exam 1 – acct 414 – spring 2008 - university of idaho · web viewexam 1 – acct 414 – spring...

TRANSCRIPT

Exam #__________

Name: __________________________________

Exam 1Acct 414 – Corporate Accounting & Reporting II

Spring 2010

Show any necessary computations if you want to be eligible for partial credit. Present your work in a neat, well-organized manner. When you are using a financial calculator, spell out what you put in for n, i, PMT, FV, PV, etc. You could also draw a time-line if that would explain your thinking to me. You may use abbreviations in your essay answers but I need complete thoughts.

Follow the instructions and answer all parts of the question as directed.

1-3. Time Value of Money (45 points total)

4. Loan Impairment (30 points total)

5. Leases (70 points total)

IFRS points______________ (item b)

US GAAP points____________ (items a, c, d & e)

6. Fair value & fair value option (25 points)

7. Serial Bonds (30 points)

Total points earned (max = 200)

To be completed by professor:After Exam 1 - Course GradeTotal Points = __________/__________ = _________%

Quiz and HW percentage = ___________%

Projects percentage = ___________%

Exam 1 – Acct 414 – Spring 2010 Page 2

[1] Sinking Fund. [15 points]Wegman Waterbeds, Inc. needs to accumulate $5,000,000 on December 31, 2018 to retire a bond. The company deposits $500,000 in a savings account on January 1, 2010 which will earn interest at 4% per annum but compounded quarterly. Wegman wants to know what additional amount it has to deposit at the end of each quarter for the 9 years to have $5,000,000 available at the end of 2018. The periodic deposits will earn interest at the same rate as the original deposit.

REQUIRED: What is the amount of the necessary deposit? $_____________________

[2]. Deferred Compensation [15 points]Your client, Monroe Mopeds, has agreed to pay $30,000 per year for five years to a retiring executive. The payments were in lieu of a year-end bonus which would have been taxed at a combined federal and state income tax rate of over 50%. The payments, which start four years from the end of the current year, have not yet been recorded in the accounting records. The company regularly borrows money at 8% per annum.

The company should record a liability in the amount of $____________________________

Exam 1 – Acct 414 – Spring 2010 Page 3

3. Lessor. [15 points]Assume that you are working for a leasing company. The boss asks you to compute the monthly lease payment that the company should charge to earn a 12% return on the following lease: Fair market value of leased asset $450,000. The first payment on lease will be made immediately upon signing and the second payment will be made at the end of the first month. The lease term is 4 years and the useful life of the asset is 6 years. At the end of the lease, the lessee must return the leased asset to the leasing company. The leasing company estimates that the asset will be worth $75,000 at the end of the lease term. [15 points]

REQUIRED: What is the monthly payment? $__________________________

Extra credit: Consider the facts in #3 above. The lessee wants an option to purchase the asset for $40,000 at the end of the lease. All other terms remain the same including the payment you computed above. If the lessor agrees to these terms, what will be the revised implicit interest rate?

