evaluating the conservative and labour party manifestos · consequently, each of the party...

TRANSCRIPT

EVALUATING THE CONSERVATIVE AND LABOUR PARTY MANIFESTOS

Professor Graeme Leach Chief Economist, Macronomics

Professor Patrick Minford Professor of Applied Economics, Cardiff University

November 2019

Within a fortnight, there will be a new government.

If the Tories win with a working majority, it can be expected that the pending deal with the EU will

be passed quickly in Parliament and signed off by the EU. The Tory manifesto - like Labour - commits

them to higher spending on infrastructure, to be financed by higher borrowing, but on a smaller

scale: an extra £25 billion a year as against as much as £200 billion. But they would do so under the

full Brexit on which they have campaigned. This would simultaneously push the economy to free

trade, lower prices and more competition/productivity; accompanied by moves toward more pro-

business/pro-innovation regulation; and a new immigration policy based on importing skills. This

opens up the possibilities of a new supply-side reform process, similar to the Thatcher revolution.

In contrast, if Labour wins, the UK effectively will stay in the EU due to Labour’s referendum offering

essentially two flavours of Remain. Ironically, it might find its programme of nationalisation via

confiscation of shares and other property under pressure from EU law. In effect it would be left as

just a very high-spending, very high-taxing, very high-borrowing government – on a different plateau

to that of the Conservatives.

This paper assesses the two Party Manifestos from a macroeconomic perspective – both

qualitatively and projecting quantitatively what impact these manifesto policies might have on the

economy. The reader will observe, because of the relative financial conservatism of the

Conservative Manifesto, inevitably most of our comments are directed toward the Labour

Manifesto.

In addition, we argue that a burst of fiscal expansion is now needed in order to push interest rates

well away from the Zero Lower Bound. Normalised interest rates will enable monetary policy to

become effective again so that financial markets cease to be so badly distorted by the Zero Lower

Bound and massive money-printing. We believe a new Conservative Government could well go

further in pursuing this.

There are three sections to this paper:

I. A qualitative macroeconomic assessment of the Labour and Conservative Manifestos

II. Macroeconomic projections of the following scenarios:

The Post-Brexit Base Line that assumes no change in policy from where we are now, other than delivering the EU Deal on Brexit, and then moving to free trade agreements with both the EU and the rest of the world

The Conservative Manifesto with effects essentially identical to the Post-Brexit Baseline

The Labour Manifesto that could likely create a financial crisis

2

A Brexit Supply-Side Reform Policy that could enable additional spending/tax cuts and higher growth while reducing the debt-to-GDP ratio to manageable levels

III. Concluding Remarks

ECONOMIC ASSESSMENT OF THE MANIFESTOS

It has been widely noted that the Conservative Manifesto, while breaking free of ‘austerity’ and expanding spending/borrowing more than normal for the Tories, represents only a pale imitation of that proposed by Labour. Indeed, the moniker, ‘timid’ has been used. There is no significant expansion of the State or regulatory intrusion found in the Conservative Manifesto. All of the radical ‘innovation’ is to be found in the Labour Manifesto. Therefore, this section of the paper will concentrate on proposals of the Labour Manifesto commenting only where applicable on the Conservative Manifesto. Labour’s economic manifesto has been widely and sharply criticised, in some cases by traditional allies of the Labour Party. The Financial Times was scathing in its criticism: “Jeremy Corbyn’s hard left programme will wreck the UK economy. The combination of punitive tax increases, sweeping nationalisation and the end of Thatcher-era union reforms turns the clock back 40 years. Set alongside a vast expansion of the state … Labour’s plans are a recipe for terminal economic decline”. Yet only a few days after this was written, 163 economists and other academics wrote to the Financial Times arguing that Labour’s proposals for higher investment would kick start growth and raise productivity. Such views are driven by demand-side economic models of the economy or demand side models where a weak supply side based on arbitrary rules is employed (eg, OBR). In such models more current and capital expenditure increases overall spending and GDP. The bottom line in such models is that more spending under Labour means more growth. They might also show that higher infrastructure investment would have a positive supply-side benefit boosting productivity. There can be no doubt that the main aim and focus of the Labour Party Manifesto is the demand-side of the economy and higher spending as summarised below. As we will see, the Manifesto ignores negative supply-side consequences. The analytical problem is quantifying all these effects; such is the breadth and depth of Labour’s Manifesto proposals ranging across spending, taxation and regulatory intervention.

Spending Resource and Capital Spending. The Labour economic manifesto document, Funding Real Change, sets out the proposed £83 billion increase in resource spending – day to day expenditure – by 2023-24. On top of this it is proposed that capital expenditure be increased by £55 billion per annum (£30 billion per annum for a Social Transformation Fund and £25 billion per annum for a Green Transformation Fund). The £138 billion per annum increase in proposed annual spending was subsequently increased further with a £58 billion pledge to compensate women affected by the increase in the state pension age. This equates to just under £12 billion per annum over 5 years. Consequently, Labour is committed to a total increase in public spending of £150 billion per annum.

3

This is double the total increase in public spending proposed in its 2017 General Election manifesto - seen as profligate at the time. The 2019 Manifesto doubles down in an unprecedented manner. Nationalisation. Labour’s sweeping proposals for the privatisation of mail, part of BT and the energy utilities could cost a further £196 billion according to the CBI. Over the course of a 5-year Parliament this equates to almost £40 billion per annum. The Shadow Chancellor ignores this cost by arguing that Parliament, not financial markets, will determine the value of these companies. But this is easier said than done. The proposed expropriation of property rights risks alarming financial markets. Seizing control of private companies breaks the number one assurance required by investors, that property rights are inviolable. And, the proposal for local councils to take over public bus routes must be added to this. The Shadow Chancellor also tries to dismiss the costs of nationalisation by arguing that the public sector will acquire an asset – leaving its net worth unchanged – and that any borrowing costs will be serviced by profits from the nationalised company. This of course assumes that such companies would be able to make profits, when interfered with by meddling politicians with little concern for the bottom line. The Shadow Chancellor promises he will reset the fiscal rules so that borrowing for investment falls outside borrowing targets, but he cannot change the rules to stop the reality that borrowing is borrowing, targeted or not. Knock-On Effects. There is a further addition to public spending that is almost assured. This is the addition to spending arising from the fact that

The economy is already close to full-employment and massively higher public spending alongside a tight labour market could lead to acceleration in wage growth. Such acceleration would likely become most apparent in the construction sector as a result of massive infrastructure spending. The end result would be even more spending in order to maintain real inflation adjusted levels of output.

Implementation of many of Labour’s labour market proposals, such as reduction in the working week to 32 hours, will add directly to public spending when applied across the state sector

Any government ideologically inclined to more fiscal largesse is likely to be poor at ‘looking after the pennies’, and so spending is likely to increase even further above Labour manifesto estimates. Marginal additional incremental expenditure across all Government departments could add up to billions given that total managed expenditure (TME) under existing Conservative plans is projected to reach £955 billion by 2023-24.

Thus, it is a reasonable assumption that un-costed expenditure under Labour from inflation,

implementation and incrementalism – across 25 Ministerial departments - will amount to at least

£10 billion per annum, around 0.5 percent of GDP. Adding in the costs of nationalisation and this

additional expenditure brings the average annual increase in total public spending to £200 billion

(£150 billion plus £40 billion and £10 billion). Any UK government attempting to increase spending

by £150 to £200 billion per annum exposes the economy to extreme risk.

During the post war period total public spending peaked at 46.4 percent of GDP in 1975-76, but only briefly, falling under the Labour Government to 41.5 percent of GDP in 1978-79 before the Conservatives came to power. What is now proposed by Labour is to raise public spending, as a proportion of GDP, back to its highest ever level in our peacetime history. Depending on the precise

4

measure chosen Labour proposes – as described above - to increase spending by between 6 percent (£150 billion per annum) and 8 percent plus (£200 billion per annum) of GDP. Comparing Party Spending Figures. The Labour spending figures above are based on the absolute amounts cited in the Labour Manifesto costing. The current and capital expenditure projections are based on the absolute increase in public spending and taxation by 2023-24 as promised in the Manifesto. To that total the cost of WASPI compensation, estimated incremental additions to spending and the potential costs from nationalisation have been added. In order to compare fiscal policies across each of the leading parties the same baseline needs to be employed. The Conservatives are proposing an extra £3 billion per annum in current day-to-day spending in their Manifesto, and this figure is actually over and above existing policy commitments - eg, the already announced increases in NHS spending. The Conservative March 2019 Spring Statement increased real current spending by £18 billion per annum by 2023-24. The 2019 Spending Round added a further £16 billion to annual current spend by 2023-24. Consequently, each of the party manifestos needs to be estimated on the basis of the increase in spend over and above the £34 billion already committed to by the Government. The IFS1 has undertaken this analysis and it shows that Labour increases current annual spending by £73 billion per annum over and above the existing £34 billion baseline, the Liberal Democrats increases it by £33 billion and the Conservatives by £3 billion. However, the IFS total excludes the costs of WASPI compensation, and it also excludes the potential additional costs cited above by the author. So, the day-to-day spending gap between the parties is actually much wider. The Conservatives also propose to raise public investment by £20 billion per annum in contrast to Labour’s proposed £55 billion per annum increase. The Conservatives have pursued a policy of safety first with regard to their own Manifesto. They’ve addressed the austerity charge with pre-manifesto commitments on spending - particularly on the NHS – and distanced themselves from Labour with a day-to-day spending increase of just £3 billion in their Manifesto. Whilst this might be good politics, there is surely an issue in the remarkable shift in Conservative policy towards accepting that more spending is good for the economy, as long as it’s much less than under Labour. Nobody is making the case for a smaller state. The Conservative Manifesto postponed previously announced Corporation Tax cuts in spite of Corporation Tax revenue increasing since 2010 even while the headline rate was reduced. Part of the explanation must be the supply-side stimulus from lower rates. However, whilst this has occurred, the Government has also found ways to increase Corporation Tax revenues by reducing so-called tax expenditures such as the reduction in capital allowances, restricting the use of past losses and a raft of anti-avoidance measures. Labour proposes to take these measures even further with a review of tax allowances and expenditures. More widely, it is surprising that a Conservative Government has poured so much more money into the NHS, but has asked for nothing in return in terms of structural reform to a state monopoly, to make the service more efficient. The danger with the Conservative’s acceptance of the idea that 1 https://www.ifs.org.uk/uploads/IFS-General-election-analysis-2019-Christine-Farquharson-Spending-on-public-services.pdf

5

there is no political problem more money can’t solve is that such thoughts have to be paid for. The electorate yet again is being bribed with its own money. Responding to the Conservative Manifesto, the IFS questioned whether the Conservatives could avoid future tax increases if their spending commitments were to be met. These estimates of increased spending as a proportion of GDP are based on the assumption of continued economic growth. If there was to be a sharp future downturn or recession, then so-called automatic stabilisers – such as unemployment and welfare benefits – would kick-in and public expenditure would rise even more. Recessions easily can add 4-5 percent of GDP in public spending. This economic impact of this incremental spending added to the spending increases outlined above could be devastating - a very real prospect. Thus, a recession under a Labour Government, alongside unchanged Manifesto commitments, could see public spending rise to 50 percent or more of GDP. The supply-side consequences of this shift in economic resources from a higher productivity growth private sector to a lower productivity growth public sector would results in lower overall GDP growth simply because one sector is more productive than the other.

