exchange rate fluctuations and oil price … charles uche.pdfi title page effect of exchange rate...

TRANSCRIPT

EFFECT OF EXCHANGE RATE FLUCTUATIONS AND OIL PRICE SHOCKS: THE NIGERIAN EXPERIENCE, 1986 – 2008.

A

Ph.D THESIS

BY

UGWUANYI, CHARLES UCHE (PG/Ph.D/03/34674)

DEPARTMENT OF ECONOMICS UNIVERSITY OF NIGERIA, NSUKKA

i

TITLE PAGE

EFFECT OF EXCHANGE RATE FLUCTUATIONS AND OIL PRICE SHOCKS: THE NIGERIAN EXPERIENCE, 1986 – 2008.

BY

UGWUANYI, CHARLES UCHE (PG/Ph.D/03/34674)

THESIS SUBMITTED IN FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF DOCTOR OF PHILOSOPHY,

DEPARTMENT OF ECONOMICS, UNIVERSITY OF NIGERIA, NSUKKA.

JUNE, 2011

ii

APPROVAL

___________ __________ PROF. F.E. ONAH SIGNATURE DATE (SUPERVISOR) PROF. S.I. UDABA ____________ __________ (EXTERNAL EXAMINER) SIGNATURE DATE ____________________ _____________ __________ (INTERNAL EXAMINER) SIGNATURE DATE _____________ __________ PROF. C.C. AGU SIGNATURE DATE (HEAD OF DEPARTMENT) PROF. E.O. EZEANI ______________ __________ (DEAN OF THE FACULTY) SIGNATURE DATE

1

DEDICATION

TO THE ALMIGHTY GOD AND ALL ERUDITE

iii

2

ACKNOWLEDGEMENT

My sincere and profound gratitude goes to my supervisor Prof. F.E.

Onah in particular and in general to all the academic and non academic

staff of Department of Economics, University of Nigeria, Nsukka for their

unquantifiable contributions in my educational pursuit.

I am highly indebted to Dr. F.O. Asogwa for his painstaking

assistance and constructive criticisms to the work.

I equally recognize my ebullient professors of Economics; Professors

C.C. Agu (Head Department of Economics UNN), N.I. Ikpeze, O.E. Obinna,

Ukwu I. Ukwu and Dr. (Mrs.) Gladys Aneke whose words of advice and

encouragement put me through to this stage.

I also owe a lot of thanks to Dr. P.C. Omoke Messrs I.O. Agwu, N.U.

Onwukwe, Thom. Okoro, D. Nnachi, G.E. Onwe, C.C. Udude and other

colleagues in the Department of Economics, Ebonyi State University,

Abakaliki.

Also, special to be mentioned are E.R. Ukwueze, Joseph Nnadi, Jude

Chukwu, S.E. Ugwuanyi, Prof. O.S. Abonyi, Dr. E.S. Obe, Dr. B.M. Mba,

Dr. Boniface Ugwuishiwu, Dr. Oscar. O. Eze, Dr. O.C. Eze, S.G.

Edoumiekumo and a host of other friends and relations for their support. I

remain grateful.

iv

3

I am equally grateful to my computer operator Miss Chizoba

Ugwuoke for her dedication to the job.

My thanks equally go to Mrs. Veronica Ugwuanyi (Nee Agbowo) the

woman through whom I came to be), my wife Caroline Ugwuanyi and my

children Amuche, Chibueze, Ebuka, Elendu and Nchetachukwu for being

behind me through out the studies.

Above all, I remain grateful to Almighty God for giving me life and

good health.

