financial bulletin_mmc_ibs_oct_2012

DESCRIPTION

Financial bulletin is the monthly newsletter of the official finance club of IBS Hyderabad. It covers topics related to finance & economics.TRANSCRIPT

D A T E D : 3 0 O C T O B E R , 2 0 1 2

V O L U M E 1 7 , I S S U E 1

T H E F I N A N C I A L B U L L E T I N

I N S I D E S T O R Y

The fall of microfinance 3

Basel III and its impact on banking industry

13

Euro Crisis simplified 17

Understanding high frequency trading

20

A new bold arbitrage play 23

Will FDI provide safe landing to Indian Aviation

28

Money Laundering: A major concern

32

CRR:A necessary evil 6

Responsible banking for sustainable development

9

From The Editors Desk

TEAM

Dear Readers,

With the view that we are in the age of change and reformation of the economic, social ,financial structure. And with so many developments taking place in the country for strengthening the macro and micro economic factors through various fiscal and monetary policies. It is necessary to understand the pros and cons of the various measures. As newton says “every action has a reaction” hence changes will have consequences, but the fact that they are important for society to move on to newer heights they cannot be avoided. In this volume you will find out the various measures being taken by the government in pursuit of increasing the GDP growth rate, like FDI, CRR, Basel III etc. and what will be the pros and cons of it. Hope you will appreciate the perspectives of our contributors and gain an insight into what’s going on in the country.

Happy Reading!!!

C O N T R I B U T O R S

Rakesh Kumar Reddy, IFMR Chennai

Manoj Shankar, IFMR Chennai

Abhay Kumar, IIT Roorkee.

Prateek katariya, IFMR Chennai

Vivek Srivastava,IFMR Chennai

Krishnendu Saha ,MDI Gurgaon

Shovik Kar ,MDI Gurgaon

Akshay Iyer ,SIBM Pune

Aravind Ganesan ,IIM Indore

Rohit Maloo ,IIM Indore

Madusudanan, NMIMS

Harish, NMIMS

Varun Sanghi, MDI Gurgaon Sibojyoti Chakrabarti , ITM Navi Mumbai

D A T E D : 3 0 O C T O B E R , 2 0 1 2 V O L U M E 1 7 , I S S U E 1

Advisor:

Dr. V. Narendra

Faculty Co-ordinator: Dr. S. Vijaylakshmi

Student Co-ordinator: Roshni nair

Edited and designed by:

Vikas Singh

Banisha Chopra

WINNERS OF ARTICLE OF THE MONTH:

CONGRATULATIONS!!!

Rakesh Kumar Reddy

&

Manoj Shankar

IFMR,Chennai

“100% repayment rate”, the newspaper headlines screamed - a treat to cherish about if it was in any other occasion but it is all about the microfinance world for now. An industry which started for all the right reasons, ended up in the news for all the wrong ones. This article wishes to highlight how and why the heroes became villains.

Crisis of Conscience

Microfinance was started as the financial world’s answer to the millions at the bottom of the pyramid who could not afford regular financial services. Microfinance came to be seen as the silver bullet to a large variety of problems faced by the poor. The inception of organizations like Grameen Bank in Bangladesh followed by the Self Employed Women’s Association (SEWA) in India heralded a new way in which the world reached out to help the poorest of the poor. The initial notion was to provide small loans and other financial service sat a manageable interest rate much lesser than that which was offered by the local money lenders to the BPL families thus helping them to become sustainable micro entrepreneurs. The system had the mission to help the poor to survive and thrive. The self help groups (SHG)

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

An industry

which started

for all the

right reasons,

ended up in

the news for

all the wrong

ones.

Page 3 V O L U M E 1 7 , I S S U E 1

Rakesh Kumar Reddy IFMR,Chennai

Manoj Shankar IFMR,Chennai

which were started as a part of microfinance initiative tried to inculcate a savings culture among poor and by that way they were able to provide the poor with loans from their own capital. By creating this group lending system, whereby if one member of the group defaulted on the payment, the entire group had to pitch in for his payment, or be barred from new loans, they ensured that no one defaulted, hence the very close to 100% repayment rate.

Grameen Bank, which gave its first loan of $27 to a group of 42 families1, believed that by empowering the poor with small loans they could help create sustenance and provide them with earnings for the future. Initially these ventures were sustained and supported by like-minded individuals and institutions which saw microfinance as a genuine way for helping the poor. Most of the initial funding came from institutions and people in the not-for profit sector, for e.g., The Ford Foundation supported Grameen Bank with an initial grant. Hence, when newer players came into the sector they also tried to mimic the model which was first originated in Bangladesh and then followed successfully by nations all over the world.

Initially in the later part of the 20th

century newer entrants into the microfinance sector started out with the same aims as those of its peers in the industry. Helping the underprivileged and the needy through micro loans was a way they thought they could make an impact on the society. But as things progressed, all is not what it seemed. Most of the newer entrants had plans to go beyond the microfi-nance space for various reasons including the restrictions and regulations imparted on them by regulatory authorities and wanted to morph into Non-banking finance corporations (NBFCs) or wanted to go the for-profit way, although staying true to their microfinance roots. This created a “crisis of conscience” as several of those who founded these new companies or had been on their boards, questioned this transformation. To add fuel to the fire, the source of funding for these new institutions came from new age finance organizations like private equity whose motives where for profit. The intentions of promoters were also being questioned, as allegations of diversions of funds came to light. Final nail in the coffin came, when some of these institutions wanted to go public by listing on stock exchanges. Hence the question arose, that whether those who are a part of the field are for the people or for profit?

Crisis of confidence

As any industrialist will tell you, an industry exists with the for-profit motive, but not with the microfinance industry, as it was seen as a benevolent venture to help the poor. So when allegations of profiteering and mismanagement came to light, its second crisis started. What people saw and what was being heard about these institutions did not go well with the public at large. From the lay man on the street

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 4 V O L U M E 1 7 , I S S U E 1

to those whom the industry served, began questioning the intentions and motives of their perceived benefactors. As this was not enough allegations of heavy handedness in debt collection and news of suicides gave a big blow to the already fragile image of microfinance. Over indebtedness among the poor due to competing firms offering competing loans also became a huge social issue. The once benevolent image was now replaced by the image of the Frankenstein monster. What went wrong? Whom to blame? Could they have done things differently?, these were questions on everyone’s mind. As the confidence began to dry up, and very fast at that, people within these organizations and outside began to wonder about the ways and means by which the problem was being approached. Investors wanted returns, people wanted institutions that were there to help them, the public at large wanted to believe in the story of the rich helping the poor, all these expectations created the perfect recipe for disaster, as it happened in this industry. To make things worse, internal conflicts within the management of these firms took a life of their own, thus shaking the very foundations on which these firms rested on, “peoples trust”, thereby leading to a crisis that was neither expected nor called for.

Crisis of Faith

Were the promoters at fault, or was it the staff? Or was it the microfinance model they followed itself wrong from the start? The answers to these questions are not easy to come by. It is always

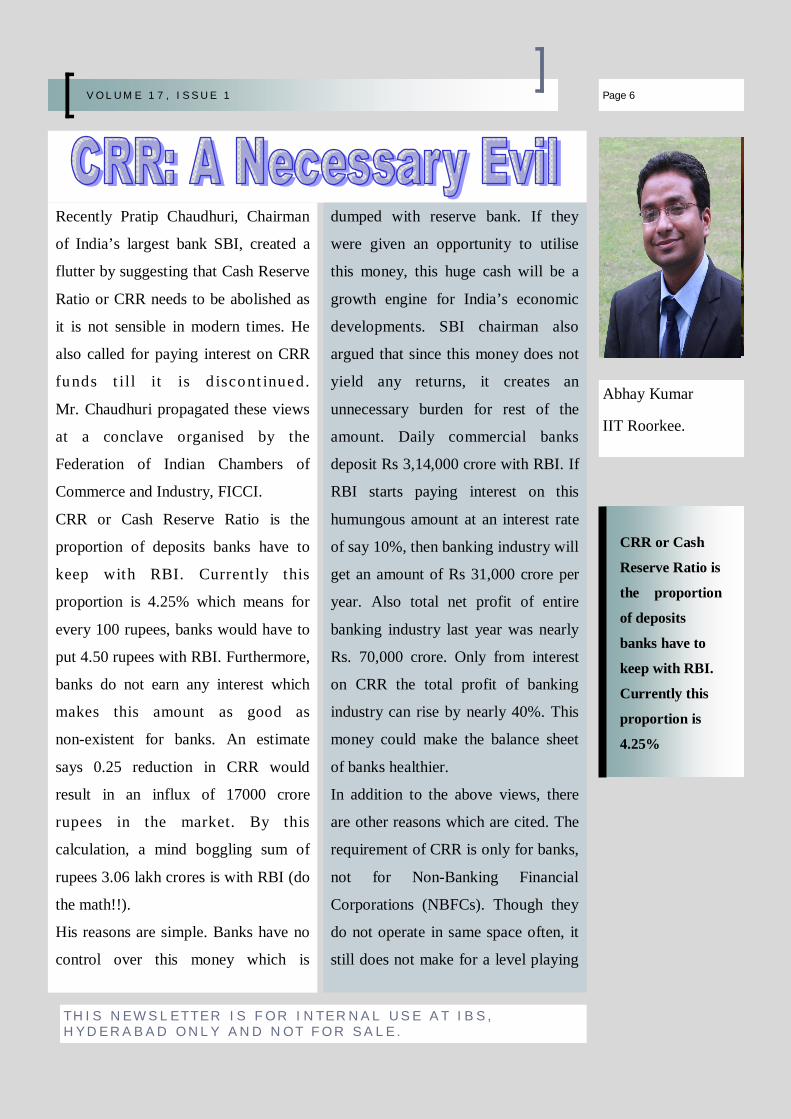

easy to point the finger of blame at the actors, but the truth, as always, might be far from what it seems. Yes, some blame has to be borne by the founders and representatives of these firms, but blame also lies on the investors, the regulators, and also the public at large for being naïve and not concerned about the workings in such a crucial sector and solely focusing on their individual objectives alone. As the events of SKS Microfinance of India involving its founder, Mr. Vikram Akula2 and the management of the firm shows that people in general have lost faith in the idea of the rich coming out to help the poor. As these firms have tried to tap the equity markets with share offerings, it is good to ask, how long before the good faith they had and have in these firms turns into a “crisis of faith”

Conclusion

The last decade has been a roller-coaster ride for the microfinance industry with tremendous highs and lows. Those who were a part of it and those who witnessed it from outside, will take their learning well. For all the ills of the microfinance model, it still remains one of the best ways to serve the poor and the needy in many part of the world untouched by general finance. Time has come to pay more attention to this field by the general pub-lic as closer public scrutiny is the only way we can make sure that microfinance achieves its fullest potential of serving the underserved. Tougher regulatory options, and new laws will always remain on the table as other options to regulate the sector and make it more open and transparent, but as the following crisis’s have shown that if the people themselves do not come forth and take the

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 5 V O L U M E 1 7 , I S S U E 1

responsibility no amount of regulations or laws will stop this industry from falling again.

