financing for village electrification mini- grids: bridging · pdf filefinancing for village...

TRANSCRIPT

Financing for village

electrification mini-

grids:

Bridging the gaps to

attract capital

March 19, 2014

Upendra Bhatt

cKinetics

New Delhi Palo Alto

Gist of our conversation…

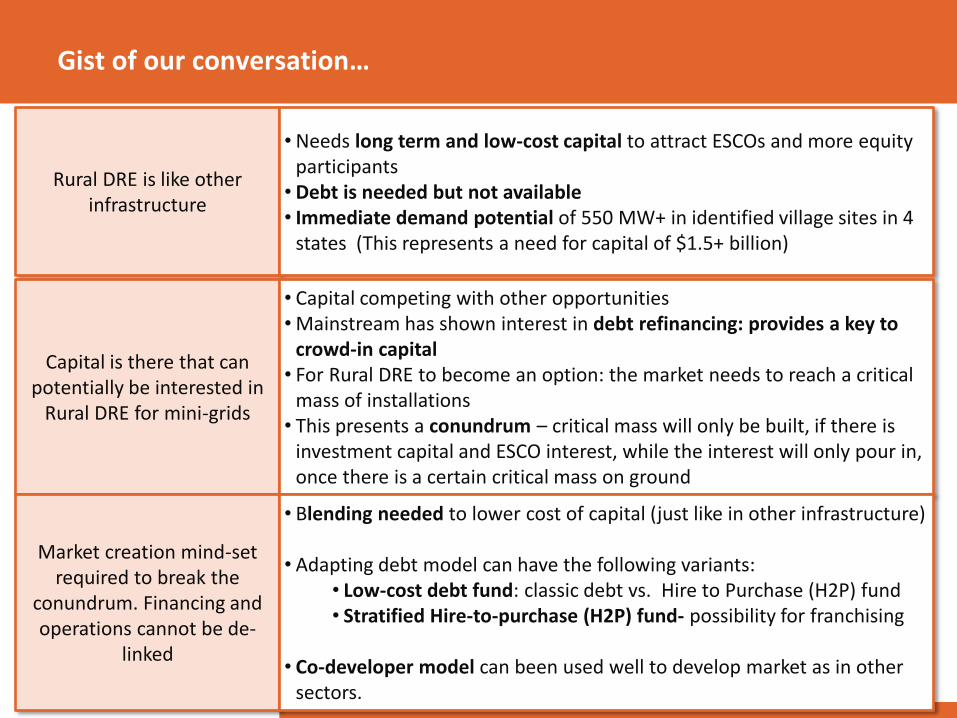

Rural DRE is like other infrastructure

•Needs long term and low-cost capital to attract ESCOs and more equity participants • Debt is needed but not available • Immediate demand potential of 550 MW+ in identified village sites in 4

states (This represents a need for capital of $1.5+ billion)

Capital is there that can potentially be interested in

Rural DRE for mini-grids

• Capital competing with other opportunities •Mainstream has shown interest in debt refinancing: provides a key to

crowd-in capital • For Rural DRE to become an option: the market needs to reach a critical

mass of installations • This presents a conundrum – critical mass will only be built, if there is

investment capital and ESCO interest, while the interest will only pour in, once there is a certain critical mass on ground

Market creation mind-set required to break the

conundrum. Financing and operations cannot be de-

linked

• Blending needed to lower cost of capital (just like in other infrastructure) • Adapting debt model can have the following variants:

• Low-cost debt fund: classic debt vs. Hire to Purchase (H2P) fund • Stratified Hire-to-purchase (H2P) fund- possibility for franchising

• Co-developer model can been used well to develop market as in other

sectors.

• Big picture: view from 30,000 ft

• ESCO overview and implications for Financing – ESCO types and economics

– Risks/gaps with mini-grid projects that make an investment unattractive

– Kind of capital required for Rural DRE: Debt capital

• Making it real: State of the market and how debt capital can be deployed to develop the market

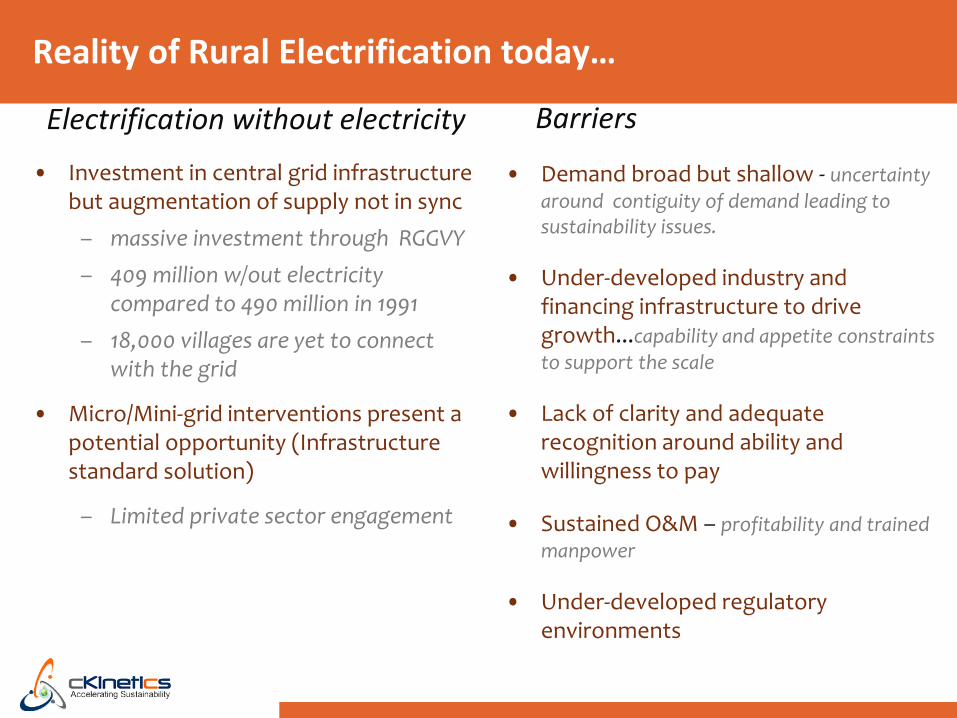

Reality of Rural Electrification today…

• Demand broad but shallow - uncertainty

around contiguity of demand leading to sustainability issues.

