file 43304

TRANSCRIPT

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 1/76

ENERGY TRENDSDECEMBER 2007

A NATIONAL STATISTICS PUBLICATION

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 2/76

Contact points

To subscribe to Energy Trends and Quarterly Energy Prices

For new subscription queries please telephone:Amey on 01633 224712 or write to:

Amey, 7th Floor, Clarence House, Clarence Place, Newport South Wales NP19 7AA

A subscription form is also available on our Internet site

www.berr.gov.uk/energy/statistics/publications/trends/index.html

Energy Trends is prepared by the Energy Strategy and International Unit in BERR.

More information on BERR energy publications is available at:

www.berr.gov.uk/energy/statistics/publications/index.html

Further information on Oil and Gas is available at: www.og.berr.gov.uk/

For enquiries please contact: Telephone

Name 020 7215 E-mail

Publication and other general Clive Sarjantson 2698 [email protected]

(Helpdesk) enquiries on energy statistic

Total energy statistics Chris Michaels 2710 [email protected]

Coal and other solid fuels David Bovill 3839 [email protected]

Natural gas consumption

Gas and petroleum investment Suhail Siddiqui 5262 [email protected]

Indicative tariffs

Natural gas production Clive Evans 5189 [email protected]

Petroleum production

Petroleum consumption and stocks Lisa Vine 6072 [email protected]

Electricity statistics Joe Ewins 5190 [email protected]

Regional and local authority Jennifer Knight 6490 [email protected]

energy statistics

All the above can be contacted by fax on 020 7215 2723

This is a National Statistics publication

National Statistics are produced to high professional standards set out in the National Statistics Code

of Practice. They undergo regular quality assurance reviews to ensure that they meet customer needs.

They are produced free from any political interference.You can find a range of National Statistics on the Internet – www.statistics.gov.uk

Explanatory notes are to be found inside the back cover

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 3/76

December 20071

Contents

Introduction 2

Section 1 - Total Energy 3

Section 2 - Solid Fuels and Derived Gases 6

Section 3 - Oil and Oil Products 8

Section 4 - Gas 12

Section 5 - Electricity 14

Section 6 - Special FeaturesElectricity generation and supply figures for Scotland, Wales,Northern Ireland and England, 2005 and 2006

16

Regional and local electricity consumption statistics for 2006 21Regional and local gas consumption statistics for 2006 30Regional and local estimates of non gas, non electricity and non roadtransport fuels in 2005

38

Regional and local total energy consumption statistics for 2005 39The UK road transport biofuels market 45

Statistics of the installed capacity of solar photovoltaics 492008 Update of “Energy Consumption in the UK” 50The future of “Energy- Its impact on the Environment and Society” 51Recent and forthcoming publications of interest to users of energystatistics

52

Tables1.1: Indigenous production of primary fuels 531.2: Inland energy consumption: primary fuel input basis 541.3: Supply and use of fuels 55

2.1: Supply and consumption of coal 572.2: Supply and consumption of coke oven coke, coke breeze and other

manufactured solid fuels

58

2.3: Supply and consumption of coke oven gas, blast furnace gas,benzole and tars

59

3.1: Supply and use of crude oil, natural gas liquids and feedstocks 603.2: Supply and use of petroleum products 613.3: Supply and use of petroleum products - annual data 623.4: Supply and use of petroleum products - latest quarter 633.5: Demand for key petroleum products 643.6: Stocks of petroleum at end of period 653.7: Drilling activity on the UK Continental Shelf 66

4.1: Natural gas supply and consumption 67

5.1: Fuel used in electricity generation and electricity supplied 685.2: Supply and consumption of electricity 69

List of special feature articles published in Energy Trends between June2006 and September 2007

70

The cover illustration used for Energy Trends and other BERR energy statistics publications is from aphotograph by David Askew. It was a winning entry in the DTI News Photographic Competition in 2002.

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 4/76

December 2007 2

IntroductionEnergy Trends and Quarterly Energy Prices are produced by the Department for Business,Enterprise & Regulatory Reform on a quarterly basis. Both periodicals are published concurrentlyin June, September, December and March. The December editions cover the third quarter of thecurrent year.

Energy Trends includes information on energy as a whole and by individual fuels. The text and

charts provide an analysis of the data in the tables. The tables are mainly in commodity balanceformat, as used in BERR’s annual Digest of UK Energy Statistics. The 2007 edition of the Digestwas published on 26 July 2007. Printed and bound copies of the 2007 Digest can be obtainedfrom The Stationery Office and an electronic version is available on our web site atwww.berr.gov.uk/energy/statistics/publications/dukes/page39771.html . The balance format showsthe flow of a commodity from its sources of supply, through to its final use. The articles in EnergyTrends provide in-depth information on current issues within the energy sector.

The text and tables included in this publication represent a snapshot of the information available atthe time of publication. However, the data collection systems operated by BERR, which producethis information, are in constant operation. New data are continually received and revisions tohistoric data made. To ensure that those who use the statistics have access to the most up-to-date information, revised data will be made available as soon as possible, via the electronicversions of these tables. The electronic versions are available free of charge from the BERR website. In addition to quarterly tables, the main monthly tables that were published in the period up toMay 2001 when Energy Trends was produced monthly, continue to be updated and are alsoavailable on the BERR web site. Both sets of tables can be obtained fromwww.berr.gov.uk/energy/statistics/source/index.html

Energy Trends does not contain information on Foreign Trade, Temperatures and Prices. ForeignTrade and Temperatures tables are, however, available on the BERR web site and information onPrices can be found in the Quarterly Energy Prices publication. Prices information is also availableon our web site at www.berr.gov.uk/energy/statistics/publications/prices/tables/page18125.html

If you have any comments on Energy Trends or Quarterly Energy Prices publications please sendthem to:

Clive Sarjantson

BERR, Energy Strategy & International Unit,Bay 299, 1 Victoria StreetLondon SW1H 0ET Tel: 020 7215 2698E-mail: [email protected] Fax: 020 7215 2723

The main points for the third quarter of 2007:

• Total energy production was 3½ per cent lower than in the third quarter of 2006.

• Oil production remained virtually unchanged when compared with the third quarter of 2006. Productionfrom older established fields continued to decline but this decline was offset by eight new fields, includingthe very large Buzzard field.

• Gas production was 11 per cent lower than the third quarter of 2006. Gas imports increased by 31½ per cent and gas exports decreased by 25 per cent. The UK was a net importer of gas in the third quarter of

2007, whereas the UK was a net exporter in the same period of 2006. Gas demand was 5 per centhigher than the third quarter of 2006.

• Total primary energy consumption for energy uses was 1½ per cent higher than during the third quarter of 2006, this is equivalent to a 2 per cent decrease when adjusted to take account of weather differencesbetween the third quarters of 2006 and 2007.

• Coal production in the third quarter of 2007 was 27 per cent higher than the third quarter of 2006. Coalimports were 22½ per cent lower and generators’ demand for coal was down by 2½ per cent.

• Gas supplied 1½ per cent more electricity than in the third quarter of 2006 while coal supplied 5 per centless and nuclear 9 per cent less. Net imports of electricity were 64 per cent higher.

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 5/76

Total Energy

December 20073

Section 1 - Total Energy

Chart 1.1 Production of indigenousprimary fuels

0

10

20

30

40

50

60

70

80

90

C oa l Pet ro leum N atural Gas P rim ary

Electric ity(1)

M i l l i o n t o n n e s o f o i l e q u i v a l e

n t

2006 Total

2006 Q1-Q32007 Q1-Q3

(1) Nuclear and natural flow hydro electricity.

Chart 1.2 Total inland consumption(primary fuel input basis)(1)

(1) Seasonally adjusted and temperature corrected annual rates.

• Total production in the third quarter of 2007 was41.0 million tonnes of oil equivalent, 3.6 per centlower than in third quarter of 2006.

• Production of natural gas fell by 10.9 per cent

between the third quarter of 2006 and the thirdquarter of 2007; gas production is declining asNorth Sea reserves deplete.

• Production of petroleum was 0.2 per cent lower inthe third quarter of 2007 than in the third quarter ayear earlier.

• Primary electricity output was 6.8 per cent lower,within which nuclear electricity output was 8.8 per cent lower but output from wind and natural flowhydro increased by 49.3 per cent.

• In the third quarter of 2007 production of coal andother solid fuels was 22.0 per cent higher than inthe third quarter of 2006.

• Total inland consumption on a primary fuel inputbasis was 230.7 million tonnes of oil equivalent inthird quarter of 2007 (temperature corrected,seasonally adjusted annualised rate). Theaverage temperature during the third quarter of 2007 was 14.9 degrees Celsius, 2.4 degreesCelsius cooler than the third quarter of 2006.

• Total seasonally adjusted and temperaturecorrected consumption in the third quarter of 2007was 2.1 per cent lower than the same period ayear earlier.

