financial planning & budgetary control - nhsggclibrary.nhsggc.org.uk/mediaassets/chp west...

TRANSCRIPT

COMMUNITY HEALTH AND CARE PARTNERSHIPS

Financial Planning & Budgetary Control

December 2008

COMMUNITY HEALTH & CARE PARTNERSHIPS

Financial Planning and Budgetary Control

Table of Contents

Section No Section Title

1 Introduction & Background

2 Audit Remit

3 Audit Opinion

4 Conclusions

5 Recommendations

6 Recommendation for Committee

7 Acknowledgements

Action Plan

8 Detailed Findings, Conclusions & Recommendations

Community Health & Care PartnershipsFinancial Planning and Budgetary Control

1. INTRODUCTION & BACKGROUND

The reliability of any organisation’s budgetary procedures is crucial to itssuccess. The budget represents a model of the intended activity for theorganisation and is an essential element of planning for the delivery ofservices and operational objectives.

Budgetary control is delegated to the Community Health Care Partnerships(CHCPs) which were established in 2006 involving Glasgow City Council(GCC) and NHS Greater Glasgow and Clyde (NHSGG&C). There are 5CHCPs within the GCC boundary and each manages a wide range ofcommunity based health and care services. The governance structure of theCHCPs is shown in the diagram below:

Each CHCP is responsible for managing resources within budgets delegatedfrom GCC and devolved from NHSGG&C, whose standing financialinstructions govern the CHCPs. The CHCP Committee itself is not a formaldecision making body of the Council. Financial information is held on twodifferent financial ledger systems: the NHSGG&C Cedar system and the GCCSAP system.

Since their inception in 2006, the five Glasgow CHCPs have been allocatedtotal funding of £1.75 billion, equating to approximately £481million from GCCand £1.27 billion from NHSGG&C. The table below outlines reported budgetvariances for each Glasgow CHCP (figures shown in brackets refer tooverspends).

CHCP COMMITTEECHCP COMMITTEE

Glasgow City CouncilSocial Work Services

Glasgow City CouncilSocial Work Services

NHS Greater Glasgowand Clyde

NHS Greater Glasgowand Clyde

Staff PartnershipForum

Staff PartnershipForum

Public PartnershipForum

Public PartnershipForum

Professional ExecutiveGroup

Professional ExecutiveGroup

CHCP ExecutiveTeam

CHCP ExecutiveTeamCHCP COMMITTEECHCP COMMITTEE

Glasgow City CouncilSocial Work Services

Glasgow City CouncilSocial Work Services

NHS Greater Glasgowand Clyde

NHS Greater Glasgowand Clyde

Staff PartnershipForum

Staff PartnershipForum

Public PartnershipForum

Public PartnershipForum

Professional ExecutiveGroup

Professional ExecutiveGroup

CHCP ExecutiveTeam

CHCP ExecutiveTeam

CHCP

2006/07 2007/08 2008/09 (as

at period 5)

Total

£m £m £m £m

North GCC (0.31) 0.05 (0.30) (0.56)

NHS 0.21 0.20 (0.02) 0.39

West GCC (0.12) (0.49) (0.47) (1.08)

NHS 0.72 0.48 0.00 1.20

East GCC (2.16) (0.45) (0.52) (3.13)

NHS 1.03 0.00 (0.13) 0.9

South East GCC (1.49) (0.94) (0.20) (2.63)

NHS 0.12 0.42 (0.11) 0.43

South West GCC (0.43) (0.91) (0.52) (1.86)

NHS 0.51 0.27 0.07 0.85

Total GCC (4.51) (2.74) (2.01) (9.26)

NHS 2.59 1.37 (0.19) 3.77

The table highlights that GCC has recorded adverse variances in almostevery CHCP in the last three years (cumulative overspend - £9.26 million).By contrast, NHSGG&C has recorded favourable budget results in almost allCHCPs over the last three years (cumulative underspend - £3.77 million)

The magnitude of the funding and the variances in budgetary performancehighlight the need for effective financial planning and robust budgetary controland monitoring within GCC and NHSGG&C, but more importantly within theCHCPs themselves.

2. AUDIT REMIT

GCC Internal Audit and PricewaterhouseCoopers LLP (PwC), the internalaudit provider for NHGGG&C, have agreed an approach and programme ofjoint working to audit CHCPs. This partnership approach is designed tomaximise efficiencies and ensure consistency and knowledge sharing in theinternal audit service provided to CHCPs.

