final iba lecture 6

TRANSCRIPT

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 1/36

1

Financial Accounting

LECTURE 6

LECTURER: MD. REZAUL KABIR

E-MAIL: [email protected]

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 2/36

2

Learning objectives

After this lecture you should be able to:

A. Under stand the natur e and purpose of income statement

B. Under stand the implications of main profit measur ement

issues

C. Interpr et the information contained within a income statement.

Reading

Atrill & McLaney (2005) Financial Accounting for Decision Makers, Chapter 3.

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 3/36

3

Objective 1

EXAMINE THE NATURE AND PURPOSE OF

INCOME STATEMENT

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 4/36

4

A. UNDERSTAND THE NATURE AND PURPOSE OF

INCOME STATEMENT

1. What is

income stat

ement?

± to measure and report the profit or loss

± during a particular accounting period.

2. Relationship between Income Statement andBalance Sheet

± B/S shows financial position at a particular moment intime

± P & L statement shows the flow of wealth over an

accounting period.

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 5/36

5

2. Relationship between Income

Statement and Balance Sheet

The following equations better explain the

relationship:

Assets - Liabilities = Capital + (Revenues ± Expenses) «« (1)

Assets - Liabilities = Capital + (-) Profit (Loss) «« (2)

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 6/36

6

3. Format of income statementXYZ Limited

Income Statement for the year ended 30th September 2007.

£ £Sales 7000

Cost of goods sold:

Opening stock 2000

Purchases 4000

6000

Less: Closing stock 10005000_

Gross profit 2000

Less: Expenses:

Salaries and wages 700

Rent and rates 500Heat and light 200

Loan interest 100

Depreciation 100

1600

Net profit

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 7/36

7

Objective 2

UNDERSTAND THE IMPLICATIONS OF MAIN

PROFIT MEASUREMENT ISSUES

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 8/36

8

1. Revenue Recognition

Revenues are recognised:

± when the goods or services are delivered to,

and accepted by, the customer.

± not until the realisation of revenue in cash.

However , revenue recognition criteria

could vary from business to business. For example, construction business.

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 9/36

9

2. Accruals and Pr epayments

The general rule is:

All expenses of a particular accounting period must be matched with the

relevant income of that period

± irrespective of the matter whether they¶re

paid or received in cash.

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 10/36

10

Accrued Expenses

Outstanding expenses at the end of accountingperiod.

Example: ± outstanding rent £100

± already paid rent £900.

Treatment: ± P&L: £1000 (900+100)

± B/S: current liability £100.

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 11/36

11

Pr epaid Expenses

Expenses paid in the current year for thenext year.

Example: Annual rent is £1200. But £1400 is paid in the current year.

Treatment: ± P&L: £1200 as current year¶s expenses

± B/S: £200 as current asset.

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 12/36

12

Outstanding Income

Income earned but not received within thecurrent period.

Example: ± fees outstanding £200.

± fees already received £1800

Treatment: ± P& L: under income (1800+200=£2000)

± B/S: outstanding fees £200 under current asset.

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 13/36

13

Income r eceived in advance

You received next year¶s revenue in this

year.

Example: ± You¶ve received both current (£2000) and

next year¶s fees (£2000) together.

Treatment:

± P& L: Only £2000 as current year¶s income.

± B/S: The balance £2000 as current liability.

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 14/36

14

Progress Check 1

For the accounting period 1st January to

31st December 2006 a trader paid £2800 as

r ent. The trader¶s monthly r ent is £200 only.

Calculate how much r ent should be shownin the P& L Statement for the year ended

31st December, 2006.

a. £2800

b. £2400

c. £2600

d. £3000

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 15/36

15

3. Depr eciation Accounting

Basis

of calculation: It is calculated on the basis of costs less residual values.

Residual values are the minimum nominal value thatyou would receive at the end of useful life of an asset.

Calculation methods: ± straight line method and

± r educing balance method.

Which method to choose? ± Remember the purpose here is to choose the method that best

matches the depreciation expense with the benefits or incomethat the related asset would help to generate.