• Between the third quarter of 2006 and the thirdquarter of 2007 (on a seasonally adjusted andtemperature corrected basis) coal and other solidfuel consumption fell by 6.6 per cent .

• Also on a seasonally adjusted and temperaturecorrected basis, oil consumption fell by 0.4 per cent.

• On the same basis, gas consumption fell by 0.7

per cent.

215

220

225

230

235

240

245

250

255

Q1 Q2 Q3 Q4

M i l l i o n t o n n e s o f o i l e q u

i v a l e n t

2005

0

2004

2006

2007

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 6/76

Total Energy

December 2007 4

Chart 1.3 Final energy consumptionby user

0

5

10

15

20

25

30

35

40

45

50

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

M i l l i o n t o n n e s o f o i l e q

u i v a l e n t

Transport

Domestic

Industry

Services

2004 2005 2006 2007

Background

Relevant tables1.1: Indigenous production of primary fuels…………………………………………………….. Page 531.2: Inland energy consumption: primary fuel input basis………………………………………. Page 541.3: Supply and use of fuels………………………………………………………………….. Pages 55-56

Production

Indigenous production of energy was 9.1 per cent lower in 2006 than in 2005, continuing a year onyear decline for each year since 1999. Coal and other solid fuel production was lower by 9.6 per cent, gas production fell by 9.1 per cent and petroleum production by fell 9.6 per cent.Indigenous production continued to fall in 2007, with total production in each quarter of 2007 todate being lower than the same quarter in 2006. Petroleum accounted for 46.1 per cent of total

indigenous production in the third quarter of 2007 while coal and other solid fuels accounted for 8.1per cent, and natural gas 35.8 per cent. A year earlier the proportions were petroleum 44.5 per cent, coal and other solid fuels 6.4 per cent and natural gas 38.8 per cent.

Total inland consumption

In 2006 consumption of primary fuels was 1.1 per cent lower than in 2005. The largest contributionto this decrease in absolute terms was from natural gas (which decreased by 5.0 per cent). On atemperature corrected basis consumption in 2006 was 1.5 per cent lower than in 2005.

Total inland energy consumption, on a primary fuel input basis (not temperature corrected or seasonally adjusted), decreased by 8.8 per cent in the first quarter of 2007 compared with thesame period in 2006; this was followed by a 3.4 per cent reduction in the second quarter. In thethird quarter of 2007 consumption was 48.4 million tonnes of oil equivalent, which is 1.6 per cent

higher than in the corresponding period a year ago.

Consumption by final users

Final energy consumption shows a strong seasonal pattern with more energy being consumed inthe winter months and less in the summer months, particularly in the domestic and service sectors.

In the third quarter of 2007 the transport sector was responsible for the largest share of finalconsumption at 45 per cent of all energy consumed by final users. The industrial sector wasresponsible for a further 21 per cent, the domestic sector for another 17 per cent and the serviceindustries, including agriculture, consumed 11 per cent. The remaining 7 per cent was made up byfuel use for non-energy purposes.

• Total final energy consumption increased by 2.0per cent between the third quarter of 2006 and thethird quarter in 2007.

• Service sector energy consumption increased by6.2 per cent

• Domestic sector energy consumption increased by13.3 per cent.

• Transport energy consumption decreased by 1.6per cent.

• Industrial energy consumption increased by 7.4 per cent

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 7/76

Total Energy

December 20075

Final energy consumption rose by 2.0 per cent between the third quarter of 2006 and the thirdquarter of 2007, mainly due to increases in the domestic sector (a 13.3 per cent rise), the industrialsector (a 7.4 per cent rise) and the service sector (a 6.2 per cent rise). There was a decrease inthe transport sector of 1.6 per cent.

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 8/76

Solid Fuels and Derived Gases

December 2007 6

Section 2 - Solid Fuels and Derived Gases

Chart 2.1 Coal production and imports

0

2

4

6

8

10

12

14

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

M i l l i o n t o n n e s

Coal imports

Opencast coalDeep mined coal

20052004 2006 2007

• Provisional figures for the third quarter of 2007show that coal production (including an estimate

for slurry) was 26.8 per cent higher than the thirdquarter of 2006 at 4.6 million tonnes, with deepmined production up 35.3 per cent and opencastproduction up 20.4 per cent. These percentageincreases are high because production wasparticularly low in the third quarter of 2006 due tomine closures, geological difficulties and other one-off factors. The percentage increase from thesecond quarter of 2007 was not as high, with totalcoal production rising by only 4.3 per cent.

• Imports of coal in the third quarter of 2007 were22.7 per cent lower than in the third quarter of 2006 at 9.7 million tonnes.

• 79 per cent of the coal imported in the third quarter

of 2007 (7.7 million tonnes) was steam coal,largely for the power stations market.

Chart 2.2 Coal consumption

0

4

8

12

16

20

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

M i l l i o n t o n n e s

Electricity generators

Generators trend (=average of 4 quarters ending)

Collieries, coke ovens and other conversion industries

Final consumers

20052004 2006 2007

• Demand for coal in the third quarter of 2007, at13.1 million tonnes, was 1.9 per cent lower than inthe third quarter of 2006. Consumption byelectricity generators was down by 2.6 per cent to10.6 million tonnes.

• Electricity generators accounted for 81 per cent of total coal use in the third quarter of 2007, the sameproportion as a year earlier.

• Provisionally, final consumption (as measured bydisposals to final consumers) increased by 6.0 per cent in the third quarter of 2007 compared with ayear earlier, with consumption by the domesticsector increasing by 77 per cent and industrialconsumption falling by 17.5 per cent. Note that for 2007 there has been a change of methodology in

terms of the proportional allocation of coal fromtraders and this is the reason for the large increasein domestic sector consumption.

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 9/76

Solid Fuels and Derived Gases

December 20077

Chart 2.3 Coal stocks

0

2

4

6

8

10

12

14

16

18

20

J a n

A p r

J u l

O c t

J a n

A p r

J u l

O c t

J a n

A p r

J u l

O c t

J a n

A p r

J u l

O c t

M i l l i o n t o n n e s

UndistributedOther distributedPow er stations

20052004 2006 2007

• Coal stocks at the end of the third quarter of 2007were 0.8 million tonnes (4.4 per cent) higher thanat the end of the third quarter of 2006 and stood at18.7 million tonnes. Provisionally, by the end of October 2007 coal stocks had fallen back to 18.1million tonnes.

• The level of coal stocks at power stations were 0.5million tonnes higher than at the end of the thirdquarter of 2006 at 15.7 million tonnes, an increaseof 3.4 per cent.

• Stocks held by producers (undistributed stocks) inthe third quarter of 2007 were 0.8 million tonnes(8.4 per cent) lower than at the end of the thirdquarter of 2006.

Background

Relevant tables2.1: Supply and consumption of coal………………………………………………………………Page 572.2: Supply and consumption of coke oven coke, coke breeze

and other manufactured solid fuels………………………………………………………….. Page 582.3: Supply and consumption of coke oven gas, blast furnace gas, benzole and tars……….Page 59

Coal production and importsIn 2006 indigenous production of coal fell by 2.0 million tonnes. Deep mined production fell to arecord low of 9.4 million tonnes, while opencast coal production was at its lowest level since 1970,and 17.3 per cent lower than in 2005. In 2005, for the first time ever, opencast productionexceeded deep mined production. Deep mined production recovered towards the end of 2005 and

in the first half of 2006. However, it fell back in the second half of 2006 with the closure of Rossington at the end of March 2006 and the run down in production and eventual mothballing of Harworth in September 2006. These closures, geological difficulties and other one-off factorscontinued to suppress deep mined production in the first quarter of 2007, but in the second andthird quarters of 2007 deep mined production increased again. Opencast production has alsobeen on an upward trend since the third quarter of 2006 and remains higher than deep minedoutput. Coal imports have reached record levels in each of the last three years, but with demandfor coal lower in the first three quarters of 2007, coal import levels peaked at the end of 2006.

Coal consumptionIn 2005 coal use by electricity generators was 1.6 million tonnes higher than in 2004 as higher gasprices made coal more competitive for generation. This trend continued into 2006 with the demandfrom electricity generators up 5.3 million tonnes on 2005. With gas prices becoming morecompetitive in the first half of 2007, the trend has reversed and coal consumption by electricitygenerators in the third quarter of 2007 was down by 2.6 per cent compared with the third quarter of 2006. The use of coal for coke making and at blast furnaces increased by 6.8 per cent (nearly 0.5million tonnes) in 2006. This upward trend appears to have continued in 2007.

StocksEnd of winter stock levels have risen over the past two years from the low levels of 2004/05. Theseasonal rise in stocks over the summer periods of 2005 and 2006 was strong, boosted by recordlevels of coal imports over the period. The rise was less strong in summer 2007 and coal stockspeaked at the same level (18.7 million tonnes) as in October 2006.

