financial literacy and entrepreneurial intention of

TRANSCRIPT

351

25 FINANCIAL LITERACY AND ENTREPRENEURIAL INTENTION OF GENERATION “Y” GRADUATES: AN ANALYSIS BASED

ON THE THEORY OF PLANNED BEHAVIOR

ABSTRACT

A cross-sectional survey was carried out and data was collected from 226 graduates. Descriptive statistics, factor loading, reliability statistic and multiple regression were used based on Statistical Package for the Social Sciences (SPSS) and Structural Equation Modeling (SEM) the research model. Result of the analysis shows that FL has positive and significant relationship with attitude towards new venture creation (AVC), social norms (SN) and perceived behavioural control (PBC) and concludes that This research recommends that institutions of higher learning should emphasize pedagogies in financial management that encourage graduates toward self-employment Also financial institutions need to emphasize business plan, character and education as foremost consideration for advancing entrepreneurial loan to prospective graduate entrepreneurs

Keywords: Financial literacy, graduate entrepreneurial behavior.

Graduate entrepreneurship intention is a major determinant of entrepreneurial behaviour. However, the factors affecting entrepreneurial intention to influence the behaviour have not been adequately investigated. How financial literacy (FL) affects generation Y graduate entrepreneurial intention remains unknown. In order to cover this important gap, FL is conceptualized as financial knowledge (FK), financial attitude (FK), and financial behaviour (FB).

HASSAN BARAU SINGHRY PhD (Mgt), MSc (Mgt), MBA, MBF, BSc

Faculty of Management Sciences, Abubakar Tafawa Balewa University Bauchi

and PATRICK BOGORO PhD (Mgt), MBA, BSc

Faculty of Management Sciences, Abubakar Tafawa Balewa University Bauchi

26

IJMSR Vol. 2 No. 1

1.0 INTRODUCTION: unemployed (Chinyere & Faith, 2012NBS, Graduate entrepreneurial intention (GEI) 2014). Although entrepreneurship study is remains an interesting research topic with compulsory to all undergraduates, macro and micro impact on employment, researchers are not sure of its impact on income generation, wealth creation, graduates FL. Lack of FL could make poverty alleviation and economic GenYG unable to participate in the formal development. Despite these advantages, the financial system and also identify the best prospect of graduates' employability in sources of funding new venture. (Abbasian Nigeria's public and organized private & Yazdanfar, 2013; Central Bank of sector is uncertain. Statistics showed that of Nigeria, 2015). Fourth, most GenYGs are the total level of employment across poor as such lack the seed capital for new economic activities in Nigeria, only 11.9% venture creation (Nkundabanyanga, graduates are employed (NBS, 2014) Kasozi, Nalukenge, & Tauringana, 2014). Although factors such as cognitive model In order to cover the gaps and provide ((Liñán & Chen, 2009); education and recommendation for solving the problems psychological factors ((Marques, Ferreira, above, this paper attempts to investigate Gomes, & Rodrigues, 2012), and how FL could influence GEI. entrepreneurial capabilities (Karra, Phillips, & Tracey, 2008; Singhry, 2015) FL refers to knowledge and understanding affect entrepreneurial intention, empirical of financial concepts and risks, and the literature shows that the factors affecting skills, motivation and confidence to apply entrepreneurship intention have not been such knowledge and understanding in order identified and examined adequately. This to improve the financial well-being of research attempted to cover this gap by individuals and society, and to enable exploring how financial literacy (FL) participation in economic life (OECD, influence GEI. FL is an important capability 2015). It also means the possession of in the long process of new venture creation knowledge and skills by individuals to (Xiang & Worthington, 2015). manage financial resources effectively in

order to enhance their economic well-being This study is motivated by three factors. (Central Bank of Nigeria, 2015). FL can First, empirical research on GEI mostly help GenYGs to make effective financial focus on developed countries despite the decisions so as to intelligently source, finding that GEI is stronger in developing s p e n d , a n d m a n a g e m o n e y f o r countries (Iakovleva, Kolvereid, & entrepreneurial, personal and societal well-Stephan, 2011; Nabi & Lin, 2011). Second, being (Caroline, Potrich, Vieira, & Mendes-while antecedents such as education , Da-Silva, 2016; Hasnol & Salleh, 2015; motivation and obstacle (Olufunso, 2010) Te'eni-Harari, 2016). FL could help and FL in south Africa ((Oseifuah, 2010), graduate not only identify and source start-such study is unknown in Nigeria. Third, up fund but also manage finance for Nigeria's generation Y graduates (GenYG) successful business operations. are facing high rate of structural unemployment. Statistics showed that It can also help Gen YGs to access credit, institutions of higher learning turn-up budget, control spending, handle debt, approximately 1.8 million graduates each participate in both formal and informal year and more than 80% remain structurally financial markets, and attain financial,

352

FINANCIAL LITERACY AND ENTREPRENEURIAL INTENTION OF GENERATION “Y” GRADUATES:

AN ANALYSIS BASED ON THE THEORY OF PLANNED BEHAVIOR

IJMSR Vol. 2 No. 1

mental and emotional health (Abubakar, intends to perform the behavior; Social 2012). In this study, financial literacy norms explains how the opinion of consists of financial knowledge, financial important people influence ones intention to behavior and financial attitudes. perform a particular behavior; perceived

behavioral control captures the ease and/or Graduate entrepreneurship is the difficulty to perform a certain behavior “interaction between the graduate as the (Ajzen, 1991). TPB posits that intention to product of university education and perform a given behavior is determined by business start-up in terms of an individual's attitude toward behavior; subjective norms; career-orientation and mindset towards self- and perceived behavioral control (Ajzen, employment” (Davey, Plewa, & Miemie, 1991; Maresch, Harms, Kailer, & Wimmer-2011). GenYG is a group of young people wurm, 2016). Personal attitude reflects the born between 1981 and 2000, who have perceived desirability of performing the obtain a degree and higher national diploma behaviour while perceived behavioural certificates, grew up in a world with global control reflects perceptions that the e c o n o m i c p r o s p e r i t y a n d l o w behaviour is personally controllable. unemployment but are now experiencing an Attitude towards self-employment is the era of economic recession and structural perceptions of the personal desirability of u n e m p l o y m e n t . G e n Y G s a r e performing the behaviour. High attitude technologically savvy and have work towards self-employment often indicates experience from internship and part-time that the respondent is more in favour of self-work during their studies (Fok & Yeung, emp loymen t t han o rgan i za t i ona l 2016) employment (Küttim, Kallaste, Venesaar,

