final investor day slides 2016 genworth canada - print version

TRANSCRIPT

1 Genworth MI Canada Inc. 2016 Investor Day

December 7th, 2016

2016 INVESTOR DAY

Smarter M.I.

2 Genworth MI Canada Inc. 2016 Investor Day

Forward-looking and non-IFRS statements

DRIVING VALUE THROUGH CUSTOMIZED SERVICE EXPERIENCE

Public communications, including oral or written communications such as this document, relating to Genworth MI Canada Inc. (the

“Company”, “Genworth Canada” or “MIC”) often contain certain forward-looking statements. These forward-looking statements

include, but are not limited to, statements with respect to the implementation of the changes introduced by the Government and the

potential impact on new insurance written, as well as the Company’s future operating and financial results, sales expectations

regarding premiums written, capital expenditure plans, dividend policy and the ability to execute on its future operating, investing and

financial strategies, the Canadian housing market, and other statements that are not historical facts. These forward-looking

statements may be identified by their use of words such as “may”, “would”, “could”, “will,” “intend”, “plan”, “anticipate”, “believe”,

“seek”, “propose”, “estimate”, “expect”, and similar expressions. These statements are based on the Company’s current

assumptions, including assumptions regarding economic, global, political, business, competitive, market and regulatory matters.

These forward-looking statements are inherently subject to significant risks, uncertainties and changes in circumstances, many of

which are beyond the ability of the Company to control or predict. The Company’s actual results may differ materially from those

expressed or implied by such forward-looking statements, including as a result of changes in the facts underlying the Company’s

assumptions, and the other risks described in the Company’s Annual Information Form dated March 16, 2016, its Short Form Base

Shelf Prospectus dated August 9, 2016, its most recently issued Management’s Discussion and Analysis and all documents

incorporated by reference in such documents. Management’s current views regarding the Company’s financial outlook are stated as

of the date hereof and may not be appropriate for other purposes. Other than as required by applicable laws, the Company

undertakes no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future

developments or otherwise.

To supplement its financial statements, the Company uses select non-IFRS financial measures. Such non-IFRS financial measures

include net operating income, operating earnings per common share (diluted), operating return on equity, insurance in-force, new

insurance written, loss ratio, delinquency ratio, investment yield, credit score, gross debt service ratio, ordinary dividend payout ratio,

and book value per Common Share (diluted) including accumulated other comprehensive income (“AOCI”). The Company believes

that these non-IFRS financial measures provide meaningful supplemental information regarding its performance and may be useful

to investors because they allow for greater transparency with respect to key metrics used by management in its financial and

operational decision making. Non-IFRS measures do not have standardized meanings and are unlikely to be comparable to any

similar measures presented by other companies. These measures are defined in the Company’s glossary, which is posted on the

Company’s website at http://investor.genworthmicanada.ca. A reconciliation from non-IFRS financial measures to the most readily

comparable measures calculated in accordance with IFRS, where applicable, can be found in the Company’s most recent

Management’s Discussion and Analysis, which is posted on the Company’s website and is also available at www.sedar.com.

3 Genworth MI Canada Inc. 2016 Investor Day

Agenda and key themes

Strategic outlook

Dynamic risk management

Financial strategy and insights

Question and answer session

Smarter M.I.

4 Genworth MI Canada Inc. 2016 Investor Day

Stuart Levings President and Chief Executive Officer

Strategic outlook

5 Genworth MI Canada Inc. 2016 Investor Day

$3.0 billion* Market capitalization

92 million Shares outstanding

$6.6 billion Total assets

$3.6 billion Shareholders’ equity

Genworth Canada overview

WHO WE ARE

LARGEST private residential mortgage insurer in Canada

Helped ~1M+ families achieve homeownership

Supported 250+ Canadian lenders

WHAT WE DO1

1 2

4 3

Mortgage Application Mortgage Insurance Application and Premium

Mortgage Loan Insurance Contract

MARKET FACTS (Q3 2016)

• Mandatory for less than 20% down payment

• Covers 100% of loan, secured by property

• Upfront non-refundable premium

• Lender receives protection against loss from

mortgage default

• Capital relief for lenders

Homebuyer Mortgage lender (originates mortgage)

Mortgage insurer

Note: Company sources

1. Denotes transactional mortgage insurance. * As at December 2nd, 2016.

6 Genworth MI Canada Inc. 2016 Investor Day

Conservative first-time homebuyer profile

Greater Toronto

Single-detached residential median prices well below market….

Greater Vancouver Greater Calgary

$579k $778k

$585k

$1.4M

$442k

$466k

Greater Toronto Greater Vancouver Greater Calgary

$97k

$98k

$90k

$93k

$92k

$133k

….with similar household median incomes

Genworth Canada

Market

Genworth Canada

Market

Source: Genworth internal data, market data median price (CREA); market income (calculated using Stats Canada national income and regional population)

Note: % of multiple borrowers and % of borrowers buying condos based on transactional NIW data as at Q3 ’16 YTD.

Greater Toronto Greater Vancouver Greater Calgary

% of loans with

multiple

borrowers

70% 72% 70%

% of borrowers

buying condos 21% 31% 12%

7 Genworth MI Canada Inc. 2016 Investor Day

2016 key accomplishments

DRIVING VALUE THROUGH MORTGAGE INSURANCE THOUGHT LEADERSHIP

Risk well-distributed;

portfolio re-balancing in

response to tougher

economic environment

High quality and diversified

insurance portfolio1

Portfolio insurance market

leader with approximately

50% market share in 2016

Strong financial

performance; 5% increase

in quarterly dividend

CREDIT SCORE

752

Note: Company sources. Portfolio insurance market share based on Q215-Q216.

