equity derivatives: regulation and uncertainty a dissertation …bp567tk3535/elizabeth_stone... ·...

TRANSCRIPT

EQUITY DERIVATIVES:

REGULATION AND UNCERTAINTY

A DISSERTATION

SUBMITTED TO THE DEPARTMENT OF ECONOMICS

AND THE COMMITTEE ON GRADUATE STUDIES

OF STANFORD UNIVERSITY

IN PARTIAL FULFILLMENT OF THE

REQUIREMENTS FOR THE DEGREE OF

DOCTOR OF PHILOSOPHY

Elizabeth Connor Stone

July 2010

http://creativecommons.org/licenses/by-nc/3.0/us/

This dissertation is online at: http://purl.stanford.edu/bp567tk3535

© 2010 by Elizabeth Connor Stone. All Rights Reserved.

Re-distributed by Stanford University under license with the author.

This work is licensed under a Creative Commons Attribution-Noncommercial 3.0 United States License.

ii

I certify that I have read this dissertation and that, in my opinion, it is fully adequatein scope and quality as a dissertation for the degree of Doctor of Philosophy.

Nicholas Bloom, Primary Adviser

I certify that I have read this dissertation and that, in my opinion, it is fully adequatein scope and quality as a dissertation for the degree of Doctor of Philosophy.

Nir Jaimovich

I certify that I have read this dissertation and that, in my opinion, it is fully adequatein scope and quality as a dissertation for the degree of Doctor of Philosophy.

Monika Piazzesi

Approved for the Stanford University Committee on Graduate Studies.

Patricia J. Gumport, Vice Provost Graduate Education

This signature page was generated electronically upon submission of this dissertation in electronic format. An original signed hard copy of the signature page is on file inUniversity Archives.

iii

Abstract

The synthesizing element of this dissertation is the use of financial data to research topics relevant for the

regulation of financial markets and for policy aimed at stimulating economic activity. The first chapter, entitled

“The Effect of Uncertainty on Investment: Evidence from Options" and co-authored with Luke Stein, uses

information incorporated in securities prices to understand firm behavior. In particular, the research presents

new empirical evidence on the relationship between uncertainty and firm-level investment.

The chapter’s contributions fall into two categories: measurement and identification. We use the expected

volatility of stock prices as implied by equity options as a proxy for the uncertainty faced by firms. Rather than

relying on econometric methods to generate a forecast of future stock price volatility using information in past

volatility, the implied volatility from an equity option is the market’s own forecast of explicitly forward-looking

uncertainty. In addition, we introduce a natural instrument strategy that relies upon variation in firms’ exposure

to the volatility of energy prices and currency exchange rates. These instruments are appealing in their ability

to capture factors that are fundamentally relevant for the uncertainty faced by firms.

Results are reported for both Ordinary Least Squares and Two-Stage Least Squares estimations. We find a

negative and statistically significant relationship between uncertainty and investment that is robust across a

variety of specifications. The coefficient estimates are larger in magnitude after addressing the endogeneity of

the uncertainty measure, suggesting potential reverse causation that biases the OLS estimates towards zero.

The second and third chapters use financial data to analyze topics capturing regulatory attention in equity

markets. The second chapter evaluates the Securities Exchange Commission’s implementation of a “penny

pricing" pilot in the exchange-traded equity options market in February 2007. The initial phase of this trial

required options exchanges to reduce the minimum bid-offer spread from five or ten cents to a penny for the

options corresponding to thirteen underlying equity securities. The catalyst for this pricing change was the

improved electronic capabilities of the exchanges. Over the course of the preceding decade, the exchanges

invested in the development of electronic trading systems that allowed for more efficient quoting and trading

of options securities. The SEC’s mandated pricing change effectively redistributes the gains of innovation

from the exchanges’ market makers to individual investors.

iv

The chapter presents an analysis of the market impact of the Penny Pilot and highlights the SEC’s central

role in shaping the options market’s innovations and competitive environment. Beyond a reduction in bid-

offer spreads, the pilot has stimulated a variety of changes in trading dynamics and market structure. These

repercussions include thinner markets, changes in market maker fee structures, the introduction of alternative

trading venues, and incentives for the exchanges to prioritize further technological innovation.

