experience of indian corporates in implementation of ifrs ray.pdf · scenarios for transition...

TRANSCRIPT

© Infosys Technologies Limited 2007-08

Experience of Indian Corporates in

implementation of IFRS

2

Global developments

Global developments in the past:

• In December 2007, the United States Securities Exchange Commission

(SEC) proposed to allow foreign private issuers (Companies like Infosys,

Siemens, Wipro, etc.) to submit their financial statements in accordance

with International Financial Reporting Standards as issued by the

International Accounting Standards Board (“IFRS”) without reconciliation

to generally accepted accounting principles as used in the United

States. (“U.S. GAAP”).

• The companies could adopt IFRS regardless of whether its previous

financial statements were prepared in accordance with U.S. GAAP or in

accordance with the requirements of their home country regulations.

• The Institute of Chartered Accountants of India (“ICAI”) had issued a

Concept Paper on Convergence with IFRS in India which laid down the

roadmap to convergence by 2011.

3

Background of the Company..

Infosys has always set high standards in financial reporting and corporate

governance and has been on the fore front of innovation and change ..

• First Indian Company to complete public offering of ADSs in the United

States

• First Indian Company to be Sarbanes-Oxley compliant

• First Indian Company to file its XBRL statements under the SEC‟s

voluntary filing program

• First Indian Company to be a part of the major global indices like

NASDAQ-100 Index

• First Indian Company to file our primary financial statements in

compliance with International Financial Reporting Standards.

Scenarios for transition

Transition options available to a company adopting IFRS:

• Company filed its last Form 20-F (Annual Report) with SEC in

accordance with U.S. GAAP – It could transition to IFRS from

U.S. GAAP.

• Company filed its last Form 20-F (Annual Report) with SEC in

accordance with requirements of its home country regulations

– It could transition to IFRS from its local GAAP.

Selection of Previous GAAP required considerable thought as

IFRS 1, First time adoption of IFRS could be adopted only once

and certain benefits/ exemptions available under IFRS 1 could

be utilised only once.

4

Issues faced by Infosys upon transition

Selection of Previous GAAP:

• Historically, Infosys had provided its Indian shareholders financialstatements prepared in accordance with Indian GAAP and its holders ofits American Depositary Shares financial statements prepared inaccordance with U.S. GAAP.

• Adoption of U.S. GAAP as its Previous GAAP could have led to aproblem when India transitioned to IFRS in 2011. It could have resultedin a potential non-compliance for Indian statutory purposes on thepresumption that ICAI permitted only Indian GAAP to be adopted as theprevious GAAP

• As India has made a conscious decision to adopt IFRS it was prudent forthe Company to choose Indian GAAP as its Previous GAAP.

However the problem lied as there was no precedence to the same…

5

Issues faced by Infosys upon transition

Detailed discussions were held with the SEC and they agreed with the rationale provided by Infosys.

SEC suggested disclosure of certain additional information during the first year of our transition:

• Unaudited interim U.S. GAAP financial statements in compliance with SEC Regulations including the relevant footnotes in the interim quarterly reports.

• Reconciliations between U.S. GAAP and Indian GAAP in addition to the required reconciliations between Indian GAAP and IFRS.

Infosys has adopted IFRS for the fiscal year ending March 31, 2009 with a transition date of April 1, 2007. All interim filings (i.e. quarters ending June 30, 2008, September 30, 2008 and December 31, 2008) with the SEC have also been in compliance with IFRS.

6

Key exemptions availed by Infosys upon

First -Time Adoption

• Business combinations exemption - Non-application of IFRS 3,

Business Combinations, to business combinations consummated

prior to April 1, 2007.

• Goodwill stated at carrying value as per Previous GAAP

• Intangible Assets remaining subsumed in Goodwill and were not

recognized separately.

• Share-based payment transaction exemption - Application of IFRS 2,

Share Based Payment, only to grants made after November 7, 2002

and that remained unvested as at the date of transition.

• Vesting of all stock options under the 1998 and 1999 were

accelerated on March 12, 2007.

• Share based payment charges for only stock options granted to IBPO

employees on March 12, 2007 was required to be recognized.

7

Approach taken for IFRS adoption

• Transactions affecting equity were analyzed since 1999 under U.S.GAAP, Indian GAAP and IFRS.

• A complete equity balance break up was drawn up upto the date oftransaction under IFRS by giving effect of appropriate transactions at thehistoric rate where exemptions were not available.

