expats: in & out of australia - payroll

TRANSCRIPT

EXPATS: IN & OUT OF AUSTRALIA

19 October 2017

Alice Chudowolski– Senior Manager, Employment Taxes James Ortner – Senior Manager, Global Mobility

Page 2 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

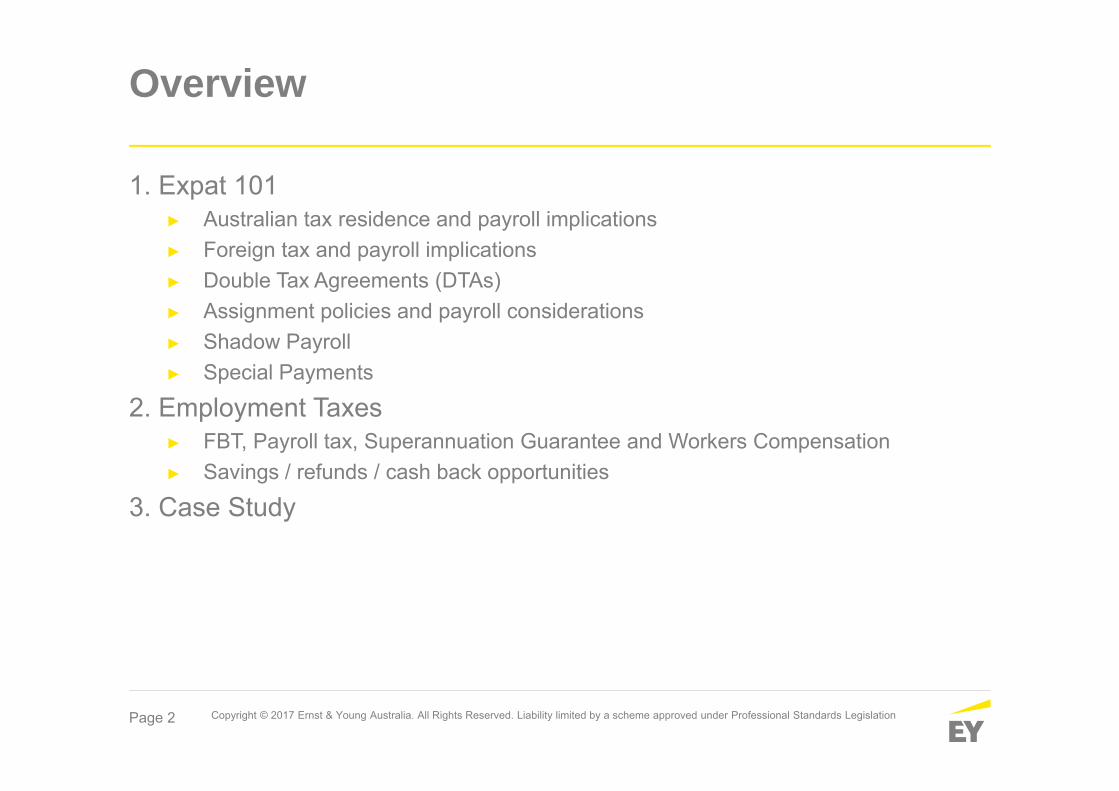

Overview

1. Expat 101► Australian tax residence and payroll implications► Foreign tax and payroll implications► Double Tax Agreements (DTAs)► Assignment policies and payroll considerations► Shadow Payroll► Special Payments

2. Employment Taxes► FBT, Payroll tax, Superannuation Guarantee and Workers Compensation► Savings / refunds / cash back opportunities

3. Case Study

Expat 101

James Ortner

Page 4 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Ordinary Resident

Temporary Resident

Expat 101: Australian tax residence

Non-resident

How does tax residence impact payroll?

RESIDENT

Page 5 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Expat 101: Australian tax residence cont.

