establishing good billing practices to avoid collection headaches

TRANSCRIPT

Establishing Good Billing Practices to Avoid Collection HeadachesIn this chapter:

•Getting prompt payment through effective billing practices

•Keeping your billing practices organized

•Training employees on billing procedures

Chapter 4

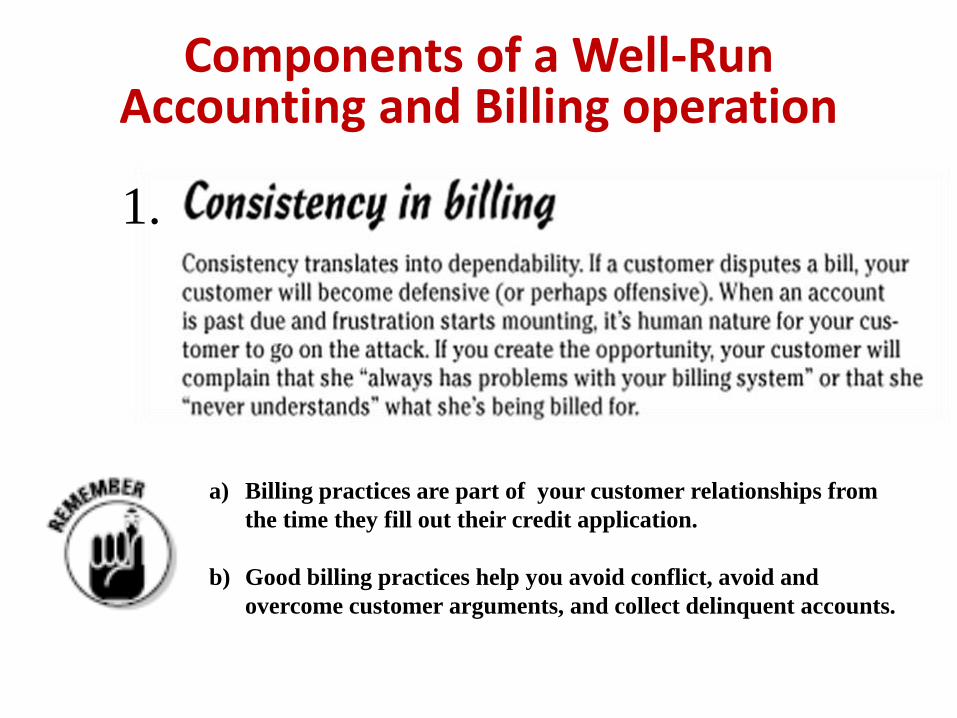

1.

a) Billing practices are part of your customer relationships from

the time they fill out their credit application.

b) Good billing practices help you avoid conflict, avoid and

overcome customer arguments, and collect delinquent accounts.