• Under-developed industry and financing infrastructure to drive growth...capability and appetite constraints to support the scale

• Lack of clarity and adequate recognition around ability and willingness to pay

• Sustained O&M – profitability and trained manpower

• Under-developed regulatory environments

• Investment in central grid infrastructure but augmentation of supply not in sync

– massive investment through RGGVY

– 409 million w/out electricity compared to 490 million in 1991

– 18,000 villages are yet to connect with the grid

• Micro/Mini-grid interventions present a potential opportunity (Infrastructure standard solution)

– Limited private sector engagement

Barriers Electrification without electricity

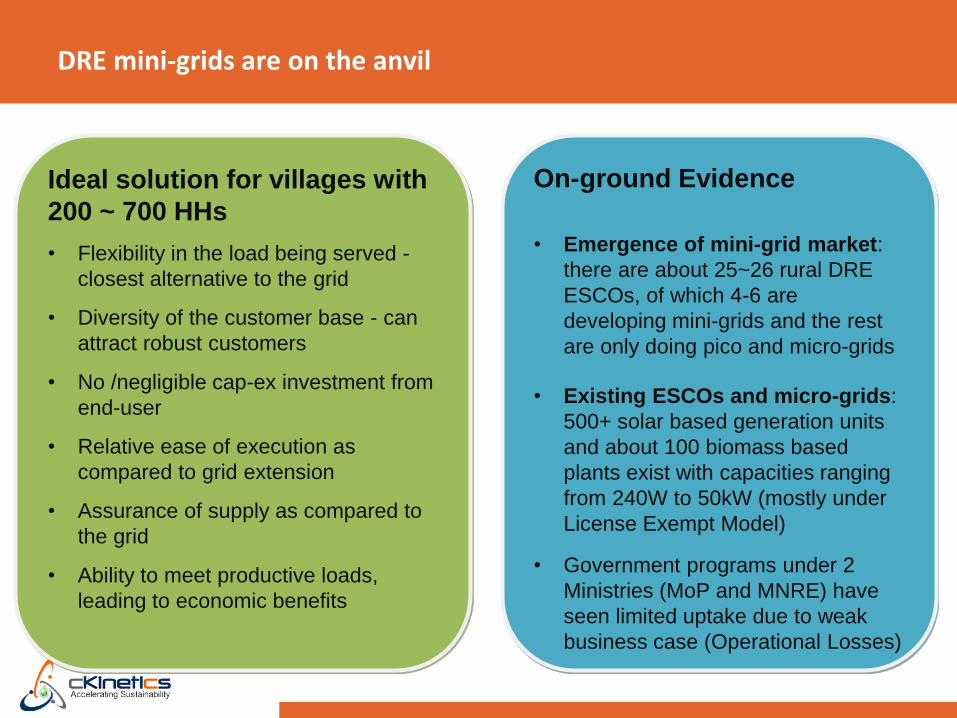

DRE mini-grids are on the anvil

Ideal solution for villages with

200 ~ 700 HHs

• Flexibility in the load being served -

closest alternative to the grid

• Diversity of the customer base - can

attract robust customers

• No /negligible cap-ex investment from

end-user

• Relative ease of execution as

compared to grid extension

• Assurance of supply as compared to

the grid

• Ability to meet productive loads,

leading to economic benefits

On-ground Evidence

• Emergence of mini-grid market:

there are about 25~26 rural DRE

ESCOs, of which 4-6 are

developing mini-grids and the rest

are only doing pico and micro-grids

• Existing ESCOs and micro-grids:

500+ solar based generation units

and about 100 biomass based

plants exist with capacities ranging

from 240W to 50kW (mostly under

License Exempt Model)

• Government programs under 2

Ministries (MoP and MNRE) have

seen limited uptake due to weak

business case (Operational Losses)

