Completion Report

Project Numbers: 41116-013 and 41116-043

MFF Number: 0012

Loan Number: 3132

June 2021

India: Jammu and Kashmir Urban Sector Development Investment Program (Project 3 and Multitranche Financing Facility)

This document is being disclosed to the public in accordance with ADB’s Access to Information Policy.

CURRENCY EQUIVALENTS

Currency unit – Indian rupee/s (₹)

At Appraisal At Project Completion

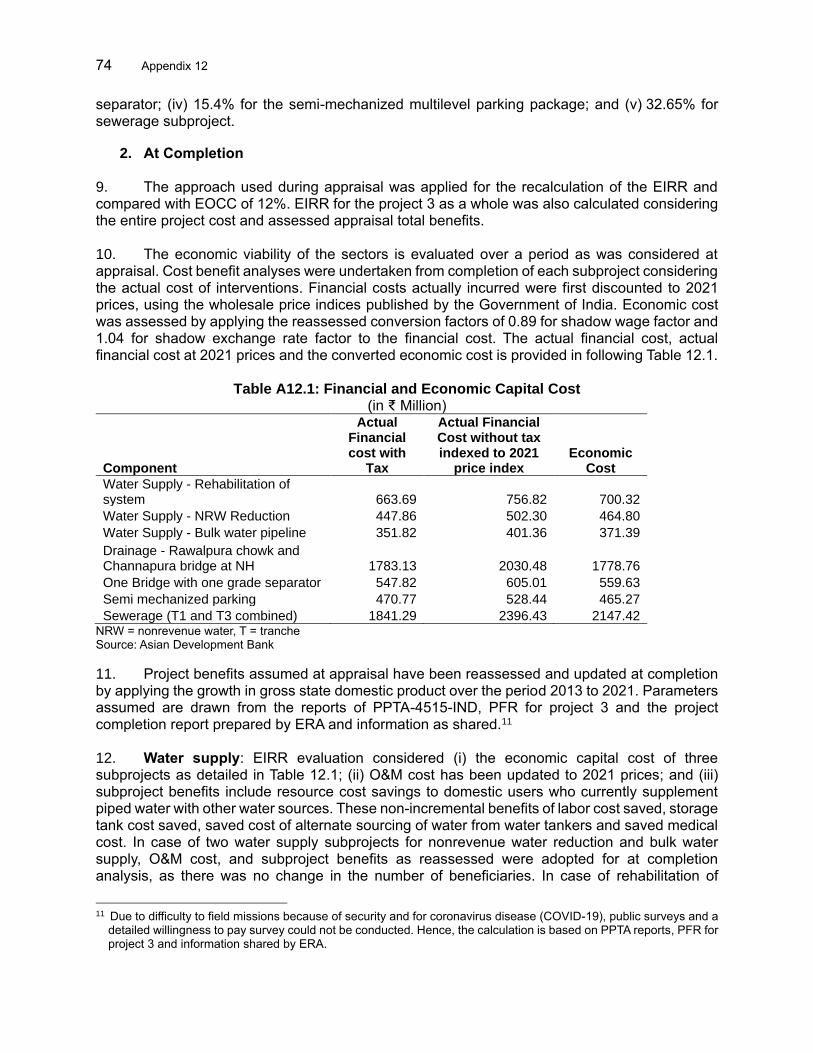

16 February 2007 2 November 2017 ₹1.00 = $0.0236 $0.0154 $1.00 = ₹42.375 ₹64.935

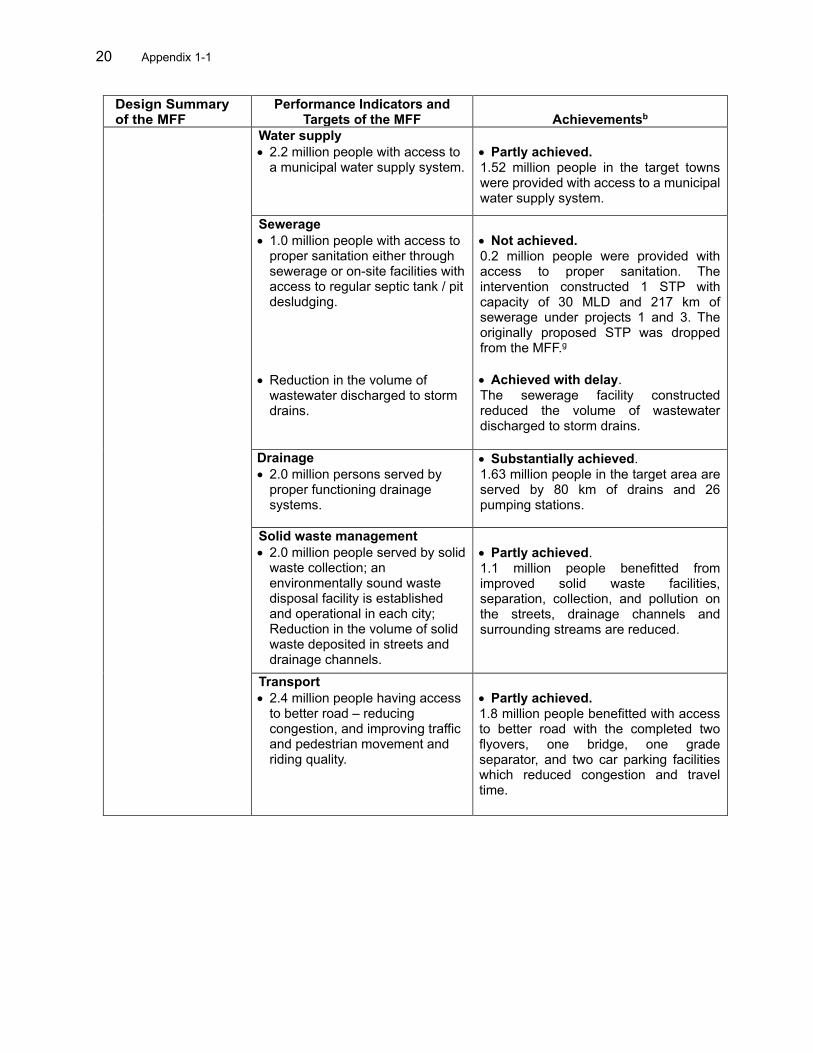

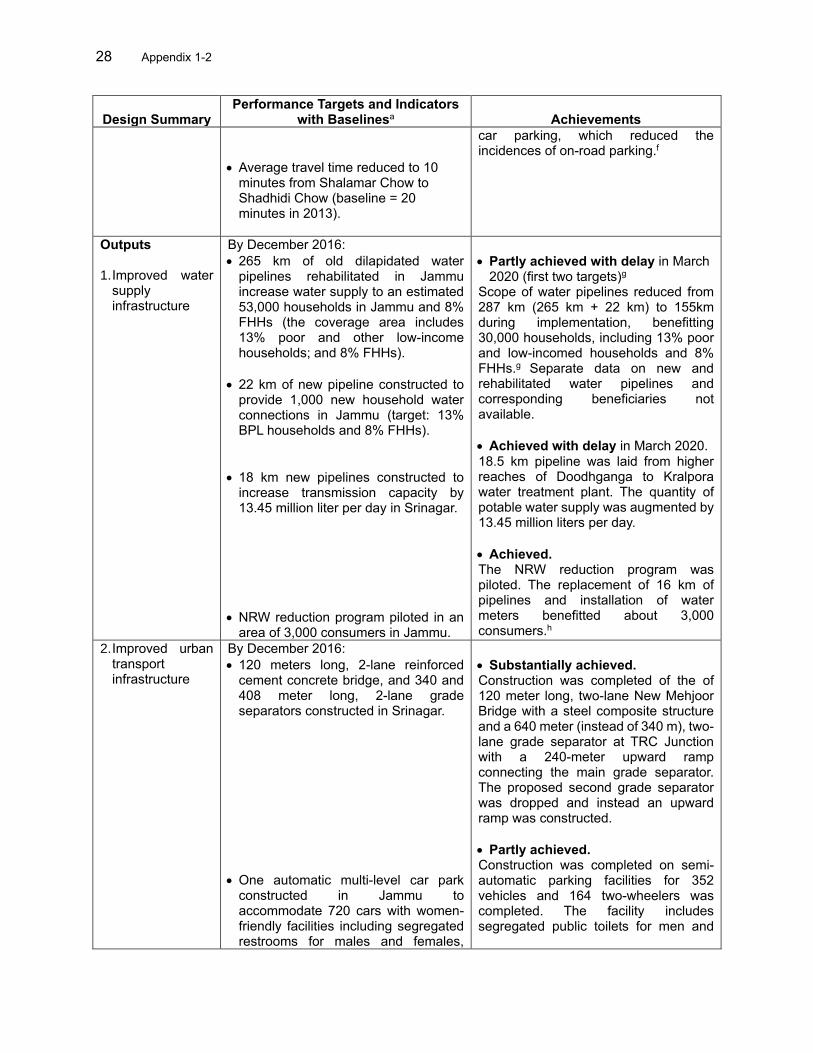

ABBREVIATIONS

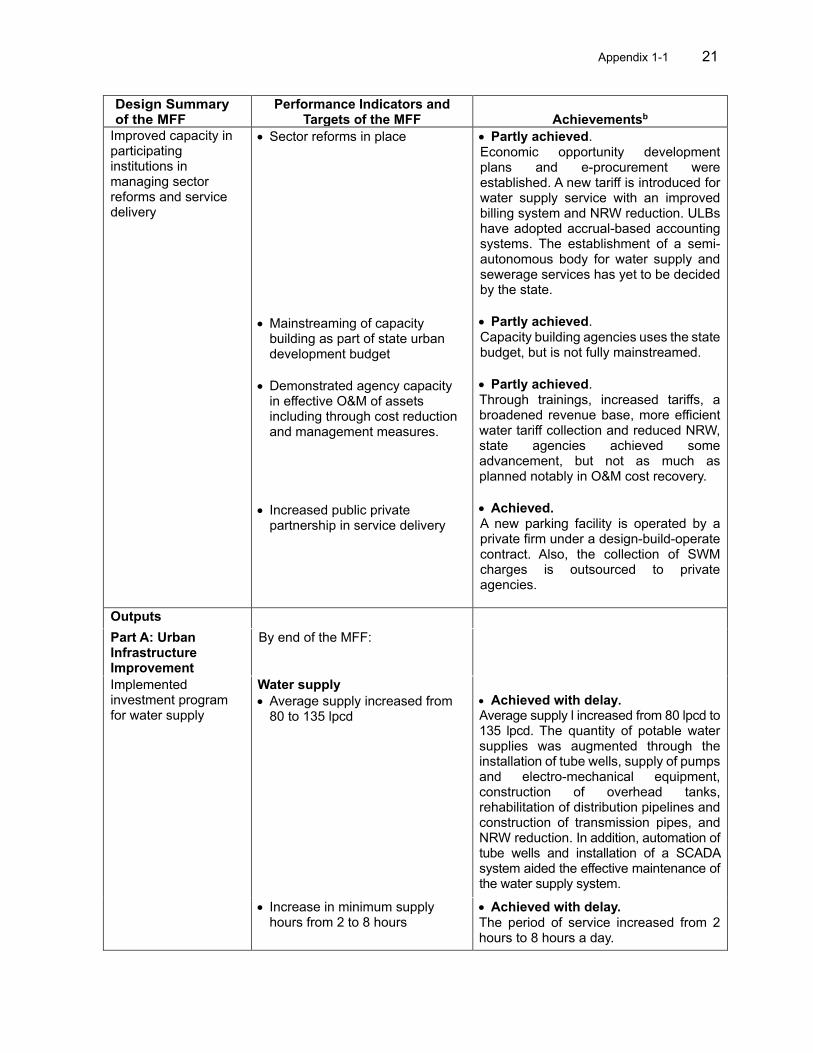

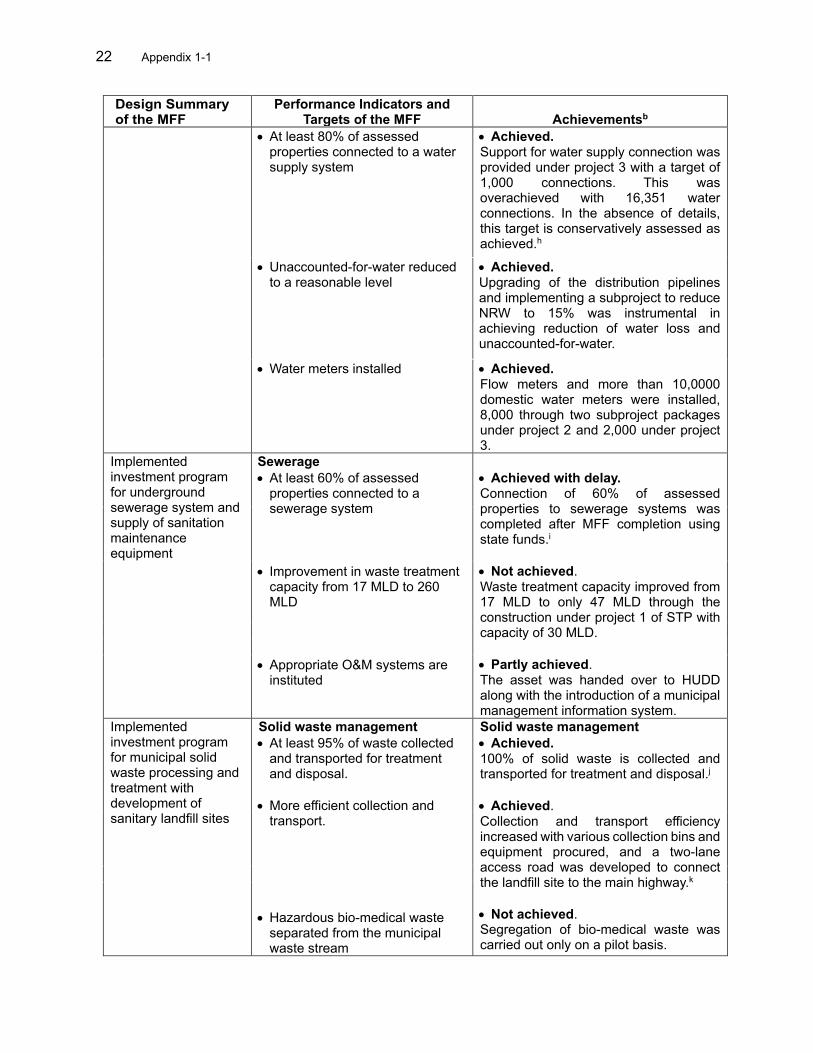

ADB – Asian Development Bank AEFS APFS CAGR

– – –

audited entity financial statement audited project financial statement compound annual growth rate

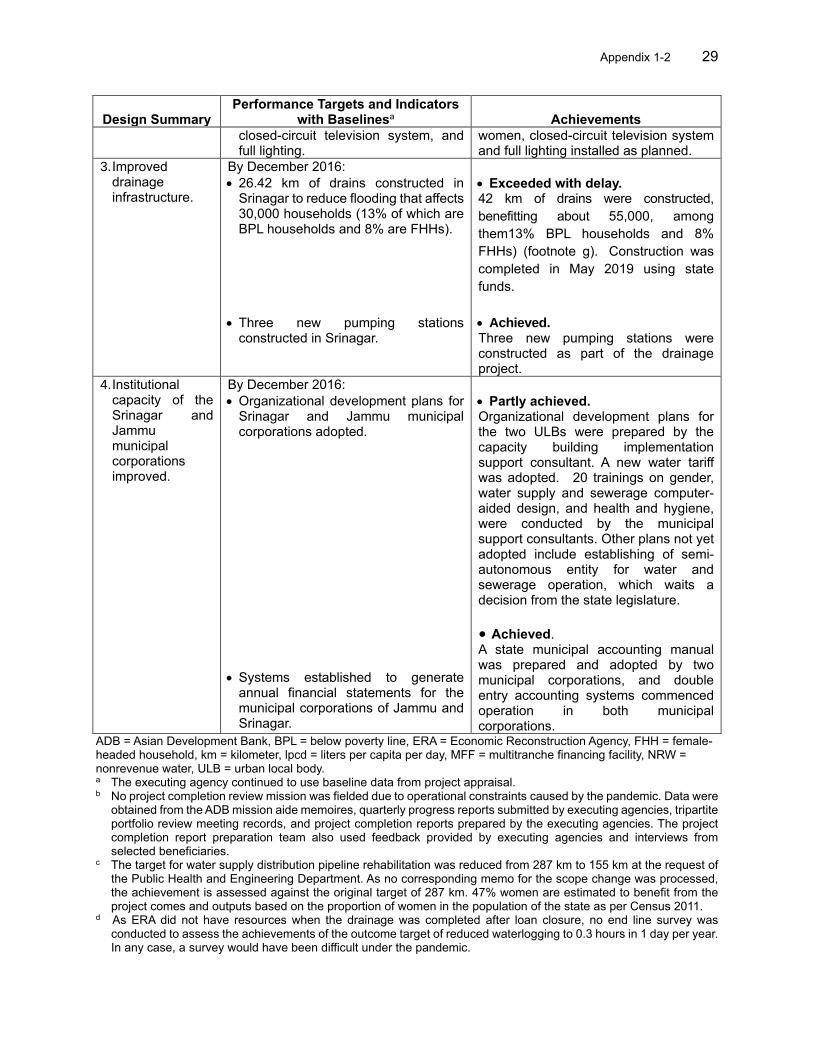

DMF – design and monitoring framework DSC – design and supervision consultant EIRR – economic internal rate of return

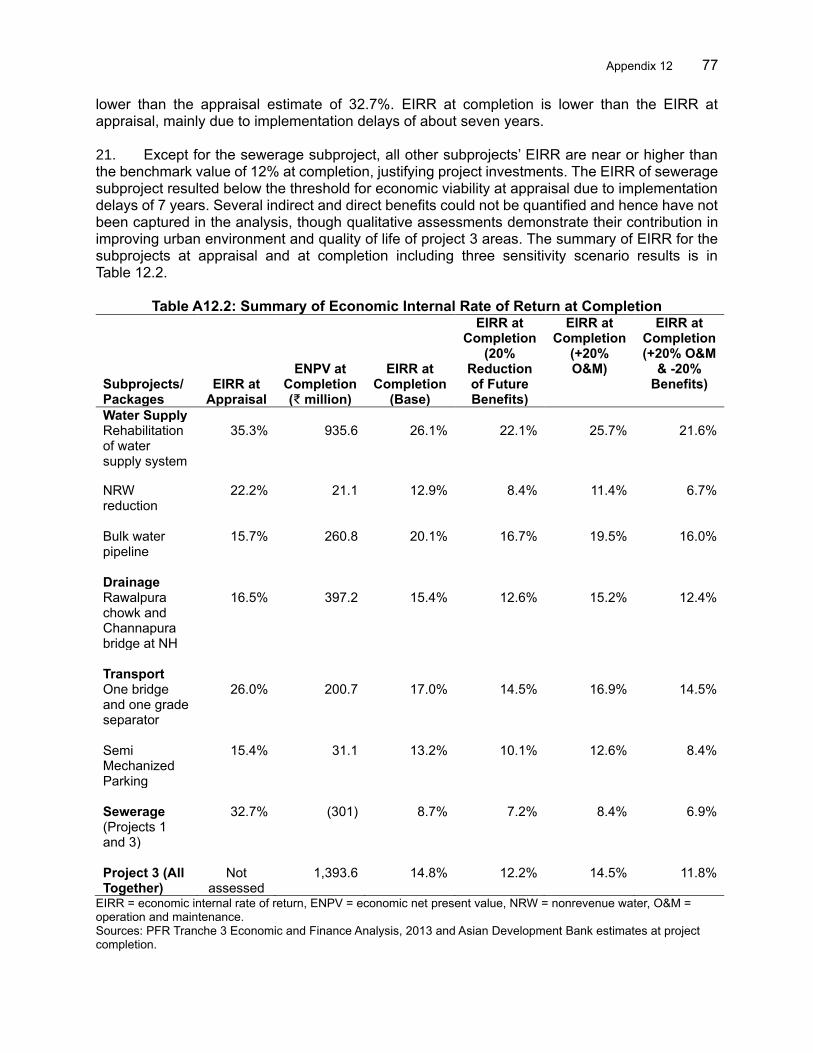

ERA – Economic Reconstruction Agency GAP – gender action plan HUDD – Housing and Urban Development Department IEE – initial environmental examination km – kilometer lpcd – liters per capita per day MFF – multitranche financing facility m mld NRW

