final solution sketches note for multiple-choice questions: choose the closest answer

TRANSCRIPT

Final solution sketches

Note for multiple-choice questions: Choose the closest

answer

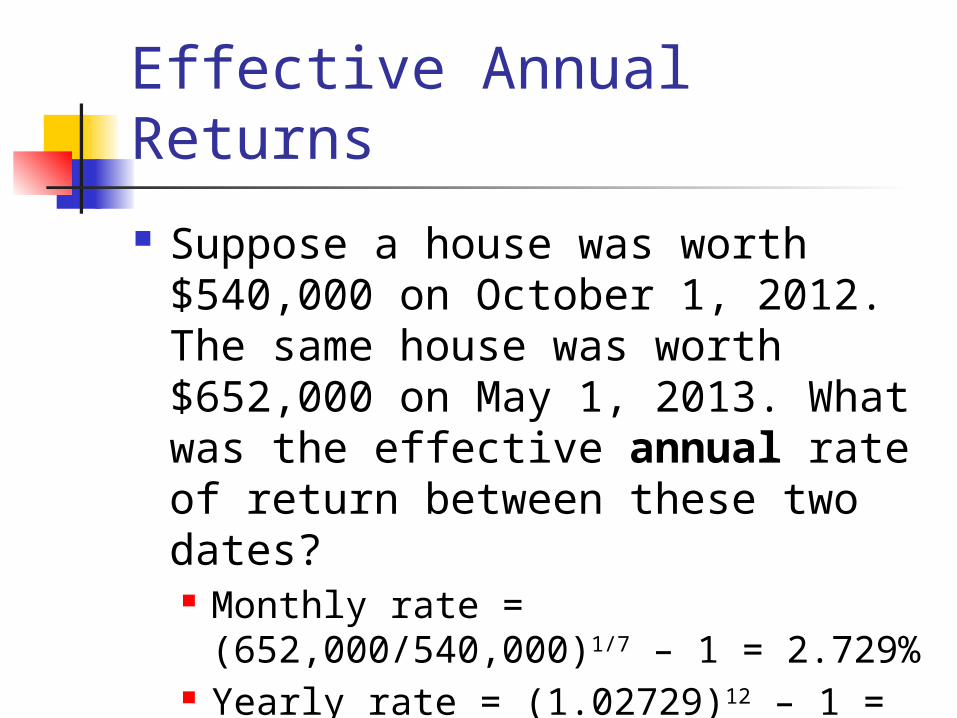

Effective Annual Returns

Suppose a house was worth $540,000 on October 1, 2012. The same house was worth $652,000 on May 1, 2013. What was the effective annual rate of return between these two dates? Monthly rate = (652,000/540,000)1/7 –

1 = 2.729% Yearly rate = (1.02729)12 – 1 =

38.1404%

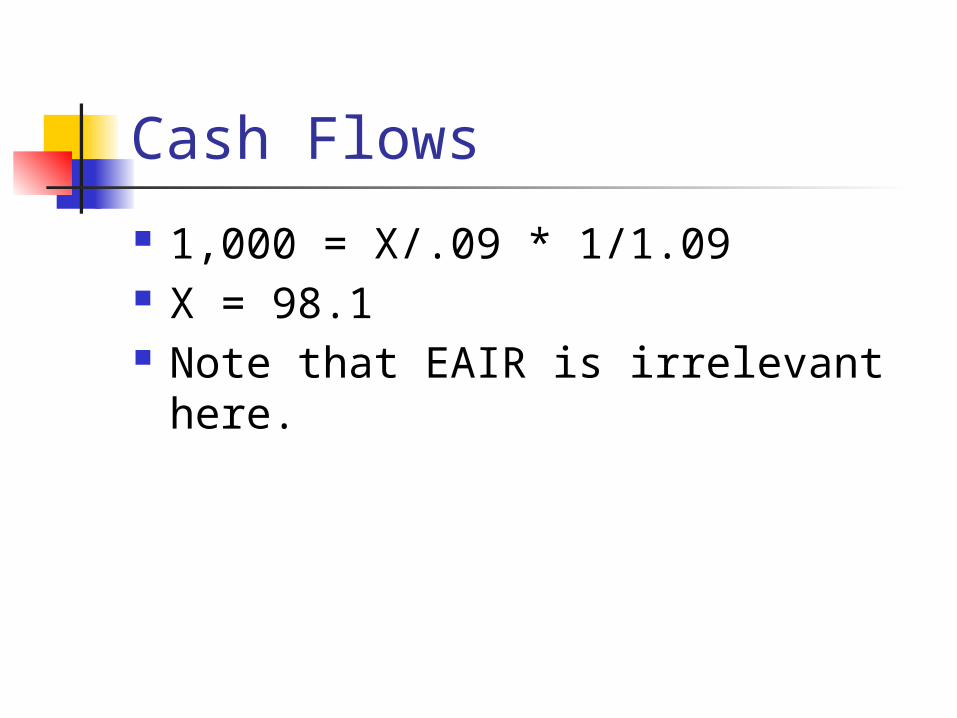

Cash Flows

Dave is investing in a stuffed bug toy company. He knows the following: if he invests $1,000 today, he will receive $X every year, forever, starting two years from now. His effective annual discount rate is 12%. The IRR for this project is 9%. Find X.