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 10/76

Oil and Oil Products

December 2007 8

Section 3 - Oil and Oil Products

Chart 3.1 Production of crude oil andNGLs

Chart 3.2 UK trade in crude oils, NGLs

and petroleum products

• Total indigenous UK production of crude oil andNGLs in the third quarter of 2007 was virtuallyunchanged when compared with a year earlier.

• In the nine months to September 2007 eight newfields started production. This includes the verylarge Buzzard field. During this period these fieldsproduced 6.9 million tonnes of crude oil. Withoutthese new fields production in the third quarter of 2007 would have been 18.8 per cent lower than ayear ago.

• During the third quarter of 2007 the UK was a netimporter of oil and oil products by 2.0 milliontonnes, similar to the third quarter of 2006 whereby the UK was a net importer by 2.8 milliontonnes.

• The UK was a net importer of crude oil, NGLs andfeedstocks in the third quarter of 2007 (by 3.8million tonnes). Both imports and exportsincreased, by 4.8 and 9.0 per cent respectively.

• In the third quarter of 2007 the UK was a netexporter of petroleum products (by 1.8 million

tonnes).

• Both imports and exports of petroleum productsfell during the third quarter of 2007, by 13.5 and5.3 per cent respectively.

4

5

6

7

8

9

J a n

F e b

M a r

A p r

M a y

J u n

J u l

A u g

S e p

O c t

N o v

D e c

T o t a

l o i l p r o d u c t i o n ( m i l l i o n t o n n e s )

0

2004

2005

2006

2007

-30

-20

-10

0

10

20

30

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

M i l l i o n t o n n e s

Exports Imports Net Exports

20072004 2005 2006

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 11/76

Oil and Oil Products

December 20079

Chart 3.3 Demand for key transportfuels

Chart 3.4 Super/hypermarket shares of

retail deliveries

• Total deliveries of transport fuels were virtuallyunchanged in the third quarter of 2007 whencompared with the third quarter of 2006.

• Motor spirit deliveries fell by 5.5 per cent.

• Deliveries of Diesel engined road vehicle fuel(DERV) increased by 7.8 per cent.

• DERV fuel’s share of road transport fuels in thethird quarter of 2007 was 55.5 per cent comparedto 52.2 per cent in the third quarter of 2006.

• Deliveries of aviation turbine fuel were 4.1 per cent lower.

• Sales of motor spirit by super/hypermarketcompanies accounted for 42.9 per cent of retailsales of petrol in the third quarter of 2007, up from40.9 per cent in the third quarter of 2006.

• Sales of DERV by super/hypermarket companiesaccounted for 37.0 per cent of retail sales of DERV in the third quarter of 2007, compared with34.1 per cent in the third quarter of 2006.

0

1

2

3

4

5

6

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 D e l i v e r i e s i n t o c o n s u m p t i o n ( m i l l i o n t o n n e s )

2007

Aviation turbine fuel

DERV fuel

Unleaded motor spirit

20052004 2006

DERV fuel

0

1

2

3

4

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

M i l l i o n t o n n e

s

Super/hypermarkets

Other retailers

20052004 2006 2007

Petrol

0

1

2

3

4

5

6

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Other retailers

Super/hypermarkets

20052004 2006 2007

M i l l i o n t o n n e s

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 12/76

Oil and Oil Products

December 2007 10

Chart 3.5 Stocks of key oil products(1)

(1) This includes motor spirit, DERV fuel, other gasdiesel oils, aviation turbine fuel, kerosene and fuel oils.

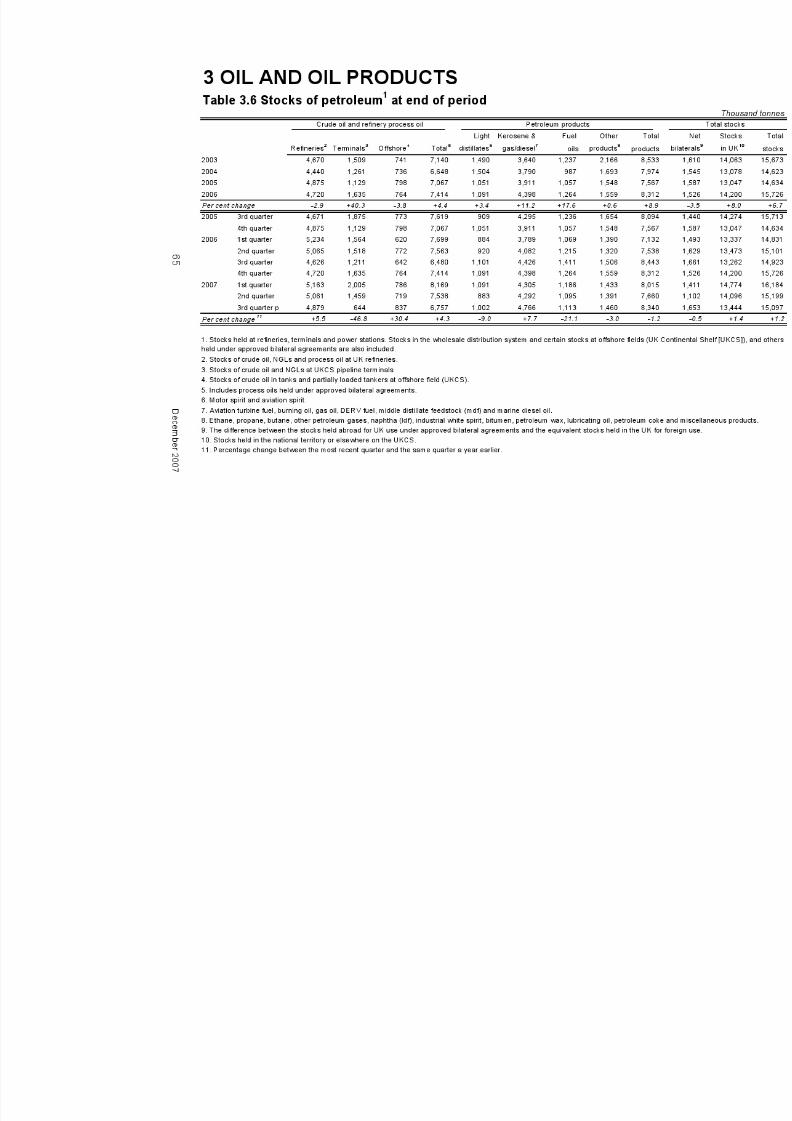

• Overall, stocks of crude oil and petroleum productswere 1.2 per cent higher at the end of the thirdquarter of 2007 than a year earlier.

• Crude oil and refinery process oil stocks were 4.3per cent higher, and stocks of products were 1.2per cent lower.

• Stocks at UKCS pipeline terminals fell by 47 per cent (half a million tonnes) in the third quarter of 2007. However, crude and process oil stockselsewhere increased by 0.8 million tonnes givingan overall increase of 0.3 million tonnes in the thirdquarter of 2007.

• Chart 3.5 combines stocks of products with theproduct equivalent of stocks of crude oil to give anoverall level of UK stocks of key products.

• At the end of the third quarter of 2007, the UK heldstocks equal to 75½ days of consumption of thesekey products, compared with an obligation of 67½

days (see Background for more details).

Chart 3.6 Drilling activity on the UKCS

0

20

40

60

80

100

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

N u m b e r o f w e l l s

Exploration & Appraisal (Offshore)Development (Off shore)

Exploration & Appraisal (Onshore)Development (Onshore)

20062004 20072005

• Drilling figures for the third quarter of 2007 showeda rise in the number of exploration and appraisalwells started offshore to 39 against 22 in thecorresponding quarter of 2006.

• The number of development wells drilled offshorefell to 35, compared with 53 in the correspondingquarter of 2006.

• 7 development wells were drilled onshore in thethird quarter of 2007, compared with 3 in thecorresponding quarter a year earlier.

• 3 exploration or appraisal wells were startedonshore in the third quarter of 2007. The samenumber of exploration or appraisals wells wasstarted onshore in third quarter of 2006.

Background

Relevant tables3.1: Supply and use of crude oil, natural gas liquids and feedstocks…………………………. Page 603.2: Supply and use of petroleum products………………………………………………………. Page 613.3: Supply and use of petroleum products - annual data……………………………………… Page 623.4: Supply and use of petroleum products - latest quarter……………………………………..Page 633.5: Demand for key petroleum products………………………………………………………….Page 643.6: Stocks of petroleum at end of period………………………………………………………… Page 653.7: Drilling activity on the UK Continental Shelf………………………………………………… Page 66

0

2

4

6

8

10

12

14

16

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

M i l l i o n t o n n e s

Oil Stocks Obligation

200720052004 2006

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 13/76

Oil and Oil Products

December 200711

Crude oil production and tradeTotal UK production of crude oil and NGLs was virtually unchanged in the third quarter of 2007when compared to the same period last year. In the nine months to September 2007, eight newfields started production, including the very large Buzzard field. The UK was a net importer of oiland oil products in the third quarter of 2007. Imports and exports of crude oil and NGLs both rose,meaning the UK remained a net importer of crude and NGLs. Both imports and exports of petroleum products fell, (by 13.5 and 5.3 per cent respectively), but exports decreased at a slower rate leading to the UK being a net exporter of petroleum products. The majority of UK production of

crude oil and NGLs is exported, as indigenous UK crude oil tends to be the more valuablelight/sweet type with lower sulphur levels and the relative modernity of UK refineries allows their use of less valuable or lower grade crude oil. Therefore the economics of crude oil markets resultsin significant volumes of crude oil being imported into the UK.

