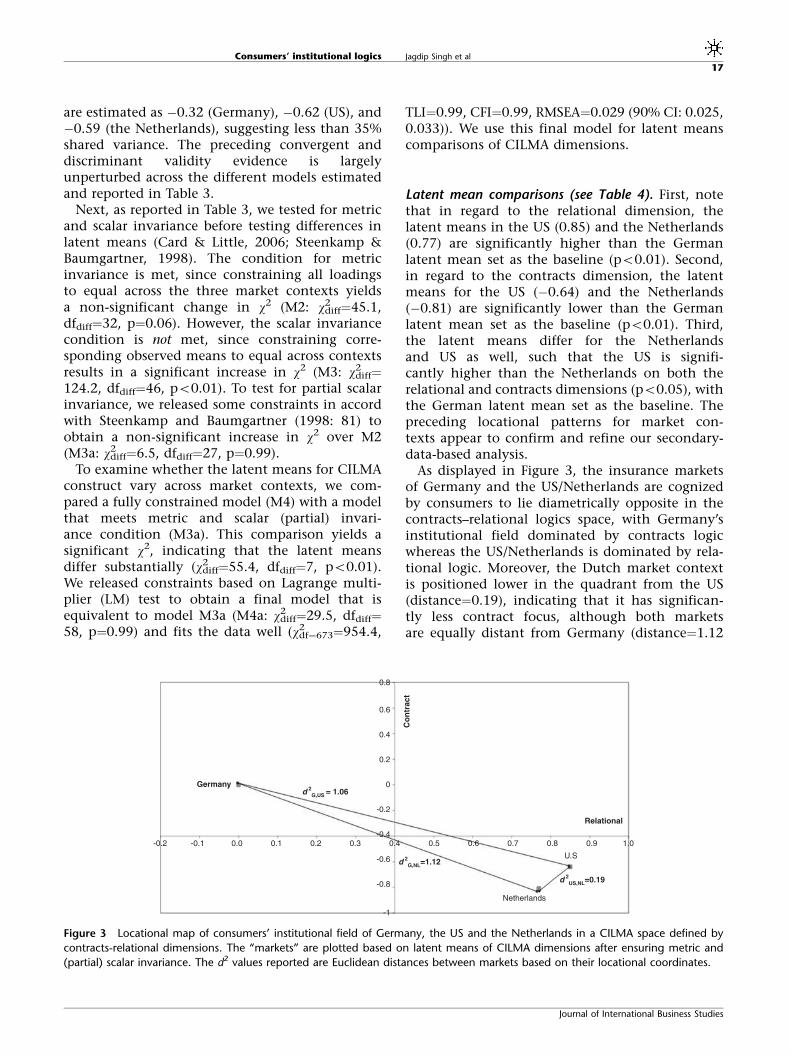

Latent mean comparisons (see Table 4). First, notethat in regard to the relational dimension, thelatent means in the US (0.85) and the Netherlands(0.77) are significantly higher than the Germanlatent mean set as the baseline (po0.01). Second,in regard to the contracts dimension, the latentmeans for the US (�0.64) and the Netherlands(�0.81) are significantly lower than the Germanlatent mean set as the baseline (po0.01). Third,the latent means differ for the Netherlandsand US as well, such that the US is signifi-cantly higher than the Netherlands on both therelational and contracts dimensions (po0.05), withthe German latent mean set as the baseline. Thepreceding locational patterns for market con-texts appear to confirm and refine our secondary-data-based analysis.

As displayed in Figure 3, the insurance marketsof Germany and the US/Netherlands are cognizedby consumers to lie diametrically opposite in thecontracts–relational logics space, with Germany’sinstitutional field dominated by contracts logicwhereas the US/Netherlands is dominated by rela-tional logic. Moreover, the Dutch market contextis positioned lower in the quadrant from the US(distance¼0.19), indicating that it has significan-tly less contract focus, although both marketsare equally distant from Germany (distance¼1.12

Co

ntr

act

0.8

0.6

0.4

0.2

0

-0.2

-0.4

-0.6

-0.8

-1

-0.2 -0.1 0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0

Relational

U.S

Netherlands

d 2US,NL=0.19

d 2G,NL=1.12

d 2G,US = 1.06

Germany

Figure 3 Locational map of consumers’ institutional field of Germany, the US and the Netherlands in a CILMA space defined by

contracts-relational dimensions. The ‘‘markets’’ are plotted based on latent means of CILMA dimensions after ensuring metric and

(partial) scalar invariance. The d2 values reported are Euclidean distances between markets based on their locational coordinates.