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 16/36

16

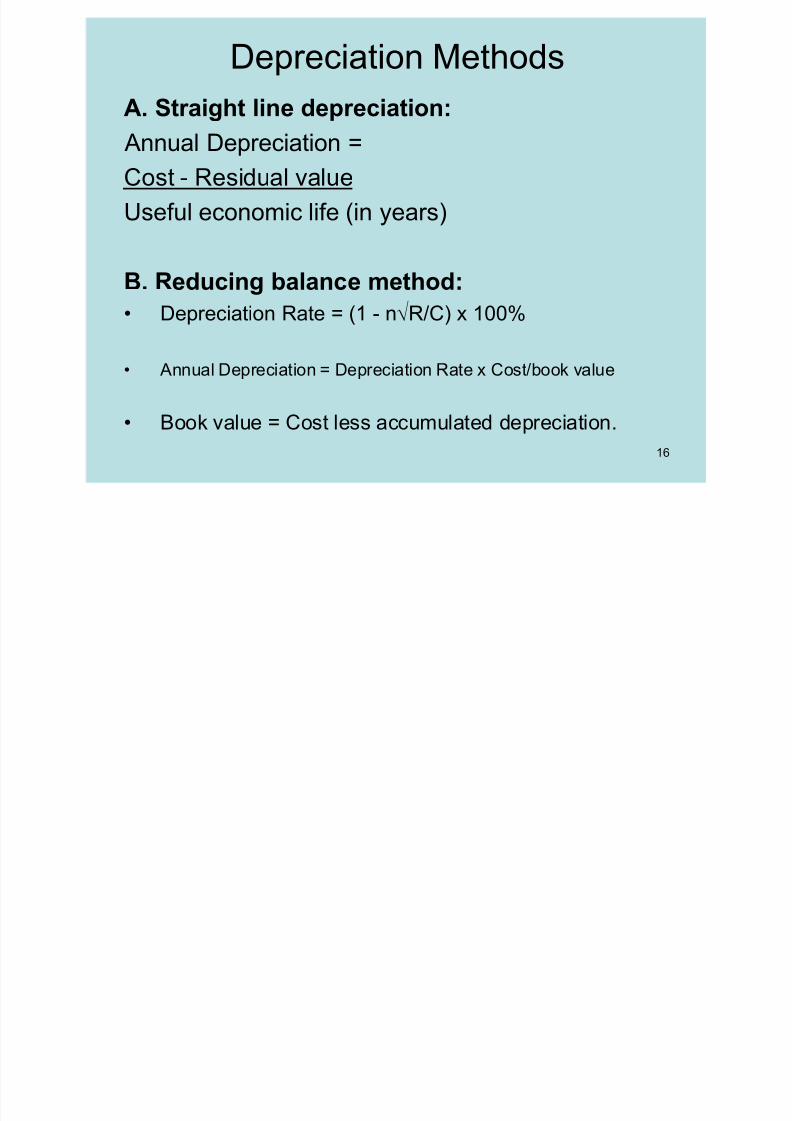

Depreciation Methods

A. Straight line depr eciation: Annual Depreciation =

Cost - Residual value

Useful economic life (in years)

B. Reducing balance method:

Depreciation Rate = (1 - nR/C) x 100%

Annual Depreciation = Depreciation Rate x Cost/book value

Book value = Cost less accumulated depreciation.

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 17/36

17

Example

Plant and machinery was bought on the 1

January 2007

Cost: £1,000 Expected useful economic life of 3 years

Estimated residual value of £343.

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 18/36

18

Example

1. Straight line method:

(£1,000 - £343) z 3 = £219 p.a.

2. Reducing balance method:

____

Rate = (1 - 3£343 z £1,000) x 100 = 30%2007: 30% x £1,000 = £300

2008: 30% x (£1,000 - £300) = £210

2009: 30% x (£1,000 - [£300 + £210]) = £147

Under this method book value/written down value of the asset at the end of 2007 would be £700 (1000-300).

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 19/36

19

Example of Corporate Practice

Tangible fixed assets are stated at costless a provision for depreciation.Depreciation is calculated to write off the

cost of tangible fixed assets, excludingfreehold land, in equal annual instalmentsover their expected useful lives.

(Extract from Glaxo Annual Report, 2002, P.84)

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 20/36

20

Progress Check 2

A machinery was purchased on 1st Jan.

2005 at a cost of £10,000. Depr eciation was

charged @ 10% following the r educing

balance method. What will be the annualdepr eciation charge for the year ended 31st

December, 2006?

a. £1000

b. £900

c. £810

d. £100

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 21/36

21

4. Stock Valuation 1 C ost of Goods Sold = Opening Stock + Purchases ±

C losing Stock.