Charles Uche Ugwuanyi

v

4

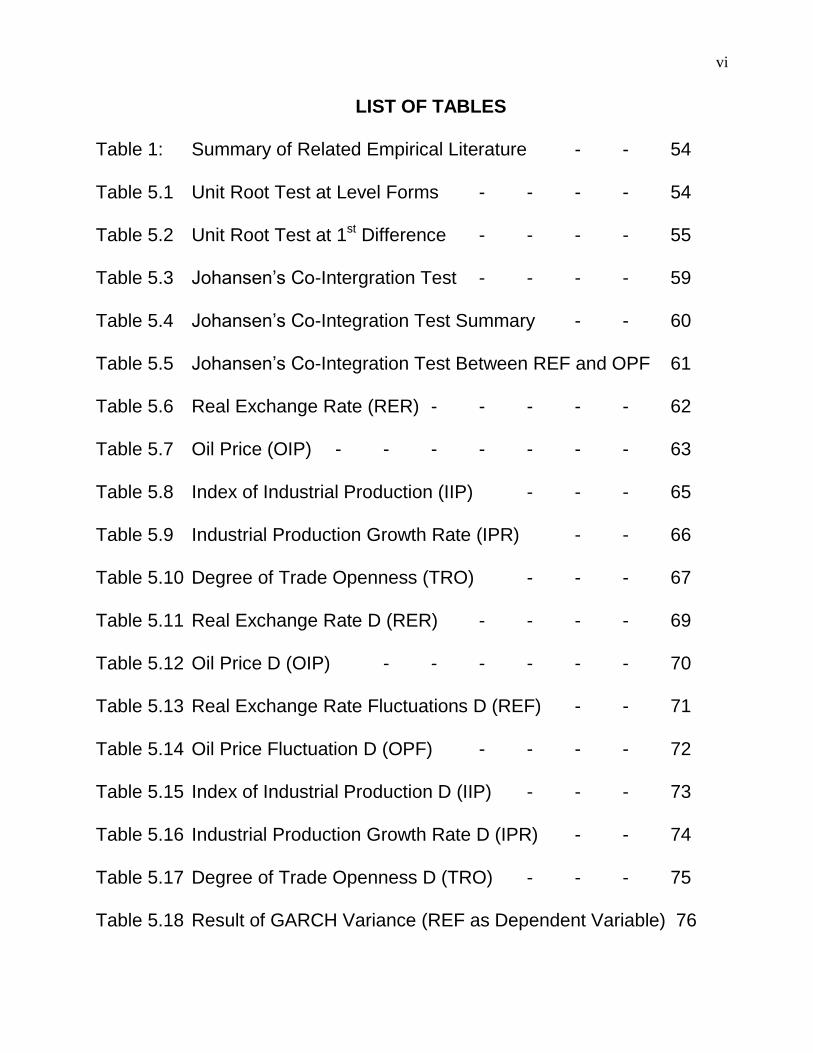

LIST OF TABLES

Table 1: Summary of Related Empirical Literature - - 54

Table 5.1 Unit Root Test at Level Forms - - - - 54

Table 5.2 Unit Root Test at 1st Difference - - - - 55

Table 5.3 Johansen‟s Co-Intergration Test - - - - 59

Table 5.4 Johansen‟s Co-Integration Test Summary - - 60

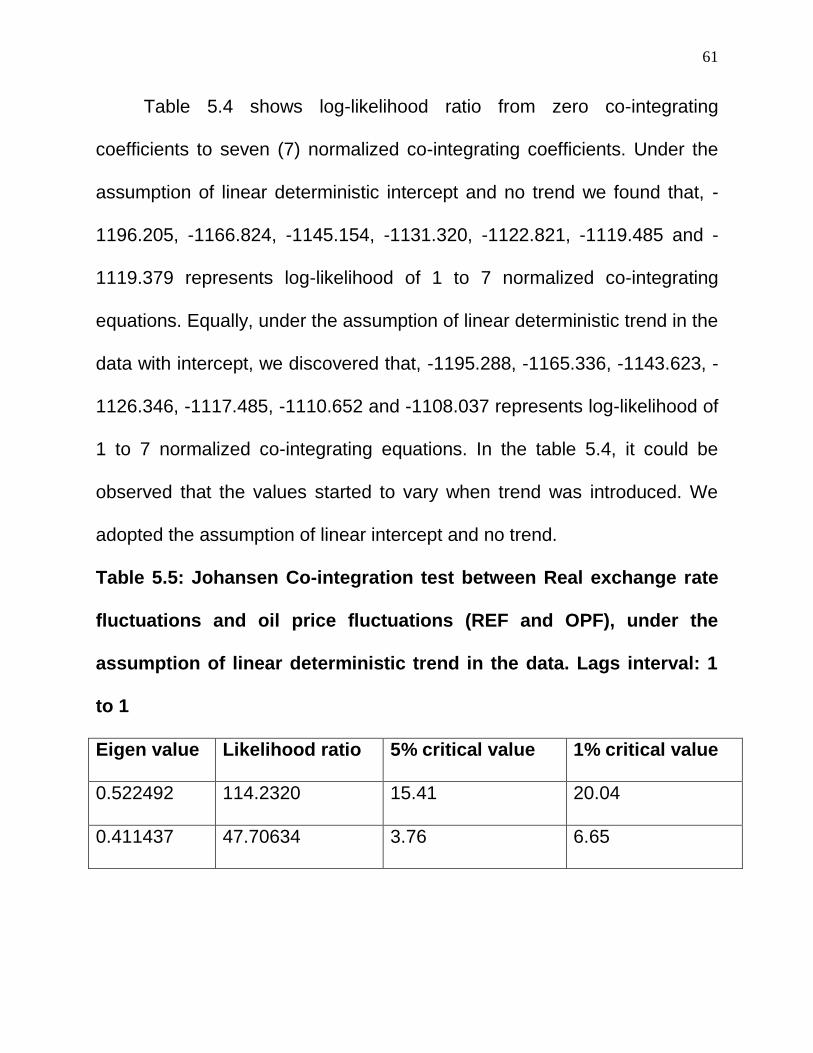

Table 5.5 Johansen‟s Co-Integration Test Between REF and OPF 61

Table 5.6 Real Exchange Rate (RER) - - - - - 62

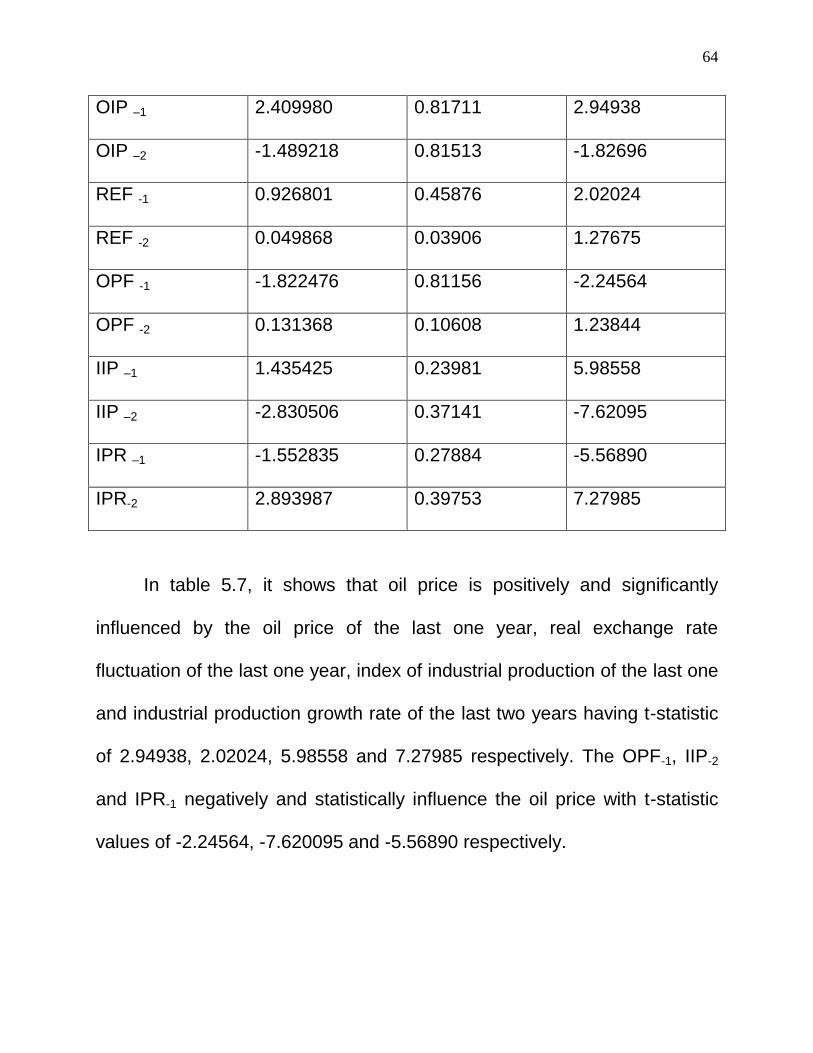

Table 5.7 Oil Price (OIP) - - - - - - - 63

Table 5.8 Index of Industrial Production (IIP) - - - 65

Table 5.9 Industrial Production Growth Rate (IPR) - - 66

Table 5.10 Degree of Trade Openness (TRO) - - - 67

Table 5.11 Real Exchange Rate D (RER) - - - - 69

Table 5.12 Oil Price D (OIP) - - - - - - 70

Table 5.13 Real Exchange Rate Fluctuations D (REF) - - 71

Table 5.14 Oil Price Fluctuation D (OPF) - - - - 72

Table 5.15 Index of Industrial Production D (IIP) - - - 73

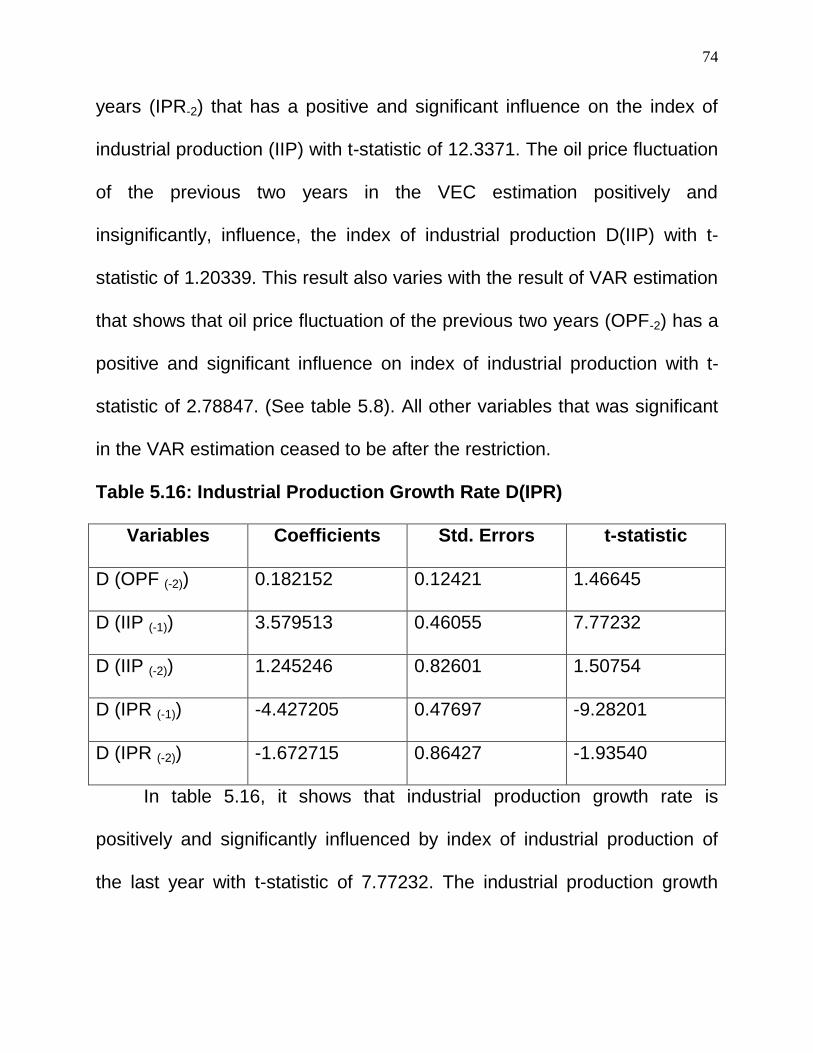

Table 5.16 Industrial Production Growth Rate D (IPR) - - 74

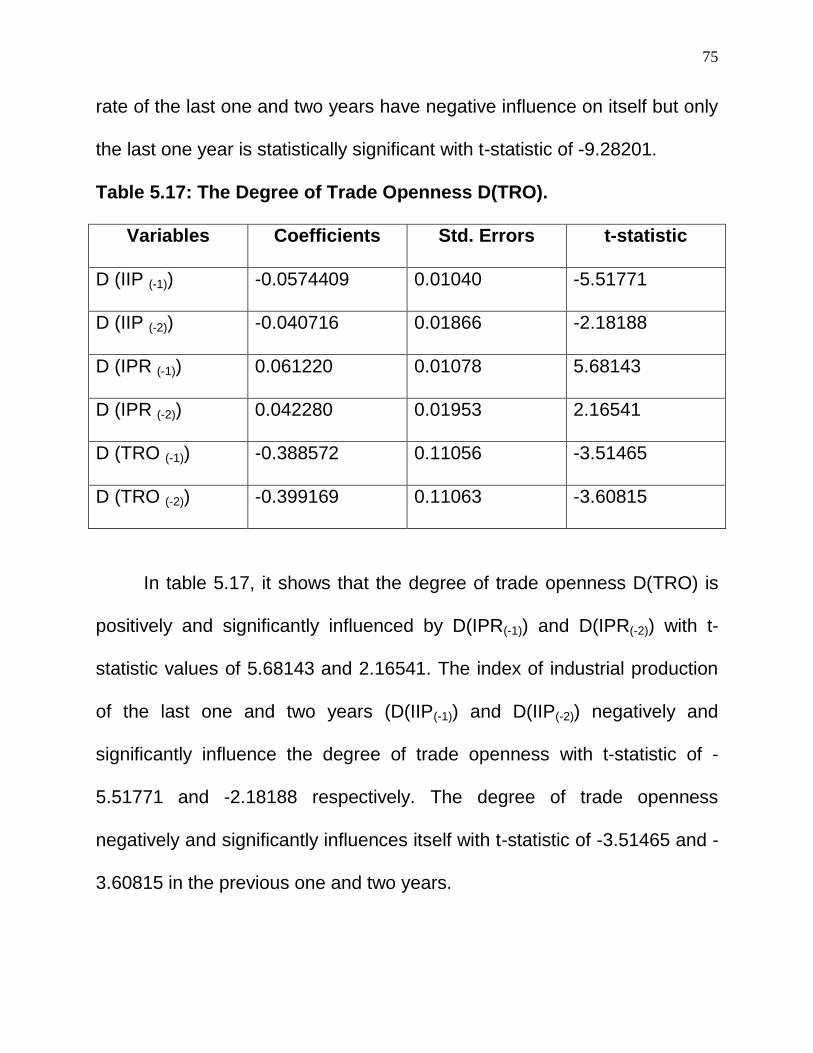

Table 5.17 Degree of Trade Openness D (TRO) - - - 75

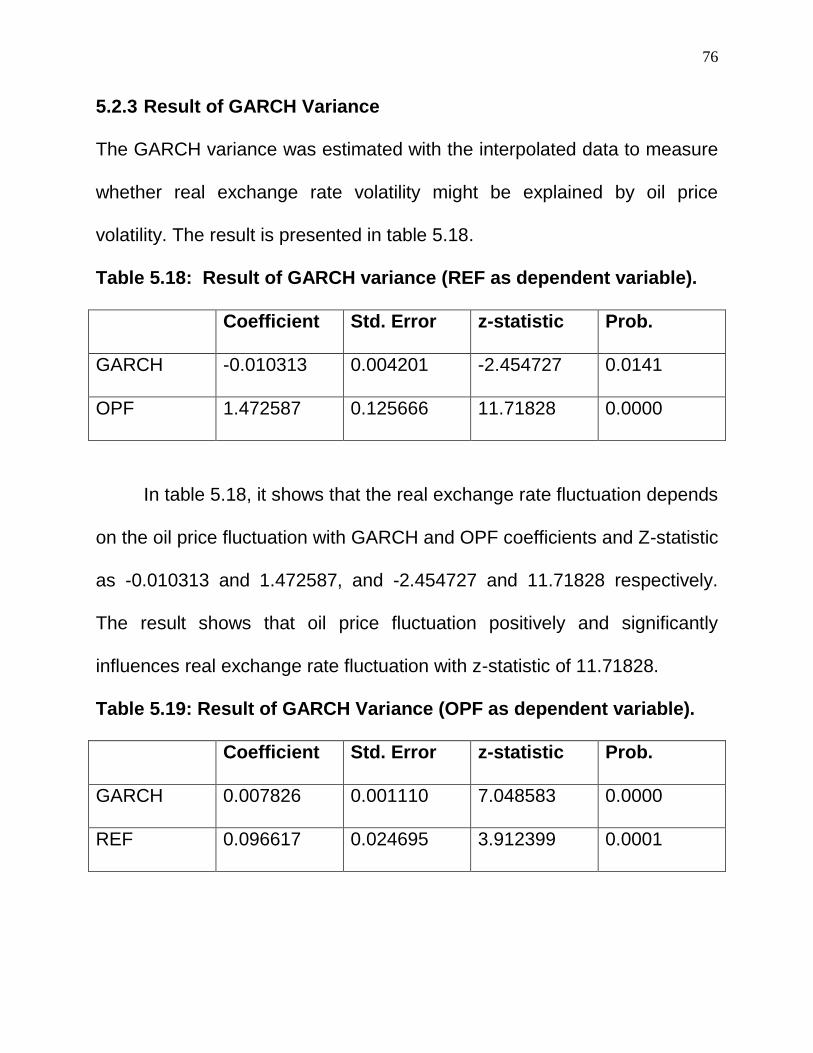

Table 5.18 Result of GARCH Variance (REF as Dependent Variable) 76

vi

5

Table 5.19 Result of GARCH Variance (OPF as Dependent Variable) 76

Table 5.20 Result of EGARCH Model (RER as Dependent Variable) 77

Table 5.21 Variance Equation for OIP - - - - - 78

vii

6

LIST OF FIGURES

Figure 5A: Real Exchange Rate and Oil Price - - 57

Figure 5B: Oil Price Fluctuations and Real Exchange Rate

Fluctuations - - - - - - 58

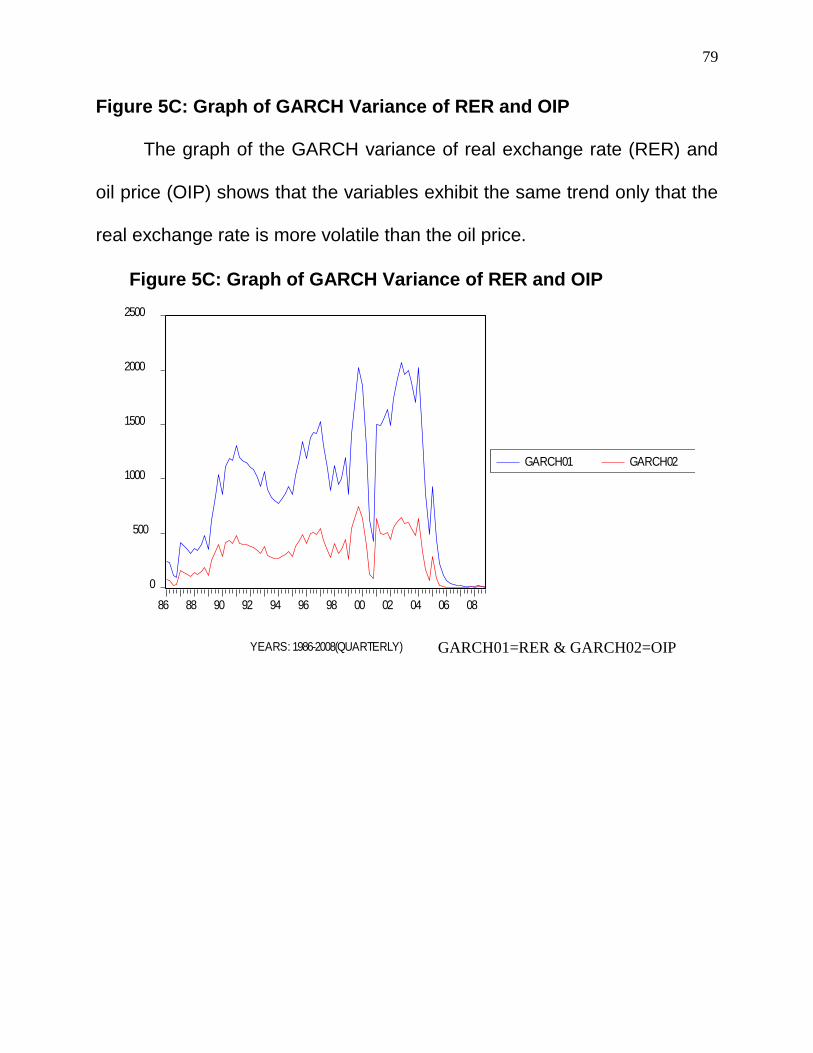

Figure 5C: Graph of GARCH Variance of RER and OIP - 79

viii

7

LIST OF APPENDICES

Appendix A: List of Figures 5D – 5J - - - - 104

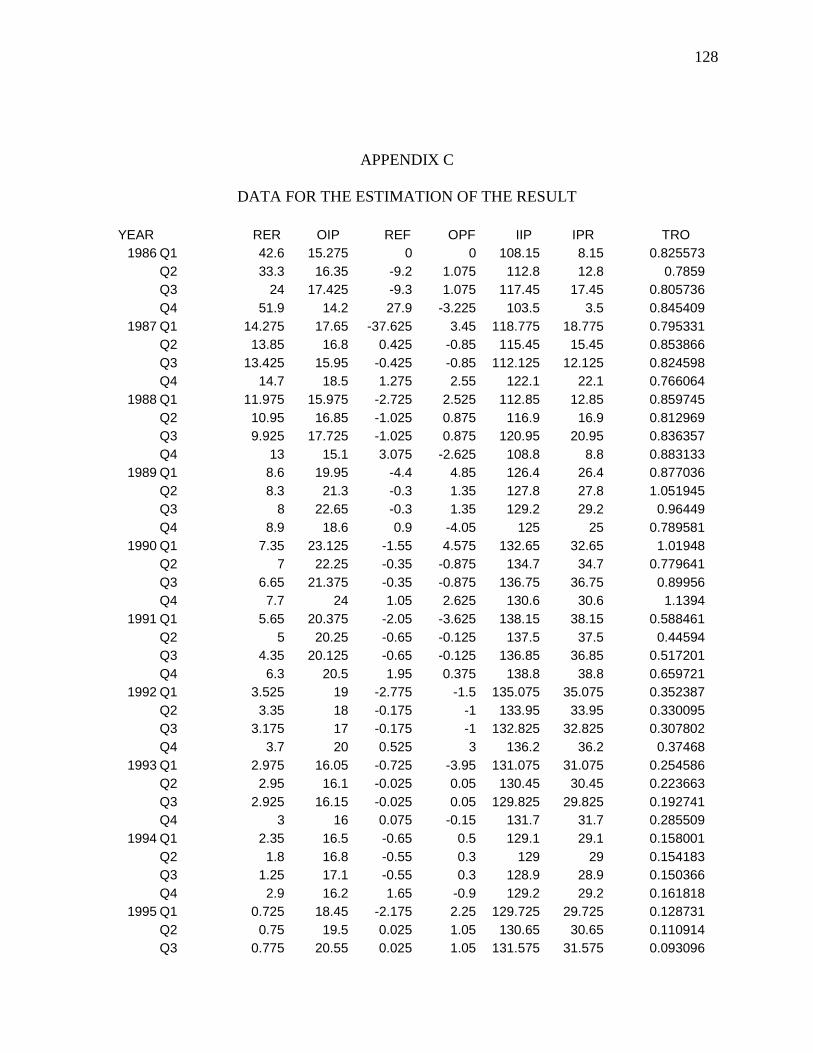

Appendix B: Estimated Results from Data on RER, OIP, REF, OPF,

IIP, IPR, and TRO (1986-2008, Quarterly) - 108

Appendix C: Data for the Estimation of the Results. - - 128

ix

8

TABLE OF CONTENT

Title Page - - - - - - - - - i

Approval - - - - - - - - - ii

Dedication - - - - - - - - - iii

Acknowledgment - - - - - - - - iv

List of Tables - - - - - - - - - v

List of Figures - - - - - - - - - vi

List of Appendices - - - - - - - - vii

Table of Content - - - - - - - - viii

Abstract - - - - - - - - - ix

CHAPTER ONE

1.0 INTRODUCTION - - - - - - - 1

1.1 Background of the Study - - - - - - 1

1.2 Statement of Research Problems - - - - 3

1.3 Objectives of the Study - - - - - 6

1.4 Research Hypothesis - - - - - - - 6

1.5 Significance of the Study - - - - - - 7

CHAPTER TWO

2.0 REVIEW OF RELATED LITERATURE - - - 9

2.1 Theoretical Literature - - - - - - - 9

2.1.1 Theories of Exchange rate - - - - - 10

2.1.2 Real Exchange Rate Variable - - - - - 14

2.1.3 Demand and Supply of Oil- - - - - - - 16

2.1.4 Oil Price Shock - - - - - - - - 20

2.2 Empirical Literature - - - - - 21

2.2.1 Summary of Related Empirical Literature - - - 29

x

9

CHAPTER THREE

3.0 OVERVIEW OF THE NIGERIAN ECONOMY AND POLICY

RESPONSES - - - - - - - - 33

3.1 Conceptual Issues - - - - - - - 39

CHAPTER FOUR

4.0 METHODOLOGY - - - - - - - 41

4.1 Methodological Framework - - - - - - 41

4.2 The Model - - - - - - - 44

4.3 Battery Tests - - - - - - - 44

4.3.1 Unit Root Test - - - - - - - 45

4.3.2 Co-integration Test - - - - - - - 45

4.3.3 Estimation Procedure - - - - - - - 45

4.4 Model Specification -l - - - - - - 47

4.4.1 Exponential GARCH Model - - - - - - 47

4.4.2 Estimation Procedure - - - - - - - 47

4.4.3 Vector Error Correction Model (ECM) - - - - - 48

4.4.4 Estimation Procedure - - - - - - 49

4.4.5 Justification of the Models - - - - - - 51

4.5 Package for Estimation - - - - - - 52

4.6 Data - - - - - - - - - 52

4.7 Estimation of Variables - - - - - - 52

CHAPTER FIVE

5.0 PRESENTATION AND ANALYSIS OF RESULTS - 54

5.1 Battery Tests - - - - - - - - 54

5.1.1 Unit Root Test - - - - - - - - 54

5.1.2 Co-integration Test - - - - - - - 58

5.2.2 Results of the VAR Model - - - - - - 62

