feb 10 12conference - ncfcncfc.org/wp-content/uploads/2016/02/2016-lta-conference-book...david...

TRANSCRIPT

Feb 10-12

National Council ofFarmer Cooperatives

Legal, Tax, & Accounting

Conference

Tel: 202-626-8700 Fax: 202-626-8722

50 F Street, NW Suite 900 Washington, DC 20001

www.ncfc.org

Representing the Business Interests of Agriculture

To: Legal, Tax and Accounting Committee Members and Guests Welcome to Phoenix! I think you’ll find that we have a great lineup of topics and speakers this year. The conference program qualifies for CLE and CPE credits, so remember to sign-in each day for credit. The CFO Roundtable will take place on Wednesday afternoon from 2:00-5:00 in Kierland 1A. All CFOs are invited to attend. Conference participants, spouses, and guests are invited to attend the Welcome Reception from 6:00pm – 8:00pm on the Northern Sky Terrace. On Thursday morning the LTA sessions open with an informal roundtable discussion of current tax developments in the Powell room from 7:00 to 8:15 – all are welcome and breakfast will be provided. The LTA Conference begins on Thursday morning at 8:30 with participation in the NCFC General Session in the Kierland Grand Ballroom 1/2/3. The LTA session starts at 10:30a.m. right next door in Kierland 4B/C. Please plan to attend the Cooperators reception on Thursday evening from 6:00-8:00 in the Trailblazers Ballroom C/D/E; spouses and guests are also welcome. On Friday morning you are invited to hear Terry Barr give his economic outlook for 2016 in the Paradise Ballroom from 7:00 to 8:15. A plated breakfast will be served. The LTA Conference begins at 8:30 in Kierland 4B/C and ends at noon. NCFC welcomes your feedback on all aspects of the conference, so please take the time to complete the evaluation form you will find on your chair each day or provide feedback within the conference app. If you need additional information or assistance, please contact my assistant Stefanie Hallett at 202-344-6513 or see the NCFC staff at the registration desk. Best regards,

Marlis Carson Senior Vice President & General Counsel

Tel: 202-626-8700 Fax: 202-626-8722

50 F Street, NW Suite 900 Washington, DC 20001

www.ncfc.org

Representing the Business Interests of Agriculture

2015 LTA Committee Acknowledgments LTA Committee members contributed significant time and expertise to NCFC and the activities of the LTA Committee in 2015. The Executive Committee would like to especially thank the following committee members for their contributions. Bylaw Working Group Early in 2015, members of the LTA Committee began work on a set of model bylaws for cooperatives to serve as guidance for NCFC members. The group plans to develop sample bylaw provisions and commentary on tax, securities, membership eligibility, voting rights, board composition, escheat, operating on a cooperative basis, and other topics. The working group will present the findings at a future LTA conference. Working Group Members: Teree Castanias, CPA (Co-Chair) Charlie Sullivan, Bond Schoeneck & King PLLC (Co-Chair) Todd Eskelsen, Schiff Hardin LLP Bob Glass, Land O’ Lakes Inc. Daniel Hall, GROWMARK, Inc.

John Kenley, Northwest Dairy Association/Darigold Eric Krienert, Moss Adams LLP Daniel Mott, Fredrikson & Byron, P.A. Ronald Peterson, Hanson Bridgett LLP David Swanson, Dorsey & Whitney LLP

Section 199 Working Group The Section 199 Working Group continues to monitor legislative, regulatory, and case developments involving the Section 199 deduction. In 2015 the group had the opportunity to draft and submit comments to Treasury on proposed regulations under Section 199. Working Group Members: George Benson, McDermott Will & Emery LLP (Co-Chair) Teresa Castanias, CPA (Co-Chair) Kevan Acord, BridgeBuilder Tax & Legal Services David Antoni, KPMG LLP Stan Dvorak, CHS, Inc. Robert Glass, Land O' Lakes, Inc. James Heine, CHS Inc.

Brett Huston, KPMG LLP Ron Kottke, Land O' Lakes, Inc. Eric Krienert, Moss Adams LLP Christine Lau, Sunsweet Growers, Inc. Greg Lawler, GROWMARK, Inc. Lisa Maloy, American Crystal Sugar Company Carrie Parrish, Sunkist Growers, Inc. Dan Schultz, Cooperative Consulting, LLC

Tel: 202-626-8700 Fax: 202-626-8722

50 F Street, NW Suite 900 Washington, DC 20001

www.ncfc.org

Representing the Business Interests of Agriculture

2015 LTA Committee Acknowledgments (continued) IC-DISC Working Group Farmer cooperatives would like to utilize Interest-Charge Domestic International Sales Corporations (IC-DISCs) to receive favorable tax rates on exports of commodities. However, IRS regulations do not specify how farmer cooperatives and their members should calculate the amount of income eligible for the preferred tax treatment. A working group of LTA Committee members is providing input as NCFC urges Treasury to provide guidance on how farmer cooperatives can best obtain the benefits of this export-promoting tax code provision. LTA members and NCFC staff met with IRS, Treasury, White House, and USDA officials June of 2015 to discuss this issue, and NCFC staff has followed up with meetings with Senate Finance Committee staff. Treasury officials have said they will decide soon whether to issue guidance applicable to farmer cooperatives. Working Group Members: David Antoni, KPMG LLP Sharon Appelt, Northwest Dairy Association/Darigold Braden Bender, Sun-Maid Growers LLP George Benson, McDermott Will & Emery LLP Larry Boyle, Ocean Spray Cranberries Inc. John Caragozian, Sunkist Growers, Inc. Teresa Castanias, CPA Conrad Davis, Crowe Horwath LLP

Eric Krienert, Moss Adams LLP Kevin Feeley, McDermott Will & Emery LLP Bob Glass, Land O’ Lakes Inc. Christine Lau, Sunsweet Growers, Inc. Dean LaVallee, Blue Diamond Growers Ana Klein, Sunsweet Growers, Inc. Brian Powell, Moss Adams LLP

Tel: 202-626-8700 Fax: 202-626-8722

50 F Street, NW Suite 900 Washington, DC 20001

www.ncfc.org

Representing the Business Interests of Agriculture

2015 LTA Committee Acknowledgments (continued)

We would also like to thank the chairs and vice chairs of the LTA Subcommittees, discussion forums, and working groups. They are responsible for writing annual subcommittee reports and/or providing leadership on a wide variety of topics.

Chairs and vice chairs include:

David Longinotti, Hanson Bridgett LLP Kimberly Lowe, Fredrikson & Byron, P.A. Lisa Maloy, American Crystal Sugar Company Jay McWatters, Dopkins & Company LLP David Moss, Tennessee Farmers Cooperative Daniel Mott, Fredrikson & Byron, P.A. Sue Ann Nelson, Fredrikson & Byron, P.A. Chris Ondeck, Proskauer Rose LLP Ronald Peterson, Hanson Bridgett LLP Daniel Schultz, Cooperative Consulting LLC David Simon, Attorney-At-Law Richard Stamm, Ocean Spray Cranberries, Inc. Charles Sullivan, Bond Schoeneck & King PLLC David Swanson, Dorsey & Whitney LLP Alan Weinstein, CoBank Joe Werstak, United Producers Inc. Randon Wilson, Jones Waldo Holbrook & McDonough Stephen Zovickian, Bingham McCutchen LLP

David Antoni, KPMG LLP Marla Aspinwall, Loeb & Loeb LLP Donald Barnes, Porter Wright McMorris & Arthur LLP George Benson, McDermott Will & Emery LLP Brent Bostrom, GROWMARK, Inc. Kimberly Bram, Southern States Cooperative Inc. Andrew Brown, Dorsey & Whitney LLP Teresa Castanias, Teresa Castanias, CPA Richard Cisne, Hudson, Cisne & Co. Terry Costello, Costello Law Firm John Cowell, Ocean Spray Cranberries, Inc. Todd Eskelsen, Schiff Hardin LLP Robert Glass, Land O' Lakes Inc. Dan Hall, GROWMARK, Inc. Julian Heron, Tuttle Taylor & Heron Brett Huston, KPMG LLP William Hutchison, Lane Powell PC Barry Jencik, Greendyke Jencik & Associates CPAs, PLLC Ana Klein, Sunsweet Growers, Inc. Michael Lindsay, Dorsey & Whitney LLP

With our appreciation,

2015 LTA Executive Committee Richard Cisne, Chair Kevin Feeley Alan Weinstein

2016 LTA Conference Attendees Name Company Anthony Aaron Ice Miller LLP Kevan Acord BridgeBuilder Tax + Legal Services PA David Antoni KPMG LLP Sharon Appelt Darigold, Inc. Tricia Arnold Alabama Farmers Cooperative, Inc. Josep Barenys Michigan Milk Producers Association Donald Barnes Porter Wright Morris & Arthur David Barrett Barrett, Easterday, Cunningham & Eselgroth LLP Braden Bender Sun-Maid Growers of California George Benson McDermott Will & Emery LLP Scott Blickenstaff Amalgamated Sugar Company Brent Bostrom GROWMARK, Inc. Larry Boyle Ocean Spray Cranberries, Inc. Jeff Brandenburg CliftonLarsonAllen LLP David Buck AKT, LLP David Burlage CoBank Linda Buss West Central John Caragozian Sunkist Growers, Inc. Teresa Castanias Teresa Castanias CPA Amy Chambers KFSA Dick Cisne Hudson, Cisne & Co. CPA's Kevin Cody Dairy Farmers of America, Inc Robert Condron MFA Oil Company Renee Cool Dairy Farmers of America, Inc. William Covey GROWMARK, Inc. Jon Cowell Ocean Spray Cranberries, Inc. Andrew Dallas Riceland Foods, Inc. Conrad Davis Crowe Horwath LLP Casey Delaney Welch's Robert Dowd Griswold LaSalle Cobb Dowd & Gin Russell DuBose D. Williams &Co, PC, CPAs Chris Duggan Dorsey & Whitney LLP Carolyn Eselgroth Barrett, Easterday, Cunningham & Eselgroth LLP Todd Eskelsen Schiff Hardin LLP Gail Faries D. Williams &Co, PC, CPAs Kevin Feeley McDermott Will & Emery LLP Philip Fileri Harter Secrest & Emery LLP Michael Fincher Deloitte Tax LLP Jo Ann Fuller Alabama Farmers Cooperative, Inc. Dennis Gardiner Gardiner Thomsen CPAs Mark Gardiner Gardiner Thomsen CPAs John Gerken West Central Robert Glass Land O'Lakes, Inc. Jon Greeley NORPAC Foods, Inc James Griggs Saalfeld Griggs PC Barry Groebel Herbein+Company, Inc. Tara Guler Baker Tilly Virchow Krause, LLP Daniel Hall GROWMARK, Inc. Jennie Haverkamp CoBank

Jim Heine CHS Inc. William Hendry Florida's Natural Growers Robert Hensley Dorsey & Whitney LLP Julian Heron Blue Diamond Growers Todd Hoppe Foster Swift Collins & Smith P.C. Shannon Huff Tennessee Farmers Cooperative Amy Humphreys Northwest Dairy Association/Darigold, Inc. Brett Huston KPMG LLP Bill Hutchison Lane Powell PC Vanessa Jacobsen Eimer Stahl LLP Peter Janzen Land O'Lakes, Inc. Edward Kacsuta U.S. Tobacco Cooperative Inc. Richard Kasper Minn-Dak Farmers Cooperative Patrick Kautzman Eide Bailly LLP John Kenley Northwest Dairy Association/Darigold, Inc. Dustin Klinger Thede Culpepper Moore Munro & Sillman LLP Eric Krienert Moss Adams Eric Kroll Baker Tilly Virchow Krause, LLP Peter Latham Florida's Natural Growers Dean LaVallee Blue Diamond Growers Michael Lensmire CliftonLarsonAllen LLP Michael Lindsay Dorsey & Whitney LLP David Longinotti Hanson Bridgett LLP Mashenka Lundberg CoBank Lisa Maloy American Crystal Sugar Company Mike Mayhew CliftonLarsonAllen LLP Sandra Morgan Riceland Foods, Inc. David Moss Tennessee Farmers Cooperative Dan Mott Fredrikson & Byron, P.A. Sue Ann Nelson Fredrikson & Byron, P.A. Marissa Nelson PwC Chris Ondeck Proskauer Rose LLP Jill O'Toole Shipman & Goodwin LLP Daniel Otto Minn-Dak Farmers Cooperative Mike Perda Welch's Ronald Peterson Hanson Bridgett LLP Brynjar Peterson Northwest Dairy Association/Darigold, Inc. Bill Pieper Land O' Lakes, Inc. Zeb Rocha Pacific Coast Producers Steve Rosenau American Crystal Sugar Company Ron Rufener AKT, LLP Naomi Schefcik Oregon Cherry Growers, Inc. Harold Schenker Sunsweet Growers Inc. Scott Simmelink Ag Processing Inc Rebecca Smith CliftonLarsonAllen LLP Keith Spackler Ag Processing Inc Richard Stamm Ocean Spray Cranberries, Inc. S. Eric Steinle Martindell Swearer Shaffer Ridenour Sheilah Stewart Land O'Lakes, Inc. Matt Strong Pacific Coast Producers Dave Swanson Dorsey & Whitney LLC Chuck Telk Gardiner Thomsen CPAs

Sarah Tucher Fredrikson & Byron, P.A. Rick Vanderheiden West Central Teresa Warne American Crystal Sugar Company Rocky Weber Nebraska Cooperative Council Alan Weinstein CoBank Greg Wickham Dairy Farmers of America, Inc Caleb Williams Saalfeld Griggs PC Randon Wilson Jones Waldo Holbrook & McDonough James Zappa CHS Inc. Stephen Zovickian Morgan, Lewis & Bockius LLP

