fin500j topic 5 1 fall 2010 olin business school fin500j: mathematical foundations in finance topic...

TRANSCRIPT

Fin500J Topic 5 1Fall 2010 Olin Business School

Fin500J: Mathematical Foundations in Finance

Topic 5: Numerical Methods for Optimization

Philip H. DybvigReference: Optimization Toolbox User’s Guide in Matlab, 2008 by the

MathWorks, Inc.Slides designed by Yajun Wang

x

f(x)

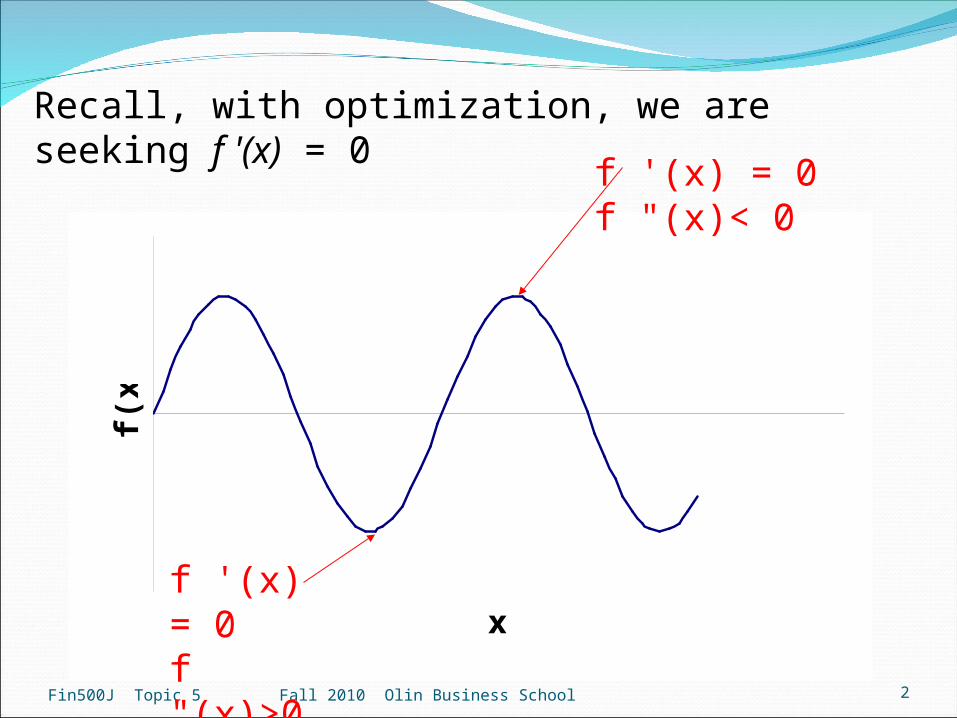

Recall, with optimization, we are seeking f '(x) = 0

Fin500J Topic 5 2Fall 2010 Olin Business School

f '(x) = 0f "(x)< 0

f '(x) = 0f "(x)>0

10sin2)(

2xxxf Find the maximum of

Fin500J Topic 5 3Fall 2010 Olin Business School

05

cos2)(' x

xxf

To solve the root problem for

and the second condition is satisfied at the root

05

1*sin2*)('' xxf

Fin500J Topic 5 Fall 2010 Olin Business School 4

-6 -4 -2 0 2 4 6-5

-4

-3

-2

-1

0

1

2

x

y=2s

inx-

x2 /10

We can solve f '(x) =0 by Bisection using initial interval [1,2], Newton’s with initial point 1.2 or Secant method with initial points 1.2 and 2 presented in Topic 3.

We can also solve it in Matlab.

>> f=@(x) 2*cos(x)-1/5*x;

>> fzero(f,[1,2]) ans =1.4276

Objectives : Using Optimization Toolbox in Matlab to

Solve unconstrained optimization with multiple variables

Solve linear programming problemSolve quadratic programming problem (for example:

optimal portfolio)Solve nonlinear optimization with constraintsMostly, we will focus on minimization in this topic,

max f(x) is equivalent to min –f(x)

Fin500J Topic 5 5Fall 2010 Olin Business School

Linear Programming/Quadratic Programming/Nonlinear Programming

If f(x) and the constraints are linear, we have linear programming

If f(x) is quadratic, and the constraints are linear, we have quadratic programming

If f(x) in not linear or quadratic, and/or the constraints are nonlinear, we have nonlinear programming

Fin500J Topic 5 6Fall 2010 Olin Business School

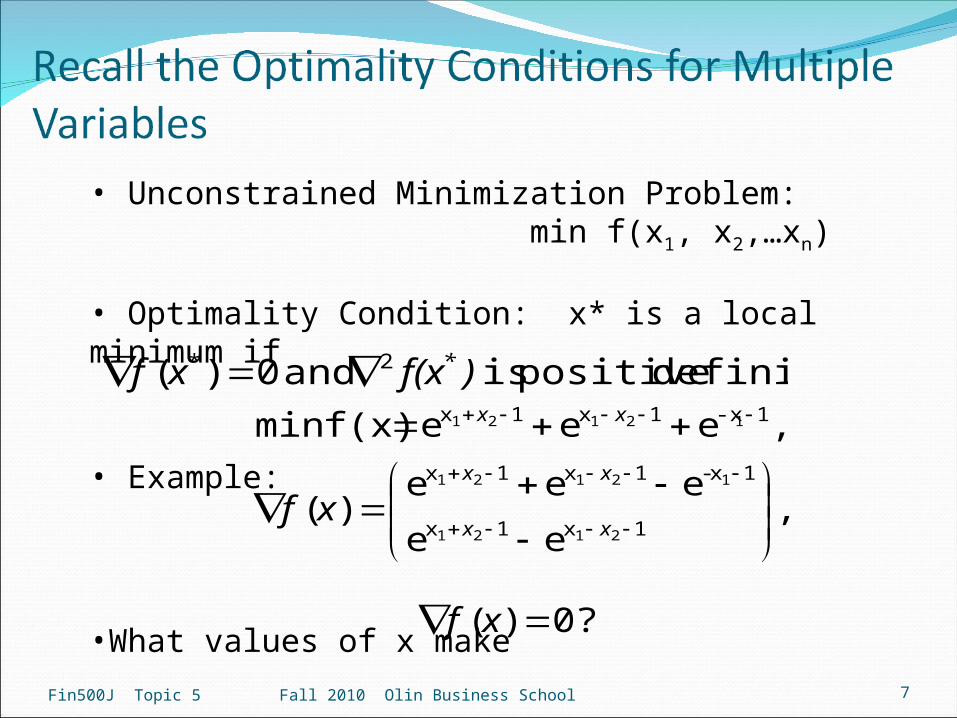

• Unconstrained Minimization Problem: min f(x1, x2,…xn)

• Optimality Condition: x* is a local minimum if

• Example:

•What values of x make

Fin500J Topic 5 7Fall 2010 Olin Business School

definite. positive is and 0)( 2* )f(xxf *

,ee

eee)(

,eeef(x)min

1x1x

1x-1x1x

1-x1x1x

2121

12121

12121

xx

xx

xx

xf

?0)( xf

Fin500J Topic 5 Fall 2010 Olin Business School 8

Step 1: Write an M-file objfun.m and save under the work path of matlab

function f=objfun(x) f=exp(x(1)+x(2)-1)+exp(x(1)-x(2)-1)+exp(-x(1)-1);

Step 2: >>optimtool in the commend window to open the optimization toolbox

Fin500J Topic 5 Fall 2010 Olin Business School 9

We use the function fminunc to solve unconstrained optimization problem “objfun”

Fin500J Topic 5 Fall 2010 Olin Business School 10

).()(-x

:case variableMultiple.)(

)(x

)()()()(

12

''

'

'''''

kk

k

k

kkkk

xfxf

xf

xf

x

xf

x

xfxxfxf

Fin500J Topic 5 Fall 2010 Olin Business School 11

Newton’s method may fail if Hessian is not positive definite

Fin500J Topic 5 Fall 2010 Olin Business School 12

The function “fminunc” uses BFGS (Broyden, Fletcher, Goldfarb and Shanno) Hessian Update in the Quasi-Newton algorithm. The formula given by BFGS is

Fin500J Topic 5 13Fall 2010 Olin Business School

Both the objective function and the constraints are linear

Example: maximizing profit or minimizing costObjective function Max or Min Z = c1x1 +c2x2 +…..cnxn

where cj = payoff of each unit of the jth activity xj = magnitude of the jth activityThe constraints can be represented by ai1x1 +ai2x2+…..ainxn bi

where aij = amount of the ith resource that is consumed for each

unit of the jth activity, bi = amount of the ith resource available

Finally, we add the constraint that all activities have a positive value, xi 0

Total Profit = 150 x1 + 175 x2

Maximize Z = 150 x1 + 175 x2Objective function

Resource Regular Premium Resource Availability

120

Storage 9 6(tonne)

Profit (/tonne) 150 175

77

10 8

Product

Raw Gas

(m3/tonne)

Production Time (hr/tonne)

7 11

Fin500J Topic 5 14Fall 2010 Olin Business School

x1 = amount of regular and x2 = amount of premium

7x1 + 11x2 77 (material constraint)10x1 + 8x2 120 (time constraint)x1 9 (storage constraint)x2 6 (storage constraint)x1,x2 0 (positivity constraint)

(5) x1,x2 0

Fin500J Topic 5 15Fall 2010 Olin Business School

(1) 7x1 + 11x2 77→x2 -7/11 x1 +7

(2) 10x1 + 8x2 120→ x2 -5/4x1 + 15

(3) x1 9

(4) x2 6

Now we need to add the objective function to the plot. Start withZ = 0 (0=150x1 + 175x2)and Z = 500 (500=150x1 + 175x2)

Fin500J Topic 5 16Fall 2010 Olin Business School

Z=1200Z=1550

Still in feasible regionx1*= 9x2* 1.5

Fin500J Topic 5 17Fall 2010 Olin Business School

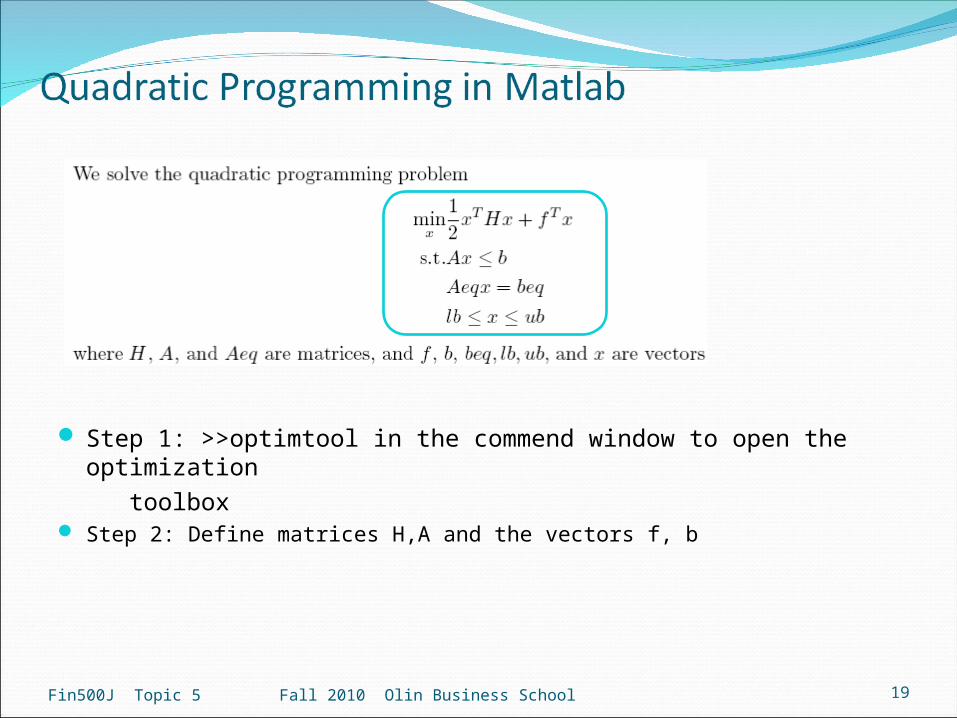

Step 1: >>optimtool in the commend window to open the optimization

toolbox Step 2: Define matrices A, Aeq and

the vectors f, b, lb, ub

Example:

Fin500J Topic 5 18Fall 2010 Olin Business School

File->export to workspace

can export the results including lambda,etc.

Fin500J Topic 5 19Fall 2010 Olin Business School

Step 1: >>optimtool in the commend window to open the optimization

toolbox Step 2: Define matrices H,A and the vectors f, b

Fin500J Topic 5 20Fall 2010 Olin Business School

Fin500J Topic 5 21Fall 2010 Olin Business School

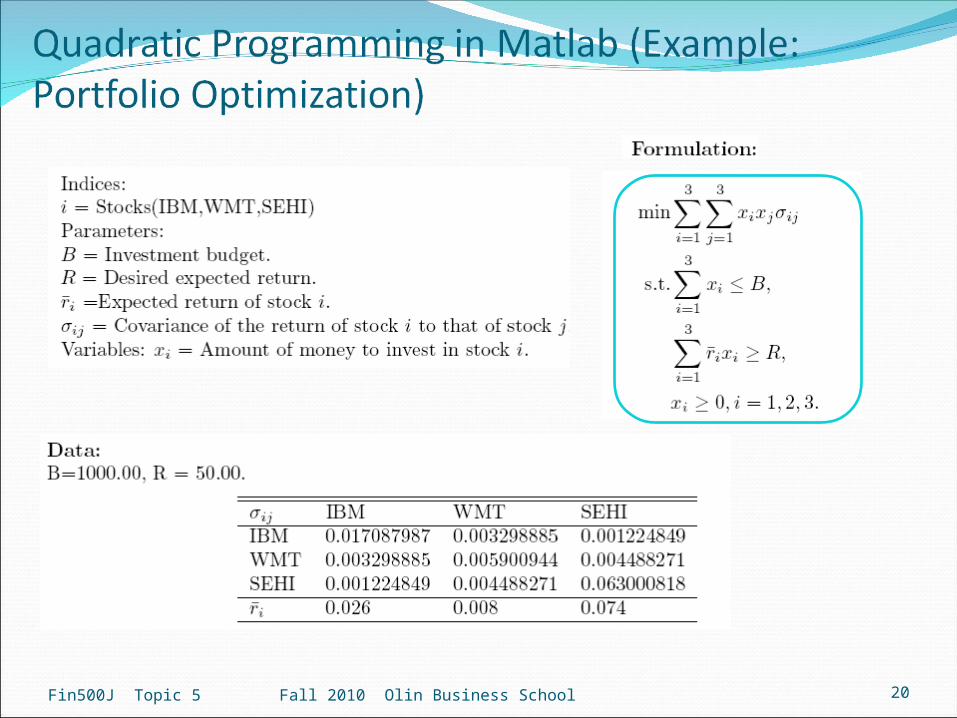

H=[0.017087987 0.003298885 0.001224849; 0.003298885 0.005900944 0.004488271; 0.001224849 0.004488271 0.063000818]

f=[0; 0; 0]A=[1 1 1; -0.026 -0.008 -0.074;

-1 0 0; 0 -1 0; 0 0 -1]b=[1000; -50; 0; 0; 0]

The function ‘quadprog ’ uses an active set strategy. The first phase involves the calculation of a feasible point. The second phase involves the generation of an iterative sequece of feasible points that converge to the solution.

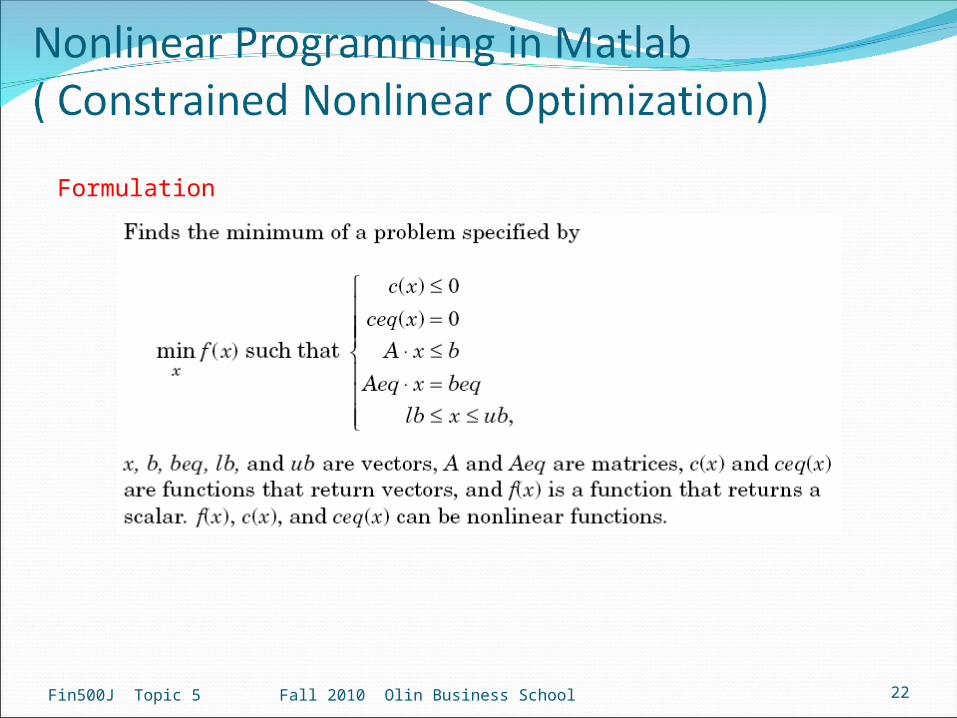

Fin500J Topic 5 22Fall 2010 Olin Business School

Formulation

Fin500J Topic 5 23Fall 2010 Olin Business School

Find x that solves

Step 1: Write an M-file objfunc.m for the objective function. function f=objfunc(x) f=exp(x(1))*(4*x(1)^2+2*x(2)^2+4*x(1)*x(2)+2*x(2)+1);

Step 2: Write an M-file confun.m for the constraints. function [c, ceq]=confun(x) %Nonlinear inequality constraints c=[1.5+x(1)*x(2)-x(1)-x(2); -x(1)*x(2)-10]; %Nonlinear equality constraints ceq=[]; Step 3: >>optimtool to open the optimization toolbox

Fin500J Topic 5 24Fall 2010 Olin Business School

Fin500J Topic 5 Fall 2010 Olin Business School 25

The basic idea is analogous to Newton’s method for unconstrained optimization.

In unconstrained optimization, only the objective function must be approximated, in the NLP, both the objective and the constraint must be modeled.

An sequential quadratic programming method uses a quadratic for the objective and a linear model of the constraint ( i.e., a quadratic program at each iteration)

,...m.mi(x)g

.,...mi(x)g

f(x),

ei

ei

x

10

10

subject to

min