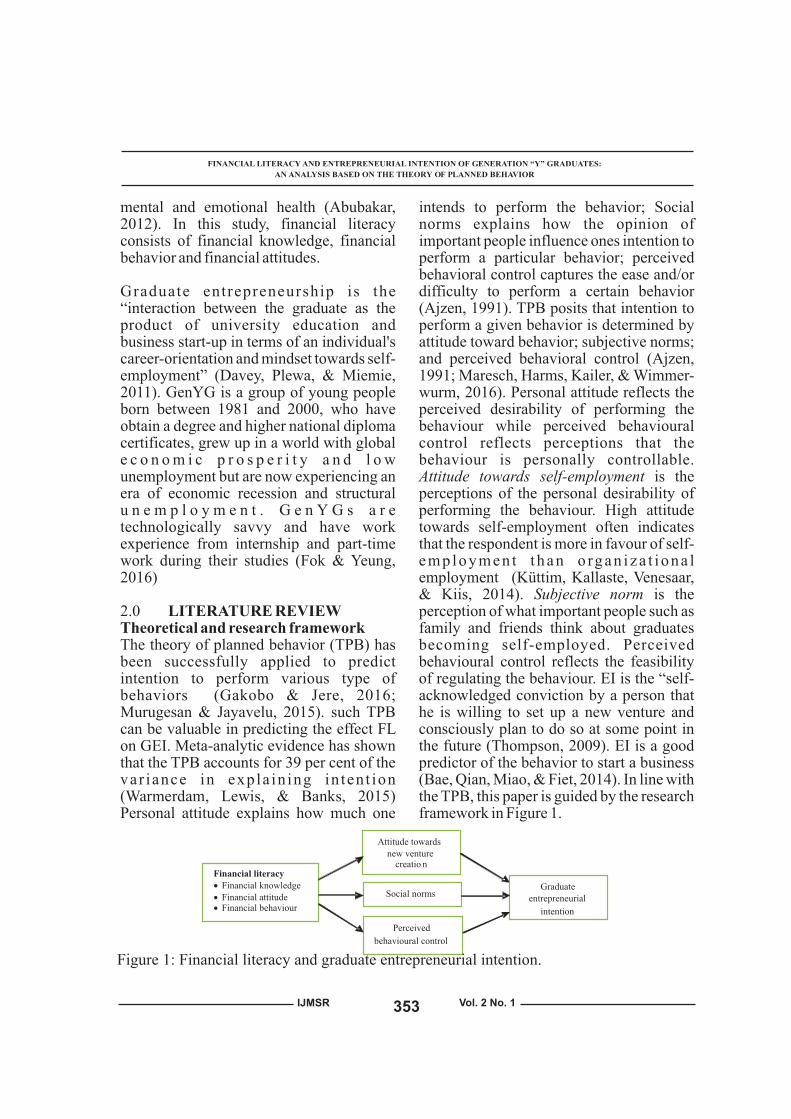

& Kiis, 2014). Subjective norm is the 2.0 LITERATURE REVIEW perception of what important people such as Theoretical and research framework family and friends think about graduates The theory of planned behavior (TPB) has becoming self-employed. Perceived been successfully applied to predict behavioural control reflects the feasibility intention to perform various type of of regulating the behaviour. EI is the “self-behaviors (Gakobo & Jere, 2016; acknowledged conviction by a person that Murugesan & Jayavelu, 2015). such TPB he is willing to set up a new venture and can be valuable in predicting the effect FL consciously plan to do so at some point in on GEI. Meta-analytic evidence has shown the future (Thompson, 2009). EI is a good that the TPB accounts for 39 per cent of the predictor of the behavior to start a business var iance in expla in ing in ten t ion (Bae, Qian, Miao, & Fiet, 2014). In line with (Warmerdam, Lewis, & Banks, 2015) the TPB, this paper is guided by the research Personal attitude explains how much one framework in Figure 1.

Attitude towards

new venture creatio n

Financial literacy

· Financial knowledge · Financial attitude · Financial behaviour

Graduate

entrepreneurial

intention

Social norms

Perceived

behavioural control

Figure 1: Financial literacy and graduate entrepreneurial intention.

353

FINANCIAL LITERACY AND ENTREPRENEURIAL INTENTION OF GENERATION “Y” GRADUATES:

AN ANALYSIS BASED ON THE THEORY OF PLANNED BEHAVIOR

IJMSR Vol. 2 No. 1

The construct of financial literacy is based relationship between FL and investment on the model built by(Caroline et al., 2016). decision. Lack of access to finance is a The model conceptualizes FL as a second- major obstacle that inhibit entrepreneurial order construct measured by 3 first order spirit (Azmat & Azmat, 2013). On top of constructs such as financial behavior, this problem, studies are rare if not unknown financial knowledge and financial attitude. about how FL could predicts GEI. As such The model was the idea of OECD (2013), this study argues that the theory of planned Atkinson & Messy (2012) and Agarwalla, behaviour could help explore the Barua, Jacob, & Varma (2013) as relationship. Therefore, it is hypothesized determinants of FL. Financial knowledge is that:a capability to manage income, expenditure and savings; financial attitude is a

Financial literacy and subjective normcombination of concepts, information and H1 (a): There is a significant relationship emotions about learning which results in a between FL and AVC.readiness to react favorably; financial H1 (b): There is a significant relationship behavior is an essential determinant of between FL and SN.financial literacy (Caroline et al., 2016). H1 (c): There is a significant relationship between FL and PBC.Hypotheses development

Financial literacy and attitude, TPB factors (AVC, SN, and PBC) and subjective norm, and perceives Entrepreneurial intention behavioural control TPB postulates that personal attitude, Nigerian graduates are trained to develop subjective/social norms and PBC are the the self-efficacy toward self-employment. antecedents of intention that influences T h i s o w e s t o t h e c o m p u l s o r y actual behavior (Ajzen, 1991). The entrepreneurial educat ion for a l l relationship among these TPB factors on u n d e rg r a d u a t e p r o g r a m m e s . T h e intention are mixed. Kalafatis, Pollard, East, entrepreneurial syllabus comprises of & Tsogas (1999) and Shahriar, Michael, & pedagogies in financial management, Polonsky (2013) found significant marketing, innovation, business creation, relationship between TPB constructs and hands-on practical for different type of (attitude, subjective norms, and perceived ventures. Abubakar (2012) suggests that behavioural control) on EI. Although Maes, graduates' FL could be shaped through Leroy, & Sels (2014) did not examine the lectures on sources of finance and financial relationship between subjective norm and management. Previous studies have shown EI, the study found significant and positive that FL is positively related to self-relation of attitudes and perceived beneficial economic behavior. For example, behavioural control on EI. Similarly, a positive relationship between FL and Solesvik, Westhead, Kolvereid, and Matlay youth entrepreneurship (Oseifuah, 2011), (2012) suggest that attitude has significant wealth creation (Jappelli & Padula, 2011), influence on entrepreneurial intention. access to capital (Nkundabanyanga et al., Overall, only the relationship between 2014), portfolio diversification (Abreua and attitudes toward the behaviour is Mendes, 2010) were suggested. However, consistently found to influence intention. Jappelli & Padula (2011) found a negative

354

FINANCIAL LITERACY AND ENTREPRENEURIAL INTENTION OF GENERATION “Y” GRADUATES:

AN ANALYSIS BASED ON THE THEORY OF PLANNED BEHAVIOR

IJMSR Vol. 2 No. 1

The other construct of subjective norms and help of 2 research assistants. It was perceived behavioural control received sugges ted tha t se l f -adminis te red mixed findings (Carsrud & Brannback, questionnaire is more effective in terms of 2011). Although social norms influenced response rates, though costly than mail and intention (Kolvereid & Isaksen, 2006; telephone surveys (Szolnoki and Hoffmann Venkatesh, James, & Xu, 2012; Wu, Tao, & 2013). The response rate was 84% and Yang, 2008), Liñán & Chen (2009) found a greater than 76% (Sudman, Greeley, & non-significant relationship between SN Pjnto, 1965). The sample size was and intention. Equally, Jimmieson, White, computed from the Table of sample size & Zajdlewicz (2009) found positive effect determination for indefinite population as of attitude and SN on intention but not PBC. suggested by Krejcie and Morgan (1970). The inconsistent findings of TPB factors on Table 1 shows that the male graduates were intention could be due to role of research 159 (70.4%) while females were 67 setting and context as well as the nature of (29.6%). Other respondents' characteristics the respondents. This paper argues that all investigated are age, qualification, the TPB factors could have positive employment s ta tus and years in relationship on GEI in the Nigerian context. employment (if any). Based on this argument, it is proposed that:H2 (a): There is a significant relationship All research instruments were validated in AVC and GEI. previous literature. Some were directly H2 (b): There is a significant relationship adopted and adapted while others modified between SN and GEI to suit the research context. All scales/items H2 (c): There is a significant relationship have been measured on 7 point Likert-type between PBC and GEI scale from 1 = strongly disagree to 7 =

strongly agree. The scale measuring the 3.0 METHODOLOGY three construct of FL was adopted and Method and measurement modified. Financial knowledge was This paper employs quantitative research adopted from Rooij, Lusardi, & Alessie methodology based on cross-sectional (2009) as used by Caroline, Potrich, Vieira, survey. Data was collected from graduates & Mendes-Da-Silva (2016); financial in Bauchi State of Nigeria. Because there is attitude from Chen & Volpe (1998) as used no database of graduates in Bauchi state, the by Caroline et al. (2016) and financial study adopted the convenience sampling knowledge from OECD (2015) The method. Targets were asked to determine measurement for AVC was based on Ajzen their educational status and age before (1991) which was used by Shinnar, Hsu, & requested to fill a questionnaire. Thus, only Powell (2014). SN was adopted and graduates with minimum qualification of modified from Moen & Kolvereid (1997) as HND and degree as well as generation Y used by Maresch, Harms, Kailer, & (1981-2000) were qualified in this survey. Wimmer-wurm (2016). Kolvereid (1996) 300 questionnaires were distributed of six-item measurement of PBC was adopted which 252 were returned and 226 found and modified as used by Murugesan & usable for analysis. The questionnaire were Jayavelu (2015). GEI was measured using self-administered (face-to-face) with the the scales of Iakovleva, Kolvereid, &

355

FINANCIAL LITERACY AND ENTREPRENEURIAL INTENTION OF GENERATION “Y” GRADUATES:

AN ANALYSIS BASED ON THE THEORY OF PLANNED BEHAVIOR

IJMSR Vol. 2 No. 1

thus avoided problems associated with Stephan (2011) and Liñán & Chen (2009) replication of data collection. Similarly, the which were also used by Murugesan & identity of the researchers were concealed Jayavelu (2015) and Warmerdam et al. to reduce leniency biases. Lastly, the (2015).statistical remedy was based on the Harman's one-factor test (Podsakoff et al., Common method bias2003). Through an exploratory factor Common method bias is a major issue in analysis (EFA), FL (15 items), TPB factor quantitative studies. It occurs when data is (11 items), and GEI (5 items) were loaded collected based on self-report from single together. Analysis showed Kaiser-Meyer-respondents. It is a source of both Olkin Measure of Sampling Adequacy = measurement and systematic errors. When 9.25 and significant, 7 dimensions with common method bias occurs, correlation eigenvalues > 1.0 and total variance estimates among constructs are inflated to explained (TVE) of 69.69%. The first factor the extent that the results give spurious explained 15.19% and was < 50% of the relationship (Podsakoff and Oran, 1986). TVE (Podsakoff et al., 2003) . Based on the This paper reduce the potential for common procedural and statistical remedies, it can method bias through procedural and be concluded that the effect of common statistical remedies as suggested by method bias is not substantial and could be Podsakoff, MacKenzie, Lee, and Podsakoff tolerated. (2003). On the procedural remedies, the

exogenous and endogenous constructs were 4.0 DATA ANALYSIS & DISCUSSION selected from different sources. Secondly, OF FINDINGSthe instruments were modified for clarity, Results of this paper comprised of simplicity, and comprehension. Third, respondent profiles, EFA, confirmatory issues regarding consistency and social factor analysis (CFA), and the structural desirability were resolved by pledging the model. The respondents' profiles are anonymity of the respondents. Issue of presented in Table 1. consistency motif was resolved by

collecting data from respondents once and

Table 1. Respondent profile

Profile

Variable

Frequency

Per cent

Gender

Male

159 70.4

Female

67 29.6

Total

226

100.0

Age 20-25 30 13.3 26-30 99 43.8 31-36 97 42.9 Total 226 100.0 Qualification PhD 07 03.1 Masters 46 20.4

Degree HND

173 76.5

Total

226 100.0

356

FINANCIAL LITERACY AND ENTREPRENEURIAL INTENTION OF GENERATION “Y” GRADUATES:

AN ANALYSIS BASED ON THE THEORY OF PLANNED BEHAVIOR

IJMSR Vol. 2 No. 1

Employment status

Unemployed 134 59.3 Private institution 41 18.1 Self-employed 39 17.3 NGO 08 3.5 others please specify 04 1.8 Total 226 100.0

Specialization/ discipline

Management sciences 107 47.3 Arts and humanities 49 21.7 Engineering and technology

