financing education beyond high school

DESCRIPTION

Financing Education Beyond High School. University of Puget Sound November 1, 2012. Financing Your Education . How to apply How eligibility is determined What aid is available. Financial Aid Application Process. Free Application for Federal Student Aid (FAFSA) - PowerPoint PPT PresentationTRANSCRIPT

National Association of Student Financial Aid Administrators Presents…

© NASFAA 2003

Financing Education Beyond

High SchoolUniversity of Puget Sound

November 1, 2012

Slide 2 © NASFAA 2003

Financing Your Education

• How to apply

• How eligibility is determined

• What aid is available

Slide 3 © NASFAA 2003

Financial Aid Application Process

• Free Application for Federal Student Aid (FAFSA)

• Check each school’s financial aid website for applications required:– FAFSA, CSS Profile, Institutional

Application• Application deadlines

Slide 4 © NASFAA 2003

FAFSA on the Web

• Web site: www.fafsa.gov • 2013-14 FAFSA available on January 1, 2013• Tip: Do not go to www.fafsa.com! • The FAFSA is FREE• Apply for FAFSA PINS: Student AND Parent• IRS DATA RETRIEVAL

Slide 5 © NASFAA 2003

To Register for a PIN: www.pin.ed.gov

Slide 6 © NASFAA 2003

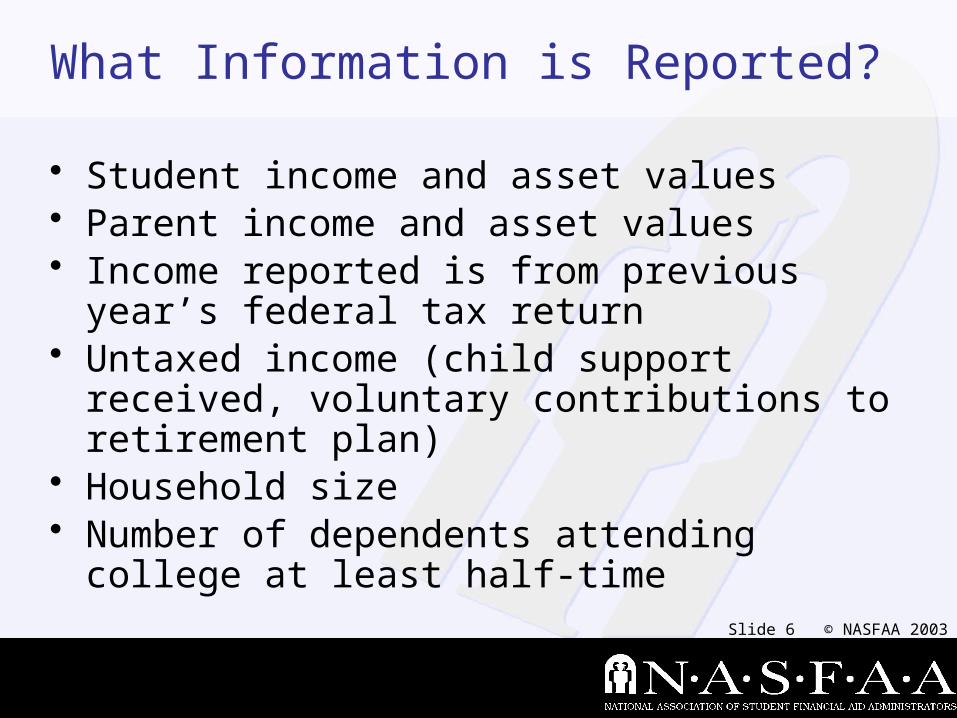

What Information is Reported?

• Student income and asset values• Parent income and asset values• Income reported is from previous year’s federal

tax return• Untaxed income (child support received, voluntary

contributions to retirement plan)• Household size• Number of dependents attending college at least

half-time

Slide 7 © NASFAA 2003

Reporting Income

• Income based on federal tax return• For 2013-14 school year, use 2012 tax

return• Okay to estimate until you have filed your

return• Wages (from W-2), AGI, Taxes Paid,

Business Income, Capitol Gains• Untaxed Income

Slide 8 © NASFAA 2003

Reporting Assets

• Cash, Savings and Checking acct. balances as of date FAFSA signed

• Net Investment and Real Estate values, including college savings, trust funds, vacation properties, etc.

• Do not include primary residence or funds held in retirement accounts (IRA, 401K, etc)

• Investment farm value• Net Business value only if over 100 employees

Slide 9 © NASFAA 2003

Corrections

If a correction to applicant data is needed, the correction may be made:

• www.fafsa.gov if student has a PIN; or• By the school

• IRS Data Retrieval-when taxes are completed

Slide 10 © NASFAA 2003

How Will My School(s) Receive my FAFSA?

