exam content and outline - financialops.orgpreparation+packet_new_08.16.13.pdfthe exam includes 200...

TRANSCRIPT

Exam Content and Outline

Page 1

The exam includes 200 multiplechoice questions, via computerbased testing (CBT), and allows threehours for completion. The difficulty level of this exam is similar to the CPA (Certified Public Accountant)and CPP (Certified Payroll Professional) exams.

The outline below reflects the subject areas/domains tested on the CAPP certification exam. Thepercentage of exam items relative to each area/domain is noted below as well.

Domain 1 – Relationships and Responsibilities (16%)

01 Management Responsibilities (10%)01 – Create department mission statement.02 – Communicate corporate and department mission statements.03 – Ensure compliance with corporate and department mission statements.04 – Develop department job descriptions.05 – Recruit potential employees and hire.06 – Interview applicants.07 – Define staff roles, responsibilities, and segregation of duties.08 – Identify/determine department policies and procedures.09 – Document department policies and procedures.10 – Update department policies and procedures.11 – Communicate department policies and procedures.12 – Establish and communicate employee and department goals.13 – Assess training requirements.14 – Develop training program.15 – Crosstrain employees.16 – Rotate staff.17 – Establish department communication tools.18 – Develop departmental conflict resolution process.19 – Establish formal evaluation feedback and review process.20 – Establish employee recognition program.21 – Develop a succession plan and mentoring program.22 – Ensure compliance with companydefined business ethics.23 – Develop and monitor department budget and forecasts.

02 Customer Relations/Partnerships (2%)01 – Develop and maintain customer relationship policies and procedures.02 – Follow established customer relationship policies and procedures.03 – Resolve customer disputes.04 – Create customer surveys and solicit feedback (including create action plan and followup

communications).

03 Staff Motivation and Morale (2%)01 – Effectively communicate change (reason for change, benefits of change, what the change

means to the employees, implementation plan, followup).

Page 2

02 – Build an effective team (coaching, mentoring, celebrating, establishing communication,recognition/rewards).

03 – Promote accounts payable value to upper management (share key statistics and valueaddedprojects, communicate the value of CAPP/certification).

04 Project Management (2%)01 – Develop project charter (develop mission statement, identify team resources, establish

timelines, develop scope document).02 – Identify budget requirements03 – Develop project plan and perform testing.04 – Execute steps in the project plan.05 – Monitor and report progress of project.06 – Ensure that project objectives have been met.07 – Conduct postproject plan review.

Domain 2 – Processing Functions (16%)

01 Invoice Handling (6%)01 – Open and process source documents (date stamp, image, sort, distribute).02 – Determine whether invoice or statement is valid.03 – Research and document resolution of problem invoices.04 – Review and recover debit balances.05 – Reconcile or resolve open items on vendor statements.06 – Review requests for payment for: purchase order number, signature and approval, general

ledger codes, vendor information.07 – Review requests for payment for: policy compliance.08 – Review requests for payment for: payment terms and discounts, taxability, tax rates, type of

currency.09 – Identify special handling requirements.10 – Process vendor refunds.11 – Set up recurring payments.

02 Matching (1%)01 – Understand matching requirements and rules.02 – Perform matching functions.03 – Resolve discrepancies that fall out of the matching process.

03 Procurement Card (3%)01 – Define guidelines for Pcard program.02 – Communicate guidelines for Pcard program to users.03 – Ensure compliance with Pcard program.04 – Reconcile Pcard statements and resolve disputes.

05 – Maintain appropriate records as per company retention policy.06 – Process and verify Pcard transactions.

Page 3

07 – Review Pcard transactions for governmental tax compliance.

04 Payment Processing (6%)01 – Determine payment type (check or electronic).02 – Determine payment frequency.03 – Determine cash requirements.04 – Print checks.05 – Secure signatures per company policy.306 – Create electronic payment file.07 – Distribute checks.08 – Resolve payment exceptions (special handling).09 – Process voids/stop payments/reissues.10 – Print and review payment document reports.11 – Create positive pay file.