xi

10

5.2.3 Results of the VEC Model - - - - - - 69

5.2.4 Results of the GARCH Variance - - - - - 76

5.2.5 Results of the EGARCH Model - - - - - 77

5.3.0 Evaluation of Hypotheses - - - - - - 80

5.3.1 Test of Hypothesis One - - - - - - 80

5.3.2 Test of Hypothesis Two - - - - - - 80

5.3.3 Test of Hypothesis Three - - - - - - 81

5.3.4 Test of Hypothesis Four - - - - - - 82

CHAPTER SIX

6.0 SUMMARY, POLICY RECOMMENDATION AND

CONCLUSION - - - - - - - - 84

6.1 Summary - - - - - - - - - 84

6.2 Policy Implications - - - - - - - 88

6.3 Conclusion - - - - - - - - 92

References - - - - - - - - 95

Appendix - - - - - - - - 104

xii

11

ABSTRACT

The rate at which different macroeconomic variables are fluctuating has constituted severe problems for policy analysis. Some macroeconomic variables‟ volatility has become a key determinant as well as a consequence of poor economic management in Nigeria. The exchange rate is arguably the most difficult macroeconomic variable to model empirically. It has been recognized that if one could find a missing real shock that were sufficiently volatile to influence exchange rate, one could potentially, take an important step towards resolving the purchasing power parity puzzle. This is why the adoption of different exchange rate regimes to minimize fluctuations in the Nigerian economy could not achieve significant results. Many researchers have used cross-country regression models to find out the causes of fluctuation in exchange rate. Many of these researches could not yield significant results because some of the techniques employed suffer from either inappropriate measurement or specification bias or both. The results may not also be robust because of the heterogeneity of macroeconomic data, especially the data from the developing countries. This study adds to the existing literature by identifying that real exchange rate fluctuation depends on the oil price fluctuation using country specific regression. It also addresses the problem of the relationship between oil price shocks and some other macroeconomic variables in Nigeria. It further addresses the problem of transmission of shocks from oil price to real exchange rate and to some macroeconomic variables. The study equally, looks at the problem of how current shocks on oil price relates with its conditional volatility in periods ahead. This work adopted the generalized Autoregressive conditional Heteroscedasticity (GARCH) variance, exponential generalized Autoregressive conditional Heteroscedasticity (EGARCH) and Vector Error correction VEC) models to capture different hypotheses specified in the work. The GARCH variance was used to explain that real exchange rate volatility might be determined by oil price volatility. The EGARCH model was used to determine whether current shock on oil price has any relationship with its conditional volatility in periods ahead. The VEC model was used to trace the transmission of shocks among the variables. The results show that oil price fluctuation positively and significantly influence real exchange rate fluctuation with z-statistic of 11.71828 and coefficient of 1.472587. It also shows that all the explanatory variables except industrial production growth rate (IPR) are statistically significant in explaining the real exchange rate. It equally, shows that there is transmission of structural shocks among the variables. The News Impact Curve (NIC) indicates that the current shock in oil price is influenced by the previous shocks and its effect on other periods‟ ahead, decays exponentially.

xiv

1

CHAPTER ONE

1.0 INTRODUCTION

1.1 Background of the Study:

There has been controversy among researchers on what policy

response that will bring about or causes fluctuations in aggregate economic

activities. Some believe that monetary policy response should be assigned

more weight, while others still argue that the fiscal policy should be the

most appropriate. Yet other researchers have identified oil price shocks as

of very great importance in influencing economic growth and aggregate

economic activities.

