ey french venture capital barometer...2015 2016 €1.01 billion (297 deals) €1.2 billion (277...

TRANSCRIPT

EY French Venture Capital BarometerAnnual Results 2019

2 | EY French Venture Capital Barometer | Annual Results 2019 3EY French Venture Capital Barometer | Annual Results 2019 |

€5.03 bn in funds raised in 736 deals with an average deal size of €6.8 m.

Where will #FrenchTech stop?

Year after year, innovative French companies raise more and more funds. Thus, setting a new record, 736 companies raised just over €5 billion in 2019, an amount up 39% in value and 14% in volume.

The next French unicorns should be born from this fertile soil, demonstrating the ability of the French ecosystem to grow businesses in this segment.

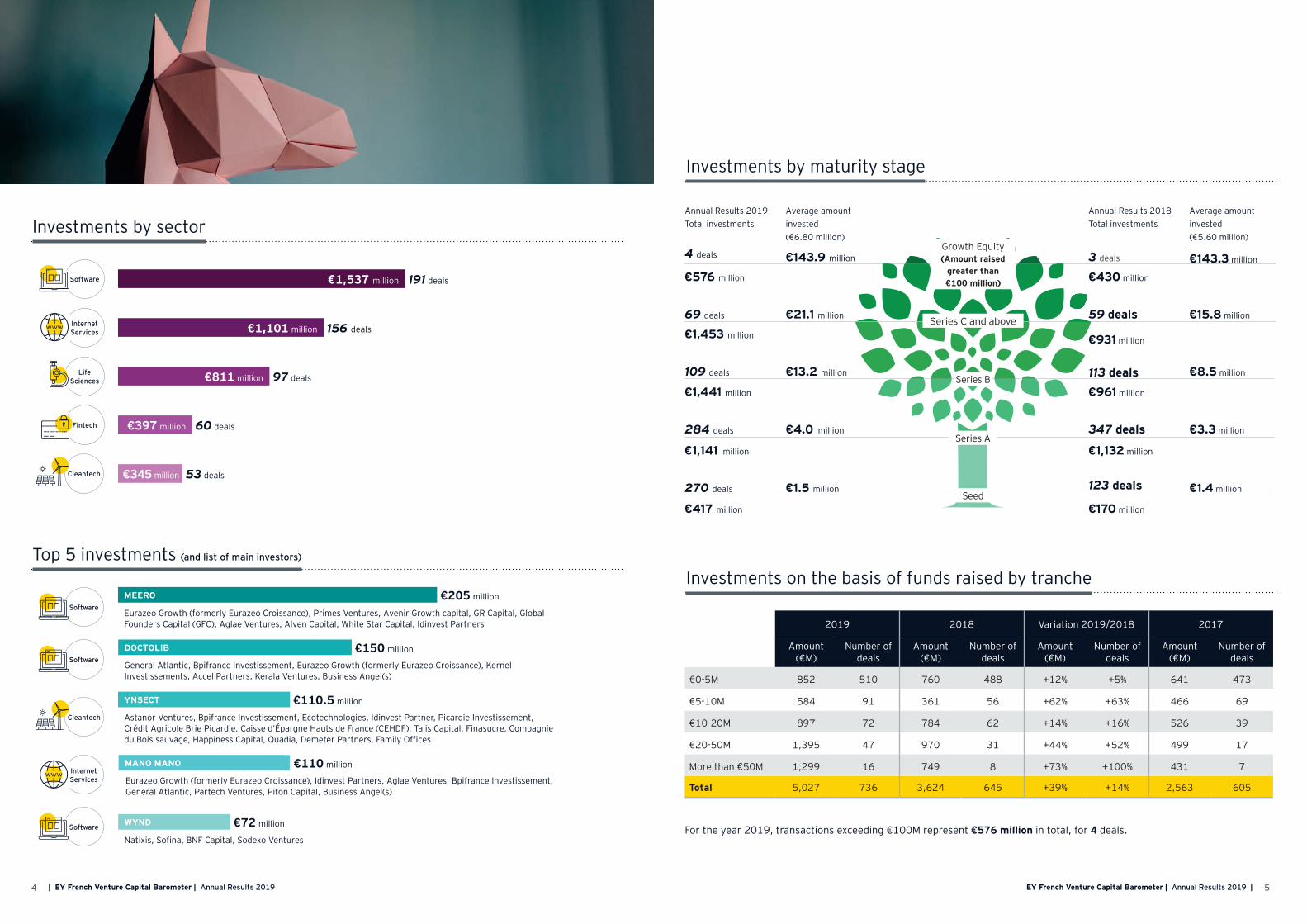

The Top 5 for the year 2019, identical to that published by EY at the end of the first half of the year, is made up of Meero, with €205 million of funds raised, Doctolib (€150 million), Ynsect (€110.5 million), Mano Mano (€110 million) and Wynd (€72 million).

In terms of the sector, software companies stand out, posting a meteoric 206% increase in funds raised, which amounted to €1.5 billion compared with just €745 million a year earlier, followed by internet services (€1.1 billion, stable). The Life Sciences companies also posted very good growth (€811 million versus €574 million, +41%). This growth is mainly due to the virtual absence of IPOs in this sector in 2019.

Two factors explain these very good results: an increase in the average round value, which rose this year from €5.5 million to €6.8 million; a 60% jump in volume and value of rounds over €20 million.

Île-de France remains the driver of the French economyGeographically, Île-de-France remains the undisputed regional leader of this ecosystem, with its start-ups accounting for 70% of the amounts raised and 59% of deals in 2019. Lagging way behind is the Auvergne-Rhône-Alpes region, which retained second place with 8% of investments in terms of value (10% in terms of number), followed by the Provence-Alpes-Côte d’Azur region, which takes third place with 6% of investments in terms of both value and number, followed by Hauts-de-France and Occitania this year.

