essential learning for ctp candidates new york cash...

TRANSCRIPT

1

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

New York Cash Exchange: 2016Essential Learning for CTP CandidatesSession #3: Wed. Afternoon (6/01)

ETM4-Chapter 8:Introduction to Working Capital Management

ETM4-Chapter 9:Working Capital Metrics

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 1

Essentials of Treasury Management, 4th Ed. (ETM4) is published by the AFP which holds the copyright and all rights to the related materials.

As a prep course for the CTP exam, significant portions of these lectures are based on materials from the Essentials text.

Overview of Chapter 8 Overview of Working Capital The Working Capital Cash

Conversion Cycle (CCC) How Changes in Current

Accounts Impact External Financing

Working Capital Investment and Financing Strategies

Management of Credit and A/R Management of Inventory Management of A/P Multinational Working Capital

Management Tools

2© 2016 - The Treasury Academy, Inc. - All Rights Reserved

Overview of Working CapitalWorking capital can be obtained by: Collection cash flow from operations

Increasing debt

Selling assets and investments

Selling equity

And it can be reduced by: Using cash flow in operations

Repaying debt

Purchasing assets and investments

Paying dividends and buying back stock/equity

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 3

2

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

Cash Conversion Cycle

Build Inventory

Provide/Sell Services & Products

Collect Revenues (A/R)

Purchase Supplies, Facilities, Etc.

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 4

Borrow orLiquidate

Investments

Invest orPay Down

Borrowings

Operating Cash Flows

© 2016 - The Treasury Academy, Inc. - All Rights Reserved

CashInflows

CashInflows

CashInflows

Concentration Account

ConcentrationFlows

ConcentrationFlows

Cash Outflows

Cash Outflows

Cash Outflows

FundingFlows

FundingFlows

Short-Term Investments

Short-Term Borrowing

LiquidityMgmt Flows

LiquidityMgmt Flows

5

Purchase-to-Pay Cycle

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 6

Source: ETM4 - © AFP

3

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

Focus of Treasury on Cash Flow Timeline

Treasury focus is on the payment portion of the cycle

Calculation: Float Neutral Calculation◦ TD = total days difference in payment timing◦ r = Opportunity cost as an annual rate

© 2016 - The Treasury Academy, Inc. - All Rights Reserved

1Discount 1

r1 TD

365

7

Float Neutral Calculation Assume r = 12% and TD = 3 days

© 2016 - The Treasury Academy, Inc. - All Rights Reserved

1Discount 1

12%1 3

365

11 1 0.99901467

1.0009863

0.00098533

0.001 (Rounded) or 0.10%

If the buyer is allowed to take a discount of 0.10 %, they would be indifferent (in present value terms) between paying by check or by electronic transfer (a speedup of 3 days in loss of value)

8Source: ETM4 - © AFP

Group Exercise Working in your groups,

answer the following questions: What is the difference between

collection float and disbursement float?

What are the key components of each of these float concepts?

What is the most important component to manage for your company?

9© 2016 - The Treasury Academy, Inc. - All Rights Reserved

4

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

Collection/Disbursement Float

Components◦ Mail Float Mail Time

◦ Processing Float Deposit Preparation Time

◦ Availability Float Check Availability Time

◦ Clearing Float Check Clearing Time

Measurement of Float◦ Dollar-Days

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 10

The working capital cash conversion cycle(CCC)

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 11

Day 1 Day 30 Day 45 Day 80

PurchaseOf Materials

Payment ForMaterials

Sale ofProduct

CollectAccounts

Receivable

Days Inventory

Days Receivables

Days Payables

Cash Conversion Cycle

Source: ETM4 - © AFP

The Working Capital Cash Conversion Cycle (CCC)

◦ Days’ Inventory orInventory Conversion Period

◦ Days’ Receivables orReceivables Conversion Period

◦ Days’ Payables orPayables Conversion Period

◦ Calculating the CashConversion Cycle (CCC)