The current global energy crisis poses a great challenge to policy

makers across countries. The price of crude oil slumped in the world

market during the first half of 1980s. Thus, Nigeria‟s crude oil which sold at

slightly above US $41 a barrel in early 1981, fell precipitously to less than

US $9 a barrel by August 1986 (Uwubanmen 2002). The price of oil

fluctuates between $17 and $26 at different times in 2002, around $53 per

barrel by October 2004, around $89 per barrel by January 2008. In fact,

the price of oil has witnessed noticeable fluctuations since the past three

decades after the collapse of the Breton woods.

ii

2

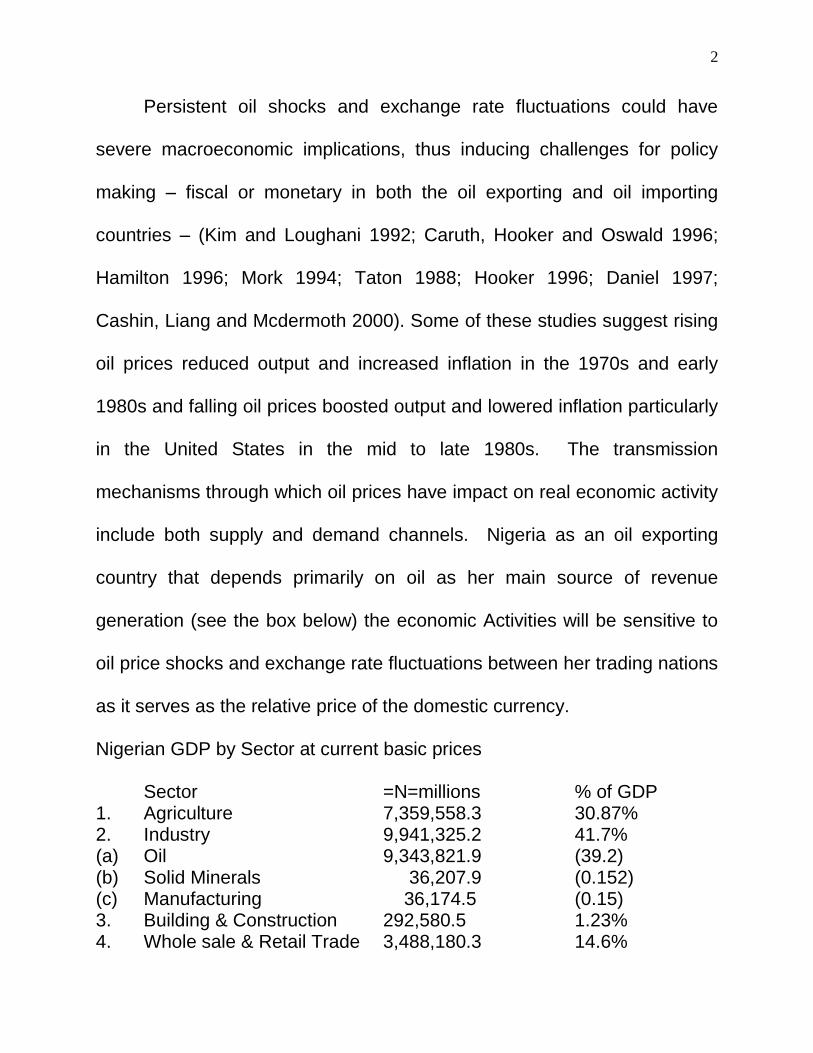

Persistent oil shocks and exchange rate fluctuations could have

severe macroeconomic implications, thus inducing challenges for policy

making – fiscal or monetary in both the oil exporting and oil importing

countries – (Kim and Loughani 1992; Caruth, Hooker and Oswald 1996;

Hamilton 1996; Mork 1994; Taton 1988; Hooker 1996; Daniel 1997;

Cashin, Liang and Mcdermoth 2000). Some of these studies suggest rising

oil prices reduced output and increased inflation in the 1970s and early

1980s and falling oil prices boosted output and lowered inflation particularly

in the United States in the mid to late 1980s. The transmission

mechanisms through which oil prices have impact on real economic activity

include both supply and demand channels. Nigeria as an oil exporting

country that depends primarily on oil as her main source of revenue

generation (see the box below) the economic Activities will be sensitive to

oil price shocks and exchange rate fluctuations between her trading nations

as it serves as the relative price of the domestic currency.

Nigerian GDP by Sector at current basic prices

Sector =N=millions % of GDP 1. Agriculture 7,359,558.3 30.87% 2. Industry 9,941,325.2 41.7% (a) Oil 9,343,821.9 (39.2) (b) Solid Minerals 36,207.9 (0.152) (c) Manufacturing 36,174.5 (0.15) 3. Building & Construction 292,580.5 1.23% 4. Whole sale & Retail Trade 3,488,180.3 14.6%

3

5. Services 2,760,526.5 11.6% (a) Finance & Insurance 366,059.1 (1.54) Total G.D.P 23,842,170.7 100% Source: CBN Statistical Bulletin Dec. 2008 Golden Jubilee Edition

Note: Oil represents by far the largest sector of the economy by this

measure, over 39%. In contrast, the non-oil private manufacturing was

0.15%, mining was 0.1525, and building and construction represents just

1.23% of GDP. The financial sector was minimal with 1.54%. As at 2000

Nigeria had earned about $300 billion from oil exports since the mid 1970s

but its per capita income was 20 percent lower than in 1975. Between

1975 and 2000 Nigeria‟s broad macroeconomic aggregates-growth, the

terms of trade, the real exchange rate, government revenue and spending

– were among the most volatile in the developing world. Macroeconomic

volatility has become a key determinant – as well as a consequence – of

poor economic management (NEEDS 2005).

1.2 Statement of Research Problems:

Over reliance on oil has made macroeconomic activities in Nigeria to

react sharply to shocks emanating from sudden fluctuation in the price of

crude oil. This is why NEEDS 2004 states that: “perhaps the greatest

hindrance to progress has been the boom and bust mode of economic

management encouraged by the dominance of oil in the economy”.

4

The advent of oil boom has led to a decline in the contribution of the

non-oil sectors in most of the oil exporting countries, a phenomenon

referred to as the “Dutch – Disease”. The implication of this is that while oil

price increase should be considered good news in oil exporting countries

and bad news in oil importing countries, the reverse should be expected

when oil price decreases. For instance, the downturn in the oil prices after

1980 led to disastrous economic consequences in many oil exporting

countries leading to large fiscal imbalances, poor export performance, high

level of foreign balance of account deficits, large and growing external

debts, stagflation, large and rising unemployment and alarming

deterioration of social and economic infrastructures (Jimenez and Sanchez

2003). The different transmission mechanisms of oil price shocks to the

real economy have different features in each of the countries, which thus

respond some what differently to such shocks. In light of the different levels

of oil dependence, different policies are implemented to smooth out the

consequences of such shocks in different oil exporting countries.

Exchange rate on its own part has witnessed frequent fluctuations since

after the collapse of the Breton wood.

Studies on oil price and U.S. real exchange rate have shown that the

U.S. real exchange rate is a positive function of the real oil price (Amano,

5

and Van Norden 1998; Lahtinen 2000). This positive relationship between

U.S. dollar and oil price is partly problematic because being a major

importer of crude oil, higher oil price worsens the U.S. terms of trade (Chen

and Rogoff 2001). Backus and Crucini 1998, also argue that higher oil

price should depreciate the U.S. dollar and not to appreciate it. Also relative

to the German mark, oil price changes affect negatively the United States

terms of trade than German terms of trade. In their own study, Amano and

Van Norden (1995), presents a special case for Canada, where higher oil

price led to a weaker Canadian dollar relative to U.S. dollar despite the fact

that Canada is a substantial exporter of oil and the U.S. a net importer of

crude oil. Nigeria may not be different from Canadian experience. The

increase in oil price over the years has witnessed a depreciation of naira

exchange rate to most foreign currencies such as U.S dollar, British pounds

sterling, and Euro. Based on the above discussion, this paper intends to

address the following questions.

i Can real exchange rate volatility be explained by oil price volatility in

Nigeria?

ii Is there any significant impact of oil price shocks on real exchange

rate fluctuations in Nigeria?

6

iii Do shocks transmit from oil price and real exchange rate fluctuation

to some macroeconomic variables in Nigeria?

iv What are the relationships between the current shock on oil price and

its conditional volatility in other periods ahead?

1.3 Objectives of the Study:

The broad objective of this study is to estimate the impact of oil price

shocks on real exchange rate and trace the transmission of structural

shocks from oil price to exchange rate and other factors affecting it. The

specific objectives are:

1) To determine whether real exchange rate volatility can be explained

by oil price volatility in Nigeria.

2) To determine the significant of the impact of oil price shocks on real

exchange rate fluctuations in Nigeria.

3) To trace how shocks transmit from oil price and real exchange rate

fluctuation to some macroeconomic variables in Nigeria.

4) To estimate the relationship between the current shock on oil price

and its conditional volatility in other periods ahead.

1.4 Research Hypothesis

The research hypotheses of the study are:

7

i) Real exchange rate volatility cannot be explained by oil price

volatility in Nigeria.

ii) There is no significant impact of oil price shocks on real exchange

rate fluctuations in Nigeria.

iii) There is no transmission of shocks from oil price and real

exchange rate fluctuations to some macroeconomic variables in

Nigeria.

iv) Current shock on oil price has no relationship with its conditional

volatility in other periods ahead.

1.5 Significance of the Study:

The interface between real exchange rate fluctuations and oil price

shocks has been over looked in the existing empirical literature in Nigeria in

spite of Nigeria‟s dependent on crude oil revenue.

Nigeria‟s underlying current account balance is a function of three

major determinants its oil exports, priced at a sustainable long term trend

value; the competitiveness of its non-oil exports; the pace of remittances

from Nigerians living abroad. Nigeria‟s balance of payments have been

subject to a high degree of variability caused by: variability in government

spending, which often creates surge in import payments for capital projects;

variability in the price of oil; variability in capital flight caused by periodic

8

exchange rate uncertainty. These swings are difficult to predict, but they

can have a substantial impact on monetary expansion and the exchange

rate.

Literature has shown that oil price volatility affects the real exchange

rate for Germany, Japan and the United states and not much has been said

about Nigeria. Many studies used cross-country regression to study the link

between exchange rate fluctuations and macroeconomic activities of

various countries. The result of cross-country regression is prone to biased

ness as a result of the heterogeneous nature of data obtained in less

developed countries. Most of the studies reviewed were on oil importing

countries.

These create a need for this study that uses country-specific

regression to determine the impact of oil price shocks on real exchange

rate fluctuations in Nigeria. The ability of the models in this work to

determine the conditional volatility of current real exchange rate and to

trace the relationship between current shocks on oil price and its

conditional volatility in periods ahead make this work very important and

will help to ginger a policy debate in the area. This is equally, very vital for

policy forecasting and adjustment especially in this era where every country

is aiming at targeting rules.

9

CHAPTER TWO

2.0 REVIEW OF RELATED LITERATURE

2.1 Theoretical Literature:

Hooper and Mann (1989) and Blundell – Wignall and Browne (1991)

spearheaded the works on the fundamental determination of the real

exchange rate. The identified fundamentals are real interest rate

(differentials) and current account imbalances. The model asserts that

shocks that drive the exchange rate away from the fundamentals will

ultimately release it back to levels projected by those variables. There are

number of factors that might be associated with the long-run real exchange

rate in transition economies (Motiel 1999). First, domestic supply side

factors should be considered, especially variables related to the Balassa –

Samuelson effect (Note: The Balassa – Samuelson theorem assumes that

purchasing power parity (PPP) holds for the market of traded goods, but

that ratio of prices of traded and non-traded goods may evolve differently in

one country than in another, as productivity in poorer countries grows faster

in the traded-goods sector than in the non-traded goods sector. The

potential for productivity growth in the traded goods sector of poorer

countries is higher than in richer countries. It is further presumed that

productivity in the non-traded sector rises more slowly, while wages remain

10

the same in both sectors. In such cases, the real exchange rate

appreciates in the country with higher growth).