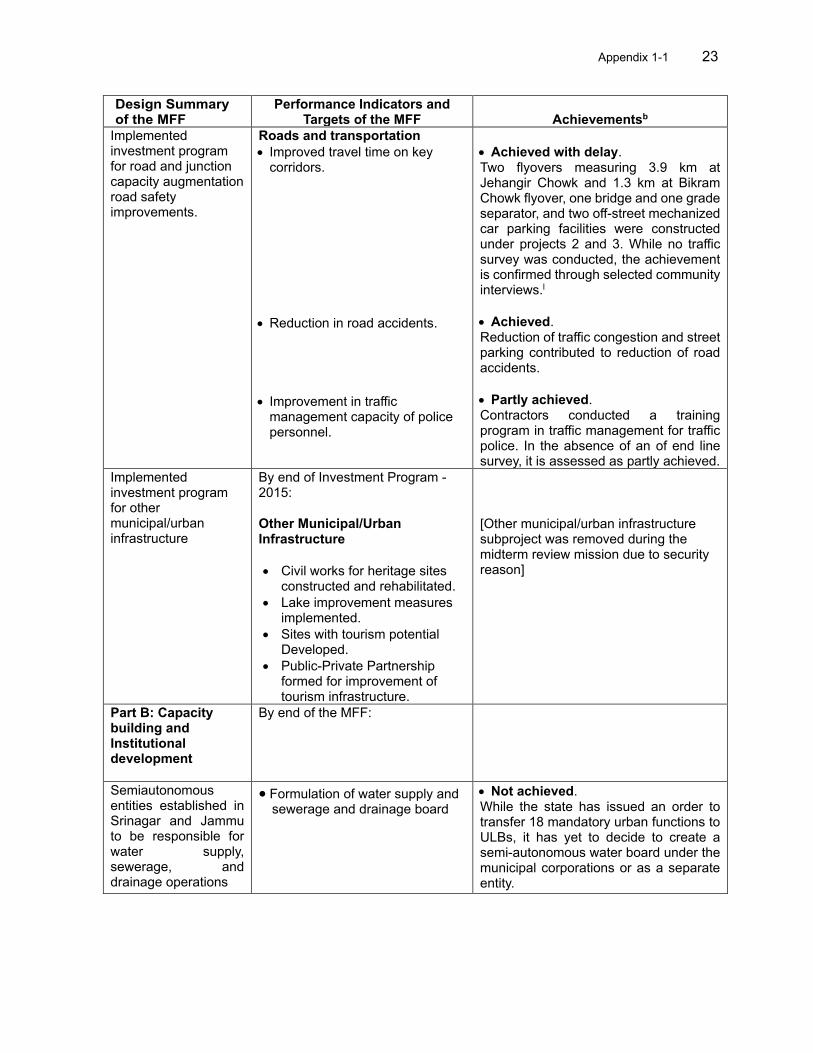

– – –

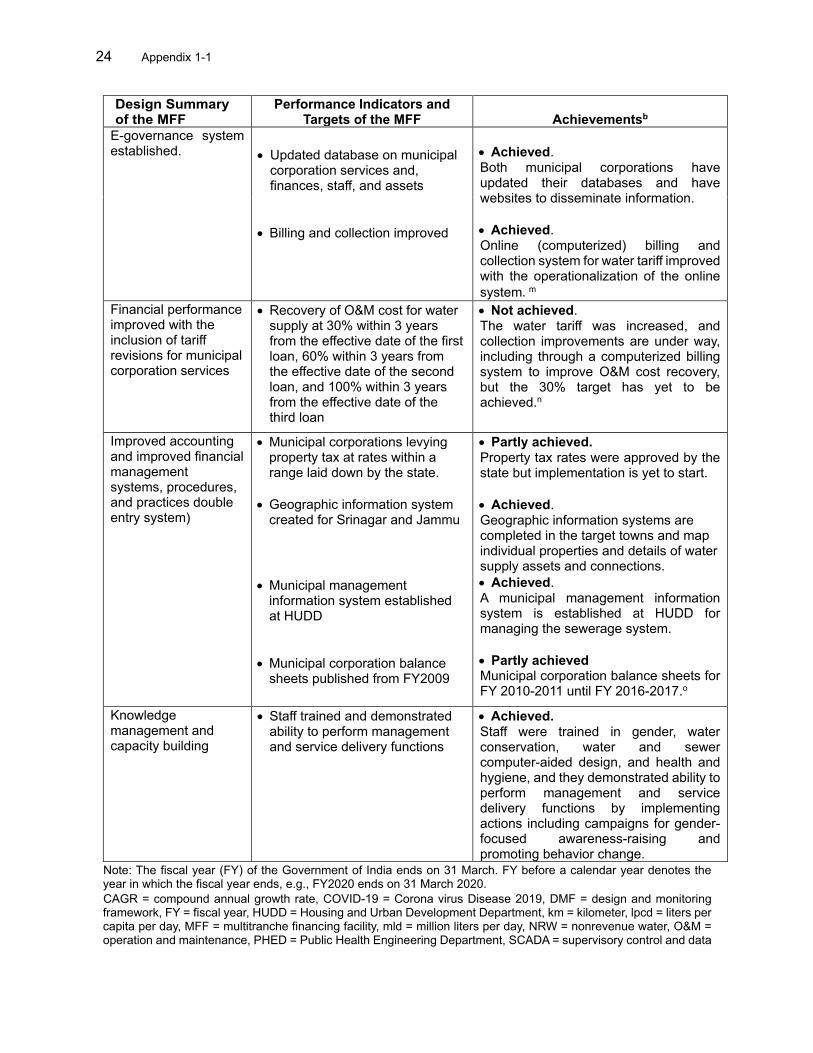

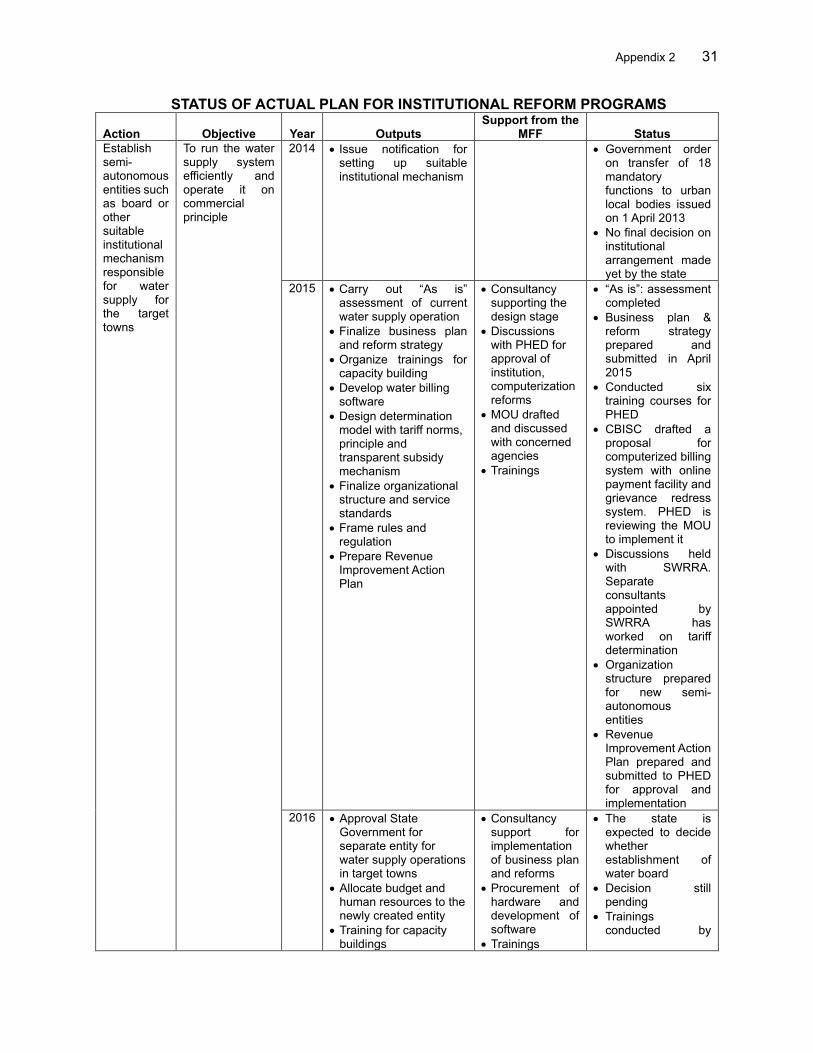

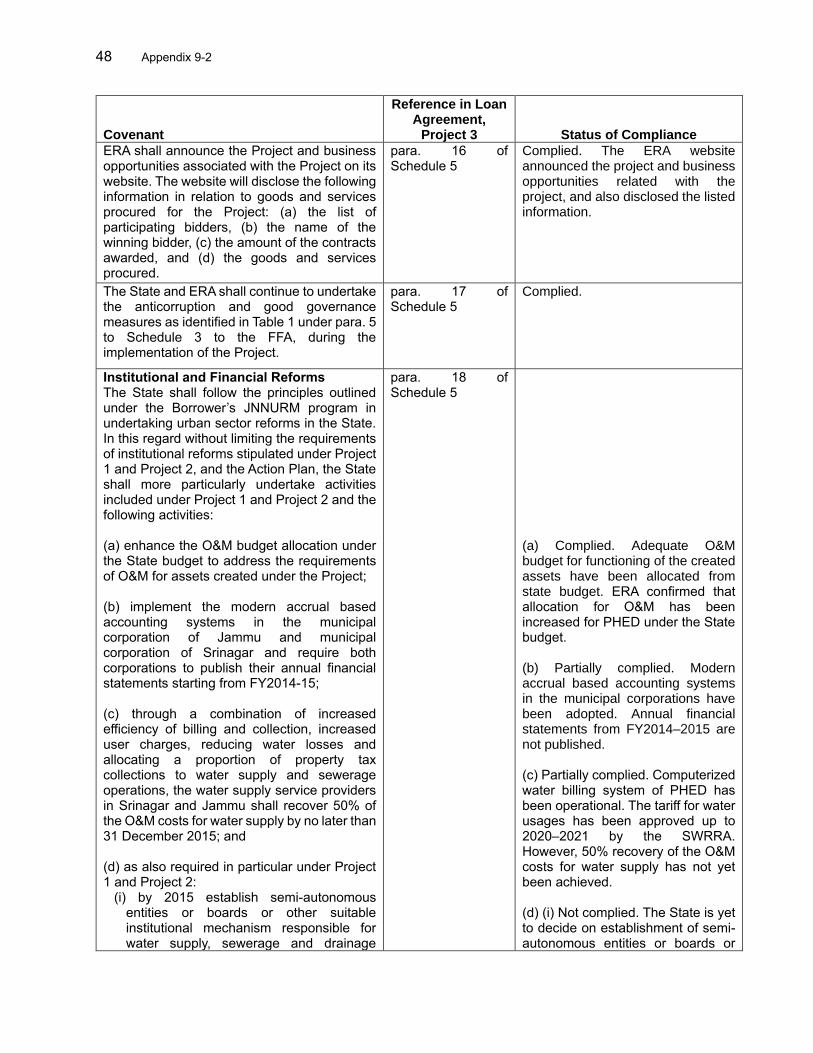

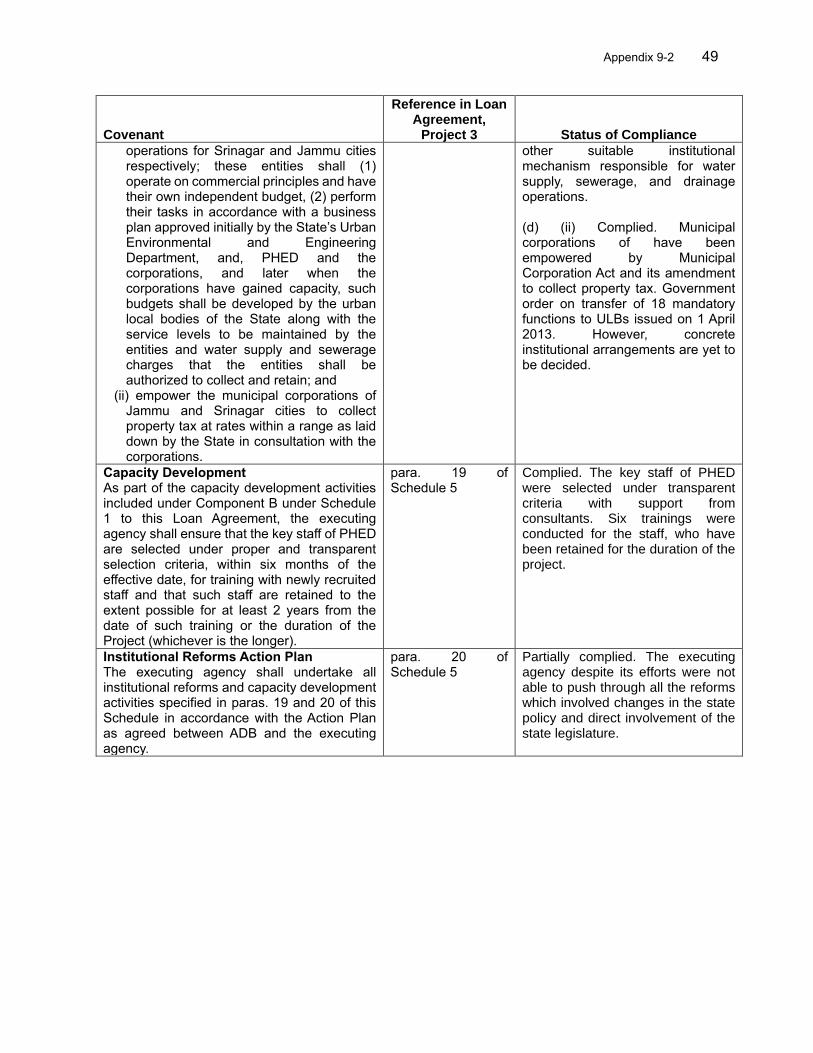

meter million liters per day nonrevenue water

O&M – operation and maintenance PHED – Public Health Engineering Department PIU – project implementation unit PMC – program management consultant PMU – project management unit PWD – Public Works Department STP – sewage treatment plant SWM TA

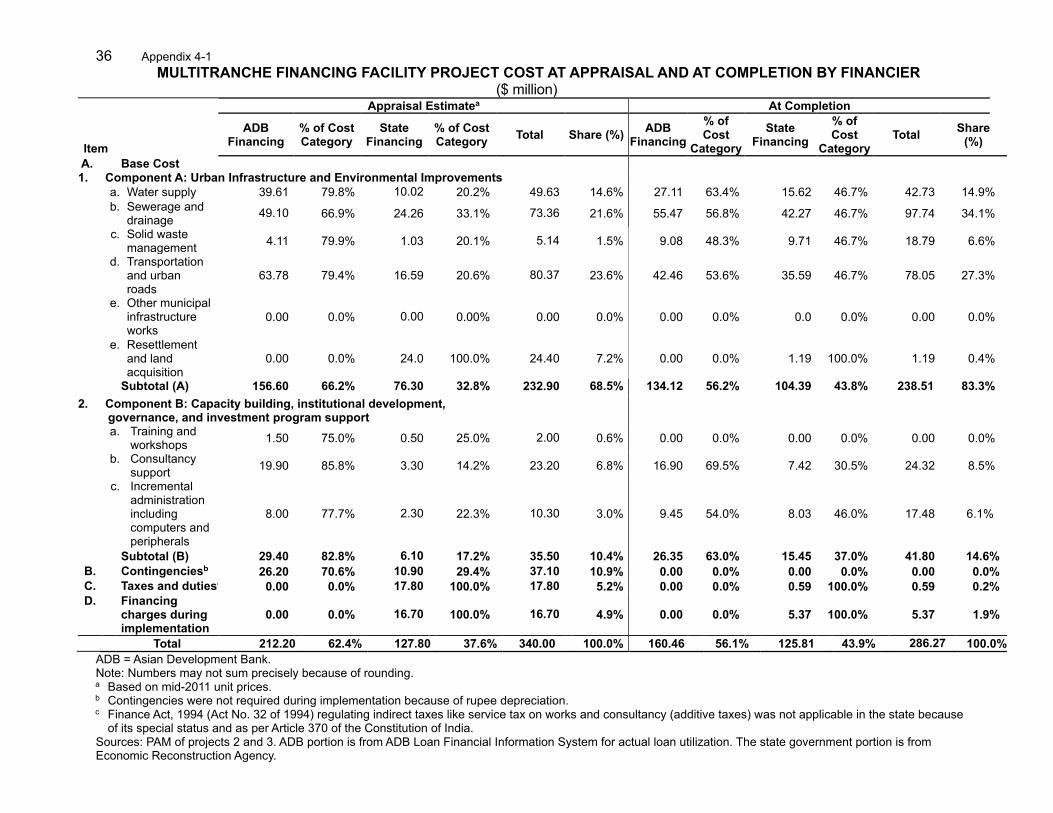

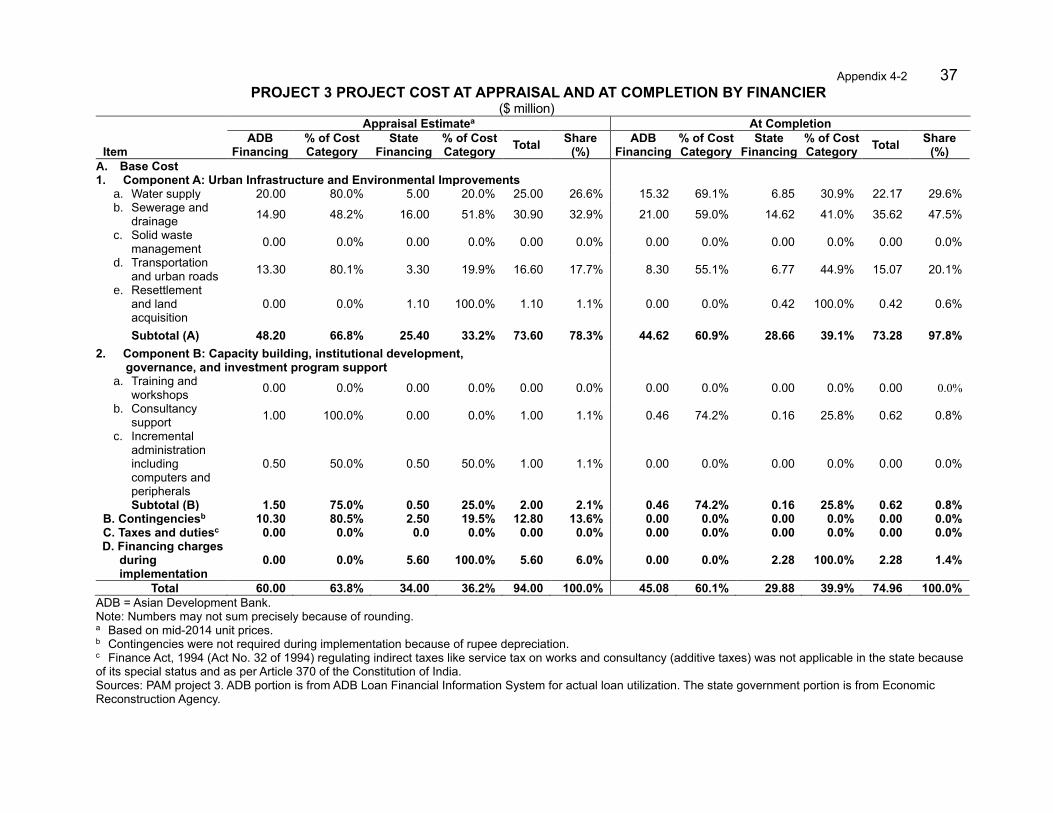

– –

solid waste management technical assistance

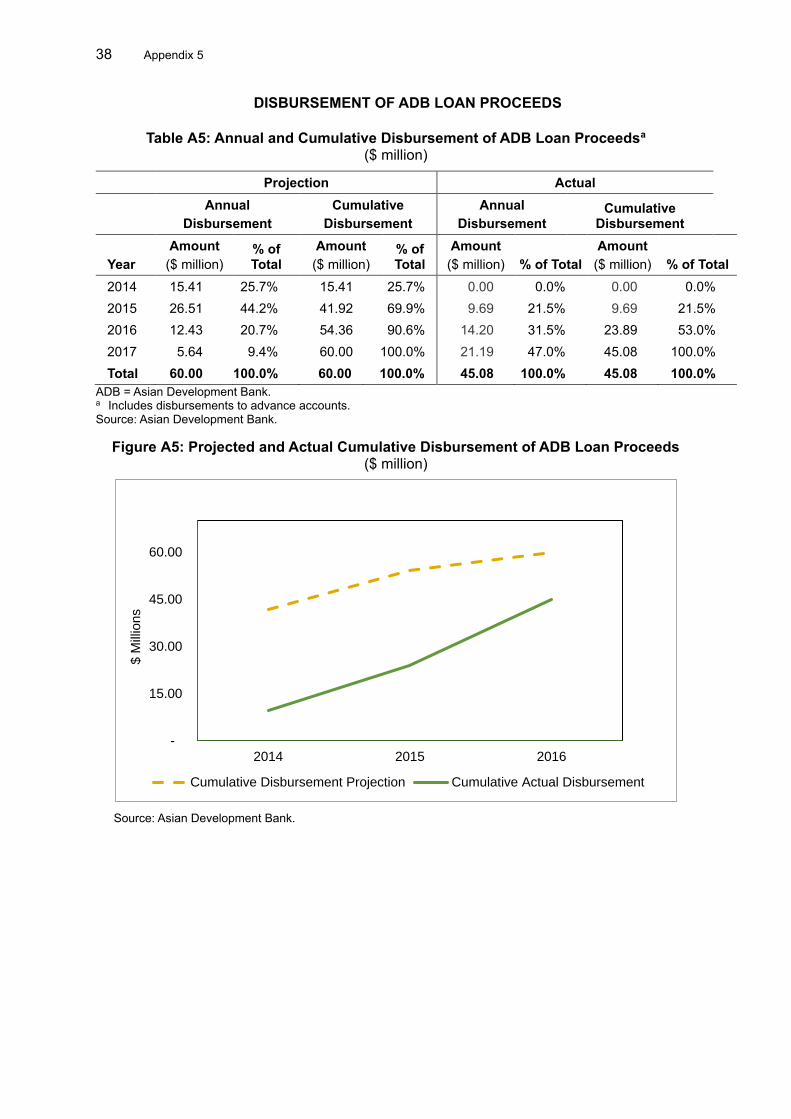

ULB – urban local body

WTP – water treatment plant

NOTES

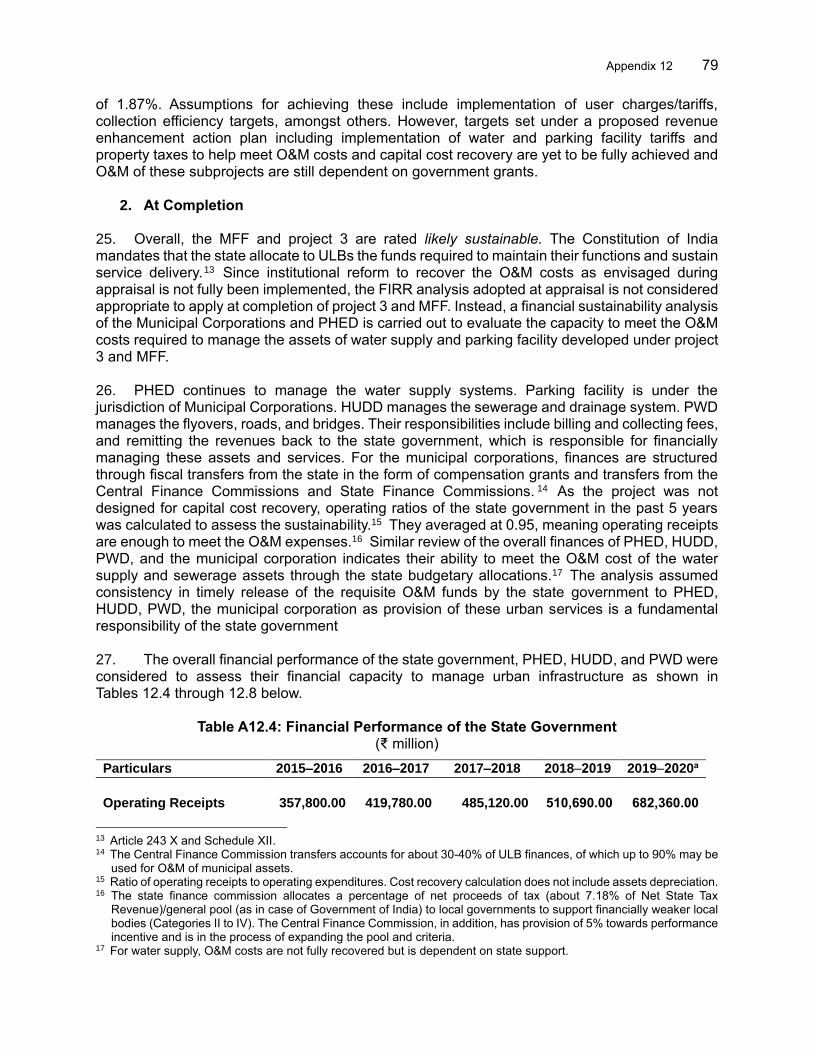

(i) The fiscal year (FY) of the Government of India ends on 31 March. “FY” before a calendar year denotes the year in which the fiscal year ends, e.g., FY2021 ends on 31 March 2021.

(ii) In this report, “$” refers to United States dollars.

Vice-President Shixin Chen, Operations 1

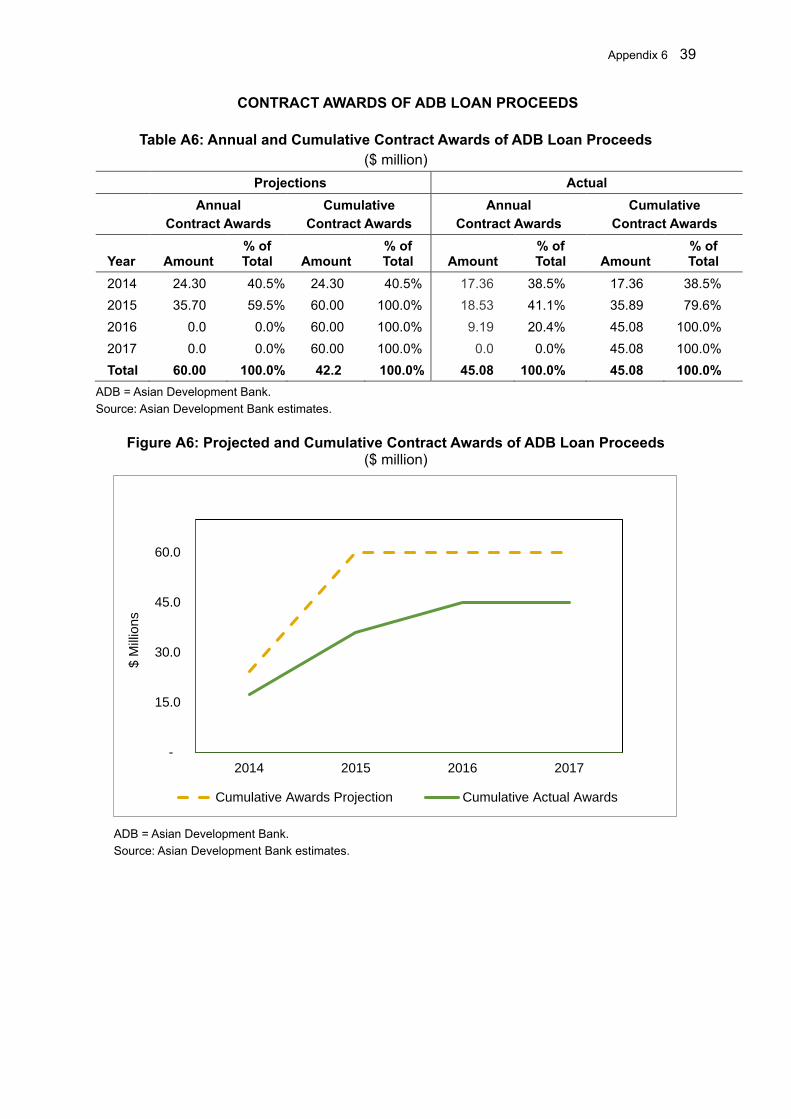

Director General Kenichi Yokoyama, South Asia Department (SARD)

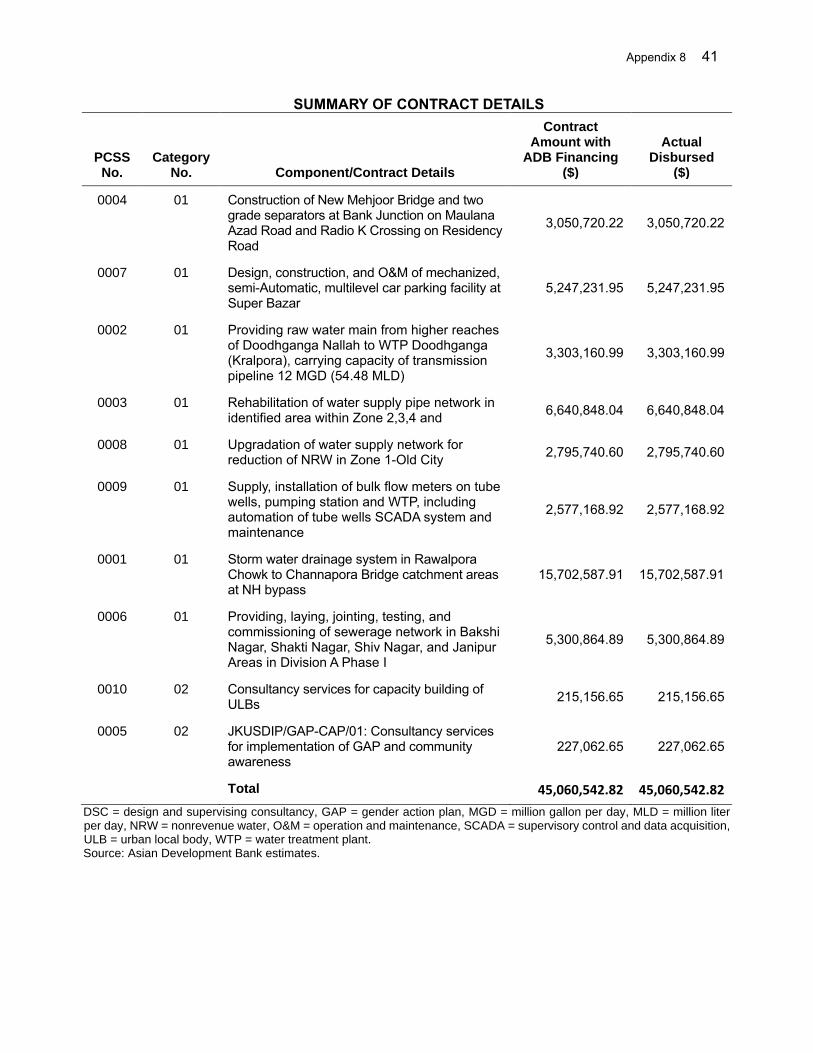

Director Norio Saito, Urban Development and Water Division (SAUW), SARD

Team leader Momoko Tada, Urban Development Specialist, SAUW, SARD

Team members Deepa Ahluwalia, Senior Social Development Officer (Gender), India Resident Mission (INRM), SARD

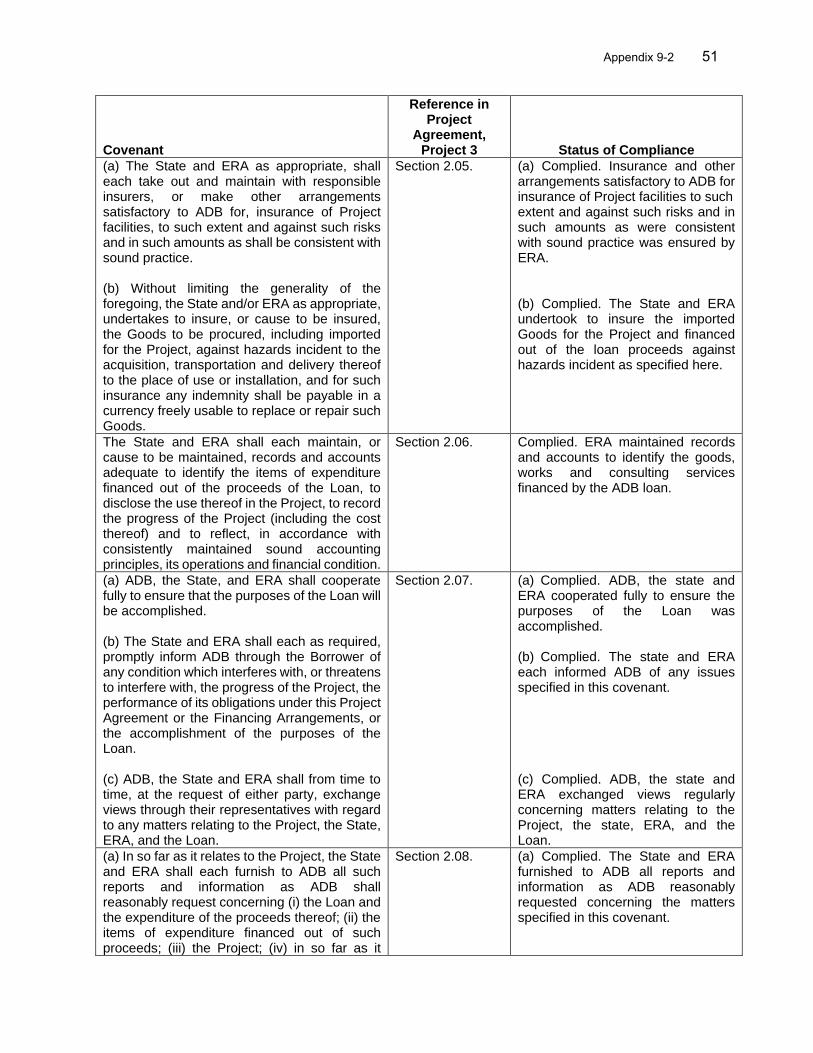

Saswati Belliappa, Safeguards Specialist, SAUW, SARD Bhawna Kulshreshtha, Executive Assistant, INRM, SARD Pradeep Kumar Pandey, Associate Operations Analyst, INRM, SARD Girish Mahajan, Senior Environment Officer, INRM, SARD Rodellyn Manalac, Operations Assistant, SAUW, SARD Suhail Mircha, Safeguard Officer, INRM, SARD