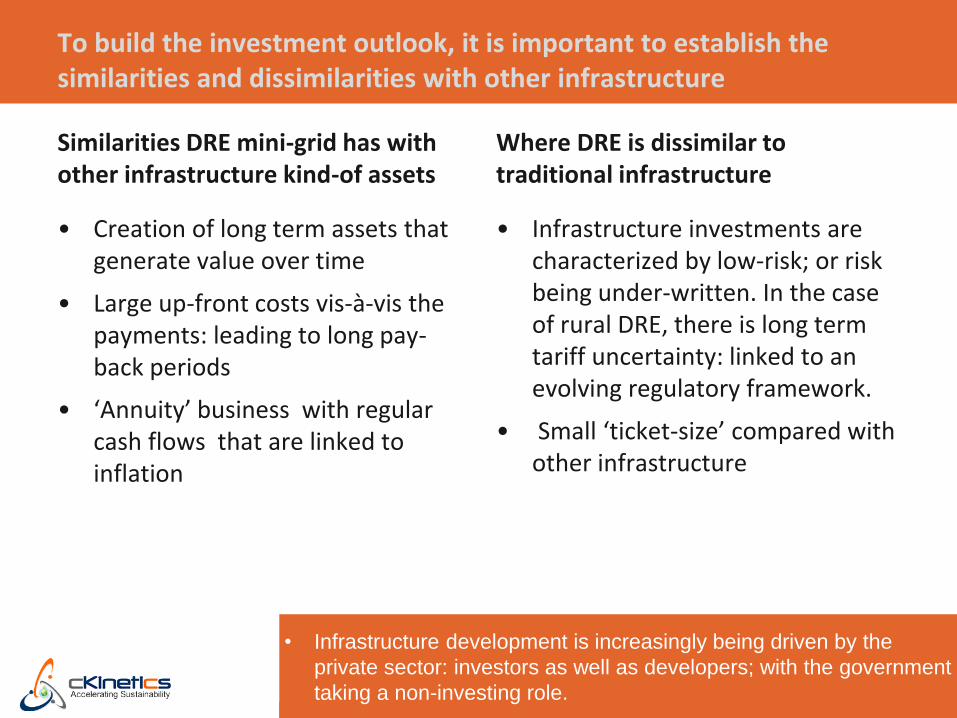

To build the investment outlook, it is important to establish the similarities and dissimilarities with other infrastructure

Similarities DRE mini-grid has with other infrastructure kind-of assets

• Creation of long term assets that generate value over time

• Large up-front costs vis-à-vis the payments: leading to long pay-back periods

• ‘Annuity’ business with regular cash flows that are linked to inflation

Where DRE is dissimilar to traditional infrastructure

• Infrastructure investments are characterized by low-risk; or risk being under-written. In the case of rural DRE, there is long term tariff uncertainty: linked to an evolving regulatory framework.

• Small ‘ticket-size’ compared with other infrastructure

• Infrastructure development is increasingly being driven by the

private sector: investors as well as developers; with the government

taking a non-investing role.

• Big picture: view from 30,000 ft

• ESCO economics and implications for Financing – ESCO types and economics

– Risks/gaps with mini-grid projects that make an investment unattractive

– Kind of capital required for Rural DRE: Debt capital

• Making it real: State of the market and how debt capital can be deployed to develop the market

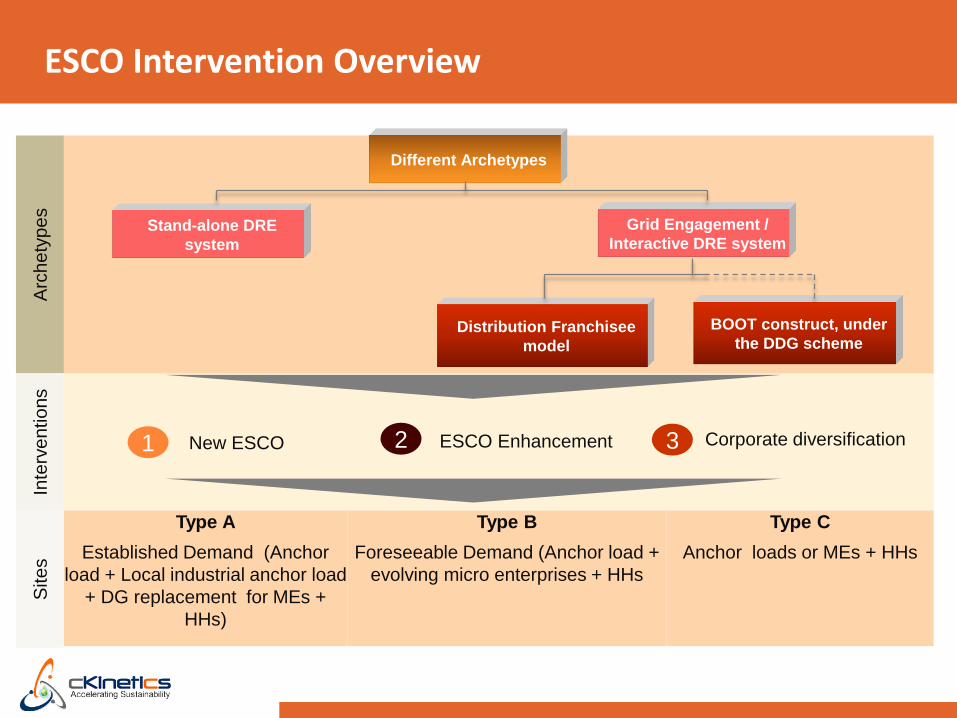

ESCO Intervention Overview

Type A

Established Demand (Anchor

load + Local industrial anchor load

+ DG replacement for MEs +

HHs)