Resident (including Temporary Resident)

• Maintains place of abode in Australia

• Continuing strong ties (family and economic) in Australia

Non –resident

• Reside out of Australia 2+ years

• Family will accompany• Sets up overseas place of

abode• Spends less than 183 days

Inbound Outbound Ordinary Resident

• Australian citizen or permanent resident

• Spends greater than 183 days

Temporary Resident

• Temporary visa holder e.g. 457 visa holder

• Spends greater than 183 days

Non – resident • Spends less than 183 days

Ordinary Resident

Worldwide employment income

Temporary Resident

Worldwide employment income

Non-resident

Australian sourced employment income

Page 6 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Expat 101: Australian payroll implications

Residency statusPayroll implications

Taxable employment income

Resident YesWorldwide employment

income

Temporary resident YesWorldwide employment

income

Non-resident YesBased on Australian

workdays*

► Payroll implications exist for all residency types► You need to have access to expat compensation data

*Unless Double Tax Agreement (DTA) exemption is available

Page 7 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Expat 101: Foreign tax implications

► Each country has their own rules to assess taxability of an individual

► May be based on residence, day count thresholds or presence

Country Top tax rate Considerations

UK 45%If work days > 1 tax implication. Statutory residence test applies

USA39.6% Federal and State

tax rate variesUS Citizens/Green Card taxable

else based on days present

New Zealand 33% If work days > 1 tax implication

Singapore 22%If days > 60 filing implication. If

days > 183 tax implication

Hong Kong 17% If work days > 1 tax implications

Page 8 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Expat 101: Foreign payroll implications

CountryWithholding tax required

Penalties for non-withholding

UK

USA

New Zealand

Singapore × n/a

Hong Kong × n/a

► Employers may have foreign payroll implications based on the requirements of each country

► Withholding tax and social security may need to be calculated on worldwide income

► Your payroll teams overseas need to have access to expat compensation data including benefits

Page 9 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Expat 101: Double Tax Agreements (DTA)

► Bi-lateral agreements between two countries addressing cross-border taxation

► Provides guidance on:► residence determinations; and ► alleviation of double taxation.

► May allow for remuneration to be exempt from tax in a host country if presence is below 183 days* and other conditions met

► Australia adopts Economic Employer concept► If services are integrated into the activities of an Australian entity

more than the overseas entity, then the Australian entity may be the “economic employer”. This means that no exemption is allowed.

Page 10 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Tax Equalised

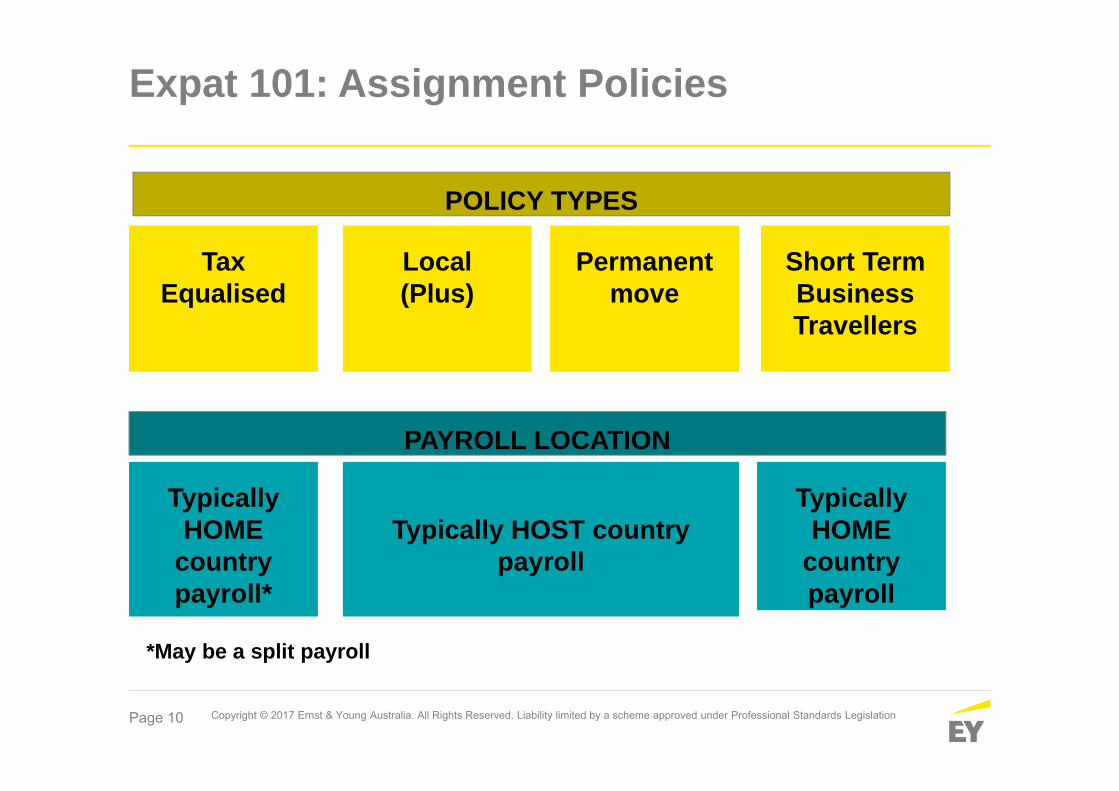

Expat 101: Assignment Policies

Typically HOME

country payroll*

Typically HOST country payroll

PAYROLL LOCATION

POLICY TYPES

Local (Plus)