52 23.0

Agricultural sciences 13 5.8 Education 5 2.2 Total 226 100.0

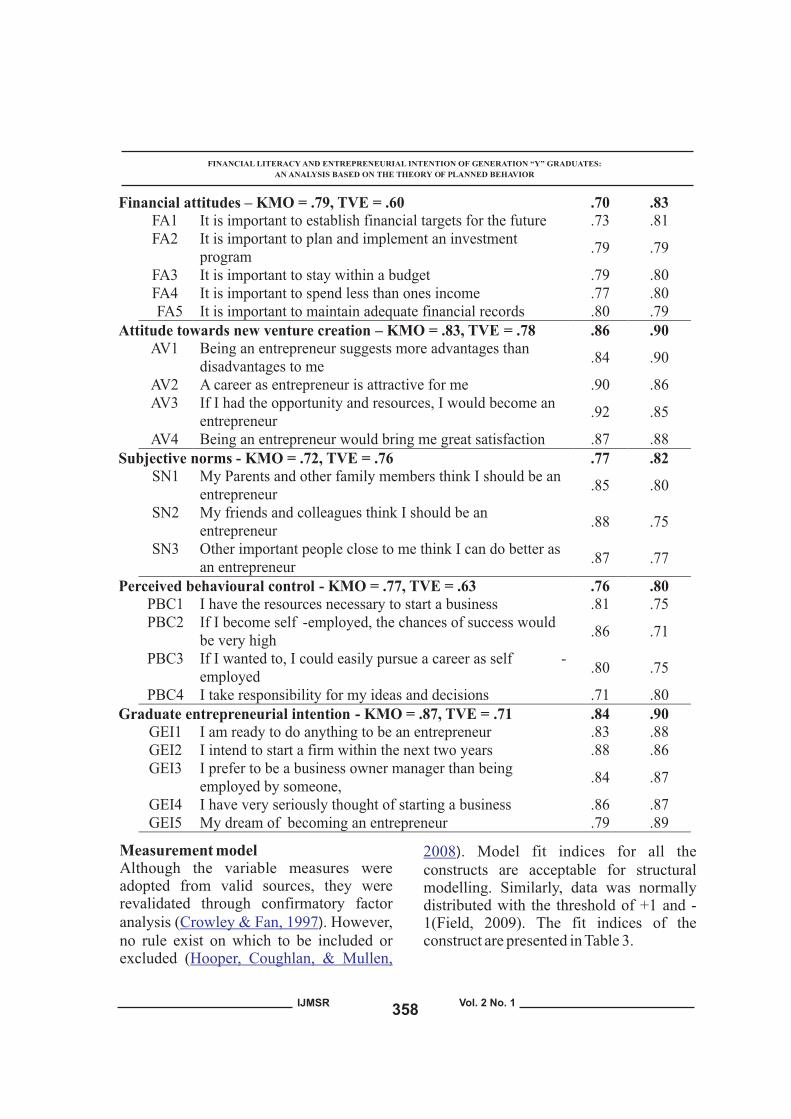

Exploratory factor analysis (EFA) prefer to buy things on credit than pay A total of 33 items were initially designed to outright cash). Table 2 shows that factor measure the model. EFA based on the loading (FL) of all items ranges between .64 principal component method of extraction and .92. Cronbach's alpha ranges for dropped 2 items from the FK scale due to constructs between .80 and .90 while items items appearing in a dimension not between .64 and .92. The alphas are above supposed to (these items were FL1 - I find it the 0.5 threshold and therefore satisfied the more satisfying to spend money than save requirement for reliability. and plan for business tomorrow, and FL2 – I

Table 2. Factor loading (FL), and reliability (RL)

CODE

Measurement scale and item FL RL

Financial knowledge – KMO = .81, TVE = .62 .80 .84 FK1 I am very organized when it comes to managing my money .79 .81

FK2 I am never late at paying my bills .78 .82

FK3 I have the skill to be well-informed about financial changes in the economy

.79 .82

FK4 I have the knowledge to keep track of new business financing options

.85 .79

FK5 I am aware of the different financial products offered by banks

.72 .84

Financial behaviour – KMO = .87, TVE = .72 .72 .90 FB1 I always pay my bills on time to avoid extra charges. .70 .89

FB2 I follow a weekly or monthly plan for expenses. .72 .88 FB3 I analyze my financial situation before a major purchase. .77 .87 FB4 I am satisfied with the way I control my finances .79 .87 FB5 I try to save some money for unforeseen events .64 .90

357

FINANCIAL LITERACY AND ENTREPRENEURIAL INTENTION OF GENERATION “Y” GRADUATES:

AN ANALYSIS BASED ON THE THEORY OF PLANNED BEHAVIOR

IJMSR Vol. 2 No. 1

Financial attitudes – KMO = .79, TVE = .60 .70 .83 FA1 It is important to establish financial targets for the future .73 .81

FA2 It is important to plan and implement an investment program

.79 .79

FA3 It is important to stay within a budget .79 .80 FA4 It is important to spend less than ones income .77 .80

FA5 It is important to maintain adequate financial records .80 .79 Attitude towards new venture creation – KMO = .83, TVE = .78 .86 .90 AV1 Being an entrepreneur suggests more advantages than

disadvantages to me .84 .90

AV2 A career as entrepreneur is attractive for me .90 .86 AV3 If I had the opportunity and resources, I would become an

entrepreneur .92 .85

AV4 Being an entrepreneur would bring me great satisfaction .87 .88 Subjective norms - KMO = .72, TVE = .76 .77 .82

SN1

My Parents and other family members think I should be an entrepreneur

.85

.80

SN2

My friends and colleagues think I should be an entrepreneur

.88

.75

SN3

Other important people close to me think I can do better as an entrepreneur

.87

.77

Perceived behavioural control -

KMO = .77, TVE = .63

.76

.80

PBC1

I have the resources necessary to start a business

.81 .75

PBC2

If I become self -employed, the chances of success would be very high

.86 .71

PBC3

If I wanted to, I could easily pursue a career as self -employed

.80 .75

PBC4

I take responsibility for my ideas and decisions

.71

.80

Graduate entrepreneurial intention -

KMO = .87, TVE = .71

.84 .90

GEI1

I am ready to do anything to be an entrepreneur

.83 .88

GEI2

I intend to start a firm within the next two years

.88 .86

GEI3

I prefer to be a business owner manager than being employed by someone,

.84 .87

GEI4

I have very seriously

thought of starting a business

.86

.87

GEI5

My dream of becoming an entrepreneur

.79 .89

Measurement model ). Model fit indices for all the Although the variable measures were constructs are acceptable for structural adopted from valid sources, they were modelling. Similarly, data was normally revalidated through confirmatory factor distributed with the threshold of +1 and -analysis ( ). However, 1(Field, 2009). The fit indices of the no rule exist on which to be included or construct are presented in Table 3.excluded (

2008

Crowley & Fan, 1997

Hooper, Coughlan, & Mullen,

358

FINANCIAL LITERACY AND ENTREPRENEURIAL INTENTION OF GENERATION “Y” GRADUATES:

AN ANALYSIS BASED ON THE THEORY OF PLANNED BEHAVIOR

IJMSR Vol. 2 No. 1

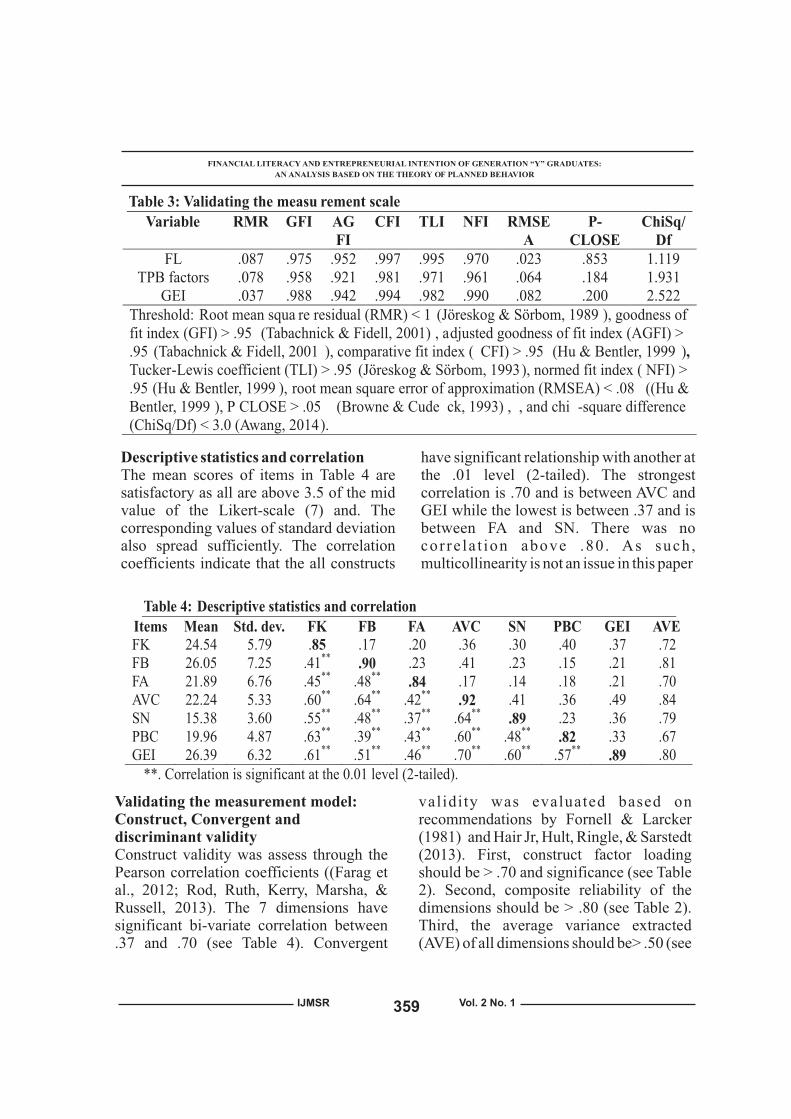

Table 3: Validating the measu rement scale

Variable RMR GFI AGFI

CFI TLI NFI RMSEA

P-CLOSE

ChiSq/Df

FL .087 .975 .952 .997 .995 .970 .023 .853 1.119 TPB factors .078 .958 .921 .981 .971 .961 .064 .184 1.931

