financial summary for bob smith jill smithfinancial summary for bob smith and jill smith solution:...

TRANSCRIPT

Financial Summaryfor

Bob SmithJill Smith

May 6, 2016

Allan Norman, M.Sc., CFP, CIM

Atlantis Financial Inc48A Alliance BlvdSuite 208Barrie, ON L4M 5K3Phone: 705-726-6884 x 230Fax: 705-726-9884Email: [email protected]

Prepared by:

The calculations and output of the VisionWorks program are for demonstration purposes only. While every effort has been made to ensure that the results are accurate, the planner and Vision Systems Corp. (the owner of the software that produces the plan) expressly disclaim any liability, loss, or risk - financial or otherwise - incurred as a consequence - directly or indirectly - of the use and/or application of any of the ideas, advice, suggestions, or techniques demonstrated.

VisionWorks™ is a registered trademark of Vision Systems Corp.

Table of Contents

Section Page

Prologue 1

Introduction 2

Plan Parties 3

4Family Tree

Goals and Objectives 5

Challenges and Problems 6

Reccomendations 7

To Do List 9

Values 10

Financial Attitudes 11

Net Worth 12

12Net Worth Statement (Current Solution)

Cash Sources 14

14Cash Sources (Income Plan)

Cash Uses 15

15Cash Uses (Spending Plan)

18T1 General Income Tax Return

22Tax Rate Table

25Tax Rate Graph

Compare 27

Private Company Dividends 33

Trust Distributions 35

Table of Contents

Section Page

Net Cash Flow Forecast 36

36Cash Sources and Cash Uses

41Retirement Cash Sources and Uses

44OAS, CPP / QPP, GIS Table

Net Worth Forecast 50

50Net Worth Forecast

Income Assets Forecast 54

54Income Assets Forecast

Estate Summary 59

59Forecasted Estate Value

61Residue for Distribution

Epilogue 62

Appendix A1

A1General Assumptions

Financial Summary for Bob Smith and Jill Smith Solution: Dividends/ Investco/ Solutions

Prologue

Habit 2Begin with the End in Mind

To begin with the end in mind means to start with a clear understanding of your destination. It means to know where you're going so that you better understand where you are now and so that the steps you take are always in the right direction.

By keeping that end clearly in mind, you can make certain that whatever you do on any particular day does not violate the criteria you have defined as supremely important, and that each day of your life contributes in a meaningful way to the vision you have of your life as a whole.

Stephen R. CoveyThe Seven Habits of Highly Effective PeopleSimon & Schuster, 1989.

Prepared by Allan Norman, M.Sc., CFP, CIM - 1 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Introduction

Solution: Dividends/ Investco/ Solutions

The only purpose of planning is to clarify your vision of life and discover how to act effectively to achieve that vision.

To do this, we will create your life plan. Because you will be involved in the planning process, you will learn the implications of different decisions.

Through Atlantis Financial you have a powerful new technology at your disposal. You have discovered a new way to make the most informed decisions possible in the future. As your life unfolds, you will face new choices. You will be able to model them and discover their long-term implications. You will make mistakes on the software's practise field, rather than making costly and irreversible mistakes in real life.

We all have to manage change. By using the software as a decision-making model, you will master change. You will have a greater sense of control. You will be more satisfied with your new decisions and feel more fulfilled. And most importantly, you will easily recognize opportunities that will help you achieve your vision. These are the lasting benefits of life planning.

Prepared by Allan Norman, M.Sc., CFP, CIM - 2 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

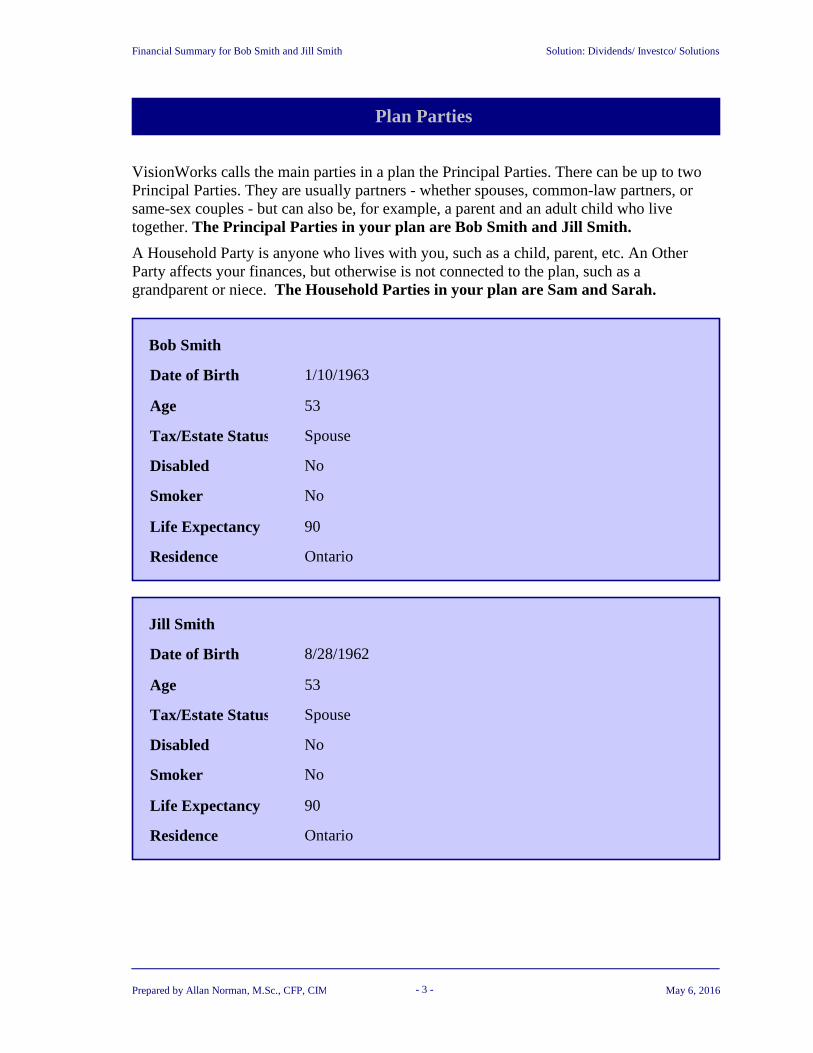

Plan Parties

Solution: Dividends/ Investco/ Solutions

VisionWorks calls the main parties in a plan the Principal Parties. There can be up to two Principal Parties. They are usually partners - whether spouses, common-law partners, or same-sex couples - but can also be, for example, a parent and an adult child who live together. The Principal Parties in your plan are Bob Smith and Jill Smith.

A Household Party is anyone who lives with you, such as a child, parent, etc. An Other Party affects your finances, but otherwise is not connected to the plan, such as a grandparent or niece. The Household Parties in your plan are Sam and Sarah.

Bob Smith

Date of Birth 1/10/1963

Age 53

Tax/Estate Status Spouse

Disabled No

Smoker No

Life Expectancy 90

Residence Ontario

Jill Smith

Date of Birth 8/28/1962

Age 53

Tax/Estate Status Spouse

Disabled No

Smoker No

Life Expectancy 90

Residence Ontario

Prepared by Allan Norman, M.Sc., CFP, CIM - 3 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Family Tree

Solution: Dividends/ Investco/ Solutions

Bob1/10/1963

Jill8/28/1962

Sam4/15/1994

Sarah3/6/1996

Prepared by Allan Norman, M.Sc., CFP, CIM - 4 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith Solution: Dividends/ Investco/ Solutions

Goals and Objectives

Goals

• He would like to be in a position to retire at age 61 (End of December 2024)

• She would like to retire today but is prepared to work until she turns 62 (August 2024)

• Pay for their children's university education and help them with their first home

• Home renovations; three bathrooms, basement, kitchen, sprinkler system and paved drive

• In retirement she would like to be in Florida 6 months of the year, he would prefer just a few weeks.

• In retirement they would like to fund one family vacation a year that would include children and future grand children

• The would like to leave their children a minimum inheritance of $500,000 each

• Ultimately, they don't want to worry about money and they want to have enough so they can have and do the things they want when they want.

They do not want to include the potential sale of his business or any possible inheritances in their plan

Objectives

• Accumulate $1 million in retirement savings by the time they are age 60.

• Pay off their $350,000 debt

• Contribute $25,000/child/year to get them through university debt free

• Set aside $25,000 - $50,000 for each child for a down payment on their first house (optional).

• Complete a home renovation project each year for the next 5 years. Master bath $10,000; basement and bath $15,000, Sprinkler system $10,000, Driveway $10,000, Kitchen $20,000. He would like to do most of the work himself.

• An after tax retirement income of $70,000/yr inflated at 3%

• At age 75 or 80 reduce spending to $60,000/yr after tax

Prepared by Allan Norman, M.Sc., CFP, CIM - 5 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith Solution: Dividends/ Investco/ Solutions

Challenges and Problems

Challenges

• As a business owner he made very little money when their children where young so they did not save for their children's education

• In the past few years his income has increased and now they are not eligible for government education grants, and the children are not eligible for student loans.

• The children have not been able to get summer jobs

• They are using their line of credit to fund education expenses so the debt is increasing rather than decreasing.

• They have maximized their RRSP and TFSA accounts and they are not sure where to save their money so they aren't tempted to spend it.

• He is losing a lot of his income to tax which means less money for investing, paying down debt, and helping the kids with their education.

• She is not sure she able to continue working for another 8 years.

• With the debt and their kids in University, they are concerned about their financial well-being and are afraid to spend money on. This has affected their lifestyle and they have become home bodies

Problems

• They owe $350,000 and they anticipate having to borrow another $100,000 to pay for their children's education.

• He makes $190,000 and pays about $50,000 in tax.

• She earns $42,000/yr. and wonders where it all goes because she doesn't pay household bills.

• Like most couples, they don't know where all of their money is going. If this “leaked” money was captured and saved, they would have an additional $388,000 by the time they retire in 2024.

• If they save all of the money that is leaking from their household budget over their lifetime they would have an additional $2.5 million.

• When the last surviving spouse passes away they will lose $1.1 million (future $) or $392,000 (current $) of what they have built over their life time to tax.

Prepared by Allan Norman, M.Sc., CFP, CIM - 6 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith Solution: Dividends/ Investco/ Solutions

Reccomendations

1. Recommendations

• Set up a family trust where all family members are beneficiaries. Pay enough to the family trust to cover the children's university costs. Then pay the children a dividend to pay their tuition.

• Keep the family trust until the children are established and then review if it makes sense to keep it. This may be used to help the kids with a down payment for a house?

• Reduce his income to what they need to run the household, $80,000. Continue to pay her $10,000.

• Set up a holding company to own shares in his OPCO. Send $85,000 in dividends over to the holding company for long term investments

• We will follow an all equity passive investment strategy with low distributions in the HOLDCO, rather than corporate class funds. Corporate class funds were considered, as in theory they don't pay taxable distributions and taxes are deferred into the future, however, in our experience corporate class funds can pay distributions and their fee is slightly higher so we have decided not to use them.

• Stop making RRSP contributions

• Continue to deposit $11,000/yr (maximum) to the TFSA for life.

• Once retired review income needs and sources. In the current projection he draws $20,000/yr in dividends and she draws $10,000/yr. The income shortage is made up with RRIF payments. The aim is to keep their taxable income just below the next tax bracket. Retirement income needs should be reviewed each December or January to anticipate taxable income for the upcoming year.

• Although the debt appears to be large it is not an issue and should not be the measure of financial well-being. If they continue to pay $24,000/year toward the mortgage it will be paid off by the time he wants to be in a position to retire. They should continue to pay interest only on the 2 loans where the interest is tax deductible. Once the mortgage is paid off then they can continue paying $24,000 a year until all loans are paid off. Note that the projections show that their net worth will be higher if they do not pay off the two smaller loans so again, debt should not scare them. There is a whole life policy in place that will pay off most of the loans and they are accumulating money in a TFSA which can be withdrawn at any time tax free to pay down the loan.

• They have adequate life insurance. He has $750,000 of 10yrt and $130,000 whole life premium which we recommend that he continues to pay for life. She has $250,000 of

Prepared by Allan Norman, M.Sc., CFP, CIM - 7 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith Solution: Dividends/ Investco/ Solutions

Reccomendations

10yrt and $50,000 of employee insurance.

• He has disability insurance and she has coverage at work plus $50,000 return of premium CI policy. They have both agreed that if he died or became disabled they/she would sell the home, pay off the debt and move to a smaller house.

• At some point in the future it is going to have to be decided what to do with the assets building in the holding company. Estate freeze, buy life insurance, or draw it down faster.

2. Investment Allocation Recommendation

It is recommended to follow an asset dedication strategy rather than an asset allocation strategy.

• An all equity portfolio until 5 years prior to retirement. Passive funds 30% Canada, 30% US, 30% international, 10% REIT.

• 5 years prior to retirement begin to add bonds to the portfolio. For example if we need $40,000/year from an investment account then 5 years prior to retirement move 1 year's ($40,000) income to bonds. Repeat this each year so that when retirement happens you have 5 years of income in bonds or cash. In retirement you will draw money from the bonds and replace that with money from the equities only if equities are up. If investment markets are down we have a 5 year cash bridge to wait until markets recover.

Prepared by Allan Norman, M.Sc., CFP, CIM - 8 - May 6, 2016

To Do List

Financial Summary for Bob Smith and Jill Smith Solution: Dividends/ Investco/ Solutions

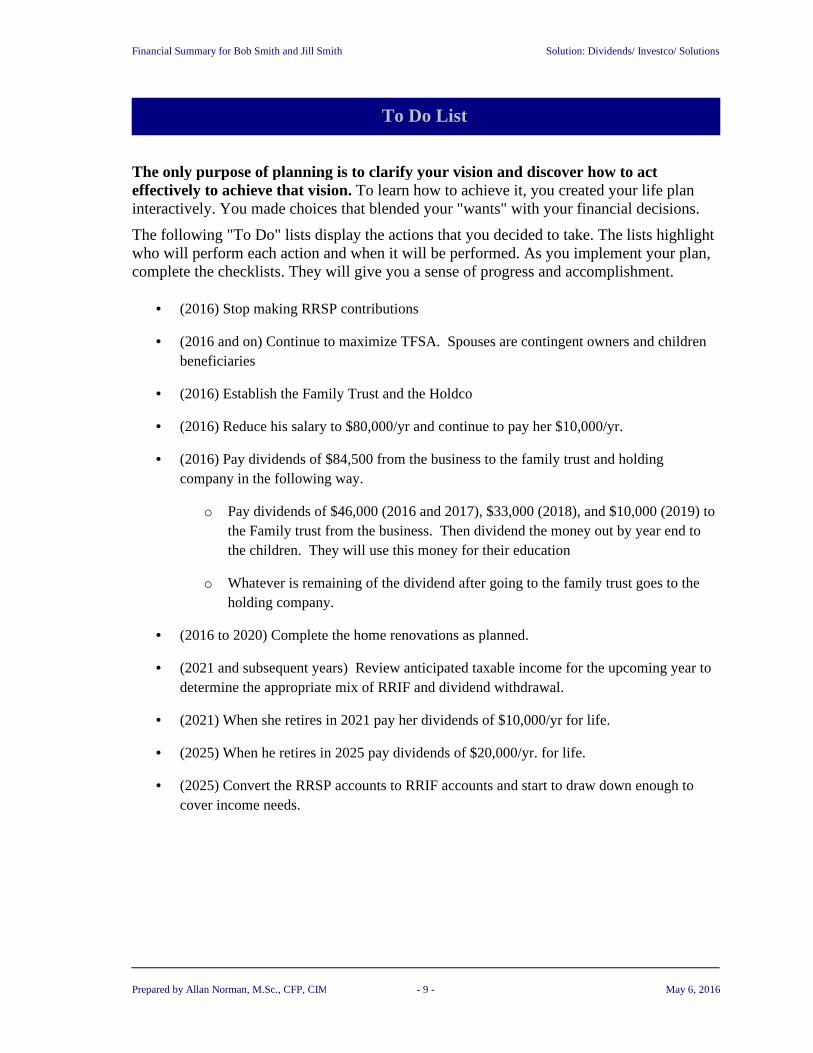

The only purpose of planning is to clarify your vision and discover how to act effectively to achieve that vision. To learn how to achieve it, you created your life plan interactively. You made choices that blended your "wants" with your financial decisions.