Four reviews will be completed by GCC and PwC as part of the 2008/09Internal Audit Plan, with each focusing on two different CHCPs to ensure acomplete coverage over the year. Either GCC or PwC will act as lead auditoron each review.

This review was led by GCC and completed jointly with staff from both GCCand PwC. It was designed to examine the specific arrangements for financialplanning and budgetary control within North Glasgow and West GlasgowCHCPs.

The areas reviewed included:

the budget setting process, and the system for recording amendmentsand reconciling the annual budget;

approval of budgets and nomination of the budget holders by themanagement;

procedural instructions and financial training provided to budget holders; monitoring and reporting of the progress against the budget each

financial period; and scrutiny of the reported financial position undertaken by CHCP

management and partner bodies.

Specifically outwith the scope of this audit was a review of the operation of thefinancial systems of GCC and NHSGG&C, and the organisationalarrangements and financial responsibilities of both partner organisations.

3. AUDIT OPINION

Based on the fieldwork carried out only limited assurance could be gainedthat the funding provided by GCC and NHSGG&C was consistently managedand scrutinised by CHCPs.

Since the completion of the fieldwork, certain actions have already beentaken by management to improve these arrangements.

4. CONCLUSIONS

The key conclusions resulting from the audit can be summarised as follows:

Budget Setting

There is a formal sign-off process covering roles and responsibilities forthe management of GCC annual budgets which has not beenimplemented for CHCPs. There is no identical process for NHSGG&C;

The roles and responsibilities of the CHCPs are documented in variouspapers. Despite this the audit established that certain communicationproblems exist in terms of budget setting and budgetary controlresponsibilities, particularly between GCC and CHCPs;

The link between the detailed plans and budgets of GCC and NHSGG&Cto the CHCP detailed budgets should be more transparent; and

Officers within CHCPs have responsibility for delegated budgets from apartner organisation, which is not their employer. This raises difficultissues of accountability which have still to be resolved despite theexistence of CHCPs for almost 3 years.

Budget Monitoring

Monitoring takes place to compare actual financial results to budgets.However, there are different budget monitoring arrangements within theCHCPs in relation to the two Partnership organisations ranging fromgreater central direction from GCC to greater devolved responsibility fromNHSGG&C;

The NHSGG&C process appears to be more transparent and efficient.There appears to be a degree of breakdown in communication betweenthe CHCPs and GCC in relation to the requirements for budgetmonitoring, arrangements for processing adjustments and involvement inthe probable outturn exercise;

Since completion of the fieldwork, the Executive Director of FinancialServices, GCC now holds 4 weekly meetings with CHCP Directors andHeads of Finance and GCC staff to monitor and manage the GCCelement of CHCP budgets.

Financial Reporting

The scrutiny of financial information by CHCP Committees is notconsistent between the two CHCPs under review as evidenced from theminutes of North and West CHCPs.

Financial Training & Procedural Instruction

Financial training sessions were provided for CHCP staff but not allsenior executive management were present; and

There is a need for procedural instructions to be issued to budgetholders.

5. RECOMMENDATIONS

All of the above conclusions result in a need for action by all parties toimprove the quality of budget setting, budgetary control and scrutiny.

The audit work has resulted in 11 specific recommendations, 6 rated highpriority, and 5 medium priority.

The recommendations and management responses are contained in theAction Plan which follows. It is the responsibility of those charged withgovernance of the CHCPs to ensure that these recommendations areimplemented on time and in full.

The recommendations made are based upon the areas reviewed at the twoCHCPs and consideration should be given to the applicability of these mattersto all CHCPs.

6. RECOMMENDATION for COMMITTEE

It is recommended that the Head of Audit & Inspection (GCC) and ChiefInternal Auditor (NHSGG&C) submit a further report to the Audit Committeesof GCC and NHSGG&C, providing an update on the implementation of therecommendations contained in this report in due course.

7. ACKNOWLEDGEMENTS

We would like to thank all staff involved in this review for their co-operation,openness and assistance.