Cash Flows

1,000 = X/.09 * 1/1.09 X = 98.1 Note that EAIR is irrelevant here.

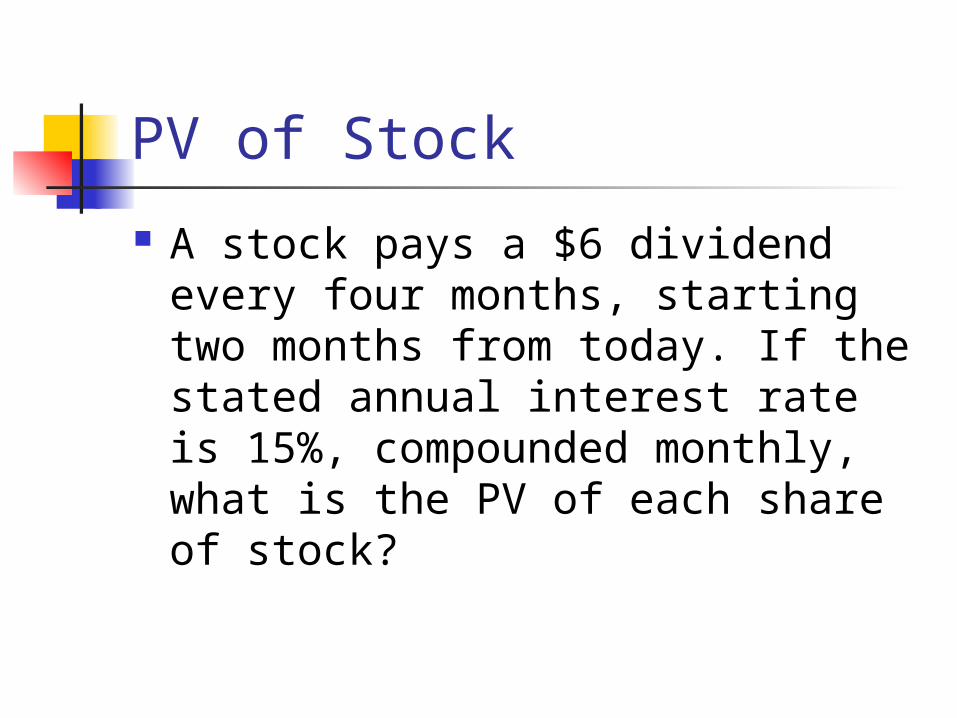

PV of Stock

A stock pays a $6 dividend every four months, starting two months from today. If the stated annual interest rate is 15%, compounded monthly, what is the PV of each share of stock?