1. Credit score references the Q3 2016 YTD timeframe.

2016 loss ratio trending

towards lower half of range

25% to 35% range

Proactive engagement

with regulator to influence

new capital framework

8 Genworth MI Canada Inc. 2016 Investor Day

Our environment today

Risk Assessment

Economic

Housing

Insurance

Portfolio

Regulatory

Key takeaways

GDP growth projection supportive in 2017 (Canada 2.0%;

US 2.1%)1

Oil prices stabilizing

Housing risk in Toronto and Vancouver remains elevated

Government changes contributing to soft landing

NIW quality & mix remains strong

Mortgage reg. changes to have positive long-term impact

on portfolio quality

Mortgage reg. changes impacting market size, but driving

safety and soundness

New capital framework driving higher capital requirements

Private MI PRMHIA limit increasing to $350 billion

STABLE TO IMPROVING MACROECONOMIC ENVIRONMENT

1. Source: GDP projections sourced from Bank of Canada Monetary Policy Report October 2016.

9 Genworth MI Canada Inc. 2016 Investor Day

Regulatory changes

Portfolio insurance

‘Purpose Test’ rules Moderately lower net

premiums written in

the near term

Regulatory change Business implications Performance implications

Portfolio insurance

product restrictions

Mortgage rate stress test

New capital framework

Smaller portfolio

insurance market size;

opportunity for private

mortgage insurance

Improved portfolio

quality

Short-term reduction

in transactional

market size

Premium rate

increases required to

address higher capital

Reduced loss ratio

volatility due to

higher premium rates

Risk sharing proposal

Targeting pricing

ROE of ~13%

10 Genworth MI Canada Inc. 2016 Investor Day

4% 7%

5%

17%

66%

Impact of rate ‘stress test’

Q3 YTD transactional NIW1 GDS & TDS breach drill-down2

BORROWER BEHAVIOUR EXPECTED TO EVOLVE….REDUCING THE IMPACT

OF CHANGES TO 15%-25% OF 2017 TRANSACTIONAL NEW INSURANCE WRITTEN

Eligible NIW (within debt servicing limits)

Ineligible products TDS > 44% limit

Within 200 bps of limit

Large proportion impacted by TDS breach only,

which is within borrowers’ control to change

>200 above limit

Borrowers within 200 bps of GDS breach

can reduce target house price by ~10%

and qualify to make a purchase

Both GDS and TDS breach

GDS > 39% limit

1. Product exclusions include: refinances, rentals, credit score <600, property value >$1MM excluded. 2. GDS/TDS re-calculated to determine eligibility under 4.64% interest rate

50%

50%

11 Genworth MI Canada Inc. 2016 Investor Day

Market evolution

STRONG DESIRE FOR HOMEOWNERSHIP DRIVES MARKET RECOVERY

Data Sources: CREA; all data is monthly and as at Q3’16.

Existing Canadian home sales (Monthly, number of transactions)

Represents

regulatory

changes to

mortgage

insurance

20,000

30,000

40,000

50,000

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

Average

• 2015: minimum down payment requirements

increased for homes >$500,000

• 2016: new qualifying rate requirements and

product restrictions in portfolio insurance

Recent mortgage rule changes

• Six rounds of housing rule changes

since 2008

• Housing activity typically rebounds

within 6-12 months of change

• House price appreciation should return

to more sustainable levels in 2017

12 Genworth MI Canada Inc. 2016 Investor Day

Maintain strong capital

and profitability

Prudent growth focus

Risk management

discipline

Strategic priorities

RESOURCES ALIGNED TO ADDRESS DYNAMIC

ENVIRONMENT AND CAPITALIZE ON NEW OPPORTUNITIES

Key outcomes

Modest market

share accretion

High quality,

diversified

portfolio

Capitalize on

new

opportunities

Appropriately

priced risk

Strategic priorities Key risks

Economic

Insurance Portfolio

Regulatory

Housing

Influence

government

policy

13 Genworth MI Canada Inc. 2016 Investor Day

Strategic execution

BUILDING ON SOLID BUSINESS FUNDAMENTALS

1

Invest in

process

innovation to

drive prudent

market share

expansion

4

Leverage

government

relations

strategy to

influence

regulatory

environment

3

Maintain

risk management

and expense

discipline

2

Drive pricing

strategy for

appropriate

premium rates

and timing of

implementation

5

Explore private

mortgage

insurance

strategy to

differentiate

MIC’s offerings

14 Genworth MI Canada Inc. 2016 Investor Day

MIC investment thesis

How we measure success

Market

share

High quality,

diversified

portfolio

EPS, ROE

and BVPS

growth

Strong

employee

engagement

Potential for top-line

growth through market

size recovery, share

growth, and premium rate

increases

Seasoned risk

management

experience and high

quality portfolio

ROE

improvement

and emerging

business

opportunities

PROVEN BUSINESS MODEL AND DEEP MORTGAGE INSURANCE EXPERTISE

Sound product design

and strong regulatory

environment

15 Genworth MI Canada Inc. 2016 Investor Day

Craig Sweeney Senior Vice President and Chief Risk Officer

Dynamic risk

management

16 Genworth MI Canada Inc. 2016 Investor Day

Insurance risk framework

• Portfolio analytics

• Identification of emerging loss

trends

• Dynamic underwriting guidelines

• Proactive loss mitigation

Portfolio risk

management

• Underwriting fundamentals

• Risk limits and triggers

• Proprietary mortgage scoring

model

• Robust quality assurance

Manage the quality

of new business

RISK PILLARS

• Macro-economic environment

• Housing market trends

• Regional risk factors

Identify & assess

key risks

Strong

regulatory

framework

• Defined underwriting best practices (OSFI’s B20 / B21 guidelines support

safety and soundness)

• Borrower recourse

• Efficient and effective mortgage foreclosure process

• Risk-sensitive capital framework

REGULATORY & LEGAL FRAMEWORK

17 Genworth MI Canada Inc. 2016 Investor Day

Drivers of losses on claims

UNEMPLOYMENT & PORTFOLIO QUALITY

DRIVE PROBABILITY OF DEFAULT

Mortgage arrears and

unemployment rate

2. Portfolio quality

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

'13

'14

'15

'16

Mortgage Arrears

UE Rate (R)

Strong correlation

1. Unemployment 3. House prices

200

250

300

350

400

450

500

'07 '08 '09 '10 '11 '12 '13 '14 '15 '16

MIC Market

Median house price appreciation

(‘$000s)

PRICE APPRECIATION & EFFECTIVE LTV

DRIVE LOSS GIVEN DEFAULT

49% 48%

64%

68%

72%

76%

81%

86%

91%

40%

50%

60%

70%

80%

90%

100%

Port

folio

<=

2009

20

10

20

11

20

12

20

13

20

14

20

15

Q3'1

6 Y

TD

Bulk

Transactional

O/S

Insured

Mortgage

Balances

($B)

$101 $19 $8 $9 $12 $14 $19 $8 $9 $18 $24 $16 $102

Effective LTV ($223B outstanding insured mortgage balance, national,

as at September 30, 2016)

Sources: (UE Rate) Statistics Canada, (Mortgage arrears) Canadian Bankers Association, (Eff LTV) Company sources; (Median price) CREA

All data as at Q3’16 except mortgage arrears (Q2’16).