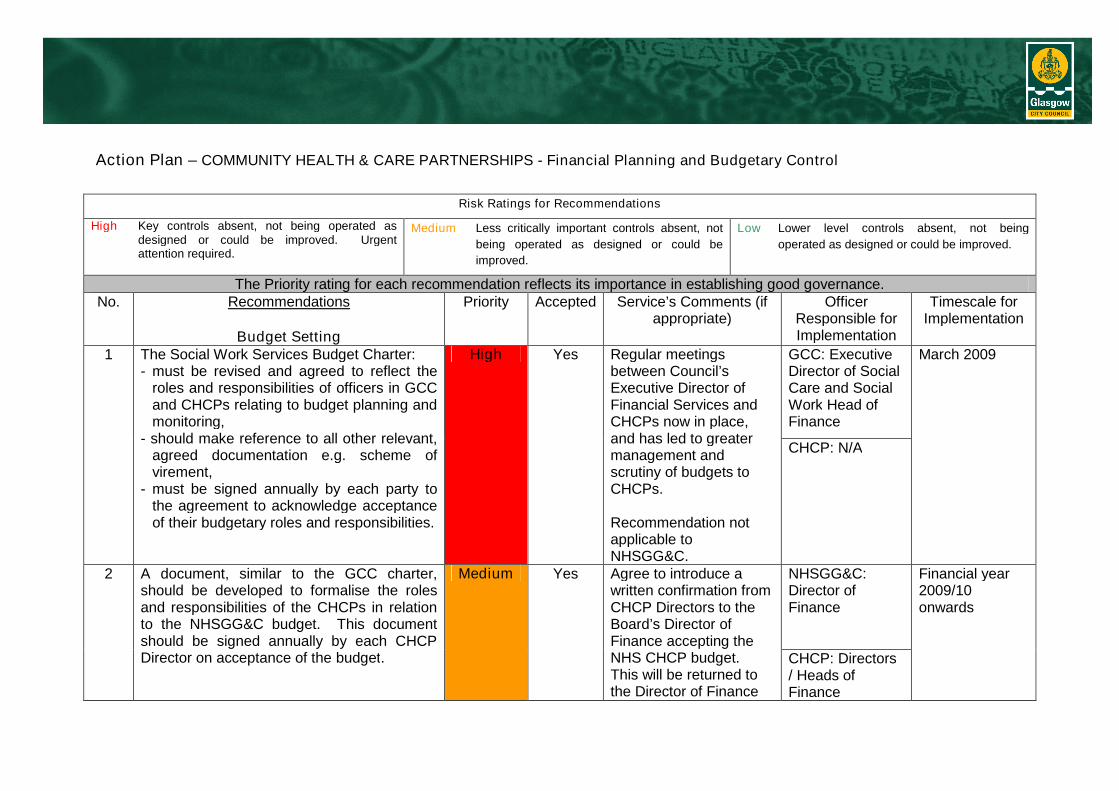

Action Plan – COMMUNITY HEALTH & CARE PARTNERSHIPS - Financial Planning and Budgetary Control

Risk Ratings for Recommendations

High Key controls absent, not being operated asdesigned or could be improved. Urgentattention required.

Medium Less critically important controls absent, not

being operated as designed or could be

improved.

Low Lower level controls absent, not being

operated as designed or could be improved.

The Priority rating for each recommendation reflects its importance in establishing good governance.No. Recommendations

Budget Setting

Priority Accepted Service’s Comments (ifappropriate)

OfficerResponsible forImplementation

Timescale forImplementation

GCC: ExecutiveDirector of SocialCare and SocialWork Head ofFinance

1 The Social Work Services Budget Charter:- must be revised and agreed to reflect the

roles and responsibilities of officers in GCCand CHCPs relating to budget planning andmonitoring,

- should make reference to all other relevant,agreed documentation e.g. scheme ofvirement,

- must be signed annually by each party tothe agreement to acknowledge acceptanceof their budgetary roles and responsibilities.

High Yes Regular meetingsbetween Council’sExecutive Director ofFinancial Services andCHCPs now in place,and has led to greatermanagement andscrutiny of budgets toCHCPs.

Recommendation notapplicable toNHSGG&C.

CHCP: N/A

March 2009

NHSGG&C:Director ofFinance

2 A document, similar to the GCC charter,should be developed to formalise the rolesand responsibilities of the CHCPs in relationto the NHSGG&C budget. This documentshould be signed annually by each CHCPDirector on acceptance of the budget.

Medium Yes Agree to introduce awritten confirmation fromCHCP Directors to theBoard’s Director ofFinance accepting theNHS CHCP budget.This will be returned tothe Director of Finance

CHCP: Directors/ Heads ofFinance

Financial year2009/10onwards

after the CHCP budgetapproved by CHCPCommittee in June ofeach year.

