financials: how to present your data to attract outside investors [email protected] july...

TRANSCRIPT

F i n a n c i a l s : H o w t o P r e s e n t Yo u r

D a t a t o A t t r a c t O u t s i d e I n v e s t o r s

July 24, 2014

2

W h a t i s A c c o u n t i n g ?

“The language of business”

Accounting communicates financialinformation to users for decision-making.

Users of financial information include:shareholders, debtors, creditors, and investors.

3

W h a t i s A c c o u n t i n g ?

Accurate financial information provides:

Information on your historical results(where you have been)

Your current financial position(where you are today), and

Insight into your future plans (where you plan to go)

4

W h y A c c u r a t e a n d C o m p l e t e B o o k s a n d R e c o r d s a r e I m p o r t a n t

1. Credibility when dealing with investors, vendors and lendersWhen confidence in the numbers and underlying

assumptions is lost, questions are raised and opportunities may be delayed or lost

2. Vital tool in running your businessCash managementTracking sales and expenses

3. Ability to respond to inquiries by regulators on a timely basis

IRS

4. When opportunities arise, you need to be readyPotential investorsSale of the company

5

C o m m o n F i n a n c i a l M i s t a k e s T h a t S t a r t u p s M a k e

• Not doing anything – until it’s too late i.e. not maintaining any accounting books and records

• Not seeking professional advice – accounting and tax

• Not using accounting software or maintaining accounting records in a spreadsheet database i.e. excel.

• Not separating the Company accounts from personal accounts i.e. having a separate bank accounts

• Lack of proper backup (offsite or cloud preferred)

6

C o m m o n F i n a n c i a l M i s t a k e s T h a t S t a r t u p s M a k e

• Not understanding the difference between cash and accrual basis accounting

• Not understanding their revenue model and the assumptions underlying financial projections.

• Not keeping accurate and complete supporting records i.e. invoices, contracts, notices, etc.

• Not maintaining an accurate capitalization table

7

Ta x M i s t a k e s T h a t S t a r t u p s M a k e

• Sloppy record-keeping

• Employees vs. independent contractors – a hot button with the IRS

• Creating deductions you can’t use or lack of support for deductions taken

• Making short-sighted decisions when deciding the type of legal entity to form, i.e. C- corp, S-corp, LLC

8

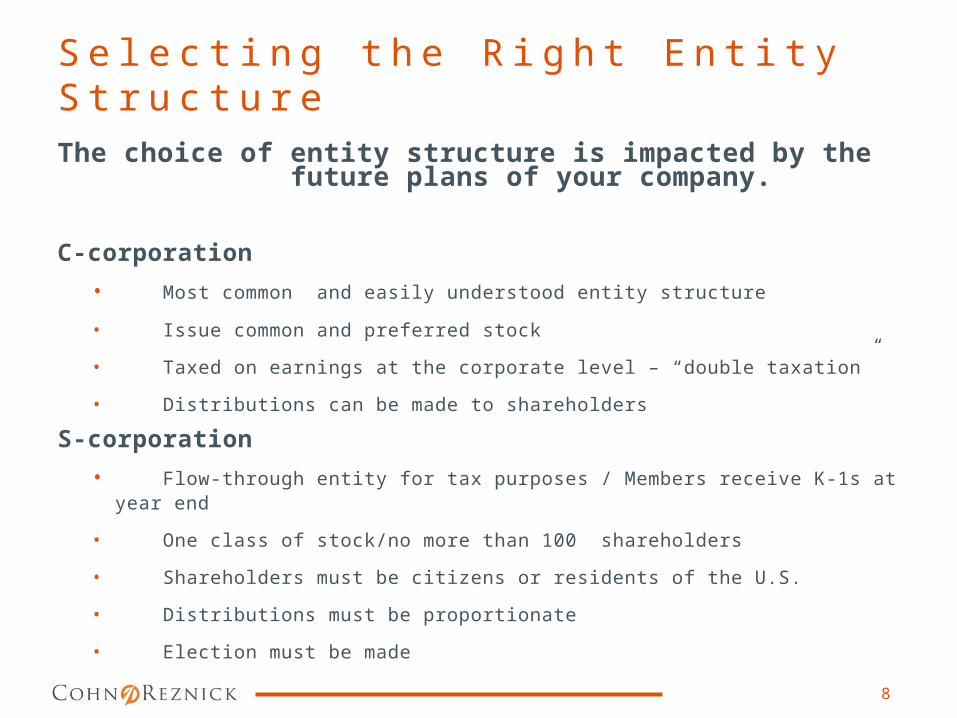

S e l e c t i n g t h e R i g h t E n t i t y S t r u c t u r eThe choice of entity structure is impacted by the future plans of your company.