Components of a Well-RunAccounting and Billing operation

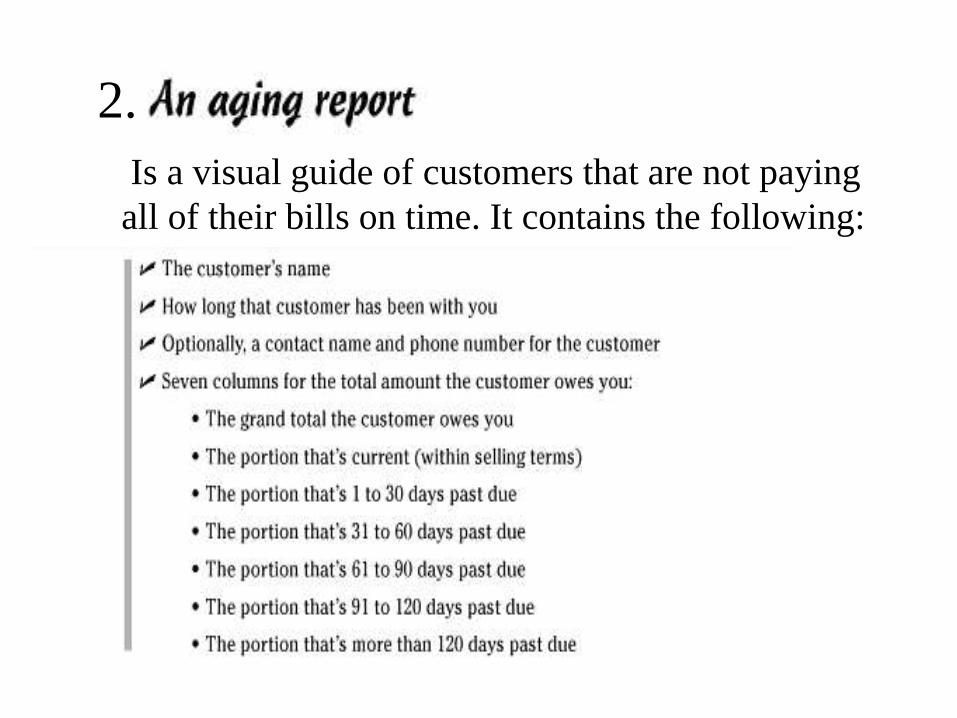

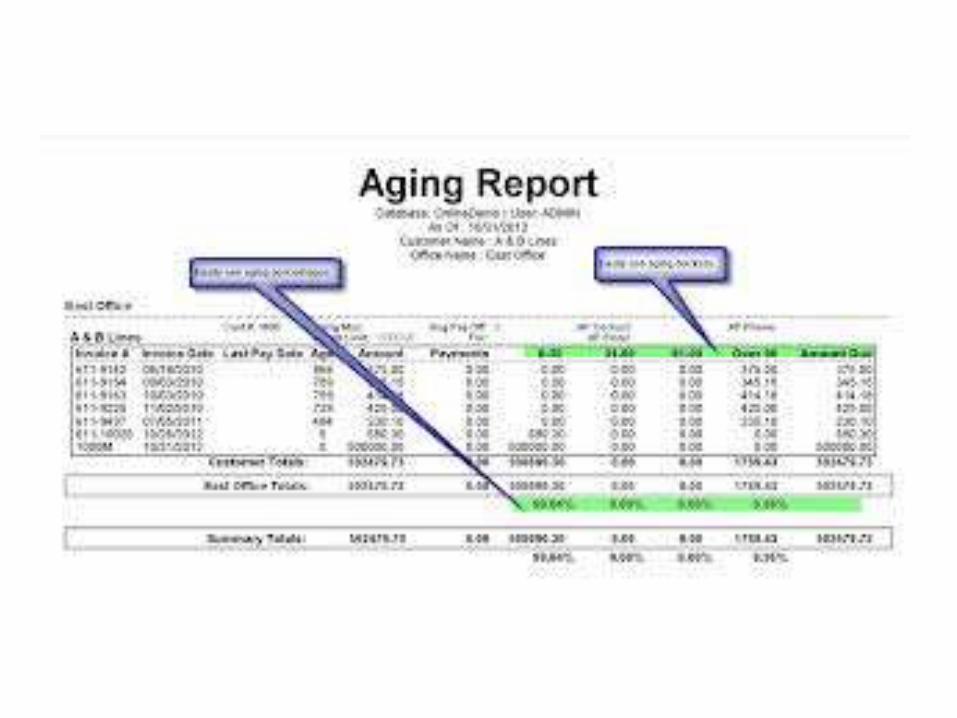

2.

Is a visual guide of customers that are not paying

all of their bills on time. It contains the following:

3. Interest charges for late payments

• Charging interest on delinquent accounts, can

help prompt your customer to want to pay your

bills before interest starts to accrue.

• You should disclose interest charges in your

purchase contracts or credit applications.