• IFRS 1, required only an equity reconciliation. Our approach was tocarry out a complete reconciliation of each asset and liability to provide afull picture and detailed explanation to the investors.

• Two way reconciliation as required by SEC i.e. Indian GAAP to IFRS andU.S. GAAP to Indian GAAP provided complete transparency toinvestors.

• Condensed approach not adopted even for the Interim FinancialStatements. Full disclosures as applicable to an Annual Report wereprovided.

8

Recent Developments in India

• A high level task force was set up in India to expedite the convergence

process India

• 2 Committees were constituted

Technical Committee

CFO Sub Group

• Extensive Research and surveys were carried out to understand the state of

readiness of the companies on adoption of IFRS.

9

Status of Sensex 30 and Nifty Companies

• The survey results depicted that the majority of the SENSEX 30 and Nifty 50

companies were already in a state of readiness and most of them had

completed pilot phase

• Initiatives had been taken by Organizations like Indian Banking Association

and Insurance Regulatory and Development Authority (IRDA) to ensure that

the banking Companies and the Insurance Companies are geared up for

IFRS Adoption.

10

Status of Readiness of SME

• Concerns were raised in survey by the Small and Medium Scale

Enterprises as the new concepts under IFRS were unclear to them.

• Fair Valuation led to apprehensions within small scale community.

11

The Approach taken on Convergence

MCA wide Press Release dated 22nd January 2010, issued the proposed time lines

for convergence of IFRS. Details are given below:

12

Questions which arose consequent to the Circular

• What would be the transition date for companies who have already adopted

IFRS?

• If, subsequent to the adoption, the company does not meet the IFRSadoption criteria, should it discontinue IFRS?

• What is included in the „Net worth‟ and how to determine that?

• Is there any option to choose the IFRS v/s Indian converged accounting

standards where differences exist?

• Does the Conversion Road Map make it mandatory for all companies,including unlisted companies to prepare CFS?

• What about changes required for other laws and regulations (i.e.) TaxationLaws, SEBI & RBI Regulations, etc.?

13

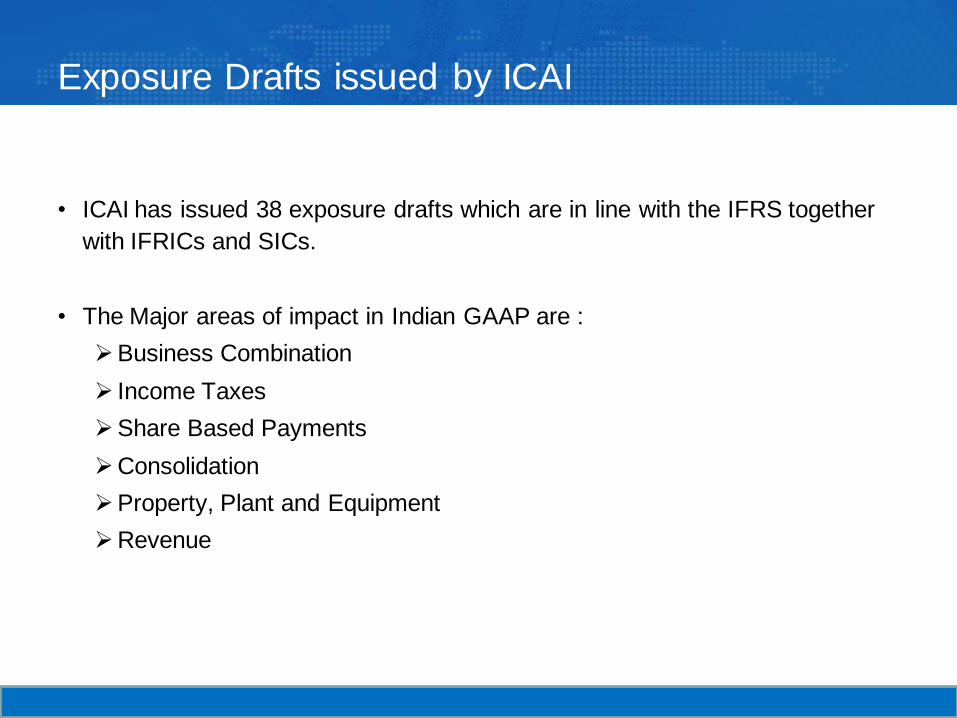

Exposure Drafts issued by ICAI

• ICAI has issued 38 exposure drafts which are in line with the IFRS together

with IFRICs and SICs.