______________% per year (please show with at least 2 decimal places). [5 points extra credit]

Exam 1 – Acct 414 – Spring 2010 Page 4

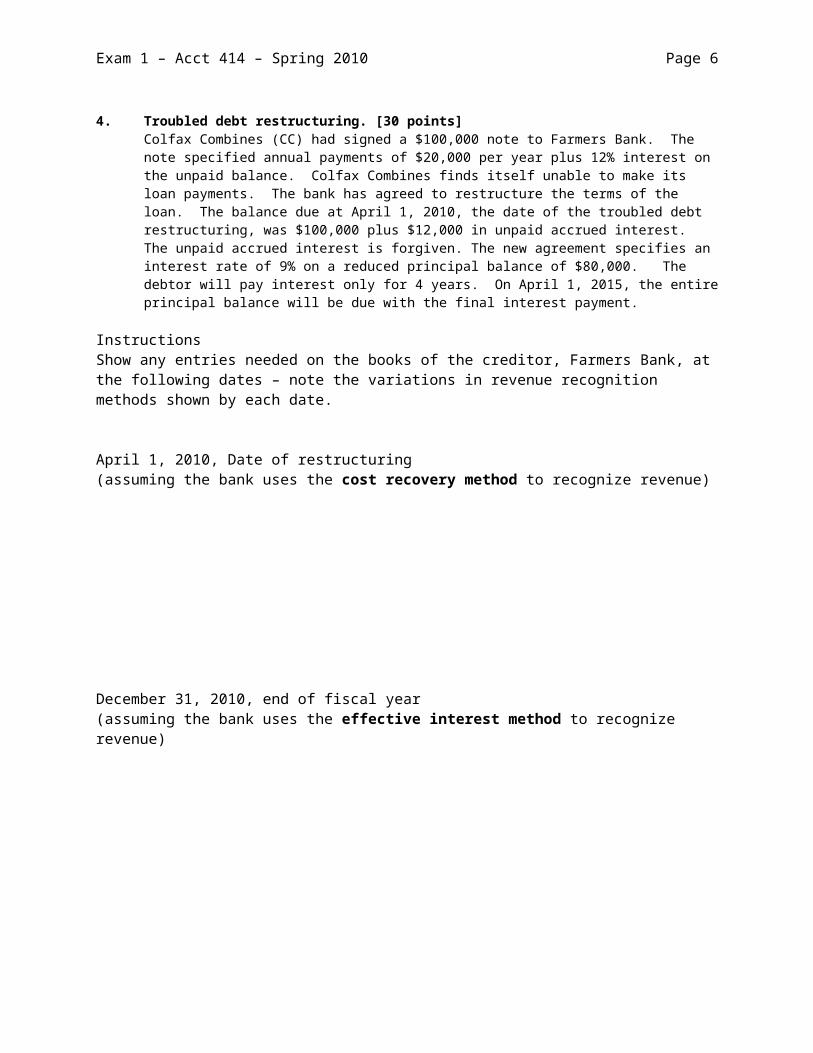

4. Troubled debt restructuring. [30 points]Colfax Combines (CC) had signed a $100,000 note to Farmers Bank. The note specified annual payments of $20,000 per year plus 12% interest on the unpaid balance. Colfax Combines finds itself unable to make its loan payments. The bank has agreed to restructure the terms of the loan. The balance due at April 1, 2010, the date of the troubled debt restructuring, was $100,000 plus $12,000 in unpaid accrued interest. The unpaid accrued interest is forgiven. The new agreement specifies an interest rate of 9% on a reduced principal balance of $80,000. The debtor will pay interest only for 4 years. On April 1, 2015, the entire principal balance will be due with the final interest payment.

InstructionsShow any entries needed on the books of the creditor, Farmers Bank, at the following dates – note the variations in revenue recognition methods shown by each date.

April 1, 2010, Date of restructuring (assuming the bank uses the cost recovery method to recognize revenue)

December 31, 2010, end of fiscal year(assuming the bank uses the effective interest method to recognize revenue)

December 31, 2010, end of fiscal year (assuming the bank uses the cost recovery method to recognize revenue)

Exam 1 – Acct 414 – Spring 2010 Page 5

5.Lease Accounting. On February 28, 2010, Joy Jewelers (lessee) and Franklin Fixtures Corp. (lessor) signed a lease with the following terms:

1. Term: 8 years 2. Annual payments of $32,093 3. Implicit interest rate (not known to lessee) 10% 4. There are no cost uncertainties for lessor. 5. Fair value of asset $200,000 6. Cost of asset $150,000 (not known to lessee) 7. Incremental borrowing rate: 12% 8. First payment due upon signing 9. Estimated useful life of asset: 12 years 10. The residual value is NOT guaranteed by lessee11. Est. fair value of asset at end of lease: $25,000. 12. At end of lease term, lessee can buy the asset for $25,00013. A commission of 1% of the fair value of the leased asset is

paid to the salesperson who negotiated the lease.14. Lessor and lessee both use straight-line depreciation for

fixed assets and have fiscal years that end on December 3115. Joy Jewelers is a start-up company so there may be

collectability problems for the lessor.16. Lessor retains ownership of asset at end of lease (unless

the purchase option (#12) is exercised.