Type B

Foreseeable Demand (Anchor load +

evolving micro enterprises + HHs

Type C

Anchor loads or MEs + HHs

Different Archetypes

Stand-alone DRE

system

Grid Engagement /

Interactive DRE system

Distribution Franchisee

model

BOOT construct, under

the DDG scheme

New ESCO ESCO Enhancement Corporate diversification 1 2 3

Arc

he

typ

es

Inte

rve

ntio

ns

Site

s

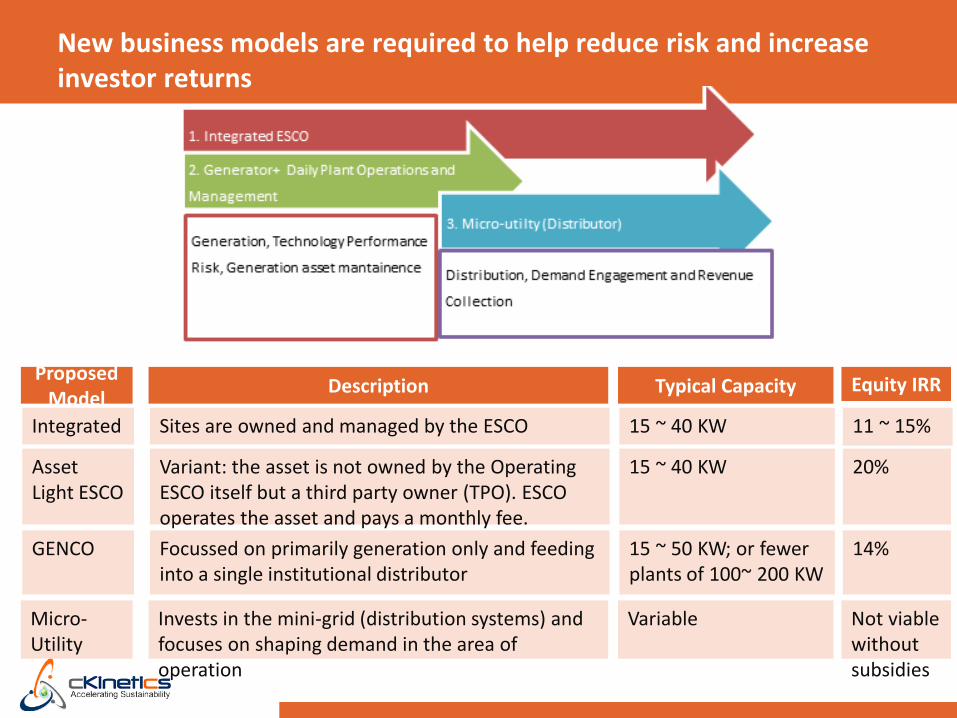

New business models are required to help reduce risk and increase investor returns

FIGURE ERROR! NO TEXT OF SPECIFIED STYLE IN DOCUMENT.-1: DRE MINI-GRIDS CAN BE OPERATED IN THREE MODELS

Proposed Model

Description Typical Capacity Equity IRR

Micro-Utility

Invests in the mini-grid (distribution systems) and focuses on shaping demand in the area of operation

Variable Not viable without subsidies

Integrated Sites are owned and managed by the ESCO 15 ~ 40 KW 11 ~ 15%

Asset Light ESCO

Variant: the asset is not owned by the Operating ESCO itself but a third party owner (TPO). ESCO operates the asset and pays a monthly fee.

15 ~ 40 KW 20%

GENCO Focussed on primarily generation only and feeding into a single institutional distributor

15 ~ 50 KW; or fewer plants of 100~ 200 KW

14%

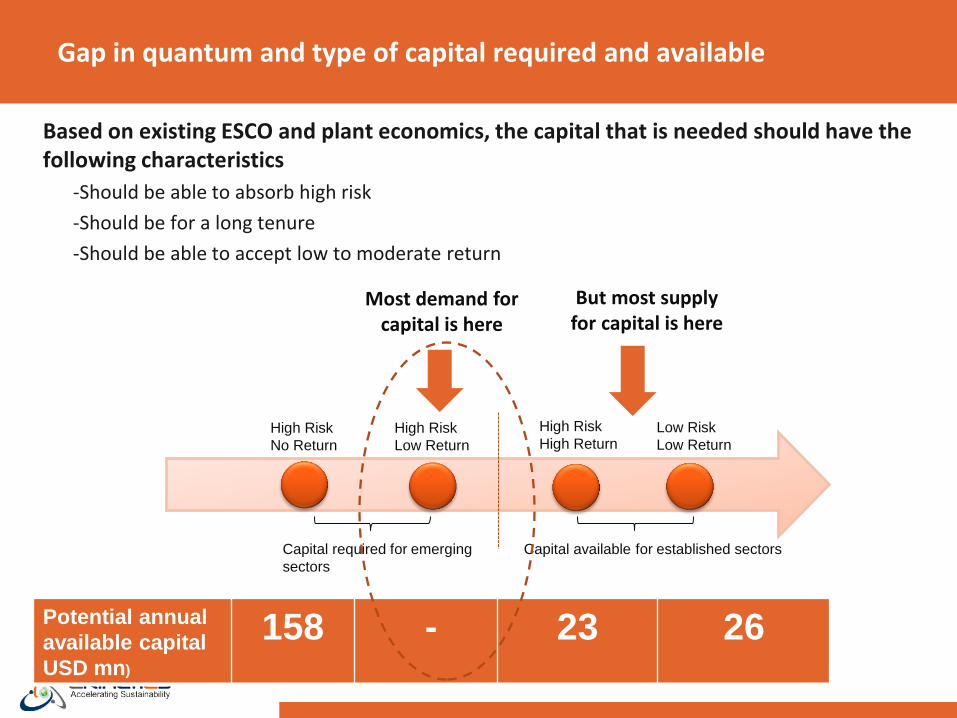

Gap in quantum and type of capital required and available

High Risk

No Return

High Risk

Low Return

Low Risk

Low Return

High Risk

High Return

Capital required for emerging

sectors

Capital available for established sectors

Potential annual

available capital

USD mn)

158 - 23 26

Most demand for capital is here

But most supply for capital is here

Based on existing ESCO and plant economics, the capital that is needed should have the following characteristics