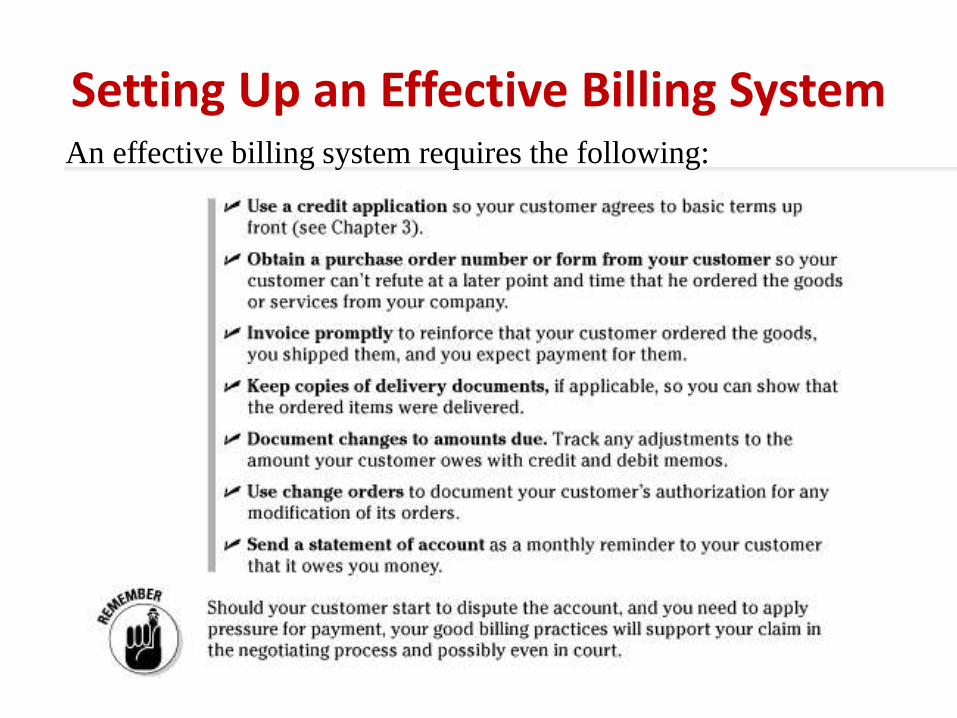

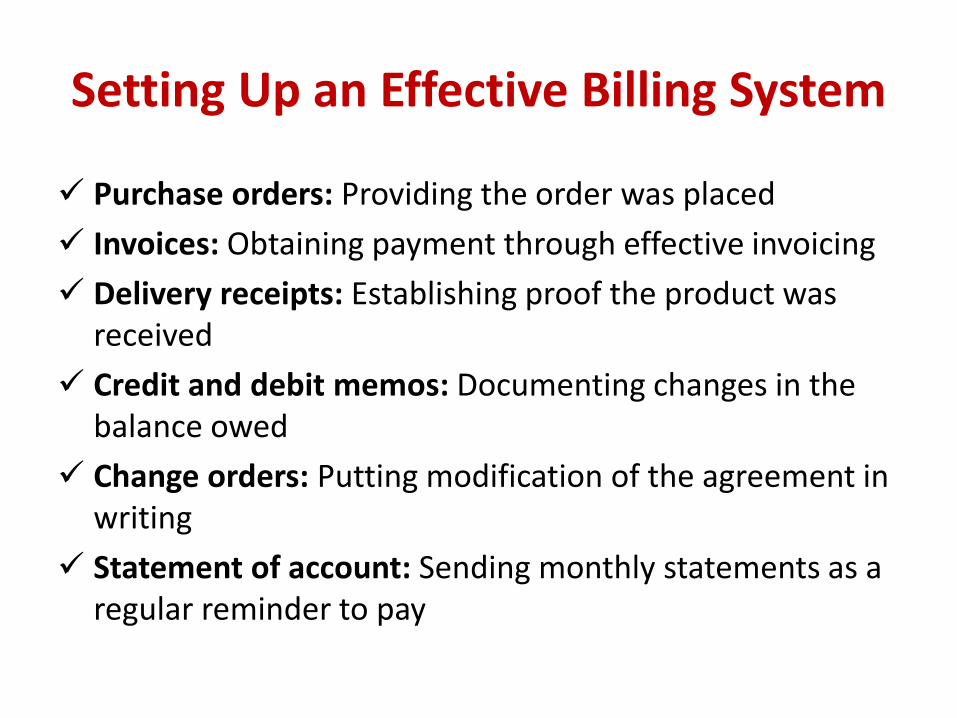

Setting Up an Effective Billing SystemAn effective billing system requires the following:

Purchase orders: Providing the order was placed

Invoices: Obtaining payment through effective invoicing

Delivery receipts: Establishing proof the product was received

Credit and debit memos: Documenting changes in the balance owed

Change orders: Putting modification of the agreement in writing

Statement of account: Sending monthly statements as a regular reminder to pay

Setting Up an Effective Billing System

Purchase Orders are documents that your customer ordered your product or service.