Book year

18 Genworth MI Canada Inc. 2016 Investor Day

100

120

140

160

180

200

38

40

42

44

46

2007 2009 2011 2013 2015 2017 F

Affordability (L)

5.0%

6.0%

7.0%

8.0%

9.0%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

2007 2009 2011 2013 2015 2017 F

GDP growth expected to improve in 2017.

Unemployment rate expected to be relatively

stable

Canadian environment

Flat to modest house price depreciation

expected in 2017

STABLE TO IMPROVING MACROECONOMIC ENVIRONMENT

GDP Growth (L)

UE Rate (R) Average

Teranet Index (R)

Economic Indicators Housing Affordability1 (Aggregate)

Data sources: GDP & Unemployment Rate (Statistics Canada); Teranet Index (Teranet); Affordability (RBC Economics); 2017 forecast as per management discretion.

1 . Affordability measures the proportion of median pre-tax household income needed to service mortgage payments (P+I), property taxes and utilities. Aggregate refers to all property types.

19 Genworth MI Canada Inc. 2016 Investor Day

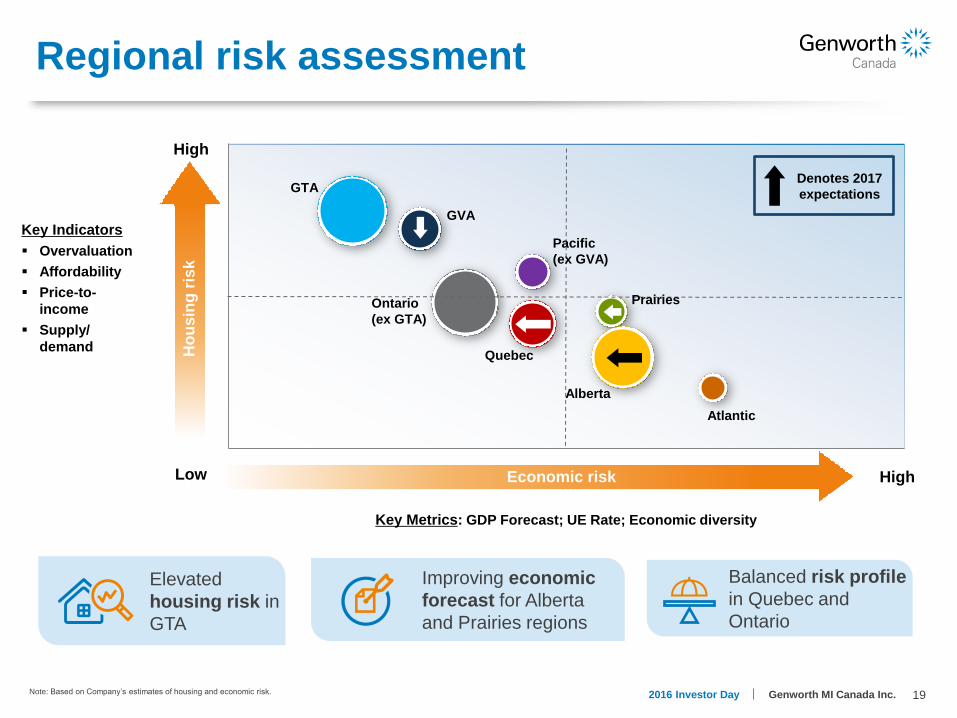

Regional risk assessment

Note: Based on Company’s estimates of housing and economic risk.

Improving economic

forecast for Alberta

and Prairies regions

Elevated

housing risk in

GTA

Balanced risk profile

in Quebec and

Ontario

Ho

us

ing

ris

k

Economic risk Low High

High

GTA

GVA

Quebec

Alberta

Atlantic

Ontario

(ex GTA)

Prairies

Key Indicators

Overvaluation

Affordability

Price-to-

income

Supply/

demand

Key Metrics: GDP Forecast; UE Rate; Economic diversity

Pacific

(ex GVA)

Denotes 2017

expectations

20 Genworth MI Canada Inc. 2016 Investor Day

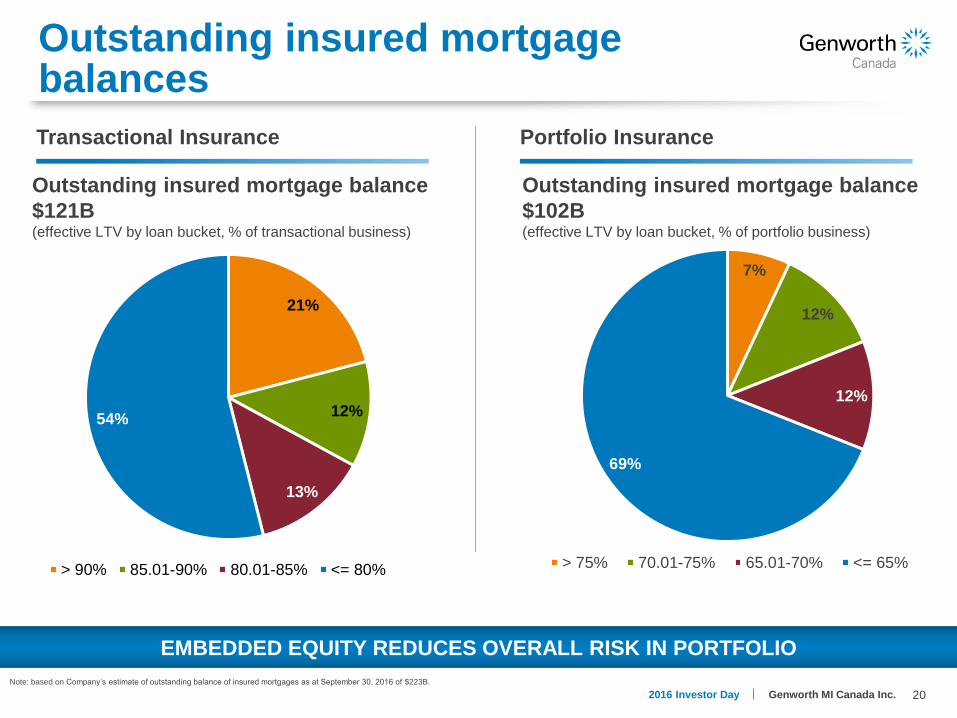

Portfolio Insurance

Outstanding insured mortgage balances

EMBEDDED EQUITY REDUCES OVERALL RISK IN PORTFOLIO

Transactional Insurance

Outstanding insured mortgage balance

$121B (effective LTV by loan bucket, % of transactional business)

Outstanding insured mortgage balance

$102B (effective LTV by loan bucket, % of portfolio business)

Note: based on Company’s estimate of outstanding balance of insured mortgages as at September 30, 2016 of $223B.