Recently Pratip Chaudhuri, Chairman

of India’s largest bank SBI, created a

flutter by suggesting that Cash Reserve

Ratio or CRR needs to be abolished as

it is not sensible in modern times. He

also called for paying interest on CRR

funds t ill it is d iscont inued.

Mr. Chaudhuri propagated these views

at a conclave organised by the

Federation of Indian Chambers of

Commerce and Industry, FICCI.

CRR or Cash Reserve Ratio is the

proportion of deposits banks have to

keep with RBI. Current ly this

proportion is 4.25% which means for

every 100 rupees, banks would have to

put 4.50 rupees with RBI. Furthermore,

banks do not earn any interest which

makes this amount as good as

non-existent for banks. An estimate

says 0.25 reduction in CRR would

result in an influx of 17000 crore

rupees in the market. By this

calculation, a mind boggling sum of

rupees 3.06 lakh crores is with RBI (do

the math!!).

His reasons are simple. Banks have no

control over this money which is

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

CRR or Cash

Reserve Ratio is

the proportion

of deposits

banks have to

keep with RBI.

Currently this

proportion is

4.25%

Page 6 V O L U M E 1 7 , I S S U E 1

Abhay Kumar

IIT Roorkee.

dumped with reserve bank. If they

were given an opportunity to utilise

this money, this huge cash will be a

growth engine for India’s economic

developments. SBI chairman also

argued that since this money does not

yield any returns, it creates an

unnecessary burden for rest of the

amount. Daily commercial banks

deposit Rs 3,14,000 crore with RBI. If

RBI starts paying interest on this

humungous amount at an interest rate

of say 10%, then banking industry will

get an amount of Rs 31,000 crore per

year. Also total net profit of entire

banking industry last year was nearly

Rs. 70,000 crore. Only from interest

on CRR the total profit of banking

industry can rise by nearly 40%. This

money could make the balance sheet

of banks healthier.

In addition to the above views, there

are other reasons which are cited. The

requirement of CRR is only for banks,

not for Non-Banking Financial

Corporations (NBFCs). Though they

do not operate in same space often, it

still does not make for a level playing

field. That might be the reason why some people are

supporting the theory of doing away with CRR. For

example, Mr. V Jagan Mohan, MD of AP State

Cooperative Bank Ltd. appreciated the SBI chairman’s

views. He questions the relevance of CRR in this

information age where RBI can get any figures by just

a click.

Though the above views are interesting, not everybody

is ready to accept them. RBI deputy governor K C

Chakrabarty openly came out against SBI chairman’s

opinion. He stressed that CRR is a part of monetary

policy and banks should work in the established

framework. He seems to imply that CRR is a crucial

liquidity management tool which provides regulatory

power to RBI. Below diagrams shows how liquidity is

affected by change in CRR.

CHANGE IN SUPPLY OF MONEY DUE TO CRR

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 7 V O L U M E 1 7 , I S S U E 1

By eliminating CRR, RBI would lose its

power to control or regulate the money

supply. Very few people would want a central

bank to dilute the influence. This has achieved

more significance particularly in the wake of

worldwide economic crisis.

There are other reasons too which are more

technical in nature. If banks are exempted

from CRR then banks would stand as a more

risky option. Adhering to Basel norms, the

change in CRR would also alter Capital

Adequacy Ratio, a ratio of bank’s capital to its

risk. Basically banks may have to set aside

even a larger quantity of cash (though not

with RBI) for risk management which would

prove counterproductive in the long run. No

wonder ICICI bank chairman K V Kamath

joined RBI for continuing with the current

structure.

Lastly with a surging inflation rate, CRR can

be a necessity for handling the money flow.

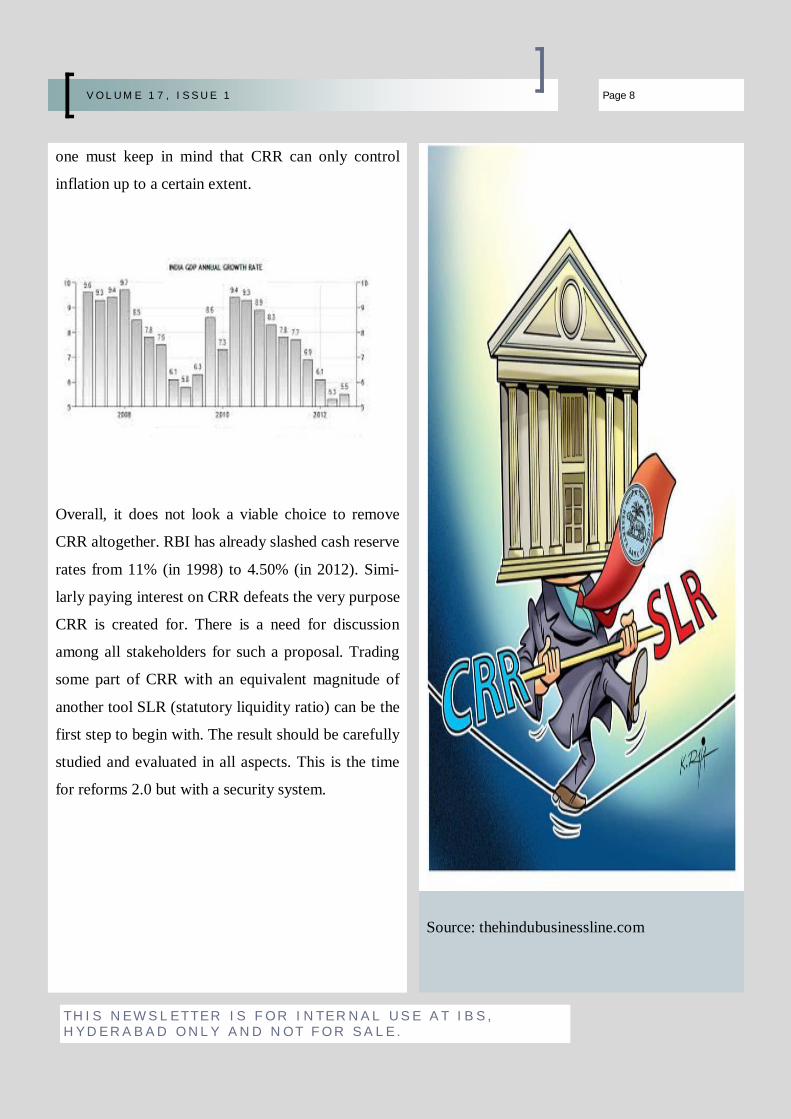

India’s GDP growth was at 5.5 percent in the

second quarter which is lowest in the two

decades; it is expected to be near or less than

5.5 percent in 2012-13 as well. On the other

hand, inflation is near 8% and it is persistently

hovering in double digits for the last 2 years.

For any government, controlling inflation is

prime objective we have to do trade-off

between GDP growth and Inflation, However

At equilibrium CRR increased, decrease in supply of money

CRR decreased, increase in supply of money

one must keep in mind that CRR can only control

inflation up to a certain extent.

Overall, it does not look a viable choice to remove

CRR altogether. RBI has already slashed cash reserve

rates from 11% (in 1998) to 4.50% (in 2012). Simi-

larly paying interest on CRR defeats the very purpose

CRR is created for. There is a need for discussion

among all stakeholders for such a proposal. Trading

some part of CRR with an equivalent magnitude of

another tool SLR (statutory liquidity ratio) can be the

first step to begin with. The result should be carefully

studied and evaluated in all aspects. This is the time

for reforms 2.0 but with a security system.

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 8 V O L U M E 1 7 , I S S U E 1

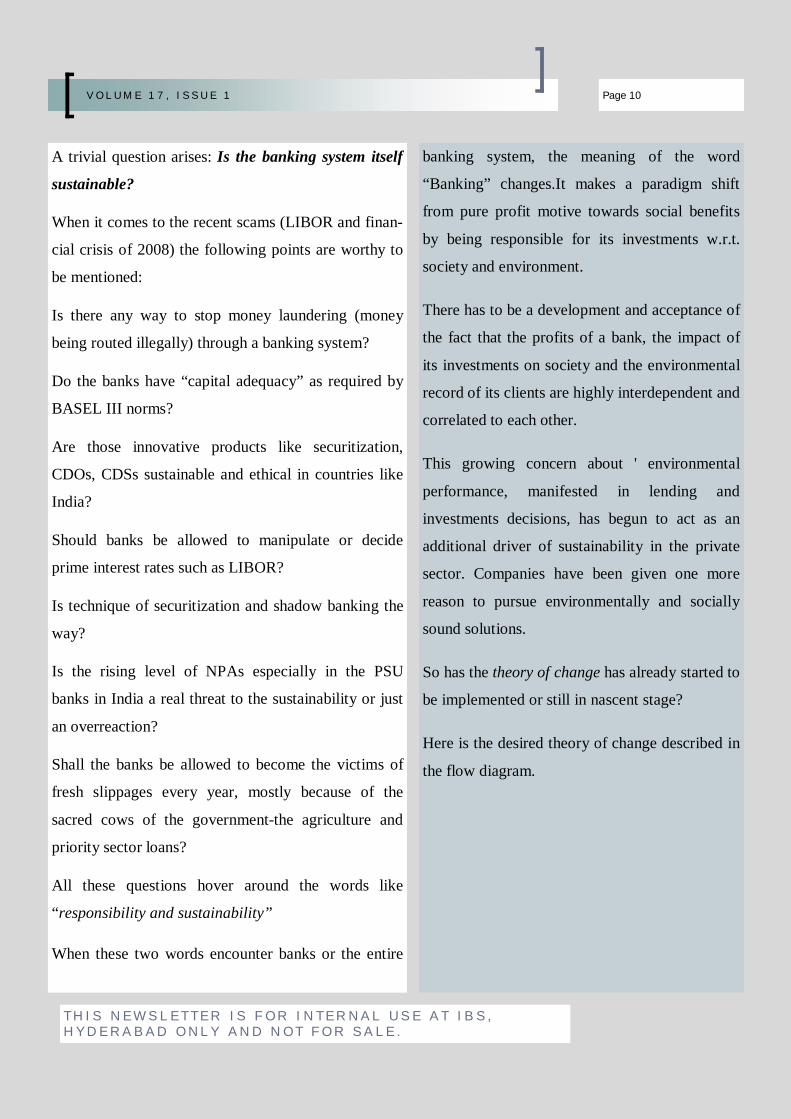

Source: thehindubusinessline.com

Banks, amidst the global economic

meltdown post 2008 crisis, have been

looked upon the most reliable source of

“compassionate capitalism” which aims

to extend its hands towards those who

need the financial inclusion for a

sustained development.

