finacial management

TRANSCRIPT

Chapter 5

FINANCIAL

MANAGEMENT8 marks

Sagar Vetal | E &TC | GGSP

Topics

1. Financial Management

-Objectives & Functions

2. Capital Generation & Management

- Types of capital

- Sources of raising the finance

3. Budgets and accounts

- Types of Budgets

- Profit, Loss accounts & Balance sheet

4. Types of taxes

Sagar Vetal | E &TC | GGSP

5.1 Financial Management

Defination:

“It is study of relationship between

raising the finance and the deployment

of finance.

”Sagar Vetal | E &TC | GGSP

5.1.1 Objectives of Financial Management

- To raise the funds

- To allocate funds properly

- To reduce the misuse of funds

- To maximise the profit in long run

- To maximise the value of the compony

- To fulfill the social responsibility

- To maximize the profit of shareholders

Sagar Vetal | E &TC | GGSP

5.1.2 Function of Financial Management

⊸ Understand and estimate the capital requirement

⊸ Determination of Capital composition

⊸ Choosing sources of funds

⊸ Allocation of funds

⊸ Investment of funds

⊸ Managing of fixed assets (Infrastructure, Machines, etc.)

⊸ Managing of woking capital( Capital for day-to-day

operations)

⊸ Management of cash flow

⊸ Management of earning (profit is distributed to all

shareholders, called divident)

Sagar Vetal | E &TC | GGSP

5.2 Capital

⊸ Capital means each an every element that that

required by busunessman needs to start an

enterprise.

⊸ e.g. money, land, building, machinery, material,

etc.

⊸ It is a measure of amount of resources of an

enterprise

⊸ Also known as Life-blood of business

⊸ It is lubricant that keeps enterpise dynamic

Sagar Vetal | E &TC | GGSP

5.2 Types of Capital

5.2.1 Fixed Capital (Block Capital)

⊸ Capital associalted with long term asstes

⊸ Assets which are used over and over again for a

number of years

⊸ e.g. Building

Equimpments and machinary

Tools

Furniture

Sagar Vetal | E &TC | GGSP

5.2 Types of Capital

5.2.2 Working Capital

⊸ Capital required for day-to-day needs and

expenditures⊸ e.g. - Purchase of raw material and supplies

- Payment of employees

- Storage cost

- Equipment and plant maintenance cost

- Transportation and shipping expenses

- Expenditure during the time lag between the

sale of the product and payment for them.

Sagar Vetal | E &TC | GGSP

5.2 Types of Capital

5.2.2 Working Capital⊸ Net Working capital= total assets – current liabilities

⊸ Working capital management refers to managing both

total assets and current liabilities

⊸ Sources:

- Funds from business operations

- Dividents, donations, interest from investment made in

other companies

- sale of useless fixed assets

- long term borrowing

Sagar Vetal | E &TC | GGSP

5.2 Sources of finance

1. Internal Sources

2. External Sources

a. Permanent or long term sources

b. Medium term sources

c. Short term sources

d. Specialist Institutions

Sagar Vetal | E &TC | GGSP

Sources of finance

1. Internal Sources

1.1 Retained Equity Earning

retaining of earning of shareholders for

internal investments

1.2 Depreciation Provision

Old machinery has less amount of tax

(e.g. Car Insurance)

1.3 Deferred Taxation

Relaxation in taxes if time lag between the

earning of profit and payment is more, In this

case profit in balance sheet less, less amount,

so less tax

1.4 Personal Funds saved or inherited

Sagar Vetal | E &TC | GGSP

Sources of finance

2. External Sources

a. Permanent or long term sources of finance

- Sources raised for the period of more than 10 years

i. Savings: Life insurance, shares, mutual funds, bonds, fixed

deposits

ii. Loans: From friends and relations, money lending institutes,

banks

iii. Shares: issuing shares to investors in return of cash

iv. Public Deposits: deposits or loans collected from general

public, employees and shareholders

v. Adding partner to businessSagar Vetal | E &TC | GGSP

Sources of finance

2. External Sources

a. Permanent or long term sources of finance

vi. Debentures: - Debentures is certificate of indebtedness issued by corporations

- Investment is similar to shares but unlike shareholders debenture

holders has no control over affairs of the company

- Shareholders paid dividend, debenture holders paid a fixed rate of

interest over a stated number of years in debentures

- Debentures are paid weather company is in profit or loss

- Liquidation: debentures gets their money first

vii. Corporate bonds- Unsecured bonds: also known as debentures

- Secured bonds: claim on assets of corporations if they failed to

pay interest

Sagar Vetal | E &TC | GGSP

Sources of finance

2. External Sources

b. Medium term sources of finance

- finance raised for a period of more than 1 year

i. Bank Loans

ii. Hire Purchase: buying goods in installments

iii. Sale and lease back: For getting funds, sell some if the

property with rights to lease back at agreed rent.

iv. Equipment leasing

v. Profit plowback : Whole profit is not distributed to shareholders

as dividend, rather a portion of it is retained in business and used

for growth and finance expansion Sagar Vetal | E &TC | GGSP

Sources of finance

2. External Sources

c. Short term sources of finance

- finance raised for a period of less than 1 year

i. Credit facilities: Obtain goods and services on credit

ii. Trade credit: Purchase goods without paying cash or paying

the supplier at later time

d. Financial Institutions

- finance may be obtained by borrowing from

i. Insurance Company

ii. Investment company

iii. Industrial development corporationsSagar Vetal | E &TC | GGSP

Sagar Vetal | E &TC | GGSP

5.3 Budget

Defination:

“It is an instrument of management used as an aid

in planning, programming and control of business

activity.”

It is a written plan of action, includes financial

requirement of different sections of the business for

a specific duration to achieve an estimated profit

Sagar Vetal | E &TC | GGSP

5.3 Budget:Objectives of budget

1. It should specify units to be produced, precies size, style,

and cost of production

2. It should analyze all the factors affecting the department

as well as business

3. It should help in removing waste and raise profit of the

business

4. Prediction about capital expenditure for future

5. It should help in coordiantion among departments,

stabilizing the production

Sagar Vetal | E &TC | GGSP

5.3 Budget:Advantages of budget

1. Polcy, plans and actions taken are all reflected in bugdet

2. Target, goals and policies of business are clearly defined

3. Better understanding, coordination in business, as all are

takes part in budget preparation

4. It provides management a guide for their current, future

spending’s

5. It facilitates finance control

Limitations:1. Budget is based on estimations, it may need periodic

revision, as estimation may not cent per cent true.

2. Budget may not work properly if the idea of budgeting is not

properly understood by all department

Sagar Vetal | E &TC | GGSP

5.3 Budget:

Types of budget

1. Fixed Budget:

A fixed or static budget shows one plan, one volume of

output or sales and the related fixed cost

It depends upon the ability to predict income, sales with

accuracy and no provision is made for any changes that

may occur during the budget period

E.g. research project, hospitals, schools and collages, etc.

Sagar Vetal | E &TC | GGSP

5.3 Budget:

Types of budget

1. Fixed Budget:

Sagar Vetal | E &TC | GGSP

5.3 Budget:

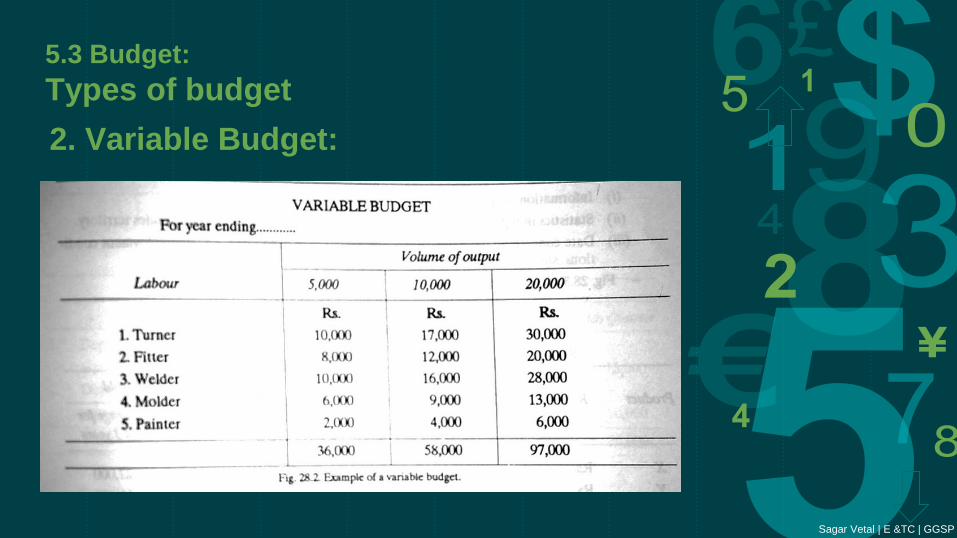

Types of budget

2. Variable Budget:

A variable or flexible budget recognizes the unreliability of

income or sales predictions and makes provision in advance

for variation in production and expenditure in accordance

with the variation

It shows the range of volumes or sales or cost for each

spending’s

Variable budget takes account only those cost which varies

the output and over which department has control over it.

Sagar Vetal | E &TC | GGSP

5.3 Budget:

Types of budget

2. Variable Budget:

Sagar Vetal | E &TC | GGSP

5.3 Budget:

Types of budget

Production Budget

⊸ Prepared by production manager

⊸ It includes quantity of product to be manufacture based on

- Sales budget

- Factory Capacity

- Stock Requirement

- Availability raw

⊸ Production budget is a part of manufacturing budget

⊸ Manufacturing budget helps in keeping production at even rate

And controlling the use of labor, material, equipment, etc.

Sagar Vetal | E &TC | GGSP

5.3 Budget:

Types of budget

Production Budget:It incudes estimated volume of production, division of estimated output into types of

product, scheduling of operation by month and quarters, etc.

Sagar Vetal | E &TC | GGSP

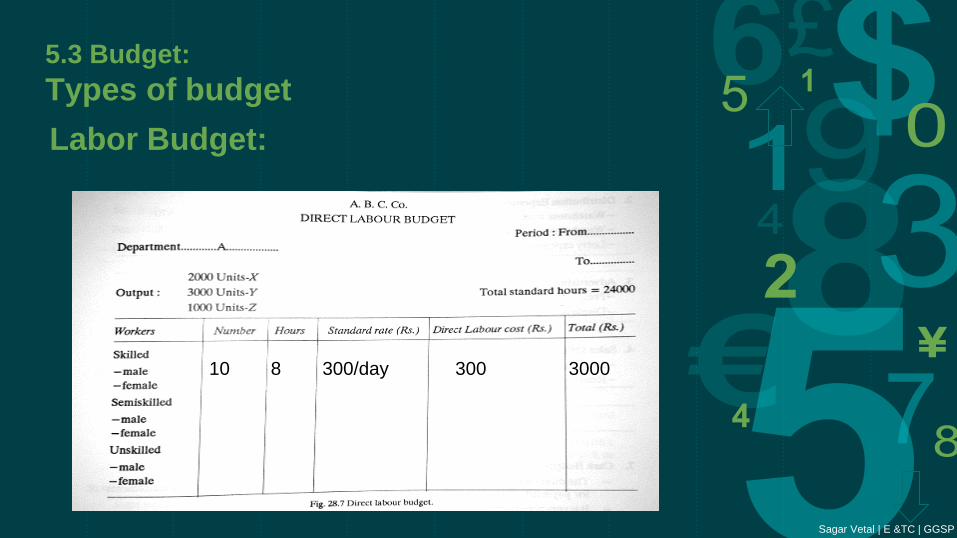

5.3 Budget:

Types of budget

Labor Budget⊸ It contains an estimation of labor required to manufacture the product

shown on production budget

⊸ How to calculate labor requirement

i. Split the product into operation

ii. Using work study calculate the standard time for each

operation

iii. from step (ii), calculate total no. of hours required for

production

iv. Convert hours into labor requirement

⊸ While Preparing labor budget following this are considered

- Calculation of ma power requirement's for the department,

determine the grade(i.e. male or female) and the number of

workmen/worker

- Set standard wage rate for workmen

Sagar Vetal | E &TC | GGSP

5.3 Budget:

Types of budget

Labor Budget:

10 8 300/day 300 3000

Sagar Vetal | E &TC | GGSP

Tax

“A fee charged by govt. on product, income or service

is called Tax.”

Why Govt. needs tax

- Administration service

- Defense service

- Police for maintenance of law and order

- Judicial courts for administration of justice

- Schools and collages for giving education to people

- Hospitals for preservation of health, etc.

Principles of taxation

• Taxation should be equal

• Taxation should be certain/fix

• Taxation should be timely

• Taxation should be economical to collectSagar Vetal | E &TC | GGSP

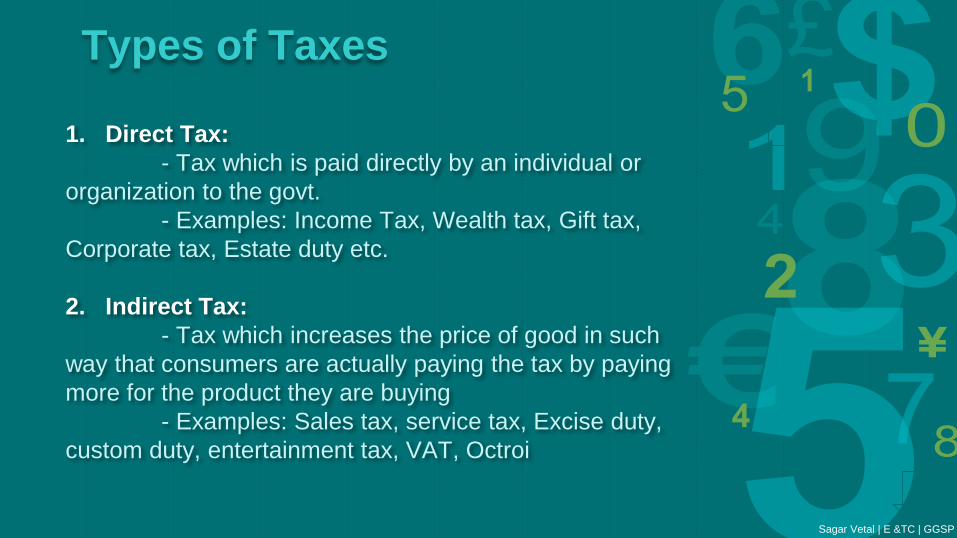

Types of Taxes

1. Direct Tax:

- Tax which is paid directly by an individual or

organization to the govt.

- Examples: Income Tax, Wealth tax, Gift tax,

Corporate tax, Estate duty etc.

2. Indirect Tax:

- Tax which increases the price of good in such

way that consumers are actually paying the tax by paying

more for the product they are buying

- Examples: Sales tax, service tax, Excise duty,

custom duty, entertainment tax, VAT, Octroi

Sagar Vetal | E &TC | GGSP

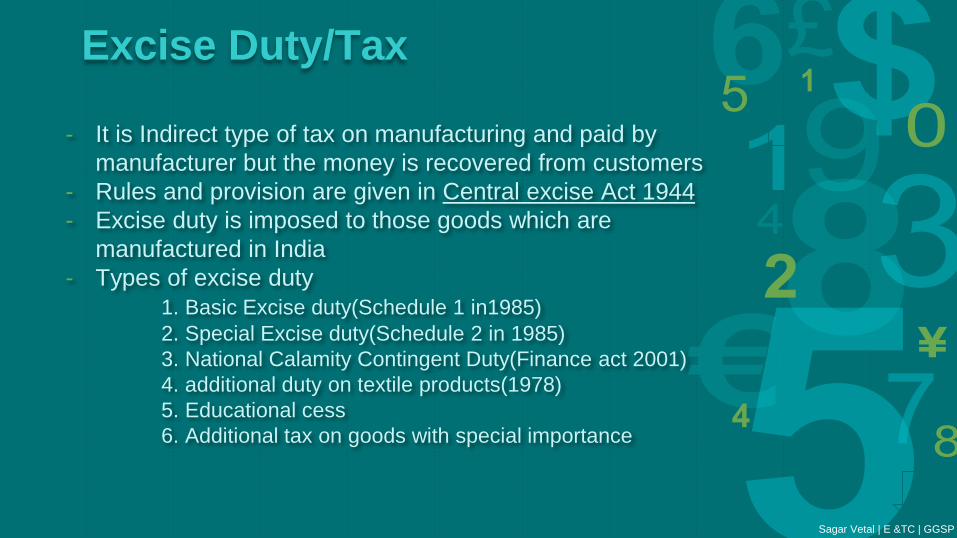

Excise Duty/Tax

- It is Indirect type of tax on manufacturing and paid by

manufacturer but the money is recovered from customers

- Rules and provision are given in Central excise Act 1944

- Excise duty is imposed to those goods which are

manufactured in India

- Types of excise duty

1. Basic Excise duty(Schedule 1 in1985)

2. Special Excise duty(Schedule 2 in 1985)

3. National Calamity Contingent Duty(Finance act 2001)

4. additional duty on textile products(1978)

5. Educational cess

6. Additional tax on goods with special importance

Sagar Vetal | E &TC | GGSP

Service Tax

- It is indirect type of tax imposed on services provided by an

entity

- Service tax rate: 14% since April 2015

- It is exempted for small scale service provides if total value

of service provided by them is during a year is less than 10

lakh

- VAT is the Indirect type of tax, imposed on the sale of

movable goods

- VAT is multipoint destination taxation system, where tax is

imposed on value addition at each stage of transaction in

production or supply chain

- State govt. responsible for imposing and collection of tax

VAT(Value added Tax)

Sagar Vetal | E &TC | GGSP

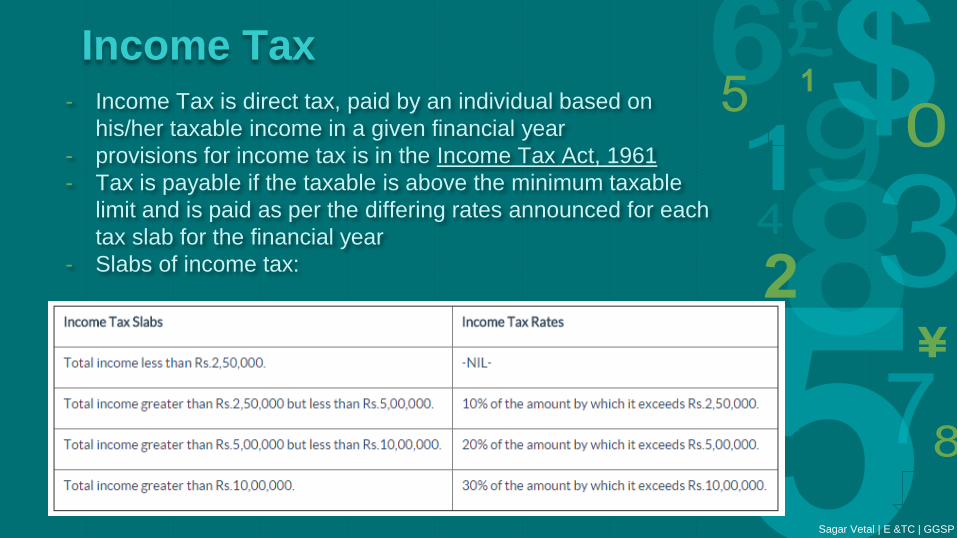

Income Tax- Income Tax is direct tax, paid by an individual based on

his/her taxable income in a given financial year

- provisions for income tax is in the Income Tax Act, 1961

- Tax is payable if the taxable is above the minimum taxable

limit and is paid as per the differing rates announced for each

tax slab for the financial year

- Slabs of income tax:

Sagar Vetal | E &TC | GGSP

Custom Duty

- Custom duty is the tax on import or export of goods

- It controls the flow of goods including animals, personal

artifacts, hazardous items in and out of country

- Custom duty includes

- Import Duty

- Export Duty

HomeWork:- Profit and loss account

- Balance sheet

Sagar Vetal | E &TC | GGSP

Thanks!Any questions?

Referance:

Industrial Engineering and Management

- O. P. Khanna

Sagar Vetal | E &TC | GGSP