21%

12%

13%

54%

> 90% 85.01-90% 80.01-85% <= 80%

7%

12%

12%

69%

> 75% 70.01-75% 65.01-70% <= 65%

21 Genworth MI Canada Inc. 2016 Investor Day

Strong portfolio quality – credit score

PORTFOLIO QUALITY SIGNIFICANTLY IMPROVED COMPARED TO ‘07/08

Note: Company sources for transactional new insurance written.

Canada Greater Vancouver Area

16%

3% 716

752

'07

'08

'09

'10

'11

'12

'13

'14

'15

Q3'1

6 Y

TD

% Score <660 (R) Avg score (L)

Greater Toronto Area

16%

2% 714

759

'07

'08

'09

'10

'11

'12

'13

'14

'15

Q3'1

6Y

TD

% Score <660 (R) Avg score (L)

13%

2% 719

756

'07

'08

'09

'10

'11

'12

'13

'14

'15

Q3

'16

YT

D

% Score <660 (R) Avg score (L)

22 Genworth MI Canada Inc. 2016 Investor Day

Limiting stacked risk factors

DYNAMIC RESPONSE TO INCREASED ECONOMIC AND HOUSING RISK IN 2016

67%

26%

4%

2%

>90-95 >85-90 >80-85 >75-80 <=75

95 LTV – credit score

3% 4% 7%

24%

35%

26%

<=660 <=680 <=700 <=740 <=780 780+

29%

34%

21%

16%

>40 >35-40 >30-35 <=30%

95 LTV – TDSR

Stacked risks (% of NIW)

Halifax Montreal Ottawa Toronto Calgary Vancouver National

2016 0.6% 0.1% 0.4% 0.3% 0.5% 0.2% 0.4%

2015 0.8% 0.8% 1.2% 0.7% 0.9% 0.8% 1.0%

LTV mix - transactional

Note: Company sources.

2016 stacked risks based on Oct‘15 to Sep‘16 New Insurance Written (NIW), purchase only, excludes Alt-A. 2015 stacked risks based on July ‘14 to June ‘15 New Insurance Written (NIW), purchase only deal, excludes Alt-A.

Stacked Risk = >90% LTV and <= 660 score and >40 total debt service ratio (TDSR).

23 Genworth MI Canada Inc. 2016 Investor Day

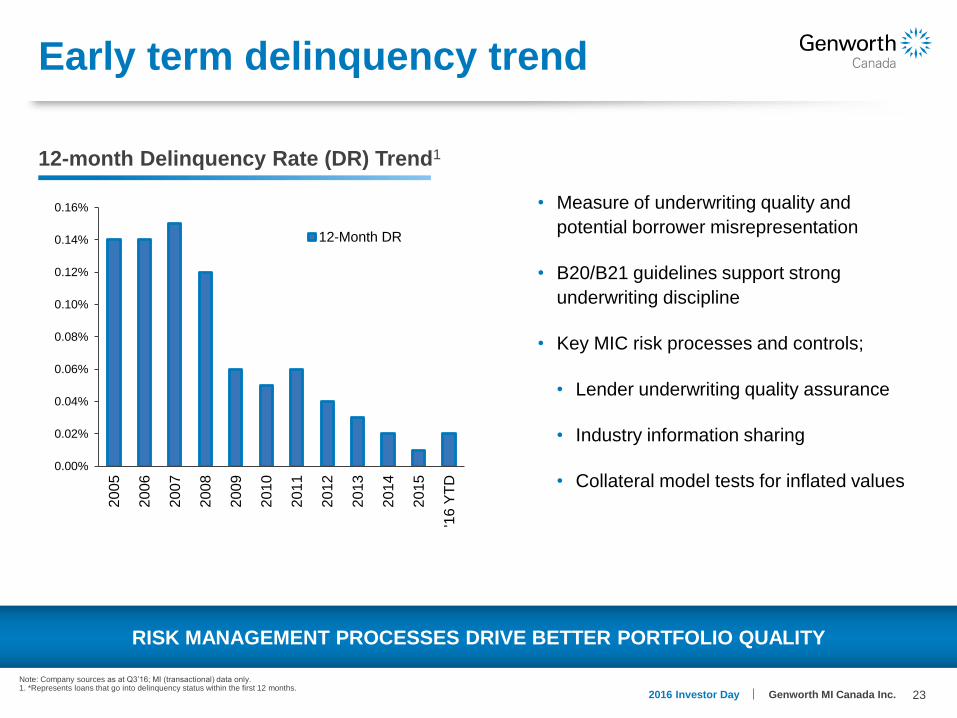

Early term delinquency trend

Note: Company sources as at Q3’16; MI (transactional) data only. 1. *Represents loans that go into delinquency status within the first 12 months.

12-month Delinquency Rate (DR) Trend1

RISK MANAGEMENT PROCESSES DRIVE BETTER PORTFOLIO QUALITY

• Measure of underwriting quality and

potential borrower misrepresentation

• B20/B21 guidelines support strong

underwriting discipline

• Key MIC risk processes and controls;

• Lender underwriting quality assurance

• Industry information sharing

• Collateral model tests for inflated values 0.00%

0.02%

0.04%

0.06%

0.08%

0.10%

0.12%

0.14%

0.16%

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

'16 Y

TD

12-Month DR

24 Genworth MI Canada Inc. 2016 Investor Day

Proactive risk management

GEOGRAPHICALLY DIVERSIFIED … ALBERTA EXPOSURE REDUCED TO 17%

Note: Company sources.

1. NIW represents new insurance written.

2. Pacific includes BC and Territories.

Regional Highlights

Increased focus on appraisals

and quality of real estate in

Greater Vancouver Area

38% 37% 39% 42%

25% 27% 23% 17%

14% 12% 12% 13%

10% 12% 13% 14%

13% 13% 12% 13%

2013 2014 2015 2016 YTD

Ontario Alberta Quebec Pacific Other

Regional NIW1 dispersion (Transactional)2

Underwriting actions resulting

in smaller but better quality

Alberta portfolio in 2016

Strong economic conditions in

Ontario. Key growth region in

2016 & 2017

25 Genworth MI Canada Inc. 2016 Investor Day

Highlights

Alberta: improving portfolio quality

ALBERTA PORTFOLIO QUALITY SIGNIFICANTLY IMPROVED COMPARED TO ‘07/08

Credit score Gross debt service ratio (%)

17%

2% 713

754

'07

'08

'09

'10

'11

'12

'13

'14

'15

Q3'1

6 Y

TD

% Score <660 (R) Avg score (L)

Steady credit score

improvement year-

over-year

Stable home

prices for First Time

Homebuyer

Relatively stable

GDS from Alberta

borrowers

Note: Company sources for transactional new insurance written.

