finance 541 cases in managerial finance. today’s class... introductions and house keeping current...

TRANSCRIPT

FINANCE 541

Cases in Managerial Finance

Today’s class...

• Introductions and house keeping

• Current Events

• Financial planning and analysis

• Seminal ideas in corporate finance

My Background

• NAME: Ken Shah• BORN: Bombay, India• PhD: University of Oregon• INDUSTRY EXPERIENCE:

– 4 yrs Floor Trader / Stock Broker - Bombay Stock Exchange

– 3 yrs Quantitaive Portfolio Management Research, Portland, Oregon

Academic Experience

• Taught at– University of Oregon– University of Auckland– Southern Methodist University

• Courses in capital budgeting, corporate finance, investments, and money and banking

Recent Research• Capital Structure

– How do investors react to capital structure changes?• The nature of information conveyed by capital structure

changes, Journal of Financial Economics, 1994

• Initial Public Offerings– Investigate/explain perfomance over the long haul

after going public• The performance of firms that go public, Journal of

Financial Economics, 1996

Please Introduce yourself...

• Please fill out the student information sheet

• Drop by my office!

• Name cards

Course Objectives• Expose you to anticipated managerial decisions in

finance

• Inculcate financial way of thinking

• Bridge theory and practice

• Increase proportion of good financial decisions to bad ones!!

Course Prerequisites

• Willingness to learn & work hard!• Understanding of:

– Financial statements– Rudimentary statistics– Spreadsheets– Fundamentals corporate finance

• Valuation, M&M propositions, agency theory

• Pre-requisite: FINC 515

Anticipate...

• About 6 - 8 hours of work outside of class

• Frustrations with unstructured problem solving!

• Frustrations with computer work!

Texts

• Required: – Bruner, Case Studies in Finance– Packet of Readings

• Optional: – Brealey & Myers, Principles of Corporate Finance– Higgins, Analysis for Financial Management

Evaluation

• Group Case Presentation 250• Participation 250• Midterm Case 250• Final Case 250

• TOTAL 1000

Participation Grade• Peer Evaluation

• At the end of quarter, you will give one point each to roughly 1/3 of the class who contributed, in your opinion, to the discussion in a positive way

Grading Policy• If you attend all classes and diligently complete

all required work, you would be assured of a B- grade

• In order to get an A/A-, you must show work of superior quality and make a meaningful contribution to the class discussions– roughly top 15% of the class

Class Attendance• Mandatory

– Particularly important in a case class

• Please inform me of anticipated absences– More than 1 absence will adversely affect your grade

Case Presentations

• In groups• About 30 minutes in length• Formal write up• Field questions

Non-presenting groups

• Demonstrate preparedness

• Come to class with solution to the selected case question (in bold in the handout)

