final corporate plan 2012-2017 - uprvunl plan 2012-2017.pdf · projected power consumption in 2010...

TRANSCRIPT

UTTAR PRADESH RAJYA VIDYUT UTPADAN NIGAM LIMITED

2011

Final Corporate Plan 2012-2017

M. Akbar

INDIAN INSTITUTE OF MANAGEMENT LUCKNOW

P R A B A N D H N A G A R O F F S I T A P U R R A O D L U C K N O W - 2 2 6 1 0 1 3

2

Contents Acknowledgments ................................................................................................................................... 4

Executive Summary (Corporate Plan 2017) .............................................................................................. 5

Employee Welfare ............................................................................................................................... 8

Corporate Social Responsibility ............................................................................................................ 8

Methodology ................................................................................................................................... 10

Table1: Demand Pattern from 2000-2010 (MU) ............................................................................. 10

Table2: Demand Projections 2010-17............................................................................................. 12

Projected Power consumption in 2010-11 & 2016-17 ........................................................................ 12

Graph: Projections based on linear trend ............................................................................................... 13

Graph showing regression based on lead indicators ........................................................................... 14

Table 4: Capacity Required in MU and MW in UP ........................................................................... 15

Supply Projections ................................................................................................................................. 15

Estimating Supply of power in UP .......................................................................................................... 15

Methodology ......................................................................................................................................... 16

Table 5: Assumptions ..................................................................................................................... 16

Table 6: showing average cost/MW by different Project Process ....................................................... 17

Table 7: NPV of Investment in different Project processes ................................................................. 17

Conclusion ......................................................................................................................................... 17

Table 8: Existing Projects ............................................................................................................... 18

Table 9: Sector and Raw material wise availability in 2009-10 ........................................................ 18

Table 10: Ongoing up rating of UPRVUNL Plants ............................................................................ 19

Table 11: Expected project completion dates of UPRVUNL Projects (As on March, 2011) .............. 19

Table12: 11th five year Plant availability of power with UPRVUNL................................................... 20

Table 13: Total power availability in 12th Plan in MW ..................................................................... 20

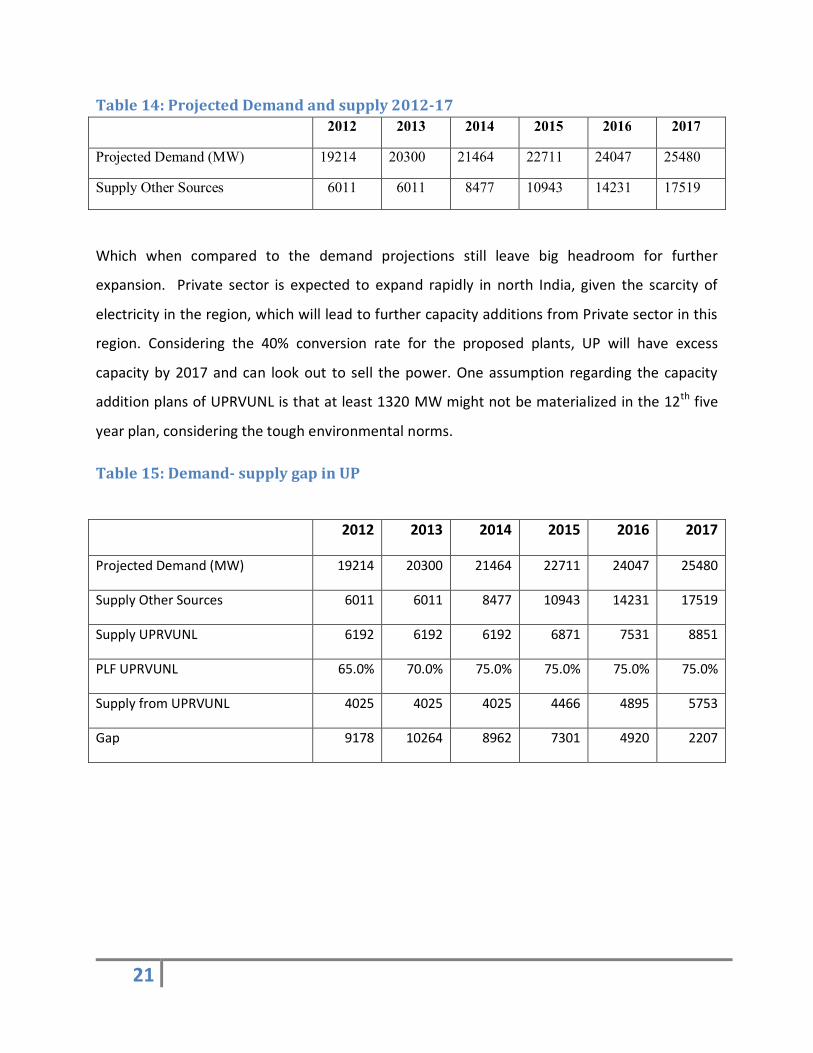

Table 14: Projected Demand and supply 2012-17 .............................................................................. 21

Table 15: Demand- supply gap in Up .............................................................................................. 21

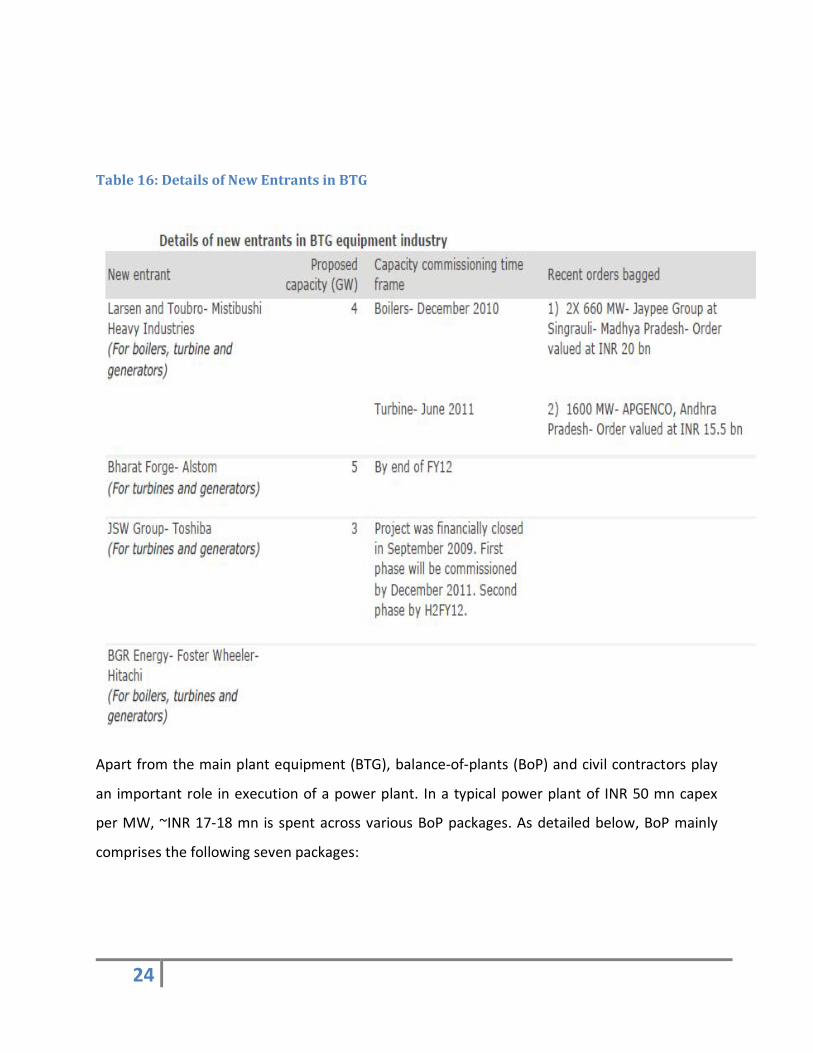

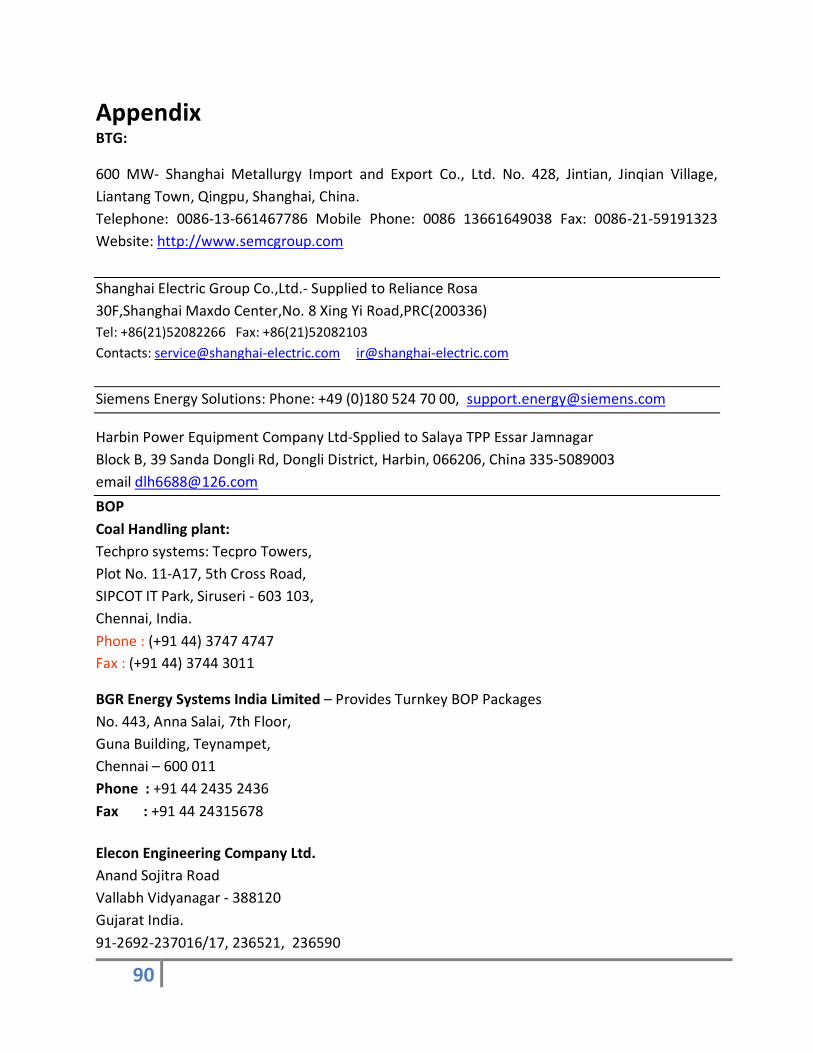

Table 16: Details of New Entrants in BTG ....................................................................................... 24

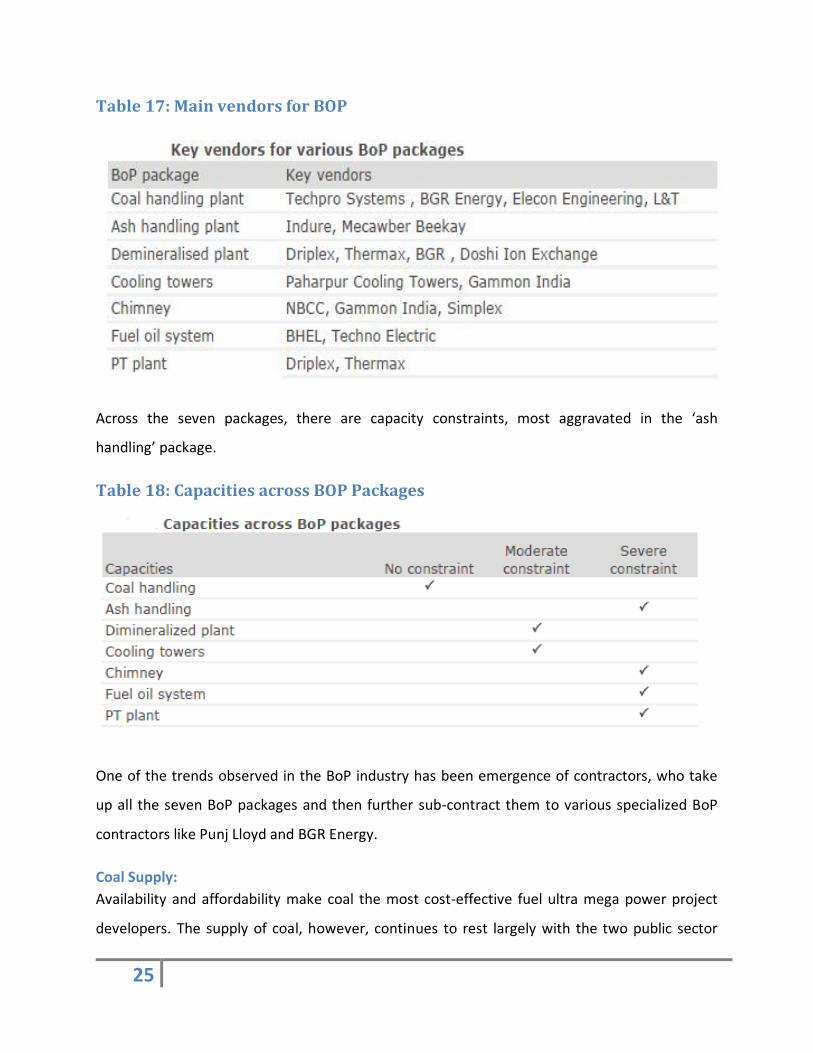

Table 17: Main vendors for BOP ........................................................................................................ 25

Table 18: Capacities across BOP Packages .......................................................................................... 25

Coal Supply: ....................................................................................................................................... 25

Progress on captive blocks hit by forest clearance, land acquisition hurdles ....................................... 27

3

Captive blocks in forest land face maximum delay in commissioning .................................................. 28

Captive coal supply to rise significantly from 2012-13 ........................................................................ 30

Private sector to dominate production, Jharkhand to top supplier states ............................................ 32

Strategic Intent...................................................................................................................................... 33

Vision .................................................................................................................................................... 34

Mission.................................................................................................................................................. 34

Mission Statement ................................................................................................................................ 37

Corporate Values ............................................................................................................................... 37

Corporate Objectives ......................................................................................................................... 37

SWOT Analysis ................................................................................................................................... 38

Strengths ............................................................................................................................................... 38

Weaknesses .......................................................................................................................................... 39

Opportunities ........................................................................................................................................ 41

Threats .................................................................................................................................................. 43

Corporate & Business Strategies ............................................................................................................ 44

Managing Dynamic Environment ........................................................................................................... 45

Business Portfolio .................................................................................................................................. 46

Smoothening Supply Chain .................................................................................................................... 47

Operations including project management ............................................................................................ 48

Human resource management .............................................................................................................. 50

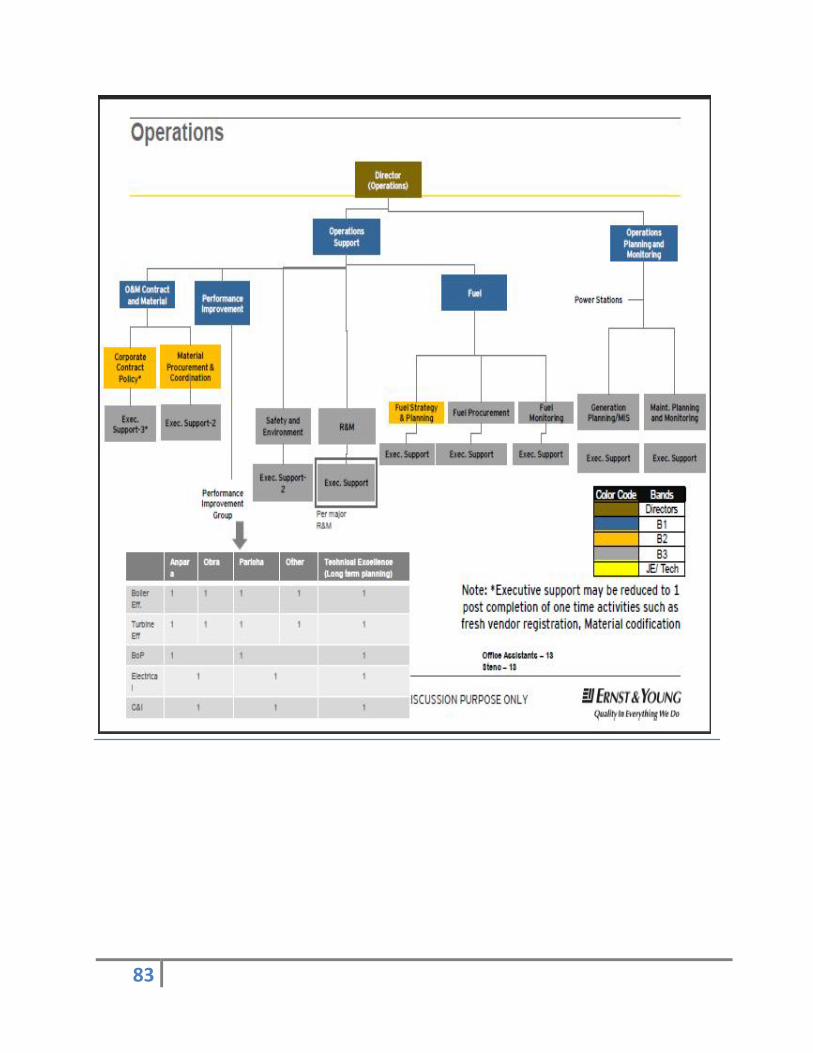

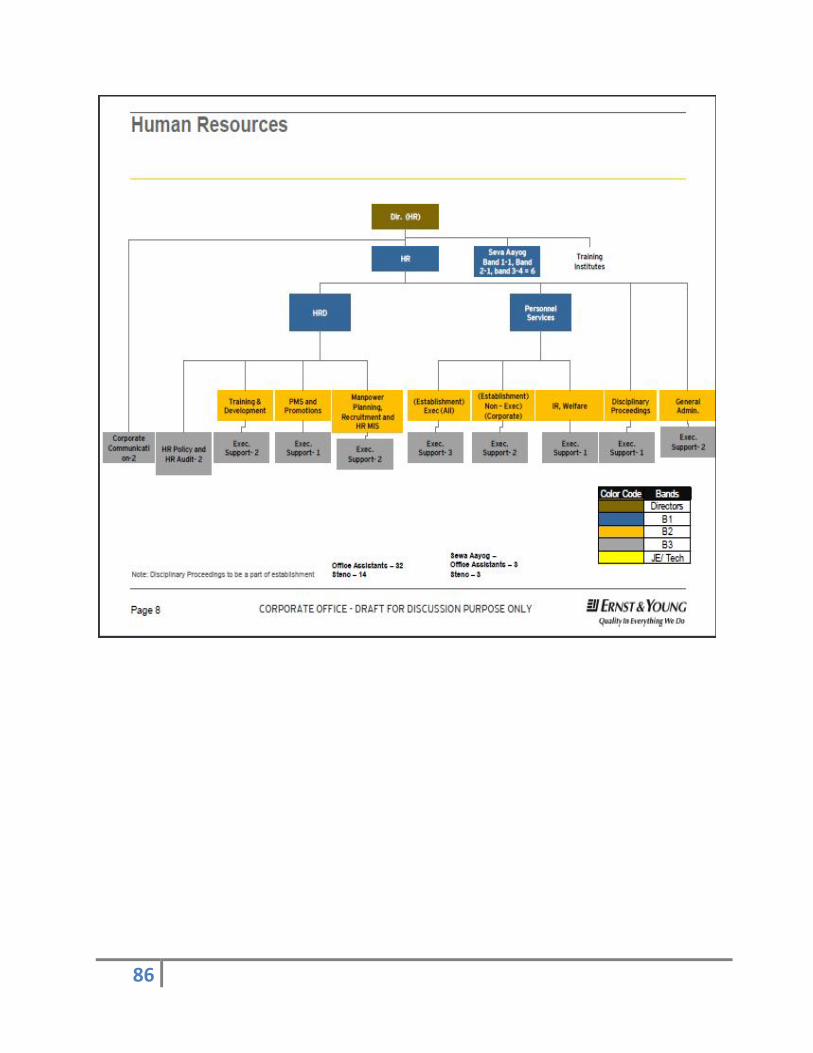

Organizational Restructuring ................................................................................................................. 52

Board of Directors ................................................................................................................................. 54

Board of Directors ................................................................................................................................. 55

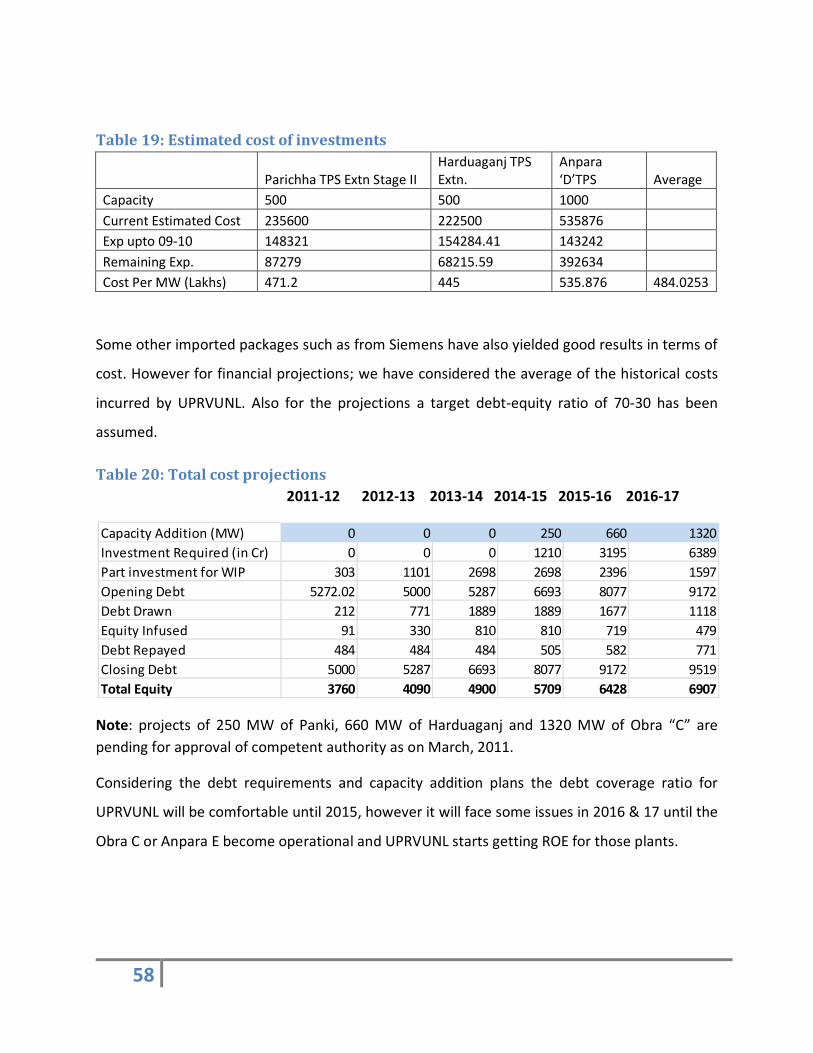

Investment management ................................................................................................................... 57

Financial projections .......................................................................................................................... 57

Table 19: Estimated cost of investments ............................................................................................ 58

Table 20: Total cost projections ......................................................................................................... 58

Table21: ROE and Liquidity projections .............................................................................................. 59

Employee Welfare ............................................................................................................................. 59

Corporate Social Responsibility .............................................................................................................. 59

WAY FORWARD ..................................................................................................................................... 62

Table 6: showing average cost/MW by different Project Process ....................................................... 67

4

Table 7: NPV of Investment in different Project processes ................................................................. 67

Table 3 .............................................................................................................................................. 72

Table 4: Nigam Manpower: An Overall View .................................................................................. 73

Table 5: ................................................................................................................................................. 74

Table -6 ................................................................................................................................................. 75

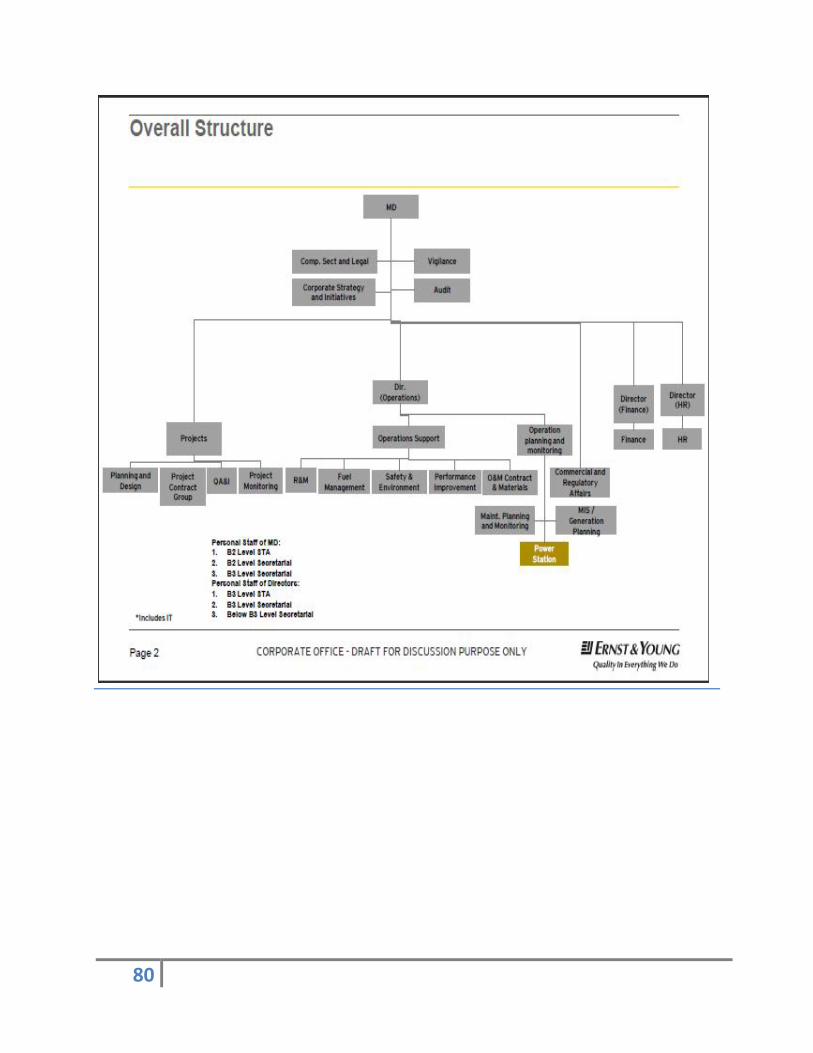

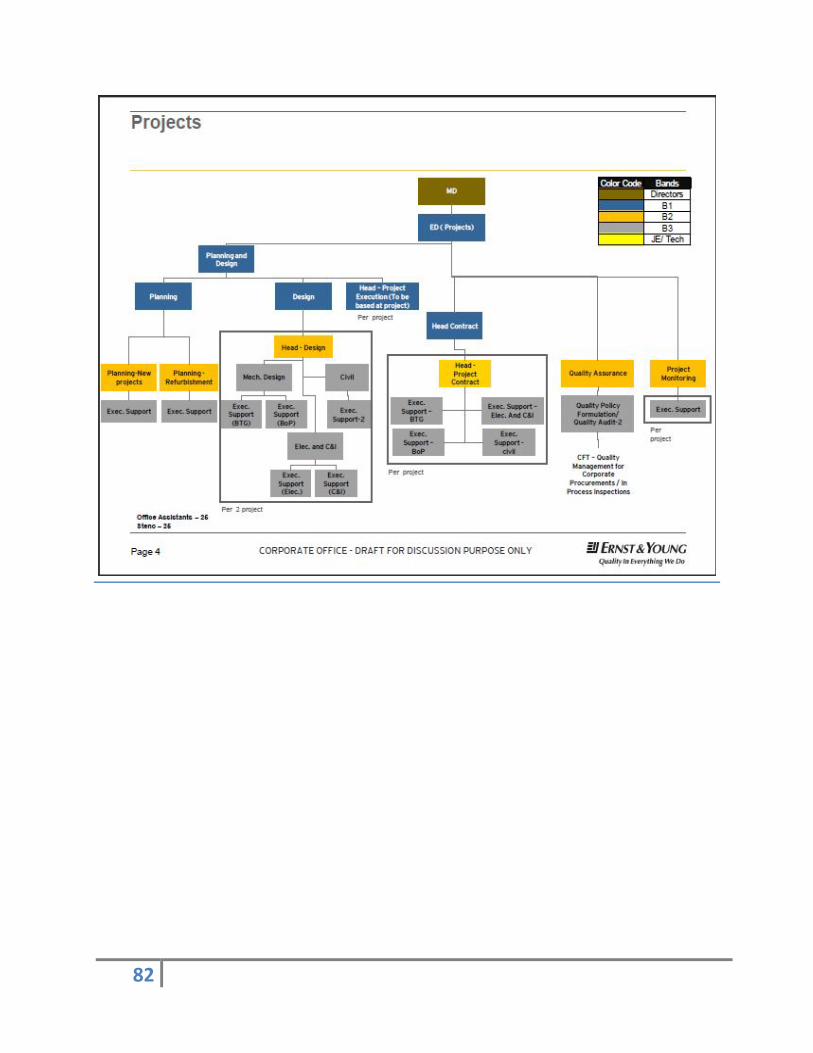

Annexure III: Organizational Structure (Copyright E&Y) ...................................................................... 79

Acknowledgments

Let me take this opportunity to acknowledge all those who have contributed to the

understanding and support to the study carried for developing the corporate Plan 2017 for

Uttar Pradesh Rajya Vidyut Utpadan Nigam Ltd., UPRVUNL or Nigam in short. The cooperation

received from the top management which includes the CMD, Mr Alok Tandon, the functional

and plant managers who have participated in the open meeting at the very stage of the project.

In particular the support received from Mr. Rajiv Goyal, Chief Engineer (HR) , Mr. Dileep Kumar

and Vijay Kumar Gupta who have continuously worked and prodded me to bring in the report

to a respectable level. Many consultants from E&Y who had cooperated and shared their

insights and work with me. My thanks to all of them

At IIM Lucknow I have received help from Research Assistant, Mr. Ashish Hajela , my FPM

student and four of my very bright PGP students- Ashutosh Singh Chandel, Siddhrath Shankar

Choudhary and Siddrath Srivastava- who worked tirelessly for my study along with their course

commitment. There had been many other innumerable people who made this study possible

deserve our sincere thanks. Even after so much cooperation if anything has gone wrong or

missing, I am entirely responsible for those failings.

M. Akbar

Professor, IIM Lucknow

April 19, 2011

5

Executive Summary (Corporate Plan 2017)

The environment for UPRVUNL looks good because of very high demand for electricity for which

deficit would last for next 6-7 years. Managing ongoing and new projects is critical to benefit

from the market demand. The corporation has enough experience in implementing the projects,

but the equipment supplies and receivables had been major concerns.

One of the strongest point is the established business and early mover advantage for UPRVUNL

in the State of Uttar Pradesh with deeper technical processes like the design and development,

erection and commissioning with very experienced people and 5 major plants with about 4000

MW capacity.

The very strengths are converting into debilitating liabilities. The plants are ageing, the people

have become somewhat complacent with obsolescing skills with increasing burden of wages

and inefficiencies resulting into not so good financial performance. The non-cooperative

suppliers, increasing competition are threatening the financial health of the corporation.

In the review report 2005-12 it became clear as in corporate plan 2012-17 that the corporation

needs to handle some of these critical problems. We suggest that to reduce monopoly power of

suppliers like BHEL, the corporation needs to diversify BTG supplier base with internationally

recognized and cheaper vendors especially from China. The coal supply chain needs to be further

smoothened and internal project teams are constituted with capable/ well trained people in

project management skills and technical capabilities. Sadly the experienced managers and the

top management in spite of being highly committed to the physical and financial progress have

not been able to reach performance levels that were targeted.

6

Therefore the whole organization needs to be revamped : corporate and plant structures,

organizational cadres, re-allocation of employees to right jobs , strengthening project

management and building new capabilities for larger sized projects, get off from up rating

projects to new projects at the same premises, except those projects which can give services at

least for next 15 years with PLF above 60%, benchmarked auxiliary consumption, reduced

outages, SHR, cost per unit. The regulator cannot perpetually fund the inefficiently generated

power by compensating with higher tariffs. The competitive pressure will be felt immediately

after the supply deficit is overcome.

Each of the ten areas recommended must be worked upon if the corporation needs to reach its

desired vision and meet it mission commitments: Managing dynamic environment, balancing

business portfolio, smoothening supply chain, operations including project management,

Human resource management, organizational restructuring, Board of Directors, and investment

management , Employee welfare and corporate social responsibility .

Managing dynamic environment

There is need to establish the environmental intelligence group assisting both in operations,

strategic areas like new investment, divestment, closure etc to help make more discipline

decisions

Balancing business portfolio

Although O&M, R&M and refurbishment will remain important areas given more than average

aging plants, however the investment should shift towards new projects due to better economy

and better market control. Retirement of many aging units may be a wise strategy

Smoothening Supply chain

The most critical aspect here is the BTG and BOP timely supplies. Diversified vendor base will

help timely commissioning of projects. In case of contractual failures penalty clause should be

enforced on undue delays. The coal and oil supply chains must be studied for better efficiencies

and environmental compliance perspective.

7

Operations including project management

Here the most critical area is to build critical project management competencies and

empowered structural positions of project management teams. Operational benchmarks as

targets be pursued vigorously through well designed organizational structures, clear

accountability and incentive systems. ERP and IT project should be implemented at faster speed

to derive returns from this investment.

Human resource management

This being the only source of competitive advantage enough resources must be diverted

towards training and development with at 3% budget of revenue dedicated to training and

development for the employees. The cadre restructuring should be done keeping in mind that

the internal environment is enabling and empowering with adequate responsibility and

accountability

Organizational Restructuring

The PRAGATI team’s proposed organizational structure (draft) appears to meet the new

requirements of the organizations. However, a concept of executive teams is proposed at the

corporate and each plant levels. The strategy and project management should be given higher

emphasis. The divisional structure ( with profit responsibility) will un-clutter information

overload as well as more effective operations because of clear accountability.

Board of Director

We suggest that board of directors should also be restructured by bringing in more independent

directors and create more transparency so that in future it could be listed on stock exchanges.

In some critical areas board committees should be constituted

Investment management

Emphasis should be placed on profitability and more internal generation of funds for investment

in future projects, without perpetually depending on the UP Government. This is necessary

8

especially in future if capital markets were to be tapped. By 2017 it should acquire financial

autonomy. It is necessary the government continue funding until then and it should issue bonds

to fund investment against receivables from its customers.

It is suggested that if the above areas are successfully navigated the corporation has the

potential to meet its vision and mission spirit.

Employee Welfare

Employees are the greatest resource of any organization, especially if they are considered the

source of competitive advantage. The developmental needs of employees on the job must be

seriously considered and their socio-psychological needs beside physical comfort. The working

environment should have hazard free and physically comfortable working ambience especially

in plants. Medical facilities, recreation needs and religious and social needs may be considered

with very clear policy and programmes.

Corporate Social Responsibility

It is essential to build a focus of CSR activity to have impact. Beside R&R guidelines, which are

very well elaborated by NTPC, which can be modified as per Nigam needs and vision, the

corporation should focus on an impact area like education, especially scholarship scheme for

higher education. The other important are to which Nigam can look into is the construction of

electricity distribution network around 5 Kms. radii around each of the plants for the local

communities. A mobile health van can provide assistance through an NGO engaged in health

sector in the proximity of each plant. Finally drinking water facilities can be provided to the

local communities.

9

Introduction Energy is the most important building block of every civilization. Most of the modern day war in

fact is, overtly or covertly fought over energy security. Much of the past slow social-economic

development can directly or indirectly be attributed to lack of energy resources specially

electricity. To power the growth of the country to gain and sustain 10% growth in GDP will raise

more energy demands, including hydrocarbons and electricity. The later still the cheapest

source and possibly one of the cleanest sources of energy, notwithstanding the polluting supply

side of generation if oil or coal is used. UPRVUNL represents the pride place in electricity

generation in the state of Uttar Pradesh. The common man and the government look at it with

considerable expectations to solve the problem of energy needs in the State. It is therefore

imperative that UPRVUNL go beyond what it is doing today in meeting these expectations or it

will be dumped by its stakeholders. It is the onus on its managers to make it a more vibrant ,

responsive and responsible organization to all its stakeholders and thus it needs to review its

functioning and improve management systems in order to meet the expectations raised by its

stakeholders: common man, immediate customers, suppliers, owners , managers and many

thousand employees, regulators, lenders and supporters . But before we begin with articulating

its strategic intent in the form of vision, mission and objectives, we need to analyze the demand

and supply scenario.

Demand Projection

Business forecasting can be done by:

1. Trend projection method

10

This methodology is quantitative in nature and gives us figures based on regressing the

past time series data.

2. Barometric method

The government has an ambitious program “Power all by 2012” (a lead indicator) which

indicates higher demand prospects for electricity in coming years. Uttar Pradesh being

the second largest state-economy of India contributes 8.17% to India’s GDP. Given the

fact that Uttar Pradesh’s economy has grown by 7% in last 5 years we expect that this

will continue leading to higher demand of manpower, capital, and infrastructure

including electricity (coincidental indicators).

We have used the trend projection method to forecast the demand for the next seven years viz.

2011-2017.

Methodology The time series forecasting can be done using the trend of past years. These trends can be

captured as linear, exponential functions. Following the demand breakup in previous years, we

feel that a linear estimation will be a better indicator. The past data has been taken from the

power census done by central government. Data for some years was not available and has been

interpolated from the other years.

Table1: Demand Pattern from 2000-2010 (MU)

Sector

Industrial (I)

Domestic (D)

Utilities (U)

Agricultural (A)

Total

2000-01 7177 7513 752 4473 22865 2001-02 7301.4 9265.8 928.5 4986.6 25238.4 2002-03 7286.77 9245.96 926.51 4974.92 25184.36 2003-04 7374 9311 1861 5814 26907 2004-05 7686.89 9668.2 1932.39 6037.05 27989.25 2005-06 8801.5 12567.1 2082.48 5321.8 30109.3 2006-07 10097.77 14406.48 2389.19 6105.53 34543.73 2007-08 10971.26 15682.69 2596.86 6633.74 37531.88 2008-09 11446.75 16329.66 2708.13 6920.64 39155.1 2009-10 11111.28 18578.06 2786.2 7774.65 40283.86

11

Looking closely we can observe that the trend was different before 2003 where it was relatively

flatter. Demand has grown at a higher rate in last 6 years. Hence we will forecast the total

demand using linear regression over last 6 years. The sector-wise demand in following years

will be done on the basis of current (2009-10) sector-wise allocation.

By 2015, the state will require about 54211 MU of power, an increase of about 14000 MU

over current demand. The projections for different sectors for the next five years using this

technique are:

12

Table2: Demand Projections 2010-17

Sector

Industrial (I)

Domestic (D)

Utilities (U)

Agricultural (A)

Total (in MU)

2010-11 12184

20371.97 3055.2 8525.4 44174

2011-12 12876

21529.21 3228.8 9009.7 46683

2012-13 13568

22686.44 3402.3 9494 49192

2013-14 14261

23843.68 3575.9 9978.2 51702

2014-15 14953

25000.91 3749.5 10463 54211

2015-16 15645

26214.10 3923 10947 56720

2016-17 16337

27487.20 4096.6 11431 59485.20

Projected Power consumption in 2010-11 & 2016-17

13

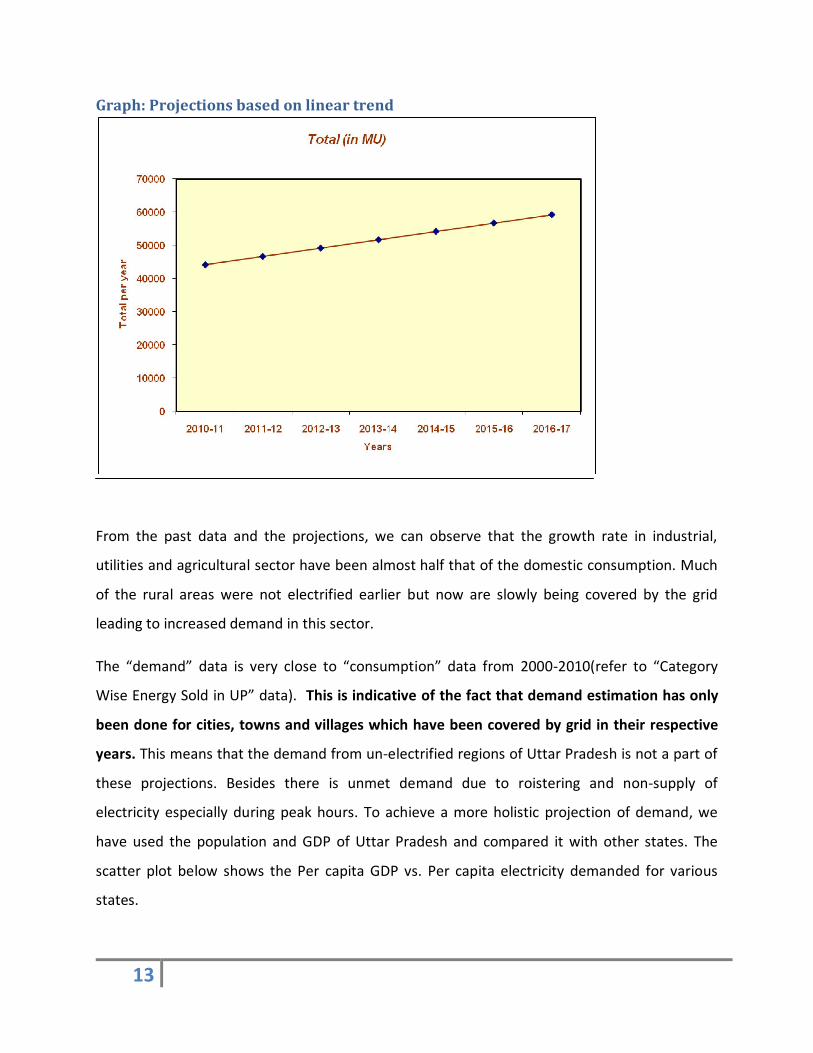

Graph: Projections based on linear trend

From the past data and the projections, we can observe that the growth rate in industrial,

utilities and agricultural sector have been almost half that of the domestic consumption. Much

of the rural areas were not electrified earlier but now are slowly being covered by the grid

leading to increased demand in this sector.

The “demand” data is very close to “consumption” data from 2000-2010(refer to “Category

Wise Energy Sold in UP” data). This is indicative of the fact that demand estimation has only

been done for cities, towns and villages which have been covered by grid in their respective

years. This means that the demand from un-electrified regions of Uttar Pradesh is not a part of

these projections. Besides there is unmet demand due to roistering and non-supply of

electricity especially during peak hours. To achieve a more holistic projection of demand, we

have used the population and GDP of Uttar Pradesh and compared it with other states. The

scatter plot below shows the Per capita GDP vs. Per capita electricity demanded for various

states.

14

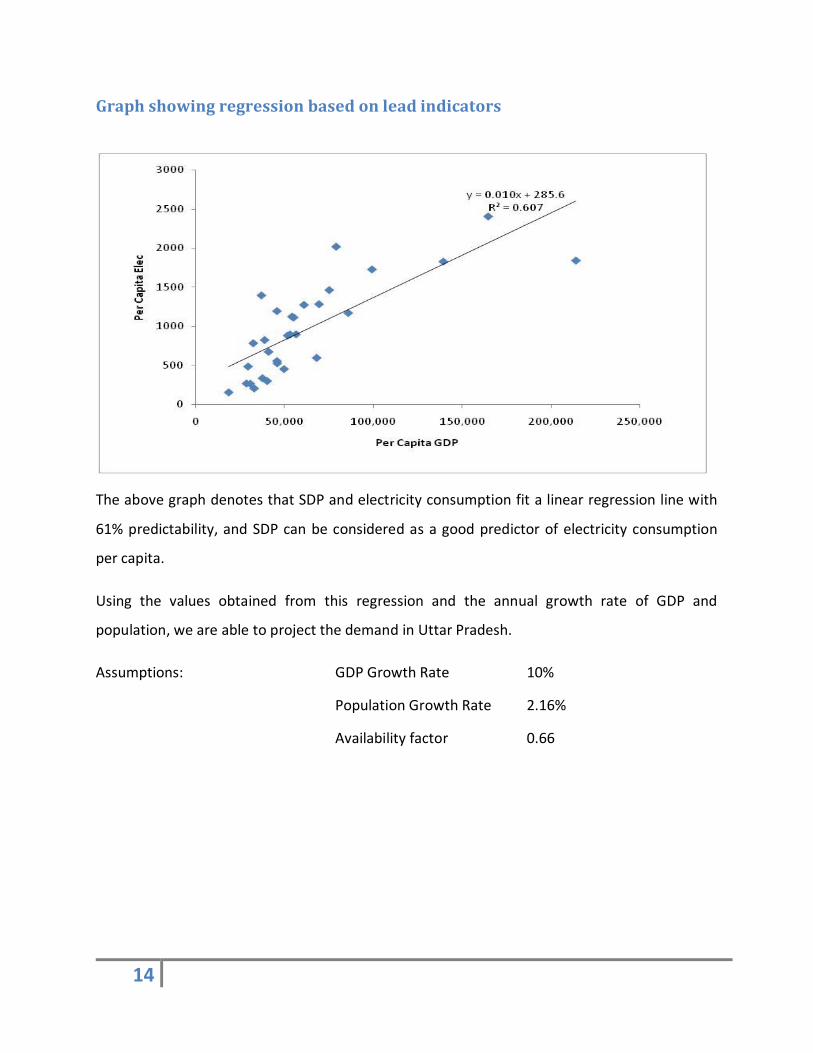

Graph showing regression based on lead indicators

The above graph denotes that SDP and electricity consumption fit a linear regression line with

61% predictability, and SDP can be considered as a good predictor of electricity consumption

per capita.

Using the values obtained from this regression and the annual growth rate of GDP and

population, we are able to project the demand in Uttar Pradesh.

Assumptions: GDP Growth Rate 10%

Population Growth Rate 2.16%

Availability factor 0.66

15

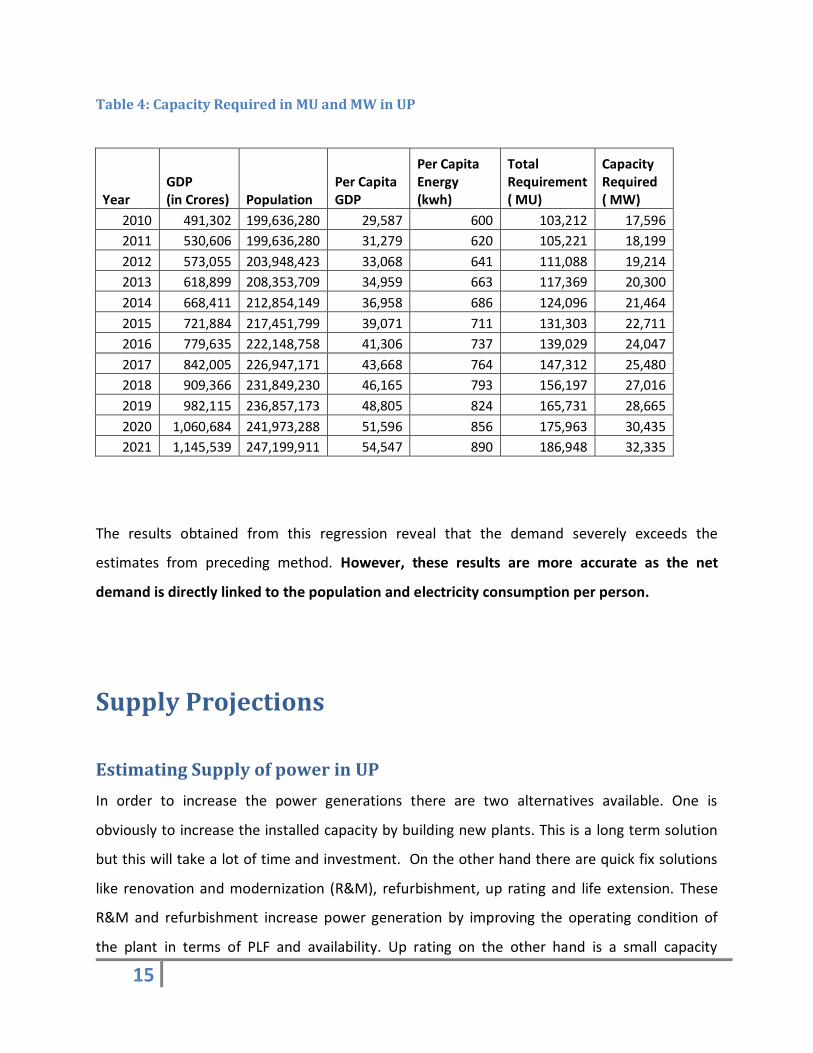

Table 4: Capacity Required in MU and MW in UP

Year GDP (in Crores) Population

Per Capita GDP

Per Capita Energy (kwh)

Total Requirement ( MU)

Capacity Required ( MW)

2010 491,302 199,636,280 29,587 600 103,212 17,596 2011 530,606 199,636,280 31,279 620 105,221 18,199 2012 573,055 203,948,423 33,068 641 111,088 19,214 2013 618,899 208,353,709 34,959 663 117,369 20,300 2014 668,411 212,854,149 36,958 686 124,096 21,464 2015 721,884 217,451,799 39,071 711 131,303 22,711 2016 779,635 222,148,758 41,306 737 139,029 24,047 2017 842,005 226,947,171 43,668 764 147,312 25,480 2018 909,366 231,849,230 46,165 793 156,197 27,016 2019 982,115 236,857,173 48,805 824 165,731 28,665 2020 1,060,684 241,973,288 51,596 856 175,963 30,435 2021 1,145,539 247,199,911 54,547 890 186,948 32,335

The results obtained from this regression reveal that the demand severely exceeds the

estimates from preceding method. However, these results are more accurate as the net

demand is directly linked to the population and electricity consumption per person.

Supply Projections

Estimating Supply of power in UP

In order to increase the power generations there are two alternatives available. One is

obviously to increase the installed capacity by building new plants. This is a long term solution

but this will take a lot of time and investment. On the other hand there are quick fix solutions

like renovation and modernization (R&M), refurbishment, up rating and life extension. These

R&M and refurbishment increase power generation by improving the operating condition of

the plant in terms of PLF and availability. Up rating on the other hand is a small capacity

16

addition to existing plants. Life extension increases the life of the plant, which otherwise is 25

years. These solutions require less investment compared to new plant and can be implemented

quickly. However their benefits are limited in terms of useful life and the power output.

Methodology We have compared refurbishment and uprating to new plant in terms of Net Present Value of

the Capex required for a 1MW capacity and the additional revenues generated. The detailed

calculations and the assumptions taken can be seen in the excel sheet attached as Annexure IV

All the inputs and assumptions to the model are kept in a separate tab “Assumptions and

Inputs” of table 5 bellow. In case of any disagreement with any of the assumptions/values or to

carry any sensitivity analysis the value can be changed in the assumptions sheet. All the related

changes will get reflected in the calculations and results.

Table 5: Assumptions Assumptions

Per Mega Watt cost of establishment of new plant = 5 Crore Economic viable life of new plant = 25 Years

Average PLF ove life of a plant = 85 % Percentage increase in PLF due to refurbishment = 25 %

Time after which new plant will require R&M = 10 Years Yearly R&M expenses as percentage of gross block = 3.5 %

Per Mega Watt cost of refurbishment = 1.8 crore Number of years of benefit from refurbishment = 15 Years

Per Mega Watt cost of uprating = 3 Crore Number of years of benefit from uprating = 15 Years

Discount rate for finding present value of benefits = 7 % Approved tariff = 1.8 Rs/unit

Auxiliary Power consumption = 8 % Outage = 7 %

Variable operating costs are assumed to be same for new and refurbished plants In case of refurbishment or upration R&M expenses will continue to occur at the

same rate as in 10yr old plant

In fact the Operating costs will be lower thus improving NPV.

17

The excel sheet is provided as Annexure IV separately in electronic form. However, the result

summary is presented below:

Table 6: showing average cost/MW by different Project Process Average Cost/MW

Row Labels Average of cost/MW

R&M 0.806 Refurbishment 1.879 uprating 3.015 Grand Total 1.484

Table 7: NPV of Investment in different Project processes

Project Process

NPV in Crores

New Plant 7.47 Refurbishment -0.80 Uprating 5.78

Conclusion From the calculation it was seen that a new plant would be most beneficial followed by

uprating in terms of the net present value. Refurbishment was not found profitable for the

given set of benefits it is expected to provide. Therefore it is not recommendable to carry out

refurbishment unless it is the only possibility due to resource crunch or pressure from demand

side. However other than financial criteria should be considered, which may temper the above

conclusion.

Other major issue discovered in case of refurbishment and R&M is the delay of supplies from EPC

contractor. This has caused delay in repair and maintenance activities and caused permanent damage to

facilities besides decreasing efficiency. A penalty clause for delay should be incorporated in EPC

contracts to account for any delay.

18

Table 8: Existing Projects

Plant Age of Plant

Unit Nature Capacity Capacity Addition

(MW) cost/MW

Obra 43 1,2 Refurbishment 100 20 1.72 Harduaganj 33 5 R&M 60 0 0.34 Obra B (5*200) 30 Refurbishment 1000 80 1.51

Anpara A 23 R&M 630 0 1.25

Harduaganj 32 7 uprating 120 10 3.02 Obra A 35 7,8 R&M 188 0 0.95

Anpara B (2*500) 30 R&M 1000 0 0.69

Parichha 25 1,2 Refurbishment 220 0 2.40

Capacity Projection Uttar Pradesh Currently has 10369 MW of installed power generation capacity of which 4082 MW comes from UPRVUNL. Following is the breakup of the current capacity in UP.

Table 9: Sector and Raw material wise availability in 2009-10

Current Capacity (till 2009)

Uttar

Pradesh

Installed Capacity of Power Plants in UP (in MW)

Thermal

Total

Terms

Nuclear

Hydro

(Renew-

able)

RES

(MNRE)

Grand

Total

Coal Gas Diesel

State 4082 0 0 4082 0 524.1 25.1 4621.2

Private 0 0 0 0 0 0 545.5 545.5

Central 2540.84 549.97 0 3090.81 203.72 1073.32 0 4367.85

Sub-Total 6612.84 549.97 0 7162.81 203.72 1597.42 570.6 9534.55

19

In addition to this UPRVUNL has undertaken/ proposed uprating of its existing plants which will

enhance its capacity by another 110 MW.

Table 10: Ongoing up rating of UPRVUNL Plants

UPRVUNL also has some ongoing projects which will come up in the near future increasing the

UPRVUNL’s capacity by 2000 MW. Following are the details of UPRVUNL’s projects:

Table 11: Expected project completion dates of UPRVUNL Projects (As on March, 2011)

Name of the Project

Ownership Capacity Status Schedule for synchronization

Paricha TPS Stage II

UPRVUNL 500 Under construction Expected by the Nov, 2011 and Dec, 2011

Harduaganj TPS Extn (Stage II)

UPRVUNL 500 Under construction Expected by May,11 and Jul, 2011

Anpara D TPS Unit I

UPRVUNL 500 Under construction Expected by the Dec,2011

Anpara D TPS Unit II

UPRVUNL 500 Under construction Expected in 12th plan

Four private sector/NTPC projects are also in progress in UP, which will give varying share of

their output to the state:

Plant Age of Plant

Unit Nature Status Life Exp Capacity Addition (MW)

Obra 43 1,2 Refurbishment Completed 15 20 Obra B (5*200) 30 Refurbishment Ongoing 15 80 Harduaganj 32 7 uprating Ongoing 15 10

20

Table12: 11th five year Plant availability of power with UPRVUNL 11th Five Year Plan (in MW)

Private Sector 1530

MOUs 450

Central Govt. 1571

Total 3551

In addition there have been several MOU’s signed by UPPCL in the recent past with the various

power producers to setup their facilities in the state, and there are several other projects in the

pipeline including a few from UPRVUNL (Panki Extn, Harduaganaj Extn Stage II, Obra C, Anapara

E). Following are the details for the 12th Five year plan.

Table 13: Total power availability in 12th Plan in MW

Source: UPRVUNL

For these projects a conversion rate of 50% can be assumed considering the various hurdles

they may face.

Considering these capacity addition plans in UP, the total available power to UP is given in table

12

12th Five Year Plan (in MW)UPRVUNL 3550Joint Ventures 3300Private Sector (Competetive Bidding) 8600Private Sector (MOUs) 10940Case -1 (Planned) 5000From Central Govt. 5040Total 36430

21

Table 14: Projected Demand and supply 2012-17 2012 2013 2014 2015 2016 2017

Projected Demand (MW) 19214 20300 21464 22711 24047 25480

Supply Other Sources 6011 6011 8477 10943 14231 17519

Which when compared to the demand projections still leave big headroom for further

expansion. Private sector is expected to expand rapidly in north India, given the scarcity of

electricity in the region, which will lead to further capacity additions from Private sector in this

region. Considering the 40% conversion rate for the proposed plants, UP will have excess

capacity by 2017 and can look out to sell the power. One assumption regarding the capacity

addition plans of UPRVUNL is that at least 1320 MW might not be materialized in the 12th five

year plan, considering the tough environmental norms.

Table 15: Demand- supply gap in UP

2012 2013 2014 2015 2016 2017

Projected Demand (MW) 19214 20300 21464 22711 24047 25480

Supply Other Sources 6011 6011 8477 10943 14231 17519

Supply UPRVUNL 6192 6192 6192 6871 7531 8851

PLF UPRVUNL 65.0% 70.0% 75.0% 75.0% 75.0% 75.0%

Supply from UPRVUNL 4025 4025 4025 4466 4895 5753

Gap 9178 10264 8962 7301 4920 2207

22

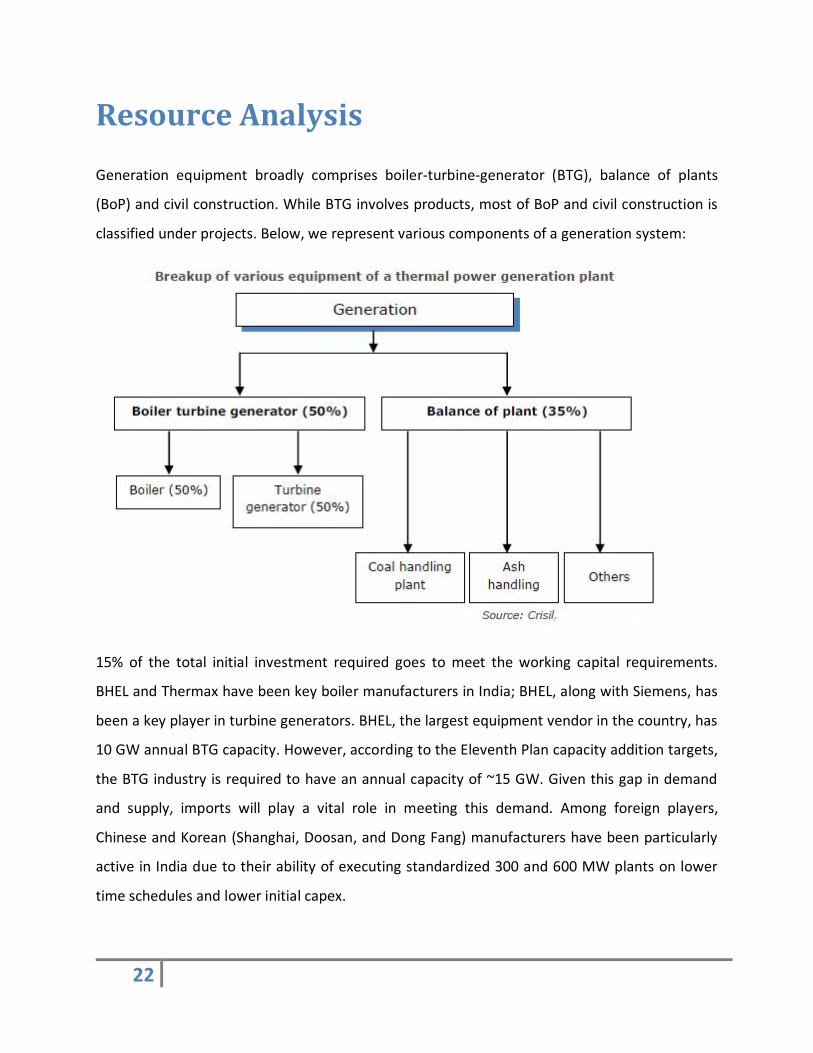

Resource Analysis

Generation equipment broadly comprises boiler-turbine-generator (BTG), balance of plants

(BoP) and civil construction. While BTG involves products, most of BoP and civil construction is

classified under projects. Below, we represent various components of a generation system:

15% of the total initial investment required goes to meet the working capital requirements.

BHEL and Thermax have been key boiler manufacturers in India; BHEL, along with Siemens, has

been a key player in turbine generators. BHEL, the largest equipment vendor in the country, has

10 GW annual BTG capacity. However, according to the Eleventh Plan capacity addition targets,

the BTG industry is required to have an annual capacity of ~15 GW. Given this gap in demand

and supply, imports will play a vital role in meeting this demand. Among foreign players,

Chinese and Korean (Shanghai, Doosan, and Dong Fang) manufacturers have been particularly

active in India due to their ability of executing standardized 300 and 600 MW plants on lower

time schedules and lower initial capex.

23

All plants commissioned after 2017 shall have to be supercritical (e.g. 660MW and above) and

to have a coal linkage. Chinese and Korean manufacturers have the capabilities to produce

supercritical.

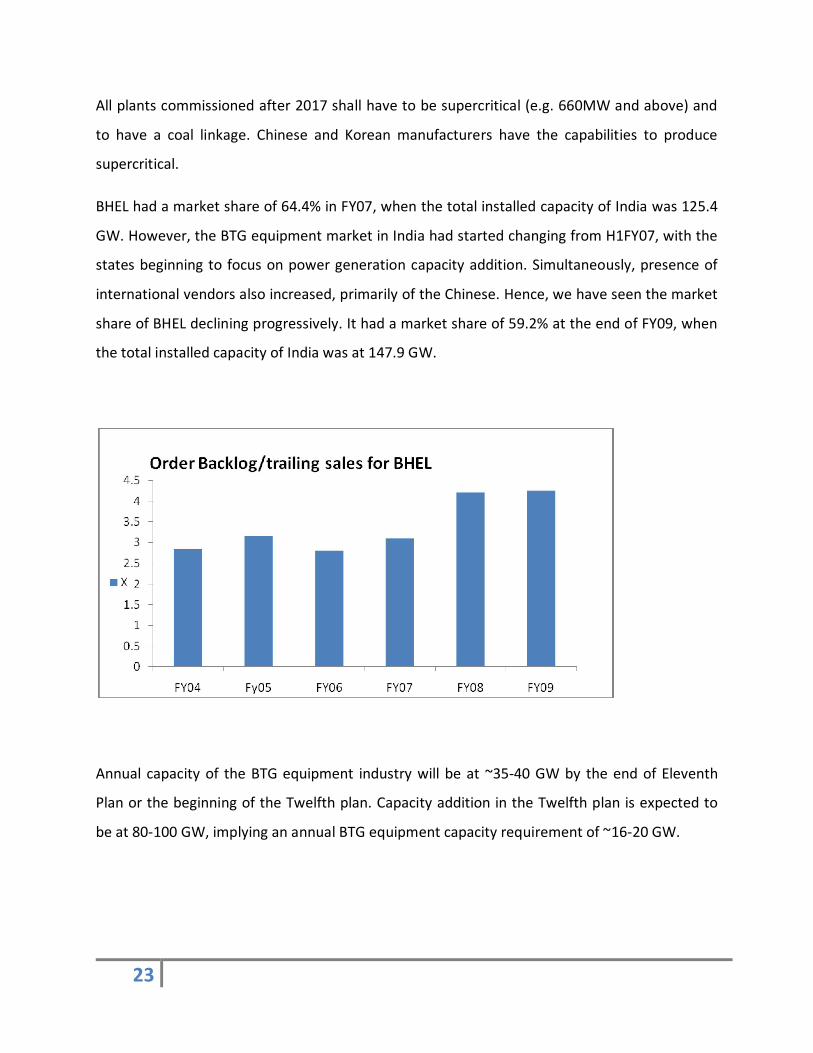

BHEL had a market share of 64.4% in FY07, when the total installed capacity of India was 125.4

GW. However, the BTG equipment market in India had started changing from H1FY07, with the

states beginning to focus on power generation capacity addition. Simultaneously, presence of

international vendors also increased, primarily of the Chinese. Hence, we have seen the market

share of BHEL declining progressively. It had a market share of 59.2% at the end of FY09, when

the total installed capacity of India was at 147.9 GW.

Annual capacity of the BTG equipment industry will be at ~35-40 GW by the end of Eleventh

Plan or the beginning of the Twelfth plan. Capacity addition in the Twelfth plan is expected to

be at 80-100 GW, implying an annual BTG equipment capacity requirement of ~16-20 GW.

24

Table 16: Details of New Entrants in BTG

Apart from the main plant equipment (BTG), balance-of-plants (BoP) and civil contractors play

an important role in execution of a power plant. In a typical power plant of INR 50 mn capex

per MW, ~INR 17-18 mn is spent across various BoP packages. As detailed below, BoP mainly

comprises the following seven packages:

25

Table 17: Main vendors for BOP

Across the seven packages, there are capacity constraints, most aggravated in the ‘ash

handling’ package.

Table 18: Capacities across BOP Packages

One of the trends observed in the BoP industry has been emergence of contractors, who take

up all the seven BoP packages and then further sub-contract them to various specialized BoP

contractors like Punj Lloyd and BGR Energy.

Coal Supply: Availability and affordability make coal the most cost-effective fuel ultra mega power project

developers. The supply of coal, however, continues to rest largely with the two public sector

26

coal mining companies - Coal India Ltd and Singareni Collieries Company Ltd, which together

meet over 80 per cent of the country's coal demand. Imported coal bridges the demand-supply

gap to some extent, but at prices which are at premiums in excess of 30-35 per cent even after

adjusting for its higher calorific value.

Though the public sector miners sell coal at regulated prices, which are at a substantial discount

to market determined (e-auction) prices and prices of comparable imported coal, the supply of

cheap domestic coal via this route is not assured. Public Sector Undertaking (PSU) miners are

obligated to supply coal to the extent of the Annual Contracted Quantity (ACQ) set in the Fuel

Supply Agreement (FSA), but are free to make up for any short-fall in ACQ by supplying

imported coal paid for by the buyer. The newly formulated FSA which PSU miners will sign with

all future consumers (except those opting for Central Electricity Authority (CEA) allocated ACQ),

has lowered the committed fuel supply from 90 per cent of the ACQ for power utilities (60 per

cent of ACQ for non-power sector industries) earlier to 50 per cent of ACQ, indicating that PSU

miners do not expect their production to catch up with demand, going forward. In such a

scenario, captive coal blocks play a crucial role in addressing the fuel security concerns of

consumers.

However, the development of captive blocks is a challenging and time-consuming process, with

a whole host of issues slowing down the timely commissioning of mines.

27

Progress on captive blocks hit by forest clearance, land acquisition hurdles Captive Blocks allotment since 1993

Source: Ministry of Coal, CRISIL Research

Progress on Captive Blocks allotted since 1993 Coal block allotment was initiated in 1993 when the Sarshatoli coal block was allotted to

Integrated Coal Mining Ltd, an RPG group company, for power generation. Coal block allocation

then picked up only in 2003 when 21 coal blocks with geological reserves of more than 1.4

billion tonnes were allotted. The period 2003 to 2008 saw a surge in block allotment with 179

blocks allotted during this period. Of all the captive coal blocks in the country, 26 currently

produce coal, nine of which are legacy blocks. However, out of the 208 coal blocks allotted

since 1993, only 17 have commenced production as of 2009-10, reflecting the dismal state of

progress on captive block development by allocatees. The principle reasons for the slow pace of

28

development are the inordinate delays in land acquisition and in obtaining environmental and

forest clearances.

Source: Ministry of Coal, CRISIL Research

Captive blocks in forest land face maximum delay in commissioning Actual mine development time (Months from date of allocation)

29

Source: Ministry of Coal, CRISIL Research Captive blocks take an average of 76 months to begin production as against the norm of 3-4

years laid down by the government. Forest clearance is the single biggest hurdle as it requires

multi-level clearances - at district, state, and union government levels. It is estimated that an

application for forest clearance has to pass through anywhere between 50-60 desks, before

approval is granted. As a result, blocks located in forest areas average 83 months to begin

production as against 72 months for non-forest blocks. Land acquisition is the second biggest

hurdle in timely commissioning of mines. Land can be acquired by a block allocatee either

through the state government or by direct negotiation with the land owners. Direct negotiation

can speed up the acquisition process as acquisition by the state government is a lengthy

process involving multiple rounds of public hearings with land owners before the land transfer

is officially notified. Underground mines commence production up to 10 months faster than

30

opencast mines, mainly because mining can commence in patches even before the entire land

earmarked for the project is acquired.

Captive coal supply to rise significantly from 2012-13 Production by captive coal mines

P: Provisional, F: forecasted Source: Ministry of Coal, CRISIL Research Blocks starting production, reserves thereof

31

P: Provisional, F: forecasted Source: Ministry of Coal, CRISIL Research

Captive production has grown at a CAGR of 16.3 per cent from 2005-06 to 2009-10 (including

production by legacy mines and in Meghalaya) reflecting the poor progress in block

development. However, expected captive production is a CAGR of 21.6 per cent from 2010-11

to 2014-15, primarily due to a quantum shift in production in 2012-13 as many of the blocks

allocated during 2003 to 2007 will commence production. Also 60 of the 208 blocks that

currently stand allocated are expected to start production by 2014-15 even after factoring in

the slow pace of captive block development.

Over the next 5 years (2010-11 to 2014-15), over 80 per cent of captive coal production will be

non-coking coal with power generation and sponge iron being the biggest beneficiaries. Within

non-coking coal, ‘E' and ‘F' grades will account for over 70 per cent of captive non-coking coal

production.

32

Private sector to dominate production, Jharkhand to top supplier states Production outlook - by sector

Source: CRISIL Research .

33

Production outlook -state wise distribution

Source: CRISIL Research

The vendor list is provided in Appendix at the end of the report.

Having given the analysis of the Electricity generation and supplier industry we are in a position

to draft the Strategic Intent of the Nigam, SWOT Analysis and strategy recommendations.

Strategic Intent Strategic intent is the hierarchy of objectives which moves from broad to narrow objectives and from long-term to short-term; this includes corporation vision, mission and corporate objectives.

34

Vision Vision statements have become fashionable for every organization. This helps galvanize energy

of stakeholders to provide support to the mission of the organization. However for many

organizations it turns into a bitter dream causing demoralization among stakeholders. This

happens because the vision is not supported by strategic plans and actions due to poor

resource base or poor resource allocation or environmental vagaries or just appear incredulous

to stakeholders. UPRVUNL will avoid this vision trap by avoiding such possible pitfalls. The

vision statement should be broad enough to capture the future diversity of actions by bearing

on internal competencies, and changing when the environment changes. We sate the vision

statement as follows:

“Act as catalyst in making Uttar Pradesh an electricity surplus state by 2018 and help energize

every electric device in the country beyond 2018”

Catalyst: This is because UPRVUNL cannot hope to accomplish the growing energy needs on its

own but by developing partnerships with many other suppliers, competitors and buyers.

Electricity surplus State: Based on the demand projections UPRVUNL will go beyond what it is

already doing today, and by other states, national and private players , it will build

collaborations and also produce on its own the future needs of the sate and the country .

Help energize every electric device in the country: UPRVUNL will not stop functioning in 2018

but will continue to add to the generation of electricity, if need be by other input methods

beyond coal: hydrocarbons, hydropower, nuclear, non-conventional sources by learning

through R&D and collaborations with technology partners; maintaining a catalytic role.

Mission

While almost every organization has a vision many do not have written statements because on

paper they look less convincing. Most firms therefore move beyond the vision and articulate

their mission statements that are more tangible, credulous and more often written. Typically

firms and corporations articulate their mission statements which drive from the vision, written

35

or unwritten. While visions are futuristic intensions, aspirations and dreams , mission seem to

reflect of either short term future direction or the businesses they operate in. The key elements

that mission statements contain are obligations to stakeholders, scope of business, sources of

competitive advantage and view of the future consistent with the long-term vision. In general

they contain the role that the company wishes to adopt for itself, a description of what the

company hopes to accomplish, a definition of the business and means to gauge the future

success. Base on these guidelines we develop below the components of the mission statements

and then a more integrative mission statement.

Obligation to stakeholders

There are many stakeholders who have stake in the business of UPRVUNL: Shareholders,

lenders, the UP Government , business partners, customers both intermediaries and

consumers, the employees of all cadres- managers, engineers, ministerial, support staff and

labor contractors, regulators, environmental groups, broad communities, and society in

general. It is important to recognize that these stakeholders benefit or get impacted by the

operation of UPRVUNL who may have conflicting interest and degree of power and may

demand management to pay more attention to the specific stakeholders group at the expense

of others. It is the role of the managers to minimize these conflicts so that their positive

energies are utilized to realize the sated vision. Obviously it must address their emotions and

their interests. We may state “we will serve each of our stakeholders amicably through a

democratic process”

Scope of Business

This defines the boundaries of the business. It is necessary to maintain focus on the business. It

should not be too narrow to miss future energy trends nor should be too broad that it loses its

direction. While it should maintain its focus on electricity generation but it cannot lose sight of

opportunities in transmission, distribution on the value chain nor could the other sources of

energy.

36

UPRVUNL will remain in the generation activity through thermal power stations using

predominantly coal and gas with oil as auxiliary feed. However it may get involved with the

generation by using other raw material like LNG and hydro electric generation as and when the

need so arises, besides working with partners in non-conventional/ renewable sources of

energy in the very long term. In the short run however, it will focus on generating energy by

using coal, which is its area of competence. Any other ventures beyond the thermal power

based on coal feed it will explore the joint venture route as and when the opportunity arises.

Thus, “UPRVUNL strives to produce and supply electric energy in the most efficient manner”

Sources of Competitive advantage

No business survives in the long-run without any competitive advantage or uniqueness.

Although electricity generation is the commodity business but the way it is supplied or

generated at the right frequency can have distinct impact on the performance, which implies

least cost production among its peer group. Since UPRVUL is still the largest producer of

electricity it would continue to do so , even better, what it is doing by building operational

excellence by encouraging, motivating and incentivizing its technical people which are

engineers of high quality, which most competitors do not have access to. This can define its

distinctiveness if it builds enabling systems for engineers to deliver their best. Therefore

smoothening the operating systems which can provide it the distinctive competence that it

needs to compete in the future competitive environment. Therefore” it will compete on the

basis of its technical core”

View of the future

“UPRVUNL will be the most efficient and one of the most responsive electric energy supplying

utility in the country with a pride in its technical core” with a leadership role in the state of

Uttar Pradesh where it will be leader in catalyzing the resources for the development of the

State .

37

Mission Statement

UPRVUNL will be leader in generating, transmitting and distributing electric energy most

efficiently through collaborations with its partners by using its technical people as its

competitive advantage while balancing and serving the interest of all of its stakeholders.

Corporate Values 1. Excellence in everything it does

2. Respectful and fair to each employee

3. Committed to nurturing of its technical talent

4. Fair to its partners

5. Will remain environmentally and socially responsible

Corporate Objectives

1. Build a strong competence in customer responsiveness by leveraging human resources through training, development and motivation

2. Expansion and growth by improving the efficiency of existing plants and adding new generation capacities

3. Reducing supply chain bottlenecks and operating costs

4. Diversifying both into vertical chain activities and diversifying the input base that lead to the leading market share

5. By taking advantage of economies of scale becoming the lowest cost generator of electricity in the state and the country

6. Partnering with other entities to minimize investment needs and reducing the investment risk

7. Becoming one of the leaders in environmental management and socially responsible citizenship in its peer group

38

In order to meet the objectives, mission, vision of the corporation, UPRVUNL needs to take

stock of its Strengths and weaknesses and assess the environmental future threats and

opportunities in order to allocate resources judiciously. There we attempt the SWOT Analysis

SWOT Analysis

Strengths 1. Ownership is with state government that reduces the risk of liquidation who can make

investment in public interest should the things turn hostile

2. It has R&D support from Central Electricity Authority keeping the research and

development costs almost zero.

3. It is easy to get land and environmental clearances from respective authority without

suspecting foul play

4. It has top management who very competent and committed who work for the

government as well as for the corporation- facilitating government support as and when

required

5. UPRVUNL has a rich history and competence of generating electricity through coal and

oil, water with priority allocation of inputs

6. The input costs are cushioned against market price vagaries and thus helps in realizing

costs through regulated tariff system

7. It has access to large real estate which is now free of cost and does not require fresh

investment with all the facilities required for a TPS like water, transport access.

8. It has the largest market share of about 50% of capacity in generation business as

compared to its competitors. The actual capacity for generation is 3933 MW as on 31st

March, 2011 after excluding unit 6 of Obra and unit no. 3 of Harduaganj

39

9. Assured market reducing the cost of marketing because of historical relationships and

scarcity of electricity. Demand is not an issue for next 10 years.

10. Most of the plants are depreciated leading to less strain on the balance sheet

11. It has the largest number of technical manpower in the state and one of the largest in

the country that is well experienced.

12. The percentage of youngsters is growing beyond 50% (about 750 out of 1450) at

executive (technical) level which are well educated , getting good training and are very

motivated

13. Corporate values are already articulated and are in place

14. Security of employment provides stability to the knowledge base which does not migrate

continuously and good compensation policy.

Weaknesses 1. Being state owned organization it suffers from slow decision making process and dealing

with less risky but expensive suppliers and buyers which also limit speed of decision

making

2. Because of SOE employees do not have commercial mindset

3. The top management comes from Government which also has its negative side: the

commitment levels are not very high because of uncertain tenure

4. Cost, quality, and schedules for “works” lowers efficiency in O&M and Project

management

5. Has already adequate input linkages

6. Three Full time directors’ positions are vacant, substituted by part time director finance,

and former technical director serving as advisor. Post of Director Personnel is vacant.

40

7. Disputes on seniority are quite frequent which delays the promotion on senior positions

since last many years lowering motivation

8. Promotions are not based on competence but other politically determined criteria

9. Old organization continue which is not consistent with today’s ground realities

10. Induction on compassionate ground has resulted in work inefficiencies and high cost

work force, which UP Government has already stopped in its own departments.

11. Roles and responsibilities are not commensurate with compensation, which are needed

to be defined and refined.

12. Deferred or partial payments by customers adversely affect the cash cycle

13. It is difficult to mobilize equity and thereby loans due to profit/loss account losses and

because government also takes very long time in implementing financial

recommendations

14. Supply of coal comes from distantly located pit heads increasing input transportation

costs.

15. Government ownership provides cushion against inefficient working resulting in lower

efficiencies.

16. Very high age of plants keeps the breakdowns as frequent resulting in lower PLF and

high input costs

17. Project implementation is a very serious drawback for lack of project management skills

and bureaucratic procedures

18. Poor contract reinforcement with equipment suppliers like the virtual monopolist BHEL

resulting into high cost and time overruns

19. Coal linkages for plants are inadequate for future needs

41

20. Aging work force has acted as a drain for long time which is addressed only recently

21. Coordination and communication processes are very slow

22. Technology enablers such as IT has only been addressed recently whose implementation

is moving at a slow pace

23. Inadequate focus on regulatory affairs. Handled at plant level instead of corporate level.

24. Auxiliary consumptions are very high compared to its competitors like NTPC

25. Political interference at the level of supplies (favored), operations- lack of proper

allocation of manpower at right jobs/ place, sub-contractors, and employees (transfers/

promotions)

26. Lower PLF compared to competitors and national average makes operations expensive.

27. It is estimated that the balance sheet may have the losses until 31st March 2010 to the

tune of Rs. 585.7 crore as per provisional balance sheet, whereas we have repayments

from customer of the same tune, therefore the interest cost without any benefits to

corporation.

Opportunities 1. BOP and BTG can be awarded through bidding system instead of single supplier as is

given to BHEL which do not adhere to timelines of the contract who do not pay

penalties for project time over runs

2. Possibility of increasing revenues through CDM, PAT( Perform, Achieve and Trade)

mechanism of BEE (Bureau of Energy Efficiency)

3. There is a good opportunity to increase the PLF close to national average of 75% thereby

raising higher generation of electricity

4. Revenues can further increased by gains from UI provisions through disciplined

management of its resources

42

5. There is going to be about 10-20% gap until 2017 in the demand and supply which will

ensure that whatever is produced is consumed- no demand risk.

6. Fuel security through JVs with mining companies

7. Productivity improvements through usage of IT applications

8. Improving financial health by setting outstanding receivables from UPPCL through inter-

department coordination

9. New projects can improve the PLF, and higher energy generation which will have

positive impact on the financial health

10. Automated equipments / super critical plants can produce higher levels of energy at

reduced prices

11. Renewable sources especially solar energy can be a good opportunity in future

especially in UP which eventually translate into more energy with lower costs.

12. Availability of land from ash ponds, which can be utilized for further expansion by

converting that land planting Jatropha plants which can be converted into diesel, and

we can earn carbon credits too.

13. Scrapping the non-functional units that are officially deleted. They can be sold out in

market and vacated land can be used for new plants eg. Obra and Harduaganj units. The

scrapped units can be sold through MMTC.

14. Scope for Joint venture exist today more because private sector has already moved in

generation and many are willing to join the business who normally do not have

experienced manpower

15. Value chain partners and competitors are willing to join forces to produce electricity like

NTPC, Coal India limited, even transmission and distribution companies.

43

16. The distribution sector is opened for participation by generation companies improving

scope for vertical integration.

17. Government, including SERC is very responsive and accommodating if willing to improve

electricity generation.

Threats 1. BTG had be given without tender to BHEL, which has become a liability because of non-

compliance of the agreement- non competitive rates and late completion of the projects

against DPR/Work Order

2. BHEL has taken advance money for R&M but may not start work even in future. which

may result in closure notice from Central Pollution Control Board and other regulatory

authorities, which may cause higher penalties and closure of old plants draining

production capacity and profitability

3. Integrity of employees, suppliers as mafias with political linkage are a serious threat to

the functioning of UPRVUNL.

4. The deregulated generation sector may see more competition in future which may

threaten the leadership position of UPRVUNL Operations.

5. New plants have long gestation periods making the progress slow towards leadership

position.

6. The aging plants underperform but maintenance cannot be done on schedule because

of demand pressure

7. Pollution control regulation is becoming more stringent under international guidelines

whose compliance can threaten closure of many units, if not acted upon in time

8. Coal mafia continues to exert pressure on the prices, quality and quantity of coal.

44

9. The constant pressure on input prices may build pressure on energy prices which

because of more competitive output may force regulator to reduce prices which may

adversely affect the expansion plans

10. Government is rather reluctant to provide additional equity required for expansion of

capacities and thus affecting expansion plans

11. The skill gap appeared because of attrition due to retirement or lack of training in ABT

regime

12. Continuing government mindset may result in serious lag in financial viability of future

investments

13. The state of monopoly has already been threatened by larger firms with adequate

investment capacity which is likely to threaten the leadership position of Nigam.

14. At some point in time the UP State may get trifurcated reducing the power of the Nigam

as happened in case of Uttrakhand

15. The stranglehold of politician may become worsen in future in curbing the freedom of

the professionally managed corporation, because of 100% ownership.

16. Increasing inflation may lead to higher interest rates, wages and cost of electricity

unless competition bring in commensurate reduction in operating costs

17. The continuous changes in the business environment makes it difficult for companies to

keep environmental knowledge undated regularly which calls for continuous learning to

which old timers are ill-equipped to handle.

Corporate & Business Strategies

We classify our recommendations into Ten broad categories: managing dynamic environment,

business portfolio, Smoothening supply chain, Operations including project management,

45

Organizational restructuring, Human Resource management, Board of Directors, Investment

management, Employee welfare and Corporate Social responsibility.

Managing Dynamic Environment

1. There is a need for a business planning Department to collect, generate and collate data

so that informed decision can be made. This unit can scan information regarding

customers, suppliers, regulatory changes, business opportunities, partnership

opportunities, Human resource related practices, new technologies, competitor

activities, political changes, social changes, economic and financial matters , pollution,

energy audit reports , related technologies , issues of sustainability.

2. This department can be headed by a Director Corporate Strategy (25-30 years

experience) trained or experienced enough in strategic Planning who may be supported

by other managers (see corporate structure) and young business analysts (2-3 years

experience with MBA degree) with some specialization in economics , statistics,

environmental engineering/ pollution control , business development, with skills in

competitor and customer analysis , a financial manager, an electrical technologist,

3. The roles will be to analyze related issues through different disciplinary perspectives and

build a comprehensive view of the issue at the planning levels. They will also be

responsible to continuously review the current business environment and suggest

future trends with respect to new emerging trends. They will assist the operating

managers on various issues including the related data/ information availability. Some of

the hard data will be stored in the computers which will be accessible to anyone who

want any relevant information. They will help set up monthly, quarterly targets, annual

targets and plans and 20 years rolling plan. They will also alert respective operating

managers about any significant changes that might affect their functions.

We have recommended this entity on environmental intelligence because the future leaders

will compete on the basis of superior knowledge and information and also we think the high

46

quality manpower is going to be the basis of competition at least for UPRVUNL as we have

recommended in the mission statement. This unit will work as a brain of the corporation.

Needless to mention that highly qualified people should be brought in or developed through

extensive training in their respective areas. It will help identify future threats and opportunities

and at the same deepen the organized and disciplined decision making which is right now in a

very ad hoc and rudimentary form.

Business Portfolio

1. The capacity additions through R&M, up rating and new capacity additions are projected

in tables 7-10 in the report.

2. Consider continuous evaluations of each generating unit which can perform above 60%

PLF with low maintenance, otherwise scrapped. We have analyzed below that the new

capacity additions are more beneficial than renovation & modernization beyond certain

performance point.

3. Any future generating unit should not be below 500 MW as the new entrants will come

with super critical plants who will threaten the leadership position of UPRVUNL. The

larger plants have higher fixed costs but lower running expenses and thus making

smaller plants or less capacity plants as unviable in 10-15 years time period.

4. Since most places land and utilities are already developed and there is ample scope of

putting up new plants which may not face demand crunch and it should help UPRVUNL

to maintain its leadership profitably at least until 2017. We need to explore new plot of

land for future expansion

5. We can consider LNG based thermal plants if the LNG linkages could be tied up in the

medium term.

6. In the meantime we also explore the nonconventional energy sources for which we can

create a new cell and recruit experienced engineers for experimentation. The special

47

interest areas could be solar energy, Jatropha plant based fuel. This may help in getting

renewable sources of energy. The technological Institutes may be made partner in R&D

beside exploring R&D based small firms or joint partners for exploring newer

technologies (0.5% of sales could be allocated to this unit on new product or process

development). They pay offs could be long-term

7. In addition we put up at least limited resources (1%of sales) in R&D and get external

consultants to assist in R&D lab to find ways and means of improving operational

efficiencies in plant which look for reduction in auxiliary consumption in operations

and examine the whole input supply chain.

8. Also the planning unit can explore possible partners who can work as partners in joint

ventures which will ease input supplies, or bring in much needed equity into new plants.

Part of employees could be shifted to the joint venture. This will give a chance to bring

in efficiencies in our own plant as the JVs can work and learn in less bureaucratic

environment away from political interference or operational fire fighting.

Smoothening Supply Chain

1. There had been major problems in getting BTG Equipment because BHEL had been a

sole supplier, which had not delivered equipments in time whether related to R&M or

new turbines, which is the major cause of concern at UPRVUNL as many projects are

delayed because of BHEL. It is suggested that both BTG and BOP supplier base must by

necessity be diversified and the tendering process strengthened. There are now

international vendors in these areas which are allowed by the government to sell

equipments in the county. We have provided some vendor addresses in the report in

the Appendix.

2. On oil supply there are not many problems as we source material from Sate owned oil

enterprises, although adulteration issues can be more rigorously monitored. However

coal supplies that reach the plants are either underweight, or of poor quality. The

48

corporation has taken many effective steps like the management has appointed agents

who can procure the coal in right quantity and quality. The supplies come from distant

places and thus reducing the quantity reached. Some coal reaches in the form of mud

due to open wagons and some reach with big stones. The corporation should further

look into the ways and means to further reduce any losses either because of quality,

quantity or transportation issues. It is recommended that a committee of procurement

managers/ engineers representing each plant is constituted which will make further

recommendations on the issue.

Operations including project management

1. Barring a few plants, there is more focus on administration by the engineers than on

engineering work resulting into poor operations management. There are multiple

vendors in the same plant and across different plants. It is suggested that this function

be centralized and engineers are relieved from administrative functions as much as

possible. There must be a single vendor development department for “works” at the

plant level under the direct supervision of the Chief of the plant. The tender must be

invited through UPRVUNL website in order to reduce the impact of local political

influence. The vendor should also be empanelled. There should also be a head office

representative in the vendor selection committee at the plant level

2. Inventory and store systems should be computerized and proper system established so

that the items can be identified easily. This can be automated with the help of inventory

order system available from many vendors. Physical verification each year should be

carried out regularly and physical stock reconciled with the database.

3. ERP needs to be implemented urgently so that data is available for informed decision

making. It calls for an experienced vendor especially with organizations in electricity

generation. The store/purchase employees should be trained in IT applications for store

and purchase.

49

4. Ash disposal is a major concern around the plants. It is suggested that like NTPC regular

auction be carried out. The neighborhood cement manufacturing companies/ road

construction companies should be invited to submit tenders/ bids.

5. The major concern as witnessed during plant visits and also the review of performance

of plants indicate that the project management is the weakest link in spite of the fact

many managers are interested in getting job posting in these departments., resulting

into delays and higher costs. Since the corporation is expanding operations there is a

need to create a special group properly experienced in electricity generation and project

management techniques in order to keep good control on cost and time over runs. Since

projects are left to operating managers who are busy firefighting operational glitches

especially in the light of aging plants, cannot pay adequate attention to the progress of

projects and thus it must be separated.

6. Although utilities maintenance is found to be reasonably all right except ash disposal,

There is need for continuous improvements after setting standards for each activity,

including, water, land, roads, electrification, hospitals. Schools etc in proper form.

7. The bench mark studies against CEA norms and/or NTPC comparable plants indicate

that most of UPRVUNL plants are underperforming: PLF, availability factor, Station Heat

Exchange Ratio, Auxiliary consumption, outages; which have adverse impact on the

cost/ MU and also the profitability of the corporation. The reasons of course are old

plants, poor execution of R&M, O&M and delayed projects for up rating or new capacity

additions. The targets must be revised upward. As a thumb rule there ought to be at

least 2-3% improvement in each operational parameter with 2010-11 as base year. We

expect until 2017 an improvement of 12-15% over the base year. The same can be

translated into each plant and unit so that disaggregated targets can be set. Needless to

mention that in addition to enabling corporate environment, including, restructuring of

organization, cadres, smoothening supply chain; monetary incentives be linked with the

weighted average of PLF, Auxiliary consumption, SHR, Outages with 40%, 30%, 20%,

50

30%. If the savings are indeed achieved which may have impact of 8-10% every year.

The cash incentives of 1-2% of the savings or growth may be passed on to employees

8. The main reasons of lower performance are the aging plants, lower machine loads,

forced outages, high auxiliary consumption, Station Heat Rate, and also because of slow

progress of R&M due to lack of structural focus and non-supply of equipments by BHEL,

who go scot free without penalties . Serious competition among vendors be introduced

by inviting tenders from international suppliers

9. Energy accounting and billing are still weak areas and there is something to learn from

NTPC. That is why beside organizational and cadre restructuring, training and

development are emerging key thrust areas especially Strategic management, HR,

financial and project planning and implementation.

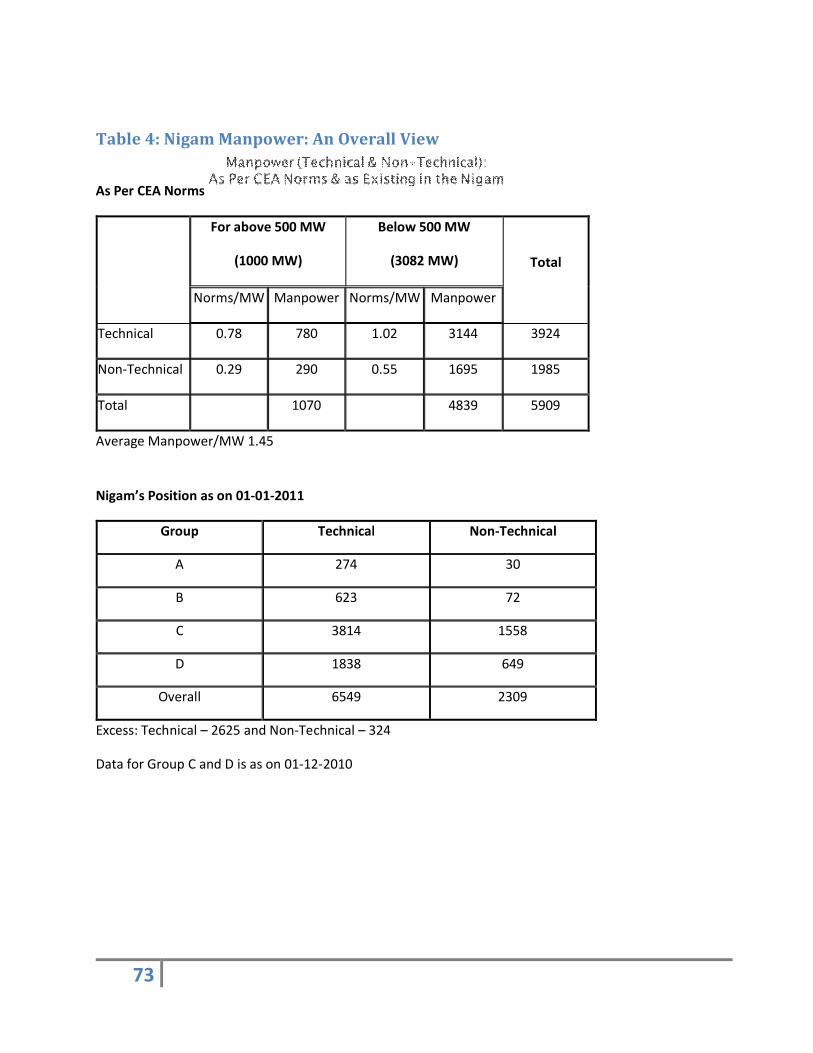

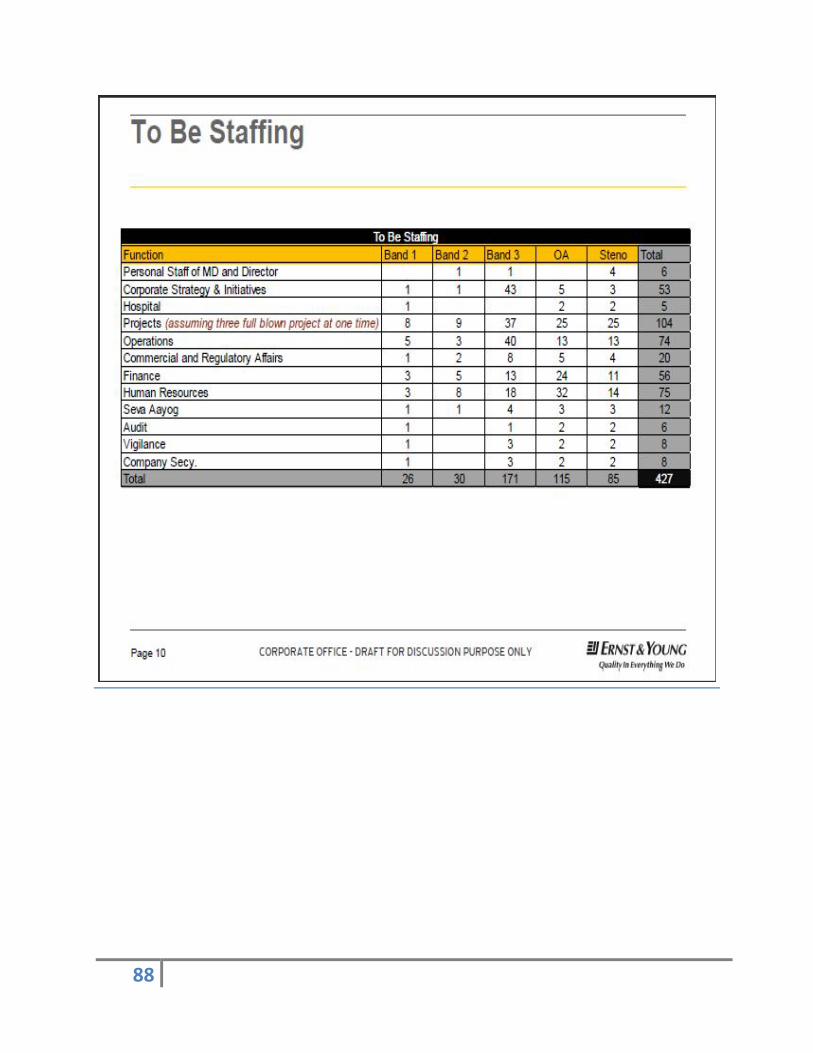

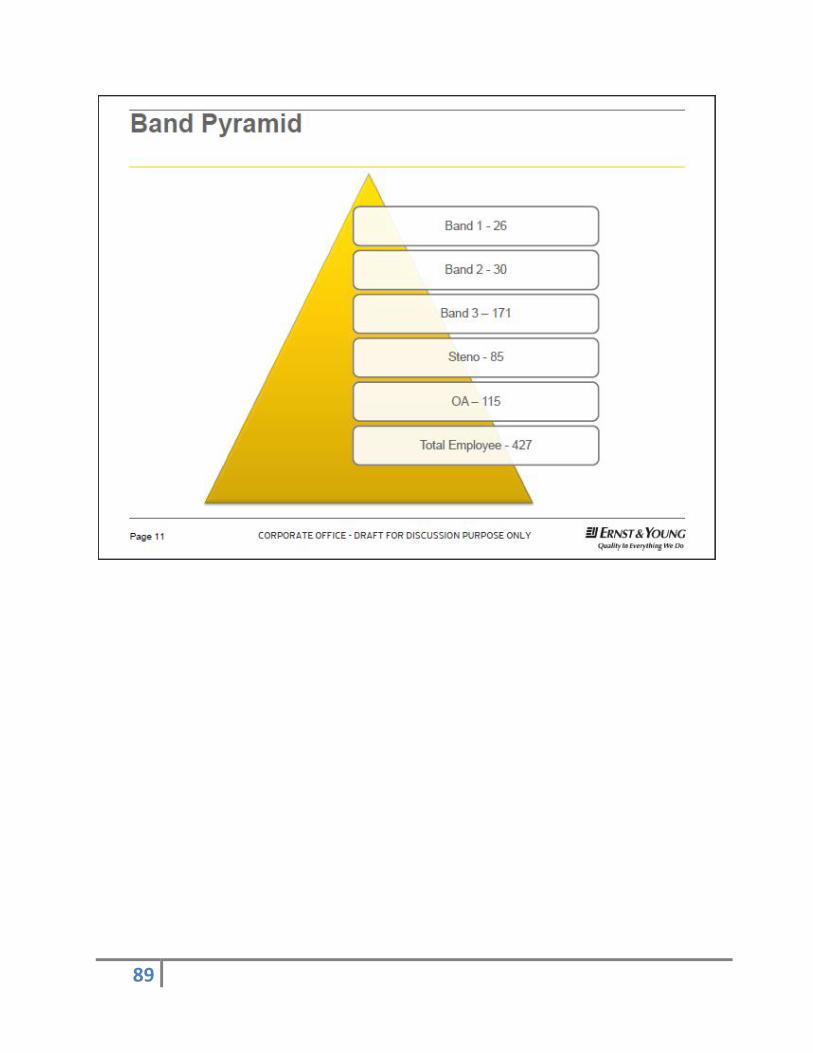

Human resource management

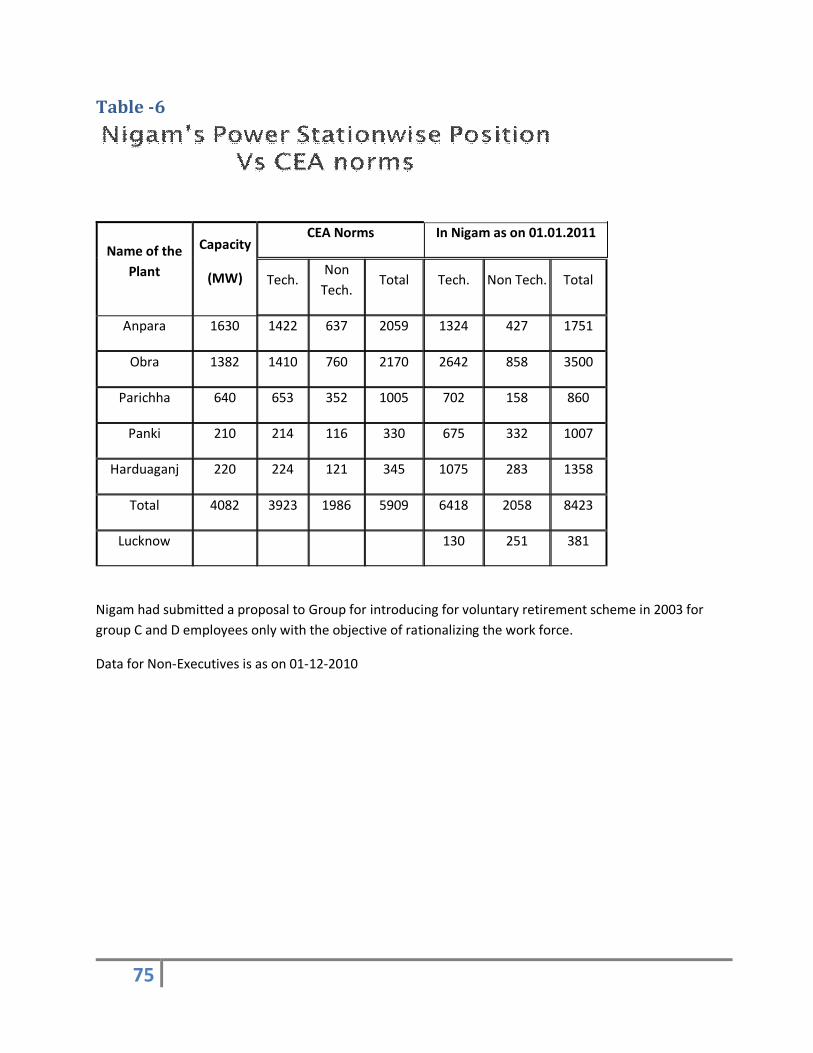

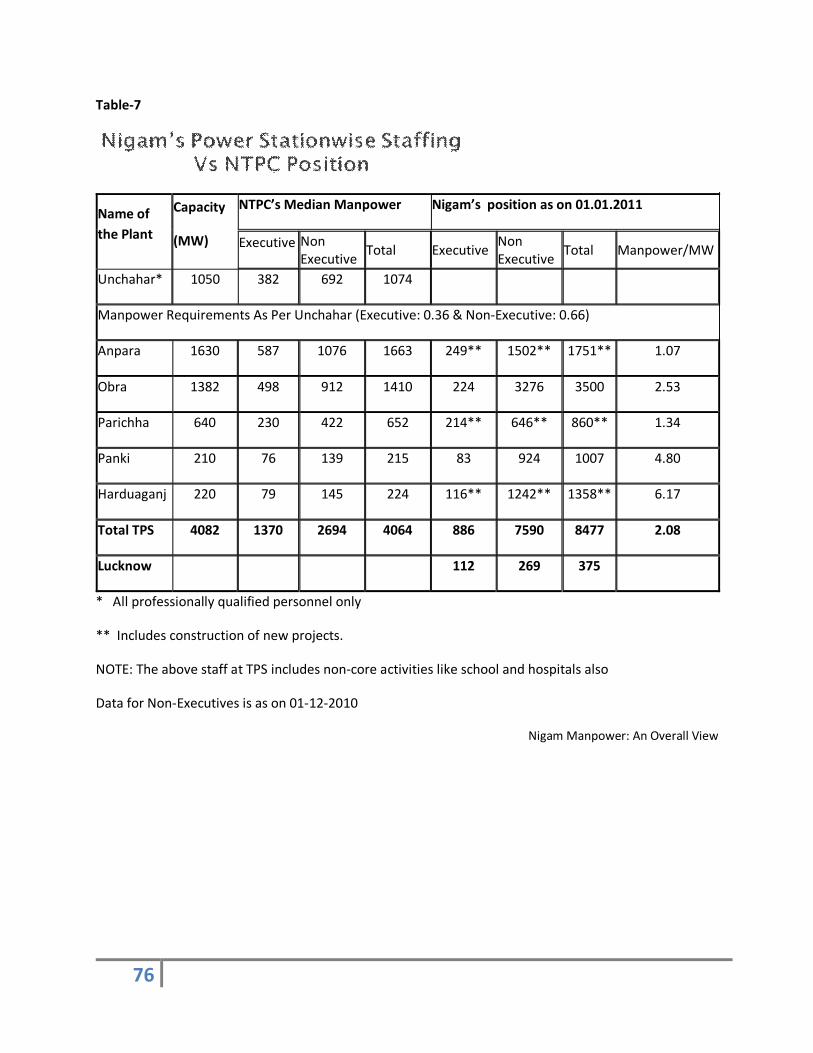

The analyses carried out by the HR department of the Nigam (the tables are placed in Annexure II) indicate excess manpower by any standard. The major concerns indicated are

1. Many units are deleted (Panki 2 units, Harduaganj 4 units, and Obra 3 units) but the

positions have not been scrapped. Contrarily some of the new units are established: 2

units are Paricha and 2 units at Hurduaganj. The new positions are not created inducing

murkiness in the manpower allocation. This notwithstanding the CEA norms are

available beside NTPC benchmarks (see Annexure II)

2. Similarly positions required for new tasks have not been articulated: HR, Fuel, R&M,

Environment, IT and commercial. These entities are working against positions

sanctioned under PPMM, thermal operations and plants which are needed to be

regularized. The commissioning staff required for new projects has not been provided

with new positions sanctioned.

51

3. There are shortages in technical cadres as against the support staff. Although there

appears to be shortage against the sanctioned staff across board but many units have

been closed down.

4. There is a lack of role clarity at different levels some of which is caused by the number

of employees working against the sanctioned strength drawing salaries with lower level

designations, known as Resultant Seniority concept . There is lack of specialization. No

clear cut policy exists besides the relative disliking for operational jobs as against project

jobs. This requires job restructuring of work which is being currently carried out by E&Y

Consultants

5. Engineering staff is dominated by non-degree holders due to promotions.

6. The appraisal system does not reflect the actual performance which is more driven by

human concerns and relationships rather than contributions, partly affected by internal

political influences.

7. There is a need to redesign the cadres followed by role analysis and competence

mapping study to find gaps and transfer employees after retraining for right jobs. To

minimize discontent among educationally well qualified personnel the assessment of

educational background and promotions linked to proper appraisal based on

competence mapping profile and actual performance should be introduced.

Introduction of a block/ cadre system like E-1,E-2, E-3, E-4 AND E-7 and E-8 and above,

to provide flexibility in promotions. Cadre restructuring can be inspired by the system

implemented at NTPC

8. Training programmes should be organized according to the competence assessment and

training gap thereof with respect to hard and soft skills, including leadership