The third chapter, entitled “Fails to Deliver: The Price Impact of Naked Short Sales", presents research

on the effect of naked short selling on asset prices and trading dynamics. This is a prominent topic of debate

among academic researchers, market participants, regulators, and the popular press. The chapter evaluates

the validity of the claim that naked shorting leads to negative excess returns by creating additional selling

pressure. While data on naked short sales is not available, Securities Exchange Commission data on failures to

deliver is a strong proxy. Fail to deliver data for 2004 covers a period during which the prevalence of naked

short selling was not public knowledge since neither the fail to deliver data nor the Regulation SHO Threshold

List was publicly available. In excluding information and regulation effects, the analysis isolates potential

microstructure price effects.

Using a methodology that constructs daily portfolios according to the quantity of naked short selling, I

find no evidence that stocks subject to naked short selling experience negative excess returns. Rather, I find

evidence that these stocks outperform on the day the trades occur. Naked short sellers appear to target stocks

that outperform during the trading day and cover existing fails on days when the stocks underperform. This

outperformance is not evident for stocks subject to the greatest amount of naked short selling, suggesting that

positive excess returns may be offset by the additional selling pressure.

v

Acknowledgments

My research has greatly benefited from the advice and guidance of faculty and fellow students at Stanford

University. Special thanks to Paul A. David and to the members of my Dissertation Reading Committee:

Nicholas Bloom, Nir Jaimovich and Monika Piazzesi.

Thank you to Luke Stein, the co-author of the first chapter of my dissertation, for his inspiring commitment

to academic excellence.

As always, thank you to my family for encouraging my academic and career pursuits and for their unfailing

support in times of both challenge and success.

vi

Contents

1 The Effect of Uncertainty on Investment: Evidence from Options 1

1.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.2 Theoretical Foundations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