This discussion upon a much sought

after theory of change, which is now

required for the social and economic

upliftment as well as ensuring that the

lost confidence rests again with the

system.

In the modern capitalistic approach,

where the global economy is a “market

driven “mechanism, there has always

been a debate between “pure profit

motives” and the “social benefit

motives”.

In the wake of the Global crisis of 2008,

which had its origins in the banking

system of the US. The fault was neither

in the structure of the system nor in the

fundamentals. The subprime crisis was

the result of “unethical banking

decisions”. The way the “stressed

assets” were bundled together and sold

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

modern capitalistic

approach, where

the global

economy is a

“market driven

“mechanism, there

has always been a

debate between

“pure profit

motives” and the

“social benefit

motives”.

Page 9 V O L U M E 1 7 , I S S U E 1

Prateek katariya IFMR Chennai

as securitized products to the investors,

which, with the busted loans ( the

underlying securities), made those

institutional investors falter which were

considered “ too big to fail”.

The problem did not start with

securitization of potentially bad loans,

but it had its roots in the immoral and

unethical subprime lending to the

housing sector of the economy.

The contagion effect worked, engulfing

the whole global economy into a tryst

of recession, pessimism and faltering

institutions like Lehman Bros and even

AIG.

One would argue that the main cause

for the aforesaid crisis was “slippage of

loans made to the housing sector” but

was it really the one?

Wasn’t it evolution of the greed

component in the banking system

which, pursuing its full profit motive,

led the banks to forget their goals of

ex is t e nce : r e spo ns ib i l it y a nd

sustainability.

Vivek Srivastava IFMR Chennai

A trivial question arises: Is the banking system itself

sustainable?

When it comes to the recent scams (LIBOR and finan-

cial crisis of 2008) the following points are worthy to

be mentioned:

Is there any way to stop money laundering (money

being routed illegally) through a banking system?

Do the banks have “capital adequacy” as required by

BASEL III norms?

Are those innovative products like securitization,

CDOs, CDSs sustainable and ethical in countries like

India?

Should banks be allowed to manipulate or decide

prime interest rates such as LIBOR?

Is technique of securitization and shadow banking the

way?

Is the rising level of NPAs especially in the PSU

banks in India a real threat to the sustainability or just

an overreaction?

Shall the banks be allowed to become the victims of

fresh slippages every year, mostly because of the

sacred cows of the government-the agriculture and

priority sector loans?

All these questions hover around the words like

“responsibility and sustainability”

When these two words encounter banks or the entire

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 10 V O L U M E 1 7 , I S S U E 1

banking system, the meaning of the word

“Banking” changes.It makes a paradigm shift

from pure profit motive towards social benefits

by being responsible for its investments w.r.t.

society and environment.

There has to be a development and acceptance of

the fact that the profits of a bank, the impact of

its investments on society and the environmental

record of its clients are highly interdependent and

correlated to each other.

This growing concern about ' environmental

performance, manifested in lending and

investments decisions, has begun to act as an

additional driver of sustainability in the private

sector. Companies have been given one more

reason to pursue environmentally and socially

sound solutions.

So has the theory of change has already started to

be implemented or still in nascent stage?

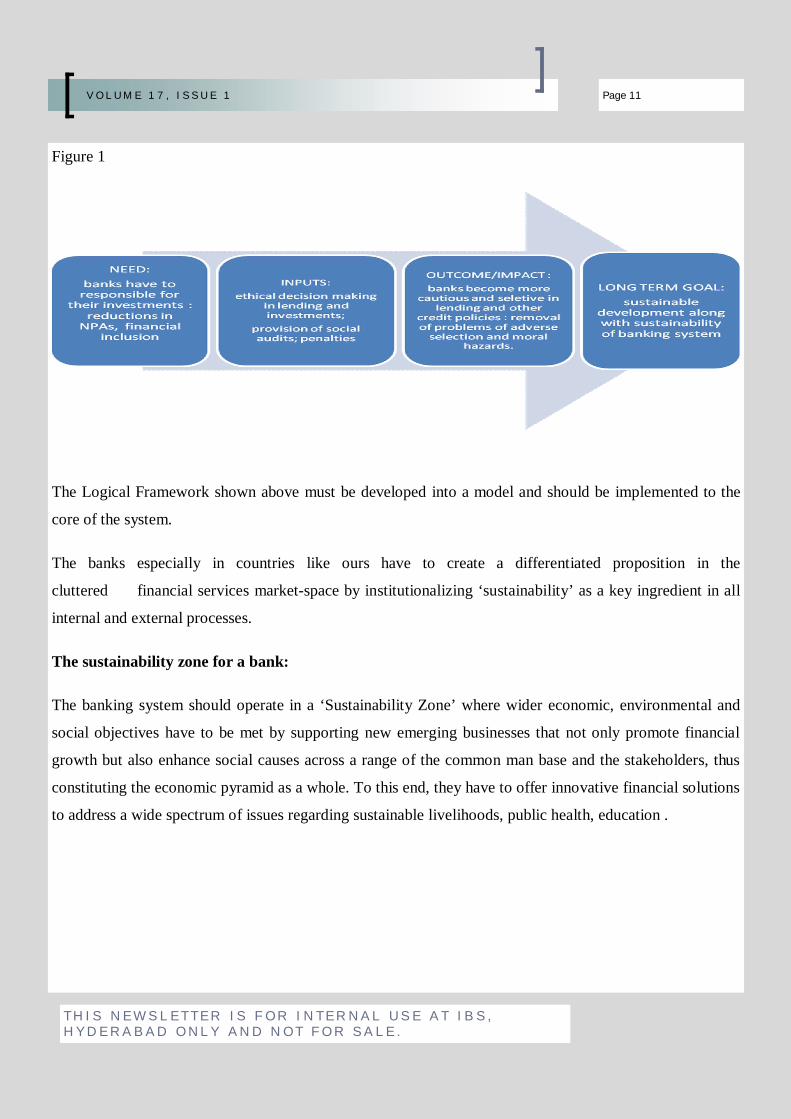

Here is the desired theory of change described in

the flow diagram.

Figure 1

The Logical Framework shown above must be developed into a model and should be implemented to the

core of the system.

The banks especially in countries like ours have to create a differentiated proposition in the

cluttered financial services market-space by institutionalizing ‘sustainability’ as a key ingredient in all

internal and external processes.

The sustainability zone for a bank:

The banking system should operate in a ‘Sustainability Zone’ where wider economic, environmental and

social objectives have to be met by supporting new emerging businesses that not only promote financial

growth but also enhance social causes across a range of the common man base and the stakeholders, thus

constituting the economic pyramid as a whole. To this end, they have to offer innovative financial solutions

to address a wide spectrum of issues regarding sustainable livelihoods, public health, education .

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 11 V O L U M E 1 7 , I S S U E 1

Figure 2

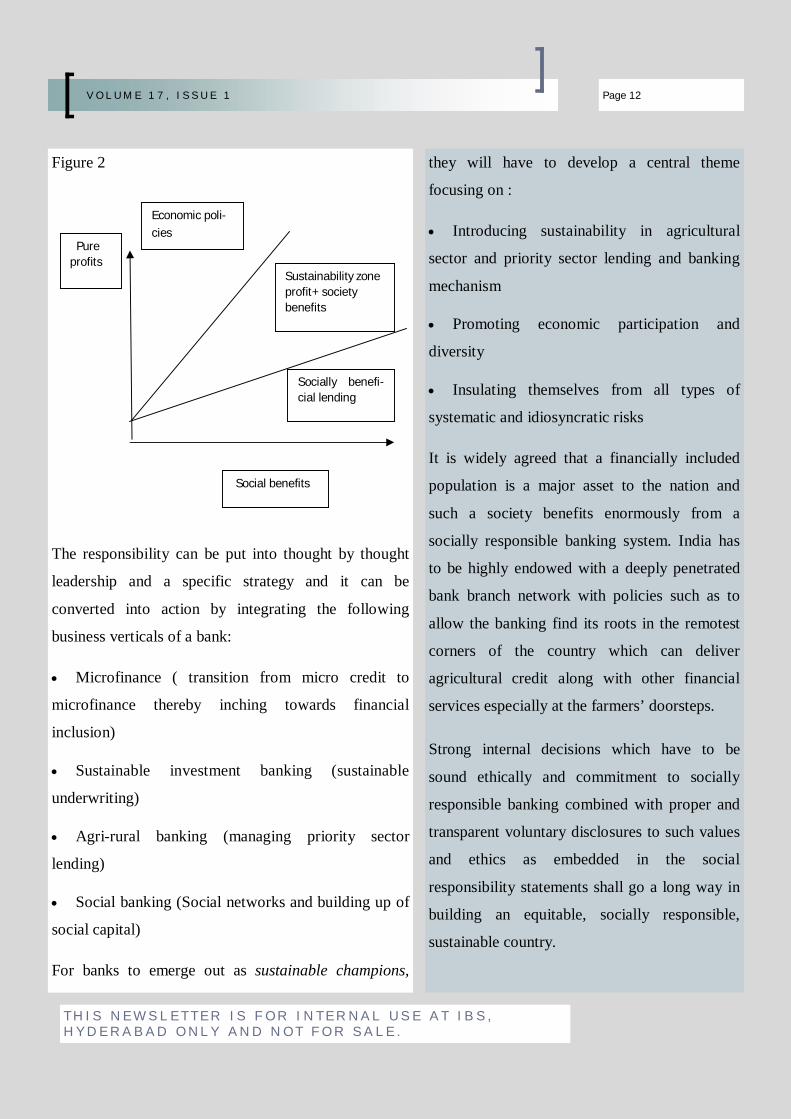

The responsibility can be put into thought by thought

leadership and a specific strategy and it can be

converted into action by integrating the following

business verticals of a bank:

Microfinance ( transition from micro credit to

microfinance thereby inching towards financial

inclusion)

Sustainable investment banking (sustainable

underwriting)

Agri-rural banking (managing priority sector

lending)

Social banking (Social networks and building up of

social capital)

For banks to emerge out as sustainable champions,

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 12 V O L U M E 1 7 , I S S U E 1

they will have to develop a central theme

focusing on :

Introducing sustainability in agricultural

sector and priority sector lending and banking

mechanism

Promoting economic participation and

diversity

Insulating themselves from all types of

systematic and idiosyncratic risks

It is widely agreed that a financially included

population is a major asset to the nation and

such a society benefits enormously from a

socially responsible banking system. India has

to be highly endowed with a deeply penetrated

bank branch network with policies such as to

allow the banking find its roots in the remotest

corners of the country which can deliver

agricultural credit along with other financial

services especially at the farmers’ doorsteps.

Strong internal decisions which have to be

sound ethically and commitment to socially

responsible banking combined with proper and

transparent voluntary disclosures to such values

and ethics as embedded in the social

responsibility statements shall go a long way in

building an equitable, socially responsible,

sustainable country.