Median home price (In ‘$000s)

$3

03

$3

15

$3

00

$3

19

$3

20

$3

28

$3

38

$3

55

$3

60

$3

54

$270

$280

$290

$300

$310

$320

$330

$340

$350

$360

$370

'07

'08

'09

'10

'11

'12

'13

'14

'15

Q3'1

6 Y

TD

25

%

25

%

24

%

25

%

25

%

24

%

24

%

25

%

25

%

25

%

'07

'08

'09

'10

'11

'12

'13

'14

'15

Q3'1

6 Y

TD

26 Genworth MI Canada Inc. 2016 Investor Day

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

0 3 6 9

12

15

18

21

24

27

30

33

36

39

42

45

48

51

54

57

60

63

66

69

72

75

78

81

84

87

90

93

96

99

102

105

108

111

114

117

120

2007 2008 2009 2010 2011 2012 2013 2014

Book year delinquency development

2007/08 books experienced

significant economic and

housing stress

Note: delinquency rate based on original insurance in-force.

2011-14 books benefitting

from strong portfolio quality

and more stable economic

environment

Positive seasoning trends

27 Genworth MI Canada Inc. 2016 Investor Day

Delinquency performance

1,177 1,415

1,232 1,047

735 619 517 396 385 383 349 331

108

240 388

493

481

344 296

270 181 187 166 163

165

484 862 1,048

722

437

284

222 303 424 467 617

413

561

645 552

554

515

482 569 624

656 578 504

183

240

254 261

260

238

251 299 336

384 401 412

2007 2008 2009 2010 2011 2012 2013 2014 2015 Q1 '16 Q2 '16 Q3 '16

Number of reported delinquencies

Loss

Ratio2 19% 31% 42% 33% 37% 33% 25% 20% 21% 24% 21% 25%

3,381 3,401

2,752

2,153

1,830 1,756 1,829

2,940

2,046

Ontario

BC Alberta

Quebec

Other

Sep. 30, 2016

delinquency

rate1

0.34%

0.34%

0.40%

0.14%

0.08%

Note: Company sources.

1. Based on outstanding insured mortgages as at Sep. 30, 2016.

2. Loss ratio in 2009 excludes the impact of the change to the premium recognition curve in the first quarter of 2009.

2,034

0.21% Total

8%

61%

23%

8%

Portfolio insurance

Core transactionalproducts

Refinance >80%LTV

100% LTV

Products

Eliminated

2010 delinquency

mix by

product

Elimination of higher risk products

1,961 2,027

28 Genworth MI Canada Inc. 2016 Investor Day

0%

10%

20%

30%

40%

50%

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%

0.9%

20

06

2007

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Q3 Y

TD

2016

Canada loss ratio - MIC (RS) Canada DR-CBA Alberta DR-CBA

2017 annual loss ratio expectations

MIC loss ratio & CBA delinquency rates

PRELIMINARY 2017 ANNUAL LOSS RATIO RANGE: 25% TO 35%

Preliminary

2017 Loss

Ratio Range

• WTI price-per-barrel in the

$40-60 US range

• Canadian dollar remains

stable in the 70-80 cent range

• Modest increase in mortgage

interest rates

2017 assumptions

UE Rate House

Prices

Alberta ~8.1% (4.0%)

National ~7.2% (2.0%)

Note: 2017 assumptions based on Company estimates; denote exit rates.

Data Sources: Canadian Bankers Association, Company sources; all data as at Q3’16 except CBA delinquency rates (Q2’16)

2009 excludes the impact of the change to the premium recognition curve in Q1’09

29 Genworth MI Canada Inc. 2016 Investor Day

Key takeaways

Prudent risk management

Underwriting actions reducing

risk

Well positioned to address

regional economic pressures

2017 annual loss ratio range:

25% to 35%

Strong portfolio quality

30 Genworth MI Canada Inc. 2016 Investor Day

Philip Mayers Senior Vice President and Chief Financial Officer

Financial strategy and

insights

31 Genworth MI Canada Inc. 2016 Investor Day

$1,9

71

$1,9

02

$1,8

24

$1,7

85

$1,7

24

$1,7

99

$2,0

21

$2,1

36

200

9

201

0

201

1

201

2

201

3

201

4

201

5

Q3'1

6

$2

2.4

0

$2

4.4

4

$2

6.9

4

$3

0.6

2

$3

2.5

3

$3

5.0

2

$3

6.8

2

$3

9.0

1

200

9

201

0

201

1

201

2

201

3

201

4

201

5

Q3'1

6

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

Creating shareholder value

Operating earnings per share (C$, diluted)

Book value per share (C$, including AOCI, diluted)

Unearned premiums reserve (C$ millions)

EPS (net of dividends)2

Ordinary dividends paid

Buybacks & special dividends

(C$ millions)

EMBEDDED PROFITS IN $2.1 BILLION UNEARNED PREMIUMS

RESERVE DRIVING ONGOING PROFITABILITY

$2.6

7

$3.0

2

$3.0

8

$3.4

3

$3.6

0

$3.8

6

$4.0

5

$3.0

9

Total

EPS

9% CAGR

Unearned premiums growth driven

by strong recent top-line

Seven consecutive

years of EPS growth

7% CAGR1

1. EPS CAGR represents compounded annual growth rate from 2009 to 2015. 2. 2013 operating EPS excludes the impact of the government guarantee exit fee reversal. Reported operating EPS (diluted) in 2012 was $4.67. 2009 operating EPS excludes the impact of the change to the premiums earned recognition curve. Reported operating EPS (diluted) in 2009 was $3.01.

0 325 209 0 0 105 116 50

3Q

YTD

32 Genworth MI Canada Inc. 2016 Investor Day

Strong balance sheet

($ millions) Sept. 30,

2016

Dec. 31,

2015

Assets

Cash and investments $ 6,248 $ 5,917

Other assets 338 322

Total assets $ 6,586 $ 6,239

Liabilities

Loss reserves 161 132

Unearned premiums 2,136 2,021

Long-term debt 433 433

Other liabilities 233 233

Total liabilities 2,963 2,819

Shareholders’ equity

(incl. AOCI) 3,623 3,420

Total liabilities and

shareholders’ equity $ 6,586 $ 6,239

Strong capital position to support transition

to new capital framework

$2.1 billion of unearned premiums could

include significant embedded profits

Translates to over $7 of unrecognized

book value per share

High quality investment portfolio ~95%

investment grade fixed income

Note: Amounts may not total due to rounding.

