exploring financial instability through agent-based...

TRANSCRIPT

Exploring Financial InstabilityThrough Agent-based Modeling

Part 3: Summary and Future

Blake LeBaronInternational Business School

Brandeis University

Mini courseCIGI-INET: False Dichotomies

November 2012, Waterloo, Ontario

Where are we going?

LeBaron CIGI/INET November 2012 – 2 / 20

⊲ Part 1:

•What are agent-based models?

•Simple models from finance

⊲ Part 2:

•Adaptation and time series

•Heterogeneous gain learning

⊲ Part 3:

•Current directions in agent design and applications

•Empirical validation

• Instability and macro connections

Overview

LeBaron CIGI/INET November 2012 – 3 / 20

Agent Technology Issues

Empirical Validation

Related Interesting Models

Instability, Macroeconomics and Policy

Agent Technology Issues

Agent TechnologyIssues

Empirical Validation

Related InterestingModels

Instability,Macroeconomics andPolicy

LeBaron CIGI/INET November 2012 – 4 / 20

Levels of agent intelligence

LeBaron CIGI/INET November 2012 – 5 / 20

⊲ Simple agents

•Zero intelligence (ZI)

•Empirically driven

•Model driven (forced selling)

⊲ Sophisticated

•Adaptive/learning (how much?)

•Dynamic optimization

•Behavioral

Future/current advances

LeBaron CIGI/INET November 2012 – 6 / 20

⊲ Multiple asset markets

⊲ Networks

⊲ Asynchronous actions

Analytic models

LeBaron CIGI/INET November 2012 – 7 / 20

⊲ Important for estimation/understanding

⊲ Computational overlaps/testing

⊲ Problems for analytics?

•Distributions matter (hard to summarize)

• Infra marginal traders and pricing

•Emergence/reducibility

Software

LeBaron CIGI/INET November 2012 – 8 / 20

⊲ Standard languages (objective)

•C++

•Python

•Matlab

•netLogo

•Repast/Swarm

• · · ·

Empirical Validation

Agent TechnologyIssues

Empirical Validation

Related InterestingModels

Instability,Macroeconomics andPolicy

LeBaron CIGI/INET November 2012 – 9 / 20

Estimation

LeBaron CIGI/INET November 2012 – 10 / 20

⊲ Challenges

•Compute time

•Ergodicity/path dependence

•Model complexity/parameters

⊲ Techniques and data to use

•Experiments (Hommes (2010))

•Micro calibration

•Model identification/estimation/comparison

Cars H. Hommes. The heterogeneous expectations hypotheis: Some evidence from

the lab. Technical report, CeNDEF, University of Amsterdam, 2010

Some estimated models

LeBaron CIGI/INET November 2012 – 11 / 20

⊲ Alfarano et al. (2005)Lux/Marchesi

⊲ Boswijk et al. (2007)Long term stock market mean reversion

⊲ Kouwenberg and Zwinkels (2010)Real estate

⊲ Westerhoff and Reitz (2003)Foreign exchange

⊲ Winker and Gilli (2001)Kirman model

Readings

LeBaron CIGI/INET November 2012 – note 1 of slide 11

S. Alfarano, T. Lux, and F. Wagner. Estimation of agent-based models: The case of an asymeetric herding model. Computational Eco-nomics, 26(19-49), 2005

H. Peter Boswijk, Cars H. Hommes, and Sebastiano Manzan. Behavioral heterogeneity in stock prices. Journal of Economic Dynamicsand Control, 31(6):1938–1970, 2007

Roy Kouwenberg and Remco C. J. Zwinkels. Chasing trends in the u.s. housing market. Technical report, Erasmus Univeristy, Rotterdam,The Netherlands, 2010

F. H. Westerhoff and S. Reitz. Nonlinearities and cyclical behavior: The role of chartists and fundamentalists. Studies in NonlinearDynamics and Econometrics, 7, 2003

P. Winker and M. Gilli. Indirect estimation of the parameters of agent based models of financial markets. Technical Report 38, FAME, 2001

Validation

LeBaron CIGI/INET November 2012 – 12 / 20

⊲ Computational reliability

⊲ Docking (robust across software)