PV of Stock Rate every 4 months = (1.0125)4 – 1

= 5.0945% Rate every 2 months = (1.0125)2 – 1

= 2.5156% PV = 6/.050945 * 1.025156 =

$120.74

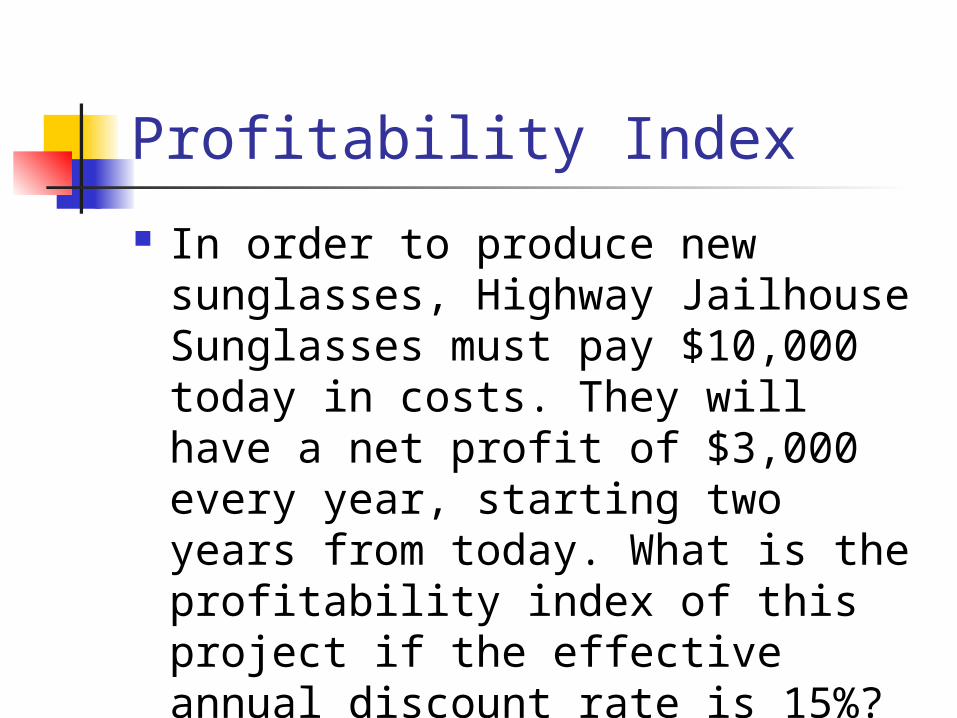

Profitability Index

In order to produce new sunglasses, Highway Jailhouse Sunglasses must pay $10,000 today in costs. They will have a net profit of $3,000 every year, starting two years from today. What is the profitability index of this project if the effective annual discount rate is 15%?

Profitability Index

PVbenefits = 3000/.15 * 1/1.15 = $17,391.30

PI = 17,391.30 / 10,000 = 1.73913

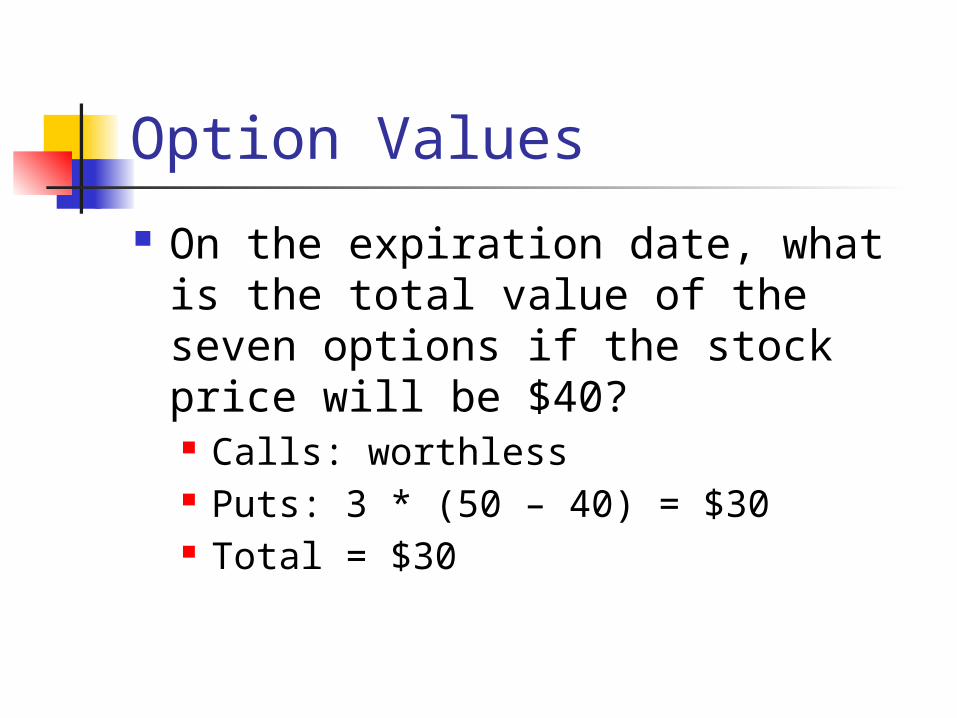

Option Values

For the next 3 questions: Angela has purchased three put options with an exercise price of $50, and four call options with an exercise price of $45. All options can be exercised for one share of stock, and the expiration date for all options will be one month from today. The stated annual interest rate is 12%, compounded monthly.

Option Values

On the expiration date, what is the total value of the seven options if the stock price will be $40? Calls: worthless Puts: 3 * (50 – 40) = $30 Total = $30

Option Values

On the expiration date, what is the total value of the seven options if the stock price will be $48? Calls: 4 * (48 – 45) = $12 Puts: 3 * (50 – 48) = $6 Total = $18

Option Values Angela predicts that the value of

the stock could be $46, $47, or $48, each with 1/3 probability. What is the expected value of the option if this assessment is true? FV = 1/3*[4*(46-45) + 3*(50-46)] +

1/3*[4*(47-45) + 3*(50-47)] + 1/3*[4*(48-45) + 3*(50-48)]