• Can list up to 10 schools on FAFSA on web

• FAFSA data will be electronically transmitted to all schools listed

• Each School is required to review the data for all admitted students, and to calculate eligibility for federal student aid

Slide 11 © NASFAA 2003

Expected Family Contribution

EFC = Expected Family Contribution

• Calculated using a formula established by Congress

• Results in a dollar value between $0 and $99,999

• Not a prediction of how much cash you actually have on hand. Rather, it's the best estimate of your capacity (over time) to absorb the costs of education.

Slide 12 © NASFAA 2003

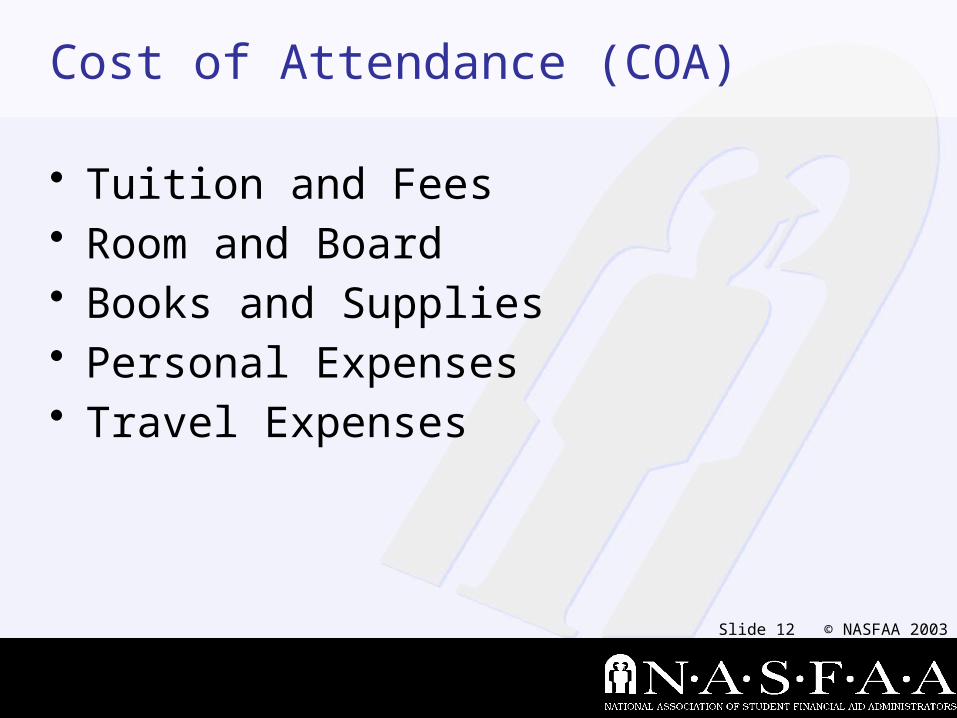

Cost of Attendance (COA)

• Tuition and Fees• Room and Board• Books and Supplies• Personal Expenses• Travel Expenses

Slide 13 © NASFAA 2003

Definition of Need

Cost of Attendance (COA)

– Expected Family Contribution (EFC)