• The Major areas of impact in Indian GAAP are :

Business Combination

Income Taxes

Share Based Payments

Consolidation

Property, Plant and Equipment

Revenue

14

Major Exemptions granted for First Time Adoption

• Business Combination

• Share Based Payments

• Property, Plant and Equipment

• Cumulative Translation Differences

15

Changing Roadmap of IFRS

The IFRS scenario is constantly changing even as we speak..

• Highlights of the Staff Draft “Financial Statement Presentation”

released jointly by the IASB and FASB:

• Presentation of cohesive set of financial statements i.e. aligning

each line items, its description and order of presentation across

the statement of financial position, comprehensive income

statement and cash flow statement.

• Mandatory preparation of Direct Cash flows

• Disaggregation Principle

• Sample Statement of financial position on adoption of this

standard would look like-

16

Changing Roadmap of IFRS

17

As at

BUSINESS

Operating

Short-term assets

Total short-term assets -

Long-term assets

Total long-term assets -

Short-term liabilities

Total short-term liabilities -

Long-term liabilities

Total long-term liabilities -

Net operating assets -

Investing

Assets

Total investing assets -

NET BUSINESS ASSETS -

FINANCING

Assets

Total financing assets -

NET FINANCING ASSETS -

INCOME TAXES

NET INCOME TAX ASSETS -

NET ASSETS -

EQUITY

Share capital

Retained earnings

Other components of equity

TOTAL EQUITY -

Exposure Draft on Employee Benefits

Salient Features of the Exposure Draft

• Mandatory immediate recognition of all actuarial gains and

losses through OCI

• Classification of interest costs net of gains as Finance Costs.

• Measurement of Interest on Plan Assets at the discount rate

18

Need of the hour..

Corporates need to gear themselves for constant updation and

not only for the first time adoption:

• Keep track of changes at IASB

• Broadening the pool of trained resources, both in the industry

and the audit firms.

• Active participation in the standard setting process by

commenting on the Exposure Drafts and Staff Drafts

• Management would need to spend significant time and efforts

in order to educate the investors, lenders, analysts , Board of

Directors, regarding the impact of IFRS on the financial

position and performance .

19

20

Questions?

© Infosys Technologies Limited 2007-08 21

Thank you

www.infosys.com

22

Additional Information

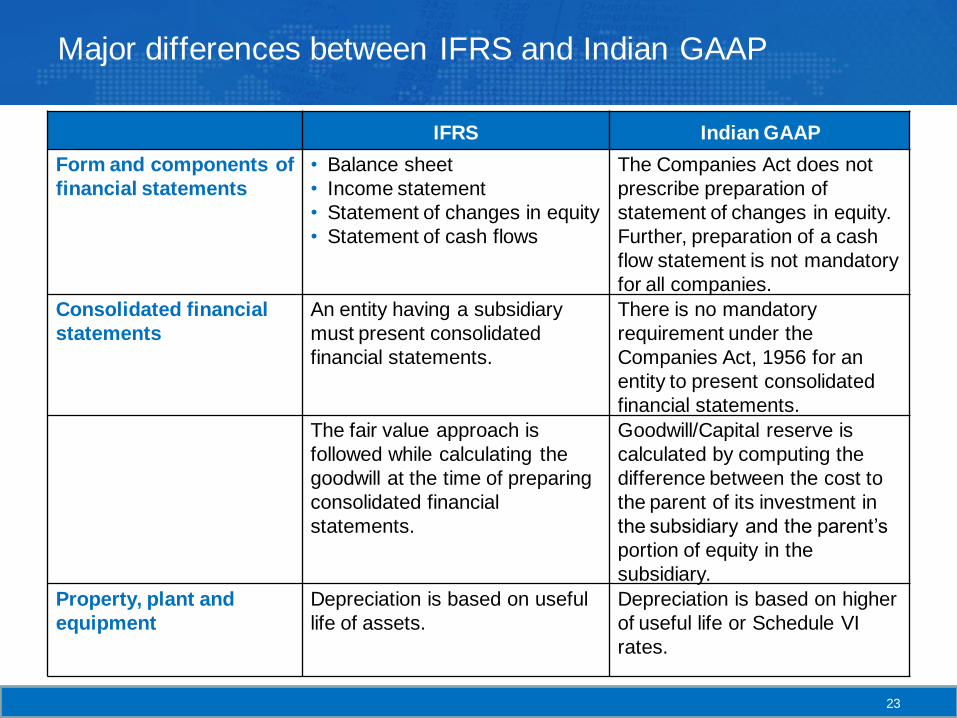

Major differences between IFRS and Indian GAAP

IFRS Indian GAAP

Form and components of

financial statements

• Balance sheet

• Income statement

• Statement of changes in equity

• Statement of cash flows

The Companies Act does not

prescribe preparation of

statement of changes in equity.

