european nations needing official financial assistance as a result of the crisis national and...

TRANSCRIPT

European Nations Needing Official Financial Assistance as a Result of the Crisis

National and Regional Policy Failures & Quality of the International Response

UNDP Regional Policy Roundtable in Eastern Europe & Central Asiaon “Economic Crisis Responses from a Governance Perspective”

Jolly Alon Hotel, Chisinau, Republic of Moldova, 07 July 2010

Professor CHRISTOS HADJIEMMANUILUniversity of Piraeus & London School of Economics

From global to national: the crises of 2009

• An “American” crisis revealing global macroeconomic & financial problems– American consumption / growth fuelled with Asian savings / credit flows– Easy money and asset bubbles– Bursting of the bubble & the drying up of international interbank markets

• European banks also affected by lack of transparency / shift in risk perceptions

• From financial crisis to real depression:– European national crises of 2008-09:

(e.g. Britain, PIIGS, Baltics, Hungary, Ukraine, Romania)• Single cause or the expression of diverse national problems?

Greece & the failure of fiscal discipline

• Oct. 2009: self-reporting by Greece (for the 2nd time!) of severe irregularities in national accounting; this came after a long series of problems, reservations and corrections of Greek fiscal data

• Greece as a serial violator of European fiscal norms• A public debt crisis threatening to engulf all Southern Europe – and

more• Is fiscal irresponsibility the problem? Assuming that it offers an

explanation of the Greek crisis, can it explain other cases? • Is the Greek experience of any value to CEE & CIS countries?

A failure of national self-discipline?

• “Unsustainable levels of debt” / lack of “fiscal space” as a common post-Greek-crisis explanation of public debt refinancing difficulties / inability to tap banking markets

• PIIGS v the rest: “profligacy” of the former, “rectitude” of the latter– Is this a true explanation of what went wrong?– Or simply a convenient “just-so” story, unsupported by evidence?

• PIIGS: Family resemblances & critical governance differences– Not all PIIGS were fiscally profligate

• Inapplicability of the theory to CEE countries• Is there a common thread?

– The “good”, the “bad” and the ugly truth: the world of easy money, the asymmetrical impact of European monetary policy & the build-up of current account imbalances

Eurozone fiscal performance

• European fiscal rules (EDP as operationalised by the SGP) require annual deficits of below 3% of GDP in normal times, and total debt-to-GDP ratios that stay below or, if starting from higher levels, move towards the benchmark of 60%

• For Eurozone as a whole, until 2007 deficits stayed below 3% of Eurozone GDP on all but one occasion

• However, violations of the fiscal rules took place with great frequency at the national level: Greece, Italy & Portugal, together with Germany and France were major sinners; Ireland and Spain were paragons of rectitude

• Fiscal coordination & rule enforcement by the Commission and the Eurogroup has been particularly weak

Eurozone country performance, 2000-07

(Baldwin & Gros, 2010)

Looking beyond fiscal considerations:the broader picture

• Differential impact of common nominal interest rates / free availability of credit

– Northern export economies (in particular, Germany after the reunification spree / subsequent sustained effort to regain competitiveness; but also France, Austria, Netherlands, Belgium and Luxembourg) experienced lower than average growth and inflation, with positive real interest rates

– The PIIGS periphery experienced rapid growth and higher than average inflation, fuelled by low or negative real interest rates

• Financial flows & imbalances: the bank lending / current account nexus– The emergence of pan-European (or, at least, regional) banking groups– Private borrowing in periphery was supported by foreign banking groups’

home deposits or wholesale funds– Also: home-grown credit expansion, based on pan-European interbank

borrowing: Irish, French, Spanish and Italian banking groups increased aggressively their lending

– Bank lending fuelled asset bubbles in certain economies: real estate booms in Ireland, Latvia, Spain