12© 2016 - The Treasury Academy, Inc. - All Rights Reserved

5

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

More on Cash Conversion Cycle (CCC)

Assume the following◦ Days’ Inventory = 45 days◦ Days’ Receivables = 35 days◦ Days’ Payables = 30 days◦ Then: CCC = 45 + 35 – 30 = 50 days

Now assume the company can reduce inventory and A/R, while extending payables◦ Days’ Inventory = 40 days◦ Days’ Receivables = 32 days◦ Days’ Payables = 33 days◦ Then New CCC = 40 + 32 – 33 = 39 days

Cash Turnover = 365 / CCC◦ At CCC = 50 days, Cash Turnover = 7.3 times◦ At CCC = 39 days, Cash Turnover = 9.4 times

13© 2016 - The Treasury Academy, Inc. - All Rights Reserved

CCC = Days’ Inventory + Days’ Receivables – Days’ Payables

Problems in “Managing” CCC Components

Potential lost sales

Production stoppages

Stretched payables

Foregone cost-saving trade discounts

Higher prices assessed by vendors on smaller orders or slow payments

Refusal to sell to weak customers

Excessive reliance on A/P rather than S/T bank credit

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 14

Working Capital Investment and Financing Strategies

15© 2016 - The Treasury Academy, Inc. - All Rights Reserved

AssetBreakdown

MaturityMatching

ConservativePolicy

AggressivePolicy

Fixed AssetsPermanent

Current AssetsFluctuating

Current Assets

Long-Term SourcesShort-Term

Sources

Long-Term SourcesS/T

Sources

Long-Term SourcesShort-Term

Sources

Selecting a Current Asset Investment Strategy◦ Restrictive current asset investment

◦ Relaxed current asset investment

Selecting a Current Asset Financing Strategy

Source: ETM4 - © AFP

6

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

Group Exercise Working in your groups,

answer the following questions: For the practitioners: What are some

of the key issues related the management and financing of working capital at your company?

For the bankers: What kinds of products/services to you offer to help your customers in this area?

16© 2016 - The Treasury Academy, Inc. - All Rights Reserved

Management of Credit and Accounts Receivable (A/R) Relationship Between Treasury and Credit Management

Trade Credit Policies

Billing and Collection Methods

Forms of Credit Extension

Cash Application

Considerations Pertaining to Terms of Sale

Financing Accounts Receivable (A/R)

Cross-Border Trade Management

Developments in Credit and Accounts Receivable (A/R)

Legislation Affecting on Credit and Collections in the U.S.

17© 2016 - The Treasury Academy, Inc. - All Rights Reserved

Relationship Between Treasury and Credit Management

Separate functions

Credit manager administers policies that establish credit standards, define terms of sale, approve credit sales, and set individual and aggregate credit limits

A/R is created once a sale is made and trade credit is extended

A/R management includes billingand processing payments,monitoring payment patterns, and collecting delinquent accounts

18© 2016 - The Treasury Academy, Inc. - All Rights Reserved 18

7

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

Credit Information Sources

Company must consider the type, quantity and cost of information when establishing a method for analyzing credit requests

Credit information is gathered in stages from both internal and external sources

At each stage, costs are weighedagainst expected benefits

Sources include:◦ Internal payment history◦ Financial statements◦ Trade references◦ Credit reports or ratings

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 19

The Five C’s of Credit

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 20

Character An intent or willingness to pay as evidenced by payment history

CapacityCurrent and future financial resources that can be committed to pay obligations

CapitalShort- and long-term financial resources to supplement insufficient cash flow for payments

CollateralAssets or guarantees available to secure an obligation if payment is not made

ConditionsGeneral economic environment and economic conditions for the customer and the seller

Quantitative Credit Analysis Most often used measures:◦ Liquidity and WC ratios◦ Debt management and

coverage ratios◦ Profitability measures

Consumer Credit Scoring Process 1. Differentiating risks2. FICO Score3. Set cutoff score4. Applying further analysis

where necessary

21© 2016 - The Treasury Academy, Inc. - All Rights Reserved

8

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

Group Exercise

Working in your groups,answer the following questions:

Why might quantitative credit scoring be less effective for B2B sales than it is for B2C sales?