C-corporation

• Most common and easily understood entity structure

• Issue common and preferred stock

• Taxed on earnings at the corporate level – “double taxation”

• Distributions can be made to shareholders

S-corporation

• Flow-through entity for tax purposes / Members receive K-1s at year end

• One class of stock/no more than 100 shareholders

• Shareholders must be citizens or residents of the U.S.

• Distributions must be proportionate

• Election must be made

9

S e l e c t i n g t h e R i g h t E n t i t y S t r u c t u r e

Limited Liability Company• Flow-through entity for tax purposes/Members receive K-1s at year

end

• Flexibility based on Operating Agreement

• Can be taxed as partnership or corporation based on election of members

• Single member LLC is disregarded for tax purposes

• Distributions do not need to follow ownership

• Members cannot be employees. Guaranteed payments instead of W-2 wages

• Certain jurisdictions may not recognize the LLC as a flow-through entity

10

G u i d e t o F i n a n c i a l S t a t e m e n t s

There are four main financial statements.

Balance sheets - show what a company owns and what it owes at a fixed point in time.

Income statements - show how much money a company made and spent over a period of time.

Cash flow statements - show the exchange of money between a company and the outside world also over a period of time.

Statements of shareholders’ equity - shows changes in the interests of the company’s shareholders over time.

11

G u i d e t o F i n a n c i a l S t a t e m e n t s

Balance Sheet

Assets −Anything tangible or intangible that is capable of

being owned or controlled to produce value.Liabilities

−An obligation of an entity arising from past transactions or events,

Shareholders’ Equity −Sometimes called capital or net worth. −Represents the money that would

be left if a company sold all of its assets and paid off all of its liabilities.

12

G u i d e t o F i n a n c i a l S t a t e m e n t s

December 31

2013 2012

ASSETS

Current assets:Cash and cash equivalents 3,161,602$ 405,848$ Accounts receivable - trade 38,187 291,974 Prepaid expenses 163,060 119,109 Related party receivable 13,945 5,329 Other current assets 81,236 302,676

Total current assets 3,458,030 1,124,936

Property and equipment, net 2,364,328 2,428,779 Deposits 43,868 29,543

Total assets 5,866,226$ 3,583,258$

13

G u i d e t o F i n a n c i a l S t a t e m e n t s

.

December 312013 2012

Liabilities and Stockholders' Deficit

Current liabilities:Accounts payable 155,449$ 558,676$ Accrued expenses and other current liabilities 578,777 929,396 Deferred revenue 5,088,522 1,418,685 Revolving line of credit - 1,936,927 Accrued income taxes 179,714 93,622

Total current liabilities 6,002,462 4,937,306

Noncurrent liabilities:Other long-term liabilities 1,391,668 1,335,743

Total liabilities 7,394,130 6,273,049

Commitments and contingencies - -

Stockholders' deficit:Common stock - $0.01 par value, 50,000 shares authorized,

15,888 shares issued and outstandingat December 31, 2013 and 2012, respectively 159 159

Additional paid-in capital 3,573,876 3,481,659 Accumulated deficit (5,101,939) (6,171,609)

Total stockholders' deficit (1,527,904) (2,689,791)