STRONG FINANCIAL FOUNDATION….SIGNIFICANT EMBEDDED FUTURE PROFITS

Unearned premiums* $2.1 B

Future losses & expenses (1.2)

Future pre-tax income 0.9

Future net income contribution $0.7 B

*Assumes future combined ratio of 55%

33 Genworth MI Canada Inc. 2016 Investor Day

2014 and prior years

2014 and prior years

2015

2015

2016

2016

2016 2017 illustrationfrom premiums

earned

526 483 447

555

703

470

19 77 65

85

106

118

2011 2012 2013 2014 2015 YTDQ3

2016

Premiums earned growth

PREMIUMS EARNED EXPECTED TO GROW MODESTLY IN 2017….

.... AFTER Q3‘16 YTD INCREASE OF 9% YEAR-OVER-YEAR

Premiums written (C$, millions, by type of business) Earnings curve

Premiums earned (Contribution by book year)1

Transactional

Portfolio

545 560 512

640

809

588

Years

3Q

YTD

Increasing

Decreasing

Q4/16

and 2017

premiums

written1

Run-off of unearned premiums reserve

will drive 2017 premiums earned

Q4/16 premiums

written1

2016

0%

5%

10%

15%

20%

25%

30%

1 2 3 4 5 6 7 8 9

Note: Earnings curve assumes no material change in the curve with respect to above depiction. 1 Estimates of Q4/16 and 2017 premiums written are for illustrative purposes only and are not to scale.

34 Genworth MI Canada Inc. 2016 Investor Day

32%

16%

35%

6%

6%

5%

Federals

Provincials

Preferred shares

Emerging markets debt3

Investment grade

corporates2

Cash & short term

investments

High quality investments

Duration: 3.8 years

Book yield: 3.2%1

Invested assets (C$ millions, unless noted)

Note: Company sources.

1. Book yield represents pre-tax equivalent book yield after dividend gross-up of portfolio (as at September 30, 2016).

2. Market value, includes CLOs

Total invested assets (Market value of $6.2 billion) Industry / Sector concentration

$5,917

$5,867

MAINTAINING QUALITY FOCUS IN LOW RATE ENVIRONMENT

$104 million of

maturities in

Q4 2016 and a

further $471M

in 2017

5,641 5,940

276 305

Q4 2015 Q3 2016

Book value

Net

unrealized

gain

$5.9B $6.2B

Corporate bonds & emerging market debt

(41% of portfolio)

Preferred shares (6% of portfolio)

58% 24%

15%

3%

41%

40%

9%

5%

Pipelines

& Distribution

Energy

Financials

Industrials,

Utilities & Other

4%

Infrastructure

Pipelines

& Distribution

Energy

Financials

Industrials,

Utilities & Other

35 Genworth MI Canada Inc. 2016 Investor Day

Investments generate steady income stream

AUM (C$B) 4.3 5.4 5.4 5.4 5.9 6.2

Pre-tax book

yield1 4.3% 4.0% 3.7% 3.5% 3.3% 3.2%

After-tax book

yield 2.4% 2.4%

Historical performance

Investment priorities

Based on forward curve

at Dec. 1, 2016

Current

book

yield1

Current

duration

Sept. 30/16

(years)

1-year

forward

rates2

Cash & short-term 0.51% 0.1 0.50%

Federal agency bonds3 2.10% 3.8 2.05%

Provincial gov’t bonds 3.50% 4.8 2.00%

Corporate bonds (Single A) 3.30% 3.5 2.05%

Emerging market debt 3.69% 5.5 3.60%

Preferred shares 6.70% 4.9 6.70%

Total 3.20% 3.8

Interest &

dividend income

Net gains

• Targeting book yield around 3.2% with duration around 3.8 years

• Rate reset preferred shares offer higher yields and negative correlation to rising interest rates

• Hedging a portion of interest rate risk using fixed-for-floating swaps (approx. 45% currently hedged)

$171 $169 $179 $173

$169

$130

$7 $12

$37 $22 $32

-$9

2011 2012 2013 2014 2015 2016

1. Pre-tax equivalent yield including gross-up of dividend income. 2. As at December 1, 2016. 3. Federal government bonds constitute government agency bonds and NHA MBS.

Yield and duration (by asset class)

3Q

YTD

36 Genworth MI Canada Inc. 2016 Investor Day

Overview of new capital framework

• Unearned Premiums

Reserve

• Reserve for Incurred But

Not Reported Losses on

Claims

Premium Liabilities

Triggered When Price to

Income Metric Exceeds OSFI

Prescribed Threshold:

• Toronto

• Vancouver

• Calgary

• Edmonton

• Victoria

Supplementary Requirement

More Risk Sensitive Based

on:

• Outstanding Balance

• Modified LTV (outstanding

balance / original property

value)

• Remaining Amortization

• Credit Score

Base Requirement

Total Assets Required =

= Capital Required for Insurance Risk

CREATES APPROPRIATE PRICING INCENTIVE .... FOR EXAMPLE,

HIGHER PREMIUM RATE REDUCES CAPITAL REQUIREMENT

+ -

37 Genworth MI Canada Inc. 2016 Investor Day

New capital framework LTV illustration

$0

$5,000

$10,000

$15,000

$20,000

$25,000

1 2 3 4 5 6 7 8 9 10 11 12

To

tal A

sset

Req

uir

em

en

t at

Ori

gin

ati

on

• Premium rate increases likely in 2017 in response to higher capital levels from proposed base and

supplementary requirement

Table above based on Sept. 23rd, 2016 OSFI draft advisory entitled “Capital Requirements for Federally Regulated Mortgage Insurers”.

* New Base Requirement and New Combined Base & Supplementary Requirement are shown at 150% MCT.