Taxation Labour proposes major changes to the tax system in order to increase revenues by £83 billion. Among the proposed changes:

Corporation Tax rates will be raised to 26 percent by 2023.

1.6 million people with taxable income of more than £80,000 per annum will pay a new 45 percent rate of Income Tax.

Those having taxable income of more than £125,000 will pay a new top rate of 50 percent.

The Capital Gains Tax regime will be reorganised to equalise rates with Income Tax.

A new Financial Transactions Tax will be introduced.

Corporate tax allowances will be reviewed, which is code for removed or reduced. Those affected by the Income Tax rises already pay around half of all Income Tax. There is a significant risk that there will be significant behavioural changes by such taxpayers because of the reduced incentives to work. This might result in fewer hours worked or an earlier move into retirement. Whilst the behavioural response is unknowable in advance, the IFS2 has acknowledged that, “the taxable incomes of individuals at the very top of the income distribution are relatively responsive to income tax changes”. Behavioural responses will not be confined to individuals. Companies will adjust as well. The proposed increase in the rate of Corporation Tax, will, according to the IFS, result in the UK raising more in Corporation Tax, as a proportion of GDP, than any other G7 economy. This could lead to divestment from the UK and FDI outflows rather than inflows, and other actions that could reduce the expected £20 billion in revenues.

2 Labour’s proposed income tax rises for high income individuals, IFS Briefing Note BN265, S. Adam, R. Joyce and X. Xu.

6

Consequently, it is highly likely that the proposed tax changes will reduce the size of the tax base on which Income, Corporation and Capital Gains Tax can be levied. This will result in tax revenues below those projected leaving the Chancellor with difficult choices:

Increase public sector net borrowing even more, remembering that the proposed spending

increase already vastly exceeds the projected £83 billion increase in revenues

Raise rates of taxation even higher, with all the associated negative effects on incentives to work, save and invest

Curtail spending plans. It seems quite likely that the Chancellor would ignore this option.

Because Labour’s proposed tax increases are likely to induce behavioural changes on a scale not seen before, they are not captured by existing economic models. Thus, over the past decade, a new approach - known as narrative identification - has been developed to analyse the impact of fiscal policy. It is used to assess exogenous tax changes – ie, those tax changes aimed at either improving long term growth (via tax cuts) or reducing a deficit (tax hikes). Developed by Romer and Romer, two Democrat supporting economists in the US, it has yielded dramatic results. Romer and Romer estimate that in response to an increase in tax liabilities of 1 percent of GDP in the US, output 10 quarters later is still 3 percent below the level it would have been had no shift in taxation occurred. This is a very large decline and a very large tax multiplier. More general rules of thumb, based on widespread econometric modelling across the advanced economies, suggests that a 10 percent of GDP increase in the tax burden, reduces GDP growth by between 0.5 and 1.0 percentage points. These results are consistent with other findings that the output losses from deficit reduction based on tax increases are much greater than for spending cuts. These are all different ways of saying that there are very significant supply-side consequences to Labour’s proposed tax hikes. And this would occur with the proposed £83 billion tax increase. Imagine how much worse the problem would become if the tax take has to be raised even more to close the gap between a £200 billion increase in spending and the proposed extra £83 billion in revenue.

Regulatory Intervention The total economic impact of a Labour Government would not be confined to tax and spend alone. Any assessment of the total scale of intervention has to include regulatory changes, as well as other interventions. The Labour Manifesto proposes a host of regulatory and other interventions that are difficult to quantify in total but are likely to have significant detrimental economic effects. These proposed interventions include:

Progressive introduction of a 32-hour working week.

Reversal of trade union law reforms in the 1980s.

Compulsory transfer of 10 percent of equity to workers.

Raising the Minimum Wage to £10 per hour.

Freezing the State Pension Age.

Ending zero-hours contracts.

Extended maternity and paternity leave.

Introduction of rent controls.

7

Many of these proposals wouldn’t just increase costs in the private sector, there would be significant extra cost for the public sector as well. But the main effect would be to undermine productivity and potential output growth. In other words, they would introduce severe damage to the supply-side of the economy. Nevertheless, it remains the case that the difference between Labour and Conservative Manifesto plans is night and day. The Conservative Manifesto won’t unleash the supply-side of the economy, but the Labour manifesto could crush it. In the next section of the paper, we provide a quantitative macroeconomic assessment of the Manifestos by comparing post-election economic projections of the Manifesto policies.

PROJECTING POST-ELECTION ECONOMIC SCENARIOS This section assesses the macroeconomic implications of the Manifesto Policies by comparing economic projections resulting from the respective Manifesto policies relative to a Post-Brexit Baseline projection, which assumes no change in Government policy from where we are now, other than delivering the EU Deal on Brexit, and then moving to free trade agreements with both the EU and the rest of the world. The long-proven and empirically verified Cardiff Models are employed to do this. For background on these models, see Appendix A. In addition to projecting the usual economic parameters, the projections also calculate the required future tax increases that might be required in order to sustain the policies. This will act as a key constraint on what the government can afford to do. Based on this analysis, we conclude the following:

The cautious policies of the Conservative Manifesto result in an economic outcome that is essentially identical to the Post-Brexit Baseline thereby creating no financial risk but equally not capitalising on available opportunities

The radical policies of the Labour Manifesto create a financial crisis

A Brexit Supply-Side Reform Policy would enable additional spending/tax cuts relative to the Baseline scenario while reducing the debt-to-GDP ratio to approximately 60 per cent by 2027 and increasing GDP growth by one percentage point

The above are evaluated relative to the Post-Brexit Baseline (see Appendix B). See Charts 1–5 for

the projected trends in GDP growth, unemployment, exchange rate, inflation, and interest rates for

these scenarios.

Projecting the Effects of The Conservative Manifesto

The Conservatives have hewn to the latest fiscal rules, in which the current budget should be in

surplus in the near future, while extra money may be borrowed to pay for capital investment. Given

their priority on enhancing various spending flows, notably on the NHS, they have cancelled the

8

planned cut in Corporation Tax to 17% to pay for these under the current budget. The only tax cut

they have put forward is a rise in the NI contribution threshold by workers.

When one adds up all these changes, the Conservatives would spend approximately an extra £25

billion a year, borrowing to finance the £20 billion of capital spending in this. The rest involves a net

rise in taxes. If we assess the supply-side effect of infrastructure spending on a par with that of

taxcuts to the same value (as we believe is reasonable) then the programme raises growth by 0.2%

per annum over the Post-Brexit Base Line.

Because fiscal expansion is so limited, interest rates continue much as in the Baseline, rising slowly

to around 3% by the mid-2020s (see Appendix C). The PSBR projection is small and turns negative in

the late-2020s.

Summary Table for the Conservative Manifesto

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

GDP Growth1 1.4 1.5 2.2 2.5 2.1 2.1 2.2 2.2 2.2 2.3 2.3 2.3 2.3

Inflation CPI 2.5 2.0 2.1 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0

Wage Growth 3.1 3.7 3.0 3.2 3.3 3.2 3.2 3.3 3.3 3.3 3.4 3.3 3.2

Unemployment (Mill.)2 0.9 0.9 0.8 0.7 0.7 0.6 0.6 0.6 0.6 0.6 0.6 0.6 0.6

Exchange Rate3 78.6 80.2 80.6 80.6 80.6 80.4 80.2 80.0 79.9 79.8 79.7 79.6 79.5

3 Month Interest Rate 0.7 0.9 1.1 1.8 2.5 3.2 3.1 2.6 2.3 2.1 2.1 2.1 2.1

5 Year Interest Rate 1.0 1.0 1.3 2.4 3.3 3.4 3.3 2.6 2.4 2.2 2.0 2.0 2.0

Current Balance (£bn) -81.3 -86.6 -41.3 -31.3 -23.2 -14.9 -11.8 -11.1 -14.3 -9.2 -5.8 0.1 3.1

PSBR (£bn) 40.8 37.6 30.0 16.4 12.4 9.0 5.0 2.2 -9.9 -25.7 -38.9 -53.0 -67.3

1 Expenditure estimate at factor cost 2U.K. Wholly unemployed excluding school leavers (new basis) 3Sterling effective exchange rate, Bank of England Index (2005 = 100)

Listed below are the values of key parameters as of 2027:

2027 PV of Debt (relative to the Post-Brexit Base Case): No Change

2027 Nominal GDP (relative to the Post-Brexit Base Case): 17% greater

2027 PV Debt/2027 Nominal GDP ratio: 63%

2027 PV of future steady-state tax revenues : 40% of GDP

2027 PV of future steady-state spending including debt interest : 40% of GDP The Fiscal Gap = 40% - 40% = 0% of GDP. Thus, no new tax rises are required.

9

Fiscal Projection for the Conservative Manifesto

PSBR Debt GDP (Mkt Price)

Debt/GDP %

2018 41.4 1559 2127 73.3

2019 37.4 1716 2215 77.5

2020 30 1746 2310 75.6

2021 16 1762 2401 73.4

2022 12 1774 2506 70.7

2023 9 1783 2614 65.4

2024 5 1788 2726 65.6

2025 2 1790 2842 63.0

2026 -10 1780 2963 60.1

2027 -45 1936 3092 62.6

What we see from these projections is that they leave the Baseline largely unchanged in terms of

fiscal outcomes.

Projecting the Effects of the Labour Manifesto Having described above the impact of Labour’s public spending, taxation and other interventions, we now examine how these policies are likely to play out in terms of their impact on the economic cycle. The standard Keynesian textbook model of the impact of increased public spending on the economy would quickly be undermined as other factors offset any stimulus to GDP growth from public spending. If the public sector increases its borrowing, this money has to come from somewhere and this diversion will reduce the spending power of other sectors in the economy. Because financial markets are not expecting a Labour Government to come to power, a sharp reversal in financial markets is likely to occur. The impetus for this would be fears over the potential size of the budget deficit, future public debt levels and the potential damage to the supply-side of the economy from tax and regulatory changes. Nationalisation and the increase in trade union power - from reversing 1980s reforms - would add to the air of economic crisis. There could be a significant exodus of capital from the UK and a flight to safety overseas. FDI inflows into the UK could dry up, equity markets could fall sharply, a sterling crisis could deepen, and gilt yields could spike. Simultaneous with this could be a sharp increase in precautionary saving by households and companies, with a reduction in consumption and investment. Individuals and businesses could see the surge in spending as a portent of future tax increases and adjust their levels of savings upwards in advance. A shift towards precautionary behaviour by households could be intensified by negative

10

wealth effects from falling equity and house prices as well. An already weak economy could fall into recession. Business caution would be made worse by the continued uncertainty surrounding Brexit as a result of attempts at renegotiation with EU and a second referendum. Unfortunately, this would only be the beginning not the end of the economic difficulties. Negative supply-side effects would begin to kick-in, further undermining growth as the public sector displaced and crowded out the more productive private sector. An exploding deficit would emerge at a time when the economy was becoming less and less able to finance it. The end result would be an economic implosion with soaring unemployment and budget deficits and sustained economic collapse until the advancement of the state was reversed. While econoimic modelling canot quantify all aspects of the Labour Manifesto (eg, the impact of requiring companies to give 10 per cent of their shares to employees), the projections below are consistent with the above comments. The projection suggests that the negative impact of the Labour Manifesto on GDP could result in greater output losses than was experienced during the financial crisis. It might be asked, why - given the benign projections of the Conservative Manifesto when they have increased spending and borrowing significantly – should Labour’s Manifesto policies produce such worse results? If the post-Labour economy were to remain robust and continue to grow as projected under the

Labour programme, then the mere fact of it borrowing large amounts could potentially be absorbed

safely. The difficulties with the Labour programme come from two damaging elements :

The first and most problematic is that the Labour’s Manifesto policies’ are highly damaging to growth, via effects on the economy’s supply side. Labour has said it will raise income tax rates on ‘the rich’ ; these will damage growth for just the same reasons we argue that investment plus tax cuts raise growth. In fact, these higher rate tax rates raise little, if any, money; so that income tax rates (or similar taxes on consumption) will need to rise.

