financial market regulation and intermediation program

TRANSCRIPT

Completion Report

Project Number: 38276 Loan Numbers: 2278, 2715 September 2013

Philippines: Financial Market Regulation and

Intermediation Program

CURRENCY EQUIVALENTS

Currency Unit – peso (P)

Subprogram 1 At Appraisal Program Completion

(15 October 2006) (22 December 2006) P1.00 = $0.020 $0.020 $1.00 = P50.00 P49.40

Subprogram 2

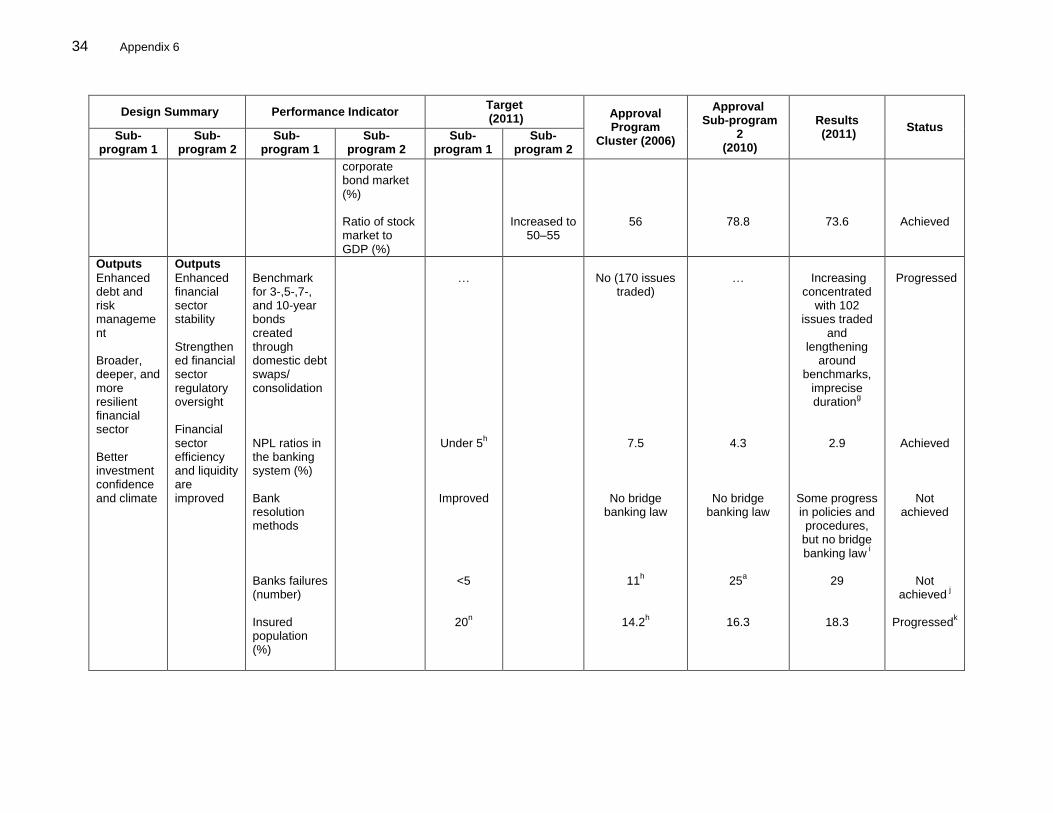

At Appraisal Program Completion (NA) (15 April 2012)

P1.00 = NA $0.023 $1.00 = NA P42.84

ABBREVIATIONS ADB – Asian Development Bank ASEAN – Association of Southeast Asian Nations BSP – Bangko Sentral ng Pilipinas BTr – Bureau of the Treasury CSP – country strategy and program CMDP – Capital Market Development Plan DBM – Department of Budget and Management DIF – Deposit Insurance Fund DMF – design and monitoring framework DOF – Department of Finance DSA – debt sustainability assessment FMRIP – Financial Market Regulation and Intermediation Program FSAP – Financial Sector Assessment Program FSCC – Financial Stability Coordination Council FSF – Financial Stability Forum GDP – gross domestic product GFC – global financial crisis IAIS – International Association of Insurance Supervisors IAS – International Accounting Standards IMF – International Monetary Fund IOSCO – International Organization of Securities Commissions LCY – local currency M2 – money and close substitutes for money MCR – minimum capital requirements MOU – memorandum of understanding MTPDP – Medium Term Philippine Development Plan 2004–2010 NPL – non-performing loan OECD – Organization for Economic Cooperation and Development OIC – office of the Insurance Commission P3F – post-program partnership framework PDIC – Philippine Deposit Insurance Corporation PDEx – Philippine Dealing and Exchange Corporation

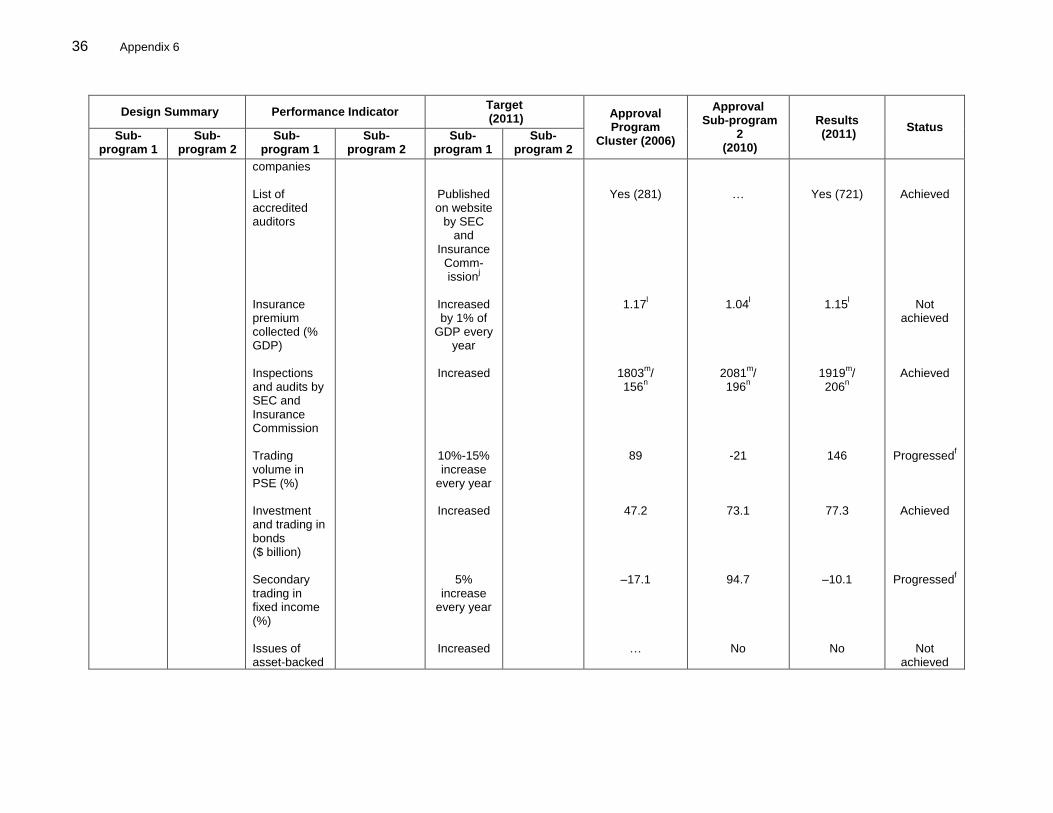

PSE – Philippine Stock Exchange Q – quarter SP1 – subprogram 1 SP2 – subprogram 2 S&P – Standard & Poor’s SEC – Securities and Exchange Commission SPV – Special Purpose Vehicle SRC – Securities Regulation Code SRO – self-regulatory organization TA – technical assistance

NOTES

(i) The fiscal year (FY) of the Government and its agencies ends on 31 December.

(ii) In this report, "$" refers to US dollars.

Vice-President S. Groff, Operations 2 Director General J. Nugent, Southeast Asia Department (SERD) Director S. Hattori, Public Management, Financial Sector, and Trade Division,

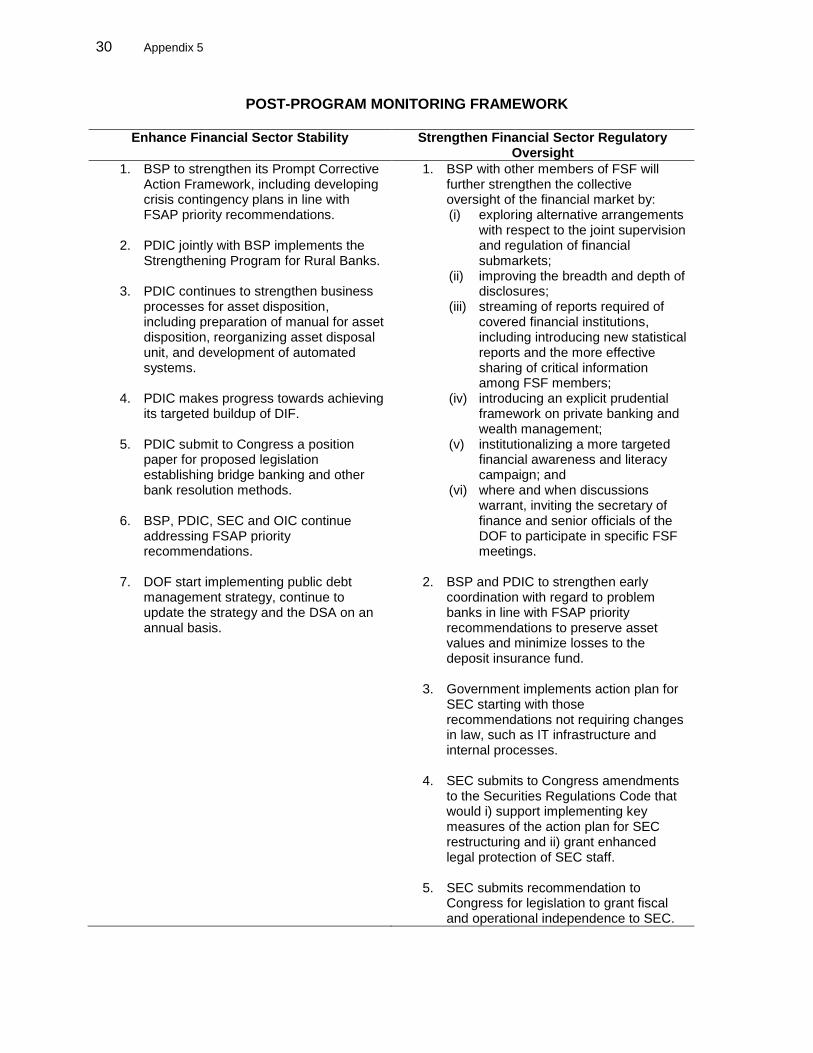

SERD Team leader S. Schuster, Senior Financial Sector Specialist, SERD Team members R. Aquino, Associate Project Analyst, SERD

M. Bezemer, Results Management Specialist, Strategy and Policy Department M. Parra, Operations Assistant, SERD

In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area.