• One group will be randomly selected to turn in the solution

Midterm & Final

• Formal 3 page case evaluation

• Take home

• One week to complete

• Individual effort

Readings

• Required: – Please be prepared to discuss them in class

• Background:– To expose you to practice, analysis, and theory in

the case subjects– Necessary but not explicitly discussed

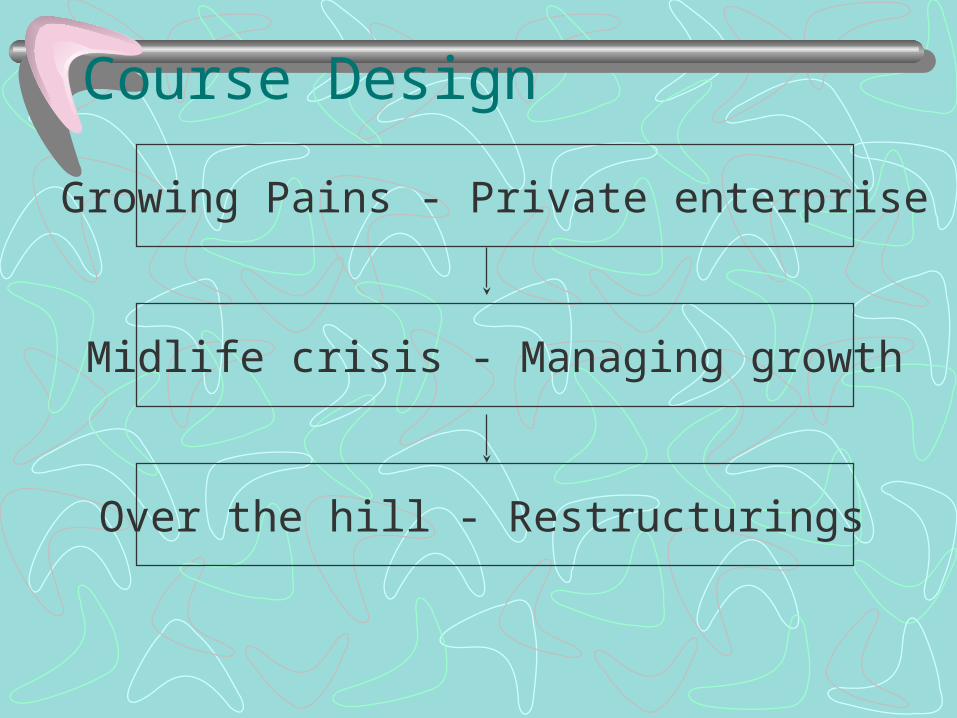

Course Design

Growing Pains - Private enterprise

Midlife crisis - Managing growth

Over the hill - Restructurings

Case Progression• Managing Growth / Private enterprise:

– Short term financing / Managing growth– Going public– WACC

• Sustaining Growth / Financing Policy:– Corporate disbursement policy– Capital structure polic

• Lower Growth / Corporate Reorganizations:– Takeovers– LBOs– Bankruptcy

Cases...

• Are deliberately vague!

• Have information deliberately presented in random order - not in the order of importance

• Offer little guidance on method of solution

My approach to a case...

• Read it twice, ignore numbers• List all issues• Rank issues in order of importance• Articulate the central issue• Identify relevant theory and evidence• Formulate assumptions for analysis• Perform data analysis• Recommend a course of action

Repeat

Analyzing a case...• At first, see the forest, not the trees

• Analyzing numbers is necessary but NOT an end in itself– it is presumed that you know how to analyze

numbers

• Put yourself in the shoes of the decision maker

Analyzing a case...• Identify the decision makers and their pressures and

stakes in the situation• Thoroughly understand the nature of the business,

product, firm’s competence, competitors, structure of the industry etc.

• What are firms goals? How well has it pursued them?– DuPont, ratio analysis, growth rates, measures of value

creation

Analyzing a case...• Is the problem at hand a symptom of a larger

problem?

• E.g. a lender is often asked to provide cash to tide over shortfall.

• Study may reveal that it’s really the product obsolescence, unexpected competition etc.

Analyzing a case...• An executive rarely thinks of a problem as an

exercise in forecasting techniques or discounting method.

• But rather, thinks of it as a problem of judgement, deciding on which people, concepts or environmental conditions to bet.

• Get the #’s right - but go further!!• Prepare to take a stand - and defend it!

Case Write-up• Do NOT simply regurgitate the information in the

case in your introduction to the case

• Distill and analyze the information and present it only if you believe it has an impact on your analysis and solution

Learning from case method

• It’s not passive - the more you participate and think, the more you learn

• It’s cumulative - should not measure the success of your progress on the basis of any single case discussion– You will arrive at a better understanding over time,

after many cases - sometimes after the course is over!

Financial Planning

• Analyze financing and investment decisions

• Project future consequences of present decisions

• Decide on which alternative to undertake

• Measure subsequent performance against goals

Elements of Financial Planning

• Forecasting– Pro-forma statements

• Finding the optimal financial plan

• Watching the plan unfold

Analyzing performance

• Financial ratios

• Beware of accounting definitions

• Choosing a benchmark– trend over time– industry counterparts (Dept. of Commerce, Dun &

Bradstreet, Robert Morris Assoc.)

