family law update support 2006

DESCRIPTION

Presented by Brian Vertz, Esq., MBA, AVA at Pennsylvania Bar Institute Family Law Update in October 2006. Describes current issues and case law in child support, spousal support, and alimony pendente lite.TRANSCRIPT

Family Law Update 2006Family Law Update 2006

Brian C. Vertz, Esq.Brian C. Vertz, Esq.

Pollock Begg Komar Glasser LLCPollock Begg Komar Glasser LLC

A married couple in their early 60s was celebrating their 35th wedding anniversary in a quiet, romantic little restaurant.

Suddenly, a tiny yet beautiful fairy appeared on their table saying:

"For being such an exemplary married

couple and for being loving to each other for all this time, I will

grant you each a wish."

Oh, I want to travel around the world with my darling husband.

The husband thought for a moment:

The fairy waved her magic wand and - poof! – two tickets for the Queen Mary II appeared in her hands.

"Well, this is all very romantic, but an opportunity like this will never come again. I'm sorry my love, but my wish is to have a

wife 30 years younger than me."

The wife, and the fairy, were deeply

disappointed, but a wish is a wish.

So the fairy waved her magic wand and - poof! –

the husband became 92 years old.

The moral of this story: Men who are ungrateful bastards should remember

fairies are female.

Child Support, Spousal Support Child Support, Spousal Support and Alimony Pendente Liteand Alimony Pendente Lite

• Income Issues• Support Guidelines and Deviation• Melzer Issues• Other Issues

What is “Income”?What is “Income”?

• 42 Pa.C.S. § 4302 and Rule 1910.16-2More than “taxable income”

• Gift Income – Jacobs• Double dipping – Berry• Earning Capacity - Baehr• “Above the line” deductions – Chapman-Rolle

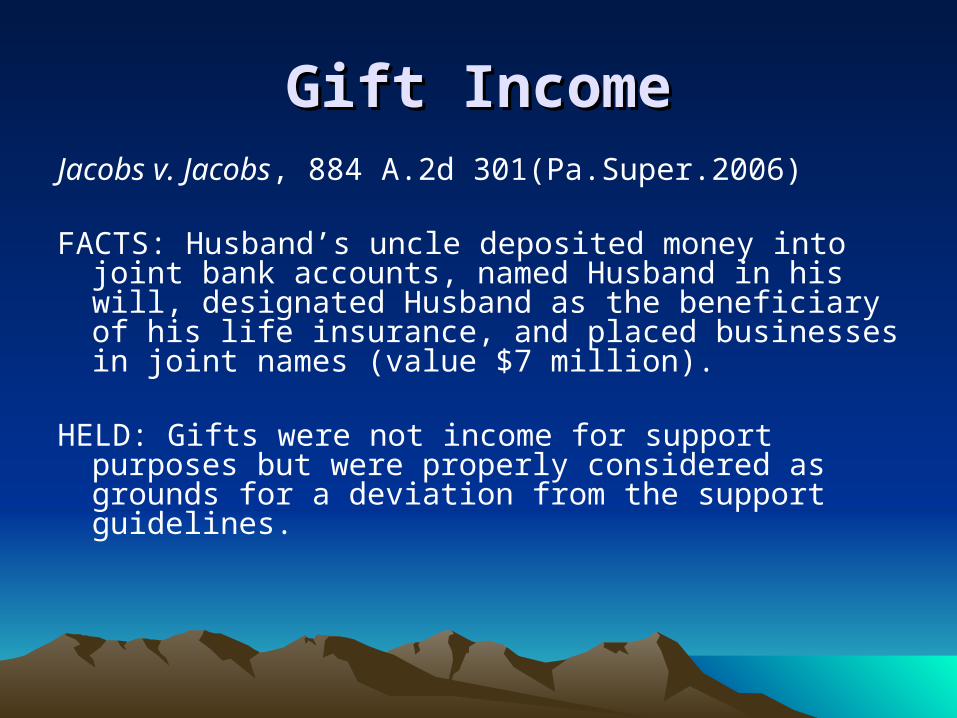

Gift IncomeGift IncomeJacobs v. Jacobs, 884 A.2d 301(Pa.Super.2006)

FACTS: Husband’s uncle deposited money into joint bank accounts, named Husband in his will, designated Husband as the beneficiary of his life insurance, and placed businesses in joint names (value $7 million).

