financial crisis and brazil’s economic...

TRANSCRIPT

Otaviano CanutoVice President & Head of Network

Poverty Reduction and Economic ManagementThe World Bank

The 11th International Academic Conference on Economic and Social Development

April 6-8, 2010

Moscow

Main Messages Aggressive counter-cyclical policies minimized the

impact of the crisis on the Brazilian economy

The use of foreign reserves, monetary, fiscal and quasi-fiscal policies was made possible because of policy space previously acquired

Looking forward, a main challenge will be to increase the role of knowledge in competitiveness

Poverty reduction may help growth by strenghteningdomestic demand as a growth driver

2

Brazil: From Decoupling to Derailing… to Decoupling again?

Mechanisms of Transmission of the Crisis

Weak global demand and lower prices of exports

The Systemic Sudden Stop and foreign capital flows

Effects on exchange rates

Lines of Defense

Uses of international reserves

Easing of monetary policy

Uses of fiscal and para-fiscal policies

3

The Brazilian Economy seemed to be decoupling at high speed… until it came to a sudden stop

Source: IBGE

Domestic Demand and Supply GDP growth – IIIQ08

Source: Itau (presentation by Tomas Malaga)

4

5Source: IBGE, Secex e Funcex.

Trade, Credit Sudden Stop and Inventory Adjustments were the main channels of transmission

104.4

96.8 92.4

80.682.5

69.6

100

65

70

75

80

85

90

95

100

105

110

Jan-0

8

Feb-08

Mar-0

8

Apr-08

May-

08

Jun-0

8

Jul-0

8

Aug-08

Sep-08

Oct-0

8

Nov-08

Dec-08

Jan-0

9

Feb-09

Mar-0

9

Apr-09

May-

09

Jun-0

9

Jul-0

9

Aug-09

Sep-09

Exports of Manufactured goods

Industrial Production

Retail Sales

Industrial Production, Retail Sales and Exports(index: September 2008=100)

Back to the long-term growth path

6

Real GDP

Source: JPMorgan,GDW 03/12/10

7

9.32007

8.0 20082009

6.8

2010

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Average unemployment rate (%) - IBGE

8.2

7.2

Unemployment Rate Dropped—despite the initial shock— from 9.3% in Jan ’07 to 7.2% in Jan ’10… and Wages Increased

Source: IBGE

REAL WAGES - Average for the last 12 months

R$ Billion

29.56

29.36

28.66

26.68

25.13

23.61

21.93

21

22

23

24

25

26

27

28

29

30

Aug

-04

Dec

-04

Apr

-05

Aug

-05

Dec

-05

Apr

-06

Aug

-06

Dec

-06

Apr

-07

Aug

-07

Dec

-07

Apr

-08

Aug

-08

Dec

-08

Apr

-09

Aug

-09

Dec

-09

Source: IBGE

8

Sectors

US$ billion

Growth

2005-2008 2010-2013

Oil and Gas 112 171 8.8

Mining 29 25 (3.1)

Steel 15 20 5.7

Petrochemical 5 17 28.9

Vehicles 12 17 7.3

Electronics 8 12 6.7

Pulp & Paper 10 10 0.5

Industry 191 271 7.3

Source: BNDES

Investments strongly rebounding

16.4

17.6

19.0

21.2

20.2

18.6

16.9

15.0

16.0

17.0

18.0

19.0

20.0

21.0

22.0

2006 2007 2008 2009 2010 2011 2012

Forecast

Domestic-led Sectors Have Already Recovered Investment in Industry

Forecast of Investment Ratio 2009-2012 (% of GDP)

Crisis Response (1):Injection of Liquidity in Foreign Currency Market

9

o Sales of USD in spot market;

o Sales of USD in repurchase agreement auctions;

o Reduction of reserve requirements for banks acquiring USD with repurchase agreement;

o Sales of USD swap contracts;

o Export financing;

o Authorization for BCB to engage in currency swap transactions with other central banks (US$ 30 billion swap line with Federal Reserve);

o Loans to rollover external debt of Brazilian companies.