Second, Labour has suggested it will not pay full market value to the shareholders and landlords whose property it nationalises. Such a wealth tax would undermine the confidence of investors and act like other taxes in lowering growth.

In addition, Labour would negotiate effectively not to have a Brexit - neither with its proposed deal

to stay in the EU in all but name nor with its referendum alternative of straight Remain. This would

imply a supply-side hit to the economy relative to our Post-Brexit Base Case projection. This is

without counting the effects of more prolonged uncertainty on the economy.

Then, there is the proposal for a four day week, which again will reduce output by about a fifth (the

equivalent of a 20% tax on employment) unless the government pays workers an over-time subsidy,

requiring yet more income taxes.

On top of it all, Labour proposes to bring back the union laws abolished by Mrs Thatcher, returning

our industrial relations to 1970s chaos. However, in our modeling, we have not included the effects

of this, which on its own would cause massive supply-side damage.

There is much else in the fine print of Labour’s programme that plans openly to replace the

‘capitalist’ economy we have with one of overwhelming state ownership and direction. This explicit

11

model of state planning has been widely experimented with in other countries : Russia, Cuba,

Venezuela are three prominent examples. The results have been uniformly disastrous.

So Labour’s programme threatens growth directly. That is its fundamental flaw. As for its borrowing

plans, it appears to plan to borrow massively for an infrastructure programme of about £100 billion

a year, about £55 billion above the Post-Brexit Baseline. Cumulatively by 2027, this would come to

an extra £440 billion on the Baseline. On non-infrastructure spending it plans to borrow to fund the

extra tax rises just mentioned, with their consequential damage to growth.

Thus, the Labour programme’s effect on growth also seriously undermines projected ongoing tax

revenue, causing a need for yet more new taxes, which must undermine confidence in its ability to

remain solvent.

The siver lining in the cloud is that, in the short run, it is likely to remove the Zero Lower Bound issue

rapidly. However, Sterling would collapse, sending inflation up sharply and causing a large outflow

from the gilts market, with fears of future UK government insolvency from the fall in future

revenues. Long term and short term interest rates would rise sharply. However, monetary policy

would be unable to stimulate the economy by lowering rates because of the effects on inflation. So

this would be an expensive ‘cure’ of the Zero Lower Bound problem, ushering in a monetary policy

as fettered as before, but in a different way.

The table below summarises the projection (see Appendix D). Note that for this projection, we make

the most favourable possible assumptions about the manifesto commitments; namely, that the

taxes Labour proposes to raise (the ‘basic top’income tax rate from 40 to 45% ; and the corporation

tax rate from 19% to 26%) are sufficient in their yield to fund its non-infrastructure commitments to

spend more (£80 billion per yea)r. This assumption coud easily turn out not be valid.

Summary Table for the Labour Manifesto

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

GDP Growth1 1.4 1.5 -0.2 -0.2 -0.1 0.0 -0.1 -0.2 0.0 -0.2 0.2 0.1 0.1

Inflation CPI 2.5 1.9 4.9 5.2 5.2 4.8 5.1 4.9 4.9 4.8 4.7 4.7 4.7

Wage Growth 3.1 3.6 3.8 5.8 6.3 6.0 6.3 6.1 6.2 6.1 6.0 6.1 6.0

Unemployment (Mill.)2 0.9 1.0 1.0 1.3 1.5 1.9 2.3 2.8 3.4 4.1 5.1 6.2 7.5

Exchange Rate3 78.6 80.1 69.6 66.8 64.5 62.5 60.4 58.6 57.0 55.5 54.0 52.7 51.4

3 Month Interest Rate 0.7 0.9 4.9 5.2 4.6 4.8 4.7 4.7 4.7 4.9 4.9 4.9 4.9

5 Year Interest Rate 1.0 1.0 5.0 5.0 5.1 4.9 4.9 4.7 4.8 4.8 4.8 4.8 4.8

Current Balance (£bn) -81.3 -86.6 -12.2 -1.1 4.1 8.9 12.0 14.7 12.8 19.4 23.6 27.8 31.6

PSBR (£bn) 40.8 47.4 59.5 70.5 92.8 121.7 154.5 199.2 234.0 275.9 319.3 369.5 424.8

1 Expenditure estimate at factor cost 2U.K. Wholly unemployed excluding school leavers (new basis) 3Sterling effective exchange rate, Bank of England Index (2005 = 100)

12

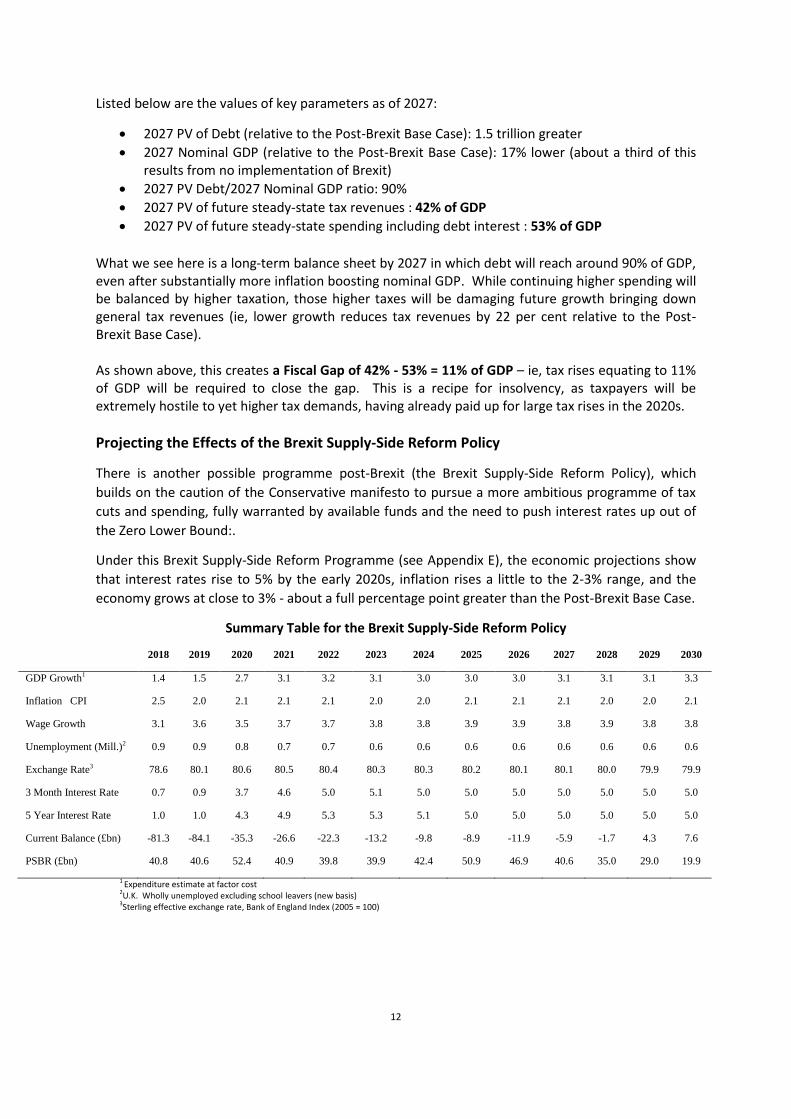

Listed below are the values of key parameters as of 2027:

2027 PV of Debt (relative to the Post-Brexit Base Case): 1.5 trillion greater

2027 Nominal GDP (relative to the Post-Brexit Base Case): 17% lower (about a third of this results from no implementation of Brexit)

2027 PV Debt/2027 Nominal GDP ratio: 90%

2027 PV of future steady-state tax revenues : 42% of GDP

2027 PV of future steady-state spending including debt interest : 53% of GDP

What we see here is a long-term balance sheet by 2027 in which debt will reach around 90% of GDP, even after substantially more inflation boosting nominal GDP. While continuing higher spending will be balanced by higher taxation, those higher taxes will be damaging future growth bringing down general tax revenues (ie, lower growth reduces tax revenues by 22 per cent relative to the Post-Brexit Base Case). As shown above, this creates a Fiscal Gap of 42% - 53% = 11% of GDP – ie, tax rises equating to 11% of GDP will be required to close the gap. This is a recipe for insolvency, as taxpayers will be extremely hostile to yet higher tax demands, having already paid up for large tax rises in the 2020s.

Projecting the Effects of the Brexit Supply-Side Reform Policy

There is another possible programme post-Brexit (the Brexit Supply-Side Reform Policy), which

builds on the caution of the Conservative manifesto to pursue a more ambitious programme of tax

cuts and spending, fully warranted by available funds and the need to push interest rates up out of

the Zero Lower Bound:.

Under this Brexit Supply-Side Reform Programme (see Appendix E), the economic projections show

that interest rates rise to 5% by the early 2020s, inflation rises a little to the 2-3% range, and the

economy grows at close to 3% - about a full percentage point greater than the Post-Brexit Base Case.