FV = 1/3 * (16 + 17 + 18) = $17 PV = 17 / 1.01 = $16.83

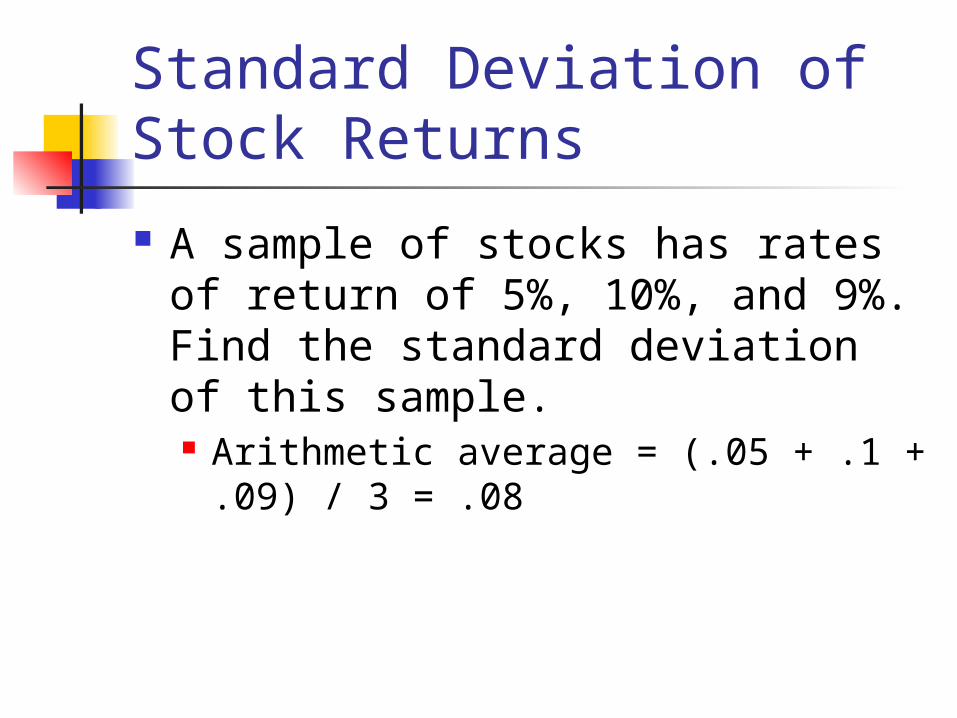

Standard Deviation of Stock Returns

A sample of stocks has rates of return of 5%, 10%, and 9%. Find the standard deviation of this sample. Arithmetic average = (.05 + .1

+ .09) / 3 = .08

Standard Deviation of Stock Returns

Variance= 1/2 * [(.05-.08)2 + (.1-.08)2 + (.09-.08)2]