The following "To Do" lists display the actions that you decided to take. The lists highlight who will perform each action and when it will be performed. As you implement your plan, complete the checklists. They will give you a sense of progress and accomplishment.

• (2016) Stop making RRSP contributions

• (2016 and on) Continue to maximize TFSA. Spouses are contingent owners and children beneficiaries

• (2016) Establish the Family Trust and the Holdco

• (2016) Reduce his salary to $80,000/yr and continue to pay her $10,000/yr.

• (2016) Pay dividends of $84,500 from the business to the family trust and holding company in the following way.

o Pay dividends of $46,000 (2016 and 2017), $33,000 (2018), and $10,000 (2019) to the Family trust from the business. Then dividend the money out by year end to the children. They will use this money for their education

o Whatever is remaining of the dividend after going to the family trust goes to the holding company.

• (2016 to 2020) Complete the home renovations as planned.

• (2021 and subsequent years) Review anticipated taxable income for the upcoming year to determine the appropriate mix of RRIF and dividend withdrawal.

• (2021) When she retires in 2021 pay her dividends of $10,000/yr for life.

• (2025) When he retires in 2025 pay dividends of $20,000/yr. for life.

• (2025) Convert the RRSP accounts to RRIF accounts and start to draw down enough to cover income needs.

Prepared by Allan Norman, M.Sc., CFP, CIM - 9 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Values

Solution: Dividends/ Investco/ Solutions

Your vision is based to a great extent on what means the most to you. Our values largely determine what we want. We base many important decisions on them.

The table below presents your most important family values.

Value Definition

Health To be healthy and lead a healthy lifestyle.

Enjoyment To enjoy life and have fun.

Family To contribute to family members.

Friendship To have close companionship.

Activity To be fully occupied at all times.

Self-Development To be the best that I can be.

Academics

Academics

Academics

Academics

Achievement

Achievement

Achievement

Achievement

Activity

Activity

Activity

Activity

Advancement

Advancement

Advancement

Advancement

Adventure

Adventure

Adventure

Adventure

Enjoyment

Enjoyment

Enjoyment

Enjoyment

Expertise

Expertise

Expertise

Expertise

Family

Family

Family

Family

Friendship

Friendship

Friendship

Friendship

Health

Health

Health

Health

Independence

Independence

Independence

Independence

Location

Location

Location

Location

Power

Power

Power

Power

Prestige

Prestige

Prestige

Prestige

Routine

Routine

Routine

Routine

Security

Security

Security

Security

Self-Development

Self-Development

Self-Development

Self-Development

Self-Realization

Self-Realization

Self-Realization

Self-Realization

Social Service

Social Service

Social Service

Social Service

Wealth

Wealth

Wealth

Wealth

VeryImportant

QuiteImportant

Important

SomewhatImportant

NotImportant

Values Graph

Prepared by Allan Norman, M.Sc., CFP, CIM - 10 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Financial Attitudes

Solution: Dividends/ Investco/ Solutions

We base many everyday decisions on our financial attitudes. They are important for three reasons. First, you will act on a life plan that suits your attitudes because you feel comfortable with it. Second, your attitudes suggest what you should change. What suits you best? Work? Reduced spending? More risk? Third, we prefer to base our life plan on our attitudes. We feel that it will endure, because it is under our direct control.

The table below shows the results of the financial attitudes exercise that you completed.

AttitudeBob Jill

Low Avge High Low Avge High

Accountability 43.8 66.7 77.8 43.8 50.0 77.8

Work 54.8 75.0 86.0 50.0 54.8 86.0

Spending 50.0 56.5 80.5 33.3 56.5 80.5

Appearance 25.0 41.0 75.3 41.0 41.7 75.3

Contentment 41.7 58.6 89.4 33.3 58.6 89.4

Risk 58.3 59.0 76.0 41.7 59.0 76.0

Trust 28.2 41.7 62.8 28.2 50.0 62.8

Participation 50.0 69.0 86.8 41.7 69.0 86.8

Learning 61.3 82.9 91.7 58.3 61.3 82.9

Financial attitude scores are compared to a national survey, then placed in one of three columns.Average (middle column): It offers no meaningful insight. The low and high boundary scores for the Average Range, which are displayed in blue numbers in the grey columns, are from the national survey.Low (left column): It indicates that the majority of the population would score higher than you.High (right column): It indicates that the majority of the population would score lower than you.

DefinitionAttitude

Willingness to accept responsibility for future results.Accountability

Willingness to achieve your wants by creating wealth through work.Work

Tendency to spend rather than save.Spending

Concern about how one appears to others.Appearance

Satisfaction with your lifestyle and a willingness to defer, alter, or eliminate wants.Contentment

Willingness to accept unpredictable outcomes.Risk

Willingness to delegate responsibilities to others.Trust

Tendency to be involved in the management of your finances and portfolio.Participation

Tendency to learn from past financial decisions and reflect on them when makingcurrent ones.

Learning

Prepared by Allan Norman, M.Sc., CFP, CIM - 11 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Net Worth

Net Worth Statement

Solution: Dividends/ Investco/ Solutions

Net worth is the value of what you own less the value of what you owe - that is, your assets less your liabilities. Your net worth includes your possessions such as your home and your income assets such as your portfolios and RRSPs. The Net Worth Statement below is based on amounts that you estimated. It is the starting point for your life plan.

Bob Jill TotalAssets and Liabilities

Dividends/ Investco/ Solutions (Current Values)

Assets

Homes Our house $544,500 $5,500

Subtotal $544,500 $5,500 $550,000

Vehicles 2013 Car $9,000 $1,000

2015 Car $15,000 $15,000

Subtotal $24,000 $16,000 $40,000

Non-Reg. Portfolios SM Non-Reg. Portfolio $100,659

Subtotal $100,659 $100,659

Other Accounts/Plans TFSA $35,254

TFSA $35,258

Subtotal $35,258 $35,254 $70,512

Pension Plans RRSP - Atlantis $30,605

RRSP $254,323

Subtotal $254,323 $30,605 $284,928

Private Companies INVESTCO: Common A $146,049

INVESTCO: Common C $146,049

Subtotal $146,049 $146,049 $292,098

Life Insurance Whole Life - Sun Life $36,651

Subtotal $36,651 $36,651

$1,141,440AssetsTotal $233,408 $1,374,848

Liabilities

Homes Our house - Line of credit ($179,542) ($1,814)

Prepared by Allan Norman, M.Sc., CFP, CIM - 12 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Net Worth

Solution: Dividends/ Investco/ Solutions

Bob Jill TotalAssets and Liabilities

LiabilitiesSubtotal ($179,542) ($1,814) ($181,356)

Vehicles 2015 Car - Finance ($9,305) ($9,305)

Subtotal ($9,305) ($9,305) ($18,610)

Other Business line of credit ($68,524)

SM Line of credit ($113,588)

Subtotal ($182,112) ($182,112)

$370,959LiabilitiesTotal $11,119 $382,078

Net Worth $770,481 $222,289 $992,770

Category PercentAmount

Total Assets Chart for 2016

Homes $550,000 40.00Vehicles $40,000 2.91Non-Reg. Portfolios $100,659 7.32Other Accounts/Plans $70,512 5.13Pension Plans $284,928 20.72Private Companies $292,098 21.25Life Insurance $36,651 2.67

Total $1,374,848 100.00

Trust Bob Jill Total

Norman Family Trust 2014 $0 $0 $0

Prepared by Allan Norman, M.Sc., CFP, CIM - 13 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

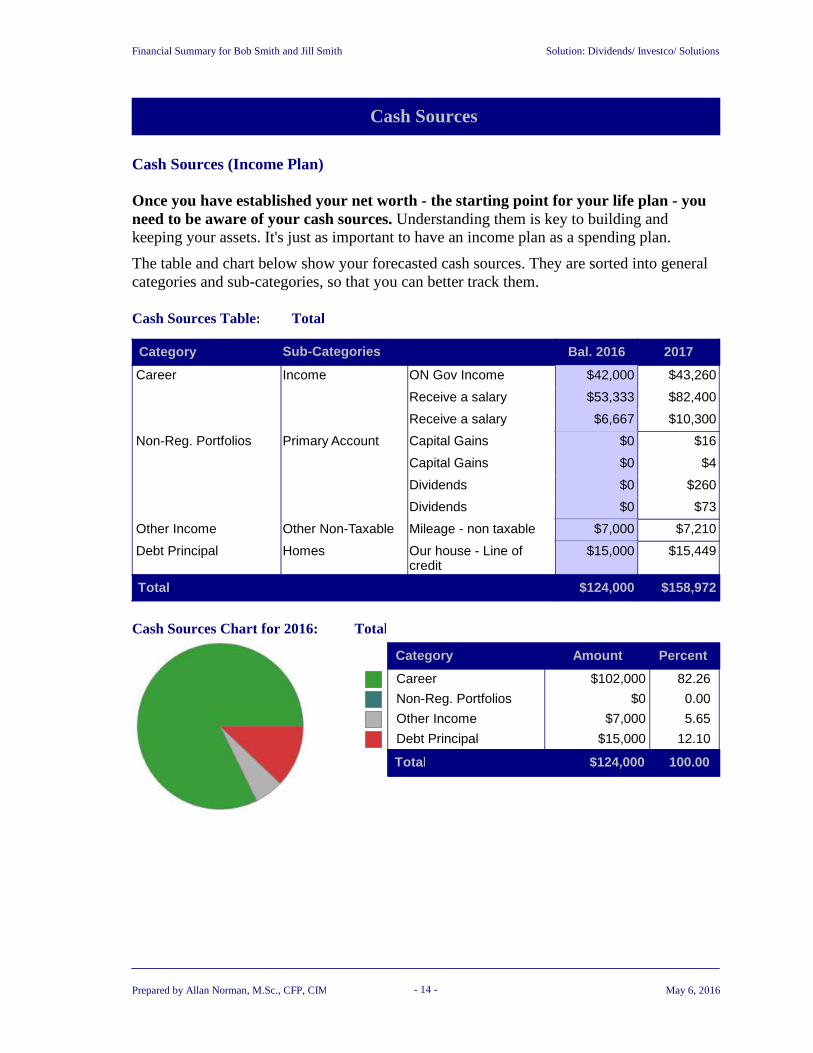

Cash Sources

Cash Sources (Income Plan)

Solution: Dividends/ Investco/ Solutions

Once you have established your net worth - the starting point for your life plan - you need to be aware of your cash sources. Understanding them is key to building and keeping your assets. It's just as important to have an income plan as a spending plan.

The table and chart below show your forecasted cash sources. They are sorted into general categories and sub-categories, so that you can better track them.

Category Sub-Categories Bal. 2016 2017

TotalCash Sources Table:

IncomeCareer ON Gov Income $42,000 $43,260

Receive a salary $53,333 $82,400

Receive a salary $6,667 $10,300

Primary AccountNon-Reg. Portfolios Capital Gains $0 $16

Capital Gains $0 $4

Dividends $0 $260

Dividends $0 $73

Other Non-TaxableOther Income Mileage - non taxable $7,000 $7,210

HomesDebt Principal Our house - Line ofcredit

$15,000 $15,449

Total $124,000 $158,972

Category PercentAmount

TotalCash Sources Chart for 2016:

Career $102,000 82.26

Non-Reg. Portfolios $0 0.00

Other Income $7,000 5.65

Debt Principal $15,000 12.10

Total $124,000 100.00

Prepared by Allan Norman, M.Sc., CFP, CIM - 14 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Cash Uses

Cash Uses (Spending Plan)

Solution: Dividends/ Investco/ Solutions

Once you have established your net worth and cash sources, you need to be aware of your cash uses. Understanding them is key to building and keeping assets. If you intend to achieve your vision, you should monitor your cash uses - your spending plan.

The table and chart below show your forecasted cash uses. They are sorted into general categories and sub-categories, so that you can better track them.