No Brexit effectAt European level, it has to be said that, for the time being, Brexit has not yet altered the United Kingdom’s power of attraction. In fact, investments increased by 55% - compared with an increase of 7% in 2018 (€7.4 billion) - to €11.4 billion in 2019. The United Kingdom remains the European champion in Growth Capital, i.e. fund-raising deals exceeding €100 million, with 13 deals in this segment, totalling €4.1 billion (+273% year-on-year).

Behind the United Kingdom, while France is outshining Germany in terms of total number of deals in the Venture Capital segment (<€100 million raised), it is being outperformed in Growth Equity. In fact, in this segment alone, Germany attracted five times more funds than France (€2.9 billion compared with €0.6 billion for France). This is all the more remarkable given that between 2018 and 2019, while France only slightly increased in value, Germany managed to more than double the number of its deals (12 vs 5) and to multiply the amounts from deals exceeding €100 million by 2.5.

Cruel comparison with the American and Asian marketsWhat can we expect from this new financial year? In 2020, #FrenchTech should again be able to deliver on its promises. Even though some people think that money is too abundant, it is clear that in comparison with some other European countries, especially with what is happening in America or Asia, that is not the issue. In 2020, the challenge remains the same as in previous years: to enable the creation of undisputed leaders who will be able to meet the challenges of the future, in France, in Europe and throughout the world.

Franck SebagPartner, EY & Associés In charge of the Fast Growing Companies sector Western Europe & Maghreb

1st semester 2nd semester

20162015

€1.01 billion

(297 deals)

€1.2 billion

(277 deals)

€2.21 billionfor 574 deals

€0.76 billion

(240 deals)

€1.05 billion

(244 deals)

€1.81 billionfor 484 deals

2017

€1.22 billion

(301 deals)

€1.35 billion

(304 deals)

€2.57 billionfor 605 deals

2018

€1.95 billion

(333 deals)

€1.67 billion

(312 deals)

€3.62 billionfor 645 deals

2019

Amounts raised by start-ups in France

+21%

+12%

+16%

+32%

+14%

+22% +24%

+61%

+41% +34%

+43%

+39%

€5.03 billionfor 736 deals

€2.79 billion

(387 deals)

€2.24 billion

(349 deals)

Editorial

4 | EY French Venture Capital Barometer | Annual Results 2019 5EY French Venture Capital Barometer | Annual Results 2019 |