Pure profits

Socially benefi-cial lending

Sustainability zone profit+ society benefits

Economic poli-cies

Social benefits

Basel III (third installment of Basel

Accords), was developed in the wake of

the 2008 US sub-prime crisis. Basel III

will come to effect in Jan. 2013 and has

to be fully implemented by 31st March

2018.The norms of Basel III are far

stricter than the preceding Basel II

norms. The primal focus of the Basel III

norms has been to strengthen the

lenders’ capital base and improve their

ability to withstand shocks. As a result,

capital requirements are stricter. It also

introduces new regulations on bank

liquidity and leverage.

C H A N G E S I N B A S E L I I I

O V E R B A S E L I I N O R M S

The major allegation against Basel II is

its inability to incorporate corresponding

changes in the definition and

composition of regulatory capital to

reflect the changing market dynamics.

This meant that during the financial

crisis in 2008, all the banks in question

were not only Basel compliant but more

than adequately capitalized as far as the

Basel II norms. The market risk models

in particular were unable to capture the

risk from credit derivative products,

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

The major

allegation against

Basel II is its

inability to

incorporate

corresponding

changes in the

definition and

composition of

regulatory capital

to reflect the

changing market

dynamics.

Page 13 V O L U M E 1 7 , I S S U E 1

Krishnendu Saha MDI, Gurgaon

Shovik Kar MDI, Gurgaon

which formed a substantial part of

trading exposure.

In an effort to plug these gaps in the

wake of 2008 crisis, Basel III was

proposed. It is to create a more robust

version than the former to respond to

the current market dynamics. The

primal enhancements entail

Augmentation in the level and

quality of capital

Introduction of liquidity

standards

Capital conversion/counter

cyclical buffer

Leverage ratio

Another feature of enhancement is the

reduced dependency on external rating

agencies through more stringent form

of reporting and addition of Central

Clearing Houses.

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 14 V O L U M E 1 7 , I S S U E 1

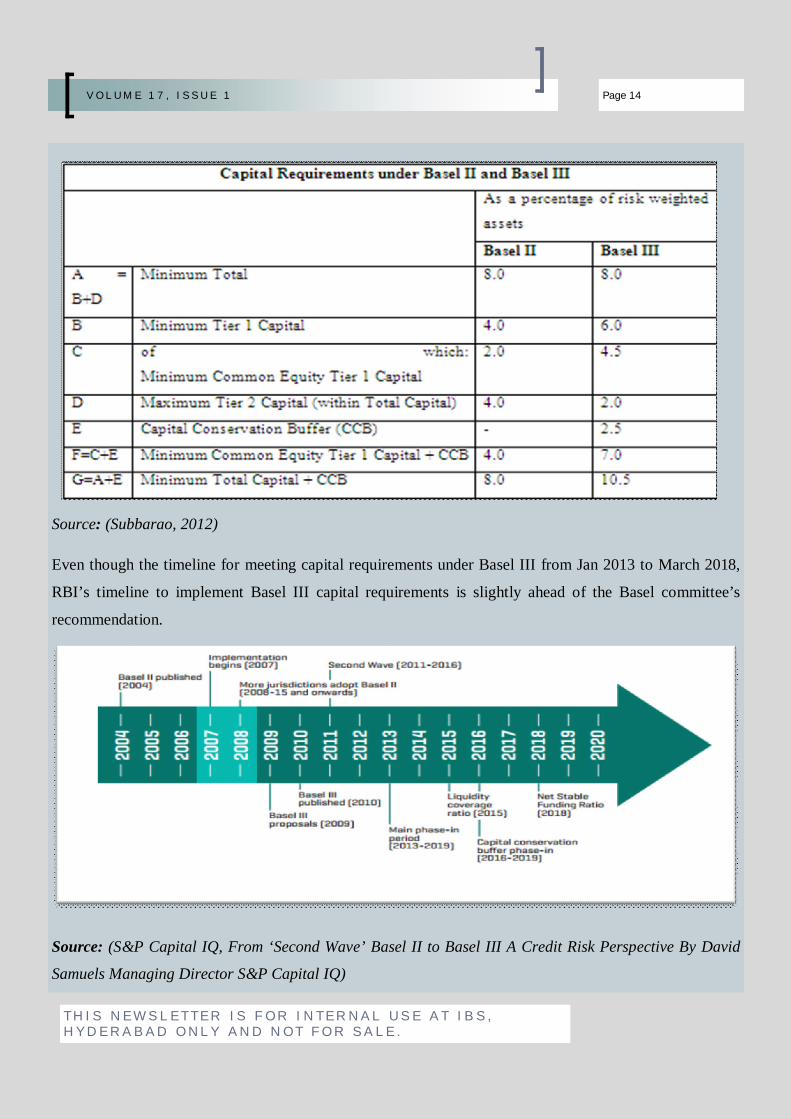

Source: (Subbarao, 2012)

Even though the timeline for meeting capital requirements under Basel III from Jan 2013 to March 2018,

RBI’s timeline to implement Basel III capital requirements is slightly ahead of the Basel committee’s

recommendation.

Source: (S&P Capital IQ, From ‘Second Wave’ Basel II to Basel III A Credit Risk Perspective By David

Samuels Managing Director S&P Capital IQ)

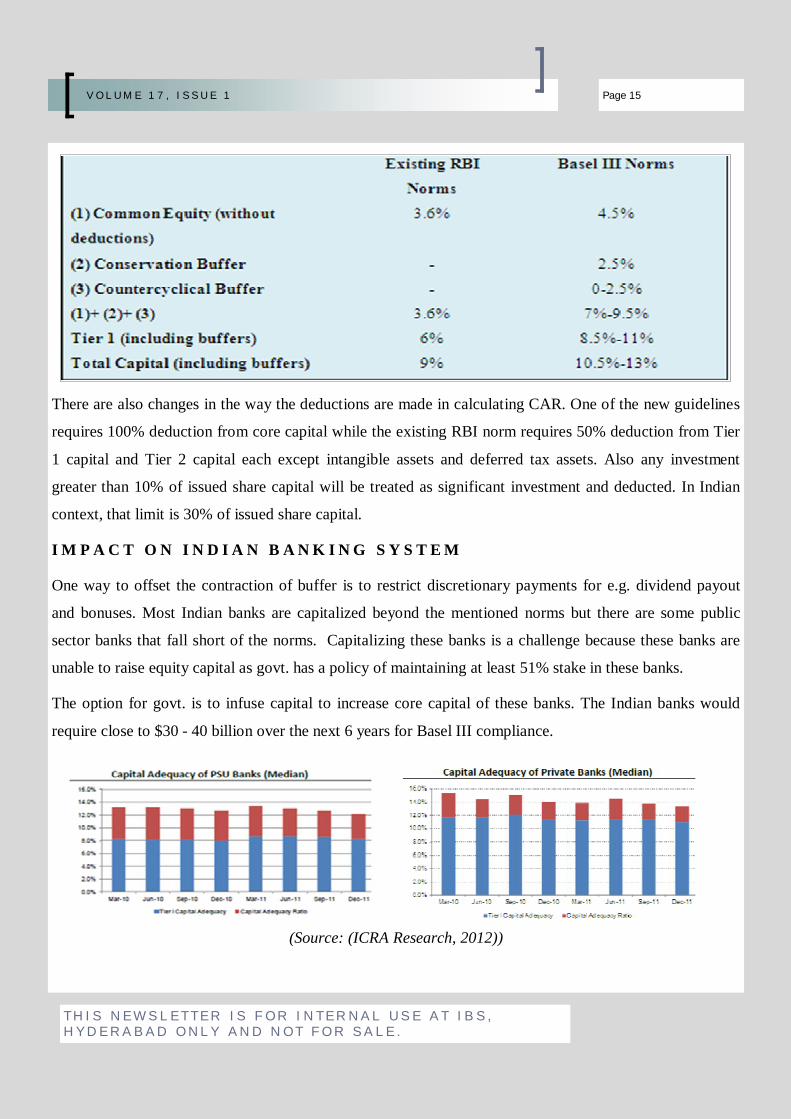

There are also changes in the way the deductions are made in calculating CAR. One of the new guidelines

requires 100% deduction from core capital while the existing RBI norm requires 50% deduction from Tier

1 capital and Tier 2 capital each except intangible assets and deferred tax assets. Also any investment

greater than 10% of issued share capital will be treated as significant investment and deducted. In Indian

context, that limit is 30% of issued share capital.

I M P A C T O N I N D I A N B A N K I N G S Y S T E M

One way to offset the contraction of buffer is to restrict discretionary payments for e.g. dividend payout

and bonuses. Most Indian banks are capitalized beyond the mentioned norms but there are some public

sector banks that fall short of the norms. Capitalizing these banks is a challenge because these banks are

unable to raise equity capital as govt. has a policy of maintaining at least 51% stake in these banks.

The option for govt. is to infuse capital to increase core capital of these banks. The Indian banks would

require close to $30 - 40 billion over the next 6 years for Basel III compliance.

(Source: (ICRA Research, 2012))

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 15 V O L U M E 1 7 , I S S U E 1

The implementation of the discretionary counter

cyclical buffer also poses many challenges as

Using the credit-GDP ratio to look for

inflexion points in the economy can be

difficult as it is an extremely volatile variable

in developing economies.

Credit growth may be a good leading

indicator of economic growth but credit

contraction is a lagging indicator of the

economic downturn.

B A S E L I I I C O M P L I A N C E O R

E C O N O M I C G R O W T H ?

A major criticism against all the three versions of

Basel including Basel III is its inclination to hurt

economic growth. In the case of India, a developing

economy shifting from services to manufacturing

paradigm (to tackle the supply constraints) there is

need for greater investment in the earlier stages.

While Basel accounts for longer term growth

prospects, it creates short term compulsions which

may hinder growth. Thus the risk lies in the transition

period which may be further incremented by

uncertainty until the rules are fully finalized and

comprehended by the banks in the manner it comes to

effect. Hence longer transition period which is

functionally equivalent to longer short term

compulsions entails costs which secures the longer

term but creates uneasiness in the present.

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 16 V O L U M E 1 7 , I S S U E 1

C O N C L U S I O N

The formation of the Basel norms primarily cater

to prevention of a financial crisis and the issues

associated with economic growth acts as collateral

on that behalf. The RBI is willingly accepting the

norms, which shows that the central bank is

willing to incur high cost and also shave off a few

percentage points of growth in the medium term

for long term financial stability. In terms of

growth, the tightening of the capital requirements

can be offset to an extent by proactive fiscal

policy reforms. With the thrust on manufacturing,

mining and infrastructure sectors on one hand and

the tight Basel III capital requirements on the

other, it will pose a huge challenge for the RBI,

government and the banking sector. Given the

slew of reforms that the government is willing to

undertake in allowing FDI in retail, aviation, the

RBI and the government will have to roll out

these reforms (financial stability and fiscal policy)

in sync so that the long term growth outlook is not

hurt.