Recommendation notapplicable to GCC.

GCC: ChiefExecutive

3 GCC and NHSGG&C must concludeagreement on how to achieve accountabilityfor budget holders.

High Yes Discussions ongoingbetween GCC andNHSGG&C ChiefExecutives.

NHSGG&C:Chief Executive

March 2009

Action Plan – COMMUNITY HEALTH & CARE PARTNERSHIPS - Financial Planning and Budgetary Control

Risk Ratings for Recommendations

High Key controls absent, not being operated asdesigned or could be improved. Urgent attentionrequired.

Medium Less critically important controls absent, not

being operated as designed or could be

improved.

Low Lower level controls absent, not being

operated as designed or could be improved.

The Priority rating for each recommendation reflects its importance in establishing good governance.No. Recommendations

Budget Monitoring

Priority Accepted Service’s Comments (ifappropriate)

OfficerResponsible forImplementation

Timescale forImplementation

CHCP: N/A4 Evidence must be maintained, in the form ofminutes, to record the attendance of staff at4 weekly Social Work budget monitoringmeetings. Minutes must be circulatedtimeously to all parties. Agreement overboth the content and the required actionswill help to ensure greater accountability.

Medium Yes Accepted by Social Work.

Recommendation notapplicable to NHSGG&C GCC: Social

Work Head ofFinance

Immediate

GCC: SocialWork Head ofFinance

5 Formal procedures for the communicationand requesting of Social Work budgetalterations should be implemented includingadequate explanations for adjustments orreasons why these cannot be processed.These should be filed along with budgetreports to enable a clear audit trail of allalterations from the original budget

High Yes All adjustments to actualsand budgets per themonitoring process arerecorded andcommunicated, and aclear audit trail ismaintained. Formalprocedures are in place forbudget adjustments, andthese will be reissued toall staff.

Recommendation not

CHCP: N/A

February 2009

applicable to NHSGG&C.

GCC: SocialWork Head ofFinance

6 CHCP Heads of Finance should beproactively involved in the Social Workprobable outturn and budget setting process

High Yes This was implemented forthe 2008/09 probableoutturn process.

Recommendation notapplicable to NHSGG&C.

CHCP: Heads ofFinance

Ongoing

Action Plan – COMMUNITY HEALTH & CARE PARTNERSHIPS - Financial Planning and Budgetary Control

Risk Ratings for Recommendations

High Key controls absent, not being operated asdesigned or could be improved. Urgent attentionrequired.

Medium Less critically important controls absent, not

being operated as designed or could be

improved.

Low Lower level controls absent, not being

operated as designed or could be improved.

The Priority rating for each recommendation reflects its importance in establishing good governance.No. Recommendations

Financial Reporting

Priority Accepted Service’s Comments (ifappropriate)