Second, demand – side factors may be important, such as fiscal

policy measures that induce changes in the composition of government

spending between traded goods and non-traded goods. (Note: if the

income elasticity of non-traded goods is larger than unity then their relative

price will move along with living standards which will cause appreciation of

the real exchange rate. Further, if government expenditure is biased

toward traded goods and the share of government expenditure in GDP

increases over time, the real exchange rate will depreciate).

Other proposed factors include changes in the international economic

environment (e.g. terms of trade), net foreign assets, and trade openness.

(Note: for example, if trade regime is more open, it is likely to expect the

real exchange rate depreciation. Trade restrictions may increase domestic

prices of traded goods, which further leads to rise in composite price index

and the real exchange rate appreciation) (Zorica Mladenovic 2004)

2.1.1 Theories of Exchange Rate:

Milton Friedman (1953), an early advocate of flexible exchange rates,

argue that one advantage of floating rates is that they could allow rapid

change in relative prices between countries: “A rise in the exchange rate ---

11

makes foreign goods cheaper in terms of domestic currency, even though

their prices are unchanged in terms of their own currency, and domestic

goods more expensive in terms of foreign currency, even though their

prices are unchanged in terms of domestic currency; this tends to increase

imports and reduce exports” (Friedman, 1953: 162). This passage makes

two assumptions; that goods prices are unchanged in the currency of the

producer of the good, and that there is significant pass-through of the

exchange rate change to the buyer of the good. On the nominal price

stickiness, Friedman argues that the choice of exchange rate regime would

matter little if nominal goods prices adjusted quickly to shocks. He argues

that, “if internal prices were as flexible as exchange rates, it would make

little economic difference whether adjustments were brought about by

changes in exchange rates or by equivalent changes in internal prices. But

this condition is clearly not fulfilled. At least in the modern world, internal

prices are highly inflexible”.

In assessing this relative-price effect and its significant for the choice

of exchange-rate regime, Friedman is certainly correct to emphasize the

importance of normal goods price stickiness. As Buiter (1999), has

forcefully emphasized, the decision to join a monetary union, or the choice

of an exchange rate regime is a monetary issue. Relative-price behaviour

12

is usually independent of monetary regime in a world of perfect goods price

flexibility. The pioneering work of Obstfeld and Rogoff (1995, 1998, 2000a)

has assumed that nominal prices are fixed in the producer‟s currencies, so

that price for consumers change one – for – one in the short-run with

changes in the nominal exchange rate. This is exactly the assumption of

Friedman.

Another theory of exchange rate is the Purchasing Power Parity

(PPP). This concept PPP is often used as an analytical tool to explain and

predict movements in exchange rates. Two types of PPP can be

distinguished: absolute PPP and relative PPP. (Note: The purchasing

power parity between any two countries is the number of units of the one

country‟s currency (e.g. naira) which endows the holder with the same

purchasing power (i.e. command over goods and services) as one unit of

the other country‟s currency (e.g. U.S. dollar). PPP can be between two

countries, in which case it is a bilateral comparison, or to parity between

the country and a group of trading partners, in which case it is a multilateral

comparison). According to the absolute PPP theory the “equilibrium”

exchange rate between two currencies is set by the ratio between the price

levels in the two countries. Thus, if goods cost more in the United States

than in Nigeria (with prices in both countries expressed in dollars, using the

13

prevailing exchange rates), the naira is under valued relative to the dollar.

Similarly, if dollar prices of goods are lower in the United States, than in

Nigeria the naira is overvalued against the dollar. Price indices are

insufficient to calculate an absolute PPP, so a cost of a basket of goods

and services is employed. For example, let us assume the cost of a basket

in January 2006 was $60 in United States and N6480 in Nigeria. These

figures imply a purchasing power parity exchange rate of $1 = 60

6480N =

N108 whereas the exchange rate prevailing at the time was about $1 =

N168.

The relative PPP theory states that changes in rates reflect

differences in relative inflation rates. Relative PPP is thus concerned with

the ratio of the equilibrium exchange rate in a current period relative to the

equilibrium exchange rate in a base period. According to this theory, PPP

is determined by the ratio of the domestic country‟s price index in the

current period to the foreign country‟s price index in the same period,

where both indices have a common base period. Thus, if dollar prices

have risen at a slower rate in the United States than naira prices have risen

in Nigeria, the dollar should appreciate against the naira compared to the

exchange rate in the common base period. Another theory is the theory of

incomplete pass-through. This theory has been addressed in various ways

14

in the literature. The most common analytical tool to examine incomplete

pass-through has probably been pricing-to-market approach that

presupposes short-term rigidities and the market power of importing

companies. These market imperfections allow foreign suppliers to set the

markup of prices over the marginal cost. According to the pricing-to-market

approach, international markets for manufacturing goods are sufficiently

segmented that producers or retailers can, at least over some horizon,

tailor the prices they charge to the specific local demand conditions

prevailing in different national markets. Thus, firms set different prices for

their goods across segmented national markets to compete with firms in

those markets. According to Dornbush (1987), the degree of pass-through

depends on (i) substitution between domestic and foreign goods (ii) market

integration (iii) market organization. Evidence seems to suggest that the

dominant component of real exchange rate behaviour is a nominal

exchange rate even in a long-run through the incomplete pass-through

(Asea and Mendoza 1994; De-Gregorio and Wolf 1994).

2.1.2 Real Exchange Rate Variable

The real exchange rate is a measure of one country‟s overall price

level relative to another country. The real exchange rate, defined with

15

respect to a general or overall price level, such as the consumer price

index (CPI) (Lahtinen 2001), is given by

qt = Pt – Pt* - St - - - - - - - - - - - - - (1)

where qt denotes the logarithm of real exchange rate, Pt denotes the log of

the domestic price level,, Pt* the log of the foreign price level and St the log

of the nominal exchange rate defined as the home currency price of a unit

of foreign currency. In this context therefore, a rise in qt denotes an

appreciation of the real exchange rate. To measure the price level,

decompose it into the traded and non-traded components and use a

geometric average of these prices in both country.

Pt = (1- ) PtT + Pt

N, < 1 -------------- (2)

where Pt denotes the logarithm of the price index, PtT is the log of the

traded goods price index, PtN is the log of the non-traded goods price index

and is the share that non-traded goods take in the price index. Letting an

asterisk represent the foreign country, one can also write;

Pt* = (1-β) Pt

T* + βPtN*, β < 1 ----------- (3)

where β is non-traded good‟s share in the foreign price index.

Thus, following Engel (1999), the real exchange rate can be written

as

qt = xt + Yt ------------------------------- (4)

where

Xt = PtT - Pt

T* - St ---------------------- (5) and

16

Yy = (PtN* - Pt

T*) -------------------- (6)

Yt defines a traditional Harrods – Balassa Samuelson condition, which

relates labour productivity to non-tradable goods prices.

Xt is the deviations from the law of one price for tradable goods.

The real exchange rate models, such as traditional Harrods – Balassa –

Samuelson Model, adequately explain only a few bilateral real exchange

rates during a few sub periods. If there were no relative structural shocks

between two currency areas, a real exchange rate should be a stationary

variable and it should follow the purchasing power parity hypothesis.

Demand and Supply of Oil

On the other hand, oil is arguably the quaint essential commodity in

the modern industrial economy. Although the industrial revolution was

initially powered by coal, since its discovery in Pennsylvania in 1869, oil

has gained increasing prominence in terms of its share of the world‟s

primary energy supply, accounting for 37 percent (the largest share) in

2001 (IEA, 2005). As an energy source, oil is used for electricity

generation, and to a lesser extent for heating and cooking. However, its

most important role is as a liquid fuel for transportation. Globally, ship,

train, airplane and road transport depend mainly on oil. Consequently, the

tourism sector in most countries is also highly reliant on oil. Industrial

17

agriculture (or agri-business) depends heavily on oil for the production of

fertilizers, herbicides and pesticides. The manufacturing sector uses oil

both for energy and as a feedstock for a myriad of products from plastics to

paints to pharmaceuticals.

Historically there have been three eras in the determination of

international crude oil prices (Nkomo, 2006). Price of oil was determined

chiefly by multinational oil companies, until in 1970, when the Organization

of Petroleum Exporting Countries (OPEC) asserted its capacity to influence

the price via its output decisions. Since the late 1980s, however, “world oil

prices have been set by a market-related pricing system which links oil

prices to the „market price‟ of a particular reference crude” (Farrell, Kahn

and Visser 2001: 69). Two important reference prices, Brent and West

Texas intermediate (WTI), are determined on the London and New York

futures exchanges respectively.

The fundamental determinant of oil prices is the demand/supply

balance in the international market; each side of this market is in turn

influenced by several factors. Over the long-term, the demand for oil is

determined primarily by rates of economic growth in the major regions of

the world, as well as by energy-related technological developments such as

efficiency gains or new found uses for oil. Such structural determinants

18

tend not to change rapidly and are therefore unlikely to provide the impetus

for an oil price shock on their own. However, China‟s extraordinary growth

has had an increasingly significant effect on the world demand for oil, most

notably in 2004. The supply side of the crude oil market is comprised of

output from OPEC and non-OPEC producing countries, whose production

decisions hinge on geological, economic and political factors (Farrell et al

2001: 72 – 78). In the long-term, oil supply depends on the rates of

extraction, depletion, and new discoveries, as well as developments in

extractive technologies that allow enhanced recovery of oil. In the short-

term, changes in OPEC production quotas and temporary supply

disruptions due to technical or political factors or natural disasters can have

important consequences for supply and hence oil prices.

In addition to these fundamentals, expectations and speculation

about future demand and (especially) supply conditions – which in turn are

stimulated by economic and political conditions – play a large part in the

determination of crude oil prices on the futures and spot markets,

particularly when inventories are low (Nkomo, 2006: 13; Farrell et al, 2001:

82). These considerations also amplify oil price volatility.

The balance between supply and demand in the oil market has been

gradually tightening over the past few years. This is partly attributable to

19

steeply rising demand on the back of robust economic growth, especially in

major emerging economies, such as China, but also in the U.S. On the

other hand, supply has expanded less rapidly than demand. Moreover,

there have been temporary or recurrent disruptions to the flow of oil in

some areas as a result of various factors, such as: the ongoing conflict in

Iraq; sporadic conflict and sabotage in Nigeria; the devastation wrought by

Hurricanes, Katrina and Rita in the Gulf of Mexico; and a leaking pipeline

leading to a temporary closure of the Prudhoe Bay field in Alaska in August

2006. Speculation in the oil market has amplified the price effects of these

relatively minor supply disruptions. In addition, fears amongst oil traders

were exacerbated by the conflict between Israel and Hezbellah in

July/August 2006 (Wakeford 2006). As a consequence, the price of crude

oil rose from around US $25 per barrel in 2003 to a high point of US $78

per barrel in July 2006, and about US $98 per barrel in January 2008. this

represents roughly four-times of oil prices over four years which may be

defined as a „trend‟ oil price shock.

It is also important to notice that the time path of oil price is not

determined in a competitive market. Although, we do not argue that oil

prices are immune to the laws of supply and demand, it seems to be a

quite reasonable argument that oil prices are strongly dependent on the

20

stability of cartels. The most important cartel for an oil price is obviously

the OPEC cartel. This cartel does not have all the elements of a successful

cartel because it is simply too fragmented culturally and politically

(Wakeford 2006). However, the history of the rise and fall of oil prices is

also very suggestive of some sort of multiple equilibrium stories. Some

analyses indicate that the historical behaviour of oil prices do not allow one

to predict how future oil prices will fluctuate. The severity of movements of

price do not provide any information about their future likely duration and

the time spent in a current boom or slump provide no information about the

likely future duration of that boom or slump. Indeed the collapse of oil

prices in 1986 also came with dramatic suddenness, again suggestive of a

collapse of an equilibrium and establishment of another. This possible

multiple equilibrium nature of the oil price makes it a very unstable variable

with possible jumps in the price process.