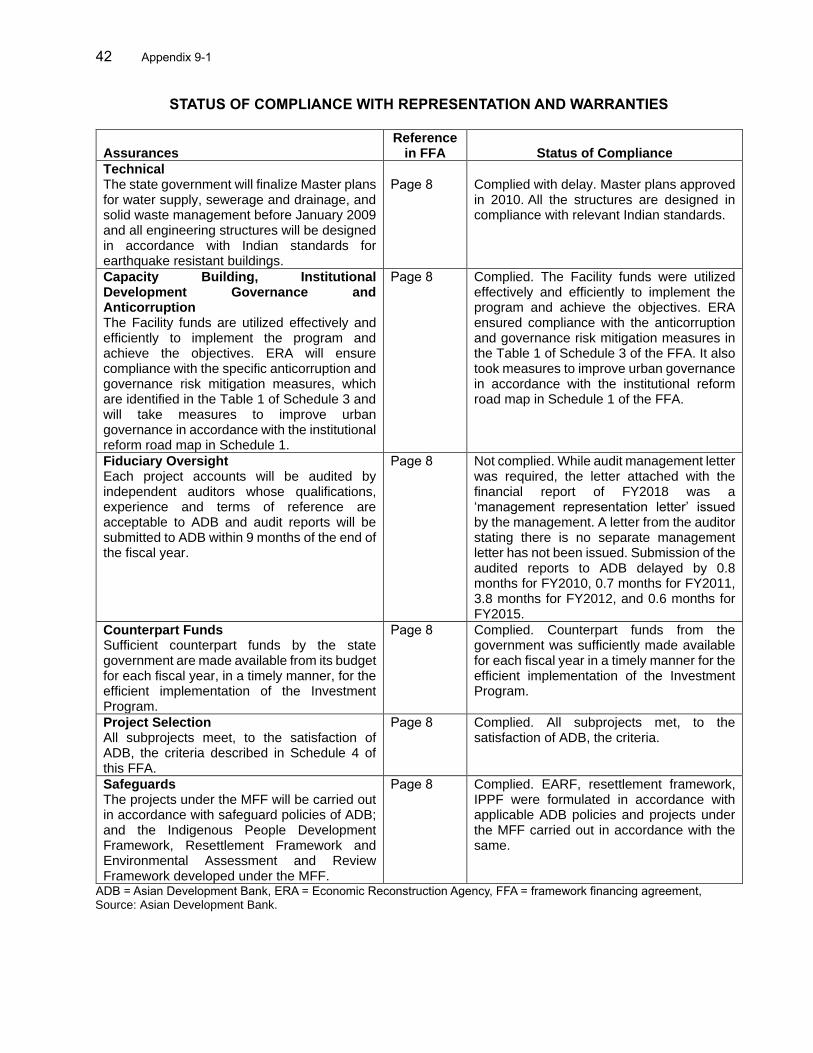

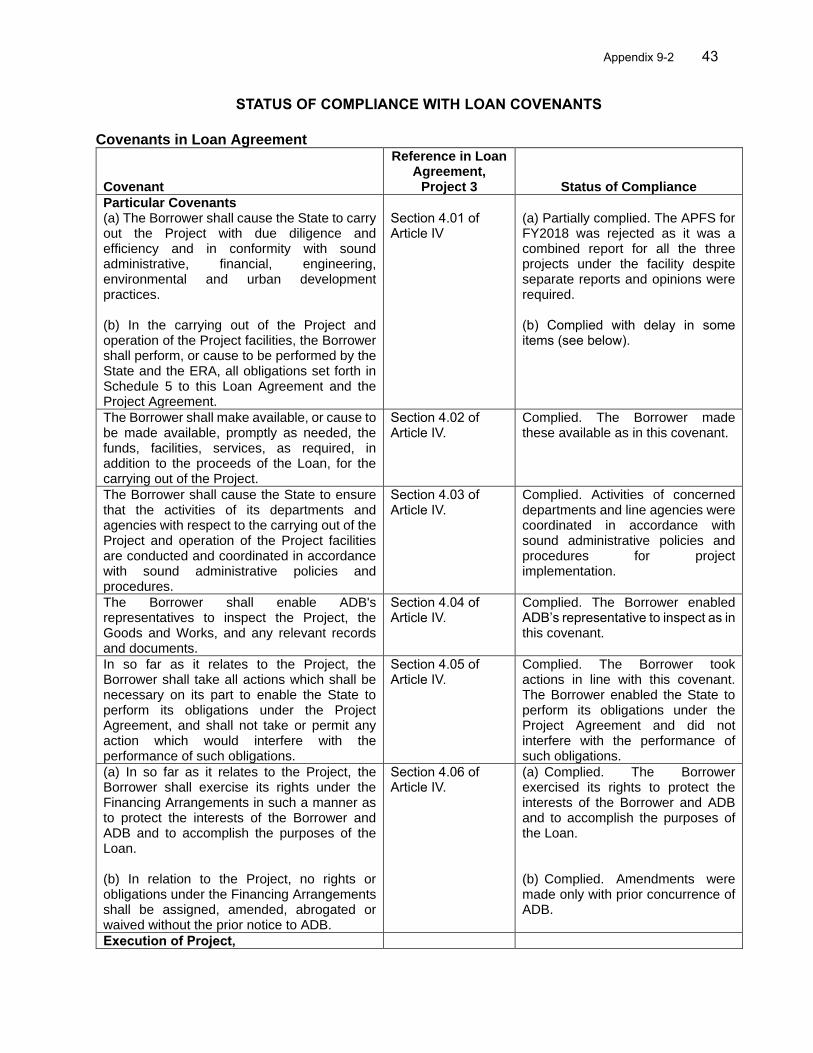

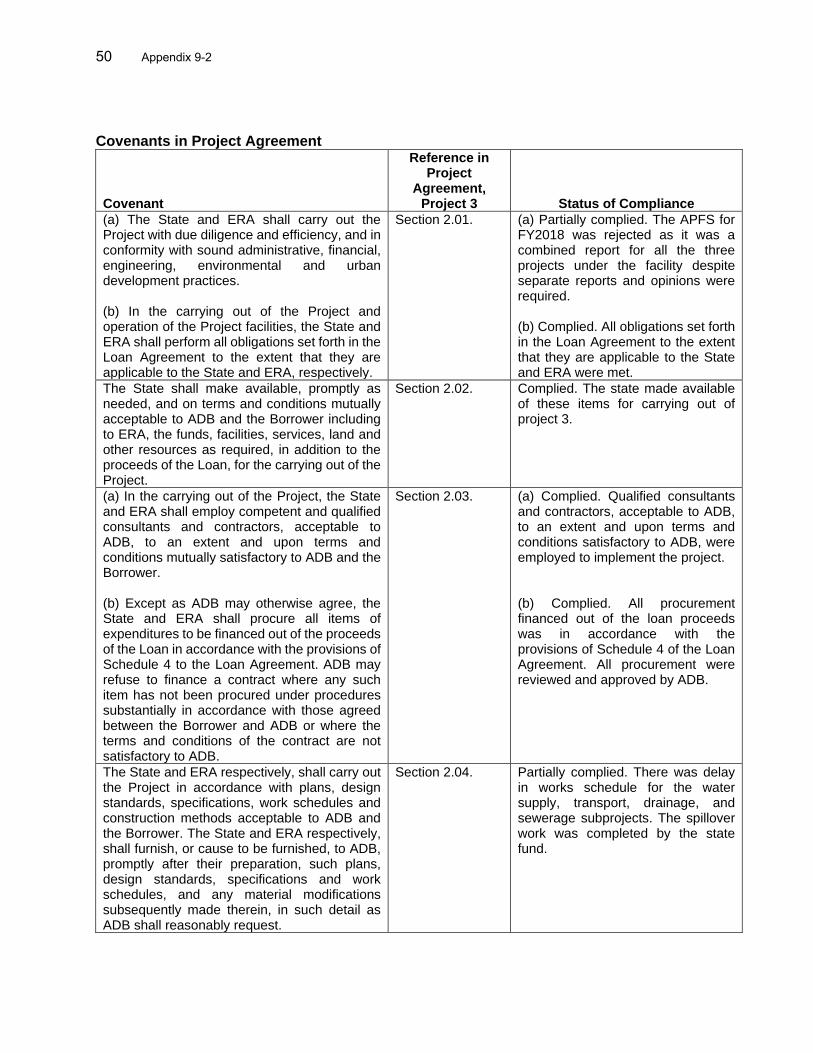

In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area.