-Should be able to absorb high risk

-Should be for a long tenure

-Should be able to accept low to moderate return

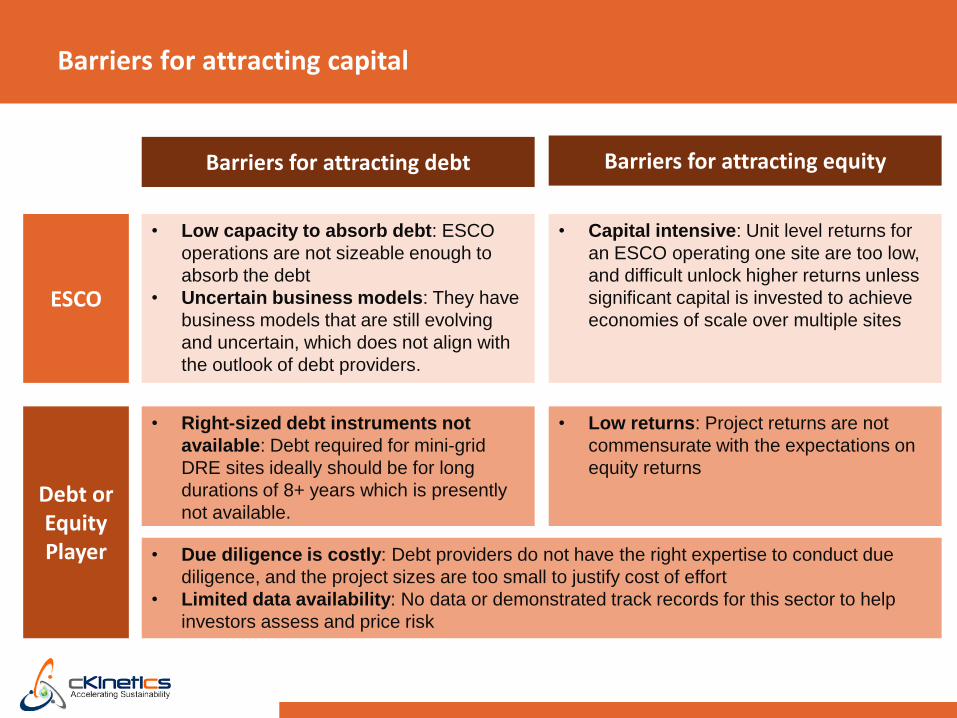

Barriers for attracting capital

Barriers for attracting debt Barriers for attracting equity

• Capital intensive: Unit level returns for

an ESCO operating one site are too low,

and difficult unlock higher returns unless

significant capital is invested to achieve

economies of scale over multiple sites

• Right-sized debt instruments not

available: Debt required for mini-grid

DRE sites ideally should be for long

durations of 8+ years which is presently

not available.

• Low returns: Project returns are not

commensurate with the expectations on

equity returns

Debt or Equity Player

ESCO

• Low capacity to absorb debt: ESCO

operations are not sizeable enough to

absorb the debt

• Uncertain business models: They have

business models that are still evolving

and uncertain, which does not align with

the outlook of debt providers.

• Due diligence is costly: Debt providers do not have the right expertise to conduct due

diligence, and the project sizes are too small to justify cost of effort

• Limited data availability: No data or demonstrated track records for this sector to help

investors assess and price risk

• Big picture: view from 30,000 ft

• ESCO overview and implications for Financing – ESCO types and economics

– Risks/gaps with mini-grid projects that make an investment unattractive

– Kind of capital required for Rural DRE: Debt capital

• Making it real: State of the market and how debt capital can be deployed to develop the market

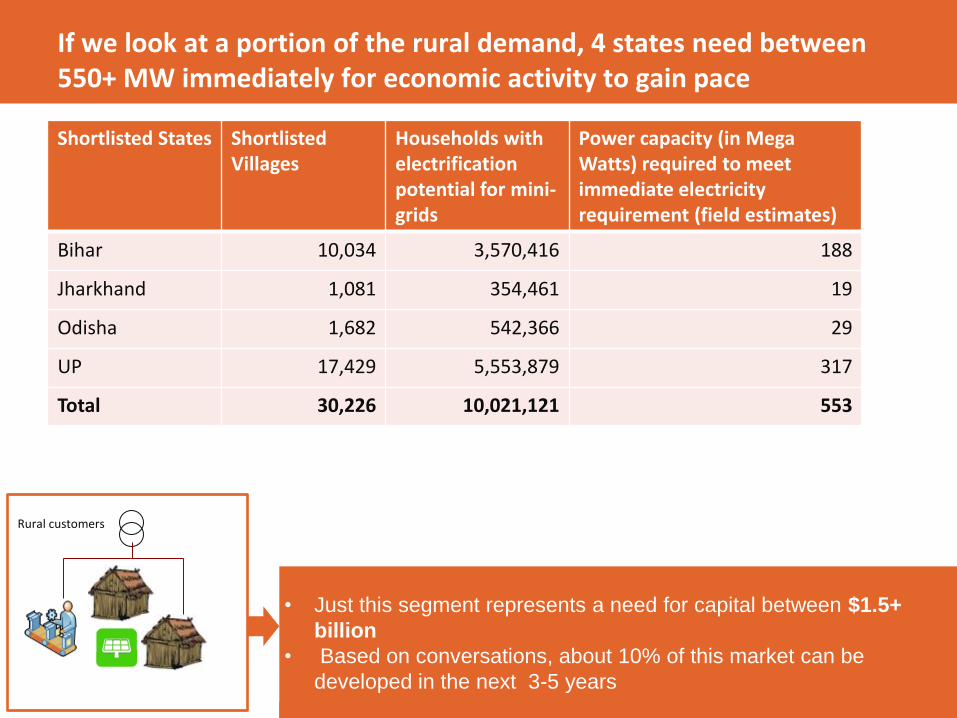

If we look at a portion of the rural demand, 4 states need between 550+ MW immediately for economic activity to gain pace