2.1.3 Oil Price Shocks

Oil shocks are usually defined in terms of price fluctuations, but these

may in turn emanate from changes in either the supply of or the demand for

oil. In practice it is unlikely for demand to grow rapidly enough to cause a

price shock unless it is motivated by fears of supply shortages. Oil price

shocks may of course be negative (a fall) or positive (a rise). There are at

21

least two important dimensions of a price shock. The first is the magnitude

of the price increase, which may be measured in absolute terms or in

percentage changes. Further, one can distinguish between nominal and

relative (or real) price changes. The second aspect is one of timing: the

speed and durability of price increases. Three cases may be identified:

1) a rapid (e.g. occurring within a few quarters) and sustained

price increase (a „break‟);

2) a rapid and temporary price hike (a „spike‟); and

3) a slower but sustained rise (a „trend‟).

The speed of a shock is important as it affects the ability of economies to

adjust, which is typically very restricted in the short run. Durability has

obvious implications for the permanence and overall extent of the

consequences.

2.2 Empirical Literature:

The exchange rate is arguably the most difficult macroeconomic

variable to model empirically. Surveys of exchange rate models, such as

Meese (1990) and Mussa (1990), tend to agree on only one point that

existing models are unsatisfactory. Monetary models that appeared to fit

the data for the 1970s are rejected when the sample period is extended to

the 1980s (for example Meese and Rogoff 1983). Later work on the

monetary approach such as Campbell and Clarida (1987), Meese and

22

Rogoff (1988), Edison and Pauls (1993), and Clarida and Gali 1994), find

that even quite general predictions about the co-movements of real

exchange rates and real interest rates are rejected by the data. However,

later works suggested more positively (but still controversial) results

emerging in three areas. First, work by researchers such as MacDonald

and Taylor (1994) has shown that a long-run relationship exists among the

variables in the monetary model of exchange rates, and that such models

perform better than a random walk in out-of-sample forecasting. The data,

however, reject most of the parameter restriction imposed by the monetary

approach, so it is uncertain whether these results are really evidence in

favour of the monetary model. This positive evidence of a long-run

monetary model also contrasts with the findings of some other researchers

such as Gardeazabal and Regulez (1992), Sarantis (1994), and Cushman,

Lee and Thorgeirsson (1995).

The second line of research has evolved around the idea of

purchasing power parity (PPP). As noted by Froot and Rogoff (1994),

researchers have found significant evidence in favour of PPP when they

use significantly long spans of data. This is a particularly confusing result,

since it is precisely over such long periods of time that we would expect

23

gradual shifts in industrial structure, relative productivity growth, and other

factors to alter real equilibrium exchange rates.

Third, structural time-series work on the determinants of real

exchange rate fluctuations indicate that real shocks or permanent

components play a major and significant role in explaining real exchange

rate fluctuations.

Univariate and Multivariate Beveridge – Nelson decompositions by

Huizinga (1987), Baxter (1994), and Clarida and Gali (1994) find that, even

though real exchange rates may not follow a random walk, most of their

movements are due to changes in the permanent components. Yet

another studies by Lastrapes (1992), and Evans and Lothian (1993),; using

the Blanchard and Quah (1989) decomposition, find that much of the

variance of both real and nominal exchange rates from a number of

countries over both short and long horizons is due to real shocks. The

conclusions from the structural time-series literature therefore seem to be

robust to both decomposition method and currencies. This has led some to

suggest that an unidentified real factor may be causing persistent shifts in

real equilibrium exchange rates.

24

In this study we try to identify this real factor by examining the ability

of real oil prices to account for permanent movements in the real effective

exchange rate of some major trading partners of Nigeria.

Agu (2002) examined the position of the observed real exchange rate

(RER) in relation to the unobservable equilibrium real exchange rate

(ERER) and estimated their time paths using the single equation procedure

and realized that over the sample period, RER misalignment was irregular

but persistent. The study ascertained the influence of these distortions

(misalignment) on the balance of payments as a gauge of the external

balance position of Nigeria. He finds that, RER misalignment, however,

affects both the trade balance and the capital account significantly. It was

observed that the misalignment spread throughout the whole of the sample

period with no more remarkable increase in period of floatation than in

period of fixation of exchange rate. He notes that the distortions could

have arisen from more fundamental factors in the economy. The question

then, is what are the more fundamental factors? On external balance, he

equally observed that capital flows are more responsive to RER distortion

than the trade balance.

A large literature exists on the theoretical and empirical linkages

between energy and economic growth (Stern and Cleveland, 2004).

25

Energy (especially oil) is a critical input in many productive processes and

therefore a causal factor for economic growth; in addition, economic growth

stimulates the consumption of oil by households. It is small wonder

therefore, that demand, supply and price of crude oil attracts so much

attention. There have been several studies on the link between oil prices

and U.S. macroeconomic aggregates (for example, Hamitton 1983,

Loungani 1986, Dotsey and Reid 1992), but exchange rates were not

included and evidence for other nations is lacking.

There has also been some analysis with calibrated macro-models (McGuirk

1983 and Yoshikawa 1990) which suggest that oil price fluctuations play an

important role in exchange rate movements, but these studies lack

econometric rigor and consider a data sample limited either in length or

number of currencies. Some studies such as Throop (1993), Zhou (1995),

and Dibooglu (1995) find evidence of a long-run relationship between

exchange rates and a number of macroeconomic factors including oil

prices. However, the tests used in these studies tend to produce false

evidence of co-integration when several variables are included in the

system (Gonzalo and Pitarakis 1994, and Godbout and Van Norden 1995).

They do not examine the causal relationship between these variables, so it

is not clear whether these are models of exchange rate determination, or

26

whether they simply capture the influence of exchange rates on a variety of

other macroeconomic variables. In another study by JEL (1996), testing for

co-integration between exchange rates and oil prices using the two-step

single equation approach developed by Engle and Granger (1987) show

strong evidence of co-integration between the price of oil measures and the

real effective exchange rates for Germany, and Japan but not for the

United States. On their further test using the augmented Dickey and Fuller

(1979) and Phillips and Ouliaris (1990) tests reject the null hypothesis of no

co-integration at the one percent level for the mark, and the five and one

percent level for the Yen. They further compare these conclusions using

an efficient (and therefore more powerful) co-integration test developed by

Johansen and Juselius (1990), the tests find evidence consistent with co-

integration for all three currencies suggesting that the price of oil captures

the permanent innovations in the real exchange rate for Germany, Japan

and the United states.

It has long been recognized that if one could find a missing real shock

that were sufficiently volatile, one could potentially take an important steps

towards resolving the PPP puzzle. Real oil price has the volatility and there

is some evidence that it is an important factor modeling the U.S. real

exchange movements. In articles such as Amano and Van Norden (1998),

27

and Lahtinen (2000), the U.S. real exchange rate is shown to be a positive

function of the real oil price, i.e. higher oil price will appreciate the U.S. real

exchange rate. Lahtinen (2000) also finds support for Harrod-Balassa –

Samuelson hypothesis if the oil price is included in the estimations. These

finding have shown to be stable, which seems to suggest that the failure of

exchange rate models to provide stable results is due to the missing

variable problem. The net effect of oil price shock on nominal exchange

rate depends on capital account changes i.e. whether, for example,

investment in dollar currency is more or less than America‟s share of the

industrial world‟s current account deficit. The unstable and unpredictable

nature of the oil price process makes it also a textbook example of the non-

discrete jump process. Krugman (2000), offers a multiply equilibrium

explanation for the oil price. On the other hand, a vast literature studying

exchange rate prediction has concluded that the best single predictor of the

exchange rate next period-tomorrow, next week, next month, maybe even

next year – is the exchange rate this period. One generally cannot do

better than a “no change” forecast for exchange rates (Meese and Rogoff

1983; Cheung et al 2002). The problem here is still the inability to find the

missing link.

28

In their own study, Olomola and Adejume (2006), using vector

autoregressive (VAR) model of the Nigerian economy, find that oil price

shocks do not have substantial effects on output and inflation rate in

Nigeria over the period covered by their study. Inflation rate depends on

shocks to output and the real exchange rates. However, their findings

demonstrated that fluctuations in oil prices do substantially affect the real

exchange rates in Nigeria. It was found out that it is not the oil price itself

but rather its manifestation in real exchange rates and money supply that

affects the fluctuations of aggregate economic activity proxy, the GDP.

They conclude that oil price shock is an important determinant of real

exchange rates and in the long-run money supply, while money supply

rather than oil price shocks that affects output growth in Nigeria. The

research ignored some important variables such as trade openness, terms

of trade, trade balance capital account that may contribute to explain the

transmission of the oil price shock to real exchange rate. One can say that

the study did not adequately capture the external sector of the economy,

hence the need to close the gap. Again, most of the available literatures

were on the demand side effect, that is, oil importing countries. There is

every need for us to look at the supply side effect, that is, the oil exporting

29

countries especially Nigeria as her major source of revenue comes from

crude oil exportation.

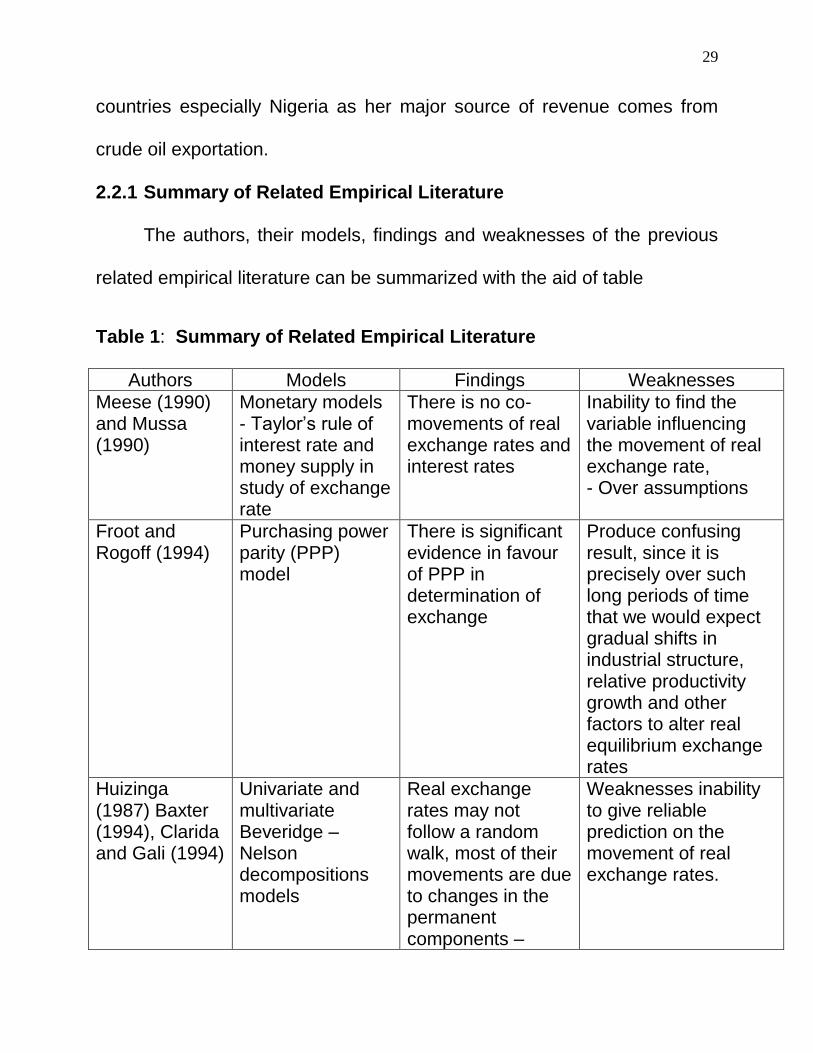

2.2.1 Summary of Related Empirical Literature

The authors, their models, findings and weaknesses of the previous

related empirical literature can be summarized with the aid of table

Table 1: Summary of Related Empirical Literature

Authors Models Findings Weaknesses

Meese (1990) and Mussa (1990)

Monetary models - Taylor‟s rule of interest rate and money supply in study of exchange rate

There is no co-movements of real exchange rates and interest rates

Inability to find the variable influencing the movement of real exchange rate, - Over assumptions

Froot and Rogoff (1994)

Purchasing power parity (PPP) model

There is significant evidence in favour of PPP in determination of exchange

Produce confusing result, since it is precisely over such long periods of time that we would expect gradual shifts in industrial structure, relative productivity growth and other factors to alter real equilibrium exchange rates

Huizinga (1987) Baxter (1994), Clarida and Gali (1994)

Univariate and multivariate Beveridge – Nelson decompositions models

Real exchange rates may not follow a random walk, most of their movements are due to changes in the permanent components –

Weaknesses inability to give reliable prediction on the movement of real exchange rates.