The idea of creation of common cur-

rency for countries belonging to the

European Union was formed so that

there is better integration among EU

countries & also there is a possibility of

creation of an alternate reserve currency

vis-à-vis the dollar. The countries which

wanted to use this common currency had

to sign the Maastricht Treaty which had

the following clauses:

Inflation rate of the participating

country should not be higher

than 1.5% of the average

inflation rate of the 3 best

performing countries in

Eurozone

The ratio to government deficit

to GDP for a year should not

exceed 3%

The ratio of government debt to

GDP should not exceed 60%

The long term interest rate for a

country should not be higher

than 2% than the 3 lowest

inflation states

Any country that satisfied the above

conditions would be allowed to use the

common currency. By adopting Euro as

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Article to explain Euro Crisis in simple words

Page 17 V O L U M E 1 7 , I S S U E 1

Akshay Iyer SIBM PUNE

their currency & being part of monetary

union countries received a higher credit

rating which helped them borrow at

lower rates. As a result countries like

Greece, Portugal & Italy borrowed

more & more money at lower interest

rates with longer maturities. Also, there

was irresponsible spending by many of

these countries in areas of public

welfare, wage hikes & no formalized

structure which would help them earn

amount of revenue that they were

spending each year. It was also reported

that some of the clauses of Maastricht

Treaty were breached by these

countries & they used creative

accounting techniques to hide these

discrepancies. The clauses mentioned

in Maastricht treaty were broken by

few member nations. Government debt

instead of being limited got doubled in

these years with only 5 countries

having their debt below 60% of GDP.

Also government deficit was not

capped, with only 4 countries falling

below 3%. Also a clause in the Treaty

which restricted countries from being

bailed out in case of economic

problems got broken when a bailout package got

designed for Greece, Portugal & Ireland.

All these were concealed in the years prior to 2008

where the governments were able to pay timely

interest on their borrowings due to well-functioning

global economy. Problems surfaced in 2008, when

there was economic downturn & countries were not

able to make timely interest payments. It was on Jan

14,2009 that for the first time, Standard & Poor

downgraded Greek government bonds to A- , the

lowest rating among Eurozone member states. It also

strangely presented the start of a big crisis that was

about to unravel.

Now that Greek bonds were downgraded, investors

started demanding a higher premium for lending to

Greece, which led to an increase in their borrowing

costs. This leads to a vicious cycle where a country

has to pay a higher cost for borrowing which further

leads to more fiscal strain, which further increases

borrowing cost. S&P also predicted in October 2009

that Greek Debt would increase to 125% of GDP by

2010.As a result, it became more costly to hedge a

Greek bond against default. On April 27, 2010

Greek debt was downgraded to junk status. Thus,

yields on 2 year Greek bonds rose 13% up from

6.3% a few days before. Also, the yield for 10 year

bonds went above 10%.Speculators used this as an

opportunity to bet on the downfall of the euro & the

fact that richer northern European countries will try

to rescue the smaller countries. They speculated us-

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 18 V O L U M E 1 7 , I S S U E 1

ing Credit Default Swaps or CDS, which is an

instrument that lets you buy insurance on a vehicle

or house you don’t own. Whenever there is

damage to that vehicle or house you get

compensated for it even though you do not own it.

Speculators used CDS to bet that Greek bonds

would lose value. If that happened investors would

get compensated for it. To avoid further damage

European Central Bank (ECB) started buying more

of Greek bonds. Thus ECB ended up owning a lot

of junk bonds which increased its risk. In countries

like Greece where economic assistance was

provided, the assistance came with a lot of

austerity requirements which led to unrest within

the country.

The root cause of the crisis was the idea to have a

monetary union within the member countries

without the presence of a fiscal union. As a result

monetary policy is designed by the central bank

but fiscal policy is designed by the member

countries independently. So if a country does not

manage its finances with responsibility it does not

have the option to devalue its currency & make its

exports more competitive & find a way to earn

money. Another outcome of the monetary union

was that countries like Spain could not increase

interest rates even though they saw a huge real

estate bubble building up. One more outcome of

the Euro has been that it has increased the friction

between states as the southern states feel that

northern states are imposing unreasonable austerity

measures on them.

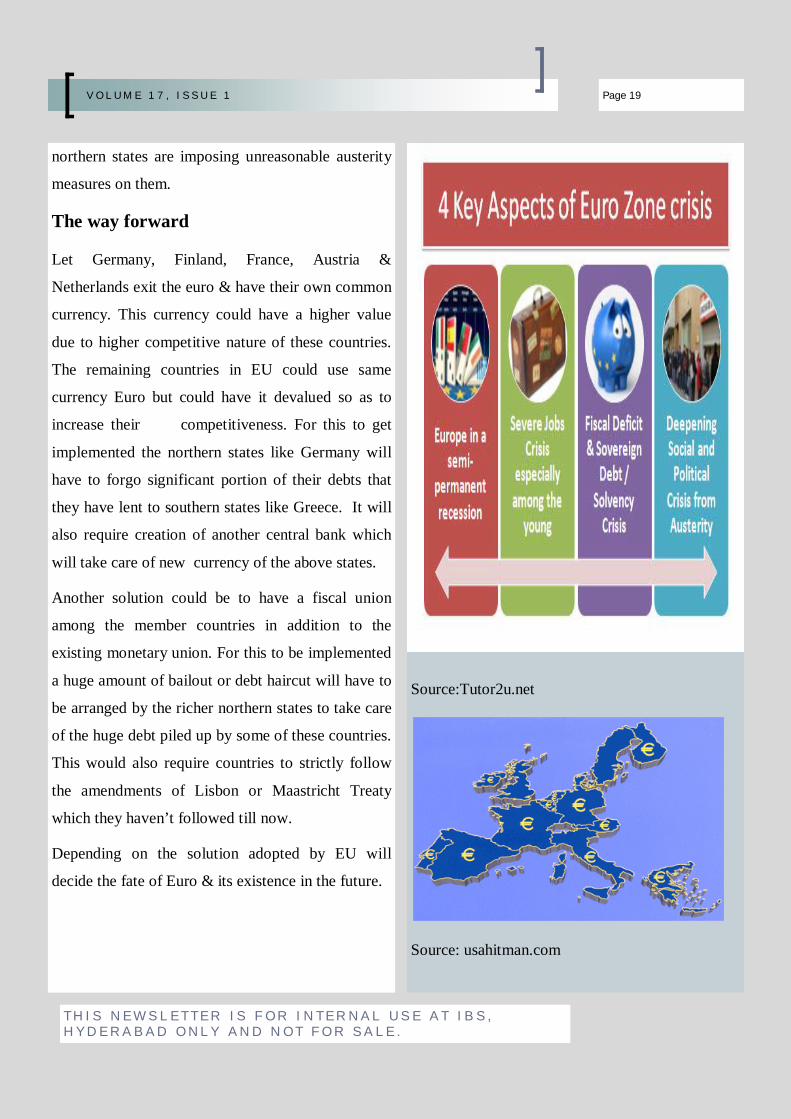

The way forward

Let Germany, Finland, France, Austria &

Netherlands exit the euro & have their own common

currency. This currency could have a higher value

due to higher competitive nature of these countries.

The remaining countries in EU could use same

currency Euro but could have it devalued so as to

increase their competitiveness. For this to get

implemented the northern states like Germany will

have to forgo significant portion of their debts that

they have lent to southern states like Greece. It will

also require creation of another central bank which

will take care of new currency of the above states.

Another solution could be to have a fiscal union

among the member countries in addition to the

existing monetary union. For this to be implemented

a huge amount of bailout or debt haircut will have to

be arranged by the richer northern states to take care

of the huge debt piled up by some of these countries.

This would also require countries to strictly follow

the amendments of Lisbon or Maastricht Treaty

which they haven’t followed till now.

Depending on the solution adopted by EU will

decide the fate of Euro & its existence in the future.

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 19 V O L U M E 1 7 , I S S U E 1

Source:Tutor2u.net

Source: usahitman.com

Abstract: High frequency trading has

marked its presence in developed

markets and has led to rapid

development in the field of computing

and networking. The concept and idea

behind HFT is here to stay but requires

regulation in order to avoid catastrophe

like the one on May 26th 2010. And its

entry into India has opened up career

opportunities for many and this article

intends to enlighten readers about what

high frequency trading is and how it has

changed the way trading is done these

days.

1. INTRODUCTION

Initially, traders used technical analysis

and analyze news in order to make their

trading decision. Then came a time

when people started quantifying the way

traders took decision and developed

programs which could take the same

decision that a trader took, only faster.

This marked the birth of algorithmic

trading. Then traders started realizing

that faster the decision making process

of their algorithm, better off they will

be. This lead to a race to reduce latency

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Certain

opportunities

exist in the

market only for

a few seconds;

though the

profit from

these trades is

very low, high

volume can yield

high returns.

Page 20 V O L U M E 1 7 , I S S U E 1

Aravind Ganesan IIM Indore

Rohit Maloo IIM Indore

in every way possible and a new kind

of traders emerged, the High frequency

traders.

High frequency trading refers to

transactions of large orders at a very

high speed. HFT trades in securities

like stocks or options, and uses

complex algorithms to analyze multiple

markets at a time and execute orders

based on market condition. To achieve

all this HFT requires effective

a lgo r it hms a nd so ph is t ic a t ed

technologies. High frequency trading is

categorized with very low holding

periods but the number of trades

executed in a given day is very high.

According to a financial research firm

TABB Group (2009), HFT accounts for

61 percent of all US equity trading

volume in 2009. Although we see some

trending decline after 2009, the

percentage in certain stocks are as high

as 80. [Source: valotrading.com]

Certain opportunities exist in the

market only for a few seconds; though

the profit from these trades is very low,

high volume can yield high returns.

High frequency traders compete on the basis of speed

with other high frequency traders and compete for

very small, consistent profits. As a result,

high-frequency trading has been shown to have a high

Sharpe ratio.

2. PARAMETERS FOR SUCCESS IN HIGH

FREQUENCY TRADING

2.1EFFECTIVE STRATEGIES

Low latency can give you an edge over others but with

lack of profitable trading strategies, speed will be of

little use. In order to stay ahead of competition a team

of highly skilled mathematicians and statisticians are

required to detect high frequency trading

opportunities. Development of a strategy is lengthy

process which takes close to 6 months. The process

starts with ideation; the idea is quantified and tested

under various conditions. And the biggest problem is

it’s easy to replicate a strategy followed by a

competitor using reverse engineering, so the shelf life

of a strategy is small. And certain strategies become

obsolete with time, so there is a need to keep

developing new strategies.

2.2 LOW LATENCY

Latency is the time delay experienced in the system.