GEI .037 .988 .942 .994 .982 .990 .082 .200 2.522 Threshold: Root mean squa re residual (RMR) < 1 (Jöreskog & Sörbom, 1989 ), goodness of fit index (GFI) > .95 (Tabachnick & Fidell, 2001) , adjusted goodness of fit index (AGFI) > .95 (Tabachnick & Fidell, 2001 ), comparative fit index ( CFI) > .95 (Hu & Bentler, 1999 ), Tucker-Lewis coefficient (TLI) > .95 (Jöreskog & Sörbom, 1993), normed fit index ( NFI) > .95 (Hu & Bentler, 1999 ), root mean square error of approximation (RMSEA) < .08 ((Hu & Bentler, 1999 ), P CLOSE > .05 (Browne & Cude ck, 1993) , , and chi -square difference (ChiSq/Df) < 3.0 (Awang, 2014). Descriptive statistics and correlation have significant relationship with another at

The mean scores of items in Table 4 are the .01 level (2-tailed). The strongest satisfactory as all are above 3.5 of the mid correlation is .70 and is between AVC and value of the Likert-scale (7) and. The GEI while the lowest is between .37 and is corresponding values of standard deviation between FA and SN. There was no also spread sufficiently. The correlation cor re la t ion above .80 . As such , coefficients indicate that the all constructs multicollinearity is not an issue in this paper

Table 4: Descriptive statistics and correlation

Items Mean Std. dev. FK FB FA AVC SN PBC GEI AVE FK 24.54 5.79 .85 .17 .20 .36 .30 .40 .37 .72 FB 26.05 7.25 .41** .90 .23 .41 .23 .15 .21 .81 FA 21.89 6.76 .45** .48** .84 .17 .14 .18 .21 .70 AVC 22.24 5.33 .60** .64** .42** .92 .41 .36 .49 .84 SN 15.38 3.60 .55** .48** .37** .64** .89 .23 .36 .79 PBC 19.96 4.87 .63** .39** .43** .60** .48** .82 .33 .67 GEI 26.39 6.32 .61** .51** .46** .70** .60** .57** .89 .80

**. Correlation is significant at the 0.01 level (2-tailed).

Validating the measurement model: validity was evaluated based on Construct, Convergent and recommendations by Fornell & Larcker discriminant validity (1981) and Hair Jr, Hult, Ringle, & Sarstedt Construct validity was assess through the (2013). First, construct factor loading Pearson correlation coefficients ((Farag et should be > .70 and significance (see Table al., 2012; Rod, Ruth, Kerry, Marsha, & 2). Second, composite reliability of the Russell, 2013). The 7 dimensions have dimensions should be > .80 (see Table 2). significant bi-variate correlation between Third, the average variance extracted .37 and .70 (see Table 4). Convergent (AVE) of all dimensions should be> .50 (see

359

FINANCIAL LITERACY AND ENTREPRENEURIAL INTENTION OF GENERATION “Y” GRADUATES:

AN ANALYSIS BASED ON THE THEORY OF PLANNED BEHAVIOR

IJMSR Vol. 2 No. 1

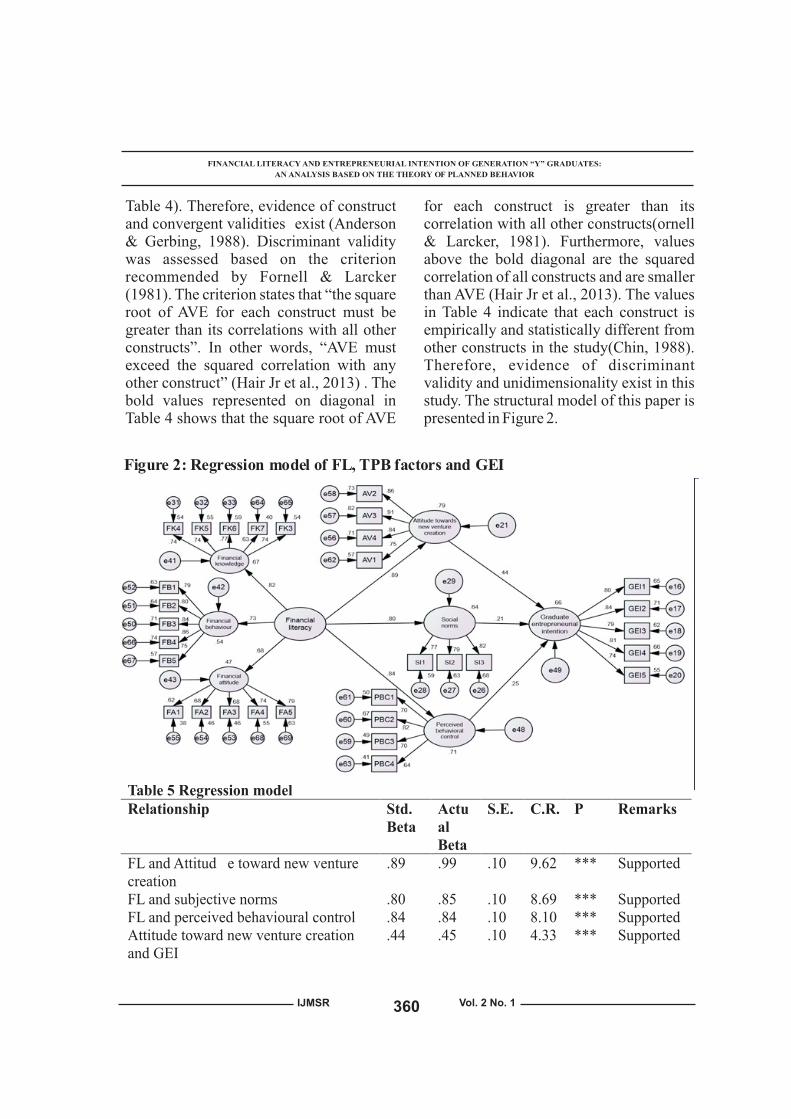

Table 4). Therefore, evidence of construct for each construct is greater than its and convergent validities exist (Anderson correlation with all other constructs(ornell & Gerbing, 1988). Discriminant validity & Larcker, 1981). Furthermore, values was assessed based on the criterion above the bold diagonal are the squared recommended by Fornell & Larcker correlation of all constructs and are smaller (1981). The criterion states that “the square than AVE (Hair Jr et al., 2013). The values root of AVE for each construct must be in Table 4 indicate that each construct is greater than its correlations with all other empirically and statistically different from constructs”. In other words, “AVE must other constructs in the study(Chin, 1988). exceed the squared correlation with any Therefore, evidence of discriminant other construct” (Hair Jr et al., 2013) . The validity and unidimensionality exist in this bold values represented on diagonal in study. The structural model of this paper is Table 4 shows that the square root of AVE presented in Figure 2.