CONTENTS

Page

BASIC DATA ii

I. PROGRAM DESCRIPTION 1

II. EVALUATION OF DESIGN AND IMPLEMENTATION 2

A. Relevance of Design and Formulation 2 B. Program Outputs 3 C. Program Costs and Disbursements 7 D. Program Schedule 7 E. Implementation Arrangements 7 F. Conditions and Covenants 8 G. Related Technical Assistance 8 H. Consultant Recruitment and Procurement 9 I. Performance of the Borrower and the Executing Agency 10 J. Performance of the Asian Development Bank 10

III. EVALUATION OF PERFORMANCE 11

A. Relevance 11 B. Effectiveness in Achieving Outcome 12 C. Efficiency in Achieving Outcome and Outputs 13 D. Preliminary Assessment of Sustainability 13 E. Impact 13

IV. OVERALL ASSESSMENT AND RECOMMENDATIONS 14

A. Overall Assessment 14 B. Lessons 14 C. Recommendations 15

APPENDIXES

1. Design and Monitoring Framework 16 2. Performance of Financial Market Regulation and Intermediation Program, Subprogram 1 – Policy Actions 19 3. Performance of Financial Market Regulation and Intermediation Program, Subprogram 2 – Policy Actions 23 4. Status of Compliance with Loan Covenants 26 5. Post-Program Monitoring Framework 30 6. Program Performance 32 7. Questionnaire – Program Completion Report: Government Survey Results 39

ii

BASIC DATA – FINANCIAL MARKET REGULATION AND INTERMEDIATION SUBPROGRAM 1

A. Loan Identification 1. Country 2. Loan Number 3. Program Title 4. Borrower 5. Executing Agency 6. Amount of Loan 7. Program Completion Report Number

Philippines 2278 Financial Market Regulation and Intermediation Program (Subprogram 1) Republic of the Philippines Department of Finance $200 million 1420

B. Loan Data 1. Appraisal – Date Started – Date Completed 2. Loan Negotiations – Date Started – Date Completed 3. Date of Board Approval 4. Date of Loan Agreement 5. Date of Loan Effectiveness – In Loan Agreement – Actual – Number of Extensions 6. Closing Date – In Loan Agreement – Actual – Number of Extensions 7. Terms of Loan – Interest Rate – Maturity (number of years) – Grace Period (number of years) 8. Terms of Relending (if any) – Interest Rate – Maturity (number of years) – Grace Period (number of years) – Second-Step Borrower

22 August 2006 29 September 2006 31 October 2006 2 November 2006 6 December 2006 11 December 2006 11 March 2007 20 December 2006 None 31 December 2008 22 December 2006 None LIBOR-based 15 years 3 years Not applicable Not applicable Not applicable Not applicable

iii

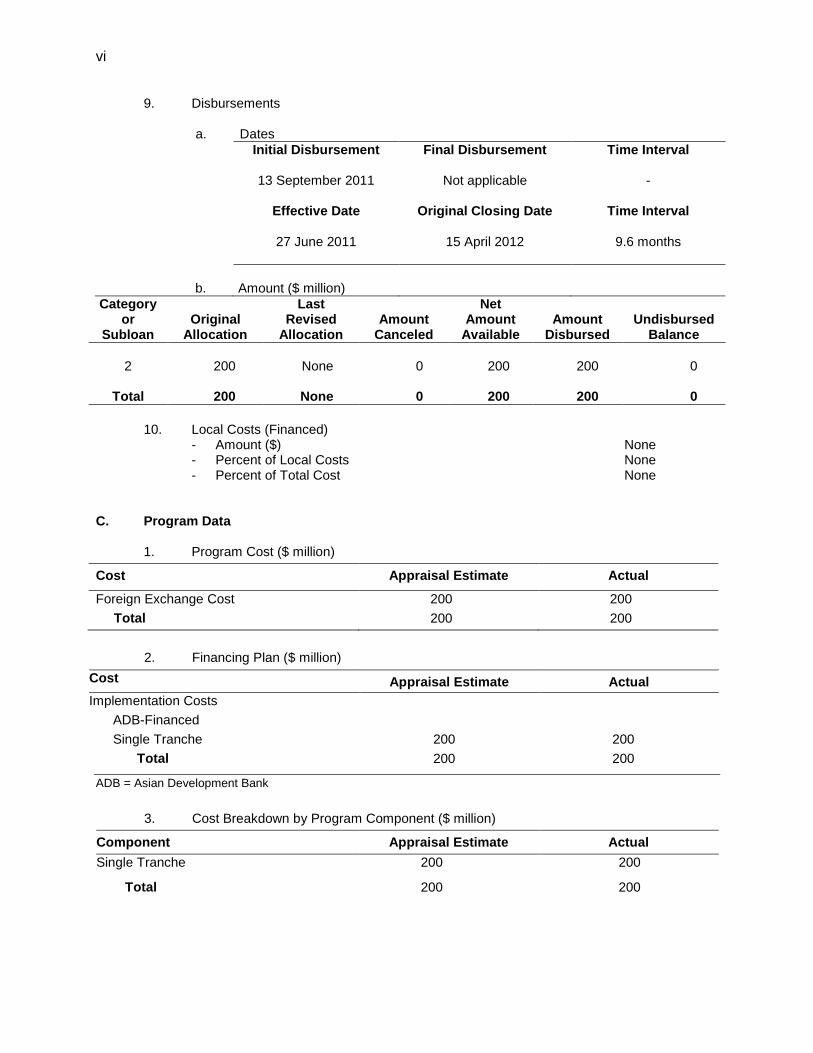

9. Disbursements a. Dates

Initial Disbursement

22 Dec 2006

Final Disbursement

Not applicable

Time Interval -

Effective Date

20 Dec 2006

Original Closing Date

31 December 2008

Time Interval

24 months

b. Amount ($ million)

Category or

Subloan

Original

Allocation

Last Revised

Allocation

Amount

Canceled

Net Amount

Available

Amount

Disbursed

Undisbursed

Balance

1 200 None 0 200 200 0

Total 200 None 0 200 200 0

10. Local Costs (Financed) - Amount ($) None - Percent of Local Costs None - Percent of Total Cost None C. Program Data

1. Program Cost ($ million)

Cost Appraisal Estimate Actual

Foreign Exchange Cost 200 200

Total 200 200

2. Financing Plan ($ million)

Cost Appraisal Estimate Actual

Implementation Costs

ADB Financed Not Applicable

Single Tranche 200 200

Total 200 200

ADB = Asian Development Bank

3. Cost Breakdown by Program Component ($ million)

Component Appraisal Estimate Actual

Single Tranche

200

200

Total 200 200

iv

4. Program Schedule

Item Appraisal Estimate Actual

Other Milestones

Single Tranche 20 December 2006 22 December 2006

5. Program Performance Report Ratings

Implementation Period

Ratings

Development Objectives

Implementation Progress

From 1 January 2007 to 31 December 2007

Satisfactory

Satisfactory

From 1 January 2008 to 31 August 2008 Satisfactory Satisfactory

D. Data on Asian Development Bank Missions

Name of Mission

Date

No. of Persons

No. of Person-Days

Specialization of Members

a

Fact Finding (intermittently) Feb–Jun 2006 2 2 a, b

Appraisal 22 Aug–29 Sep 2006 2 2 a, b

Note: a a = finance specialist, b = economist

v

BASIC DATA – FINANCIAL MARKET REGULATION AND INTERMEDIATION SUBPROGRAM 2

A. Loan Identification 1. Country 2. Loan Number 3. Program Title 4. Borrower 5. Executing Agency 6. Amount of Loan 7. Program Completion Report Number

Philippines 2715 Financial Market Regulation and Intermediation Program (Subprogram 2) Republic of the Philippines Department of Finance $200 million 1420

B. Loan Data 1. Appraisal – Date Started – Date Completed 2. Loan Negotiations – Date Started – Date Completed 3. Date of Board Approval 4. Date of Loan Agreement 5. Date of Loan Effectiveness – In Loan Agreement – Actual – Number of Extensions 6. Closing Date – In Loan Agreement – Actual – Number of Extensions 7. Terms of Loan – Interest Rate – Maturity (number of years) – Grace Period (number of years) 8. Terms of Relending (if any) – Interest Rate – Maturity (number of years) – Grace Period (number of years) – Second-Step Borrower

No Appraisal Mission 4 November 2010 4 November 2010 7 December 2010 22 February 2011 22 May 2011 27 June 2011 one 15 April 2012 15 April 2012 - LIBOR-based 15 years 3 years Not applicable Not applicable Not applicable Not applicable

vi

9. Disbursements a. Dates

Initial Disbursement

13 September 2011

Final Disbursement

Not applicable

Time Interval -

Effective Date

27 June 2011

Original Closing Date

15 April 2012

Time Interval

9.6 months

b. Amount ($ million)

Category or

Subloan

Original

Allocation

Last Revised

Allocation

Amount

Canceled

Net Amount

Available

Amount

Disbursed

Undisbursed

Balance

2 200 None 0 200 200 0

Total 200 None 0 200 200 0

10. Local Costs (Financed) - Amount ($) None - Percent of Local Costs None - Percent of Total Cost None C. Program Data

1. Program Cost ($ million)

Cost Appraisal Estimate Actual

Foreign Exchange Cost 200 200

Total 200 200

2. Financing Plan ($ million)

Cost Appraisal Estimate Actual

Implementation Costs

ADB-Financed

Single Tranche 200 200

Total 200 200

ADB = Asian Development Bank

3. Cost Breakdown by Program Component ($ million)

Component Appraisal Estimate Actual

Single Tranche 200 200

Total 200 200

vii

4. Program Schedule

Item Appraisal Estimate Actual

Other Milestone

Single Tranche

27 June 2011

13 September 2011

5. Program Performance Report Ratings

Implementation Period

Ratings

Development Objectives

Implementation Progress

From 1 January 2008 to 31 December 2008 Satisfactory Satisfactory

From 1 January 2008 to 31 December 2009

From 1 January 2009 to 31 December 2010

Satisfactory

Satisfactory

Satisfactory

Satisfactory

D. Data on Asian Development Bank Missions

Name of Mission

Date

No. of Persons

No. of Person-Days

Specialization of Members

a

Consultation 9-15 Jun 2010 2 14 a, b Fact Finding 22 Jul & 3 Aug 2010 2 4 a, b Consultation 27 Jan 2011 1 1 a Review 25 May–20 Aug 2012 1 4 a Review 12 Nov –13 Dec 2012 3 9 a Review 17 Jan – 1 Feb 2013 1 3 a Program Completion Review 2 – 23 May 2013 2 4 a Note: a a = finance specialist, b = economist.