Latency is experienced while receiving data from

exchange and while sending data to exchange. And

latency is also experienced while processing the data

to come up with an order decision. With high-

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 21 V O L U M E 1 7 , I S S U E 1

frequency trades executing in microseconds,

minimizing the delay between market data

analysis and trade submission increases the

effectiveness of trading algorithms. This

maximizes the probability that a trade generated

using that data can, and will, be executed.

3. ROLE OF TECHNOLOGY IN HIGH

FREQUENCY TRADING

3.1 The Trading Platform

An open source strategy-driven trading platform

provides enormous flexibility and control

without being beholden to proprietary vendor’s

release schedules and cost. Access to source code

enables usage, modification or enhancement to

meet business objectives and would help the firm

to get into the market more quickly because

there’s no waiting for vendors, and development

efforts need not start from scratch. Thus, trading

firms are able to spend more on intellectual

capital – the strategies and the algorithms that

will gain them competitive advantage –

instead of saddling themselves with large

capital investments in expensive and restrictive

infrastructure.

But ultra-low latency High frequency traders

have their own team of C++ coders who develop

highly efficient algorithms instead of using a

generic trading platform. But the cost of having a

team of highly efficient programmers is very high.

3.2 Co-location

An important ingredient for success in HFT is

Co-location, which is the act of placing the servers

in a facility such that the network latency is

reduced. Inside a co-location facility every server

gets the market information at the same time, so

there is no comparative advantage within a

co-location facility. Stock exchanges provide this

facility but the cost of co-locating the servers are

very high in a stock exchange, alternatively they

can be co-located in other service provider’s

facility.

3.3 Hardware

HFT computing requirement requires extreme

processing and memory performance while

offering server-class reliability, availability,

serviceability and manageability. Special attention

is given in choosing the type of server, rack or

blade server. Choosing the configuration for a

server is science with reducing latency being the

prime objective. Companies spend hundreds of

thousands of dollars on a single server which has a

shelf time of maximum of 6-8 months.

3.4 Raw data feeds

Several exchanges and ECNs provide raw data

feed containing real time trade related information.

This is in addition to the consolidated information

that each exchange sends, since it takes time to

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 22 V O L U M E 1 7 , I S S U E 1

consolidate information, High frequency traders use

raw data feeds from various exchanges to reduce the

latency introduced by consolidation. High frequency

traders also use news feed in machine

understandable format so that algorithms can exploit

trading opportunities revealed by latest happenings

in the world.

4.CONCLUSION

High frequency trading is a natural evolution from

conventional pit trading. The concept and idea

behind it is here to stay but requires regulation in

order to avoid catastrophe like the one on May 26th

2010. HFT has led to rapid development in super

computers and networking. HFT has marked its

presence in most developed countries and is slowly

entering into emerging markets as well. With apt

regulations in place, HFT is up for rapid adaptation

in India as well with many firms entering into it in

the last couple of years. And this opens up another

opportunity for finance freaks in the country, with a

fast paced and rewarding career.

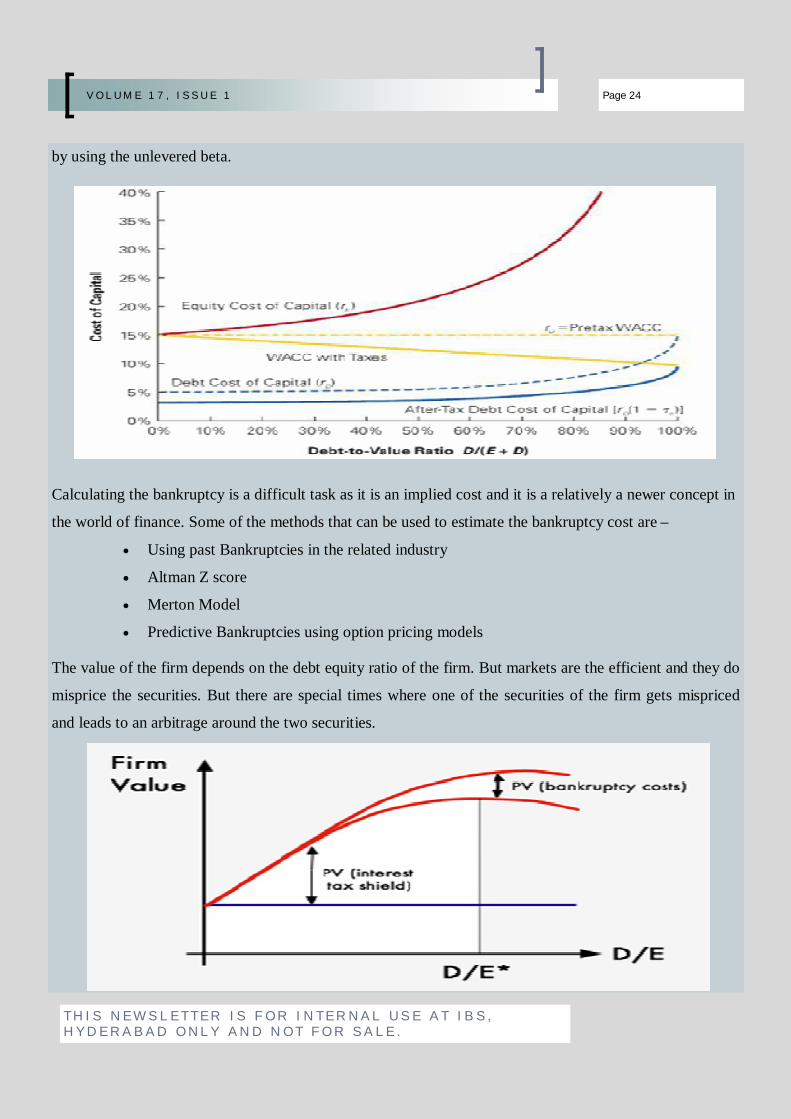

What is Capital Structure?

Capital Structure refers to the mix of

equity and debt that a firm uses to

finance operations of the firm. An ideal

capital structure can be used to optimize

the value of firm in a significant way.

The Miller-Modiginalni (M-M) model

on capital structure was one the first

theory to explain the use and benefits of

capital structure in maximizing the value

of the firm. Even though the M-M

model suffers from naïve and

impractical assumptions, it still forms

the basis of subsequent research and

thought process on capital structure.

When a firm borrows money as debt, it

adds significant amount of value to the

firm by way of tax shield. When the

firm raises debt, the form also incurs an

implicit bankruptcy cost. The optimal

debt equity ratio tries to maximize the

value of firm. Some of the more

practical approaches than the M-M

Model that could be used to arrive at the

optimal capital structure are:-

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Generally,

debt

instruments

with a rating

of BBB-/BB+

are the best to

execute the

capital

structure

Page 23 V O L U M E 1 7 , I S S U E 1

Madusudanan NMIMS

Harish NMIMS

Enhanced Cost of Capital

Approach –

The approach tries to generate a debt

equity ratio that would minimize the

cost of capital of the firm. As the firm

increases the financial leverage, the

levered beta of the firm would start to

increase. Hence higher leverage would

get reflected as higher cost of equity.

Higher leverage would also mean the

increase in risk for bond holders. This

would lead to increase yield of the

bonds and fall in credit rating of the

bond. The cost of capital at various

leverage points can be studied to find

the minimum cost of capital which

would maximize the value of firm.

A d j u s t e d P re s e n t V a lu e

Approach –

This approach tries to maximize the

value of the firm by factoring in the

implied bankruptcy cost and the gains

on account of tax shield to the value of

unlevered firm. The tax shield can be

calculated by the using the marginal tax

rate of the firm. The value of unlevered

firm is obtained by discounting the cash

flows by the cost of equity calculated

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 24 V O L U M E 1 7 , I S S U E 1

by using the unlevered beta.

Calculating the bankruptcy is a difficult task as it is an implied cost and it is a relatively a newer concept in

the world of finance. Some of the methods that can be used to estimate the bankruptcy cost are –

Using past Bankruptcies in the related industry

Altman Z score

Merton Model

Predictive Bankruptcies using option pricing models

The value of the firm depends on the debt equity ratio of the firm. But markets are the efficient and they do

misprice the securities. But there are special times where one of the securities of the firm gets mispriced

and leads to an arbitrage around the two securities.

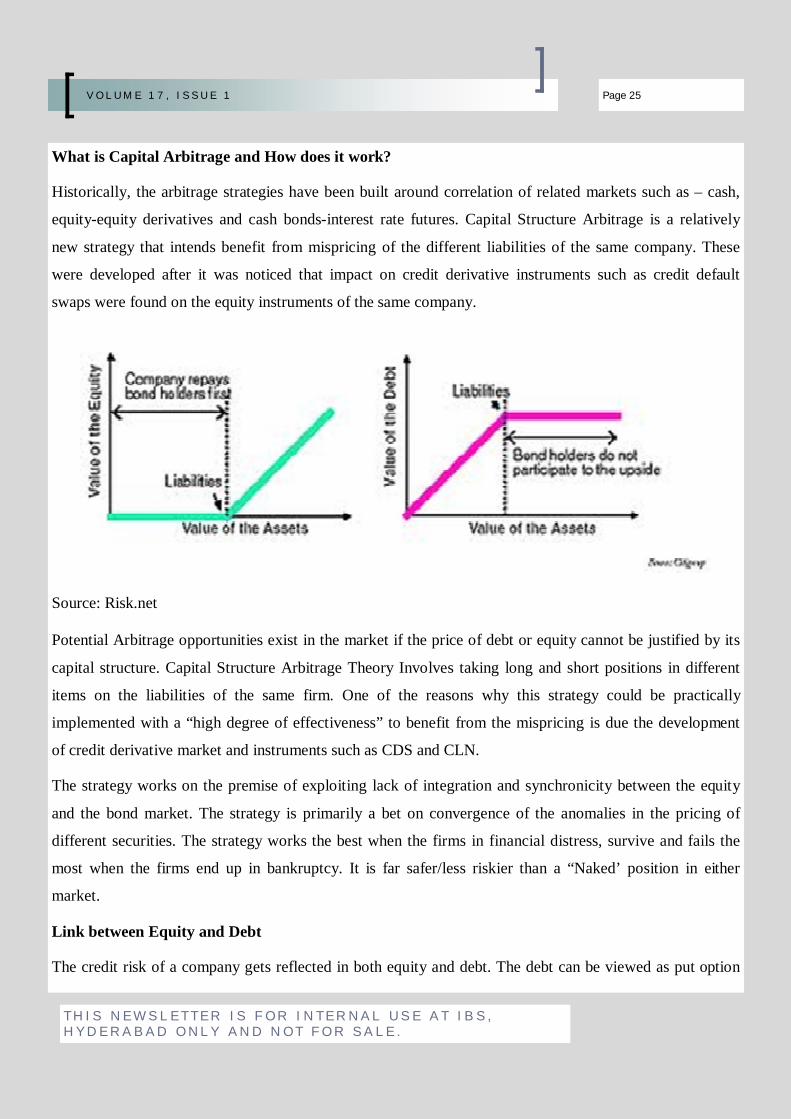

What is Capital Arbitrage and How does it work?