Total liabilities and stockholders' deficit 5,866,226$ 3,583,258$

14

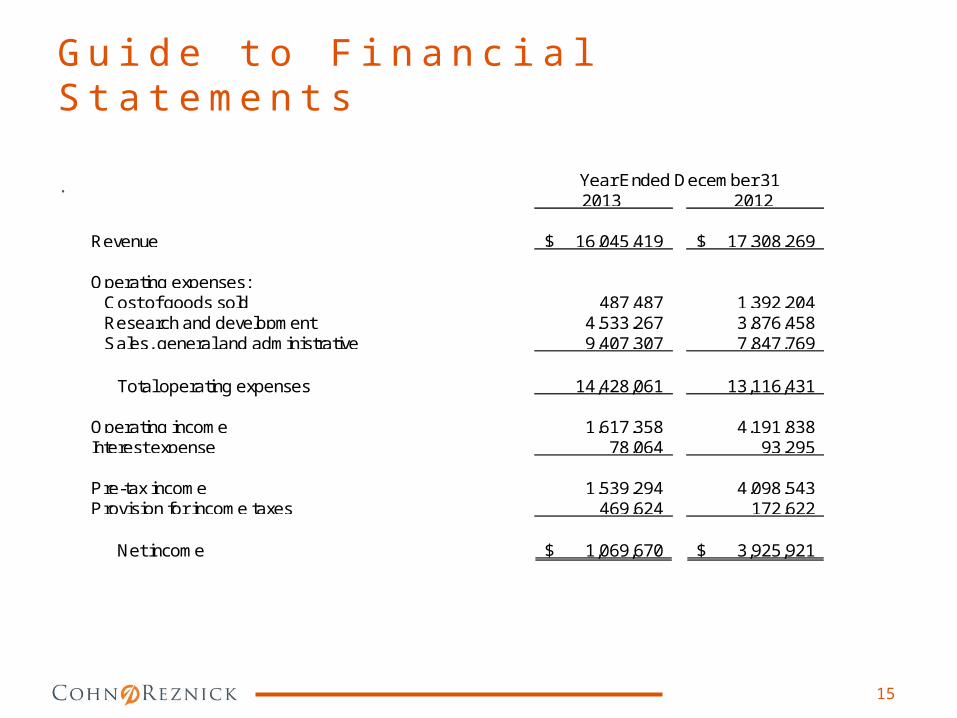

G u i d e t o F i n a n c i a l S t a t e m e n t s

Income Statement

Shows how much revenue a company earned over a specific time period (usually for a year or some portion of a year).

Shows the costs and expenses incurred.

The literal “bottom line” of the statement usually shows the company’s net earnings or losses. This tells you how much the company earned or lost over the period.

15

G u i d e t o F i n a n c i a l S t a t e m e n t s

. Year Ended December 312013 2012

Revenue 16,045,419$ 17,308,269$

Operating expenses:Cost of goods sold 487,487 1,392,204 Research and development 4,533,267 3,876,458 Sales, general and administrative 9,407,307 7,847,769

Total operating expenses 14,428,061 13,116,431

Operating income 1,617,358 4,191,838 Interest expense 78,064 93,295

Pre-tax income 1,539,294 4,098,543 Provision for income taxes 469,624 172,622

Net income 1,069,670$ 3,925,921$

16

G u i d e t o F i n a n c i a l S t a t e m e n t s

Cash Flow Statements

Reports a company’s inflows and outflows of cash.

Important because a company needs to have enough cash on hand to pay its expenses and purchase assets.

A cash flow statement can tell you whether the company generated cash.

17

G u i d e t o F i n a n c i a l S t a t e m e n t s

.

Year Ended December 312013 2012

Cash flows from operating activitiesNet income 1,069,670$ 3,925,921$ Adjustments to reconcile net income to net cashprovided by (used) in operating activities:

Depreciation and amortization 539,350 357,959 Loss of disposal of fixed assets - 66,494 Stock-based compensation 83,594 98,134 Stock warrants issued for services 8,623 2,024 Decrease (increase) in assets:

Accounts receivable - trade 253,787 173,385 Prepaid expenses (43,951) (119,109) Related party receivable (8,616) 1,979 Deposits (14,325) (20,564) Other current assets 221,440 (320,834)

Increase (decrease) in liabilities:Accounts payable (403,227) 412,145 Accrued expenses and other current liabilities (350,619) 483,279 Accrued income taxes 86,092 160,667 Deferred revenue 3,912,485 (9,739,541)