= Financial Need

Slide 14 © NASFAA 2003

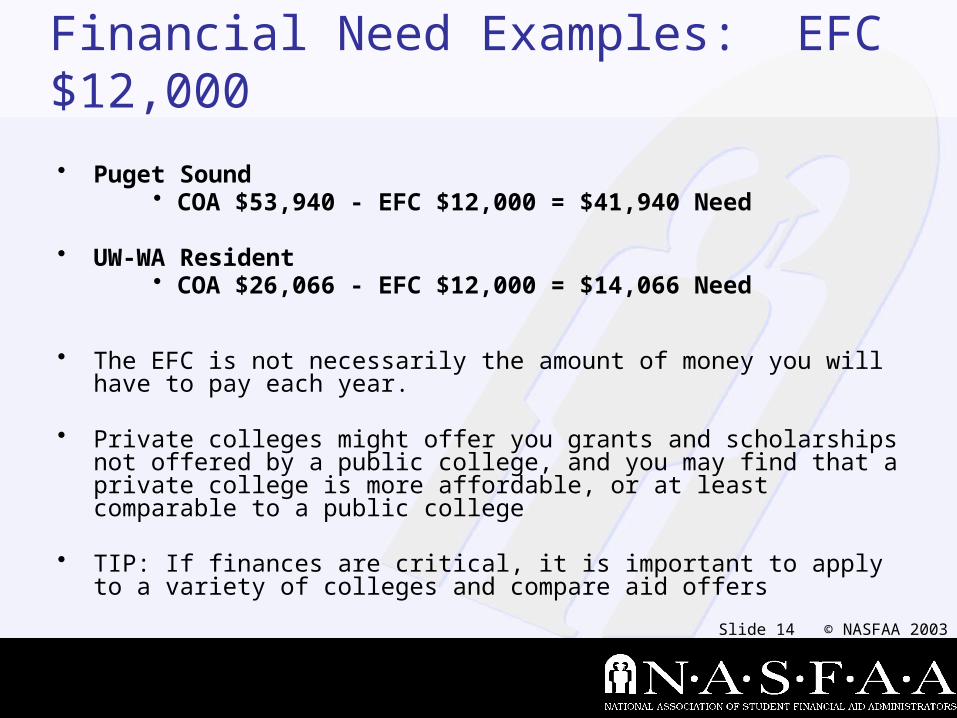

Financial Need Examples: EFC $12,000

• Puget Sound • COA $53,940 - EFC $12,000 = $41,940 Need

• UW-WA Resident• COA $26,066 - EFC $12,000 = $14,066 Need

• The EFC is not necessarily the amount of money you will have to pay each year.

• Private colleges might offer you grants and scholarships not offered by a public college, and you may find that a private college is more affordable, or at least comparable to a public college

• TIP: If finances are critical, it is important to apply to a variety of colleges and compare aid offers

Slide 15 © NASFAA 2003

What Types of Financial Aid ?

• Grants

• Scholarships

• Loans

• Work-Study

Slide 16 © NASFAA 2003

Sources of Aid

• Federal, State, Institutional, Private

• Private universities have their own institutional scholarships and grants funded through their endowments

• Public universities may or may not offer institutional scholarships and grants

Slide 17 © NASFAA 2003

Federal Aid

• Pell Grant • SEOG (Supplemental Educational Opportunity Grant)• Federal Work-Study• Perkins Loan for students• Stafford Loan for students • Plus Loan for parents

Detailed descriptions in The Student Guidehttp://studentaid.ed.gov

Slide 18 © NASFAA 2003

State Financial Aid

• Washington State Need Grant: for low income families

• State Work Study

Slide 19 © NASFAA 2003

Stafford Loans (Subsidized and Unsubsidized)• Subsidized Stafford: Must demonstrate “need”

(3.4% 2012-13 fixed interest rate)• Unsubsidized Stafford: Need is not a

consideration (6.8% 2012-13 fixed interest rate)• Base annual loan limits (combined subsidized

and unsubsidized)– $5,500 for 1st year undergraduates– $6,500 for 2nd year undergraduates– $7,500 for each remaining undergraduate year

Slide 20 © NASFAA 2003

Work-Study

• Undergraduate students are eligible• Employment may be on or off campus• Hours average 10-12 hours/week• Great way to cover personal expenses

and develop valuable job skills

Slide 21 © NASFAA 2003

Scholarships

• Institutional scholarships and grants vary by college and are typically funded through donor and alumni support

• Merit scholarships based on review of academic profile to include H.S. GPA, Rigor of coursework completed, and SAT/ACT scores

• The more time you invest in scholarship searches the more likely you will receive something. No time/effort = no money. Make the effort!

Slide 22 © NASFAA 2003

Private Scholarships

• Private Scholarships are available from a wide variety of sources, including employers, clubs, community organizations, credit unions and even your own high school. (i.e. Elks, Rotary, Kiwanis)

• MIGHT result in decreased aid from other areas, especially if you are admitted to college that “meets full need”.

• Don’t ever pay for a scholarship search!!

Slide 23 © NASFAA 2003

Private Scholarship Search• Free Internet scholarship search engines:

– GoCollege.com: The Collegiate Websource – http://www.gocollege.com

– Fast Web www.fastweb.com– College Board Scholarship Search

http://apps.collegeboard.com/cbsearch_ss/welcome.jsp

– TIP: open a separate yahoo account for scholarship search email. Online searches generate a lot of mail.

Slide 24 © NASFAA 2003

Other Options

• Parent PLUS Loan – (7.9% fixed interest rate)

• Monthly Payment Plan– Balance is divided into 10 monthly payments. – Fee.

• Consider a combination of the PLUS parent loan and a payment plan

Slide 25 © NASFAA 2003

Special Circumstances

Let your college know if you experience:

• Loss of employment, or reduction in income

• Unusually high out-of-pocket medical expenses, not including insurance premiums

• Tuition for siblings attending private K-12

Slide 26 © NASFAA 2003

TIPS

• Apply to at least 5 colleges if finances are very important. Aid packages will vary.

• Compare costs to aid package to determine net amount you will pay. Use that number when comparing aid offers. Private college might turn out to be comparable to public college.

• Examine total loan debt you will have to repay once you graduate!

Slide 27 © NASFAA 2003

NET PRICE CALCULATOR

• All schools must provide a Net Price Calculator

• Net Price Calculator is an estimate, based on specific questions, of what a student’s aid package could be at that particular school.

• www.pugetsound.edu/sfs

Slide 28 © NASFAA 2003

Good Luck!