1.3 Empirical Evidence . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

1.4 Data Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

1.5 “Naïve” Estimation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

1.6 Instrumental Variables Estimation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

1.6.1 Endogeneity of Uncertainty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

1.6.2 Endogeneity of Tobin’s q . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

1.6.3 Two-Stage Least Squares Results . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

1.7 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

1.8 Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

1.8.1 Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

1.8.2 Robustness of Timing Assumption . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

1.8.3 Alternative Implied Volatility Durations . . . . . . . . . . . . . . . . . . . . . . . . 29

1.8.4 Alternative Energy Intensity Measure . . . . . . . . . . . . . . . . . . . . . . . . . 30

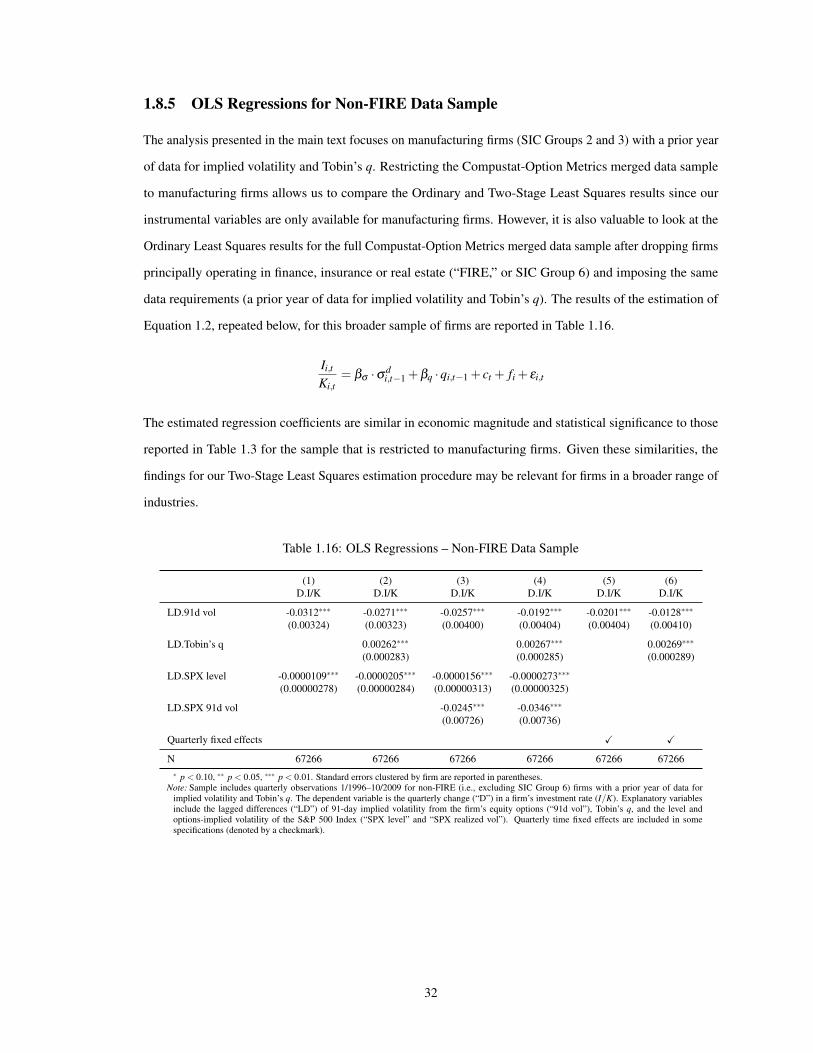

1.8.5 OLS Regressions for Non-FIRE Data Sample . . . . . . . . . . . . . . . . . . . . . 32

1.8.6 Results Using Realized Volatility Measure . . . . . . . . . . . . . . . . . . . . . . . 33

1.8.7 Relationship Between Implied Volatility and Tobin’s q . . . . . . . . . . . . . . . . 34

Bibliography . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

2 Regulated Technology Diffusion: The SEC and the Impact of Penny Pricing in Electronic Op-

tions Trading 39

2.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

2.2 Implementation of the Penny Pilot . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

2.3 Market Impact . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

vii

2.3.1 Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

2.3.2 Descriptive Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

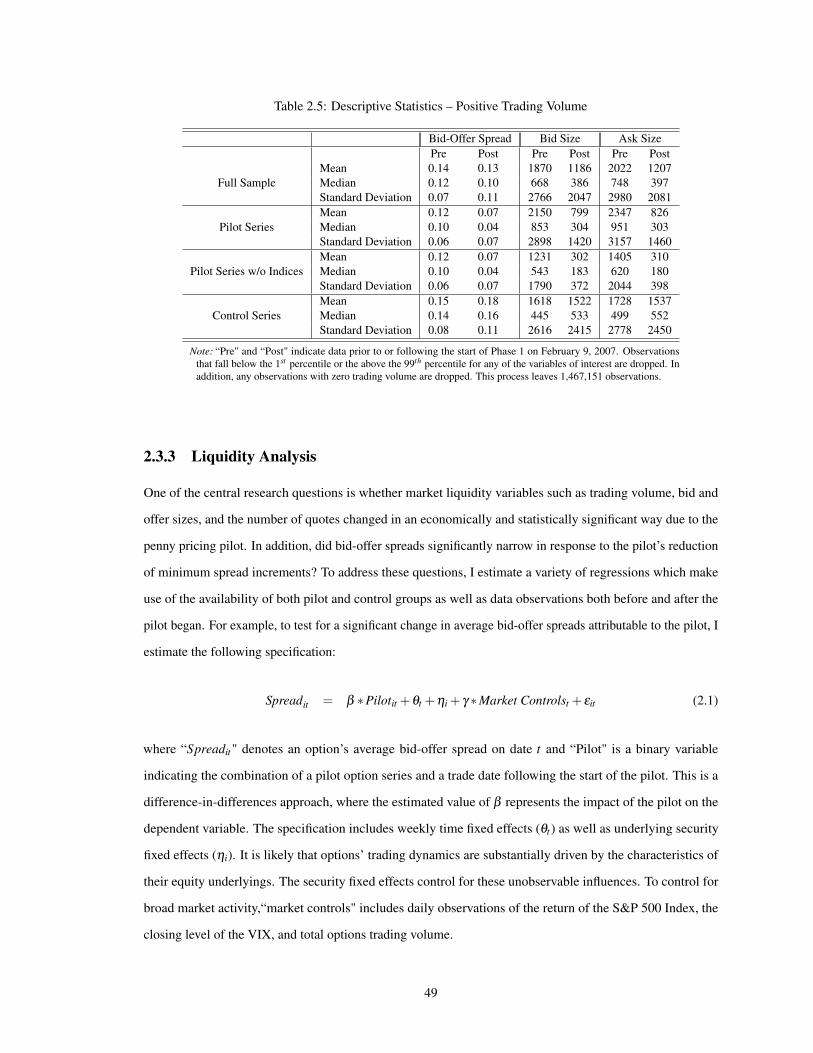

2.3.3 Liquidity Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