Investments by maturity stage

Average amount invested (€5.60 million)

Annual Results 2018Total investments

Average amount invested (€6.80 million)

Annual Results 2019Total investments

€430 million

€143.3 million€143.9 million4 deals 3 deals

€576 million

€931 million

€15.8 million€21.1 million 59 deals69 deals

€1,453 million

€8.5 million€13.2 million 113 deals€961 million

109 deals

€1,441 million

€3.3 million€4.0 million 347 deals284 deals

€1,132 million€1,141 million

€1.4 million€1.5 million 123 deals270 deals

€170 million€417 million

Series B

Series C and above

Investments on the basis of funds raised by tranche

2019 2018 Variation 2019/2018 2017

Amount (€M)

Number of deals

Amount (€M)

Number of deals

Amount (€M)

Number of deals

Amount (€M)

Number of deals

€0-5M 852 510 760 488 +12% +5% 641 473

€5-10M 584 91 361 56 +62% +63% 466 69

€10-20M 897 72 784 62 +14% +16% 526 39

€20-50M 1,395 47 970 31 +44% +52% 499 17

More than €50M 1,299 16 749 8 +73% +100% 431 7

Total 5,027 736 3,624 645 +39% +14% 2,563 605

For the year 2019, transactions exceeding €100M represent €576 million in total, for 4 deals.

Investments by sector

Fintech €397 million 60 deals

Life Sciences €811 million 97 deals

Software 191 deals€1,537 million

Internet Services €1,101 million 156 deals

€345 million 53 dealsCleantech

Top 5 investments (and list of main investors)

€110.5 millionYNSECT

Astanor Ventures, Bpifrance Investissement, Ecotechnologies, Idinvest Partner, Picardie Investissement, Crédit Agricole Brie Picardie, Caisse d’Épargne Hauts de France (CEHDF), Talis Capital, Finasucre, Compagnie du Bois sauvage, Happiness Capital, Quadia, Demeter Partners, Family Offices

Cleantech

Eurazeo Growth (formerly Eurazeo Croissance), Primes Ventures, Avenir Growth capital, GR Capital, Global Founders Capital (GFC), Aglae Ventures, Alven Capital, White Star Capital, Idinvest Partners

€205 millionMEEROSoftware

WYND €72 million

Natixis, Sofina, BNF Capital, Sodexo VenturesSoftware

€150 millionDOCTOLIB

General Atlantic, Bpifrance Investissement, Eurazeo Growth (formerly Eurazeo Croissance), Kernel Investissements, Accel Partners, Kerala Ventures, Business Angel(s)

Software

Internet Services

€110 millionMANO MANO

Eurazeo Growth (formerly Eurazeo Croissance), Idinvest Partners, Aglae Ventures, Bpifrance Investissement, General Atlantic, Partech Ventures, Piton Capital, Business Angel(s)

Growth Equity(Amount raised

greater than €100 million)

Series A

Seed

6 | EY French Venture Capital Barometer | Annual Results 2019 7EY French Venture Capital Barometer | Annual Results 2019 |

Methodology

The EY Venture Capital Barometer for France includes the equity financing transactions of businesses at the set-up stage or during their initial years of existence, with transaction dates between 1 January and 31 December 2019 and published prior to 8 January 2020. Those French companies raised funds from French and/or foreign VCs. The French data presented in this survey is based on data from Dow Jones VentureSource, CFNEWS, Capital Finance and Dealroom.co. The data on Germany and the United Kingdom is based on Dealroom.co. Processing of this data and analysis were based on EY methodology and carried out by EY & Associés. All transactions in excess of €100M have been restated as Growth Equity.

Venture Capital includes all transactions below €100M. In this study we have only taken into consideration transactions in which the amount was disclosed publicly.The Internet services sector encompasses activities such as e-commerce, marketing and performance (lead, listing), geomarketing and mobile applications. The Life Sciences sector includes the biotech and medtech sectors. The Fintech sector includes start-ups using technology to reshape financial and banking services (on-line banking, crowd funding, new payment methods, etc.) The Technology sector encompasses activities such as hardware, semiconductors, etc.