1

I. PROGRAM DESCRIPTION

1. The Medium Term Philippine Development Plan (MTPDP) for 2004–2010 established targets for increased and sustainable growth and job creation.1 This was expected to translate into real gross domestic product (GDP) growth rates of 5.3%–6.3% in 2005 and 7%–8% by 2010, with exports and investments as primary drivers of growth. However, in 2005, financial markets lacked the size and depth to support the investment needs of the MTPDP: banking assets equaled just 63% of GDP, equity market capitalization 40% of GDP, and bonds outstanding 37% of GDP, proportions much lower than those found in the Philippine’s regional peers (e.g., Thailand, Malaysia, and Singapore). The financial sector’s ability to intermediate was further constrained by low levels of foreign ownership of the banking sector, which capped the lending limit. Significant efforts were required to broaden and deepen the financial system to support economic growth and development. 2. To reform and expand domestic capital markets, the Philippines needed to overcome three primary challenges. First, the government needed to achieve a level of financial sector development comparable to its regional peers. Most importantly, a vision for financial market development was needed. While the Securities Regulation Code (SRC) provided a sound basis for regulation, it did not clarify the role of the Securities and Exchange Commission (SEC) in promoting capital market development. At the same time, the fragmented government debt market had no recognized benchmarks and was biased toward shorter maturities. Secondary trading in government bonds was not supported by an efficient price discovery mechanism. This inhibited the publication of key prices and trading volumes, which blocked the development of a reliable yield curve and a vibrant corporate debt market. 3. Second, the government needed to restore investor confidence, because other vulnerabilities contributed to increased systemic risk and volatility. Between 1999 and 2004 the government’s debt as a share of GDP increased from 55% to 74%, or 101% when including government-owned and -controlled corporations. Non-performing loans (NPLs) represented 7% of total banking sector loans as of May 2006, deterring more capital-intensive lending and encouraging investment in safer government debt. Combined with persistent high government budget deficits, this crowded out the private sector and reduced credit availability. 4. Third, the technical and regulatory capacity of supervisory institutions needed to be improved to maintain reforms and to participate in the integration of regional capital markets. By 2005, 440 banks were pending liquidation by the Philippine Deposit Insurance Corporation (PDIC). Slow response times and elevated liquidation losses were commonplace because PDIC lacked resolution powers, was understaffed, and had ineffective asset administration and disposal processes. Increases in the number of problem banks and in deposit insurance coverage—without a corresponding increase in premium assessments—caused the unfunded liabilities of the Deposit Insurance Fund (DIF) to rise to nearly P40 billion. Moreover, the SEC suffered from chronic underfunding and was not providing adequate supervision. A framework had not been established to encourage effective supervision by self-regulatory organizations (SROs) and the legal framework provided little protection to minority shareholders. Price discovery was weak, and international standards such as the International Organization of Securities Commissions (IOSCO) principles and International Accounting Standards (IAS) had not been embraced by the market. Statutory capital requirements for the insurance sector were inadequate.

1 Government of the Republic of the Philippines, National Economic Development Authority. 2004. Medium-Term

Philippines Development Plan (MTPDP) 2004–2010. Manila.

2

5. The Financial Market Regulation and Intermediation Program (FMRIP) and the linked technical assistance (TA) were designed to assist the government in achieving the objectives set out in the MTPDP and to ensure the financial sector could provide the required intermediation.2 The program’s desired impact was an increased contribution of the financial sector to economic growth, poverty reduction, and development. Specifically, the program was structured to: (i) enhance financial system stability by strengthening the government’s debt issuance and management processes, (ii) improve resolution of problem banks and strengthen the solvency and administration of PDIC, (iii) strengthen nonbank financial sector governance, and (iv) increase the efficiency and transparency of the securities market. Subprogram 1 (SP1) focused on the debt and equity markets, deposit insurance, and insurance sector, but was primarily intended to increase investor confidence by reducing financial sector vulnerabilities. Subprogram 2 (SP2) was initially structured to continue the reform agenda with an increasing emphasis on securities market efficiency. However, the design of SP2 reflected the intent of the Asian Development Bank (ADB) that its scope and schedule could be modified if needed. 6. This flexibility proved indispensable in meeting two significant unrelated challenges. First, the office of the Insurance Commission (OIC) and SEC were unable to implement indicative actions agreed to under the original program within specified timelines. As a result, SP2 was significantly delayed, while ADB continued its policy dialogue and TA to help active implementing agencies address organizational issues, capacity constraints, and critical reforms. Subsequently the global financial crisis (GFC) produced a series of economic and financial sector shocks that were unprecedented in size and scope. The resulting delay provided an opportunity for the incoming administration to reformulate elements of SP2 in response to lessons from the GFC. Specifically, the GFC highlighted issues that, to various degrees, were insufficiently addressed by the original SP2, including: (i) the need to maintain financial stability and reduce vulnerabilities, (ii) the need to ensure effective system-wide regulatory oversight, (iii) the need for efficient resolution methodologies, and (iv) the importance of an adequately funded deposit insurance mechanism to minimize the risk of depositor flight and contagion. It is important to note that post-GFC global policy responses created a unique external environment that impacted several program performance indicators (e.g., stock market capitalization).

II. EVALUATION OF DESIGN AND IMPLEMENTATION

A. Relevance of Design and Formulation

7. The initial design of the program was fully aligned with ADB’s country strategy and program (CSP) 2005–2007 and is considered highly relevant.3 Six thematic constraints were identified that impaired the government’s capacity to reduce poverty more rapidly.4 The CSP proposed significant policy-based support, conditioned on the government meeting a budget deficit reduction target and developing sector-specific reform agendas. In addition, the CSP supported the concurrent development of an enhanced investment climate and improved governance to complement increased fiscal discipline. To address these constraints, ADB targeted its policy engagement in three broad areas: the power sector, financial markets (targeting efficiency of intermediation), and governance (including reforms of local government and the judicial system).

2 ADB. 2006. Report and Recommendation of the President to the Board of Directors: Proposed Program Cluster,

Loan, and Technical Assistance Grant to the Republic of the Philippines for the Financial Market Regulation and Intermediation Program. Manila (Loan 2278-PHI, approved on 6 December).

3 ADB. 2005. Country Strategy and Program: Philippines, 2005–2007. Manila.

4 These constraints were: (i) fiscal imbalances; (ii) a weak investment climate; (iii) inadequate infrastructure; (iv) poor

management of assets, land, and resources; (v) low institutional capacity; and (vi) geographical inequalities.

3

8. The program was fully aligned with the MTPDP reform agenda, and together with the associated TA directly supported initiatives promoting a more efficient financial sector that could finance profitable private investment projects at reduced cost and risk. To achieve these objectives, SP1 focused on capital markets and other nonbank services, and included measures to reduce financial sector vulnerabilities and increase the depth and diversity of financial intermediation. SP1 also sought to strengthen investor confidence through improved regulation, governance, and transparency, and to improve operational efficiency of the securities market. 9. SP2 was initially structured to continue the reform agenda with an increasing emphasis on securities market efficiency. However, the decision to proceed was conditioned on the attainment of deficit reduction targets for 2008 contained in the CSP, as well as progress in implementing reforms under SP1, including reforming the insurance sector and resolving problem banks.5 Proposed policy reforms under SP2 were mostly indicative, reflecting ADB’s intent that its scope and schedule could be modified if necessary based on a review of SP1 accomplishments, the external environment, and any changes to the government’s reform priorities.6 The program’s relevance was enhanced by taking advantage of its inherent flexibility, and in 2010 the program was reformulated to address lessons from the GFC. This enabled the government to focus on strengthening financial sector stability and supervision, and addressing weaknesses in the SEC and OIC; these changes led to delays in SP2 implementation.7 B. Program Outputs

10. The original program outcomes were: (i) enhance financial sector stability, (ii) strengthen nonbank financial subsector governance, and (iii) improve the efficiency of the securities market. Outputs included enhanced debt and risk management; a broader, deeper, and more resilient financial sector; and a better investment confidence and climate. Under SP2, the outcome and outputs were transposed to better reflect their focus and time horizon. In addition, the outputs for SP2 were then modified slightly to capture the government’s refocused priorities. Specifically, output 2 was refocused and broadened to “strengthened financial sector regulatory oversight”, and output 3 was broadened to “improve efficiency and liquidity in securities markets”. This subsection summarizes the sector analysis underpinning the program design at the time of processing, and the main measures implemented under the cluster. 1. Enhanced Financial Sector Stability 11. Under SP1, the government developed the Capital Market Development Plan (CMDP) for 2005–2010.8 The CMDP was anchored in the MTPDP and set out 11 objectives with specific initiatives for 19 key stakeholders. In addition, the government focused on parallel efforts to reform public debt management to achieve a more balanced fiscal position. After establishing regular and predictable issuance schedules, the Bureau of the Treasury (BTr) exchanged P111 billion in notes to create fewer, more liquid instruments, and identified benchmark securities with 3-, 5-, 7- and 10-year maturities. This reduced the number of domestic outstanding debt issues traded to 102 in 2011 from 170 in 2005. The total annual value of government securities traded increased from P438 billion to P4,163 billion over the same period.