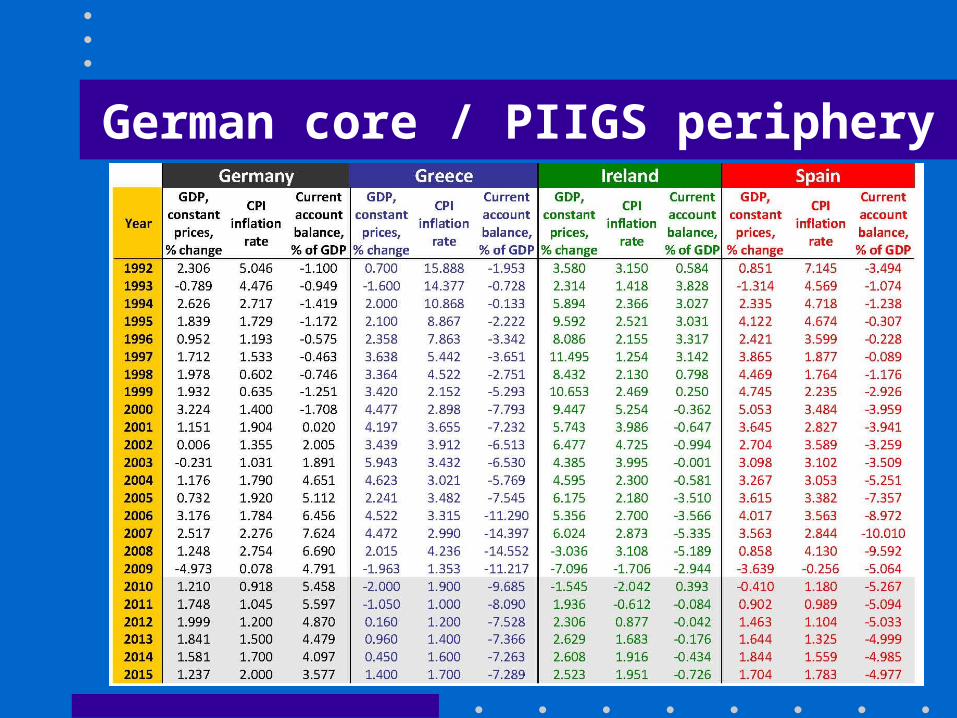

German core / PIIGS periphery

The build-up of European imbalances(Four figures from Baldwin & Gros, 2010)

Competitiveness & long-term imbalances• The asymmetric development of output / competitiveness has resulted

in massive current account imbalances• Structural reform (Lisbon) agenda failed to promote convergence; to the

extent that it was meaningful, was implemented in totally random manner

• If in the Greek case the problem is primarily fiscal, in other countries it is primarily linked to the current account and the financing of local private-sector consumption & overinvestment in non-tradeables (e.g. houses) with foreign loans

– This applies to some CEE countries as much as to the Eurozone periphery• Interconnectedness: the exposure to periphery economies turns the

debt crisis of the periphery into a banking crisis at the center– The European equivalent of investing in toxic assets– The crisis is more symmetric / universal than Germans leaders would want

you to believe

Intra-Eurozone banking exposure: core countries’ banks’ holdings of PIIGS debt

(Baldwin & Gros, 2010)

Failure of European financial regulation (1)

• Failure of the banking sector to foresee the impending crisis / act prudently

– Massive increase in private lending to the periphery, often in the form of financing of non-tradeable sectors

– Involvement in asset bubbles– Interconnectedness (primarily through exposure to those countries that

were more perfectly integrated in the European banking system!)• Suspicion of financial markets amongst Western European political elite

is not accompanied by any coherent regulatory attempt to “correct” their failures

• Misreading of the true problem: theory that banking regulation is “left to national governments, with only loose coordination”

Failure of European financial regulation (2)• Banking regulation focused on what were, in all likelihood, the wrong

questions – Capital adequacy, based on increasingly “market based” measurements of

risk – Incorporation of credit ratings in private and public decision-making

processes– Promotion of internationalisation, without concern for the systemic effects,

especially in relation to concentrated country/currency risk – Excessive reliance on active asset and liability management (especially in the

form of access to pan-European wholesale markets) with no concern for liquidity risks, maturity mismatches & imbalances in national savings / loan-to-deposit ratios

– Extensive currency mismatches, e.g. in Romania, Baltics– Absence of concern for the rapid growth of bank indebtedness / rapid

increase in the total debt burden (including public, consumer & business debts) of particular nations, or for total indebtedness to foreign lenders

Did the crisis activate a public debt trap?