Domain 3 – Travel and Entertainment (9%)

01 Travel Card Administration and Management (4%)01 – Review and analyze report data (disputed items, exceptions, unexpensed items).02 – Define guidelines for T&E program.03 – Create statistical management reports.04 – Reconcile statements.05 – Identify and analyze opportunities for cost savings and rebates.06 – Communicate guidelines for T&E program to users.07 – Identify and communicate reimbursement options to staff and other employees.08 – Maintain appropriate records as per company retention policy.09 – Process and verify T&E transactions.

02 Governmental Guidelines (2%)01 – Interpret guidelines.02 – Review guidelines with staff.03 – Train staff and other employees on guidelines.04 – Update and communicate guidelines.05 – Ensure W2, VAT, and other reportable data is identified and reported.

03 Expense Reporting (3%)01 – Scan, dataenter, or interface documents.02 – Reject noncompliant/incomplete T&E documents.

Page 4

03 – Contact employees for T&E documents.04 – Review T&E documentation for completeness (accounting, approval, receipts, compliance to

company and governmental guidelines, and employee identification).05 – Approve and process payment.06 – File documents.

Domain 4 – Controls (15%)

01 Vendor Master Files (4%)01 – Establish rules for vendor master files.02 – Maintain vendor master files.03 – Obtain governmental regulatory forms (W9, GST, W8, etc.).04 – Assign appropriate code classification (e.g., merchant commodity codes).05 – Research for possible duplicate records in the vendor master file.06 – Establish remittance controls and currency exchange.07 – Archive and purge vendor files.08 – Ensure segregation of duties and manager review.09 – Establish document controls and record retention.

02 Cash Management (3%)01 – Follow rules to improve cash flow.402 – Forecast cash requirements.03 – Follow float guidelines.04 – Follow guidelines for letters of credit.05 – Manage impact to income statement (payment terms, discounts, cost of borrowing).06 – Follow rules for petty cash.07 – Void stale dates checks from bank file.08 – Follow process for electronic payment options.09 – Follow process for foreign payments and hedged dollars.

03 Audits (4%)01 – Evaluate compliance with internal procedures and control.02 – Retrieve documentation required for audits.03 – Review audit findings.04 – Provide responses to audit findings.05 – Take corrective actions.06 – The controls selfassessment process.07 – Manage internal and external relationships.08 – Establish criteria for performing recovery audit reviews.

Page 5

09 – Respond to audit confirmations from vendors.

04 Fraud (4%)01 – Identify areas of potential fraud (vendor, employee, check, T&E, etc.).02 – Assess risks for areas of fraud (vendor, employee, check, T&E, etc.).03 – Establish and promote mitigating controls to minimize exposure.04 – Document risk and control procedures.05 – Follow standards for check security features.06 – Promote electronic payment initiatives (i.e., ACH, direct deposit, etc.).07 – Establish positive pay and reverse positive pay control procedures.08 – Confirm that personnel have appropriate levels of system access.

Domain 5 – Tax and Regulatory Issues (21%)

01 Sales and Use Tax (3%)01 – Identify state of jurisdiction02 – Determine whether item is taxable.03 – Selfassess use tax if required.04 – Resolve overcharges for taxes billed in error.05 – Calculate tax due based on state, city, or county rates.06 – Send vendors sales tax exemption certificates.07 – Maintain current exemption certificates.

02 1099 Reporting (7%)01 – Request Transmittal Control Code for electronic filing.02 – File extension with government.03 – Consolidate various payment sources into appropriate file.04 – Run and review payment files.05 – Review final payment reports.06 – Determine 1099 form and record payment in appropriate box.07 – Send 1099 to recipient.08 – Correct and send recipient copies as needed.509 – Create and send 1098 reports to government.10 – Research BNotice Items (due diligence).11 – Send corrected 1099 files to government.12 – Send BNotice forms to recipients.13 – Record due diligence in files.14 – Exercise backup withholding per government requirements.15 – Correct vendor files.16 – Flag second notice vendors.17 – Retain records according to government guidelines.