Summary Table for the Brexit Supply-Side Reform Policy

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

GDP Growth1 1.4 1.5 2.7 3.1 3.2 3.1 3.0 3.0 3.0 3.1 3.1 3.1 3.3

Inflation CPI 2.5 2.0 2.1 2.1 2.1 2.0 2.0 2.1 2.1 2.1 2.0 2.0 2.1

Wage Growth 3.1 3.6 3.5 3.7 3.7 3.8 3.8 3.9 3.9 3.8 3.9 3.8 3.8

Unemployment (Mill.)2 0.9 0.9 0.8 0.7 0.7 0.6 0.6 0.6 0.6 0.6 0.6 0.6 0.6

Exchange Rate3 78.6 80.1 80.6 80.5 80.4 80.3 80.3 80.2 80.1 80.1 80.0 79.9 79.9

3 Month Interest Rate 0.7 0.9 3.7 4.6 5.0 5.1 5.0 5.0 5.0 5.0 5.0 5.0 5.0

5 Year Interest Rate 1.0 1.0 4.3 4.9 5.3 5.3 5.1 5.0 5.0 5.0 5.0 5.0 5.0

Current Balance (£bn) -81.3 -84.1 -35.3 -26.6 -22.3 -13.2 -9.8 -8.9 -11.9 -5.9 -1.7 4.3 7.6

PSBR (£bn) 40.8 40.6 52.4 40.9 39.8 39.9 42.4 50.9 46.9 40.6 35.0 29.0 19.9

1 Expenditure estimate at factor cost

2U.K. Wholly unemployed excluding school leavers (new basis) 3Sterling effective exchange rate, Bank of England Index (2005 = 100)

13

Listed below are the values of key parameters as of 2027:

2027 PV of Debt (relative to the Post-Brexit Base Case): £200 billion lower

2027 Nominal GDP (relative to the Post-Brexit Base Case): 27% greater

2027 PV Debt/2027 Nominal GDP ratio: 55%

2027 PV of future steady-state tax revenues : 41% of GDP

2027 PV of future steady-state spending including debt interest : 40% of GDP In this case, the Fiscal Gap = 40-41 = -1% of GDP – ie, there is a Fiscal Surplus of 1% of GDP. This provides an opportunity for greater spending/tax cuts than with the current Conservative Manifesto. In the Table that follows, we show the updated Cardiff Macro Group calculations for projected

government borrowing post-Brexit. We build in assumptions about the government’s projected

additional post-Brexit spending plans, which we have called the ‘Fiscal Fund’.

The projection show that additional measures (in addition to those already included in the

Conservative Manifesto) costing £25 billion a year from 2020 and an extra £65 billion a year from

2025 are consistent with bringing public debt down to around 60% of GDP by 2027. This debt is

counted free of any Bank monetary operations, on the assumption that the Bank of England unwinds

all its operations in public debt, reversing QE; this is in line with the assumption that monetary policy

would be normalised by then. This implies that all public debt is held outside the public sector itself-

at present about a third is held by the Bank and so is not public sector debt at all in theory.

The Path of Public Borrowing and Debt with Brexit Supply-Side Reform Policy (£ Billion, Current Prices)

PSBR +Fiscal Fund

Debt GDP (Mkt Price)

Debt/GDP %

2018 41.4 1559 2127 73.3

2019 37.4 1716 2215 77.5

2020 20.4 +25 1761 2310 76.2

2021 7 +25 1793 2410 74.4

2022 3 +25 1821 2514 72.4

2023 -10 +25 1836 2630 69.8

2024 -15.5 +25 1846 2753 67.0

2025 -25 +65 1885 2891 65.2

2026 -35 +65 1916 3035 63.1

2027 -45 +65 1936 3187 60.7

Note- Public sector net debt (excluding public sector banks) estimated at £1646 billion at end 2017-18 FY

(in Sept 2017 £1638 billion, source ONS.)

14

The Need to Raise Interest Rates. However, a key point to note is the great need, explained above,

for fiscal policy to drive up interest rates. This could well call for more borrowing than is pencilled

into the table; we cannot know how much is needed until we see how interest rates respond.

But to those who fear the government risks insolvency by being so aggressive in fiscal policy, it is

important to note that in the current market place government bond issues are being priced at

extremely low interest rates (around 1% pa currently) because they are seen uniquely as entirely

safe - the UK government has never defaulted and is backed by UK taxpayers, law-abiding

people/firms who always pay up.

Most commentators, including the OBR, the IFS and most macro forecasters, and even it would

seem the Treasury itself, have not caught up with these key facts of the macro situation. As Lord

Keynes once said ‘If the facts change, I change my mind; what do you do?’.

Example of Brexit Supply-Side Reform Policy. Matters do not end there. This policy will have

dynamic effects on the UK economy, by cutting taxes and boosting growth-friendly infrastructure.

The arithmetic above computes the debt evolution on the basis of £65 billion pa fiscal expansion by

2025 on the assumption that solvency concerns drive debt to a ‘safe’ 60% of GDP by 2027. In

practice, fiscal policy may likely need to be more aggressive than this in order to drive up interest

rates to reasonable levels at which monetary policy bites again. Such rates might be around 5%, and

require more borrowing than we have assumed in our ‘safe’ arithmetic; indeed, to drive UK rates up.

If world rates remain mired around 2-3%, the UK has to look ‘more risky’ by seriously aggressive

borrowing. For illustrative purposes we will assume the extra borrowing reaches £100 billion pa by

2025 - we will call this ‘Fiscal Fund Plus’.

This would make possible various tax cuts that could boost the UK’s competitiveness. Here is the

current cost of such tax cuts – ie, a 1% rate cut in

Corporation tax would cost £3.2 billion by 2025

The standard rate of income tax, £5.6 billion

The top rate of income tax, £1.5 billion

The very top (‘additional’) rate, £0.2 billion.

So a cocktail of pro-entrepreneur tax cuts and spending changes worth £100 billion could be :

Cut corporation tax by 10% : £32 billion

Abolish the very top additional 45% rate : £1 billion

Cut the top rate of income tax to 30% : £15 billion.

Cut the standard rate of income tax by 5% : £28 billion.

This would give a total of £76 billion, representing a weighted average tax cut across all income of

about 15%, leaving £24 billion extra (about 1% of GDP) for spending on public services and

infrastructure. According to the Liverpool supply side model of the UK, every 2% off the average tax

rate gains 1% on GDP in the long run by making the labour market more competitive. The second

round effects of Brexit through the Fiscal Fund-Plus would therefore boost the economy by a further

7% over the decade from 2020 - or another 0.7% pa on growth from 2020-2030.

15

How should we evaluate the effects of the remaining £24 billion extra spend on public services ? We

know that these also boost growth by raising private productivity, we assume by the same as the

same amount in tax cuts. This would add another 0.23% per annum to the growth rate.

On this basis we could project the whole programme could boost growth from 2025 by some 1% per

annum.

In the Fiscal Fund Table we projected the programme before counting the extra spending/tax cuts

made necessary to eliminate the Zero Lower Bound. We suggested this could push the Fiscal Fund

up to £100 billion by 2025. We assume this extra amount would come in gradually, reaching a

further £35 billion by 2025. The idea of these higher deficits is to stimulate the economy and so

raise interest rates to normal rates close to 5%. The amount needed would be kept under review in

the light of the interest rate situation. But so stubborn is the Zero Lower Bound proving that these

figures look a likely projection as of now.

They would raise the debt/GDP ratio to 67% of GDP by 2027 - before taking account of present value

effects resultng from higher interest rates. This would delay the date at which the safe 60% debt

ratio would be reached until 2031. However, taking into account the present value effects resulting

from higher interest rates would imply that the safe debt/GDP ratio would be reached by around

2024.

This illustrates how a bold fiscal strategy designed to generate supply-side improvements and

stimulate interest rates up to normal rates is entirely feasible and safe in current circumstances.

CONCLUDING REMARKS

A decade ago, the Conservative-Liberal Democrat Coalition Government embarked on a policy of deficit reduction that became synonymous with ‘austerity’3. At the time, one of the arguments proposed in favour of austerity was the idea of an expansionary fiscal contraction, or expansionary austerity4. This went against the traditional textbook Keynesian economic model whereby lower/higher public spending led to lower/higher economic growth. A decade on, our work suggests that it can be argued that the Labour Party Manifesto, if implemented, would result in the emergence of a new and completely opposite idea, namely a contractionary fiscal expansion. The primary reason for a contractionary fiscal expansion would be the negative supply-side effects on the economy, but there are likely to be very significant negative demand-side consequences as well.

3 Fiscal policy, despite received wisdom as to its austerity, was actually not that austere. Public sector net borrowing (PSNB)

was 9.3 percent of GDP in 2010, falling to 4.2 percent of GDP in 2015 and 1.4 percent last year. In other words, for the first half of the decade the UK ran a very large deficit and has subsequently remained in deficit albeit smaller.

4 Those arguing for expansionary austerity weren’t saying that every time the government cut public spending the

economy would expand, rather that in certain circumstances the direct GDP cost of spending cuts could be more than

compensated for by increases in other components of aggregate demand such as consumer expenditure and business

investment. With the budget deficit (public sector net borrowing PSNB) at almost 10 percent of GDP in 2010, the

exceptional circumstances argument seemed well made. A new book, Austerity – When it Works and When it Doesn’t, by

Alberto Alesina, Carlo Favero and Franceso Giavezzi, 2019, highlights the conditions under which austerity has resulted in

faster growth.

16

In a sense, the idea of a contractionary fiscal expansion is not new at all. Socialist experiments have been tried and failed many times. In his book, Socialism – The Failed Idea That Never Dies, Kristian Niemietz documents that, over the past 100 years, there have been more than two dozen attempts to build a socialist society - from the USSR, to Cuba to Maoist China to Venezuela. Niemietz points out that: “All of them have ended in varying degrees of failure”. Even relatively modest attempts, such as the French Mitterand expansion in the 1980s, had to be quickly reversed. The most recent example of these has been the socialist policies of Venezuela5 – strongly supported by the Leader of the Opposition - despite the utter failure of what should be the most affluent economy in South America, given its oil reserves. The government budget deficit in Venezuela ballooned from 4.7 percent of GDP in 20106, to 15.6 percent of GDP in 2014 and on to an explosive 30.6 percent of GDP in 2018, as the economy collapsed. Thus, we have ample evidence showing that large fiscal expansions and state interventions in the economy have a nasty habit of ending in tears, creating an economy in a worse position than before. Our macroeconomic analysis and projections suggest the policies of the Labour Manifesto will prove this yet again. The result of these Labour’s Manifesto policies would very likely be a large short-term sterling criss,

causing inflation to spike, and forcing the Bank to raise interest rates sharply. While this would

rapidly end the Zero Lower Bound, it would do so in a way that effectively stops monetary policy

from being free to stimulate the economy. The cure would be worse than the disease.

As far as the long-term is concerned, these policies would cause a severe weakening of the public

sector balance sheet, with the debt/GDP ratio rising to about 90% and future tax revenues down

over 20%, precipitating fears of long-run insolvency. There would be a large Fiscal Gap, needing to

be closed by further tax rises.

Assuming a Labour Government is not elected, there is a need for fiscal expansion in order to lift the

economy off the Zero Lower Bound and return power to monetary policy. With Brexit creating a

strong post-Brexit supply side, a Conservative government would have an opportunity to spend

more, on top of using the growing public finance surplus, as well as cutting taxes, and still hit a safe

60% debt/GDP ratio well before 2027. Following a political decision to minimise fiscal risk, the

actuel Conservative Manifesto is far more cautious.

5 Dangerous Hero – Corbyn’s Ruthless Plot for Power, Tom Bower, 2019.

6 IMF Fiscal Monitor, October 2019, Table A9.

17

CHART 1

18

CHART 2

19

CHART 3

20

CHART 4

21

CHART 5

22

APPENDIX A

BASIS OF CARDIFF MODELS

At the heart of our estimates lie models which assume a world of tough long run competition in

which industries can only survive by matching the competitive norm. By contrast the consensus

among trade theorists is that competing firms have significant monopoly power due to their unique

brands; this theory is known as ‘gravity’ modelling, in which natural monopoly power arises simply

from size and proximity to consumers. On this view cutting into rival markets is hard, and this fact

also protects their own market position. Along with this view goes an interventionist theory of

regulation: that ‘rights’ can be awarded to ‘stakeholders’ at the expense of monopolist firms, with

little damage to their competitive position. Along with it too goes the view that productivity

growth occurs automatically as a result of growing trade, itself a product of proximity.

