f2 advanced financial reporting€¦ · group accounts – cima f1 to cima f2 group accounting for...

TRANSCRIPT

F2 Advanced Financial Reporting

Module: 07

The Income Statement

1. Overview

Next up in our tour through the world of consolidated financial statements we

have the consolidated Income Statement, or the CIS. Here the focus is on

the consolidation of expenses and revenue, with many of the same

principles applied as for the CSFP.

Group accounts – CIMA F1 to CIMA F2

Group accounting for the income statement is studied both in CIMA F1 and

CIMA F2. This chapter examines the basics of how to produce the income

statement for groups as already studied in CIMA F1. If you're confident in

this material, please feel free to skim through it quickly as a recap. If it's

been a while since your F1 exam, or you simply want to a recap of the

basics before tackling the new material then please do work through this

chapter in full.

Basic principle

The aim of the consolidated income statement is to show the profit

generated by the net assets of the parent company (P) and its

subsidiary (S). As a result, it shows the profit for the group as a single

entity.

The consolidated income statement follows these basic principles:

• Include all of P’s income and expenses plus all of S’s income

and expenses (reflecting the fact that P controls S).

• Ignore investment income from S to P (e.g. dividend payments or

loan interest) as these are just transfers within the group (similar to

intra-group trading in the CSFP).

• After profit for the period, show the profit split between amounts

attributable to the parent's shareholders and other shareholders

(known as shareholders with a non-controlling interest) to reflect

ownership. Note: There is no non-controlling interest in a 100% owned

subsidiary.

Structure of the consolidated income statement

The consolidated income statement looks a lot like the income statement for

an individual company.

The main difference is this split at the end of the statement between the

parent and other shareholders (non-controlling interests).

It looks as follows:

X Group

Revenue x

Cost of Sales (x)

Gross Profit x

Operating expenses (x)

Operating profit x

Investment income x

Profit before interest x

Finance cost (x)

Profit before tax x

Tax (x)

Profit for period xx

Attributable to:

Non-controlling interests x

Parent's shareholders x

xx

As mentioned, there is no non-controlling interest when a parent owns 100%

of the subsidiary. In this case, there would be no need for the NCI line in the

statement.

2. Fully owned subsidiary

Let's use an example of a simple fully owned subsidiary to help illustrate the

fundamentals of consolidating the income statement.

Example

P Ltd acquired 100% of the equity in S Ltd on 1 Jan 20X8. For the year ended

31 Dec 20X9 the income statement extracts for P Ltd and S Ltd are:

P Ltd S Ltd

£'000 £'000

Revenue 2,500 850

Cost of Sales (2,150) (750)

Gross Profit 350 100

Investment income:

Dividend from S Ltd 8 -

Profit before tax 358 100

Tax (72) (20)

Profit for period 286 80

Prepare the consolidated income statement for the year ended 31 Dec 20X9.

Answer

Right, so the key thing to look out for in a question like this is any intra-

group activity. In this question we can see that S Ltd has paid a dividend to

P Ltd, and since this is internal to the group it needs to be eliminated in the

consolidated statement.

However, once we've done that, it's a fairly simple task to add together the income

and expenses of the parent and subsidiary!

Method

Step 1. Remove the dividend from S Ltd (as this is intra-group).

Step 2. Aggregate the income and expenses for P Ltd and S Ltd.

Consolidation matrix

Okay, so following step 1, the first thing we do is eliminate the intra-group

dividend of £8,000. Once we've done that, we just go line by line adding P

and S's figures together.

P Ltd S Ltd Step 1 Step 2 P Group

£'000 £'000 £'000 £'000

Revenue 2,500 850 P+S 3,350

Cost of Sales (2,150) (750) P+S (2,900)

Gross Profit 350 100 450

Dividend from S Ltd 8 0 (8) P+S 0

Profit before tax 358 100 450

Tax (72) (20) P+S (92)

Profit for period 286 80 358

Attributable to:

P Ltd shareholders 358

358

Note that when we get to a summation line for the group (the figure

immediately below a horizontal line on the statement) then we need to

perform the calculation vertically rather than horizontally. If you look at the profit

for period line, for instance, 286+80 is not 458. To get the 458 you have to

take the total profit before tax of 450 and take off the 92.