CONTENTS Page

BASIC DATA i

I. PROJECT DESCRIPTION 1

II. DESIGN AND IMPLEMENTATION 2

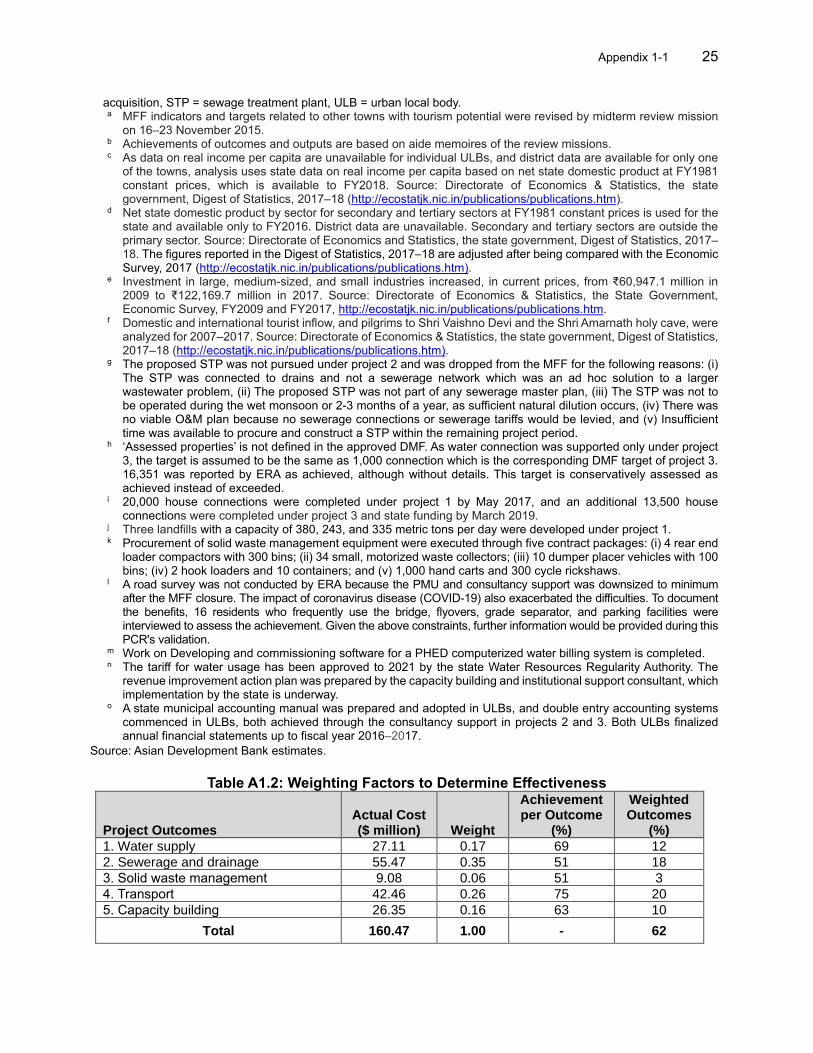

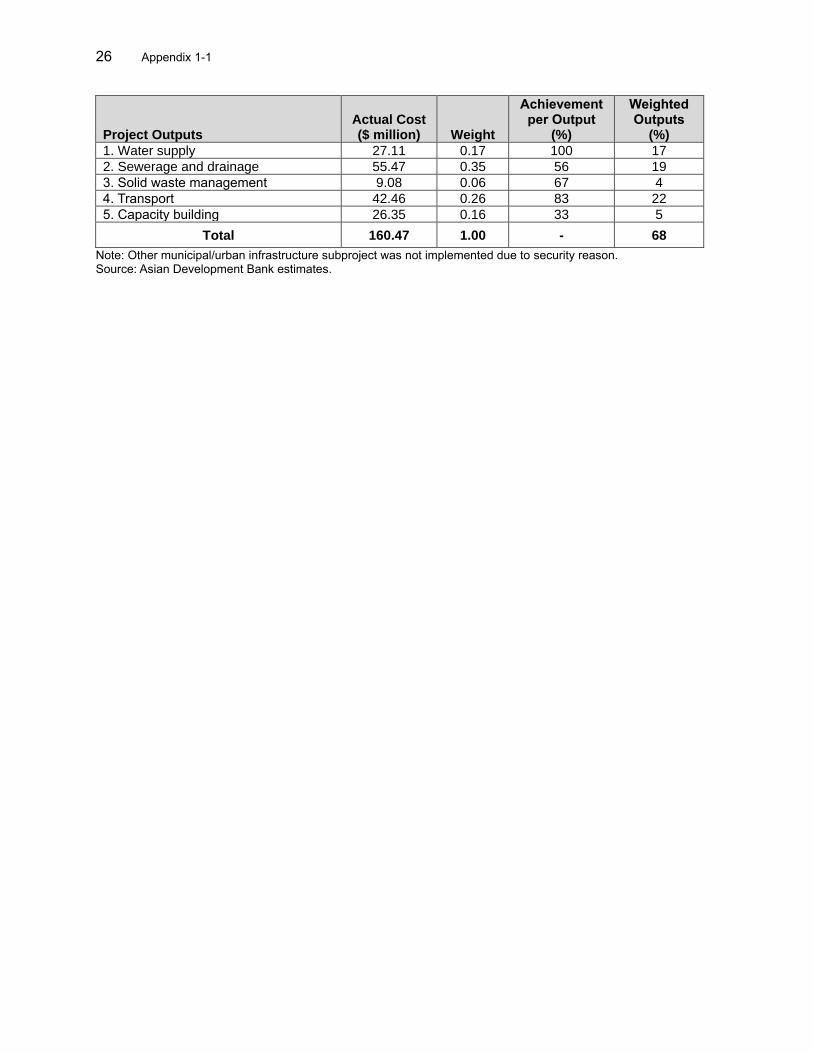

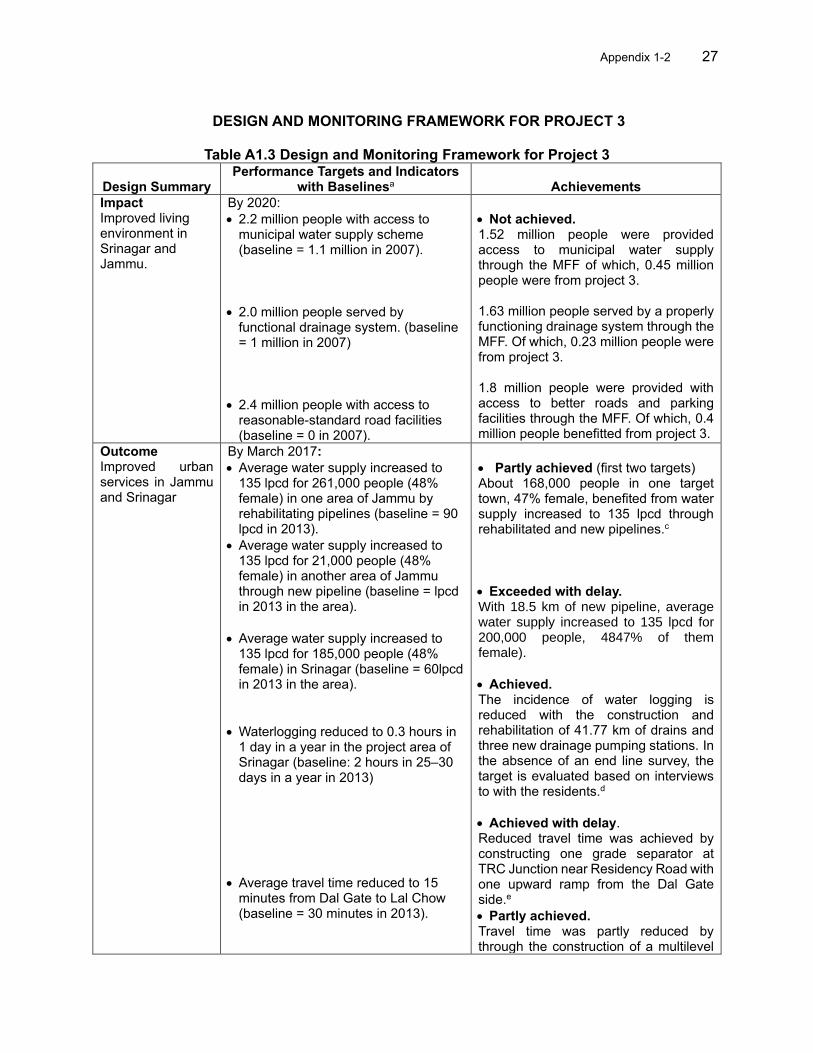

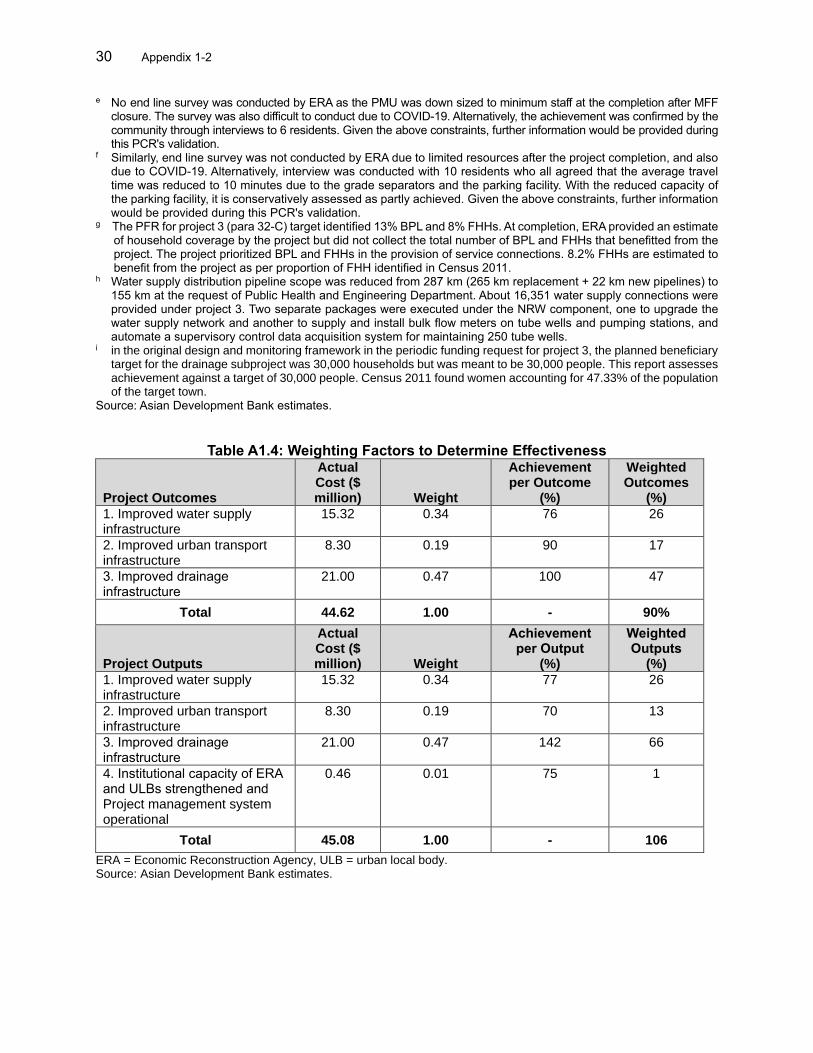

A. Project Design and Formulation 2

B. Facility and Project Outputs 4

C. Project Costs and Financing 6

D. Disbursements 7

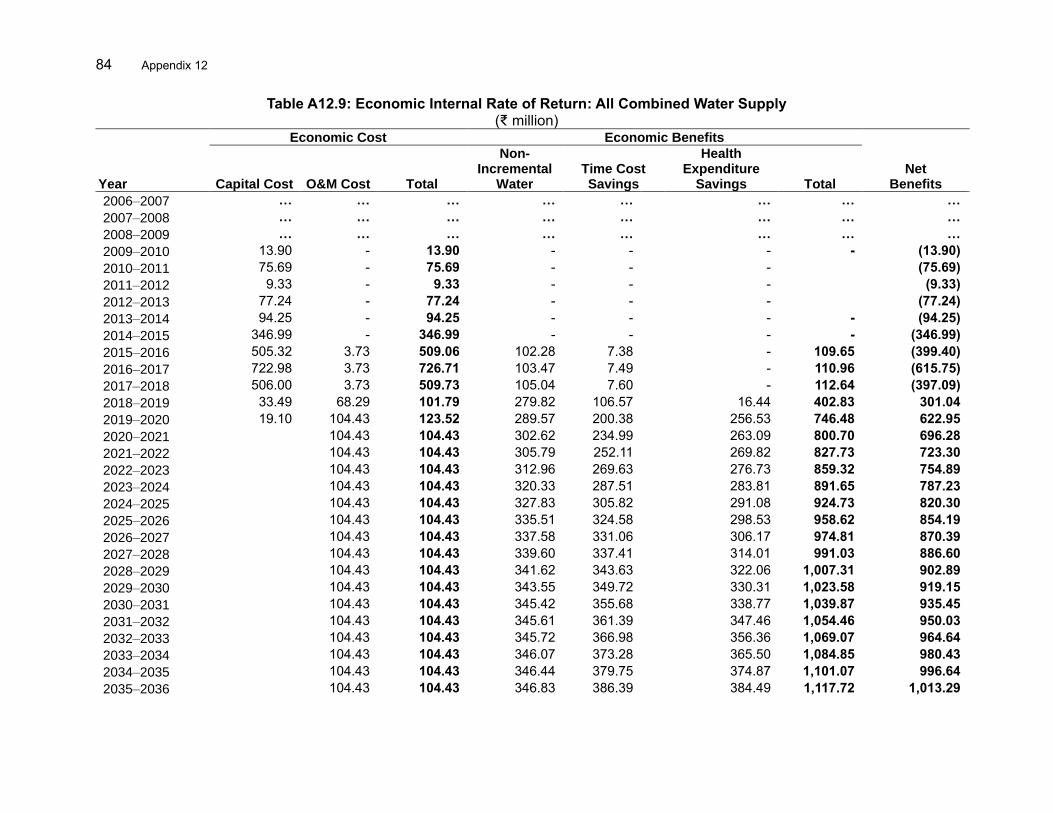

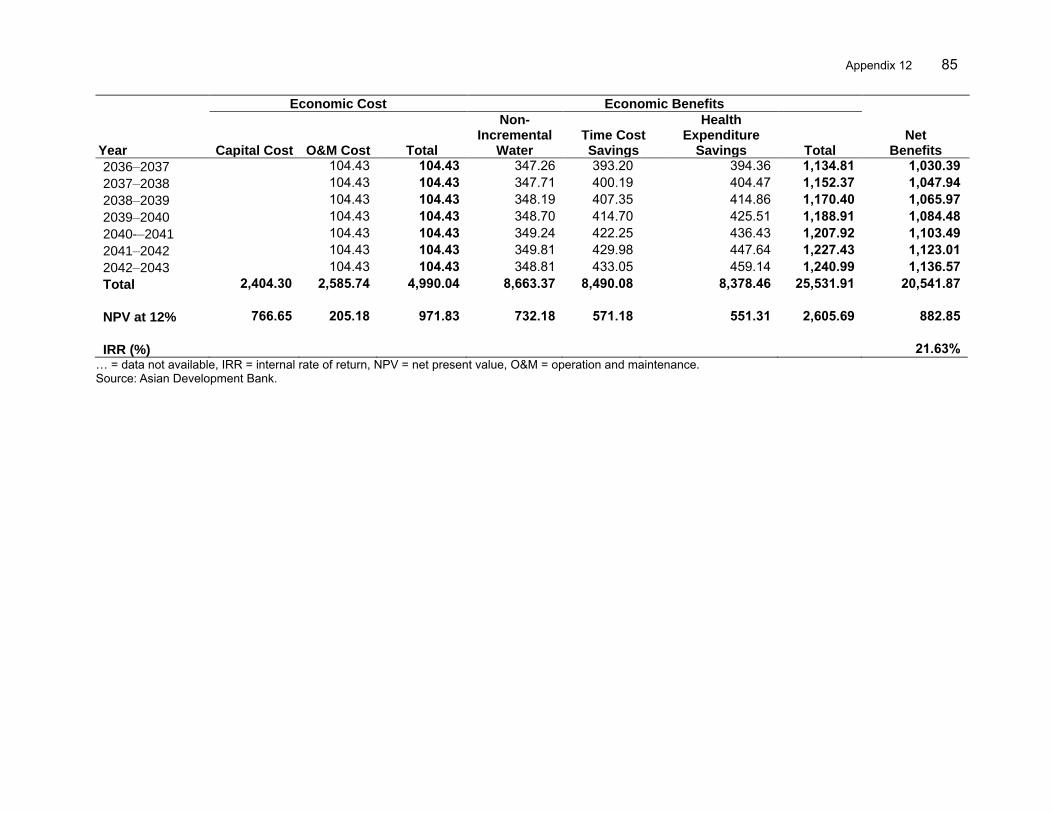

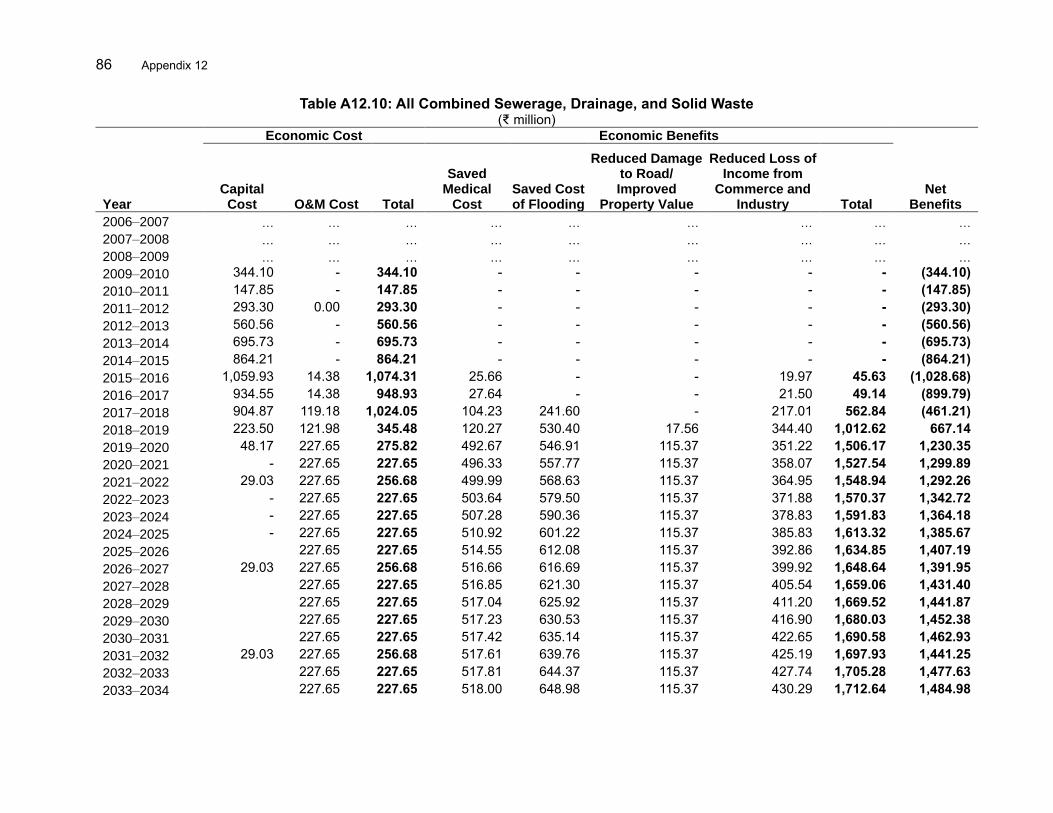

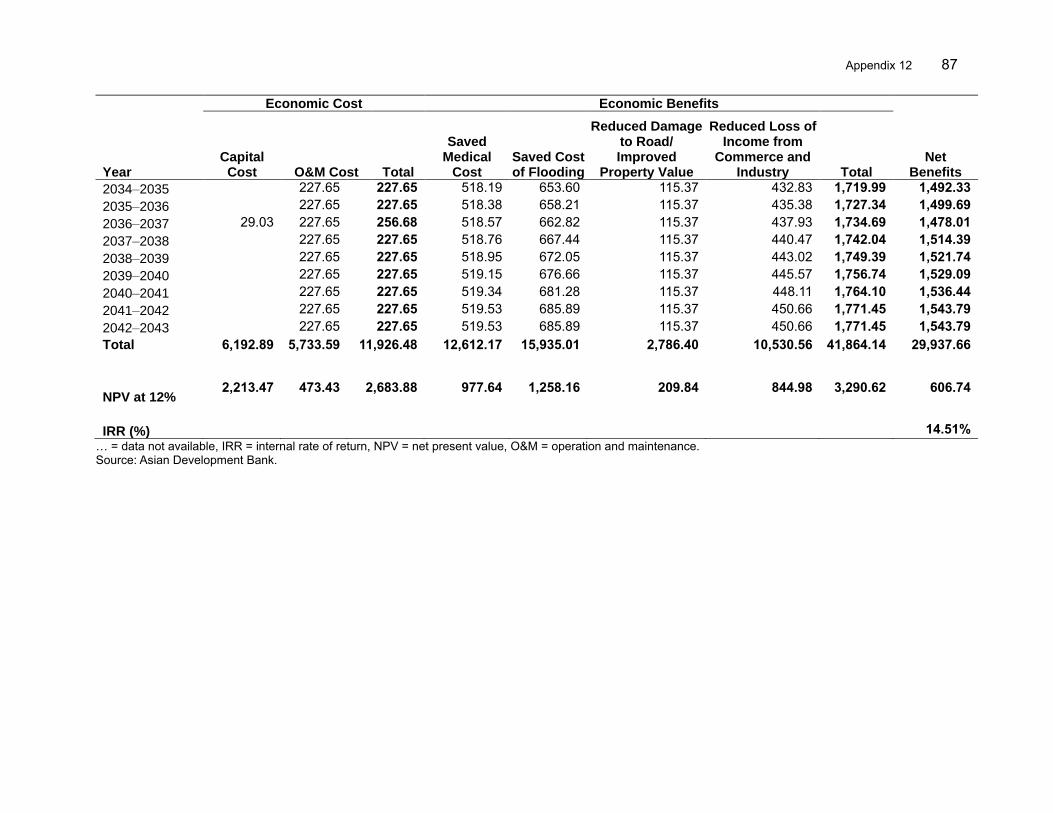

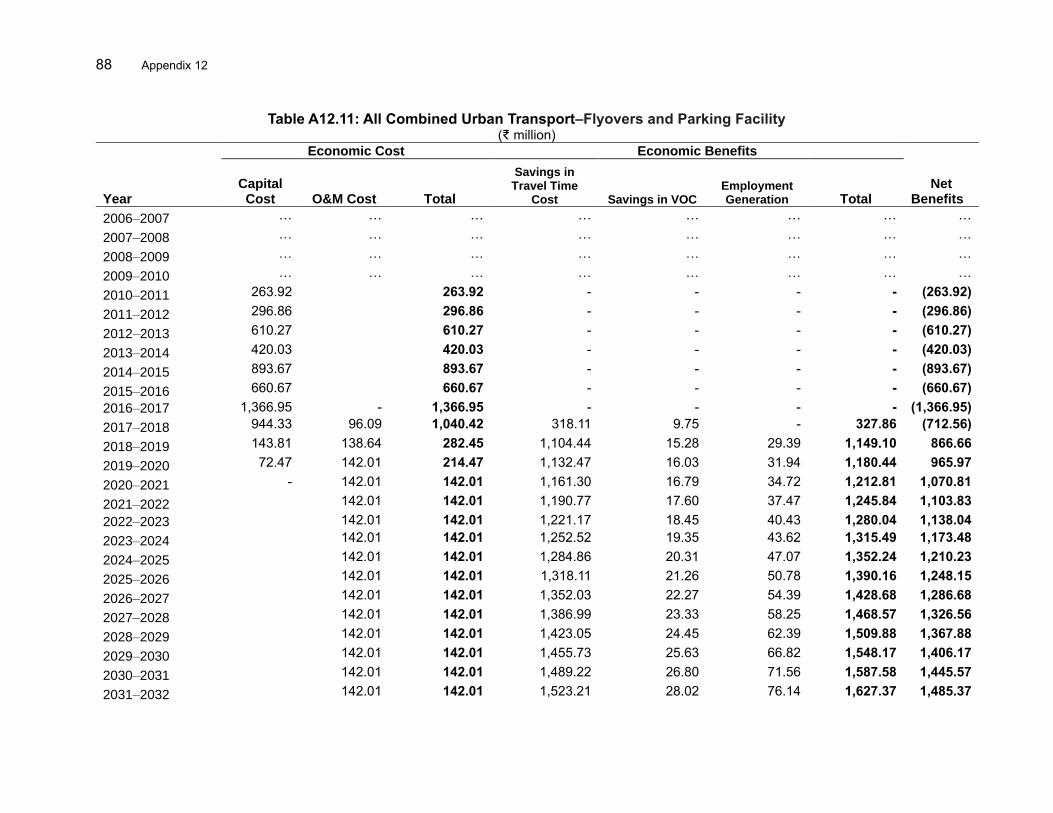

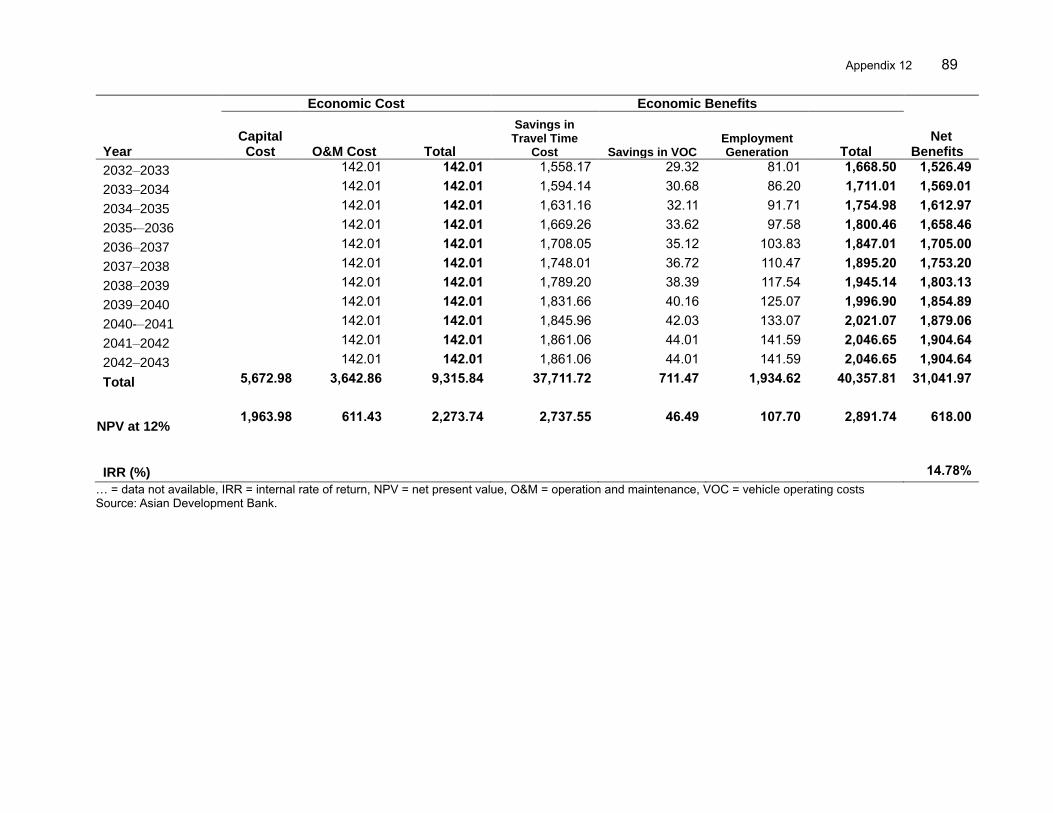

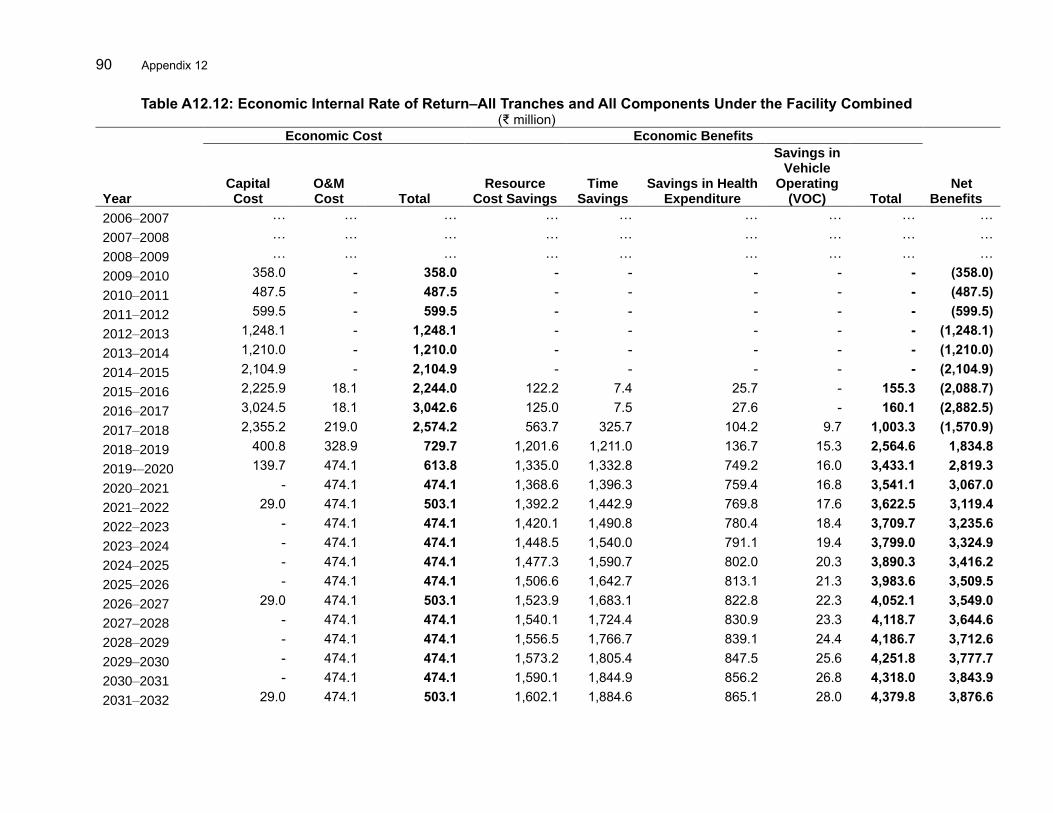

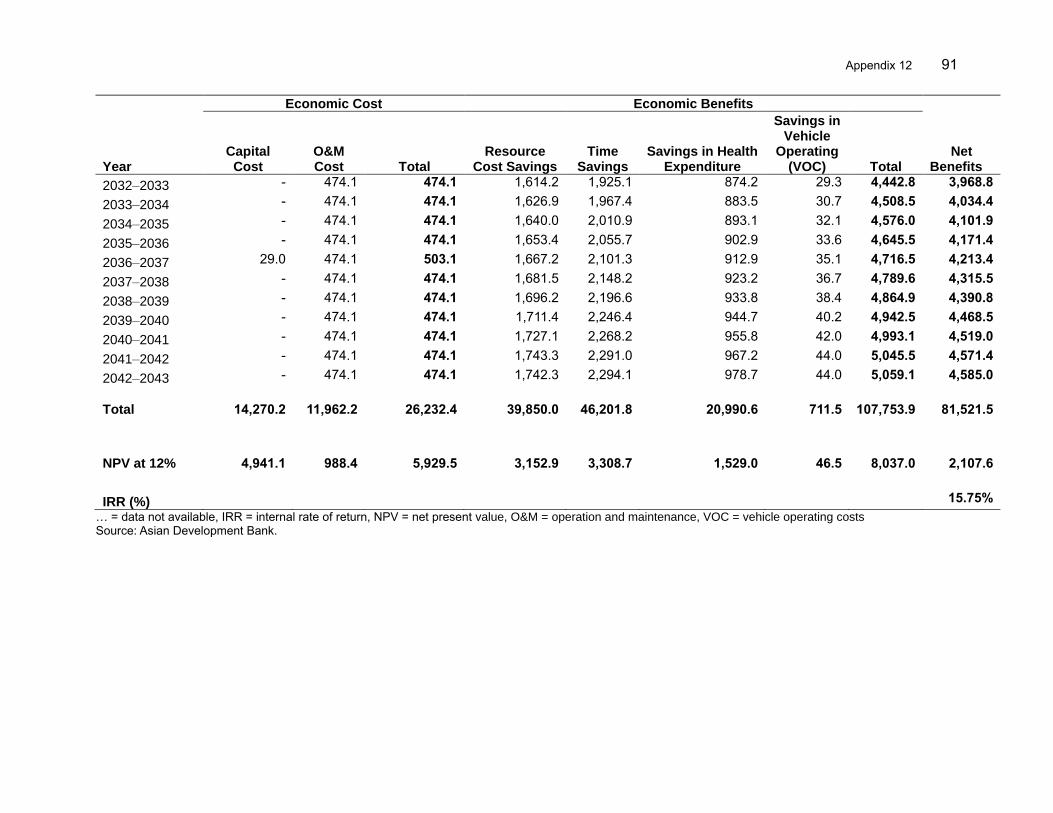

E. Project 3 and Facility Schedule 7

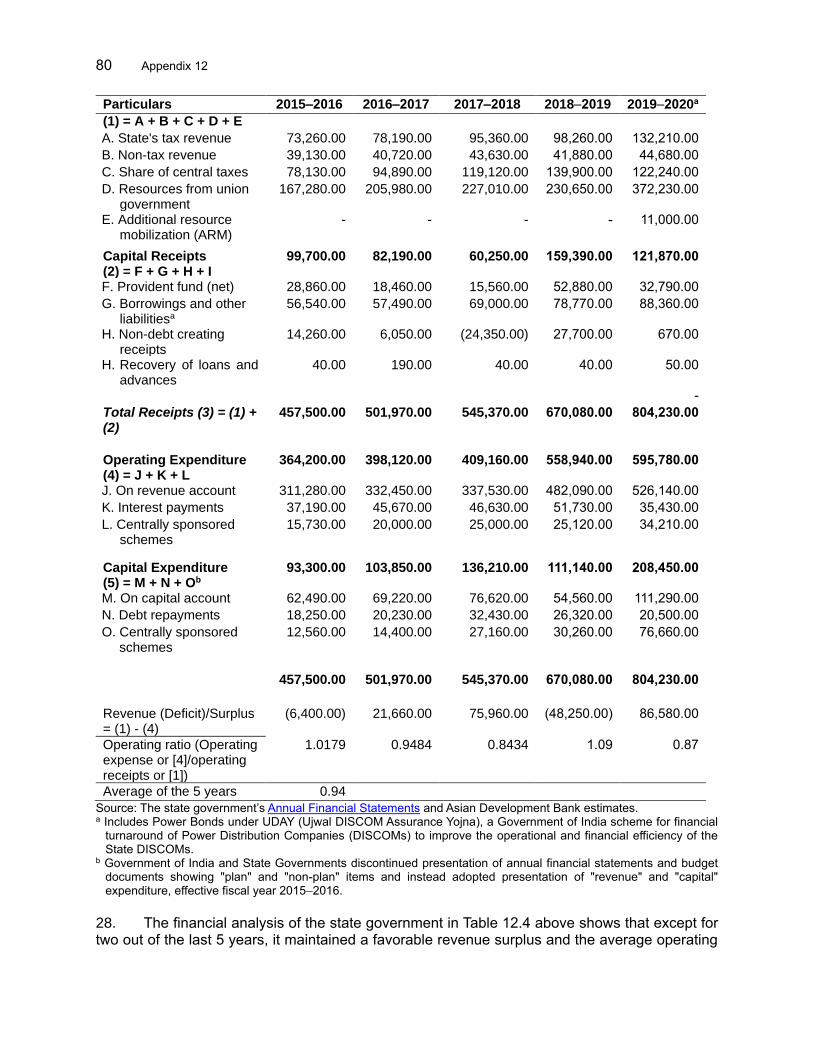

F. Implementation Arrangements 8

G. Technical Assistance 8

H. Consultant Recruitment and Procurement 8

I. Gender Equity 9

J. Safeguards 10

K. Monitoring and Reporting 10

III. EVALUATION OF PERFORMANCE 11

A. Relevance 11

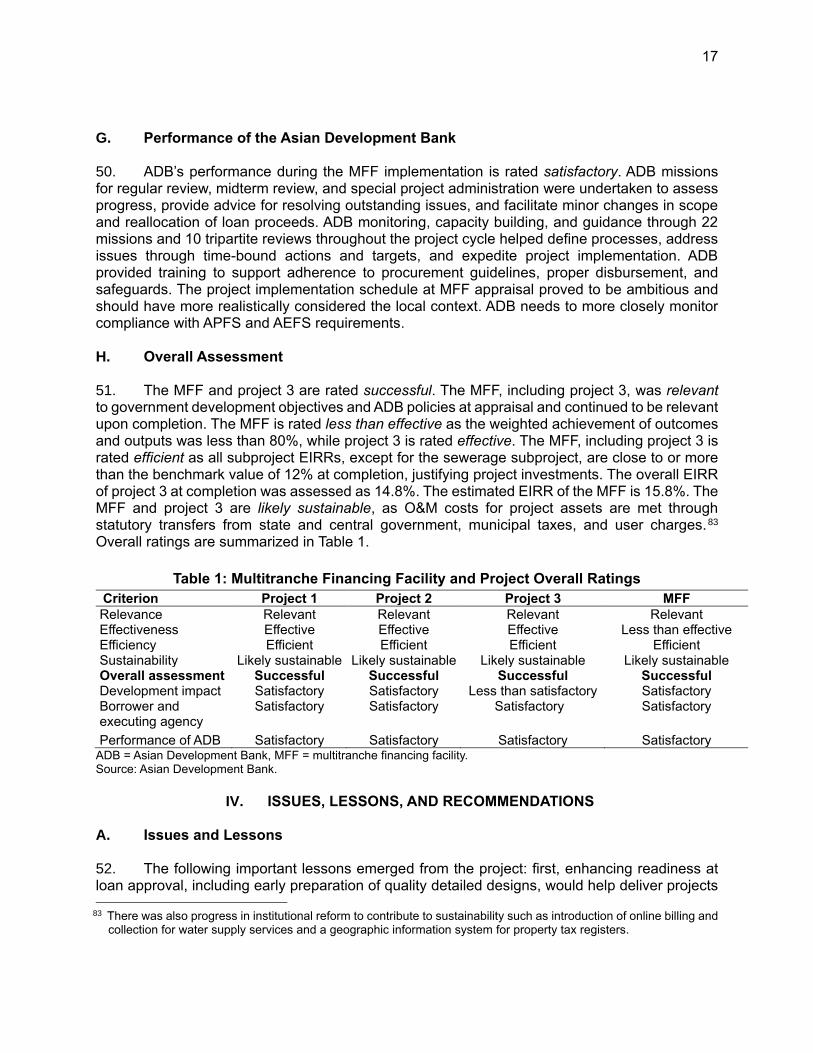

B. Effectiveness 12

C. Efficiency 13

D. Sustainability 14

E. Development Impact 15

F. Performance of the Borrower and the Executing Agency 16

G. Performance of the Asian Development Bank 17

H. Overall Assessment 17

IV. ISSUES, LESSONS, AND RECOMMENDATIONS 17

A. Issues and Lessons 17

B. Recommendations 18 APPENDIXES

1-1. Design and Monitoring Framework for Multitranche Financing Facility 19

1-2. Design and Monitoring Framework for Project 3 27

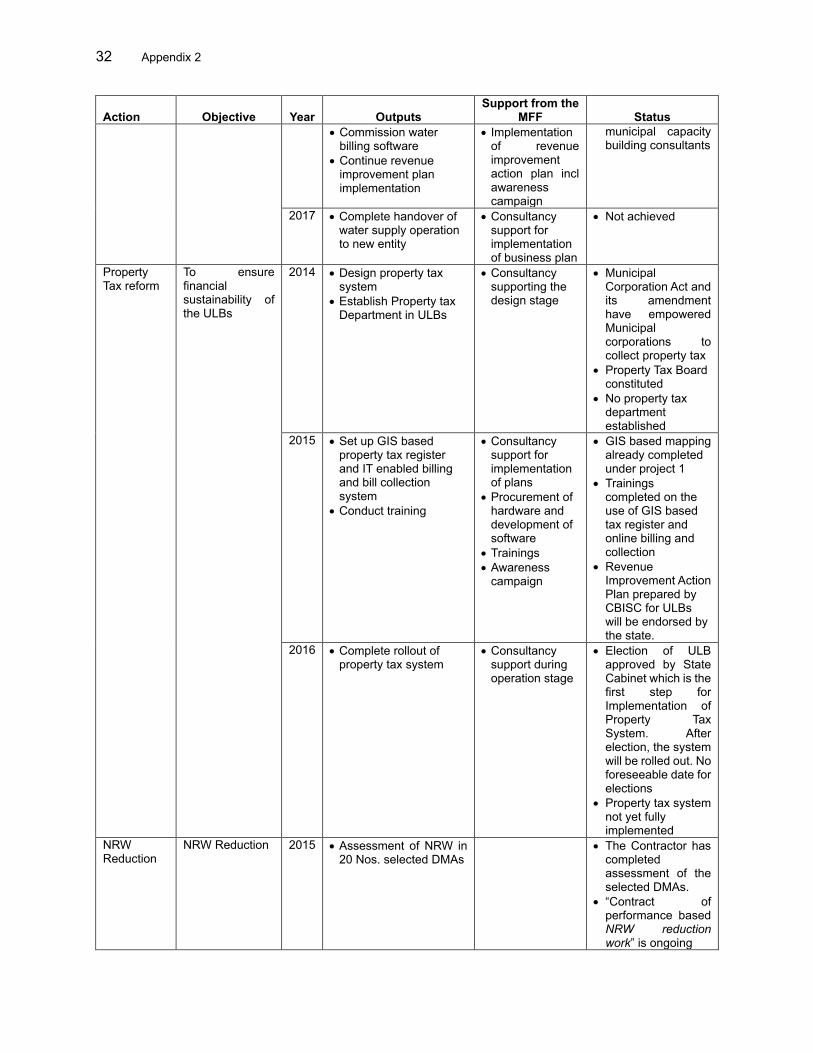

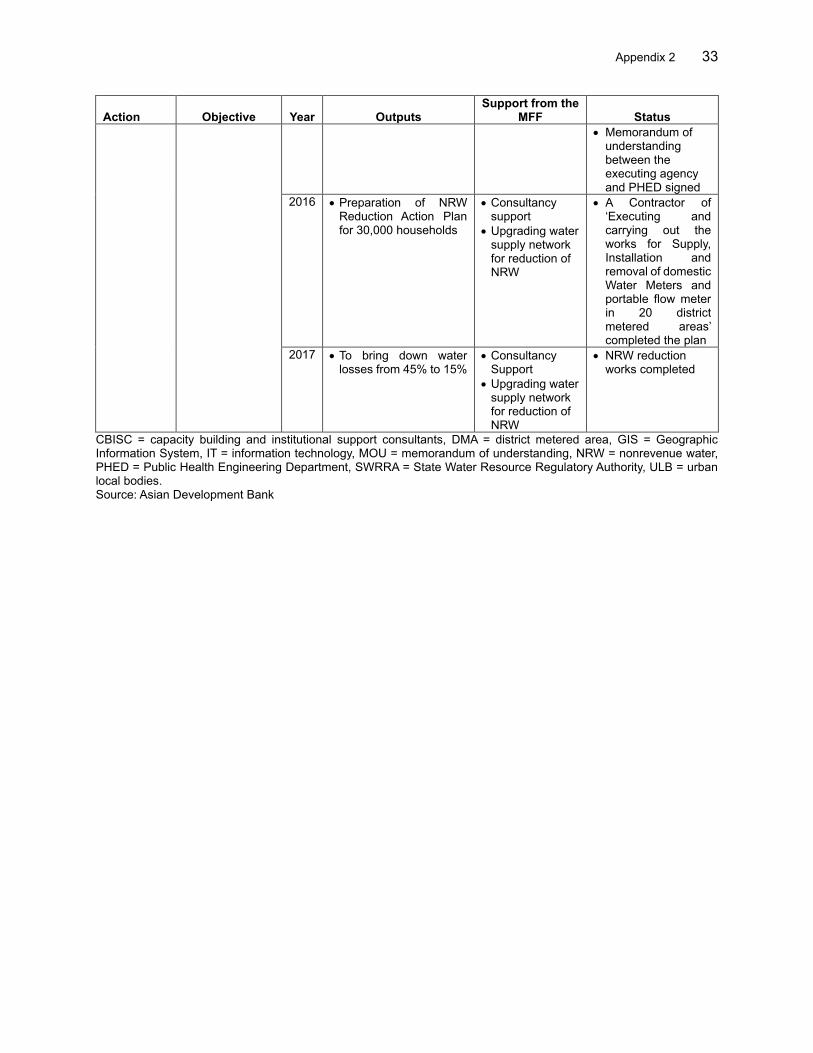

2. Status of Actual Plan for Institutional Reform Programs 31

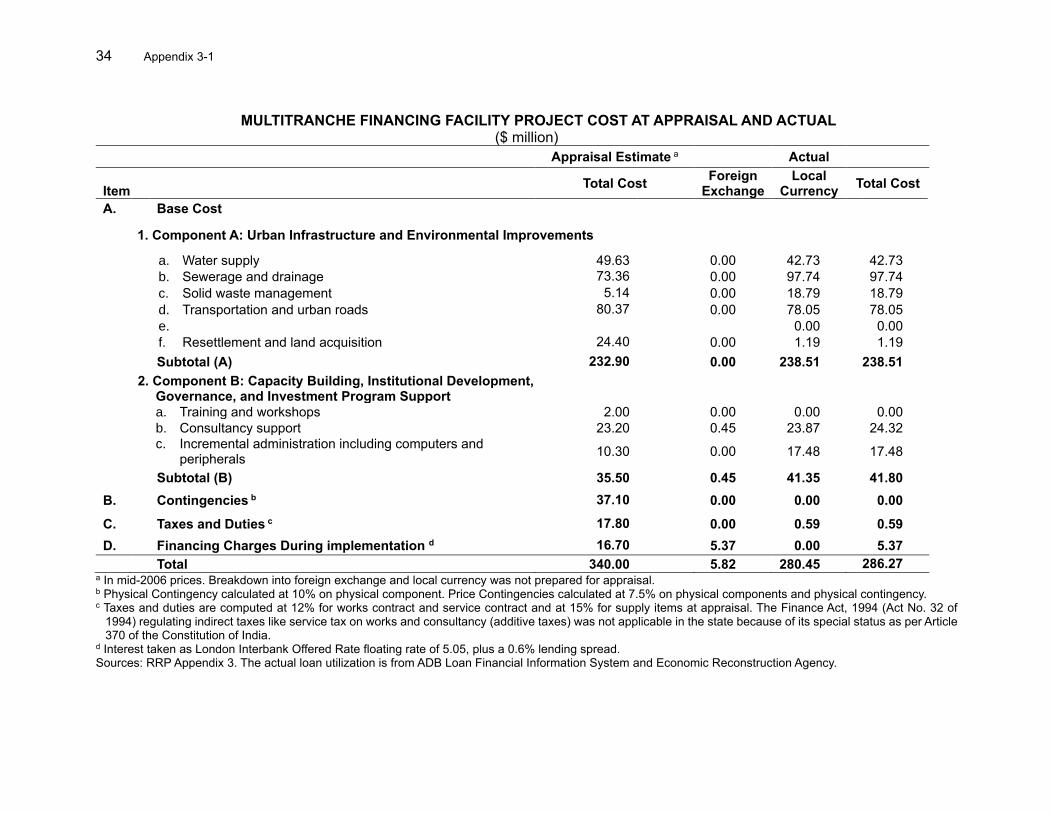

3-1. Multitranche Financing Facility Project Cost at Appraisal and Actual 34

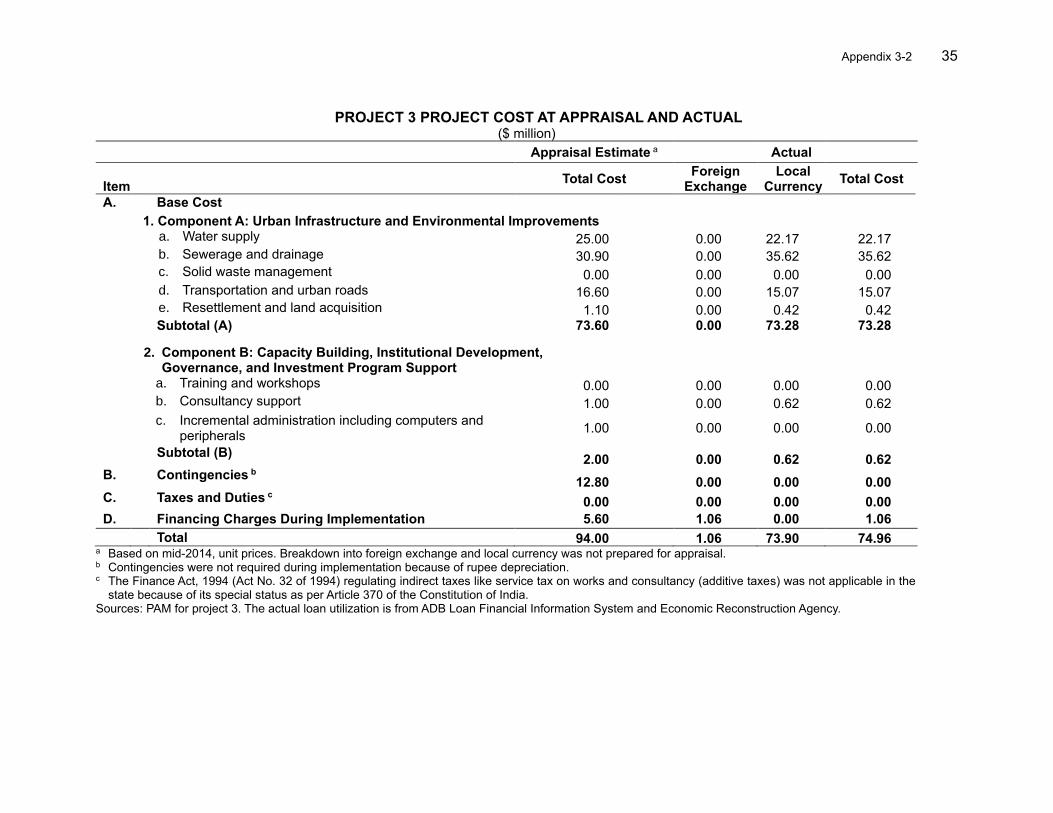

3-2. Project 3 Project Cost at Appraisal and Actual 35

4-1. Multitranche Financing Facility Project Cost at Appraisal and at Completion

by Financier 36

4-2. Project 3 Project Cost at Appraisal and at Completion by Financier 37

5. Disbursement of ADB Loan Proceeds 38

6. Contract Awards of ADB Loan Proceeds 39

7. Chronology of Main Events 40