What are some of the other factors that should be considered in B2B credit and sales?

22© 2016 - The Treasury Academy, Inc. - All Rights Reserved

Why Quantitative Credit Analysis is Not as Effective for B2B

The available databases are much smaller for B2B

The per-transaction exposure is usually much larger

Impact of one large default Difficult to obtain financial info

for some customers, especially for smaller, private companies

23© 2016 - The Treasury Academy, Inc. - All Rights Reserved

Billing and Collection Methods Major objective of collection

policy is to convert A/R into cash quickly while minimizing collection expense and bad debt losses

Effective A/R management includes reducing invoicing float as much as possible

Clear collection policies should be established and enforced

24© 2016 - The Treasury Academy, Inc. - All Rights Reserved

9

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

Credit & Payment Application

Forms of Credit Extension◦ Open account◦ Installment credit◦ Revolving credit◦ Letter of credit (L/C)

Offering Discounts◦ Evaluate costs

versus benefits Cash Application◦ Open item◦ Balance forward

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 25

Common Terms of Sale

Cash before delivery (CBD) Cash on delivery (COD) Cash terms Net terms Discount terms Monthly billing Draft/Bill of lading Seasonal dating Consignment

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 26

Financing Accounts Receivable

Borrow unsecured funds to support A/R

Pledge A/R as collateral for secured loan

Securitize receivables

Use captive finance subsidiary

Third-party financing

Card Payments

Factoring

Private-label financing

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 27

10

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

Financing A/R – Card Payments Advantages◦ No direct costs of running a credit department

◦ Seller doesn’t have to finance A/R

◦ Credit card issuer absorb debt losses

◦ Sales increased

◦ Payback more quickly

Disadvantages◦ Seller relinquishes control over credit decision

◦ Seller loses promotional opportunities

◦ Seller incurs discount costs and transaction fees.

◦ Maintenance expense

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 28

Elements of Basic Inventory Policy Inventory policy of most

companies includes elements such as:◦ Reasons for holding inventory◦ Types of inventory held◦ Levels of inventory◦ Obsolescence and Spoilage◦ Costs and benefits associated with

holding inventory◦ Financing of inventory

29© 2016 - The Treasury Academy, Inc. - All Rights Reserved

Management of Inventory

Management of Accounts Payable (A/P)

A/P is a major source of s-t financing for many companies

A/P manager’s primary responsibility is to verify incoming invoices and authorize payments –sometimes referred to as “vouchering”

Three-way Match Treasury & A/P Coordination◦ How & when invoices are paid◦ Reconciliation of cleared (paid) items

30© 2016 - The Treasury Academy, Inc. - All Rights Reserved

11

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

Disbursement System Considerations

Four Considerations◦ Information Access

◦ Fraud Prevention

◦ Relationship Maintenance with Payees

◦ Timing of Payments

Centralized vs. Decentralized

31© 2016 - The Treasury Academy, Inc. - All Rights Reserved

Three-Way Match

Purchase Order

ReceivingAdvice

Invoice

ApprovedVendorList ??

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 32

Considerations for Global Management of Working Capital

Global Working Capital Management Tools and Techniques

Multicurrency Accounts Netting Leading and Lagging Re-invoicing Center Internal Factoring In-House Banking Export Financing

© 2016 - The Treasury Academy, Inc. - All Rights Reserved33

12

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

Before Netting

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 34

Source: ETM4 - © AFP

With Multilateral Netting

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 35

Source: ETM4 - © AFP

Benefits/Costs of Netting System

Benefits◦ A reduction in the number of FX transactions and

cross-border wire transfers, and benefits from natural hedging

◦ More favorable FX rates due to the potential for larger FX trades resulting from consolidation

◦ Improved cash and currency exposure forecasting for both the subsidiary and the parent company as a result of the ability to preplan cross-border payments