Figure 2: Regression model of FL, TPB factors and GEI

Table 5 Regression model Relationship Std.

Beta

Actual Beta

S.E. C.R. P Remarks

FL and Attitud e toward new venture creation

.89 .99 .10 9.62 *** Supported

FL and subjective norms

.80

.85 .10

8.69

***

Supported

FL and perceived behavioural control .84

.84

.10

8.10

***

Supported

Attitude toward new venture creation and GEI

.44

.45 .10

4.33

***

Supported

360

FINANCIAL LITERACY AND ENTREPRENEURIAL INTENTION OF GENERATION “Y” GRADUATES:

AN ANALYSIS BASED ON THE THEORY OF PLANNED BEHAVIOR

IJMSR Vol. 2 No. 1

Subjective norms and GEI Perceived behavioural control and GEI r2 of Attitude toward new venture creation = .80 r2 of Subjective norms = .64 r2 of Perceived behavioural control = .71 r2 of Graduate entrepreneurial intention = .66

Discussion of findings (â = .84, P < .001). This shows that when FL goes up by 1, PBC goes up by .80. The The major contribution of this study is the regression weight for FL in the prediction significant relationship between FL and of PBC is significantly different from zero TPB factors (AVC, SN, and PBC). To the at the .001 level (two-tailed). best of the researcher's knowledge, no Hypotheses 2 (a) suggests that AVC has study has explored the relationship significant relationship with GEI (â = .44, between these factors. The test of H1 (a) P < .001). Hypothesis 2 (b) shows that SN suggest a significant relationship between is significantly related to GEI (â = .21, P FL and attitude towards new venture < .005). Lastly, test of H2 (c) that PBC creation (â = .89, P < .001). The finding positively and significantly predicts GEI. indicates that the higher the financial Results for H2 (a, b, c) demonstrate that the literacy, the greater the tendency to create higher the AVC, SN, and PBC, the higher new firm. Statistically, it means that when the GEI. This finding is consistent with FL goes up by 1, attitude goes up by .89. Shahriar, Michael, & Polonsky (2013) who The regression weight estimate of FL in the found significant relationship between the prediction of attitude is significantly TPB factor (AVC, SN and PBC) on EI. different from zero at the .001 level (two-Overall the coefficients of determination tailed). Although no direct relationship (r²) of AVC, SN, and PBD due to the exist between FL and attitude to new influence of FL are .79, .64, and .71 venture creation, the finding is similar with respectively while the coefficient of GEI Abreua & Mendes (2010) who found that due to the combined influence of AVC, SN, FL has a significant relationship with and PBC is .66. Higher r² (.79) on AVC investment behavior and portfolio suggests that financially literate graduates diversification. Similarly, Cole, Simpson, are more in favour of self-employment than and Zia (2009) found that FL influences organizational employment. Higher r² (.64) behavior. Additionally, Abubakar (2012) of SN indicates that graduates' with suggests that FL has a positive impact on financial literacy could be encouraged by

the financial behavior of entrepreneurs. parents, family members, friends,

The test of H1 (b) found a significant colleagues and other important people to

relationship between FL and SN (â = .80, P opt for self-employment. Similarly, Higher

< .001). This shows that when FL goes up r² (.71) of PBC shows that graduates who by 1, SN goes up by .80. The regression have control over their finances, weight for FL in the prediction of SN is entrepreneurial ideas and have self-significantly different from zero at the .001 confidence to succeed are more likely to level (two-tailed). Test of H1 (c) suggests a start new ventures positive relationship between FL and PBC

361

FINANCIAL LITERACY AND ENTREPRENEURIAL INTENTION OF GENERATION “Y” GRADUATES:

AN ANALYSIS BASED ON THE THEORY OF PLANNED BEHAVIOR

IJMSR Vol. 2 No. 1

Conclusion this paper could help reduce graduates' This paper suggests that FL is an important structural unemployment and poverty. determinant of GEI. Theoretically, it is the Socially, graduates entrepreneurship could first to develop a theoretical model with FL be an antidote for the boko-haram as exogenous constructs which exert insurgency in the north-east Nigeria, the influence on GEI through the indirect effect militancy and oil bunkering and stealing in TPB factors. Practically, this paper the south-south, tribal and religious crises proposes a promising framework for in the middle belt, cyber-crimes and tackling problems associated with desperate journeys to Europe and the U.S.A financing graduate venture creation. Thus, for greener posture among Nigerian it demonstrates the importance of FL as generation Y graduates.precondition for graduates to access seed capital from financial institutions. Despite the findings of the study, it was not Practically, the paper has implication for without limitations. First, convenient graduate students, institutions of higher sampling was used due to lack of graduate learning, formal financial institutions, and database in Bauchi state. Thus, the study policy makers regarding venture creation. suggests for probability sampling The paper shows how graduates could method(s) if a sampling frame is available. utilize their financial skills to become self- Second, future studies should examine the employed and job creators. Institutions of effect of work values on generation Y higher learning should emphasize graduates attitudes and behaviour. pedagogies in financial management that Soininen et al. (2013) msuggest that encourage graduate toward self- intrinsic work values influence attitudes employment. Through, this study, financial and behaviors. Third, this framework institutions can develop confidence in should be tested in other research setting. graduates entrepreneurial spirits. They The future test of this framework should need to emphasize business plan, character control for age. Lastly, a case-based and education as foremost consideration approach through interview would also for advancing entrepreneurial loan to provide in-depth insights that would not be prospective graduate entrepreneurs. This is provided by cross-sectional survey. Finally, against the current norms of advancing loan the current findings should be interpreted based collaterals and GYG may not have with caution and within the cultural the tangible collaterals to offer. As such, contexts of the respondent entrepreneurial financial institutions can use this study to environment. This is because data came design loan strategies for prospective f rom graduates in a f inancia l ly graduates' entrepreneurs. disadvantaged environment.

Policy makers could benefit from the REFERENCES findings of this paper by designing policies Abbasian, S., & Yazdanfar, D. (2013). for financing graduates' entrepreneurial

Exploring the financing gap between development. Awareness should be created native born women- and immigrant to help families and friend, and other women-owned firms at the start-up important people to encourage graduates stage. International Journal of Gender toward self-employment. Furthermore, and Entrepreneurship, 5(2), 157–173. policy makers should provide favorable doi:10.1108/17566261311328837

facilitating conditions for the success of Abreua, M., & Mendes, V. (2010). Financial graduate entrepreneurship. Economically, literacy and portfolio diversification.

362

FINANCIAL LITERACY AND ENTREPRENEURIAL INTENTION OF GENERATION “Y” GRADUATES:

AN ANALYSIS BASED ON THE THEORY OF PLANNED BEHAVIOR

IJMSR Vol. 2 No. 1

Quantitative Finance, 10(5), 515–528. Browne, M. W., & Cudeck, R. (1993). doi:10.1080/14697680902878105 Alternative ways of assessing model fit.