• Crisis and the explosion in deficit levels– The recession sets in motion the automatic stabilizers – Potential recourse to discretionary fiscal stimuli, over and above the

automatic fall in revenue– In current crisis, additional fiscal costs for bank support packages and the

transformation of private debt into public guarantees / debt– End result: rapid worsening of the fiscal situation

• Does this imply lack of sustainability? Not necessarily – Fiscal sustainability as a function of privately set risk-premia– Why did banks and credit rating agencies only now realized the lack of “fiscal

space”? • Who should pay for the subsidization of banks through the blanket

safety-nets offered in Oct 2008?

Failure of European crisis management• Limits of European legalism

– The EU “community of law”, used to operate by legislative initiative, has proved unable to take rapid, decisive, discretionary action in the face of crisis

– Legalism, bureaucratic groupthink, policy inertia, abhorrence of discretionary decision making, low capacity for joint action

• Evident ineffectuality of the standing fiscal rules / enforcement practice• Inability to modulate / recalibrate economic policy stance over the

economic cycle: too little too late • Lack of coherent analysis / comprehensive strategy for dealing with crisis• Gaps in institutional design: no attempt to establish “fire brigade”

(economic governance, bank resolution mechanisms) in good times• Half-baked pronouncements in relation to Greek rescue / EFSF• Complete lack of concern for correction of structural trade imbalances:

“It’s the PIIGS’ problem” – Increasingly nationalistic rhetoric in the core countries, esp. Germany

IMF lending arrangements to the region(as of 31 May 2010, in thousands of SDRs)

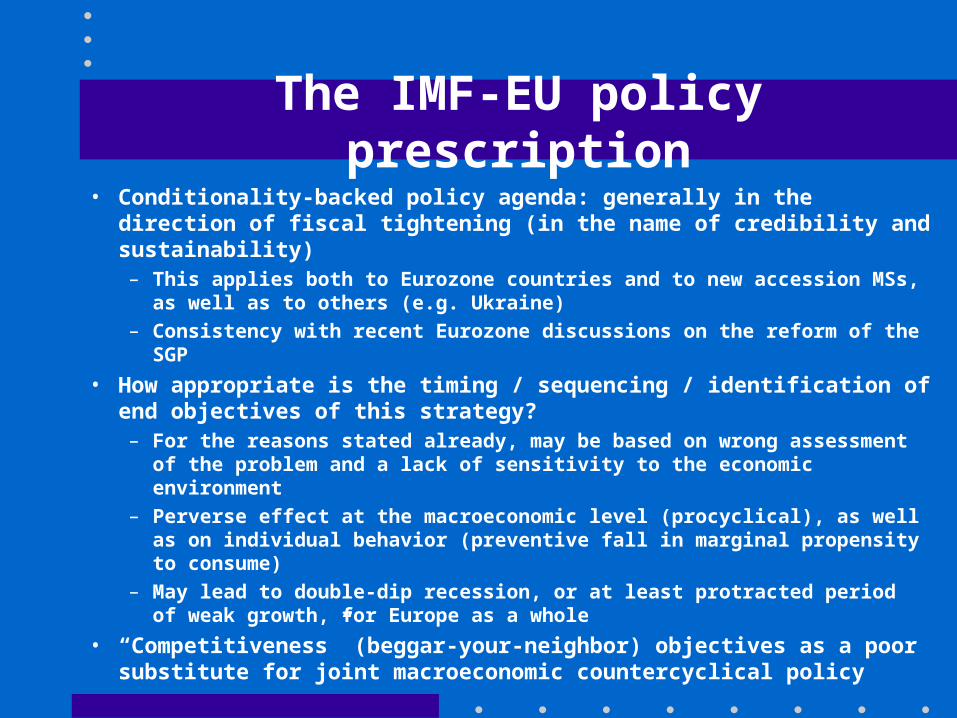

The IMF-EU policy prescription• Conditionality-backed policy agenda: generally in the direction of fiscal

tightening (in the name of credibility and sustainability) – This applies both to Eurozone countries and to new accession MSs, as well as

to others (e.g. Ukraine) – Consistency with recent Eurozone discussions on the reform of the SGP

• How appropriate is the timing / sequencing / identification of end objectives of this strategy?