5 The central government fiscal deficit improved significantly (from –3.8% in 2004 to –0.9% in 2008). Following the

GFC, priorities shifted to stabilizing the economy, resulting in a sharp decline (to –3.7%) in 2009. The central government fiscal deficit decreased (to –2.3%) in 2012.

6 For adjustments in indicative actions: http://www.adb.org/sites/default/ files/linked-docs/38276-02-phi-oth-04.pdf

7 ADB. 2010. Report and Recommendation of the President to the Board of Directors: Proposed Loan for

Subprogram 2 to the Republic of the Philippines: Financial Market Regulation and Intermediation Program. Manila (Loan 2715-PHI, approved on 6 December).

8 Securities and Exchange Commission. 2006. Capital Market Development Plan: Blueprint for Growth and

Expanded Contributions to the Philippine Economy, 2005–2010. Manila.

4

12. Legislation providing for special purpose vehicles to dispose of distressed assets was extended by 18 months in 2006.9 This contributed to a decline in NPLs to 2.9% in 2011 from 7.5% in 2006.10 After completing a comprehensive study of the DIF in 2006, PDIC formulated an investment and trading policy, and strengthened its risk management system. In addition, PDIC identified a number of legal impediments to effectively resolving bank failures, including a lack of bridge banking. Administrative weaknesses were addressed by strengthening asset valuation, management and disposal of acquired assets, and a framework to select strategic investors as an integral part of bank failure resolution. PDIC further enhanced its framework for administering bank failures, for instance through policies to prohibit benefits to existing shareholders by way of dilution or divestiture as a condition for assistance, and by requiring burden sharing from investors.11 Lastly, the OIC increased the minimum capitalization for both insurance companies and brokers through a sequenced build-up program, and issued regulations to implement a risk-based capital adequacy regime. 12 The SEC introduced risk-based capital rules for broker-dealers and required compliance reporting on a monthly basis. 13. Under SP2, the government increased its focus on strengthening the financial system through a series of initiatives to pre-empt the effects of the GFC. Additional liquidity was provided to the banking sector and a framework for Bangko Sentral ng Pilipinas (BSP) to carry out open market operations with its own bills was established. To support confidence, Congress approved a change to the Deposit Insurance Law, as recommended under SP1, which allowed PDIC to double deposit insurance to P500,000 and deny coverage to accounts that do not represent bona fide deposits. Legislation was also adopted to support the build-up of the DIF and expand the borrowing powers of the PDIC, thereby reducing the financing gap identified in SP1. By the end of 2012, the DIF had increased to 5.7% of insured deposits, exceeding the targeted 5% minimum. To preempt bank failures and strengthen the banking system, BSP and PDIC implemented the Strengthening Program for Rural Banks and approved an electronic matching system to facilitate mergers, acquisitions, and consolidations among banks. The government also continued to build on its successful fiscal consolidation by strengthening public financial management. The Department of Finance (DOF) carried out a needs assessment of its new Debt and Risk and Management Division, followed by a draft public debt management strategy for 2011 and the first internally developed debt sustainability assessment (DSA).

2. Strengthened Nonbank Financial Subsector Governance/Strengthened Financial Sector Regulatory Oversight

14. Under SP1, the SEC finalized and published the CMDP along with an implementation timetable and tracking mechanism. The SEC also became a signatory to Appendix B of IOSCO’s Multilateral Memorandum of Understanding to strengthen enforcement. In turn, the SEC adopted IAS into the Philippine Generally Accepted Accounting Standards, beginning in 2005. The SEC also conducted an audit of the compliance function of the Philippine Stock

9 Republic Act 9343, April 2006.

10 Banks sold about 28% of their non-performing assets to these special purpose vehicles over the past decade.

11 Bank failures increased from 11 in 2008–2009 to 29 in 2011, significantly above the targeted threshold of 5. This

target may have been inappropriate because (i) a spillover from prior years, when failures were held artificially low; and (ii) prompt resolution reduces the cost and increases financial sector stability.

12 After initially waiving the step increase in minimum capital requirements (MCRs) for insurance companies

provided for under subprogram 1, the OIC raised the MCRs in line with Department Order 27-06 and enforced these by June 2013. Department Order 27-06 provided for a stepped increase to P250 million. As of December 2012, 27% of life insurance companies and 30% of non-life insurance companies were not compliant with this MCR. Department Order 15-12, which would take effect after Department Order 27-06 implementation, was intended to gradually increase MCRs to P1,000 million by 2020, but was successfully challenged in court. In response, Congress approved a legislative amendment in 2013 that would replace both Department Orders and provide for a stepped increase to P1,300 million by 2022.

5

Exchange (PSE), which led to improvements in the effectiveness of its SRO. Likewise, the SEC moved to further strengthen compliance by approving the Philippine Dealing and Exchange Corporation (PDEx) as an SRO and requiring all government securities dealers to appoint a compliance officer. To strengthen the insurance sector, DOF approved the reorganization proposal submitted by the OIC, which assessed its own compliance with IAS core principles and identified priority reforms. 15. However, SP1 was hobbled by the failure to pass a number of revised laws. For example, the SEC was unable to gain approval to subpoena bank records during investigations of fraud and to enhance the rights of minority shareholders. Planned reforms to the OIC, including the proposed reorganization, were withdrawn and guidelines to enforce anti-money laundering protocols in the insurance sector were not strictly enforced. Under SP2, the GFC provided an incentive to address some outstanding legal challenges and deficiencies in the regulatory structure that had been identified in SP1. For example, Congress approved amendments to PDIC’s charter, authorizing it to revise its organizational structure as needed and enhancing legal protections for staff. It also permitted special examinations in coordination with BSP in case of elevated risk of bank closure and provided expanded powers, including the ability to lift bank secrecy in case of unsafe and unsound practices, and to rescind splitting of deposits within 120 days before bank closure. 16. A presidential executive order placed the SEC back under DOF jurisdiction and a reorganization plan was launched that refocused operations on core functions, revised the organizational structure and job descriptions, adjusted salary scales, and proposed eventual fiscal autonomy. Interim steps included a rationalization of fees and expenses to boost revenue generation. The Department of Budget and Management (DBM) increased the SEC’s budget from P359 million in 2010 to P541 million in 2011. 13 In addition, the SEC upgraded its surveillance systems. To uniformly enhance supervisory capacity across the financial sector, the newly formed Financial Stability Forum (FSF) undertook a series of actions to improve coordination. First, a memorandum of understanding (MOU) was signed between BSP and other financial sector regulators, which enhanced information exchange and provided a platform to harmonize policies to mitigate regulatory arbitrage. Standing committees were established to address standardization of supervision and risk measurement across regulators, and to optimize the regulatory architecture. Special committees were also formed to address financial advocacy and reporting and information exchange.

3. Improved Efficiency and Liquidity of the Securities Market 17. Under SP1, the government focused on increasing transparency and efficiency in the secondary market and providing for an increased variety of investment alternatives. The SEC issued rules and regulations to implement the Securitization Act of 2004 and drafted amendments for the SRC and Corporation Code to allow dematerialized securities. PDEx and BTr signed an MOU providing PDEx access to the Registry of Scripless Securities, which facilitated the introduction of straight-through processing. The SEC then adopted rules requiring over-the-counter trades to be reported to a central trade register. PDEx followed with an interdealer, order-driven system to process these trades. As a result, price disclosure was enhanced significantly, although data is disseminated only through a fee-based subscription.14

13

The 2011 value includes an allocation of P187 million from excess income. As of the date of this program completion report, the P165 million salary increase for SEC personnel for 2012 and 2013 had not been released.

14 The Fixed Income Broker Internet Order System launched in 2009 extended broker market reach, allowing

nationwide real time access to the trading system and reducing latency for entering client orders. Trading volume transacted through the system increased rapidly from P284 million as of May 2010 to P1,942 million for all of 2010.

6

18. Under SP2, the SEC continued reforms initiated under SP1 by approving PDEx’s central trade reporting system for fixed-income securities. The system provides post-trade transparency as trades must be reported within 30 minutes and are posted daily on PDEx’s website. In addition, the SEC approved PDEx’s rules for listing and trading corporate debt. The government continued initiatives to introduce financial instruments and to improve market liquidity. 15 Specifically, Congress enacted a permanent stamp duty exemption for secondary trading of listed companies over the PSE in 2009.16 The increase in trading volume on the PSE averaged 11.9% during 2006–2011, significantly above the 5% target. Congress approved the Personal Equity Retirement Account Act in 2008 (which provides individuals with a tax free personal retirement account), and approved the law on Real Estate Investment Trust in 2009 (which opens real estate as an investment class to individual investors). In 2008, Congress provided the legal basis for the establishment of a credit bureau.

4. Post-Program Partnership Framework 19. The government and ADB agreed to a post-program partnership framework (P3F) to establish a direction for continuing reforms.17 Learning from the GFC, the FSF has begun to explore de facto joint supervision and regulation of financial submarkets. It consolidated and streamlined reporting requirements by reducing the number of prudential reports required from conglomerates to 50 from 165. Moreover, the government proceeded to further strengthen consolidated financial sector oversight through the Financial Stability Coordinating Council (FSCC), which is an extension of the FSF that also includes the DOF. The FSCC meets bi-monthly and has five primary focus areas: (i) capital market development, (ii) corporate leverage, (iii) shadow banking in real estate, (iv) shadow banking in repurchase agreements, and (v) managing capital flows. It is supported by subcommittees, including one covering the Basel Capital Accord that is evaluating the introduction of over-the-counter derivatives. 20. BSP and PDIC continued the Strengthening Program for Rural Banks, under which rural, thrift and cooperative banks are encouraged to merge, with select regulatory relief provided. As of April 2013, 10 financial institutions had enrolled, covering approximately 3% of total rural bank insured deposits. The government also recognized a need for more efficient and timely resolution of failed banks.18 To meet this goal, PDIC developed, tested and continued to refine bank stress testing and bank failure prediction models. BSP reinforced its Prompt Corrective Action Framework and developed a crisis management protocol. BSP and PDIC also strengthened early coordination to minimize losses to the DIF, under which BSP provides early notification on banks exhibiting a poor supervisory rating, breach of critical performance ratios, or unsafe and unsound activities. This triggers joint examinations, which are increasing from nine banks during October 2009 to May 2010, to 29 banks in the following 7 months. PDIC also established an early trigger mechanism through the Threatened or Impending Bank Closure Framework, which initiates the conduct of a special bank examination that will enable the PDIC to determine the integrity of bank records and appropriate early intervention of failure resolution actions. The PDIC also introduced enhancements in the standard operating procedures for deposit insurance payments, which reduced claims settlement timelines significantly. For example, the average time between bank closure and start of deposit payout has been reduced from 39 days in 2010 to 10 days for the six banks that closed in early 2013 and used the

15 Investment and trading in bonds increased from $47.2 billion in 2006 to $77.3 billion in 2011. Secondary trading in

fixed-income securities increased on average by 8.1% annually in this period. The quarterly yield volatility index decreased from 2.66 in 2006 to 0.14 in 2011, still above the targeted 0.07.