a. Classify the lease under US GAAP for both the lessor and the lessee. Explain. Let me know that YOU know all the rules. Abbreviations are fine as long as they are obvious. You MUST find the present value and provide the inputs you used even if otherwise not necessary. [15 points]

LESSEE = ______________________________________

LESSOR = ______________________________________

b. Classify the lease under International Financial Reporting Standards (IFRS) for both the lessor and lessee. Discuss why the answer is different (or could be different) than it would be under US GAAP. [10 points]

Exam 1 – Acct 414 – Spring 2010 Page 6

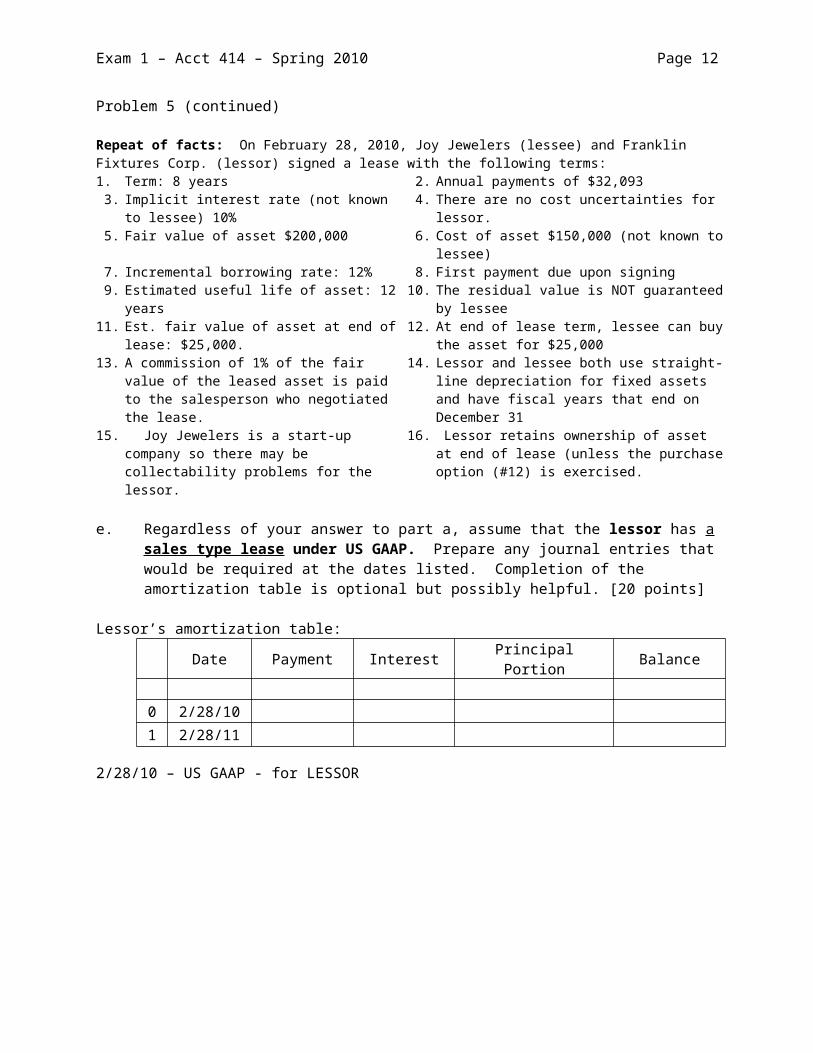

Problem 5 (continued)