Page 6

03 1042/1042S Reporting (.5%)01 – Create report of payments subject to 1042/1042S filing.02 – Review report prior to filing.03 – Send 1042S to recipient.04 – File required forms with government by due date.

04 Independent Contractor (3%)01 – Review W9 to determine filing status.02 – Review supporting documentation to further determine that the payee qualifies as an

independent contractor.03 – Set up Vendor Master File with 1099 information for reporting.04 – Ensure compliance with government regulations.05 – Determine whether backup withholding is required.06 – Determine and comply with state reporting.07 – Report on independent contractors.

05 Escheatment (3%)01 – Identify unclaimed property.02 – Exercise due diligence to locate owner of unclaimed property.03 – Research and verify that property is truly unclaimed.04 – Identify state of jurisdiction for unclaimed property.05 – Comply with state reporting requirements.06 – Archive filed reports.07 – Coordinate customer refunds with accounts receivable.08 – Clear stale dated checks to escheatment account.

06 Value Added Tax (1%)01 – Identify recoverable VAT items.02 – Prepare documentation for reporting.03 – Review report.04 – File report with government.05 – Prepare accrual for anticipated recovery/payment.06 – Reconcile general ledger account to receipts.07 – Archive reports.

07 Minority and WomenOwned Businesses (.5%)01 – Setup and maintain MWOB indicator in vendor master file.

08 Sarbanes Oxley (3%)01 – Prioritize general ledger accounts and account disclosures.02 – Consider significance to financial reporting and risk of misstatement.

Page 7

03 – Document transaction flows that materially impact financial reporting elements, which areconsidered priority.

04 – Identify controls and determine who owns them.605 – Document entity level controls.06 – Document controls at the “source of the risk” or downstream in the process.07 – Assess the effectiveness of the controls design at the entity and process levels.08 – Determine whether controls are appropriate and comprehensive.09 – Consolidate, disclose, and report results.

Domain 6 – Technology (9%)

01 – Processing Software (1%)01 – What is AP Automation?02 – Paper Invoice Management and OCR03 – Stages of AP Automation04 – Benefits of AP Automation

02 – Imaging and Data Capture (2%)01 – Prepare Documents for Scanning02 – Scan Documents03 – Index Documents04 – Verify Image of Documents05 – Destroy or Retain Paper Documents per Company Policy06 – Reconcile Imaged Documents vs. Indexed Documents

03 – Workflow (3%)01 – Define Business Rules02 – Define Roles03 – Create Workflow (e.g., vendor master setup, invoice approval, problem resolution, workdistribution, accounting validation)04 – Monitor and Maintain Workflow

04 – Electronic Invoicing (2%)01 – Electronic Invoicing Solutions02 – Vendor Adoption03 – Convergence of Imaging and eInvoicing04 – Selecting a Solution

05 – Procure to Pay (1%)01 – Procure to Pay Universe02 – Determine Trading Partners03 – Determine Security Levels04 – Monitor Compliance to Electronic Standards

Domain 7 – Other Topics (14%)

Page 8

01 Operational Analysis (3%)01 – Determine benchmarking criteria (industry, source, size of company).02 – Develop internal metrics.03 – Gather data for internal analysis.04 – Compare internal metrics to benchmark results.05 – Identify process improvements based upon metrics and benchmark reviews.

02 Disaster Recovery (3%)01 – Assess potential risks of business interruption.02 – Prioritize operational tasks.703 – Develop plan for continuous operation.04 – Document plan.05 – Incorporate AP plan into company plan.06 – Conduct periodic reviews.07 – Communicate approved plans.08 – Test recovery plan.

03 Outsourcing and/or Shared Services (3%)01 – Understand benefits and liabilities.02 – Identify opportunities.03 – Perform cost benefits analysis.04 – Identify and research potential vendor sources.05 – Negotiate vendor contracts.