Further, preparation of a cash

flow statement is not mandatory

for all companies.

Consolidated financial

statements

An entity having a subsidiary

must present consolidated

financial statements.

There is no mandatory

requirement under the

Companies Act, 1956 for an

entity to present consolidated

financial statements.

The fair value approach is

followed while calculating the

goodwill at the time of preparing

consolidated financial

statements.

Goodwill/Capital reserve is

calculated by computing the

difference between the cost to

the parent of its investment in

the subsidiary and the parent‟s

portion of equity in the

subsidiary.

Property, plant and

equipment

Depreciation is based on useful

life of assets.

Depreciation is based on higher

of useful life or Schedule VI

rates.

23

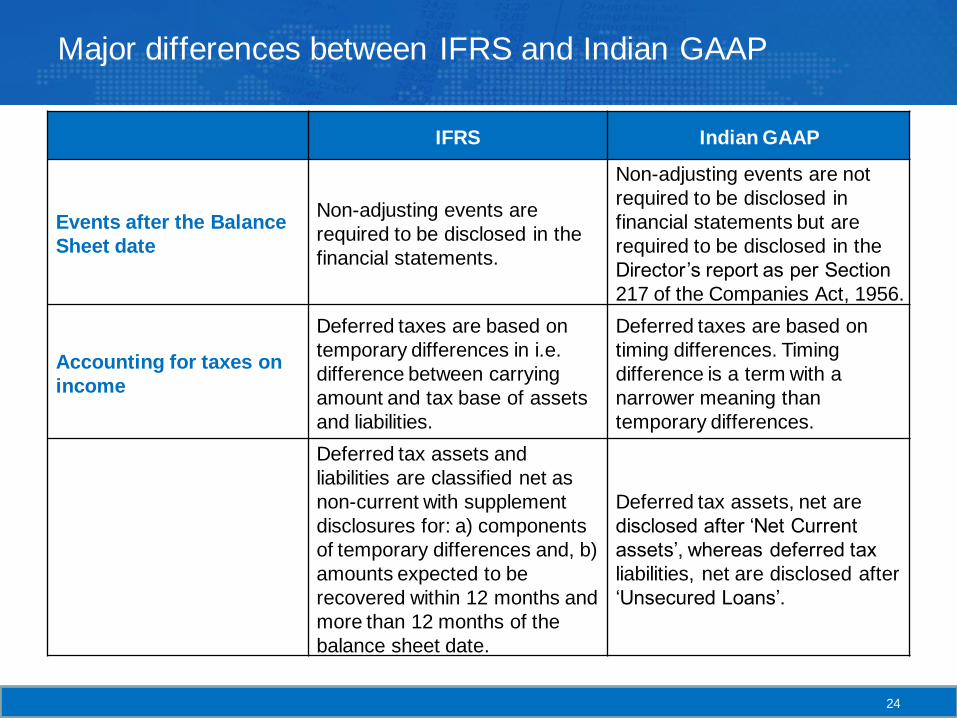

Major differences between IFRS and Indian GAAP

IFRS Indian GAAP

Events after the Balance

Sheet date

Non-adjusting events are

required to be disclosed in the

financial statements.

Non-adjusting events are not

required to be disclosed in

financial statements but are

required to be disclosed in the

Director‟s report as per Section

217 of the Companies Act, 1956.

Accounting for taxes on

income

Deferred taxes are based on

temporary differences in i.e.

difference between carrying

amount and tax base of assets

and liabilities.

Deferred taxes are based on

timing differences. Timing

difference is a term with a

narrower meaning than

temporary differences.

Deferred tax assets and

liabilities are classified net as

non-current with supplement

disclosures for: a) components

of temporary differences and, b)

amounts expected to be

recovered within 12 months and

more than 12 months of the

balance sheet date.

Deferred tax assets, net are

disclosed after „Net Current

assets‟, whereas deferred tax

liabilities, net are disclosed after

„Unsecured Loans‟.

24

Major differences between IFRS and Indian GAAP

IFRS Indian GAAP

Interim Financial reporting IFRS does not require public

entities to furnish interim

financial statements, though it

encourages interim reporting.

The listing agreement in India

requires all listed companies to

furnish interim financial results

on a quarterly basis.