OfficerResponsible forImplementation

Timescale forImplementation

GCC: ExecutiveDirector of SocialCare Services

NHSGG&C:Director ofFinance

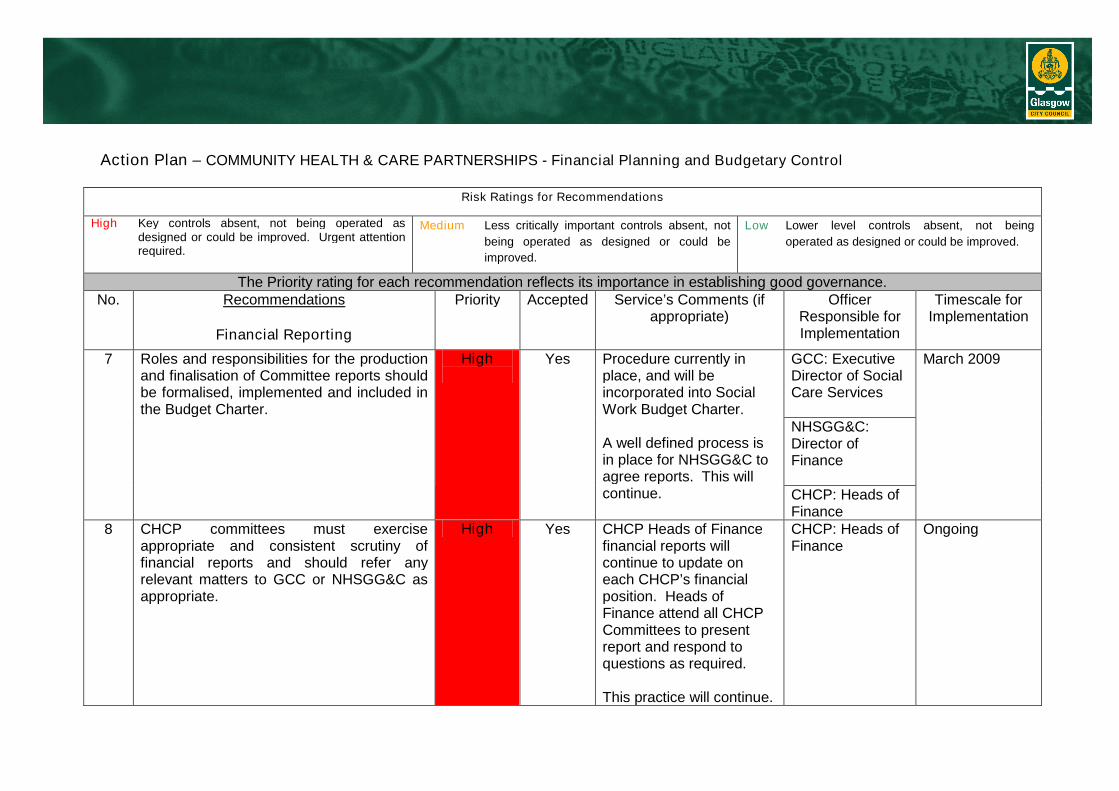

7 Roles and responsibilities for the productionand finalisation of Committee reports shouldbe formalised, implemented and included inthe Budget Charter.

High Yes Procedure currently inplace, and will beincorporated into SocialWork Budget Charter.

A well defined process isin place for NHSGG&C toagree reports. This willcontinue. CHCP: Heads of

Finance

March 2009

8 CHCP committees must exerciseappropriate and consistent scrutiny offinancial reports and should refer anyrelevant matters to GCC or NHSGG&C asappropriate.

High Yes CHCP Heads of Financefinancial reports willcontinue to update oneach CHCP’s financialposition. Heads ofFinance attend all CHCPCommittees to presentreport and respond toquestions as required.

This practice will continue.

CHCP: Heads ofFinance

Ongoing

Heads of Finance will alsoconsider ways ofdeveloping the financialreports throughconsultation withCommittee members toensure they meet theirneeds.

9 An assessment of the requirement for theprovision of training to CHCP Committeemembers on the requirements andresponsibilities of the scrutiny functionshould be conducted and training providedwhere necessary

Medium Yes CHCP Directors andHeads of Finance toundertake training needsassessment for Officersand Committee Members.

CHCP: Directors /Heads of Finance

March 2009onwards

Action Plan – COMMUNITY HEALTH & CARE PARTNERSHIPS - Financial Planning and Budgetary Control

Risk Ratings for Recommendations

High Key controls absent, not being operated asdesigned or could be improved. Urgent attentionrequired.

Medium Less critically important controls absent, not

being operated as designed or could be

improved.

Low Lower level controls absent, not being operated

as designed or could be improved.

The Priority rating for each recommendation reflects its importance in establishing good governance.No. Recommendations

Financial Training & ProceduralInstruction

Priority Accepted Service’s Comments (ifappropriate)

OfficerResponsible forImplementation

Timescale forImplementation

10 An assessment of further officer trainingrequirements should be conducted, andtraining carried out where necessary.

Medium Yes CHCP Directors andHeads of Finance toundertake training needsassessment for Officersand Committee Members.

CHCP: Directors/Heads ofFinance

March 2009onwards

GCC: N/A

NHSGG&C: N/A

11 Good practice in one CHCP should beshared across all CHCPs. This shouldinclude procedural instructions andguidance on managing budgets e.g. thebudget briefing sessions carried out at NorthCHCP are considered to be good practiceand should be replicated elsewhere.

Medium Yes The ongoing discussionsbetween GCC andNHSGG&C will addressthese issues.

CHCP: Directors

March 2009onwards

8. DETAILED FINDINGS, CONCLUSIONS and RECOMMENDATIONS

8.1 Overview

8.1.1 The CHCPs are accountable to both GCC and NHSGG&C. Both organisationsoperate different financial ledger systems, and monitor on different accountingperiods:

● NHSGG&C monitors on 12 monthly periods; and● GCC monitors on 13 4-weekly periods.