• Just this segment represents a need for capital between $1.5+

billion

• Based on conversations, about 10% of this market can be

developed in the next 3-5 years

Rural customers

Shortlisted States Shortlisted Villages

Households with electrification potential for mini-grids

Power capacity (in Mega Watts) required to meet immediate electricity requirement (field estimates)

Bihar 10,034 3,570,416 188

Jharkhand 1,081 354,461 19

Odisha 1,682 542,366 29

UP 17,429 5,553,879 317

Total 30,226 10,021,121 553

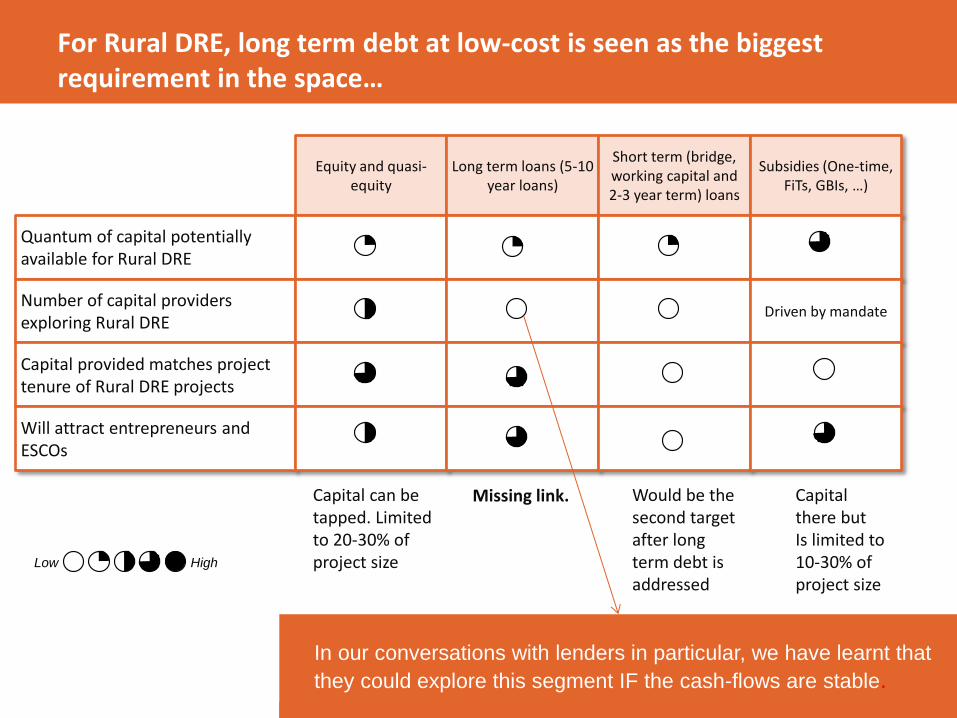

For Rural DRE, long term debt at low-cost is seen as the biggest requirement in the space…

Equity and quasi-equity

Long term loans (5-10 year loans)

Short term (bridge, working capital and 2-3 year term) loans

Subsidies (One-time, FiTs, GBIs, …)

Low High

Quantum of capital potentially available for Rural DRE

Number of capital providers exploring Rural DRE

Driven by mandate

Capital provided matches project tenure of Rural DRE projects

Will attract entrepreneurs and ESCOs

Capital can be tapped. Limited to 20-30% of project size

Missing link. Would be the second target after long term debt is addressed

Capital there but Is limited to 10-30% of project size

In our conversations with lenders in particular, we have learnt that

they could explore this segment IF the cash-flows are stable.

• Big picture: view from 30,000 ft

• ESCO economics and implications for Financing – ESCO economics

– Risks/gaps with mini-grid projects that make an investment unattractive

– Kind of capital required for Rural DRE: Debt capital

• Making it real: State of the market and how debt capital can be deployed to develop the market

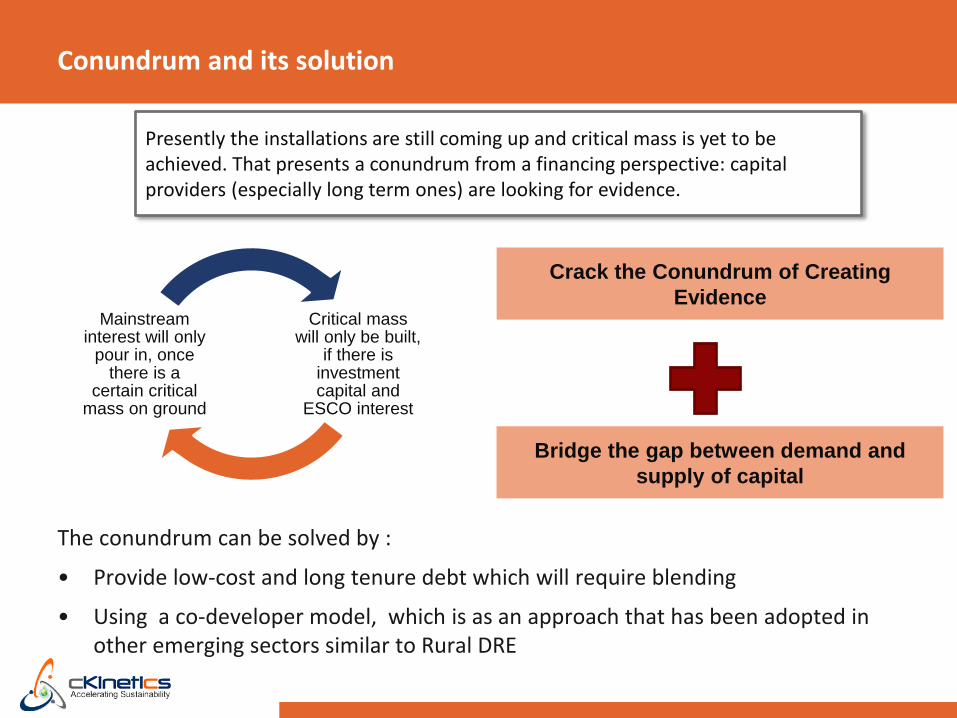

Conundrum and its solution

The conundrum can be solved by :