2.3.4 Probit Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

2.3.5 Transition Dynamics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

2.4 Market Structure Changes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

2.4.1 Maker Taker . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

2.4.2 Institutional Investors and Alternative Trading Venues . . . . . . . . . . . . . . . . 60

2.4.3 Incentives for Further Technological Progress . . . . . . . . . . . . . . . . . . . . . 62

2.5 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

2.6 Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

2.6.1 Control Selection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

2.6.2 Robustness to Inclusion of Observations with Zero Trading Volume . . . . . . . . . 68

Bibliography . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

3 Fails to Deliver: The Price Impact of Naked Short Sales 71

3.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

3.2 Literature Review . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

3.3 Finnerty Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74

3.4 Data Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

3.5 Fail to Deliver Portfolio Returns . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

3.6 Portfolio Returns by Decile . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

3.7 Post Regulation SHO . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

3.8 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87

3.9 Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 89

3.9.1 Covered versus Naked Short Selling . . . . . . . . . . . . . . . . . . . . . . . . . . 89

3.9.2 Regulation SHO . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 89

3.9.3 Results for 2005 Fail to Deliver Data . . . . . . . . . . . . . . . . . . . . . . . . . 90

Bibliography . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94

viii

List of Tables

1.1 Summary Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1.2 Summary Statistics – Manufacturing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