HELD: Gifts were not income for support purposes but were properly considered as grounds for a deviation from the support guidelines.

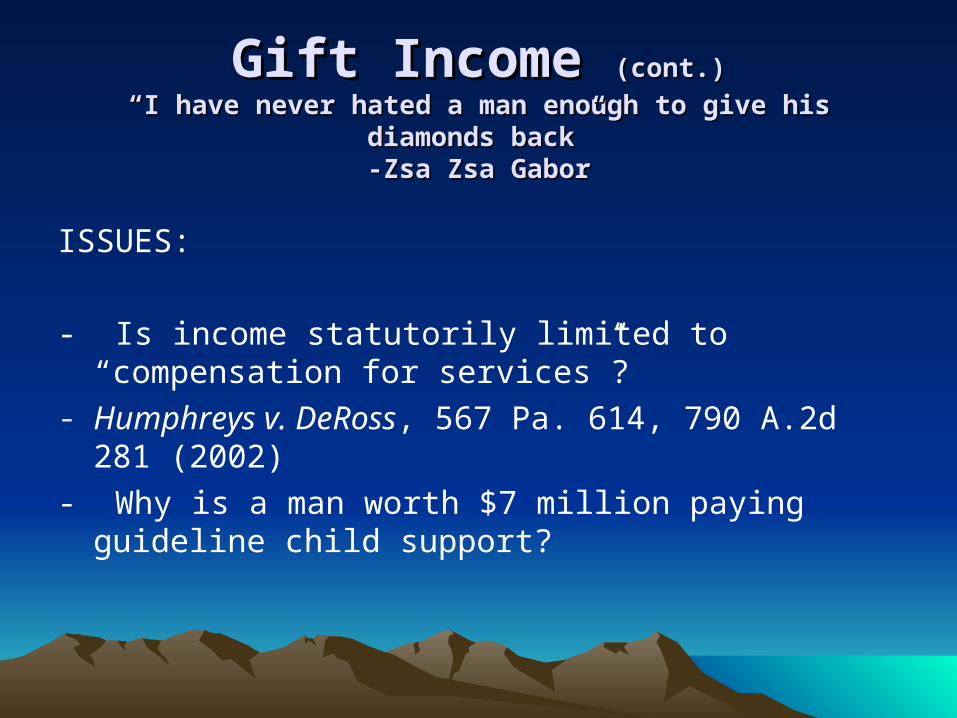

Gift Income Gift Income (cont.)(cont.)

“I have never hated a man enough to give his diamonds back”“I have never hated a man enough to give his diamonds back”-Zsa Zsa Gabor-Zsa Zsa Gabor

ISSUES:

- Is income statutorily limited to “compensation for services”?

- Humphreys v. DeRoss, 567 Pa. 614, 790 A.2d 281 (2002)

- Why is a man worth $7 million paying guideline child support?

Gift IncomeGift Income (cont.)(cont.)

• Look at where the semi-colons are placed.....

• “Income.” Includes compensation for services, including, but not limited to, wages, salaries, bonuses, fees, compensation in kind, commissions and similar items; income derived from business; gains derived from dealings in property; interest; rents; royalties; dividends; annuities; income from life insurance and endowment contracts; all forms of retirement; pensions; income from discharge of indebtedness; distributive share of partnership gross income; income in respect of a decedent; income from an interest in an estate or trust; military retirement benefits; railroad employment retirement benefits; social security benefits; temporary and permanent disability benefits; workers' compensation; unemployment compensation; other entitlements to money or lump sum awards, without regard to source, including lottery winnings; income tax refunds; insurance compensation or settlements; awards or verdicts; and any form of payment due to and collectible by an individual regardless of source.

Double DippingDouble DippingBerry v. Berry, 898 A.2d 1100 (Pa.Super.2006)

FACTS: When he was terminated from employment as a partner at KPMG, Father received severance pay and a refund of his partnership capital account.

HELD: Capital account was marital property and could not be counted also as income for child support purposes.

Double DippingDouble Dipping

ISSUES:

- Double dipping undermines equitable distribution

- What if this were a post-divorce case or the parents were never married? Would the capital account distribution constitute income?

- Are undistributed partnership earnings in a capital account protected under Fennell?