16 The Philippine regulation ranking of securities exchanges improved from 38th in 2006 to 33rd in 2011.

17 This medium-term action plan contained a series of indicative actions designed to continue the momentum of

reform beyond subprogram 2. However, these actions do not represent conditionalities or formal commitments. 18 Since 2006 BSP adopted a risk-based supervisory approach and resolved some 160 weak banks.

7

enhanced procedures. Finally, PDIC has acted to strengthen the proposed Closed Bank Liquidation Act by proposing amendments that would clarify the definition of failure, remove the mandatory 90-day receivership period, and provide for additional resolution methodologies. 21. The government also strengthened nonbank regulators. The SEC began implementing recommendations contained in the action plan developed under SP2 that did not require changes in law. With support of ADB, it has begun to build capacity to bring on-site examinations in line with international standards and to strengthen market surveillance. The SEC is preparing a submission to Congress to amend the SRC to support remaining key reforms in the action plan, and to provide enhanced legal protection of SEC staff. Over the longer term, the SEC plans to submit recommendations for legislation to grant it fiscal and operational independence. In the interim, DBM further increased the SEC budget to P602 million in 2012. Concurrently, the OIC developed and began implementing a restructuring plan similar to that of the SEC, which included (i) a revised organizational structure, (ii) additional deputy commissioners, (iii) an added layer of department managers in line with BSP and the SEC, (iv) modifications to job descriptions and salary structures, and (v) an enhanced budget to ensure the OIC can function effectively as an oversight agency. The DOF has begun to implement its public debt management strategy. DSAs are updated annually, but coverage has been expanded to all financial assets of the national government. The DSA has been strengthened through the inclusion of stochastic simulations and the results are now reported in the more comprehensive Annual Fiscal Risk Statement. C. Program Costs and Disbursements

22. The cost of the program cluster was $400 million. It was funded from ADB’s ordinary capital resources and consisted of two single-tranche loans, comprising $200 million equivalent for SP1 and $200 million for SP2. The first tranche of $200 million was released on 22 December 2006. The second tranche of $200 million for SP2 was released on 13 September 2011. D. Program Schedule

23. The original program cluster period was to run from January 2005 to December 2009. SP1 covered December 2006 to June 2008, while SP2 was to be submitted for Board consideration approximately 18 months after the effectiveness of SP1. However, the program was delayed by the inability of the OIC and SEC to implement indicative actions agreed to under the original program within the specified timelines. While ADB continued its policy dialogue to resolve these issues, events were overtaken by the GFC, which led to the incoming government revising its reform priorities. The delays provided an opportunity to exercise the program’s built-in flexibility to revise SP2 to better reflect the new priorities. The changes were complemented by the strong reform agenda of the newly elected administration. Ultimately SP2 was delayed by almost 2 years, which lengthened the program period to April 2012. E. Implementation Arrangements

24. DOF was the executing agency responsible for the overall implementation of the two subprograms, including compliance with the policy actions, program administration, disbursements, and maintenance of all program records. Under SP1, the SEC served as the sole implementing agency. The SEC established a program coordination committee headed by the SEC chairperson, and comprising representatives from the BSP, DOF, OIC, PDEx, PDIC, SEC, and PSE. The committee was responsible for implementing and sustaining the program components, and in particular, implementing the CMDP action plan. However, SEC retained

8

responsibility for day-to-day program implementation activities and reporting in coordination with the OIC and the PDIC. 25. Under SP2, implementation arrangements improved as DOF took more responsibility by naming the DOF, SEC, BSP, PDIC and OIC as implementing agencies. Further, DOF replaced the SEC as chair of the coordinating committee. This change was precipitated, in part, by dissatisfaction with the performance of SEC as the sole implementing agency under SP1. Also, DOF was in a better position to promote coordination among the agencies. The committee continued to meet semi-annually to coordinate and ensure effective implementation of the proposed reforms. Under the P3F, the DOF would become the coordinating agency and rely on bi-monthly meetings of the FSF to coordinate policy matters related to financial sector regulators. F. Conditions and Covenants

26. The program cluster had 28 policy triggers (see Appendix 2 and 3). In addition to these policy triggers, both subprograms had additional covenants on administering the program, all of which were complied with (see Appendix 4). G. Related Technical Assistance

27. The Strengthening Regulation and Governance TA was processed together with SP1 and strengthened the program by supporting the PDIC, the SEC, and the OIC with specific outputs to meet indicative policy actions necessary for SP2.19 The impact of the TA was an increased contribution by the non-banking and capital markets subsectors to economic growth and development. Its scope parallels that of the program and shares the same objectives: (i) strengthen macroeconomic stability; (ii) strengthen governance, regulation, and intermediation; (iii) enhance transparency and market efficiency; and (iv) improve operational efficiency and reduce financial sector vulnerabilities. The TA was rated partly successful given the disparate level of success across its components:

(i) Component I. Programmed assistance to PDIC included strengthening its bank resolution methods by developing a framework to increase the efficiency of asset disposal. The component was considered to be highly successful and led to a change in the PDIC’s Charter in 2009, which strengthened its powers and flexibility. PDIC also established policies to support investigating the causes of bank failures and to pursue civil and criminal charges as appropriate. Asset disposition methodologies were enhanced, but bank resolution methods could not be further improved within the TA timeframe due to a lack of enabling legislation.

(ii) Component II. The second component was designed to strengthen the SEC’s capacity to supervise and regulate secondary trading of fixed-income securities and supported the development of an action plan for moving to a dematerialized environment. The TA was to provide training to ensure that compliance with IAS 39 was effectively monitored and that material information would be promptly disclosed by public companies and insiders.20 It also included advice on standardizing books and records of investment houses and other non-bank financial institutions, while also strengthening related audit procedures. Additional accomplishments included

19

Two TA projects supported the SEC: ADB. 2003. Technical Assistance to the Republic of the Philippines for the Support for Nonbank Financial Governance II. Manila (TA 4168-PHI for $500,000) and ADB. 2004. Technical Assistance to the Republic of the Philippines for Strengthening Governance of Securities Trading Markets. Manila (TA 4321-PHI for $250,000).

20 IAS 39 (Financial Instruments: Recognition and Measurement) outlines the requirements for the recognition and

measurement of financial assets, financial liabilities, and some contracts to buy or sell non-financial items.

9

the acquisition of a new trading surveillance system and standardized reporting for broker-dealers. Nevertheless, the SEC component was considered partially successful as wider objectives such as capital market development and improved governance were not attained within the TA period. For example, the CMDP was overly prescriptive. Implementation was incomplete and a sizable number of deviations were noted.21 Efforts to broaden the shareholder base of the PSE after demutualization stalled and requirements to increase the free float of public companies and add liquidity to the market were suspended. While an SRO was introduced to govern secondary trading in the debt markets, the SEC has yet to conduct a comprehensive onsite audit of PDEx and its participants due to legal and human resource constraints.

(iii) Component III. The TA was scheduled to provide the OIC support to: (i) develop practices and methodologies to implement risk-based supervision; (ii) develop a strategy to fully implement the International Association of Insurance Supervisors 28 core principles; (iii) design a road map to guide development of the insurance sub-sector; (iv) implement a reorganization; and (v) develop analytical processes and manuals to support the upgrading of information and communication technology, including the introduction of electronic filing and analysis. This component was considered unsuccessful as few of the targeted reforms were introduced within the timeframe of the TA and the assistance had to be withdrawn by ADB due to performance issues associated with the OIC’s contribution to FMRIP, although performance improved substantially under the new commissioner.22

28. The TA was to be implemented over 8 months, ending on or before September 2007. Total consultant input was estimated at 21 person-months of international consultant and 24 person months of national consultant services. At the time of approval, the TA cost was estimated at $800,000, but actual disbursements amounted to $547,000. The TA closed on 16 March 2010, compared to the originally foreseen date of 5 August 2007. This extension reflects the difficulties encountered during implementation as well as the crucial role that the TA played in assisting SEC and PDIC to prepare for and support SP2. H. Consultant Recruitment and Procurement

29. The TA clearly spelled out the activities and the detailed terms of reference for individual consultants. Six international consultants were recruited for an aggregate total of 18 person months: (i) a banking resolution expert, (ii) a financial supervision and deposit insurance legal expert, (iii) an asset management and disposal expert, (iv) a capital markets regulatory expert, (v) a risk management expert, and (vi) a bond market expert. Two national consultants were recruited for an aggregate total of 11 person months: (i) a legal expert (scripless securities), and (ii) an accounting expert. The project was supported by a national project administrator. All consultants delivered on their individual terms of reference and submitted final reports, which

21

As of 30 September 2007, 116 achievements were noted. Of these 116 actions, 46 represented original actions called for in the plan, 17 had been revised or expanded, and 53 reflected entirely new actions which were not contemplated by the original plan. Around 85% of initiatives were eventually completed.

22 DOF approved an OIC reorganization plan, which served as a policy trigger for the disbursement of SP1. Under

the P3F, the commission was to implement a re-organization as contemplated by this plan along with revised job descriptions and qualifications. However, subsequent to disbursement, the OIC implemented a significantly different reorganization plan without addressing the structural weaknesses that had given rise to the original plan, or notifying ADB. The OIC delayed implementation of higher minimum capital levels for the insurance subsector. The insurance market continued to develop, however, with an increase in insured population from 14.2% in 2006 to 18.3% in 2011 (below the 20% SP1 target). Insurance premiums as a percentage of GDP increased from 1.04% in 2010 to 1.15% in 2011.