Repeat of facts: On February 28, 2010, Joy Jewelers (lessee) and Franklin Fixtures Corp. (lessor) signed a lease with the following terms:1. Term: 8 years 2. Annual payments of $32,093 3. Implicit interest rate (not known to lessee) 10% 4. There are no cost uncertainties for lessor. 5. Fair value of asset $200,000 6. Cost of asset $150,000 (not known to lessee) 7. Incremental borrowing rate: 12% 8. First payment due upon signing 9. Estimated useful life of asset: 12 years 10. The residual value is NOT guaranteed by lessee11. Est. fair value of asset at end of lease: $25,000. 12. At end of lease term, lessee can buy the asset for $25,00013. A commission of 1% of the fair value of the leased asset is

paid to the salesperson who negotiated the lease.14. Lessor and lessee both use straight-line depreciation for

fixed assets and have fiscal years that end on December 3115. Joy Jewelers is a start-up company so there may be

collectability problems for the lessor.16. Lessor retains ownership of asset at end of lease (unless

the purchase option (#12) is exercised.

c. Regardless of your answer to part b, assume that Joy Jewelers (the lessee) follows US GAAP and classifies the lease as a capital lease. Prepare the appropriate amortization table for the first two payments (10 points).

Date Payment Interest Principal Portion Balance

0 2/28/101 2/28/11

d. Regardless of your answer to (b), assume that (under US GAAP) the lease is a capital lease for Joy Jewelers. Provide the necessary journal entries to record the transactions for Joy Jewelers (the lessee) at the indicated dates. (15 points)

2/28/10 –under US GAAP – LESSEE

12/31/10

Exam 1 – Acct 414 – Spring 2010 Page 7

Problem 5 (continued)

Repeat of facts: On February 28, 2010, Joy Jewelers (lessee) and Franklin Fixtures Corp. (lessor) signed a lease with the following terms:1. Term: 8 years 2. Annual payments of $32,093 3. Implicit interest rate (not known to lessee) 10% 4. There are no cost uncertainties for lessor. 5. Fair value of asset $200,000 6. Cost of asset $150,000 (not known to lessee) 7. Incremental borrowing rate: 12% 8. First payment due upon signing 9. Estimated useful life of asset: 12 years 10. The residual value is NOT guaranteed by lessee11. Est. fair value of asset at end of lease: $25,000. 12. At end of lease term, lessee can buy the asset for $25,00013. A commission of 1% of the fair value of the leased asset is

paid to the salesperson who negotiated the lease.14. Lessor and lessee both use straight-line depreciation for

fixed assets and have fiscal years that end on December 3115. Joy Jewelers is a start-up company so there may be

collectability problems for the lessor.16. Lessor retains ownership of asset at end of lease (unless

the purchase option (#12) is exercised.

e. Regardless of your answer to part a, assume that the lessor has a sales type lease under US GAAP. Prepare any journal entries that would be required at the dates listed. Completion of the amortization table is optional but possibly helpful. [20 points]

Lessor’s amortization table:Date Payment Interest Principal Portion Balance

0 2/28/101 2/28/11

2/28/10 – US GAAP - for LESSOR

12/31/10 (end of fiscal year)

Exam 1 – Acct 414 – Spring 2010 Page 8

6. Fair Value Option. [25 points]Lackey Inc. has one asset, a bond issued by Mercedes Company that Lackey Inc. purchased at face value as an investment (accounted for at fair value as trading security). Lackey Inc. has only one liability, a bond that was issued at face value to finance the purchase of the Mercedes Company bond. There is no initial shareholder investment. Neither bond is traded but bonds of similar risk characteristics are actively traded (market rates are provided below as of the end of the year).