Double Dipping – Severance pay is income only if it is not a Double Dipping – Severance pay is income only if it is not a marital asset? marital asset?

Majority Rule – Compensation for past service is marital Majority Rule – Compensation for past service is marital property. Compensation to replace future earnings is property. Compensation to replace future earnings is separate property (and therefore income).separate property (and therefore income).

Formula based on length of service does not necessarily Formula based on length of service does not necessarily mean that severance pay is deferred compensation.mean that severance pay is deferred compensation.

Severance Pay

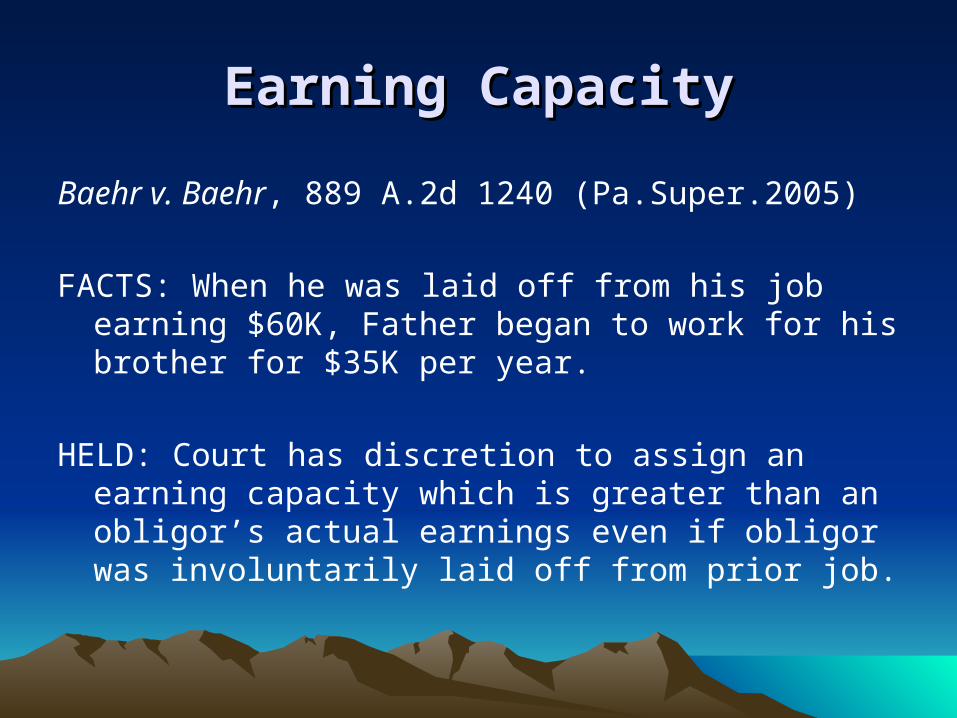

Earning CapacityEarning Capacity

Baehr v. Baehr, 889 A.2d 1240 (Pa.Super.2005)

FACTS: When he was laid off from his job earning $60K, Father began to work for his brother for $35K per year.

HELD: Court has discretion to assign an earning capacity which is greater than an obligor’s actual earnings even if obligor was involuntarily laid off from prior job.

““Above the line” deductionsAbove the line” deductions

Chapman-Rolle v. Rolle, 893 A.2d 770 (Pa.Super.2006)

FACTS: The trial court did not deduct Mother’s malpractice insurance premiums, continuing education expenses, and medical association dues from her gross revenues when calculating her income.

HELD: Because Wife included those items as budgetary expenses in her Melzer budget, the trial court did not err by failing to deduct them from her income.