In our research we find a very different world: a world in which lagging firms can be largely de-

stroyed, with examples like Nokia and Blackberry coming to mind. We see the role of supply

chains as squeezing out uncompetitive intermediate producers who do not devote enough effort

to raising productivity via innovation. In this world business regulation can easily damage compet-

itiveness. This is particularly true of labour market regulation, for which we have good estimates

of the damage based on UK experience (see chapter 2 of Minford et al, 2015).

In our Cardiff World Trade Model we embed these assumptions and test their predictions against

the facts of UK trade. We also set up a rival ‘gravity model’ as set out above. We test these mod-

els by indirect inference against the UK facts (Minford and Xu, Open Economies Review, 2018).

This test is based on simulating each model many times to generate a full range of counterfactual

histories due to randomly chosen reruns of historical shocks; we then ask how probable the actual

UK history would have been if the model were correct. What we find is that the gravity model is

highly improbable, well below a 5% minimum threshold of rejection, whereas the Cardiff model is

fairly probable, comfortably above this rejection level.

The implications of the Cardiff models for Brexit are radical. Brexit will usher in a world in which

for the first time in our post-war history the UK market will be entirely dominated by world com-

petition, finally admitted by abandoning EU protection of farming and manufacturing. UK firms

and farms will have to be competitive with the best the world has to offer; this plainly will lower

prices to the consumer and raise UK productivity. Notice that because UK service sectors have

never had EU protection, not much changes for them in terms of necessary world competitive-

ness.. To ensure this competitiveness UK regulations will have to be business-friendly; utterly

gone will be the idea that there is some ‘free lunch’ of ‘rights’ to be exacted from the business

community for the benefit of particular constituencies.

What then of the position of EU firms in these UK markets? It will have fundamentally changed.

Instead of being able to sell food and manufactures to UK consumers at inflated prices, owing to

the lack of world competition, they will have to sell here at world prices, some 20% lower if EU

protection is entirely removed. Were they not to match these prices they would simply be pushed

out of the UK market, to sell nothing at all.

It needs to be understood just how large a change this is for EU exporters to the UK. The UK con-

23

stitutes about a quarter of the whole EU consumer market. If prices fall by a fifth, their margins on

a quarter of their sales may well be entirely wiped out.

24

APPENDIX B

THE POST-BREXIT BASELINE PROJECTION In this baseline post-Brexit forecast we make assumptions about the Brexit effects as follows. The

long-run gains, come from four main sources (Minford, 2017):

Moving to free trade with non-EU countries that currently face high EU protection in

goods trade

Substituting UK-based regulation for EU-based Single Market regulation

Ending the large subsidy that the ‘four freedoms’ forces the UK to give to EU unskilled immi-grants

Ending our Budget contribution to the EU.

In total these four elements create a rise in GDP in the long term over the next decade and a half

of about 7%, which is equivalent to an average rise in the growth rate of around 0.5% per an-

num.

Baseline Forecast

1 Expenditure estimate at factor cost 2U.K. Wholly unemployed excluding school leavers (new basis) 3Sterling effective exchange rate, Bank of England Index (2005 = 100)

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

GDP Growth1 1.4 1.5 1.9 1.9 2.1 2.1 2.0 2.0 2.0 2.0 2.1 2.1 2.0

Inflation CPI 2.5 1.9 2.1 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0

Wage Growth 3.1 3.6 3.1 3.1 3.1 3.2 3.2 3.3 3.3 3.3 3.4 3.3 3.2

Unemployment (Mill.)2 0.9 0.9 0.8 0.7 0.7 0.6 0.6 0.6 0.6 0.6 0.6 0.6 0.6

Exchange Rate3 78.6 80.1 80.7 80.6 80.5 80.4 80.3 80.2 80.1 79.9 79.8 79.7 79.5

3 Month Interest Rate 0.7 0.9 4.7 4.2 3.3 3.0 2.5 2.3 2.1 2.0 2.0 2.0 2.0

5 Year Interest Rate 1.0 1.0 1.3 2.4 3.3 3.4 3.3 2.6 2.4 2.2 2.0 2.0 2.0

Current Balance (£bn) -81.3 -86.5 -41.3 -3.14 -23.3 -15.0 -11.9 -11.3 -14.5 -9.4 -59. -0.1 3.0

PSBR (£bn) 40.8 37.8 20.7 8.2 3.9 0.5 -3.2 -5.4 -17.4 -30.2 -45.1 -58.6 -71.9

25

Prices, Wages, Interest Rates and Exchange Rate Forecast (Seasonally Adjusted)

Inflation

%1

(CPI)

Short Dated

(5 Year)

Interest

Rates

3 Month

Int.

Rates

Nominal

Exchange

Rate

(2005=100) 2

Real Ex-

change

Rate3

Real 3

Month

Int. Rates

%4

Infla-

tion

(RPIX)

Real Short

Dated Rate

of

Interest5

2017 2.6 0.6 0.4 77.4 75.7 -1.7 3.8 -1.5

2018 2.5 1.0 0.7 78.6 76.5 -1.3 3.3 -0.5 2019 1.9 1.0 0.9 80.1 74.7 -1.0 2.6 0.5

2020 2.1 1.3 1.1 80.7 76.0 -1.1 2.9 1.4

2021 2.0 2.4 1.9 80.6 76.3 -1.0 2.8 0.9 2022 2.0 3.3 2.4 80.5 76.6 0.1 2.7 0.6

2023 2.0 3.4 3.1 80.4 76.8 1.0 2.7

2024 2.0 3.3 3.1 80.3 77.1 1.1 2.7 -1.5 2025 2.0 2.6 2.6 80.2 77.3 0.1 2.7 -1.7

2026 2.0 2.4 2.3 80.1 77.5 -0.2 2.7 -1.5

2027 2.0 2.2 2.0 79.9 77.8 -0.5 2.7 -1.3 2028 2.0 2.0 2.0 79.8 78.0 -0.5 2.8

2029 2.0 2.0 2.0 79.7 78.2 -0.2 2.8 -1.1

2030 2.0 2.0 2.0 79.5 78.5 -0.1 2.8 -1.1

2018:1 2.5 1.0 0.5 79.2 78.1 -1.6 3.7 -1.1 2018:2 2.5 1.0 0.7 79.3 77.9 -1.9 3.4 -1.0

2018:3 2.5 1.0 0.8 78.0 75.9 -1.3 3.2 -0.9

2018:4 2.3 1.0 0.8 78.0 74.2 -0.5 3.0 -0.9

2019:1 1.9 0.9 0.8 79.0 72.8 -0.6 2.4 -1.1

2019:2 2.0 1.0 0.8 80.4 75.3 -1.2 2.7 -1.0 2019:3 2.0 1.1 1.0 80.3 75.3 -1.2 2.6 -0.9

2019:4 1.9 1.1 1.0 80.6 75.5 -1.1 2.6 -0.9

2020:1 2.1 1.1 1.0 80.7 75.5 -1.0 2.9 -0.9

2020:2 2.0 1.2 1.1 80.9 76.3 -1.0 2.8 -0.8

2020:3 2.0 1.3 1.1 80.7 76.2 -1.0 2.8 -0.7 2020:4 2.1 1.7 1.2 80.6 76.1 -1.4 3.0 -0.3

2021:1 2.0 2.3 1.8 80.7 76.0 -0.8 2.7 0.3 2021:2 2.0 2.5 1.9 80.8 76.5 -0.9 2.7 0.5

2021:3 2.0 2.4 2.0 80.6 76.5 -1.2 2.7 0.4

2021:4 2.1 2.5 2.0 80.4 76.3 -1.0 2.8 0.5

2022:1 1.9 2.9 2.1 80.7 76.2 -0.9 2.6 0.3

2022:2 2.0 2.9 2.1 80.6 76.8 -0.3 2.8 0.5 2022:3 2.0 3.7 2.1 80.5 76.7 0.1 2.7 0.4

2022:4 2.0 3.8 3.3 80.3 76.6 1.4 2.8 0.5

2023:1 2.0 3.5 3.2 80.5 76.5 1.1 2.7 0.3

2023:2 1.9 3.4 3.0 80.6 77.0 0.9 2.6 0.5

2023:3 2.0 3.4 3.0 80.4 76.9 0.9 2.7 0.4 2023:4 2.0 3.3 3.2 80.2 76.8 1.2 2.8 0.5

2024:1 2.0 3.3 3.2 80.4 76.7 1.2 2.7 0.3 2024:2 2.0 3.3 3.3 80.4 77.3 1.3 2.7 0.5

2024:3 2.0 3.5 2.9 80.3 77.2 0.9 2.7 0.4

2024:4 2.0 3.1 3.0 80.0 77.1 1.0 2.8 0.5

2025:1 2.0 2.7 3.1 80.3 77.0 0.6 2.7 -1.1

2025:2 2.0 2.6 2.5 80.3 77.5 0.0 2.7 -1.0 2025:3 2.0 2.5 2.6 80.1 77.4 0.1 2.7 -0.9

2025:4 2.0 2.5 2.2 79.9 77.3 -0.3 2.7 -0.9

2026:1 2.0 2.5 2.1 80.2 77.2 -0.4 2.7 -1.1

2026:2 2.0 2.3 2.3 80.2 77.7 -0.2 2.8 -1.0

2026:3 2.0 2.3 2.6 80.0 77.7 0.1 2.8 -0.9 2026:4 2.0 2.3 2.1 79.8 77.6 -0.4 2.7 -0.9

2027:1 2.0 2.2 2.1 80.1 77.4 -0.4 2.7 -0.9 2027:2 2.0 2.2 2.0 80.1 78.0 -0.5 2.7 -0.8

2027:3 2.0 2.2 2.0 79.9 77.9 -0.5 2.7 -0.7

26

2027:4 2.0 2.1 2.0 79.7 77.8 -0.5 2.8 -0.3

2028:1 2.0 2.1 2.0 80.0 77.7 -0.5 2.7 0.3

2028:2 2.0 2.0 2.0 80.0 78.2 -0.6 2.7 0.5

2028:3 2.0 2.0 2.0 79.7 78.1 -0.6 2.8 0.4 2028:4 2.0 2.0 2.0 79.6 78.0 -0.6 2.7 0.5

2029:1 2.0 2.0 2.0 79.9 77.9 -0.2 2.7 0.3 2029:2 2.0 2.0 2.0 79.8 78.4 -0.1 2.7 0.5

2029:3 2.0 2.0 2.0 79.6 78.4 -0.2 2.8 0.4

2029:4 2.0 2.0 2.0 79.4 78.3 -0.2 2.7 0.5

2030:1 2.0 2.0 2.0 79.7 78.1 -0.2 2.7 0.3

2030:2 2.0 2.0 2.0 79.7 78.7 -0.1 2.8 0.5 2030:3 2.0 2.0 2.0 79.4 78.6 0.0 2.8 0.4