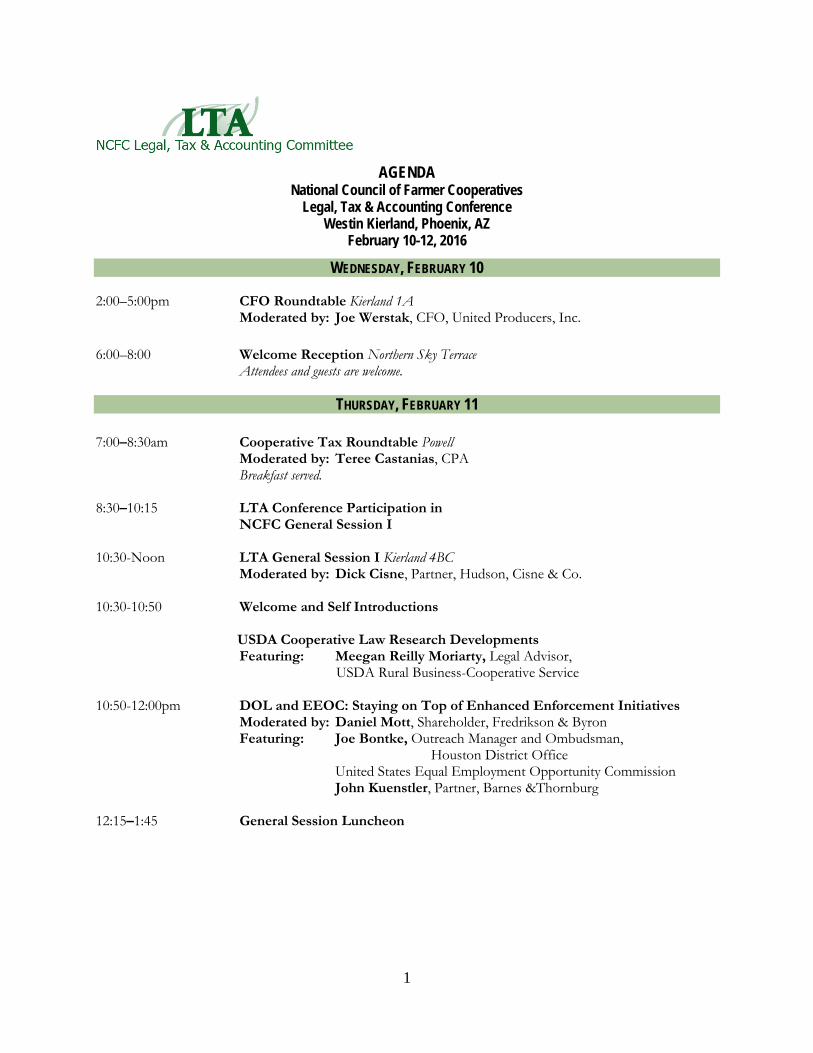

Agenda

1

WEDNESDAY, FEBRUARY 10

2:00–5:00pm CFO Roundtable Kierland 1A Moderated by: Joe Werstak, CFO, United Producers, Inc. 6:00–8:00 Welcome Reception Northern Sky Terrace

Attendees and guests are welcome.

THURSDAY, FEBRUARY 11 7:00–8:30am Cooperative Tax Roundtable Powell Moderated by: Teree Castanias, CPA Breakfast served. 8:30–10:15 LTA Conference Participation in NCFC General Session I 10:30-Noon LTA General Session I Kierland 4BC

Moderated by: Dick Cisne, Partner, Hudson, Cisne & Co.

10:30-10:50 Welcome and Self Introductions

USDA Cooperative Law Research Developments Featuring: Meegan Reilly Moriarty, Legal Advisor,

USDA Rural Business-Cooperative Service

10:50-12:00pm DOL and EEOC: Staying on Top of Enhanced Enforcement Initiatives Moderated by: Daniel Mott, Shareholder, Fredrikson & Byron

Featuring: Joe Bontke, Outreach Manager and Ombudsman, Houston District Office

United States Equal Employment Opportunity Commission John Kuenstler, Partner, Barnes &Thornburg 12:15–1:45 General Session Luncheon

AGENDA National Council of Farmer Cooperatives

Legal, Tax & Accounting Conference Westin Kierland, Phoenix, AZ

February 10-12, 2016

2

12:15–1:45 LTA In-House Luncheons (By invitation only) CFO Working Group Powell In-House General Counsels Cushing A

Tax Directors Forum Cushing B 2:00-4:50 LTA General Session II Kierland 4BC

Moderated by: Kevin Feeley, Partner, McDermott Will & Emery

2:00-2:50 The Tri-State Case: Is a Federated Cooperative Liable for Its Members’ Actions? Featuring: Ty Thompson, Vice President & Deputy General Counsel for

Director and Member Legal Services, NRECA Jay Sturhahn, Member, Sherman and Howard, LLC

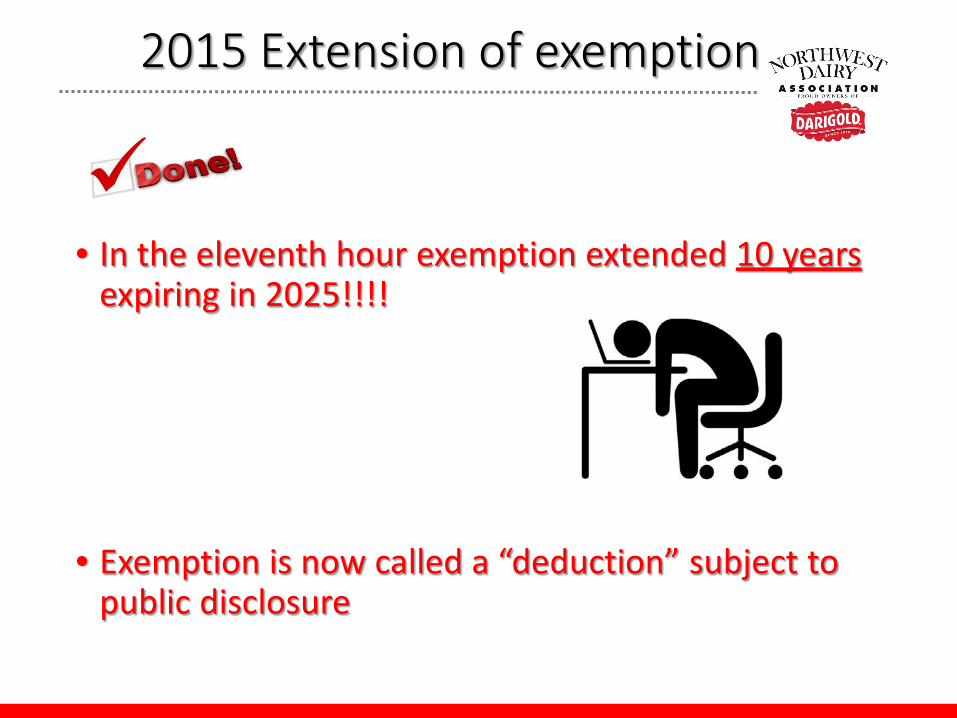

2:50-3:40 The Making of a Gross Receipts Tax Exemption

Featuring: Dan Coyne, Darigold Sharon Appelt, Tax Director, Darigold

3:40–4:00 Break 4:00-4:50 Capper-Volstead and Activist Consumers: How to Operate Under the Immunity Featuring: Chris Ondeck, Partner, Proskauer Rose LLP 5:30–7:30pm Cooperators Reception Trailblazers C/D/E Attendees and guests are welcome.

FRIDAY, FEBRUARY 12 7:00-8:15am LTA Conference Participation in NCFC General Session II Kierland 2 Economic Outlook Featuring: Dr. Terry Barr, Senior Director, Knowledge Bank, CoBank Breakfast served. 8:30-Noon LTA General Session III Kierland 4BC

Moderated by: Dick Cisne, Partner, Hudson, Cisne & Co. 8:30-9:20 Washington Update

Featuring: Lisa Van Doren, Vice President and Chief of Staff, Government Relations, NCFC