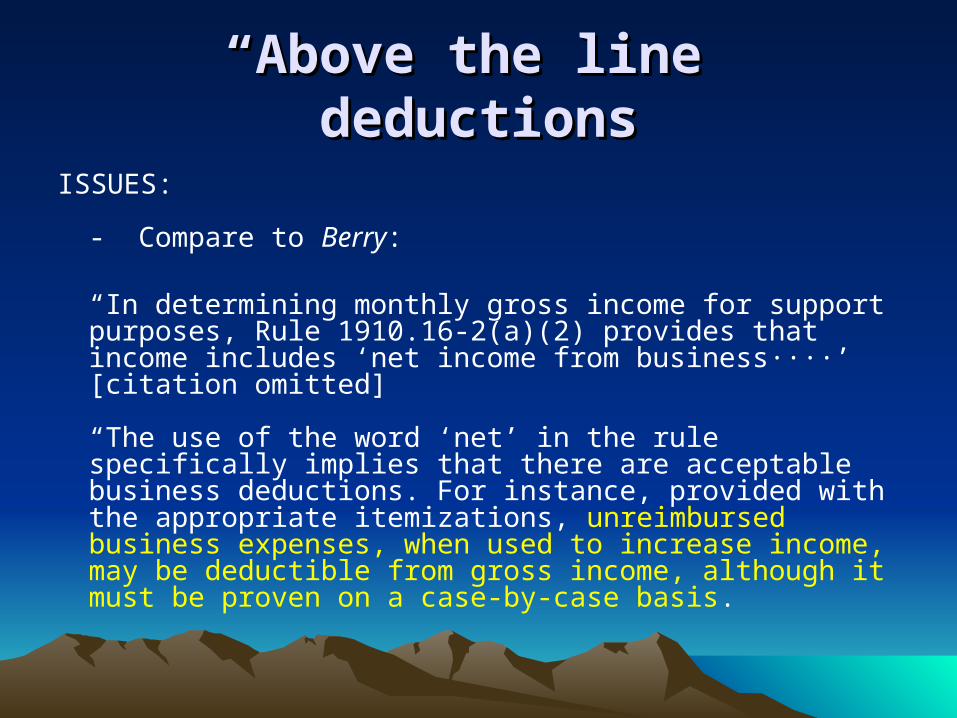

““Above the line” deductionsAbove the line” deductions

ISSUES:

- Compare to Berry:

“In determining monthly gross income for support purposes, Rule 1910.16-2(a)(2) provides that income includes ‘net income from business····’ [citation omitted]

“The use of the word ‘net’ in the rule specifically implies that there are acceptable business deductions. For instance, provided with the appropriate itemizations, unreimbursed business expenses, when used to increase income, may be deductible from gross income, although it must be proven on a case-by-case basis.

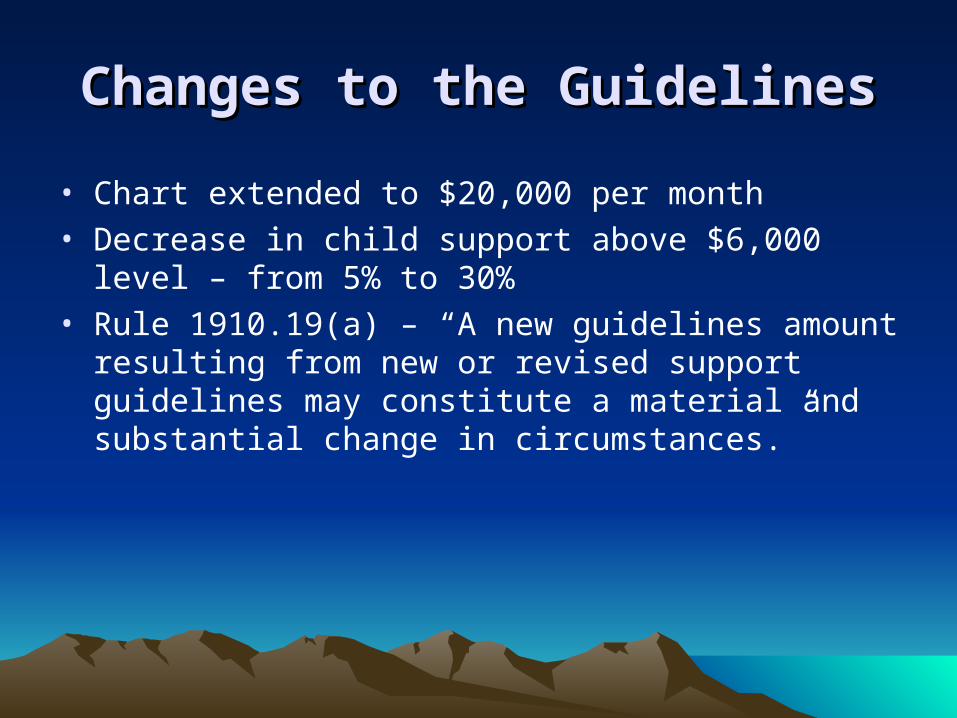

Changes to the GuidelinesChanges to the Guidelines

• Chart extended to $20,000 per month• Decrease in child support above $6,000 level – from 5%

to 30%• Rule 1910.19(a) – “A new guidelines amount resulting

from new or revised support guidelines may constitute a material and substantial change in circumstances.”