Costs◦ Setup, administration and maintenance expenses

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 36

13

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

Leading and Lagging

Lagging• Executing cross-border

payments between subsidiaries behind the scheduled payment date

• Used when a subsidiary country’s currency is expected to appreciate relative to the parent company’s currency

Leading• Executing cross-border

payments between subsidiaries ahead of the scheduled payment date

• Used when a subsidiary country’s currency is expected to depreciate relative to the parent company’s currency

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 37

Re-invoicing Center Purpose

Buys goods from an exporting subsidiary

Resells the goods to an importing subsidiary

Company Owned Subsidiary

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 38

Source: ETM4 - © AFP

Before Re-invoicing

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 39

Source: ETM4 - © AFP

14

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

With Re-invoicing

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 40

Source: ETM4 - © AFP

Overview of Chapter 9 Topics Introduction Basic Financial Concepts Fundamental Working

Capital Metrics Calculation of the Cash

Conversion Cycle(CCC) Cash Discount Calculation Accounts Receivable(A/R)

Monitoring and Control Collections and

Concentration Calculation

© 2016 - The Treasury Academy, Inc. - All Rights Reserved41

Time Value of MoneyThe value of cash flow is determined by:

• Amount of the cash flows.• Appropriate interest rate.• At what future period the

cash flow is expected to occur.

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 42

15

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

Concept of Opportunity Cost

What is the appropriate rate to use for time value analysis?◦ Investors look to alternative investments in a

particular risk class to discover the best rate of return available

◦ By investing in one particular company or investment, the investor loses the opportunity to invest in other securities

◦ The firm must provide a return that equals the investors’ opportunity cost

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 43

Cost of Capital This refers to the permanent sources of

capital such as LT debt, preferred stock and common equity

All costs of capital should be determined on an after-tax basis

Equity costs are already on an after-tax basis, so only debt costs need to be adjusted for marginal income taxes

Concept of Weighted Average Cost of Capital (WACC)

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 44

Fundamental Working Capital Metrics

Current Ratio Quick Ratio Cash Flow to Total Debt Ratio Total Working Capital

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 45

16

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

Liquidity or Working CapitalCurrent Ratio

Measures the degree to which current obligations are covered by current

assets

Total Current AssetsCurrent Ratio =

Total Current Liabilities

$8,000= = 2.35

$3,400

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 46

Source: ETM4 - © AFP

Liquidity or Working Capital: Quick Ratio

Measures the degree to which a company’s current liabilities are covered by its most liquid current assets

(Cash) + (S-T Investments) + (A/R)Quick Ratio =

Total Current Liabilities

($1,500 + $1,300 + $1,700)= = 1.32

$3,400

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 47

Source: ETM4 - © AFP

Liquidity or Working Capital: Cash Flow to Total Debt Ratio

Measures ability to repay debt (a relatively low ratio indicates an inability to repay debt and can predict financial failure; a higher ratio would imply more safety)