Terms of the bondsMercedes Company Bond

Investment Lackey Inc. Bond PayableFace value 1,000,000 1,000,000Coupon rate (annual) 9% 7%Term (in years) 20 10Semiannual interest payment 45,000 35,000Market yield rate at year end for similar bonds (simple interest) 7.00% 8.00%

a. Prepare a balance sheet for Lackey Inc. at the END of the first year assuming Lackey selected the fair value option for the bond payable.

Assets Liabilities & Owners Equity

Cash Bonds payable

Bond Investment Owner’s equity

Total Total

b. Prepare a balance sheet for Lackey Inc. at the END of the first year assuming that the fair value option was not selected for the bond payable.

Assets Liabilities & Owners Equity

Cash Bonds payable

Bond Investment Owner’s equity

Total Total

5 point extra credit: What level of measurement is Lackey using to determine fair values? (circle one)Level 1 Level 2 Level 3 Level 4 Level 5Explain your selection (briefly):

Exam 1 – Acct 414 – Spring 2010 Page 9

7. Serial Bonds (30 points). On Nov. 1, 2009, Trains R Us Corporation issued $9,000,000 in serial bonds. The bond principal will be repaid in $3,000,000 increments beginning on Nov. 1, 2010 with the final payment to be made on Nov. 1, 2012. The bonds pay interest semi-annually on Nov. 1 and May 1. The coupon rate is 9% per annum. An investment banker handled the transaction and the company has just received a check for $9,161,500. The fiscal year of Trains R Us ends on December 31.

You may choose either the bonds outstanding method or the effective interest method of amortizing bond premiums. Check the appropriate box so I’ll know what you are attempting! Prepare all necessary journal entries on the dates listed.

I’m using the bonds outstanding method for a maximum of 30 points I’m using the effective interest method for a maximum of 28 points. If you choose this option, you may assume

that the interest rate per year is 8% per annum compounded semi-annually.

December 31, 2009 (NOT the date of issue)

May 1, 2010

Exam 1 – Acct 414 – Spring 2010 Page 10

SOLUTIONS

Problem 3 - Find the lease payment Problem 1 - accumlation Annual rate=n= 48 n= 36 4%i= 1% per month i= 1.00% pmts are quarterly

pv= (450,000.00) PMT=fv= 75,000.00 pv= 500,000

1 Face value = (5,000,000)

i=? 0 =payment 10,519.99 Solve for pmt $ 99,464.39 Extra credit answer - find implicit rate with BPO Problem 2 deferred compensation ( deferred annuity problem)Future value $ 40,000 n= 5 Step 1 find PV atpmt 10,519.99 i= 8.00% beginning of ord annNumber of payments 48 monthly PMT= (30,000)Future value (residual) pv= ? pv= $ (450,000) fv= -

ordinary=0; due=1 1 annual= 0 solve for implicit rate 0.786% 9.4370% Solve for PV 119,781.30 in four years so ord

PV=FV 119,781.30 ann begins 3 yrs fromNote that #2 was very similar to Problem 4-2 in HW #1 n= 3.00 msmt date

i= 8%PMT= 0.00

Solve for PV 95,086.26

ordinary annuity = 0; annuity due = 1 ordinary

annuity=0;annuity due=1

ordinary annuity=0;annuity due=1

Problem 4 journal entries:The creditor always finds the present value of the revised cash flows using the original interest rate (both US GAAP and IFRS). In this case: PMT=$80,000 * 9% (new rate) = 7,200; i=12% (original rate) FV=$80,000, n=5 and therefore PV of restructured debt is $71,348.54. Don’t forget to remove accrued interest (old balance * original rate). For the effective interest method, multiply new carrying value times original interest rate and prorate for partial year. In this case: $71,348 * 12% = 8,562 * 9/12 = 6,421.32. No cash changes hands until April 1, 2011. Under the cost recovery method, no entry is needed at 12/31/10 since we never accrue principal.