Consumers’ institutional logics Jagdip Singh et al

17

Journal of International Business Studies

and 1.06, respectively). For this reason, the USinstitutional market context is identified in Table 4as reflecting ‘‘intermediate’’ focus on contracts,whereas the Netherlands is identified as relatively‘‘low’’ focus on contracts. Both institutional mar-ket contexts are noted as relatively high on rela-tional logics.

Test of Hypotheses Using Firm–consumerRelationships Data

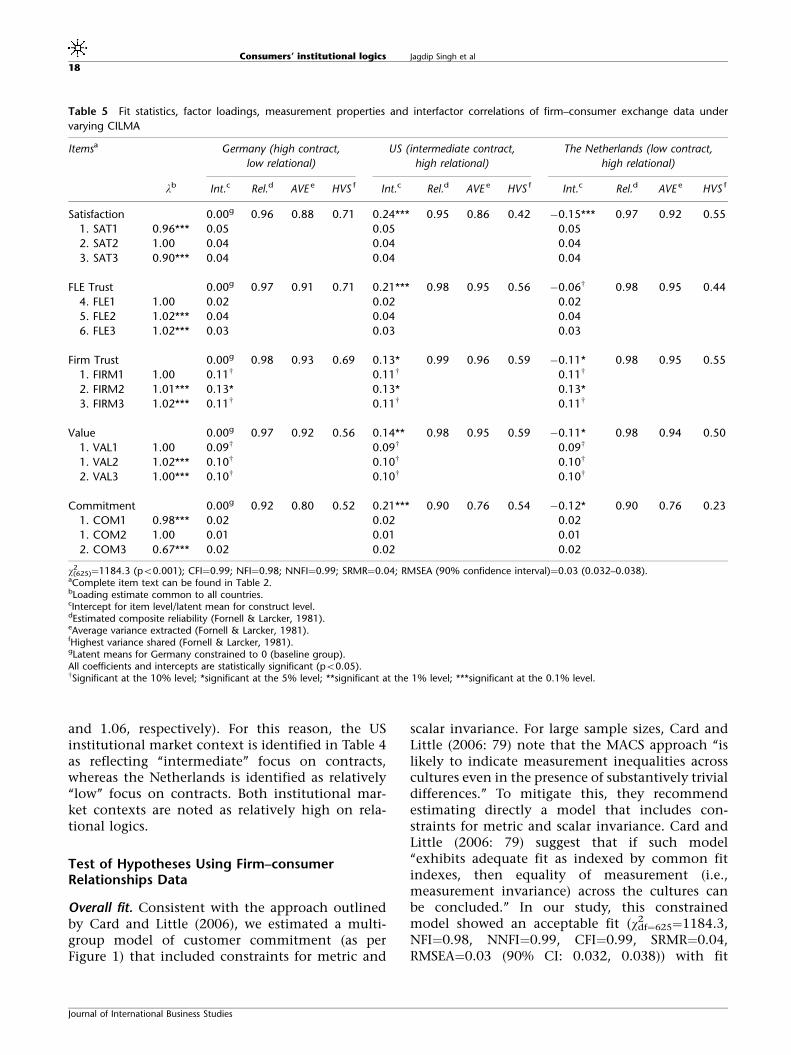

Overall fit. Consistent with the approach outlinedby Card and Little (2006), we estimated a multi-group model of customer commitment (as perFigure 1) that included constraints for metric and

scalar invariance. For large sample sizes, Card andLittle (2006: 79) note that the MACS approach ‘‘islikely to indicate measurement inequalities acrosscultures even in the presence of substantively trivialdifferences.’’ To mitigate this, they recommendestimating directly a model that includes con-straints for metric and scalar invariance. Card andLittle (2006: 79) suggest that if such model‘‘exhibits adequate fit as indexed by common fitindexes, then equality of measurement (i.e.,measurement invariance) across the cultures canbe concluded.’’ In our study, this constrainedmodel showed an acceptable fit (w2

df¼625¼1184.3,NFI¼0.98, NNFI¼0.99, CFI¼0.99, SRMR¼0.04,RMSEA¼0.03 (90% CI: 0.032, 0.038)) with fit

Table 5 Fit statistics, factor loadings, measurement properties and interfactor correlations of firm–consumer exchange data under

varying CILMA

Itemsa Germany (high contract,

low relational)

US (intermediate contract,

high relational)

