esop for young entrepreneur(s)

TRANSCRIPT

JUNE 2014

ESOP(s) for Young Entrepreneurs

MANU GROVER (FCS, LLB, LIII, IIM-C)

✪ ESOPs – General Parlance

✪ Importance of ESOP(s)

✪ Entitlement for ESOP(s)

✪ Pricing for ESOP(s)

✪ Key terminology

✪ Life Cycle of ESOP – Employee and Company Perspective

✪ Taxation on ESOP

✪ Statutory applicable legistation

✪ FAQ

Index

ESOPs is an agreement between a Company and its employees that gives

employees right to acquire a predefined number of equity shares of the

Company at the pre-agreed value within a stipulated time frame. Thus,

ESOP scheme is important which contains the exhaustive details.

ORIGIN:

The concept was first introduced in USA in 1950’s and Infosys pioneered

the same in India in 1994. The whole idea was to bring the sense of

ownership which acts as a strong motivational force towards the growth of

the Company.

ESOP(s) – General Parlance

ESOPs – It’s a investment in the vision and growth story of the Company.

The ESOP(s) in young enterprise becomes valuable due to its pace and

scalability potential.

Unlike cash salaries which has a present cash value, ESOP has a high

potential value which can have an extra motivational factors for future

growth potential.

“HIGH RISK (CASH SALARY FORGO) = HIGH VALUE (GOOD VALUATION)”

Importance of ESOP(s)

Entitlement for ESOP(s)

ESOPs – is a right but not an obligation for following persons;

a) Permanent employee (whether working in India / or abroad);

b) Director of the Company (excludes independent Director)

c) The above persons of a subsidiary/holding or associate company

Excludes, an employee who is a promoter or Director who either himself

or through relative holds more than 10% of the outstanding equity

shares of the Company.

ESOPs – are ‘freely’ priced. Though there are vaious accounting principles

guiding the norms vis-a-vis INTRINSIC VALUE METHOD OR FAIR VALUE

METHOD

Illustration:

Company ‘A’ sold equity shares in the last round at INR 5000 per share to

an investor. An employee who works at a salary of INR 7 Lacs per annum.

Thus, we will propose allotting you 140 ESOP shares, valued at INR 7 Lacs

per annum (towards 50% variable pay) i.e. 140 shares x INR 5000 per

share.

Pricing of ESOP(s)