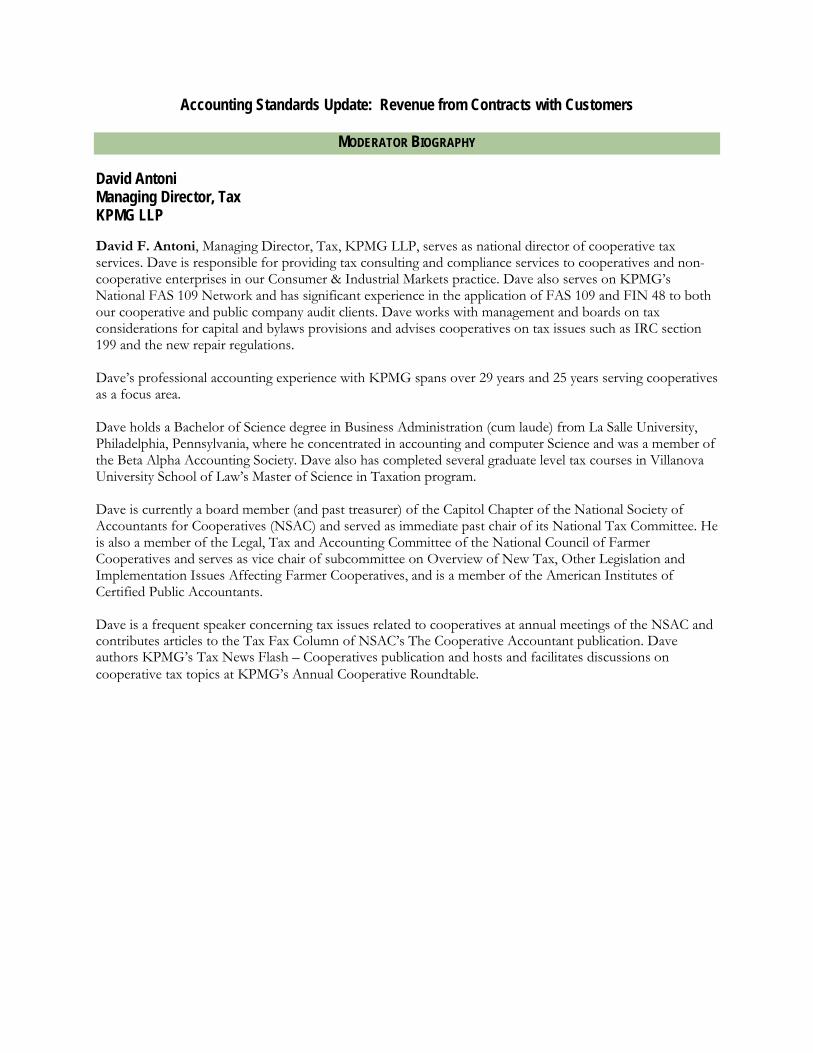

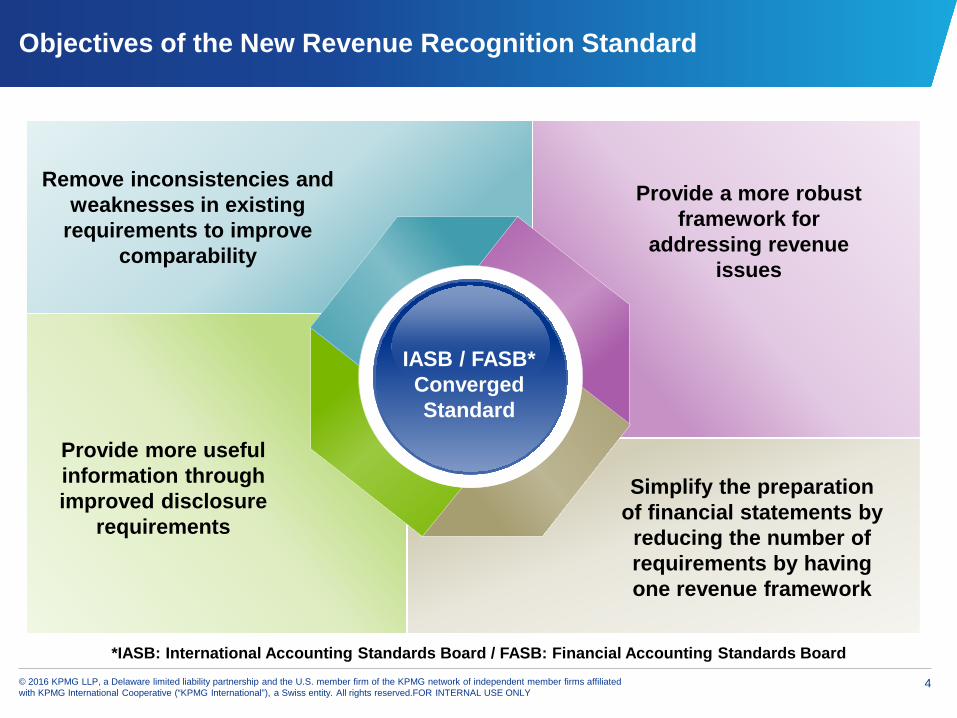

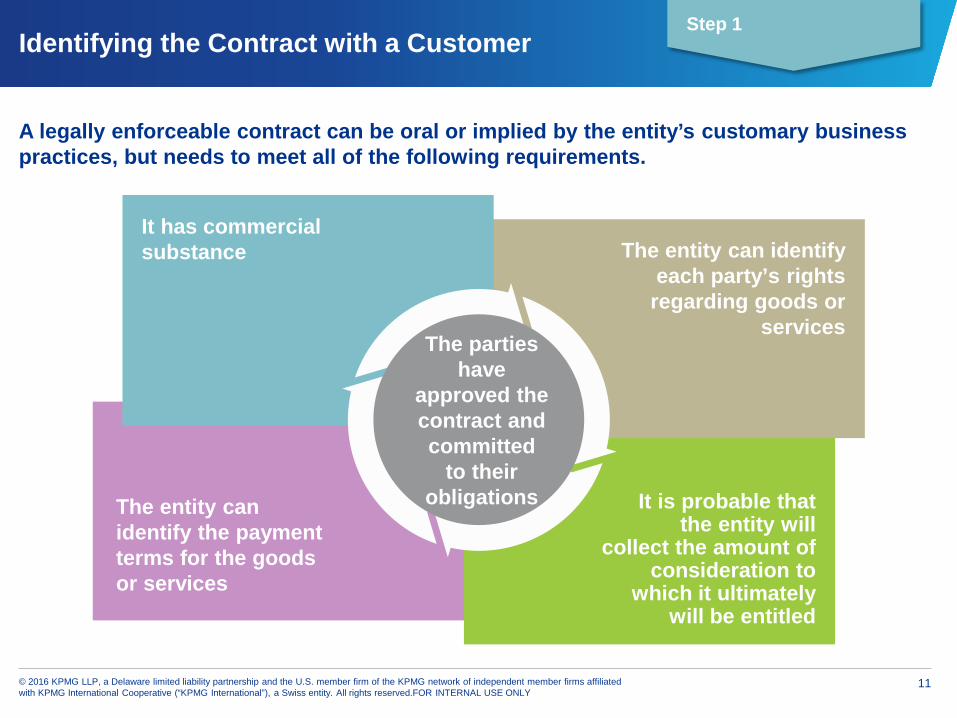

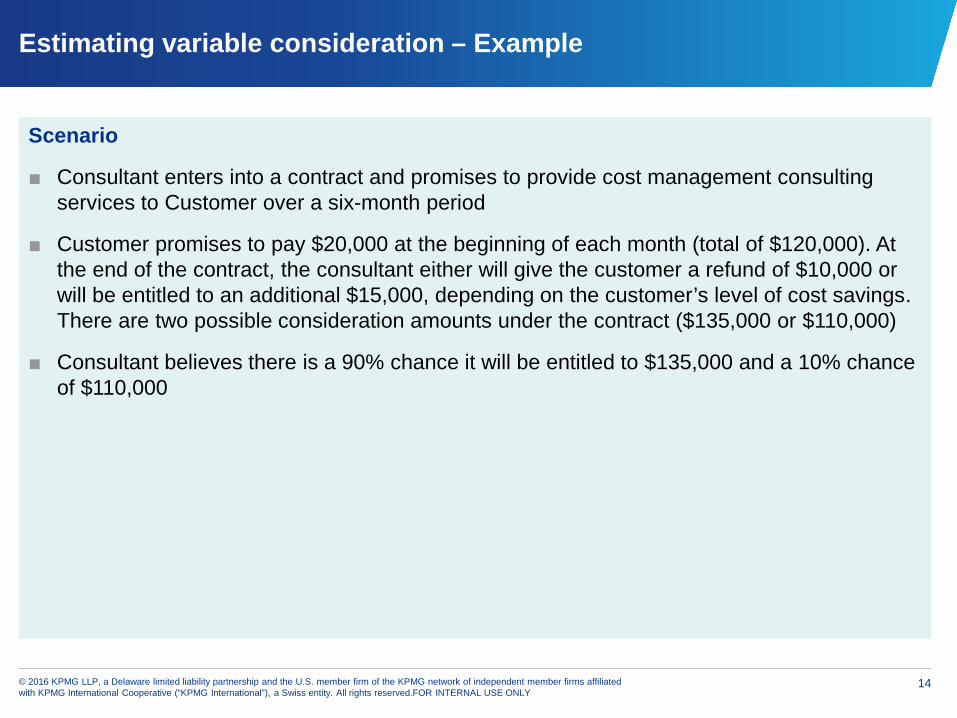

9:20-10:10 Accounting Standards Update: Revenue from Contracts with Customers Moderated by: David Antoni, Tax Managing Director, KPMG LLP Featuring: Catherine Lee, Director, Advisory, KPMG LLP Eric Lucas, Principal, Tax and Accounting Group, KPMG LLP 10:10-10:20 Break

3

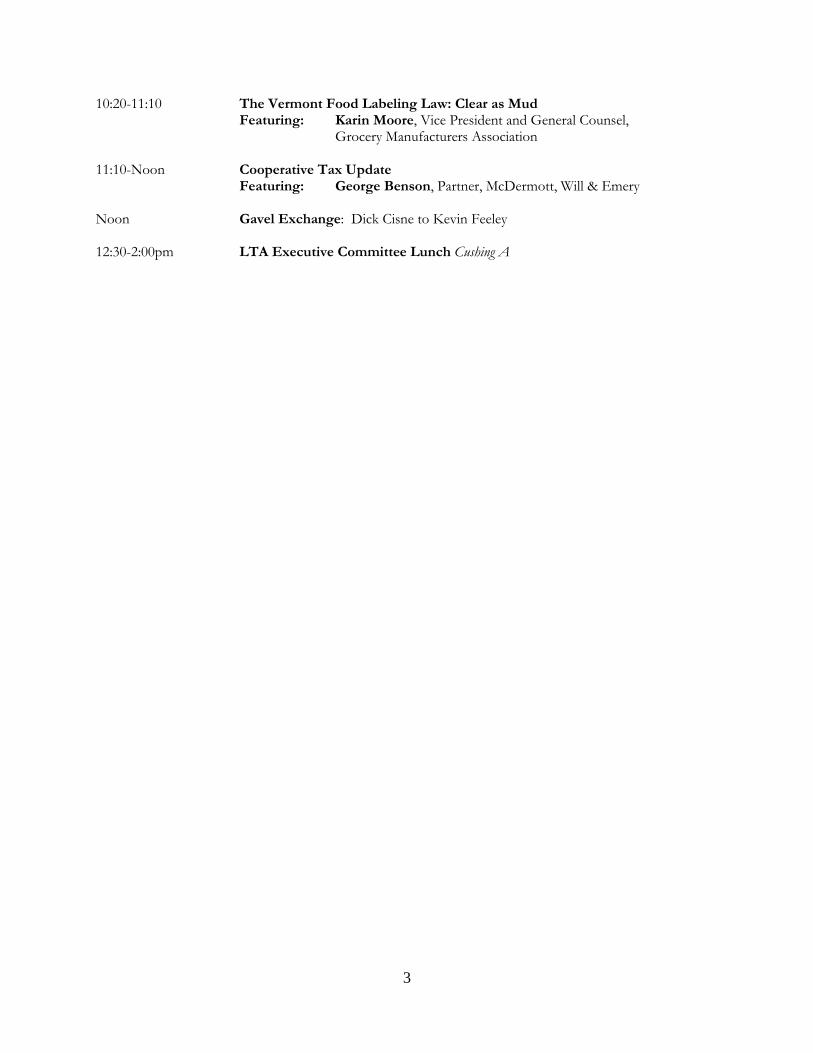

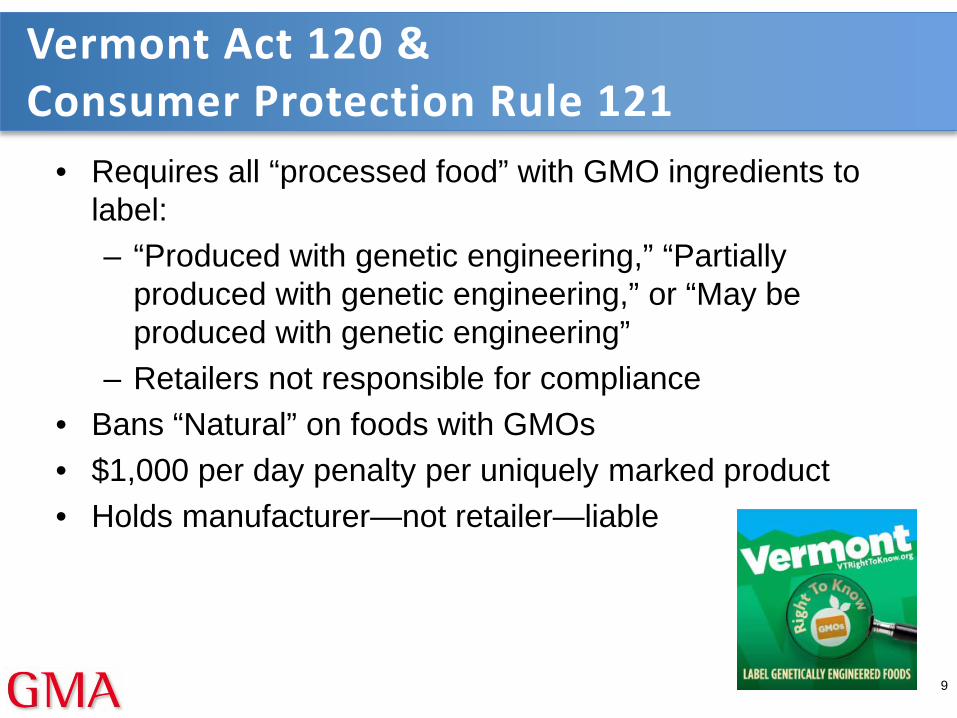

10:20-11:10 The Vermont Food Labeling Law: Clear as Mud Featuring: Karin Moore, Vice President and General Counsel, Grocery Manufacturers Association 11:10-Noon Cooperative Tax Update Featuring: George Benson, Partner, McDermott, Will & Emery Noon Gavel Exchange: Dick Cisne to Kevin Feeley 12:30-2:00pm LTA Executive Committee Lunch Cushing A

DOL and EEOC

DOL and EEOC: Staying on Top of Enhanced Enforcement Initiatives

MODERATOR BIOGRAPHY Daniel Mott Shareholder Fredrikson & Byron, P.A. Daniel Mott is a shareholder in Fredrikson & Byron’s Corporate Group and leads the firm’s Cooperative & Agribusiness Group. Dan works throughout the country with both large and small cooperatives and other businesses. Dan also advises clients on securities, tax and anti-trust issues that are unique to cooperatives and other member-owned organizations. Dan is a frequent speaker on structure and governance issues affecting cooperatives, including the use of new cooperative/LLC hybrid statutes in place in a number of states. Dan is an experienced “general counsel” and assists his clients in achieving their business objectives in the context of the increasingly complex legal environment in which businesses operate today. Dan counsels his clients by providing practical, business oriented advice that can be utilized in making decisions that have legal implications. Dan is the past chair of the Legal, Tax and Accounting Committee of the National Council of Farmer Cooperatives, and the Subcommittee on Venture Capital, Capital Formation and Financial Structures. Dan is a director and past Chairperson of the United Hospital Foundation in St. Paul and currently serves as the Chair of Innovative Quality Schools, an authorizer of public charter schools.

PRESENTER BIOGRAPHIES John Kuenstler Partner Barnes & Thornburg LLP John F. Kuenstler is a partner in the Chicago and Los Angeles offices of Barnes & Thornburg LLP and a member of the Labor and Employment Department. John dedicates his practice exclusively to the representation of employers in labor and employment and business matters. He counsels and represents a diverse client base on a national and regional basis in virtually all aspects of labor and employment law, including defense of wrongful discharge, discrimination, sexual harassment, retaliation, Title VII, ADA, ADEA, Section 1981, FMLA, FLSA, ERISA, USERRA, WARN and OSHA claims in federal and state courts and administrative agencies, as well as collective and class actions. John routinely represents management’s interests in workplace tort, breach of contract, non-compete, non-solicitation and other restrictive covenant cases. He is experienced in various forms of alternative dispute resolution, helping clients avoid the costs of prolonged legal disputes. In addition to his litigation practice, John also represents clients at all levels of administrative proceedings, including matters before the EEOC, NLRB, OSHA, and DOL. For clients with organized workforces or those striving to remain union free, John acts as the lead company negotiator for collective bargaining, defends employers in union grievance hearings and arbitrations, helps craft union avoidance campaigns, and counsels on a range of issues that can arise under the NLRA.

John has guided employers through workforce reorganizations, reductions in force, mass layoffs, plant closings, wage and hour investigations, and whistleblower claims, avoiding litigation through proactive responses and creative business strategies. He provides counseling on matters such as employment practice audits, effective human resources strategies and reviewing and drafting employment policies, social media policies, handbooks, employment contracts, independent contractor agreements, employee leasing agreements and severance agreements. To assist in effective implementation of best practices policies, John provides training and seminars to managers on all matters that impact the employment relationship. John was selected as a 2012 BTI Client All-Star by the BTI Consulting Group, Inc., being one of merely 272 lawyers nationwide to receive this recognition. He is a member of the American, Illinois, and Chicago Bar Associations, the Bar Association of Metropolitan St. Louis, and the Society for Human Resource Management. Joe Bontke Outreach Manager and Ombudsman, Houston District Office United States Equal Employment Opportunity Commission Joe Bontke is the outreach manager and ombudsman for the Houston District office of U.S. Equal Employment Opportunity Commission. Joe has been in the field of Human Resources & Civil Rights for the past 27 years and has experience in employment law and adult education. With a Bachelor's in Philosophy and a Masters in Education, he has been a Human Resources Director, a Training Coordinator for the American Disabilities Act (ADA) Technical Assistance Center for Federal Region VI, was appointed as Assistant Professor at Baylor College of Medicine and recently has been named Chair of the Governors’ Committee for People with Disabilities by Governor Rick Perry. Using his entertaining style, Joe has educated groups throughout the country and most recently, his work at the EEOC has enabled him to empower employers and employees with the understanding they need to work effectively at their jobs. Joe's philosophy of education is - that 90% is knowing where to find the information ... when you need it.

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

How to Avoid FLSA Lawsuits DOL Notice of Proposed Rulemaking DOL Guidance on Independent Contractors February 11, 2016

John F. Kuenstler (312) 338-5924 [email protected]

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

Wage and Hour Lawsuits • Wage and Hour Lawsuits are on the rise; why? Because

there is significant money to be made by plaintiffs’ attorneys

• Damages for Wage and Hour lawsuits are greater than damages for discrimination cases because the lawyer typically represents more than one plaintiff (class actions); availability of unlimited double damages; and damages are limited in discrimination suits

• Federal and state governments focus on this issue • Wage and Hour lawsuits can be brought under the

federal Fair Labor Standards Act (“FLSA”) or based on state wage and hour laws

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

FLSA Lawsuits • What leads to FLSA lawsuits?

– Misclassification of employees as exempt from overtime

– Requiring/allowing off the clock work (running errands, getting supplies, working before clocking in, or working after clocking out including checking e-mail)

– Bad recordkeeping – These are all things an employer can fix and avoid

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

FAIR LABOR STANDARDS ACT

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

This Sounds Easy, Right?

• Federal law governing the payment of minimum & overtime wages.

• Covered, non-exempt employees must receive one and one-half his/her regular rate of pay for all hours worked over 40 in a workweek.

• Compliance is determined by workweek and each workweek stands by itself (7 consecutive 24 hour periods --168 hours).

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

AS IF THIS IS NOT ENOUGH! TWO POSSIBLE HAZARDS THAT LIE AHEAD

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

PROPOSED CHANGES TO WHITE COLLAR EXEMPTIONS

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

June 30, 2015: Proposal • Proposed changes to white collar

exemptions by focusing on salary threshold

• According to DOL Secretary Thomas Perez: “employers have a range of options in terms of how to comply. That’s why it’s difficult to predict with precision what the economic effects will be.”

