financial inclusion measurement for regulators

TRANSCRIPT

Data Working Group21-22 June 2010, Kuala Lumpur, Malaysia

Financial Inclusion measurement for regulators

2

2) Defining & measuring financial inclusion

3) Selecting the appropriate approach

1) Understanding the rationale and scope

To create a common framework of understanding of the issues and choices surrounding the measurement of financial inclusion

Rationale: Why measure financial inclusion?

Questions which data can answer

Category

Questions one may ask of the data

Decisions taken based on the data

One time financial access data

Internationally comparable data

Data collected over time

Data designed to show causality

Dia

gnos

is

Which population segment lacks what type of financial services?

- Targeted regulation- Further research / deeper survey

X

Why do they lack access?- Begin to identify barriers to formulate policy X

How much use takes place from informal / unregulated services?

- Begin to identify at risk consumers X

Is there evidence of consumer abuse?

-Targeted regulation X

Questions which data can answer (2)

Category

Questions one may ask of the data

Decisions taken based on the data

One time financial access data

Internationally comparable data

Data collected over time

Data designed to show causality

Polic

y&

regu

lato

ry re

form

How does country X compare to a peer group? (by regional or level of income)

- Whether any reform or action is required

X

What targets for access can be measured credibly?

- Choice of targets X X X

Is inclusion and protection improving over time?

- Targeted regulation X

Mon

itori

ng What has been the impact of a particular regulatory change?

- Modification of regulation

X X

6

2) Defining and measuring financial inclusion

3) Selecting the appropriate approach

1) Understanding the rationale and scope

To create a common framework of understanding of the issues and choices surrounding the measurement of financial inclusion

Financial inclusion goals need clear definition to be measurable

UNCDF - Vision of Inclusive Finance

With a view to significantly increase outreach… each developing country should have a continuum of financial institutions that… would be characterized by: a) access at a reasonable cost of all households and

enterprises to the range of financial services for which they are “bankable,” including savings, credit, leasing and factoring, mortgages, insurance, pensions, payments and local and international transfers;

b) sound institutions, guided by appropriate internal management systems, industry performance standards and performance monitoring by the market, as well as by sound prudential regulation where required;

c) financial and institutional sustainability as a means of providing access to financial services over time; and

d) Multiple providers of financial services, so as to bring cost-effective and a wide variety of alternatives to customers.

SA Financial Sector CharterEffective Access means:a) Being within a distance of 20 kms to the nearest

service point at which first-order retail financial services can be undertaken, and includes ATM and other origination points …

b) Being within a distance of 20 kms to the nearest accessible device at which an electronic (other than ATM) service can be undertaken

c) A sufficiently wide range of first-order retail financial products and services …which are aimed at and are appropriate for individuals who fall into the All Media Product Survey (AMPS) categories of LSM 1-5…

First order retail products and services means:a) Transaction products and services… for day to day

purposesb) Savings products and servicesc) Credit for low-income housing (definition provided)d) Insurance products and services

7

Vision must be translated to actionable standards at country level

Specific standards provide benchmarks against which to measure progress

Definition of financial inclusion: e.g. Center for Financial Inclusion (2010)

“A state in which all people who can use them have access to a full suite of quality financial services, provided at affordable prices, in a convenient manner, and with dignity for the clients. Financial services are delivered by a range of providers, most of them private, and reach everyone who can use them, including disabled, poor, rural, and other excluded populations”.

Four dimensions:• What is provided: full range in four main areas• How it is provided: quality=convenience, affordability, safety and

dignity• Who receives: everyone who can use• Who provides: a range of providers led by mainstream financial

institutions

2. Usage

• Actual usage of financial services / products:

• Regularity• Frequency• Patterns

The four dimensions of financial inclusion in the AFI policy note

• Ability to use formal financial services, i.e. minimal barriers to opening an account:

• Physical proximity• Affordability • Eligibility

1. Access

• Product attributes match the needs of customers e.g. portfolio• Choice available

3.Quality

• Effect on the livelihoods of the customers

• Welfare/ consumption• Personal/ business productivity

4.Welfare

Financial inclusion

More complex definitions require additional measurement resources

9

Towards a cross country definition of financial inclusion

• Emphases and targets will and should vary by country since circumstances differ widely

• However, the underlying components can be standardized to enable cross country dialog and measurement

• This would require developing and agreeing common definitions or understandings of the main building block concepts: e.g.