1.3 OLS Regressions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

1.4 OLS Regressions – Realized Volatility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

1.5 Volatility Partial First Stage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

1.6 Tobin’s q Partial First Stage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

1.7 Full First Stage Regression . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

1.8 Two-Stage Least Squares Estimation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

1.9 Currency Exposure – Countries Considered . . . . . . . . . . . . . . . . . . . . . . . . . . 25

1.10 Energy Intensity by 2-digit SIC Code . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

1.11 Relevant Timing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

1.12 Correlation of Implied Volatility Durations . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

1.13 Implied Volatility Duration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

1.14 Full First Stage Regression – Alternative Energy Intensity Measure . . . . . . . . . . . . . . 31

1.15 Two-Stage Least Squares Estimation – Alternative Energy Intensity Measure . . . . . . . . 31

1.16 OLS Regressions – Non-FIRE Data Sample . . . . . . . . . . . . . . . . . . . . . . . . . . 32

1.17 Relevant Timing – Realized Volatility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

1.18 OLS Regressions – Implied and Realized Volatility . . . . . . . . . . . . . . . . . . . . . . 33

1.19 Two-Stage Least Squares Estimation – Realized Volatility . . . . . . . . . . . . . . . . . . . 34

1.20 Relationship between Implied Volatility and Tobin’s q . . . . . . . . . . . . . . . . . . . . . 35

2.1 Phase 1 and Comparable Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

2.2 Descriptive Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

2.3 Descriptive Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

2.4 Descriptive Statistics – Positive Trading Volume . . . . . . . . . . . . . . . . . . . . . . . . 48