(Net Income + Depreciation)CF to Total Debt Ratio =

Short-Term Debt + Long-Term Debt

($850 + $200) $1,050= = = 0.184

$1,800 + $3,900 $5,700

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 48

Source: ETM4 - © AFP

17

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

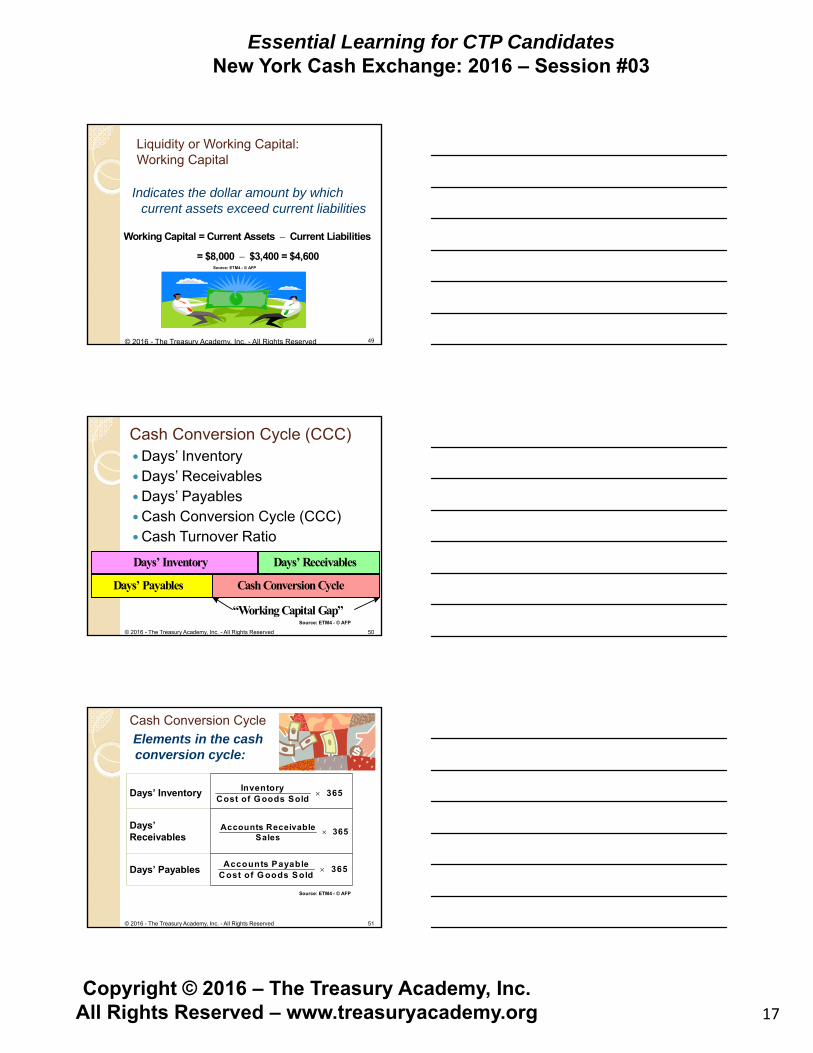

Liquidity or Working Capital: Working Capital

Indicates the dollar amount by which current assets exceed current liabilities

Working Capital = Current Assets Current Liabilities

= $8,000 $3,400 = $4,600

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 49

Source: ETM4 - © AFP

Cash Conversion Cycle (CCC)Days’ InventoryDays’ ReceivablesDays’ PayablesCash Conversion Cycle (CCC)Cash Turnover Ratio

Days’ Inventory Days’ Receivables

Days’ Payables Cash Conversion Cycle

“Working Capital Gap”

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 50

Source: ETM4 - © AFP

Cash Conversion Cycle

Elements in the cash conversion cycle:

Days’ Inventory

Days’ Receivables

Days’ Payables

Inventory365

Cost of G oods Sold

Accounts Receivable 365Sales

Accounts Payable365

Cost of G oods Sold

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 51

Source: ETM4 - © AFP

18

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

Cash Conversion Cycle

Elements in the cash conversion cycle:

Days’ Inventory

Days’ Receivables

Days’ Payables

Days 103.15 3659,200

2,600 365

COGS

Inv

Days 41.36 36515,000

1,700 365

Sales

A/R

Days 63.48 3659,200

1,600 365

COGS

A/P

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 52

Source: ETM4 - © AFP

Cash Conversion Cycle (CCC)

Calculates the time required to convert cash outflows (necessary to produce goods) into cash inflows (through the collection of accounts receivable)

Days 81.03 63.48 - 41.36 103.15

Pay. Days' - Rec. Days' Inv. Days' CCC

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 53

Cash Turnover RatioIf a company has a cash

conversion cycle of 81.03 days, how many cash conversion cycles does the company go through in a year (cash turnover)?