– The main dimensions of inclusion– Access : e.g. “The availability to a given person of affordable and appropriate

financial services”. ACCION Glossary– Basic categories of financial service: transaction/payments, savings, insurance,

credit– % Banked, unbanked, underbanked, previously banked: what is the denominate– Active/ dormant

10

Examples of indicators associated with the dimensions

Dimension Component Possible Indicators

1. Access

Distribution Channels• No. of access points/ 100,000 • % of population lying beyond define

distance from access point

Demographic/geographic• No. or % of people ‘banked’• No. of accounts open by product type• Profile of who is banked

Product eligibility• % of population excluded as a result of

particular product rules

2. UsageProducts & services

• Transaction profile per account• Cost of average profile account

Sustainability• % active accounts• Transactions profile per touch point

Examples of Indicators contd.

Dimension Component Indicator

3. Quality (suitability)

Consumer protection• Number and type of complaints by

channel and type of consumer

Financial literacy• % of households able to answer

defined question

Choice• Range of competing products in

defined markets

4. WelfareDefined behavior • Increased savings behavior

Desired outcomes• Improved consumption of food,

education, etc

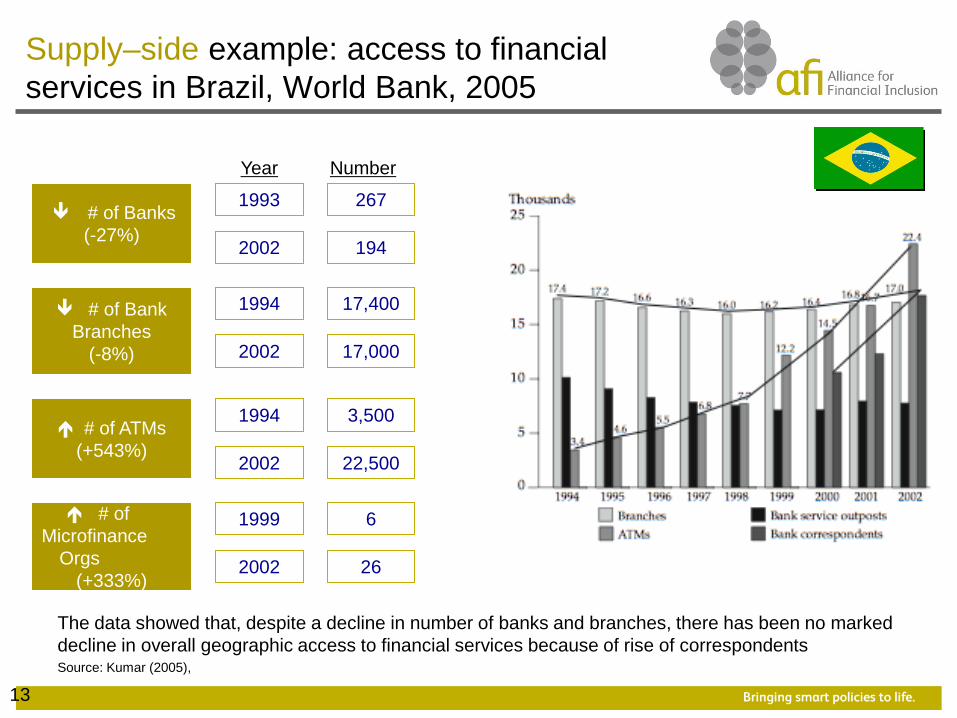

Supply–side example: access to financial services in Brazil, World Bank, 2005

# of Banks(-27%)

# of Bank Branches

(-8%)

# of ATMs(+543%)

# ofMicrofinance

Orgs(+333%)

Year

1993

2002

267

194

1994

2002

17,400

17,000

1994

2002

3,500

22,500

1999

2002

6

26

Number

The data showed that, despite a decline in number of banks and branches, there has been no marked decline in overall geographic access to financial services because of rise of correspondents

13Source: Kumar (2005),

Various cross country supply side efforts are gathering pace…

14

Survey Name Institution # of countries Frequency Data collectedCGAP Global Survey on Access Financial Services(ff Banking the Poor)

135 countries (2009)

Annual

Number of accounts in regulated institutions, ATM cards, machines and loans as well as data on costs, collateral and disclosure.

International Financial Statistics(Upcoming, to be presented)

190 countries. Annual

8 indicators using number of all financial institutions, including branches, ATMs, number of depositors and borrowers, and financial services (deposits, loans, insurance technical reserves).