8.1.2 GCC delegates budgets to the CHCPs; it has no powers to devolve budgets tothem. In contrast, the budget from NHSGG&C is devolved to CHCPs.

8.1.3 NHSGG&C assigns budgets to the CHCPs on a geographical basis followingthe previous Primary Care allocations for those areas. In addition each CHCPhas a hosted NHS service whereby they have responsibility for managingexpenditure for Glasgow-wide programmes.

8.1.4 GCC Social Work monitors and reports at Care Group level (such as Children& Families) which cuts across all CHCPs.

8.1.5 The CHCP Heads of Finance have reporting responsibility to the CHCPDirector, and in addition one of the CHCP Directors is designated lead forfinancial matters and therefore has an involvement with all CHCP Heads ofFinance. At the time of the audit fieldwork, CHCP Heads of Finance hadindirect responsibility to senior management within GCC and NHSGG&C.Subsequently, the GCC Executive Committee agreed revised arrangementswhich involve financial staff continuing to be based in service departments butline managed by the Executive Director of Financial Services. The revisedcame into place on 1st January 2009, for two years.

8.1.6 Both GCC and NHSGG&C are in a period of severe financial funding pressureand this report should be considered in this context.

8.2 The Budget Setting Process

Findings

8.2.1 Overall CHCP budgets are set by the two Partner organisations (NHSGG&Cand GCC).

8.2.2 Although CHCP Heads of Finance said they had no involvement in the budgetsetting process, the GCC Acting Head of Finance confirmed that both theCHCP Directors and Heads of Finance were involved in the 2008/09 budgetand service planning process and the savings programme, and were given anopportunity to influence the process. The involvement of the CHCPs isconsistent with the recommendation of a previous review by GCC.

8.2.3 CHCPs do not formally approve or accept the budget from the partnerorganisations. For the last two financial years, GCC has issued a BudgetCharter document to the CHCPs for signature detailing the roles andresponsibilities relating to budgetary control and monitoring within Social WorkServices. The Budget Charter document is issued to all Social Work clientgroups. The CHCP Heads of Finance consider that the current Charterdocument requires amendment for CHCPs.

8.2.4 The roles and responsibilities are also detailed in various policy documents,such as the Scheme of Virement. However communication problems wereidentified during the audit which calls into question the implementation of theseroles and responsibilities.

8.2.5 There is an NHSGG&C Development Plan in place for each CHCP detailingthe priorities for the year. The development plans for North and West CHCPwere obtained and reviewed. However, there was no clear link between thepriorities as outlined in the current Development Plan and the budget settingprocess for 2008/09.

8.2.6 NHSGG&C budgets are developed on an incremental basis reflecting minorvariations in service delivery year on year and the majority of staff workingstandard hours. CHCPs can request amendments to individual budget lines,enabling them to direct funds to areas of need whilst remaining within overallbreak-even limits.

8.2.7 NHSGG&C do not request formal acceptance of the budget from the CHCPDirectors or Heads of Finance. In addition, the overall budgetary responsibilityin relation to hosted services was not clear.

8.2.8 An exercise is currently underway to update and realign the DevelopmentPlans with the proposed budgets to ensure that services are prioritised andfunds directed accordingly.

8.2.9 The two CHCPs reviewed have been given net expenditure budgets from GCCand NHSGG&C of approximately £715m over the past three years. Officerswithin CHCPs have responsibility for delegated budgets from a partnerorganisation which is not their employer which raises issues of accountabilitywhich have still to be resolved, despite the existence of CHCPs for almost 3years.

Conclusions

8.2.10 There is a formal sign-off process covering roles and responsibilities for themanagement of the GCC annual budget which has not been implemented forCHCPs. There is no identical process for NHSGG&C.

8.2.11 The roles and responsibilities of the CHCPs are documented. Despite this, theaudit established communication problems particularly between GCC andCHCPs.

8.2.12 The link between the detailed plans and budgets off GCC and NHSGG&C tothe CHCP detailed budgets should be more transparent.

8.2.13 Officers within CHCPs have responsibility for delegated budgets from a partnerorganisation which is not their employer. This raises issues of accountabilityregarding budgets which have still to be resolved, despite the existence ofCHCPs for almost 3 years.

Recommendations

8.2.14 The GCC Budget Charter:

● must be revised and agreed to reflect the roles and responsibilities ofofficers in GCC and CHCPs relating to budget planning and monitoring;

● should make reference to all other relevant, agreed documentation e.g.scheme of virement; and

● must be signed annually by each party to the agreement toacknowledge acceptance of their roles and responsibilities (action point1).