Net cash provided by (used in) operating activities 5,354,303 (4,518,061)

Cash flows from investing activitiesPurchases of property and equipment (474,899) (1,090,988)

Net cash used in investing activities (474,899) (1,090,988)

Cash flows from financing activitiesRepayments of promissory notes payable to related parties (2,200,000) (1,950,000) Proceeds from exercise of stock warrants and options - 24,104 Proceeds from issuance of promissory notes payable 700,000 3,450,000 Proceeds from revolving line of credit, net (623,650) 623,650 Dividends paid - (14,000)

Net cash (used in) provided by financing activities (2,123,650) 2,133,754

Net increase (decrease) in cash and cash equivalents 2,755,754 (3,475,295)

Cash and cash equivalents, beginning of year 405,848 3,881,143

Cash and cash equivalents, end of year 3,161,602$ 405,848$

18

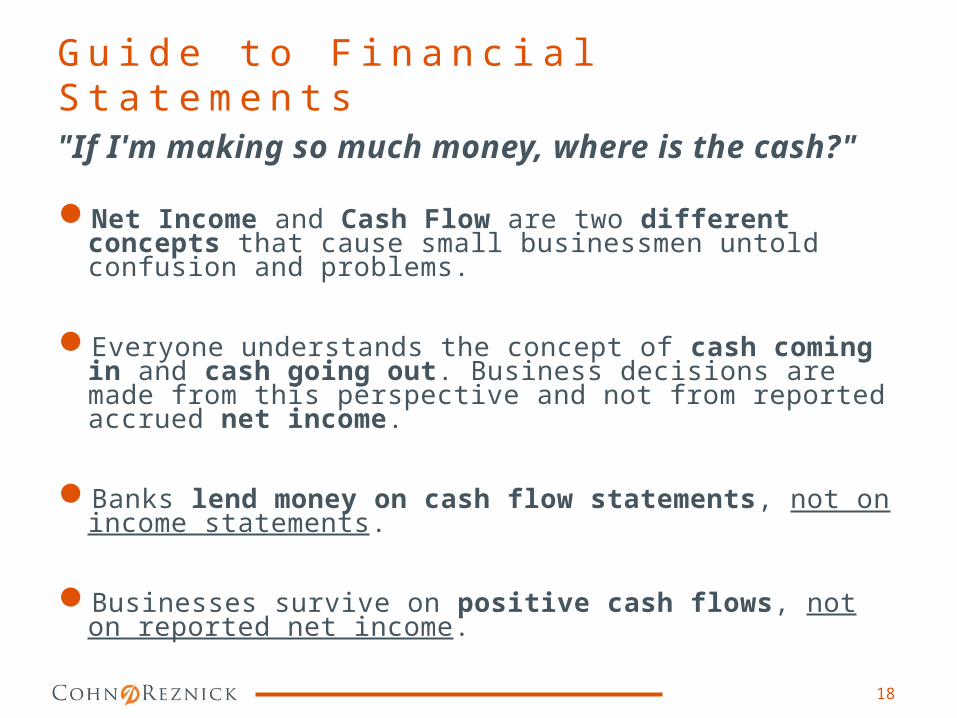

G u i d e t o F i n a n c i a l S t a t e m e n t s

"If I'm making so much money, where is the cash?"

Net Income and Cash Flow are two different concepts that cause small businessmen untold confusion and problems.

Everyone understands the concept of cash coming in and cash going out. Business decisions are made from this perspective and not from reported accrued net income.

Banks lend money on cash flow statements, not on income statements.

Businesses survive on positive cash flows, not on reported net income.