Farmers Bank Creditor journal entries Debit Credit4/1/2010 Restructured note receivable 71,348

Loss on loan impairment (or Allowance for bad debts) 40,652 Accrued interest receivable 12,000 Note receivable (old) 100,000

12/31/2010 Effective interest method:Interest receivable 6,421 Interest revenue 6,421

12/31/2010 Cost recovery method = no entry -

#5aFor the lessee, this is an operating lease. There is no title transfer or bargain purchase option and the lease term is only 67% of economic life. The present value of the minimum lease payments is $178,558 [n=8, i=12%, pmt=32,093 ,fv=0, type=begin] which is less than 90% of fair market value. Therefore, the lessee fails all 4 of the basic tests. Note that the lessee uses the incremental borrowing rate of 12% per US GAAP. An acceptable answer

Exam 1 – Acct 414 – Spring 2010 Page 11

would show the inputs used to compute the PVMLP and then the “essay” could be abbreviated something like this: No TT, No BPO, LT=67% < 75%, PVMLP=178,558 = 89% of FMV < 90%, Therefore operating since fails all 4 tests.

A few students said there was a bargain purchase option (untrue) and then failed to follow instructions to compute PVMLP anyways. Some of you included the $25,000 purchase option in the PVMLP which is incorrect because this is an unguaranteed residual value for both lessee and lessor. Recall that we always exclude unguaranteed residual values from PVMLP.

For lessor, it is an operating lease because there are collection uncertainties (but no cost uncertainties). Otherwise it would be a sales-type lease since it meets the 90% of FMV rule because the lessor always uses the implicit rate which was 10% in this problem and there is a profit (FMV > Cost). PVMLP = 188,335 [n=8, i=10%, pmt=32093,fv=0, type=begin] which is > 90% of FMV. If there were no collection uncertainties, it would be a sales type lease because there is a profit.

Some students included the residual value but you should NEVER include an unguaranteed residual value when doing the 90% of FMV test. Note that the lessor DOES include the residual value as part of the receivable (unless there is a TT or BPO) and you must include the residual value in computing the payment or implicit rate. We only leave it out for the 90% of FMV test).

#5b I asked whether your answer would (or could) be different under IFRS. For the facts presented, the lessee would have a finance lease which would be capitalized at $188,335 because the lessee would use the implicit rate (assuming it was practicable to determine). Reason: the PVMLP is fairly close to fair market value. The lessor would also have a finance lease for the same reasons as lessee because IFRS doesn’t have the extra collectability and cost uncertainty rules.

This is the type of lease that has a profit so a sale would be recorded at PVMLP and any initial direct costs would be expensed in the year the lease begins – just like accounting for a sales-type lease under US GAAP.

Some students provided more general answers. You could discuss the fact that IFRS does not have bright-line rules and therefore requires more judgment in classifying leases. You could have said that the leases are given different titles under IFRS but that the journal entries are basically the same (a finance lease instead of a capital lease for the lessee, etc.) You might also have recalled that there are FIVE basic guidelines and mentioned that a highly specialized asset might need to be capitalized even if it failed the other four rules. You also might have noted that IFRS doesn’t have the collectability and cost uncertainty “extra rules” for lessors. Finally, lessees would often use a different interest rate to compute PVMLP under IFRS by the lessee: the lessee uses the implicit rate unless it is not practical to figure it out.

#5c amortization table – uses 12% under US GAAP because implicit rate is not known. The lessee’s table always begins with the PVMLP unless that amount is greater than fair value (in which case we would start with fair value).

No BPO and RV is unguaranteed by LesseePV OF MLP: 178,557.64 INCEPTION DATE:INTEREST RATE: 12.000% ANNUAL LAST PMT:

Scroll right PAYMENT: 126,750.00 TERM IN YRS 8 for lessee IF FIRST PYMT DUE AT INCEPTION, 1, OTHERWISE 0

useful life = 12 % of useful life = 67%alternate formula for i Lease 12% Reduction in

9.9996% Date Payment Interest Lease178,557.64 Expense Obligation

To find i 02/28/10 (167,907.00) 0 02/28/10 32,093.00 0.00 32,093.00

32,093.00 1 02/28/11 32,093.00 #VALUE! #VALUE!