04Accounting (5%)01 – Identify, document, and communicate accounting terminology and acronyms.02 – Create fiscal calendar for AP department.03 – Determine tasks for period closings.04 – Prepare accruals.05 – Reconcile cash and payables.06 – Post invoices to general ledger.07 – Review outstanding payables.08 – Close accounting period.09 – Correct journal entries.10 – Understand and apply accounting principles impacting financial statements

Page 9

Study Questions

Page 10

1. Which of the following is NOT a function or aspect of the evaluated receipt settlement process?

a. Eliminates the invoices from the matching process.b. REquires a packing slip in order to complete the process.c. Reduces costs for both accounts payable and the vendor.d. Clears existing invoices from the accounts payable system.

2. Which of the following travel expenses are considered ordinary and necessary?

a. First class airfareb. Frequent flyer club membershipc. Customer gifts and entertainmentd. Mileage and gas for use of personal car

3. Certain types of suppliers can be excluded from a travel card program of “blocked” transactionsbased on:

a. SICb. UPCc. UCC

Page 11

d. MCC

4. The IRS eased the amount of paperwork associated with travel and entertainment reports byrequiring receipts only on those expenses that exceed what amount?

a. $50b. $55c. $70d. $75

5. What IRS form is required for reporting amounts paid, or treated as paid, for excessreimbursement or allowance paid to an employee?

a. Form W2b. Form W4c. Form 1099INTd. Form 1099MISC

6. Who usually remits sales and use tax when the seller has established nexus in the taxingjurisdiction?

a. Sellerb. Purchaserc. Seller’s stated. Purchaser’s state

7. The IRS Form 4419 is used for:

a. Reporting federal income tax withheld on Form 1099.b. Applying to file information returns electronically.c. Requesting an extension to file.d. Reporting dividend payments.