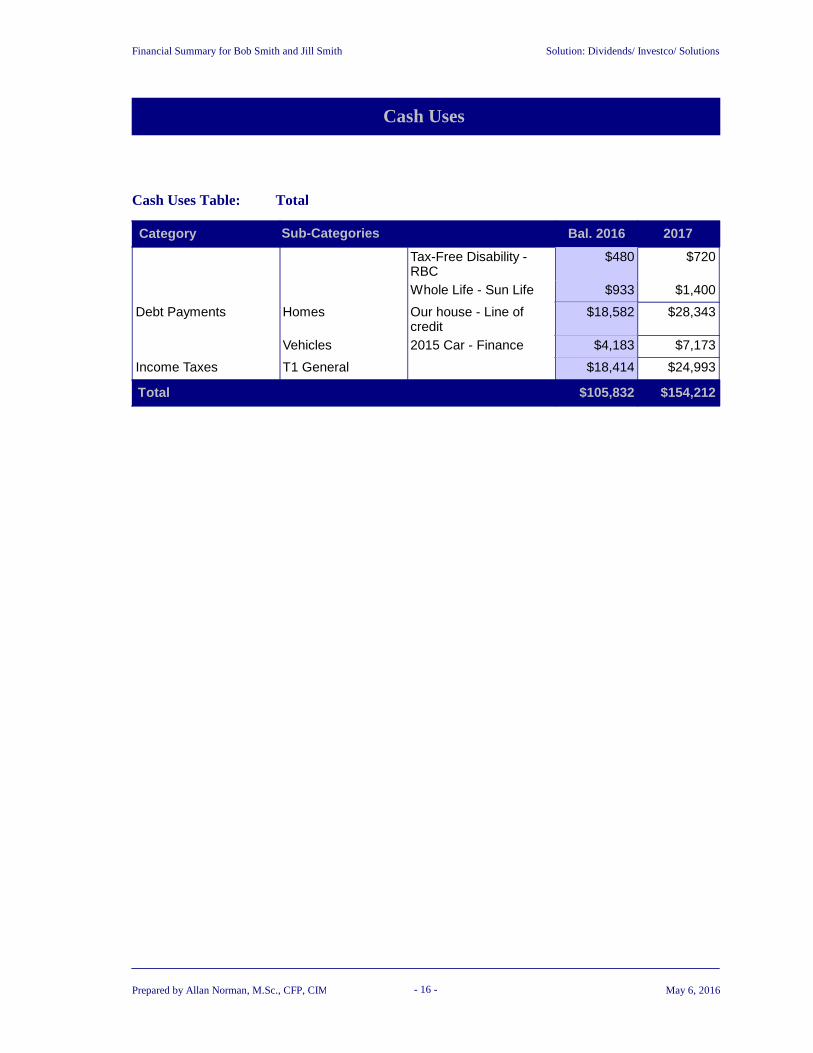

Category Sub-Categories Bal. 2016 2017

Cash Uses Table: Total

Operating Expenses $8,267 $12,772Our houseHomes

Property Taxes $2,667 $4,120

Renovations $10,000 $15,450

General entertainment $1,334 $2,060EntertainmentLifestyle Expenses

Alcohol $333 $515General Expenses

Clothing $1,733 $2,678

Groceries $5,600 $8,652

kids $666 $1,030

Miscellaneous Cash $2,200 $3,399

Personal $333 $515

Travel to a hot, busy allinclusive beach resortwith the kids for 2weeks every MarchBreak

$3,333 $5,150Vacations

2013 Car $6,841 $10,570Vehicles

2015 Car $2,000 $3,090

$3,296 $5,148CPP/QPPContributions

Career

$637 $818EI premiums

Pay union orprofessional dues

$167 $257Expenses

TFSA $5,500 $5,500ContributionsOther Accounts/Plans

TFSA $5,500 $5,500

OPSU $600 $927ContributionsRRSP / Pension Plans

Health and dental policy $1,833 $2,832PremiumsInsurance

Tax-Free C.I. - RBC $400 $600

Prepared by Allan Norman, M.Sc., CFP, CIM - 15 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Cash Uses

Solution: Dividends/ Investco/ Solutions

Category Sub-Categories Bal. 2016 2017

Cash Uses Table: Total

Tax-Free Disability -RBC

$480 $720

Whole Life - Sun Life $933 $1,400

Our house - Line ofcredit

$18,582 $28,343HomesDebt Payments

2015 Car - Finance $4,183 $7,173Vehicles

$18,414 $24,993T1 GeneralIncome Taxes

Total $105,832 $154,212

Prepared by Allan Norman, M.Sc., CFP, CIM - 16 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Cash Uses

Solution: Dividends/ Investco/ Solutions

Category PercentAmount

Cash Uses Chart for 2016:

$20,934 19.78Homes

$24,373 23.03Lifestyle Expenses

$4,100 3.87Career

$11,000 10.39Other Accounts/Plans

$600 0.57RRSP / Pension Plans

$3,646 3.45Insurance

$22,765 21.51Debt Payments

$18,414 17.40Income Taxes

Total $105,832 100.00

Category PercentAmount

Cash Uses Chart for 2017:

$32,342 20.97Homes

$37,659 24.42Lifestyle Expenses

$6,223 4.04Career

$11,000 7.13Other Accounts/Plans

$927 0.60RRSP / Pension Plans

$5,552 3.60Insurance

$35,516 23.03Debt Payments

$24,993 16.21Income Taxes

Total $154,212 100.00

Prepared by Allan Norman, M.Sc., CFP, CIM - 17 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Cash Uses

Estimated Income Taxes Payable

Solution: Dividends/ Investco/ Solutions

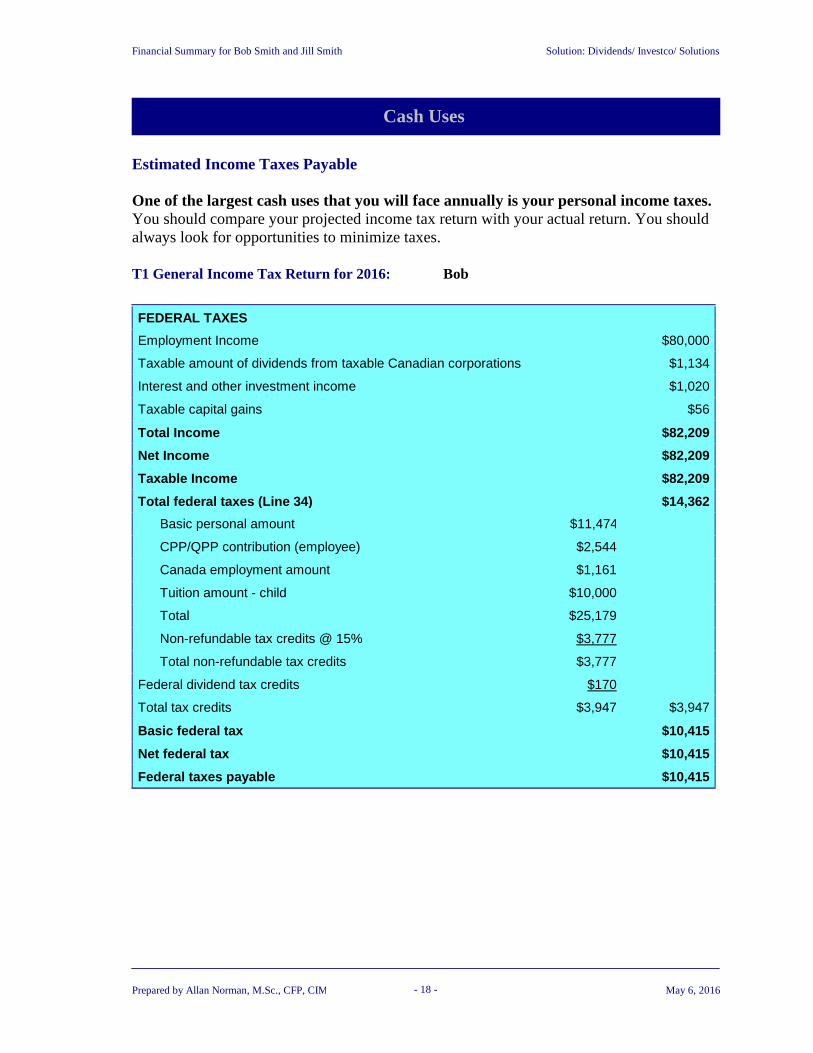

One of the largest cash uses that you will face annually is your personal income taxes. You should compare your projected income tax return with your actual return. You should always look for opportunities to minimize taxes.

T1 General Income Tax Return for 2016: Bob

FEDERAL TAXES

Employment Income $80,000

Taxable amount of dividends from taxable Canadian corporations $1,134

Interest and other investment income $1,020

Taxable capital gains $56

Total Income $82,209

Net Income $82,209

Taxable Income $82,209

Total federal taxes (Line 34) $14,362

Basic personal amount $11,474

CPP/QPP contribution (employee) $2,544

Canada employment amount $1,161

Tuition amount - child $10,000

Total $25,179

Non-refundable tax credits @ 15% $3,777

Total non-refundable tax credits $3,777

Federal dividend tax credits $170

Total tax credits $3,947 $3,947

Basic federal tax $10,415

Net federal tax $10,415

Federal taxes payable $10,415

Prepared by Allan Norman, M.Sc., CFP, CIM - 18 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Cash Uses

Solution: Dividends/ Investco/ Solutions

T1 General Income Tax Return for 2016: Bob

PROVINCIAL TAXES

Ontario tax on taxable income $5,819

Basic personal amount $10,011

CPP/QPP contribution (employee) $2,544

Tuition amount - child $10,000

Total $22,555

Total non-refundable tax credits @ 5.05% $1,139

Ontario non-refundable tax credits $1,139

Ontario dividend tax credit $113

Ontario Health Premium $750

Ontario tax $5,317

TAXES PAYABLE $15,732

Prepared by Allan Norman, M.Sc., CFP, CIM - 19 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Cash Uses

Solution: Dividends/ Investco/ Solutions

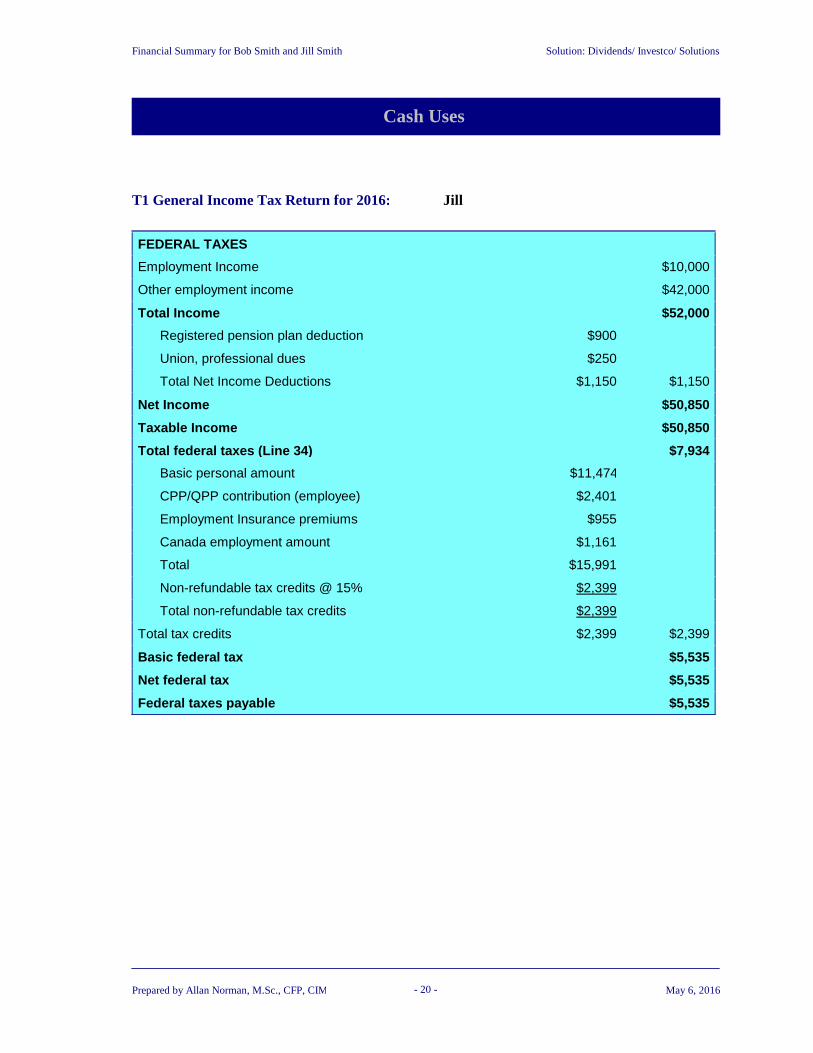

T1 General Income Tax Return for 2016: Jill

FEDERAL TAXES

Employment Income $10,000

Other employment income $42,000

Total Income $52,000

Registered pension plan deduction $900

Union, professional dues $250

Total Net Income Deductions $1,150 $1,150

Net Income $50,850

Taxable Income $50,850

Total federal taxes (Line 34) $7,934

Basic personal amount $11,474

CPP/QPP contribution (employee) $2,401

Employment Insurance premiums $955

Canada employment amount $1,161

Total $15,991

Non-refundable tax credits @ 15% $2,399

Total non-refundable tax credits $2,399

Total tax credits $2,399 $2,399

Basic federal tax $5,535

Net federal tax $5,535

Federal taxes payable $5,535

Prepared by Allan Norman, M.Sc., CFP, CIM - 20 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Cash Uses

Solution: Dividends/ Investco/ Solutions

T1 General Income Tax Return for 2016: Jill

PROVINCIAL TAXES

Ontario tax on taxable income $2,950

Basic personal amount $10,011

CPP/QPP contribution (employee) $2,401

Employment Insurance premiums $955

Total $13,367

Total non-refundable tax credits @ 5.05% $675

Ontario non-refundable tax credits $675

Ontario Health Premium $600

Ontario tax $2,875

TAXES PAYABLE $8,410

Prepared by Allan Norman, M.Sc., CFP, CIM - 21 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Cash Uses

Tax Rate Table

Solution: Dividends/ Investco/ Solutions

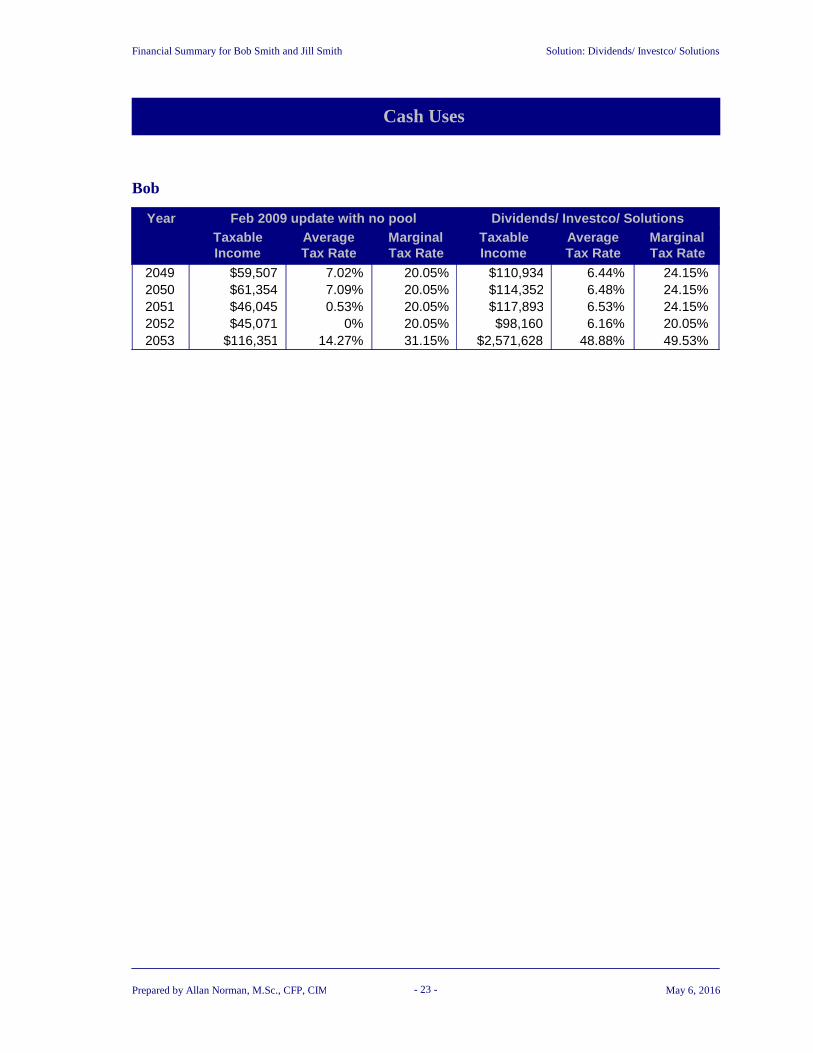

The following table displays your average and marginal tax rates over time. Notice that the original solution "All Salary" is compared to the new solution "Dividends/Investco" where we reduced Bob's salary and paid the children dividends and saved for retirement in Investco.