Variance= 1/2 * [.0009 + .0004 + .0001] = .0007

Standard deviation = (.0007)1/2 = .02646

Standard deviation = 2.646%

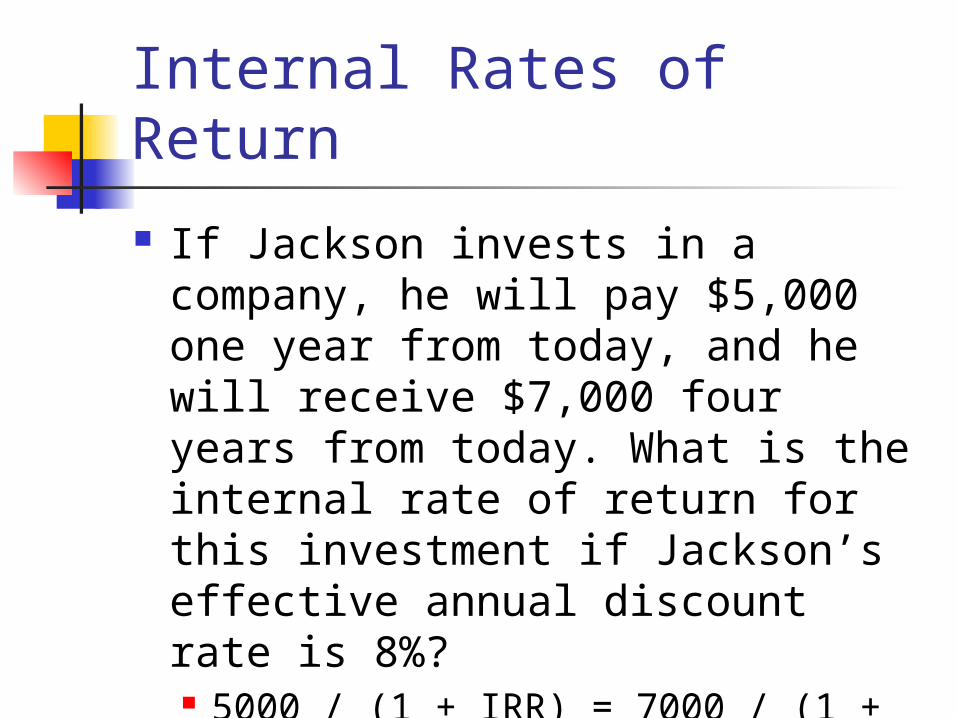

Internal Rates of Return

If Jackson invests in a company, he will pay $5,000 one year from today, and he will receive $7,000 four years from today. What is the internal rate of return for this investment if Jackson’s effective annual discount rate is 8%? 5000 / (1 + IRR) = 7000 / (1 + IRR)4

(1 + IRR)3 = 1.4 IRR = 11.869%

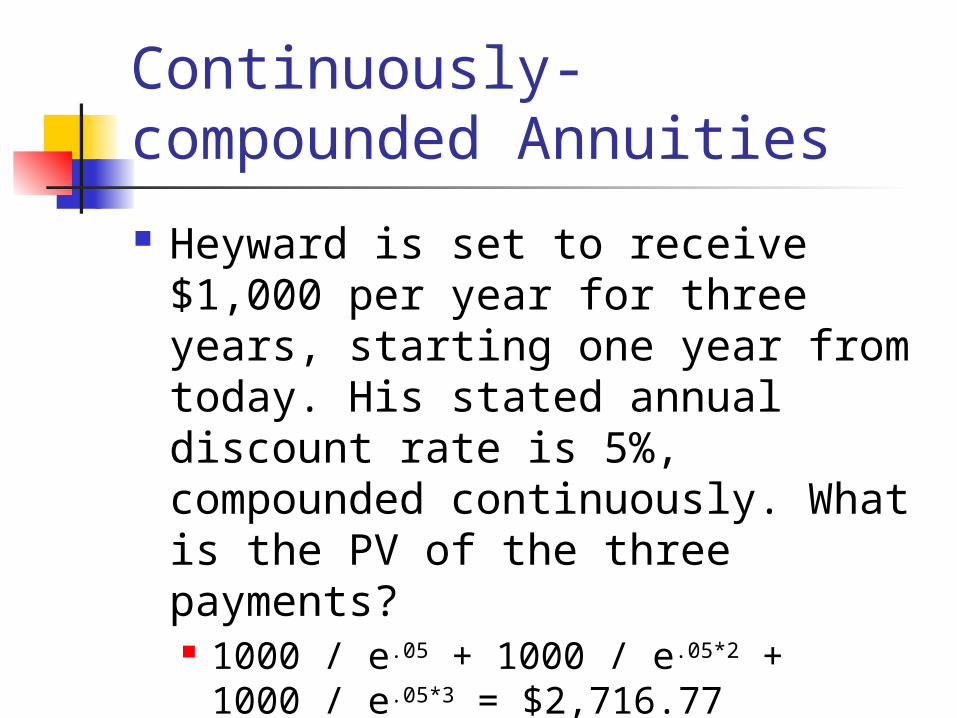

Continuously-compounded Annuities

Heyward is set to receive $1,000 per year for three years, starting one year from today. His stated annual discount rate is 5%, compounded continuously. What is the PV of the three payments? 1000 / e.05 + 1000 / e.05*2 + 1000 /

e.05*3 = $2,716.77

Growing Dividends

Neon Yellow Paper, Inc. is expected to pay a dividend of $2.50 per share later today. The dividend is expected to go up by 20% each of the next three years, followed by a constant dividend forever after. What is the PV of this stock if the effective annual interest rate for this stock is 14%?