• DOL has made staggering prediction: “We believe, given our study of the literature that, on an annual basis, workers will get roughly $1.2 to $1.3 billion in additional wages as a result of this rule.”

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

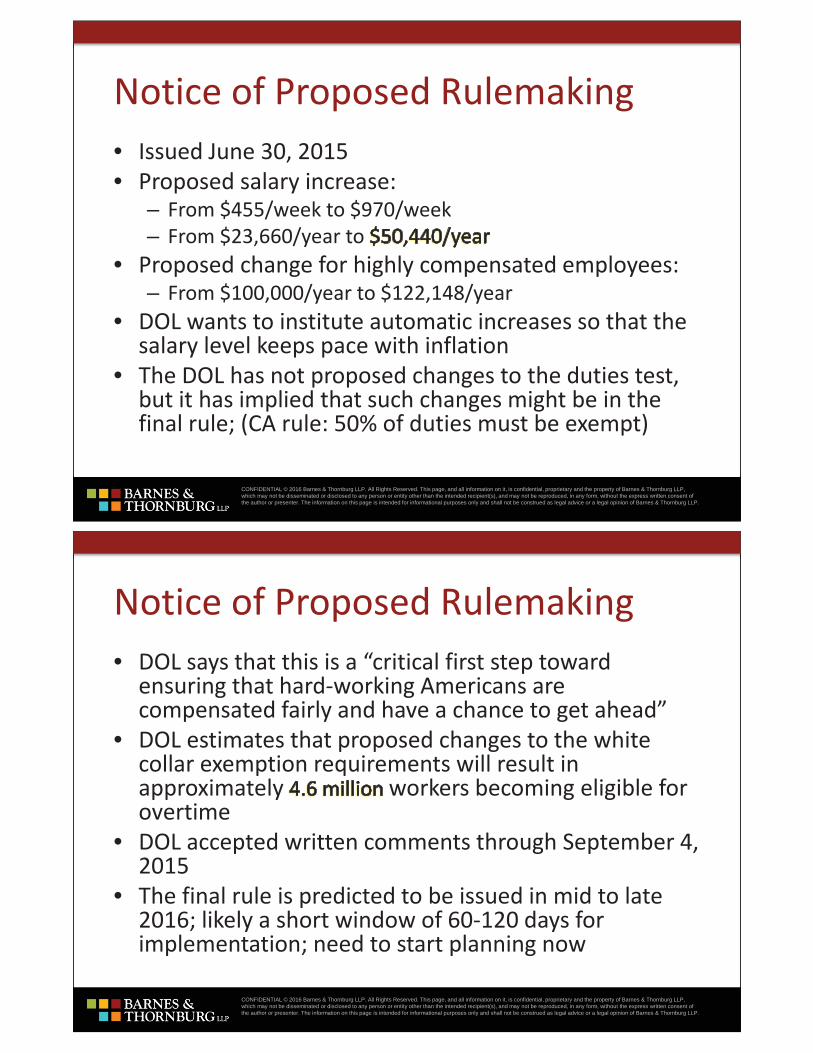

Notice of Proposed Rulemaking • Issued June 30, 2015 • Proposed salary increase:

– From $455/week to $970/week – From $23,660/year to

• Proposed change for highly compensated employees: – From $100,000/year to $122,148/year

• DOL wants to institute automatic increases so that the salary level keeps pace with inflation

• The DOL has not proposed changes to the duties test, but it has implied that such changes might be in the final rule; (CA rule: 50% of duties must be exempt)

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

Notice of Proposed Rulemaking • DOL says that this is a “critical first step toward

ensuring that hard-working Americans are compensated fairly and have a chance to get ahead”

• DOL estimates that proposed changes to the white collar exemption requirements will result in approximately workers becoming eligible for overtime

• DOL accepted written comments through September 4, 2015

• The final rule is predicted to be issued in mid to late 2016; likely a short window of 60-120 days for implementation; need to start planning now

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

SO WHAT THE HECK ARE “WHITE COLLAR EXEMPTIONS” ANYWAY?

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

White Collar Exemptions • The most common FLSA minimum wage and OT

exemption is the “White Collar” exemption that applies to certain job classifications: – Executive Employees; – Administrative Employees; – Professional Employees; – Outside Sales Employees; – Computer-related Employees; and – Highly-Compensated Employees.

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

White Collar Exemptions • Three tests for white collar exemption:

– Salary Level Test – Salary Basis Test – Job Duties Test – Why are these important; failure to comply results in liability

which can be significant

• Salary Level Test – For most employees, the minimum salary level required for

the exemption is $455/week (proposed increase to $970/week)

– Annual equivalent: $23,660 (proposed increase to $50,440)

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

White Collar Exemptions • Salary Basis Test

– Regularly receives a predetermined amount of compensation each pay period (on a weekly or less frequent basis).

– The compensation cannot be reduced because of variations in the quality or quantity of the work performed.

– Must be paid the full salary for any week in which the employee performs any work.

– Need not be paid for any workweek in which no work is performed. – An employee is not paid on a salary basis if deductions from the

predetermined salary are made for absences occasioned by the employer or by the operating requirements of the business.

– If the employee is ready, willing and able to work, deductions may not be made for time when work is not available.

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

White Collar Exemptions • Job Duties Test – Executive Duties

– Primary duty is management of the enterprise (or a customarily-recognized department or subdivision);

– Customarily and regularly directs the work of two or more other full-time employees; and

– Has the authority to hire or fire other employees (or, at least, the recommendations that the “executive” makes as to hiring, firing, advancement, promotion or other change of status must be given particular weight).

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

White Collar Exemptions • Job Duties Test – Administrative Duties

– Primary duty is the performance of office or non-manual work directly related to the management or general business operations of the employer or the employer’s customers; and

– Primary duty includes the exercise of discretion and independent judgment with respect to matters of significance.

– This is the most difficult test

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

White Collar Exemptions • Examples of Administrative Exempt Employees

include the Following: – Insurance claims adjusters – Financial services industry employees – Team Leaders – if the team is tasked with completing

major projects for employer – Executive/Administrative Assistant – if the employee has

authority over matters of significance, without prescribed instructions or procedures (higher level duties, not just clerical)

– HR Managers – Office Managers

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

White Collar Exemptions • Job Duties Test – Professional Job Duties

– Primary duty is the performance of work requiring knowledge of an advanced type in a field of science or learning customarily acquired by a prolonged course of specialized intellectual instruction.

– Primary duty is the performance of work requiring invention, imagination, originality, or talent in a recognized field of artistic or creative endeavor.

• Predominately intellectual in character. • Includes work requiring the consistent exercise of discretion and

judgment. • The advanced knowledge is generally used to analyze, interpret or

make deductions from varying facts or circumstances. • Not work involving routine mental, manual, mechanical, or physical

work.

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

“White Collar Exemptions” • Occupations with recognized professional status include the

following: – Doctors; – Registered Nurses; – Lawyers; – Teachers; – Accountants; – Pharmacists; – Engineers; – Actuaries; – Chefs; – Certified Athletic Trainers; and – Licensed Funeral Directors or Embalmers.

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

“White Collar Exemptions” • Highly Compensated Employees defined as

follows: – Receives total annual compensation of at least

$100,000; proposed increase to $122,148 with upward adjustments for inflation

– Receives at least $455 per week on a salary or fee basis; proposed increase to $970/week

– Performs office or non-manual work; and – Customarily and regularly performs any one or more

of the exempt duties identified in the standard tests for the executive, administrative or professional exemptions.

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

Planning for Proposed Changes to White Collar Exemption Requirements • Employers will face many complicated issues

as a result of the proposed changes • Employers should be considering these issues

now because of the impact they will have on budget, operations, staffing, and resources

• Employers should plan as much as possible, but do not make any final decisions until the final rule is announced

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

Auditing Exempt and Non-Exempt Positions • Employers should seriously consider conducting an

audit of all job classifications • Determine whether audit will be conducted under the

attorney-client privilege • Does the position meet the current duties test? • If not, will this rulemaking be good “cover” for

reclassification? • Are there currently exempt employees who earn less

than the new salary level in the proposed rule? • Are there positions with employees both above and

below the new salary level? If so, is it important to keep them all in the same classification?

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

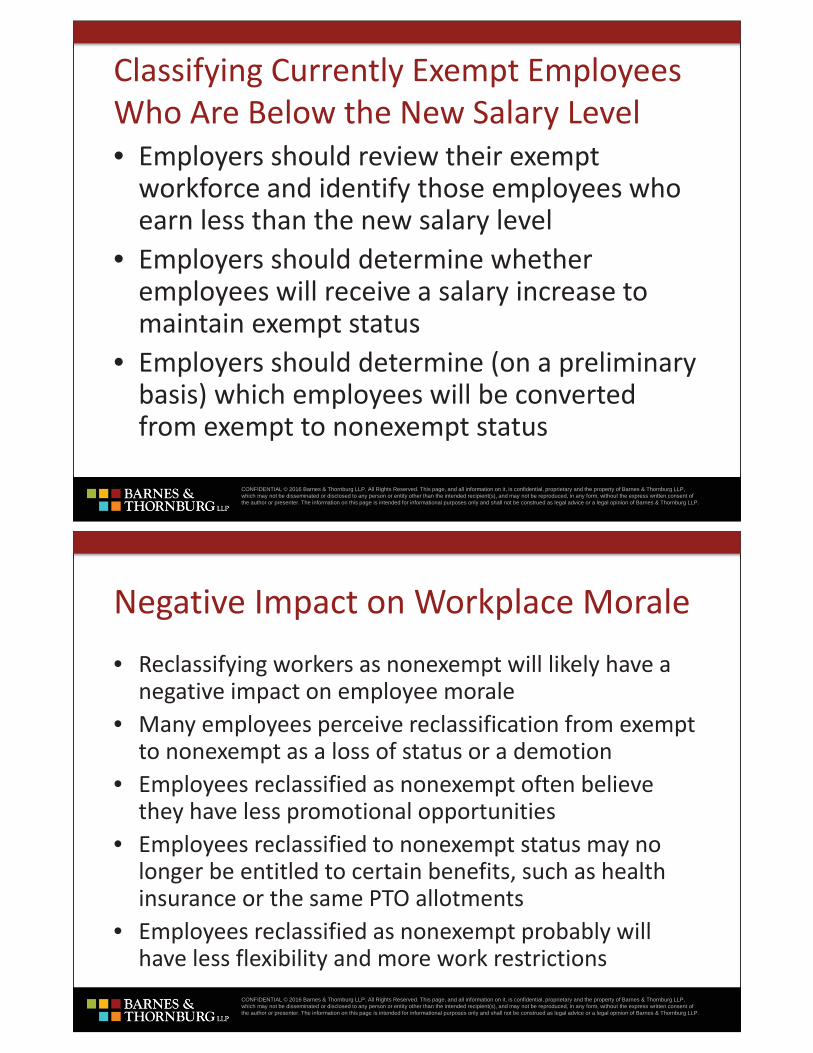

Classifying Currently Exempt Employees Who Are Below the New Salary Level • Employers should review their exempt

workforce and identify those employees who earn less than the new salary level

• Employers should determine whether employees will receive a salary increase to maintain exempt status

• Employers should determine (on a preliminary basis) which employees will be converted from exempt to nonexempt status

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

Negative Impact on Workplace Morale • Reclassifying workers as nonexempt will likely have a

negative impact on employee morale • Many employees perceive reclassification from exempt

to nonexempt as a loss of status or a demotion • Employees reclassified as nonexempt often believe

they have less promotional opportunities • Employees reclassified to nonexempt status may no

longer be entitled to certain benefits, such as health insurance or the same PTO allotments

• Employees reclassified as nonexempt probably will have less flexibility and more work restrictions

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

DEPARTMENT OF LABOR’S NEW GUIDANCE REGARDING

MISCLASSIFICATION OF EMPLOYEES AS INDEPENDENT CONTRACTORS

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

DOL Issues New Guidance That Defines Independent Contractor • Use of independent contractors is on the rise; one reason is

to avoid the Affordable Care Act • DOL issued Administrator’s Interpretation on July 15, 2015

regarding identification of employees who are misclassified as independent contractors

• It narrows the classification of independent contractors • It states that most workers in the U.S. are employees, not

independent contractors, and are covered under the FLSA • Enforcement in this area will increase • Why is this important; impact on state and federal budgets

through lower Social Security, Medicare and unemployment fund contributions, this is a strong message by the DOL

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

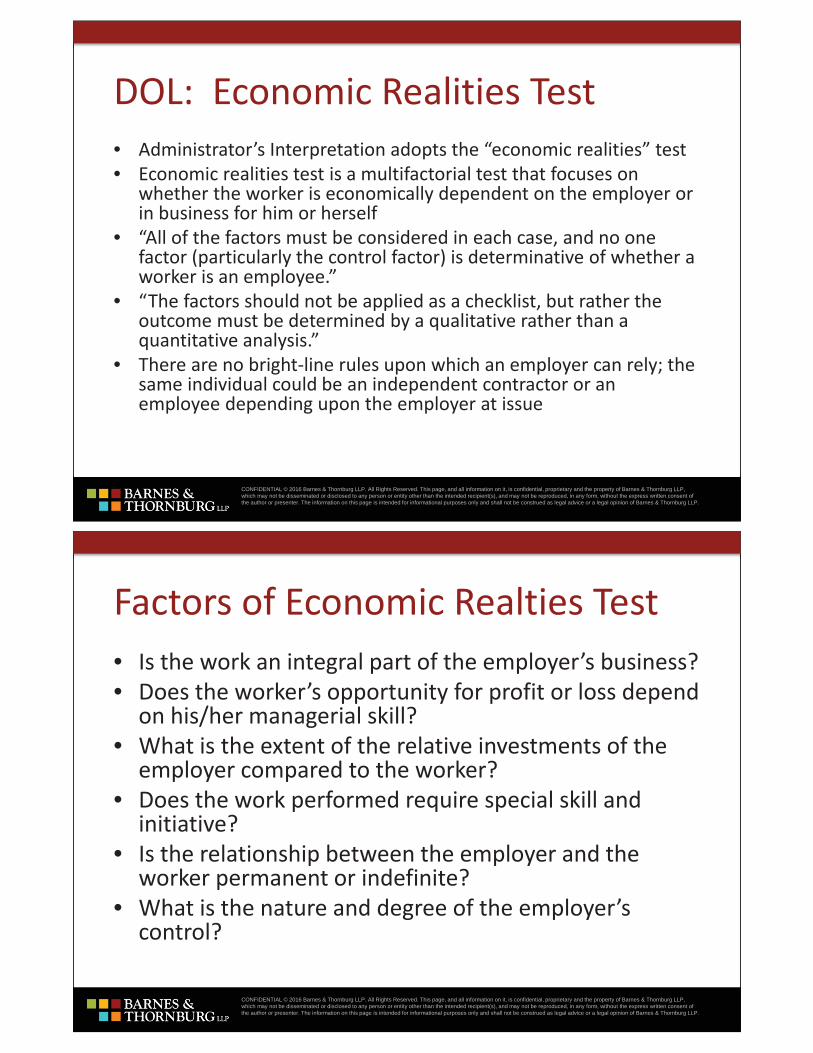

DOL: Economic Realities Test • Administrator’s Interpretation adopts the “economic realities” test • Economic realities test is a multifactorial test that focuses on

whether the worker is economically dependent on the employer or in business for him or herself

• “All of the factors must be considered in each case, and no one factor (particularly the control factor) is determinative of whether a worker is an employee.”