8. Summary of Contract Details 41

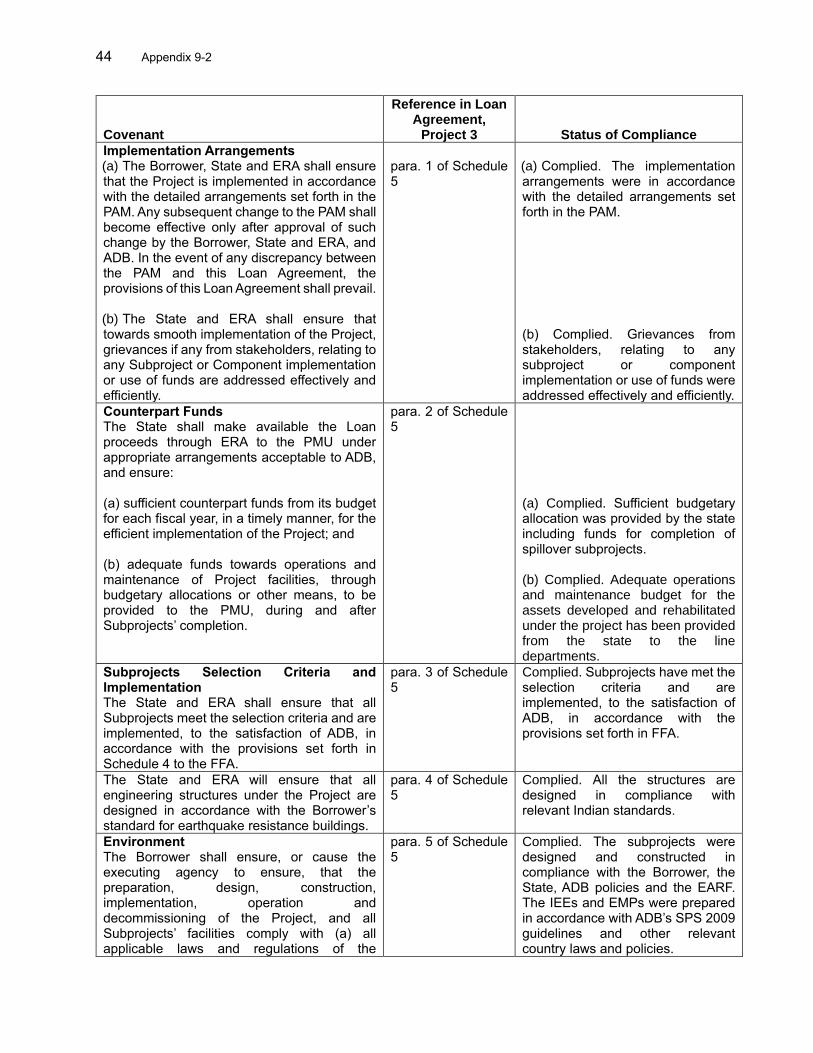

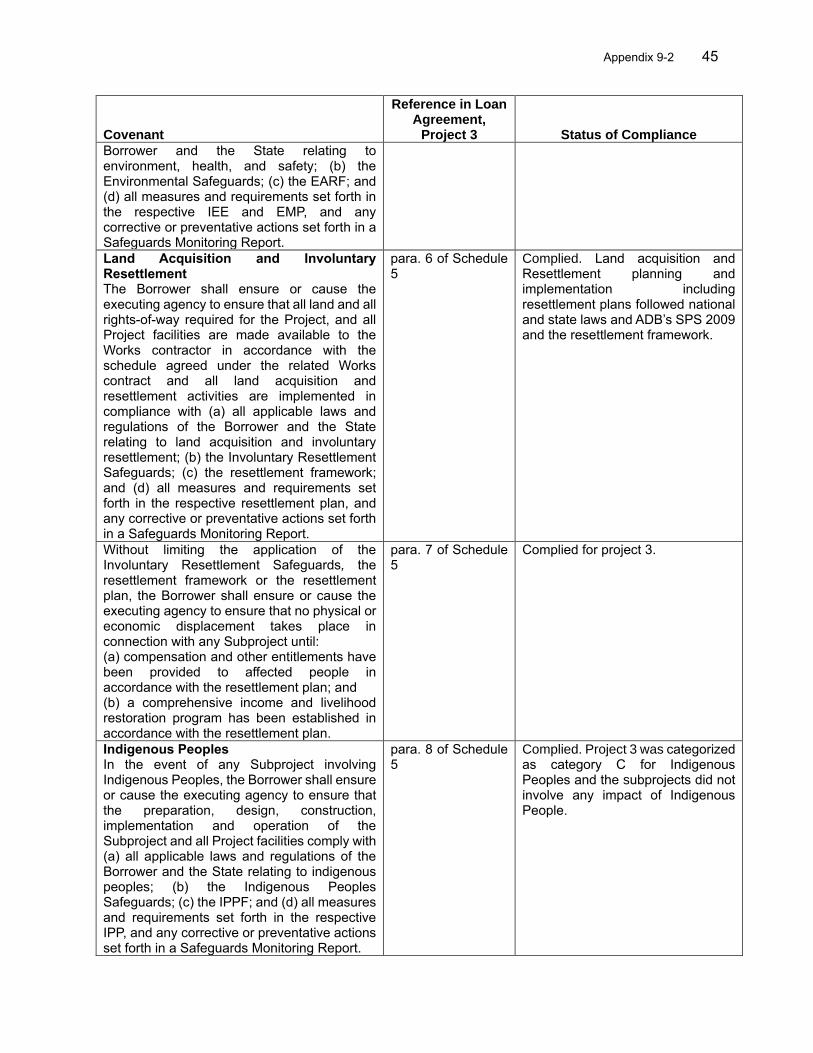

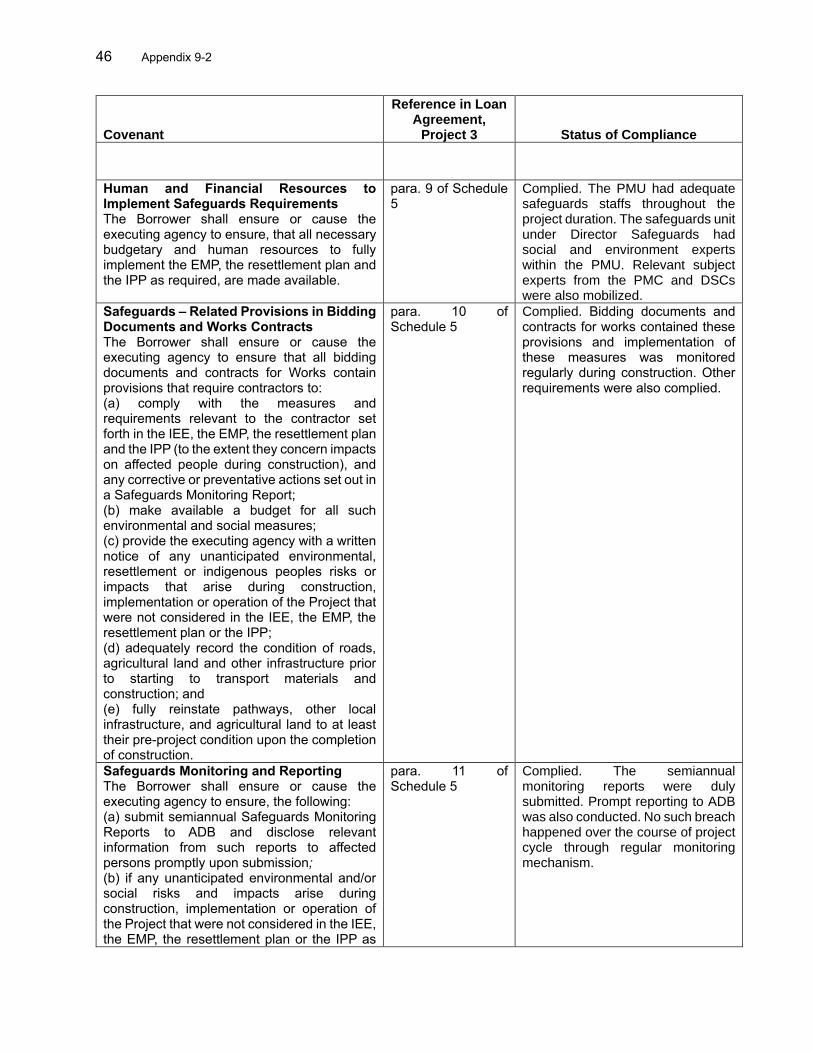

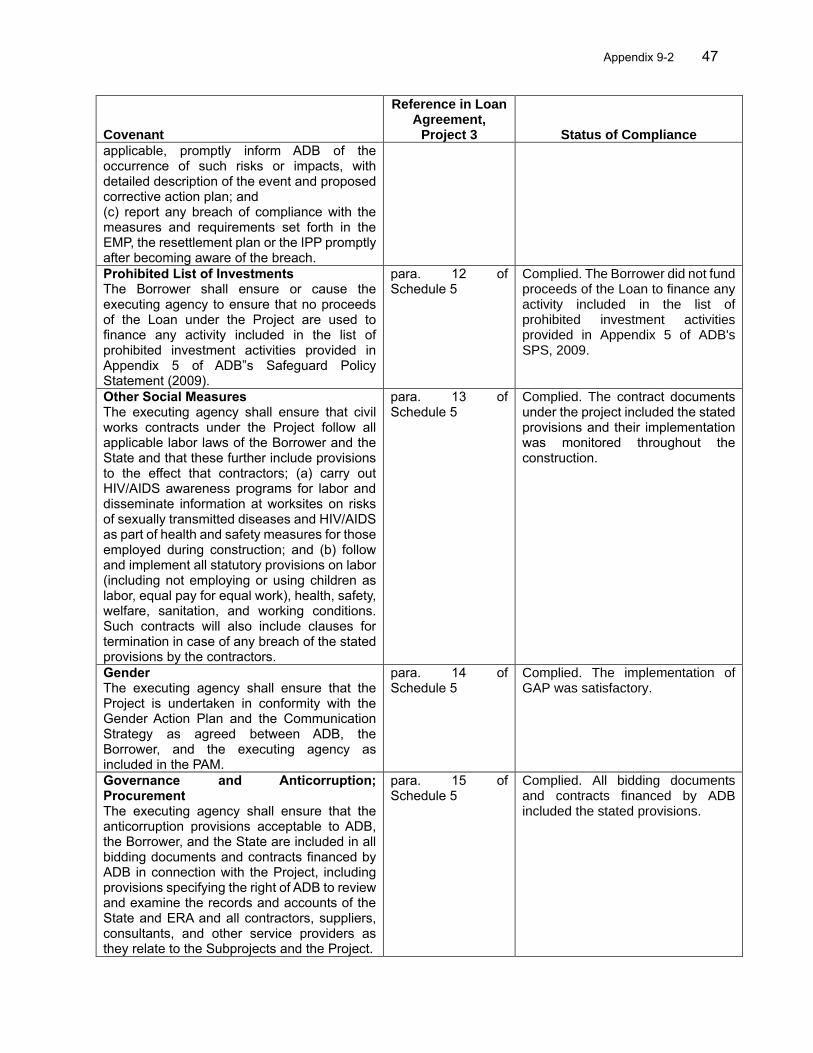

9-1. Status of Compliance with Representation and Warranties 42

9-2. Status of Compliance with Loan Covenants 43

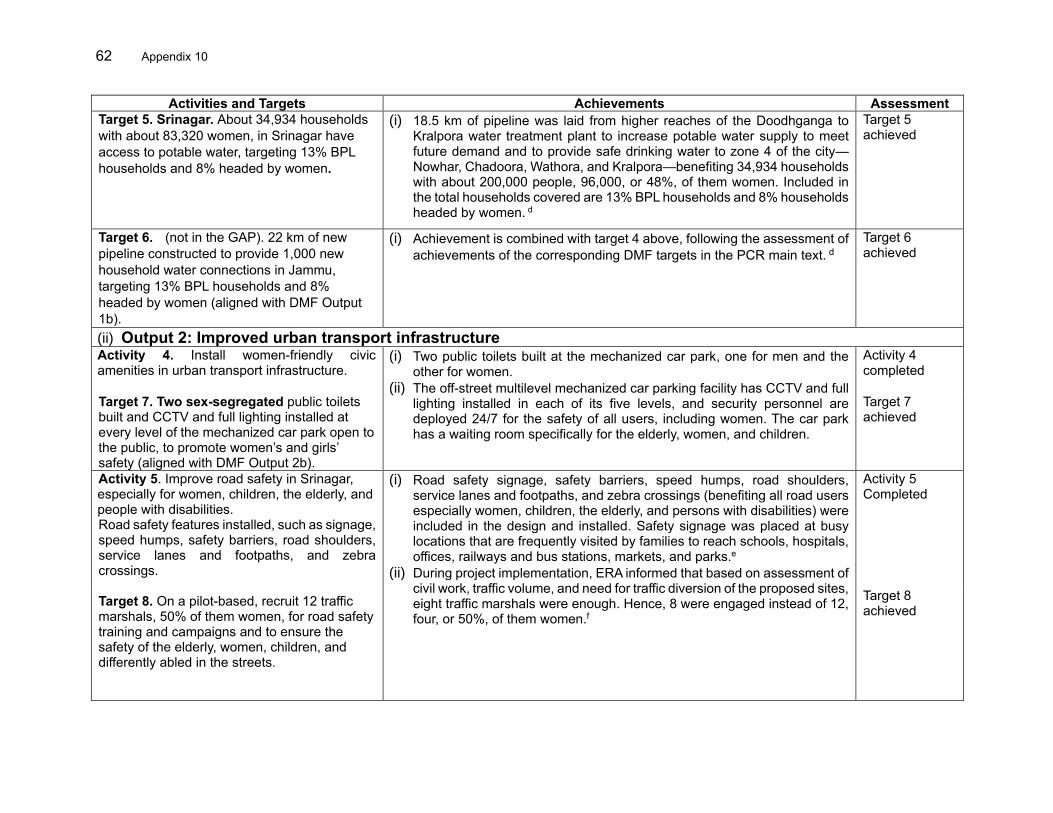

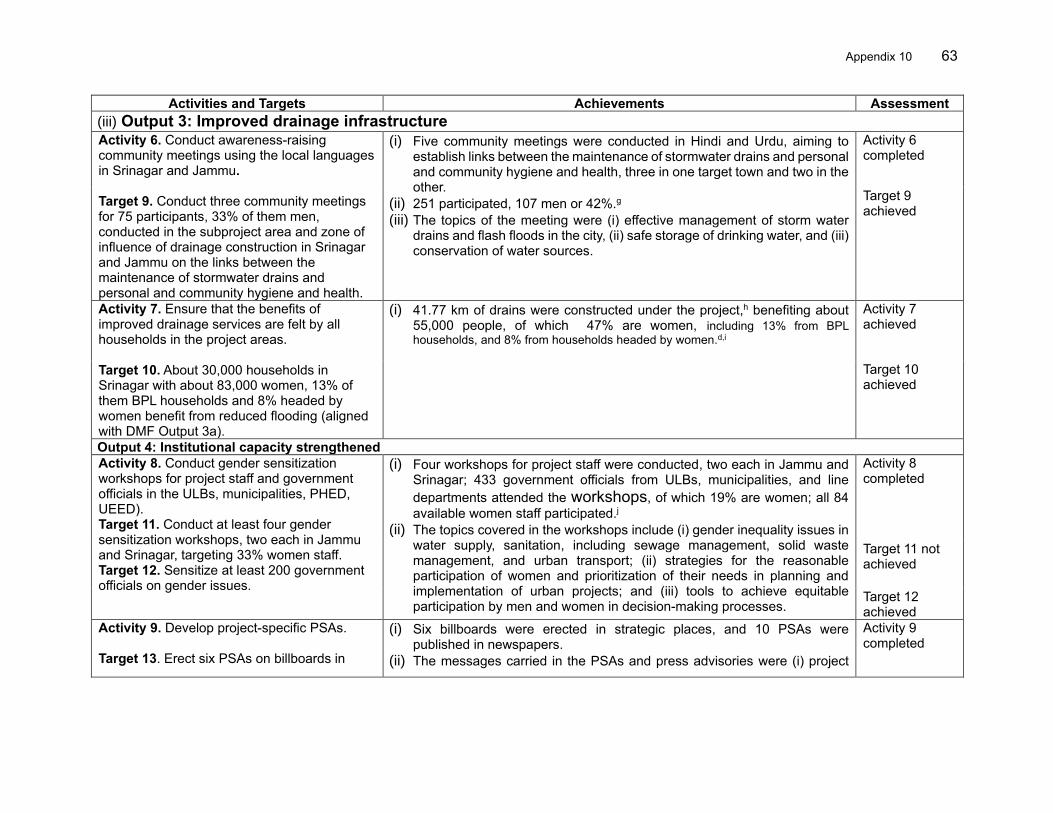

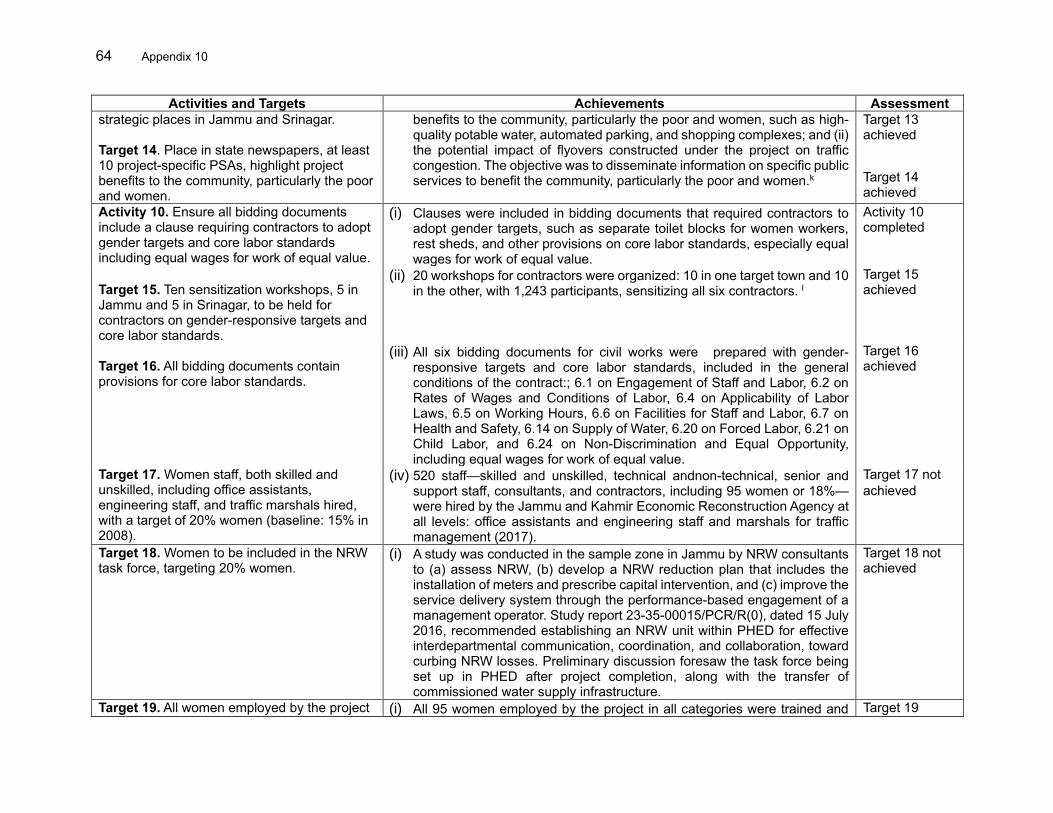

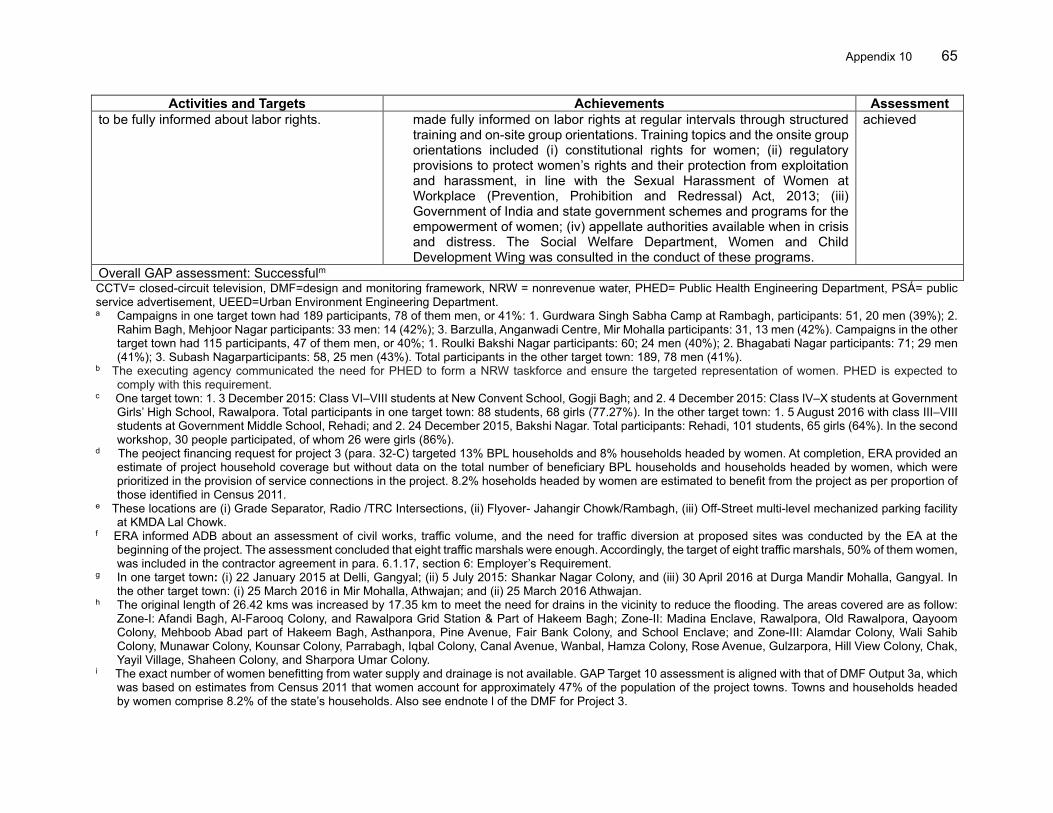

10. Implementation of Gender Action Plan and Achievements 56

11. Safeguards Assessments 68

12. Economic and Financial Analysis 72

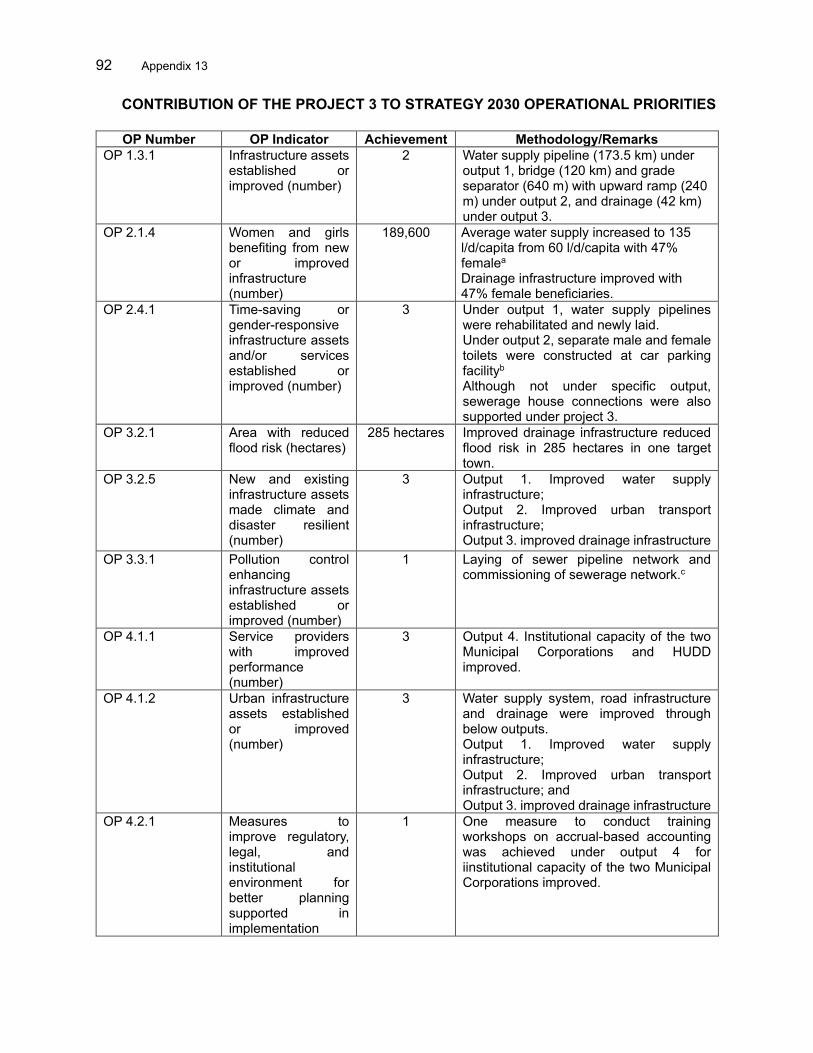

13. Contribution of the Project 3 to Strategy 2030 Operational Priorities 92

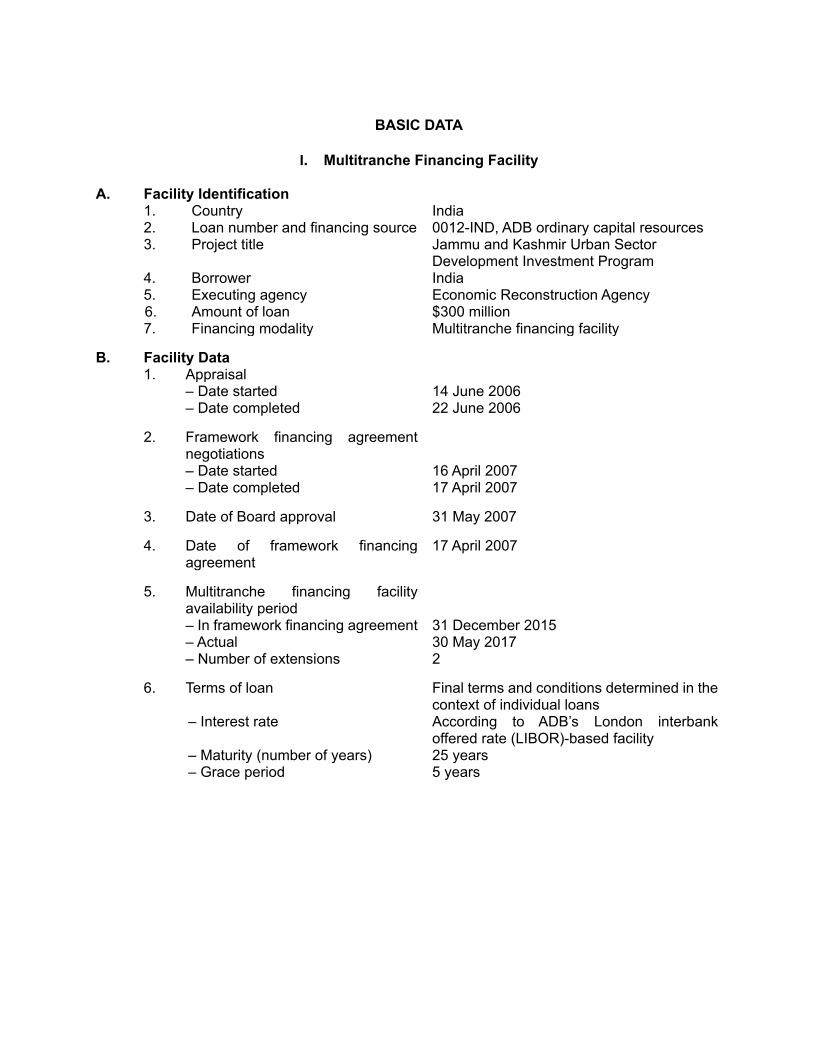

BASIC DATA

I. Multitranche Financing Facility

A. Facility Identification 1. Country 2. Loan number and financing source 3. Project title 4. Borrower 5. Executing agency

6. Amount of loan 7. Financing modality

India 0012-IND, ADB ordinary capital resources Jammu and Kashmir Urban Sector Development Investment Program India Economic Reconstruction Agency $300 million Multitranche financing facility

B. Facility Data 1. Appraisal – Date started – Date completed

2. Framework financing agreement negotiations

– Date started – Date completed

3. Date of Board approval

4. Date of framework financing agreement

5. Multitranche financing facility availability period

– In framework financing agreement – Actual – Number of extensions

6. Terms of loan – Interest rate – Maturity (number of years) – Grace period

14 June 2006 22 June 2006

16 April 2007 17 April 2007

31 May 2007

17 April 2007

31 December 2015 30 May 2017 2

Final terms and conditions determined in the context of individual loans According to ADB’s London interbank offered rate (LIBOR)-based facility 25 years 5 years

ii

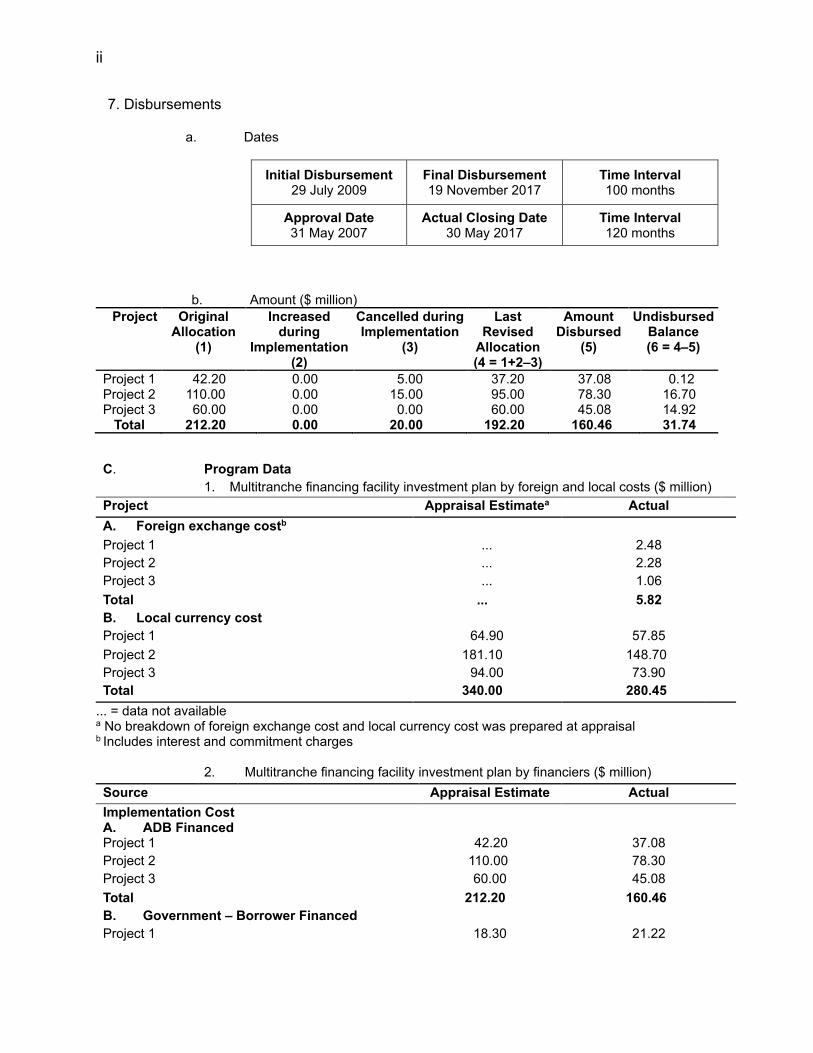

7. Disbursements

a. Dates

Initial Disbursement

29 July 2009

Final Disbursement 19 November 2017

Time Interval 100 months

Approval Date 31 May 2007

Actual Closing Date 30 May 2017

Time Interval 120 months

b. Amount ($ million)