10

were discussed with the executing or implementing agency before finalization. All but one of the individual consultants performed their assigned tasks satisfactorily. I. Performance of the Borrower and the Executing Agency

30. The performance of the government is rated less than satisfactory, although it improved significantly during SP2. Implementing agency performance varied widely under SP1 and a lack of sufficient progress in program implementation resulted in significant delays. In retrospect, too much authority for managing reforms may have initially been delegated to the SEC, which was not able to exercise unilateral authority to implement reforms; the level of ownership and support of the CMDP also varied across agencies and private sector organizations. Given these constraints, even the SEC’s commitment to pursuing CMDP objectives declined over time.23 The government was also unable to swiftly approve essential legislation within the timeframe of SP1 or, in some situations, even the program cluster. 31. Internal arrangements improved over time as the executing agency took more control at the onset of SP2 and replaced the SEC as chair of the coordinating committee. The addition of the DOF, BSP, PDIC and OIC as implementing agencies provided additional incentives for the agencies to play an active role in program implementation. In conjunction with TA support, a range of other policy reforms and capacity development was successfully implemented (see Appendixes 2 and 3). By 2011, program activities and TA under the program cluster had contributed to the target achievement of 48% of 44 performance indicators in the original and the revised design and monitoring framework (DMF). Progress was visible in another 30% of the DMF indicators, while performance deteriorated for the remaining 23% (see Appendix 6). J. Performance of the Asian Development Bank

32. The performance of ADB has been satisfactory. A key determinant in this assessment is the ADB’s response to slow progress in SP1 amidst a rapidly changing external environment. ADB actively engaged with the government, seeking to resolve outstanding issues, improve implementation arrangements, and ensure program readiness at implementing agencies. ADB also made the cluster program more relevant by using its built-in flexibility and increasing the focus on financial sector stability and supervision. 33. The design of the associated TA project was relevant and partially satisfactory. TA resources were increasingly targeted at implementing agencies that showed sufficient commitment to reform, facilitating their readiness for SP2. The decision to withhold resources from an implementing agency that had become less committed to implementing required reforms was considered appropriate and efficient. As part of the program completion review, ADB requested the government to provide its assessment of the program through a survey questionnaire completed by the implementing agencies (see Appendix 7). Overall, the government rated the program favorably in terms of relevance, efficiency, effectiveness, and likely sustainability (see Appendix 7).

23

The SEC was responsible for 25 of 39 indicative policy actions for SP2, nine of which were treated as fully and one as partially accomplished in a government readiness assessment in 2009. It did not strengthen market surveillance, monitoring of broker-dealers, and PSE self-regulatory functions in the planned timeframe. It also failed to lodge required legislative amendments with Congress. The OIC faced most significant delays, with only two of six indicative policy actions accomplished, while PDIC showed the most commitment to reforms.

11

III. EVALUATION OF PERFORMANCE A. Relevance 34. At time of approval, the program cluster was relevant to the government’s reform agenda. The FMRIP and its linked TA were designed to support implementation of the CMDP and in turn, to assist the government in achieving the objectives of the MTPDP. Its desired impact was an increased contribution of the financial sector to economic growth, poverty reduction, and development through: (i) enhanced financial system stability by strengthening the government’s debt issuance and management processes, (ii) improved resolution of problem banks and strengthened solvency and administration of PDIC, (iii) strengthened nonbank financial sector governance, and (iv) improved efficiencies and transparency in the securities market. In 2010, the relevance of the program was further enhanced by increasing its focus on financial sector stability and supervision, in line with changes in the external environment and the government’s reform priorities. The initial program design was also fully aligned with the CSP 2005–2007, which targeted ADB’s engagement in three broad areas: the power sector, financial markets, and governance, including reforms of local government and the judicial system. 35. The program cluster remained largely relevant at time evaluation. The Philippine Development Plan 2011–2016 contained a broad range of financial sector reforms in support of sustainable and inclusive growth. It shared or built on many important elements of FMRIP, including (i) alignment of the mandates of regulatory and supervisory authorities with international best practice; (ii) providing an enabling environment for long-term savings; (iii) reliable capital market infrastructure; (iv) strengthened legislative mandates for the BSP, SEC and OIC; (v) harmonized regulatory and supervisory oversight through cooperative arrangements; and (vi) risk-based capital adequacy frameworks. At the same time, there was a shift in emphasis to issues such as financial literacy, national financial inclusion, microfinance, development of auxiliary markets through forwards and cash markets, and faster integration of the financial system in the ASEAN region.24 Most implementing agencies rated the program as relevant both at the time of formulation and after its completion (see Appendix 7). B. Effectiveness in Achieving Outcome

36. The program is rated effective in achieving the outcome: a deeper, more diversified and resilient financial sector. Eight out of nine outcome indicators in the original and revised DMF, including those discontinued in SP2, either met their target (five) or progressed (three). While identifying a range of continuing challenges, assessments provide a picture of a financial sector that—supported by improvements in financial market infrastructure, regulation, and supervision—has become more healthy, efficient, and balanced. Most importantly, the government’s improved fiscal position, declining budget deficits and the extended maturity structure of outstanding government debt has led to an upgrade of the Philippines’ credit rating to Investment Grade. External assessments such as the World Economic Forum’s Financial Development Report and the International Monetary Fund’s Financial Sector Assessment Program also document qualitative improvements in financial sector health and governance.

37. With regard to tangible and measurable results, the program cluster achieved or progressed on 78% of the performance indicators in the original and the revised DMF, including those discontinued in SP2. In particular, significant progress was achieved in reducing the level of NPLs within the banking system. While the share of nonbank financial sector as a percentage

24

Government of the Republic of the Philippines, National Economic Development Authority. 2011. Philippine Development Plan 2011–2016. Manila.

12

of total financial assets just met the revised target of 23%, the size of the local debt and equity markets have both increased with issuances of equity and bonds now representing 40% of total financing in 2012 (Figures 1 and 2). Overall, domestic bank credit as a proportion of total domestic financing has declined to 28% as of September 2012 from a high of 41% in December 2008.25 Liquidity has also improved as evidenced by increased trading volumes on the PSE and PDEx. The stock market to GDP ratio significantly overshot the targeted 50%–55% with a ratio of 73.6% in 2011, although this may be due in large part to the accommodative monetary policy in the United States and Europe. The contractual savings sector expanded as the percentage of the population insured has risen to 18% in December 2012 from 14% in December 2006.

38. Over the program period, the Philippines experienced improved macroeconomic conditions, a steady inflow of remittances, and a low dependence on exports. Combined with the financial sector reforms supported by the program, and a nominal exposure to structured products, the Philippines avoided the worst difficulties encountered by other economies during

25

AsianBondsOnline, http://asianbondsonline.adb.org/

Figure 1: Equity Financing (P billion)

Source: International Monetary Fund, 2013 Note: based on Philippine Stock Exchange, Bloomberg, and International Monetary Fund staff data.

Figure 2: Corporate Bond Issuance (P billion)

Source: International Monetary Fund, 2013 Note: based on Philippine Stock Exchange, Bloomberg, and International Monetary Fund staff data.

13

the GFC.26 The government’s own assessment shows that, overall, the program was viewed as effective (see Appendix 7). C. Efficiency in Achieving Outcome and Outputs

39. The program is rated less than efficient in achieving its outcome and outputs. Significant delays in implementation of SP1 required an extension of the program cluster period by almost 2 years. This delay was due primarily to a lack of political will to complete difficult reforms in the insurance sector, the time needed to develop legislation, and resistance to a narrow range of reforms within the SEC and select capital market stakeholders. Nevertheless, the delays were managed efficiently by the DOF, implementing agencies and ADB. In terms of cost, ADB withdrew TA resources from unresponsive implementing agencies and projects. Under SP2, the incoming government strongly supported the resumption of financial sector reforms and led reformulation of SP2 to address emerging issues that enjoyed strong stakeholder support. Overall, the government rated the program as efficient (see Appendix 7). D. Preliminary Assessment of Sustainability

40. The program is considered likely to be sustainable. While legislative changes may have been associated with delays during program implementation, the eventual adoption of legislation to strengthen PDIC’s charter and operations, increase capitalization in the insurance sector and facilitate the expansion of the capital markets are difficult to delay or reverse. The adoption of international best practices such as IAS and IOSCO Memorandum Annex B have been accepted into the markets and are also considered permanent in nature. At the same time, efforts to improve the capacity of supervisory and regulatory agencies such as the SEC and OIC have been supported by higher budget allocations, salary increases, and more legal protection for staff. Although there are higher budget allocations for SEC in the appropriation law, these have not yet been matched with actual fund releases from the budget department, which has hampered reforms and could adversely affect the sustainability of SEC-related reforms if budgeted funds are not released. However, institutional arrangements, such as the FSF, seem to be strengthening and resilient to changes in financial, economic, and political conditions. E. Impact

41. The impact of the program is rated moderate. While it is difficult to isolate the impact of FMRIP reforms, particularly in a post-GFC environment, performance indicators paint an increasingly positive picture of financial sector development overall and indicate improved access to finance and an increased contribution of the financial sector to economic growth. Of the 10 impact indicators in the original and revised DMF, four targets were achieved, four indicators progressed, and two regressed. Real GDP growth increased from 5.2% in 2006 to 7.6% in 2010—in the middle of the target range of 7% to 8%—but dropped sharply to 3.9% in 2011 due to the carryover effects of the GFC.27 In the same period, the savings to GDP rate increased from 16.2% to 18.6%, but remained below the target range of 25%–30%. The investment to GDP ratio increased from 18.0% to 21.7%, falling short of the SP1 target but exceeding the SP2 target by 1.7%. Neither target set for the M2/GDP ratio was met, although it increased slightly (from 45.1% to 47.1%).

26

Government of the Republic of the Philippines, National Economic Development Authority. 2011. Philippine Development Plan 2011–2016. Manila.

27 Note that GDP growth is impacted by many other factors. In 2010 the contribution of the finance subsector to GDP

growth was estimated at 0.4 percentage points, up from 0.3 percentage points in the preceding year.