• “The factors should not be applied as a checklist, but rather the outcome must be determined by a qualitative rather than a quantitative analysis.”

• There are no bright-line rules upon which an employer can rely; the same individual could be an independent contractor or an employee depending upon the employer at issue

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

Factors of Economic Realties Test • Is the work an integral part of the employer’s business? • Does the worker’s opportunity for profit or loss depend

on his/her managerial skill? • What is the extent of the relative investments of the

employer compared to the worker? • Does the work performed require special skill and

initiative? • Is the relationship between the employer and the

worker permanent or indefinite? • What is the nature and degree of the employer’s

control?

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

Suggestions and Key Takeaways • Audit current independent contractor relationships; are they really

employees; look for high risk situations • Maintain records on the independent contractor determination

process (business licenses, business cards, contractor tax records, project plans, correspondence, and other supporting records)

• Carefully review the nature of work to be performed before engaging the services of any non-employee; who will truly exercise control; evaluate worker independence

• Remember that entering into an independent contractor agreement or hiring a business entity does not necessarily protect you from liability; pay a LLC rather than an individual

• When entering into agreements with service providers, obtain the appropriate indemnification provisions

• Use independent contractors sparingly

CONFIDENTIAL © 2016 Barnes & Thornburg LLP. All Rights Reserved. This page, and all information on it, is confidential, proprietary and the property of Barnes & Thornburg LLP, which may not be disseminated or disclosed to any person or entity other than the intended recipient(s), and may not be reproduced, in any form, without the express written consent of the author or presenter. The information on this page is intended for informational purposes only and shall not be construed as legal advice or a legal opinion of Barnes & Thornburg LLP.

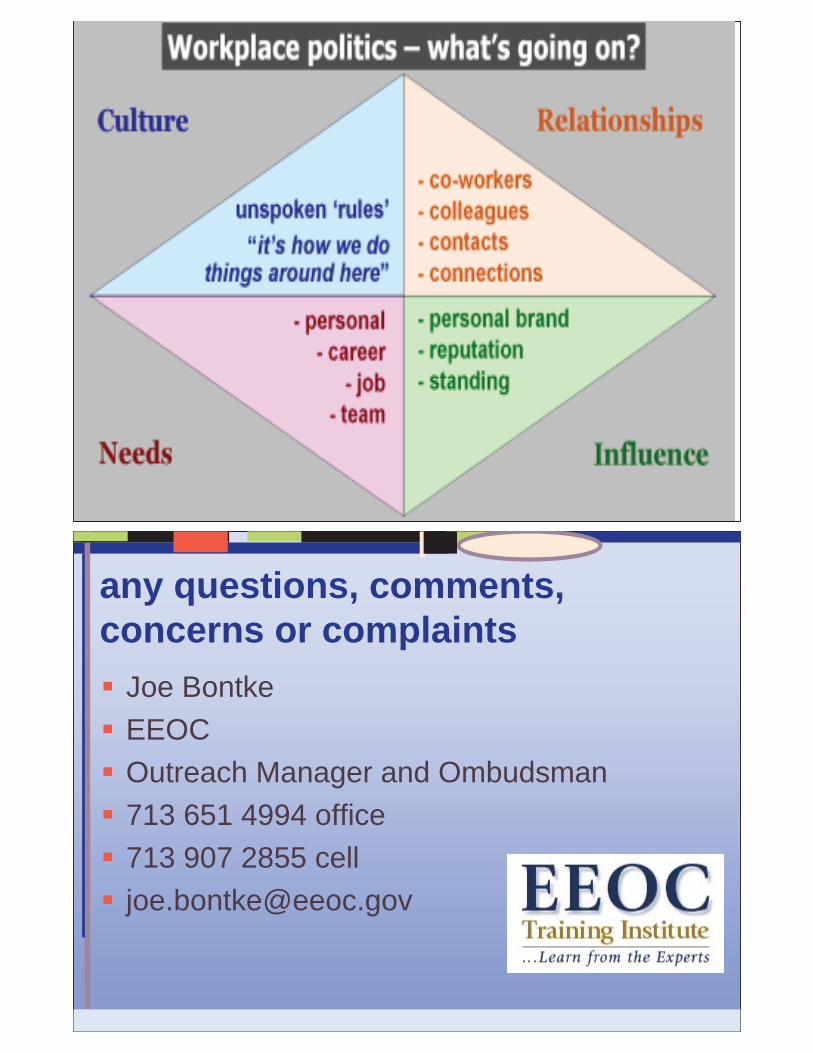

What’s new at the EEOC for 2016 & why you should care

Joe Bontke

713 651 4994 office [email protected]

We’ve Been BusyEEOC Select Taskforce on the Study of Harassment in the WorkplaceBacklash against employees who are Muslim or are perceived to be MuslimGender stereotyping/Gender identify/Sexual orientationArrest and conviction recordsPregnancy discrimination

Young v. UPSADA and pregnancy

Caregiver discriminationNew Technology

Employer portalStrategic plan (Farm worker outreach)

January 14, 2015: The Commission met to discuss why WORKPLACE HARASSMENTis still a major problem – 30% of all charges

receivedby EEOC – and how to address it.

EEOC Select Task Force on the Study of Harassment in the Workplace

EEOC Select Task Force on the Study of Harassment in the Workplace

Led by Commissioners Chai Feldblum and Victoria LipnicPurpose is to study the pervasive issue of harassment in the workplace and suggest tools employers can use for addressing it.Some observations:

Prevention starts at the top – Organizational CultureIf the issue is important to the boss, it will be important to everyone elseStudies show organizational conditions, rather than characteristics of individuals, are biggest indicators of the prevalence of harassment in the workplace (organizational tolerance)

TrainingMandatory and periodic

EEOC Select Task Force on the Study of Harassment in the Workplace

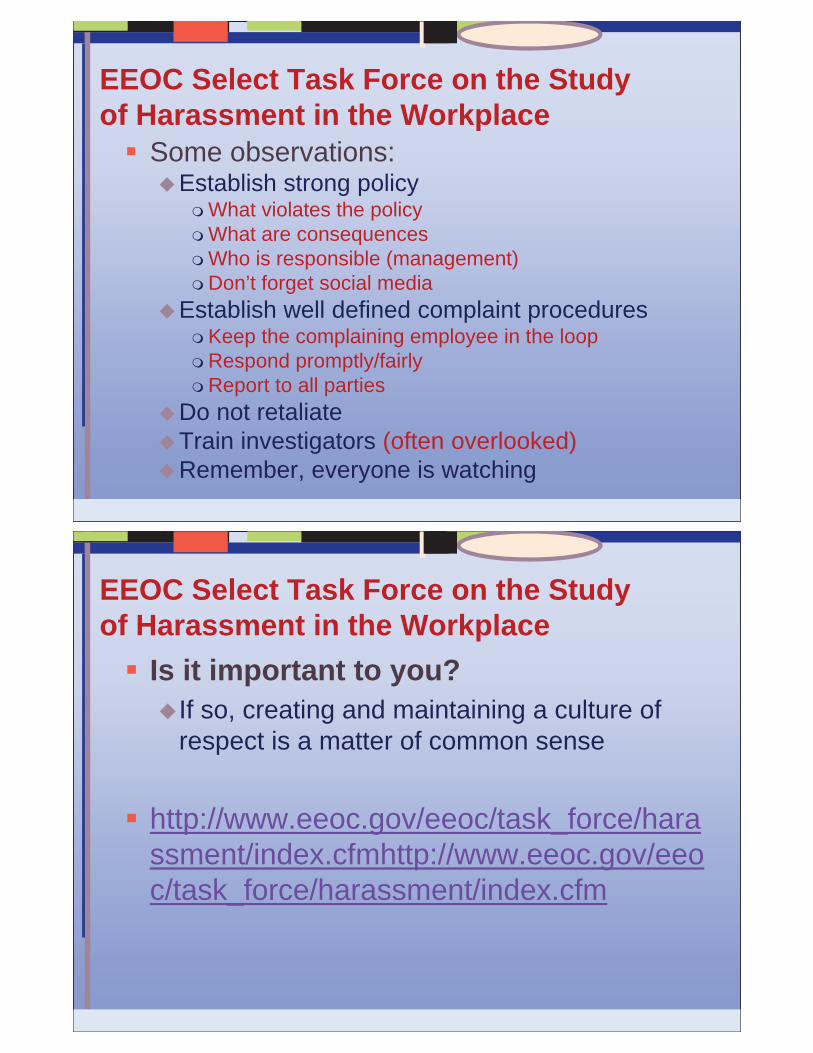

Some observations:Establish strong policy

What violates the policyWhat are consequencesWho is responsible (management)Don’t forget social media

Establish well defined complaint proceduresKeep the complaining employee in the loopRespond promptly/fairlyReport to all parties

Do not retaliateTrain investigators (often overlooked)Remember, everyone is watching

EEOC Select Task Force on the Study of Harassment in the Workplace

Is it important to you?If so, creating and maintaining a culture of respect is a matter of common sense

http://www.eeoc.gov/eeoc/task_force/harassment/index.cfmhttp://www.eeoc.gov/eeoc/task_force/harassment/index.cfm

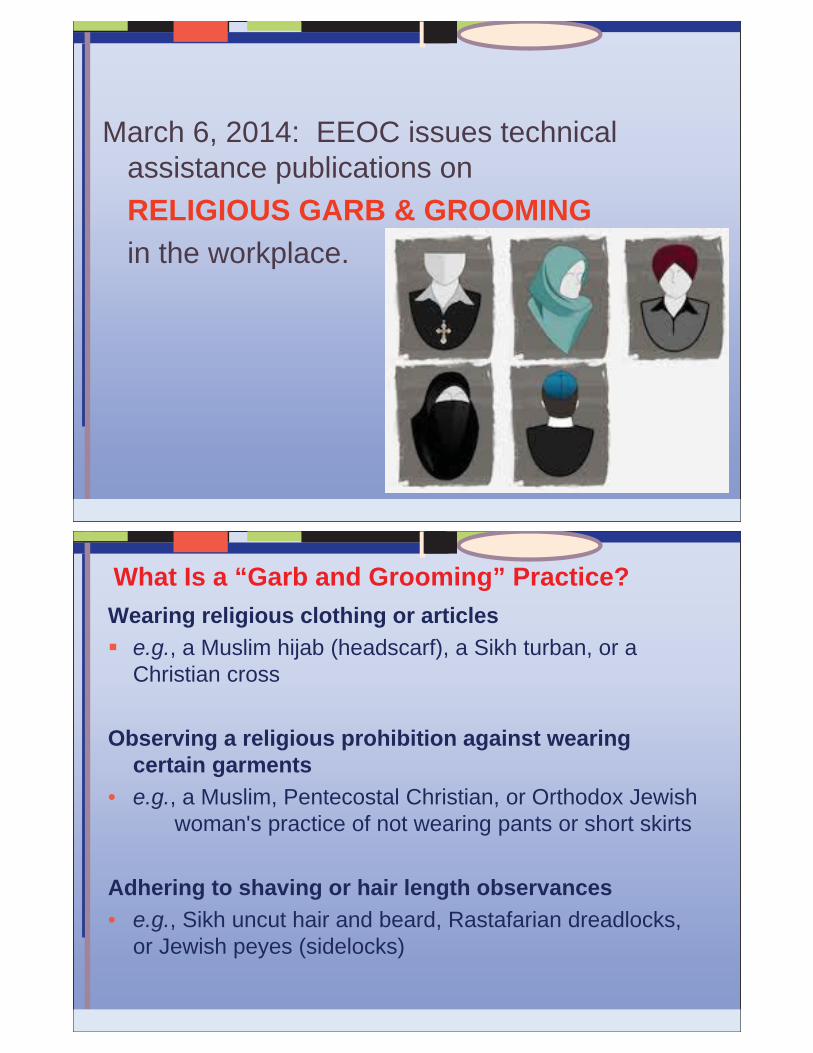

March 6, 2014: EEOC issues technical assistance publications on RELIGIOUS GARB & GROOMING in the workplace.

What Is a “Garb and Grooming” Practice?Wearing religious clothing or articles

e.g., a Muslim hijab (headscarf), a Sikh turban, or a Christian cross

Observing a religious prohibition against wearing certain garments

• e.g., a Muslim, Pentecostal Christian, or Orthodox Jewish woman's practice of not wearing pants or short skirts

Adhering to shaving or hair length observances • e.g., Sikh uncut hair and beard, Rastafarian dreadlocks,

or Jewish peyes (sidelocks)

Backlash DiscriminationFrom 9/11/01 to 9/30/15

EEOC took 9679 charges alleging discrimination Religion –MuslimNearly 4X’s the number of Religion – Muslim charges filed 11 years prior to 9/11

From 9/11/01 to 9/30/15EEOC took 1054 charges alleging backlash discrimination –MuslimApproximately 24% have been closed as “merit resolutions” (finding of discrimination, settlement, withdrawal with benefits)

Texas has 2nd highest number of backlash charges (142)

Religion DiscriminationWhen religion issues go bad in the workplace, they can go very bad, very quicklyBe proactiveEstablish a culture where all beliefs are respected

Our beliefs define us They usually cannot be negotiated or reasoned awayTitle VII balances the individual’s right to free exercise of her or his religious beliefs and the employer’s right to run its organization as it chooses.