– For the reasons stated already, may be based on wrong assessment of the problem and a lack of sensitivity to the economic environment

– Perverse effect at the macroeconomic level (procyclical), as well as on individual behavior (preventive fall in marginal propensity to consume)

– May lead to double-dip recession, or at least protracted period of weak growth, for Europe as a whole

• “Competitiveness” (beggar-your-neighbor) objectives as a poor substitute for joint macroeconomic countercyclical policy

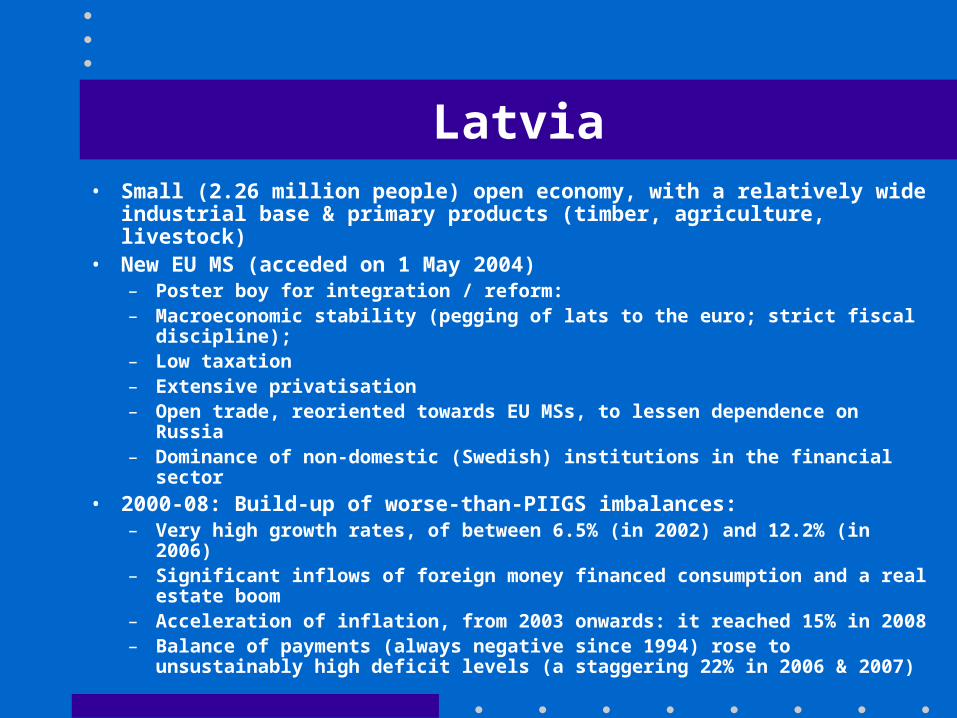

Latvia• Small (2.26 million people) open economy, with a relatively wide

industrial base & primary products (timber, agriculture, livestock)• New EU MS (acceded on 1 May 2004)

– Poster boy for integration / reform: – Macroeconomic stability (pegging of lats to the euro; strict fiscal discipline);

– Low taxation – Extensive privatisation– Open trade, reoriented towards EU MSs, to lessen dependence on Russia – Dominance of non-domestic (Swedish) institutions in the financial sector

• 2000-08: Build-up of worse-than-PIIGS imbalances:– Very high growth rates, of between 6.5% (in 2002) and 12.2% (in 2006)– Significant inflows of foreign money financed consumption and a real estate

boom– Acceleration of inflation, from 2003 onwards: it reached 15% in 2008– Balance of payments (always negative since 1994) rose to unsustainably

high deficit levels (a staggering 22% in 2006 & 2007)