365 DaysCash Turnover =

Cash Conversion Cycle

365= 81.03 Days

= 4.5 Times© 2016 - The Treasury Academy, Inc. - All Rights Reserved 54

19

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

Cash Conversion Efficiency If the cash flow of a company is $550

and its revenue is $15,000, then its Cash Conversion Efficiency will be:

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 55

Cost of a Buyer Not Taking a Cash Discount (Terms: 2/10, net 30)

© 2016 - The Treasury Academy, Inc. - All Rights Reserved

D 365Discount Cost = 100 D N T

2 365= 100 2 30 10

2 365= = .0204 18.25 =.3723 or 37.23%98 20

WhereD = Discount percentage is 2%N = Net period is 30 daysT = Discount period is 10 days

The cost of not taking the discount can be compared with the organization’s opportunity cost to borrow short-term funds. If we assume a rate of 8% for this example, then borrowing cost would be less than the cost of not taking the discount – so the organization should borrow the funds and TAKE the discount.

56Source: ETM3 - © AFP

Group Exercise

Working in your groups,answer the following questions:

Under what circumstances would a buyer forego (not take) a cash discount if offered?

Why would a seller be willing to offer a cash discount in the first place?

57© 2016 - The Treasury Academy, Inc. - All Rights Reserved

20

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

When Should a Buyer Forgo an Offered Discount

Short-term investment rates above annualized discount rate

Buyer’s cost of short-term borrowing greater than annualized discount rate

Buyer can “stretch” payables enough to sufficiently lower annualized discount rate

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 58

Benefit to Seller of Offering a Cash Discount

© 2016 - The Treasury Academy, Inc. - All Rights Reserved

Disc Pmt

Total Amount of Full Pmt × 1 Disc RatePV

Annual Opp Cost1 Days in Disc Period ×

365

Disc Pmt

$100 1 .02 $98PV

.08 1 .00221 10

365

$98$97.78

1.0022

Assume credit terms of 2/10, net 30 and opp. cost = 8%

Present Value of Receiving Discounted Payment Amount

59Source: ETM3 - © AFP

Benefit to Seller of Offering a Cash Discount

© 2016 - The Treasury Academy, Inc. - All Rights Reserved

Assume credit terms of 2/10, net 30 and opp. cost = 8%

Present Value of Receiving Full Payment Amount

Full Pmt

Total Amount of Full PmtPV

Annual Opp Cost1 Days in Net Period ×

365

Full Pmt

$100 $100PV

.08 1 .00661 30

365

$100$99.34

1.0066

NPV = PVDay 10 – PVDay 30 = $97.78 – $99.34 = – $1.56

60Source: ETM4 © AFP

21

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

Accounts Receivable (A/R) Monitoring and Control

Days’ Sales Outstanding (DSO)

A/R Aging Schedule

Accounts Receivable (A/R) Balance Pattern

© 2016 - The Treasury Academy, Inc. - All Rights Reserved61

Days’ Sales Outstanding (DSO) Assume that a company has outstanding receivables of $285,000 at the end of the first quarter and credit sales of $310,000 for the quarter. Using a 90-day averaging period, the DSO for this company can be computed as follows:

Sales During Period $310,000Avg. Daily Credit Sales = = = $3,444.44Number of Days in Period 90

Outstanding A/R $285,000DSO = = = 82.74 DaysAvg. Daily Credit Sales $3,444.44

Average Past Due = DSO Avg. Days of Credit Terms

= 82.74 Days 60 Days = 22.74 Days

If the company’s credit terms are net 60, the average past due is computed as follows:

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 62

Source: ETM4 - © AFP

A/R Aging ScheduleSeparates A/R into current and past-due receivables in 30-day increments (on a customer or aggregate basis) and can determine the percent past due