Shows up in:ExpressionHarassmentDiscriminationReasonable accommodations

Respond to issues or complaints quickly and fairly

Gender Stereotyping Gender IdentitySexual Orientation

The decision is pretty unambiguous.See page 6, 1st paragraph,

"We conclude that sexual orientation is inherently a sex-based consideration, and an allegation of discrimination based on sexual orientation is necessarily an allegation of sex discrimination under Title VII."

Gender Stereotyping

In Price Waterhouse v Hopkins, 490 U.S. 228 (1989), the Supreme Court found that acting within the context of sex stereotyping is acting on the basis of gender.

Ann Hopkins was denied a partnership at the accounting firm; comments made by decision makers were that she was “macho,” should “take a course in charm school,” and should “walk more femininely, talk more femininely, dress more femininely, wear make-up, have her hair styled, and wear jewelry.”

Gender Stereotyping & Gender Identity“When an employer discriminates against someone because the person is transgender, the employer has engaged in disparate treatment related to the sex of the victim….This is true regardless of whether an employer discriminates against an employee because the individual has expressed his or her gender in a non-stereotypical fashion, because theemployer is uncomfortable with the fact that the person has transitioned or is in the process of transitioning from one gender to another, or because the employer simply does not like that the person is identifying as a transgender person. In each of these circumstances, the employer is making a gender-based evaluation, thus violating [Price Waterhouse’s] admonition that an employer may not take gender into account in making an employment decision.’” Macy v Dept of Justice (April 20, 2012)

Arrest & Conviction Records

Background ChecksWhy is the Commission interested in this?

Using blanket policies to exclude applicants for employment based on conviction records, arrest records and credit checks may adversely impact certain protected groupsReports contain errors

Disparate TreatmentDon’t deviate from the policy because an applicant is in a certain protected group

Adverse Impact:Griggs v Duke Power Company (1971)Neutral policyAdverse impactJob related and consistent with business necessity

Background ChecksTwo circumstances employers will meet “job relatedness and consistent with business necessity”

The employer validates the criminal conduct screen for the position in question per the Uniform Guidelines on Employee Selection Procedures (Uniform Guidelines) standards (if data about criminal conduct as related to subsequent work performance is available and such validation is possible);The employer develops a targeted screen considering at least the nature of the crime, the time elapsed, and the nature of the job (the three Green factors), and then provides an opportunity for an individualized assessment for people excluded by the screen to determine whether the policy as applied is job related and consistent with business necessity.

Background ChecksMust show job relatedness and business necessity (Green v Missouri Pacific Railroad)

The nature and gravity of the offense or conduct;The time that has passed since the offense or conduct and/or completion of the sentence; and The nature of the job held or sought.

Some level of risk is inevitable in all hiring. It’s ultimately about risk managementMust accurately distinguish between those applicants who pose an unacceptable risk and those who do not (be careful of blanket exclusions)

Background ChecksArrests

An arrest does not establish that criminal conduct has occurredFinal dispositions are often not reportedAn arrest should not be the reason for the employment decision, but the underlying conduct may be a reason, if objectively known

Background Checks (best practices)Eliminate policies or practices that exclude people from employment based on any criminal record.Train managers, hiring officials, and decision makers about Title VII and its prohibition on employment discrimination.Develop a Policy

Identify essential job requirements and the actual circumstances under which the jobs are performed. Determine the specific offenses that may demonstrate unfitness for performing such jobs. Identify the criminal offenses based on all available evidence. Determine the duration of exclusions for criminal conduct based on all available evidence. Include an individualized assessment. Record the justification for the policy and procedures.Note and keep a record of consultations and research considered in crafting the policy and procedures. Train managers, hiring officials, and decision makers on how to implement the policy and procedures consistent with Title VII.

Background Checks (best practices)Questions about Criminal Records

When asking questions about criminal records, limit inquiries to records for which exclusion would be job related for the position in question and consistent with business necessity.

ConfidentialityKeep information about applicants’ and employees’ criminal records confidential. Only use it for the purpose for which it was intended.

• Georgia (2015) • Delaware (2014) • Nebraska (2014) • Illinois (2014) • New Jersey (2014) • California (2013) • Maryland (2013) • Minnesota (2013) • Rhode Island (2013) • Colorado (2012) • Connecticut (2010) • Massachusetts (2010) • New Mexico (2010) • Hawaii (1998)

July 14, 2014: EEOC issues updated enforcement guidance on PREGNANCY DISCRIMINATION.

Pregnancy

The Pregnancy Discrimination Act (PDA)

First clause:

“The terms ‘because of sex’ or ‘on the basis of sex’ include, but are not limited to, because of or on the basis of pregnancy, childbirth, or related medical conditions”; and

42 U.S.C. § 2000e (k) (emphasis added).

PDA: “Related Medical Conditions”Examples of “related medical conditions”:

Complications requiring bed restGestational diabetesAfter-effects of C-sectionLactation – EEOC v. Houston Funding, 2013 WL 2360114 (5th Cir. 2013)

The PDA’s Second Clause“[W]omen affected by pregnancy, childbirth, or related medical conditions shall be treated the same for all employment-related purposes, including receipt of benefits under fringe benefit programs, as other persons not so affected but similar in their ability or inability to work, and nothing in section 703(h) of this title shall be interpreted to permit otherwise. . . .”

Examples of such benefits: “light duty,” leave, health insurance

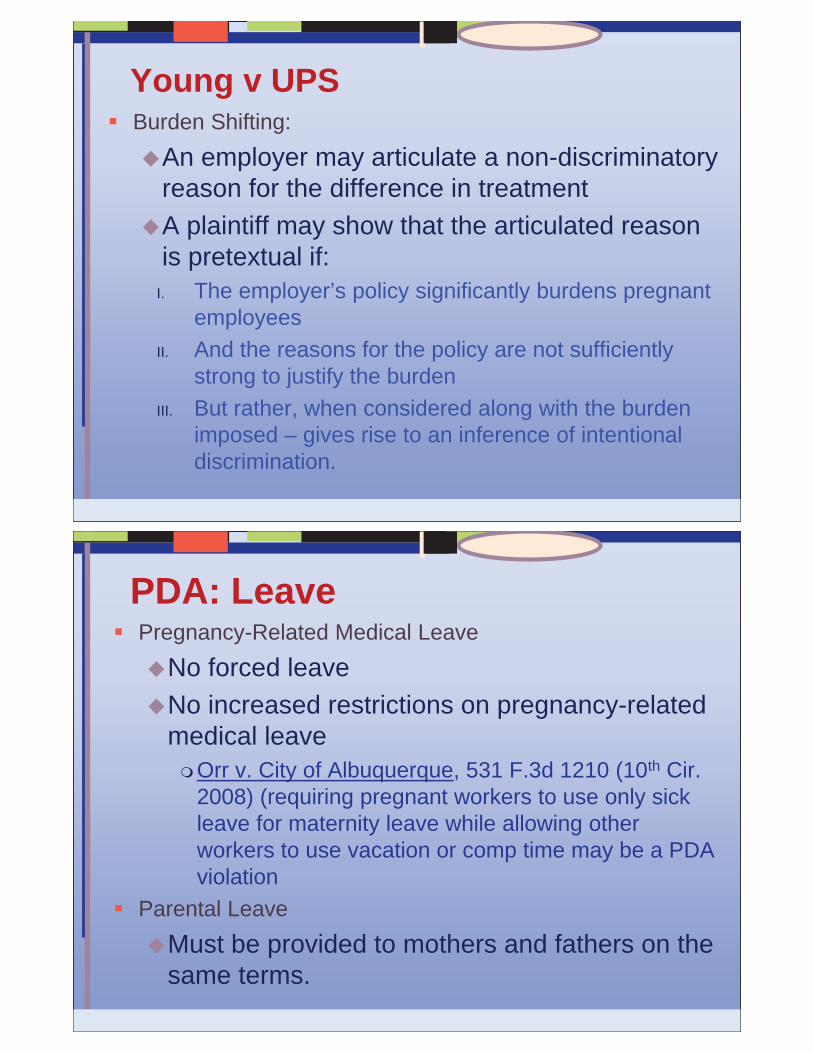

Young v UPSThe case involved a benefits policy.Young was a part time driver and became pregnantShe requested a light duty assignmentUPS denied her request based on policy that light duty assignments were given to employees who 1) were unable to perform their jobs due to on the job injuries, 2) had a disability covered under the ADA, or 3) had lost DOT certification because of a failed medical exam, a lost driver’s license, or involvement in a motor vehicle accident.

Young v UPSBurden Shifting:

An employer may articulate a non-discriminatory reason for the difference in treatmentA plaintiff may show that the articulated reason is pretextual if:

I. The employer’s policy significantly burdens pregnant employees

II. And the reasons for the policy are not sufficiently strong to justify the burden

III. But rather, when considered along with the burden imposed – gives rise to an inference of intentional discrimination.

PDA: LeavePregnancy-Related Medical Leave

No forced leaveNo increased restrictions on pregnancy-related medical leave

Orr v. City of Albuquerque, 531 F.3d 1210 (10th Cir. 2008) (requiring pregnant workers to use only sick leave for maternity leave while allowing other workers to use vacation or comp time may be a PDA violation

Parental LeaveMust be provided to mothers and fathers on the same terms.

Pregnancy & the ADAAAEEOC regulations still make a distinction between “normal” pregnancies and those with complications.See EEOC’s Questions and Answers on the Final Rule Implementing the Amended ADA, at Question 23, available at http://www.eeoc.gov/laws/regulations/ada_qa_final_rule.cfm

Generally, under the ADAAA’s expanded rules of construction and definitions, many more pregnancy-related conditions now may qualify as “physical impairments” supporting “actual disability” and “record of such disability” claims.

For example, someone with an impairment resulting in a 20-pound lifting restriction that lasts or is expected to last for several months is substantially limited in the major life activity of lifting.

ADA: Pregnancy-Related Impairments that May Be Substantially Limiting

Pelvic inflammation – may substantially limit walkingPregnancy-related carpal tunnel – may substantially limit liftingDisorders of uterus or cervix – may substantially limit reproductive functionPregnancy-related sciatica – may substantially limit musculoskeletal functionGestational diabetes – may substantially limit endocrine functionPreeclampsia – may substantially limit cardiovascular or circulatory functions

More Pregnant Women in the Workforce

• 1961-65: 35% of first-time mothers who worked during pregnancy worked into their final month.

• Compare to 2006-08: 82% of first-time mothers who worked during pregnancy worked into their final month.

1970: Mean age at first birth was 21.4.

Compare to 2013: Mean age at first birth was 26.

2012: 41 % of all births were to single women.

CaregiverDiscrimination

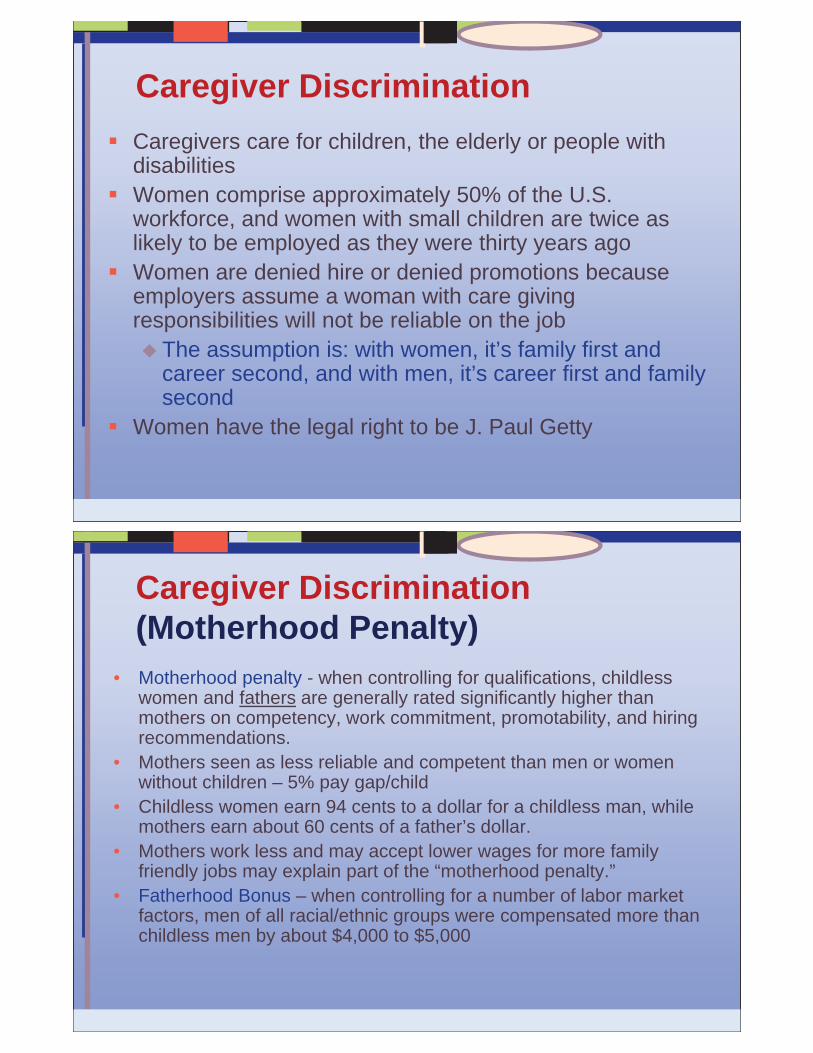

Caregiver DiscriminationCaregivers care for children, the elderly or people with disabilitiesWomen comprise approximately 50% of the U.S. workforce, and women with small children are twice as likely to be employed as they were thirty years agoWomen are denied hire or denied promotions because employers assume a woman with care giving responsibilities will not be reliable on the job

The assumption is: with women, it’s family first and career second, and with men, it’s career first and family second

Women have the legal right to be J. Paul Getty

Caregiver Discrimination (Motherhood Penalty)

• Motherhood penalty - when controlling for qualifications, childless women and fathers are generally rated significantly higher than mothers on competency, work commitment, promotability, and hiring recommendations.