Employee benefits In IFRS, IAS 19, provides an

option with regard to recognition

of actuarial gains and losses i.e.

in equity or profit and loss

account.

AS 15 Revised does not provide

any option with regard to

recognition of actuarial gains and

losses. It requires such gains

and losses to be recognized

immediately in the statement of

profit and loss.

Share-based payments Share- based payments are

accounted as per Fair Value

method.

Share- based payments are

accounted as per the Guidelines

issued by SEBI and the

Guidance note on accounting for

employee share-based

payments both of which permit

the use of Intrinsic Value method

as an alternate to the Fair value

method.

25

Major differences between IFRS and Indian GAAP

IFRS Indian GAAP

Accounting policies, errors

and estimates

Accounting policy changes and

corrections of prior period errors

are accounted for retrospectively

by restating equity and

comparatives, unless

impracticable.

There is no concept of re-

statement of comparatives except

in financial statements prepared for

certain specific purposes like public

offers.

Business combination Business combination has a wider

scope and are accounted using

the purchase accounting method.

Indian GAAP deals only with

amalgamations and there is liberal

use of pooling of interests method

which in not permitted under IFRS.

Inventories IFRS requires same cost formula

to be used for all inventories

having a similar nature and use.

Where inventories have a different

nature and use, different cost

formulas may be justified.

Indian GAAP provides that the

cost of inventories should be

assigned by using FIFO, or

weighted average cost formula.

26

Major differences between IFRS and Indian GAAP

IFRS Indian GAAP

The Effects of Changes in

Foreign Exchange Rates

An entity measures its assets,

liabilities, revenues and

expenses in its functional

currency, i.e. the currency of the

primary economic environment

in which the entity operates.

Functional currency of an entity

may be different from the local

currency.

In Indian GAAP, there is no

concept of functional currency.

Financial statements need to be

in Indian Rupees only.

Related party

transactions

IFRS provides for including non-

executive director under key

management personnel.

A non-executive director of a

company should not be

considered as a key

management person by virtue of

merely his being a director

unless he has the authority and

responsibility for planning,

directing and controlling the

activities of the enterprise.

27

Reconciliations- Indian GAAP- IFRS

STATEMENTOF FINANCIAL POSITION

April 1, 2007 March 31, 2008

Indian GAAP IFRS Indian GAAP IFRS

Goodwill 137 152 172 174

Intangibles - - - 11

Equity 2,611 2,722 3,448 3,916

28

April 1, 2007

• Goodwill of $4 million• Deferred purchase agreement entered with the minority shareholders of Infosys BPO in February

2007, to purchase equity shares of Infosys BPO by February 2008 did not qualify as an investmentunder Company Law.

• The same was recognized in IFRS as the risks and rewards of ownership were considered transferredin February 2007 itself.

• Goodwill Offset of $11 million- Gains from changes in proportionate share of subsidiary resulting fromissuance of stock by subsidiary was offset against goodwill under Previous GAAP was grossed up in equity

in IFRS.

• Retained Earnings $101- Liability for dividends (incl. corporate dividend tax) declared and approved after

the reporting period are not recognized in IFRS.

Indian GAAP- IFRS

March 31, 2008

• Intangible assets of $11 million - Customer contract upon acquisition was included in

goodwill under Previous GAAP, have been recognized separately under IFRS.

• Retained earnings of $456 million - Liability for dividends (incl. corporate dividend tax)

declared and approved after the reporting period, are not recognized under IFRS.

• Share-based compensation of $3 million - Share based compensation for grants made to

IBPO employees was recognized in IFRS.

• INCOME STATEMENT- No significant impact

• Share-based compensation of $3 million for grants made to IBPO employees was

recognized in IFRS.

• CASH FLOWS- Minor presentational impacts

• Interest and dividends received may be classified as operating, investing or financing

activities under IFRS. However, Indian GAAP mandates the classification of such cash flows

under Investing activities.