14

42. The revised DMF added a number of quantitative and independently verifiable performance indicators that exhibited a more causal relationship with the program’s activities. The Business Constraint Index for access to credit declined significantly from 31.8 in 2005 to 16.7 in 2011, almost reaching the targeted 15, but rose to 18.6 in 2012 as credit conditions tightened slightly. However, the Overall Financial Access score produced somewhat counter-intuitive results, dropping from to 53rd place in 2012 from 43rd in 2008. Otherwise, the projected improvements in the Financial Stability Index and levels of bond market turnover were achieved.

IV. OVERALL ASSESSMENT AND RECOMMENDATIONS

A. Overall Assessment

43. The program is rated successful. The FMRIP program cluster was a relevant program with strong links to the government’s reform agenda, its national development plan, the CMDP, and ADB’s country strategy and program at the time of approval. Although as designed the program was driven by demand, initial commitment to the CMDP varied across agencies and suffered from slow legislative processes. However, over time, a renewed commitment emerged from the government, DOF, supervisory and regulatory agencies, SROs, and other stakeholders to prioritize financial sector reforms. This commitment accelerated the pace of reforms and contributed to the completion of key accomplishments which appear to be highly sustainable.

B. Lessons

44. FMRIP and its associated TA underscored some of the key lessons noted in the program completion report for the Second Nonbank Financial Governance Program.28 First, programs and TA should not depend on passage of law in countries where legislative processes are slow and cumbersome. In this case, reforms to the bank resolution process, such as the authorization of bridge banking powers for PDIC, rely on the passage of legislation, and are still pending. The administrative increase in minimum capital requirements for the insurance subsector was embroiled in controversy and delay, but now appears to be required by law, but only following a 7-year delay (footnote 13). Therefore, where legal amendments are necessary or can make reforms more sustainable, programs and TA should support drafting of legislation, but also enhance the regulatory framework that complements legislative changes. 45. Second, there should be strong and widespread political will. For example, the CMDP was initiated unilaterally by the SEC and clearly was not reflective of industry sentiment and therefore did not enjoy widespread support. In the case of the OIC, pressure from the industry to postpone higher required capitalization contributed to a change in the Insurance Commissioner and a reduction in political will in support of reform. However, the pace of program implementation and reforms accelerated significantly under the new government. A new capital market development plan was launched, under the close leadership of the MOF, which benefited from widespread stakeholder consultations and support. Likewise, increased capital standards have been applied legislatively to the insurance sector with strong MOF support. 46. Third, program design should focus on implementing reforms not only where commitment is strong, but where resources and external factors are adequate to ensure successful implementation. In the case of the SEC, a persistent and chronic shortage of funding initially compromised its ability to provide effective surveillance and supervision to the capital markets. Additional budget increases still appear necessary to bring OIC and SEC remuneration

28

ADB. 2013. Philippines: Local Government Financing and Budget Reform Program Cluster. Program Completion Report. Manila.

15

in line with the BSP, as mandated by Republic Act No. 8799 and Republic Act No. 9829. Further, until enforcement officials are sufficiently protected from frivolous and intimidating lawsuits, expectations of strong enforcement actions may be unrealistic. C. Recommendations

1. Program Related

47. Future monitoring. As legislative processes can be slow, it is essential to continue to monitor the status of essential amendments that are still pending in Congress, such as PDIC’s request for enhanced resolution powers. In addition, adequate budget resources are required to strengthen the capacity of the non-bank regulatory agencies. Given their lack of fiscal independence, ADB should monitor ongoing budget allocations and expeditious fund releases to both the SEC and OIC to assure funding remains adequate to complete the proposed reforms. In future program loans and projects ADB should request that the government, through its budget department and project beneficiaries, submit progress reports on actual funding releases and retention of fees to ensure completion of reforms. 48. Additional assistance. Although the country partnership strategy for 2011–2016 does not prioritize financial sector development, it remains a government priority.29 Furthermore, political will is currently high with a potential that significant reforms will continue until 2016. It is therefore important to sustain reform momentum and ADB’s engagement in this sector throughout this period. Considering the effective role that TA played in sustaining policy reform and building capacity at specific agencies, targeted TA should be continued that focuses on the government’s efforts to implement the Treasury Single Account and any associated required capital market reforms.

2. General

49. The success of proposed financial sector and other reforms in the Philippines is highly dependent on political will, which is likely to be highest in the early years of an administration. In the case of the program, the reform agenda of the previous administration faded over time, which contributed to implementation delays. The GFC and the strong reform agenda of the current administration combined to accelerate reforms, while the built-in flexibility of SP2 provided ADB with the means to capture this momentum and complete the program. Thus, ongoing policy dialogue should prepare ADB to react quickly to meet emerging reform champions and sufficient flexibility should be incorporated into program design to accommodate modifications of program scope and coverage. Such flexibility is a necessary component for successful financial sector programs, in particular, given the increased volatility in global financial markets. In addition, ongoing small-scale TA should be provided to increase the capacity of the weaker regulatory organizations, while larger and more focused TA should be directed at individual agencies that exhibit both the willingness and technical capacity to complete more complex reforms. 50. To the extent possible, DMF performance indicators should exhibit a close causal relationship with contemplated program activities. Use of broad economic indicators introduces additional factors into the assessment and complicates the evaluation of effectiveness. For example, the effects of the GFC produced a setback in a number of indicators despite the completion of fundamental reforms that otherwise increased participation in, and the activity of, various financial subsectors.

29

ADB. 2011. Country Partnership Strategy: Philippines, 2011–2016. Manila.

Appendix 1

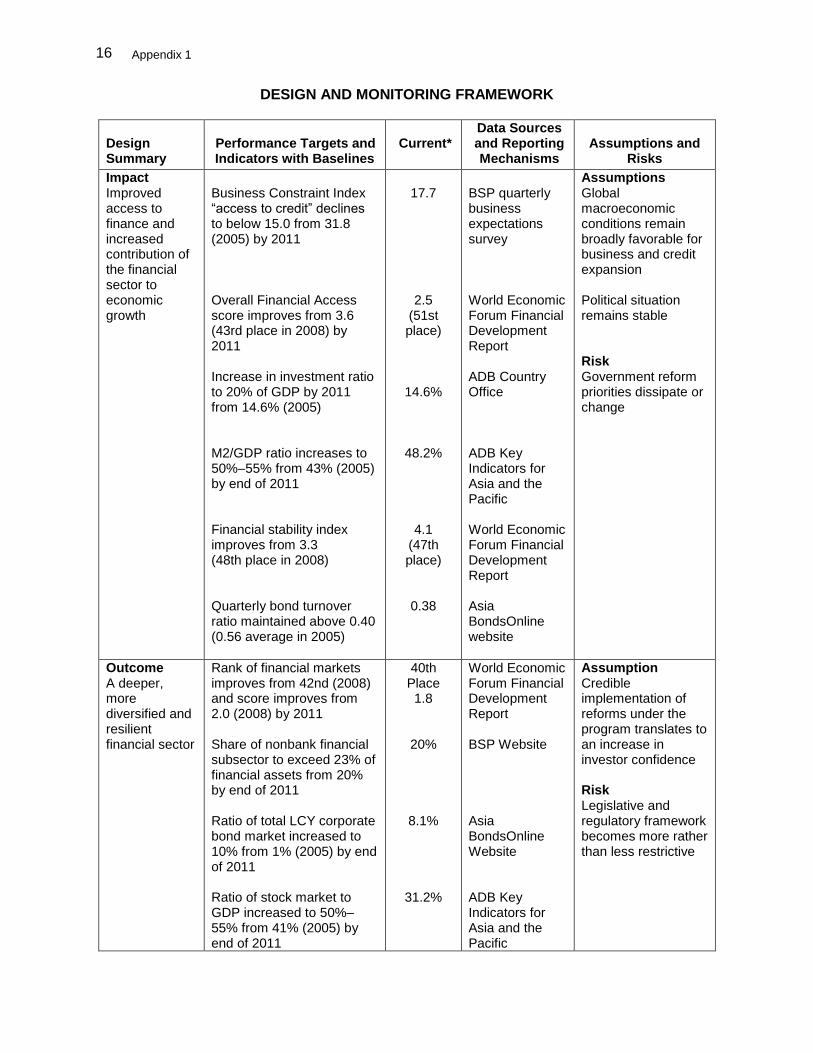

16

DESIGN AND MONITORING FRAMEWORK

Design Summary

Performance Targets and Indicators with Baselines

Current*

Data Sources and Reporting Mechanisms

Assumptions and

Risks

Impact Improved access to finance and increased contribution of the financial sector to economic growth

Business Constraint Index “access to credit” declines to below 15.0 from 31.8 (2005) by 2011 Overall Financial Access score improves from 3.6 (43rd place in 2008) by 2011 Increase in investment ratio to 20% of GDP by 2011 from 14.6% (2005) M2/GDP ratio increases to 50%–55% from 43% (2005) by end of 2011 Financial stability index improves from 3.3 (48th place in 2008) Quarterly bond turnover ratio maintained above 0.40 (0.56 average in 2005)

17.7

2.5 (51st place)

14.6%

48.2%

4.1 (47th place)

0.38

BSP quarterly business expectations survey World Economic Forum Financial Development Report ADB Country Office ADB Key Indicators for Asia and the Pacific World Economic Forum Financial Development Report Asia BondsOnline website

Assumptions Global macroeconomic conditions remain broadly favorable for business and credit expansion Political situation remains stable Risk Government reform priorities dissipate or change

Outcome A deeper, more diversified and resilient financial sector

Rank of financial markets improves from 42nd (2008) and score improves from 2.0 (2008) by 2011 Share of nonbank financial subsector to exceed 23% of financial assets from 20% by end of 2011 Ratio of total LCY corporate bond market increased to 10% from 1% (2005) by end of 2011 Ratio of stock market to GDP increased to 50%–55% from 41% (2005) by end of 2011

40th Place 1.8

20%

8.1%

31.2%

World Economic Forum Financial Development Report BSP Website Asia BondsOnline Website ADB Key Indicators for Asia and the Pacific

Assumption Credible implementation of reforms under the program translates to an increase in investor confidence Risk Legislative and regulatory framework becomes more rather than less restrictive