Refinery production of petroleum products and trade The net refinery output in the third quarter of 2007 was 21.7 million tonnes, 0.5 million tonnes (2.2per cent) lower than the third quarter of 2006.

Demand for petroleum productsOverall demand for petroleum products in the third quarter of 2007 was 1.2 per cent lower than inthe third quarter of 2006. Deliveries of motor spirit were lower by 5.5 per cent, however, DERVdeliveries increased by 7.8 per cent to 5.5 million tonnes. Deliveries of aviation turbine fuel fell by

4.1 per cent.

Stocks of crude oil and petroleum productsThe UK has an obligation under EU law to maintain stocks of key oil products at or above a certainlevel to ensure adequate supplies would exist for any international oil supply emergency. Theseobligations are based on the UK's annual consumption of the key products motor spirit, DERV fueland other gas diesel oils, aviation fuel and other kerosenes and fuel oils. These obligations areusually updated every 1st July as consumption data for the previous year are finalised. Chart 3.5above combines data on stocks of key oil products with the product equivalent of stocks of crude oilto give an overall level of UK stocks of key oil products to show how the UK is complying with theseobligations at an overall level. The UK's current overall obligation, based on 2006 consumptiondata, is to hold a total of 11 million tonnes of these products, equal to 67½ days of consumption.

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 14/76

Gas

December 2007 12

Section 4 – Gas

Chart 4.1 Production of natural gas

40

50

60

70

80

90

100

110

120

J a n

F e b

M a r

A p r

M a y

J u n

J u l

A u g

S e p

O c t

N o v

D e c

P r o d u c t i o n ( T W h )

0

2006

2004

2005

0

2007

Chart 4.2 UK trade in natural gas

• Total indigenous UK production of natural gas inthe third quarter of 2007 was 11.2 per cent lower than in the corresponding quarter a year earlier.

• Two new import pipelines were commissioned inthe fourth quarter of 2006.

• In the third quarter of 2007, compared with thesame period of 2006, exports of natural gas fell by25.0 per cent and imports rose by 31.3 per cent.

• The UK was a net importer of gas in the thirdquarter of 2007 by 21.0 TWh, whereas in the thirdquarter of 2006 the UK was a net exporter.

-130

-120

-110

-100

-90

-80

-70

-60

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2004 2005 2006 2007

T r a d e ( T W h )

Exports Impor ts Net Expor ts

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 15/76

Gas

December 200713

Chart 4.3 Natural gas consumption -average of four quarter ending

0

10

20

30

40

50

60

70

80

90

100

110

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

T W h

Iron and steelHeat sold Other final

users

Other

industries

Electricity

generators

Domestic

2004 20062005 2007 Background

Relevant table4.1: Natural gas supply and consumption………………………………………………………... Page 67

Gas production and tradeIn the third quarter of 2007, gas production was 11.2 per cent lower than a year ago. The UK was anet importer of gas in the third quarter of 2007 whereas the UK was a net exporter in the sameperiod of 2006. Imports of gas were 31.3 per cent higher than a year ago and exports were 25.0per cent lower.

The UK currently exports gas to the Netherlands from the Markham, Windermere, Grove andMinke fields, to the Irish Republic via the two Irish – UK gas interconnectors and to Belgiumthrough the Bacton-Zeebrugge interconnector. Imports to the UK are from Belgium, via theinterconnector, Norway, via the Langeled and Vesterled pipelines, and the Tampen Link (fromStatfjord to FLAGS), and Algeria, Egypt, Qatar and Trinidad (liquefied natural gas). In the thirdquarter of 2007, Norwegian gas accounted for 76 per cent of UK natural gas imports, compared to80 per cent a year ago.

Gas consumptionUntil the middle of 2000 the growth in consumption of natural gas was dominated by growth inconsumption for electricity generation, mainly in Combined Cycle Gas Turbine stations. However,high gas prices led to the use of gas for generation levelling off after 2000, rising slightly in some

years and falling back in others. While much of this switchback pattern is the result of the relativeprices of gas and coal, the 2004 growth can also be attributed to the three newest CCGT stationsoperating at high levels throughout the year, while the downturn in 2005 results from generatorspreferring coal when prices reached very high levels at the end of the year. This continued intoearly 2006. However gas use in the fourth quarter of 2006 rose back to the levels of 2003 and2004 as prices fell back. Gas use in the domestic sector is particularly dependent on temperaturesnot only during the heating season, but also in summer, when the weather can affect the amount of gas used for water heating and cooking. Temperatures in the third quarter of 2007 weresignificantly lower than a year earlier, boosting domestic consumption of gas by about 15 per centon the low levels of the third quarter of 2006.

• Demand for gas in the third quarter of 2007 was5.0 per cent higher than the level in the thirdquarter of 2006.

• Gas use for electricity generation was 0.9 per centhigher than in the third quarter of 2006.

• Provisionally, consumption in the domestic sector rose by 15.2 per cent from the low levels of a year earlier.

• In public administration, commerce and agricultureconsumption rose by 14.5 per cent compared witha year earlier. In the industrial sector gas saleswere provisionally 17.1 per cent higher than in thethird quarter of 2006.

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 16/76

Electricity

December 2007 14

Section 5 - Electricity

Chart 5.1 Fuel used for electricitygeneration

0

2

4

6

8

10

12

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

M i l l i o n t o n n e s o f o i l e q u i v a l e n t

200620052004

Coal

Gas

Nuclear

Net imports

2007

Oil, renewable and other

• Fuel used by generators in the third quarter of 2007 was, in total, 1.4 per cent lower than in the

third quarter of 2006.

• Gas use was 1.1 per cent up on the third quarter of 2006.

• Coal use in the quarter was 2.6 per cent lower thana year earlier and nuclear sources were 8.8 per cent lower.

• Hydro sources were up by 51.3 per cent on thethird quarter of 2006, due to higher rainfall andsnowfall over the winter period. Oil use fell by 6.0per cent.

Chart 5.2 Electricity supplied

• Total electricity supplied by all generators in thethird quarter of 2007 was 0.1 per cent lower (-0.1

TWh) than a year earlier.

• Indigenous supply was also 0.1 per cent lower thanin quarter 3 2006 while net imports were 64.2 per cent (+ 1.0 TWh) higher than a year earlier.

• The supply from coal fell by 4.8 per cent (-1.3TWh), while from gas fired stations supply rose by1.6 per cent (+0.6 TWh).

• The supply from nuclear stations fell by 8.8 per cent (-1.5 TWh).

• Between the third quarter of 2006 and the thirdquarter of 2007 coal’s share of electricity suppliedfell by 1.5 percentage points and nuclear’s sharefell by 1.7 percentage points while gas’s share rose

by 0.7 percentage points. The share of oil,renewables and other fuels rose by 1.3 percentagepoints.

Q3 2006Nuclear

19.9%

Oil,renew ables

and other

5.9%

Coal

31.3%

Gas

41.1%

Net imports

1.9%

Q3 2007 Nuclear

18.2%

Coal

29.8%

Gas

41.8%

Net imports

3.1%

Oil,

renewablesand other

7.2%

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 17/76

Electricity

December 200715

Chart 5.3 Electricity consumption

0

10

20

30

40

50

60

70

80

90

100

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

T W

h

2004 200720062005

Commercial and Other

Domestic

Industrial

• Final consumption of electricity fell by 1.1 per cent inthe third quarter of 2007.

• Consumption by the domestic sector rose by 1.1 per cent while industrial consumption of electricity fell by

1.3 per cent. Consumption by other final users(including transport sector use) fell by 2.7 per cent.

• In this period temperatures were on average about2½ degrees lower than in the third quarter of 2006.

Background

Relevant tables5.1: Fuel used in electricity generation and electricity supplied……………………………….. Page 685.2: Supply and consumption of electricity……………………………………………………….. Page 69

Fuel useCoal prices rose in 2004, so gas use became more attractive for generation and increased to anew record level, 3 per cent higher than 2002’s previous record. Conversely, rising gas prices over the later part of 2005 led to a preference for coal as the main fuel source for electricity generation.Generators used much more coal during 2006 as a whole, because a further rise in gas pricesmade coal fired generation more competitive. However, gas prices fell in the first quarter of 2007and continued to fall during the second and third quarters, reversing the trend with coal use fallingby 15 per cent and gas use rising 20 per cent compared with the first three quarters of 2006. Additionally, two of the oldest nuclear stations closed at the end of December 2006 and increased

coal and gas fired generation replaced these stations’ contribution.