Page 12

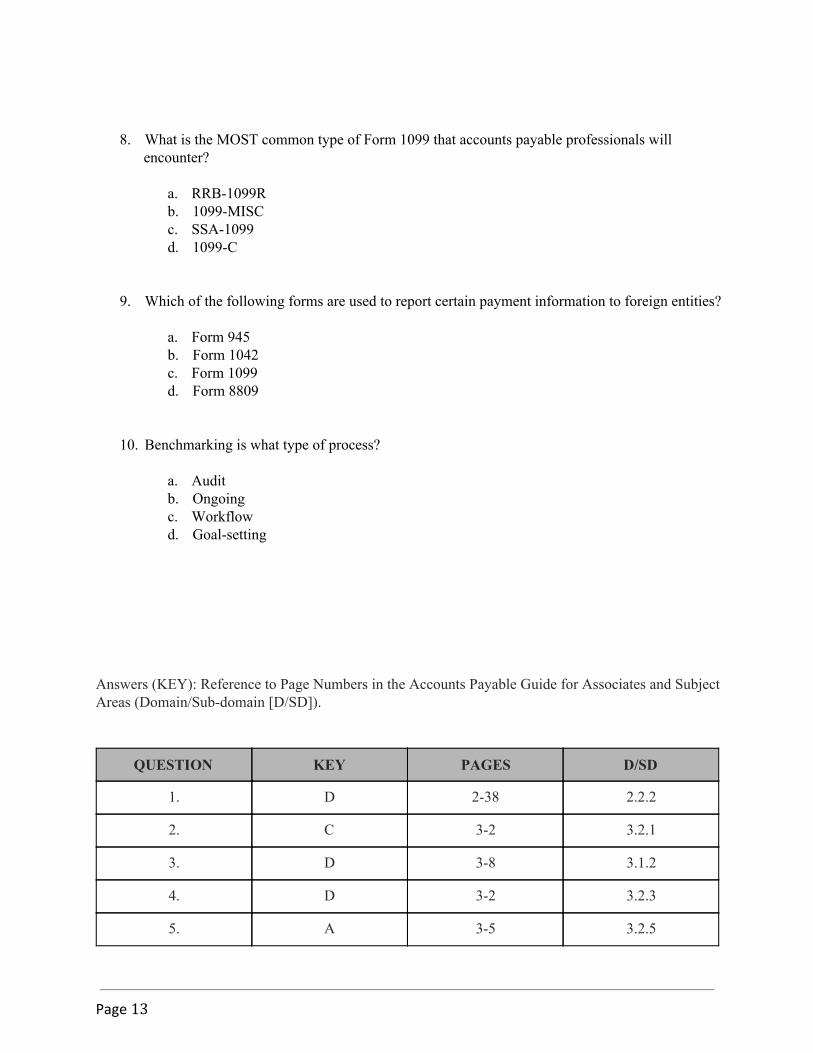

8. What is the MOST common type of Form 1099 that accounts payable professionals willencounter?

a. RRB1099Rb. 1099MISCc. SSA1099d. 1099C

9. Which of the following forms are used to report certain payment information to foreign entities?

a. Form 945b. Form 1042c. Form 1099d. Form 8809

10. Benchmarking is what type of process?

a. Auditb. Ongoingc. Workflowd. Goalsetting

Answers (KEY): Reference to Page Numbers in the Accounts Payable Guide for Associates and SubjectAreas (Domain/Subdomain [D/SD]).