2030:4 2.0 2.0 2.0 79.3 78.5 0.0 2.7 0.5 1 Consumer’s Expenditure Deflator 2 Sterling Effective Exchange Rate Bank of England 3 Ratio of UK to other OECD consumer prices adjusted for nominal exchange rate 4 Treasury Bill Rate less one year forecast of inflation 5 Short Dated 5 Year Interest Rate less average of predicted 5 year ahead inflation rate

27

Labour Market and Supply Factors (Seasonally Adjusted)

Average

Earnings

(1990=100)1

Wage

Growth2

Unemployment (New Basis)

Percent3

Millions

Real Wage

Rate4

(1990=100)

2017 259.1 2.8 2.2 0.8 141.9

2018 266.6 3.1 2.5 0.9 142.8

2019 275.8 3.6 2.4 0.9 145.2 2020 284.4 3.1 2.2 0.8 146.7

2021 293.3 3.1 1.9 0.7 148.4

2022 302.4 3.1 1.8 0.7 150.0 2023 312.2 3.2 1.6 0.6 151.9

2024 322.2 3.2 1.6 0.6 153.7

2025 332.7 3.3 1.5 0.6 155.7 2026 343.7 3.3 1.5 0.6 157.7

2027 355.0 3.3 1.5 0.6 159.7

2028 367.0 3.4 1.5 0.6 161.9 2029 378.9 3.3 1.5 0.6 164.0

2030 391.1 3.2 1.4 0.6 165.9

2018:1 264.6 3.0 2.3 0.8 142.6

2018:2 263.4 2.8 2.5 0.9 141.5

2018:3 268.0 3.0 2.5 0.9 143.2 2018:4 270.2 3.8 2.7 1.0 144.0

2019:1 273.4 3.9 2.9 1.0 145.4 2019:2 273.4 3.8 2.2 0.8 144.1

2019:3 276.9 3.3 2.2 0.8 145.2

2019:4 279.3 3.4 2.2 0.8 146.1

2020:1 282.1 3.2 2.3 0.9 147.0

2020:2 281.8 3.1 2.2 0.8 145.6 2020:3 285.5 3.1 2.2 0.8 146.7

2020:4 288.2 3.2 2.2 0.8 147.6

2021:1 290.7 3.1 2.0 0.8 148.6

2021:2 290.9 3.2 2.0 0.8 147.4

2021:3 294.5 3.2 1.9 0.7 148.5 2021:4 297.1 3.1 1.9 0.7 149.1

2022:1 299.6 3.1 1.9 0.7 150.3 2022:2 299.7 3.1 1.9 0.7 148.9

2022:3 303.7 3.1 1.7 0.7 150.1

2022:4 306.7 3.2 1.7 0.7 150.9

2023:1 310.0 3.5 1.7 0.7 152.5 2023:2 309.6 3.3 1.6 0.6 150.9

2023:3 313.1 3.1 1.6 0.6 151.8

2023:4 315.9 3.0 1.6 0.6 152.4

2024:1 320.0 3.2 1.6 0.6 154.4

2024:2 320.1 3.4 1.6 0.6 153.1 2024:3 322.8 3.1 1.5 0.6 153.4

2024:4 325.7 3.1 1.5 0.6 154.1

2025:1 330.7 3.4 1.5 0.6 156.5

2025:2 331.1 3.4 1.5 0.6 155.2

2025:3 333.5 3.3 1.5 0.6 155.4 2025:4 335.6 3.0 1.5 0.6 155.7

2026:1 341.6 3.3 1.5 0.6 158.5 2026:2 342.0 3.3 1.5 0.6 157.2

2026:3 344.8 3.4 1.5 0.6 157.6

2026:4 346.4 3.2 1.5 0.6 157.6

2027:1 353.5 3.5 1.5 0.6 160.8

2027:2 353.7 3.4 1.5 0.6 159.5 2027:3 355.7 3.2 1.5 0.6 159.4

2027:4 356.9 3.0 1.5 0.6 159.2

2028:1 365.1 3.3 1.5 0.6 162.9

28

2028:2 366.0 3.5 1.5 0.6 161.8

2028:3 367.8 3.4 1.5 0.6 161.6

2028:4 369.0 3.4 1.5 0.6 161.4

2029:1 377.2 3.3 1.5 0.6 165.0 2029:2 377.3 3.1 1.5 0.6 163.6

2029:3 380.7 3.5 1.5 0.6 164.0

2029:4 380.5 3.1 1.5 0.6 163.2

2030:1 388.7 3.0 1.5 0.6 166.7

2030:2 388.7 3.0 1.5 0.6 165.2 2030:3 393.4 3.3 1.4 0.6 166.2

2030:4 393.5 3.4 1.4 0.6 165.5 1 Whole Economy 2 Average Earnings 3 Wholly unemployed excluding school leavers as percentage of employed and unemployed, self employed and HM Forces 4 Wage rate deflated by CPI

29

Estimates and Projections of the Gross Domestic Product1 (£ Million 1990 Prices)

Expenditure

Index

£ Million

‘90 prices

Non-Durable

Consumption2

Private Sector

Gross Investment

Expenditure3

Public

Authority

Expenditure4

Net Exports5 AFC

2017 163.3 781822.0 441518.3 300818.9 200522.0 -60310.0 103083.7

2018 165.5 792730.9 445869.9 310567.1 201139.6 -41308.9 106758.3

2019 168.0 804347.9 451568.4 303830.7 204617.4 -52551.8 103116.9 2020 171.2 820012.3 457805.4 294079.0 207575.4 -30702.2 108745.3

2021 174.6 835951.9 464216.7 297988.4 210896.4 -25838.3 111311.2

2022 178.3 853622.4 470251.4 305835.5 214271.0 -22730.0 114005.6 2023 182.0 871244.7 476835.8 312486.6 217699.0 -19317.0 116459.8

2024 185.6 888911.0 484228.1 320908.1 221182.1 -18405.4 119001.7

2025 189.3 906370.2 491734.9 330032.2 224721.0 -18606.0 121512.2 2026 193.0 924204.2 498619.1 340265.4 228316.7 -18991.2 124005.5

2027 196.9 943113.8 506225.7 350023.8 231969.6 -18449.5 126655.7

2028 201.0 962562.9 513313.0 360878.0 235681.4 -17978.0 129331.4 2029 205.1 982303.6 521142.0 369850.7 239452.5 -16181.1 131960.5

2030 209.3 1002075.4 528564.9 380125.9 243284.5 -15585.3 134314.6

2018/17 1.4 1.0 3.2 0.3 22.7

2019/18 1.5 1.3 -1.8 1.7 -18.0

2020/19 1.9 1.4 -3.0 1.5 6.0

2021/20 1.9 1.4 1.3 1.6 2.3

2022/21 2.1 1.3 2.6 1.6 2.1 2023/22 2.1 1.4 2.2 1.6 2.1

2024/23 2.0 1.6 2.7 1.6 2.1

2025/24 2.0 1.6 2.8 1.6 2.1 2026/25 2.0 1.4 3.1 1.6 2.1

2027/26 2.0 1.5 2.9 1.6 2.1

2028/27 2.1 1.4 3.1 1.6 2.1 2029/28 2.1 1.5 2.5 1.6 2.0

2030/29 2.0 1.4 2.8 1.6 1.8

2018:1 164.4 196809.2 110809.6 73337.2 51591.3 -10814.1 28114.8

2018:2 165.1 197627.5 111248.1 78845.0 49253.6 -10094.0 31625.2

2018:3 166.1 198830.2 112094.9 76125.8 49822.6 -10001.3 29211.8 2018:4 166.6 199464.1 111717.3 82259.2 50472.1 -10399.5 34585.0

2019:1 167.6 200618.5 111589.5 85538.7 52691.8 -27678.5 21523.0 2019:2 167.8 200870.1 113657.2 74871.8 50827.1 -14036.4 24449.6

2019:3 167.9 201001.6 113170.0 70256.8 50222.0 -5107.9 27539.3

2019:4 168.6 201857.7 113151.8 73163.4 50876.5 -5729.0 29605.0

2020:1 170.9 204650.4 113061.1 79372.3 53218.7 -14821.9 26179.8

2020:2 170.6 204203.2 115141.3 70795.9 51640.8 -7012.1 26362.7 2020:3 171.3 205098.3 114754.0 70595.7 51025.1 -4284.8 26991.7

2020:4 172.1 206060.4 114849.0 73315.1 51690.8 -4583.4 29211.1

2021:1 174.3 208707.0 114530.9 79879.0 54070.2 -12598.7 27174.4

2021:2 173.8 208060.4 116753.6 71214.3 52466.7 -5258.2 27116.0

2021:3 174.7 209116.9 116475.3 72045.6 51841.5 -3856.3 27389.2 2021:4 175.4 210067.6 116456.9 74849.5 52517.9 -4125.1 29631.6

2022:1 178.0 213153.4 116019.8 81471.9 54935.4 -11338.8 27934.9 2022:2 177.4 212360.5 118387.8 72688.1 53306.5 -4208.0 27813.9

2022:3 178.4 213584.3 117873.0 74497.6 52670.9 -3470.7 27986.5

2022:4 179.2 214524.2 117970.9 77178.0 53358.2 -3712.6 30270.3

2023:1 181.8 217658.9 117644.1 82945.9 55814.4 -10205.0 28540.5

2023:2 181.0 216648.1 120164.0 74099.7 54159.1 -3365.5 28409.2 2023:3 182.1 217971.7 119405.3 76420.6 53513.7 -2776.5 28591.4

2023:4 182.9 218966.0 119622.5 79020.4 54211.9 -2970.1 30918.7

2024:1 185.5 222098.3 119408.7 85352.0 56707.4 -10205.0 29164.8

2024:2 184.6 221010.1 122086.8 75946.6 55025.5 -3028.6 29020.2

2024:3 185.8 222387.1 121315.8 78418.7 54369.9 -2498.9 29218.4 2024:4 186.6 223415.5 121416.8 81190.8 55079.3 -2673.1 31598.3

2025:1 189.3 226598.7 121199.9 88794.0 57614.7 -11225.5 29784.4

2025:2 188.2 225360.7 124040.2 77773.5 55905.9 -2725.8 29633.1

30

2025:3 189.3 226687.5 123256.9 80278.8 55239.8 -2249.0 29839.0

2025:4 190.2 227723.3 123238.1 83186.0 55960.6 -2405.7 32255.7

2026:1 193.0 231025.0 122896.7 92345.2 58536.5 -12348.0 30405.4

2026:2 191.9 229792.9 125776.5 79907.5 56800.5 -2453.9 30237.7 2026:3 193.0 231078.8 125105.7 82328.9 56123.7 -2024.1 30455.4

2026:4 193.9 232307.5 124840.1 85683.7 56855.9 -2165.2 32907.0

2027:1 196.7 235554.5 124617.2 94981.5 59473.1 -12471.4 31045.9

2027:2 195.9 234514.2 127663.4 82237.1 57709.2 -2207.8 30887.7

2027:3 197.0 235852.5 127107.4 84658.9 57021.7 -1821.7 31113.8 2027:4 198.1 237192.6 126837.6 88146.4 57765.6 -1948.7 33608.3