Since P own 100% of S, there is no non-controlling interest to worry about,

and so the consolidated statement of comprehensive income looks as

follows:

P Group: Consolidated Income Statement for period end 31 Dec 20X9

Revenue

P Group

£'00

0

3,350

Cost of Sales (2,900)

Profit before tax 450

Tax (92)

Profit for period 358

Attributable to:

P Ltd shareholders

358

358

3. Investment: Dividends

Group versus intra-group dividends

We have already seen that, a payment of a dividend by a subsidiary (S) to a

parent (P) will need to be cancelled. This is because it is effectively an

intra-group payment. The effects of the cancellation on the consolidated

income statement are:

1. Only dividends paid by P to its own shareholders appear in the

consolidated financial statements. These are shown within the

consolidated statement of changes in equity (which you were not required

to prepare for the F1 examination);

2. Any dividend income shown in the consolidated income

statement must arise from investments other than those in

subsidiaries or associates.

Example – Dividend not from a subsidiary

Continuing the same example as used earlier, assume that P Ltd’s income

from investment is £20,000 and that it includes a dividend of £8,000 from S

Ltd. The remaining balance of £12,000 is from dividends from stock

exchange listed investments. During the year, P Ltd paid a dividend of

£30,000. Prepare the consolidated income statement for the year ended 31

Dec 20X9 and calculate the retained earnings of the group.

Answer

Method

1. Remove the dividend from subsidiary (as this is intra-group).

2. Aggregate the income and expenses for P Ltd and S Ltd.

Consolidation matrix

P Ltd S Ltd Step 1 Step 2 P Group

£'000 £'000 £'000 £'000

Revenue 2,500 850 P+S 3,350

Cost of Sales, CoS (2,150) (750) P+S (2,900)

Gross Profit 350 100 450

Investment income 20 0 (8) P+S 12

Profit before tax, PBT 370 100 462

Tax (74) (20) P+S (94)

Profit for period, PAT 296 80 368

Attributable to:

P Ltd shareholders 368

368

Retained earnings of P Group

£'000

Group profit for the period 368

P Ltd dividend (ordinary) (30)

Retained earnings 338

P Group Consolidated Income Statement for period end 31 Dec 20X9

Revenue

P Group

£'00

0

3,350

Cost of Sales (2,900)

Gross Profit 450

Investment income 12

Profit before tax 462

Tax (94)

Profit for period 368

Attributable to:

P Ltd shareholders

368

368

Income from investments is not restricted to dividends, it can also be as a

result of income from preference shares and loan interest. The impact of

these on the consolidated income statement will be covered in the next

section.

4. Investment: loans and preference shares

Loans

A parent can earn investment income from a subsidiary by providing loans to it

and charging (preferential) interest for them. This will result in:

• Loan interest received in the parent’s books (investment income);

• Loan interest paid in the subsidiary’s books (finance cost).

These inter-company interest amounts must not appear in the

consolidated income statement as they are amounts owing within the

group. If they were to be included, elements such as investment income and

finance cost would be overstated as, balances would appear in both the parent

and subsidiary accounts. Note: the same principle applies for a cash rich

subsidiary supplying loans to its parent.

Consolidation treatment of loan interest

The relevant amount of interest should be deducted from group investment

income and group finance costs. The following reconciling adjustment will be

required:

DR Group investment income

CR Group finance cost

Preference shares

The same adjustment concept is followed in respect of preference shares. Preference shares will almost always be classified as liabilities, rather than equity,

and so preference dividends constitute part of the finance cost.

Example – Loans and preference shares

The draft income statements of A Ltd and B Ltd are shown below as of 31

Dec 20X7. A Ltd acquired 100% of B Ltd on 1 Jan 20X6. A Ltd has provided

B Ltd with a £100k loan at an interest rate of 10%. The loan was outstanding

at the year end. B Ltd paid a dividend of £6,000 to A Ltd (included in the

investment income of A Ltd).