29

Reconciliations- U.S. GAAP- Indian GAAP

STATEMENTOF FINANCIAL POSITION

April 1, 2007 March 31, 2008

US GAAP Indian GAAP US GAAP Indian GAAP

Goodwill 128 137 172 172

Intangibles 20 - - -

Equity (including minority) 2,717 2,611 3,448 3,448

30

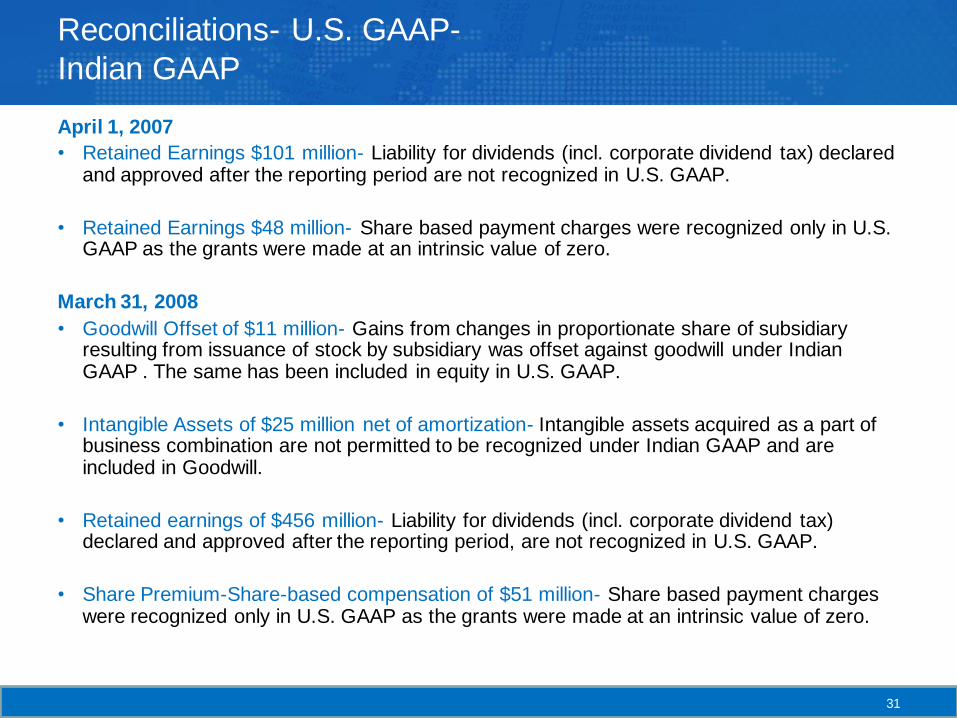

April 1, 2007

• Goodwill of $4 million

• Deferred purchase agreement entered with the minority shareholders of Infosys BPO in

February 2007, to purchase equity shares of Infosys BPO by February 2008 did not qualify as

an investment under Company Law.

• The same was recognized in U.S. GAAP as the risks and rewards of ownership were

considered transferred in February 2007 itself.

• Goodwill Offset of $11 million: Gains from changes in proportionate share of subsidiary resulting

from issuance of stock by subsidiary was offset against goodwill under Indian GAAP which had

been presented in equity in U.S. GAAP.

• Intangible Assets of $20 million net of amortization - Intangible assets acquired as a part of

business combination are not permitted to be recognised under Indian GAAP and included in

Goodwill.

Reconciliations- U.S. GAAP-

Indian GAAP

April 1, 2007

• Retained Earnings $101 million- Liability for dividends (incl. corporate dividend tax) declared and approved after the reporting period are not recognized in U.S. GAAP.

• Retained Earnings $48 million- Share based payment charges were recognized only in U.S. GAAP as the grants were made at an intrinsic value of zero.

March 31, 2008

• Goodwill Offset of $11 million- Gains from changes in proportionate share of subsidiary resulting from issuance of stock by subsidiary was offset against goodwill under Indian GAAP . The same has been included in equity in U.S. GAAP.

• Intangible Assets of $25 million net of amortization- Intangible assets acquired as a part of business combination are not permitted to be recognized under Indian GAAP and are included in Goodwill.

• Retained earnings of $456 million- Liability for dividends (incl. corporate dividend tax) declared and approved after the reporting period, are not recognized in U.S. GAAP.

• Share Premium-Share-based compensation of $51 million- Share based payment charges were recognized only in U.S. GAAP as the grants were made at an intrinsic value of zero.

31

Reconciliations- U.S. GAAP- Indian GAAP

INCOME STATEMENT

• Share-based compensation of $3 million- Share-based

compensation for grants made to IBPO employees was

recognized in U.S. GAAP but not in Indian GAAP.

• Amortization of Intangible Assets of $8 million- Intangible

assets subsumed in Goodwill were never amortized in Indian

GAAP.

CASH FLOWS- Only presentational impacts

• Interest and dividends received are classified under operating

activities in U.S. GAAP. However, Indian GAAP mandates the

classification of such cash flows under Investing activities.

32