Analytical Tools

• Sensitivity (what-if) analysis

• Scenario analysis

• Monte Carlo simulation

• Decision Trees

Sensitivity Analysis

• Analyze the impact of changing a single variable one at a time– e.g. Formulate “Optimistic”, “Pessimistic”, “Expected”

cases• Identifies key variables• Ignores interrelations among variables

Scenario Analysis

• Consider alternative plausible combinations of variables

• Account for interrelations among variables– e.g. rise in oil prices -> increase scooter sales AND

increase costs• Overcomes limitations of sensitivity analysis

Monte Carlo Simulations

• Model the strategy• Identify key variables• Draw from probability distributions of key

variables• Calculate results of strategy• Do that many, many times (computer)• Get distribution of outcomes• Range of answers - difficult to reconcile

Decision Trees

• Used for sequential decisions• Evaluate decisions at each node starting

backwards (reverse iteration)• Compute expected value

• Trees can quickly become complex• Incorrect handling of risk (discount rate)

Is theory a dirty word?

• Theory is simply an exercise in ridding distractions

• It can aid to clarify thinking • However, theory for its own sake serves no

useful purpose in this class• Theory does provide a framework to start the

analysis

Bridging Finance Theory and Managerial Finance...• CAPM

– NPV, capital budgeting, WACC• Modigliani-Miller Propositions

– Dividends, capital structure, WACC• Agency Theory

– Corporate governance, compensation• Option Pricing

– Risk management, real options in capital budgeting• Asymmetric Information Models

CAPM

• Widely used in NPV, capital budgeting• Efficient Portfolios, CML, SML• Recently under attack (is beta dead?)

• Rivals: APT, Empirical Multifactor Models

M-M Propositions

• Proposition I: Firm cannot change its total value by splitting cash flow into different streams (ie shareholders, debtholders)

• Proposition II: Expected return on common stock increases in proportion to its market debt to equity ratio

M-M & Corporate Taxes

• Firm Value = value if all equity financed+ PV(tax shield)

• Tax shields increase with the proportion of debt in the capital structure

• All debt firm? absurd

M-M: Add personal taxes

• Tax gain at corporate level offset by tax at personal level

• Post-TRA 1995 tax rates favor debt

• Irrelevance again if :(1-Tp) = (1-Tg) * (1-Tc)

Bankruptcy Costs

• Higher levels of debt involve– Direct bankruptcy costs– Indirect bankruptcy costs

• These serve to offset the tax advantage of debt

• Bankruptcy and liquidation are separate issues!!

Bankruptcy Costs

• Direct costs estimates

• 3% of book assets

• 20% of market equity

• Quite substantial!

Agency Costs

• Conflicts are inherent between– Share holder - Management– Share holder - Bond holder

• Firm value is reduced by– Excessive perk consumption– Taking unwarranted risk– Forgoing profitable investments with debt

Agency Cost Models

• Used successfully in explaining

– LBOs, Takeover, restructuring activity– Debt covenants– Design of board of directors– Design of incentive compensation

Asymmetric Information Models

• Presupposes management have superior information about own firm value

• Changes in dividends, capital structure convey information to investors about firm value

• Do managers deliberately signal?

Optimal Capital Structure

• Maximizing firm value involves balancing

– Tax benefits of debt– Bankruptcy costs– Agency costs of debt– Agency costs of equity– Information signalling costs

Option Pricing Models• The most successful pricing models in finance

• Used to value complex securities– convertibles, callables, warrants

• Adjustments to NPV in sequential decisions– Real options in capital budgeting

• Value incentive compensation– ESOPs

Option Pricing Models

• Binomial– When outcomes at each node are limited in number

• Black - Scholes (& variants)– For continuous range of outcomes such as market

prices

Working Capital Issues

• How much cash should a company hold?

• What collections and payment policies should a company follow?

• What is the optimal level of inventory?

Working capital Mgmt• Common sense rather than theory guides the

issue

• Trial and error!!

• There is some effort to apply economic principles to account receivables management and trade credit(see readings)

Short term Fin’l Planning

• Requires forecast of cash requirements• Method of raising required cash; consider

explicit and implicit costs• Monitoring cash inflows and outflows, debt

covenants• Taking corrective steps as necessary

ST vs. LT sources of funds

• Again, no clear theory to guide us

• Attempt is usually made to match duration of assets and liabilities similar to banks

• Firms can be conservative (using LT sources) or aggressive (using ST sources)