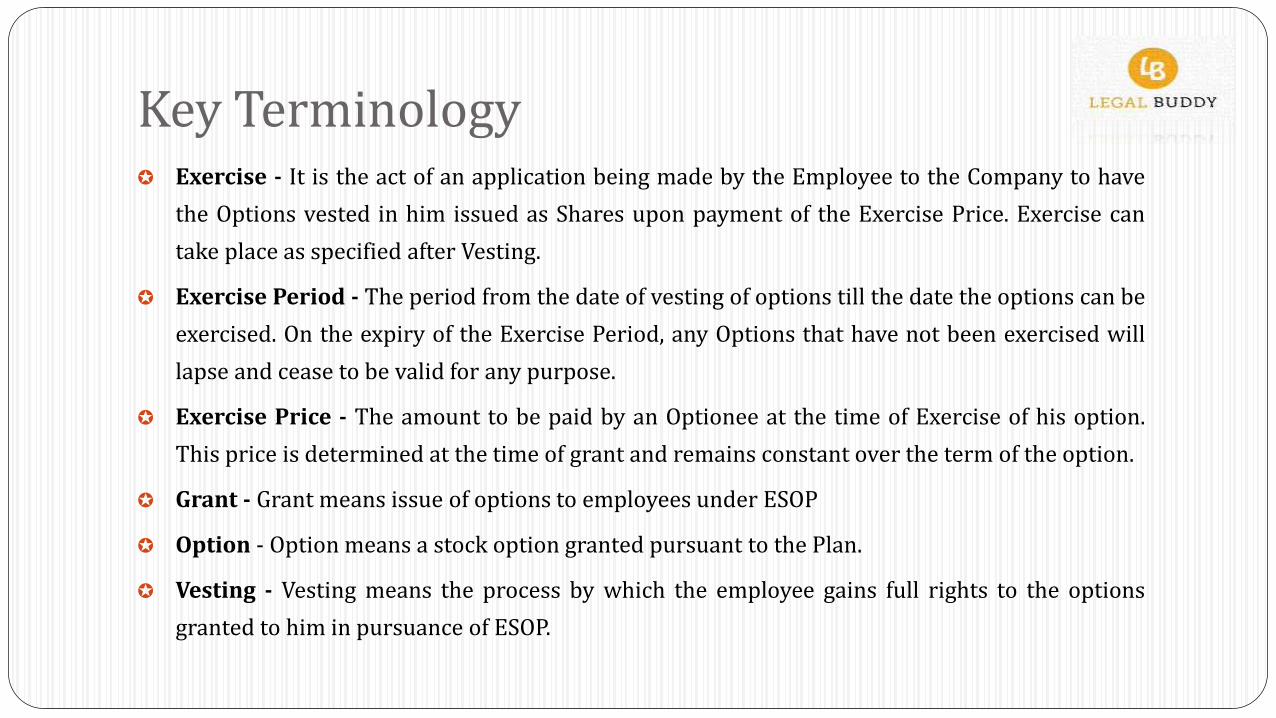

✪ Exercise - It is the act of an application being made by the Employee to the Company to have

the Options vested in him issued as Shares upon payment of the Exercise Price. Exercise can

take place as specified after Vesting.

✪ Exercise Period - The period from the date of vesting of options till the date the options can be

exercised. On the expiry of the Exercise Period, any Options that have not been exercised will

lapse and cease to be valid for any purpose.

✪ Exercise Price - The amount to be paid by an Optionee at the time of Exercise of his option.

This price is determined at the time of grant and remains constant over the term of the option.

✪ Grant - Grant means issue of options to employees under ESOP

✪ Option - Option means a stock option granted pursuant to the Plan.

✪ Vesting - Vesting means the process by which the employee gains full rights to the options

granted to him in pursuance of ESOP.