SupplyTotal electricity supplied in the UK in 2006 was ½ per cent lower than in 2005, whereas theaverage rate of growth over the previous 5 years had been +½ per cent per year. Supply from thecoal fired power stations of all generating companies rose by 11 per cent in 2006, with electricitysupplied from gas falling 7½ per cent to be 10 per cent below 2004’s record level. Supply fromnuclear sources fell by 8 per cent in 2006 although the nuclear sector was again affected by a highlevel of outages for repairs and maintenance. Imports and exports of electricity from and tocontinental Europe are volatile with suppliers taking advantage of price differentials that havearisen during periods of extreme weather or industrial disputes. Despite a high level of electricityimports in the third quarter of 2007, imports in the first 9 months of the year were 21 per cent lower than in the corresponding period of 2006.

ConsumptionAfter the near absence of growth in 2002, electricity demand by final consumers grew by 1¼ per cent in 2003 but only by ¾ per cent in 2004 (although this rises to just above the 1½ per cent per year trend rate of growth when allowance is made for the change to reporting on a calendar year basis in 2004). In 2005, growth in electricity demand was closer to 2 per cent, the highestpercentage rise since 2000. In 2006 final consumption of electricity fell by ½ per cent, the first fallsince 1994. Consumption in 2006 was divided 29 per cent to the domestic, 28½ per cent toindustry and 27 per cent to commerce, public administration, transport and agriculture. Fuelindustries accounted for a further 8 per cent with the remaining 7½ per cent accounted for bytransmission and distribution losses.

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 18/76

Special feature – Sub national electricity figures

December 2007 16

Electricity generation and supply figures for Scotland, Wales, NorthernIreland and England, 2005 and 2006.

IntroductionThis article updates that published in December 2006. As before, there are confidentialityconstraints that mean that some data for generation by fuel in Northern Ireland cannot be shownseparately from those for England. The United Kingdom figures shown in the tables in this articleare taken from the Digest of United Kingdom Energy Statistics (DUKES) 2007, Chapter 5 and 7and so the definitions used are identical to those in the Digest. Tables 1 and 2 are shown in“landscape” format at the end of the main text.

Generation and net exportsIn 2005 12.4 per cent of the electricity generated in the UK was generated in Scotland, 8.7 per centin Wales, 2.4 per cent in Northern Ireland and 76.5 per cent in England. These percentages rosein 2006 to 13.5 per cent, 8.8 per cent and 2.6 per cent respectively in Scotland, Wales andNorthern Ireland, but fell in England to 75.2 per cent (Table 1).

Both Scotland and Wales are net exporters of electricity with England importing electricity fromboth countries and from continental Europe. Northern Ireland trades electricity with the Republic of Ireland to which it is a net exporter. It also imports electricity from Scotland via the Moyle

interconnector opened in 2002 but these imports are less than the net exports to the Irish Republic.In 2005 Scotland exported 14.9 per cent of the electricity generated there to consumers elsewherein the UK, but this rose to 20.4 per cent in 2006. The increase in generation in Scotland betweenthese two years was broadly equivalent to the increase in exports to England. Wales exported theequivalent of 13.0 per cent of its generation to consumers in England in 2005, falling back to 11.1per cent in 2006.

Generation by fuelTable 2 sets out the generation of electricity by the fuel categories used in Table 5.6 of the Digestof UK Energy Statistics 2007. The position in 2006 is shown in Chart 1. Unplanned outages atnuclear stations in Scotland and Wales saw reductions in output and hence nuclear’s share of generation from 38 per cent to 26 per cent in Scotland and from 23 to 20 per cent in Wales. The

Chart 1: Generation by fuel in 2006 by major power producers and other generators

0

50,000

100,000

150,000

200,000

250,000

300,000

England Scotland Wales Northern Ireland

G W h

Generators other than MPPs

Oil and renewables

Nuclear

Coal

Gas

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 19/76

Special feature – Sub national electricity figures

December 200717

high price of gas in 2006 meant that gas’ share of generation in England and Wales was lower than in 2005, but in Scotland the share increased because of the large reduction in nuclear’s shareof Scottish generation. In Northern Ireland gas accounted for around two thirds of generation. Correspondingly coal’s share rose in all countries compared with 2005. In Scotland coal’s share of generation was 33 per cent, up from 25 per cent. In Wales 26 per cent of generation in 2006 wasfrom coal (up from 19½ per cent) while in England the increase was from a 37 per cent share to a40 per cent share. In Northern Ireland the share of coal in generation increased by 1 percentage

point. The role of renewables is discussed in a separate section below. Combined heat andpower (CHP) forms the bulk of “Other generators” generation, although some major power producers (MPPs) also operate generators that are partially CHP. CHP statistics for 2006 on asub-national and regional basis were published in the September 2007 issue of Energy Trends.The share of generation accounted for by generators other than major power producers variesacross the UK. In Scotland in 2006 other generators had a 15 per cent share, while in England theshare was 8½ per cent, in Wales 8 per cent and in Northern Ireland 4½ per cent.

Chart 2: Electricity consumption in 2006

Wales

6.7%

Scotland

10.1%

NorthernIreland

2.4%

England

80.8%

Consumption and salesTransmission and distribution losses are notseparately available for Scotland, Wales,Northern Ireland and England so estimates

have been made using the same proportionsof electricity supplied as for the UK as awhole. Consumption figures have then beencalculated by deducting net transfers andlosses figures from the electricity suppliedfigures shown in Table 1. These show(Chart 2) that in 2006 10.1 per cent of electricity consumption in the UK was inScotland, 6.7 per cent in Wales, 2.4 per centin Northern Ireland and 80.8 per cent inEngland, all little changed from thepercentage shares in 2005.

Since 2001 separate data have beencollected for sales of electricity from thepublic supply system in Scotland, Englandand Wales, and Northern Ireland andpublished as monthly Table 5.5 on theBERR Energy Statistics web site (seereferences at the end of the article).

Because of definitional and other differences set out in the Technical Notes to Chapter 5 of theDigest of UK Energy Statistics 2007, there is a statistical difference between the calculatedconsumption and the sales data in Table 1. As part of its commitment to improving the quality of its statistics, BERR continues to examine this statistical difference and look further at thecomponent series to see where the differences might be arising and thus where improvements tothe data might be made. Statistical differences reported in Table 1 are lower than reported in last

year’s corresponding table.

RenewablesThe share of renewables in electricity generation or sales is measured in two different ways in theUK1. First there is the “headline” overall measure that shows the percentage of electricitygeneration accounted for by all renewables. Secondly there is the measure that is based on theRenewables Obligation (RO) (and the analogous Renewables Obligation (Scotland) - ROS) whichshows the percentage of electricity sales accounted for by renewables eligible under these

1There is also a third method used by the EU – a Renewables Directive basis – see Chapter 7 of the Digest of UK

Energy Statistics 2007, paragraph 7.8.

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 20/76

Special feature – Sub national electricity figures

December 2007 18

obligations. The main differences are the exclusion from the RO of large-scale hydro and non-biodegradable wastes2. Table 3 shows the overall measure for 2004, 2005 and 2006.

Table 3: Renewables percentagesUK Scotland Wales Northern Ireland England

2004 3.58 11.56 2.96 2.03 2.352005 4.23 13.13 3.56 2.87 2.92

Overallrenewablespercentage 2006 4.55 12.99 4.04 3.42 3.14

Scotland’s and Wales’ hydro outputs in 2003 and 2006 were affected by the dryer weather thatcaused a 34.5 per cent reduction in UK hydro generation in 2003 compared with 2002 and a 6.4per cent reduction in 2006 compared with 2005.

Under the headline measure, the high proportion of natural flow hydro in Scotland took the 2005renewables percentage to 13.13, but it fell back to 12.99 in 2006. This share is very much higher than other parts of the UK can produce. On a RO basis, the percentage measure for the UK (2.21per cent in 2003, 3.06 per cent in 2004, 3.99 per cent in 2005, and 4.15 per cent in 2006) is notmeaningful at sub-national level because electricity generated in one part of the UK can be sold ina different part of the UK. However, in Scotland the renewables target (which is to reach 31 per cent by 2011 and 50 per cent by 2050) is expressed as generation as a proportion of grosselectricity consumption (defined as generation plus transfers into Scotland less transfers out of

Scotland). In 2004 this percentage was 13.9 rising to 15.4 in 2005 and 16.3 in 20063. The amountof electricity from renewable sources transferred from Scotland or Wales to England, or fromScotland to Northern Ireland is not known. What is known from Table 2 is that the amount of ROSeligible electricity generated in Scotland in 2006 was 16½ per cent greater than in 2005 and theamount of RO eligible electricity generated in Wales in 2006 was 23 per cent more than in 2005. In England the increase was 7½ per cent and in Northern Ireland 26 per cent. In the UK as awhole RO eligible electricity production increased by 11 per cent. Renewables statistics for 2006on a sub-national and regional basis were published in the September 2007 issue of EnergyTrends.