Bob

Year Dividends/ Investco/ SolutionsFeb 2009 update with no poolTaxableIncome

MarginalTax Rate

MarginalTax Rate

TaxableIncome

AverageTax Rate

AverageTax Rate

2016 $150,001 47.97% $82,209 35.39%30.55% 19.14%2017 $126,727 43.41% $84,807 35.39%27.61% 19.17%2018 $125,483 43.41% $87,415 35.39%27.98% 19.21%2019 $125,810 43.41% $90,518 35.39%27.62% 20.41%2020 $126,706 43.41% $94,159 35.39%27.32% 21.57%2021 $127,459 43.41% $101,358 39.41%27% 22.17%2022 $128,589 43.41% $98,629 35.39%26.73% 21.37%2023 $301,902 49.53% $141,681 43.41%39.23% 27.07%2024 $19,384 20.05% $145,049 43.41%4.21% 26.91%2025 $32,362 20.05% $68,029 31.15%12.41% 12.25%2026 $34,097 20.05% $68,420 31.15%12.6% 11.91%2027 $34,395 20.05% $68,837 31.15%11.42% 11.56%2028 $42,772 20.05% $62,982 24.15%10.02% 6.45%2029 $39,745 20.05% $72,124 31.15%8.96% 9.16%2030 $39,418 20.05% $80,872 31.15%8.56% 11.33%2031 $49,582 20.05% $82,453 31.15%10.97% 11.17%2032 $42,831 20.05% $85,135 31.15%7.96% 11.28%2033 $39,543 20.05% $88,631 31.15%6.63% 11.55%2034 $40,269 20.05% $104,430 31.15%6.53% 14.17%2035 $41,172 20.05% $98,306 31.15%6.49% 12.35%2036 $42,159 20.05% $97,858 31.15%6.48% 11.59%2037 $43,572 20.05% $99,337 31.15%6.58% 11.25%2038 $44,968 20.05% $75,827 20.05%6.67% 4.28%2039 $46,342 20.05% $78,322 20.05%6.74% 4.42%2040 $47,761 20.05% $80,926 20.05%6.81% 4.58%2041 $59,728 20.05% $88,944 24.15%9.49% 6.31%2042 $48,664 20.05% $89,084 24.15%6.7% 5.74%2043 $49,530 20.05% $92,193 24.15%6.6% 5.96%2044 $51,045 20.05% $95,436 24.15%6.66% 6.17%2045 $52,641 20.05% $98,824 24.15%6.74% 6.36%2046 $54,283 20.05% $99,037 20.05%6.81% 5.82%2047 $55,973 20.05% $102,842 24.15%6.88% 6.05%2048 $57,717 20.05% $106,821 24.15%6.95% 6.24%

Prepared by Allan Norman, M.Sc., CFP, CIM - 22 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Cash Uses

Solution: Dividends/ Investco/ Solutions

Bob

Year Dividends/ Investco/ SolutionsFeb 2009 update with no poolTaxableIncome

MarginalTax Rate

MarginalTax Rate

TaxableIncome

AverageTax Rate

AverageTax Rate

2049 $59,507 20.05% $110,934 24.15%7.02% 6.44%2050 $61,354 20.05% $114,352 24.15%7.09% 6.48%2051 $46,045 20.05% $117,893 24.15%0.53% 6.53%2052 $45,071 20.05% $98,160 20.05%0% 6.16%2053 $116,351 31.15% $2,571,628 49.53%14.27% 48.88%

Prepared by Allan Norman, M.Sc., CFP, CIM - 23 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Cash Uses

Solution: Dividends/ Investco/ Solutions

Jill

Year Dividends/ Investco/ SolutionsFeb 2009 update with no poolTaxableIncome

MarginalTax Rate

MarginalTax Rate

TaxableIncome

AverageTax Rate

AverageTax Rate

2016 $17,624 20.05% $50,850 31.15%4.48% 16.54%2017 $20,179 20.05% $52,687 31.15%6.78% 16.58%2018 $19,269 20.05% $54,433 31.15%5.4% 16.56%2019 $31,630 20.05% $56,273 31.15%12.18% 16.55%2020 $22,859 20.05% $58,174 31.15%8.31% 16.53%2021 $23,803 20.05% $23,188 20.05%8.74% 0.79%2022 $21,087 20.05% $32,842 20.05%5.41% 5.5%2023 $24,295 20.05% $51,533 24.15%9.89% 11.55%2024 $22,259 20.05% $52,914 24.15%7.52% 11.51%2025 $25,505 20.05% $43,106 20.05%10.01% 9.76%2026 $26,385 20.05% $43,162 20.05%10.09% 9.48%2027 $23,896 20.05% $40,074 20.05%0% 2.18%2028 $31,096 20.05% $48,513 20.05%4.02% 5.84%2029 $32,309 20.05% $54,944 20.05%4.31% 7.26%2030 $33,560 20.05% $65,245 24.15%4.6% 9.5%2031 $35,709 20.05% $67,940 24.15%5.36% 9.65%2032 $40,681 20.05% $70,729 24.15%7.32% 9.8%2033 $42,234 20.05% $74,312 31.15%7.48% 10.3%2034 $43,144 20.05% $89,930 31.15%7.43% 13.52%2035 $44,047 20.05% $83,247 31.15%7.38% 11.27%2036 $45,034 20.05% $82,631 31.15%7.34% 10.36%2037 $46,447 20.05% $84,094 31.15%7.42% 9.98%2038 $47,843 20.05% $75,827 20.05%7.48% 7.6%2039 $49,217 20.05% $78,322 20.05%7.82% 7.5%2040 $50,636 20.05% $80,926 20.05%7.86% 7.41%2041 $54,133 20.05% $88,944 24.15%8.35% 8.32%2042 $51,539 20.05% $89,084 24.15%7.45% 7.64%2043 $52,405 20.05% $92,193 24.15%7.34% 7.53%2044 $53,920 20.05% $95,436 24.15%7.38% 7.44%2045 $55,516 20.05% $98,824 24.15%7.43% 7.36%2046 $57,158 20.05% $99,037 20.05%7.47% 6.68%2047 $58,848 20.05% $102,842 24.15%7.52% 6.6%2048 $60,592 20.05% $106,821 24.15%7.57% 6.5%2049 $62,382 20.05% $111,018 24.15%7.62% 6.46%2050 $64,229 20.05% $116,288 24.15%7.67% 6.61%2051 $60,596 20.05% $121,832 24.15%6.59% 6.74%2052 $387,062 47.97% $115,963 20.05%35.15% 6.28%

Prepared by Allan Norman, M.Sc., CFP, CIM - 24 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Cash Uses

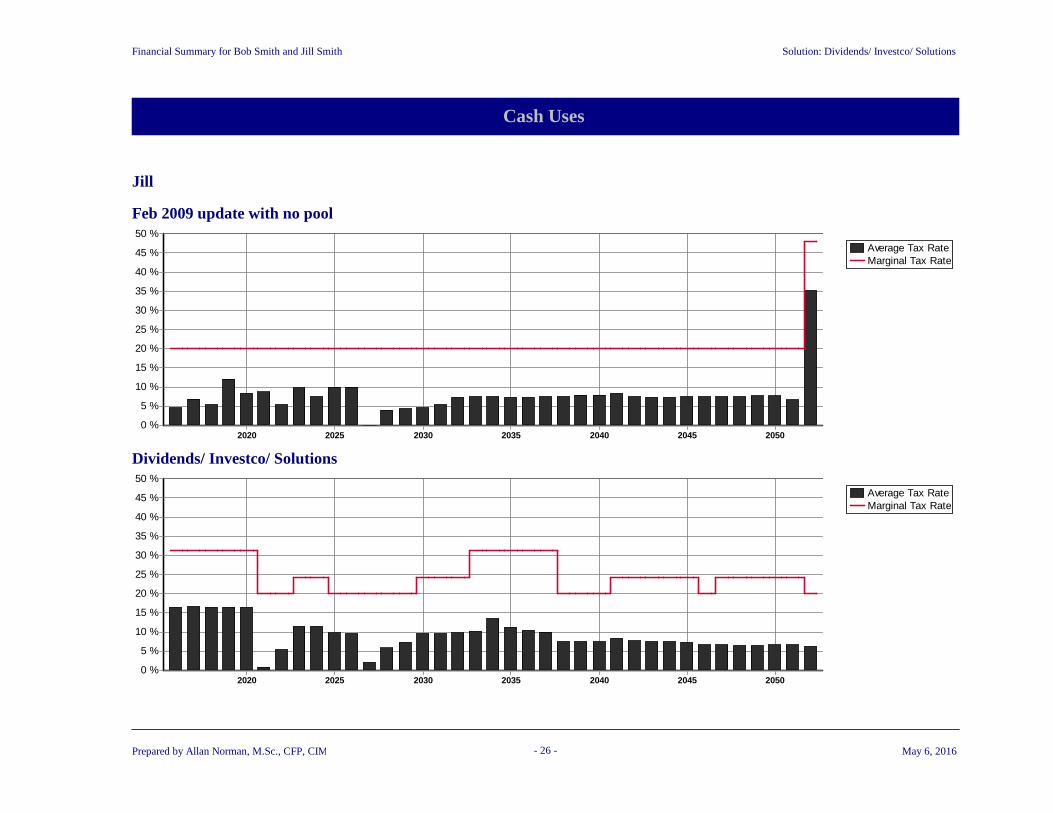

Tax Rate Graph

Solution: Dividends/ Investco/ Solutions

Bob

Average Tax RateMarginal Tax Rate

2050204520402035203020252020

50 %

45 %

40 %

35 %

30 %

25 %

20 %

15 %

10 %

5 %

0 %

Feb 2009 update with no pool

Average Tax RateMarginal Tax Rate

2050204520402035203020252020

50 %

45 %

40 %

35 %

30 %

25 %

20 %

15 %

10 %

5 %

0 %

Dividends/ Investco/ Solutions

Prepared by Allan Norman, M.Sc., CFP, CIM - 25 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Cash Uses

Solution: Dividends/ Investco/ Solutions

Jill

Average Tax RateMarginal Tax Rate

2050204520402035203020252020

50 %

45 %

40 %

35 %

30 %

25 %

20 %

15 %

10 %

5 %

0 %

Feb 2009 update with no pool

Average Tax RateMarginal Tax Rate

2050204520402035203020252020

50 %

45 %

40 %

35 %

30 %

25 %

20 %

15 %

10 %

5 %

0 %

Dividends/ Investco/ Solutions

Prepared by Allan Norman, M.Sc., CFP, CIM - 26 - May 6, 2016

Solution: Dividends/ Investco/ Solutions

Compare

Financial Summary for Bob Smith and Jill Smith

On the following pages we have compared your current approach to the new planned approach. The first page compares your total net worth over time, the next compares your income assets (investments you will use to provide an income), and the last section compares your taxes over time.

Total Net Worth ($000)

Feb 2009 update with no pool Dividends/ Investco/ Solutions

0

2,000

4,000

6,000

8,000

2016 2022 2028 2034 2040 2046 2052

53/54 59/60 65/66 71/72 77/78 83/84 89/90

0

2,000

4,000

6,000

8,000

2016 2022 2028 2034 2040 2046 2052

53/54 59/60 65/66 71/72 77/78 83/84 89/90

Year Net Worth Year Net Worth

2016 $940,123 2016 $1,100,088

2017 $981,794 2017 $1,232,389

2018 $1,043,663 2018 $1,388,859

2019 $1,108,476 2019 $1,581,264

2020 $1,172,076 2020 $1,799,519

2021 $1,240,783 2021 $2,000,051

2022 $1,314,926 2022 $2,214,726

2023 $1,316,938 2023 $2,443,915

2024 $1,322,683 2024 $2,625,184

2025 $1,324,519 2025 $2,432,238

2026 $1,326,013 2026 $2,536,448

2027 $1,334,372 2027 $2,662,524

2028 $1,348,793 2028 $2,782,393

2029 $1,364,869 2029 $2,911,215

2030 $1,368,558 2030 $3,062,527

2031 $1,372,939 2031 $3,223,837

2032 $1,380,940 2032 $3,393,721

2033 $1,391,418 2033 $3,595,147

2034 $1,403,164 2034 $3,782,288

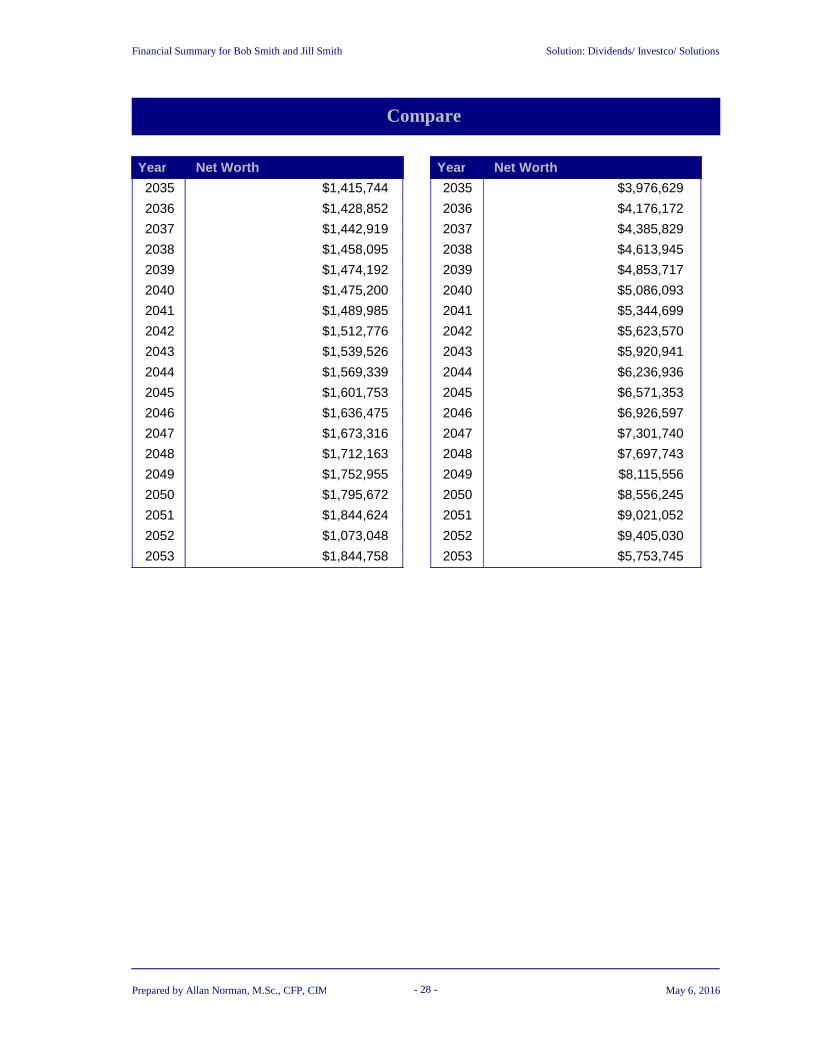

Prepared by Allan Norman, M.Sc., CFP, CIM - 27 - May 6, 2016

Solution: Dividends/ Investco/ Solutions

Compare

Financial Summary for Bob Smith and Jill Smith

Year Net Worth Year Net Worth

2035 $1,415,744 2035 $3,976,629

2036 $1,428,852 2036 $4,176,172

2037 $1,442,919 2037 $4,385,829

2038 $1,458,095 2038 $4,613,945

2039 $1,474,192 2039 $4,853,717

2040 $1,475,200 2040 $5,086,093

2041 $1,489,985 2041 $5,344,699

2042 $1,512,776 2042 $5,623,570

2043 $1,539,526 2043 $5,920,941

2044 $1,569,339 2044 $6,236,936

2045 $1,601,753 2045 $6,571,353

2046 $1,636,475 2046 $6,926,597

2047 $1,673,316 2047 $7,301,740

2048 $1,712,163 2048 $7,697,743

2049 $1,752,955 2049 $8,115,556

2050 $1,795,672 2050 $8,556,245

2051 $1,844,624 2051 $9,021,052

2052 $1,073,048 2052 $9,405,030

2053 $1,844,758 2053 $5,753,745

Prepared by Allan Norman, M.Sc., CFP, CIM - 28 - May 6, 2016

Solution: Dividends/ Investco/ Solutions

Compare

Financial Summary for Bob Smith and Jill Smith

Total Income Assets ($000)