A Ltd B Ltd

£'000 £'000

Revenue 600 300

Cost of Sales, CoS (360) (140)

Gross Profit 240 160

Operating expenses (80) (45)

Operating profit 160 115

Investment income 16 -

Profit before interest, PBIT 176 115

Finance cost (4) (15)

Profit before tax, PBT 172 100

Tax (35) (25)

Profit for period, PAT 137 75

Prepare the consolidated income statement for the year ended 31 Dec 20X7.

Answer

Method

1. Remove the dividend from subsidiary (as this is intra-group).

2. Remove the loan interest from subsidiary (as this is intra-group).

3. Aggregate the income and expenses for A Ltd and B Ltd.

Consolidation matrix

A Ltd

£'000

B Ltd

£'000

Step 1

£'000

Step 2

£'00

0

(W1)

Step 3

£'000

A Group

£'000

Revenue 600 300 A+B 900

Cost of Sales, CoS (360) (140) A+B (500)

Gross Profit 240 160 400

Operating expenses (80) (45) A+B (125)

Operating profit 160 115 275

Investment income 16 0 -6 -10 A+B 0

Profit before interest 176 115 275

Finance cost (4) (15) 10 A+B (9)

Profit before tax, PBT 172 100 266

Tax (35) (25) A+B (60)

Profit for period, PAT 137 75 206

Attributable to:

P Ltd shareholders 206

206

Workings

W1) Intra-group loans & interest

Loan interest = loan, £100k x interest charge, 10% = £10k per year.

Deduct subsidiary interest paid from group investment income and group

finance costs.

DR Group investment income £10k

CR Group finance charge £10k

A Group: Consolidated Income Statement for period end 31 Dec 20X7

A Group

£'000

Revenue 900

Cost of Sales (500)

Gross Profit 400

Operating expenses (125)

Operating profit 275

Investment income 0

Profit before interest 275

Finance cost (9)

Profit before tax 266

Tax (60)

Profit for period 206

Attributable to:

P Ltd shareholders 206

206

5. Intra-group trading: sales and purchases

Sales and purchases: balances

Ali runs a small business that also owns a small subsidiary. He really wants to

make the business seem bigger than it is so he's got an idea. Why not sell

goods to the subsidiary for £1m and then sell them back the next day for

another £1m. Suddenly he's got a business with a £2m revenue and it looks

like he's built a substantial business. Has he? Of course not, he's just fiddling

the books to make it look that way. Not surprisingly this is not allowed and on

consolidation these transactions are cancelled out. Even if the sale was

genuine (e.g. Ali sells a machine to the subsidiary that it genuinely needs) it's

still not allowed. A sale to yourself isn't really a sale.

In summary

If a parent was selling items to its subsidiary this would result in the recording

within the income statement of:

• Revenue in the selling company’s books;

• Purchases (part of cost of sales) in the buying company’s books.

A group is seen as a single entity and as such cannot sell to itself. Only

sales external to the group should be recorded. The effect of intra-group

trading must be eliminated from the consolidated income statement.

Consolidation adjustment for intra-group sales and purchases

Upon consolidation the following adjustment is made:

Consolidated revenue = P’s revenue + S’s revenue – intra-group sales.

Consolidated cost of sales =

P’s Cost of Sales + S’s Cost of Sales – intra-group purchases.

Sales and purchases: unrealised profit

Let's say a parent sells a £10 item and makes a £5 profit on it. If the

subsidiary then sells that product on, say for £12, it makes a further £2, and

the group as a whole makes £7. That's fine and no adjustment is needed

because the total group profit of £7 is fully realised. There is no 'unrealised

profit'.

What if the associate did not sell the item though? The parent has a £5 profit

which is 'unrealised'. It's not a true profit. What's actually happened is that that

purchased item was carried over in the subsidiary's closing inventory and

that's caused the profit for the group to be too high.