Mike JanesEnergy Statistics and AnalysisTel: 020 7215 5186

Fax: 020 7215 2723E-mail: [email protected]

References:Digest of UK Energy Statistics 2007. Published for BERR by The Stationery Office £40.00, but also availableon the BERR web site at: www.berr.gov.uk/energy/statistics/publications/dukes/page39771.htmlEnergy Trends monthly Table 5.5: www.berr.gov.uk/energy/statistics/source/electricity/page18527.html “Combined Heat and Power in Scotland, Wales, Northern Ireland and the regions of England in 2006” –Energy Trends September 2007, page 26: www.berr.gov.uk/files/file41460.pdf “Renewable energy in Scotland, Wales, Northern Ireland and the regions of England in 2006” – EnergyTrends September 2007, page 16: : www.berr.gov.uk/files/file41460.pdf

2Specific exclusions from eligibility for the RO are existing hydro plant over 20 MW; all plant using renewable

sources built before 1990 (unless re-furbished); and energy from mixed waste combustion unless the waste is firstconverted to fuel using advanced conversion technology.3

The corresponding percentages for the UK as a whole are 3.51 in 2004, 4.15 in 2005 and 4.47 in 2006 which aresimilar to the overall renewables percentages in Table 3

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 21/76

Table 1: Generation and supply of electricity in Scotland, Wales, Northern Ireland and England,2005 and 2006

2005 2006

UK total Scotland WalesNorthern

Ireland England UK total Scotland Wales

Generated by Major power producers 362,212 41,848 32,201 9,239 278,925 361,656 45,525 32,203

Other generators 36,160 7,399 2,448 399 25,914 36,670 8,084 2,711

Total generated 398,372 49,246 34,649 9,638 304,838 398,326 53,609 34,914 Own use by Other generators 1,608 329 109 18 1,152 1,495 330 111

Electricity supplied (net) by Other generators 34,552 7,070 2,340 381 24,762 35,175 7,754 2,600

Used in pumping at pumped storage and other ownuse by MPPs 19,972 3,403 4,601 325 11,643 21,991 4,267 5,594

Electricity supplied (net) by MPPs 342,241 38,445 27,600 8,915 267,282 339,666 41,259 26,609

Electricity transferred to England (net of receipts) - 5,628 4,497 - -10,125 - 10,036 3,888Electricity transferred to Northern Ireland (net of receipts)

- 1,687 - -1,687 - - 905 -

Electricity transferred to Europe (net of receipts) -8,321 - - 2,073 -10,394 -7,517 - - Transfers from other generators to public supply 9,777 2,170 1,009 277 6,322 12,145 2,851 1,308

Transmission losses 5,777 573 382 134 4,688 5,736 571 380

Distribution losses 24,861 1,874 1,388 512 21,086 24,902 1,826 1,366 Consumption from public supply [A] 329,733 30,859 22,344 8,160 268,370 328,722 30,779 22,286

Consumption by autogenerators 24,744 4,894 1,329 104 18,418 22,999 4,896 1,290

Total Electricity consumption 354,476 35,753 23,672 8,264 286,788 351,720 35,675 23,576

Electricity sales (public supply) [B] 329,073 30,975 23,125 7,647 267,326 328,299 29,866 23,064 Statistical difference +660 -115 -781 +512 +1,044 +423 +913 -778

between calculated consumption [A] and sales [B]

Figures in this table do not sum exactly to the UK totals shown because of rounding

1 9

D e c

em b er 2 0 0 7

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 22/76

Table 2: Generation of electricity by fuel in Scotland, Wales, Northern Ireland and England, 2005 and

2005 2006

UK total Scotland WalesNorthern

Ireland England UK total Scotland WalesMajor power Coal 130,894 12,092 6,772 2,455 109,576 146,356 17,488 8,992

producers: Oil 2,716 556 - 331 1,829 2,883 890

Gas 137,483 6,250 14,984 6,454 109,795 126,637 8,347 13,272Nuclear 81,618 18,681 7,842 - 55,095 75,451 14,141 7,010

Thermal renewables 2,746 - 176 - 2,570 2,750 - 36

Hydro natural flow 3,826 3,626 196 - 4 3,727 3,476 226

Hydro pumped storage 2,930 643 2,231 - - 3,853 1,184 2,668

Total 362,212 41,848 32,201 9,239 278,925 361,656 45,525 32,203

Other Coal 3,954 51 - 3,903 3,926 30

Generators: Oil 2,419 1,346 41 1,031 2,116 1,251 105

Gas 15,227 3,121 967 11,139 14,705 3,287 802

Thermal renewables 6,291 595 60 6 5,630 6,546 714 231

Other thermal 3,683 - 585 3,089 3,615 - 648

Hydro natural flow 1,096 962 68 19 46 878 749 49

Non thermal renewables 2,912 1,281 715 253 663 4,232 2,023 867

Wastes 578 43 11 524 651 29 9Total 36,160 7,399 2,448 399 25,914 36,670 8,084 2,711

Total generation by fuel 398,372 49,246 34,649 9,638 304,838 398,326 53,609 34,914

within

which: Renewables Hydro 4,922 4,588 281 19 34 4,605 4,225 275

Wind, wave, solar 2,912 1,281 715 253 663 4,232 2,023 867

Other 9,036 595 236 4 8,200 9,296 714 267

Total 16,870 6,464 1,232 277 8,897 18,133 6,961 1,409

Renewables eligible under the renewablesobligation 13,138 4,051 1,059 277 7,751 14,554 4,576 1,286

Percentage Coal 33.9% 24.7% 19.5% 36.9% 37.7% 32.7% 25.8%

shares of Oil 1.3% 3.9% 0.1% 1.0% 1.3% 4.0% 0.3%

generation: Gas 38.3% 19.0% 46.0% 40.5% 35.5% 21.7% 40.3%

Nuclear 20.5% 37.9% 22.6% 17.5% 18.9% 26.4% 20.1%

Hydro natural flow 1.2% 9.3% 0.8% -% 1.1% 7.9% 0.8%Other renewables 3.0% 3.8% 2.8% 2.9% 3.4% 5.1% 3.2%

Other 1.8% 1.3% 8.2% 1.2% 2.0% 2.3% 9.5%

Total 100% 100% 100% 100% 100% 100% 100%

Shaded areas indicate where separate figures for Northern Ireland cannot be given and the data have been merged with data for England

Figures in this table do not sum exactly to the UK totals shown because of rounding

2 0

D e c em b er 2 0 0 7

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 23/76

Special feature – Regional and local electricity consumption

Regional and local electricity consumption statistics for 2006

The fourth annual exercise to collect and publish electricity consumption data at a regional andlocal level has now taken place. This has been conducted by BERR which replaced DTI in June2007. The first exercise was reported in the December 2004 edition of Energy Trends with anupdated article in the March 2005 edition of Energy Trends. The results of the second exercise

were presented in an article in the December 2005 edition of Energy Trends and the results of thethird in an article in the December 2006 edition of Energy Trends.

SummaryEstimates of final electricity consumption at both local authority (NUTS4 1) and government officeregion (NUTS1) levels assist local and regional bodies to monitor and implement the energyefficiency programmes in their own areas. Once again excellent co-operation from electricitysuppliers, distributors and data aggregators, has led to total and average consumption levels fordomestic and industrial/commercial sectors being made available here. As before, the informationhas been taken from the administrative systems of the electricity companies’ data aggregators, butwhile the quality of the data is a further improvement on that for previous years, the statistics

shown here are again classed as “experimental” while detailed comparisons are made between thefour years of data to ensure that all the shortcomings of the earlier years’ data have beenunderstood and allowed for.

MethodologyTo produce 2006 annualised data at both local authority (NUTS4) and government office regional(NUTS1) levels, data were collected for all electricity metering points and then aggregated for eachof the sub national areas. Every metering point has a unique reference number called an MPAN ormeter point administration number – which may have one or more meters. Consumption data forall MPANs are held on the systems of the data aggregators (DAs), the agents of the electricitysuppliers who collate/aggregate electricity consumption levels for each meter. To find thegeographical location of each MPAN, the services of a company called Gemserv are used.

Gemserv is the company that provides one central access point for suppliers, distributors and theiragents to obtain address and postcode information about each MPAN. By merging the DAs’consumption data with Gemserv’s postal address information, local and regional consumptionestimates were compiled. Gemserv provided BERR with the full address and postcode from theirnew on-line system ECOES2 at the end of 2006.