Short Term Business Travellers

Permanent move

Typically HOME

country payroll

*May be a split payroll

Page 11 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Expat 101: Assignment Policy and Payroll

Tax Equalised

Hypothetical tax payroll withheld

Benefits provided

Employer may fund tax liabilities in host country

Local (Plus)

Short Term Business Travellers

Permanent move

Benefits provided

Employer may fund tax liabilities on certain benefits

Usually same as resident employee –may have relocation benefits

Benefits provided

Employer may fund tax liabilities in host country

Home or Split between Home

and HostHost Payroll

PAYROLL LOCATION

Home payroll

Page 12 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Expat 101: Shadow Payroll

► Shadow payroll is a notional or phantom payroll► Allows employers to meet withholding tax obligations

when their employees are paid through home payroll► Gross up of tax liability = no FBT► Operation of shadow payroll facilitates other employer

obligations:► Pay-As-You-Go (PAYG) withholdings► Payroll tax► Superannuation ► Fringe Benefits Tax

► Key that payroll has access to compensation and benefits data from home and host

Page 13 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Expat 101: Special Payments

Employee Share Schemes (Equity)

• Equity has country specific tax rules on timing of taxation and amount subject to tax• Australia has no PAYG withholding tax on equity• Other countries have withholding tax on equity• There may be tax due on equity for individuals in home and host locations

Trailing Bonuses

• Bonuses paid AFTER individual leaves country may be subject to withholding tax• There may be tax due in both home and host countries

Termination/Redundancy

• There are country specific tax rules and concessions for termination payments. • There may be tax due in both home and host countries

Page 14 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

457 Visa Reform

The Government announced that the Temporary Work (Skilled) visa (subclass 457 visa) will be abolished and replaced with the completely new Temporary Skill Shortage (TSS) visa in March 2018.

The TSS visa programme will be comprised of a Short-Term stream of up to two years and a Medium-Term stream of up to four years and will support businesses in addressing genuine skill shortages

Employment Taxes

Alice Chudowolski

Page 16 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Disruption

Payroll Systems Workforce Changes

Mobile WorkforceBusiness Transformation

Disruptors to Employment Taxes

Page 17 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Tax resident

Superannuation Guarantee

Payroll tax

Tax non-resident

How does tax residency impact employment taxes?

Residency implications

Page 18 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

FBT - Expat Benefits

Risks!

• LAFHA (International)No FBT Exemption

• Private Health InsuranceSubject to full FBT

• Superannuation to a Foreign FundPermanent Resident

Opportunities

• LAFHA (Domestic)Up to 12 months FBT exempt

• Leasing of Household GoodsCan be FBT Exempt

• Children’s Education CostsCan be FBT Exempt

• Home leave50% FBT reduction for one annual trip

Look out for theseOpportunities and Risks

when managing Expat Benefits!

Page 19 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

FBT - Exempt Relocation Benefits

► Lease of Household Goods

► Temporary Accommodation

► Sale and/or acquisition of permanent residence

► Connection/ reconnection of utilities following relocation

► Relocation transport

► Relocation consultant

► “Look & See” trips

FBT Savings!

FBT Savings!