The Netherlands (low contract,

high relational)

lb Int.c Rel.d AVE e HVS f Int.c Rel.d AVE e HVS f Int.c Rel.d AVE e HVS f

Satisfaction 0.00g 0.96 0.88 0.71 0.24*** 0.95 0.86 0.42 �0.15*** 0.97 0.92 0.55

1. SAT1 0.96*** 0.05 0.05 0.05

2. SAT2 1.00 0.04 0.04 0.04

3. SAT3 0.90*** 0.04 0.04 0.04

FLE Trust 0.00g 0.97 0.91 0.71 0.21*** 0.98 0.95 0.56 �0.06w 0.98 0.95 0.44

4. FLE1 1.00 0.02 0.02 0.02

5. FLE2 1.02*** 0.04 0.04 0.04

6. FLE3 1.02*** 0.03 0.03 0.03

Firm Trust 0.00g 0.98 0.93 0.69 0.13* 0.99 0.96 0.59 �0.11* 0.98 0.95 0.55

1. FIRM1 1.00 0.11w 0.11w 0.11w

2. FIRM2 1.01*** 0.13* 0.13* 0.13*

3. FIRM3 1.02*** 0.11w 0.11w 0.11w

Value 0.00g 0.97 0.92 0.56 0.14** 0.98 0.95 0.59 �0.11* 0.98 0.94 0.50

1. VAL1 1.00 0.09w 0.09w 0.09w

1. VAL2 1.02*** 0.10w 0.10w 0.10w

2. VAL3 1.00*** 0.10w 0.10w 0.10w

Commitment 0.00g 0.92 0.80 0.52 0.21*** 0.90 0.76 0.54 �0.12* 0.90 0.76 0.23

1. COM1 0.98*** 0.02 0.02 0.02

1. COM2 1.00 0.01 0.01 0.01

2. COM3 0.67*** 0.02 0.02 0.02

w2(625)¼1184.3 (po0.001); CFI¼0.99; NFI¼0.98; NNFI¼0.99; SRMR¼0.04; RMSEA (90% confidence interval)¼0.03 (0.032–0.038).

aComplete item text can be found in Table 2.bLoading estimate common to all countries.cIntercept for item level/latent mean for construct level.dEstimated composite reliability (Fornell & Larcker, 1981).eAverage variance extracted (Fornell & Larcker, 1981).fHighest variance shared (Fornell & Larcker, 1981).gLatent means for Germany constrained to 0 (baseline group).All coefficients and intercepts are statistically significant (po0.05).wSignificant at the 10% level; *significant at the 5% level; **significant at the 1% level; ***significant at the 0.1% level.

Consumers’ institutional logics Jagdip Singh et al

18

Journal of International Business Studies

indices meeting all relevant criteria (see Table 5).Moreover, each study construct has estimatedreliabilities exceeding 0.85, and an AVE greaterthan 0.75, indicating acceptable convergent vali-dity. Finally, as summarized in Table 5, each con-struct meets Fornell and Larcker’s (1981) criterionfor discriminant validity (AVE4HVS). Overall,the constructs indicate acceptable psychometricproperties.

First-order effects (Hypothesis 1). The results aresummarized in Table 6. As per Hypothesis 1, wehad predicted that relational-dominated con-texts would be associated with higher trust andcommitment (Hypothesis 1b), while contracts-dominated contexts will evidence higher levelsof satisfaction (Hypothesis 1a). Relative to theGerman context, the estimated latent mean forsatisfaction is significantly higher in the US context(0.24), but lower in the Dutch context (�0.15, allcomparisons po0.05). This provides mixed sup-port for Hypothesis 1a. Likewise, the estimatedlatent means for commitment and trust (frontlineemployee and firm) are significantly higher in theUS context than in the German context (0.21, 0.21and 0.13, all po0.05). The preceding pattern oflatent means is not obtained for the Netherlands,where the estimated latent means are generallylower than in Germany (�0.12 (po0.1), �0.06 (ns),and �0.11 (po0.05)). Thus our findings providepartial support for Hypothesis 1b.

Second-order effects (Hypotheses 2 and 3). We pre-dicted that the effect of social trust on commitmentwould be stronger for relational-dominated con-texts (Hypothesis 2a), while the effect of satisfac-tion would be stronger for the contract-dominatedcontext (Hypothesis 2b). As per Hypothesis 2a,Table 6 shows that frontline employee trust hasa significant ‘‘motivator’’ effect on consumer com-mitment in the Netherlands (B¼0.18 and 0.31for linear and quadratic terms respectively) butnot in the German context (B¼0.18 and �0.00respectively). Likewise, firm trust has a strongereffect on commitment in the Netherlands (B¼0.24and 0.14 for linear and quadratic terms respec-tively) than in the German context (B¼0.24 and0.04 for linear and quadratic terms respectively),although the difference is not statistically signi-ficant at p¼0.05. However, the estimated effectsof social trust on commitment do not vary signifi-cantly between the German and US contexts.Overall, Hypothesis 2a is supported for the Dutchdata, but not for the US data.