Main Valuation Rule: ± It is normally valued at cost or net realisable value (NRV)

whichever is lower.

± It needs to be done on an item by item basis

Example: if cost of stock is £100 and NRV is £80 it¶ll bevalued at £80.

NRV = estimated selling price less estimatedexpenditures required to complete and sell the stockitem.

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 22/36

22

Progress Check 3The stock of Cher Ltd at the end of its accounting year was composed of the following

three items:

Cost Net realizable value

£ £

Product A 1,000 1,200

Product B 2,000 2,300

Product C 3,000 2,400

6,000 5,900

This stock would be shown in the balance sheet at an amount of:

A. £5,400B. £5,900

C. £6,000

D. £6,500

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 23/36

23

Stock Valuation 2

Determination of cost depends on the

following assumptions:

± First in, first out (FIFO) - earlier stocks held

are the first to be sold.

± Last in, first out (LIFO) ± the latest stocks held

are the first to be sold.

± Weighted average ± under this method newunit price are calculated every time a new

stock item arrives in the store.

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 24/36

24

Example (Atrill & McLaney, 2005)

1 October opening stock 1000 units @ £10

2 October purchased 5000 units @ £11

3 October purchased 8000 units @ £126 October sold 9000 units @ £20

R equired: Find the value of closing stock.

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 25/36

25

FIFO

£

1000X10 = 10000

5000X11 = 550003000X12 = 36000

101,000 Cost of sales

5000x12 = 60,000 Closing Stock

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 26/36

26

LIFO

£

1000X11 = 11000

8000X12 = 96000107,000 Cost of sales

4000x11 = 44,000

1000x10 = 10,00054,000 Closing Stock

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 27/36

27

WEIGHTED AVERAGE

1000X10 = 10000

5000X11 = 55000

8000X12 = 9600014,000 £161,000 / 14,000 = £11.5 per unit

9000x£11.5 = £103,500 Cost of sales

5000x£11.5 = £57,500 Closing stock

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 28/36

28

Impact on Profits

FIFO LIFO WA

Sales (9000x£20) 180,000 180,000 180,000

Cost of goods sold 101,000 107,000 103,000

Gross Profit 79,000 73,000 76,500

Impact on balance sheet

Closing stock 60,000 54,000 57,500

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 29/36

29

Corporate Practice

Stocks ar e included in the financialstatements at the lower of cost

(including manufacturing overheads,

wher e appropriate) and net r ealisable value. Cost is generally determined ona fir st in, fir st out basis.

(Extract from Glaxo Annual Report, 2002, P.85)

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 30/36

30

5. Provision for bad and

doubtful debts Not all customers to whom you sell on

credit will pay.

You¶re required to make some provisionsfor bad and doubtful debts.

Realistically we can assume that aproportion of them will default.

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 31/36

31

Example

Trade debtors £300,000 at 30th June,

2003.

Out of them £10,000 was found to beirrecoverable (bad) on investigation.

To be on the safer side, management

decided to make another provision for

doubtful debts at 10%.

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 32/36

32

Solution to Example

Profit and Loss

Bad debts written off 10,000

Provision for doubtful debts (300,000 ± 10,000) x 10% 29,000

Balance Sheet

Trade debtors 300,000

Less: Bad debts written off 10,000

Recoverable debt 290,000

Less: Provision for doubtful debts 29,000261,000

======

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 33/36

33

6. Capital and Revenue Expenditur e

Capital Expenditures: ± The benefits go beyond one accounting year.

± It is long-term in nature and non-recurrent.

± Examples: fixed assets ± Treatment: balance sheet.

Revenue expenditures: ± are incurred to run day to day business.

± short-term and recurrent in nature.

± Example: heating and lighting.

± Treatment: income statement.

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 34/36

34

Objective 3

INTERPRET THE INFORMATION CONTAINED

WITHIN AN INCOME STATEMENT

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 35/36

35

P & L Analysis 1

Comparisons:

±Yearly

±with budget

±with competitor ± industry average.

8/3/2019 Final IBA Lecture 6

http://slidepdf.com/reader/full/final-iba-lecture-6 36/36

36

P & L Analysis 2

Gross Profit Ratio = Gross Profit/Sales x

100.

± XYZ limited: 28.5% (2000/7000 x100).

Net Profit Ratio = Net Profit/Sales x100.

± XYZ: 5.7% (400/7000 x 100).