Feb 2009 update with no pool Dividends/ Investco/ Solutions

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2016 2022 2028 2034 2040 2046 20522016 2022 2028 2034 2040 2046 2052

53/54 59/60 65/66 71/72 77/78 83/84 89/9053/54 59/60 65/66 71/72 77/78 83/84 89/90

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2016 2022 2028 2034 2040 2046 20522016 2022 2028 2034 2040 2046 2052

53/54 59/60 65/66 71/72 77/78 83/84 89/9053/54 59/60 65/66 71/72 77/78 83/84 89/90

Income AssetsPrimary Account

Year Income Assets Year Income AssetsPrimary Account Primary Account

2016 $593,750 2016 $864,292($7,633) $18,166

2017 $601,861 2017 $955,803$10,954 $23,664

2018 $610,068 2018 $1,065,544($2,603) $20,955

2019 $618,373 2019 $1,204,205$24,992 $28,912

2020 $626,780 2020 $1,361,983$45,938 $30,590

2021 $635,290 2021 $1,524,323$97,255 $30,469

2022 $643,906 2022 $1,697,724$150,870 $32,303

2023 $272,630 2023 $1,843,120$455,950 $75,695

2024 $281,466 2024 $1,936,056$436,872 $98,712

2025 $290,417 2025 $1,678,589$412,341 $118,374

2026 $299,485 2026 $1,716,474$386,164 $140,521

2027 $308,672 2027 $1,768,228$365,709 $169,492

2028 $317,983 2028 $1,832,321$350,279 $181,065

2029 $327,479 2029 $1,895,667$335,475 $200,760

2030 $337,106 2030 $1,959,952$278,494 $237,263

2031 $345,546 2031 $2,025,483$260,130 $278,481

2032 $348,404 2032 $2,092,295$247,603 $323,403

2033 $351,037 2033 $2,159,023$235,194 $406,889

2034 $353,416 2034 $2,202,262$222,261 $513,151

Prepared by Allan Norman, M.Sc., CFP, CIM - 29 - May 6, 2016

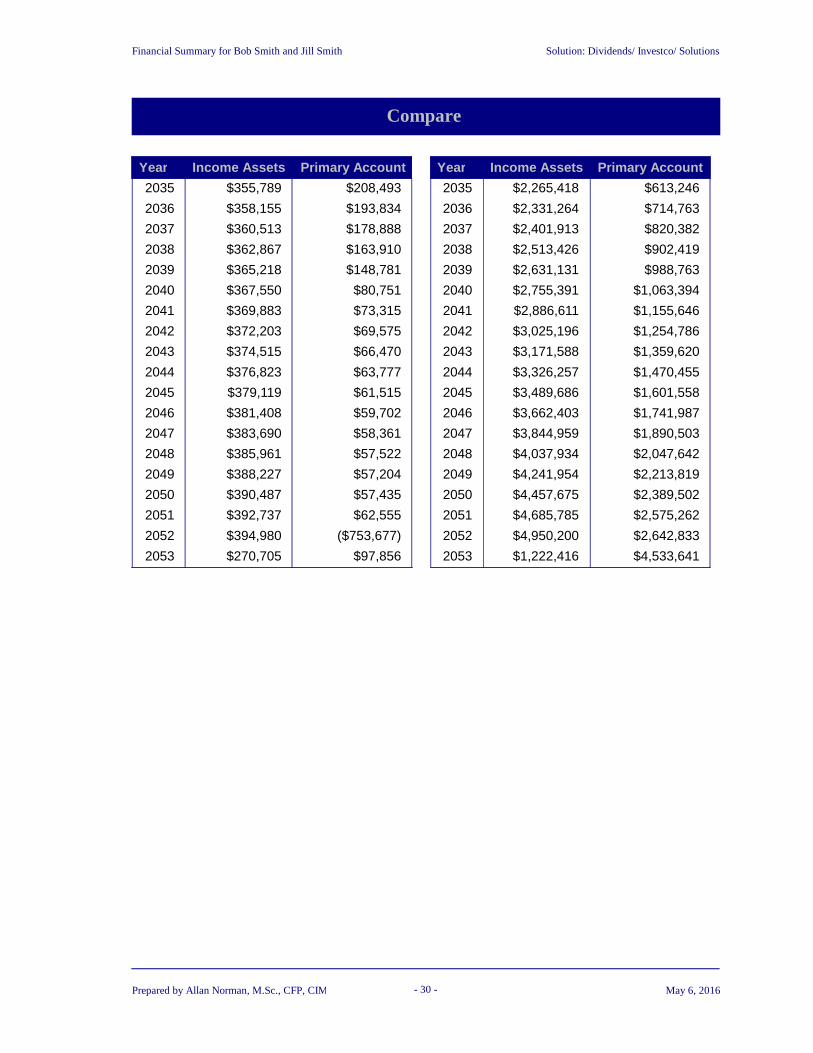

Solution: Dividends/ Investco/ Solutions

Compare

Financial Summary for Bob Smith and Jill Smith

Year Income Assets Year Income AssetsPrimary Account Primary Account

2035 $355,789 2035 $2,265,418$208,493 $613,246

2036 $358,155 2036 $2,331,264$193,834 $714,763

2037 $360,513 2037 $2,401,913$178,888 $820,382

2038 $362,867 2038 $2,513,426$163,910 $902,419

2039 $365,218 2039 $2,631,131$148,781 $988,763

2040 $367,550 2040 $2,755,391$80,751 $1,063,394

2041 $369,883 2041 $2,886,611$73,315 $1,155,646

2042 $372,203 2042 $3,025,196$69,575 $1,254,786

2043 $374,515 2043 $3,171,588$66,470 $1,359,620

2044 $376,823 2044 $3,326,257$63,777 $1,470,455

2045 $379,119 2045 $3,489,686$61,515 $1,601,558

2046 $381,408 2046 $3,662,403$59,702 $1,741,987

2047 $383,690 2047 $3,844,959$58,361 $1,890,503

2048 $385,961 2048 $4,037,934$57,522 $2,047,642

2049 $388,227 2049 $4,241,954$57,204 $2,213,819

2050 $390,487 2050 $4,457,675$57,435 $2,389,502

2051 $392,737 2051 $4,685,785$62,555 $2,575,262

2052 $394,980 2052 $4,950,200($753,677) $2,642,833

2053 $270,705 2053 $1,222,416$97,856 $4,533,641

Prepared by Allan Norman, M.Sc., CFP, CIM - 30 - May 6, 2016

Solution: Dividends/ Investco/ Solutions

Compare

Financial Summary for Bob Smith and Jill Smith

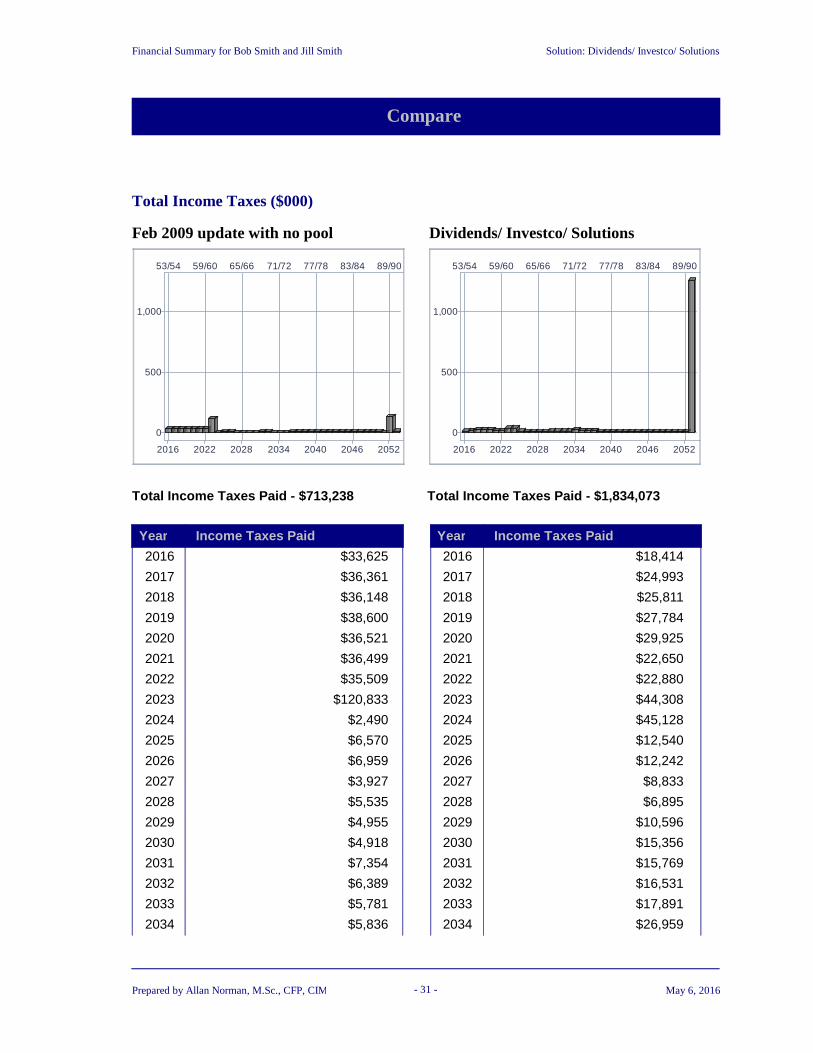

Total Income Taxes ($000)

Feb 2009 update with no pool Dividends/ Investco/ Solutions

0

500

1,000

2016 2022 2028 2034 2040 2046 2052

53/54 59/60 65/66 71/72 77/78 83/84 89/90

0

500

1,000

2016 2022 2028 2034 2040 2046 2052

53/54 59/60 65/66 71/72 77/78 83/84 89/90

Total Income Taxes Paid - $713,238 Total Income Taxes Paid - $1,834,073

Year Income Taxes Paid Year Income Taxes Paid

2016 $33,625 2016 $18,414

2017 $36,361 2017 $24,993

2018 $36,148 2018 $25,811

2019 $38,600 2019 $27,784

2020 $36,521 2020 $29,925

2021 $36,499 2021 $22,650

2022 $35,509 2022 $22,880

2023 $120,833 2023 $44,308

2024 $2,490 2024 $45,128

2025 $6,570 2025 $12,540

2026 $6,959 2026 $12,242

2027 $3,927 2027 $8,833

2028 $5,535 2028 $6,895

2029 $4,955 2029 $10,596

2030 $4,918 2030 $15,356

2031 $7,354 2031 $15,769

2032 $6,389 2032 $16,531

2033 $5,781 2033 $17,891

2034 $5,836 2034 $26,959

Prepared by Allan Norman, M.Sc., CFP, CIM - 31 - May 6, 2016

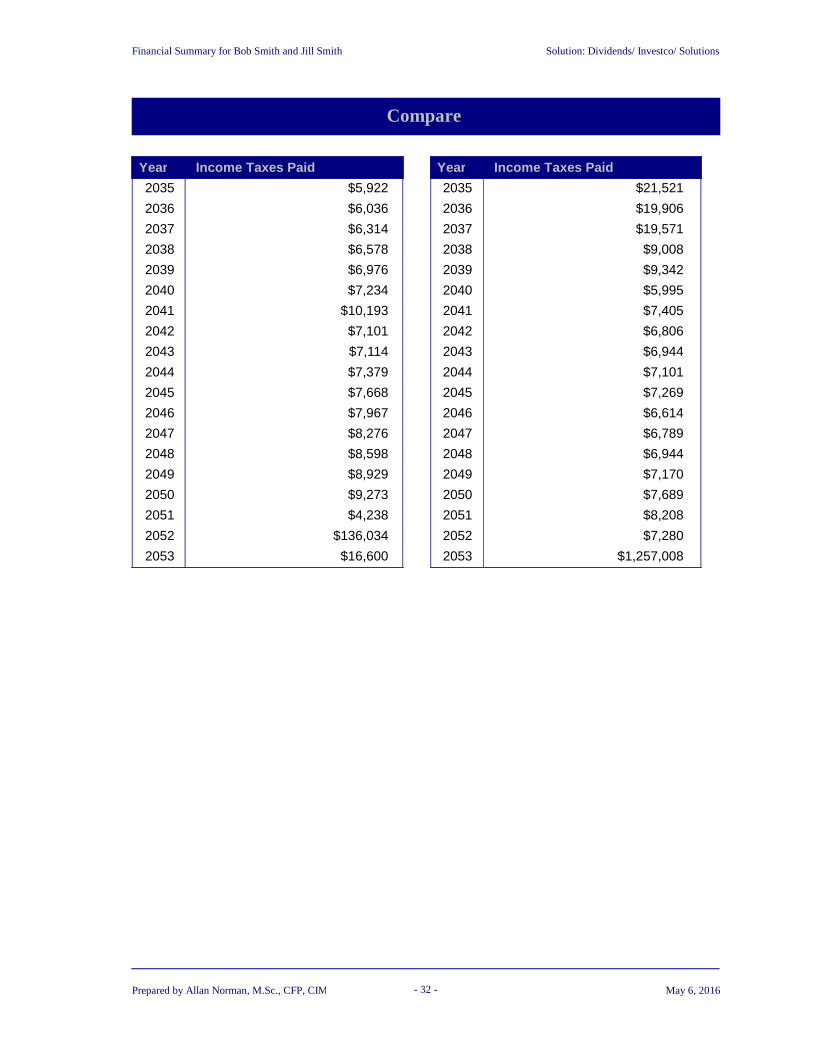

Solution: Dividends/ Investco/ Solutions

Compare

Financial Summary for Bob Smith and Jill Smith

Year Income Taxes Paid Year Income Taxes Paid

2035 $5,922 2035 $21,521

2036 $6,036 2036 $19,906

2037 $6,314 2037 $19,571

2038 $6,578 2038 $9,008

2039 $6,976 2039 $9,342

2040 $7,234 2040 $5,995

2041 $10,193 2041 $7,405

2042 $7,101 2042 $6,806

2043 $7,114 2043 $6,944

2044 $7,379 2044 $7,101

2045 $7,668 2045 $7,269

2046 $7,967 2046 $6,614

2047 $8,276 2047 $6,789

2048 $8,598 2048 $6,944

2049 $8,929 2049 $7,170

2050 $9,273 2050 $7,689

2051 $4,238 2051 $8,208

2052 $136,034 2052 $7,280

2053 $16,600 2053 $1,257,008

Prepared by Allan Norman, M.Sc., CFP, CIM - 32 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Private Company Dividends