Appendix 1 17

Design Summary

Performance Targets and Indicators with Baselines

Current*

Data Sources and Reporting Mechanisms

Assumptions and

Risks

Outputs 1. Enhanced financial sector stability 2.Strengthened financial sector regulatory oversight 3. Financial sector efficiency and liquidity are improved

Quarterly average yield volatility index remains below 0.07 in 2011 from 0.135 (average in 2006) External debt ratings improve (BB- negative) Improved coordination and disclosures from FSF by 2011 Increase from 38th place (4.8 in 2008) in regulation of securities exchanges External assessments of regulatory strength and effectiveness Quarterly bond market trading volume sustained above $25 billion ($12 billion Q4 2005) Average daily trading volume on PSE increases from P1.5 billion (2005) to P6 billion by end of 2011

0.089 (2010

(year-to date)

average

BB– stable

--

44th place

4.2

--

$22 billion (Q2 2010)

P4.1 billion

Asia BondsOnline website External ratings agencies (S&P) FSF website (pending development) World Economic Forum Global Competitiveness Report IMF mission reports Credit rating agency reports Asia BondsOnline website SEC website

Assumption Improved public debt management practices generate additional revenues Risk Fiscal deficit is not contained Assumption Agencies possess adequate absorptive capacity and skill sets and are jointly harmonized Risk Agency budgets do not receive adequate support

Activities with Milestones

A. Enhance Financial Sector Stability 1.1 Take measures to enhance financial sector stability 1.2 BSP introduced a set of short-term measures to enhance financial

sector stability (November 2008) 1.3 BSP submitted draft amendments to Congress to strengthen monetary

policy (June 2009) 1.4 PDIC board approves Strengthening Program for Rural Banks (November

2010) 1.5 Congress passed amendments to the PDIC Act (April 2009) 1.6 PDIC adopted an appropriate build-up strategy for the deposit insurance

fund (June 2009) 1.7 PDIC board to approve a proposal for legislation to establish bridge

banking and other resolution methods (November 2010)

Inputs

ADB subprogram 2 loan: $200,000,000

18 Appendix 1

ADB = Asian Development Bank, BSP = Bangko Sentral ng Pilipinas, DBM = Department of Budget and Management, DOF = Department of Finance, FSF = Financial Stability Forum, GDP = gross domestic product, IMF = International Monetary Fund, LCY = local currency, M2 = money and close substitutes for money, PDIC = Philippine Deposit Insurance Corporation, PSE = Philippine Stock Exchange, Q = quarter, S&P = Standard & Poor’s, SEC = Securities and Exchange Commission. -- = data not available * Current refers to the most recent data available as of the Program date. Source: Asian Development Bank.

Activities with Milestones 1.8 Financial Sector Assessment Program completed (January 2010) 2.1 Strengthen public debt management 2.2 DOF to enhance capacity for public debt management (November 2010) B. Strengthen Financial Sector Regulatory Oversight 1.1 Improve interagency coordination and sharing of information 1.2 FSF improved coordination among key regulators (December 2009) 2.1 Strengthen regulators’ enforcement powers 2.2 BSP submitted draft amendments to its charter to Congress (June 2009) 2.3 Congress approved amendments to PDIC legislation (April 2009) 2.4 DOF to reassume administrative control over SEC (November 2010) 2.5 DOF to endorse action plan for restructuring SEC (November 2010) 2.6 DOF and DBM to increase SEC budget for 2011 and implement revised

budget methodology (November 2010) 3.1 Strengthen market surveillance 3.2 SEC to implement measures to enhance its capacity for market surveillance

(November 2010) 3.3 Insurance Commission initiated risk-based capital regime for life insurance,

non-life insurance, and mutual benefit associations (December 2009) C. Improve Efficiency and Liquidity of Securities Markets 1.1 Develop an efficient and liquid secondary market for government and

corporate debt 1.2 SEC approved central trade reporting system and associated listing

requirements and trading rules (January 2008) 2.1 Deepen financial markets 2.2 Congress enacted the following: Personal Equity Retirement Account Act (August 2008) Permanent stamp duty exemption for secondary trading of listed

companies (June 2009) Real Estate Investment Trusts Act (December 2009) Credit Information System Act (October 2008) 3.1 Strengthen the self-regulatory structure of the capital markets 3.2 SEC to show progress in addressing nine of the 17 deficiencies in the PSE

performance audit (November 2010)

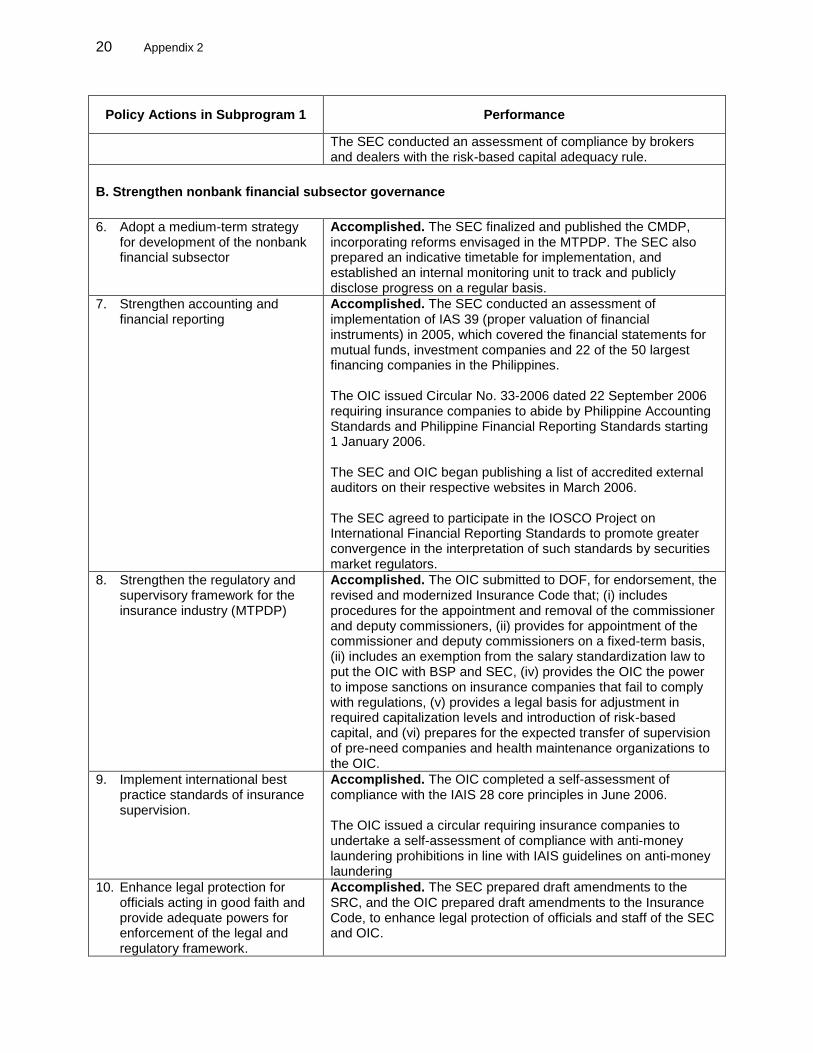

Appendix 2 19

PERFORMANCE OF FINANCIAL MARKET REGULATION AND INTERMEDIATION PROGRAM, SUBPROGRAM 1 – POLICY ACTIONS

Policy Actions in Subprogram 1 Performance

A. Enhance Financial Stability

1. Create a stable financial environment conducive to growth through improved debt and risk management.

Accomplished. BTr improved debt management by: (i) reducing the share of variable rate international bonds to below 10% of the total (all new issuances have been in fixed rates); (ii) altering the currency composition of international debt; and (iii) entering into domestic debt swaps to consolidate the number of outstanding issues to create more liquid instruments and create benchmark 3-, 5-, and 7-year peso-denominated bonds.

2. Reduce ratio of nonperforming assets in the banking system

Accomplished. Republic Act No. 9343—the Special Purpose Vehicle (SPV) Act—was amended to extend the deadline for the establishment of SPVs for 18 months from 19 September 2004, and in addition, to reset the deadline for the use of tax benefits for 2 years from April 2005.

3. Expand and enhance asset management resolution and liquidation methods and capacity

Accomplished. PDIC management submitted to the PDIC board of directors a proposal for enhancing the framework and guidelines on the provision of financial assistance to distressed banks.

4. Ensure the adequacy of the Philippine Deposit Insurance Fund (DIF) to address perceived risks

Accomplished. After the increase in deposit coverage to P250,000, PDIC conducted a comprehensive study of the DIF in 2006 to reassess the maximum insurance cover, assessment rate, and assessment base. In addition, PDIC formulated a trading and investment policy with the aim of optimizing returns on the DIF.

5. Strengthen the financial condition of nonbank financial institutions

Accomplished. DOF issued Department Order 19-6 in May 2006 to raise the minimum capitalization for new life, nonlife, and reinsurance companies. Effective 1 July 2006, the minimum capital for new life and nonlife insurance companies will be P1 billion and for new reinsurance companies, P2 billion. DOF issued Department Order 27-6 to raise minimum capitalization for existing insurance companies to P100 million effective 31 December 2006. The OIC issued new risk-based capital rules for life and nonlife insurance companies, effective August 2007, requiring that risk-based capital be computed based on annual financial statements. Insurance companies were given 2 years to comply. The OIC issued Memorandum Circular No. 1-2006 in May 2006 to raise the capital requirements for existing insurance and reinsurance brokers to P2 million by 31 December 2006, and by another P2 million each year to reach P10 million by 31 December 2010. The OIC also raised the capital requirements for new brokers undertaking either insurance or reinsurance brokerage to P20 million, and for brokers undertaking both insurance and reinsurance brokerage to P50 million, effective 1 July 2006.

20 Appendix 2

Policy Actions in Subprogram 1 Performance

The SEC conducted an assessment of compliance by brokers and dealers with the risk-based capital adequacy rule.

B. Strengthen nonbank financial subsector governance

6. Adopt a medium-term strategy for development of the nonbank financial subsector

Accomplished. The SEC finalized and published the CMDP, incorporating reforms envisaged in the MTPDP. The SEC also prepared an indicative timetable for implementation, and established an internal monitoring unit to track and publicly disclose progress on a regular basis.

7. Strengthen accounting and financial reporting