Exam 1 – Acct 414 – Spring 2010 Page 12

#5d – Lessee journal entries under US GAAP – assuming capital lease (which it is not)2/28/10 Leased asset 178,558

Lease obligation 146,465Cash 32,093

12/31/09 Depreciation expense 18,600(10/12)*(178,558/8)

Acc’d depreciation 18,600Interest expense (146,465 * .12 * 10/12) 14,647

Interest Payable 14,647Note that we use EIGHT years for depreciation since there is no BPO or TT: the asset will be returned to lessor at end of lease.

The entries in 2011 were not required:2/28/11 Lease obligation 14,517

Interest payable 14,647Interest expense 2,929

Cash 32,09312/31/11 Depreciation expense 22,320

Acc’d depreciation 22,320Interest expense 13,195

Lease obligation 13,195

#5e – Sales-Type Lease Journal Entries (table optional). Journal entries for a direct financing lease were not acceptable. If it were direct financing, the amortization table would start with FMV + initial direct costs and you’d need to solve for revised implicit rate. (Based on the facts of the problem, this was actually an operating lease because of collectability problems but you were clearly instructed to assume it was a sales-type lease.)

No BPO and RV is unguaranteed by Lessee 25,000.00 25,000.00 FMV of asset 200,000.00 INCEPTION DATE: 02/28/10 INTEREST RATE: 10.000% ANNUAL LAST PMT: 02/28/17 PAYMENT: 32,093.00 TERM IN YRS 8 IF FIRST PYMT DUE AT INCEPTION, 1, OTHERWISE 0 1

Initial direct cost if direct finacing lease $ - Lease Reduction LEASE

Date Payment Interest in lease Receivable200,000.00 10.00% receivable BALANCE

02/28/10 200,000.00 0 02/28/10 32,093.00 0.00 32,093.00 167,907.00 1 02/28/11 32,093.00 #VALUE! #VALUE! #VALUE!2 #VALUE! #VALUE! #VALUE! #VALUE! #VALUE!

You were clearly instructed to make journal entries for a SALES TYPE LEASE2/28/10 Lease receivable (from table) 167,907

Cash (given) 32,093Cost of goods sold (plug) 138,335

Sales (PVMLP) 188,335Inventory (given) 150,000

Selling expense 2,000Salaries payable (or cash) 2,000To recognize initial direct costs

12/31/10 Interest receivable 13,992Interest revenue (167,907 * 10% * 10/12) 13,992

Note: If I had asked for journal entries under IFRS, they would look exactly the same.

Exam 1 – Acct 414 – Spring 2010 Page 13

Problem 6 – Fair Value Option (FASB 159)a. Fair value option is adopted Bond payable at fair valueAssets Liabilities & Owners EquityCash 20,000 Bonds payable 936,704Bond Investment 1,208,411 Owner’s equity 291,707

Total 1,228,411 Total 1,228,411

b. Fair value option is NOT adopted Bond payable at face valueAssets Liabilities & Owners EquityCash 20,000 Bonds payable 1,000,000Bond Investment 1,208,411 Owner’s equity 228,411

Total 1,228,411 Total 1,228,411

Problem #6Supporting schedules for computations:Principal (FV) $ 1,000,000 $ 1,000,000 FVYield rate 3.50% 4.000% =iNumber of payments 38 18 =nPMT= 45,000 35,000 =PVordinary=0; due=1 0 0 Solve for PV $1,208,410.87 $936,703.52 =fair value

Beginning cash balance 0Interest revenue 90,000Interest expense -70,000Ending cash 20,000

Income statements a. Fair value option b. Fair value option(no required) ADOPTED NOT adoptedInterest revenue 90,000 90,000Interest expense -70,000 -70,000Gain/loss on bond investment 208,411 208,411Gain/loss on bond payable 63,296 0Net income 291,707 228,411

Extra Credit – the measurement of the fair value of the bonds is LEVEL 2 because it uses market inputs for similar assets. It could only be Level 1 if these particular bonds were actively traded.