2.5 Descriptive Statistics – Positive Trading Volume . . . . . . . . . . . . . . . . . . . . . . . . 49

ix

2.6 Market Impact . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

2.7 Market Impact without Averaging . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

2.8 Market Impact Excluding Index Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

2.9 Market Maker Quotes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

2.10 Probability of Positive Trading Volume . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

2.11 Probability of Positive Trading Volume Excluding Index Options . . . . . . . . . . . . . . . 56

2.12 Transition Dynamics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

2.13 Phase 1 Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

2.14 Comparable Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

2.15 Market Impact Including Zero Volume Observations . . . . . . . . . . . . . . . . . . . . . 68

2.16 Market Impact Including Zero Volume Observations - Exclude Index Options . . . . . . . . 68

3.1 Fail to Deliver Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

3.2 Summary Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

3.3 Fail-to-Deliver Portfolio Returns . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

3.4 Statistics by Decile . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

3.5 Equal-Weighted Decile Returns . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

3.6 Value-Weighted Decile Returns . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

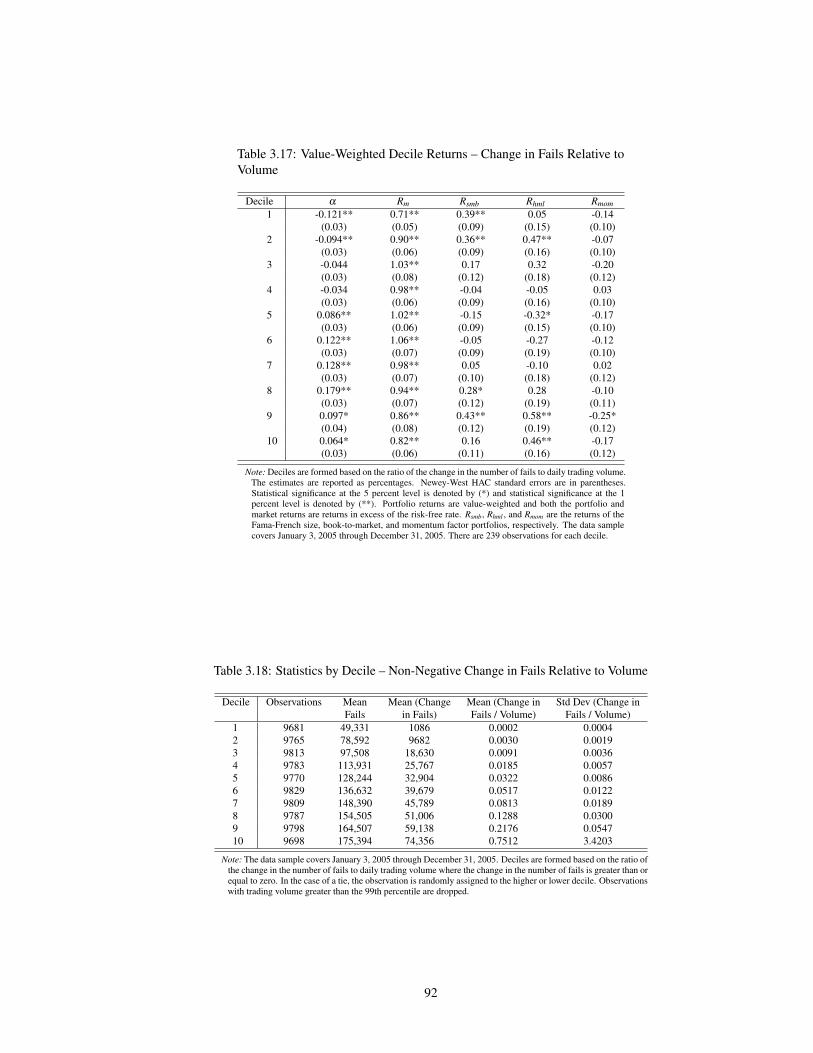

3.7 Statistics by Decile – Change in Fails Relative to Volume . . . . . . . . . . . . . . . . . . . 83

3.8 Equal-Weighted Decile Returns – Change in Fails Relative to Volume . . . . . . . . . . . . 84

3.9 Value-Weighted Decile Returns – Change in Fails Relative to Volume . . . . . . . . . . . . 84

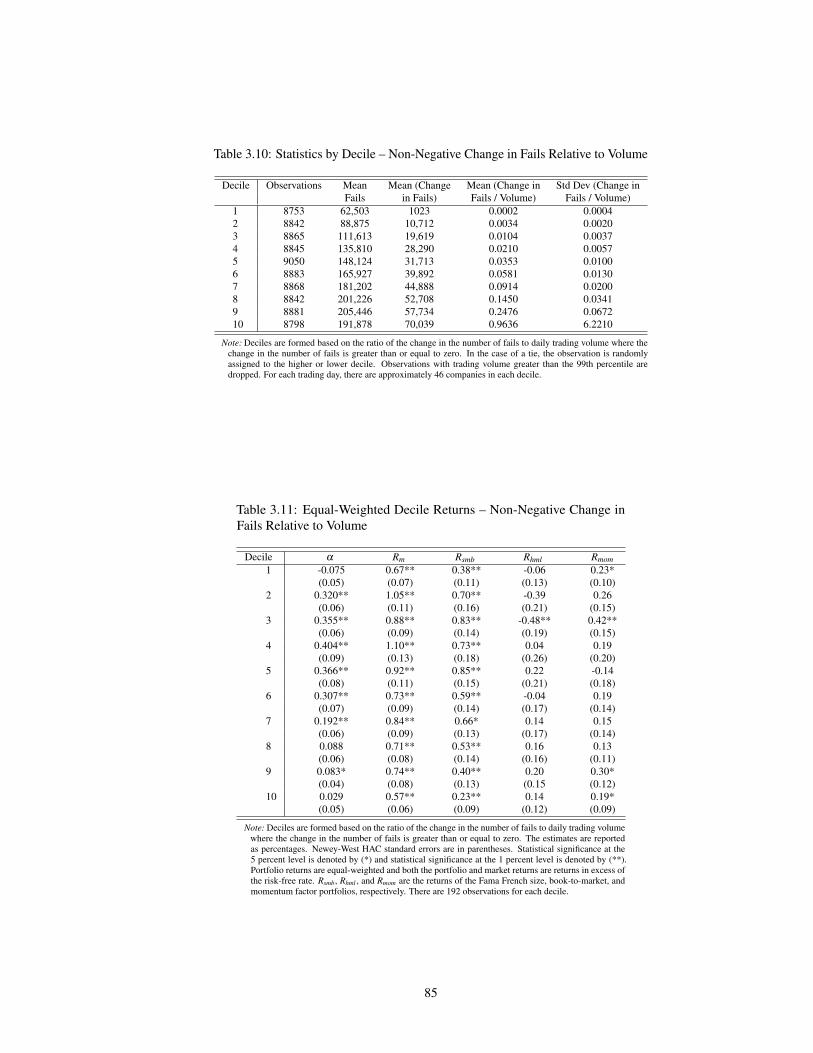