QUESTION KEY PAGES D/SD

1. D 238 2.2.2

2. C 32 3.2.1

3. D 38 3.1.2

4. D 32 3.2.3

5. A 35 3.2.5

Page 13

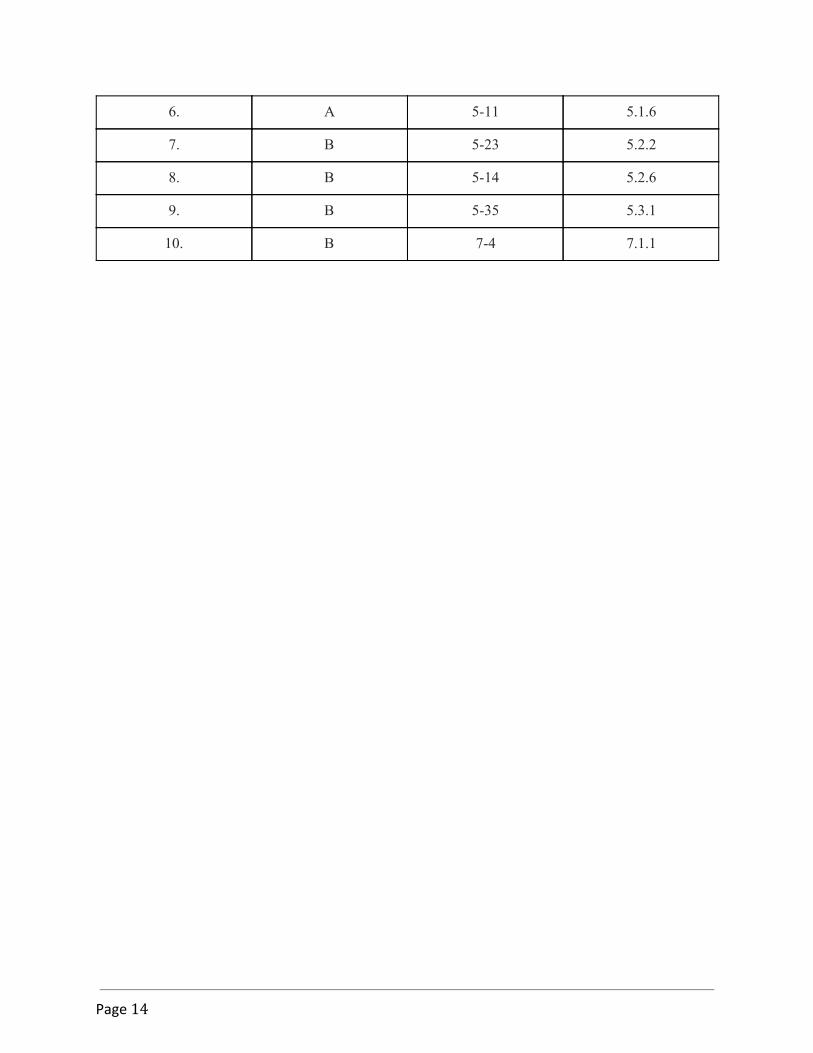

6. A 511 5.1.6

7. B 523 5.2.2

8. B 514 5.2.6

9. B 535 5.3.1

10. B 74 7.1.1

Page 14

Study Guide

Table Of Contents

1. Studying for the Exam 16

Page 15

1.1 Studying and Concentration 16

1.2 What Can Be Controlled within your Study Process 16

1.3 Using Memory Effectively 16/17

1.4 Additional Study Methods 17

1.5 Additional Tips 17

2. Test Preparation Process 18

2.1 Test Preparation and Avoidance of Test Taking Anxiety 18

2.2 Test Preparation to Reduce Anxiety 18

3. During the Exam 18

3.1 Test Taking Tips 19

3.2 Multiple Choice Tests 19

3.3 Strategies to answer difficult questions 19

References 20

Page 16

1. Studying for the Exam

1.1. Studying and Concentration

Think of the times when you were "lost" in something you enjoyed: a sport, playing music, a goodgame, a movie. These are examples of when you experienced total concentration.

Even though we all have the ability to concentrate, sometimes:Our minds wander from one thing to another; our worries sidetrack us;The material we are studying may seem “boring”, difficult, and/or not interesting.

When this happens, it is best to focus on what you can control while studying. The approacheslisted below may help with your focus and assist you to make the best use of your time.

1.2. What Can Be Controlled within your Study Process

Know how many weeks/months you have to study for the test. Make a calendar andidentify how much material will need to be studied on a daily/weekly basis to ensure youare ready on test day.

Set up a dedicated space, which should include your own chair, table, lighting, andenvironment.

Avoid your cell phone or telephone. Put up a sign to avoid disturbances or interruptions. You may use music for “background”, but do not let it be a distraction. Before you begin studying, take a few minutes to focus. Summarize a few objectives,

gather what you will need, and think of a general strategy of accomplishment. Create an incentive, if necessary, for successfully completing a task, such as calling a

friend, a foodtreat, a walk, etc. Change the subject you study every one to two hours for variety. And, if possible, vary

your study activities – alternate reading with more active learning exercises.

1.3. Using Memory Effectively

1. Acronyms and Acrostics: (for information involving key words)An acronym is an invented combination of letters. Each letter is a cue to an idea you need toremember. Example: BRASS is an acronym for how to shoot a rifleBreath, Relax, Aim,Sight, and Squeeze.

An acrostic is an invented sentence where the first letter of each word is a cue to an ideayou need to remember. Example: EVERY GOOD BOY DESERVES FUN is an acrostic toremember the order of Gclef notes on sheet musicE, G, B, D, F.

2. RhymeKeys: (for ordered or unordered lists)First, memorize key words that can be associated with numbers. For instance, bun with one;shoe with two, tree with three, door with four, hive with five, etc.

Next, create an image of the items you need to remember with key words. For example, ifyou had to remember the four basic food groups dairy products; meat, fish, and poultry;

Page 17

grains; and fruit and vegetablesimagine cheese on a bun, livestock, a sack of grain, and aroom stocked with fruits and vegetables.

3. The ImageName Technique: (for remembering names)Simply invent any relationship between the name and the physical characteristics of theperson. For example, if you had to remember Shirley Temple's name, you might ingrain thename in memory by noticing that she has "curly" (rhymes with Shirley) hair around hertemples.

1.4. Additional Study Methods

The methods below will provide you with an accurate perception of how well you know thematerial. It will force you to think about the material, rather than just look it over.

Take notes and review them frequently, so the material is "fresh.” As you are reading your textor reviewing your notes, generate and write down questions about the material.

Imagine you are teaching the course. What questions would you ask on the exam? Keep track of any terms you need to know. Write each question or term on the back of an index card.