30

interest rate differentials and current account balance

Lastrapes (1992), Evans and Lothian (1993)

Blanchard and Quah (1989) decomposition model

There was much variance of both real and nominal exchange rates from a number of countries over both short and long horizons.

Inability to identify the real shocks

Agu (2002) Structural time-series using the single equation procedure

Discovered that over the sample period real exchange rate (RER) misalignment was irregular but persistent. He also notes that the distortions could have arisen from more fundamental factors in the economy

Inability to identify the fundamental factors that cause shocks in real exchange rate.

McGuirk (1983) and Yoshikawa (1990)

Calibrated macro models

Discovered that oil price fluctuations play an important role in exchange rate movements

These studies lack econometric rigour and consider a data sample limited either in length or number of currencies.

Throop (1993) Zhou (1995), and Dibooglu (1995)

Cointegration models

Find evidence of a long-run relationship between exchange rates and a number of macroeconomic factors including oil prices

They did not examine the causal relationship between these variables

31

JEL (1996) Co-integration model, between exchange rates and oil prices using the two-step single equation approach developed by Engle and Granger (1987)

Found strong evidence of co-integration between the price of oil and the real effective exchange rates for Germany and Japan

It did not sufficiently explain causal effect

Olomola and Adejume (2006)

Vector autoregressive (VAR) model

Their findings demonstrated that fluctuations in oil prices do substantially affect the real exchange rates in Nigeria. It is not the oil price itself but rather its manifestation in real exchange rates and money supply that affects the fluctuations of aggregate economic activity proxy, the GDP

The research ignored some important variables such as trade open-ness that may contribute to explain the transmission of the oil price shock to real exchange rate. Inability to trace causal effect sufficiently.

Shortcoming of Previous Works

1) They did not treat the order in which the exogenous variables will be

absorbed in the model.

2) The previous works were concentrated on oil importing countries i.e.

the demand side effect.

3) Inability to handle country specific effect.

32

4) The previous works could not trace the sources of real exchange rate

fluctuations through monetary models, PPP models and country

specific regression

5) Available work received could not trace the transmission of structural

shocks in real exchange rate and factors affecting it.

6) The relationship between current shock on oil price and its conditional

volatility in other periods ahead was not emphasized.

There is no much work on Exchange rate fluctuations and oil price and the

very few existing work did not use oil price shocks as an explanatory

variable in their model.

33

CHAPTER THREE

3.0 OVERVIEW OF THE NIGERIAN ECONOMY AND POLICY

RESPONSES

The major sources of government finances are oil and non-oil

revenues. The oil revenue includes proceeds from sales of crude oil,

petroleum profit tax (PPT), rents and royalties while the components of

non-oil revenue are companies income tax, customs and excise duties,

value-Added Tax (VAT) and personal income tax. Since the 1970s, oil

revenue has been the dominant source of government revenue,

contributing over 70 percent to federally collected revenue.

For the need to diversify the economy, foster rapid and sustainable

real growth, since after independence in 1960, the country has embarked

on many development plans. The first was the 1962-1968 plan that was

broadly expected to facilitate the achievement and maintenance of a high

rate of increase in the standard of living as well as provide necessary

conditions for wealth creation. The plan was met with many obstacles. Fifty

percent of the planned revenue was expected to come from external

sources in the form of aid and loans, much of which was never realized.

For this, annual average planned investment for the public sector was

never achieved. Again the political crisis in 1966 that ended up in civil war

34

marred the plan. In spite of all these obstacles, the plan recorded

successes in completion of the Port-Harcourt oil refinery; the Nigerian

security printing and minting plant; the Nigerian paper mill, Jebba; the

sugar company, Bacita; the Kainji Dam; the Niger Bridge Onitsha.

The second post-independence plan, the 1970-1974 was designed,

among other things, to provide a blue print for the task of reconstruction,

rehabilitation and reconciliation. The plan envisaged an average rate of

growth in real GDP of 6.6 percent. The target was exceeded as an average

growth rate of 8.2 percent was achieved. This significant achievement

came from unprecedented inflow of crude oil money. The original planned

expenditure was revised upwards by the availability of funds.

The third national development plan 1975-1980 was launched to use

the huge foreign reserves accumulated from the oil sales to provide

employment opportunities, to enhance the diversification of the economy,

to encourage balanced development and indigenization of the economy.

The implementation of the plan suffered a major financial set back owing to

the glut in the world crude oil market. To meet with the financial demand of

the plan, the government went into massive borrowing from the Eurodollar

market and from multi-national institutions. The economy was plunged into

35

debt. The projected 9.5 percent annual average growth rate of the GDP

was never achieved instead it declined from 8.2 percent to 5.5 percent.

The economy already in Debt trap, the fourth national development

plan 1981-1985 was launched amidst serious financial constraints. The

plan was designed to reduce the dependence of the economy on a narrow

range of activities, and to develop the technological base and thereby

increase productivity. The plan targets were not realized owing largely to

financial constraints. The world crude oil market had virtually collapsed, so

oil money was not coming, as it should be. The GDP declined in real terms

by 2.9 percent during the plan period as against the 4.0 percent increase

projected (CBN2000). The government went into a second round of

borrowing under the cover that Nigeria was “under-borrowed” to increase

the government foreign debt outstanding. Thus, the problem of the poor

performance of the plan was compounded with high debt overhang.

In 1986-1988, the government introduced the structural Adjustment

Programme. Hither to, the government had introduced austerity measures

by the end of 1985 to cut down consumer goods expenses in order to

encourage savings and investments. The structural Adjustment Programme

(SAP) was put in place with a view to removing, cumbersome

administrative controls and adopting more market-friendly measures and

36

incentives that would encourage private enterprise and more efficient

allocation and use of resources. The objectives of SAP among others

include

(i) Restructuring and diversifying the productive base of the

economy in order to reduce its dependence on the oil sector

and on imports,

(ii) Achievement of fiscal and balance of payments viability in the

short to medium term.

One of the major policy instruments employed to address these

objectives was exchange rate adjustment that resulted in a drastic

devaluation of the Naira vis-à-vis major trading currencies. This was aimed

at removing what the government observed as persistent over-valuation

hitherto induced by exchange controls.

A three-year rolling plan was adopted in the management of the

economy and it took effect from the end of 1988. One of the reasons for the

adoption of a rolling plan was that it was becoming increasingly difficult to

project resources over a long period, especially for a mono-cultural

economy that relied on crude oil, whose market had been very volatile and

over which the authorities had no control. The three-year rolling plan (1990-

37

92) was first formally launched in 1990 with the primary objective of

consolidating the achievement of the SAP.

Since inception, the rolling plans have been guided by the policy of

economic deregulation and the need for rapid economic recovery. The high

dependence of the economy on the sale of crude oil in the world market

makes it imperative to examine the indicators of a country‟s external sector

performance. The external sector reflects the economic transactions

between the residents of an economy and the rest of the world. The sector

can be in equilibrium or disequilibrium (surplus or deficit). An ideal external

sector is one that is stable and in equilibrium overtime. Equilibrium is

achieved when external receipts and payments are equal, the exchange

rate is not misaligned and stable and external reserves are adequate. A

state of equilibrium may not necessarily elicit policy actions, a state of

disequilibrium calls for urgent action to reverse the trend. The ability of

policy makers to introduce such timely and appropriate measures often

determines the speed at which equilibrium is restored. The management of

the external sector aggregates-exchange rate, external reserve and

external debt-could help in reversing trends in the balance of payments.

In a policy of deregulation the exchange rate is determined by market

forces but that is not totally the case with the country, there is duality of

38

exchange rate in the foreign exchange market. The foreign exchange

market was made up of two principal segments, the official and the parallel

market, between 1960 and 1985. During this period, a fixed exchange rate

system was in place. At the end of 1998, the market was made up of the

official, Bureau de change, inter-bank, Autonomous Foreign Exchange

Market (AFEM) and the parallel segments. In the official foreign exchange

market, the exchange rate is fixed while a market determined exchange

rate is applied in the other segments. Over the years the exchange rate has

been fluctuating, for examples, an average exchange rate of N0.8938 to

US$1 in 1985, the naira exchange rate went up to N2.0206 to US$1 in

1986. In 1987 it went up to N4.0179 to US$1. In 1990 it was N7.5916 to

US$1. In 1993 it was N22.1105 to US$1. The naira exchange rate to a US

dollar, keep increasing in nominal value and the real value keep

decreasing.

The exchange rate fluctuation is demand propelled and the supply of

foreign exchange is mainly determined by the sale of crude oil whose price

is determined by the world oil market. The exchange rate volatility cannot

be stable through exchange rate management alone but could be achieved

through increased non-oil export receipts, especially of the basket of

39

currencies-US dollar, British pound sterling, German Deutschemark, Swiss

Francs, French Francs, Japanese yen and Dutch guilder.

The Nigerian oil sector has a lot of contradictions that play, a major

role in naira exchange rate. The contradiction is more glaring with rise in

crude oil price at the global market; the rise will mean more external

earnings for Nigeria but will increase the expense burden on imported

refined petroleum products. This has been so because our local refineries

are not in operation and we rely on imported refined petroleum products.

3.1 Conceptual Issues

Petroleum production and export play a dominant role in Nigeria‟s

economy and account for about 90% of her gross earnings. This dominant

role has pushed agriculture, the traditional mainstay of the economy, from

the early fifties and sixties, to the background. While the discovery of oil in

the eastern and mid-western regions of the Niger Delta pleased hopeful

Nigerians, giving them an early indication soon after independence that

economic development was within reach, at the same time it signaled a

danger of grave consequence. Between, 1966-1970 Nigeria was into crisis

and civil war. But soon after the war, followed a three-year oil boom the

country was awash with oil money, and indeed there was money for

virtually all the items in its development plan.

40

The world oil boom and bust is collectively known as the “oil shock”.