Page 20 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

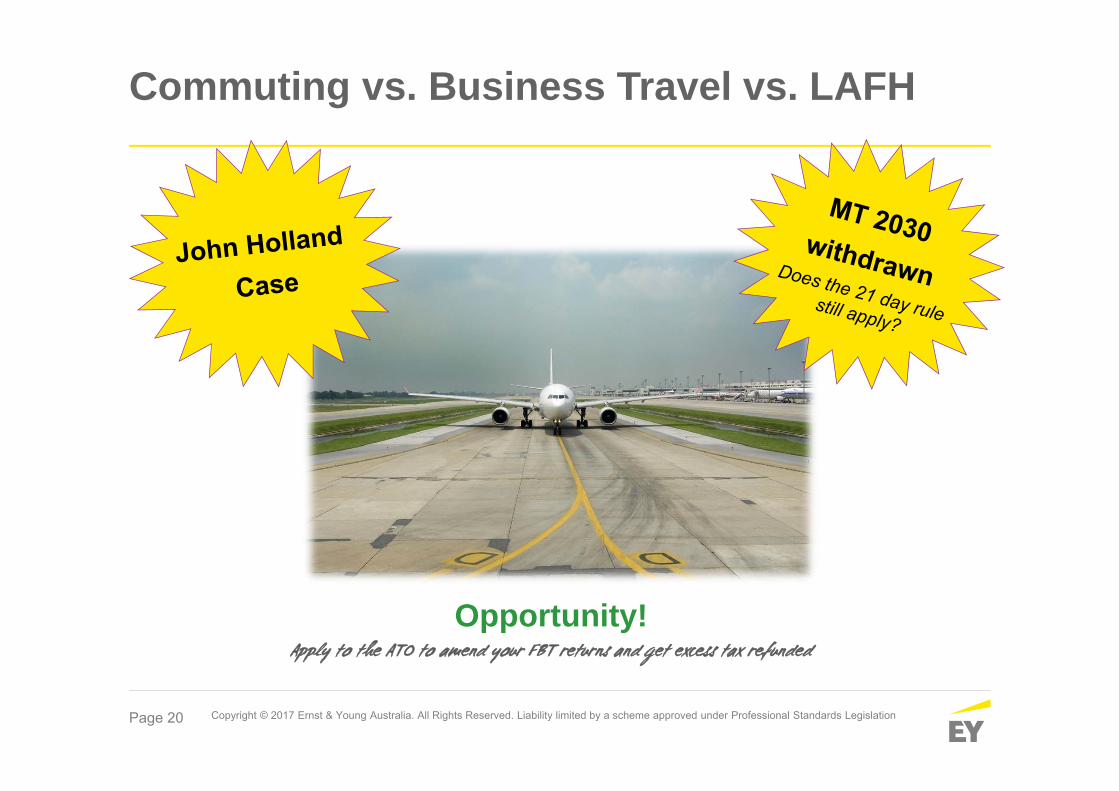

Commuting vs. Business Travel vs. LAFH

Opportunity!Apply to the ATO to amend your FBT returns and get excess tax refunded