⊲ Benchmarks

⊲ Multiple time horizons

⊲ Interacting with data/people

⊲ Visualizations

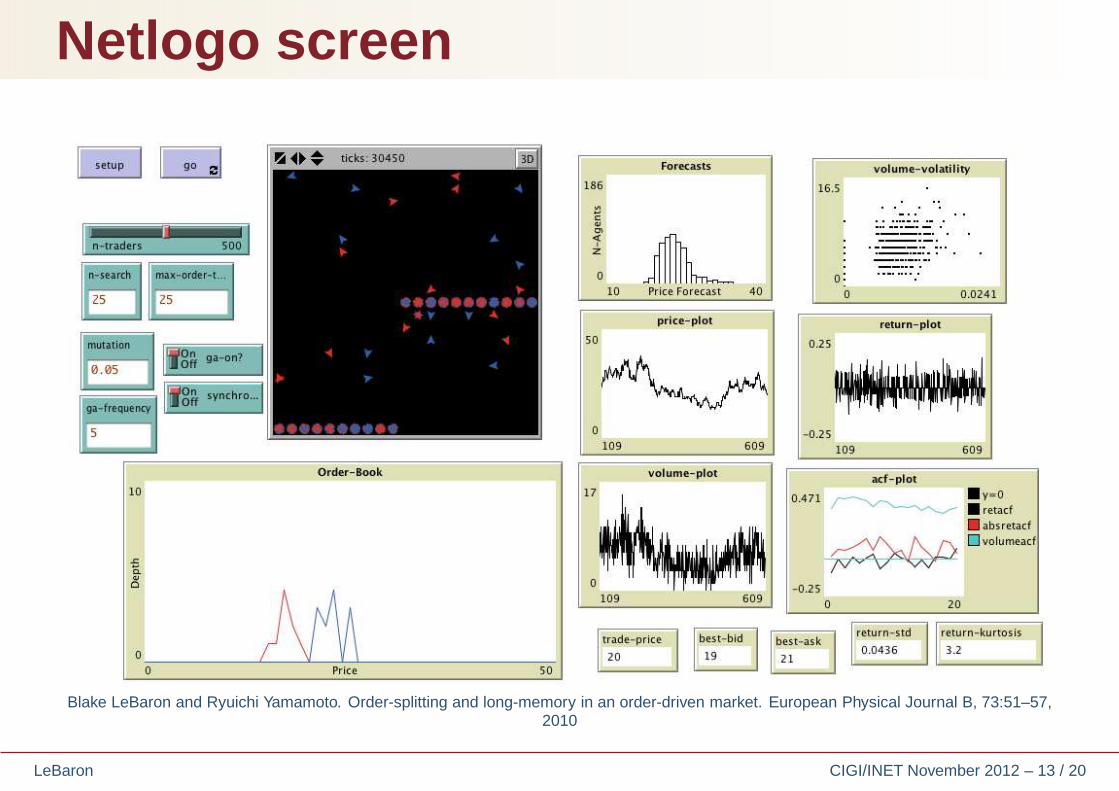

Netlogo screen

LeBaron CIGI/INET November 2012 – 13 / 20

Blake LeBaron and Ryuichi Yamamoto. Order-splitting and long-memory in an order-driven market. European Physical Journal B, 73:51–57,2010

Dynamic interfaces

LeBaron CIGI/INET November 2012 – 14 / 20

⊲ Visualization important

⊲ Flight simulators

⊲ Learning tools

Related Interesting Models

Agent TechnologyIssues

Empirical Validation

Related InterestingModels

Instability,Macroeconomics andPolicy

LeBaron CIGI/INET November 2012 – 15 / 20

Related recent finance/macro models

LeBaron CIGI/INET November 2012 – 16 / 20

⊲ Market microstructureChiarella et al. (2009)Cohen-Cole et al. (2010)

⊲ Real estateKhandani et al. (2009)Geanakoplos et al. (2012)

⊲ Labor marketsGuerrero and Axtell (2012)

Readings

LeBaron CIGI/INET November 2012 – note 1 of slide 16

Carl Chiarella, Giulia Iori, and Josep Perello. The impact of heterogeneous trading rules on the limit order book and order flows. Journalof Economic Dynamics and Control, 33:525–537, 2009

Ethan Cohen-Cole, Andrei Kirilenko, and Eleonora Patacchini. Are networks priced? Network topology and systemic risk in a high liquiditymarket. Technical report, Robert Smith School of Business, University of Maryland, 2010

John Geanakoplos, Robert Axtell, Doyne Farmer, Peter Howwitt, Ben Conlee, Jon Goldstein, Matthew Hendrey, Nathan Palmer, andChun-Yi Yang. Getting at systemic risk via an agent-based model of the housing market. American Economic Review, 102(3):1–9, 2012

Omar A. Guerrero and Robert L. Axtell. Unemployment volatility resulting from skew labor flow networks. Technical report, KrasnowInstitute for Advanced Study, George Mason University, 2012

Amir E. Khandani, Andrew W. Lo, and Robert C. Merton. Systemic risk and the refinancing ratchet effect. Technical report, MassachusettsInstitute of Technology, 2009

Market microstructure

LeBaron CIGI/INET November 2012 – 17 / 20

⊲ Well defined institutions

⊲ Important policy questions about stability

⊲ Empirical issues

•Persistence of signed order flows

•Persistence of volatility

•Uncorrelated returns

⊲ Does this matter at longer horizons?

Instability, Macroeconomicsand Policy

Agent TechnologyIssues

Empirical Validation

Related InterestingModels

Instability,Macroeconomics andPolicy

LeBaron CIGI/INET November 2012 – 18 / 20

Connecting to macroeconomics

LeBaron CIGI/INET November 2012 – 19 / 20

⊲ Macro channels: asset prices → investment

⊲ Volatility/shocks

•Too much?

•Realistic?

⊲ Institutions?

Policy uses

LeBaron CIGI/INET November 2012 – 20 / 20

⊲ Reduction and analysis

•Small versus large models

•Calibrated testbeds: Flash Crash

⊲ Breaking standard models

⊲ Resilient institutions