Historically, the arbitrage strategies have been built around correlation of related markets such as – cash,

equity-equity derivatives and cash bonds-interest rate futures. Capital Structure Arbitrage is a relatively

new strategy that intends benefit from mispricing of the different liabilities of the same company. These

were developed after it was noticed that impact on credit derivative instruments such as credit default

swaps were found on the equity instruments of the same company.

Source: Risk.net

Potential Arbitrage opportunities exist in the market if the price of debt or equity cannot be justified by its

capital structure. Capital Structure Arbitrage Theory Involves taking long and short positions in different

items on the liabilities of the same firm. One of the reasons why this strategy could be practically

implemented with a “high degree of effectiveness” to benefit from the mispricing is due the development

of credit derivative market and instruments such as CDS and CLN.

The strategy works on the premise of exploiting lack of integration and synchronicity between the equity

and the bond market. The strategy is primarily a bet on convergence of the anomalies in the pricing of

different securities. The strategy works the best when the firms in financial distress, survive and fails the

most when the firms end up in bankruptcy. It is far safer/less riskier than a “Naked’ position in either

market.

Link between Equity and Debt

The credit risk of a company gets reflected in both equity and debt. The debt can be viewed as put option

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 25 V O L U M E 1 7 , I S S U E 1

and equity as a call option. Hence, debt is less

sensitive to company fundamentals than equity,

especially when the fundamentals improve. Higher

the leverage, the credit spread of the company

increases, this increases the higher the correlation

between equity and debt. Generally, debt

instruments with a rating of BBB-/BB+ are the

best to execute the capital structure arbitrage

strategies, as this is where the correlation between

equity and debt is the highest. This reason why

effectiveness of debt instruments with a rating of

BBB-/BB+ improves is because these debt

instruments are quite volatile and start behaving

like equity to various developments of the firm.

A typical Capital Structure Arbitrage

A investor believes either the debt or equity

is underpriced

He purchases a put option on the equity

and CDS on a cheap bond (with a high

YTM)

He has build a kind of hedge by buying

both these securities

In case of a default by the firm, he receives the

money from the put writer and the compensation

from the CDS issuer. In case of recovery/non

default, the investor benefits from the improve-

ment in credit position of the firm by holding CDS

and losses the premium paid for put option.

Some of option a player has are–

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 26 V O L U M E 1 7 , I S S U E 1

Some of the traditional ways/strategies of benefitting

from the capital structure arbitrage are -

Set-up trades between the debt and equity of

a company

Play between senior debt and junior

securities

Convertible Bond Arbitrage by purchasing

convertible bond and shorting the shares in

the delta hedge ratio

Some of the newer strategies are

Equity Options

Credit Derivatives

Using both Equity options and credit

derivatives

Capital Structure Arbitrage can be implemented

using Equity Derivatives. Deterioration in a

company’s credit worthiness is often an indicative

future decline in the firm’s equity stock price.

Theoretically, the derivative market should take

cognizance of this movement in the credit derivative

market. In Real time, the equity markets either over

react or under react to these shocks in the credit

derivative markets. In those times, the strategy to be

used are companies whose equity prices have over

reacted, a call should be brought and companies

whose equity prices have under reacted, a put should

be brought .

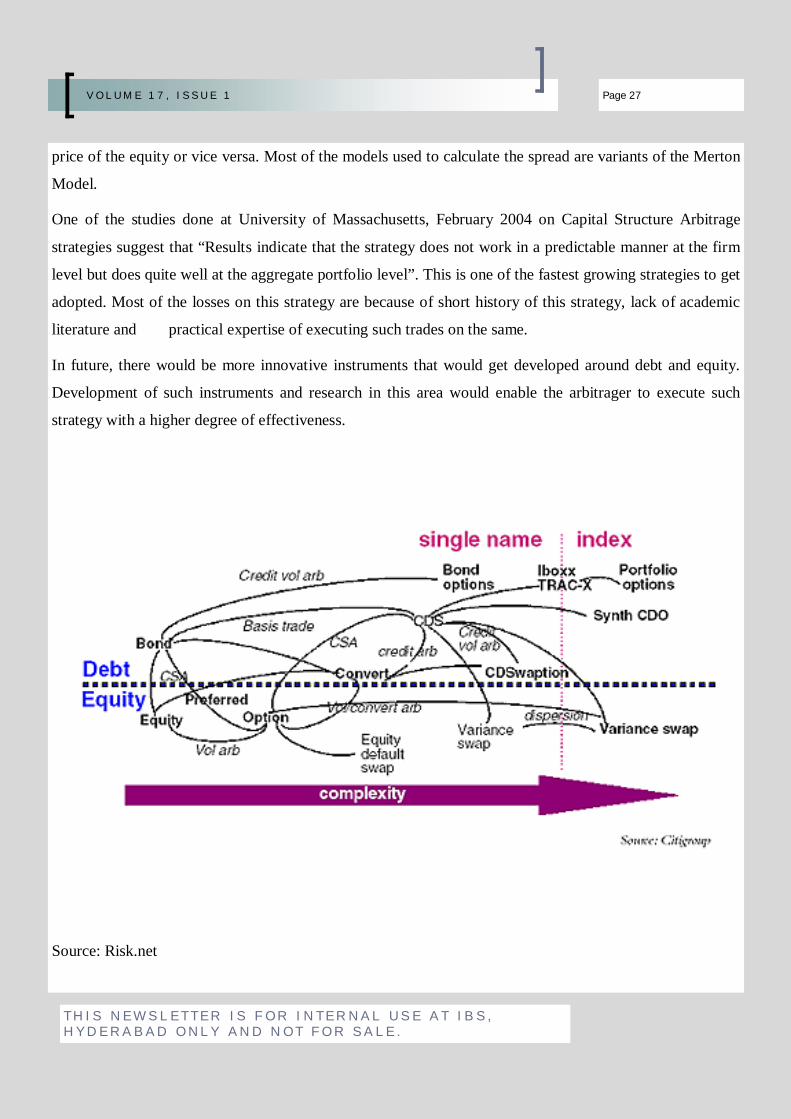

Most of the capital structure arbitrager uses a model

to gauge the value left in a CDS after considering the

price of the equity or vice versa. Most of the models used to calculate the spread are variants of the Merton

Model.

One of the studies done at University of Massachusetts, February 2004 on Capital Structure Arbitrage

strategies suggest that “Results indicate that the strategy does not work in a predictable manner at the firm

level but does quite well at the aggregate portfolio level”. This is one of the fastest growing strategies to get

adopted. Most of the losses on this strategy are because of short history of this strategy, lack of academic

literature and practical expertise of executing such trades on the same.

In future, there would be more innovative instruments that would get developed around debt and equity.

Development of such instruments and research in this area would enable the arbitrager to execute such

strategy with a higher degree of effectiveness.

Source: Risk.net

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 27 V O L U M E 1 7 , I S S U E 1

On September 14, 2012, Indian

government opened its skies for

Foreign Direct Investment (FDI) in

the Aviation sector. Among other

policy initiatives, the measure was

announced by the government as it

went into overdrive mode as far as

reforms are considered. While FDI

was already allowed in the sector, the

current regulation was directed at the

foreign airlines who are interested in

buying stakes in the Indian Airlines, a

measure which was previously

p r o h i b i t e d . T h o u g h t h e

announcement came late in the day,

the listed companies in the aviation

sector had already factored in the

reform in their stock prices as they

saw a significant increase in

anticipation of the reform. The

reforms look good, especially when

players in the industry are deep in the

red and there are hardly any players

that have posted profits in the near

past. They would help these

beleaguered firms to raise capital by

selling equity to foreign airlines. But

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

ATF forms

close to 40%

of the

operating

costs of the

carriers and

is thus

hurting them

the most.

Page 28 V O L U M E 1 7 , I S S U E 1

Varun Sanghi MDI GURGAON

is this the complete story that is

hurting the Indian aviation sector? It

remains to be seen as the companies

battle countless issues, both in the

short term and the long term.

While the government in its capacity

has allowed the entry of FDI into the

sector, there is still a lot more that

needs to be done to uplift the

sentiment. To have a better view,

let’s look at some of the problems

that the industry is battling with.

While no one can deny the immense

potential growth in the sector, a

close look suggests a mismatch

between capacity addition and

growth in the sector.

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 29 V O L U M E 1 7 , I S S U E 1

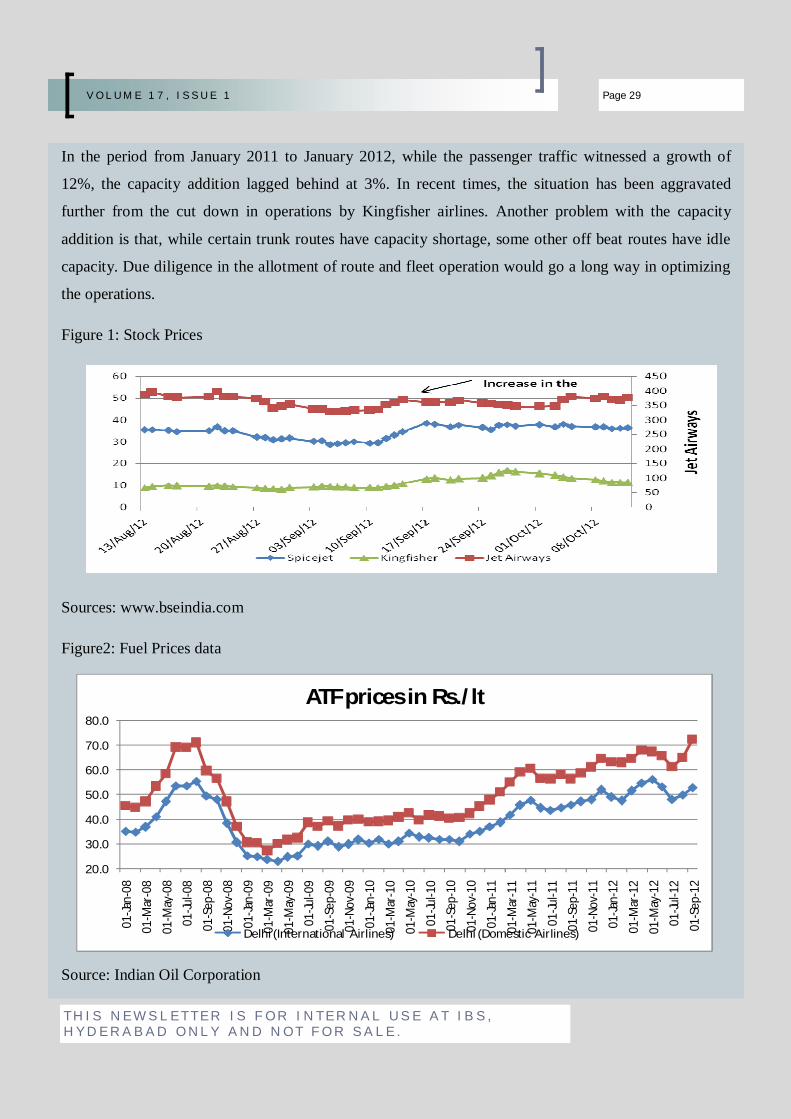

In the period from January 2011 to January 2012, while the passenger traffic witnessed a growth of

12%, the capacity addition lagged behind at 3%. In recent times, the situation has been aggravated

further from the cut down in operations by Kingfisher airlines. Another problem with the capacity

addition is that, while certain trunk routes have capacity shortage, some other off beat routes have idle

capacity. Due diligence in the allotment of route and fleet operation would go a long way in optimizing

the operations.