** Current Required Capital for insurance risk is calculated at 220% MCT.

Highlights

Draft framework increase in required assets (mix

of price increase and increased capital)

Gross Written Premium / unearned premiums reserve at origination New Base Requirement at 150% MCT* (Current Economic Environment)

Supplementary Requirement at 150% MCT* (Select Housing Markets) Current Required Capital for Insurance Risk under 2016 MCT**

Basic Loan-to-Value at Origination

(Current MCT

guideline)

Total Asset Requirement by LTV (new vs. current framework, by LTV) at origination (730 credit score at issue; $300k mortgage)

65 75 80 85 90 95

38 Genworth MI Canada Inc. 2016 Investor Day

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

1

13

25

37

49

61

73

85

97

10

9

12

1

New framework – Runoff by LTV

Modified LTV as loan ages (730 credit score at issue; $300k mortgage)

• Total asset requirement is very sensitive to modified LTV and diminishes over 5-8 years as modified LTV

approaches 55% to 60%

Highlights

Total asset requirement run-off1 (730 credit score, $300k mortgage)

To

tal a

sset re

qu

ire

me

nt

Months

95% LTV

65%

LTV

90% LTV

85% LTV

80% LTV

75%

LTV

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

1

13

25

37

49

61

73

85

97

10

9

12

1

13

3

14

5

15

7

16

9

18

1

19

3

20

5

21

7

22

9

24

1

25

3

Months

65%

LTV

75% LTV

80% LTV

85% LTV

90% LTV

95% LTV

0

0

55% level

Annual

prepayments 1%

Full repayments

Year 1 0%

Year 2 4%

Year 3 8%

Year 4 10%

Year 5 and after 12%

Prepayment / full

repayment

assumptions

Charts above based on Sept. 23rd, 2016 OSFI draft advisory entitled “Capital Requirements for Federally Regulated Mortgage Insurers”.

1. New Base Requirement 150% MCT.

39 Genworth MI Canada Inc. 2016 Investor Day

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1

13

25

37

49

61

73

85

97

10

9

12

1

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1

13

25

37

49

61

73

85

97

10

9

12

1

New framework – credit score impact

<=600 600 to619

620 to639

640 to659

660 to679

680 to699

700 to719

720 to739

740 to759

760 to779

>=780

Tota

l R

equirem

ent

at Is

sue

Credit Score at Issue

% of YTD ‘16

transactional

business2

1 0 1 1 2 3 4 6 9 13 59

Credit score multiplier for total asset

requirement

New base requirement

CREDIT SCORE MULTIPLIER DRIVES MATERIALLY HIGHER CAPITAL

AS SCORES DECREASE….STRONG CREDIT SCORE IS BENEFICIAL

Total asset requirement run-off1 by

credit score ($300k mortgage)

690 credit

score

690 credit

score

730 credit

score

730 credit

score

770 credit score

770 credit

score T

ota

l a

sse

t re

qu

ire

me

nt

Months

4.6x

3.2x

2.8x

2.5x

2.1x

1.7x

1.4x

1.0x 0.9x

0.7x 0.6x

Multiplier to

730 credit

score

To

tal a

sset re

qu

ire

me

nt

Months 0

0

80% basic LTV

95% basic LTV Based on highest credit score for

multiple borrowers

Charts above based on Sept. 23rd, 2016 OSFI draft advisory entitled “Capital Requirements for Federally Regulated Mortgage Insurers”.

1. New Base Requirement 150% MCT.

2. Credit Score: As at Sept16. Credit Score bucket based on highest Trans Union Credit Score for all borrowers on the file at time of application.

40 Genworth MI Canada Inc. 2016 Investor Day

Today FutureToday Future

New framework – pricing implications

Transactional insurance new business (% of loan)

EXPECT 10-15%+ AVERAGE

TRANSACTIONAL INSURANCE

PRICE INCREASE IN 2017

Portfolio insurance new business (% of loan)

EXPECT 2X OR HIGHER

PORTFOLIO INSURANCE

PRICE INCREASE IN 2017

Charts above based on Sept. 23rd, 2016 OSFI draft advisory entitled “Capital Requirements for Federally Regulated Mortgage Insurers”.

1. IBNR is Incurred But Not Required Reserve

Current

framework

New

framework

Capital

Premium

Capital

Premium

Capital Required

for Insurance

Risk = Total

Asset

Requirement less

Unearned

Premiums and

IBNR1

Current

framework

New

framework Target Pricing

ROE of ~13%

41 Genworth MI Canada Inc. 2016 Investor Day

New framework MCT implications

• 220% holding target being recalibrated to 150% supervisory target

• Preliminary new internal target of 155% - 157% represents $125 - $175 million above supervisory minimum

MCT Framework (%)

Current framework New

framework

Holding target 220%

Gov’t guarantee minimum /

supervisory target 175% 150%1

Internal target 185% 155% - 157% (preliminary)

Operating range 225%+ 160%+

Dollar value per point of MCT ~$15 million ~$25 million

Highlights

1. Company expectations for government guarantee minimum.

42 Genworth MI Canada Inc. 2016 Investor Day

Sept 30 2016 Actual Sep 30 2016Pro-forma

2017 illustration

New framework Pro-forma MCT In

su

ran

ce

ris

k

Holding target Supervisory target & expected government guarantee minimum

220% 150%

Excess above target

Operational risk

Market risk

Legacy transactional

<= 25 yr. amortization

& other insurance

risk

Legacy portfolio &

transactional

extended

amortization

2017 books

236% 160%+ 155-158%

Capped at 2016

level

Immediate

transition to

new framework

Insu

ran

ce ris

k

MCT New Framework (C$, millions)

• Targeting operating with MCT above 160% in 2017

• Transitional provisions cap capital requirements for legacy portfolio insurance & extended amortization

business at Dec. 31, 2016 level (220% MCT)

• Lower capital requirements for market and operational risk due to reduction in internal target

Highlights

43 Genworth MI Canada Inc. 2016 Investor Day

Capital management strategy

Funding organic growth

with MCT > 157%

Capital priorities

Maintaining modest

leverage of <= 15%

Capital strength

At Q3 2016:

• Pro-forma MCT of 155%-158%

• 11% debt-to-capital

Holding company cash and

liquid investments > $100 MM

Credit facility of $100 MM

Capital flexibility

At Q3 2016:

• Holdco cash and liquid investments of $181

million

• $100 MM undrawn credit facility

Sustainable

ordinary dividend

Return of capital when

excess capital available

Capital efficiency

At Q3 2016:

• Increased ordinary dividend by 5%

• Payout ratio of 41%

44 Genworth MI Canada Inc. 2016 Investor Day

ROE drivers

ROE drivers

2016 ROE ~11%

Year

New capital framework

for legacy books

Impact of price increases Interest rate outlook Capital management

initiatives

2017 Neutral

2018

2019

TARGETING 12%+ ROE IN THE MEDIUM TERM

-

+

+ +

+ + +

+ +

+ +

- - -

- -

45 Genworth MI Canada Inc. 2016 Investor Day

Key takeaways

Proven business model has positioned

MIC for future financial performance

Smaller MI market size could lead to

moderate decline in premiums written in 2017,

despite expected higher premium rates

Managing capital to greater than 160% MCT

under new framework

Premiums earned expected to modestly

increase in 2017 due to large recent books

of business

Estimated 25% to 35% loss ratio range

for 2017

Investment income expected to be

relatively flat in 2017

46 Genworth MI Canada Inc. 2016 Investor Day

Stuart Levings President and Chief Executive Officer

Wrap up

47 Genworth MI Canada Inc. 2016 Investor Day

Key takeaways

Solid business model

Strong regulatory environment

Disciplined risk management

MIC is well-positioned

for future

success

Robust profitability drivers

M.I. thought leadership

48 Genworth MI Canada Inc. 2015 Investor Day

Q A

49 Genworth MI Canada Inc. 2015 Investor Day

Senior management team

Stuart Levings, President & CEO

15+ years of mortgage insurance experience

Mr. Levings assumed his current role as President and Chief Executive Officer in January

2015. Prior to that Mr. Levings served in such senior leadership positions as Senior Vice

President, Chief Operating Officer, Senior Vice President, Chief Operations Officer and

Senior Vice President, Chief Risk Officer. Mr. Levings joined the Company in July 2000 as

the Financial Controller, and has also held positions in finance and product development,

including five years as Chief Financial Officer. Before that, Mr. Levings spent seven years

with Deloitte & Touche. Mr. Levings holds a CPA, CA professional designation with over

15 years of professional experience in a variety of industry sectors. Mr. Levings holds a

Bachelor of Accounting Science degree from the University of South Africa and is a

member of both the South African and Canadian Institutes of Chartered Accountants.

Philip Mayers, SVP & Chief Financial Officer

25+ years of mortgage insurance experience

Mr. Mayers became Chief Financial Officer of the Company in 2009. He has over 25

years of finance and general management experience in financial services businesses.

Since joining the Company in 1995, Mr. Mayers has held several senior positions,

including Vice President, Finance, Vice President, Operations, and Senior Vice President,

Business Development. Prior to joining the Company, he held finance positions with

Mortgage Insurance Company of Canada (“MICC”), Esso Petroleum Canada and Deloitte

& Touche. He holds CPA, CA and CMA professional designations and has a Master of

Accounting degree from the University of Waterloo.

50 Genworth MI Canada Inc. 2015 Investor Day

Senior management team

Craig Sweeney, SVP & Chief Risk Officer

15+ years of mortgage insurance experience

Mr. Sweeney has more than 18 years of professional experience in the mortgage and

banking industry. Since joining the Company in 1998, Mr. Sweeney has held senior

positions in Operations and Business Development, including Director of Risk Operations

and Director of Product Development. Mr. Sweeney received an honours Bachelor of Arts

degree in Economics from Carleton University in 1994.

Winsor Macdonell, SVP, General Counsel & Secretary

15+ years of mortgage insurance experience

Mr. Macdonell is responsible for all of the Company’s legal and compliance matters, as

well as government relations. Mr. Macdonell joined the Company in 1999. He was called

to the Bar in Ontario in 1994. Prior to joining the Company, he spent three years in the life

and property and casualty industry, and prior to that was in private practice. Mr.

Macdonell received an honours Bachelor of Commerce degree from Queens University in

1988 and his LL.B. from Dalhousie University in 1992 and his ICD.D in 2014.

51 Genworth MI Canada Inc. 2015 Investor Day

Senior management team

Debbie McPherson, SVP, Sales and Marketing

25+ years of mortgage insurance experience

Ms. McPherson has over 25 years of experience and success in sales and quality

management with the Company. Prior to her current position, Ms. McPherson was the

Company’s Ontario Regional Sales Director. Ms. McPherson plays an active role in many

industry organizations, including the Canadian Association of Accredited Mortgage

Professionals, the Canadian Homebuilders Association and the Canadian Real Estate

Association. Ms. McPherson graduated from the University of Toronto with a Bachelor of

Arts degree.

Scott Gorman, SVP, Operations

15+ years of experience

Mr. Gorman has more than 19 years of International Industry and Consulting experience

within the Financial Services Industry. Prior to joining Genworth Canada, Mr. Gorman

worked for TD Financial Group as VP, Head of Card Operations & Initiatives, and Royal

Sun Alliance (RSA) as the Regional Chief Operating Officer for their Asia and Middle East

Region as well as VP of RSA’s Canadian National Operations. Mr. Gorman has a

Bachelor’s of Commerce from Memorial University of Newfoundland and an MBA from

Schulich School of Business, York University.

52 Genworth MI Canada Inc. 2015 Investor Day

Senior management team

Mary-Jo Hewat, SVP, Human Resources and Facilities

20+ years experience

Ms. Hewat brings over 20 years of human resources expertise spanning numerous

industries and geographies. Ms. Hewat assumed her current role of Senior Vice President,

Human Resources and Facilities in May, 2016. Prior to joining Genworth Canada, she was

Senior Vice President, HR Business Partnerships at Ontario Municipal Employees

Retirement System (OMERS) as well as Vice President, Human Resources. Her career

has also included senior HR roles with Sherritt and Hudson’s Bay. Ms. Hewat has a

Bachelor of Commerce from Ryerson University and a Masters in Business Administration

from the Schulich School of Business, York University.

Brian Hurley, Executive Chairman

20+ years of mortgage insurance experience

Mr. Hurley led the establishment of Genworth into the Canadian marketplace in 1994 and later led it through its initial public offering in 2009. He stepped down as President and CEO of Genworth Canada and assumed the role of Executive Chairman in January 2015. Mr. Hurley has more than 20 years of senior management experience in the mortgage insurance industry worldwide, including leading Genworth’s activities in key international markets from 2004 to 2009. Prior roles include Senior VP, International of General Electric’s U.S. mortgage insurance business and Senior VP of Sales and Operations. Mr. Hurley graduated from Assumption College in Worcester, Massachusetts with a Bachelor of Science degree in Economics.

53 Genworth MI Canada Inc. 2015 Investor Day

[email protected] investor.genworthmicanada.ca

Investor Relations

Jonathan A. Pinto, MBA, LL.M

Vice President, Investor Relations

[email protected] 905.287.5482