DAs responsible for non half hourly (NHH) meters (domestic and small commercial customers)were asked to use a standard run on their systems over the 2007 August Bank Holiday weekend togenerate annualised consumption rates for the period from 30 January 2006 to 29 January 2007. This ensured that the data generated were consistent, that the task could be easily accommodatedwithin the work schedules of the DAs, and that the costs to the electricity industry of providing thedata were minimised. The information that was provided by the data aggregators was as follows:

• Consumption data, based on either an annualised advance (AA) or an estimated annualconsumption (EAC). The AA is based on actual meter readings, whilst the EAC is anestimate of consumption based on historical information and the profile class of thecustomer. The DAs’ systems for NHH meters work around a 14-month settlement period,which ensures that around 80 per cent of the data are based on AAs after 7 months and

1 NUTS (Nomenclature of Units for Territorial Statistics) is a hierarchical classification of spatial units that

provides a breakdown of the European Union’s territory for producing regional statistics which arecomparable across the EU. NUTS1 refers to the 9 Government Office Regions in England, and separatelyWales, Scotland, (and Northern Ireland), totalling 12 UK NUTS1 regions. NUTS4 refers to the 354 individualLondon boroughs/metropolitan districts/unitary authorities/local authority districts in England, the 22individual unitary authorities in Wales, the 41 individual or groups of whole/part unitary authorities and/or

local enterprise company areas in Scotland, (and the 26 individual district unitary authorities in NorthernIreland), totalling 443 UK NUTS4 regions. NUTS5 areas are broadly Electoral Wards; there are about10,000 NUTS5 areas in Great Britain. 2 ECOES is the Electricity Central Online Enquiry Service

December 200721

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 24/76

Special feature – Regional and local electricity consumption

approximately 92 per cent after 14 months. So by generating the data for BERR in August2007, around 80 per cent of NHH MPAN data collected for this exercise was based onelectricity consumption taken from actual meter readings. There are around 28¾ milliondomestic, industrial and commercial NHH MPANs in Great Britain.

• For NHH meters the profile attached to each MPAN was also given and profiles 1 and 2were allocated to the Domestic sector and profiles 3 to 8 to Industrial and Commercial. AllHH meters were allocated to Industrial and Commercial.

• For half hourly (HH) meters (larger commercial customers), DAs ran a simple report ontheir systems to give the total amount of consumption for the calendar year 2006. Thereare currently around 109,000 HH meters in Great Britain (up from 105,000 in 2005).

• In addition to data linked to domestic and commercial properties, the data files alsoprovided consumption levels for unmetered sites including street lighting and electricityused by the electrified railway network, based mainly in the south of England.

For the 2003 analysis DTI used the Office for National Statistics’ (ONS) Postcode Lookup File inorder to assign postcodes first to NUTS5 areas and from there to NUTS4 areas. For 2004 and2005 the Gemserv data was matched against the All Fields Postcode Directory (AFPD) to obtain aNUTS5 code and the NUTS5 code was truncated to 7 characters, giving a NUTS4 code. The

AFPD was re-named as the NSPD (National Statistics Postcode Directory) in May 2006. For the2006 exercise the February 2007 NSPD was used. Out of the 31.1 million records in the Gemservdataset, it was not possible to allocate a NUTS code to around 900,000 records. This was due tothe postcode being incomplete, invalid or missing. A number of invalid postcodes were correctedby automated methods, for example, changing those that started 1P to IP, those ending II to LL,and standardising on postcode spacing. Where a NUTS code could not be allocated in this way,the street and post town, or just post town, was used to allocate a NUTS code. These changesresulted in reducing the number of unmatched Gemserv records to 323,000. During the last 12months, BERR/DTI has worked its way through those Gemserv data with incomplete, invalid ormissing postcodes and added complete postcodes from other sources including Royal Mail’sPostcode Address File. This work resulted in reducing the number of MPANs with consumptionthat could not be allocated to a NUTS4 area to around 30,000. Because allocation to NUTS area

is by postcode, any address containing a PO Box number will be assigned to the NUTS area of thePost Office sorting depot. This is particularly important for interpretation of data at a level belowthat of NUTS4 such as the middle layer super output area (MLSOA) analyses described below. Inallocating MPANs to MLSOAs (or Dzones in Scotland), the NSPD did not have correspondingcodes for all postcodes. In addition, on occasions it was only possible to allocate a NUTS4 codebut not a lower level MLSOA code. As a result around 570,000 MPANs did not have an MLSOAcode allocated.

Any nominally domestic MPANs with consumption over 100,000 kWh (ie profile codes 1 and 2)were allocated to the industrial and commercial sector in the same way as they had been forprevious years. Inspection of the individual data showed that there were very few recognisableprivate addresses with consumptions over 100,000 kWh, but a significant number between 50,000

and 100,000 kWh per year. Additionally, where the third to sixth variable of the address includedtext that indicated the address to be of a commercial nature by containing UNMET or UMS (ieunmetered supply) or STR (street lighting) or LAND or LLO (Landlord supply) or STAIR (staircaselighting), TEMP (temporary builders’ supply), LTD, PLC, SHOP or HOTEL consumption wasmoved to the industrial and commercial category. (This refinement was introduced for 2004 but forthat year and 2005 only the third variable of the address was searched and LTD, PLC, SHOP andHOTEL were not included in the search). The 100,000 kWh cut off is known to have classifiedsome very large domestic users to the industrial and commercial sector but this is more thanoutweighed by the number of small industrial and commercial consumers that will have beenallocated to the domestic sector. In 2006 this process has resulted in 6,000 meters being re-allocated with around 3,600 of this being due to consumption being greater than 100,000 kWh.

December 2007 22

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 25/76

Special feature – Regional and local electricity consumption

Regional and local estimates of final electricity consumption data Table 3 shows the amount of electricity consumed by selected local authorities within eachgovernment office region. The table is broken down by domestic and commercial/industrialcustomers and shows the total amount of electricity consumed in GWh and the number ofcustomers. Average consumption levels for domestic and non-domestic MPANs are also provided.The local authorities within each region have been selected to show those areas with the highest

and lowest average consumptions. Commercial and industrial customers may have more than oneMPAN per site. The number of domestic sector MPANs in Great Britain is larger than the numberof households by about 6 per cent, although in Scotland there are around 19 per cent moredomestic MPANs than households. This is because in Scotland it is estimated that some 280,000domestic customers are on two-rate or three-rate meters using dynamic teleswitching to control when cheaper rate electricity is made available to consumers and these customers will have twoMPANs per address. A similar system (resulting in multiple MPANs per customer) is available tohouseholds in England and Wales (“Economy 10” being one example) but this is less widespread(around 800,000 customers in total). Second homes, holiday homes and additions to the housingstock will also lead to the number of MPANs exceeding the number of households. This meansthat the sales per MPAN figures understate consumption per household for most local authorities.The full table showing all NUTS4 areas3 within these regions is available on the BERR Energy

statistics web site at:www.berr.gov.uk/energy/statistics/regional/index.html www.berr.gov.uk/files/file42925.xls

Electricity consumption not covered by the data collection exerciseThe consumption estimates provided here cover only Great Britain, and exclude those largeconsumers of electricity that are connected to the high voltage lines of the transmission system.Northern Ireland has been excluded because the structure of the electricity industry in NorthernIreland differs from the rest of the United Kingdom, where in 2006 there was a single monopolysupplier to domestic customers, Northern Ireland Electricity plc. This creates problems withdisclosure. However, any consumer of more than 500 MWh per year can select its supplier from

one of 6 licensed suppliers. In November 2007 the electricity market was further opened so thatany Northern Ireland consumer can select their supplier. BERR has been in contact with NorthernIreland about extending this analysis in time for 2007 so that the whole of the United Kingdom iscovered.

In addition, DAs do not hold information on their systems for consumption levels for those industrialconsumers, such as very large sites or plant, who receive their electricity as CVA (Central VolumeAllocation) users via the high voltage transmission system. CVA users have differentarrangements with their electricity suppliers to NHH and HH meter customers. CVA consumptionis particularly important in Wales and so the consumption figure for Wales in Table 3 is lower thanconsumption estimate given on page 25.

Also excluded is electricity used by companies that generate their own electricity and consume itwithout it passing over the public distribution network. This amounted to 24.5 TWh in the UK as awhole in 2006. Much of this “autogeneration” is from CHP schemes and an indication of theregional importance of such schemes can be obtained from an article on pages 26 to 32 of theSeptember 2007 edition of Energy Trends (“Combined Heat and Power in Scotland, Wales,Northern Ireland and the regions of England in 2006”).

Comparison with other published annual figures for 2006Table 1 compares the total figures shown in Table 3 with corresponding electricity figurespublished in Chapter 5 of the Digest of United Kingdom Energy Statistics 2007 (DUKES). Afterallowing for electricity not included in consumption in Table 3 (CVA and Northern Ireland), there is

3 The NUTS4 areas in Scotland do not match exactly the Scottish Local Authority Areas. There are moreNUTS4 areas in Scotland than Local Authorities. In the analysis in the full table Scottish Local Authorities areused in place of NUTS4 giving a total of 408 local areas in Great Britain.