Figure 1: Stock Prices

Sources: www.bseindia.com

Figure2: Fuel Prices data

Source: Indian Oil Corporation

20.0

30.0

40.0

50.0

60.0

70.0

80.0

01-Ja

n-08

01-M

ar-0

8

01-M

ay-0

801

-Jul-0

8

01-S

ep-0

801

-Nov

-08

01-Ja

n-09

01-M

ar-0

9

01-M

ay-0

901

-Jul-0

9

01-S

ep-0

901

-Nov

-09

01-Ja

n-10

01-M

ar-1

001

-May

-10

01-Ju

l-10

01-S

ep-1

0

01-N

ov-1

001

-Jan-

11

01-M

ar-1

101

-May

-11

01-Ju

l-11

01-S

ep-1

1

01-N

ov-1

101

-Jan-

12

01-M

ar-1

2

01-M

ay-1

201

-Jul-1

2

01-S

ep-1

2ATF prices in Rs./lt

Delhi (International Airlines) Delhi (Domestic Airlines)

Capacity addition is something that takes time to

build up and is fixed in nature, but the operating

aspect that is hurting the industry the most, is the

high Aviation Turbine Fuel (ATF) charges. ATF

forms close to 40% of the operating costs of the

carriers and is thus hurting them the most.

The above data highlights the issue of domestic

carriers at loss as they are being charged the highest

for ATF. The Indian ATF prices are generally

among the highest in the world, making operation of

aircrafts all the more costly. The taxes and duties

further imposed by state governments compound the

problem. The price of ATF for International airlines

is cheaper as the fuel supplied is deemed export and

thus escape the myriad of taxes imposed on fuel for

domestic consumption. Though the Indian

government has given a go ahead to the airlines for

direct fuel import, the issues related to the handling

and storage of fuel have done little good as the

airlines will have to rely on the existing oil

companies. A reduction in duties will certainly

provide some breathing space to the players.

High airport fees is another area where the Indian

players are at the receiving end as they pay some of

the highest airport fees in the world. The recent

steep increase in airport fees at Delhi and the one

proposed in Mumbai will exacerbate the problem.

Their exists intense competition in the industry and

the pricing strategies of the players reflects this. The

state owned Air India has off late been dropping its

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 30 V O L U M E 1 7 , I S S U E 1

fares considerably and as a result the other

players are following the suite, as they are

left with few choices. This has not only

inflated the debt of Air India, but also had a

profound effect on the other players as the

industry is witnessing a deadly combination

of high costs and price based competition

which can be lethal in the long term.

Coupled with these issues, the companies are

facing acute shortage of funds and are not

even able to meet their daily operational

expenses. Most of them have already

exhausted their credit limits and banks are

now wary of extending more credit. So on

paper, most of the players are not even worth

Re. 1 as mentioned in a newspaper headline.

According to a report the entire sector has

loans worth Rs. 1,10,000crores, but the net

worth of the sector is just 25 percent of the

total loans and thus the sector is worth

nothing when looked purely from the

accounting perspective.

While problems are plenty for the sector, the

FDI regulation will certainly provide some

relief to the cash crunch players in the

industry. The immense growth potential that

the sector offers is one of the many attractive

facts that would bring in foreign investments.

Another major advantage for the Indian

players is the operational expertise that the

foreign players bring along with them. This will certainly help in optimizing the operations of the

national players. Also FDI will give a boost to the Maintenance Repair and Overhaul (MRO) industry

that serves as the backbone for the industry. The Indian players must now justify their positions so as to

seem attractive for foreign airlines to infuse capital in them. For the Foreign Airline, this is a valuable

opportunity to enter one of the fastest growing aviation markets globally and gain a substantial share in

the market that is still developing. It thus becomes clear that FDI alone would not be able to rescue the

Indian aviation sector as it faces a humongous task ahead. It has to be coupled with many other allied

reforms in the sector to make the sector come out of the red.

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 31 V O L U M E 1 7 , I S S U E 1

Money Laundering is a matter of grave concern as of late. Money laundering is the process of concealing the source of money obtained by illicit means. In simple words, Money laundering is the process of making illegally-gained proceeds appear legal.

The concept of “Money Laundering” is quite old, though the impact is felt recently. After the attacks on World Trade Centre on 11th September, 2009, countries have become much cautious in combating terrorism. But to combat terrorism, we must know how does it originate and how are the terrorists funded. The answer is quite simple, terrorist activities are funded through money laundering techniques and hence they go unnoticed.

Recently in India, attacks on the Taj Hotel in Mumbai have also raised serious concerns in this regard. Money Launderers do their job so swiftly and smoothly, which make them a bit d ifficult to be caught . Money Laundering is usually resorted to fund illegal activities like Drug Trafficking, Smuggling, funding terrorist activities, Trafficking of Human Beings.

Ways of Money Laundering

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Three stages in Money Laundering- viz Placement, Layering and Integration.

Page 32 V O L U M E 1 7 , I S S U E 1

Sibojyoti Chakrabarti ITM ,Navi Mumbai

Usually there are three stages in Money Laundering- viz Placement, Layering and Integration.

In placement, usually illegal funds are brought into the financial system. Funds obtained by illegal means are introduced into an economy.

In Layering, various types of accounts with banks in different names, are o p e n e d , m u l t i p l e t y p e s o f intermediaries, trusts and countries are used by the launderers to disguise the origin of funds. Here the main motive is to conceal the origin of illegally obtained funds in bulk, through various methods.

Finally in Integration, laundered funds are apparently made to appear as legitimate funds, by utilising various financial institutional channels like banks.

Measures to Fight This Menance- A Reference to KYC.

To fight this menace, stringent measures have been introduced by the Concerned Regulatory Authorities of various states. At first banks which are an easy source to channelize funds from criminal activities, have been cautioned in this regard. The concept of KYC has been made mandatory, for all banks and financial institutions to follow.

KYC is being promoted by an international organization called “Financial Action Task Force”, since 1989. Under KYC, all financial transactions will be monitored and identified by a bank. In India, RBI has instructed all banks to follow the KYC norms in terms of PML Act, 2002(w.e.f December, 31st, 2005) .

The main objective of KYC Norms are:

To prevent banks from being used intentionally or unintentionally, by criminal elements from money laundering activities.

Enable banks to understand customers and manage their risk prudently.

Avoid opening of accounts with fictitious name and address.

Minimize frauds and protect banks reputation.

How to Prevent Money Laundering?

In India legislations have been implemented to foresee money laundering activities. The Prevention of money Laundering Act, 2002 has been enacted to prevent money laundering and provide for

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 33 V O L U M E 1 7 , I S S U E 1

confiscation of property derived from money laundering. Under the provisions of the above mentioned Act, The Enforcement Directorate is empowered to investigate and prosecute offences relating to money laundering.

“Prevention is better than Cure”.

In its working the Enforcement Directorate is assisted by the Financial Intelligence Unit for proper functioning under the Act.

Further as per the stipulations of the RBI Guidelines all banks are required to report any suspicious transactions to the RBI. Suspicious transactions include the following :-

All cash transactions of the value of Rs.10 Lakhs and above.

Series of transactions which takes place within a month of the aggregate value of which exceeds Rs.10 Lakhs

All cash transactions where any forgery of valuable security taken place

All foreign inward remittances received by NGO’s of the value of Rs.10 Lakh or above in a month.

Apart from this all cash transactions of Rs.50,000 and above compulsorily requires quoting of PAN number.

Recent Cases In Money Laundering-

1. The Enforcement Directorate has registered a case against Satyam Computer and its tainted founder chairman B Ramalinga Raju for his involvement in alleged money laundering .

2. The Serious and Organized Crime Agency (Soca) believes that Naresh Kumar Jain is responsible for laundering millions of pounds of profits from organised crime gangs in the UK over several years. Mr Jain is suspected of laundering money for Albanian and Italian heroin dealers, and narcotics cartels in America, the United Arab Emirates, Pakistan and Britain, according to inquiries in Italy and the US. German and US police say Jain's operation has tentacles in all of the major drug and terrorism hotspots across the globe. He was also wanted by police in Spain and the Netherlands. Jain was bailed in Dubai – where he faces trial for breaking foreign exchange laws – and fled his business headquarters. He resurfaced in his native India, where authorities raided several properties owned by him and issued an all ports alert.

3. The family of NRI businessman Raj Bhojwani, facing trial in tax haven island of Jersey on the charges of money laundering in a truck sale deal to Nigeria, has alleged "racial discrimination" and is all set to move the UN Human Rights Commission and British Institute of Human Rights. Bhojwani's counsel Hitesh Jain, in a letter to prime minister Manmohan Singh, a copy of which is with PTI, has alleged International News that Jersey is interested in making a case against the businessman, confiscate his assets and share

T H I S N E W S L E T T E R I S F O R I N T E R N A L U S E A T I B S , H Y D E R A B A D O N L Y A N D N O T F O R S A L E .

Page 34 V O L U M E 1 7 , I S S U E 1

them with Nigeria.

4. On 12th Aug, 2012 Income tax dept. has decided to prosecute individuals named in the classified HSBC list for stashing illegal funds In its probe the department has found illegal funds were laundered, being categorized as criminal proceeds of crime. The IT department will carryout its prosecution in coordination with the enforcement directorate( i.e designated enforcement agency under PML Act, 2002) (Source: Financial Express).

Position in Other Countries-

In other Countries too, legislations have been en-acted and specialized agencies have been formed to curb the menace of Money Laundering. For instance in the United States Bank Secrecy Act, 1970 & Money Laundering Control Act, 1986 have been enacted and Financial Crimes Enforcement Network acts as the designated administrator of the Bank Secrecy Act.

Finally I feel it is the Financial Institutions and the financial intermediaries who are being utilized for money laundering purposes, hence the government of every country should strive to keep a strict vigilance on the working of these institutions so that a world wide disease like Money Laundering can be prevented in every step, before it proceeds further.