Key Terminology

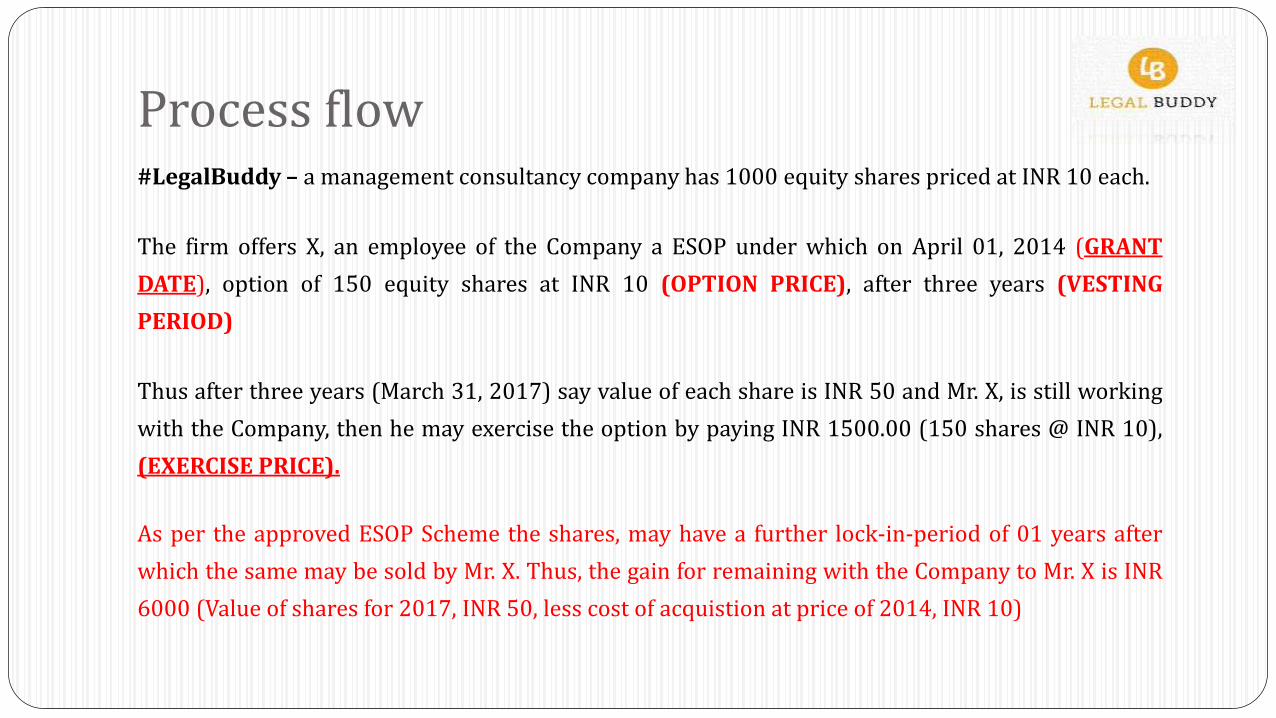

#LegalBuddy – a management consultancy company has 1000 equity shares priced at INR 10 each.

The firm offers X, an employee of the Company a ESOP under which on April 01, 2014 (GRANT

DATE), option of 150 equity shares at INR 10 (OPTION PRICE), after three years (VESTING

PERIOD)

Thus after three years (March 31, 2017) say value of each share is INR 50 and Mr. X, is still working

with the Company, then he may exercise the option by paying INR 1500.00 (150 shares @ INR 10),

(EXERCISE PRICE).

As per the approved ESOP Scheme the shares, may have a further lock-in-period of 01 years after

which the same may be sold by Mr. X. Thus, the gain for remaining with the Company to Mr. X is INR

6000 (Value of shares for 2017, INR 50, less cost of acquistion at price of 2014, INR 10)

Process flow

1 – GRANT

EMPLOYEE RECEIVES THE RIGHT

2 – VEST

EMPLOYEE EARNS THE GRANT

3 – EXERCISE

EXERCISE OF RIGHT BY THE EMPLOYEE

4 – SALE

EMPLOYEE SELLS THE SHARES

Life Cycle of ESOP

Compensation Committee

is formed

Drafted ESOP Scheme is

approved by BOD

ESOP Scheme is approved by

Shareholders

Stocks are GRANTED to

Eligible Employees

Cooling period –“Vesting period”

(ONE TIME / GRADED)