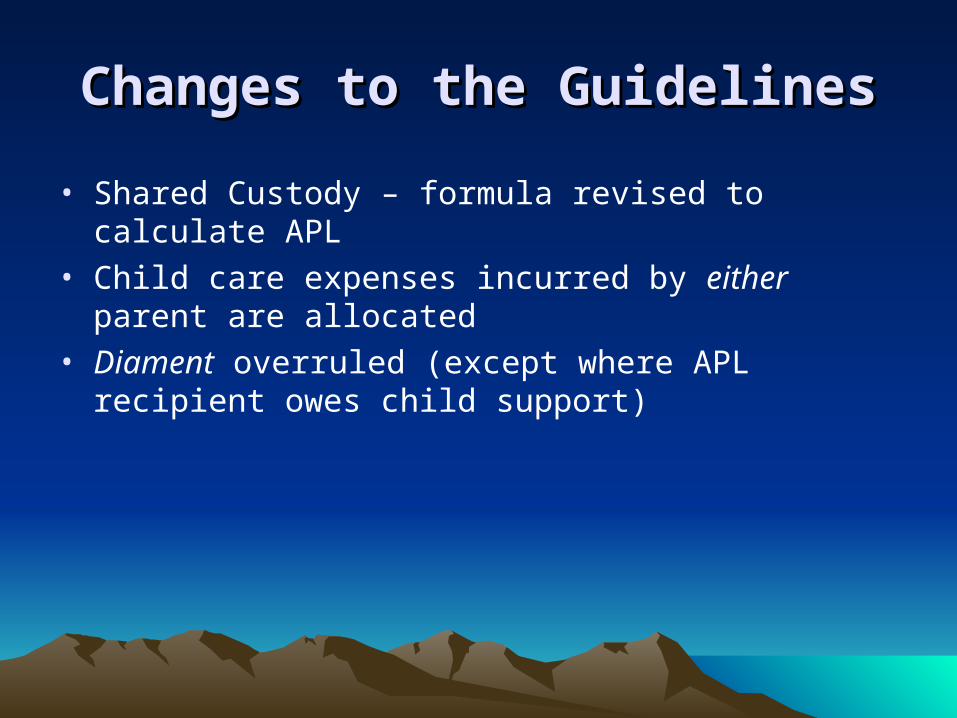

Changes to the GuidelinesChanges to the Guidelines

• Shared Custody – formula revised to calculate APL• Child care expenses incurred by either parent are

allocated• Diament overruled (except where APL recipient owes

child support)

Deviation from the GuidelinesDeviation from the Guidelines

• Standard of living - Nischal• Child Support for Noncustodial Parents -

Saunders• Special Needs - Howland

Compared to factory workers in Compared to factory workers in India, you are gettin’ way too India, you are gettin’ way too

much child support!much child support!

FACTS: Father immigrated to the U.S. from India, where his wife remained. When the parties separated, Father was ordered to pay child support in accordance with the Pennsylvania support guidelines.

HELD: No deviation based on Father’s complaint that the child support would make Mother and child “millionaires” in their native country. Nischal v. Nischal, 879 A.2d 813 (Pa.Super.2006).

Guidelines DeviationsGuidelines Deviations

ISSUES:- Why shouldn’t the court consider cost of living when the average person in India earns $250-300 per month?

- Guidelines assume that similarly situated parties will have the same needs and expenses, but are residents of a foreign country “similarly situated”?

- Goal of Guidelines is to ensure that children receive the same proportion of family income as if the parents had remained together.

SaundersSaunders – Son of – Son of Colonna?Colonna?

FACTS: Mother earned over $300,000 per year and had custody of 3 children. Father earned $67,000 per year and had partial custody.

HELD: Husband’s financial circumstances did not warrant an award of child support in addition to APL, particularly where he was not making a diligent effort to find a job after a layoff.