Project Original Allocation

(1)

Increased during

Implementation (2)

Cancelled during Implementation

(3)

Last Revised

Allocation (4 = 1+2–3)

Amount Disbursed

(5)

Undisbursed Balance (6 = 4–5)

Project 1 42.20 0.00 5.00 37.20 37.08 0.12 Project 2 110.00 0.00 15.00 95.00 78.30 16.70 Project 3 60.00 0.00 0.00 60.00 45.08 14.92 Total 212.20 0.00 20.00 192.20 160.46 31.74

C. Program Data

1. Multitranche financing facility investment plan by foreign and local costs ($ million)

Project Appraisal Estimatea Actual

A. Foreign exchange costb

Project 1 ... 2.48

Project 2 ... 2.28

Project 3 ... 1.06

Total ... 5.82

B. Local currency cost

Project 1 64.90 57.85

Project 2 181.10 148.70

Project 3 94.00 73.90

Total 340.00 280.45

... = data not available a No breakdown of foreign exchange cost and local currency cost was prepared at appraisal b Includes interest and commitment charges

2. Multitranche financing facility investment plan by financiers ($ million)

Source Appraisal Estimate Actual

Implementation Cost A. ADB Financed

Project 1 42.20 37.08

Project 2 110.00 78.30

Project 3 60.00 45.08

Total 212.20 160.46

B. Government – Borrower Financed

Project 1 18.30 21.22

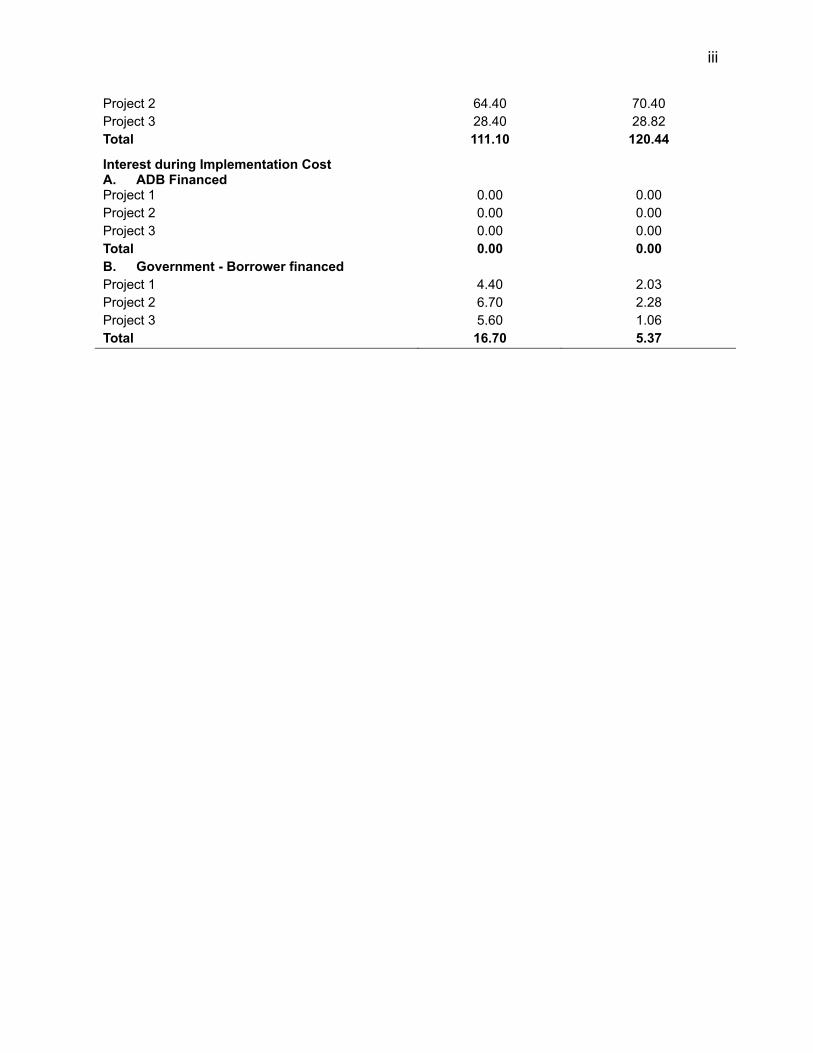

iii

Project 2 64.40 70.40

Project 3 28.40 28.82

Total 111.10 120.44

Interest during Implementation Cost A. ADB Financed

Project 1 0.00 0.00

Project 2 0.00 0.00

Project 3 0.00 0.00

Total 0.00 0.00

B. Government - Borrower financed

Project 1 4.40 2.03

Project 2 6.70 2.28

Project 3 5.60 1.06

Total 16.70 5.37

iv

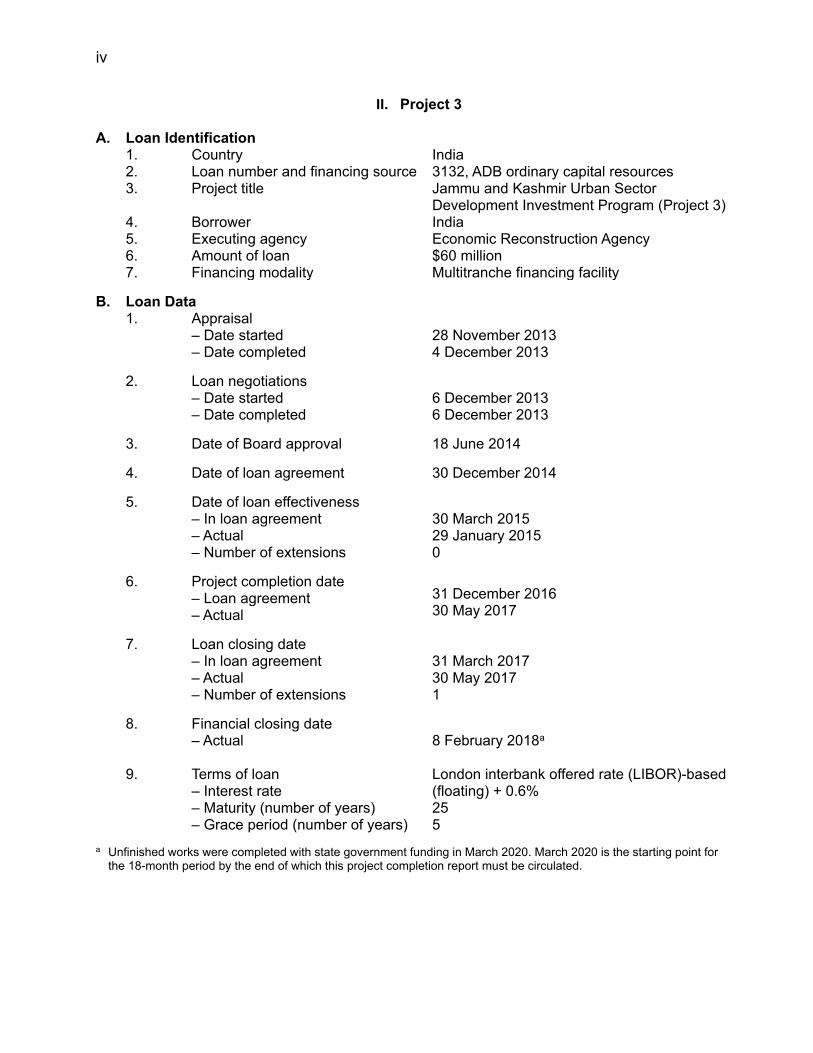

II. Project 3 A. Loan Identification 1. Country 2. Loan number and financing source 3. Project title 4. Borrower 5. Executing agency

6. Amount of loan 7. Financing modality

India 3132, ADB ordinary capital resources Jammu and Kashmir Urban Sector Development Investment Program (Project 3) India Economic Reconstruction Agency $60 million Multitranche financing facility

B. Loan Data 1. Appraisal – Date started – Date completed

2. Loan negotiations – Date started – Date completed

3. Date of Board approval

4. Date of loan agreement

5. Date of loan effectiveness – In loan agreement – Actual – Number of extensions

6. Project completion date – Loan agreement – Actual

7. Loan closing date – In loan agreement

– Actual – Number of extensions

8. Financial closing date – Actual 9. Terms of loan – Interest rate – Maturity (number of years) – Grace period (number of years)

28 November 2013 4 December 2013

6 December 2013 6 December 2013

18 June 2014

30 December 2014

30 March 2015 29 January 2015 0

31 December 2016 30 May 2017 31 March 2017 30 May 2017 1

8 February 2018a London interbank offered rate (LIBOR)-based (floating) + 0.6% 25 5

a Unfinished works were completed with state government funding in March 2020. March 2020 is the starting point for the 18-month period by the end of which this project completion report must be circulated.

v

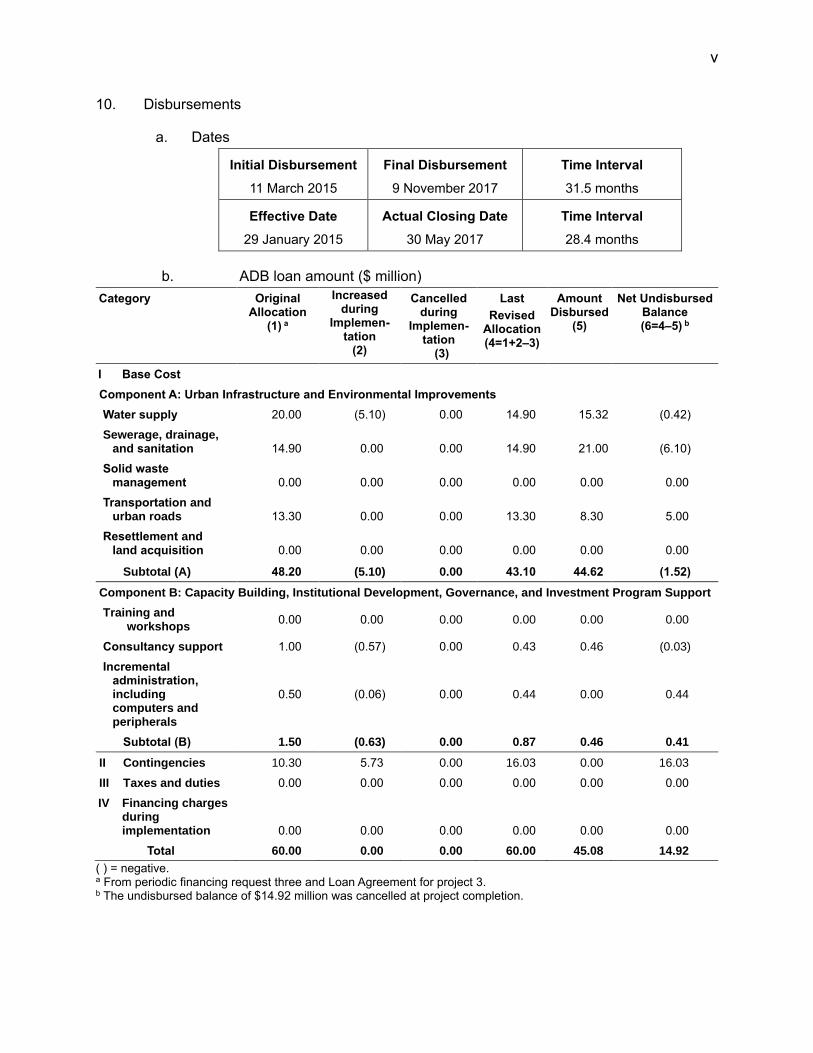

10. Disbursements

a. Dates

Initial Disbursement

11 March 2015

Final Disbursement

9 November 2017

Time Interval

31.5 months

Effective Date

29 January 2015

Actual Closing Date

30 May 2017

Time Interval

28.4 months

b. ADB loan amount ($ million)

Category Original Allocation

(1) a

Increased during

Implemen- tation

(2)

Cancelled during

Implemen- tation (3)

Last

Revised Allocation (4=1+2–3)

Amount Disbursed

(5)

Net Undisbursed Balance (6=4–5) b

I Base Cost

Component A: Urban Infrastructure and Environmental Improvements

Water supply 20.00 (5.10) 0.00 14.90 15.32 (0.42)

Sewerage, drainage, and sanitation 14.90 0.00 0.00 14.90 21.00 (6.10)

Solid waste management 0.00 0.00 0.00 0.00 0.00 0.00

Transportation and urban roads 13.30 0.00 0.00 13.30 8.30 5.00

Resettlement and land acquisition 0.00 0.00 0.00 0.00 0.00 0.00

Subtotal (A) 48.20 (5.10) 0.00 43.10 44.62 (1.52)

Component B: Capacity Building, Institutional Development, Governance, and Investment Program Support

Training and workshops

0.00 0.00 0.00 0.00 0.00 0.00

Consultancy support 1.00 (0.57) 0.00 0.43 0.46 (0.03)

Incremental administration, including computers and peripherals

0.50 (0.06) 0.00 0.44 0.00 0.44

Subtotal (B) 1.50 (0.63) 0.00 0.87 0.46 0.41

II Contingencies 10.30 5.73 0.00 16.03 0.00 16.03

III Taxes and duties 0.00 0.00 0.00 0.00 0.00 0.00

IV Financing charges during implementation 0.00 0.00 0.00 0.00 0.00 0.00

Total 60.00 0.00 0.00 60.00 45.08 14.92

( ) = negative. a From periodic financing request three and Loan Agreement for project 3. b The undisbursed balance of $14.92 million was cancelled at project completion.

vi

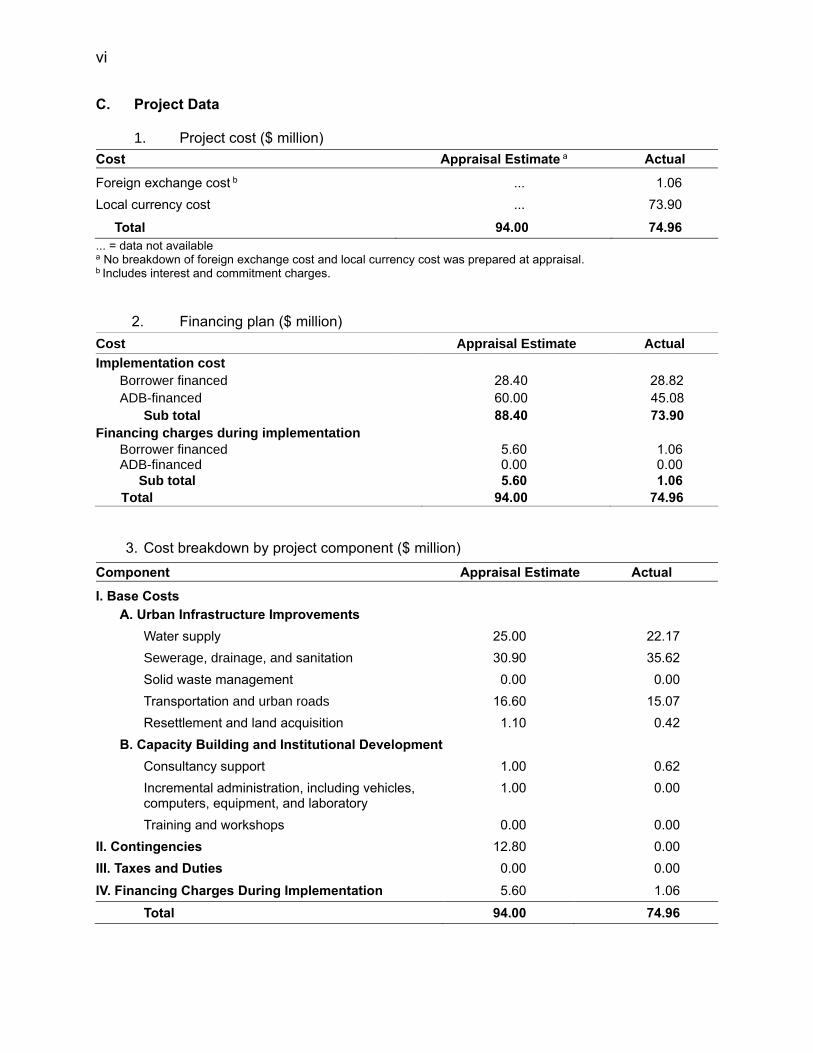

C. Project Data

1. Project cost ($ million)

Cost Appraisal Estimate a Actual

Foreign exchange cost b ... 1.06

Local currency cost ... 73.90

Total 94.00 74.96

... = data not available a No breakdown of foreign exchange cost and local currency cost was prepared at appraisal. b Includes interest and commitment charges.

2. Financing plan ($ million)

Cost Appraisal Estimate Actual

Implementation cost

Borrower financed 28.40 28.82

ADB-financed 60.00 45.08

Sub total 88.40 73.90

Financing charges during implementation

Borrower financed ADB-financed

5.60 0.00

1.06 0.00

Sub total 5.60 1.06

Total 94.00 74.96

3. Cost breakdown by project component ($ million)

Component Appraisal Estimate Actual

I. Base Costs

A. Urban Infrastructure Improvements

Water supply 25.00 22.17

Sewerage, drainage, and sanitation 30.90 35.62

Solid waste management 0.00 0.00

Transportation and urban roads 16.60 15.07

Resettlement and land acquisition 1.10 0.42

B. Capacity Building and Institutional Development

Consultancy support 1.00 0.62

Incremental administration, including vehicles, computers, equipment, and laboratory

1.00 0.00

Training and workshops 0.00 0.00

II. Contingencies 12.80 0.00

III. Taxes and Duties 0.00 0.00

IV. Financing Charges During Implementation 5.60 1.06

Total 94.00 74.96

vii

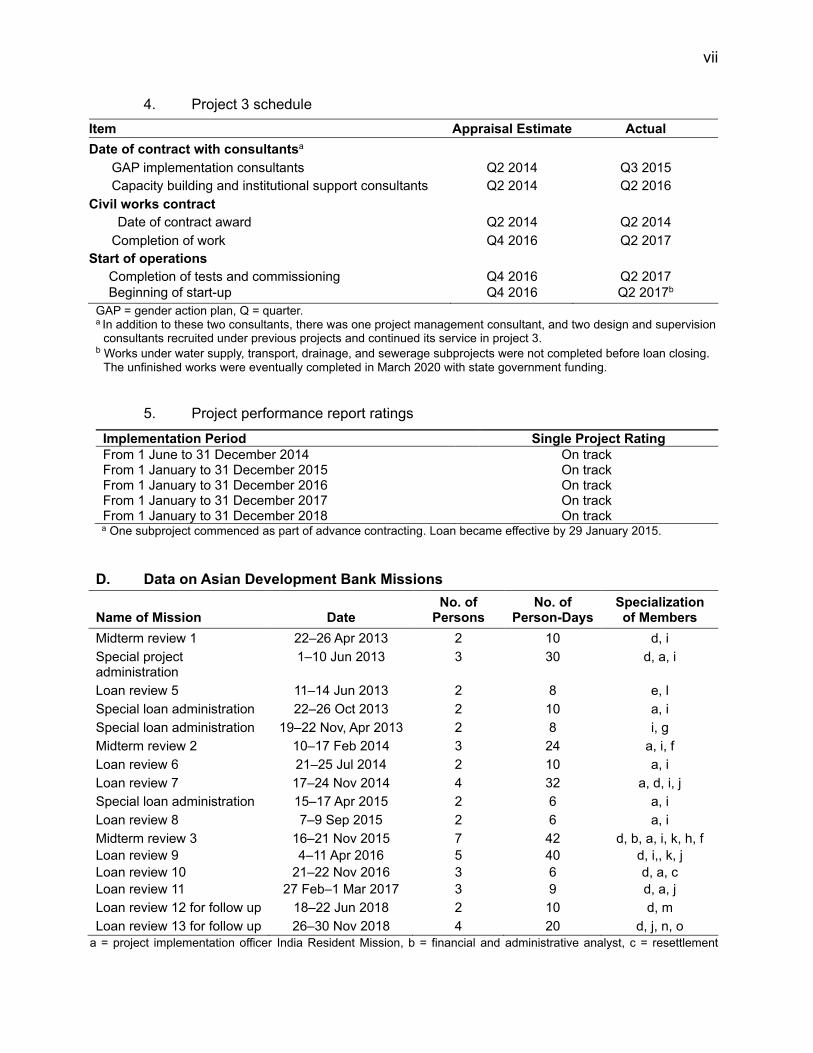

4. Project 3 schedule

Item Appraisal Estimate Actual

Date of contract with consultantsa

GAP implementation consultants Q2 2014 Q3 2015

Capacity building and institutional support consultants Q2 2014 Q2 2016

Civil works contract

Date of contract award Q2 2014 Q2 2014

Completion of work Q4 2016 Q2 2017

Start of operations

Completion of tests and commissioning Q4 2016 Q2 2017

Beginning of start-up Q4 2016 Q2 2017b

GAP = gender action plan, Q = quarter. a In addition to these two consultants, there was one project management consultant, and two design and supervision

consultants recruited under previous projects and continued its service in project 3. b Works under water supply, transport, drainage, and sewerage subprojects were not completed before loan closing.

The unfinished works were eventually completed in March 2020 with state government funding.

5. Project performance report ratings

Implementation Period Single Project Rating

From 1 June to 31 December 2014 On track From 1 January to 31 December 2015 On track From 1 January to 31 December 2016 On track From 1 January to 31 December 2017 On track From 1 January to 31 December 2018 On track a One subproject commenced as part of advance contracting. Loan became effective by 29 January 2015.

D. Data on Asian Development Bank Missions

Name of Mission Date No. of

Persons No. of

Person-Days Specialization of Members

Midterm review 1 22–26 Apr 2013 2 10 d, i

Special project administration

1–10 Jun 2013 3 30 d, a, i

Loan review 5 11–14 Jun 2013 2 8 e, l

Special loan administration 22–26 Oct 2013 2 10 a, i

Special loan administration 19–22 Nov, Apr 2013 2 8 i, g

Midterm review 2 10–17 Feb 2014 3 24 a, i, f

Loan review 6 21–25 Jul 2014 2 10 a, i

Loan review 7 17–24 Nov 2014 4 32 a, d, i, j

Special loan administration 15–17 Apr 2015 2 6 a, i

Loan review 8 7–9 Sep 2015 2 6 a, i

Midterm review 3

Loan review 9

Loan review 10

Loan review 11

16–21 Nov 2015

4–11 Apr 2016

21–22 Nov 2016

27 Feb–1 Mar 2017

7

5

3

3

42

40

6

9

d, b, a, i, k, h, f

d, i,, k, j

d, a, c

d, a, j

Loan review 12 for follow up 18–22 Jun 2018 2 10 d, m

Loan review 13 for follow up 26–30 Nov 2018 4 20 d, j, n, o

a = project implementation officer India Resident Mission, b = financial and administrative analyst, c = resettlement

viii

specialist, d = urban development specialist South Asia Urban Development Division, e = urban economist South Asia Urban Development Division, f = project analyst India Resident Mission, g = safeguard specialist, h = environmental specialist, i = associate project analyst, r = project counsel, j = consultant project specialist, k = gender consultant, l = transport specialist, m = country director India Resident Mission, n = principal portfolio management specialist, o = urban specialist India Resident Mission. Source: Asian Development Bank.

I. PROJECT DESCRIPTION 1. The Jammu and Kashmir Urban Sector Development Investment Program was designed to expand and upgrade urban services and strengthen institutional capacity in the major urban areas of the state to Indian national and state standards. The focus was on providing an improved living environment to the population including the poor and other low-income segments. The program aimed to enhance public access to water supply, sanitation, drainage, and road facilities for more than 2.4 million people living in the state’s two main cities of Srinagar and Jammu (the target towns) and other selected towns.1 It also aimed to modernize and streamline the planning, operation and maintenance (O&M), and administrative functions of the responsible departments.2 2. The Asian Development Bank (ADB) approved the program as a multitranche financing facility (MFF) on 31 May 2007 at an estimated cost of $485 million. 3 The ADB loan was $300 million, and the government contribution was $185 million. The MFF had three projects: (i) project 1 of $42 million (loan 2331-IND); (ii) project 2 of $110 million (Loan 2925-IND); and (iii) project 3 of $60 million (loan 3132-IND).4 Project 3 was approved on 18 June 2014 for project cost of $94 million including a government contribution of $34 million. It was signed on 30 December 2014 and declared effective on 29 August 2015.5 3. The MFF including project 3 aimed to achieve the expected impact and outcomes through the following outputs:

(i) Part A: Urban infrastructure improved through investments in water supply, sewerage systems, drainage, solid waste management (SWM), and urban transport. Project 3 supported water supply, drainage, and urban transport which are essential to meeting the overall objectives of the investment program.

(ii) Part B: Capacity development and institutions developed 6 through (a) establishment of semi-autonomous entities responsible for water supply, sewerage, and drainage operations; (b) establishment of e-governance system; (c) improved financial performance inclusive of tariff revisions for municipal corporation services; (d) improved accounting and financial management systems, and (e) knowledge management and capacity building.

4. At appraisal, the MFF was expected to benefit (i) 2.2 million people with access to municipal water supply; (ii) 1.0 million people with access to proper sanitation, either through sewerage or onsite facilities; (iii) 2.0 million people served by a properly functioning drainage system; (iv) 2.0 million people receiving solid waste collection services; and (v) 2.4 million people

1 During implementation, the other selected towns had to be dropped for security reasons. 2 Responsibility for basic urban services was shared among government entities as follows: capital works were

planned, designed, and implemented by the state Economic Reconstruction Agency (ERA) on behalf of the ULBs. O&M responsibility was as follows: (i) water supply systems under the state’s Public Health Engineering Department (PHED), (ii) sewerage systems were under the state Housing and Urban Development Department (HUDD), and (iii) solid waste facilities and transportation were under the ULBs. Billing and fee collection are operated by the respective entities but revenues are passed to the state. The complexity of the arrangements made capacity building essential to ensure close cooperation between the ERA and these entities.

3 ADB. 2007. Report and Recommendation of the President to the Board of Directors: Proposed Multitranche Financing Facility to India for the Jammu and Kashmir Urban Sector Development Investment Project. Manila.

4 The periodic financing requests for projects 1, 2, and 3 were; ADB. 2007, 2012, and 2014. Periodic Financing Request Report. Jammu and Kashmir Urban Sector Development Investment Program. Manila. Due to implementation delay including from local unrest, it was assessed that utilizing full $300 million was not feasible.

5 ADB. 2014. Jammu and Kashmir Urban Sector Development Investment Program - Tranche 3. Project Data Sheet. 6 Included subcomponents were continued through earlier projects and loans for the duration of the MFF.

2

having access to better road facilities.7 For institutional reforms, the MFF aimed to (i) put sector reforms in place, (ii) mainstream capacity building as part of the state urban development budget, (iii) demonstrate capacities of agencies in effective O&M, and (iv) increase public-private partnership delivery.