#7 Serial bonds. To do bonds outstanding method, just count up the face values outstanding: 9M + 9M +6M + 6M + 3M + 3M = $36 million total (each one is doubled because the bonds are semiannual and the principal payments are annual). So the discount/premium will be amortized with the 9/36 (25%) fraction for the first 2 interest payments. Since this bond was issued at a premium, the amortization of the premium DECREASES interest expense (as compared to interest paid). To use the effective interest rate, you need to know what it is – the 8% given. I’ve pasted in complete answers for study purposes but the amortization tables are NOT necessary.

Note that I did NOT ask for the journal entry when the company received the $9,161,500 in proceeds.

Exam 1 – Acct 414 – Spring 2010 Page 14

Annual7.999% Exam 1 - Spring 2010

EFFECTIVE INTEREST AMORTIZATION SCHEDULE Bonds Outstanding MethodFace Value: 9,000,000 4.50%

Amorti- Carrying BALANCE FACE Cash Flows Period Date Interest Principal Interest Amorti-zation Value PREMIUM VALUE Paid Payment Expense zation

0 9,161,500 161,500 9,000,000 (9,161,500) 0 11/01/09 - - - (53,075) 9,214,575 214,575 9,000,000 405,000 1 05/01/10 405,000 - 364,625 40,375 (55,729) 6,270,304 270,304 6,000,000 3,405,000 2 11/01/10 405,000 3,000,000 364,625 40,375 (43,515) 6,313,819 313,819 6,000,000 270,000 3 #VALUE! 270,000 - 243,083 26,917 (45,691) 3,359,510 359,510 3,000,000 3,270,000 4 #VALUE! 270,000 3,000,000 243,083 26,917 (32,975) 3,392,485 392,485 3,000,000 135,000 5 #VALUE! 135,000 - 121,542 13,458

Total 36,000,000Journal entries: Bonds Outstanding Method

Debit Credit11/01/09 Cash This entry was NOT requested 9,161,500

Premium on Bonds Payable 161,500 Bonds Payable 9,000,000

2 mo12/31/09 Interest Expense plug 121,542

Premium on Bonds Payable 13,458 161,500 discount * 9/36 * 2/6

Interest payable $9M * 4.5% * 2/6 135,000

5/1/2010 Interest Expense plug 243,083 Premium on Bonds Payable 26,917

161,500 discount * 9/36 * 4/6Interest payable Reverse 12/31 entry 135,000 Cash $9M * 4.5% 405,000

9,701,500 9,701,500

Alternate answer for #7PROCEEDS FROM BOND ISSUE 9,161,500 formula - actualYIELD PER ANUM 8.00% 8.00%NUMBER OF INTEREST PAYMENTS IN A YEAR 2 If invester, enter 1, otherwise 0 0

Exam 1 - Spring 2010 EFFECTIVE INTEREST AMORTIZATION SCHEDULE

4.50% 4.000% Face Value: 9,000,000 Period Date Interest Principal Interest Amorti- Carrying BALANCE FACE

Paid Payment Expense zation Value PREMIUM VALUEJournal entries: Effective Interest Method

Debit Credit2 mo

12/31/09 Interest Expense 122,141 $9,161,500 * 4% * 2/6

Premium on Bonds Payable plug 12,859 Interest payable $9M * 4.5% * 2/6 135,000

5/1/2010 Interest Expense 4 mo 244,283 $9,161,500 * 4% * 4/6

Premium on Bonds Payable plug 25,717 Interest payable Reverse 12/31 amount 135,000 Cash $9M * 4.5% 405,000

9,701,500 9,701,500