National demand-side surveys have been completed in more than 25 countries

Timor Leste –WB

Indonesia–WBS. Africa (Diaries),

Kenya, Lesotho, Malawi, Mozambique, Rwanda, Swaziland, Tanzania, Zambia-FinScope

Namibia, Botswana –FinScopeWB

Nigeria -FinScope

Mexico – WB

Columbia –WB

Brazil– WB

India – WB; Diaries

Bangladesh –Diaries

Pakistan –WB; FinScope

Iran– WB

Ghana - WB

Seeking international comparability of globalheadline demand-side indicators

•Global Financial Access Snapshots of high-level repeated comparable financial access indicators from demand side add-on to existing cross-country surveys.

•Being undertaken by DEC, World Bank under a Gates Foundation grant from 2010, likely to deliver first round in 2012

- Multi-country outreach (100-130 countries)

- Individual-level surveys to be conducted in household

- Repeated every three years- Ability to segment by key demographics

Attributes

Standardized questionnaire to be added onto an already existing survey- Account ownership- Frequency of use (deposit/withdrawal),

- Connection to the payment system,- Means of deposit and withdrawal of cash,

- Reasons for not having an account

Proposed Question Content

16

17

2) Defining & measuring financial inclusion

3) Selecting the appropriate approach

1) Understanding the rationale and scope

To create a common framework of understanding of the issues and choices surrounding the measurement of financial inclusion

Where does the data come from?

18

National profile of financial inclusion

National Surveys

How many use this instrument?

Who are they?

Who are the non-users and why?

Attitudes to different services & providers?

RCTs, focus groups

Panel studies

Size of financial flows and portfolio allocations?

Impact on welfare of service or policy?

Demand sideSupply side

Provider data

Fees paid?

User profiles?

Product eligibility rules?

Geographic distribution

Provider/Ombuds

Consumer vulnerabilities

Credit bureaus

Aggregate indebtedness profiles?

Different demand side survey techniques are available to meet different objectives

Type of survey Definition Survey Objective Examples

One time cross -section

Cross section of the population is randomly selected and interviewed once

Snapshot of current level of financial access

- FinScope Zambiia- World Bank Access to finance

Repeated cross section

As above, but subsequently another cross section of the population (resembling the first sample) is randomly selected and interviewed once using same or similar instrument.

Monitor progress of financial access across time.

- FinScope – South Africa, Kenya- Survey of Consumer Finances (SCF) USA

PanelThe same households/individuals are interviewed multiple times at regular intervals.

Can be used to show a causal impact of changes in policy if combined with other factors.

-Financial Diaries - ENNViH (Family life survey)-Mexico---Thailand

19

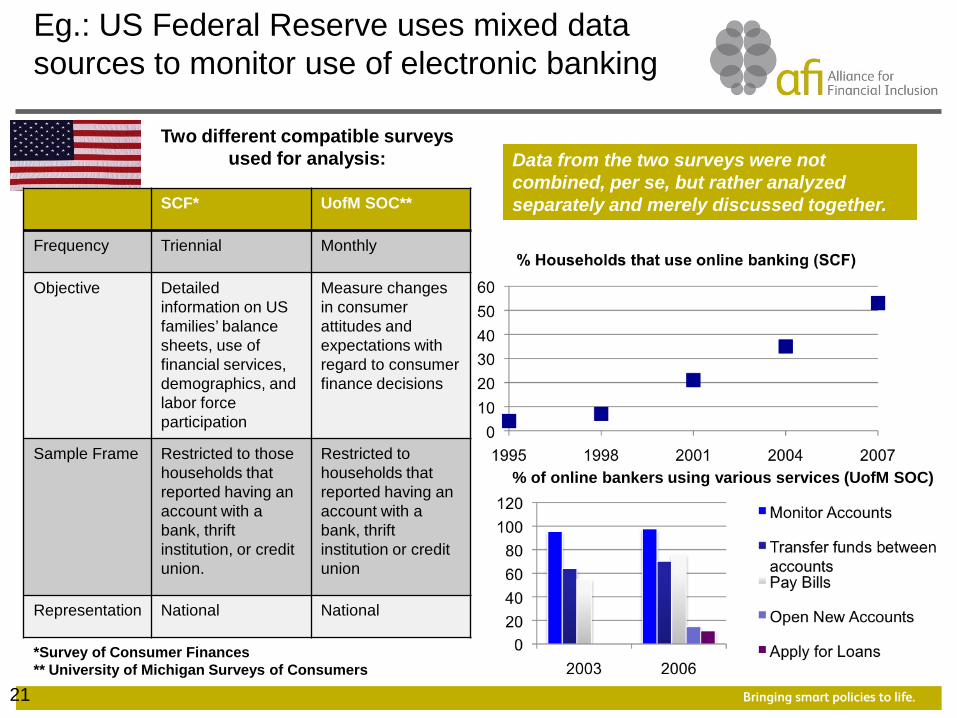

Eg.: US Federal Reserve uses mixed data sources to monitor use of electronic banking