Solution: Dividends/ Investco/ Solutions

INVESTCO

Part of your retirement income will be in the form of dividends as shown belowBob

2016Type / Class 2017 2018 2019 2020

Total Dividends Received

Common / A $0 $0 $0 $0 $0

2016Type / Class 2017 2018 2019 2020

Cash Payments

Common / A $0 $0 $0 $0 $0

CDA Dividends Ordinary Dividends Eligible Dividends

2050204520402035203020252020

30,000

25,000

20,000

15,000

10,000

5,000

0

Prepared by Allan Norman, M.Sc., CFP, CIM - 33 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Private Company Dividends

Solution: Dividends/ Investco/ Solutions

Jill

2016Type / Class 2017 2018 2019 2020

Total Dividends Received

Common / C $0 $0 $0 $0 $0

2016Type / Class 2017 2018 2019 2020

Cash Payments

Common / C $0 $0 $0 $0 $0

CDA Dividends Ordinary Dividends Eligible Dividends

2050204520402035203020252020

30,000

25,000

20,000

15,000

10,000

5,000

0

Prepared by Allan Norman, M.Sc., CFP, CIM - 34 - May 6, 2016

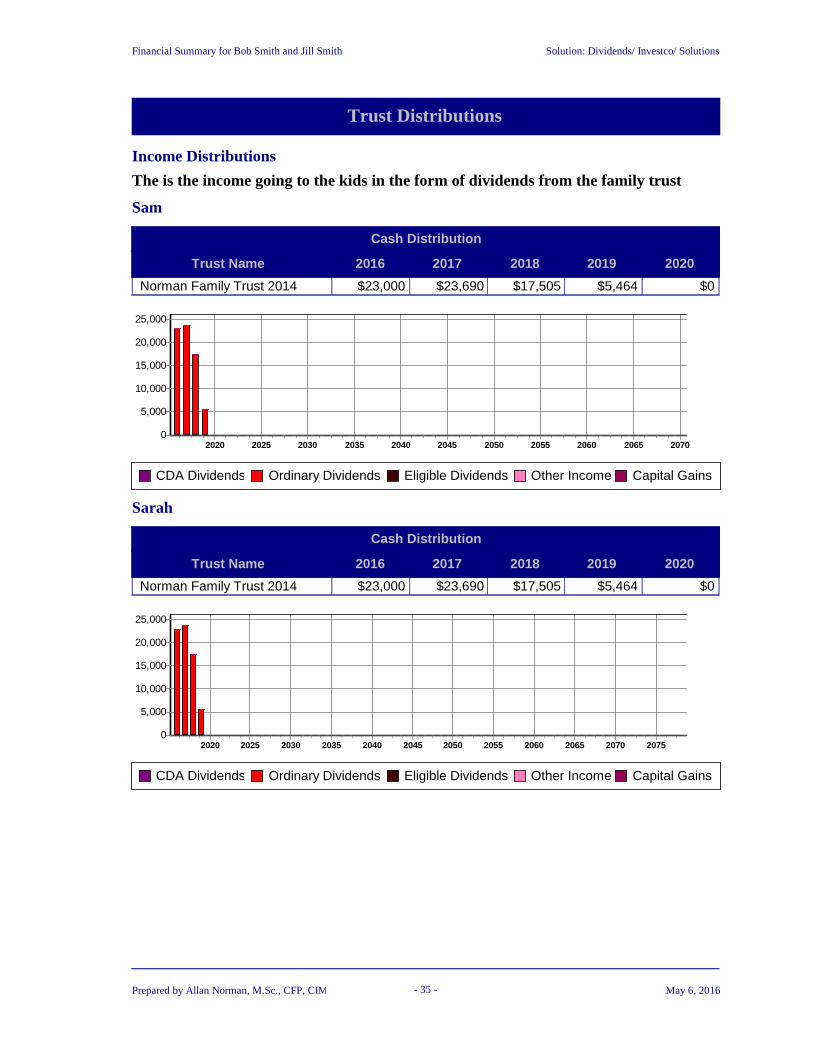

Financial Summary for Bob Smith and Jill Smith

Trust Distributions

Solution: Dividends/ Investco/ Solutions

Income Distributions

The is the income going to the kids in the form of dividends from the family trust

Sam

2016Trust Name 2017 2018 2019 2020

Cash Distribution

Norman Family Trust 2014 $23,000 $23,690 $17,505 $5,464 $0

20702065206020552050204520402035203020252020

25,000

20,000

15,000

10,000

5,000

0

CDA Dividends Ordinary Dividends Eligible Dividends Other Income Capital Gains

Sarah

2016Trust Name 2017 2018 2019 2020

Cash Distribution

Norman Family Trust 2014 $23,000 $23,690 $17,505 $5,464 $0

207520702065206020552050204520402035203020252020

25,000

20,000

15,000

10,000

5,000

0

CDA Dividends Ordinary Dividends Eligible Dividends Other Income Capital Gains

Prepared by Allan Norman, M.Sc., CFP, CIM - 35 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Net Cash Flow Forecast

Solution: Dividends/ Investco/ Solutions

Cash Sources and Cash Uses

To understand your annual savings target, you must analyze your net cash flow by dividing it into two parts - cash sources and cash uses. Years of negative savings need not be a concern as long as your forecasted income assets are positive throughout your expected lifetime. For detail, refer to the Income Assets Forecast section.

The graphs below show your forecasted cash sources and cash uses over your expected lifetime. The related table shows ten-year targets. The tables that follow display details for the next three years and then every five years.

Prepared by Allan Norman, M.Sc., CFP, CIM - 36 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Net Cash Flow Forecast

Solution: Dividends/ Investco/ Solutions

Cash Sources Stacked Bar Graph (Actual / Inflated Dollars, $000)

Debt PrincipalOther SalesInsuranceOther IncomePrivate CompaniesRRSPs / Pension PlansGovernment BenefitsNon-Reg. PortfoliosCareer

2050204520402035203020252020

230

220

210

200

190

180

170

160

150

140

130

120

110

100

90

80

70

60

50

40

30

20

10

0

Prepared by Allan Norman, M.Sc., CFP, CIM - 37 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Net Cash Flow Forecast

Solution: Dividends/ Investco/ Solutions

Cash Sources Stacked Bar Graph (Today's / Constant Dollars, $000)

Debt PrincipalOther SalesInsuranceOther IncomePrivate CompaniesRRSPs / Pension PlansGovernment BenefitsNon-Reg. PortfoliosCareer

2050204520402035203020252020

240

230

220

210

200

190

180

170

160

150

140

130

120

110

100

90

80

70

60

50

40

30

20

10

0

Prepared by Allan Norman, M.Sc., CFP, CIM - 38 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Net Cash Flow Forecast

Solution: Dividends/ Investco/ Solutions

Cash Uses Stacked Bar Graph (Actual / Inflated Dollars, $000)

Spouse's Income TaxesIncome TaxesDebt PaymentsInsuranceRRSPs / Pension PlansOther Accounts/PlansCareerLifestyle ExpensesHomes

2050204520402035203020252020

190

180

170

160

150

140

130

120

110

100

90

80

70

60

50

40

30

20

10

0

Prepared by Allan Norman, M.Sc., CFP, CIM - 39 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Net Cash Flow Forecast

Solution: Dividends/ Investco/ Solutions

Cash Uses Stacked Bar Graph (Today's / Constant Dollars, $000)

Spouse's Income TaxesIncome TaxesDebt PaymentsInsuranceRRSPs / Pension PlansOther Accounts/PlansCareerLifestyle ExpensesHomes

2050204520402035203020252020

190

180

170

160

150

140

130

120

110

100

90

80

70

60

50

40

30

20

10

0

Prepared by Allan Norman, M.Sc., CFP, CIM - 40 - May 6, 2016

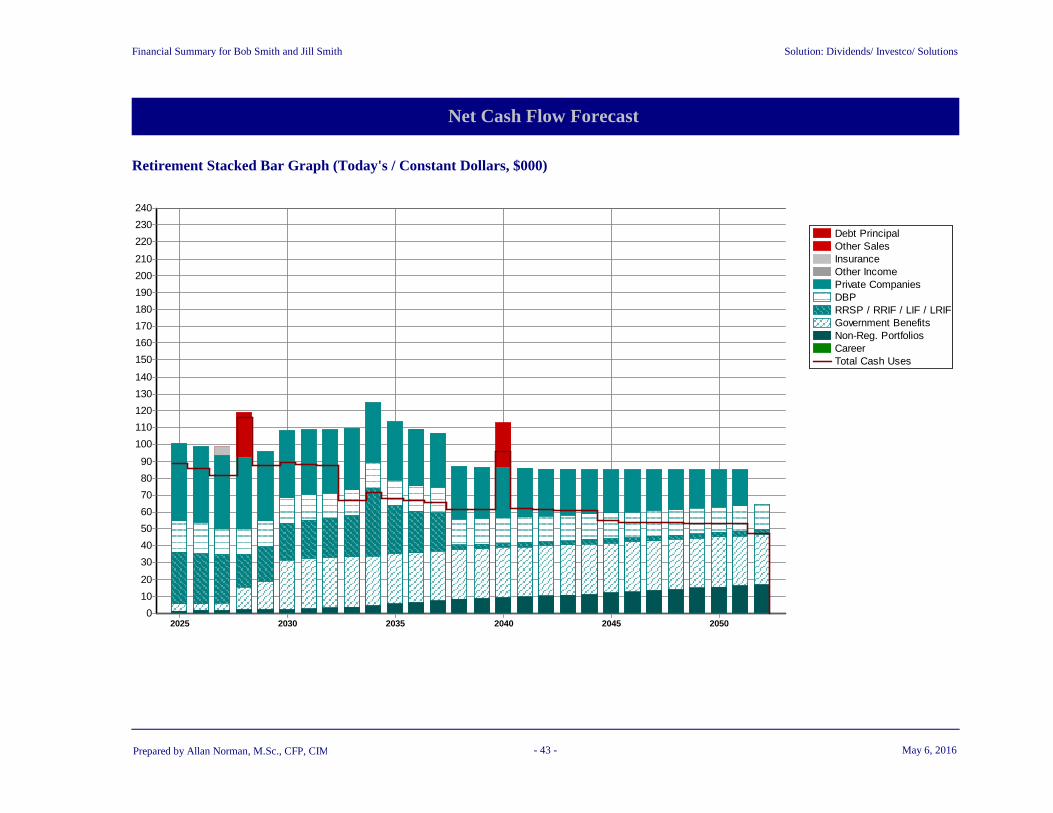

Financial Summary for Bob Smith and Jill Smith Solution: Dividends/ Investco/ Solutions

Net Cash Flow Forecast

Retirement Sources and Uses

During retirement, net cash flow includes cash sources such as from government plans that are not available at other times in your life. Your retirement years may also be a time of deficits (cash uses exceed cash sources) that may cause a decline in the value of your income assets. Should they become negative, you will have to sell your possessions.

The table below shows your forecasted cash sources and uses during your retirement years and is based on your expected lifetime.

Prepared by Allan Norman, M.Sc., CFP, CIM - 41 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith Solution: Dividends/ Investco/ Solutions

Net Cash Flow Forecast

Retirement Stacked Bar Graph (Actual / Inflated Dollars, $000)

Debt PrincipalOther SalesInsuranceOther IncomePrivate CompaniesDBPRRSP / RRIF / LIF / LRIFGovernment BenefitsNon-Reg. PortfoliosCareerTotal Cash Uses

205020452040203520302025

240

230

220

210

200

190

180

170

160

150

140

130

120

110

100

90

80

70

60

50

40

30

20

10

0

Prepared by Allan Norman, M.Sc., CFP, CIM - 42 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith Solution: Dividends/ Investco/ Solutions

Net Cash Flow Forecast

Retirement Stacked Bar Graph (Today's / Constant Dollars, $000)

Debt PrincipalOther SalesInsuranceOther IncomePrivate CompaniesDBPRRSP / RRIF / LIF / LRIFGovernment BenefitsNon-Reg. PortfoliosCareerTotal Cash Uses

205020452040203520302025

240

230

220

210

200

190

180

170

160

150

140

130

120

110

100

90

80

70

60

50

40

30

20

10

0

Prepared by Allan Norman, M.Sc., CFP, CIM - 43 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Net Cash Flow Forecast

Solution: Dividends/ Investco/ Solutions

OAS, CPP / QPP, GIS

Note: There is no OAS clawback until the final year

Bob

OAS / GIS

Year Adjusted Benefit Clawback Net BenefitBenefit GIS Benefit

$10,3552030 $10,859 $0 $10,859 $0$10,6662031 $12,202 $0 $12,202 $0$10,9862032 $12,568 $0 $12,568 $0$11,3152033 $12,945 $0 $12,945 $0$11,6552034 $13,333 $0 $13,333 $0$12,0052035 $13,733 $0 $13,733 $0$12,3652036 $14,145 $0 $14,145 $0$12,7362037 $14,569 $0 $14,569 $0$13,1182038 $15,007 $0 $15,007 $0$13,5112039 $15,457 $0 $15,457 $0$13,9172040 $15,920 $0 $15,920 $0$14,3342041 $16,398 $0 $16,398 $0$14,7642042 $16,890 $0 $16,890 $0$15,2072043 $17,397 $0 $17,397 $0$15,6632044 $17,919 $0 $17,919 $0$16,1332045 $18,456 $0 $18,456 $0$16,6172046 $19,010 $0 $19,010 $0$17,1162047 $19,580 $0 $19,580 $0$17,6292048 $20,168 $0 $20,168 $0$18,1582049 $20,773 $0 $20,773 $0$18,7032050 $21,396 $0 $21,396 $0$19,2642051 $22,038 $0 $22,038 $0$19,8422052 $22,699 $0 $22,699 $0$20,4372053 $23,380 $23,380 $0 $0

Prepared by Allan Norman, M.Sc., CFP, CIM - 44 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Net Cash Flow Forecast

Solution: Dividends/ Investco/ Solutions

CPP / QPP

Year Additional Contributions Adjusted BenefitBenefit

$13,9302028 $0 $9,078

$14,3482029 $0 $10,200

$14,7782030 $0 $10,506

$15,2212031 $0 $10,822

$15,6782032 $0 $11,146

$16,1482033 $0 $11,481

$16,6332034 $0 $11,825

$17,1322035 $0 $12,180

$17,6462036 $0 $12,545

$18,1752037 $0 $12,922

$18,7202038 $0 $13,309

$19,2822039 $0 $13,709

$19,8602040 $0 $14,120

$20,4562041 $0 $14,543

$21,0702042 $0 $14,980

$21,7022043 $0 $15,429

$22,3532044 $0 $15,892

$23,0242045 $0 $16,369

$23,7142046 $0 $16,860

$24,4262047 $0 $17,366

$25,1592048 $0 $17,887

$25,9132049 $0 $18,423

$26,6912050 $0 $18,976

$27,4912051 $0 $19,545

$28,3162052 $0 $20,131

$29,1662053 $0 $39,136

Prepared by Allan Norman, M.Sc., CFP, CIM - 45 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Net Cash Flow Forecast