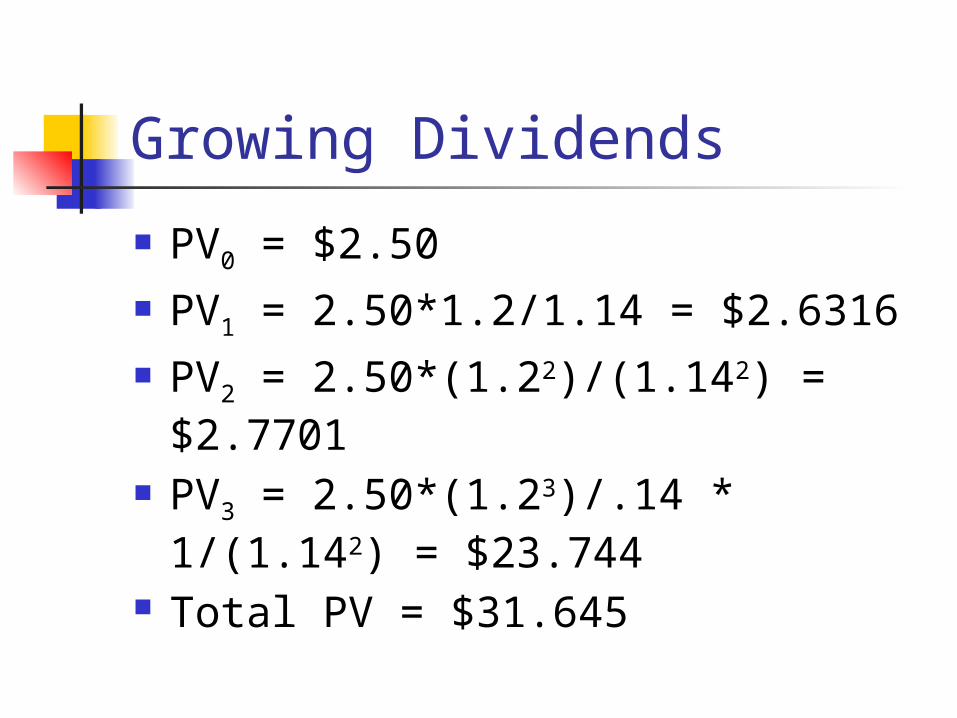

Growing Dividends

PV0 = $2.50 PV1 = 2.50*1.2/1.14 = $2.6316 PV2 = 2.50*(1.22)/(1.142) =

$2.7701 PV3 = 2.50*(1.23)/.14 * 1/(1.142) =

$23.744 Total PV = $31.645

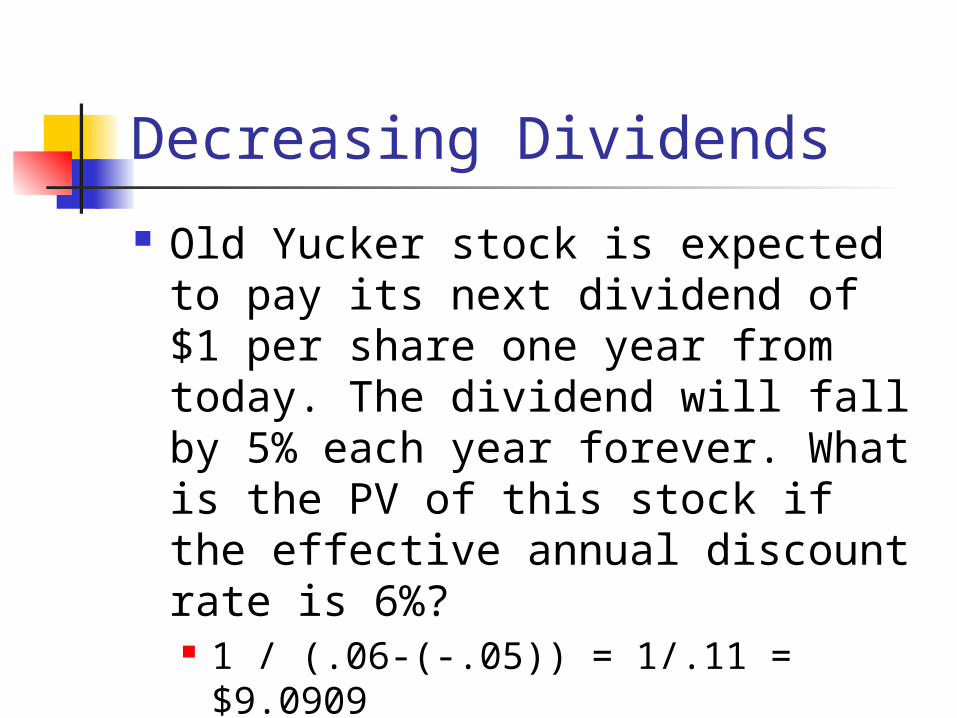

Decreasing Dividends

Old Yucker stock is expected to pay its next dividend of $1 per share one year from today. The dividend will fall by 5% each year forever. What is the PV of this stock if the effective annual discount rate is 6%? 1 / (.06-(-.05)) = 1/.11 = $9.0909

Correlated Returns

There are three known states of the world, each with 1/3 probability: good, okay, and bad. QWE stock has a 20% return in the good state, 9% in okay, and -2% in bad. ZXC stock has a 15% return in good, 6% in okay, and 3% in bad. What is the correlation of these two stocks?