Top 10 investments in Europe

Company Country Sector Amount (€M)

NORTHVOLT Sweden Energy 909

CITIZENM Netherlands Internet Services, transport 750

GREENSILL United Kingdom FinTech 728

GREENSILL United Kingdom FinTech 595

DELIVEROO United Kingdom Food 523

FERGENE Switzerland Health 518

UIPATH Romania Software, robotics 516

BABYLON HEALTH United Kingdom Health 500

VEEAM Switzerland Software, security 455

FLIXBUS Germany Transport 455

Δ: 2019/2018 variation on the amount raised

In 2019, the three most significant countries in total accounted for €22.55 billion of investments, i.e. 56% of all investments made in Europe in terms of value.

Comparison of investments in the United Kingdom, Germany and France

VENTURE CAPITAL

€7.26 billion raised 999 deals

GROWTH EQUITY

€4.17 billion raised 13 deals

€11.43 billion raised / Δ +55%

1,012 deals / Δ +44%

€5.03 billion raised / Δ +39%

736 deals / Δ +14%

Investments by region

Top 3 French regions

The Île-de-France region accounted for 70% of investments in terms of value for 2019.

The Auvergne-Rhône-Alpes region remained in 2nd place, with 8% of investments in terms of value, closely followed by the Provence-Alpes-Côte d’Azur region, which came in 3rd place with 6% of investments in terms of value.

€197 M

29

€140 M

30

HAUTS-DE-FRANCE

€58 M

18

€61 M

12

GRAND EST

€59 M

9

€20 M

7

BOURGOGNE FRANCHE-COMTÉ

€388 M

71

€267 M

54

AUVERGNE-RHÔNE-ALPES

€281 M

42

€145 M

36

PROVENCE-ALPES-CÔTE

D’AZUR

€149 M

42

€143 M

43

OCCITANIA

€130 M

20

€75 M

39

NOUVELLE-AQUITAINE

€78M

23

€39 M

25

PAYS DE LA LOIRE

€86 M

24

€71M

20

BRITTANY

€43 M

11

€11M

10

NORMANDY

€3,519 M

433

€2,648 M

366

ÎLE-DE-FRANCE

€34 M

11

€4 M

3

CENTRE-VAL DE LOIRE

€5.03 billion

€3.62 billion

736 645

2019 2018

Number of deals

Funds raised

€8 M

3

€0 M

0

CORSICA

VENTURE CAPITAL

€4.45 billion raised 732 deals

GROWTH EQUITY

€0.58 billion raised 4 deals

VENTURE CAPITAL

€3.14 billion raised 508 deals

GROWTH EQUITY

€2.95 billion raised 12 deals

€6.09 billion raised / Δ +39%

520 deals / Δ -13%

2018

€1.53 billion

10 deals €3.72 billion

24 deals

2019

Δ +243%Germany

€2.72 billion

28 deals

2018

€5.86 billion

38 deals

2019

Δ +216%United Kingdom

€749 million

8 deals

2018

€1.29 billion

16 deals

2019

Δ +173%France

Funds raised in excess of €50M in the United Kingdom, Germany and France

Δ: variation 2019/2018

ContactsEY | Assurance | Tax | Transactions | Advisory

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who together deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organisation, and may refer to one or more of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organisation, please visit www.ey.com.

© 2020 EY & Associés.All rights reserved.Studio BMC France - 1912BMC456.SCORE France No 2020-003.Photo credit: Unsplash, Shutterstock, Franck Dunouau.ED None.

Document printed in accordance with EY’s commitment to reduce its environmental footprint.

This publication is for general information only and is not intended to replace professional accounting, tax or other advice. You should consult your advisers on any specific matters.

ey.com/fr

Franck SebagPartner, EY & Associés Tel.: +33 (0)1 55 61 31 29 Email: [email protected]

Coralie ConstantMarketing, EYTel.: +33 (0)1 55 61 33 61Email: [email protected]

Quentin Hacquard Media Relations, EYTel.: +33 (0)1 55 61 35 47Email: [email protected]

Contacts