Solution: Dividends/ Investco/ Solutions

Jill

OAS / GIS

Year Adjusted Benefit Clawback Net BenefitBenefit GIS Benefit

$10,0542029 $3,834 $0 $3,834 $0$10,3552030 $11,846 $0 $11,846 $0$10,6662031 $12,202 $0 $12,202 $0$10,9862032 $12,568 $0 $12,568 $0$11,3152033 $12,945 $0 $12,945 $0$11,6552034 $13,333 $0 $13,333 $0$12,0052035 $13,733 $0 $13,733 $0$12,3652036 $14,145 $0 $14,145 $0$12,7362037 $14,569 $0 $14,569 $0$13,1182038 $15,007 $0 $15,007 $0$13,5112039 $15,457 $0 $15,457 $0$13,9172040 $15,920 $0 $15,920 $0$14,3342041 $16,398 $0 $16,398 $0$14,7642042 $16,890 $0 $16,890 $0$15,2072043 $17,397 $0 $17,397 $0$15,6632044 $17,919 $0 $17,919 $0$16,1332045 $18,456 $0 $18,456 $0$16,6172046 $19,010 $0 $19,010 $0$17,1162047 $19,580 $0 $19,580 $0$17,6292048 $20,168 $0 $20,168 $0$18,1582049 $20,773 $0 $20,773 $0$18,7032050 $21,396 $0 $21,396 $0$19,2642051 $22,038 $0 $22,038 $0$19,8422052 $22,699 $0 $22,699 $0

Prepared by Allan Norman, M.Sc., CFP, CIM - 46 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Net Cash Flow Forecast

Solution: Dividends/ Investco/ Solutions

CPP / QPP

Year Additional Contributions Adjusted BenefitBenefit

$7,6902022 $0 $1,640

$7,9202023 $0 $5,069

$8,1582024 $0 $5,221

$8,4032025 $0 $5,378

$8,6552026 $0 $5,539

$8,9142027 $0 $5,705

$9,1822028 $0 $9,903

$9,4572029 $0 $10,200

$9,7412030 $0 $10,506

$10,0332031 $0 $10,822

$10,3342032 $0 $11,146

$10,6442033 $0 $11,481

$10,9642034 $0 $11,825

$11,2932035 $0 $12,180

$11,6312036 $0 $12,545

$11,9802037 $0 $12,922

$12,3402038 $0 $13,309

$12,7102039 $0 $13,709

$13,0912040 $0 $14,120

$13,4842041 $0 $14,543

$13,8882042 $0 $14,980

$14,3052043 $0 $15,429

$14,7342044 $0 $15,892

$15,1762045 $0 $16,369

$15,6322046 $0 $16,860

$16,1012047 $0 $17,366

$16,5842048 $0 $17,887

$17,0812049 $0 $18,423

$17,5932050 $0 $18,976

$18,1212051 $0 $19,545

$18,6652052 $0 $20,131

Prepared by Allan Norman, M.Sc., CFP, CIM - 47 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Net Cash Flow Forecast

Solution: Dividends/ Investco/ Solutions

Total

YearSources

AgeUses

OAS/CPP Pensions Portfolios Other

Surplus/ Income(Deficit) Assets

Retirement Sources and Uses (Actual / Inflated Dollars)

2025 62/63 5,378 64,040 1,916 60,000 115,679 15,654 1,796,9622026 63/64 5,539 64,761 2,297 60,000 115,256 17,342 1,856,9952027 64/65 5,705 60,867 2,727 67,400 113,432 23,267 1,937,7202028 65/66 18,981 49,290 3,289 98,408 165,275 4,693 2,013,3862029 66/67 24,234 52,962 3,514 60,000 128,365 12,345 2,096,4272030 67/68 43,717 55,993 3,896 60,000 135,253 28,353 2,197,2152031 68/69 46,048 58,793 4,604 60,000 137,858 31,586 2,303,9642032 69/70 47,428 61,664 5,404 60,000 140,878 33,617 2,415,6982033 70/71 48,852 66,000 6,276 60,000 110,771 70,357 2,565,9122034 71/72 50,316 93,766 7,896 60,000 122,234 89,744 2,715,4132035 72/73 51,826 76,743 9,958 60,000 119,263 79,264 2,878,6632036 73/74 53,380 71,530 11,900 60,000 120,188 76,623 3,046,0272037 74/75 54,982 70,221 13,870 60,000 122,470 76,603 3,222,2942038 75/76 56,632 34,028 15,920 60,000 117,846 48,734 3,415,8452039 76/77 58,332 35,045 17,511 60,000 121,178 49,710 3,619,8942040 77/78 60,080 36,108 19,187 114,514 195,396 34,492 3,818,7852041 78/79 61,882 37,187 20,635 60,000 130,621 49,084 4,042,2562042 79/80 63,740 38,305 22,425 60,001 132,244 52,227 4,279,9822043 80/81 65,652 39,458 24,349 60,000 135,563 53,896 4,531,2082044 81/82 67,622 40,639 26,383 60,000 139,004 55,641 4,796,7122045 82/83 69,650 41,865 28,534 60,000 128,640 71,409 5,091,2432046 83/84 71,740 43,123 31,078 60,000 130,527 75,414 5,404,3902047 84/85 73,892 44,417 33,803 60,001 134,312 77,800 5,735,4632048 85/86 76,110 45,757 36,685 60,000 138,159 80,393 6,085,5762049 86/87 78,392 47,131 39,734 60,000 142,204 83,054 6,455,7742050 87/88 80,744 48,548 42,959 60,000 146,439 85,812 6,847,1772051 88/89 83,166 50,013 46,368 60,000 150,789 88,758 7,261,0472052 89/90 85,660 51,522 49,973 868 137,380 50,644 7,593,0322053 90/91 41,636 27,001 49,786 2,152,465 1,359,482 911,406 5,756,057

Prepared by Allan Norman, M.Sc., CFP, CIM - 48 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Net Cash Flow Forecast

Solution: Dividends/ Investco/ Solutions

Total

YearSources

AgeUses

OAS/CPP Pensions Portfolios Other

Surplus/ Income(Deficit) Assets

Retirement Sources and Uses (Today's / Constant Dollars)

2025 62/63 4,122 49,081 1,468 45,985 88,658 11,998 1,377,2222026 63/64 4,122 48,188 1,709 44,646 85,761 12,904 1,381,7792027 64/65 4,121 43,972 1,970 48,691 81,946 16,808 1,399,8502028 65/66 13,313 34,571 2,307 69,021 115,921 3,291 1,412,1482029 66/67 16,502 36,065 2,393 40,857 87,410 8,406 1,427,5652030 67/68 28,902 37,018 2,576 39,667 89,418 18,745 1,452,6182031 68/69 29,556 37,737 2,955 38,512 88,486 20,274 1,478,8272032 69/70 29,556 38,427 3,368 37,390 87,791 20,949 1,505,3832033 70/71 29,556 39,931 3,797 36,301 67,018 42,567 1,552,4192034 71/72 29,555 55,078 4,638 35,244 71,799 52,715 1,595,0192035 72/73 29,556 43,765 5,679 34,217 68,014 45,203 1,641,6612036 73/74 29,555 39,604 6,589 33,221 66,545 42,424 1,686,5112037 74/75 29,556 37,747 7,456 32,253 65,834 41,178 1,732,1422038 75/76 29,556 17,759 8,308 31,314 61,503 25,434 1,782,7042039 76/77 29,556 17,757 8,873 30,401 61,400 25,188 1,834,1702040 77/78 29,555 17,763 9,439 56,333 96,122 16,968 1,878,5892041 78/79 29,555 17,761 9,855 28,656 62,385 23,443 1,930,6042042 79/80 29,556 17,762 10,398 27,822 61,321 24,217 1,984,6052043 80/81 29,556 17,764 10,962 27,011 61,029 24,263 2,039,9002044 81/82 29,556 17,762 11,532 26,225 60,755 24,319 2,096,5312045 82/83 29,556 17,765 12,108 25,461 54,588 30,302 2,160,4512046 83/84 29,556 17,766 12,804 24,719 53,775 31,070 2,226,5372047 84/85 29,556 17,766 13,521 23,999 53,723 31,119 2,294,1112048 85/86 29,556 17,769 14,246 23,300 53,652 31,220 2,363,2552049 86/87 29,556 17,770 14,981 22,621 53,615 31,313 2,433,9962050 87/88 29,556 17,771 15,725 21,963 53,603 31,411 2,506,3742051 88/89 29,556 17,774 16,479 21,323 53,588 31,543 2,580,4562052 89/90 29,555 17,777 17,242 300 47,400 17,474 2,619,8422053 90/91 13,947 9,045 16,677 721,039 455,403 305,305 1,928,181

Prepared by Allan Norman, M.Sc., CFP, CIM - 49 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Net Worth Forecast

Net Worth Forecast

Solution: Dividends/ Investco/ Solutions

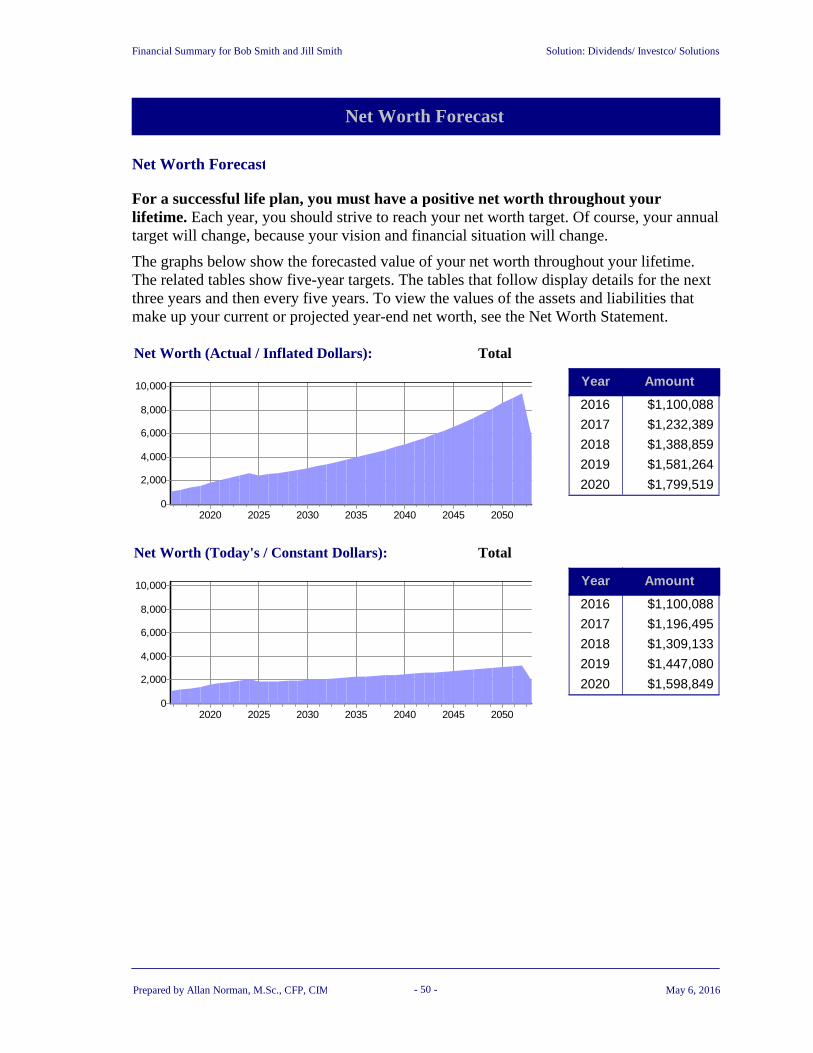

For a successful life plan, you must have a positive net worth throughout your lifetime. Each year, you should strive to reach your net worth target. Of course, your annual target will change, because your vision and financial situation will change.

The graphs below show the forecasted value of your net worth throughout your lifetime. The related tables show five-year targets. The tables that follow display details for the next three years and then every five years. To view the values of the assets and liabilities that make up your current or projected year-end net worth, see the Net Worth Statement.

TotalNet Worth (Actual / Inflated Dollars):

2050204520402035203020252020

10,000

8,000

6,000

4,000

2,000

0

Year Amount

2016 $1,100,088

2017 $1,232,389

2018 $1,388,859

2019 $1,581,264

2020 $1,799,519

TotalNet Worth (Today's / Constant Dollars):

2050204520402035203020252020

10,000

8,000

6,000

4,000

2,000

0

Year Amount

2016 $1,100,088

2017 $1,196,495

2018 $1,309,133

2019 $1,447,080

2020 $1,598,849

Prepared by Allan Norman, M.Sc., CFP, CIM - 50 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

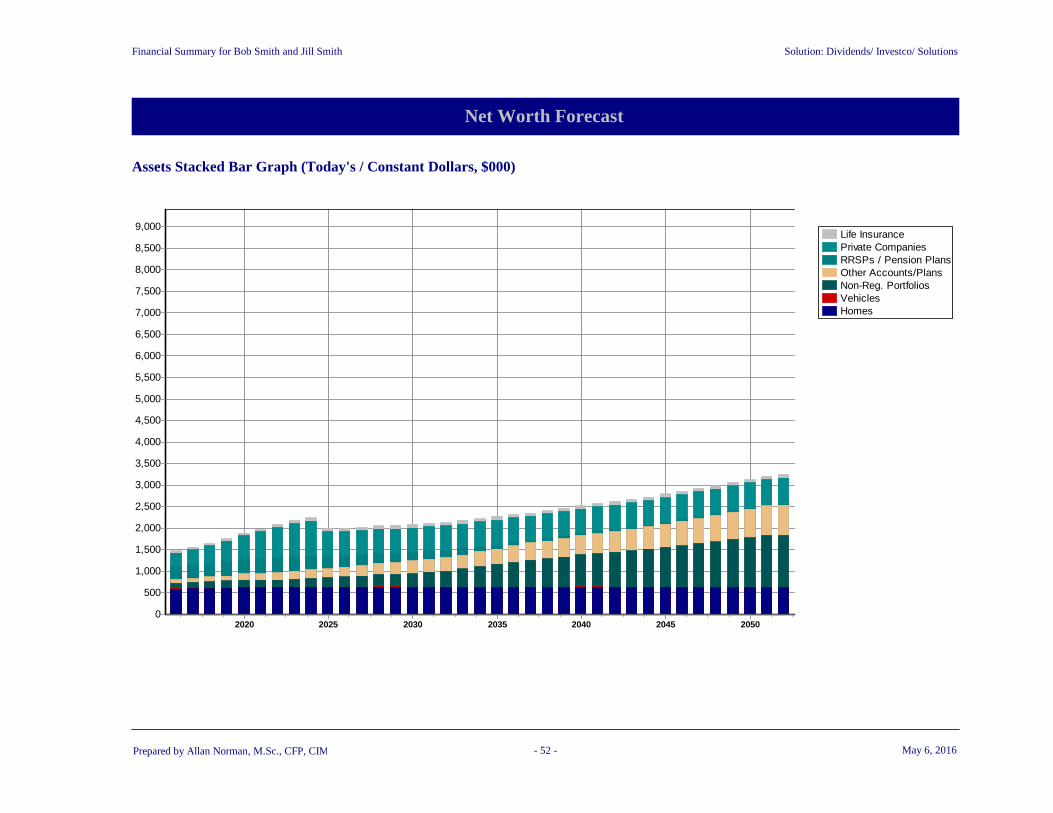

Net Worth Forecast

Solution: Dividends/ Investco/ Solutions

Assets Stacked Bar Graph (Actual / Inflated Dollars, $000)