II. DESIGN AND IMPLEMENTATION A. Project Design and Formulation 5. The MFF and project 3 were designed in accordance with government and ADB sector strategies at appraisal. They were consistent with India’s Tenth, Eleventh, and Twelfth Five-Year Plans (2002–2017), which emphasized improvement in and augmentation of economic and social infrastructure and provision of improved municipal services in urban areas.8 They were also consistent with the state government approaches and strategies to enhance the quality of life by narrowing poverty and regional disparities, improving basic services, and developing infrastructure.9 The MFF and project 3 were also aligned with the ADB country partnership strategy and program, 2003–2006, and country partnership strategy for 2009–2012 and 2013–2017 for India aimed to support faster, more inclusive, and sustainable growth as envisaged in the 5-year plans by emphasizing infrastructure development, job creation, and environmental sustainability.10 Although the MFF and project 3 predated ADB Strategy 2030, they contributed to the following operational priorities (OPs): (i) making cities more livable (OP4); (ii) strengthening governance and institutional capacity (OP6); (iii) addressing remaining poverty and reducing inequalities (OP1); and (iv) accelerating progress in gender equality (OP2).11 6. Learnings from the first ADB loan in the state that preceded the MFF, and from other ADB projects in India had shown that project sustainability depends on three main imperatives:12 (i) subprojects are selected through extensive consultation with a wide range of stakeholders and following a demand-driven approach, (ii) institutional development is undertaken to ensure that adequate O&M funds are mobilized from internal resources and there are gradual transfers from the state to responsible institutions, and (iii) capacity building in service delivery institutions is undertaken to adopt corporatized or commercially oriented operations that include user. These imperatives guided selection of subprojects under the MFF based on public consultations, as well as subsector masterplans. Also in line with these imperatives, investments under the MFF were linked with incremental reforms and substantive support to build institutional capacity and ensure

7 All interventions under the MFF were in Srinagar and Jammu. Water supply, drainage and transport improvements

were carried out in both the towns. SWM was implemented only in Srinagar and sewerage works were only in Jammu. Institutional capacity development was implemented in both the towns.

8 Government of India Planning Commission. 2002. Tenth Five-Year Plan, 2002–2007. New Delhi; Government of India Planning Commission. 2007. Eleventh Five-Year Plan, 2007–2012. New Delhi; and Government of India Planning Commission. 2013. Twelfth Five-Year Plan, 2013-2017. New Delhi.

9 State government. 2007. Eleventh Five-Year Plan (2007–2012); and State government Planning and Development Department. 2013. Twelfth Five Year Plan (2013-2017). At appraisal, the MFF was also consistent with the state’s sector road map in conjunction with the Jawaharlal Nehru National Urban Renewal Mission (JNNURM), through which the Government of India fast-tracks reform-driven development in 63 major towns of India.

10 ADB. 2003. India: Country Strategy and Program, 2003-2006. Manila; 2009. India Country Partnership Strategy, 2009-2012. Manila; and 2013. India Country Partnership Strategy 2013–2017. Manila.

11 ADB. 2018. Strategy 2030: Achieving a Prosperous, Inclusive, Resilient, and Sustainable Asia and the Pacific. Manila.

12 ADB. 2004. Report and Recommendation of the President to the Board of Directors on a Proposed Loan to India for the Multisector Project for Infrastructure Rehabilitation in Jammu and Kashmir. Manila. Being the first project in the sector in the state, this project was able to address only a small part of the large medium-term requirements. The MFF aimed to address the remaining priority development needs. Learnings from other ADB projects are summarized in ADB. 2006. Special Evaluation Study on Urban Sector Strategy and Operations. Manila.

3

financially sustainable operations after project completion. Project 3 continued to address the infrastructure gaps and build the capacity of the responsible agencies. Based on the delays in institutional reforms under projects 1 and 2, the state introduced a more systematic and gradual approach under project 3 to develop consensus for reforms through a consultation. 7. The MFF modality was an appropriate and effective approach to facilitate a long-term relationship between the Economic Reconstruction Agency (ERA), the executing agency, and ADB. The modality also suited the nature of the complex works in urban areas, which required flexibility in scope and longer implementation period necessary to coordinate multiple stakeholders, and enabled the government entities to develop capacity. Further, it allowed adjustments in ADB support to the program given the severe winters and frequent flooding conditions. A design and monitoring framework (DMF) was prepared for the entire MFF and for each project.13 The DMF of the MFF had some weaknesses such as lack of baselines and targets, and very broad indicators. It had ambitious reform targets, such as recovery of O&M cost for water supply, that required legislative decisions which were beyond the projects’ control (para. 18). Also, more applicable impact indicators could have been selected. Nevertheless, the selected subprojects and output indicators were appropriate to achieve the intended outcomes. The DMF of the MFF was revised during the midterm review in 2015.14 As the corresponding approval memo was not prepared, the achievements in this report are assessed against the original DMF targets at MFF approval in 2007. Achievements are detailed in Appendix 1-1.15 8. For project 3, five minor changes in design were made during implementation to address realities on the ground and the urgent needs following the disastrous flood in 2014.16 First, the target for water supply distribution pipelines was reduced from 287 kilometers (km) to 155 km because (i) the pipe material was changed to a more resilient and costlier type after the 2014 floods, and (ii) the rehabilitation of the remaining 132 km was found to be less urgent abased on detailed assessment. The Public Health and Engineering Department (PHED) instead rehabilitated the balance of pipelines using other fund sources (para. 11).17 Second, loan savings from the reduced water supply subproject were partly reallocated to increase the much-needed drains after the floods in 2014 from 26 km to 42 km to mitigate future flood risk (para. 15). Third, the superstructure material of a bridge was changed from prestressed concrete to steel composite after the floods in 2014 as it would result in a stronger structure (para. 17). Fourth, because of the cost increase in the change in bridge superstructure, the construction of one grade separator was dropped (para. 17). Fifth, the other grade separator was changed from the original plan of both directions to one direction, but with an additional limb for decongestion (para. 17).18 Project 3 also supported a part of the balance work of sewerage subproject originally planned under project 1. In December 2016, to support the ERA in optimizing the utilization for project 3, reallocation of loan proceeds was approved (para. 22).

9. While the design of projects 1–3 at appraisal was appropriate to achieve the expected outcomes and outputs, it could have considered incorporating comprehensive end-to-end

13 A separate DMF for project 1 was not included when the MFF was approved. In 2011, a DMF for project 1 was

formulated as part of the retrofitting of projects in eOps for all ongoing ADB projects. For both project 2 and 3, separate DMFs were prepared during loan processing. Impact indicators for projects 2 and 3 were set as the same as the outcome indicators of the MFF in line with DMF guidelines at appraisal.

14 The main changes were (i) deletion of target towns other than the two capital towns due to security reasons and (ii) revision in outcome and output targets to reflect the scope changes.

15 After the floods in 2014, the priority of the state shifted to reconstruction efforts of damages. 16 Corresponding approval memo was not prepared for these changes. In this report, achievements are assessed

against the targets in the original DMF in the periodic financing report of project 3. 17 There were multiple investment projects implemented in parallel with project 3, including those funded by the state. 18 The subproject cost increased from $6.44 million to $8.56 million.

4

solutions such as 24/7 water supply with O&M arrangements built in construction contracts and integrated SWM with source segregation, and sewerage with reuse of wastewater. While all the subprojects planned at appraisal except for tourism were implemented, the five target towns had to be dropped because of security reasons.19 Also, during implementation, the state capacity was found more constrained than assessed at appraisal, leading to delays in capacity building and the reform program.20 Nonetheless, the program remained relevant at completion as development needs for basic urban services in the project areas should be addressed. The MFF design remained consistent with the road map and policy framework prepared by the state at appraisal for basic urban services as per national standard. There were no overlaps in intervention with other development partners.21

B. Facility and Project Outputs 10. Out of 23 MFF outputs, 15 were achieved, four were partly achieved, and four were not achieved. Of 10 project 3 outputs, five were achieved or exceeded and five were partly achieved. (Appendixes 1-1 and 1-2).22

1. Part A: Urban Infrastructure Improvements 11. Water supply. Under project 3, the total target of 287 km new and rehabilitated pipelines to benefit 54,000 households was partially achieved with 155 km for 30,000 households (para. 8). Construction of 18 km of new pipelines to increase transmission capacity by 13.45 million liters per day (mld) was completed in March 2020 using state funds. Piloting of a nonrevenue water (NRW) reduction program in an area of 3,000 consumers was achieved by replacing 16 km of pipelines and water meter installations.23 12. All of the five MFF output targets for water supply were achieved although with some delay: (i) average supply level was increased from 80 liters per capita per day (lpcd) to 135 lpcd with delay; (ii) the minimum supply hours increased from 2 hours to 8 hours;24 (iii) 80% of assessed properties were connected to the water supply system by providing 16,351 house connections;25 (iv) unaccounted-for water was reduced by rehabilitating pipelines, leading to 15% NRW ratio;26 and (v) water meters were installed with more than 10,000 meters.27 13. Sewerage. While there is no output target for sewerage in the DMF for project 3, the balance of work from project 1 was executed under project 3. A total of 27 km sewer network was

19 The five target towns were deleted at the mid-term review mission in 2015 although without approval memo. The

tourism subproject was planned to be implemented only in the five target towns. The deletion was because of the elevated security situation, which were not anticipated during MFF appraisal.

20 While the government’s capacity constraint was gradually mitigated by capacity building activities throughout the program’s duration, it did not fully achieve the intended targets.

21 The MFF was consistent with the sector road map developed by the state in conjunction with the JNNURM. 22 The details of the targets achieved with delay are in para. 23. The delays were due to combination of local unrest,

floods, and weak contractor performance. 23 Additionally, a separate package for bulk meters on tube wells, pumping stations and water treatment plant (WTP),

including automation of tube wells, a supervisory control and data acquisition system was also executed under the NRW reduction component. Under project 3, 171 km (155 km plus 16 km) of water pipeline was laid.

24 These were achieved through interventions under projects 1–3, including 19 tube wells, 148 pumps, eight overhead tanks, rehabilitating 212 km of distribution pipelines and laying 23 km of transmission pipes, and reducing NRW. Works were completed in March 2020.

25 ‘Assessed properties’ is not defined in the approved DMF. As water connection was supported only under project 3, the target is assumed to be the same as 1,000 connection which is the corresponding DMF target of project 3.

26 15% is a normal level of NRW ratio at commissioning. 27 About 8,000 water meters were installed under project 2, and another 2,000 were installed under project 3.

5

laid with 13,500 house connections, of which around 3,400 were connected under state fund after project completion. This contributed to the commissioning of the overall sewer system.

14. The achievements of MFF output targets for sewerage are mixed. The connection of at least 60% of assessed properties to the sewer system was achieved, although with delay in March 2019 by the state funds after MFF completion. For the target of improving wastewater treatment capacity from 17 mld to 260 mld, only 47 mld of treatment capacity was achieved, as the fund allocation to sewerage was shifted to more urgent reconstruction and development of drainage infrastructure after the 2014 floods.28 The target of establishing an appropriate O&M systems was partly achieved through introducing a municipal management information system for water supply and sewerage, but the O&M cost was not fully recovered as planned (para. 43).

15. Drainage. Under project 3, the output target to construct 26 km of drains for 30,000 people was exceeded with 42 km of drains constructed with delay in May 2019 with the state fund, benefitting 55,000 people.29 The increased scope utilized the loan savings from the water supply subproject to address flooding risk (para. 8). The other output target of constructing three new pumping stations was achieved as planned. There is no MFF output target for drainage. 16. Solid waste management. SWM was mainly supported under project 1 and was supplemented under project 2, but not under project 3. The MFF output target of at least 95% of waste generated being collected and transported for treatment and disposal was achieved by improving and expanding landfill capacity to 380 tons per day under project 1. Two other landfill sites with increased daily capacity of 243 tons and 335 tons were also supported under project 1.30 The MFF output target of increased efficiency of solid waste collection and transport was achieved through provision of collection equipment and development of access road to landfill site.31 However, the target of separating hazardous bio-medical waste from municipal waste was not achieved as it was implemented only on a pilot basis due to limited contractor availability. 17. Urban transport. For project 3, one output target was achieved and the other was partially achieved. The construction of a 120 meters (m) long bridge was implemented as planned, although the material of the superstructure was changed to steel for improved reinforcement after the 2014 floods, leading to cost increase (para. 8). A 640 m grade separator, instead of the original proposal of 340 m, was constructed after project completion with the state fund. The other proposed 408 m grade separator was dropped due to the cost increase in the bridge. Instead, 240 meters upward ramp was constructed to connect the 640 m grade separator for smoother traffic flow. This output is assessed as substantially achieved as the design changes were justified through the benefit of the strengthened bridge to address future flood risks. The other output to construct multistory semi-automatic parking facilities to accommodate 720 cars was partly achieved to accommodate 352 vehicles and 164 two-wheelers. The detail design during project implementation concluded that the output target to construct a parking with the planned capacity was

28 Development of a sewerage treatment plant (STP) was also dropped from project 2. 29 In the original DMF in PRF of project 3, the planned target beneficiary of drainage subproject was set as 30,000

households. This was meant as 30,000 people. In this report, achievement is assessed against 30,000 people. 30 Loan savings from other subprojects, including shifting transport to subsequent projects, were reallocated to the

SWM subproject to add more scope than planned at appraisal. This component also introduced weighing scales at entry and exit points, waste segregation equipment, and other facility and equipment which greatly reduced pollution loads in the surrounding streams. Biodegradable waste is collected and treated by composting at the landfill site.

31 Procured equipment consisted of (i) four rear-end loader compactors with 300 bins, (ii) 34 small, motorized waste collectors, (iii) 10 dumper placer vehicles with 100 bins, (iv) two hook loaders and 10 containers, and (v) 1,000 hand carts and 300 cycle rickshaws.

6

not technically feasible.32 The MFF output targets for urban transport on improved travel time on key corridors and reduction in road accidents were achieved with delay through construction of two flyovers, one bridge, and one grade separator under projects 2 and 3.33 Improvement in traffic management capacities was partly achieved with relevant training conducted to limited police personnel.

2. Part B: Capacity Building and Institutional Development 18. The capacity building and institutional development under project 3 was a continuation from the preceding projects. The output target to adopt organizational development plans for the two urban local bodies (ULBs) was partly achieved, e.g., a new water tariff and property tax was introduced and approved, while other plans, including establishment of the semi-autonomous body for water supply and sewerage service, are yet to be decided at the state legislature.34 The other output target to establish systems to generate annual financial statements for the ULBs was achieved by the introduction of double-entry accounting systems along with adoption of the State Municipal Accounting Manual. Building on these, annual financial statements were prepared up to 2016–2017 at both the ULBs.35

19. For the MFF, out of the nine targets for capacity building and institutional development, five were achieved including updating the database on the ULBs’ services, introducing online billing and collection for water tariffs, creating a geographic information system, establishing municipal management information system at the Housing and Urban Development Department (HUDD), and training staff and demonstrating abilities to perform management and service delivery functions.36 The following outputs were partly achieved: (i) recovery of O&M cost of water supply, which is still largely dependent on state budget allocation although there was an increase in water tariffs and improved collection; (ii) levy of property tax by the ULBs which is approved but implementation is yet to start. Both outputs require political approval at the state legislature which is the decision-making authority; and (iii) publication of balance sheet from FY2008–2009 for the ULBs as the publishment was limited in FY2010–2011. The target of formation of a water supply and sewerage and drainage board was not achieved as the state government decision is still pending as of now. Details of the institutional reform action plan are in Appendix 2.

C. Project Costs and Financing 20. The estimated cost for project 3 at appraisal was $94.0 million, with $60.0 million of ADB loan financing and $34.0 million of government funding. Project cost at completion was $74.96 million, consisting of $45.08 million from ADB and $29.88 million from the government. A total of $14.92 million was unutilized from the loan A total of $14.92 million was unutilized from the loan and was cancelled at loan closing. The main reasons for the reduced ADB loan amount were the Indian rupee depreciation from that at the time of appraisal, and slow physical work progress by the loan closing, with no contingency disbursement required. Project costs at appraisal and

32 The parking includes separate toilets for men and women, closed-circuit television system and full lightening as

planned at every level, with 24/7 security personnel to provide safety and security for all users including women. 33 End line survey was not conducted by ERA as PMU and consultants were downsized after MFF closure and also

due to impact of coronavirus disease (COVID-19). Alternatively, the achievement was confirmed by the community through selected interviews Given the constraints, further information would be provided during this PCR's validation.

34 Also, proposed institutional strengthening of the line departments such as recovery of O&M cost is not fully achieved as planned. Total 20 relevant trainings were conducted by the municipal support consultants.

35 The annual financial statement was not prepared after consultancy support ended in 2017. 36 The tariff for water usage has been approved up to 2020–2021 by the State Water Resources Regularity Authority.

The geographic information system was later used for property tax registers and billing and collection systems. Contractors provided hands-on trainings for better O&M of new and improved facilities.

7

completion are in Appendixes 3-1–3-2 and are summarized by financier in Appendixes 4-1–4-2.

21. The MFF design was built on a plan based on an assessed investment needs for $485.0 million, with an ADB loan component of $300.0 million and state contribution of $185.0 million. Because of currency depreciation, $20.0 million was cancelled from the ADB loan ($5.0 million from project 1 and $15.0 million from project 2). Disbursement was also affected by implementation delays (para 23). At completion, $160.5 million of ADB funds were disbursed with a state contribution of $125.7 million.37

D. Disbursements

22. In the early stages of implementation of project 3, disbursement was slow because of the delays in loan signing after the 2014 floods, late mobilization of contractors, and physical work progress. Disbursement commenced in March 2015 and $9.7 million was disbursed in the same year. In 2016, disbursement picked up considerably reaching more than $14 million. In 2017, disbursement further increased to $21.2 million, but the project was not able to make up for the initial delays. Poor contractor performance, especially in three contracts (water supply pipeline, storm water drainage, and one grade separator), hindered implementation progress.38 At the MFF financial closing in February 2018, the total disbursement was 76% of the loan amount. In 2016, a reallocation of ADB loan proceeds was approved to support the ERA in optimizing the utilization of the loan amounts under project 3 and to reduce the anticipated state financial burden for spillover works.39 The change was retroactively applied to past claims.40 The disbursement projection at project effectiveness was rather optimistic given the limited contractor interest in working in the state due to increasing local unrest. All withdrawal applications were submitted to ADB through the controller of aid accounts and audit of the Ministry of Finance of the Government of India. The project used the mechanism for disbursement through statements of expenditure, direct payment and reimbursement based on documented claims.41 All disbursement-related qualifications raised by the auditors were duly addressed. Appendix 5 presents projected and actual loan disbursements.

E. Project 3 and Facility Schedule 23. The original loan closing of project 3 in March 2017 was extended once to May 2017. The spillover works financed by the state were completed by March 2020 (para. 27).42 The delays were because of the persistent slow progress of civil works and procurement caused by limited interest from contractors, combined with security reasons throughout projects 1–3. Project 3 was also affected by the historic 100-year flooding in September 2014, which delayed the loan signing until December 2014,43 and local unrest from time to time, which were factors external to the project. After the 2014 floods, the project required additional time to shift the focus of intervention to asset rehabilitation and works related to flood control. The ERA and state staff were also overloaded with multiple large projects, and an overlap period with projects 1 and 2. Based on experience in delays in projects 1 and 2, the ERA introduced contractual incentives with bonuses

37 Also, some projects were taken up under other project with state funds. The ratio of ADB loan to the state contribution

at MFF completion was reduced from 64:36 at appraisal to 60:40 at completion. 38 Delays were persistent although ERA closely monitored the works progress to resolve any implementation issues. 39 Approved memo dated 20 December 2016. The ADB financing share in civil work increased from 80% to 82%. The

change was made within the allowable cost sharing ratio of 80:20 between ADB and the Government of India. 40 Retroactively applying the changes to past claims led to an additional $5.6 million being utilized in the project 3 loan. 41 The project used a simplified process for statements of expenditure, not requiring supporting documents for

individual payments up to $100,000. 42 Water supply, drainage, sewerage, and transport subprojects were completed through the state funding. The water

supply subproject was the last to be completed in March 2020. 43 The ADB Board approved project 3 in June 2014.

8

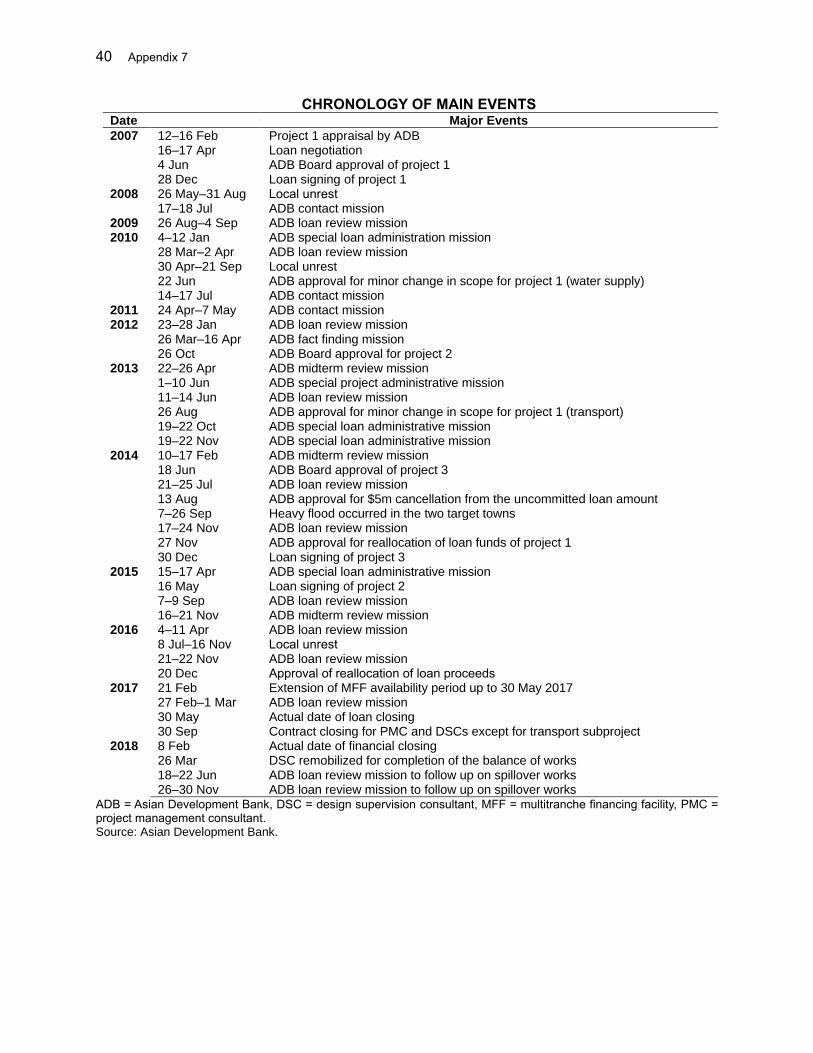

for on-time completion with a more stringent monitoring system. Despite this, contractor performance did not improve. The availability period of the MFF was extended twice, from 31 December 2015 to 31 March 2017 and then from March 2017 to May 2017, to (i) optimize loan utilization, (ii) enable the completion of ongoing works to maximize project outcomes, and (iii) reduce the state’s financial burden for spillover works (para. 22).44 A chronology of main events is in Appendix 7.

F. Implementation Arrangements 24. The implementation arrangements for the MFF and projects 1–3 were consistent with the design at appraisal, and were appropriate to achieve the envisaged outputs. The executing agency was the ERA, guided by state inter-ministerial and city committees and a works finalization committee chaired by the division commissioner. The ERA established a dedicated project management unit (PMU) and project implementation units (PIUs) in the target cities. The PMU and PIUs were assisted by a project management consultant (PMC) and design and supervision consultants (DSCs). The PMC and DSCs supported the preparation of detailed designs and bidding documents, the bidding process, and construction supervision. The following consultancies were also engaged under project 3: (i) capacity building and institutional support for the two ULBs and the PHED, (ii) implementation support of the gender action plan (GAP), and (iii) support for the preparation of a NRW reduction action plan under projects 2 and 3. Safeguard consultants were mobilized for environmental and social aspects. G. Technical Assistance 25. The preceding ADB-funded project (footnote 12) was accompanied by a $0.5 million project preparatory technical assistance (TA) to prepare a comprehensive investment plan.45 The TA supported the preparation of the program design as an MFF. Sector plans and policies to promote cost recovery through tariff reform were also prepared under the same TA, which became part of institutional strengthening under the MFF. To further support the ERA in project implementation, ADB approved $0.4 million of advisory TA in 2006.46 The advisory TA supported the ERA—especially at early stages of the MFF until the TA closure in March 2009—to (i) improve its functionality, (ii) build its project management and implementation capacity, (iii) expedite contract award and execution by providing guidance to the ERA on procurement-related issues, and (iv) assist in setting and achieving yearly targets for contract award and disbursement. H. Consultant Recruitment and Procurement 26. Consultants were recruited under the MFF in accordance with the ADB Guidelines on the Use of Consultants.47 Project 3 followed the Guidelines on the Use of Consultants (2013, as amended from time to time). The ERA followed the quality- and cost-based selection procedure to select the PMC and two DSCs. Only one local engineering firm qualified for the large consulting contracts for storm water drainage.

44 The second extension of MFF was up to the maximum allowable availability period of 10 years, and subsequently

projects were extended. The two extensions were approved by ADB on 14 August 2012 and 2 February 2017. 45 ADB. 2004. Technical Assistance for Preparation of the Jammu and Kashmir Urban Infrastructure Development

Project. Manila (TA 4515-IND, approved on 21 December 2004). 46 ADB. 2006. Technical Assistance to India for Strengthening Urban Project Management in Jammu and Kashmir.

Manila (TA 4888-IND, approved on 2 December 2006). ADB. 2010. Technical Assistance Completion Report for Strengthening Urban Project Management in Jammu and Kashmir. Manila (rated highly successful).

47 ADB. 2013. Guidelines on the Use of Consultants by Asian Development Bank and its Borrowers. Manila was followed in project 1 and project 2.

9

27. Overall consultant performance in the MFF including project 3 is rated generally satisfactory.48 The original PMC and one of the DSCs from the preceding projects had difficulty fielding and retaining experienced staff, and thus was replaced on contract completion. The new PMC, mobilized in May 2013 and the new DSC, mobilized in July 2014, performed substantially better. However, implementation of their services was delayed because of site constraints, design changes, and consequent delay in finalizing drawings. The contracts with the PMC and DSCs were retained after MFF completion to supervise the spillover works, but their inputs were gradually scaled back, leading to delays in full completion under the state funding. The end-line surveys to assess the achievements of some of the DMF targets were not conducted. The performance of the capacity building and institutional support and GAP consultants were generally satisfactory as per the required outputs. 28. Procurement was generally carried out as planned although with delays because of limited contractor interest and state capacity. The original contract award projection was rather optimistic in this regard. Procurement of all civil works contracts followed ADB Procurement Guidelines (2013, as amended from time to time). All civil work packages under project 3 estimated to cost less than $17 million were procured through national competitive bidding using single-stage, two-envelope bidding procedures. All contracts were bills of quantity based on item rates. Preparation of standard bidding documents, bid evaluations, and contract awards were per ADB guidelines. Review of all stages as per the Procurement Guidelines was conducted by ADB prior to contract award. The projected and actual contract awards are in Appendix 6. 29. The performance of contractors was unsatisfactory as the eight major contract packages were delayed and were completed using state funding (para. 23). The PMU and PIUs, assisted by the PMC and DSCs, held regular meetings with contractors to resolve hindrances and execution issues. Despite this support, three of the eight contracts proceeded especially slowly, and low personnel deployment was persistent.49 A summary of contract details is in Appendix 8. I. Gender Equity 30. Project 3 was categorized effective gender mainstreaming.50 A GAP was prepared to create equal opportunities for women to participate in and benefit from the project. The GAP focused on providing urban services for low income and households headed by women; providing for the needs, safety, and privacy of women and girls on public transport; and promoting improved health and hygiene-related practices among female household members living in the zones of influence of drainage construction works. The other GAP features were raising the awareness of people, including low-income households and households headed by women, on (i) gender issues and behavior change initiatives in water conservation; (ii) links between the maintenance of storm water drains and personal and community hygiene, health, and sanitation; and (iii) reducing, reusing, and recycling waste. The GAP also included the capacity development of the ULB and the municipal and project staff on gender concepts; the different roles of women in managing water, sanitation, hygiene, and health; and good practices in gender-inclusive urban development.

31. The project made efficient arrangements for GAP implementation, monitoring, and reporting (para. 7 of Appendix 10). The ERA’s social and resettlement experts supervised GAP implementation with the support of the social and resettlement consultant. ULBs and other line

48 In case of project 1, consultant performance is rated less than satisfactory and the original PMC and one of the DSCs

were replaced upon contract completion. 49 The three contracts with slow progress were one each in water supply, drainage, and transport subprojects. 50 Project 1 was categorized no gender elements.

10

departments were actively involved in awareness raising, community mobilization, and capacity development activities. The project converged with the ULBs and other line departments to support awareness-raising, community mobilization, and capacity development activities on gender equality aspects. The budget for GAP was adequately allocated and helped recruit a consulting firm led by a gender specialist for the timely and effective implementation of the GAP. The project collected sex-disaggregated data and submitted the progress reports on GAP implementation regularly (para. 40).