In summary: if items are sold intra-group at a profit this can only be

recognised when the item is eventually sold externally to the group i.e.

realised profit. If this is not the case, then the profit made on this internal sale

is unrealised profit and must be removed from the consolidated income

statement.

Unrealised profit in stock

Intra-group sales of stock that include unrealised profit will affect the cost of

sales (opening and closing stock) in the income statement and stock

balance in the statement of financial position. The unrealised profit's effect on

the cost of sales is as follows:

Impact Adjustment Result

Opening inventory

Purchases

X Higher

X

Remove profit Decrease CoS

Closing inventory (X) Higher Remove profit Increase CoS

Cost of sales, CoS X

Consolidation adjustment for unrealised profit in stock

Consolidated cost of sales =

P’s CoS + S’s CoS + closing inventory unrealised profit – opening inventory

unrealised profit

This can be hard to visualise and understand when you see it as the

proforma, so let's look at an example to see how this works and hopefully

then all will become clear.

Example – Unrealised profits

C Ltd (the parent company) buys goods for £600,000 and sells them to its

subsidiary, D Ltd for £900,000, making a £300,000 profit.

D Ltd sells two thirds of the goods to a third party for £750,000. As it paid

£900,000 for them the costs of two-thirds were £600,000. The remaining

stock of £300,000 is unsold at the year end and so is carried forward to the

next period and not charged to this one.

The income statement extracts for C Ltd and D Ltd are as follows:

C Ltd D Ltd

£'000 £'000

Revenue 900 750

Cost of Sales (600) (600)

Gross Profit 300 150

The total combined profit of £450,000 is obviously not a true representation of

what happened here.

The reality of the situation is that an external sale of £750,000 was made on

good that cost the group £400,000 (2/3 x 600,000). The true profit should be

£350,000 with some stock remaining at the year end.

Let's see how the consolidated income statement extract covering these

transactions should be put together.

Answer

Method

Step 1. Remove the sales from C Ltd to D Ltd (as they are intra-group).

Step 2. Remove the unrealised profit in the unsold (closing) stock of D Ltd.

Step 3. Aggregate the income and expenses for C Ltd and D Ltd.

Consolidation matrix

C Ltd

£'000

D Ltd

£'000

Step 1

£'000

Step 2

£'00

0

(W1)

Step 3

£'000

C Group

£'000

Revenue 900 750 (900) C+D 750

Cost of Sales (600) (600) 900 (100) C+D (400)

Gross Profit 300 150 350

Workings

Workings

W1) Unrealised profit in unsold stock

In D Ltd's accounts it had inventory at the year end of £300,000 (= 1/3 x

purchases from C Ltd, £900k).

In actual fact the group as a whole only paid £200,000 for those goods (1/3 x

purchase of £600,000).

Inventory for the group is therefore overstated by £100,000.

Let's remind ourselves what closing inventory is doing – it's taking costs of

inventory out of one period and into the next. In this case then £100,000 too

much has been carried forward to the next period and so the group's profit is

£100,000 too high:

£'000

Unsold stock in D Ltd 300

Original cost of unsold stock (200)

Unrealised profit 100

Overall then £100,000 needs to be added to the cost of sales to take account

of this.

When we do this (see the matrix) we find the profits are £350,000 as we

thought they would be from our analysis in the question.

Consolidation adjustment

We would also need to reduce the closing inventory by £100k in the

statement of financial position (SoFP) so the consolidation adjustment

required is:

DR Consolidated cost of sales £100k

CR Consolidated inventory (SoFP) £100k

C Group: Consolidated Income Statement extract

C Group

£'000

Revenue 750

Cost of Sales (400)

Gross Profit 350

6. Other adjustments

Impairments

Impairment exists when the fair value (i.e. market price) of an asset is

below its carry value (the carry value of an asset, is the value left once

accumulated depreciation/amortisation and any impairments have been

deducted from the original cost.) Impairments relating to the year (e.g.

goodwill impairment) will be charged as an expense usually via operating

expenses. Where non-controlling interests, NCI have been valued at fair

value, a portion of the impairment expense must be deducted from the NCI

share of profits.

