factors affecting option price assumptions and notation upper and lower bounds for option price...

TRANSCRIPT

Factors affecting option priceAssumptions and notationUpper and lower bounds for option pricePut-call parityEarly exercise : calls on a non-dividends-

paying stockEarly exercise : puts on a non-dividends-

paying stockEffect of dividends

1

2

There are six factors affecting the price of a stock option:

1.The current stock price, S0

2.The strike price, K

3.The time to expiration, T

4.The volatility of the stock prive,

5.The risk-free interest rate, r

6.The dividends expected during the life of the option

3

c p C PVariable

S0

KTrD

+ + –+

? ? + ++ + + ++ – + –

–– – +

– + – +

Summary of the effect on the price of a stock option of increasing one variable while keeping all others fixed.

We assume that there are some market participants, such as

large investment banks, for which the following statements are

true:

1.There are no transactions costs.

2.All trading profits (net of trading losses) are subject

to the same tax rate.

3.Borrowing and lending are possible at the risk-free

interest rate.

4

5

S0 : Stock price today

K : Strike price

T : Life of option

: Volatility of stock price

r : Risk-free interest rate

D : Present value of dividends during option’s life

ST : Stock price at option maturity

p : European put option price

c : European call option price

P : American Put option price

C : American Call option price

An American option is worth at least as much as the corresponding European option

C c

P p

6

American C S≦ 0 P K≦

Europeanc S≦ 0 (c C)≦

p ke ≦ -rT

(p P)≦

7

Call option can never be worth more than the stock; Put option can never be worth more than the strike price. Hence, the stock price is an upper bound to the option price.

8

A lower bound for the price of a European call option on a non-dividend-paying stock is

S0 –Ke –rT

We first look at a numerical example and then consider a more formal argument. Example

S0 =$20 , K=$18 , r = 10% per annum , T = 1 year

9

10

A lower bound for the price of a European put option on a non-dividend-paying stock is

Ke –rT – S0

We first look at a numerical example and then consider a more formal argument. Example

S0 =$37 , K=$40 , r = 5% per annum , T = 0.5 year

11

12

Portfolio A ST K≧ ST < K

c(K) ST -K 0

Ke -rT K K

Total ST K

13

Portfolio C ST K≧ ST < K

p(K) 0 K - ST

S0 ST ST

Total ST K

Suppose that c = 3 S0 = 31

T = 0.25 r = 10%

K = 30 D = 0

What are the arbitrage possibilities when

p = 2.25 ?

p = 1 ?

14

Usually there is some chance that an American option will be exercised early

This should never be exercised early

∵ c≧S0- Ke -rT and C≧c

∴ C≧c≧S0- Ke -rT≧S0- K (exercise value)

(∵Ke -rT< K)

15

No income from the stock is sacrificed

Payment of the strike price is delayed

Holding the call provides insurance

against stock price falling below strike

price 16

17

Are there any advantages to exercising an American put when

∵ p≧Ke -rT - S0 and P≧p

∴ P≧p ≧ Ke -rT - S0 > K - S0

But P must be larger than KS0 because it is always possible to exercise before maturity

18

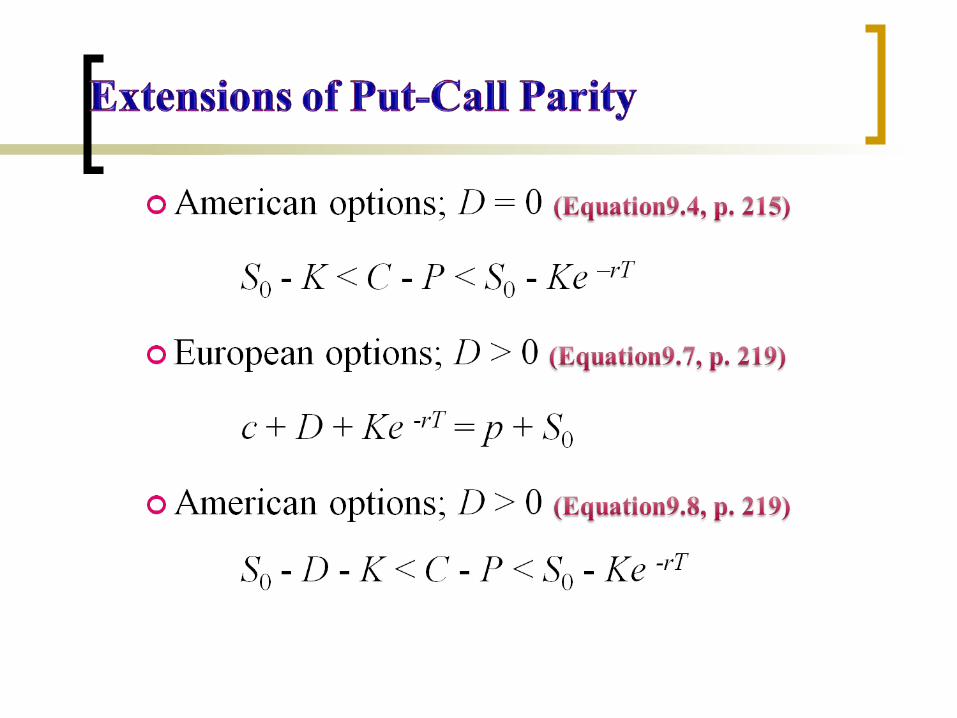

rTKeDSc 0

0SKeDp rT

We will use D to denote the present value of the dividends during the life of the option. In the calaulation of D, a dividend is assumed to occur at the time of its ex-dividend date.

19