Life InsurancePrivate CompaniesRRSPs / Pension PlansOther Accounts/PlansNon-Reg. PortfoliosVehiclesHomes

2050204520402035203020252020

9,000

8,500

8,000

7,500

7,000

6,500

6,000

5,500

5,000

4,500

4,000

3,500

3,000

2,500

2,000

1,500

1,000

500

0

Prepared by Allan Norman, M.Sc., CFP, CIM - 51 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Net Worth Forecast

Solution: Dividends/ Investco/ Solutions

Assets Stacked Bar Graph (Today's / Constant Dollars, $000)

Life InsurancePrivate CompaniesRRSPs / Pension PlansOther Accounts/PlansNon-Reg. PortfoliosVehiclesHomes

2050204520402035203020252020

9,000

8,500

8,000

7,500

7,000

6,500

6,000

5,500

5,000

4,500

4,000

3,500

3,000

2,500

2,000

1,500

1,000

500

0

Prepared by Allan Norman, M.Sc., CFP, CIM - 52 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Net Worth Forecast

Solution: Dividends/ Investco/ Solutions

OtherVehiclesHomes

2050204520402035203020252020

380

360

340

320

300

280

260

240

220

200

180

160

140

120

100

80

60

40

20

0

Liabilities Stacked Bar Graph

Prepared by Allan Norman, M.Sc., CFP, CIM - 53 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

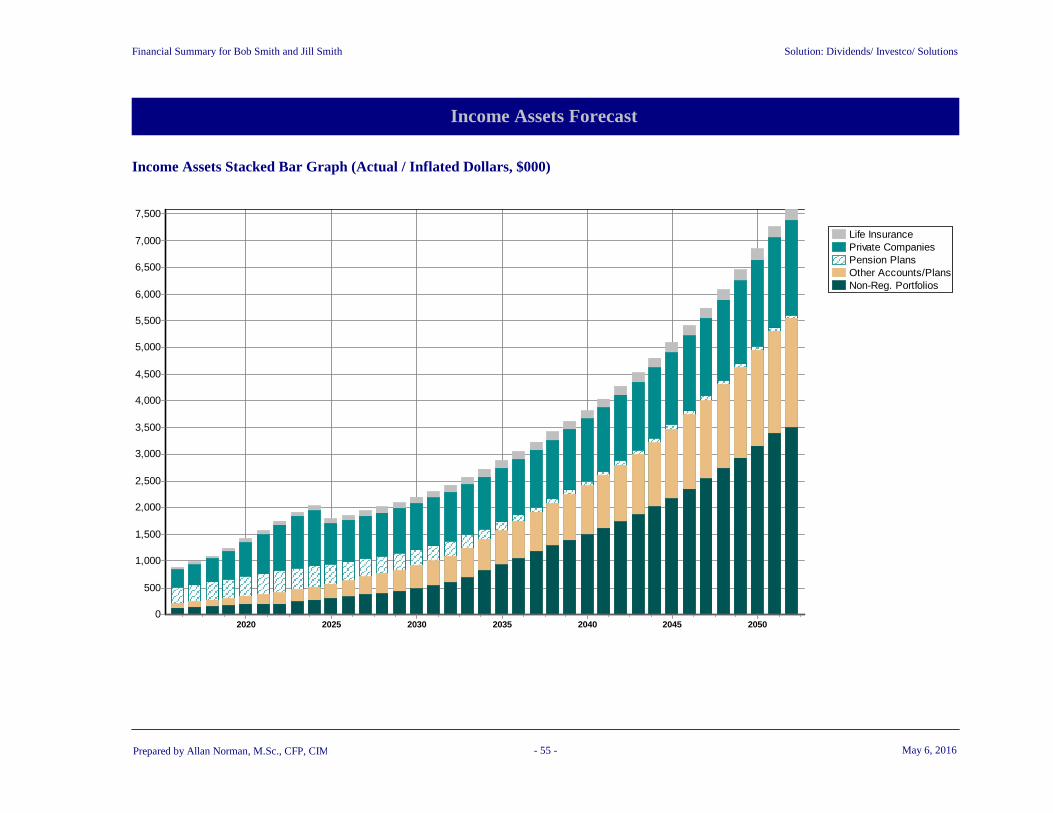

Income Assets Forecast

Income Assets Forecast

Solution: Dividends/ Investco/ Solutions

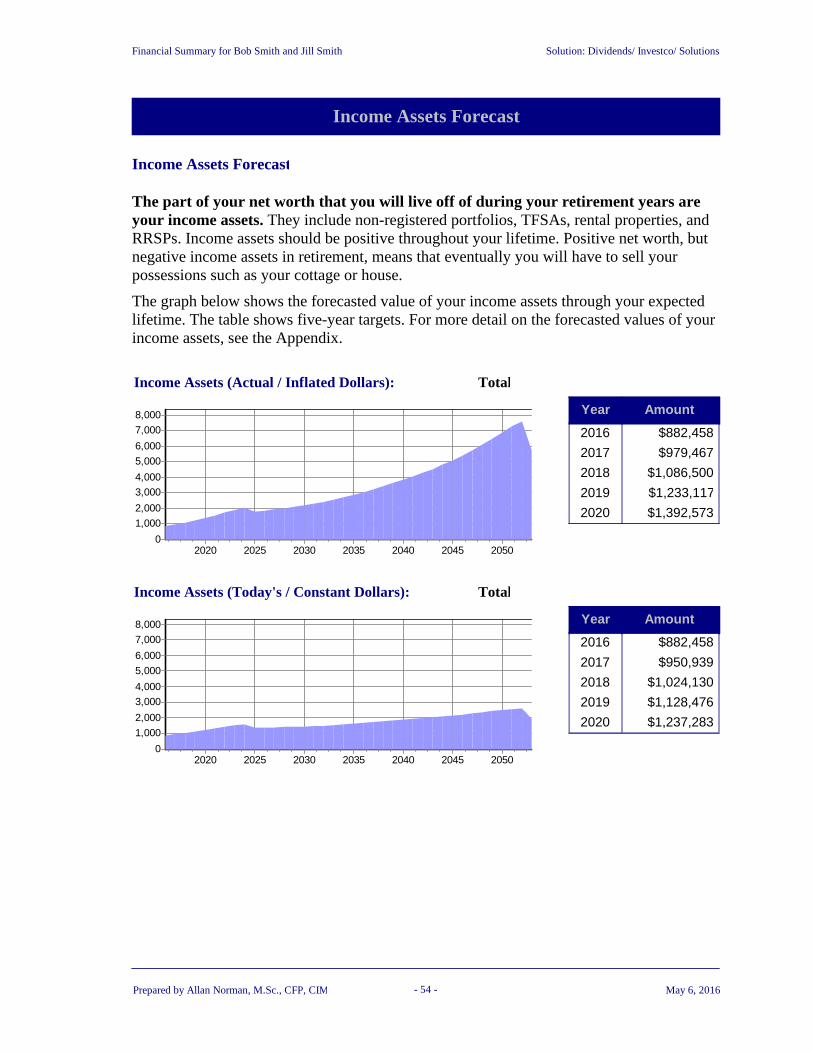

The part of your net worth that you will live off of during your retirement years are your income assets. They include non-registered portfolios, TFSAs, rental properties, and RRSPs. Income assets should be positive throughout your lifetime. Positive net worth, but negative income assets in retirement, means that eventually you will have to sell your possessions such as your cottage or house.

The graph below shows the forecasted value of your income assets through your expected lifetime. The table shows five-year targets. For more detail on the forecasted values of your income assets, see the Appendix.

TotalIncome Assets (Actual / Inflated Dollars):

2050204520402035203020252020

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

0

Year Amount

2016 $882,458

2017 $979,467

2018 $1,086,500

2019 $1,233,117

2020 $1,392,573

TotalIncome Assets (Today's / Constant Dollars):

2050204520402035203020252020

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

0

Year Amount

2016 $882,458

2017 $950,939

2018 $1,024,130

2019 $1,128,476

2020 $1,237,283

Prepared by Allan Norman, M.Sc., CFP, CIM - 54 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Income Assets Forecast

Solution: Dividends/ Investco/ Solutions

Income Assets Stacked Bar Graph (Actual / Inflated Dollars, $000)

Life InsurancePrivate CompaniesPension PlansOther Accounts/PlansNon-Reg. Portfolios

2050204520402035203020252020

7,500

7,000

6,500

6,000

5,500

5,000

4,500

4,000

3,500

3,000

2,500

2,000

1,500

1,000

500

0

Prepared by Allan Norman, M.Sc., CFP, CIM - 55 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Income Assets Forecast

Solution: Dividends/ Investco/ Solutions

Income Assets Stacked Bar Graph (Today's / Constant Dollars, $000)

Life InsurancePrivate CompaniesPension PlansOther Accounts/PlansNon-Reg. Portfolios

2050204520402035203020252020

7,500

7,000

6,500

6,000

5,500

5,000

4,500

4,000

3,500

3,000

2,500

2,000

1,500

1,000

500

0

Prepared by Allan Norman, M.Sc., CFP, CIM - 56 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Beneficiaries

Will

Solution: Dividends/ Investco/ Solutions

Your Will is a vital part of your plan. After the payment of your final expenses such as income taxes, your beneficiaries receive designated dollar amounts and specific assets. The residue of your estate is then distributed. Because the exact amount of the residue is unknown now, it is distributed by percentages.

The tables below summarize the terms of your Will.

Bob JillExpense

Expenses

Funeral and Other Expenses $44,778 $43,474

Legal and Accounting Fees $0 $0

Executor Compensation $0 $0

Spousal Equalization Payment $0 $0

Support Payments $0 $0

Trustee Fees $0 $0

Total $44,778 $43,474

Bob JillAsset

Beneficiary BeneficiaryPercent Percent

Asset Beneficiaries

EstateEstate 100 1002013 Car

BobJill 100 1002015 Car

EstateJill 100 100INVESTCO: Common A

BobEstate 100 100INVESTCO: Common C

BobJill 100 100Our house

Jill 100Tax-Free C.I. - RBC

Dollar

Bob JillBeneficiary

DollarPercent Percent

Dollar and Percent Beneficiaries

Bob 100

Jill 100

$0Total 100 $0 100

Prepared by Allan Norman, M.Sc., CFP, CIM - 57 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Beneficiaries

Other Beneficiary Designations

Solution: Dividends/ Investco/ Solutions

Naming the beneficiaries of your TFSAs, DPSPs, annuities, life insurance policies, and registered pension plans is also an important part of creating an estate plan.

Bob JillAsset

Beneficiary BeneficiaryPercent Percent

Asset Beneficiaries

Bob 100OPSU

Bob 100RRSP - Atlantis

Jill 100RRSP

Jill 100TFSA

Bob 100TFSA

Bob JillLife Insurance Policy

Beneficiary BeneficiaryPercent Percent

Life Insurance Beneficiaries

Jill 10010 yrt - Manulife

Bob 10010 yrt - Manulife

Jill 100Whole Life - Sun Life

Prepared by Allan Norman, M.Sc., CFP, CIM - 58 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Estate Summary

Forecasted Estate Value

Solution: Dividends/ Investco/ Solutions

Knowing how much your heirs should receive from your estate is part of your life plan. The Estate Value table below shows your beneficiaries and the amount that each will receive according to the terms of your Will. It also shows the beneficiaries that you named for registered plans, annuities, and life insurance policies. The amount shown is a forecast and is based on your expected lifetime. If you died today, the amount would vary.

If you die intestate (without a valid Will), the amount that each beneficiary is forecasted to receive is based on the intestacy laws of your province or territory of residence.

Estate Value: Bob

ComponentBeneficiaries

Sam Sarah

JTWROS Assets

$465,629 $465,629Assets Named In Will

Less Liabilities Transferred

Family Law Transfer

Dollar Allocation Received

50% 50%Percent Allocation Received

$2,209,273 $2,209,273

$35,883 $35,883Registered Plans, Annuities

Life Insurance Benefits

Total Received $2,710,784 $2,710,784

Name Amount

Estate Value Chart: Bob

Sam $2,710,784

Sarah $2,710,784

Prepared by Allan Norman, M.Sc., CFP, CIM - 59 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Estate Summary

Solution: Dividends/ Investco/ Solutions

Estate Value: Jill

ComponentBeneficiaries

Bob

JTWROS Assets

$902,233Assets Named In Will

Less Liabilities Transferred

Family Law Transfer

Dollar Allocation Received

100%Percent Allocation Received

$2,152,464

Total Received $4,141,460

Name Amount

Estate Value Chart: Jill

Bob $4,141,460

Prepared by Allan Norman, M.Sc., CFP, CIM - 60 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Estate Summary

Residue for Distribution

Solution: Dividends/ Investco/ Solutions

JillComponent Bob

$2,236,956Liquid Assets $5,790,649

$0Insurance Paid to Estate $0

$7,280Taxes Paid at Death $1,257,008

$0U.S. Estate Taxes $0

$33,717Estate Administration Taxes $68,005

$2,195,959After-Tax Residue Assets $4,465,636

$20Liabilities $2,312

$0Bequests and $ Allocations $0

$43,474Funeral and Other Expenses $44,778

$0Legal and Accounting Fees $0

$0Executor and Trustee Fees $0

$0Spousal Equalization / Support $0

$2,152,464Residue for Distribution $4,418,546

Prepared by Allan Norman, M.Sc., CFP, CIM - 61 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith Solution: Dividends/ Investco/ Solutions

Epilogue

Until one is committedthere is hesitancy, the chance to draw back,always ineffectiveness.Concerning all acts of initiative (and creation),there is one elementary truth,the ignorance of which kills countless ideasand splendid plans:that the moment one definitely commits oneself,then Providence moves too.All sorts of things occur to help onethat would never otherwise have occurred.A whole stream of events issues from the decision,raising in one's favour all mannerof unforseen incidents and meetingsand material assistance,which no man could have dreamtwould have come his way.

I have learned a deep respectfor one of Goethe's couplets:'Whatever you can do, or dream you can, begin it.Boldness has genius, power and magic in it.'

W.H. MurrayThe Scottish Himalayan ExpeditionJ. M. Dent & Sons Ltd., 1951.

Prepared by Allan Norman, M.Sc., CFP, CIM - 62 - May 6, 2016

Financial Summary for Bob Smith and Jill Smith

Appendix

General Assumptions

Solution: Dividends/ Investco/ Solutions

We have made the following assumptions:

a) Investments grow at 6%b) The home appreciates at 3%

General Assumptions

Inflation-Rate AssumptionCDN/U.S. Exchange-Rate Assumption

3%$1.33 CDN = $1.00 U.S.

Prepared by Allan Norman, M.Sc., CFP, CIM - A1 - May 6, 2016