Starting in 1973 the world experienced an oil shock that rippled through

Nigeria until the mid-1980s. This oil shock was initially positive for the

country, but with miss-management and military rule, it became all

economic disaster. The country was plunged into debt that eroded her

external reserve, her money (naira) was devalued and exchange rate

depreciated from N0.8938 = US$1 in 1985 to N22.1105 = US$1 in 1993.

The current (July, 2010) naira exchange rate to US dollar is about N157.00

= US$1. The enormous impact of oil shock could not escape scholarly

attention. From 1970s to date, the virtual obsession was to analyze the

consequences of oil on Nigeria, using different models and theories.

Equally, many exchange rate management strategies/policies have been

put in place to stabilize exchange rate fluctuations but to no avail.

Literature has shown that oil price shock/volatility affect the real

exchange rate of oil importing countries-Germany, Japan and United

States. A clear nexus has not been made between oil price shocks and real

exchange rate fluctuations in oil exporting countries especially, in Nigeria.

41

CHAPTER FOUR

4.0 METHODOLOGY

4.1 Methodological Framework

Capital mobility ensures the equalization of expected net yields in that

the domestic interest rate less the expected depreciation rate equals the

world rate. If the domestic currency is expected to depreciate, interest rate

on assets will exceed those abroad by the expected rate of depreciation.

r = r* + x …………………….. 4.1

where: r = domestic interest rate

r* = world rate of interest

x = expected rate of depreciation

In order to distinguish between the long-run exchange rate and the current

exchange rate, we assume the rate of depreciation to be

X = θ ( e -e) ………………………… (4.2

where: e = the logarithm of the current exchange rate

e = the long-run exchange rate

θ = the coefficient of adjustment

The demand for real money balances is assumed to be a function of

domestic interest rate and real income that will be equal to real money

42

supply in equilibrium. Under the assumption of conventional demand for

money, we have

- r + β y = m – p ………………………….. 4.3

Where:

m,p, and y = the logs of the nominal quantity of money, the price level and

the real income

The relationship between the spot exchange rate, the price level and the

long run exchange rate is given under the assumption that the money

market clears and net asset yields are equal. This is obtained by the

combination of equations 3.1, 3.2 and 3.3.

p-m = βy + r* + β ( e -e) …………………. 4.4

In a stationary money supply, long-run equilibrium implies equality

between interest rates since current and expected are equal. This makes

the long-run equilibrium price level to be:

p = m + ( r* - β y) …………………….. 4.5

The relationship between the exchange rate and the price level is derived

in the money market by substituting equation 4.5 in equation 4.4.

e = e -

1(p - p ) ………………………………. 4.6

where: all the variables remain as defined above (see Dornbusch 1988).

43

In the goods market, the demand for domestic output is a function of

the relative price of the domestic good, e – p, interest rates and real

income.

InD = δ (e – p) + y – vr + u ………………………… 4.7

where: δ, and v are the parameters

U = a shift parameter

D = the demand for domestic output

The rate of increase in the price of the domestic goods is specified as a

proportion to excess demand.

Pd = π In Y

D= π (U + δ (e-p) + -1) Y – vr ………………… 4.8

Equation 4.8 implies that the long run exchange rate is

e = p +

1(Vr* + (1- ) y – u …………………… 4.9

where: p = long run equilibrium price level.

A class of autoregressive conditional heteroscedasticity that captures

the volatility clustering of the financial time series was developed by Engle

in 1982. He specified conditional variance of the shock that occurs at time

t, as a linear function of the squares of the past shocks

ht = w + 2 t-1 ----------------------------------- 4.10

where: ht = conditional variance > 0

44

ε1t = past shocks

w > 0, 1

> 0

The only chance for more persistent auto correlations is to include

additional lagged squared shocks in equation 4.10.

ht = w + 1

ε 2

t-1 + 22

2 t + ------- + qtq 2

----------------- 4.11

In 1986, Bollerslev added lagged conditional variances to equation 4.11

and it became Generalized ARCH (GARCH) model.

ht = w +α )(212

2

111

2

1

ttt hw --------------------------- 4.12

where all the variables are still as defined above.

4.2 The Model

We used GARCH variance, exponential GARCH (EGARCH) model

and vector Error correction (VEC) model to capture different hypotheses

specified in this work. EGARCH model is principally used to trace the

volatility of exchange rate while VEC model is used in tracing the

transmission of structural shocks among the variables in the model.

4.3 Battery Tests

In this section, we tested for the order of integration and co-

integration among the variables in the model.

45

4.3.1 Unit Root Test:

We employed Augmented Dickey Fuller (ADF) to test for the order of

integration. The choice for this test is made because it is more reliable and

robust than the Dickey Fuller (DF) test. It also eliminates the presence of

autocorrelation in the model. ADF unit root test is specified as:

yi t = iti

n

i

tioUyy

1

1

11 ------------------------------ 4.13

where: yi = variables in the model

0

, 1

and = parameters in the model

ui = Error term.

A variable is stationary of the order in which its ADF test statistic is greater

in absolute value than the ADF critical values at different levels of

significance.

4.3.2 Co-integration Test

In this section, we determined whether the variables are integrated

and identified the long run relationships. A VAR – based co-integration

tests were employed using Johansen methodology.

4.3.3 Estimation Procedure

This VAR – based model of order n can be specified as:

Yt = Atyt-1 + ----- + Anyt-n+ β Xt-1 + et -------------------- 4.14

46

where: yt = K-vector of non-stationary, 1(1) variables

Xt = d vector of deterministic variables

et = vector of innovation

Equation 4.14 can be written as

1

1

1

n

i

ittyy

txtity

------------------------ 4.15

where: 1

1

n

i

iA

n

ij

jiA

1

In accordance with the Granger‟s representation theorem, if the

coefficient matrix has reduced rank, r<k there exist kxr matrices and

each with rank r in a way that = and t

y1

is stationary. In this case, r

is the number of co-integrating relations (the co-integrating rank) while

each column of is the co-integrating vector. In Johansen, we estimate the

matrix in an unrestricted form and test whether we can reject the

restriction in the reduced rank of . It is pertinent to note that the co-

integrating vector is not identified unless we impose some arbitrary

normalization (use of E-views 3.1 version).

47

4.4 Model Specification

4.4.1 Exponential GARCH Model

The Exponential GARCH (EGARCH), which allows for asymmetric

effect is specified as;

In (ht) = w + 1

Zt-1+ 1 (/Zt-1/ – E(/Zt-1/)) + β ln(ht-1) ---------------- 4.16

where: Inht = the logarithm of conditional variance

Zt-1 = past shocks

and,,11

, are the parameters which have no restriction in order to ensure

that ht-1 is non-negative.

4.4.2 Estimation Procedure

Equation 4.16 explains the relation between previous socks and the

logarithm of the conditional variance. In this model, there is no restriction

on 1

, 1

and β1 in order to ensure that the conditional variance (ht-1) is non-

negative. The properties of Zt state that it has zero mean and is

uncorrelated i.e.

g(Zt) = 1

Zt + 1

(/Zt/ - E(/Zt/)) ………………………… 4.17

The equation 4.17 is piece wise linear in Zt and can be specified as

g(Zt) = (1

+1

) ZtI(Zt > 0) + (1

-1

) Zt I (Zt < 0) - 1

E(/Zt-i/)) …………. 4.18

The negative shock impact on the log of conditional variance is 1

-1

while that of positive shock is 1

+1

. We used News Impact Curve (NIC) to

48

show how new information is incorporated into volatility. NIC shows the

relationship between the current shocks, et and the conditional volatility of

other periods ahead, ht-1, holding constant all other past and current

information. The asymmetric News Impact Curve (NIC) for this model is

specified as:

NIC (et/ht = 19.4

0exp

0exp

)

*

11

*

11

2

t

t

t

t

efore

A

efore

A

Where: A = 21

11

2 2exp(

w

The NICs are equal when et = 0. It is pertinent to note that negative

shocks in EGARCH model have larger effects on the conditional variance

than the positive shock of the same size. In this case, as et increases, the

impact on ht becomes larger in the model.

4.4.3 Vector Error Correction Model (ECM)

A vector Error Correction (VEC) is a restricted VAR transformed into

VEC because of its co-integration restriction built into its specification. This

model is designed to be used with non- stationary series that are co-

integrated. This is specified as

RERt = + 11

ε∆RERt-i + 12

ε∆OIPt-i + 13

ε∆REFt-i + 14

ε∆OPFt-i

+ 15

ε∆IIPt-i + 16

ε∆IPRt-i + 17

ε∆TROt-i 18 εECM1t + εu1t ------- 4.20

1

49

OIPt = + 21

ε∆OIPt-i + 22

ε∆RERt-i + 23

ε∆REFt-i + 24

ε∆OPFt-i

+ 25

ε∆IIPt-i + 26

ε∆IPRt-i + 27

ε∆TROt-i + 28 εECM2t+ εu2t -------- 4.21

REFt = + 31

ε∆REFt-i + 32

ε∆RERt-i + 33

ε∆OIPt-i + 34

ε∆OPFt-i

+ 35

ε∆IIPt-i + 36

ε∆IPRt-i + 37 ε∆TROt-i +

38 εECM3t+ εu3t -------4.22

OPFt = + 41

ε∆OPFt-i + 42

ε∆RERt-i + 43

ε∆OIPt-i + 44

ε∆REFt-i

+ 45

ε∆IIPt-i + 46

ε∆IPRt-i + 47

ε∆TROt-i + 48

εECM4t + εu4t ---4.23

IIPt = + 51

ε∆IIPt-i + 52

ε∆RERt-i + 53

ε∆OIPt-i + 54

ε∆REFt-i

+ 55

ε∆OPFt-i + 56

ε∆IPRt-i + 57

ε∆TROt-i + 58

εECM5 t + εu5t ----4.24

IPRt = + 61

ε∆IPRt-i + 62

ε∆RERt-i + 63

ε∆OIPt-i + 64

ε∆REFt-i

+ 65

ε∆OPFt-i + 66

ε∆IIPt-i + 67

ε∆TROt-i + 68

εECM6t + εu6t----- 4.25

TROt = + 71

ε∆TROt-i + 72

ε∆RERt-i + 73

ε∆OIPt-i + 74

ε∆REFt-i

+ 75

ε∆OPFt-i + 76

ε∆IIPt-i + 77

ε∆IPRt-i + 78

εECM6t + εu7t----- 4.26

4.4.4 Estimation Procedure

A vector error correction (VEC) model is a restricted VAR that has co-

integration in order with non- stationary series that are co-integrated. It

restricts the long-run behaviour of the explanatory variables to converge to

their co-integration relationships while allowing a wide range of short-run

dynamics (Sarte, 1997). VEC model is specified as:

iiiitiiititiuECMyyy

1,

------------ 4.27

2

3

4

5

6

7

50

where:

iy = change in individual variable in the model.

72,1

i

7722,21,1211,,,

i= parameters in the model.

1ity = lagged variables in the model

iu = Random innovations

= error correction parameter

ECM = Error correction term

(Davidson and Mackinnon 1993, Hamilton 1994, Sarte 1997)

Where: RER = real exchange rate

OIP = international oil price

REF = real exchange rate fluctuations

OPF = international oil price fluctuations

IIP = index of industrial production (as a proxy to GDP)

IPR = industrial production growth rate

TRO = GDP

MX

X = Export

M = Import

51

ECMs = Error correction terms which are generated from the co-

integrating residuals.

We call the co-integration term an error correction term because the

deviation from the long run equilibrium is gradually corrected through a

series of partial short-run adjustment. (See, Amin and Awung 1997, Parikh

1997, Cooley and Leroy 1985, Sarte 1997)

4.4.5 Justification of the Models

We employed Augmented Dickey Fuller (ADF) test statistic to test the