Page 21 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

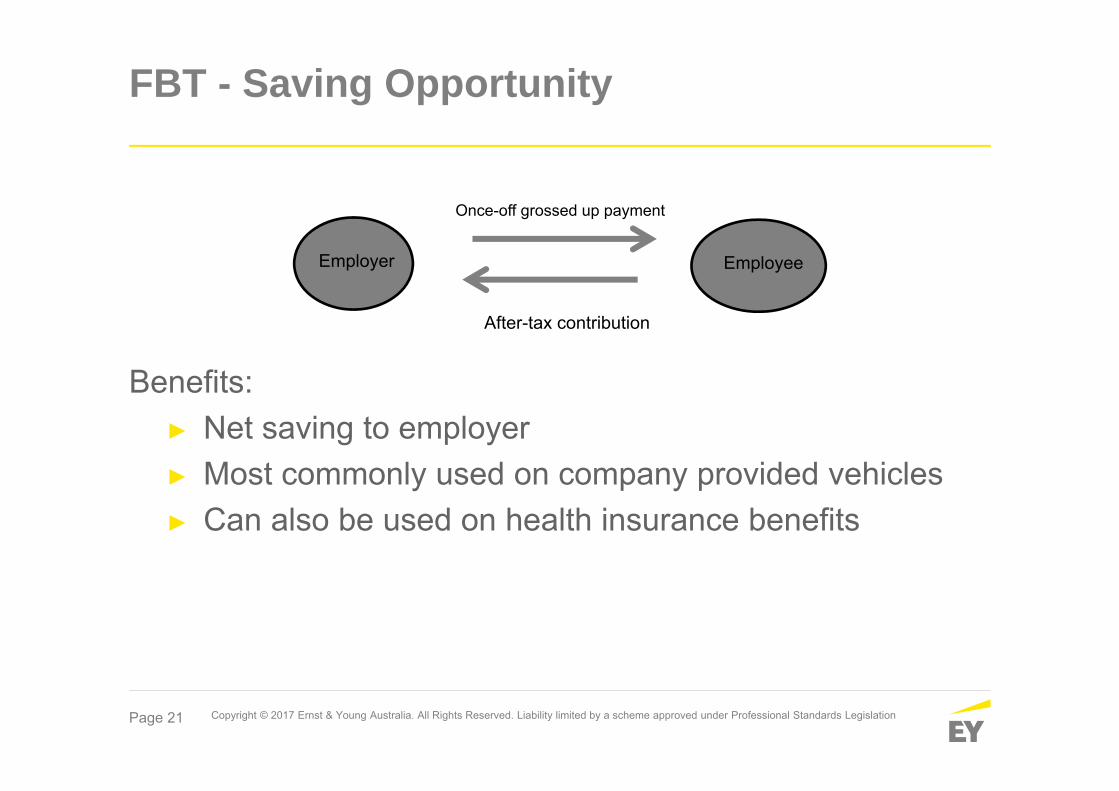

FBT - Saving Opportunity

Benefits:► Net saving to employer► Most commonly used on company provided vehicles► Can also be used on health insurance benefits

Once-off grossed up payment

After-tax contribution

Employer Employee

Page 22 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Opportunity Employee overseas

Time of grant

Opportunity Employee overseas

Time of vest

Payroll Tax – Employee Share Schemes

► You choose the taxing point: Grant or Vest/ Exercise

► Choice per person, per plan

► Consider the location of employee can result in payroll tax savings:

► When to choose Grant

► When to Choose Vest/ Exercise

Page 23 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Employment Taxes - Common Issues

Fringe Benefits Tax

LAFHA exemptions for overseas employees

Foreign Payroll

Superannuation Guarantee

Certificate of Coverage

Senior foreign executive exemption

Payroll Tax

Six month rule

Nexus provisions

Workers Compensation

Knowing when to get coverage

Page 24 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

► NSW Jobs Action Plan Rebate► Full Time Equivalent (FTE)

number of 50 or below► Businesses that hire new

employees► Applies separately to each

employing entity ► Rebate up to $6,000

► $2,000 on the first anniversary and $4,000 on the second anniversary

► Register up to 30 June 2019► Must apply within 90 days of hiring

Cash back opportunities - Are your expat numbers increasing?

Page 25 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

► Small business grant

► Small businesses (<$750,000)

► Hire new employees after 1 July 2015

Cash back opportunities – cont.

Page 26 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Best Practice – Payroll Data Analytics What can it do?

PAYG Withholding &

Superannuation

Payroll Tax

Contractors

Page 27 Copyright © 2016 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Summary: Temporary Assignments Benefits

Benefit provided International mobility into Australia

Domestic mobility within Australia

LAFH food X *LAFH rent X *Leasing household goods X *Children education costs -Home leave -Relocation consultant

Relocation costs(shipping, airfares etc.)

Temporary accommodation

? ?

* Individuals must maintain a home in Australia for their personal use for tax concessions to be available; 12 month max.

Page 28 Copyright © 2016 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Summary: FBT Exempt Relocation Benefits

Page 29 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Case Study – Background

► US citizen► On assignment from US to Australia for 2 years► Tax equalised assignment► Under a 457 temporary visa► Will receive salary, bonus and cash payments via US

payroll► Participates in an employee share scheme and will have

Restricted Stock Units (RSUs) vest during assignment► Assignment benefits provided by both US and Australia

entities

Page 30 Copyright © 2017 Ernst & Young Australia. All Rights Reserved. Liability limited by a scheme approved under Professional Standards Legislation

Case Study – Tax and Payroll implications

Considerations Australia Implications Basis

Residence Tax resident 2 year assignment

Tax implications Temporary resident and taxable on worldwideemployment income

457 temp work visa

Payroll Worldwide employment income is reportable Temporary resident

Pay As You Go (PAYG) A shadow payroll should be set up to satisfy PAYG obligations

Company has obligation as individual is taxable

Payroll Tax Payroll tax should be paid Tax resident

Fringe Benefits Tax (FBT) FBT should be paid on taxable benefits provided by both US and Australia

Tax resident

Superannuation Superannuation should be paid unless exempt (ie CoC or senior executive)

Tax resident

Equity (RSUs) Taxable at vest however no PAYG withholding required. Individual reports via tax return

Equity held whilst on Australia assignment

Double Tax Agreement (DTA) US will tax employment income including equity. Double taxation arises and DTA should be referenced to exempt income or provide relief.

US citizens are subject to tax on worldwide income.

Note: Separate US tax and payroll implications exist