Invoices are the bill for the product or servicesrendered by your company to your customer.

Delivery receipts are provided by carriers such as trucking companies that deliver your goods to your customers.

Setting Up an Effective Billing System

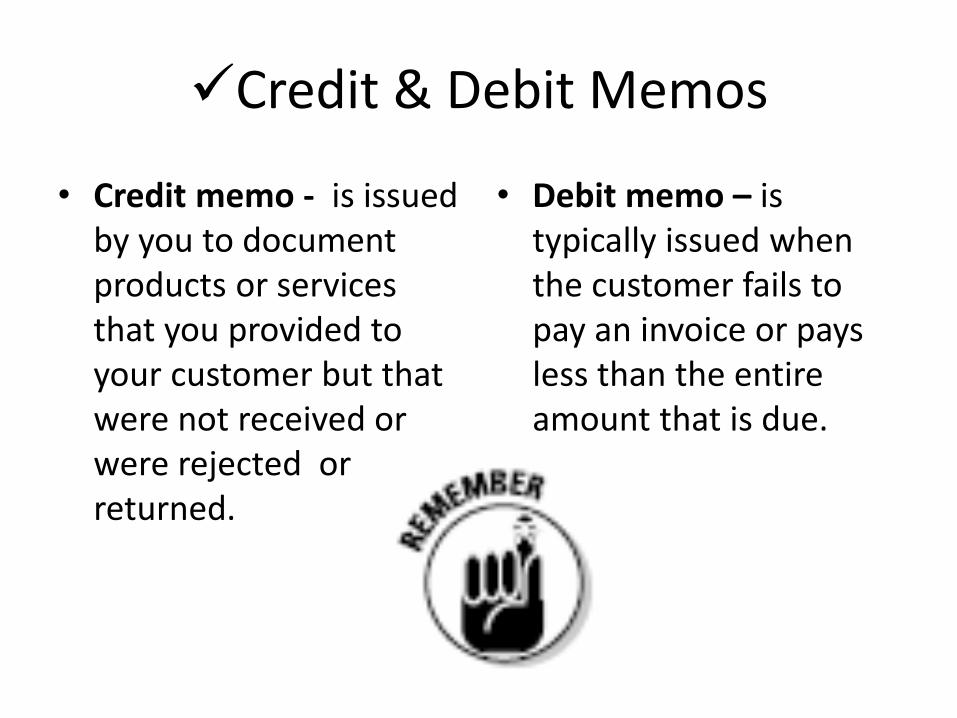

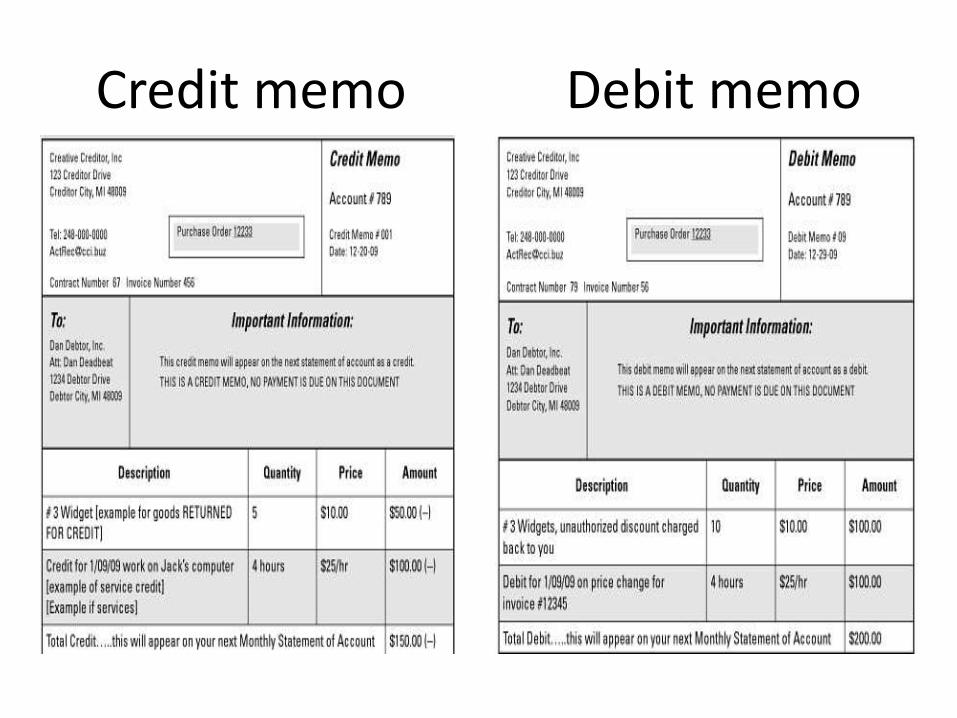

Credit & Debit Memos

• Credit memo - is issued by you to document products or services that you provided to your customer but that were not received or were rejected or returned.