Crisis Response (2) Injection of Liquidity in Domestic Credit Market

o Reduction in reserve requirements

o Incentives for banks (including public banks) and the deposit insurance fund (FGC) to acquire portfolios of small and medium size banks

o Increase of funding to BNDES (Development Bank) and rural credit;

o Guarantees for Certificates of Bank Deposits issues by small and medium size banks

10

Interventions by the Central Bank in the FX Market and International Reserves

11

12

Credit/GDP Ratio Grew Even After the Shock

Evolution of Credit/GPD ratio (%)

22.0

24.0 24.5

28.1

30.2

34.2

41.3

45.0 44.6

20

25

30

35

40

45

50

2002 2003 2004 2005 2006 2007 2008 2009 2010*

Source: Brazilian Central Bank

*Up to January

13

State-owned Banks Sustained Credit after the Crisis

BNDES alone was responsible for 37% of the increase in credit from Sept ’08 to Jan ’10

Source: Bacen

Contribution to Credit Growth (Sept. ’08-Jan ’10)

Credit Growth(Index: Sept. 2008 = 100)

Private

Banks

27%

BNDES

37%

Other State-

owned Banks 36%

100

109.0113.9

118.3121.2

100

106.9

132.9

150.1

144.6

141.2

138.8

109.5

105.6

103.2

103.3

102.4

102.9102.6

90

100

110

120

130

140

150

Sep

-08

Nov

-08

Jan-

09

Mar

-09

May

-09

Jul-0

9

Sep

-09

Nov

-09

Jan-

10

Public Banks

Private Banks

Crisis Response (3): Fiscal Policy (with low impact on public debt)

14

54.1

72.9 France

56.9

76.2 Germany

101.3

117.0 Italy

80.4

115.0 Japan

38.3

75.1 UK

42.3

66.8 US

43.4

38.8

43.9

42.0 Brazil

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

110.0

120.0

2003 2004 2005 2006 2007 2008 2009 2010

Forecast

Public Sector Net Debt (%GDP)

Source: IMF and Brazilian Central Bank.

Brazil’s Growth Drivers

15

Brazil as a natural resource-rich economy

Role of knowledge in economic competitiveness and the structure of global trade

Business environment, renewable energy, and modern agriculture as Brazil’s economic strengths

Domestic demand as an important growth driver

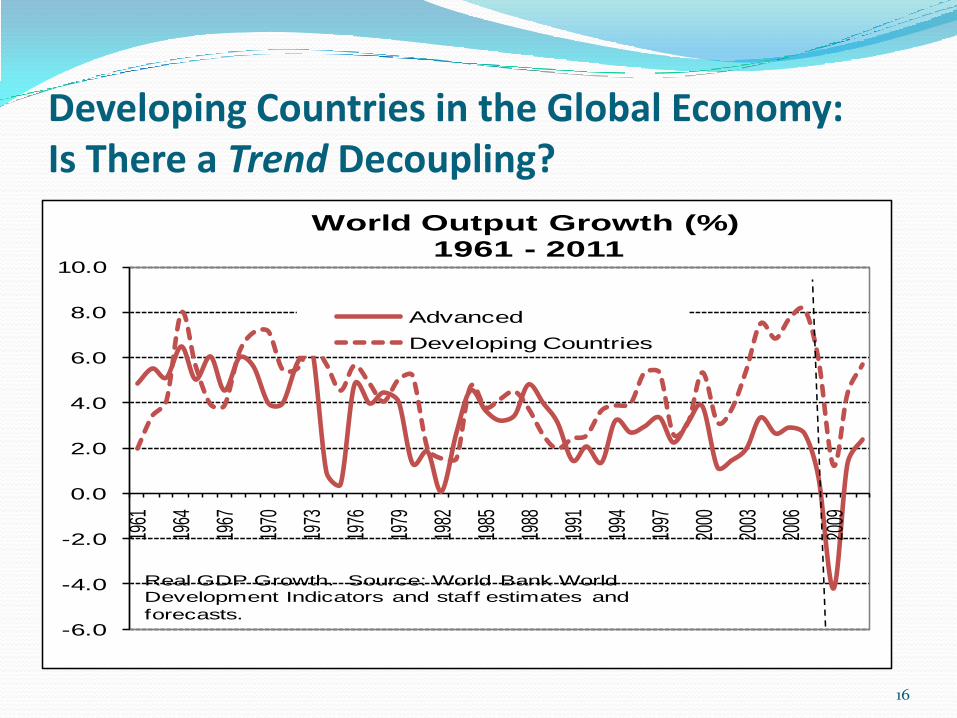

Developing Countries in the Global Economy: Is There a Trend Decoupling?