Fair value adjustments

The fair value adjustment may result in a change to the profits of the

subsidiary in the group accounts. For example, adjustment due to increased

depreciation charges resulting from depreciating non-current assets at fair

value.

Non-controlling interests

The non-controlling interest share of the subsidiary profits will be affected by

numerous adjustments. These are summarised below:

NCI % of profit after tax X

Less:

NCI % of fair value depreciation (X)

NCI % of unrealised profit (X)

NCI % of impairment (fair value method) (X)

x

Example – Other adjustments

P Ltd acquired 80% of S Ltd 3 years ago. At the date of acquisition some

fixed assets with book value £8,000 had a fair value of £12,000. These assets

have a useful life of 4 years. During the year, S Ltd sold stock to P Ltd for

£9,000. These originally cost £6,000. 50% of the stock remained unsold at

the year end. The investment income is solely composed of a dividend from S

Ltd. For the year ended 31 Dec 20X9 the income statements for P Ltd and S

Ltd are as follows.

P Ltd S Ltd

£'000 £'000

Revenue 95,000 60,000

Cost of Sales, CoS (40,000) (20,000)

Gross Profit 55,000 40,000

Operating expenses (10,000) (10,000)

Operating profit 45,000 30,000

Investment income 6,400 -

Profit before interest, PBIT 51,400 30,000

Finance cost (1,400) (5,000)

Profit before tax, PBT 50,000 25,000

Tax (10,000) (5,000)

Profit for period, PAT 40,000 20,000

Prepare the consolidated income statement for the year ended 31 Dec 20X9.

Answer

Method

1. Remove the dividend from subsidiary (as this is intra-group).

2. Remove the sales from S Ltd to P Ltd (as they are intra-group).

3. Remove the unrealised profit in the unsold (closing) stock of P Ltd.

4. Apply the fair value adjustment to group operating expenses.

5. Aggregate the income and expenses for P Ltd and S Ltd.

6. Allocate (‘give back’) the share of S Ltd adjusted profit attributable to

the non-controlling interest, NCI (based on % ownership).