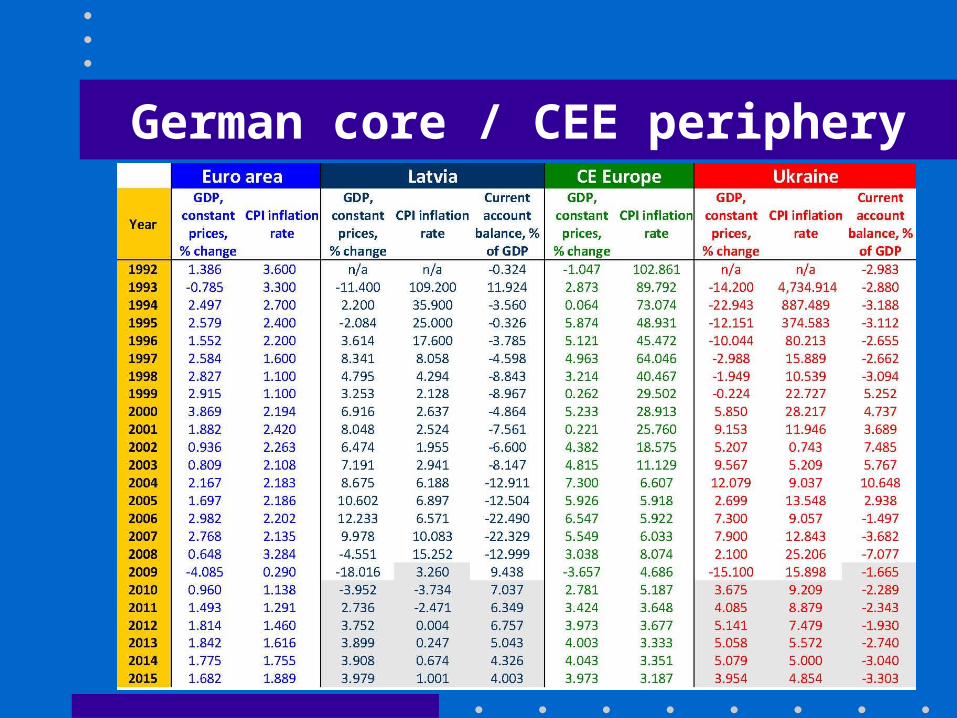

German core / CEE periphery

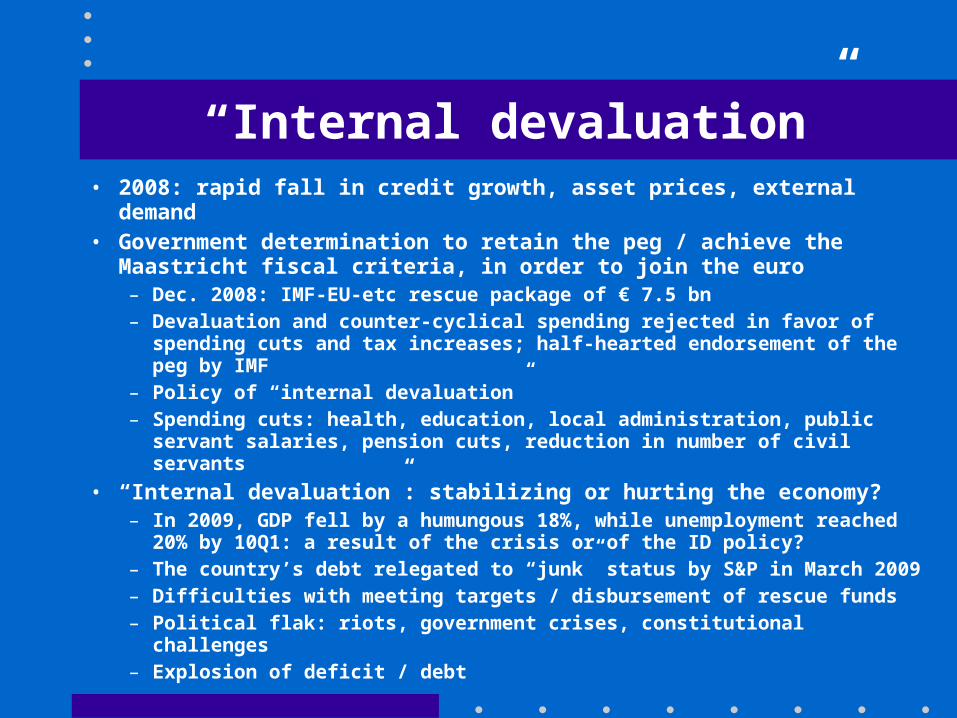

“Internal devaluation”• 2008: rapid fall in credit growth, asset prices, external demand• Government determination to retain the peg / achieve the Maastricht