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

World Output Growth (%)

1961 - 2011

Advanced

Developing Countries

Real GDP Growth. Source: World Bank World Development Indicators and staff estimates and

forecasts.

16

Unexpected Growth Resilience in Developing Countries … not just China and India

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

< -6% -6 to -4 -4 to -2 -2 to 0 0 to 2 2 to 4 4 to 6 > 6%

Freq

uenc

y

Frequency Distribution of GDP Growth

in 2009 - Developed and Developing

GDP Growth in 2009 (%)

Developing

countries (113). Median growth: 1.3%.

High Income

countries (38). Median growth: -3%.

Source: World Bank DEC Prospects Group 17

Brazil and Russia’s Export Structure, 2008

18

Primary products

37%

Manufactured products

47%

Semimanufactured

products14%

Special operations

2%

Iron ore and

concentrates 8%

Petroleum oils, crude

7%

Soybeans6%

Airplanes 3%

Meat 3%

Brazil’s exports -main products(26% of total exports)

Brazil’s Exports by aggregated factor

Source: MDIC/Secex

Source: Federal State Statistics Service, Russia

Russia’s principal exports (share of total)

Mineral products

70%

Chemicals 6%

Metals, precious stones

13%

Machinery, equipment and

transport means

5%

Other6%

Global Trends in Commodity Prices

19

0

20

40

60

80

100

120

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

Crude Oil Price: 1900-2011

(constant 2008 $/bbl)Forecasts

Source: Through 1900-2009: BP Statistical Review of World Energy and through 2010-2011: World Bank estimates

20

Knowledge-based economies grow faster

Differences between Brazil and the Republic of Korea, 1956–90

Product diversification, adding value to commodities, and improving competitiveness in manufacturing and service exports are pivotal for Brazil’s global competitiveness and long-term growth

Increasing Role of Knowledge in Competitiveness and the Structure of Global Trade

Brazil: Current-account Balance

21

Competitiveness in Business Environment

22

Global Competitiveness Index of 134 countries: Innovation and sophistication factors 2008–2009: Brazil and selected comparators

Brazil’s competitive advantage in business environment, incl. sophistication of firms’ production processes, capacity for innovation, and marketing and consumer orientation

23

Brazil’s potential to create opportunities for energy- and water-intensive industries

Competitiveness in Renewable Energy

Successful application of innovation by investing in agricultural R&D (increase in wheat and soy productivity that helped boost exports) and personnel education

Genetic improvement and more efficient production systems contributed to a revolution in the production of meat in Brazil

Strong performance in agro-energy

24

Competitiveness in Modern Agriculture

Annual growth rate of productivity

Brazil’s Long-term Challenges

Resume and strengthen long-term planning (energy, logistics, environment, IT infrastructure, ...)

Promote and stimulate domestic savings in order to provide long-term funds for investment (banks and capital market)

Develop capacity for innovation and competitiveness in manufacturing, and promote global presence of Brazilian companies (vs. significant challenges due to exchange rate appreciation – Dutch Disease)

Increase opportunities for social mobility (job expansion, development/improvement in education) and reduction of the inequality in income distribution

Promote innovation and development of renewable energy sources.

25

Concluding Remarks this crisis has returned fiscal policy to center stage as a macroeconomic

stabilization tool.

most of the pre-crisis consensus on macroeconomic policy still holds, but the crisis has shown that policy makers should adopt a broader macro-prudential view of the financial sector.

the social impact of a sharp slowdown in GDP during the crisis in emerging countries was transmitted mainly through lower employment and wages, hence the importance of targeted social safety nets and automatic stabilizers.

the post-crisis world will likely require countries to do more to improve their investment climates.

in Russia, as elsewhere the crisis has provided an opportunity for reform and impetus to rethink and accelerate public sector, financial sector, and diversification reforms; it is important to see to it that the opportunity is not wasted in the complacency and return to business-as-usual after the crisis

26