• Debit memo – is typically issued when the customer fails to pay an invoice or pays less than the entire amount that is due.

Credit memo Debit memo

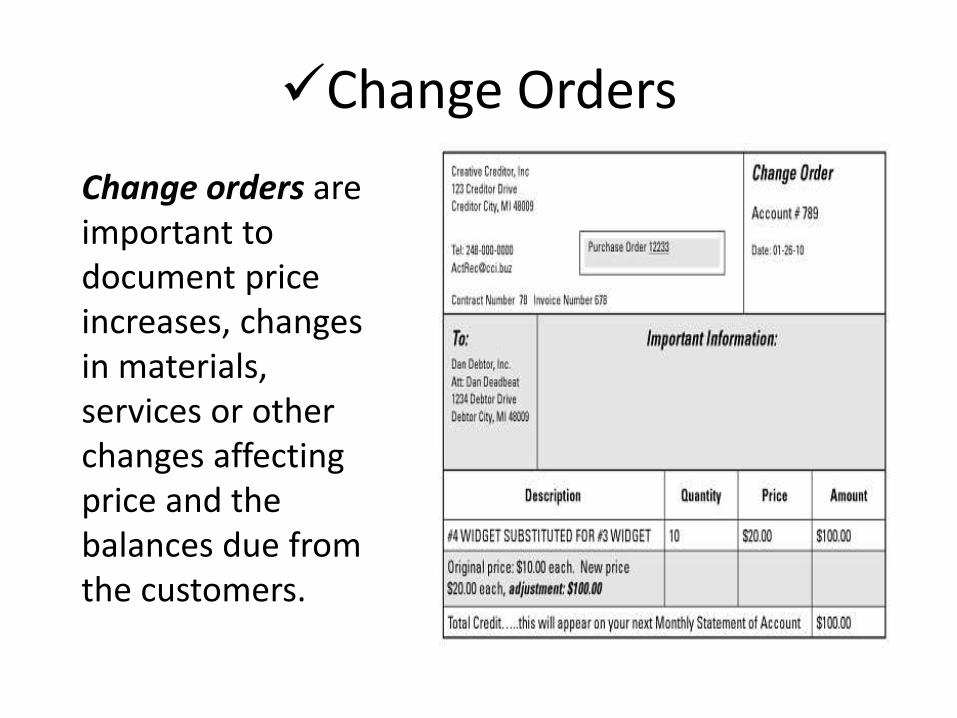

Change Orders

Change orders are important to document price increases, changes in materials, services or other changes affecting price and the balances due from the customers.

• A customer’s statement of account is a running ledger of the customers credit transactions, including all payments, payments, debits and credits.