Abubakar, H. A. (2012). "Entrepreneurship Sage Focus Editions, 154, 136–136.development and financial literacy in Caroline, A., Potrich, G., Vieira, K. M., & Africa. Journal of Entrepreneurship, Mendes-Da-Silva, W. (2016). Management and Sustainable Development of a financial literacy Development, 11(4), 281–294. model for university students.

Agarwalla, S. K., Barua, S. K., Jacob, J., & Management Research Review, 39(3), Varma, J. R. (2013). Financial literacy 356–376. doi:10.1108/MRR-06-2014-among working young in urban India 0143(No. 2013-10-02). Indian Institute of Carsrud, A., & Brannback, M. (2011). Management Ahmedabad. Entrepreneurship motivations: What do

Ajzen, I. (1991). The theory of planned we still need to knnow? Journal of behavior. Organizational Behavior and Small Business Management, 49(1), Human Decision Processes, 50(2), 9–26.179–211. Central Bank of Nigeria. (2015). Financial

Anderson, J. C., & Gerbing, D. W. (1988). literacy. Retrieved from Structural equation modeling in http://www.cbn.gov.ng/Devfin/finliteracpractice: A review and recommended y.asptwo-step approach. Psychological Chen, H., & Volpe, R. P. (1998). An analysis Bulletin,103(3), 411. of personal financial literacy among

Atkinson, A., & Messy, F. (2012). Measuring college students. Financial Services financial literacy: results of the Review, 7(2), 107–128.OECD/International Network on Chin, W. W. (1988). Commentary: Issues and Financial Education (INFE) Pilot opinion on structural equation study”, Working Paper No. 15, OECD modeling. JSTOR.Working Papers on Finance, Insurance Chinyere, T., & Faith, C. (2012). and Private Pensions OECD Entrepreneurship and Employability Publishing. Paris. Among Nigerian Graduates.

Awang, Z. (2014). A handbook on SEM for Mediterranean Journal of Social academicians and practitioners: Step Sciences, 3(December), 68–74. by step practical guides for the doi:10.5901/mjss.2012.v3n16p68begineers (Vol.2 Firs.). Perpustakan Cole, S., Simpson, T., & Zia, B. (2009). Prices Negara Malaysia: MPSW Rich of Knowledge. What Drives the Demand Resources. for Financial Services in Emerging

Azmat, F., & Azmat, F. (2013). entrepreneurs Markets? (No. Working Papers No. 09-Opportunities or obstacles? 117). Boston.Understanding the challenges faced by Davey, T., Plewa, C., & Miemie, S. (2011). migrant women entrepreneurs. Entrepreneurship perceptions and career International Journal of Gender and intentions of international students. Entrepreneurship, 5(2), 198–215. Education + Training, 53(5), 335–352. doi:10.1108/17566261311328855 doi:10.1108/00400911111147677

Bae, T. J., Qian, S., Miao, C., & Fiet, J. O. Farag, I., Sherrington, C., Kamper, S. ., (2014). The Relationship Between Ferreira, M., Moseley, A. ., Lord, S. ., & Entrepreneurship Education and Cameron, I. D. (2012). Measures of Entrepreneurial Intentions: A Meta- physical functioning after hip fracture: Analytic Review. Entrepreneurship construct validity and responsiveness of Theory and Practice, 217–254. performance-based and self-reported doi:10.1111/etap.12095 measures.

363

FINANCIAL LITERACY AND ENTREPRENEURIAL INTENTION OF GENERATION “Y” GRADUATES:

AN ANALYSIS BASED ON THE THEORY OF PLANNED BEHAVIOR

IJMSR Vol. 2 No. 1

Field, A. (2009). Discovering statistics using Jimmieson, N. L., White, K. M., & SPSS. Sage publications. Zajdlewicz, L. (2009). Psychosocial

Fok, R. H. M., & Yeung, R. M. W. (2016). predictors of intentions to engage in Work attitudes of Generation Y in change supportive behaviors in an Macau's hotel industry: management's organizational context. Journal of perspective. Worldwide Hospitality and Change Management, 9(3), 233–250.Tourism Themes, 8(1), 83–96. Jöreskog, K. G., & Sörbom, D. (1989).

Fornell, C., & Larcker, D. F. (1981). LISREL 7: A guide to the program and Evaluating structural equation models applications, (s), Spss.with unobservable variables and Jöreskog, K. G., & Sörbom, D. (1993). measurement error. Journal of LISREL 8: Structural equation Marketing Research, 39–50. modeling with the SIMPLIS command

Gakobo, T. W., & Jere, M. G. (2016). An language. Scientific Software application of the theory of planned International.behaviour to predict intention to Kalafatis, S. P., Pollard, M., East, R., & consume African indigenous foods in Tsogas, M. H. (1999). Green marketing Kenya. British Food Journal, 118(5), and Ajzen ' s theory of planned 1–16. behaviour: a cross-market examination.

Hair Jr, J. F., Hult, G M, T., Ringle, C., & Journal of Consumer Marketing, 16(5), Sarstedt, M. (2013). A primer on partial 441–460.least squares structural equation Karra, N., Phillips, N., & Tracey, P. (2008). modeling (PLS-SEM). Sage Building the Born Global Firm Publications. Developing Entrepreneurial

Hasnol, A. M., & Salleh, A. P. M. (2015). A Capabilities for International New comparison on financial literacy Venture Success. Long Range Planning, between welfare recipients and non- 41, 440–458. welfare recipients in Brunei. doi:10.1016/j.lrp.2008.05.002International Journal of Social Kolvereid, L. (1996). Prediction of Economics, 42(7), 598–613. employment status choice intentions. doi:10.1108/IJSE-09-2013-0210 Enterpreneurship Theory & Practice

Hu, L. T., & Bentler, P. M. (1999). Cutoff Theory Pract, 21, 47–57.Kolvereid, L., & Isaksen, E. (2006). New criteria for fit indexes in covariance

business start-up and subswquent entry structure analysis: Conventional criteria into self-employment. Journal of versus new alternatives. Structural Business Venturing, 21, 866–885.Equation Modeling: A

Küttim, M., Kallaste, M., Venesaar, U., & Multidisciplinary Journal, 6(1), 1–55.Kiis, A. (2014). Entrepreneurship Iakovleva, T., Kolvereid, L., & Stephan, U. education at university level and (2011). Entrepreneurial intentions in students ' entrepreneurial intentions. developing and developed countries. Procedia - Social and Behavioral Education + Training, 53(5), 353–370. Sciences, 110, 658–668. doi:10.1108/00400911111147686doi:10.1016/j.sbspro.2013.12.910Jappelli, T., & Padula, M. (2011). Investment

Liñán, F., & Chen, Y.-W. (2009). Developing in financial literacy and saving

and cross-cultural application of a decisions (No. No. 2011/07). Center for specific instrument to measure Financial Studies (CFS) Working entreprenuerial intentions. Paper. Retrieved from , http://nbn- Entrepreneurship Theory & Practice, resolving.de/ urn:nbn:de:hebis:30- 33(3), 593–617.92954 Maes, J., Leroy, H., & Sels, L. (2014). Gender

364

FINANCIAL LITERACY AND ENTREPRENEURIAL INTENTION OF GENERATION “Y” GRADUATES:

AN ANALYSIS BASED ON THE THEORY OF PLANNED BEHAVIOR

IJMSR Vol. 2 No. 1

differences in entrepreneurial Nalukenge, I., & Tauringana, V. (2014). Lending terms, financial literacy and intentions: A TPB multi-group analysis formal credit accessibility. at factor and indicator level. European International Journal of Social Management Journal, 32(5), 784–794. Economics, 41(5), 342–361. doi:10.1016/j.emj.2014.01.001doi:10.1108/IJSE-03-2013-0075Maresch, D., Harms, R., Kailer, N., &

OECD. (2013). PISA 2012 Assessment and Wimmer-wurm, B. (2016). The impact Analytical Framework: Mathematics, of entrepreneurship education on the Reading, Science, Problem Solving and entrepreneurial intention of students in Financial Literacy, OECD Publishing, science and engineering versus Paris. Paris.

business studies university programs. OECD. (2015). Toolkit for measuring Technological Forecasting & Social financial literacy and financial Change, 104, 172–179. inclusion. OECD/INFE TOOLKIT, doi:10.1016/j.techfore.2015.11.006 (March).