Correlated Returns

Note that there is a strong positive correlation (better state higher return)

AvgQWE = (20 + 9 – 2) / 3 = 9% SDQWE = [1/3 * (.2-.09)2 + (.09-.09)2 +

(-.02-.09)2]1/2 = .0898146 AvgZXC = (15 + 6 + 3) / 3 = 8%

SDZXC = [1/3 * (.15-.08)2 + (.06-.08)2 + (.03-.08)2]1/2 = .0509902

Correlated Returns

Cov(QWE, ZXC) = 1/3 * [(.2-.09)(.15-.08) + (.09-.09)(.06-.08) + (-.02-.09)(.03-.08)] = .0044

Corr = .0044 / (.0898146 * .0509902) = 0.960769

Equivalent Annual Cost

A new machine currently costs $500. The first required maintenance cost will be $25 one year from now. Each subsequent year, the maintenance cost doubles, until the last cost is paid in four years. What is the equivalent annual cost of the machine if the effective annual discount rate is 10%?

Equivalent Annual Cost

PVcosts = 500 + 25/1.1 + 50/1.12 + 100/1.13 + 200/1.14 = $775.784

EAC: 775.784 = EAC/.1 * [1 – 1/(1.16)]

775.784 = 4.35526 * EAC EAC = $178.126

Portfolio Expected Return/Risk

Two assets have zero correlation. Suppose that you invested in a portfolio of these assets that is NOT in the efficient set. Which of the following is possible if you reallocate the amount of money you have invested in each asset?

YesYes

Portfolio Expected Return/Risk

Answer: Increased expected return at the same level of risk AND increased expected on the portfolio with decreased risk, NOT same expected return with decreased risk

A

B

Opportunity Set

Efficient SetNo

Sharpe Ratio

In the Jacksonvilla stock market, the average annual risk premium was 10% in the 1970s, 15% in the 1980s, and 11% in the 1990s. The variance of the risk premium over this 30-year period was 0.04. What is the Sharpe ratio over this three-decade span?

Sharpe Ratio

Avg risk premium = (.1 + .15 + .1) / 3 = .12

SD of risk premium = (.04)1/2 = 0.2 Sharpe ratio = .12 / .2 = 0.6

Profitability Index

Paulina Poundrock is considering a new project that requires a $50,000 investment today. The next cash flow will occur in two years, a positive $10,000 cash flow. In three years, there will be a positive $18,000 cash flow. Each subsequent cash flow will be 8% higher than the previous year’s.

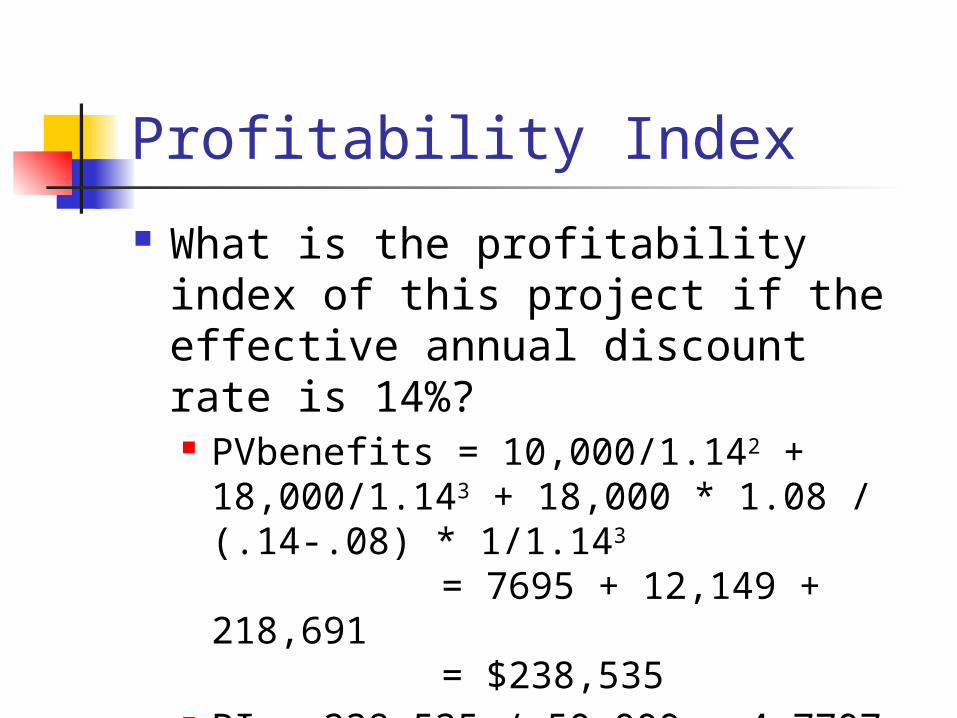

Profitability Index

What is the profitability index of this project if the effective annual discount rate is 14%? PVbenefits = 10,000/1.142 +

18,000/1.143 + 18,000 * 1.08 / (.14-.08) * 1/1.143

= 7695 + 12,149 + 218,691

= $238,535 PI = 238,535 / 50,000 = 4.7707

Option Values

DPR stock sells for $100. Every month, the stock value goes up by $5 with 60% probability and down by $4 with 40% probability. The last time the price changed was yesterday. Laura is considering buying a European call option with exercise price of $108 and expiration date in four months. Her stated annual discount rate is 12%.