fiscal criteria, in order to join the euro– Dec. 2008: IMF-EU-etc rescue package of € 7.5 bn– Devaluation and counter-cyclical spending rejected in favor of spending cuts

and tax increases; half-hearted endorsement of the peg by IMF– Policy of “internal devaluation”– Spending cuts: health, education, local administration, public servant

salaries, pension cuts, reduction in number of civil servants• “Internal devaluation”: stabilizing or hurting the economy?

– In 2009, GDP fell by a humungous 18%, while unemployment reached 20% by 10Q1: a result of the crisis or of the ID policy?

– The country’s debt relegated to “junk” status by S&P in March 2009– Difficulties with meeting targets / disbursement of rescue funds– Political flak: riots, government crises, constitutional challenges– Explosion of deficit / debt

Development of Latvian GDP & public debt(Convergence Programme of the Republic of Latvia, 2009-2012)

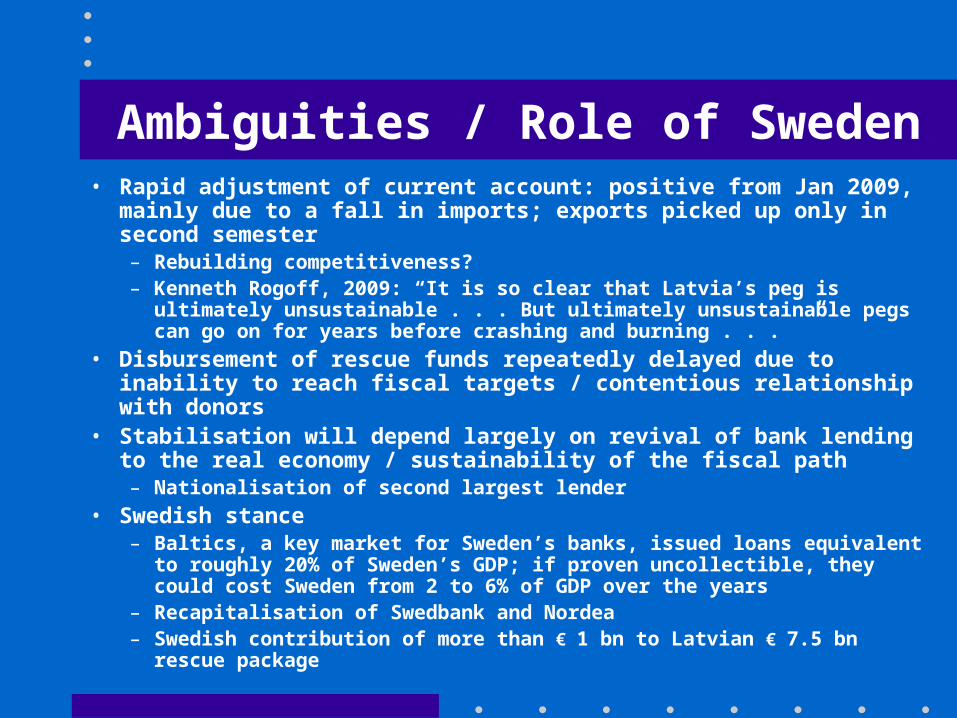

Ambiguities / Role of Sweden• Rapid adjustment of current account: positive from Jan 2009, mainly

due to a fall in imports; exports picked up only in second semester– Rebuilding competitiveness? – Kenneth Rogoff, 2009: “It is so clear that Latvia’s peg is ultimately

unsustainable . . . But ultimately unsustainable pegs can go on for years before crashing and burning . . . ”

• Disbursement of rescue funds repeatedly delayed due to inability to reach fiscal targets / contentious relationship with donors

• Stabilisation will depend largely on revival of bank lending to the real economy / sustainability of the fiscal path

– Nationalisation of second largest lender• Swedish stance

– Baltics, a key market for Sweden’s banks, issued loans equivalent to roughly 20% of Sweden’s GDP; if proven uncollectible, they could cost Sweden from 2 to 6% of GDP over the years