Two different compatible surveys used for analysis:

SCF* UofM SOC**

Frequency Triennial Monthly

Objective Detailed information on US families’ balance sheets, use of financial services, demographics, and labor force participation

Measure changes in consumer attitudes and expectations with regard to consumer finance decisions

Sample Frame Restricted to those households that reported having an account with a bank, thrift institution, or credit union.

Restricted to households that reported having an account with a bank, thrift institution or credit union

Representation National National

21

Data from the two surveys were not combined, per se, but rather analyzed separately and merely discussed together.

% of online bankers using various services (UofM SOC)

*Survey of Consumer Finances** University of Michigan Surveys of Consumers

Design new surveyImpact

Quality

Survey objective and survey approach are closely related

Usage

Access

Resources

Com

plex

ity

Survey Objective

Resources

Com

plex

ity

Survey Approach

Leverage existing surveys

Gather available

data

22

Timeline for creating a survey

23

1 4 5 6 7 8 9 102 3

Indicative timeline drawn from FinScope SA process, which spans 10 months developing, implementing, analysing and launching an annual demand-side survey

Build user/funder consortium : Determine which institutions (e.g. commercial banks but could be donors or govt agencies) will join the research effort as syndicates

Finalize Questionnaire: Collect input from syndicates members and pilot

Field Work (2 months) -contracted by a large survey house

Analysis and Verification (2 months) -Done by the market research team as well as in house analysts

Dissem-ination: high profile event

Number of Months

Survey costs vary with sample size and complexity

0

100,000

200,000

300,000

400,000

500,000

600,000

0 1000 2000 3000 4000

Sample Size

Sur

vey

Cos

t (U

SD

)

24

Legend:Panel Design Cross section – add on

moduleCross-section new survey

Other stakeholders have an interest in the data, and may support/ benefit from survey efforts

25

Regulators

Private Sector

Providers

Statistical Bureau

Other Government

Agencies

Many data needs across stakeholders will overlap…

Example: Finscope in Zambia

In Zambia, a number of banks have responded positively to headline data provided by a FinScope survey.

Barclays

Justified the re-opening of a number of branches and service centres in non-urban areas.Created a new brand and business model specifically focused on the unbanked

ZANACO

Launched a mobile banking venture similar to Wizzit

DunavantCreated a mobile payment linkage for 150,000 of its cotton-growers

Institution Initiative

The role of regulators in surveys varies widely

RegulatorsZambia Kenya US Fed Indonesia

Design FundAnalyzeDisseminatePublicly available data

Y Y Y N

26

Fully responsible

Partially responsible

No responsibility

Beyond measurement, surveys can also be used to deepen understanding of financial inclusion

1. Measurement

2. Deepen Understanding

Identify priorities

Measure progress over time

Test hypotheses about relationships between financial inclusion and other variables

Determine the impact of particular policies and programs

Main Purpose Specific Purpose

Incentivize Reform

27

Example: going deeper…

28

The Financial Diaries approach seeks to understand the usage of financial instruments by poor households at a detailed level. Diaries can track cash flows accurately in ways that

other surveys do not. In this way, the portfolios of the poor can be better understood.

Mea

n an

nual

Sav

ings

A

ccum

ulat

ion

(US

D)

Conclusion

• Measuring the dimensions of financial inclusion is both feasible and desirable but carries costs and tradeoffs– An increasing range of robust measurement approaches and

instruments is available– These must be tailored according to objective and resources

available.• The regulators’ role may not always be to provide demand side data

but at least to support its collection and use it, together with supply side information to measure and understand.– Most countries concerned about inclusion need a credible

national financial survey repeated at suitable intervals. • If financial inclusion cannot be clearly defined, it cannot be clearly

measured. While the definition will vary across country, it is possible to harmonize underlying concepts and understandings. An ISO-type approach to defining the components

29