Option Values

What is the most that Laura is willing to pay for this option?

Four possible ways for positive value: UUUU ($120) with prob. = .64 = .1296 UUUD/UUDU/UDUU/DUUU ($111) with

prob. = 4 * .63 * .4 = .3456 PV of option = 1/1.014 * [.1296*(120-

108) + .3456*(111-108)] = $2.4909

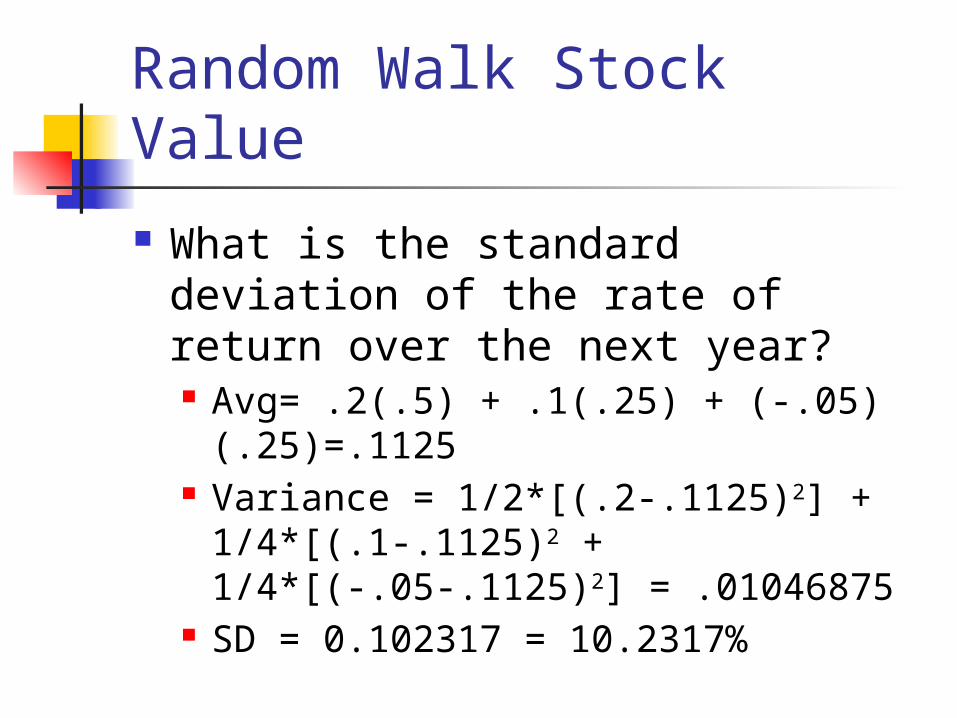

Random Walk Stock Value

For the next two questions: Arrowjones stock is currently priced at $55. Over the next year, the value of the stock could go up by 20% (with probability 50%), up by 10% (with probability 25%), or go down by 5% (with probability 25%).

Random Walk Stock Value

What is the standard deviation of the rate of return over the next year? Avg= .2(.5) + .1(.25) + (-.05)

(.25)=.1125 Variance = 1/2*[(.2-.1125)2] +

1/4*[(.1-.1125)2 + 1/4*[(-.05-.1125)2] = .01046875

SD = 0.102317 = 10.2317%

Random Walk Stock Value

Assume that the effective annual discount rate is 10%. A European call option with expiration date one year from today has a current risk-neutral value of $2. What is the exercise price of the option?

Random Walk Stock Value Possible stock values in 1 year:

50% prob of $66, 25% prob of $60.50, 25% prob of $52.25

Let X = exercise price .5 * (66 – X) / 1.10 = 2 66 – X = 4.40 X = $61.60

Note that an exercise price below $60.50 will lead to more than $2 risk-neutral value

Calculating Dividends

RTT, Inc. will pay a dividend of $X later today. The dividend will increase by $0.50 each of the next 3 years. After that, it will increase by 5% each year forever. The effective annual discount rate is 10%. What is X if the current value of RTT is $50 per share?

Calculating Dividends

50 = X + (X+.5)/1.1 + (X+1)/1.12 + (X+1.5)/1.13 + (X+1.5)(1.05)/(.1-.05) * 1/(1.13)

50 = 3.48685X + 2.40796 + (1.05X + 1.575)/.06655

50 = 19.2645X + 26.0744 X = 1.2420