• It is a summary of your transactions with your customers over the course of billing period (usually in 30 days).

Statements of Account

“How can I pay you, when you haven’t even billed me yet?”

“I never pay without a bill”

“I need something in writing”

Creating an effective billing system

Maintaining precise recordsMaking sure your forms don’t conflict with each other

Keep key records, like customer checks

Sidestepping billing discrepancies by putting everything in writing

Keeping Your Bills Accurate

Getting Bad Accounts Off the Books:You Gotta Know When to Fold ‘Em

• If the customer has been turned over for collection, the collection agencies make demands for payment using their own letters to pay the debt.

• If a debtor files for bankruptcy and the debt is being handled by the bankruptcy court, you may be in violation of the bankruptcy law if you still send bills and notices to the debtor.

Training Your Staff in Billing Matters

Inputting data accurately

Using the correct forms

Respecting confidential and sensitive data

Spotting and Reacting to Changes in Habit

In this chapter:

•Setting controls to maintain cash flow

•Avoiding payment slowdowns

•Dealing with customers’ excuses for slow payment

•Handling changes in customers’ payment behavior

•Tracking down elusive customers

Chapter 5

General Controls for Keeping Your Cash Flow Steady

Be aware of slowing payments

Be ready to respond to customers bad habits

Be considerate, yet firm

Be prepared to reduce a line of credit, require (COD) cash on credit or cut off deliveries or services

Be honest in your

communications

Tailoring Your Strategy: A Short Leash for New Customers

A. Setting tighter controls for newer customersPut the customer on a short leash, such as a 15-day watch

list, so you detect a slowdown in payments almost immediately.

Be ready to turn off the credit faucet: No credit if no payment.

Hold up further deliveries of your goods or services until the customer pay his late invoices.

Get additional assurance of payment, such as liens, guarantees, and promissory notes.

Tailoring Your Strategy: A Short Leash for New Customers (continued)

B. Helping out timely payersExtending their payment terms ( for example , payments

due in 45 days instead of 30).

Forgiving some service charges on the account

Offering a discount for early payment

Spotting Trends and Patterns of Payment

Keeping an eye (and ear) on your customer

Monitoring industry trends and bracing for slowdowns

Speeding up slow payers

• Starting with a letter

• Following up with a phone call

Reacting to customers’ excuses, bad habits, and broken promises

Spotting Dubious ChangesChanges in ownership of a client business

Changes of address or phone number

Changes in order volume• A decline in orders often precedes a decline in payment

diligence.

• An unexpected increase in orders

Changes in financial situation

Changes in customer attitude

Changes your customer’s understanding of purchase or credit terms

Dealing with Elusive Customer1) Breaking free from voice mail jail

2) Detouring around the disconnected phone Showing up on the debtor’s doorstep

E-mailing

Faxing

Texting

Elusion is a definite red flag. Put the customer at the top of your list for monitoring payments and exercise extreme caution when considering any further extensions of credit.

Dealing with Elusive Customer

When Your Late-Paying Customer Turns into Your Debtor

In this chapter:

•Creating a sense of urgency for payments

•Using frequent payment reminders effectively

•Establishing a good paper trail

Chapter 7

Creating an Atmosphere of UrgencyInterest and penalties

Attention getting words and “big red letters”

Frequent reminders

Multiple of modes of contact

Making a phone call

Communicating Effective Reminders to Pay

Writing effective collection letters

• Keep it short

• Use simple words, short sentences and paragraphs

• Customize the letter

• Demand payment by a specific date

Special concerns for consumer debtors

Still not paid? Escalating your approach

Customizing your notification approach

Don’t forget the power of a phone call

Documenting the File: Having Good Notes When You Need Them

Your customer’s entire credit file

Notes of phone calls made or received, along with dates and responses

Notes made by employees of your company

Copies of all follow-up statements

Copies of all demand letters and follow up correspondence

Documenting the File: Having Good Notes When You Need Them

1) The paper trail: How good records help you both in and out of court

2) Anticipating reactions: Playing devil’s advocate

3) Pursuing written admissions of the debt