2028:1 200.8 240416.4 126361.9 97952.5 60424.6 -12596.0 31726.6 2028:2 200.0 239402.1 129577.9 84705.9 58632.8 -1988.7 31525.8

2028:3 201.1 240710.2 128759.9 87432.8 57934.0 -1639.5 31777.0

2028:4 202.1 242034.2 128613.3 90786.8 58689.9 -1753.8 34302.0

2029:1 204.9 245361.9 128257.3 99430.6 61391.4 -11336.2 32381.2

2029:2 204.1 244303.7 131650.7 87035.5 59571.1 -1790.9 32162.7 2029:3 205.2 245650.0 130820.1 89872.2 58861.0 -1475.6 32427.7

2029:4 206.2 246988.0 130413.9 93512.5 59628.9 -1578.4 34988.9

2030:1 209.2 250421.4 130181.1 102114.7 62373.6 -11222.6 33025.4

2030:2 208.3 249377.2 133361.7 89896.0 60524.6 -1613.9 32791.2

2030:3 209.1 250350.3 132652.0 92366.2 59803.3 -1328.2 33143.0 2030:4 210.4 251926.5 132370.1 95749.0 60583.0 -1420.6 35355.0

1 GDP at factor cost. Expenditure measure; seasonally adjusted 2 Consumers expenditure less expenditure on durables and housing 3 Private gross domestic capital formation plus household expenditure on durables and clothing plus private sector stock building 4 General government current and capital expenditure including stock building 5 Exports of goods and services less imports of goods and services

31

Financial Forecast

PSBR/GDP %1 GDP1

(£bn)

PSBR

(£bn)

Financial Year

Debt Interest

(£bn)

Current

Account

(£ bn)

2017 2.6 2048.0 53.7 18.3 -68.3

2018 1.9 2111.8 40.8 23.4 -81.3

2019 1.8 2177.6 37.8 26.5 -86.5 2020 0.9 2268.0 20.7 28.9 -41.3

2021 0.4 2358.8 8.2 33.1 -31.4

2022 0.2 2457.4 3.9 36.9 -23.3 2023 0.0 2558.3 0.5 39.5 -15.0

2024 -0.1 2663.4 -3.2 39.6 -11.9

2025 -0.2 2770.3 -5.4 35.4 -11.3 2026 -0.6 2882.5 -17.4 35.1 -14.5

2027 -1.1 3000.4 -32.0 33.1 -9.4

2028 -1.4 3125.0 -45.1 32.8 -5.9 2029 -1.8 3253.2 -58.6 32.3 -0.1

2030 -2.1 3384.1 -71.9 31.6 3.0

2018:1 -2.9 517.6 -14.9 4.9 -17.7

2018:2 4.7 524.6 24.6 5.7 -19.9

2018:3 1.8 524.6 9.5 5.7 -20.5 2018:4 4.8 535.5 25.6 5.7 -23.1

2019:1 -3.6 527.1 -18.8 6.3 -37.8 2019:2 2.9 535.6 15.5 6.4 -25.4

2019:3 2.9 540.4 15.6 6.7 -10.1

2019:4 2.7 548.5 15.0 6.7 -13.2

2020:1 -1.5 553.0 -8.4 6.7 -11.3

2020:2 1.9 557.1 10.5 6.9 -11.0 2020:3 1.5 562.6 8.3 7.0 -8.3

2020:4 1.3 572.3 7.3 7.1 -10.7

2021:1 -0.9 575.9 -5.3 7.9 -6.8

2021:2 1.1 579.5 6.5 8.1 -7.6

2021:3 0.7 585.1 4.4 8.3 -7.5 2021:4 0.7 595.3 4.3 8.3 -9.5

2022:1 -1.2 598.9 -6.9 8.4 -3.6 2022:2 0.6 603.2 3.7 8.5 -4.9

2022:3 0.1 609.6 0.8 8.5 -6.4

2022:4 0.3 620.5 2.1 10.0 -8.4

2023:1 -0.4 624.1 -2.7 9.9 -0.8 2023:2 0.5 627.3 3.1 9.7 -2.9

2023:3 0.1 634.8 0.5 9.7 -4.7

2023:4 -0.1 646.4 -0.3 10.0 -6.5

2024:1 -0.4 649.8 -2.9 10.0 -0.5

2024:2 0.2 653.1 1.6 10.2 -1.9 2024:3 -0.3 660.8 -2.1 9.7 -3.9

2024:4 -0.5 673.0 -3.3 9.8 -5.6

2025:1 0.1 676.5 0.6 10.0 -2.5

2025:2 -0.3 679.4 -2.0 9.1 -0.9

2025:3 -0.7 687.2 -4.8 9.2 -3.0 2025:4 0.7 700.0 4.7 8.6 -4.7

2026:1 -0.5 703.7 -3.4 8.5 -5.7 2026:2 -0.7 707.0 -4.9 8.8 -0.7

2026:3 -1.0 714.8 -7.3 9.3 -3.1

2026:4 0.3 728.8 1.9 8.5 -4.9

2027:1 -1.0 732.0 -7.1 8.5 -5.3

2027:2 -1.1 736.2 -8.4 8.3 0.5 2027:3 -1.5 743.4 -10.8 8.3 -1.5

2027:4 -0.2 759.0 -1.2 8.3 -3.1

2028:1 -1.5 761.9 -11.6 8.2 -4.9

32

2028:2 -1.5 766.6 -11.7 8.2 1.8

2028:3 -1.9 774.7 -14.5 8.2 -0.6

2028:4 -0.5 790.4 -4.0 8.2 -2.2

2029:1 -1.9 793.3 -14.9 8.2 -1.5 2029:2 -1.9 798.2 -15.0 8.1 2.7

2029:3 -2.2 806.5 -17.8 8.1 0.2

2029:4 -0.9 822.8 -7.1 8.1 -1.5

2030:1 -2.2 825.8 -18.5 8.0 -0.8

2030:2 -2.3 831.1 -18.7 8.0 3.5 2030:3 -2.4 837.3 -20.3 7.9 1.0

2030:4 -1.2 856.3 -10.5 7.9 -0.7 1 GDP at market prices (Financial Year)

33

APPENDIX C

THE CONSERVATIVE MANIFESTO PROJECTION

Forecast scenario: Conservative Party Manifesto

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

GDP Growth1 1.4 1.5 2.2 2.5 2.1 2.1 2.2 2.2 2.2 2.3 2.3 2.3 2.3

Inflation CPI 2.5 2.0 2.1 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0

Wage Growth 3.1 3.7 3.0 3.2 3.3 3.2 3.2 3.3 3.3 3.3 3.4 3.3 3.2

Unemployment (Mill.)2 0.9 0.9 0.8 0.7 0.7 0.6 0.6 0.6 0.6 0.6 0.6 0.6 0.6

Exchange Rate3 78.6 80.2 80.6 80.6 80.6 80.4 80.2 80.0 79.9 79.8 79.7 79.6 79.5

3 Month Interest Rate 0.7 0.9 1.1 1.8 2.5 3.2 3.1 2.6 2.3 2.1 2.1 2.1 2.1

5 Year Interest Rate 1.0 1.0 1.3 2.4 3.3 3.4 3.3 2.6 2.4 2.2 2.0 2.0 2.0

Current Balance (£bn) -81.3 -86.6 -41.3 -31.3 -23.2 -14.9 -11.8 -11.1 -14.3 -9.2 -5.8 0.1 3.1

PSBR (£bn) 40.8 37.6 30.0 16.4 12.4 9.0 5.0 2.2 -9.9 -25.7 -38.9 -53.0 -67.3

1 Expenditure estimate at factor cost 2U.K. Wholly unemployed excluding school leavers (new basis) 3Sterling effective exchange rate, Bank of England Index (2005 = 100)

34

Prices, Wages, Interest Rates and Exchange Rate Forecast (Seasonally Adjusted)

Inflation %1

(CPI)

Short Dated

(5 Year)

Interest Rates

3 Month

Int. Rates

Nominal

Exchange

Rate (2005=100) 2

Real Exchange

Rate3

Real 3 Month

Int. Rates %4

Inflation

(RPIX)