1. On the front of each index card, write an answer or an explanation for the question orterm on the back.

2. Use your notes and text for a reference but put the answer or explanation in your ownwords whenever possible.

3. Shuffle the index cards (so you can't figure out any answers based on their location inthe deck).

4. Look at the card on the top of the deck. Try to answer the question or explain the term. • If you know it, great; then put it on the bottom of the deck. • If you don't know it, look at the answer, and put it a few cards down in the deck (soyou'll come back to it soon).

5. Proceed through the deck of cards until you know all of the information.

1.5. Additional Tips

Carry your cards with you everywhere. Take advantage of any extra time you have to study the exam material. If you think you know an answer, but can't put it into words, you probably don't know it well

enough. Being able to explain the information is the only way to be sure that you know the material; it is

also the best way to prevent test anxiety. Study with a colleague or study group. You can share ideas and help each other out with

concepts. In addition, you can use each other to make sure that you're explaining your answersadequately.

Page 18

2. Test Preparation Process

Create study checklists and identify all of the material that will be included in the exam. Thischecklist will enable you to break your studying into organized, manageable “chunks”, whichshould allow for a comprehensive review plan with minimal anxiety.

Create summary notes and "maps.” Briefly map out the important ideas of the material and therelationships of these ideas. Summary notes should display lists and hierarchies of ideas. Creativityand a visual framework will help you recall these ideas.

Create flashcards for definitions and lists that you need to have memorizedput topics on one sideof the card, answers on the other. Flashcards will enable you to test your ability to recognizeimportant information, but also your ability to retrieve information from scratch.

2.1. Test Preparation and Avoidance of Test Taking Anxiety

Develop good study habits and strategies. Manage your time and find ways to deal withprocrastination and distractions.

Organize study materials. Take a systematic approach to build a strategy and to prevent being overwhelmed.

The strategy should focus on new or unfamiliar material.

2.2. Test Preparation to Reduce Anxiety

Approach the exam with confidence and use whatever strategies you can to personalize success.Suggestions are visualization, logic, talking to your self, practice, and/or teamwork.

View the exam as an opportunity to show how much you've studied and to receive a reward forthe studying you've done.

Be prepared! Learn your material thoroughly and organize the materials you will need for the test. Know your test taking day, time and location: write it down and keep it with you Allow yourself plenty of time – especially for the things you need to do before the test – and get

to the testing site a little early, Avoid thinking you need to cram just before. Strive for a relaxed state of concentration. Avoid speaking with any fellow students who distract

your preparation, express negativity, or are not prepared. Get a good night's sleep the night before the exam.

3. During the Exam

If you find yourself tensing and getting anxious during the test:

Relax; you are in control. Take slow, deep breaths. Pause; think about the next step and keep on task, step by step. Use positive reinforcement for yourself. Focus on doing your best.

Page 19

Realize that anxiety can be a "habit" and that it takes practice to use it as a tool to succeed.

3.1. Test Taking Tips

Read the directions carefully, you will have 15 minutes to complete the tutorial before the exambegins.

Know how long you will have to complete the test: CAPP’s will have 3 hours CAPA’s will have 1 ½ hours

If you go “blank”, mark the question for later review and go on to the next question. Answer easy questions first. Easy questions will build confidence, score points, and mentally orient

you to vocabulary and concepts. Then, answer difficult questions. With objective tests, first eliminate those answers you know to

be wrong, are likely to be wrong, or ones that don't seem to fit. Resist the urge to leave as soon as you have completed all the items. Review your test to make sure that you have answered all questions. Change answers to

questions if you originally misread them or if you have encountered information elsewhere in thetest that indicates that your first choice is incorrect.

Don't panic when others start leaving the test area, remember they could be taking a differentexam. There's no reward for being the first one done.

3.2. Multiple Choice Tests

All questions on the exams are multiplechoice questions. They include a phrase or questionfollowed by four possible answers.