• Provide low-cost and long tenure debt which will require blending

• Using a co-developer model, which is as an approach that has been adopted in other emerging sectors similar to Rural DRE

Critical mass will only be built,

if there is investment capital and

ESCO interest

Mainstream interest will only

pour in, once there is a

certain critical mass on ground

Presently the installations are still coming up and critical mass is yet to be achieved. That presents a conundrum from a financing perspective: capital providers (especially long term ones) are looking for evidence.

Crack the Conundrum of Creating

Evidence

Bridge the gap between demand and

supply of capital

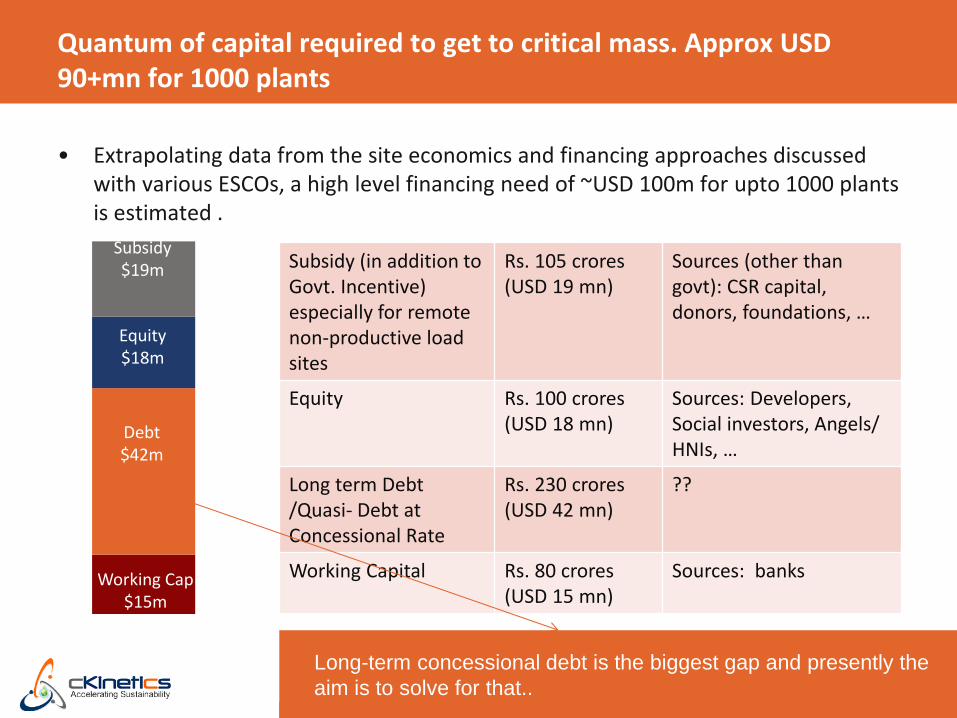

Quantum of capital required to get to critical mass. Approx USD 90+mn for 1000 plants

• Extrapolating data from the site economics and financing approaches discussed with various ESCOs, a high level financing need of ~USD 100m for upto 1000 plants is estimated .

Subsidy (in addition to Govt. Incentive) especially for remote non-productive load sites

Rs. 105 crores (USD 19 mn)

Sources (other than govt): CSR capital, donors, foundations, …

Equity Rs. 100 crores (USD 18 mn)

Sources: Developers, Social investors, Angels/ HNIs, …

Long term Debt /Quasi- Debt at Concessional Rate

Rs. 230 crores (USD 42 mn)

??

Working Capital Rs. 80 crores (USD 15 mn)

Sources: banks

Long-term concessional debt is the biggest gap and presently the

aim is to solve for that..