Employee exercise the

Option

Exercised shares are allotted

Employee does not exercise the

Option

Option expires

Employee / Company’s perspective

Taxation on ESOP

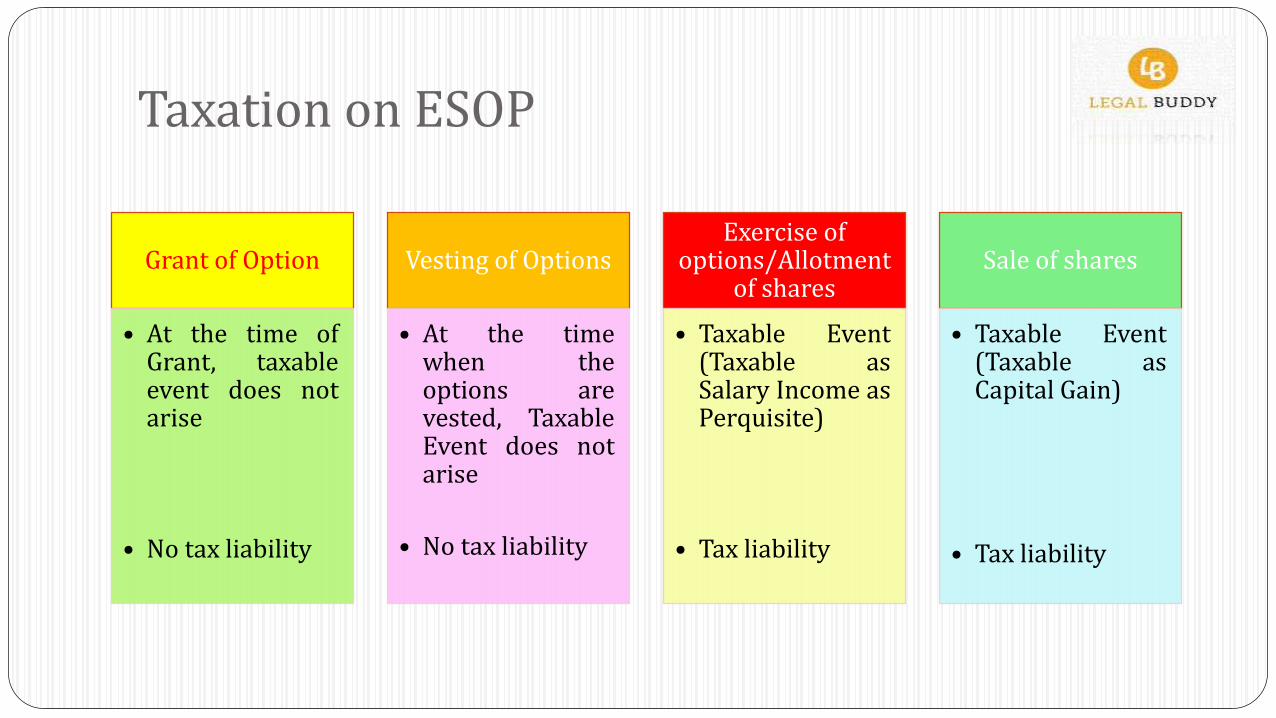

Grant of Option

• At the time ofGrant, taxableevent does notarise

• No tax liability

Vesting of Options

• At the timewhen theoptions arevested, TaxableEvent does notarise

• No tax liability

Exercise of options/Allotment

of shares

• Taxable Event(Taxable asSalary Income asPerquisite)

• Tax liability

Sale of shares

• Taxable Event(Taxable asCapital Gain)

• Tax liability

✪ The Companies Act, 2013 read with Rules made thereunder vis-à-vis

Companies (Share Capital and Debentures) Rules, 2014

✪ SEBI (Employee Stock Option Scheme and Employee Stock Purchase

Scheme) Guidelines 1999, as may be amended from time to time

✪ Unlisted Companies (Issue of Sweat Equity shares) Rules, 2003

✪ Income Tax Act, 1961

Statutory Legislation

Can a Private Limited Company have an ESOP for particular employee?

- Yes, ESOP can be for particular set of employees or all.

Can Optionee exercise the right before the vesting period?

- No, the grant can be exercised after the expiry of predefined vesting period. There needs

to be a gap of minimum one year between grant of option and commencement of

exercise period (Vesting Period).

Is option expires if Optionee leaves before end of vesting period?

- Yes, the option lapses if the employee leaves before the vesting period, though in case of

death the legal nominees are entitled to exercise the option.

FAQ(s)

Is there a lock-in period after the exercise of grant by the optionee ?

- The legislation does not provide for the same, though the management may restricts/put the

lock-in under the ESOP Scheme.

Can Optionee exercise the right after lapse of exercise period ?

- No, one the exercise period lapses the optionee cannot claim the grant.

Is the option taxable under the hand of Optionee ?

- Yes, the Optionee has to bear the tax.

- Perquisite at the time of exercise: FMV-Exercise Price

- Capital gain tax: Net sale-FMV (STCG-10%, LTCG-Nil)

FAQ(s)