Son of Son of ColonnaColonna

ISSUE:

- If the kids are living a “My Sweet Sixteen” lifestyle at Mom’s house, should they have to eat soup at Dad’s?

Deviation for Special NeedsDeviation for Special Needs

Howland v. Howland, 900 A.2d 922 (Pa.Super.2006)

FACTS: Mother enrolled defiant teenage sons in out-of-state boarding schools to correct their destructive behavior. Trial court ordered father to pay 71% of the expense. Husband’s share was over $11,000 of his $13,000 monthly income.

HELD: The boarding school expense was not a reasonable need where Mother failed to investigate less expensive local programs.

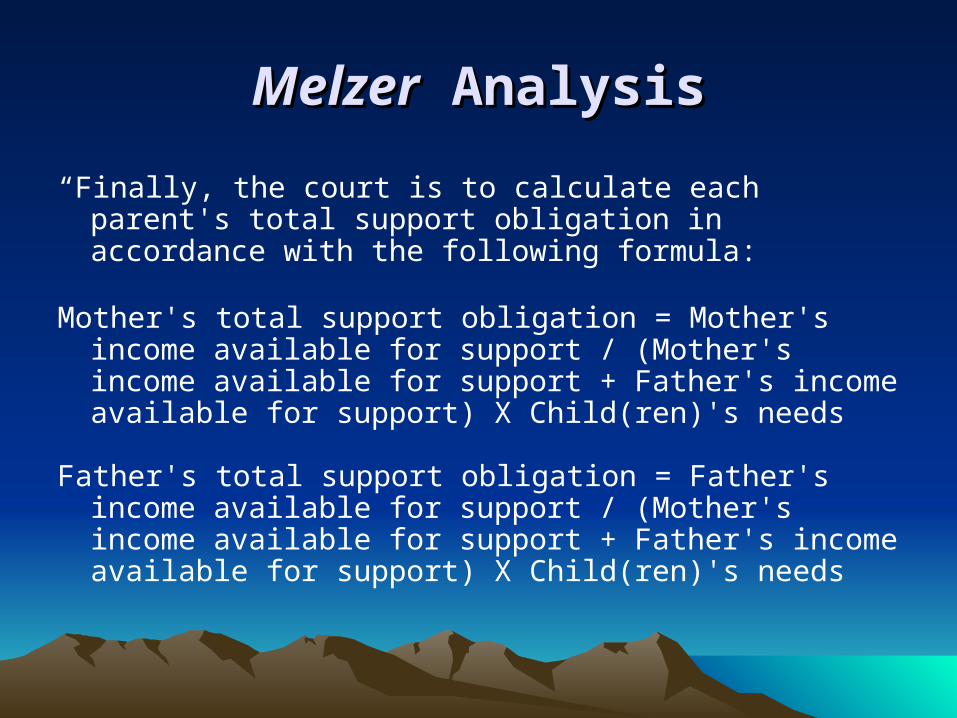

MelzerMelzer Analysis AnalysisChapman-Rolle v. Rolle, 893 A.2d 770 (Pa.Super.2006)

“In Melzer v. Witsberger, 505 Pa. 462, 480 A.2d 991 (1984), our Supreme Court held “the hearing court must first calculate the reasonable expenses of raising the children involved, based upon the particular circumstances-the needs, the custom, and the financial status-of the parties.” Melzer, at 471, 480 A.2d at 995.

“Once the reasonable needs of the children have been determined, Melzer sets forth a formula to calculate each parent's support obligation.” Mascaro v. Mascaro, 569 Pa. 255, 259, 803 A.2d 1186, 1189 (2002). Specifically, the court must determine the amount of each parent's income which remains after the deduction of the parent's reasonable living expenses. Melzer, at 472, 480 A.2d at 996.

MelzerMelzer Analysis Analysis

“Finally, the court is to calculate each parent's total support obligation in accordance with the following formula:

Mother's total support obligation = Mother's income available for support / (Mother's income available for support + Father's income available for support) X Child(ren)'s needs

Father's total support obligation = Father's income available for support / (Mother's income available for support + Father's income available for support) X Child(ren)'s needs

MelzerMelzer Mysteries Mysteries

• Ashton – Melzer is “one of the mysteries of family law”• Melzer Formula: do we allocate the kids’ budget in

proportion to the parents’ respective net incomes, or their “leftovers”? Is there an incentive to overspend?