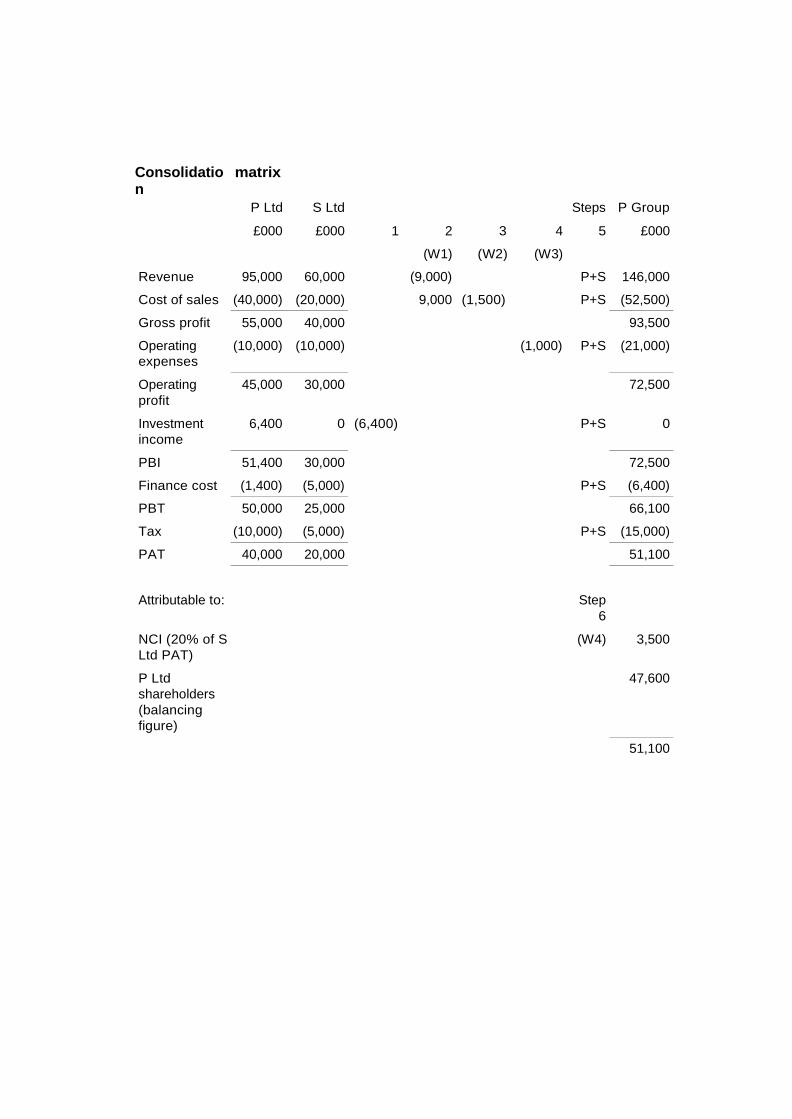

Consolidation

matrix

P Ltd

S Ltd

Steps

P Group

£000 £000 1 2 3 4 5 £000

(W1) (W2) (W3)

Revenue 95,000 60,000 (9,000) P+S 146,000

Cost of sales (40,000) (20,000) 9,000 (1,500) P+S (52,500)

Gross profit 55,000 40,000 93,500

Operating

expenses

(10,000) (10,000) (1,000) P+S (21,000)

Operating

profit

45,000 30,000 72,500

Investment

income

6,400 0 (6,400) P+S 0

PBI 51,400 30,000 72,500

Finance cost (1,400) (5,000) P+S (6,400)

PBT 50,000 25,000 66,100

Tax (10,000) (5,000) P+S (15,000)

PAT 40,000 20,000 51,100

Attributable to:

Step

6

NCI (20% of S

Ltd PAT)

(W4) 3,500

P Ltd

shareholders

(balancing

figure)

47,600

51,100

Workings

W1) Intra-group sales

£'000

S Ltd sales to P Ltd 9,000

Thus, adjustment:

DR Group revenue 9,000

CR Group cost of sales (purchases) 9,000

W2) Unrealised profit in unsold stock

Unsold stock in P (incl. unrealised

profit) 4,500 50% of purchases from S Ltd

50% of original price paid by S

Original cost of this stock 3,000

unrealised profit (PUP) 1,500

Ltd

(remove from P Ltd closing

stock)

Thus, adjustment:

DR Group CoS (closing stock) 1,500

CR Group stock 1,500

(Group CoS will thus increase)

W3) Fair value adjustment

Extra depreciation due to fair value increase:

£'000

Fair value, FV 12,000

Book value 8,000

FV adjustment 4,000

Useful life (years) 4

Extra dep'n (= FV adjustment / useful life) 1,000

W4) Non-controlling interests, NCI

Profit after tax (as per S Ltd)

£'00

0

20,000

Unrealised profit (W2) (1,500)

Fair value depreciation (W3) (1,000)

Adjusted profit after tax 17,500

NCI % of adjusted profit (20%)

3,500

P Group Consolidated Income Statement for period end 31 Dec 20X9

Revenue

P Group

£'00

0

146,000

Cost of Sales (52,500)

Gross Profit 93,500

Operating expenses (21,000)

Operating profit 72,500

Investment income 0

Profit before interest 72,500

Finance cost (6,400)

Profit before tax 66,100

Tax (15,000)

Profit for period 51,100

Attributable to:

Non-controlling interests

3,500

P Ltd shareholders 47,600

51,100

7. Mid-year acquisitions

Rule for mid-year acquisitions

When a subsidiary is acquired part way through the year, its results

should only be consolidated from the acquisition date i.e. when control is

established. The subsidiary’s results will need to be time apportioned from

the date of acquisition. It is therefore assumed the revenues and expenses

accrue evenly throughout the year.

Let's take look at an example to see how this works.