– Recapitalisation of Swedbank and Nordea – Swedish contribution of more than € 1 bn to Latvian € 7.5 bn rescue package

Harmful biases in IMF conditionality? • IMF criticised for systematically imposing procyclical, contractionary

conditions on CEE countries (CEPR, “Cases of Hungary, Latvia & Ukraine”)

– National economic policy mistakes increased vulnerability to external shocks– However, responses to the downturn caused further harm– Big chunk of rescue packages used to bail out western European banks – Latvia: pro-cyclical fiscal policy and decision to maintain the peg of lats – Hungary: pro-cyclical fiscal policy accompanied by pro-cyclical monetary

policy; IMF forecasts misjudged resilience of the financial sector, severity of contraction,

– Ukraine: decline in price of steel, rise in price of imported natural gas, reversal of capital flows; IMF prescribed fiscal retrenchment (full balance, later relaxed to a deficit of 4.0% of GDP) and a tight monetary policy, even though Ukraine’s accumulated public debt is very low (just 10.6 of GDP)

• Further research: procyclical bias in 31 of 41 current IMF arrangements• In some cases, IMF relied on excessively optimistic growth forecasts • Occasionally, loosened conditionality loosened once economic

performance proved to be much worse than originally anticipated

Failure of global macro coordination• Germany: a fiscal hawk

– Fundamental belief in sound public finances – Does not recognize that supporting its trading partners is essential– Negative political climate, punitive mindset of German public opinion (and

segments of the political and central banking leadership)– No concern for global economic imbalances, on the theory that the Eurozone

has a balanced current account • US: concern about fragility of global recovery

– Fear that premature rush to fiscal austerity in Europe might trigger double-dip recession

– Would like to see further fiscal stimuli• Global macroeconomic coordination at G20 has lost momentum

– G20 communiqué: a paper over of widely diverging viewpoints– Lack of convergence on substantive issues or agreement on concrete actions – Lip service to both debt sustainability and economic growth; but no

indication of how to proceed– Emphasis on a staggered approach to fiscal consolidation

“Slash & burn” fiscal retrenchment: institutional/governance implications

• Lack of legitimacy? – Rescue package conditionality often negotiated behind closed doors, based

on the big macro picture, without regard for local interests, and without proper consultation or in-depth discussion

• Political implications– Social unrest– Potential collapse of social dialogue – Political crises and realignments

• Administrative implications– Cost-cutting in public sector: efficiency improving or shift to bare essentials? – Undermining of governance capacity (viz. the “hollowed out” state, referred

to yesterday by Tiina Randma-Liiv)• Erosion of rule of law

– Tensions between national institutions & international/EU commitments– Government decisionism v. constitutional court challenges

The way forward (1)

• Need for greater commitment to structural reform agendas at the national level, to empower productive forces / enable the utilization of competitive advantages

• Wage-cutting measures cannot on their own restore long-term competitiveness; the same applies to “internal devaluation” policies

– They can only secure current account balance through the dampening of demand – but only at great cost in terms of economic and social dislocation

• Need to heed the lessons of the 1930s: do not try to restore fiscal discipline in the middle of a crisis; instead, go for joint expansionary macroeconomic policies, until activity has been restored to normal levels (this is also a boon to psychology)

Percent changes in real GDP since 07Q4

A way forward (2)

• Need for early financial sector rehabilitation / bank resolution, including through meaningful stress tests, as well asthe recognition of losses on portfolios of periphery assets

• Need for decisive European policy stances, to restore confidence in governability (rather than public debt sustainability):

– Less bickering – No more half-hearted pronouncements– Effort to increase capacity for discretionary policy coordination

• Need for more balanced approaches to the correction of economic imbalances: an imbalance characterizes the relationship of two sides

• For non-Eurozone members, should we revisit the possibility of devaluation?

Thank you for your attention

CHRISTOS HADJIEMMANUILProfessor of Monetary and Financial Institutions, University of Piraeus

Visiting Professor of Law, London School of EconomicsAttorney at law, Athens Bar Association

e-mail: [email protected]: +30 6936 161770