• What if the combined net incomes are $20,100? • What if one parent’s earning capacity tips the parties

over into Melzer world? • Shared custody: do we combine the kids’ budgets in

both households?

Other IssuesOther Issues

• Chen – Third Party Beneficiaries• McClain and Hyle – Purge Conditions• Schenk – Entitlement Defense to APL?

Third Party BeneficiariesThird Party Beneficiaries

Chen v. Chen, 586 Pa. 297, 893 A.2d 87 (2006)

FACTS: Mother and Father executed a child support agreement containing a clause to allow modification if Father’s income would increase. Mother never sought an increase. When the child turned 18 and the child support terminated, Mother sued for a retroactive increase. The 18 year old child intervened as a third party beneficiary to the contract. Trial court allowed the child to intervene and entered an order of retroactive arrears against the Father.

Third Party BeneficiariesThird Party Beneficiaries

HELD: Child lacks standing to enforce child support provisions of a marital settlement agreement. Child is not an “intended” third party beneficiary.

Intended and Incidental beneficiaries

(1) Unless otherwise agreed between promisor and promisee, a beneficiary of a promise is an intended beneficiary if recognition of a right to performance in the beneficiary is appropriate to effectuate the intention of the parties and either

(a) the performance of the promise will satisfy an obligation of the promisee to pay money to the beneficiary; or

(b) the circumstances indicate that the promisee intends to give the beneficiary the benefit of the promised performance.

(2) An incidental beneficiary is a beneficiary who is not an intended beneficiary.

Purge ConditionsPurge Conditions

McClain v. McClain, 872 A.2d 856 (Pa.Supr.2005)

FACTS: Upon a finding of civil contempt, trial court jailed the contemnor and set 3 purge conditions: (1) apply for tax refund; (2) get a job and (3) post a $25K bond.

HELD: The purge conditions were impermissible because the contemnor did not have the present ability to comply with them, and the “get a job” condition could be fulfilled only in the future.

Purge ConditionsPurge Conditions

• There is a difference between civil contempt and ICC• Even in a civil contempt case, where incarceration is

used, trial court must ensure “beyond reasonable doubt” that the contemnor has the present ability to meet purge conditions.

• Even work release was not enough to create the “present ability” to comply with the condition to get a job.

• Hyle, 868 A.2d 601 (Pa.Super.2005)

Entitlement DefenseEntitlement Defense

Schenk v. Schenk, 880 A.2d 633 (Pa.Super.2005)

FACTS: Parties were married from 1996 to 1999

- Husband filed divorce in March 2000

- Wife filed counterclaim for APL in September 2000

- Wife moved in with boyfriend in May 2001

- Awarded APL from September 2000 – May 2001

- Wife sought reinstatement of APL in January 2002after moving out of her boyfriend’s home

- APL was reinstated

Entitlement DefenseEntitlement Defense

FACTS:

- Master’s hearing in 2002

- Final order in January 2003 – Wife is awarded 1/3 of the marital estate but denied alimony because she had received APL for nearly 3 years after a 3 year marriage

- Wife appealed the final order and the 2001 APL order which had terminated her APL when she lived with her boyfriend

HELD: The 2001 APL order was affirmed.

Entitlement DefenseEntitlement Defense

ISSUES:

Did the Superior Court create an entitlement defense to APL?

In Miller v. Miller, 508 A.2d 550 (Pa.Super. 1998), the Superior Court found that there was not sufficient evidence of cohabitation.

Miller held that §507 (now §3706) does not apply to APL

One for the GuysOne for the Guys

Some of you may remember my ex-wife. She had started taking flying lessons around the time our divorce started. She got her license shortly before our divorce was final, later that same year.

One for the GuysOne for the Guys

Yesterday afternoon, she narrowly escaped injury in the aircraft she was piloting when she was forced to make an emergency landing in Southern Tennessee because of bad weather.

Some could call it a crash; an accident at the least. Our kids were with me at the Beach House when we heard the news.

One for the GuysOne for the Guys

The absence of a post-crash fire was likely due to insufficient fuel on board. No one on the ground was injured.

Photographs taken at the crash scene show the extent of damage to her aircraft. She was very lucky.

One for the GuysOne for the Guys