8.2.15 A document similar to the GCC Charter should be developed to formalise theroles and responsibilities of the CHCPs in relation to the NHSGG&C budget.This document should be signed annually by each CHCP Director onacceptance of the budget (action point 2).

8.2.16 GCC and NHSGG&C must conclude agreement on how to achieveaccountability for budget holders (action point 3).

8.3 Budget Monitoring

Findings

8.3.1 Budget monitoring meetings are held every four weeks by GCC to enableCHCP Heads of Finance and Social Work Finance Managers to discuss thefinancial performance and agree any adjustments for the period. Thesemeetings are a key element of the budget monitoring process. GCC andCHCP staff could not agree on attendance at these meetings. There are nominutes recorded, nor is attendance recorded and it was therefore not possibleto verify attendance at these meetings.

8.3.2 There are dedicated management accountants within NHSGG&C for eachCHCP, working in teams of 3 ensuring constant support for each CHCP in theevent of absence. The management accountants prepare the monthly budgetreports and email these to the Heads of Finance. In addition they senddetailed reports to the different budget holders within the CHCP. They alsomeet with budget holders at their request to monitor budgets, but minutes ofthese meetings do not appear to be maintained.

8.3.3 Discussion with several budget holders within North and West GlasgowCHCPs highlighted a degree of satisfaction with the “clear and comprehensive”information provided by NHSGG&C. They are able to request adjustments tobudget lines through the year and meet regularly with the managementaccountants to discuss and monitor the budgets.

8.3.4 From October 2008, NHSGG&C management accountants will producemonthly reconciliations showing all adjustments to budget lines and includethese in the monthly information distributed to the CHCPs.

8.3.5 Budget adjustments are also proposed by the CHCP Heads of Finance as theneed arises throughout the year. Discussion with the CHCP Heads ofFinance, budget holders and the NHS management accountants confirmedthat adjustments to the NHS budgets proposed by the CHCP are processed ona timely basis.

8.3.6 The majority of budget adjustments for GCC are made by the Social WorkCentral Finance Managers, who have detailed knowledge of the Care Groups.Discussion with CHCP Heads of Finance and budget holders indicated thatadjustments are often processed by the partner organisations without beingformally communicated to budget holders.

8.3.7 Discussion with staff in GCC and both CHCPs indicate conflicting views on theprocessing of budget adjustments. There is no formal process for requestingadjustments to the budget or recording whether requests have been actionedor not. As such it was not possible to either verify whether adjustments werebeing processed or ascertain reasons why requests were not actioned.

8.3.8 One of the major recommendations from the previous review by GCC was thatCHCP Heads of Finance require greater support to meet the monitoringscrutiny requirements of CHCPs. GCC have established a Financial SupportUnit in Social Work Services to address this issue. However, the CHCPHeads of Finance questioned the added value that this unit provides.

8.3.9 The Probable Outturn exercise is another key element of the monitoringprocess and can inform the budget setting process for future years. Throughdiscussion with the CHCP Heads of Finance and staff within Social Work it isapparent there needs to be greater clarity in the level of involvement of theCHCPs in this process.

Conclusion

8.3.10 Monitoring takes place to compare actual financial results to budgets.However, there are different budget monitoring arrangements within theCHCPs in relation to the two partnership organisations, ranging from greatercentral direction from GCC to greater devolved responsibility from NHSGG&C.

8.3.11 The NHSGG&C process appears more transparent and efficient. Thereappears to be a breakdown in communication between the CHCPs and GCCin relation to the requirements for budget monitoring, arrangements forprocessing adjustments and involvement in the Probable Outturn exercise.

Recommendations

8.3.12 Evidence must be maintained in the form of minutes to record the attendanceof staff at four-weekly Social Work budget monitoring meetings. Minutes mustbe circulated timeously to all parties. Agreement over both the content and therequired actions will help to ensure greater accountability (action point 4).

8.3.13 Formal procedures for the communication and requesting of Social Workbudget alterations should be implemented including adequate explanations foradjustments or reasons why these cannot be processed. These should befiled along with budget reports to enable a clear audit trail of all alterations fromthe original budget (action point 5).

8.3.14 CHCP Heads of Finance should be proactively involved in the Social Workprobable outturn and budget setting process (action point 6).