Marques, C. S., Ferreira, J., Gomes, D. N., & Olufunso, O. F. (2010). Graduate Rodrigues, R. G. (2012). Entrepreneurial Intention in South Entrepreneurship education Africa: Motivations and Obstacles. entrepreneurial intention. Education + International Journal of Business and Training, 54(8/9), 657–672. Management, 5(9), 87–98.doi:10.1108/00400911211274819 Oseifuah, E. K. (2010). Financial literacy and

Middleton, K. L. W. (2013). Becoming youth entrepreneurship in South Africa. Journal of Economic and Management entrepreneurial: gaining legitimacy in Studies, 1(2), 164–182. the nascent phase. International doi:10.1108/20400701011073473Journal of Entrepreneurial Behavior &

Oseifuah, E. K. (2011). Financial literacy and Research, 19(4), 404–424. youth entrepreneurship in South Africa. doi:10.1108/IJEBR-04-2012-0049African Journal of Economic and Moen, L. K., & Kolvereid, L. (1997). Management Studies, 1(2), 164–182. Entrepreneurship among business

graduates: does a major in doi:10.1108/20400701011073473entrepreneurship make a difference?? Podsakoff, P. M., MacKenzie, S. B., Lee, J.-Journal of European Industrial Y., & Podsakoff, N. P. (2003). Training, 21(4), 154–160. Common method biases in behavioral

Murugesan, R., & Jayavelu, R. (2015). research: a critical review of the Testing the impact of entrepreneurship literature and recommended remedies. education on business, engineering and Journal of Applied Psychology, 88(5), arts and science students using the 879–.theory of planned behaviour: A

Podsakoff, P. M., & Oran, D. (1986). Self-comparative study. Journal of reports in organizational research: Entrepreneurship in Emerging Problems and preospects. Journal of Economies, 7(3), 256–275.Managementw, 12(4), 928–940. Nabi, G., & Lin, F. (2011). Graduate doi:0803973233entrepreneurship in the developing

Rod, K. D., Ruth, P. S., Kerry, L. M., Marsha, world: intentions, education and D., & Russell, R. P. (2013). Construct development. Education + Training, Validity of Selected Measures of 53(5), 325–334.

doi:10.1108/00400911111147668 Physical Activity Beliefs and Motives NBS. (2014). Selected Tables from Job in Fifth and Sixth Grade Boys and

Creation and Employment Survey 2nd Girls. Journal Of Pediatric Psychology, - 4th Quarter 2013. Bureau National June, 38(5), 563–76 doi: Statistics, (May). 10.1093/jpepsy/jst013.

Nkundabanyanga, S. K., Kasozi, D., Rooij, M. Van, Lusardi, A., & Alessie, R.

365

FINANCIAL LITERACY AND ENTREPRENEURIAL INTENTION OF GENERATION “Y” GRADUATES:

AN ANALYSIS BASED ON THE THEORY OF PLANNED BEHAVIOR

IJMSR Vol. 2 No. 1

(2009). Financial literacy and 2(2), 57–66.retirement planning in the Tabachnick, B. G., & Fidell, L. S. (2001). Netherlands. DNB Working Paper No. Using multivariate statistics.

Shahriar, A., Michael, F., & Polonsky, J. Te'eni-Harari, T. (2016). Financial literacy (2013). Predicting Bangladeshi among children: the role of financial salespeople's ethical involvement in saving money. Young intentions and behaviour using the Consumers, 17(2), 197–208. theory of planned behaviour doi:10.1108/YC-01-2016-00579Implications for developing countries. Thompson, E. R. (2009). Individual Asia Pacific Journal of Marketing entrepreneurial intention: construct and Logistics, 25(4), 655–673. clarification and development of an doi:10.1108/APJML-01-2013-0019 internationally reliable metric.

Shinnar, R. S., Hsu, D. K., & Powell, B. C. Enterprice Theory and Practice., 33, (2014). Self-efficacy, entrepreneurial 669–694.intentions, and gender: Assessing the Venkatesh, V., James, Y. L. T., & Xu, X. impact of entrepreneurship education (2012). Consumer a cceptance and longitudinally. International Journal use of information technology?: of Management Education, 12, extending the unified theory. MIS 561–570. Quarterly, 36(1), 157–178.doi:10.1016/j.ijme.2014.09.005 Warmerdam, A., Lewis, I., & Banks, T.

Singhry, H. B. (2015). The Effect of (2015). Gen Y recruitment Technology Entrepreneurial Understanding graduate intentions to Capabilities on Technopreneurial join of Planned Behaviour. Education Intention of Nascent Graduates. + Training, 57(5), 560–574. European Journal of Business and doi:10.1108/ET-12-2013-0133Management, 7(34), 8–20. Wu, Y.-L., Tao, Y.-H., & Yang, P.-C. (2008).

Soininen, J. S., Puumalainen, K., & Durst, The use of unified theory of S. (2013). Entrepreneurial orientation acceptance and use of technology to in small firms – values- attitudes- confer the behavioral model of 3G behavior approach. International mobile telecommunication users. Journal of Entrepreneurial Behavior Journal of Statistics and Management & Research, 19(6), 611–632. Systems, 11(5), 919–949. doi:10.1108/IJEBR-10-2012-0106 doi:10.1080/09720510.2008.1070135

Solesvik, M. Z., Westhead, P., Kolvereid, L., 1& Matlay, H. (2012). context Student Xiang, D., & Worthington, A. (2015). intentions to become self-employed?: Finance-seeking behaviour and the Ukrainian context. Journal of

outcomes for small- and medium-Small Business and Enterprise sized enterprises. International Development, 9(3), 441–460. Journal of Managerial Finance, doi:10.1108/14626001211250153

Sudman, S., Greeley, A., & Pjnto, L. (1965). 11(4), 513–530The Effectiveness of Self-Administered Questionnaires. Journal of Marketing Research, II, 293–297.

Szolnoki, G., & Hoffmann, D. (2013). Online, face-to-face and telephone surveys—Comparing different sampling methods in wine consumer research. Wine Economics and Policy,

366

FINANCIAL LITERACY AND ENTREPRENEURIAL INTENTION OF GENERATION “Y” GRADUATES:

AN ANALYSIS BASED ON THE THEORY OF PLANNED BEHAVIOR

IJMSR Vol. 2 No. 1