There are no questions with all of the above none of the above never

If you have time to go through the exam a second time, you may pick up cues for answers fromthe first reading, or become more comfortable in the testing situation.

If time allows, review both questions and answers. It is possible you will have incorrectly readquestions the first time.

Treat each option as a truefalse question, and choose the "truest.”

3.3. Strategies to answer difficult questions

Eliminate options you know to be incorrect. Question any option that grammatically does not fit with the stem. Question any option that is very unfamiliar to you. Question any option that contains a negative or absolute word. Try substituting a qualified term for the absolute one, like frequently for always; or typical for

Page 20

every, to see if you can eliminate it. "Look alike options" Probably one is correct; choose the best but eliminate choices that mean the

same thing, and thus cancel each other out. Double negatives Create the equivalent positive statement and consider. EXCEPT – for example “All of the following items are good choices for an exam EXCEPT:” look for the exception to the group or category.

References

Divine, James H., and David W. Kylen. How to Beat Test Anxiety and Score Higher on YourExams. Woodbury, New York: Barron's Educational Series, Inc., 1979.How to Beat Test Anxiety and Score Higher on Your Exams begins by helping students to understandhow they experience test anxiety before helping them take steps to reduce it. Suggestions on how toreduce test anxiety include replacing negative selfstatements with selfaffirming statements, and learninghow to relax. The second half of the book focuses on developing testtaking skills, especially thoserequired for multiple choice questions.

Fleet, Joan, Fiona Goodchild, and Richard Zajchowski. Successful Learning. London, Ontario: Universityof Western Ontario, 1987.Successful Learning is an introduction to study skills, an earlier version of Learning for Success. There isan inventory at the beginning to help students identify their strengths and weaknesses followed by chapterson time management, essay writing, science problem solving, exam preparation, and others. The authorsencourage students to be strategic, to study "smarter not harder."

Hanau, Laia. The Study Game. New York: Barnes & Noble Books, 1979.The Study Game is well titled because the author approaches studying as if it were a game which studentscan learn how to win. It covers reading for information, conveying that information, consolidatinginformation for exams, and writing exams. The language is informal, frequently using point form ratherthan complete sentences, and the text accompanied by sketches, arrows, and circled major points.Students who like mindmapping and take nonlinear notes, will find this book helpful.

Jones, Bill, and Roy Johnson. Making the Grade. Manchester, UK: Manchester University Press, 1990.In two volumes, Making the Grade shows how to improve study skills. Volume I examines input, learningnew information, and Volume II examines output, presenting ideas in papers and exams. The books areorganized in brief segments with prescribed rest and reflection. There are anecdotes to illustrate points andto help students deepen their understanding of their own experience.

MacFarlane, Polly, and Sandra Hodson. Studying Effectively and Efficiently: An Integrated System.Toronto: University of Toronto, 1983.Studying Effectively and Efficiently: An Integrated System provides a brief introduction (46 pages) tostudy skills. Topics include concentration, time scheduling, listening and lecture note taking, reading andlearning from textbooks, writing papers, and preparing for exams. The book contains a brief, clear

Page 21

explanation of the mechanisms of learning and memory.

Pauk, Walter. How to Study in College. Boston: Houghton Mifflin Company, 1984.How to Study in College is a book that covers a wide range of study skills, from improving memory toanswering specific types of exam questions. It is particularly strong in dealing with reading and note takingskills, not surprising considering that the author is a researcher in reading. The book is well organized witha thorough table of contents and index. Each chapter has a selftest to promote learning and remembering.Richardson, Frank C. Coping With Exam Anxiety. Editor. Arlene Young. Athabasca, Alberta:Athabasca University, 1990.

This book uses an informational learning approach to help students understand and reduce their examanxiety. The book will help students understand the extent to which their difficulty with exams is due topreparation or anxiety. For many students, reading the book and doing the exercises will be sufficient toreduce their anxiety. Others may also wish to seek the help of a counselor. Athabasca University Studentscan obtain the book, free of charge, from the Athabasca University Students Association (AUSA).

Page 22