Subsidy $19m

Equity $18m

Debt $42m

Working Cap $15m

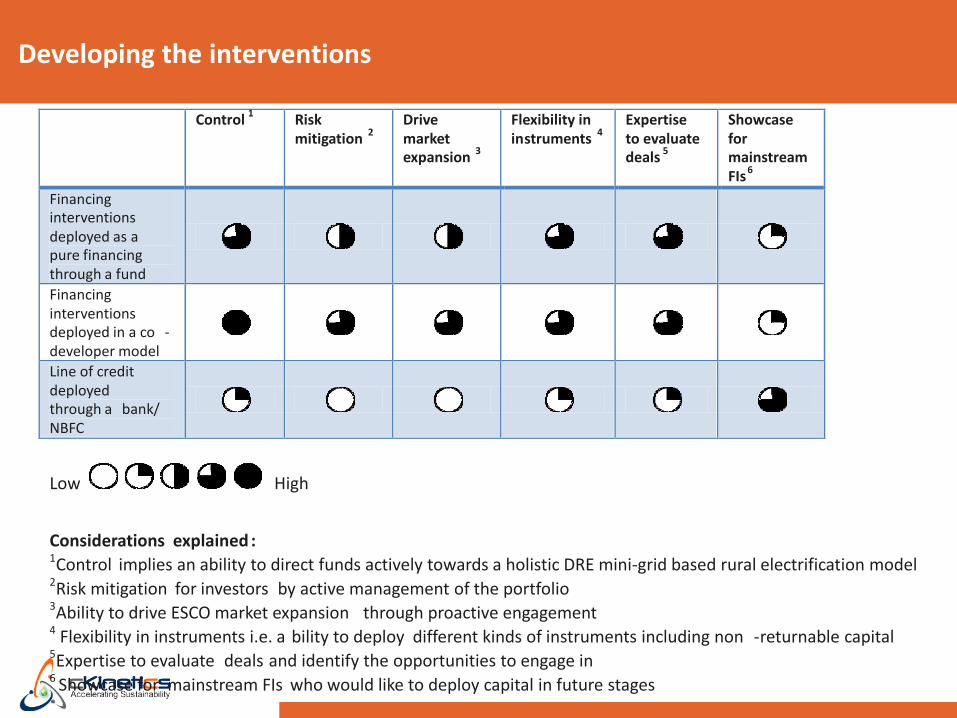

Developing the interventions

Control 1 Risk

mitigation 2

Drive market expansion

3

Flexibility in in struments

4

Expertise to evaluate deals

5

Showcase for mainstream FIs

6

Financing interventions deployed as a pure financing through a fund

Financing interventions deployed in a co - developer model

Line of credit deployed through a bank/ NBFC

Low High

Considerations explained : 1 Control implies an ability to direct funds actively towards a holistic DRE mini-grid based rural electrification model 2 Risk mitigation for investors by active management of the portfolio 3 Ability to drive ESCO market expansion through proactive engagement 4 Flexibility in instruments i.e. a bility to deploy different kinds of instruments including non - returnable capital 5 Expertise to evaluate deals and identify the opportunities to engage in 6 Showcase for mainstream FIs who would like to deploy capital in future stages

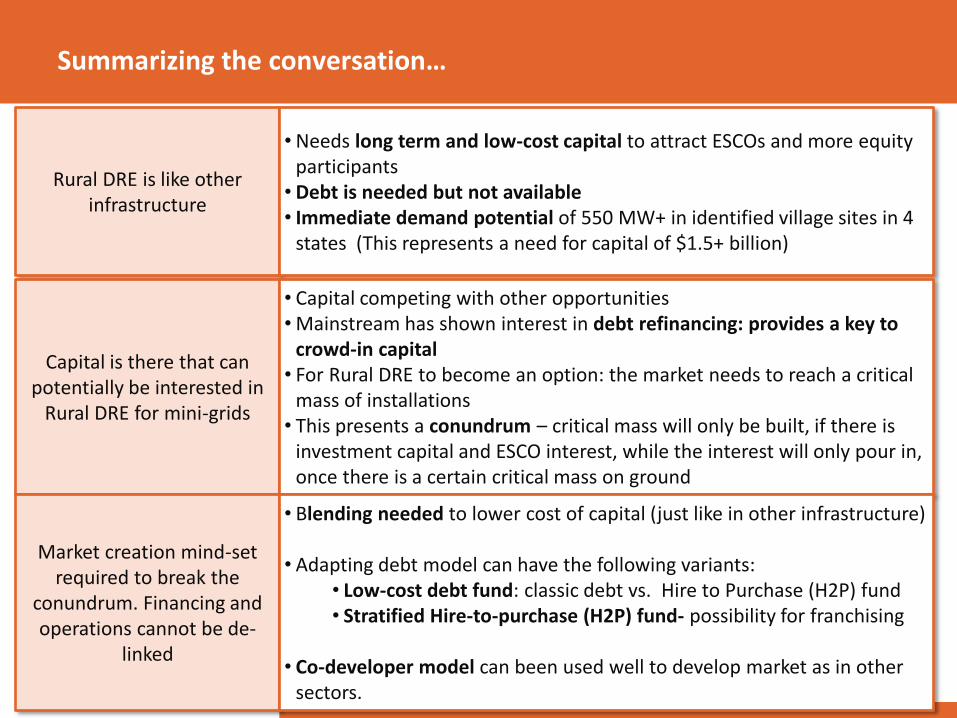

Summarizing the conversation…

Rural DRE is like other infrastructure

•Needs long term and low-cost capital to attract ESCOs and more equity participants • Debt is needed but not available • Immediate demand potential of 550 MW+ in identified village sites in 4

states (This represents a need for capital of $1.5+ billion)

Capital is there that can potentially be interested in

Rural DRE for mini-grids

• Capital competing with other opportunities •Mainstream has shown interest in debt refinancing: provides a key to

crowd-in capital • For Rural DRE to become an option: the market needs to reach a critical

mass of installations • This presents a conundrum – critical mass will only be built, if there is

investment capital and ESCO interest, while the interest will only pour in, once there is a certain critical mass on ground

Market creation mind-set required to break the

conundrum. Financing and operations cannot be de-

linked

• Blending needed to lower cost of capital (just like in other infrastructure) • Adapting debt model can have the following variants:

• Low-cost debt fund: classic debt vs. Hire to Purchase (H2P) fund • Stratified Hire-to-purchase (H2P) fund- possibility for franchising

• Co-developer model can been used well to develop market as in other

sectors.

708 Hemkunt Chambers

89 Nehru Place

New Delhi 110019

INDIA

+91.11.40507277

262 Ventura Ave

Palo Alto

California 94306

USA

+1.650.331.1931

www.cKinetics.com; [email protected]

For Queries and Engagement collaboration, contact us at: