Download - Asian Dividend Strategy

See important disclosures, including any required research certifications, beginning on page 46

Pan Asia Strategy

5 July 2019

Asian Dividend Strategy

Seeking sustainable yield in REITs, utilities, staples and telecoms (RUST) during economic uncertainty

Sustainable yield is our preferred strategy in an economic downturn, focusing highly selectively on REITs, utilities, staples and telecoms

Select “bond-proxy” equities that are high-yield, with appropriate financials and managements willing to deliver dividends in downturns

Daiwa and alliance partners’ sector research identifies 16 sustainable yield ideas; Animal Spirits includes the top-6 in our Top Picks

Paul M. Kitney, PhD(852) 2848 4947

See important disclosures, including any required research certifications, beginning on page 46

Pan Asia Strategy

“Risk off” and cyclical risks call for a sustainable yield approach. As presented in Animal Spirits – Risk off with an emerging-ASEAN & India geographical bias and an emphasis on sustainable dividend yield, 2 July 2019, we are taking a defensive stance in APAC equities, based on expectations of a sharp slowdown in 2020 economic growth that we believe will start to be priced in during 2H19. We argue that disinflation witnessed in the past year will accelerate with this slowdown, and as explained in Animal Spirits – Sustainable yield preferred strategy during disinflation, 2 April 2019, both theory and historical evidence support a sustainable yield approach to stock picking during such times. In this report, we apply the sustainable yield dividend strategy to the so-called RUST group – REITs, utilities, (consumer) staples and telecoms – in Asia ex-Japan. Sustainable yield strategy in the RUST group. We define a sustainable dividend yield strategy as one that focuses on a high current dividend yield that is likely to be maintained or increased during an economic downturn. We focus on the RUST group, but believe a blanket approach to yield among defensives is unwise due to risks related to overvaluation, refinancing risk during credit shocks, heavy capex burdens (eg, 5G), and regulation. Selectivity is therefore critical. Thus, in addition to yield, we apply certain financial metrics such as minimum free cash flow yield, maximum financial leverage, short-term debt mix, and changing capex requirements. While the ability to sustain dividends during an economic downturn is one thing, managements’ willingness to do so is another. Here, we look at managements’ capital management policies and historical track records. Animal Spirits sets a minimum requirement for sector analyst input, leaving plenty of room for sector experts to apply their own methodology, which is shown explicitly. Selecting Animal Spirits Top Picks working with our sector research. From the 16 names presented by Daiwa and our ASEAN alliance partners’ sector research, we have identified 6 names that Animal Spirits particularly likes, which are included in the Animal Spirits Top Picks list. These are: Sunlight REIT (435 HK, HKD6.01, Outperform [2]), CapitaLand Mall Trust (CT SP, SGD2.63, Outperform [2]), Digital Telecom Infrastructure Fund (DIF TB, THB17, BUY), Power Assets (6 HK, HKD57.4, Hold [3]), Guangdong Investment (270 HK, HKD15.82, Outperform [2]), and China Telecom (728 HK, HKD3.94, Buy [1]).

5 July 2019

Asian Dividend Strategy

Seeking sustainable yield in REITs, utilities, staples and telecoms (RUST) during economic uncertainty

Sustainable yield is our preferred strategy in an economic downturn, focusing highly selectively on REITs, utilities, staples and telecoms

Select “bond-proxy” equities that are high-yield, with appropriate financials and managements willing to deliver dividends in downturns

Daiwa and alliance partners’ sector research identifies 16 sustainable yield ideas; Animal Spirits includes the top-6 in our Top Picks

Animal Spirits Top PicksCompany Ticker AIA Group 1299 HK Shenzhou International 2313 HK China Telecom 728 HK Guangdong Investment 270 HK China Mengniu Dairy 2319 HK Wharf REIC 1997 HK Sunlight REIT 435 HK Power Assets 6 HK KT&G Corp 033780 KS Havells India HAVL IN Axis Bank AXSB IN Larsen & Toubro LT IN CapitaLand Mall Trust CT SP Amata Corporation AMATA TB Digital Telecom Infrastructure Fund DIF TB Sino-Thai E&C STEC TB Bank Rakyat Indonesia BBRI IJ Ayala Land ALI PM Airports Corp of Vietnam ACV VN NTT Docomo 9437 JP

Source: Daiwa

Paul M. Kitney, PhD(852) 2848 4947

2

Asian Dividend Strategy: 5 July 2019

Table of contents

Sustainable yield – why now and what to look for? .............................................. 3

Sustainable yield strategy – definition ................................................................................3

The RUST group – what is it and why is selectivity key? ....................................................3

Dividend strategy – maximising real yield spread ...............................................................3

Sustainable yield strategy is to find bond proxies, which maximise the real yield spread

in an economic downturn .................................................................................................3

Country Sector and top picks

China/Hong Kong REITS .............................................................................................. 15

Sunlight REIT (435 HK) ................................................................................................... 16

Singapore REITs ............................................................................................................ 17

CapitaLand Mall Trust (CT SP) ........................................................................................ 18

Thailand REITS .............................................................................................................. 19

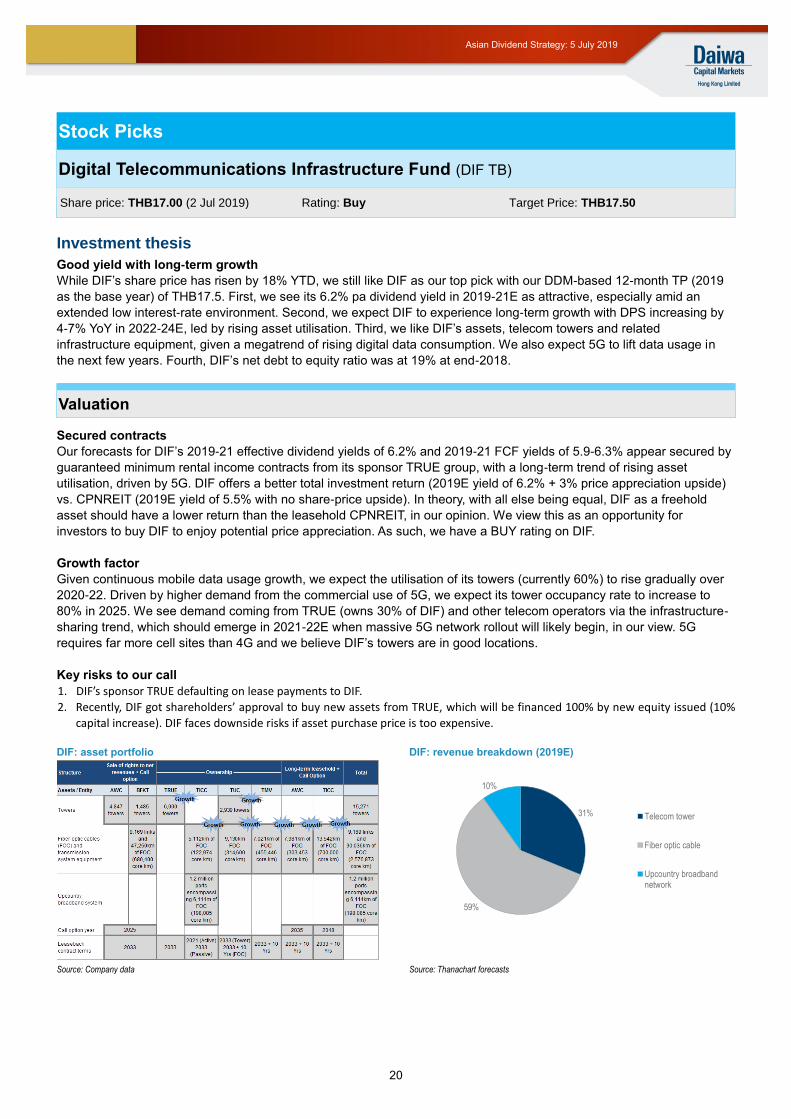

Digital Telecommunications Infrastructure Fund (DIF TB) ................................................ 20

Jasmine Broadband Internet Infrastructure Fund (JASIF TB) ........................................... 21

China/Hong Kong Utilities ............................................................................................ 23

Power Assets (6 HK) ....................................................................................................... 24

Guangdong Investment (270 HK) .................................................................................... 25

China Resources Gas (1193 HK) ..................................................................................... 26

Thailand Utilities ........................................................................................................... 27

Ratch Group (RATCH TB) ............................................................................................... 28

China/Hong Kong Staples ............................................................................................. 29

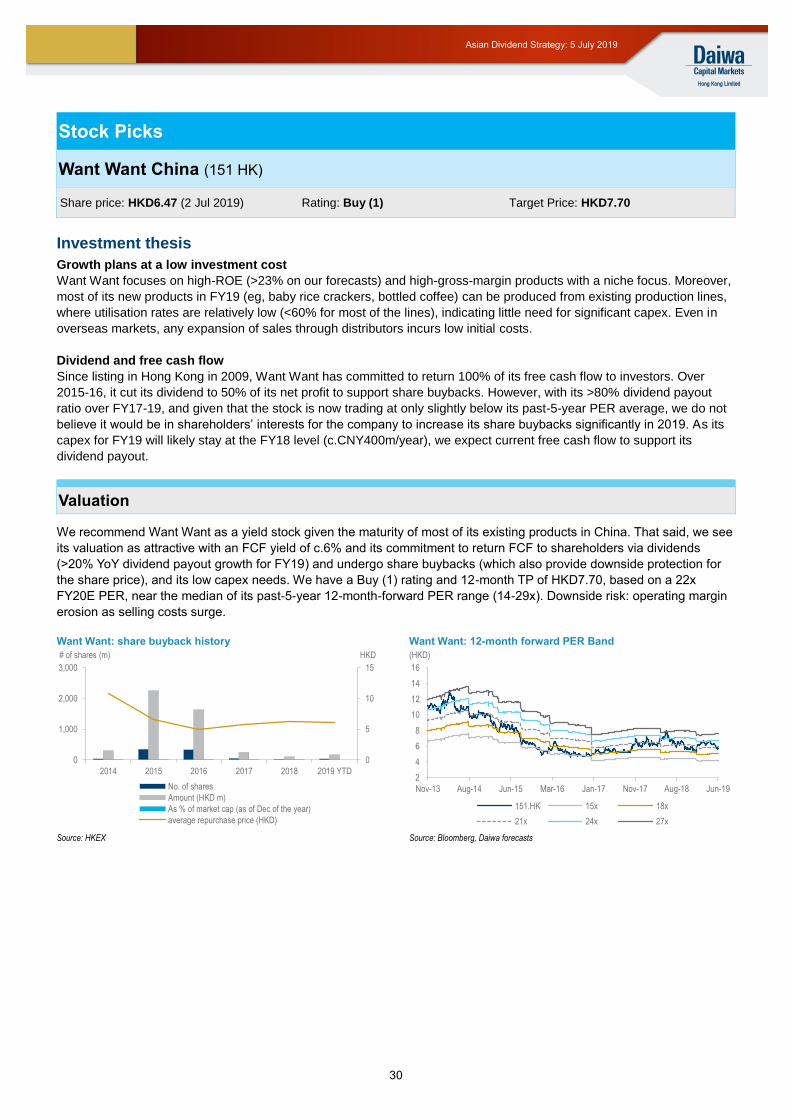

Want Want China (151 HK) ............................................................................................. 30

Hengan (1044 HK) ........................................................................................................... 31

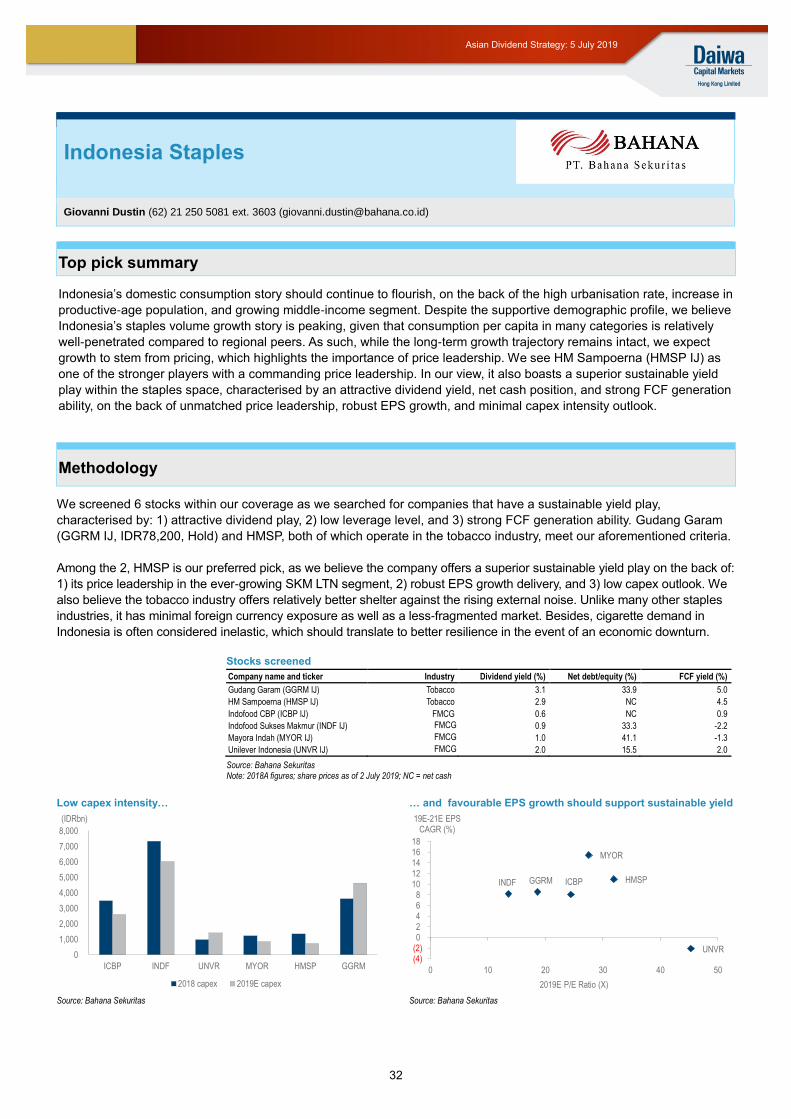

Indonesia Staples .......................................................................................................... 32

HM Sampoerna (HMSP IJ) .............................................................................................. 33

China/Singapore/Philippines Telecoms ....................................................................... 34

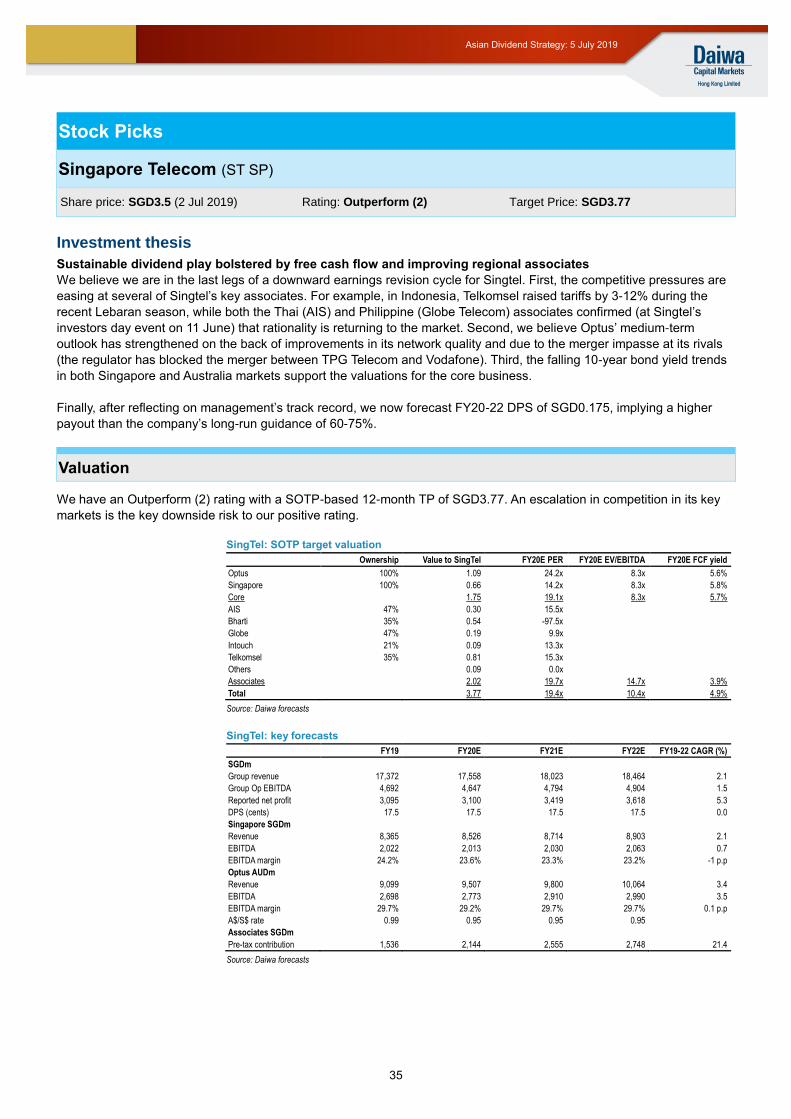

Singapore Telecom (ST SP) ............................................................................................ 35

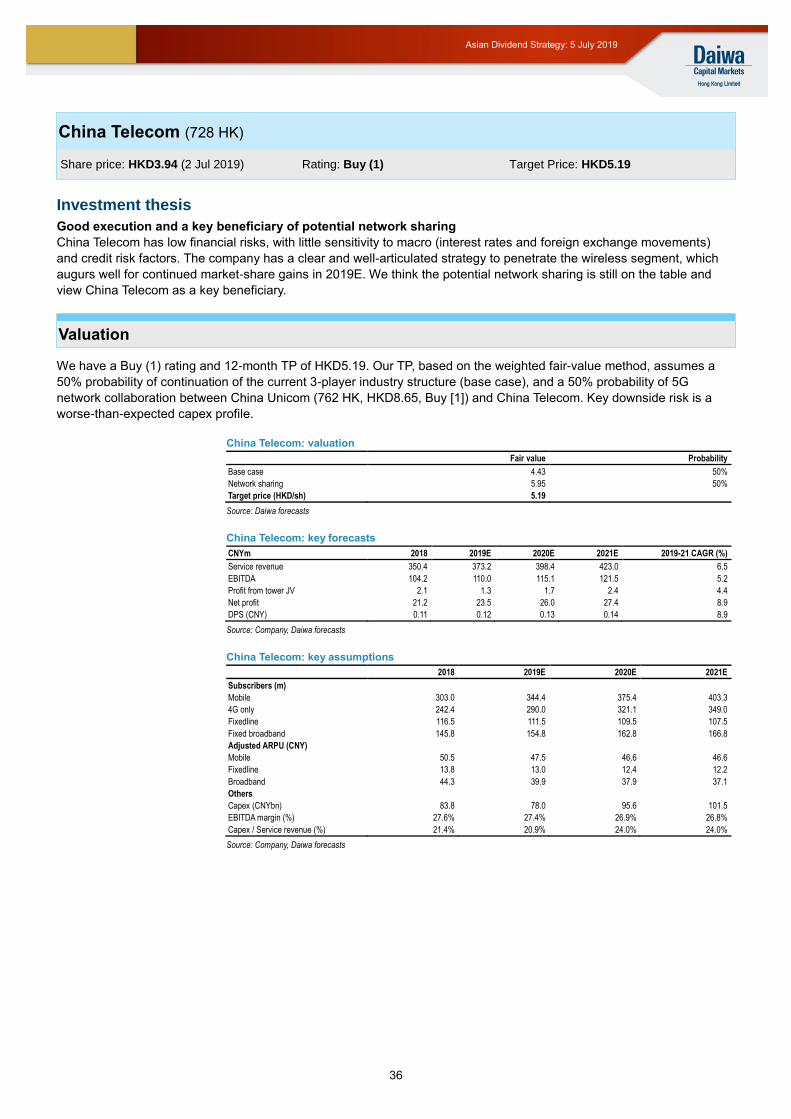

China Telecom (728 HK) ................................................................................................. 36

Indonesia Telecoms....................................................................................................... 37

Telkom (TLKM IJ) ............................................................................................................ 38

Thailand Telecoms ......................................................................................................... 39

Intouch Holdings (INTUCH TB) ........................................................................................ 40

Malaysia REITS .............................................................................................................. 41

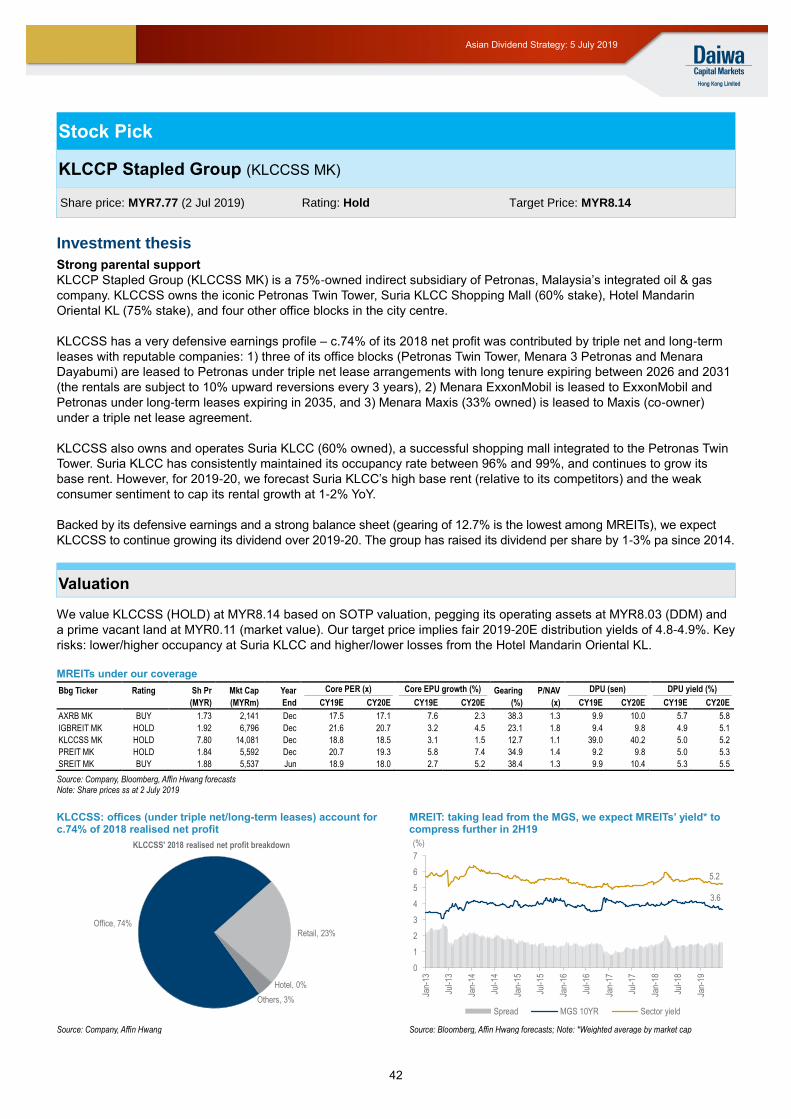

KLCCP Stapled Group (KLCCSS MK) ............................................................................. 42

3

Asian Dividend Strategy: 5 July 2019

Sustainable yield – why now and what to look for?

Sustainable yield strategy – definition

We define a sustainable dividend yield strategy as one that focuses on high current

dividend yield, which is likely to be maintained or increased during an economic downturn.

What factors do we consider important in evaluating the sustainability of dividend yield?

Broadly, these reflect considerations of both a firm’s ability and managements’ willingness

to pay out dividends in a sustained fashion, under various operating conditions.

The RUST group – what is it and why is selectivity key?

RUST is an acronym for REITs, utilities, (consumer) staples and telecom sector equities.

These are considered traditionally “defensive” industries, as demand is inelastic or not as

cyclically sensitive as many other sectors. However, we caution against a blanket

approach to the so-called RUST group, without consideration of various issues that may

preclude some RUST stocks from behaving defensively, when required – namely, during

an economic downturn or a bear market. One consideration is valuation. For example, in

Asia, Animal Spirits would argue that many consumer staples equities listed in China and

India are overvalued. In a downturn, quality factors such as balance sheet strength are

important to determine dividend sustainability as credit shocks expose levered companies.

Other risks such as regulation of utility tariffs in Korea, for example, may preclude some

equities as sustainable yield plays. 5G-related capex in the telecom sector may put free

cash flow at risk in some cases. These factors may constrain certain RUST names being

able to sustain dividends through the cycle or may prevent them behaving defensively.

Dividend strategy – maximising real yield spread

We outlined in Animal Spirits – Sustainable yield preferred strategy during disinflation, 2

April 2019, our preferred valuation metric – the real yield spread. Equity income is

preferred to fixed income when the real yield spread = nominal dividend yield – nominal

bond yield – inflation rate, is sufficiently positive. In our opinion, a sound equity income

strategy is one that chooses equities that maximises the real yield spread during any

macro conditions. During reflationary periods such as 1H18, when inflation and bond yields

were rising, the real yield spread was positive primarily for companies that were growing

their dividends sufficiently fast. That is why, during 1H18, Animal Spirits advocated a

dividend growth approach to stock picking, utilising the real yield spread approach under a

reflationary regime. Indeed, dividend growth stocks considerably outperformed high

dividend yield stocks during that period. We demonstrated this in Animal Spirits –

Sustainable yield preferred strategy during disinflation, 2 April 2019.

Sustainable yield strategy is to find bond proxies, which maximise the real yield spread in an economic downturn

In contrast, during a disinflationary paradigm – when inflation rates are falling, such as the

present day – high dividend growth stocks do not maximise real excess yield. During

disinflation, not only are inflation rates falling but so are bond yields. We are witnessing this

now. The US 10-year bond yield peaked at c.3.2% in 2018, but is now around 2%. To

maximise the real yield spread (throughout the disinflationary paradigm, which could last

years, in our view) under disinflation, we need to select high current yield stocks, where

yields are likely to be maintained during the economic down cycle that is often concomitant

with disinflation. In other words, we are seeking “bond proxies” during disinflation. We

won’t rehash our macro outlook here (see Risk off, 2 July; China-A downgrade, 1 July,

Korea Strategy – Strong headwinds, 10 June; ASEAN strategy – Cyclical Hideouts, 3

May), but our long-held roadmap calls for a sharp economic downturn, particularly

pronounced from 2H20. In our view, this will likely go hand in hand with a prolonged period

of disinflation, which motivates our sustainable yield dividend strategy.

A blanket approach to

yield among defensives

is unwise due to risks

related to overvaluation,

refinancing risk during

credit shocks, heavy

capex burdens (eg, 5G),

and regulation

In disinflation, which is

likely to persist for a

year or longer, “bond

proxies” are preferred,

which are high yield

equities able to at least

sustain their dividends

during a down cycle

4

Asian Dividend Strategy: 5 July 2019

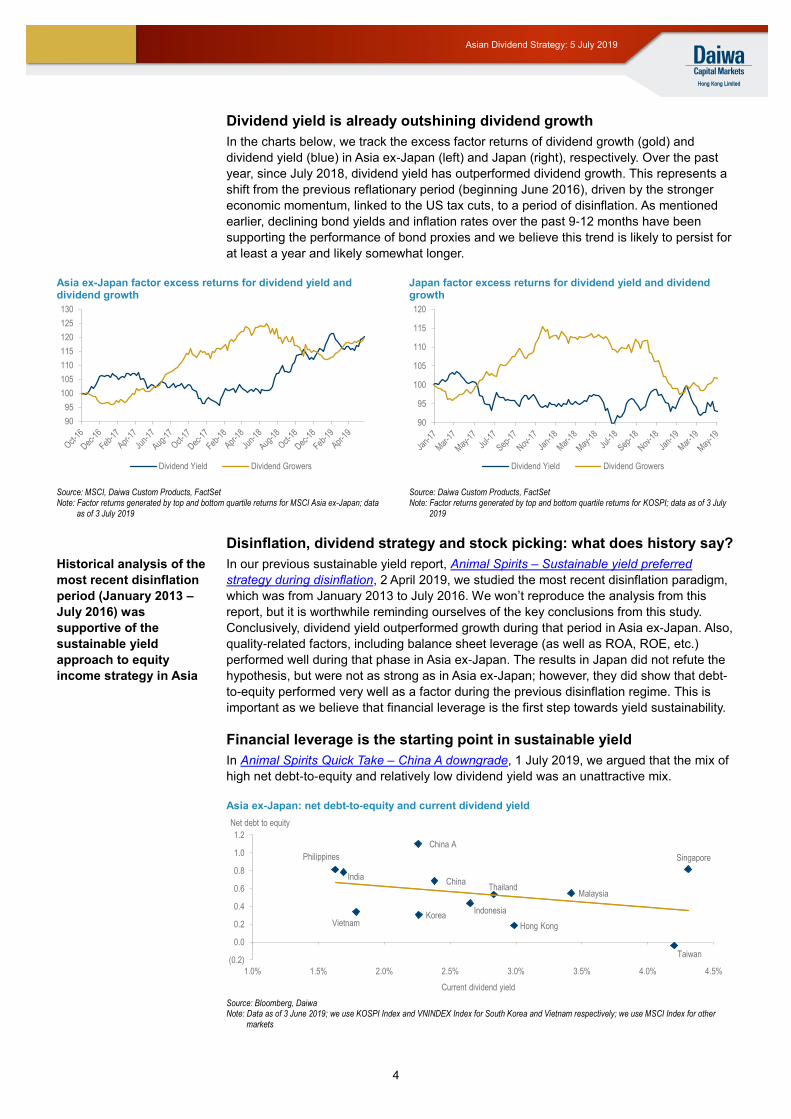

Dividend yield is already outshining dividend growth

In the charts below, we track the excess factor returns of dividend growth (gold) and

dividend yield (blue) in Asia ex-Japan (left) and Japan (right), respectively. Over the past

year, since July 2018, dividend yield has outperformed dividend growth. This represents a

shift from the previous reflationary period (beginning June 2016), driven by the stronger

economic momentum, linked to the US tax cuts, to a period of disinflation. As mentioned

earlier, declining bond yields and inflation rates over the past 9-12 months have been

supporting the performance of bond proxies and we believe this trend is likely to persist for

at least a year and likely somewhat longer.

Asia ex-Japan factor excess returns for dividend yield and dividend growth

Japan factor excess returns for dividend yield and dividend growth

Source: MSCI, Daiwa Custom Products, FactSet Note: Factor returns generated by top and bottom quartile returns for MSCI Asia ex-Japan; data

as of 3 July 2019

Source: Daiwa Custom Products, FactSet Note: Factor returns generated by top and bottom quartile returns for KOSPI; data as of 3 July

2019

Disinflation, dividend strategy and stock picking: what does history say?

In our previous sustainable yield report, Animal Spirits – Sustainable yield preferred

strategy during disinflation, 2 April 2019, we studied the most recent disinflation paradigm,

which was from January 2013 to July 2016. We won’t reproduce the analysis from this

report, but it is worthwhile reminding ourselves of the key conclusions from this study.

Conclusively, dividend yield outperformed growth during that period in Asia ex-Japan. Also,

quality-related factors, including balance sheet leverage (as well as ROA, ROE, etc.)

performed well during that phase in Asia ex-Japan. The results in Japan did not refute the

hypothesis, but were not as strong as in Asia ex-Japan; however, they did show that debt-

to-equity performed very well as a factor during the previous disinflation regime. This is

important as we believe that financial leverage is the first step towards yield sustainability.

Financial leverage is the starting point in sustainable yield

In Animal Spirits Quick Take – China A downgrade, 1 July 2019, we argued that the mix of

high net debt-to-equity and relatively low dividend yield was an unattractive mix.

Asia ex-Japan: net debt-to-equity and current dividend yield

Source: Bloomberg, Daiwa Note: Data as of 3 June 2019; we use KOSPI Index and VNINDEX Index for South Korea and Vietnam respectively; we use MSCI Index for other

markets

90

95

100

105

110

115

120

125

130

Dividend Yield Dividend Growers

90

95

100

105

110

115

120

Dividend Yield Dividend Growers

China

China A

Hong Kong

Taiwan

Korea

Philippines Singapore

MalaysiaThailand

India

Indonesia

Vietnam

(0.2)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0% 4.5%

Net debt to equity

Current dividend yield

Historical analysis of the

most recent disinflation

period (January 2013 –

July 2016) was

supportive of the

sustainable yield

approach to equity

income strategy in Asia

5

Asian Dividend Strategy: 5 July 2019

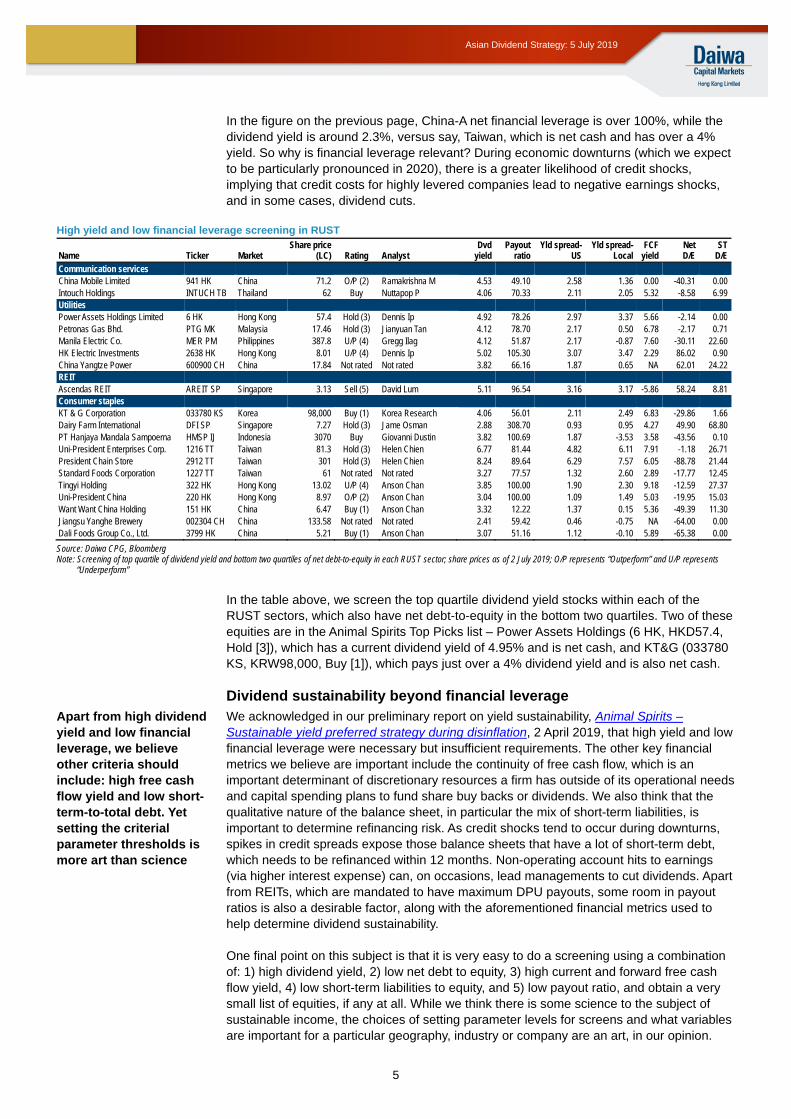

In the figure on the previous page, China-A net financial leverage is over 100%, while the dividend yield is around 2.3%, versus say, Taiwan, which is net cash and has over a 4% yield. So why is financial leverage relevant? During economic downturns (which we expect to be particularly pronounced in 2020), there is a greater likelihood of credit shocks, implying that credit costs for highly levered companies lead to negative earnings shocks, and in some cases, dividend cuts.

High yield and low financial leverage screening in RUST

Name Ticker Market Share price

(LC) Rating Analyst Dvd

yield Payout

ratio Yld spread-

US Yld spread-

Local FCF

yield Net D/E

ST D/E

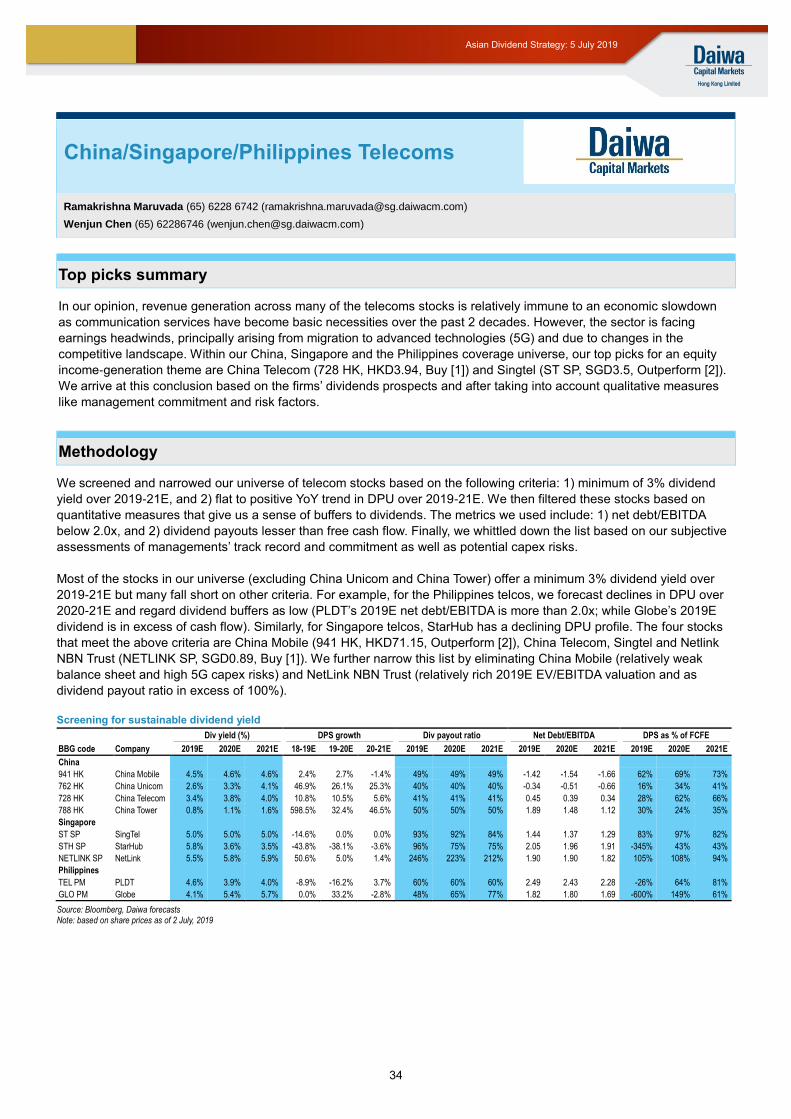

Communication services China Mobile Limited 941 HK China 71.2 O/P (2) Ramakrishna M 4.53 49.10 2.58 1.36 0.00 -40.31 0.00 Intouch Holdings INTUCH TB Thailand 62 Buy Nuttapop P 4.06 70.33 2.11 2.05 5.32 -8.58 6.99 Utilities Power Assets Holdings Limited 6 HK Hong Kong 57.4 Hold (3) Dennis Ip 4.92 78.26 2.97 3.37 5.66 -2.14 0.00 Petronas Gas Bhd. PTG MK Malaysia 17.46 Hold (3) Jianyuan Tan 4.12 78.70 2.17 0.50 6.78 -2.17 0.71 Manila Electric Co. MER PM Philippines 387.8 U/P (4) Gregg Ilag 4.12 51.87 2.17 -0.87 7.60 -30.11 22.60 HK Electric Investments 2638 HK Hong Kong 8.01 U/P (4) Dennis Ip 5.02 105.30 3.07 3.47 2.29 86.02 0.90 China Yangtze Power 600900 CH China 17.84 Not rated Not rated 3.82 66.16 1.87 0.65 NA 62.01 24.22 REIT Ascendas REIT AREIT SP Singapore 3.13 Sell (5) David Lum 5.11 96.54 3.16 3.17 -5.86 58.24 8.81 Consumer staples KT & G Corporation 033780 KS Korea 98,000 Buy (1) Korea Research 4.06 56.01 2.11 2.49 6.83 -29.86 1.66 Dairy Farm International DFI SP Singapore 7.27 Hold (3) Jame Osman 2.88 308.70 0.93 0.95 4.27 49.90 68.80 PT Hanjaya Mandala Sampoerna HMSP IJ Indonesia 3070 Buy Giovanni Dustin 3.82 100.69 1.87 -3.53 3.58 -43.56 0.10 Uni-President Enterprises Corp. 1216 TT Taiwan 81.3 Hold (3) Helen Chien 6.77 81.44 4.82 6.11 7.91 -1.18 26.71 President Chain Store 2912 TT Taiwan 301 Hold (3) Helen Chien 8.24 89.64 6.29 7.57 6.05 -88.78 21.44 Standard Foods Corporation 1227 TT Taiwan 61 Not rated Not rated 3.27 77.57 1.32 2.60 2.89 -17.77 12.45 Tingyi Holding 322 HK Hong Kong 13.02 U/P (4) Anson Chan 3.85 100.00 1.90 2.30 9.18 -12.59 27.37 Uni-President China 220 HK Hong Kong 8.97 O/P (2) Anson Chan 3.04 100.00 1.09 1.49 5.03 -19.95 15.03 Want Want China Holding 151 HK China 6.47 Buy (1) Anson Chan 3.32 12.22 1.37 0.15 5.36 -49.39 11.30 Jiangsu Yanghe Brewery 002304 CH China 133.58 Not rated Not rated 2.41 59.42 0.46 -0.75 NA -64.00 0.00 Dali Foods Group Co., Ltd. 3799 HK China 5.21 Buy (1) Anson Chan 3.07 51.16 1.12 -0.10 5.89 -65.38 0.00

Source: Daiwa CPG, Bloomberg Note: Screening of top quartile of dividend yield and bottom two quartiles of net debt-to-equity in each RUST sector; share prices as of 2 July 2019; O/P represents “Outperform” and U/P represents

“Underperform”

In the table above, we screen the top quartile dividend yield stocks within each of the RUST sectors, which also have net debt-to-equity in the bottom two quartiles. Two of these equities are in the Animal Spirits Top Picks list – Power Assets Holdings (6 HK, HKD57.4, Hold [3]), which has a current dividend yield of 4.95% and is net cash, and KT&G (033780 KS, KRW98,000, Buy [1]), which pays just over a 4% dividend yield and is also net cash. Dividend sustainability beyond financial leverage We acknowledged in our preliminary report on yield sustainability, Animal Spirits – Sustainable yield preferred strategy during disinflation, 2 April 2019, that high yield and low financial leverage were necessary but insufficient requirements. The other key financial metrics we believe are important include the continuity of free cash flow, which is an important determinant of discretionary resources a firm has outside of its operational needs and capital spending plans to fund share buy backs or dividends. We also think that the qualitative nature of the balance sheet, in particular the mix of short-term liabilities, is important to determine refinancing risk. As credit shocks tend to occur during downturns, spikes in credit spreads expose those balance sheets that have a lot of short-term debt, which needs to be refinanced within 12 months. Non-operating account hits to earnings (via higher interest expense) can, on occasions, lead managements to cut dividends. Apart from REITs, which are mandated to have maximum DPU payouts, some room in payout ratios is also a desirable factor, along with the aforementioned financial metrics used to help determine dividend sustainability. One final point on this subject is that it is very easy to do a screening using a combination of: 1) high dividend yield, 2) low net debt to equity, 3) high current and forward free cash flow yield, 4) low short-term liabilities to equity, and 5) low payout ratio, and obtain a very small list of equities, if any at all. While we think there is some science to the subject of sustainable income, the choices of setting parameter levels for screens and what variables are important for a particular geography, industry or company are an art, in our opinion.

Apart from high dividend yield and low financial leverage, we believe other criteria should include: high free cash flow yield and low short-term-to-total debt. Yet setting the criterial parameter thresholds is more art than science

6

Asian Dividend Strategy: 5 July 2019

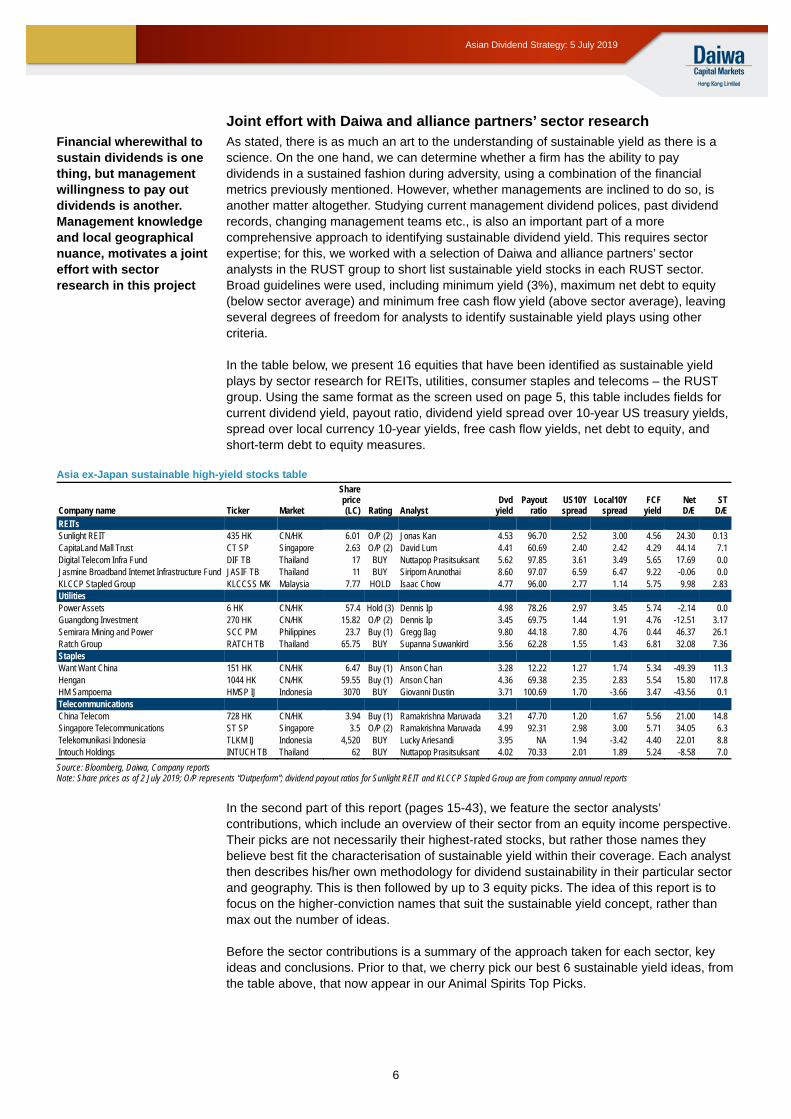

Joint effort with Daiwa and alliance partners’ sector research As stated, there is as much an art to the understanding of sustainable yield as there is a science. On the one hand, we can determine whether a firm has the ability to pay dividends in a sustained fashion during adversity, using a combination of the financial metrics previously mentioned. However, whether managements are inclined to do so, is another matter altogether. Studying current management dividend polices, past dividend records, changing management teams etc., is also an important part of a more comprehensive approach to identifying sustainable dividend yield. This requires sector expertise; for this, we worked with a selection of Daiwa and alliance partners’ sector analysts in the RUST group to short list sustainable yield stocks in each RUST sector. Broad guidelines were used, including minimum yield (3%), maximum net debt to equity (below sector average) and minimum free cash flow yield (above sector average), leaving several degrees of freedom for analysts to identify sustainable yield plays using other criteria. In the table below, we present 16 equities that have been identified as sustainable yield plays by sector research for REITs, utilities, consumer staples and telecoms – the RUST group. Using the same format as the screen used on page 5, this table includes fields for current dividend yield, payout ratio, dividend yield spread over 10-year US treasury yields, spread over local currency 10-year yields, free cash flow yields, net debt to equity, and short-term debt to equity measures.

Asia ex-Japan sustainable high-yield stocks table

Company name Ticker Market

Share price (LC) Rating Analyst

Dvd yield

Payout ratio

US10Y spread

Local10Y spread

FCF yield

Net D/E

ST D/E

REITs

Sunlight REIT 435 HK CN/HK 6.01 O/P (2) Jonas Kan 4.53 96.70 2.52 3.00 4.56 24.30 0.13 CapitaLand Mall Trust CT SP Singapore 2.63 O/P (2) David Lum 4.41 60.69 2.40 2.42 4.29 44.14 7.1 Digital Telecom Infra Fund DIF TB Thailand 17 BUY Nuttapop Prasitsuksant 5.62 97.85 3.61 3.49 5.65 17.69 0.0 Jasmine Broadband Internet Infrastructure Fund JASIF TB Thailand 11 BUY Siriporn Arunothai 8.60 97.07 6.59 6.47 9.22 -0.06 0.0 KLCCP Stapled Group KLCCSS MK Malaysia 7.77 HOLD Isaac Chow 4.77 96.00 2.77 1.14 5.75 9.98 2.83 Utilities

Power Assets 6 HK CN/HK 57.4 Hold (3) Dennis Ip 4.98 78.26 2.97 3.45 5.74 -2.14 0.0 Guangdong Investment 270 HK CN/HK 15.82 O/P (2) Dennis Ip 3.45 69.75 1.44 1.91 4.76 -12.51 3.17 Semirara Mining and Power SCC PM Philippines 23.7 Buy (1) Gregg Ilag 9.80 44.18 7.80 4.76 0.44 46.37 26.1 Ratch Group RATCH TB Thailand 65.75 BUY Supanna Suwankird 3.56 62.28 1.55 1.43 6.81 32.08 7.36 Staples

Want Want China 151 HK CN/HK 6.47 Buy (1) Anson Chan 3.28 12.22 1.27 1.74 5.34 -49.39 11.3 Hengan 1044 HK CN/HK 59.55 Buy (1) Anson Chan 4.36 69.38 2.35 2.83 5.54 15.80 117.8 HM Sampoerna HMSP IJ Indonesia 3070 BUY Giovanni Dustin 3.71 100.69 1.70 -3.66 3.47 -43.56 0.1 Telecommunications

China Telecom 728 HK CN/HK 3.94 Buy (1) Ramakrishna Maruvada 3.21 47.70 1.20 1.67 5.56 21.00 14.8 Singapore Telecommunications ST SP Singapore 3.5 O/P (2) Ramakrishna Maruvada 4.99 92.31 2.98 3.00 5.71 34.05 6.3 Telekomunikasi Indonesia TLKM IJ Indonesia 4,520 BUY Lucky Ariesandi 3.95 NA 1.94 -3.42 4.40 22.01 8.8 Intouch Holdings INTUCH TB Thailand 62 BUY Nuttapop Prasitsuksant 4.02 70.33 2.01 1.89 5.24 -8.58 7.0

Source: Bloomberg, Daiwa, Company reports Note: Share prices as of 2 July 2019; O/P represents “Outperform”; dividend payout ratios for Sunlight REIT and KLCCP Stapled Group are from company annual reports

In the second part of this report (pages 15-43), we feature the sector analysts’ contributions, which include an overview of their sector from an equity income perspective. Their picks are not necessarily their highest-rated stocks, but rather those names they believe best fit the characterisation of sustainable yield within their coverage. Each analyst then describes his/her own methodology for dividend sustainability in their particular sector and geography. This is then followed by up to 3 equity picks. The idea of this report is to focus on the higher-conviction names that suit the sustainable yield concept, rather than max out the number of ideas. Before the sector contributions is a summary of the approach taken for each sector, key ideas and conclusions. Prior to that, we cherry pick our best 6 sustainable yield ideas, from the table above, that now appear in our Animal Spirits Top Picks.

Financial wherewithal to sustain dividends is one thing, but management willingness to pay out dividends is another. Management knowledge and local geographical nuance, motivates a joint effort with sector research in this project

7

Asian Dividend Strategy: 5 July 2019

Animal Spirits selects 6 sustainable yield plays

Following the analysis in this report, we identify 6 names that Animal Spirits particularly

likes, which are included in the Animal Spirits Top Picks list. They are: 1) Sunlight REIT

(435 HK, HKD6.01, Outperform [2]), 2) CapitaLand Mall Trust (CT SP, SGD2.63,

Outperform [2]), 3) Digital Telecom Infrastructure Fund (DIF TB, THB17, BUY), 4) Power

Assets (6 HK, HKD57.4, Hold [3]), 5) Guangdong Investment (270 HK, HKD15.82,

Outperform [2]), and 6) China Telecom (728 HK, HKD3.94, Buy [1]). We will elaborate

more on each in the RUST sector discussion below.

We now summarise the salient points from each RUST sector’s analyst contributions.

REITs

In Hong Kong, Daiwa analyst Jonas Kan focuses on an important sub-theme within the H-

REITs, which is the “modernisation of capital management”, including various efficiency

measures such as the willingness to dispose of non-core assets to realize NAV. He also

notes the significance of the high valuation Link REIT has attained, and that lessons are

being learned by other REITs in Hong Kong. Jonas has identified one REIT, Sunlight REIT,

which is play on office decentralisation. He sees a 2019E DPU yield of 4.7% and expects it

to rise to 5.1% in 2021. He notes that Sunlight is one of the more advanced in the H-REITs

with regard to capital management, having sold non-core assets to fund unit buy backs, as

early as 2012. Animal Spirits particularly likes this one due to its low net debt to equity

(24.3%), low exposure to refinancing risk as short-term debt to equity is only 0.13%, high

free cash flow yield, and more than 250bps DPU yield spread over 10-year bond yields.

Sunlight has been recently added to Animal Spirits Top Picks.

In Singapore, Daiwa analyst David Lum is not so positive on the S-REITs in general. In

particular, he is concerned about the commercial real estate sector’s sensitivity to the

economy. David’s methodology also includes an examination of the continuity of DPU

during previous economic downturns. He notes that during the global financial crisis

(GFC), the only property sub-segment that was not hit by negative rental reversions was

the suburban mall segment. Going forward, David sees limited downside to Singapore

retail rents as he believes there will be negligible supply of new real space in 2020-22E

after a decade of supply growth. He sees the retail and suburban mall rents near the

bottom of the property cycle. In this context, he views CapitaLand Mall Trust (CMT) as the

best combination of DPU growth, yield and defensiveness among the large-cap S-REITs.

Portfolio occupancy for CMT is high (98.8%) and the lack of new supply should keep rental

reversions positive. Moderate financial leverage (44.14%), a low dependence on short-

term financing (7.1% short-term debt to equity) and the 240bps yield spread over 10-year

bonds are also attractive, in his opinion. CMT is an Animal Spirits Top Pick.

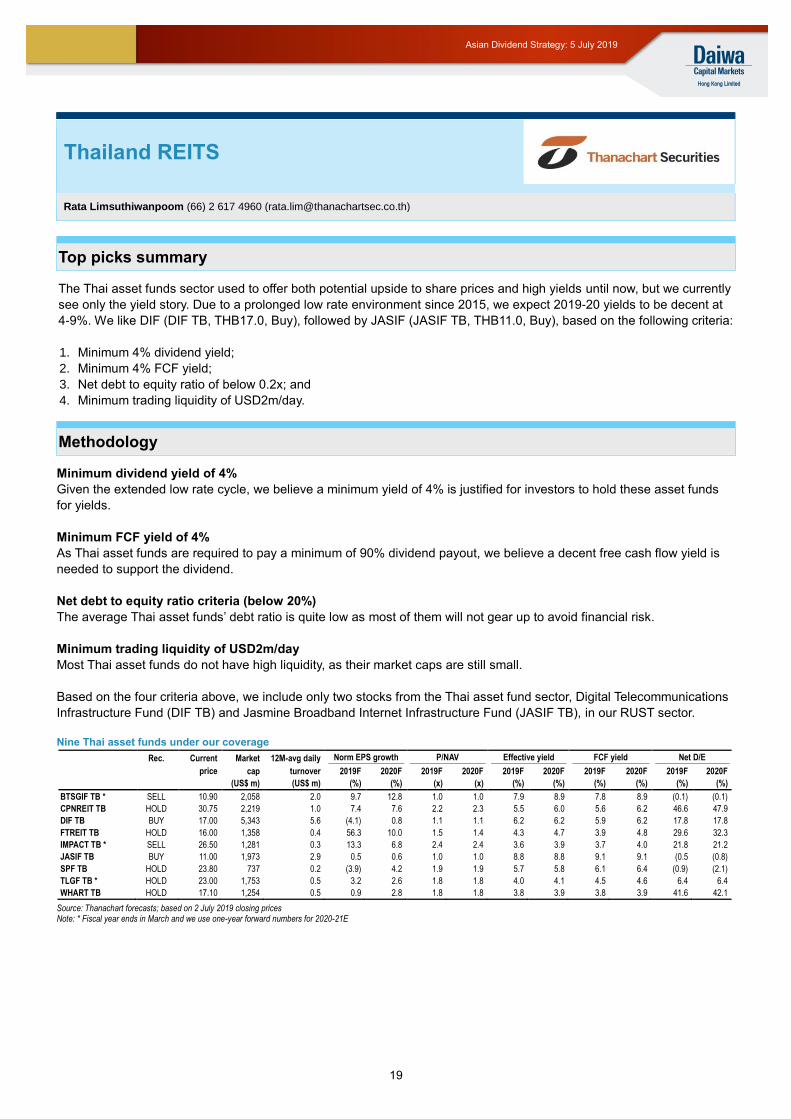

In Thailand, we look at the asset funds sector alongside the REITs and according to our

alliance partner, Thanachart Securities’ analyst, Rata Limsuthiwanpoom, the key criteria for

evaluating sustainable yield by the Thanachart team are: dividend yield above 4%, free

cash flow yield above 4%, net debt to equity below 20%, and minimum trading volume of

USD2m per day. The two stocks that fit these criteria are Digital Telecom Infrastructure

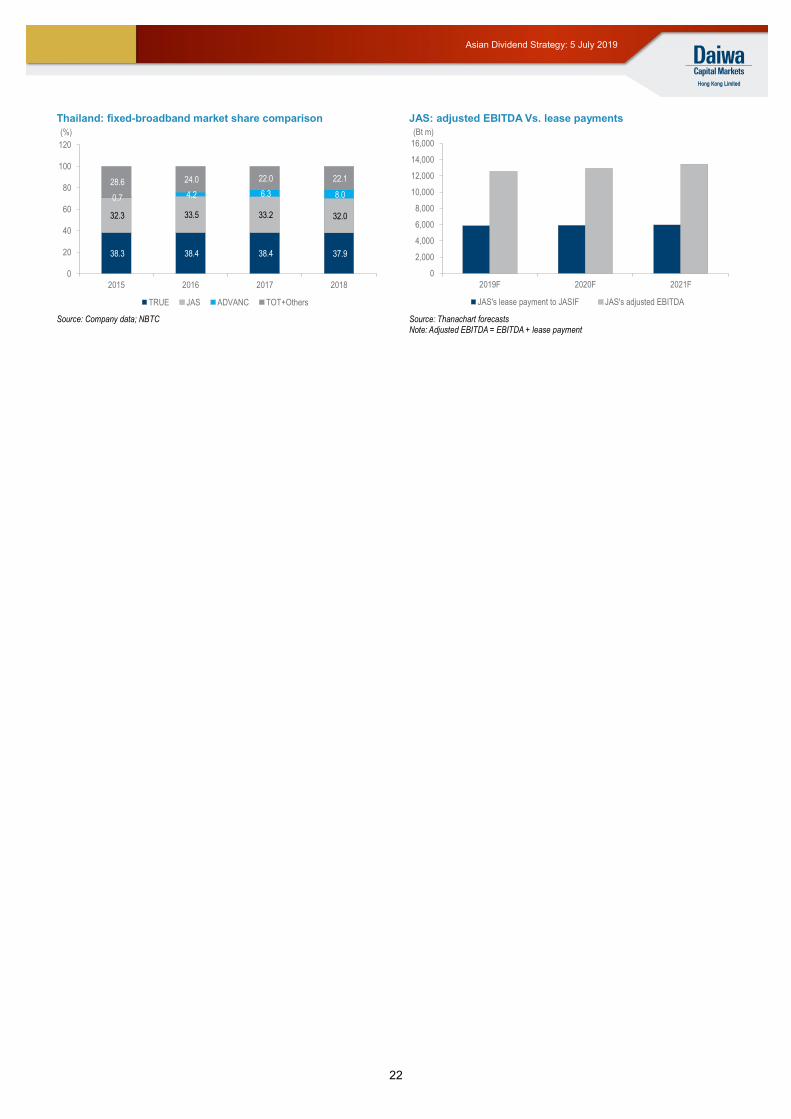

Fund (DIF TB, THB17, BUY) and Jasmine Broadband Internet Infrastructure Fund (JASIF

TB, THB11, BUY). According to the Thanachart team (coverage analyst: Nuttapop

Prasitsuksant), the dividend yield of Digital Telecom Infrastructure Fund in 2019-21E

should be 6.4% and dividend growth is expected to be 4-7% over 2022-24E on rising asset

utilisation. Increasing telecom tower utilisation rates are expected to be driven by 5G

adaptation. Animal Spirits particularly likes the yield spread over 10-year bonds, which is

c.340bps, zero short-term debt, sufficient free cash flow yield and low net financial

leverage (17.69%). We have added this name to our Animal Spirits Top Picks list.

In Malaysia, alliance partner Affin Hwang’s analyst, Isaac Chow, notes that the office

market in the M-REIT space is oversupplied. However, with overall positive rental

reversions, earnings for his top sustainable yield pick, KLCCP Stapled Group (KLCCSS

Jonas Kan sees

improved capital

management practices,

following the example of

Link REIT, in Hong Kong

as being an important

theme; Sunlight REIT is

a good candidate for

sustainable yield in the

H-REITs

8

Asian Dividend Strategy: 5 July 2019

MK), are defensive due to high occupancy for its flagship Suria KLCC Shopping Mall asset

(among other things) and low gearing, with net debt to equity at 9.98%.

We now switch to the topic of sustainable yield in the Utilities sector.

Utilities

In Hong Kong/China, Daiwa analyst Dennis Ip has a clear methodology for evaluating

sustainable yield including low beta (less than 0.35), a minimum threshold of a 3%

dividend yield, at least a 3.5% free cash flow yield, net short-term cash to equity, and a

track record of not having lowered its dividend per share since 2008. Based on Dennis’s

analysis, Power Assets (6 HK, HKD57.4, Hold [3]) meets these criteria. It has a 0.28 three-

year trailing beta; 5% dividend yield (2020); 5% free cash flow yield; 6% net short-term

cash to equity (based on Dennis’ model); and saw 3% average dividend per share growth

over 2008-18 without a yearly decline. Animal Spirits also likes this particular name, adding

that overall it is net cash and has a c.300bps yield spread over 10-year bonds, and is

included in the Animal Spirits Top Picks list. Similarly, we agree with Dennis’s assessment

of Guangdong Investment (270 HK, HKD15.82, Outperform [2]), as it meets his criteria and

is also included in our Top Picks.

In the Philippines, Daiwa analyst Gregg Ilag’s approach follows the broad Animal Spirits

guideline of a 3% minimum dividend yield and below-average financial leverage and

above-average free cash flow yield. In addition to these criteria, Greg also focuses on the

track record of maintaining dividends. In this context, he likes Semirara Mining and Power

Corp (SCC PM, PHP 23.7, Buy [1]). He notes the integration of coal mining and power

generation puts it in a strong competitive position to sustain cash flows in a downturn.

Based on his work, it has a 5.8% dividend yield, the free cash flow yield should be over 9%

for 2019-20E, and has steadily increased its dividend over the past 13 years, which

includes the GFC period.

In Thailand, alliance partner Thanachart analyst Supanna Suwankird has set specific

criteria: minimum dividend yield of 4%, at least a 2.3% free cash flow yield, maximum net

debt-to-equity of 80%; and no drop in dividend over the past 15 years. Supanna presents

one name that fits these criteria, Ratch group (RATCH TB, 65.75, BUY).

We now change the topic from dividend sustainability in the utilities sector to consumer

staples.

Staples

In Hong Kong/China, Daiwa analyst Anson Chan offers his insight on dividend

sustainability methodology. He believes that reduced capex needs, lower net gearing and

steady operating cash flow are the most important factors, but also considers a long-term

track record of maintaining dividends, in his evaluation. Anson likes Want Want China (151

HK, HKD6.47, Buy [1]) as a dividend sustainability candidate. It pays a dividend of just

over 4%, which is well within free cash flow yield of c.6%, which is supported by low capex

requirements. Anson also likes Hengan (1044 HK, HKD59.55, Buy [1]) as a sustainable

dividend yield play. He believes that capex needs will remain low, paving the way for

consistent free cash flow and dividend yields.

In Indonesia, Bahana Securities analyst Giovanni Dustin follows Animal Spirits broad

sustainable yield methodology and has selected HM Sampoerna (HMSP IJ, IDR 3070,

BUY) as a sustainable yield play. With the stock’s c.3% dividend yield, net cash and 4.5%

free cash flow yield, as well as low capital spending burden, Giovanni believes that

together with its price leadership and solid growth outlook, this is a good sustainable yield

candidate.

We shift now to the Telecoms sector.

Dennis Ip has a

methodical approach to

sustainable yield

including maximum

beta, minimum dividend

and free cash flow yield,

net short-term cash to

equity and a track record

of maintaining dividends

over 10 years

9

Asian Dividend Strategy: 5 July 2019

Telecoms

Daiwa’s China/Singapore/Philippines telecoms analyst, Rama Maruvada’s methodology for

evaluating sustainable yield has several components. First, he looks at the forward-looking

dividend yield over 2019-21E and screens for a minimum of 3%. Then over the same

period he requires a flat to positive DPU trend YoY. Then he reduces his universe to those

which have a net debt-EBITDA below 2.0x and dividend payout less than free cash flow.

Finally, he uses subjective measures of management track record and commitment to

sustain dividends, together with potential capex risks. Based on his approach, Rama likes

China Telecom (728 HK, HKD3.94, Buy [1]). Based on his model, the dividend yield in

2019E is 3.4%, growing to 4% in 2021E, net debt-to-EBITDA is 0.45x and dividends as a

percentage of free cash flow is 28%. Rama sees the prospects of 5G network-sharing as a

distinct possibility, which should help significantly in managing capex, but this is also the

risk, if 5G related capex surprises on the upside. Animal Spirits also likes the low financial

leverage, including low short-term debt mix, and includes China Telecom in the Animal

Spirits Top Picks. Rama also explains that Singapore Telecom (ST SP, SGD3.5,

Outperform [2]) fits his criteria and sees upside to the company’s dividend payout guidance

of 60-75%.

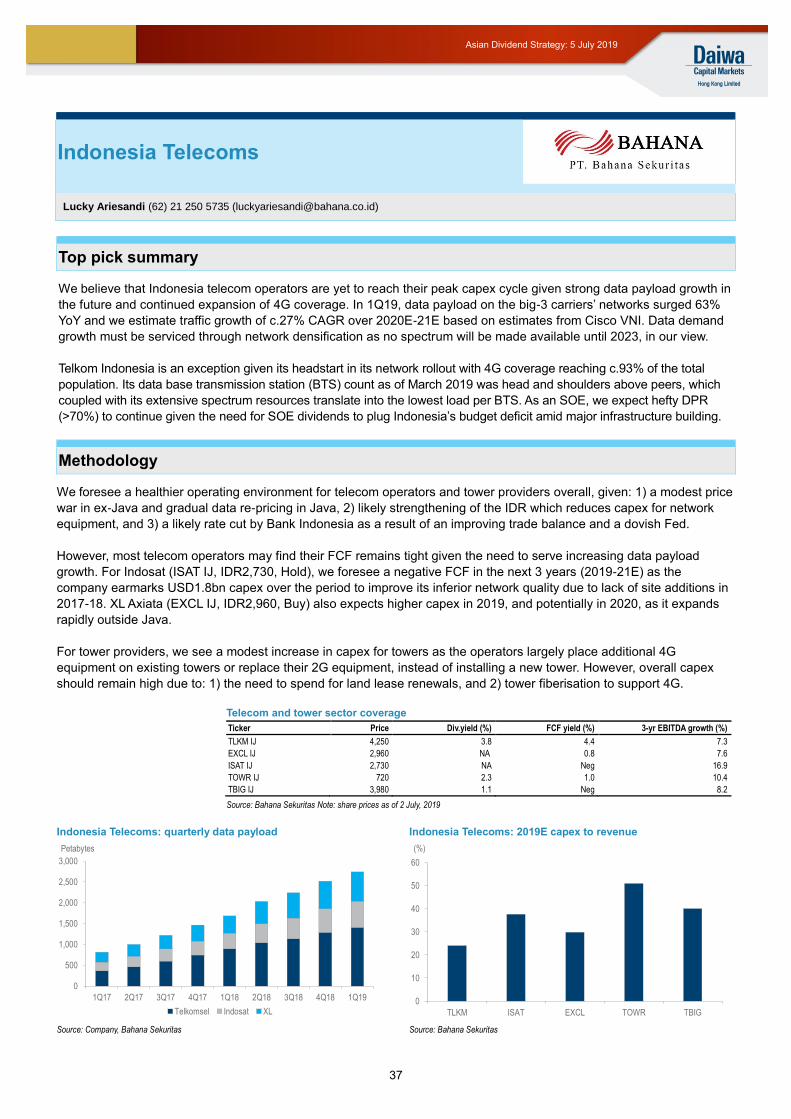

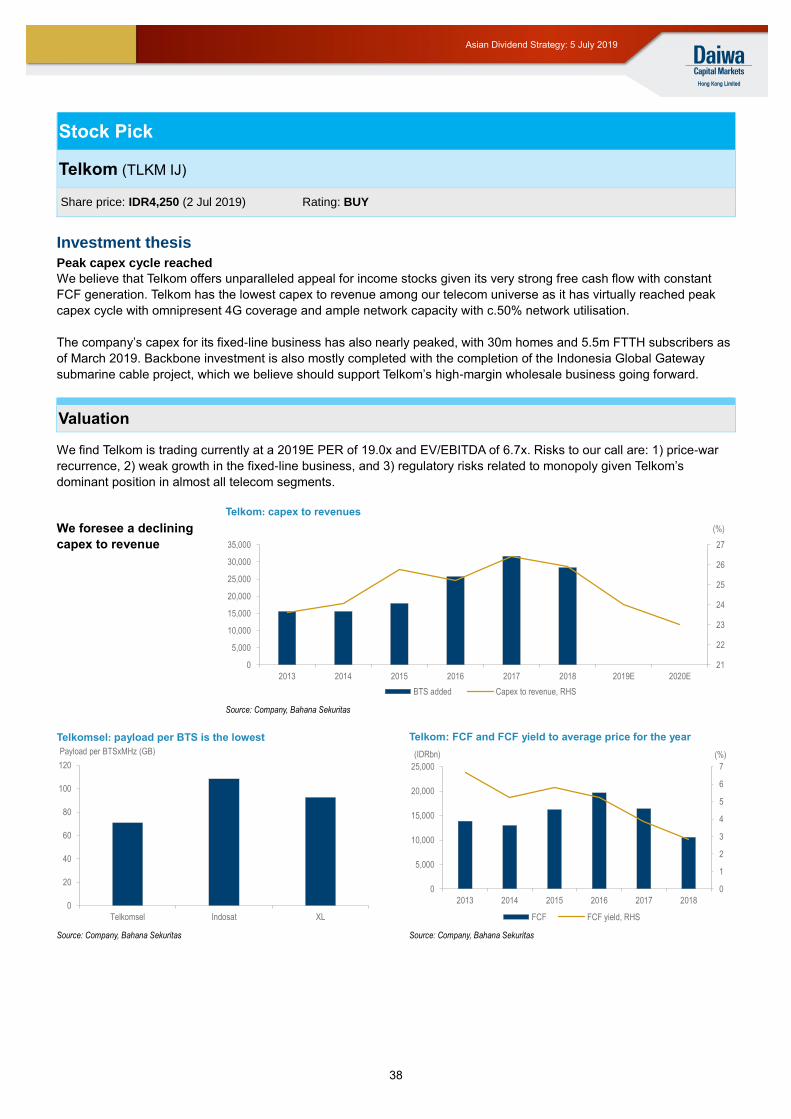

In Indonesia, Bahana Securities’ telecom analyst, Lucky Ariesandi, broadly follows the

Animal Spirits dividend sustainability criteria. He selects Telekomunikasi Indonesia (TLKM

IJ, IDR4,520, BUY). Based on his model, the 4% dividend yield and strong free cash flow

generation, with a free cash flow yield of 4.7%, are supportive of his positive sustainable

yield viewpoint. He notes that there are limited capex risks as network capacity is at c.50%

utilization. Animal Spirits does note that the yield spread with local government bonds is

negative (see table on page 6).

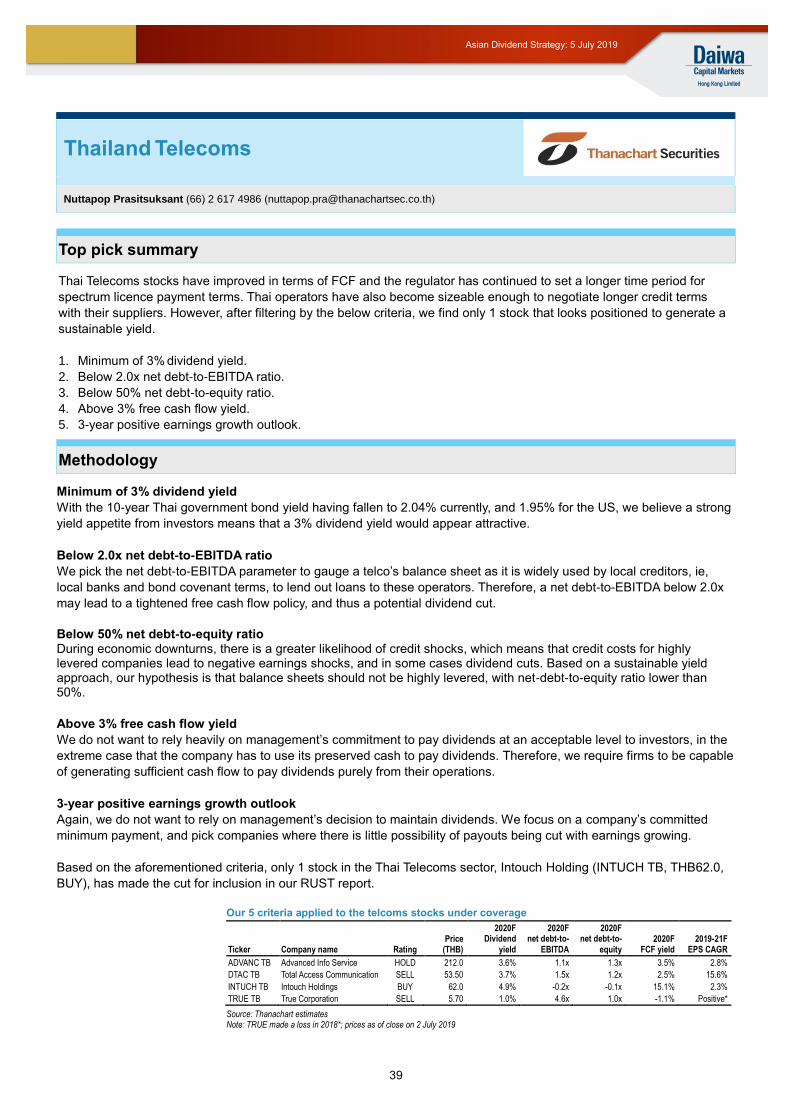

Finally, Nuttapop Prasitsuksant, Thanachart’s telecom analyst, sets out his sustainable

yield criteria as: minimum dividend yield of 3%; net debt-to-EBITDA less than 2x; greater

than 3% free cash flow yield; and 3 years’ positive earnings-growth outlook. Based on his

criteria, he picks Intouch Holdings (INTUCH TB, THB62, BUY).

This completes our summary of the sustainable yield ideas presented in this report. To

follow is a summary of Daiwa’s APAC market and sector views, together with a compilation

of our Animal Spirits Top Picks. Thereafter is a section including the detailed contributions

from Daiwa and alliance partner sector analysts.

Rama Maruvada likes

China Telecom. Based

on his model, the

dividend yield for 2019E

is 3.4%, growing to 4% in

2021E, net debt-to-

EBITDA is 0.45x and

dividends as a

percentage of free cash

flow is 28%. The risk is

an overshoot on 5G

capex but network

sharing is a good

chance. This is an

Animal Spirits Top Pick!

10

Asian Dividend Strategy: 5 July 2019

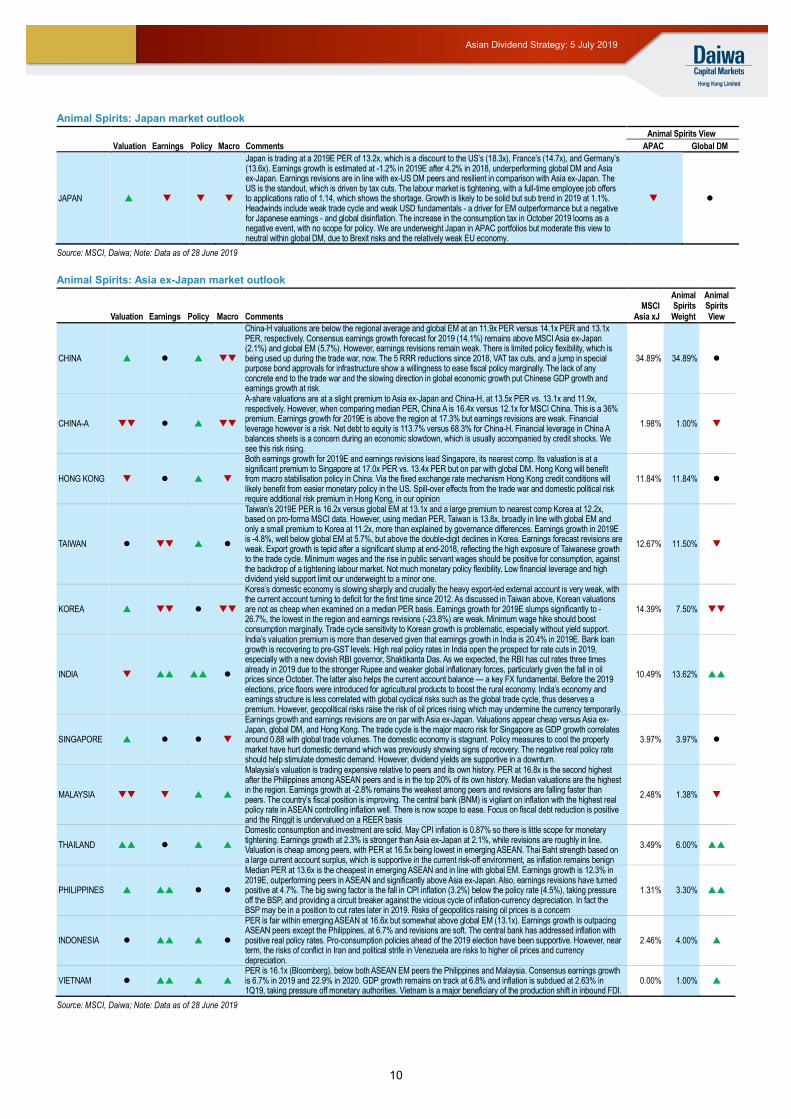

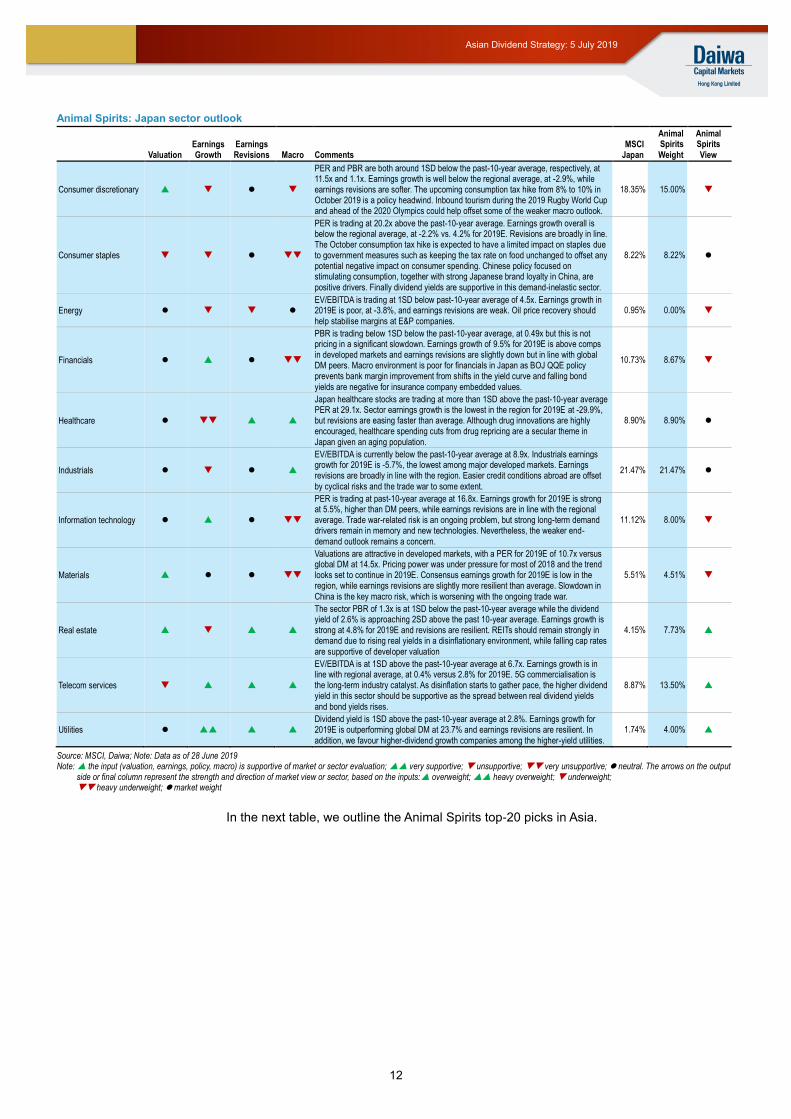

Animal Spirits: Japan market outlook

Valuation Earnings Policy Macro Comments

Animal Spirits View

APAC Global DM

JAPAN

Japan is trading at a 2019E PER of 13.2x, which is a discount to the US’s (18.3x), France’s (14.7x), and Germany’s (13.6x). Earnings growth is estimated at -1.2% in 2019E after 4.2% in 2018, underperforming global DM and Asia ex-Japan. Earnings revisions are in line with ex-US DM peers and resilient in comparison with Asia ex-Japan. The US is the standout, which is driven by tax cuts. The labour market is tightening, with a full-time employee job offers to applications ratio of 1.14, which shows the shortage. Growth is likely to be solid but sub trend in 2019 at 1.1%. Headwinds include weak trade cycle and weak USD fundamentals - a driver for EM outperformance but a negative for Japanese earnings - and global disinflation. The increase in the consumption tax in October 2019 looms as a negative event, with no scope for policy. We are underweight Japan in APAC portfolios but moderate this view to neutral within global DM, due to Brexit risks and the relatively weak EU economy.

Source: MSCI, Daiwa; Note: Data as of 28 June 2019

Animal Spirits: Asia ex-Japan market outlook

Valuation Earnings Policy Macro Comments MSCI

Asia xJ

Animal Spirits Weight

Animal Spirits View

CHINA

China-H valuations are below the regional average and global EM at an 11.9x PER versus 14.1x PER and 13.1x PER, respectively. Consensus earnings growth forecast for 2019 (14.1%) remains above MSCI Asia ex-Japan (2.1%) and global EM (5.7%). However, earnings revisions remain weak. There is limited policy flexibility, which is being used up during the trade war, now. The 5 RRR reductions since 2018, VAT tax cuts, and a jump in special purpose bond approvals for infrastructure show a willingness to ease fiscal policy marginally. The lack of any concrete end to the trade war and the slowing direction in global economic growth put Chinese GDP growth and earnings growth at risk.

34.89% 34.89%

CHINA-A

A-share valuations are at a slight premium to Asia ex-Japan and China-H, at 13.5x PER vs. 13.1x and 11.9x, respectively. However, when comparing median PER, China A is 16.4x versus 12.1x for MSCI China. This is a 36% premium. Earnings growth for 2019E is above the region at 17.3% but earnings revisions are weak. Financial leverage however is a risk. Net debt to equity is 113.7% versus 68.3% for China-H. Financial leverage in China A balances sheets is a concern during an economic slowdown, which is usually accompanied by credit shocks. We see this risk rising.

1.98% 1.00%

HONG KONG

Both earnings growth for 2019E and earnings revisions lead Singapore, its nearest comp. Its valuation is at a significant premium to Singapore at 17.0x PER vs. 13.4x PER but on par with global DM. Hong Kong will benefit from macro stabilisation policy in China. Via the fixed exchange rate mechanism Hong Kong credit conditions will likely benefit from easier monetary policy in the US. Spill-over effects from the trade war and domestic political risk require additional risk premium in Hong Kong, in our opinion

11.84% 11.84%

TAIWAN

Taiwan’s 2019E PER is 16.2x versus global EM at 13.1x and a large premium to nearest comp Korea at 12.2x, based on pro-forma MSCI data. However, using median PER, Taiwan is 13.8x, broadly in line with global EM and only a small premium to Korea at 11.2x, more than explained by governance differences. Earnings growth in 2019E is -4.8%, well below global EM at 5.7%, but above the double-digit declines in Korea. Earnings forecast revisions are weak. Export growth is tepid after a significant slump at end-2018, reflecting the high exposure of Taiwanese growth to the trade cycle. Minimum wages and the rise in public servant wages should be positive for consumption, against the backdrop of a tightening labour market. Not much monetary policy flexibility. Low financial leverage and high dividend yield support limit our underweight to a minor one.

12.67% 11.50%

KOREA

Korea’s domestic economy is slowing sharply and crucially the heavy export-led external account is very weak, with the current account turning to deficit for the first time since 2012. As discussed in Taiwan above, Korean valuations are not as cheap when examined on a median PER basis. Earnings growth for 2019E slumps significantly to -26.7%, the lowest in the region and earnings revisions (-23.8%) are weak. Minimum wage hike should boost consumption marginally. Trade cycle sensitivity to Korean growth is problematic, especially without yield support.

14.39% 7.50%

INDIA

India’s valuation premium is more than deserved given that earnings growth in India is 20.4% in 2019E. Bank loan growth is recovering to pre-GST levels. High real policy rates in India open the prospect for rate cuts in 2019, especially with a new dovish RBI governor, Shaktikanta Das. As we expected, the RBI has cut rates three times already in 2019 due to the stronger Rupee and weaker global inflationary forces, particularly given the fall in oil prices since October. The latter also helps the current account balance — a key FX fundamental. Before the 2019 elections, price floors were introduced for agricultural products to boost the rural economy. India’s economy and earnings structure is less correlated with global cyclical risks such as the global trade cycle, thus deserves a premium. However, geopolitical risks raise the risk of oil prices rising which may undermine the currency temporarily.

10.49% 13.62%

SINGAPORE

Earnings growth and earnings revisions are on par with Asia ex-Japan. Valuations appear cheap versus Asia ex-Japan, global DM, and Hong Kong. The trade cycle is the major macro risk for Singapore as GDP growth correlates around 0.88 with global trade volumes. The domestic economy is stagnant. Policy measures to cool the property market have hurt domestic demand which was previously showing signs of recovery. The negative real policy rate should help stimulate domestic demand. However, dividend yields are supportive in a downturn.

3.97% 3.97%

MALAYSIA

Malaysia’s valuation is trading expensive relative to peers and its own history. PER at 16.8x is the second highest after the Philippines among ASEAN peers and is in the top 20% of its own history. Median valuations are the highest in the region. Earnings growth at -2.8% remains the weakest among peers and revisions are falling faster than peers. The country’s fiscal position is improving. The central bank (BNM) is vigilant on inflation with the highest real policy rate in ASEAN controlling inflation well. There is now scope to ease. Focus on fiscal debt reduction is positive and the Ringgit is undervalued on a REER basis

2.48% 1.38%

THAILAND

Domestic consumption and investment are solid. May CPI inflation is 0.87% so there is little scope for monetary tightening. Earnings growth at 2.3% is stronger than Asia ex-Japan at 2.1%, while revisions are roughly in line. Valuation is cheap among peers, with PER at 16.5x being lowest in emerging ASEAN. Thai Baht strength based on a large current account surplus, which is supportive in the current risk-off environment, as inflation remains benign

3.49% 6.00%

PHILIPPINES

Median PER at 13.6x is the cheapest in emerging ASEAN and in line with global EM. Earnings growth is 12.3% in 2019E, outperforming peers in ASEAN and significantly above Asia ex-Japan. Also, earnings revisions have turned positive at 4.7%. The big swing factor is the fall in CPI inflation (3.2%) below the policy rate (4.5%), taking pressure off the BSP, and providing a circuit breaker against the vicious cycle of inflation-currency depreciation. In fact the BSP may be in a position to cut rates later in 2019. Risks of geopolitics raising oil prices is a concern

1.31% 3.30%

INDONESIA

PER is fair within emerging ASEAN at 16.6x but somewhat above global EM (13.1x). Earnings growth is outpacing ASEAN peers except the Philippines, at 6.7% and revisions are soft. The central bank has addressed inflation with positive real policy rates. Pro-consumption policies ahead of the 2019 election have been supportive. However, near term, the risks of conflict in Iran and political strife in Venezuela are risks to higher oil prices and currency depreciation.

2.46% 4.00%

VIETNAM

PER is 16.1x (Bloomberg), below both ASEAN EM peers the Philippines and Malaysia. Consensus earnings growth is 6.7% in 2019 and 22.9% in 2020. GDP growth remains on track at 6.8% and inflation is subdued at 2.63% in 1Q19, taking pressure off monetary authorities. Vietnam is a major beneficiary of the production shift in inbound FDI.

0.00% 1.00%

Source: MSCI, Daiwa; Note: Data as of 28 June 2019

11

Asian Dividend Strategy: 5 July 2019

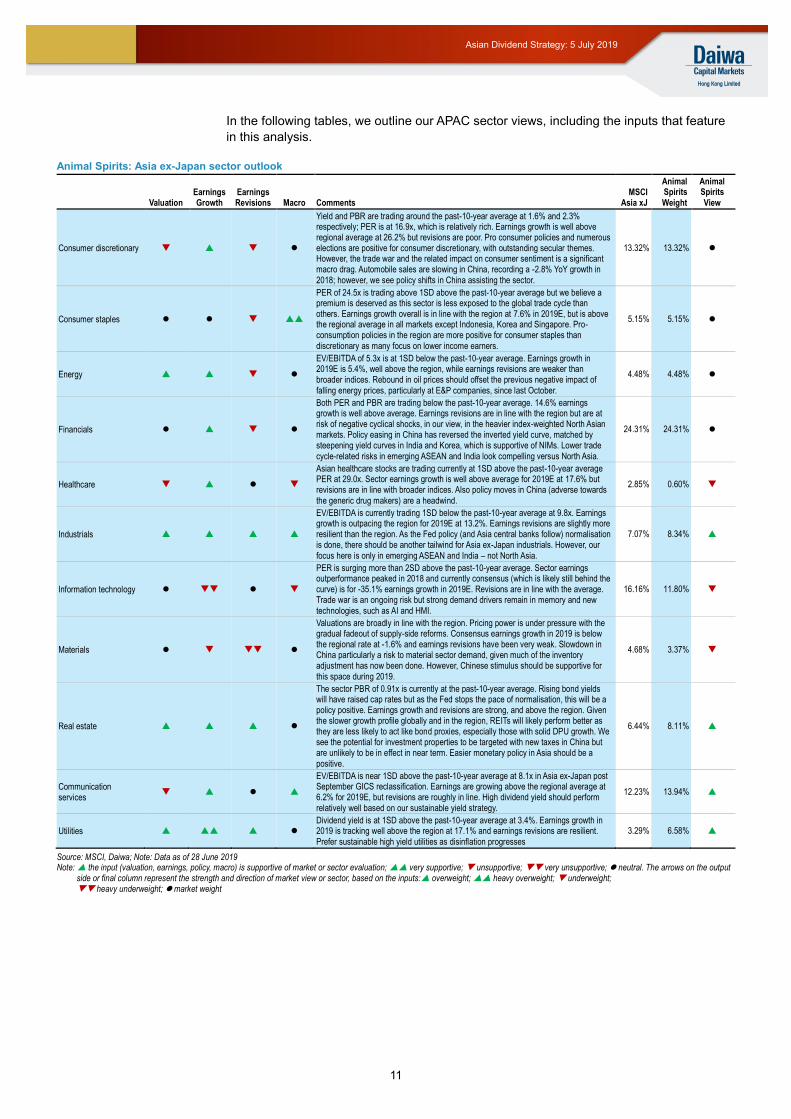

In the following tables, we outline our APAC sector views, including the inputs that feature

in this analysis.

Animal Spirits: Asia ex-Japan sector outlook

Valuation Earnings Growth

Earnings Revisions Macro Comments

MSCI Asia xJ

Animal Spirits Weight

Animal Spirits View

Consumer discretionary

Yield and PBR are trading around the past-10-year average at 1.6% and 2.3% respectively; PER is at 16.9x, which is relatively rich. Earnings growth is well above regional average at 26.2% but revisions are poor. Pro consumer policies and numerous elections are positive for consumer discretionary, with outstanding secular themes. However, the trade war and the related impact on consumer sentiment is a significant macro drag. Automobile sales are slowing in China, recording a -2.8% YoY growth in 2018; however, we see policy shifts in China assisting the sector.

13.32% 13.32%

Consumer staples

PER of 24.5x is trading above 1SD above the past-10-year average but we believe a premium is deserved as this sector is less exposed to the global trade cycle than others. Earnings growth overall is in line with the region at 7.6% in 2019E, but is above the regional average in all markets except Indonesia, Korea and Singapore. Pro-consumption policies in the region are more positive for consumer staples than discretionary as many focus on lower income earners.

5.15% 5.15%

Energy

EV/EBITDA of 5.3x is at 1SD below the past-10-year average. Earnings growth in 2019E is 5.4%, well above the region, while earnings revisions are weaker than broader indices. Rebound in oil prices should offset the previous negative impact of falling energy prices, particularly at E&P companies, since last October.

4.48% 4.48%

Financials

Both PER and PBR are trading below the past-10-year average. 14.6% earnings growth is well above average. Earnings revisions are in line with the region but are at risk of negative cyclical shocks, in our view, in the heavier index-weighted North Asian markets. Policy easing in China has reversed the inverted yield curve, matched by steepening yield curves in India and Korea, which is supportive of NIMs. Lower trade cycle-related risks in emerging ASEAN and India look compelling versus North Asia.

24.31% 24.31%

Healthcare

Asian healthcare stocks are trading currently at 1SD above the past-10-year average PER at 29.0x. Sector earnings growth is well above average for 2019E at 17.6% but revisions are in line with broader indices. Also policy moves in China (adverse towards the generic drug makers) are a headwind.

2.85% 0.60%

Industrials

EV/EBITDA is currently trading 1SD below the past-10-year average at 9.8x. Earnings growth is outpacing the region for 2019E at 13.2%. Earnings revisions are slightly more resilient than the region. As the Fed policy (and Asia central banks follow) normalisation is done, there should be another tailwind for Asia ex-Japan industrials. However, our focus here is only in emerging ASEAN and India – not North Asia.

7.07% 8.34%

Information technology

PER is surging more than 2SD above the past-10-year average. Sector earnings outperformance peaked in 2018 and currently consensus (which is likely still behind the curve) is for -35.1% earnings growth in 2019E. Revisions are in line with the average. Trade war is an ongoing risk but strong demand drivers remain in memory and new technologies, such as AI and HMI.

16.16% 11.80%

Materials

Valuations are broadly in line with the region. Pricing power is under pressure with the gradual fadeout of supply-side reforms. Consensus earnings growth in 2019 is below the regional rate at -1.6% and earnings revisions have been very weak. Slowdown in China particularly a risk to material sector demand, given much of the inventory adjustment has now been done. However, Chinese stimulus should be supportive for this space during 2019.

4.68% 3.37%

Real estate

The sector PBR of 0.91x is currently at the past-10-year average. Rising bond yields will have raised cap rates but as the Fed stops the pace of normalisation, this will be a policy positive. Earnings growth and revisions are strong, and above the region. Given the slower growth profile globally and in the region, REITs will likely perform better as they are less likely to act like bond proxies, especially those with solid DPU growth. We see the potential for investment properties to be targeted with new taxes in China but are unlikely to be in effect in near term. Easier monetary policy in Asia should be a positive.

6.44% 8.11%

Communication services

EV/EBITDA is near 1SD above the past-10-year average at 8.1x in Asia ex-Japan post September GICS reclassification. Earnings are growing above the regional average at 6.2% for 2019E, but revisions are roughly in line. High dividend yield should perform relatively well based on our sustainable yield strategy.

12.23% 13.94%

Utilities

Dividend yield is at 1SD above the past-10-year average at 3.4%. Earnings growth in 2019 is tracking well above the region at 17.1% and earnings revisions are resilient. Prefer sustainable high yield utilities as disinflation progresses

3.29% 6.58%

Source: MSCI, Daiwa; Note: Data as of 28 June 2019 Note: the input (valuation, earnings, policy, macro) is supportive of market or sector evaluation; very supportive; unsupportive; very unsupportive; neutral. The arrows on the output

side or final column represent the strength and direction of market view or sector, based on the inputs: overweight; heavy overweight; underweight; heavy underweight; market weight

12

Asian Dividend Strategy: 5 July 2019

Animal Spirits: Japan sector outlook

Valuation Earnings Growth

Earnings Revisions Macro Comments

MSCI Japan

Animal Spirits Weight

Animal Spirits View

Consumer discretionary

PER and PBR are both around 1SD below the past-10-year average, respectively, at 11.5x and 1.1x. Earnings growth is well below the regional average, at -2.9%, while earnings revisions are softer. The upcoming consumption tax hike from 8% to 10% in October 2019 is a policy headwind. Inbound tourism during the 2019 Rugby World Cup and ahead of the 2020 Olympics could help offset some of the weaker macro outlook.

18.35% 15.00%

Consumer staples

PER is trading at 20.2x above the past-10-year average. Earnings growth overall is below the regional average, at -2.2% vs. 4.2% for 2019E. Revisions are broadly in line. The October consumption tax hike is expected to have a limited impact on staples due to government measures such as keeping the tax rate on food unchanged to offset any potential negative impact on consumer spending. Chinese policy focused on stimulating consumption, together with strong Japanese brand loyalty in China, are positive drivers. Finally dividend yields are supportive in this demand-inelastic sector.

8.22% 8.22%

Energy

EV/EBITDA is trading at 1SD below past-10-year average of 4.5x. Earnings growth in 2019E is poor, at -3.8%, and earnings revisions are weak. Oil price recovery should help stabilise margins at E&P companies.

0.95% 0.00%

Financials

PBR is trading below 1SD below the past-10-year average, at 0.49x but this is not pricing in a significant slowdown. Earnings growth of 9.5% for 2019E is above comps in developed markets and earnings revisions are slightly down but in line with global DM peers. Macro environment is poor for financials in Japan as BOJ QQE policy prevents bank margin improvement from shifts in the yield curve and falling bond yields are negative for insurance company embedded values.

10.73% 8.67%

Healthcare

Japan healthcare stocks are trading at more than 1SD above the past-10-year average PER at 29.1x. Sector earnings growth is the lowest in the region for 2019E at -29.9%, but revisions are easing faster than average. Although drug innovations are highly encouraged, healthcare spending cuts from drug repricing are a secular theme in Japan given an aging population.

8.90% 8.90%

Industrials

EV/EBITDA is currently below the past-10-year average at 8.9x. Industrials earnings growth for 2019E is -5.7%, the lowest among major developed markets. Earnings revisions are broadly in line with the region. Easier credit conditions abroad are offset by cyclical risks and the trade war to some extent.

21.47% 21.47%

Information technology

PER is trading at past-10-year average at 16.8x. Earnings growth for 2019E is strong at 5.5%, higher than DM peers, while earnings revisions are in line with the regional average. Trade war-related risk is an ongoing problem, but strong long-term demand drivers remain in memory and new technologies. Nevertheless, the weaker end-demand outlook remains a concern.

11.12% 8.00%

Materials

Valuations are attractive in developed markets, with a PER for 2019E of 10.7x versus global DM at 14.5x. Pricing power was under pressure for most of 2018 and the trend looks set to continue in 2019E. Consensus earnings growth for 2019E is low in the region, while earnings revisions are slightly more resilient than average. Slowdown in China is the key macro risk, which is worsening with the ongoing trade war.

5.51% 4.51%

Real estate

The sector PBR of 1.3x is at 1SD below the past-10-year average while the dividend yield of 2.6% is approaching 2SD above the past 10-year average. Earnings growth is strong at 4.8% for 2019E and revisions are resilient. REITs should remain strongly in demand due to rising real yields in a disinflationary environment, while falling cap rates are supportive of developer valuation

4.15% 7.73%

Telecom services

EV/EBITDA is at 1SD above the past-10-year average at 6.7x. Earnings growth is in line with regional average, at 0.4% versus 2.8% for 2019E. 5G commercialisation is the long-term industry catalyst. As disinflation starts to gather pace, the higher dividend yield in this sector should be supportive as the spread between real dividend yields and bond yields rises.

8.87% 13.50%

Utilities

Dividend yield is 1SD above the past-10-year average at 2.8%. Earnings growth for 2019E is outperforming global DM at 23.7% and earnings revisions are resilient. In addition, we favour higher-dividend growth companies among the higher-yield utilities.

1.74% 4.00%

Source: MSCI, Daiwa; Note: Data as of 28 June 2019 Note: the input (valuation, earnings, policy, macro) is supportive of market or sector evaluation; very supportive; unsupportive; very unsupportive; neutral. The arrows on the output

side or final column represent the strength and direction of market view or sector, based on the inputs: overweight; heavy overweight; underweight; heavy underweight; market weight

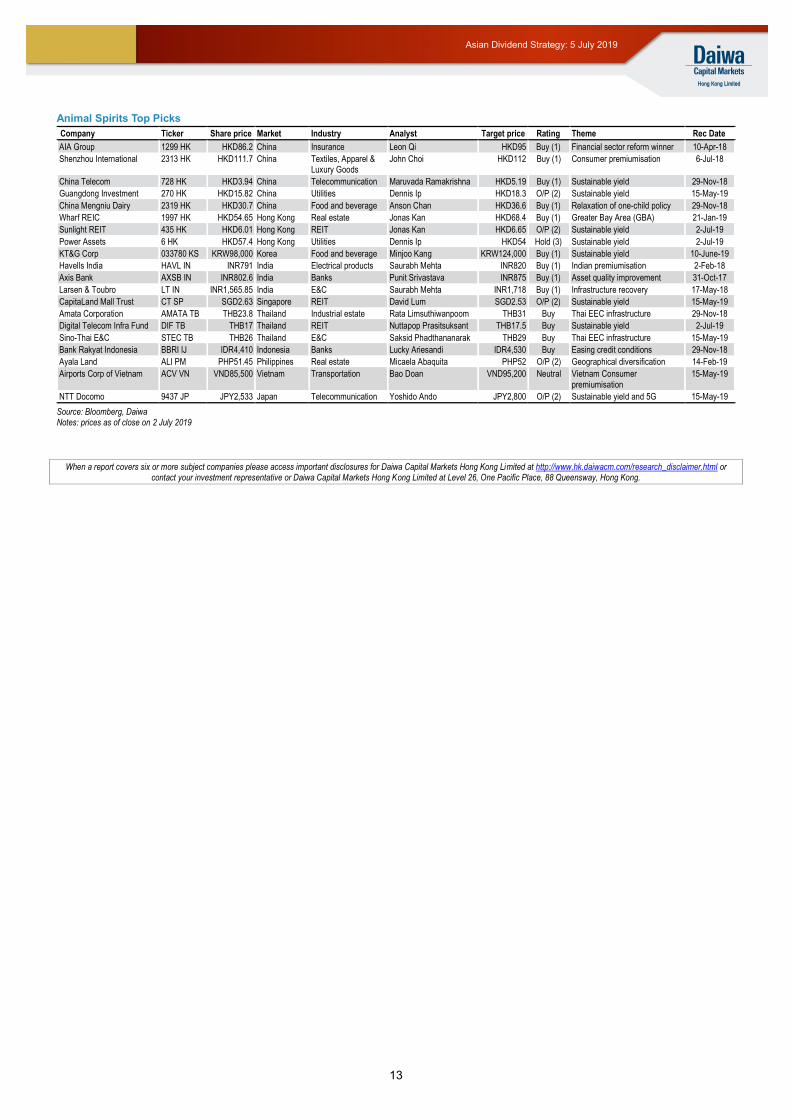

In the next table, we outline the Animal Spirits top-20 picks in Asia.

13

Asian Dividend Strategy: 5 July 2019

Animal Spirits Top Picks

Company Ticker Share price Market Industry Analyst Target price Rating Theme Rec Date

AIA Group 1299 HK HKD86.2 China Insurance Leon Qi HKD95 Buy (1) Financial sector reform winner 10-Apr-18

Shenzhou International 2313 HK HKD111.7 China Textiles, Apparel & Luxury Goods

John Choi HKD112 Buy (1) Consumer premiumisation 6-Jul-18

China Telecom 728 HK HKD3.94 China Telecommunication Maruvada Ramakrishna HKD5.19 Buy (1) Sustainable yield 29-Nov-18

Guangdong Investment 270 HK HKD15.82 China Utilities Dennis Ip HKD18.3 O/P (2) Sustainable yield 15-May-19

China Mengniu Dairy 2319 HK HKD30.7 China Food and beverage Anson Chan HKD36.6 Buy (1) Relaxation of one-child policy 29-Nov-18

Wharf REIC 1997 HK HKD54.65 Hong Kong Real estate Jonas Kan HKD68.4 Buy (1) Greater Bay Area (GBA) 21-Jan-19

Sunlight REIT 435 HK HKD6.01 Hong Kong REIT Jonas Kan HKD6.65 O/P (2) Sustainable yield 2-Jul-19

Power Assets 6 HK HKD57.4 Hong Kong Utilities Dennis Ip HKD54 Hold (3) Sustainable yield 2-Jul-19

KT&G Corp 033780 KS KRW98,000 Korea Food and beverage Minjoo Kang KRW124,000 Buy (1) Sustainable yield 10-June-19

Havells India HAVL IN INR791 India Electrical products Saurabh Mehta INR820 Buy (1) Indian premiumisation 2-Feb-18

Axis Bank AXSB IN INR802.6 India Banks Punit Srivastava INR875 Buy (1) Asset quality improvement 31-Oct-17

Larsen & Toubro LT IN INR1,565.85 India E&C Saurabh Mehta INR1,718 Buy (1) Infrastructure recovery 17-May-18

CapitaLand Mall Trust CT SP SGD2.63 Singapore REIT David Lum SGD2.53 O/P (2) Sustainable yield 15-May-19

Amata Corporation AMATA TB THB23.8 Thailand Industrial estate Rata Limsuthiwanpoom THB31 Buy Thai EEC infrastructure 29-Nov-18

Digital Telecom Infra Fund DIF TB THB17 Thailand REIT Nuttapop Prasitsuksant THB17.5 Buy Sustainable yield 2-Jul-19

Sino-Thai E&C STEC TB THB26 Thailand E&C Saksid Phadthananarak THB29 Buy Thai EEC infrastructure 15-May-19

Bank Rakyat Indonesia BBRI IJ IDR4,410 Indonesia Banks Lucky Ariesandi IDR4,530 Buy Easing credit conditions 29-Nov-18

Ayala Land ALI PM PHP51.45 Philippines Real estate Micaela Abaquita PHP52 O/P (2) Geographical diversification 14-Feb-19

Airports Corp of Vietnam ACV VN VND85,500 Vietnam Transportation Bao Doan VND95,200 Neutral Vietnam Consumer premiumisation

15-May-19

NTT Docomo 9437 JP JPY2,533 Japan Telecommunication Yoshido Ando JPY2,800 O/P (2) Sustainable yield and 5G 15-May-19

Source: Bloomberg, Daiwa Notes: prices as of close on 2 July 2019

When a report covers six or more subject companies please access important disclosures for Daiwa Capital Markets Hong Kong Limited at http://www.hk.daiwacm.com/research_disclaimer.html or

contact your investment representative or Daiwa Capital Markets Hong Kong Limited at Level 26, One Pacific Place, 88 Queensway, Hong Kong.

14

Asian Dividend Strategy: 5 July 2019

Recent Animal Spirits reports

Pan Asia Strategy Research

Risk off with an emerging-ASEAN & India geographical bias and an emphasis on sustainable dividend yield 2-Jul-19

China A downgrade – it is not personal, just cyclical 1-Jul-19

Endaka – the case for Japanese equity-JPY recoupling 20-Jun-19

Korea Strategy: Strong headwinds – trade cycle sensitivity and insufficient yield support as the global economy falters 10-Jun-19

India and emerging ASEAN are winners from oil rout 6-Jun-19

Why the Fed really cares about oil prices right now! 5-Jun-19

Spring cleaning! 16-May-19

ASEAN strategy: Cyclical hideouts, diverse themes and disinflation! 3-May-19

Sustainable yield preferred strategy during disinflation 2-Apr-19

Stealthy! Global trade cycle just dipped below zero … 26-Mar-19

Yield curve inversion, cyclical risks, roadmap, EM and APAC asset allocation 25-Mar-19

South-biased EM Asia strategy immune to DM woes? 14-Mar-19

APAC sector outlook summary 26-Feb-19

Asian bifurcation – disinflation exposes Japan to FX shocks; easing policy pressure in ASEAN and India 14-Feb-19

The Fed Pivot and 3 Key APAC Strategy FAQs 31-Jan-19

Final tactical EM-led rally? Overweight Asia ex-Japan, while downgrading Japan to underweight in APAC 21-Jan-19

G20 Takeaways - Trade De-escalation, not a Trade Ceasefire 03-Dec-18

APAC Equity Strategy - Outlook for 2019 29 Nov-18

A concise roadmap for 2019 and a peek beyond 16-Nov-18

Mixed Grill-Dividend strategy redux, the Malaysian budget, Section 7 and India central bank independence 5-Nov-18

ASEAN Focus macro, policy, valuation and earnings 31-Oct-18

Approaching but not yet in Asian Equity Value Zone 25-Oct-18

Trade Poker – Let’s go all in! 18-Oct-18

Greater China - Maintaining thematic focus, while risk-managing trade 28-Sep-18

Mense horribilis — will September mark a cathartic trough in EM, or will the bottom drop out? It depends! 7-Sep-18

APAC Consumer Themes: Patterns of force: premiumisation, Chinese tourism, pro-consumption policies, and other drivers 3-Sep-18

It’s the USD-EM pain trade but not an RMB bazooka 23-Jul-18

Summer super quick update — the consumer pivot! 06-Jul-18

Korea Strategy: Value, thematic diversity, and Northern optionality 12-Jun-18

Don’t trust the RUST! Dividend strategy and reflation 17-May-18

Micro theme — China’s growing private education firms 16-May-18

ASEAN update: focusing on the Malaysian election, Rupiah, Philippine rates, and updating our top picks 11-May-18

Détente or distraction? Korean peninsula scenarios 10-May-18

Align with the right paradigm, bottom fishers! 10-April-18

ASEAN Strategy: Infrastructure and reflationary tailwinds buffeted by the spectre of trade wars 29-Mar-18

Trade War or Skirmish - Impact on Asia? 23-Mar-18

Explaining valuation and bond yields during reflation 14-Mar-18

Stock picks in the Asian reflation trade — buy inflation sensitivity, dividend growers; avoid bond proxies 26-Feb-18

Dollar dazzlers — weak dollar ups the ante on Asian EM 02-Feb-18

The Asian inflation trade revival 02-Feb-18

Final country, sector, and Top Picks tune-up for 2017 06-Dec-17

Santa Edition — top 8 surprises for 2018 01-Dec-17

Reconciling Nifty-style and Asian small cap equities 23-Nov-17

Nifty-style, Korea, and the other seventy percent 15-Nov-17

Lighting the wick: Powell, gradualism, financial deregulation, and “risk on” in Asian equities 03-Nov-17

Source: Daiwa

15

Asian Dividend Strategy: 5 July 2019

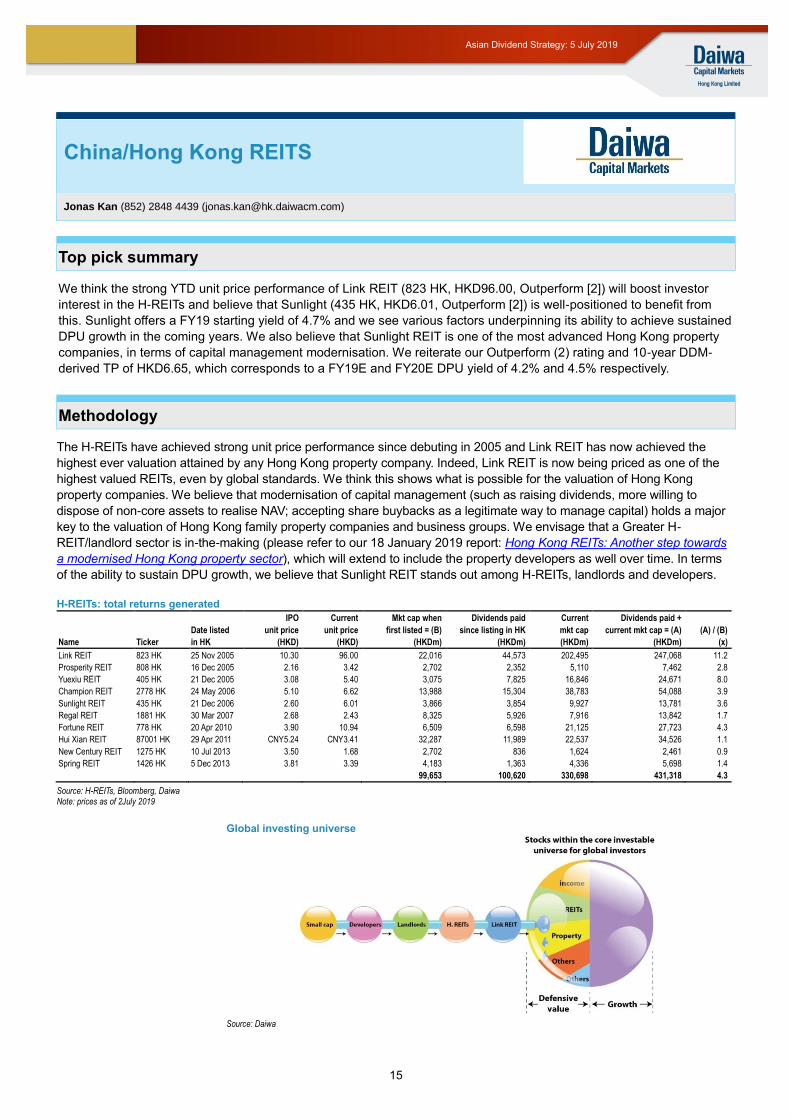

Top pick summary

We think the strong YTD unit price performance of Link REIT (823 HK, HKD96.00, Outperform [2]) will boost investor

interest in the H-REITs and believe that Sunlight (435 HK, HKD6.01, Outperform [2]) is well-positioned to benefit from

this. Sunlight offers a FY19 starting yield of 4.7% and we see various factors underpinning its ability to achieve sustained

DPU growth in the coming years. We also believe that Sunlight REIT is one of the most advanced Hong Kong property

companies, in terms of capital management modernisation. We reiterate our Outperform (2) rating and 10-year DDM-

derived TP of HKD6.65, which corresponds to a FY19E and FY20E DPU yield of 4.2% and 4.5% respectively.

Methodology

The H-REITs have achieved strong unit price performance since debuting in 2005 and Link REIT has now achieved the

highest ever valuation attained by any Hong Kong property company. Indeed, Link REIT is now being priced as one of the

highest valued REITs, even by global standards. We think this shows what is possible for the valuation of Hong Kong

property companies. We believe that modernisation of capital management (such as raising dividends, more willing to

dispose of non-core assets to realise NAV; accepting share buybacks as a legitimate way to manage capital) holds a major

key to the valuation of Hong Kong family property companies and business groups. We envisage that a Greater H-

REIT/landlord sector is in-the-making (please refer to our 18 January 2019 report: Hong Kong REITs: Another step towards

a modernised Hong Kong property sector), which will extend to include the property developers as well over time. In terms

of the ability to sustain DPU growth, we believe that Sunlight REIT stands out among H-REITs, landlords and developers.

H-REITs: total returns generated

IPO Current Mkt cap when Dividends paid Current Dividends paid +

Date listed unit price unit price first listed = (B) since listing in HK mkt cap current mkt cap = (A) (A) / (B)

Name Ticker in HK (HKD) (HKD) (HKDm) (HKDm) (HKDm) (HKDm) (x)

Link REIT 823 HK 25 Nov 2005 10.30 96.00 22,016 44,573 202,495 247,068 11.2

Prosperity REIT 808 HK 16 Dec 2005 2.16 3.42 2,702 2,352 5,110 7,462 2.8

Yuexiu REIT 405 HK 21 Dec 2005 3.08 5.40 3,075 7,825 16,846 24,671 8.0

Champion REIT 2778 HK 24 May 2006 5.10 6.62 13,988 15,304 38,783 54,088 3.9

Sunlight REIT 435 HK 21 Dec 2006 2.60 6.01 3,866 3,854 9,927 13,781 3.6

Regal REIT 1881 HK 30 Mar 2007 2.68 2.43 8,325 5,926 7,916 13,842 1.7

Fortune REIT 778 HK 20 Apr 2010 3.90 10.94 6,509 6,598 21,125 27,723 4.3

Hui Xian REIT 87001 HK 29 Apr 2011 CNY5.24 CNY3.41 32,287 11,989 22,537 34,526 1.1

New Century REIT 1275 HK 10 Jul 2013 3.50 1.68 2,702 836 1,624 2,461 0.9

Spring REIT 1426 HK 5 Dec 2013 3.81 3.39 4,183 1,363 4,336 5,698 1.4

99,653 100,620 330,698 431,318 4.3

Source: H-REITs, Bloomberg, Daiwa Note: prices as of 2July 2019

Global investing universe

Source: Daiwa

China/Hong Kong REITS

Jonas Kan (852) 2848 4439 ([email protected])

16

Asian Dividend Strategy: 5 July 2019

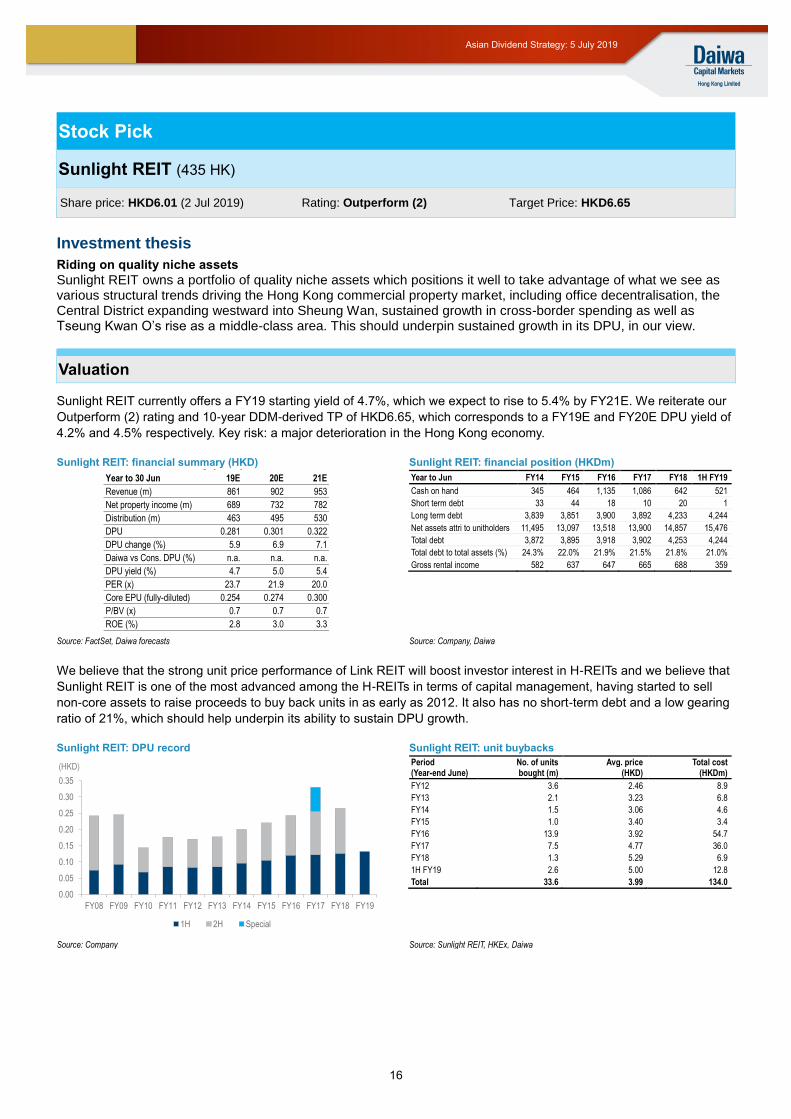

Stock Pick

Sunlight REIT (435 HK)

Investment thesis

Riding on quality niche assets

Sunlight REIT owns a portfolio of quality niche assets which positions it well to take advantage of what we see as various structural trends driving the Hong Kong commercial property market, including office decentralisation, the Central District expanding westward into Sheung Wan, sustained growth in cross-border spending as well as Tseung Kwan O’s rise as a middle-class area. This should underpin sustained growth in its DPU, in our view.

Valuation

Sunlight REIT currently offers a FY19 starting yield of 4.7%, which we expect to rise to 5.4% by FY21E. We reiterate our

Outperform (2) rating and 10-year DDM-derived TP of HKD6.65, which corresponds to a FY19E and FY20E DPU yield of

4.2% and 4.5% respectively. Key risk: a major deterioration in the Hong Kong economy.

Sunlight REIT: financial summary (HKD) Sunlight REIT: financial position (HKDm)

Year to Jun FY14 FY15 FY16 FY17 FY18 1H FY19

Cash on hand 345 464 1,135 1,086 642 521

Short term debt 33 44 18 10 20 1

Long term debt 3,839 3,851 3,900 3,892 4,233 4,244

Net assets attri to unitholders 11,495 13,097 13,518 13,900 14,857 15,476

Total debt 3,872 3,895 3,918 3,902 4,253 4,244

Total debt to total assets (%) 24.3% 22.0% 21.9% 21.5% 21.8% 21.0%

Gross rental income 582 637 647 665 688 359

Source: FactSet, Daiwa forecasts Source: Company, Daiwa

We believe that the strong unit price performance of Link REIT will boost investor interest in H-REITs and we believe that

Sunlight REIT is one of the most advanced among the H-REITs in terms of capital management, having started to sell

non-core assets to raise proceeds to buy back units in as early as 2012. It also has no short-term debt and a low gearing

ratio of 21%, which should help underpin its ability to sustain DPU growth.

Sunlight REIT: DPU record Sunlight REIT: unit buybacks

Period No. of units Avg. price Total cost (Year-end June) bought (m) (HKD) (HKDm)

FY12 3.6 2.46 8.9

FY13 2.1 3.23 6.8

FY14 1.5 3.06 4.6

FY15 1.0 3.40 3.4

FY16 13.9 3.92 54.7

FY17 7.5 4.77 36.0

FY18 1.3 5.29 6.9

1H FY19 2.6 5.00 12.8

Total 33.6 3.99 134.0

Source: Company Source: Sunlight REIT, HKEx, Daiwa

Financial summary (HKD)

Year to 30 Jun 19E 20E 21E

Revenue (m) 861 902 953

Net property income (m) 689 732 782

Distribution (m) 463 495 530

DPU 0.281 0.301 0.322

DPU change (%) 5.9 6.9 7.1

Daiwa vs Cons. DPU (%) n.a. n.a. n.a.

DPU yield (%) 4.7 5.0 5.4

PER (x) 23.7 21.9 20.0

Core EPU (fully-diluted) 0.254 0.274 0.300

P/BV (x) 0.7 0.7 0.7

ROE (%) 2.8 3.0 3.3

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19

1H 2H Special

(HKD)

Share price: HKD6.01 (2 Jul 2019) Rating: Outperform (2) Target Price: HKD6.65

17

Asian Dividend Strategy: 5 July 2019

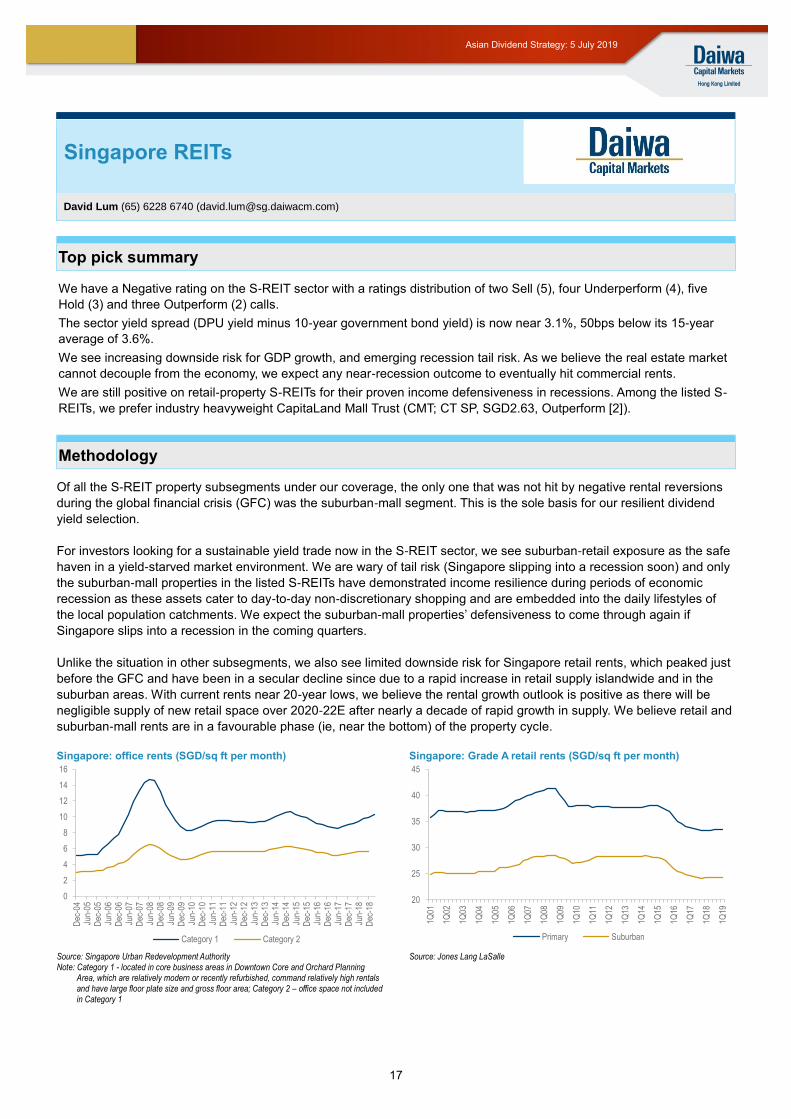

Top pick summary

We have a Negative rating on the S-REIT sector with a ratings distribution of two Sell (5), four Underperform (4), five

Hold (3) and three Outperform (2) calls.

The sector yield spread (DPU yield minus 10-year government bond yield) is now near 3.1%, 50bps below its 15-year

average of 3.6%.

We see increasing downside risk for GDP growth, and emerging recession tail risk. As we believe the real estate market

cannot decouple from the economy, we expect any near-recession outcome to eventually hit commercial rents.

We are still positive on retail-property S-REITs for their proven income defensiveness in recessions. Among the listed S-

REITs, we prefer industry heavyweight CapitaLand Mall Trust (CMT; CT SP, SGD2.63, Outperform [2]).

Methodology

Of all the S-REIT property subsegments under our coverage, the only one that was not hit by negative rental reversions

during the global financial crisis (GFC) was the suburban-mall segment. This is the sole basis for our resilient dividend

yield selection.

For investors looking for a sustainable yield trade now in the S-REIT sector, we see suburban-retail exposure as the safe

haven in a yield-starved market environment. We are wary of tail risk (Singapore slipping into a recession soon) and only

the suburban-mall properties in the listed S-REITs have demonstrated income resilience during periods of economic

recession as these assets cater to day-to-day non-discretionary shopping and are embedded into the daily lifestyles of

the local population catchments. We expect the suburban-mall properties’ defensiveness to come through again if

Singapore slips into a recession in the coming quarters.

Unlike the situation in other subsegments, we also see limited downside risk for Singapore retail rents, which peaked just

before the GFC and have been in a secular decline since due to a rapid increase in retail supply islandwide and in the

suburban areas. With current rents near 20-year lows, we believe the rental growth outlook is positive as there will be

negligible supply of new retail space over 2020-22E after nearly a decade of rapid growth in supply. We believe retail and

suburban-mall rents are in a favourable phase (ie, near the bottom) of the property cycle.

Singapore: office rents (SGD/sq ft per month) Singapore: Grade A retail rents (SGD/sq ft per month)

Source: Singapore Urban Redevelopment Authority Note: Category 1 - located in core business areas in Downtown Core and Orchard Planning

Area, which are relatively modern or recently refurbished, command relatively high rentals and have large floor plate size and gross floor area; Category 2 – office space not included in Category 1

Source: Jones Lang LaSalle

0

2

4

6

8

10

12

14

16

Dec

-04

Jun-

05D

ec-0

5Ju

n-06

Dec

-06

Jun-

07D

ec-0

7Ju

n-08

Dec

-08

Jun-

09D

ec-0

9Ju

n-10

Dec

-10

Jun-

11D

ec-1

1Ju

n-12

Dec

-12

Jun-

13D

ec-1

3Ju

n-14

Dec

-14

Jun-

15D

ec-1

5Ju

n-16

Dec

-16

Jun-

17D

ec-1

7Ju

n-18

Dec

-18

Category 1 Category 2

20

25

30

35

40

45

1Q01

1Q02

1Q03

1Q04

1Q05

1Q06

1Q07

1Q08

1Q09

1Q10

1Q11

1Q12

1Q13

1Q14

1Q15

1Q16

1Q17

1Q18

1Q19

Primary Suburban

Singapore REITs

David Lum (65) 6228 6740 ([email protected])

18

Asian Dividend Strategy: 5 July 2019

Stock Pick

CapitaLand Mall Trust (CT SP)

Investment thesis

Defensiveness plus growth

We believe CapitaLand Mall Trust (CMT) offers the best combination of DPU growth, yield and defensiveness (of DPU in

a severe-recession scenario) among the large-cap S-REITs.

With CMT having the largest absolute exposure to suburban malls, we see limited downside income risk from external

factors. CMT’s portfolio rental reversions have been weak in recent years, but we attribute the subdued performance to a

rapid build-up of retail space in recent years and CMT’s own overexposure to the Jurong East micro-market, which was

hit by a considerable portion of the new retail supply. We believe retail-space oversupply will no longer be an issue over

2020-22E with few mall openings over this period. Therefore, as long as rental reversions stay positive in the coming

years and portfolio occupancy remains high (98.8% as at 31 March 2019), CMT’s DPU is likely to be one of the most

sustainable in the sector, in our opinion.

As an added bonus, we expect CMT to achieve the strongest DPU growth (for 2020E and over a 3-year [2018-21E]

period) among the S-REITs under our coverage. We attribute the major growth driver to Funan, which opened on 28

June 2019. Funan, which closed in 2016 for a major redevelopment, has contributed nothing to CMT during its downtime.

From a zero base, we expect rental income as the retail and office tenants move in, following fit out, to progressively

ramp up from late 2019. Once operations have stabilised, we expect Funan to contribute 7% to CMT’s enlarged portfolio

on a net-property income (NPI) basis.

S-REITs under Daiwa coverage

Bloomberg ticker CCT SUN KREIT FCOT CT FCT SGREIT CRCT AREIT MINT MLT EREIT ART CDREIT Sector*

3-year DPU CAGR (%) 2.5 0.4 3.6 0.0 4.6 1.1 0.9 4.4 2.2 2.3 2.1 1.5 3.0 4.6 2.7

2019E YoY DPU growth (%) 2.6 0.2 2.3 0.0 2.8 2.0 1.1 3.2 1.8 2.8 3.9 3.0 3.9 5.0 2.6

2020E YoY DPU growth (%) 2.2 0.1 5.4 0.1 6.1 0.2 1.2 5.5 1.5 2.6 1.9 0.8 2.0 6.0 3.0

Source: Daiwa forecasts Note: *Weighted average by market cap

CMT: annual portfolio rental reversions CMT: quarterly rental reversions

Source: CMT Source: CMT

Valuation

CMT is trading at DPU yields of 4.5% for 2019E and 4.8% for 2020E. A downside risk to our call would be the