J. Safeguards

32. Project 1 of the MFF was classified as B sensitive for environment while projects 2 and 3 were category B. For involuntary resettlement, projects 1 and 3 were category B,51 while project 2 was category A. For indigenous peoples, the MFF and all its tranches were classified as category C. An environmental assessment and review framework, resettlement framework, and indigenous peoples planning framework were prepared for the MFF facility and revised during loan processing to be consistent with ADB’ Safeguard Policy Statement (2009).52 Under project 3, five initial environmental examinations (IEEs) and three resettlement plans were prepared reviewed, cleared, and disclosed by ADB and ERA on their websites in accordance with ADB and government requirements (Appendix 11). No significant environmental or resettlement impacts were observed during project 3. No indigenous peoples were affected during implementation of all three projects. While safeguard management in terms of institutional arrangements, information disclosure, consultations, project staff capacity building, and regular submission of semiannual safeguard monitoring reports—was generally satisfactory, there is an outstanding issue of pending compensation payments for one drainage subproject under project 2, as land ownership could not be established. A corrective action related to pending compensation payments under project 2 was discussed and agreed with ADB, with payment to be accomplished by July 2021. The PMU also confirmed that the decision of the High Court is awaited regarding the amount escrowed (₹21.08 million) towards payments to landowners requesting higher compensation rates for the landfill site under project 1. Safeguards compliance under projects 1 and 3 is rated effective, while with the pending required corrective action, safeguards compliance for project 2 is rated less than effective. K. Monitoring and Reporting 33. All MFF assurances and project 3 covenants were complied with, except for the eight partial compliance mainly for institutional reforms that have not yet fully achieved, and three noncompliances related to financial management. Financial empowerment of the municipalities was partially complied with, with some notable achievements such as introduction of an accrual-based accounting system. Infrastructure development or urban development taxes are being levied, albeit at low levels. Thus, the levy of a sustainable user tariff is also partially complied. Safeguard covenants were complied with, but compensation payments to the affected people in the drainage subproject under project 2 are yet to be completed (para. 32). The covenants related to procurement were partially complied with because of poor contractor performance and implementation delay, especially in the transport subproject. 34. Separate project financial accounts were maintained and audited by statutory auditors.

51 At appraisal, project 1 was classified category A for involuntary resettlement and a full resettlement plan was

prepared for the BC Road Flyover subproject. The subproject was dropped from project 1 and moved to project 2. 52 For project 1, the applicable policies were: (i) ADB. 2002. Environment Policy. Manila. (ii) ADB. 1995. Involuntary

Resettlement. Manila. and (iii) ADB. 1998. The Bank’s Policy on Indigenous Peoples. Manila. For projects 2 and 3, the policy applicable is ADB. 2009. Safeguards Policy Statement. Manila.

11

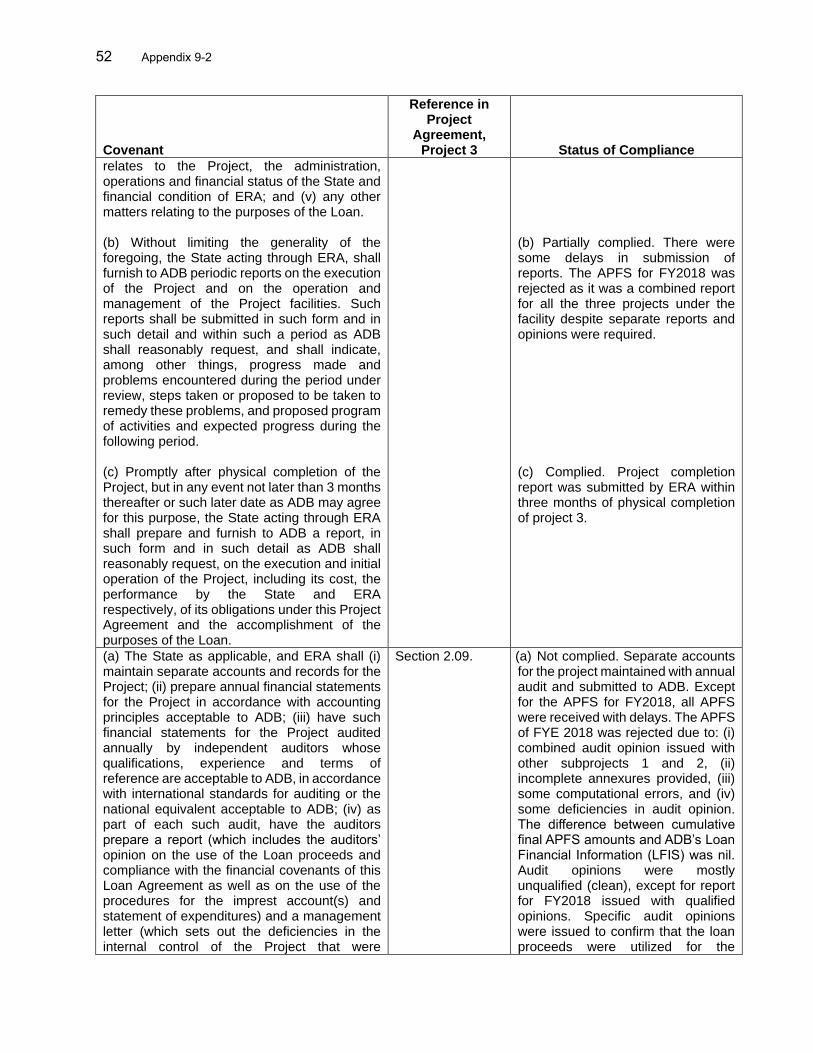

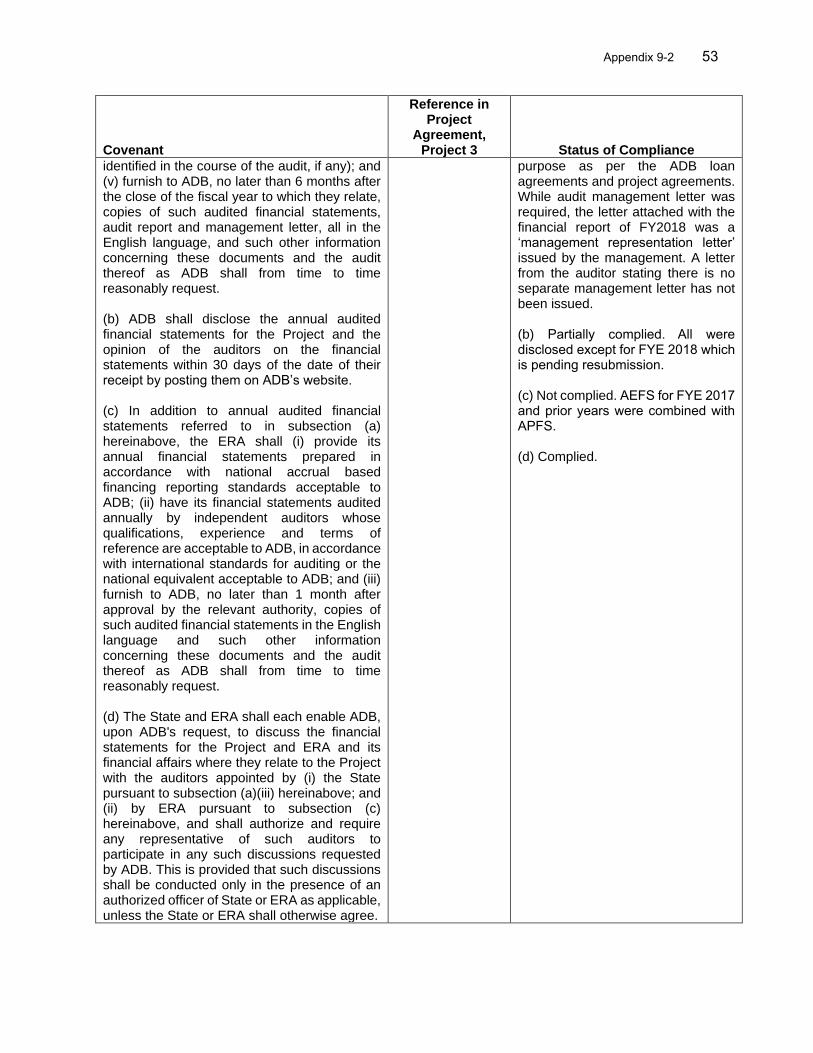

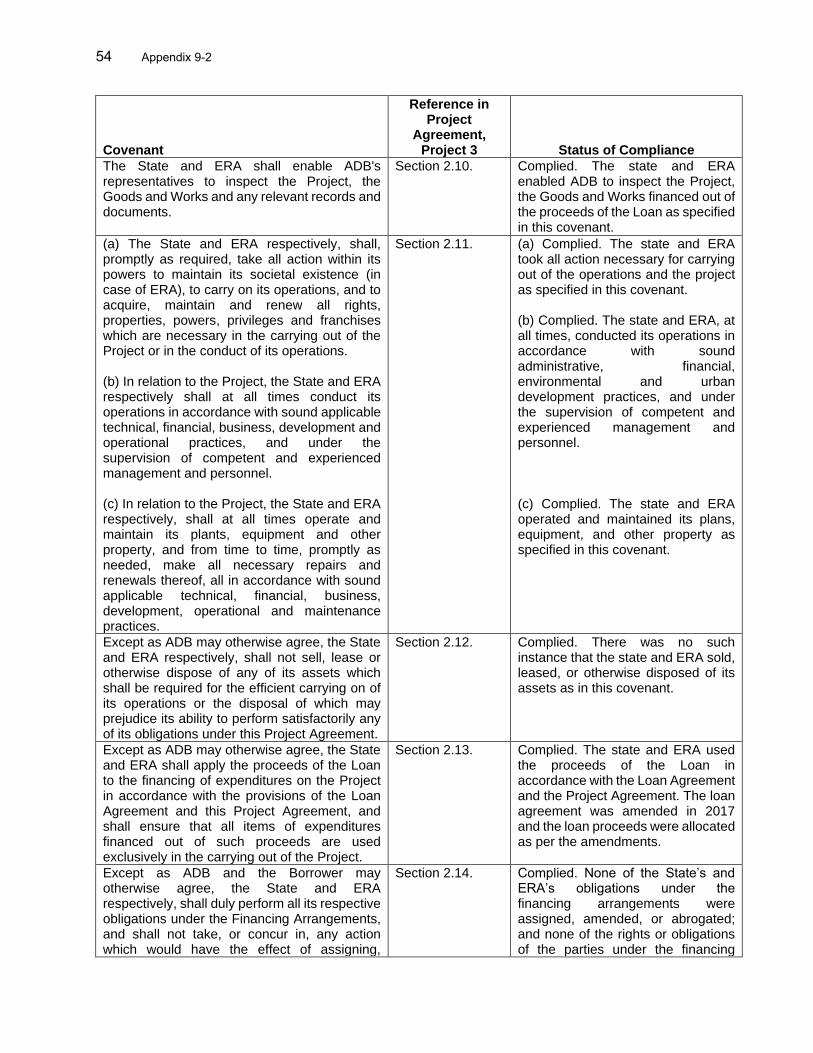

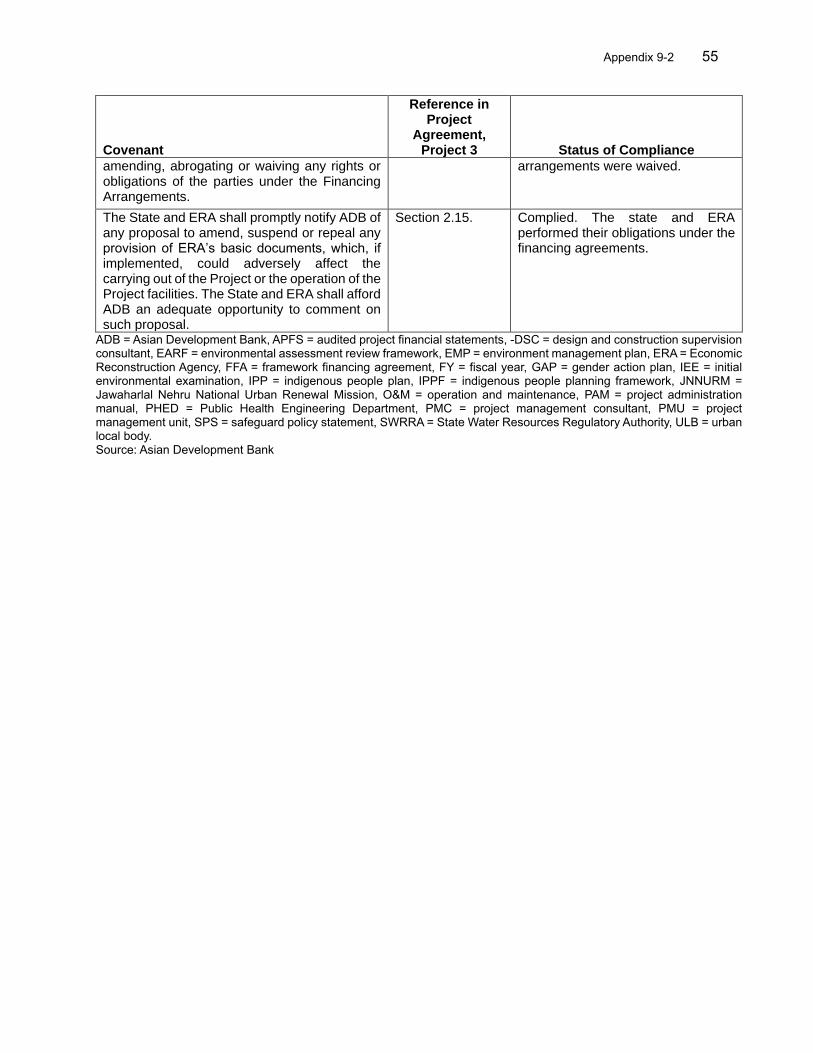

Except for fiscal year (FY) 2018, audited project financial statements (APFSs) were received, albeit with delays of 0.6–3.8 months from due dates, within the grace period of 6.0 months.53 For FY2008, no APFSs or audited entity financial statements (AEFSs) were submitted. The APFSs for FY2018 were rejected as they included a combined audit report for all three projects despite separate reports and opinions being required. Also, AEFSs for FY 2017 and prior years were combined with APFSs. These constituted non-compliances. Of 61 loan covenants of project 3, 50 were complied with, eight were partly complied with, and three were not complied with. Appendixes 9-1–9-2 detail the status of compliance with assurances and loan covenants.

III. EVALUATION OF PERFORMANCE A. Relevance 35. The investment program and project 3 is assessed relevant to government development objectives and ADB country and sector strategies, both at appraisal and completion (para. 5). Though the project predated ADB’s Strategy 2030, it aligns with its operational priorities, especially on building livable cities and providing safe and effective water and sanitation services. At completion, the project remained in line with the ADB policy focus for India on inclusive growth, infrastructure, and environmental sustainability. The project aligned with the government’s successive 5-year plans; the National Institution for Transforming India Aayog’s 3-year action agenda, FY2018–FY2020;54 and the state’s Eleventh and Twelfth Five-Year Plans, FY2007–FY2018, which prioritized potable water supply in urban areas, wastewater management, and urban poverty alleviation.55 The project currently aligns with state priorities for poverty reduction through improved access to potable water and sanitation, good governance, and private participation. The MFF did not overlap with other development partner’s initiatives. As the target towns have a relatively lower rate of participation and representation of women in community activities, the program design also included targets for participation of women in awareness-raising and capacity building activities. The program’s gender strategy ensured equal benefit for women from the water supply services, public transport, drainage improvement, which strengthened the program’s relevance. 36. The MFF modality was appropriate considering the complexity of the design, as it provided the flexibility to move outputs to other projects without affecting the facility outcome (para. 7). It also made it possible to respond to urgent development needs such as rehabilitation of damaged infrastructure after the floods which also contributed to the facility outcome. While some weaknesses in the DMF were observed (para. 7), outputs were appropriate to achieve the target outcome indicators. 56 Implementation of the program was significantly affected by external factors particularly major flooding and security issues, which were not anticipated during appraisal but necessitated adjustments in the design and scope of the projects. While there were mitigating measures, limited contractor interest and state capacity constraints also posed challenges during the implementation. Nonetheless, the state demonstrated strong ownership and commitment by completing all the remaining works using its own funds which shows that the program

53 Reports delayed by 0.8 months for FY2010, 0.7 months for FY2011, 3.8 months for FY2012, and 0.6 months for

FY2015. 54 The National Institution for Transforming India Aayog is a Government of India policy think tank that provides

directional and policy inputs, designs strategic and long-term policies and programs, and provides technical advice to the central and state governments.

55 Government of India National Institution for Transforming India Aayog. 2017. India Three-Year Action Agenda, 2017–2018 to 2019–2020. Delhi; State government, Planning Department. 2012. Eleventh and Twelfth Five-Year Plans, 2007–2018. Delhi.

56 There were efforts to adjust the DMF of the MFF at the mid-term review mission in 2015 considering the circumstances at that time, however corresponding approval memo was not processed (para. 7).

12

interventions and objectives are critical for the state. The GAP responded to gender issues identified during the project design phase, such as lower rate of participation and representation of women in community activities. The project’s gender strategy ensured equal benefit for women from the water supply services, public transport, drainage improvement.

37. Changes in scope of project 3 (para. 8) were necessary to better address emerging realities, and to mitigate the risks of flooding in the project areas. In particular, adjustments were made to strengthen the structure of the 120 m bridge and works for the drainage component were increased, both to reduce future risks from flooding. While the original targets in the DMF remain because formal changes in scope were not done, these adjustments done on the ground increased the relevance of the project. B. Effectiveness

38. Project 3 is rated effective.57 Using weights based on the actual cost of each subproject, the overall achievement of outcomes and outputs was assessed as 90% and 106%, respectively (Table A1.3).58 Urban services in the target towns improved as evidenced by: (i) increased water supply in one target town to the national standard of 135 lpcd for 200,000 people (47% female) against a target of 185,000; (ii) increased water supply to 135 lpcd for 168,000 people (47% female) in another target town against target of 282,000 people;59 (iii) reduced incidence of water logging to 0.3 hours for 1 day in a year resulting from improving drainages in one target town; and (iv) reduced average travel time from Dal gate to Lal Chow from 30 to 15 minutes due to the constructed grade separator, and parking facility.60 39. The MFF is rated less than effective.61 Using the same weighting methodology based on actual cost of each subproject, the overall achievement of outcomes and outputs was assessed as 62% and 68%, respectively (Table A1.2).62 The MFF achieved or substantially achieved the following outcome targets: (i) reduction in the volume of wastewater discharged to storm drains resulting from the constructed sewerage facilities; (ii) service to 1.63 million people with functioning drainage against a target of 2.0 million; and (iii) increase in public private partnership in service delivery through the parking facility and the collection of SWM charges. The facility partly achieved the following outcome targets: (i) 1.52 million people against the target of 2.2 million people given access to municipal water system through tube wells, overhead tanks, pipelines, and NRW reduction;63 (ii) 1.1 million people against a target of 2.0 million benefitted from improved solid waste facilities such as new and improved landfill sites served to accommodate large quantity of debris and municipal waste after the 2014 floods, which

57 Three of the six outcomes and five of the 10 outputs were achieved, including one outcome and one output exceeding

the targets. The other outcomes and outputs were all partly achieved. 58 The weighted output is more than 100% because of the exceeded achievements in the drainage output target. 59 The partial achievement of beneficiaries is due to reduced water supply pipelines (para. 8). 60 For (iii) and (iv), end-line surveys were not conducted as the PMU was downsized at the completion after MFF

closure. Based on interviews with selected residents, the targets are assessed as achieved. It is assumed that the construction of the parking facility resulted in partly reduced travel time because of less street parking although this was not up to the planned level because of a lower vehicle capacity.

61 Three out of 10 outcomes and 16 out of 24 outputs were achieved. Six outcomes and five outputs were partly achieved, and one outcome and three outputs were not achieved. At appraisal, five district towns with a total population of 0.4 million were included in the target towns. These were dropped for security reasons, leading to fewer beneficiaries in all subprojects.

62 Other municipal/urban infrastructure subproject for the five towns was not implemented due to security reason. This subproject is not considered in the overall weighted outcome of the MFF.

63 The partial achievement was largely due to reduced water supply pipelines (para. 8).

13

contributed to the town’s early recovery, and prevented disease outbreaks;64 (iii) 1.8 million people against a target of 2.4 million people given access to better road facilities such as flyovers, bridge, and grade separators;65 (iv) sector reforms such as preparation of economic opportunity development plans, establishment of e-procurement, adoption of accrual based accounting system initiated and online billing and collection for water supply service introduced, which are currently is being functional and used; (v) capacity of relevant agencies developed using state budget; and (vi) capacities of agencies in O&M of assets improved through training, increased tariff and revenue base, and efficiency in water tariff collection. The target on providing 1.0 million with access to sanitation was not achieved as only 0.2 million people benefited due to the reduced scope under projects 2 and 3 (para. 14).66 For capacity building and institutional development, creation of a semi-autonomous water board is awaiting state’s political decision. Recovery of O&M cost of water supply has also been delayed. 40. The overall safeguards compliance under projects 1 and 3 is rated satisfactory, but because the required corrective action is pending for project 2, the safeguards compliance for that project is rated less than satisfactory (para. 32). The overall implementation of gender mainstreaming supported by GAPs in projects 2 and 3 was successful. It sought to address gender and development challenges highlighted at appraisal. In summary, project 2 completed 9 of 10 (90%) activities and achieved 13 of 14 (93%) quantitative targets.67 41. Project 3 completed all 10 of 10 GAP activities (100%), and achieved 16 of 19 (84%) combined quantitative targets of the GAP and DMF (Appendix 10). The MFF, including project 3, achieved substantial strategic and practical gender benefits. The strategic gender benefits include (i) incorporation of women’s needs and priorities in project planning, design and management; (ii) a better understanding of the interrelationship between gender and transport; and (iii) enabling institutional environment and institutional capacity in gender mainstreaming. increased spaces for women to participate in the planning, designing, and management of urban infrastructure and services. The practical gender benefits are (i) reduced women’s time poverty with increased access to quality water and sanitation services, which has enabled them to spend more time for socializing with neighbors, and learning new skills; (ii) increased ability to manage household water and sanitation needs after attending awareness campaigns, behavior change workshops, and community meetings, where 60% of the participants were women; and (iii) safety and convenience in public places. The 30,000 households that benefited from the laying and rehabilitation of water pipelines and approximately 55,000 persons who benefited from the construction of the drains, include 8% households headed by women; and an estimate of 47% of the beneficiaries are women. The gender mainstreaming elements supported by projects 2 and 3 proved effective in establishing models to replicate gender equality and women’s empowerment in urban development. C. Efficiency 42. Overall, the MFF and project 3 are rated efficient as all subprojects, assessed under each of the individual projects achieved a higher economic internal rate of return (EIRR) on investment at completion against the economic opportunity cost of capital of 12% threshold, set at appraisal except one sewerage (in projects 1 and 3 combined), one water supply (in project 2), and one drainage package (in project 2). The overall EIRR for project 3, while not assessed at appraisal,

64 The SWM intervention did not expand in projects 2 and 3 except for collection equipment due to non-availability of

land. 65 The partial achievement was due to reduced scope for grade separator due to stronger and costlier material of bridge. 66 A 30 mld STP was dropped from project 2. 67 Project 1 was categorized as no gender elements.

14

was assessed at completion at 14.8%. The EIRR at completion of project 3 for the three water supply packages were assessed at 26.1%, 12.9% and 20.1% as compared to the appraisal estimates of 35.3%, 22.2%, and 15.7%, respectively.68 For the drainage package, the EIRR at completion were assessed at 15.4% as compared to the appraisal estimates of 16.5%.69 For the transport package including a bridge and a grade separator, the EIRR at completion was assessed at 17.0% as compared to the appraisal estimates of 26.0%. 70 For the delayed sewerage package, the EIRR at completion was assessed as 8.7% as compared to the appraisal estimates of 32.7%.71 For the multilevel parking facility package, the EIRR at completion was assessed at 13.2% as compared to the appraisal estimates of 15.4%.72 Except for the sewerage package, all packages’ EIRR are higher than the benchmark value of 12% at completion, justifying project investments. The EIRR of the sewerage package was below the threshold for economic viability at appraisal because of implementation delays. The overall EIRR for project 3, while not assessed at appraisal, was assessed at completion at 14.8%. The implementation delays (para. 23) were mostly attributed to frequent local unrest and the historic flood that are beyond project’s control.73 The low contractor performance also hindered the works progress especially in the sewerage subproject. However, the ERA had taken corrective action to replace the contractor and achieved 86% of physical progress at MFF completion. 74 The ADB financing share was reallocated up to the allowable 80% of the project cost, which was applied retroactively to maximize the project 3 outcome and reduce the financial burden on the state. Institutional efficiencies and grievance redress mechanisms developed by the ERA reduced transaction costs in process and time and improved transparency and accountability while significantly augmenting its administrative capacity. The MFF is rated efficient, with an overall EIRR of 15.8%. The EIRR of the sector subprojects under all the projects estimated at 21.6% for water supply; 14.5% for the sewerage, drainage, and solid waste management; and 14.8% for the urban transport. Details of the economic and financial analysis are in Appendix 12. D. Sustainability 43. Overall, the MFF and project 3 are rated likely sustainable. The Constitution of India mandates that the state allocate to ULBs the funds required to maintain their functions and sustain service delivery.75 Since the operating institutions did not achieve recovery of the O&M costs as envisaged at appraisal, the standard approach of financial internal rate of return at appraisal was not considered appropriate at completion of project 3. However, a financial sustainability analysis

68 Field missions to update the willingness-to-pay survey were not possible because of local unrest and travel

restrictions because of the coronavirus disease. For all three subprojects, projected benefits were realized. For one subproject, the EIRR at completion is higher than at appraisal because of reduced costs. For two out of three subprojects, there were implementation delay of 1–2 years.

69 For the drainage subproject, an additional 23,400 people benefitted because of increase in the length of drains constructed (42 km as compared to the 26 km envisaged at appraisal). Although there was an increase in beneficiaries, the EIRR at completion is slightly lower than at appraisal because of cost increases and implementation delay by 2 years.

70 For the transport subproject, the EIRR at completion is lower than at appraisal because of cost increase of reinforcing the bridge structure and an implementation delay of 2 years.

71 For the sewerage subproject, the EIRR at completion is lower than the EIRR at appraisal, mainly because of implementation delays of about 7 years.

72 The main reason for the EIRR at completion being lower than the appraisal EIRR is the reduced number of parking spaces for cars; there was no implementation delay. Against the original plan of 720 vehicles, the facility accommodates 352 vehicles, with targets for two-wheelers and other vehicles remaining the same.

73 For example, the contractor of transport subproject had to abandon the sites. Also, the security situation made it difficult to secure skilled engineers from other states to be deployed in the target towns.

74 The achieved sewerage beneficiaries were limited to 20% of the target. The reasons include the exclusion of the five divisional towns, that were originally planned as target towns for sewerage subproject, due to the security reason.

75 Article 243 X and Schedule XII.

15

of the operating institutions was carried out to evaluate the capacity to meet the O&M costs required to manage the project 3 assets. The PHED is responsible for O&M of water supply facilities, the Public Works Department (PWD) is responsible for flyovers, the HUDD is responsible for drainage and sewerage facilities, and ULBs are responsible for solid waste facilities and parking facilities. Their responsibilities include billing and fee collections of these services, but the revenue is remitted to the state government, which is responsible for financially managing these assets and services. For the ULBs, finances are structured through fiscal transfers from the state in the form of compensation grants and transfers from the Central Finance Commission and state finance commissions.76 As the project was not designed for capital cost recovery, the operating ratios of the state government were calculated to assess the sustainability.77 They averaged 0.94, meaning that the operating receipts are enough to meet the O&M expenses.78 Similar review of the overall finances of the PHED, PWD, HUDD, and the ULBs indicates their ability to meet the O&M cost of their assets through state budget allocations.79 The analysis assumed consistency in the timely transfer of the requisite O&M funds by the state government to the PHED, PWD, HUDD, and the ULBs, as provision of these urban services is a fundamental responsibility of the state government.80 The details of the financial re-evaluation are in Appendix 12. 44. Institutional capacities of the ULBs of the target towns and state bodies were strengthened under the MFF as part of the ongoing reforms. While the PHED, PWD, and HUDD have sufficient human resources and technical institutional capacities for O&M, the ULBs will continue augmenting human resources and institutional capacities for better asset management and governance.81 Gender mainstreaming elements supported by projects 2 and 3 proved effective in building the ERA’s capacity and establishing models to replicate gender equality and women’s empowerment in urban development. 45. The MFF, including project 3, is assessed to be environmentally sustainable as it contributes to water pollution abatement, and so reduces vector-borne diseases, thus improving quality of life and the urban environment. Social sustainability of the MFF, including project 3, is ensured by the improved access to continuous, reliable, and affordable basic urban services, thereby improving access to economic opportunities. E. Development Impact 46. The MFF is rated satisfactory, and project 3 is rated less than satisfactory in terms of development impact. Under project 3, impact achievements include the following: (i) 0.45 million people provided with access to water supply, (ii) 0.23 million people served with proper functioning drainage system, and (iii) 0.4 million people provided with access to reasonable-standard road facilities. Project 3 did not significantly contribute to the three impact indicators. In terms of the

76 The Central Finance Commission transfers accounts for about 30%–-40% of ULB finances, of which up to 90% may

be used for O&M of municipal assets. 77 The ratio of operating receipts to operating expenditures. The cost recovery calculation does not include asset

depreciation. 78 The state finance commission allocates a percentage of net proceeds of tax (about 7% of net state tax revenue) or