Age of A/R Amount of A/R % of Total A/R

Current $1,750,000 70%

1-30 Days Past Due 375,000 15%

31-60 Days Past Due 250,000 10%

Over 60 Days Past Due 125,000 5%

Total $2,500,000 100%

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 63

Source: ETM4 - © AFP

22

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

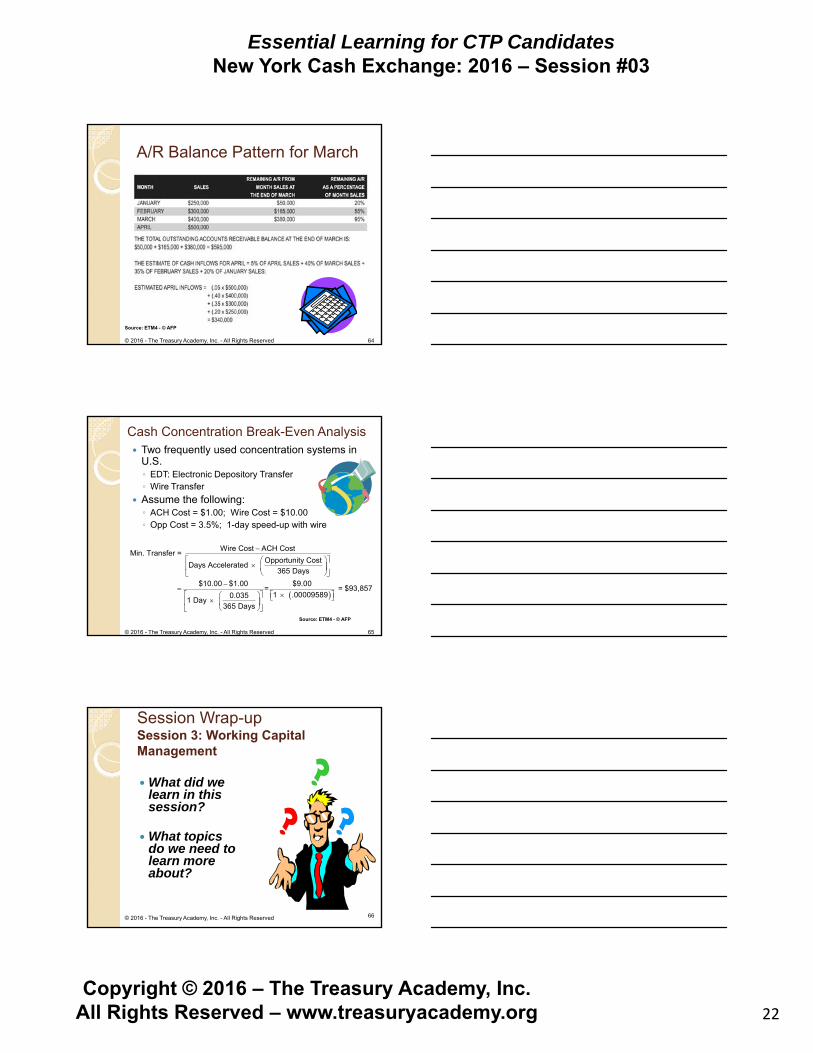

A/R Balance Pattern for March

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 64

Source: ETM4 - © AFP

Cash Concentration Break-Even Analysis Two frequently used concentration systems in

U.S.◦ EDT: Electronic Depository Transfer◦ Wire Transfer

Assume the following:◦ ACH Cost = $1.00; Wire Cost = $10.00◦ Opp Cost = 3.5%; 1-day speed-up with wire

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 65

Wire Cost ACH CostMin. Transfer =

Opportunity CostDays Accelerated

365 Days

$10.00 $1.00 $9.00= = $93,857

1 .000095890.0351 Day

365 Days

Source: ETM4 - © AFP

Session Wrap-upSession 3: Working Capital Management

What did we learn in this session?

What topics do we need to learn more about?

66© 2016 - The Treasury Academy, Inc. - All Rights Reserved

23

Essential Learning for CTP CandidatesNew York Cash Exchange: 2016 – Session #03

Copyright © 2016 – The Treasury Academy, Inc.All Rights Reserved – www.treasuryacademy.org

New York Cash Exchange: 2016Essential Learning for CTP Candidates

End of This Session

We will reconvene after a short break.

The topic will be:

More Key ConceptsFinancial Statements, Analysis & Decisions

© 2016 - The Treasury Academy, Inc. - All Rights Reserved 67