8.4 Financial Reporting

Findings

8.4.1 The CHCP Committee reports for North and West Glasgow were obtained andreviewed.

8.4.2 The CHCP Heads of Finance prepare a narrative for the CHCP Committeereport to explain all significant variances from budget. A copy of the report issent to the NHS Director of Finance, the GCC Acting Head of Finance and theCorporate Finance Accountant for review. The reports are then returned to theCHCP Heads of Finance with suggested changes and included within thepapers issued to the committee clerk.

8.4.3 Discussions with the CHCP Heads of Finance and staff within Social Workindicated a lack of clarity over final responsibility for information included in thereport.

8.4.4 The minutes of North and West Glasgow CHCP committees indicate differinglevels of scrutiny regarding reported figures. Where finance is often discussedand challenged in detail at the North CHCP there is no evidence that this is thecase at the West CHCP.

8.4.5 The table below details the budgets and variances for West CHCP and NorthCHCP since financial year 2006/2007 (figures shown in brackets highlight anoverspend). The difference in the level of scrutiny at the CHCPs appears tohave no impact on the NHSGG&C budgets, which were underspent in 2006/07and 2007/08, but could have contributed to large GCC overspends at WestCHCP in the same period. In overall terms, West CHCP appears to haveperformed better than North CHCP but the variances for West CHCP are moresignificant.

West CHCP GCC (£m) NHS (£m) CHCP Total (£m)

Budget Variance Budget Variance Budget Variance2006/07 26.32 (0.12) 108.01 0.72 134.33 0.602007/08 31.20 (0.49) 113.24 0.48 144.44 (0.01)2008/09 YTD 9.94 (0.47) 45.61 0.00 55.55 (0.47)Total 67.46 (1.08) 266.86 1.20 334.32 0.12

North CHCP GCC (£m) NHS (£m) CHCP Total (£m)

Budget Variance Budget Variance Budget Variance2006/07 29.67 (0.31) 63.09 0.21 92.76 (0.10)2007/08 32.75 0.05 68.90 0.20 101.65 0.252008/09 YTD 10.39 (0.30) 27.03 (0.02) 37.42 (0.32)Total 72.81 (0.56) 159.02 0.39 231.83 (0.17)

Conclusion

8.4.6 The scrutiny of financial information by CHCP Committees is not consistentbetween the two CHCPs under review, as evidenced from the minutes of Northand West CHCPs.

Recommendations

8.4.7 Roles and responsibilities for the production and finalisation of Committeereports should be formalised, implemented and included in the budget charter(action point 7).

8.4.8 CHCP committees must exercise appropriate and consistent scrutiny offinancial reports and should refer any relevant matters to GCC and NHSGG&Cas appropriate (action point 8).

8.4.9 An assessment of the requirement for the provision of training to CHCPCommittee members on the requirements and responsibilities of the scrutinyfunction should be conducted and training provided where necessary (actionpoint 9).

8.5 Financial Training & Procedural Instructions

Findings

8.5.1 Financial training sessions were jointly arranged by GCC and NHSGG&C forCHCP staff. The training was provided by the Chartered Institute of PublicFinance & Accountancy between January and April 2007. From a review ofthe delegate list, 40 staff from all CHCPs attended the sessions. 2 of the 5CHCP Directors and 2 of the 3 CHCP Heads of Finance attended.

8.5.2 No procedural instructions have been issued to CHCP budget holders toprovide advice on managing budgets. The Head of Finance for North CHCPhas provided budgetary briefing sessions to budget holders. However, similarsessions have not been provided at West CHCP.

Conclusions

8.5.3 Financial training sessions were provided for CHCP staff but not all seniorexecutive management were present.

8.5.4 There is a need for procedural instructions to be issued to budget holders.

Recommendation

8.5.5 An assessment of further training requirement should be conducted, andtraining carried out where necessary (action point 10).

8.5.6 Good practice in one CHCP should be shared across all CHCPs. This shouldinclude procedural instructions and guidance on managing budgets e.g. thebudget briefing sessions carried out at North CHCP are considered to be goodpractice and should be replicated elsewhere (action point 11).

8.6 Post Fieldwork Developments

8.6.1 Since the completion of the audit fieldwork, the Executive Director of FinancialServices for GCC has initiated four-weekly meetings with all CHCP Directorsand Heads of Finance and GCC staff. The purpose of these meetings is toimprove the monitoring and management of the GCC element of the CHCPbudgets.