• Mothers seen as less reliable and competent than men or women without children – 5% pay gap/child

• Childless women earn 94 cents to a dollar for a childless man, while mothers earn about 60 cents of a father’s dollar.

• Mothers work less and may accept lower wages for more family friendly jobs may explain part of the “motherhood penalty.”

• Fatherhood Bonus – when controlling for a number of labor market factors, men of all racial/ethnic groups were compensated more than childless men by about $4,000 to $5,000

New Technology

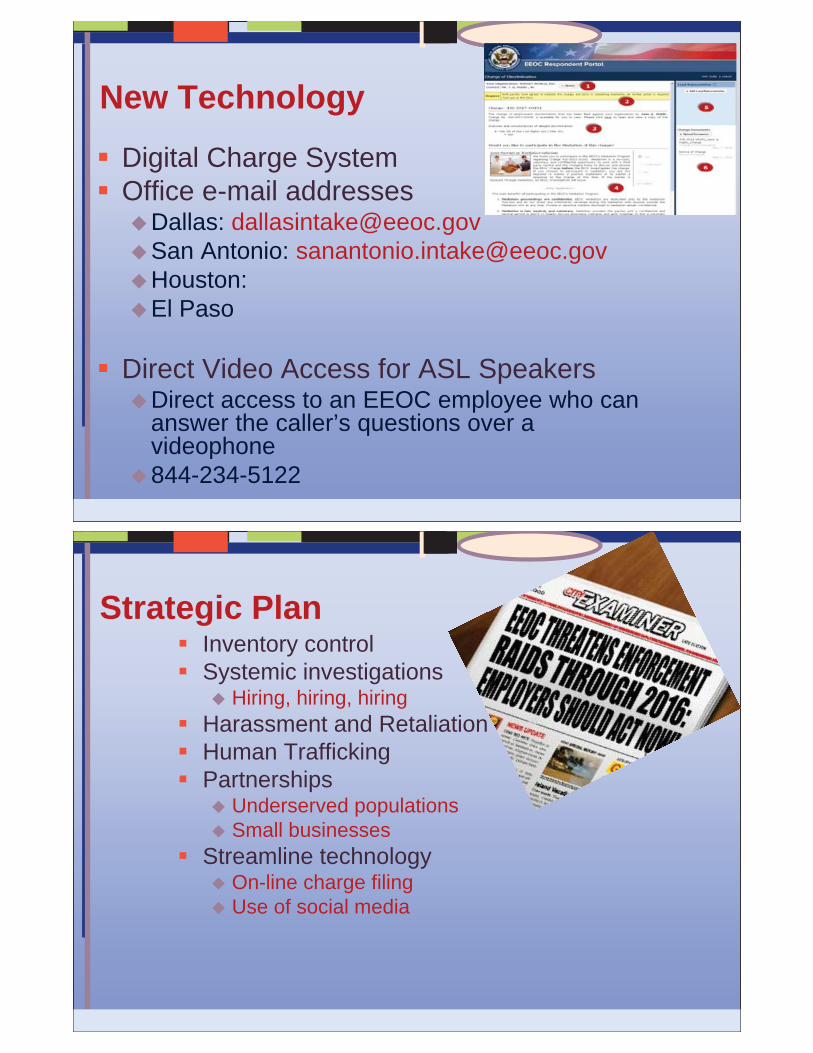

Digital Charge SystemOffice e-mail addresses

Dallas: [email protected] Antonio: [email protected]: El Paso

Direct Video Access for ASL SpeakersDirect access to an EEOC employee who can answer the caller’s questions over a videophone844-234-5122

Strategic PlanInventory controlSystemic investigations

Hiring, hiring, hiringHarassment and RetaliationHuman TraffickingPartnerships

Underserved populationsSmall businesses

Streamline technologyOn-line charge filingUse of social media

Strategic Enforcement Plan

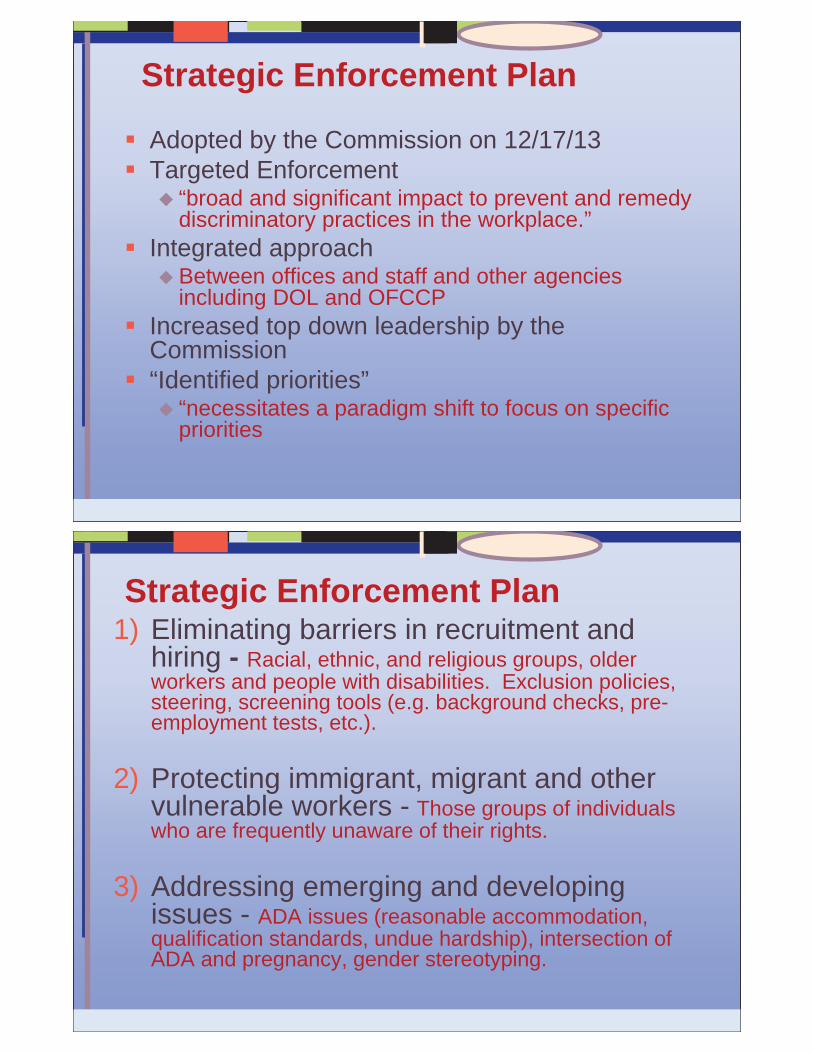

Adopted by the Commission on 12/17/13Targeted Enforcement

“broad and significant impact to prevent and remedy discriminatory practices in the workplace.”

Integrated approachBetween offices and staff and other agencies including DOL and OFCCP

Increased top down leadership by the Commission“Identified priorities”

“necessitates a paradigm shift to focus on specific priorities

Strategic Enforcement Plan1) Eliminating barriers in recruitment and

hiring - Racial, ethnic, and religious groups, older workers and people with disabilities. Exclusion policies, steering, screening tools (e.g. background checks, pre-employment tests, etc.).

2) Protecting immigrant, migrant and other vulnerable workers - Those groups of individuals who are frequently unaware of their rights.

3) Addressing emerging and developing issues - ADA issues (reasonable accommodation, qualification standards, undue hardship), intersection of ADA and pregnancy, gender stereotyping.

Intersectional Discrimination

Immigrant status – foreigner, guest worker, undocumented worker, etc.National origin, religion, race, age, etc.Socio-economic status – poverty, limited education, etc.Traditional attitudes concerning women in society in general and in work Limited English proficient – Almost half (46%) of all foreign-born workers in the U.S. are LEP. (Nearly 73% of LEP workers speak Spanish.)Domestic violence at home

Immigrant women face gender-based discrimination and other forms of “otherness” which can further disadvantage or make them vulnerable:

Population in the Fields

Every year an estimated 500,000 women work in U.S. fields.

Sexual Harassment & Farmworker Women

A study done for California State University found that more than 90% of farmworker women reported sexual harassment on the job as a major problem.

Domestic violence connection?

A 1995 survey of farmworker women conducted by the Migrant Clinicians Network found that 1 in 3 had experienced domestic violence in the last year.

Strategic Enforcement Plan4) Enforcing equal pay laws – Focus on gender,

may use directed investigations and Commissioner charges to facilitate enforcement.

5) Preserving access to the legal system –Address retaliatory actions, overly broad waivers, and settlement provisions restricting access to Commission.

6) Preventing harassment through systemic enforcement and targeted outreach – Focus on sexual harassment and harassment related to race, ethnicity, religion and age.

any questions, comments, concerns or complaints

Joe BontkeEEOCOutreach Manager and Ombudsman713 651 4994 office713 907 2855 [email protected]

The Tri-State Case

The Tri-State Case: Is a Federated Cooperative Liable for Its Members’ Actions?

PRESENTER BIOGRAPHIES

Ty Thompson Vice President & Deputy General Counsel for Director and Member Legal Services NRECA

Ty Thompson is chief member counsel for the National Rural Electric Cooperative Association in Arlington, Virginia. A native of Raleigh, North Carolina, Ty graduated magna cum laude in Industrial Engineering from North Carolina State University in 1987. After working approximately two years as an inside sales engineer in Charlotte, N.C., Ty attended the University of North Carolina School of Law in Chapel Hill and graduated in 1992.

After working briefly for a personal injury law firm in Durham, N.C., Ty practiced law four and one-half years at Crisp, Page, and Currin in Raleigh. While there, Ty worked extensively with electric cooperatives. In July 1997, Ty began working for NRECA. At NRECA, Ty works primarily with electric cooperative tax, corporate governance, and operational legal issues. In addition, Ty is an Editor for NRECA’s monthly Legal Reporting Service; presents at NRECA’s annual Legal Seminar; assists with NRECA Course 925.1, “Cooperative Bylaws: Guiding Principles and Current Issues;” researches and drafts sample electric cooperative documents like NRECA’s Bylaw Revision Guide; speaks at various conferences, seminars, and meetings regarding electric cooperative legal issues; counsels NRECA regarding corporate governance legal issues; and serves as Parliamentarian for the NRECA Board of Directors.

Jay Sturhahn Member Sherman & Howard

Jay Sturhahn is a member in Sherman & Howard’s Litigation Department. Jay represents business and individual policy-holders in disputes with their insurers, including general liability, directors and officers liability, property, builders’ risk, fidelity and surety, employer’s liability, errors and omissions, environmental, commercial auto, health, life, disability, excess/umbrella, crime, cyber risk, reinsurance and captive insurance programs. He also represents clients in general business disputes and litigation, including one of the West’s largest electricity generation and transmission cooperatives. He has represented clients across a variety of industries, including construction, energy, finance, health care, government contracting and others through the United States and internationally. Jay also represents businesses in the construction industry, assisting in claim preparation and defense on matters involving bidding, delays, defective construction or design, differing site conditions, and interference. Jay is a regular author and speaker on insurance coverage and risk avoidance issues impacting business and individuals and was recognized by Colorado Super Lawyers as a “Rising Star” in the areas of Insurance Coverage, Business Litigation and Construction Litigation.

Are a G&T and its Members a Joint Venture?

Ty Thompson, NRECA 703-907-5855, [email protected]

Jay Sturhahn, Sherman and Howard 303-297-2900, [email protected]

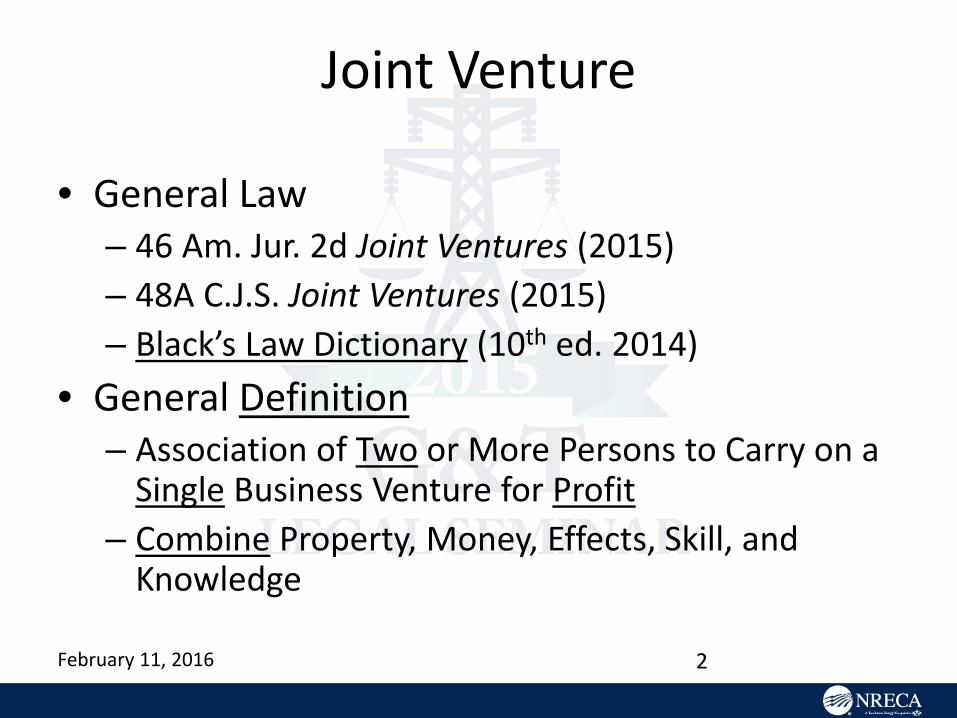

Joint Venture

• General Law – 46 Am. Jur. 2d Joint Ventures (2015) – 48A C.J.S. Joint Ventures (2015) – Black’s Law Dictionary (10th ed. 2014)

• General Definition – Association of Two or More Persons to Carry on a

Single Business Venture for Profit – Combine Property, Money, Effects, Skill, and