19

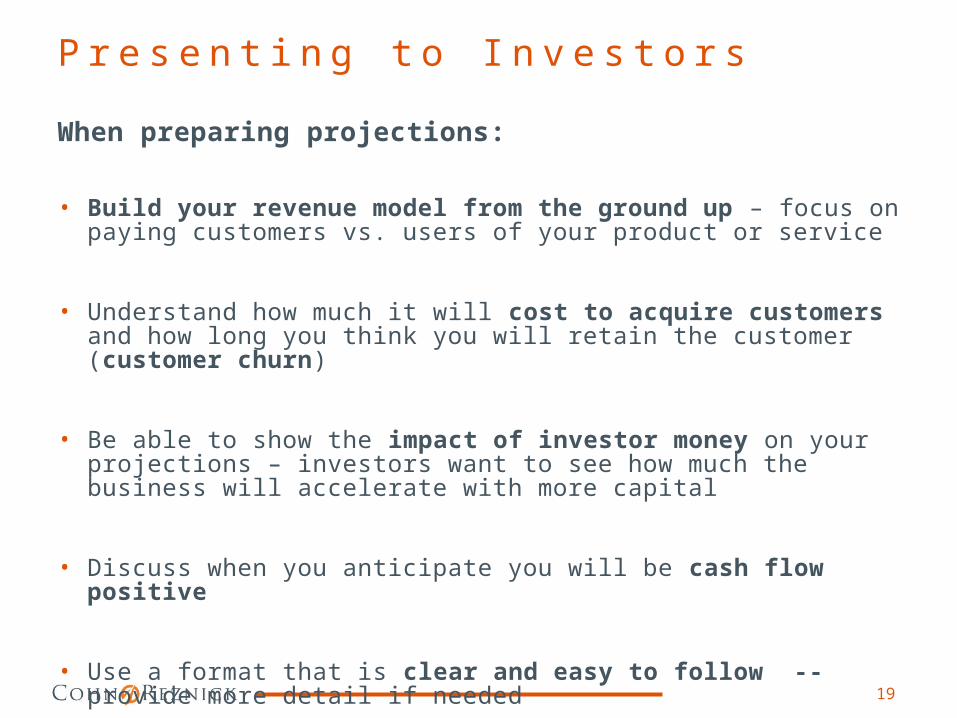

P r e s e n t i n g t o I n v e s t o r s

When preparing projections:

• Build your revenue model from the ground up – focus on paying customers vs. users of your product or service

• Understand how much it will cost to acquire customers and how long you think you will retain the customer (customer churn)

• Be able to show the impact of investor money on your projections – investors want to see how much the business will accelerate with more capital

• Discuss when you anticipate you will be cash flow positive

• Use a format that is clear and easy to follow -- provide more detail if needed

20

P r e s e n t i n g t o I n v e s t o r s

When presenting financial information:

• Keep it simple and easy to understand

• Understand your revenue model and be able to explain flat periods or delays in generating expected revenue

• In most situations, shareholder loans will become equity and not repaid

• If you invested cash in the company, show that as capital or equity. Sweat equity is NOT a financial statement line item.

• Generally, for early stage companies a balance sheet and income statement will suffice – make sure the balance sheet balances and you can explain line items on the income statement.

Don’t assume the team will be able to take significant salaries post-investment – investors still want to see you hungry and motivated.

21

C l o s i n g R e m a r k s

You, the founder, need to understand basic accounting. While you can outsource the accounting or leave it to your controller, you still are responsible for your numbers.

Not being able to present accurate financial statements to potential investors or bankers can delay or kill a deal.

It is difficult to regain credibility in your financial reporting once it is lost.

Seek advice from experienced professionals when you start your company and as needed as you grow.

Always be prepared for someone to ask to do due diligence on your financial records. Maintain complete files to support what you report.

A B O U T T H E P R E S E N T E R

A L E X C A S T E L L I , C PA , T E C H N O L O G Y & L I F E S C I E N C E S I N D U S T R Y P R A C T I C E L E A D E R

Alex Castelli is the National Leader of CohnReznick’s Technology and Life Sciences Practice which assists private, public, and venture and private-equity backed companies succeed at each stage of their life cycle. With nearly 25 years of experience managing the audit, accounting, and reporting issues of middle-market companies, he dedicates his practice to serving an entrepreneurial client base. Alex is based in the firm’s Tysons Corner office where he serves as Managing Partner.

Contact:

Alex Castelli

8045 Leesburg Pike, Suite 300

Vienna, VA 22182

703.744.6708

www.cohnreznick.com

Twitter: @CR_TechInd

22