Example

On 30 Nov 20X7 X Ltd acquired 75% of Y Ltd. No dividends were paid by

either company during the year. The investment income is from stock

exchange quoted investments. The Income statements for period end 31 Mar

20X8 as are follows:

X Ltd

£

Y Ltd

£

Revenue 305,000 220,500

Cost of Sales, CoS (145,000) (120,000)

Gross Profit 160,000 100,500

Operating expenses (71,000) (51,500)

Operating profit 89,000 49,000

Investment income 3,000 1,500

Profit before interest, PBIT 92,000 50,500

Finance cost (10,000) (5,000)

Profit before tax, PBT 82,000 45,500

Tax (20,500) (11,375)

Profit for period, PAT 61,500 34,125

Prepare the consolidated income statement for period end 31 Mar 20X8.

Answer

Method

Step 1. Aggregate all the income and expenses for X Ltd plus Y Ltd’s time

apportioned income and expenses.

Note. The group share of Y Ltd’s income and expenses is only 4 months

worth out of 12 months, so it will be time apportioned by a factor of 4/12.

Consolidation matrix

X Ltd Y Ltd Step 1 X Group

Revenue 305,000 220,500 P+(S x 4/12) 378,500

Cost of Sales (145,000) (120,000) P+(S x 4/12) (185,000)

Gross Profit 160,000 100,500 193,500

Operating expenses (71,000) (51,500) P+(S x 4/12) (88,167)

Operating profit 89,000 49,000 105,333

Investment income 3,000 1,500 P+(S x 4/12) 3,500

Profit before interest 92,000 50,500 108,833

Finance cost (10,000) (5,000) P+(S x 4/12) (11,667)

Profit before tax 82,000 45,500 97,166

Tax (20,500) (11,375) P+(S x 4/12) (24,292)

Profit for period, PAT 61,500 34,125 72,874

Step 2. Allocate (‘give back’) the time apportioned share of Y Ltd profit

attributable to the non-controlling interest, (based on % ownership).

There are 25% of shares attributable to external parties, and they are due

their share of 4 months of Y Ltd's profits. Let's see how this is calculated:

Attributable to:

Non-controlling interest

(25% x Y Ltd profit after tax x 4/12) 2,844

P Ltd shareholders (balancing figure) 70,030

72,874

The final consolidated statement will be as follows:

X Group: Consolidated income statement for period end 31 Mar 20X8

Revenue

X Group

378,500

Cost of Sales (185,000)

Gross Profit 193,500

Operating expenses (88,167)

Operating profit 105,333

Investment income 3,500

Profit before interest 108,833

Finance cost (11,667)

Profit before tax 97,166

Tax (24,292)

Profit for period 72,874

Attributable to:

Non-controlling interests

2,844

P Ltd shareholders 70,030

72,874

8. Chapter summary

So in summary…

Consolidated income statement

• The purpose of the consolidated income statement is to show the

profit of the group (parent and subsidiaries) as a single entity.

• The consolidated income statement is constructed by

aggregating the income statements of the parent and subsidiary

from revenue through to profit for the period. Intra-group items are

eliminated.

• After profit for the period, the group profit is split (to reflect control

via ownership) between amounts attributable to the parent's

shareholders and the non-controlling interest

Dividends

• Subsidiary dividends are eliminated in the consolidated income

statement as they are intra-group. Investment income consisting of

external dividends is consolidated.

• Only the parent’s dividend is factored in group retained earnings.

Loans and preference shares

• Loan interest and preference shares payments are a source of

investment income. If they are intra-group, the relevant amount of

interest should be deducted from group investment income and

group finance costs.

Intra-group sales and purchases

• Intra-group sales and purchases need to be eliminated on

consolidation. The adjustment is made to group sales and group cost

of sales.

• Unrealised profit present in inventory is removed via an adjustment

to the group cost of sales.

Non-controlling interests

• Adjustments to non-controlling interests, NCI include NCI share

of unrealised profit, fair value depreciation and impairment.

Mid-year acquisitions

• The subsidiary’s income and expenses need to be consolidated by

time apportionment from the date of acquisition.