Knowledge

February 11, 2016 2

Joint Venture

• General Tort Liability – Members are Jointly and Severally Liable to Third

Parties for Torts Committed in Conducting Venture – Negligence of One Member Imputed to Other

Members – Members are Vicariously Liable for One Another’s

Negligence

February 11, 2016 3

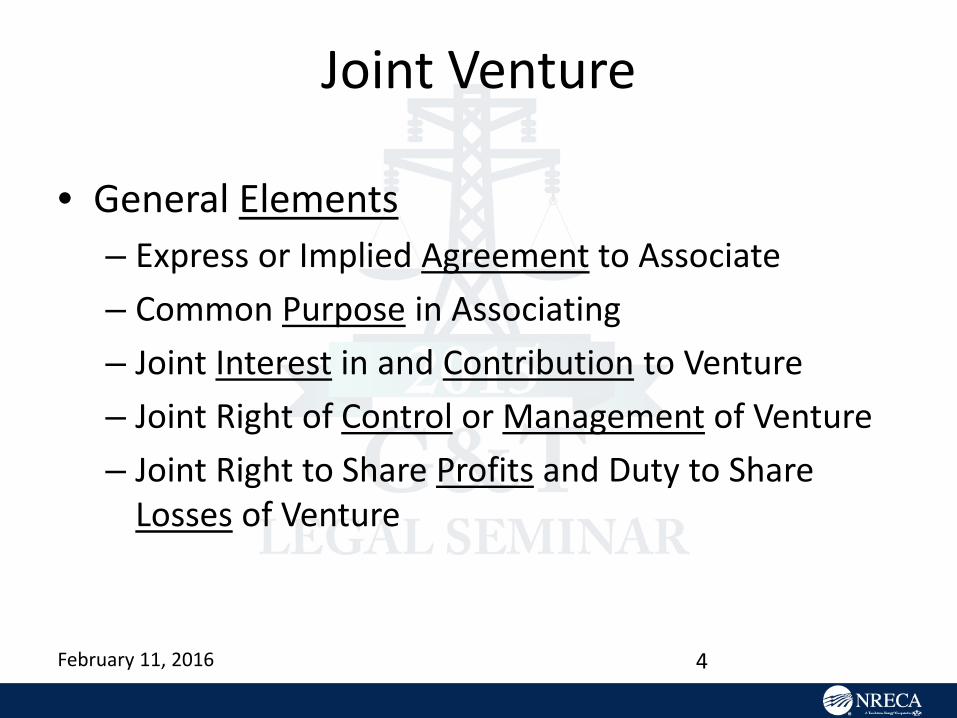

Joint Venture

• General Elements – Express or Implied Agreement to Associate – Common Purpose in Associating – Joint Interest in and Contribution to Venture – Joint Right of Control or Management of Venture – Joint Right to Share Profits and Duty to Share

Losses of Venture

February 11, 2016 4

Las Conchas Fire Litigation

• Las Conchas Fire (June 2011) – Santa Fe National Forest (New Mexico) – More than 150,000 Acres Burned – No Deaths – Smog, Soot, Property, Etc. Damage

• Danger Tree Located Outside Easement Struck Electric Distribution Line

• Property Insurers, Property Owners, and Pueblos Sued (January 2014 – First Amended Complaint) – Jemez Mountains Electric Cooperative (“JMEC”) – Tri-State Generation and Transmission Association (“TS”)

February 11, 2016 5

Las Conchas Fire Litigation

• Many Allegations, Including JMEC and TS are Joint Venture or Single Enterprise – TS Vicariously Liable for JMEC

• TS Controls JMEC – TS Bylaws and Policies

• Wholesale Power Contract • TS and JMEC Share Profits (Capital Credits)

February 11, 2016 6

Shoshone River Power, Inc.

• Tri-State Generation and Transmission Association v. Shoshone River Power, Inc., 874 F.2d 1346 (10th Cir. 1989) – United States Court of Appeals for the Tenth Circuit – Wholesale Power Contract Case

• “Shoshone’s participation in the Tri-State cooperative system and its interrelationship with Tri-State and the other members of the Tri-State system make the parties’ contractual relationship a unique one.”

February 11, 2016 7

Shoshone River Power, Inc.

• “The all-requirements contracts which form the Tri-State system are not simple requirements contracts but rather interdependent, joint and mutual contracts with a common purpose of securing the REA loans and thereby effectuating the REA policy to provide the economic means for supplying electricity to rural areas.”

• “The contracts also allow the entire system to be viewed as a whole, combining the members’ financial strength and increasing their ability to obtain funds, through Tri-State, to build facilities and obtain power in an attempt to meet the members’ actual and projected power needs.”

February 11, 2016 8

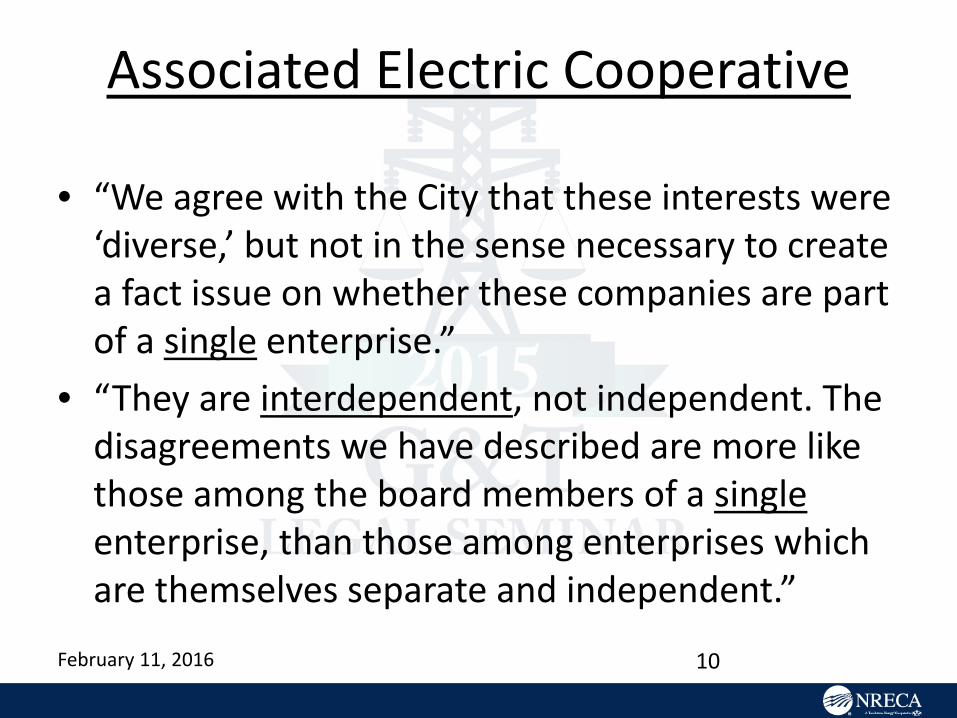

Associated Electric Cooperative

• City of Mt. Pleasant v. Associated Electric Cooperative, 838 F.2d 268 (8th Cir. 1988) – United States Court of Appeals for the Eighth Circuit – Federal Antitrust Case

• “The record bears out defendants’ claim that the cooperative organization is a single enterprise pursuing a common goal -- the provision of low-cost electricity to its rural consumer-members.”

February 11, 2016 9

Associated Electric Cooperative

• “We agree with the City that these interests were ‘diverse,’ but not in the sense necessary to create a fact issue on whether these companies are part of a single enterprise.”

• “They are interdependent, not independent. The disagreements we have described are more like those among the board members of a single enterprise, than those among enterprises which are themselves separate and independent.”

February 11, 2016 10

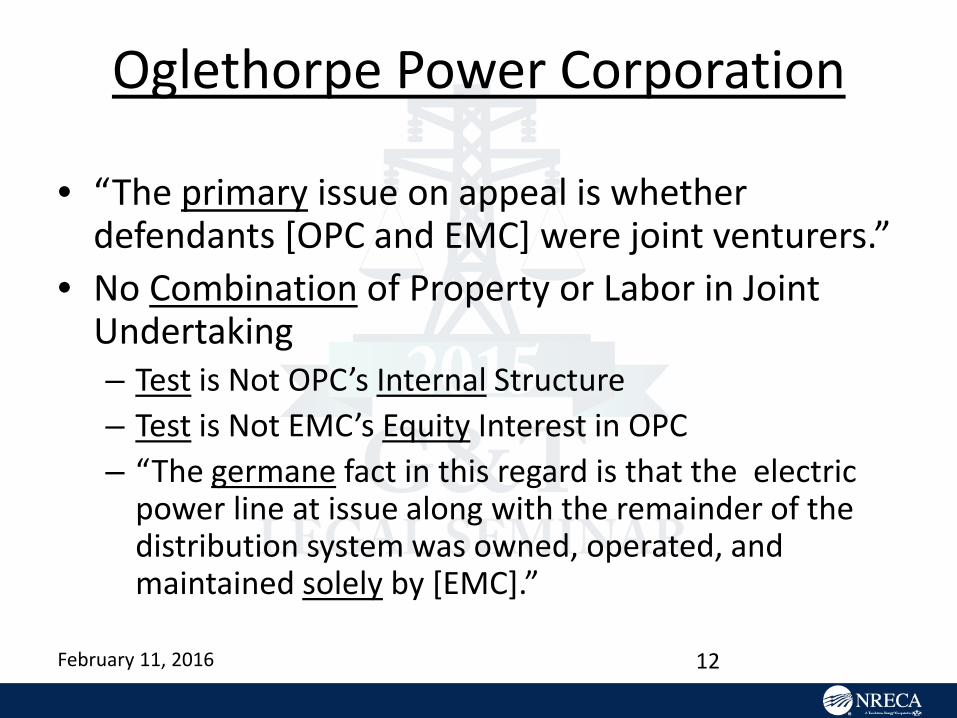

Oglethorpe Power Corporation

• Davenport v. Oglethorpe Power Corporation, 396 S.E.2d 580 (Ga. Ct. App. 1990) – Court of Appeals of Georgia

• Plaintiff Injured after Contacting Electric Line – Plaintiff Sued Rayle Electric Membership Corporation (“EMC”)

and Oglethorpe Power Corporation (“OPC”) – Plaintiff Alleged EMC and OPC were Joint Venture

• Affidavits – Line was Owned, Maintained, and Operated by EMC, and not

by OPC – OPC had No Control over EMC regarding Line

• Summary Judgment for OPC – Plaintiff Appealed

February 11, 2016 11

Oglethorpe Power Corporation

• “The primary issue on appeal is whether defendants [OPC and EMC] were joint venturers.”

• No Combination of Property or Labor in Joint Undertaking – Test is Not OPC’s Internal Structure – Test is Not EMC’s Equity Interest in OPC – “The germane fact in this regard is that the electric

power line at issue along with the remainder of the distribution system was owned, operated, and maintained solely by [EMC].”

February 11, 2016 12

Oglethorpe Power Corporation

• “Furthermore, [OPC and EMC] are not joint venturers simply because their businesses are interdependent.” – EMC Relies on OPC to Generate and Transmit Wholesale Electric Power – OPC Relies on EMC to Distribute Retail Electric Power – “However, such interdependence is universally found in a wholesaler-retailer

relationship and is not inconsistent with the operation of separate businesses.”

• Greensboro Lumber Co. v. Ga. Power Co., 643 F. Supp. 1345, 1367 (N.D. Ga. 1986) (OPC and its Members are a Single Integrated Entity for Federal Antitrust Purposes) – “not instructive in relation to the joint venture issue” – [See also Greensboro Lumber Co. v. Ga. Power Co., 844 F.2d 1538, 1541-42

(11th Cir. 1988) (“We question whether this ‘single entity theory’ is applicable to [OPC] and the EMCs. … However, we need not reach that question …”).

• Judgment Affirmed

February 11, 2016 13

Western Farmers Electric Cooperative

• Jenks v. Hill, 504 F. Supp. 1130 (W.D. Okla. 1981) – United States District Court for the Western District of

Oklahoma • Plaintiff Injured after Contacting Electric Line

while Transporting Farm Implement – Plaintiff Sued Harmon Electric Association

(“Association”) and Western Farmers Electric Cooperative (“Western”)

– Plaintiff Alleged Western Knew or Should have Known Line did Not Meet National Electric Code

February 11, 2016 14

Western Farmers Electric Cooperative

• “…, this Court is satisfied that the proper rule to be applied is that a generating company is not ordinarily liable for the negligence of a customer-distribution company when that distribution company exercises exclusive control over its distribution system.” – Association “exercised exclusive control” over Line – Western Not Liable “in the absence of some exceptional

circumstances” • Exceptional Circumstances

– Generator Constructed or Maintained Line – Generator Continued Furnishing Electric Energy after

Actual Knowledge of Defect

February 11, 2016 15

Western Farmers Electric Cooperative

• “…, this Court holds that a generating company [like Western] cannot be held liable for the negligence of a distributing company [like Association] when the distribution company exercises exclusive control over the distribution system unless the generating company continues to supply the current after having actual knowledge of some negligence in the maintenance of the distribution system.” – Deposition Testimony Indicated Western Lacked Actual

Knowledge of any Negligence or Defect • Summary Judgment for Western

February 11, 2016 16

Louisiana Sugar Cane Products

• Haywood v. Louisiana Sugar Cane Products, 692 So. 2d 524 (La. Ct. App. 1997) – Court of Appeal of Louisiana

• Louisiana Sugar Cane Products, Inc. (“Cooperative”) – Markets Raw Sugar and Molasses – Five Sugar Mill Cooperatives were Members (“Members”)

• Plaintiff Injured in Fall from Molasses Storage Tank Owned by Cooperative – Plaintiff Sued Cooperative and Members – Plaintiff Alleged Cooperative and Members were “Single

Business Enterprise” February 11, 2016 17

Louisiana Sugar Cane Products

• Summary Judgment for Members – Plaintiff Appealed

• Legislature Authorized Incorporation of Associations Like Cooperative to Market Products of Members – Inconsistent to Hold that “the same actions authorized by the

Co-operative Marketing Law justify piercing the corporate veil in order to hold the member co-operatives individually liable”

– Plaintiff’s Argument “that the relationship between [Cooperative and Members] justifies piercing the corporate veil [is] without merit.”

• No “Alter Ego” Grounds to Pierce Corporate Veil • Judgment Affirmed