December 200723

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 26/76

Special feature – Regional and local electricity consumption

a difference of around 4.2 TWh or just under 1½ per cent. Some of this will be due to the fact thataround 20 per cent of the data in the sub-national exercise is based on estimates rather thanactual meter readings while another factor is that the NHH records run from end January 2006 toend January 2007 and not for the calendar year 2006.

Table 1: Comparison with published UK statistics for 2006 GWh

GB Total in Table 3 - Domestic 117,817Industrial and Commercial 200,156Total for Great Britain 317,973

Plus Northern Ireland 8,063Plus Sales direct from high voltage lines (based on Ofgem data) 6,600

Implied UK Sales of electricity 332,636UK Sales of electricity (DUKES 2007 Table 5.5) 328,300Statistical difference +4,336

(+1.3% of UKSales)

Domestic sector (DUKES 2007 Table 5.2) 116,449Less Northern Ireland -3,242

Domestic sector GB 113,207GB Total in Table 3 - Domestic 117,817Statistical difference +4,610

(+3.9% of GBdomestic

consumption)

In addition the sub-national figures for domestic consumption appear to include about 4.6 TWh thatare included as non-domestic consumption in DUKES. Some of this will be due to the overall over-estimate of consumption described in the paragraph above, but some will also be due to theclassification of consumption by profile class (see ‘Methodology’ section, above) with smallcommercial and industrial consumers classified as domestic consumers.

Preliminary analysesThe lowest average domestic electricity consumptions (which is consumption per meter pointrather than per home or per household) are 3,466 kWh in Islington, 3,482 kWh in South Tynesideand 3,517 kWh in Blaenau Gwent while the highest is 7,291 kWh in the Isles of Scilly (although ona per household basis estimated average consumptions in the Orkney and Shetland Islands arehigher than this at around 9,500 and 11,300 kWh respectively). Commercial and industrial sectorelectricity consumption is a function of both the number of commercial and industrial sites in anarea and the volume of electricity they use. Commercial centres such as Westminster, Leeds,Glasgow, Manchester, Birmingham and Tower Hamlets (Docklands) have a high total overallvolume of consumption but they also have a large number of non-domestic consumers so average

consumption per commercial and industrial meter point is usually relatively low. The three areaswith the highest average consumption per commercial or industrial meter point (the City of London,Neath Port Talbot and Ellesmere Port and Neston) are of note because in those areasconsumption is shared between fewer but larger consumers of electricity. The lowest level ofindustrial and commercial consumption of electricity in total volume terms is recorded in the Isles ofScilly and the Orkney Islands. However, low average consumptions are found in rural areas suchas Penwith, Wealden, Torridge and the Western Isles, but also in some inner city areas such asHackney, Lewisham and Lambeth.

For Great Britain as a whole average domestic consumption per meter point in 2006 was 4,457kWh4, with the West Midlands being the closest to this average in Regional terms. The East, the

4 Households are not evenly distributed about this mean because households using electricity as their mainsource of heating will have much higher consumptions. However, the majority of households do not useelectricity as their main source of heating and the median MPAN recorded consumption of around 3,615kWh per year in 2006.

December 2007 24

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 27/76

Special feature – Regional and local electricity consumption

South East and the South West had the highest domestic sector averages and the North East thelowest. However, on an estimated consumption per household basis Scotland’s average at over5,300 kWh is the highest. For industrial and commercial use the greatest regional volume ofconsumption is in Greater London and the least in the North East. However, in terms of electricityconsumed per £ thousand of Gross Value Added, Wales ranks the highest and the North East thesecond highest with Greater London the lowest as Table 2 shows.

Table 2: Electricity consumption in 2006 in the industrial and commercial sectorcompared with economic activity

Electricity consumption(GWh)

kWh consumption per £thousand of Gross Value Added*

Wales 11,794 286.28

North East 9,315 258.53

Yorkshire and the Humber 17,157 219.67

North West 23,355 219.44

East Midlands 14,989 209.14

West Midlands 17,300 204.17

Scotland 17,452 202.19South West 15,783 185.77

East of England 16,827 179.88

South East 24,632 161.18

Greater London 29,143 143.07

Great Britain total(including unallocated)

200,156 184.76

* This uses provisional Gross Value Added in 2005 at current basic prices (workplace based) as available atwww.statistics.gov.uk/downloads/theme_economy/NUTS1_Tables_1-8.xls; Table 1.8 at 3 December 2007.

Chart 1: Average gas and electricity consumption per household, 2006

0

5,000

10,000

15,000

20,000

25,000

S c o t l a n d

E a s t o f E n g l a n d

S o u t h W e s t

S o u t h E a s t

G r e a t B r i t a i n

W e s t M i d l a n d s

E a s t M i d l a n d s

W a l e s

N o r t h W e s t

Y o r k s a n d H u m b e r

L o n d o n

N o r t h E a s t

k

W h p e r H o u s e h o l d

Electric Gas

(Corrected chart)

December 200725

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 28/76

Special feature – Regional and local electricity consumption

Charts 1 and 2 illustrate the data at regional level. Chart 1 shows regional consumption for thedomestic sector on a per household basis (rather than per MPAN) using the latest availablehousehold data. The regions are shown in order of average annual consumptions but annualaverage gas consumptions (see article on page 30) are also given.

Chart 2 similarly combines electricity and gas use per £ thousand of Gross Value Added. The

South West, South East and London use proportionately more electricity than gas per unit ofoutput on this basis.

Chart 2: Industrial and commercial electricity and gas consumption per £ thousandof value added, 2006

0

100

200

300

400

500

600

700

W a l e s

N o r t h E a s t

Y o r k s a n d

H u m b e r

N o r t h W e s t

E a s t

M i d l a n d s

W e s t

M i d l a n d s

S c o t l a n d

G r e a t B r i t a i n

S o u t h W e s t

E a s t o f

E n g l a n d

S o u t h E a s t

L o n d o n

k W h p e r £ t h o u s a n d G V A

Electric Gas

Improvements to the data since 2003Experimental results for 2005, 2004 and 2003 were published in the December 2006, December2005 and March 2005 editions of Energy Trends. The 2006 data are judged to be of better qualitythan those of the earlier years as the following improvements have been made:

• As described in the Methodology section, above, much more data have now been allocatedto NUTS4 areas than in earlier years. Unallocated consumption accounted for 0.8 per centof the Great Britain total compared with 1.7 per cent unallocated in 2005 and 6.5 per centunallocated in 2003. In terms of numbers of MPANs unallocated the proportion has fallenfrom 0.7 per cent in 2003 to 0.1 per cent in 2006.

• The 2003 data as submitted to DTI contained duplicated entries for a large number ofMPANs, although this was mainly confined to the North West region. Although theduplicated data were removed, it is suspected that the resultant dataset did not adherestrictly to the specification used by other datasets in other regions. There were noduplicated entry problems in 2004 and 2005. In 2006 the duplicate entries resulting from

one data aggregator providing data for a slightly later time period have been removed.• The system for moving non domestic data to the industrial and commercial sector through

identifying large non-private household use such as street lighting, other unmetered usage,and usage attributable to communal areas in multi-occupied dwellings and housing estateshas been extended in 2006 by identifying the words “Ltd”, “PLC”, “Shop” and “Hotel” withinthe address fields. From 2005 DTI/BERR was able to remove duplicated MPANs that canarise for new connections because of changes to building plans. Mostly these wereMPANs for which consumption was zero and full postcodes had not been allocated.

• Since 2003 there has been a general improvement in the statistical differences betweenthese data in aggregate and corresponding data published in the Digest of UK EnergyStatistics. The statistical difference has fallen from 3.4 per cent of UK electricity sales in2003 to 1.3 per cent in 2006. The statistical difference for domestic sector sales has fallen

from 14.2 per cent in 2003 to 3.9 per cent in 2006 (see Table 1, above).• These unallocated figures have shown a reduction in bias over the four years. For

domestic consumers the average consumption of the unallocated MPANs in 2003 was 10½

December 2007 26

8/3/2019 File 43304

http://slidepdf.com/reader/full/file-43304 29/76

Special feature – Regional and local electricity consumption

December 200727

per cent below the average for all domestic consumers but this reduced to 8 per cent belowin 2004, 5 per cent below in 2005 and 2½ per cent below in 2006. For the unallocatedMPANs in the industrial and commercial sector average consumption in 2003 was almost 4times the average consumption for all industrial and commercial MPANs (ie some verylarge consumers could not be allocated to a NUTS4 area). This rose in 2004 but in 2005fell back to less than 1½ times, but rose once again to 3 times the average in 2006.