Real

Short

Dated

Rate of

Interest5

2017 2.6 0.6 0.4 77.4 75.7 -1.7 3.8 -1.5

2018 2.5 1.0 0.7 78.6 76.5 -1.3 3.3 -0.5

2019 2.0 1.0 0.9 80.2 74.8 -0.9 2.7 0.5

2020 2.1 1.3 1.1 80.6 75.8 -1.4 2.9 1.4

2021 2.0 2.4 1.8 80.6 76.3 -1.0 2.8 0.9

2022 2.0 3.3 2.5 80.6 76.7 0.2 2.8 0.6

2023 2.0 3.4 3.2 80.4 76.9 1.1 2.7

2024 2.0 3.3 3.1 80.2 77.1 1.1 2.8 -1.5

2025 2.0 2.6 2.6 80.0 77.3 0.1 2.8 -1.7

2026 2.0 2.4 2.3 79.9 77.6 -0.2 2.8 -1.5

2027 2.0 2.2 2.1 79.8 77.9 -0.4 2.8 -1.3

2028 2.0 2.0 2.1 79.7 78.1 -0.4 2.8

2029 2.0 2.0 2.1 79.6 78.4 0.0 2.8 -1.1

2030 2.0 2.0 2.1 79.5 78.6 0.1 2.8 -1.1

2018:1 2.5 1.0 0.5 79.2 78.1 -1.6 3.7 -1.1

2018:2 2.5 1.0 0.7 79.3 77.9 -1.9 3.4 -1.0

2018:3 2.5 1.0 0.8 78.0 75.9 -1.3 3.2 -0.9

2018:4 2.3 1.0 0.8 78.0 74.2 -0.5 3.0 -0.9

2019:1 1.9 0.9 0.8 79.0 72.8 -0.6 2.4 -1.1

2019:2 2.2 1.0 0.8 80.2 75.1 -1.1 3.1 -1.0

2019:3 2.0 1.1 1.0 80.7 75.5 -1.0 2.7 -0.9

2019:4 1.9 1.1 1.0 80.8 75.6 -1.0 2.6 -0.9

2020:1 2.1 1.1 0.9 80.7 75.5 -1.1 3.0 -0.9

2020:2 2.0 1.1 1.0 80.6 76.1 -1.3 2.8 -0.8

2020:3 2.0 1.2 1.1 80.6 75.9 -1.4 2.7 -0.7

2020:4 2.2 1.6 1.1 80.5 75.8 -1.7 3.0 -0.3

2021:1 2.0 2.2 1.6 80.6 75.7 -1.0 2.8 0.3

2021:2 2.0 2.5 1.8 80.6 76.4 -1.0 2.8 0.5

2021:3 2.0 2.4 1.9 80.6 76.4 -1.2 2.8 0.4

2021:4 2.0 2.5 2.0 80.6 76.4 -0.9 2.8 0.5

2022:1 1.9 2.9 2.2 80.7 76.3 -0.8 2.6 0.3

2022:2 2.0 2.9 2.2 80.6 77.0 -0.1 2.7 0.5

2022:3 2.0 3.7 2.2 80.6 76.8 0.2 2.8 0.4

2022:4 2.1 3.8 3.4 80.4 76.7 1.5 2.8 0.5

2023:1 2.0 3.5 3.3 80.5 76.6 1.2 2.8 0.3

2023:2 1.9 3.4 3.1 80.5 77.2 1.0 2.5 0.5

2023:3 2.0 3.4 3.1 80.3 77.0 1.0 2.8 0.4

2023:4 2.0 3.3 3.3 80.2 76.9 1.3 2.8 0.5

2024:1 2.0 3.3 3.3 80.3 76.8 1.3 2.8 0.3

2024:2 2.0 3.3 3.4 80.3 77.3 1.4 2.7 0.5

2024:3 2.0 3.5 2.9 80.1 77.2 0.9 2.8 0.4

2024:4 2.0 3.1 3.0 80.0 77.1 1.0 2.8 0.5

2025:1 2.0 2.7 3.1 80.1 77.0 0.6 2.8 -1.1

2025:2 2.0 2.6 2.6 80.2 77.5 0.0 2.7 -1.0

2025:3 2.0 2.5 2.6 80.0 77.5 0.1 2.8 -0.9

2025:4 2.0 2.5 2.3 79.9 77.4 -0.2 2.8 -0.9

2026:1 2.1 2.5 2.1 79.9 77.2 -0.4 2.9 -1.1

2026:2 2.0 2.3 2.4 80.1 77.8 -0.1 2.8 -1.0

2026:3 2.0 2.3 2.6 79.9 77.7 0.2 2.8 -0.9

35

2026:4 2.0 2.3 2.2 79.8 77.6 -0.3 2.8 -0.9

2027:1 2.1 2.2 2.1 79.8 77.5 -0.4 2.9 -0.9

2027:2 2.0 2.2 2.1 80.0 78.1 -0.4 2.7 -0.8

2027:3 2.0 2.2 2.1 79.9 78.0 -0.4 2.8 -0.7

2027:4 2.0 2.1 2.1 79.7 77.9 -0.4 2.8 -0.3

2028:1 2.1 2.1 2.1 79.7 77.7 -0.4 2.9 0.3

2028:2 2.0 2.0 2.1 79.9 78.3 -0.5 2.7 0.5

2028:3 2.0 2.0 2.1 79.7 78.3 -0.4 2.8 0.4

2028:4 2.0 2.0 2.1 79.6 78.2 -0.4 2.8 0.5

2029:1 2.0 2.0 2.1 79.5 78.0 0.0 2.8 0.3

2029:2 2.0 2.0 2.1 79.8 78.6 0.0 2.7 0.5

2029:3 2.0 2.0 2.1 79.6 78.5 0.0 2.8 0.4

2029:4 2.0 2.0 2.2 79.5 78.4 0.0 2.8 0.5

2030:1 2.0 2.0 2.1 79.4 78.3 0.0 2.8 0.3

2030:2 2.0 2.0 2.1 79.7 78.8 0.0 2.7 0.5

2030:3 2.0 2.0 2.1 79.4 78.7 0.1 2.8 0.4

2030:4 2.0 2.0 2.2 79.3 78.7 0.1 2.8 0.5 1 Consumer’s Expenditure Deflator 2 Sterling Effective Exchange Rate Bank of England 3 Ratio of UK to other OECD consumer prices adjusted for nominal exchange rate 4 Treasury Bill Rate less one year forecast of inflation 5 Short Dated 5 Year Interest Rate less average of predicted 5 year ahead inflation rate

36

Labour Market and Supply Factors (Seasonally Adjusted)

Average

Earnings

(1990=100)1

Wage

Growth2

Unemployment (New Basis)

Percent3

Millions

Real Wage

Rate4

(1990=100)

2017 259.1 2.8 2.2 0.8 141.9

2018 266.6 3.1 2.5 0.9 142.8

2019 276.0 3.7 2.4 0.9 145.2

2020 284.3 3.0 2.2 0.8 146.6

2021 293.5 3.2 1.9 0.7 148.4

2022 303.2 3.3 1.7 0.7 150.2

2023 312.9 3.2 1.6 0.6 152.1

2024 322.9 3.2 1.5 0.6 153.9

2025 333.5 3.3 1.5 0.6 155.8

2026 344.6 3.3 1.5 0.6 157.8

2027 356.0 3.3 1.5 0.6 159.9

2028 368.2 3.4 1.5 0.6 162.1

2029 380.2 3.3 1.4 0.6 164.1

2030 392.5 3.2 1.4 0.6 166.2

2018:1 264.6 3.0 2.3 0.8 142.6

2018:2 263.4 2.8 2.5 0.9 141.5

2018:3 268.0 3.0 2.5 0.9 143.2

2018:4 270.2 3.8 2.7 1.0 144.0

2019:1 273.4 3.9 2.9 1.0 145.4

2019:2 273.9 4.0 2.2 0.8 144.0

2019:3 277.2 3.4 2.2 0.8 145.3

2019:4 279.5 3.4 2.2 0.8 146.2

2020:1 282.1 3.2 2.3 0.9 147.0

2020:2 282.1 3.0 2.2 0.8 145.4

2020:3 285.1 2.9 2.2 0.8 146.5

2020:4 288.0 3.0 2.2 0.8 147.4

2021:1 290.6 3.0 2.0 0.7 148.4

2021:2 291.4 3.3 2.0 0.7 147.3

2021:3 294.8 3.4 1.8 0.7 148.5

2021:4 297.4 3.3 1.8 0.7 149.2

2022:1 300.3 3.3 1.8 0.7 150.4

2022:2 300.7 3.2 1.8 0.7 149.1

2022:3 304.4 3.3 1.7 0.6 150.3

2022:4 307.3 3.3 1.7 0.6 151.1

2023:1 310.8 3.5 1.7 0.6 152.7

2023:2 310.5 3.3 1.5 0.6 151.1

2023:3 313.9 3.1 1.5 0.6 152.0

2023:4 316.6 3.0 1.5 0.6 152.6

2024:1 320.8 3.2 1.5 0.6 154.5

2024:2 320.9 3.3 1.5 0.6 153.2

2024:3 323.5 3.1 1.5 0.6 153.6

2024:4 326.3 3.1 1.5 0.6 154.2

2025:1 331.6 3.4 1.5 0.6 156.6

2025:2 331.8 3.4 1.5 0.6 155.3

2025:3 334.2 3.3 1.5 0.6 155.5

2025:4 336.3 3.1 1.5 0.6 155.8

2026:1 342.7 3.4 1.5 0.6 158.6

2026:2 342.8 3.3 1.5 0.6 157.3

2026:3 345.6 3.4 1.5 0.6 157.7

2026:4 347.2 3.2 1.5 0.6 157.7

2027:1 355.0 3.6 1.5 0.6 161.0

2027:2 354.6 3.4 1.5 0.6 159.6

37

2027:3 356.6 3.2 1.5 0.6 159.6

2027:4 357.7 3.0 1.5 0.6 159.3

2028:1 367.0 3.4 1.5 0.6 163.0

2028:2 367.0 3.5 1.5 0.6 162.0

2028:3 368.8 3.4 1.5 0.6 161.8

2028:4 370.0 3.4 1.5 0.6 161.6

2029:1 379.3 3.4 1.4 0.6 165.2

2029:2 378.3 3.1 1.4 0.6 163.8

2029:3 381.8 3.5 1.4 0.6 164.2

2029:4 381.6 3.1 1.4 0.6 163.4

2030:1 391.0 3.1 1.4 0.6 167.0

2030:2 389.7 3.0 1.4 0.6 165.5

2030:3 394.6 3.4 1.4 0.6 166.4

2030:4 394.8 3.5 1.4 0.6 165.8 1 Whole Economy 2 Average Earnings 3 Wholly unemployed excluding school leavers as percentage of employed and unemployed, self employed and HM Forces 4 Wage rate deflated by CPI

38

Estimates and Projections of the Gross Domestic Product1 (£ Million 1990 Prices)

Expenditure

Index

£ Million

‘90 prices

Non-Durable

Consumption2

Private Sector

Gross Investment

Expenditure3

Public

Authority

Expenditure4

Net Exports5 AFC

2017 163.3 781822.0 441518.3 300818.9 200522.0 -60310.0 100727.2

2018 165.5 792730.9 445869.9 310567.1 201139.6 -41308.9 123536.8

2019 167.9 804080.6 451574.6 303406.1 204769.4 -52338.8 103330.7

2020 171.6 821901.4 457805.7 295939.3 208259.4 -31024.2 109078.7

2021 175.8 842092.2 464217.0 306057.6 212609.2 -27895.8 112896.1

2022 179.6 859862.8 470251.9 312554.3 216879.4 -24439.4 115383.2

2023 183.3 878050.3 476836.0 318913.4 220460.7 -20123.5 118036.3

2024 187.4 897649.0 484228.1 328757.6 224535.1 -18987.7 120884.0

2025 191.5 917297.0 491735.1 339803.8 228820.5 -19322.9 123739.4

2026 195.8 937486.6 498619.4 352205.6 233213.3 -19876.1 126675.7

2027 200.2 958735.8 506225.6 364333.7 237536.5 -19593.3 129766.8

2028 204.7 980647.8 513313.2 377640.3 241975.0 -19323.3 132957.5

2029 209.4 1002924.6 521142.6 389278.8 246455.4 -17729.3 136222.8

2030 214.1 1025541.0 528565.5 402908.4 250990.1 -17388.9 139534.0

2018/17 1.4 1.0 3.2 0.3 22.6

2019/18 1.5 1.3 -1.9 1.8 -18.0

2020/19 2.2 1.4 -2.2 1.7 6.4

2021/20 2.5 1.4 3.4 2.1 2.8

2022/21 2.1 1.3 2.1 2.0 2.2

2023/22 2.1 1.4 2.0 1.7 2.3

2024/23 2.2 1.6 3.1 1.8 2.4

2025/24 2.2 1.6 3.3 1.9 2.4

2026/25 2.2 1.4 3.6 1.9 2.4

2027/26 2.3 1.5 3.4 1.9 2.4

2028/27 2.3 1.4 3.7 1.9 2.5

2029/28 2.3 1.5 3.1 1.9 2.5

2030/29 2.3 1.4 3.5 1.8 2.4

2018:1 164.4 196809.2 110809.6 73337.2 51591.3 -10814.1 28114.8

2018:2 165.1 197627.5 111248.1 78845.0 49253.6 -10094.0 31625.2

2018:3 166.1 198830.2 112094.9 76125.8 49822.6 -10001.3 29211.8

2018:4 166.6 199464.1 111717.3 82259.2 50472.1 -10399.5 34585.0

2019:1 167.6 200618.5 111589.5 85538.7 52691.8 -27678.5 21523.0

2019:2 167.5 200587.1 113663.3 74489.6 50902.6 -13829.9 24638.5

2019:3 167.9 201017.3 113170.0 70150.4 50255.7 -5067.0 27491.8

2019:4 168.6 201857.7 113151.8 73227.4 50919.3 -5763.4 29677.4

2020:1 170.9 204554.6 113061.1 79222.4 53408.8 -14598.6 26539.1

2020:2 171.1 204822.1 115141.5 71174.1 51768.6 -6977.3 26284.8