3.10 Statistics by Decile – Non-Negative Change in Fails Relative to Volume . . . . . . . . . . . 85

3.11 Equal-Weighted Decile Returns – Non-Negative Change in Fails Relative to Volume . . . . 85

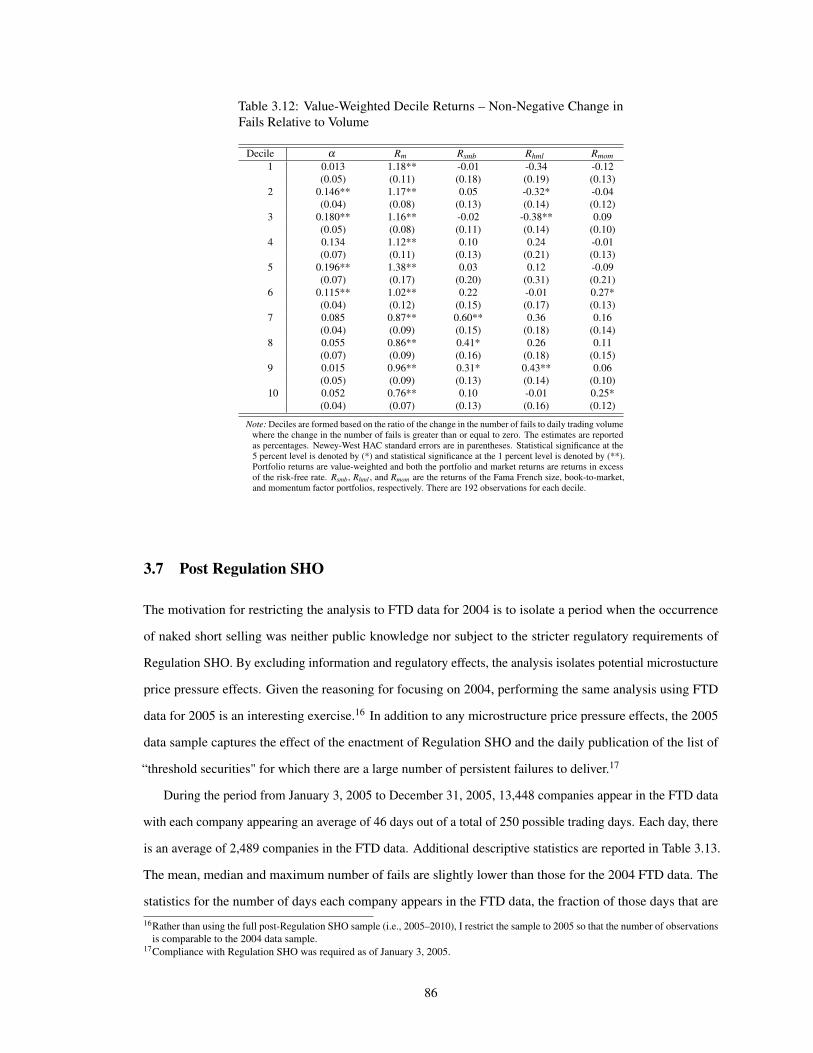

3.12 Value-Weighted Decile Returns – Non-Negative Change in Fails Relative to Volume . . . . . 86

3.13 Fail to Deliver Data – 2005 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87

3.14 Fail-to-Deliver Portfolio Returns . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90

3.15 Statistics by Decile – Change in Fails Relative to Volume . . . . . . . . . . . . . . . . . . . 91

3.16 Equal-Weighted Decile Returns – Change in Fails Relative to Volume . . . . . . . . . . . . 91

3.17 Value-Weighted Decile Returns – Change in Fails Relative to Volume . . . . . . . . . . . . 92

3.18 Statistics by Decile – Non-Negative Change in Fails Relative to Volume . . . . . . . . . . . 92

3.19 Equal-Weighted Decile Returns – Non-Negative Change in Fails Relative to Volume . . . . 93

3.20 Value-Weighted Decile Returns – Non-Negative Change in Fails Relative to Volume . . . . . 93

x

List of Figures

1.1 Distributions of Investment Rate and Implied Volatility . . . . . . . . . . . . . . . . . . . . 7

1.2 Distributions of Implied and Realized Volatility . . . . . . . . . . . . . . . . . . . . . . . . 12

1.3 Energy Intensity and Volatility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

1.4 Currency Intensity and Volatility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

1.5 Cross-Sectional Distribution of Implied Volatility . . . . . . . . . . . . . . . . . . . . . . . 24

1.6 Covered Currencies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

1.7 Currency Exchange Rate Series . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

1.8 Deflated Oil Price Series . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

2.1 Distribution of Bid-Offer Spreads . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

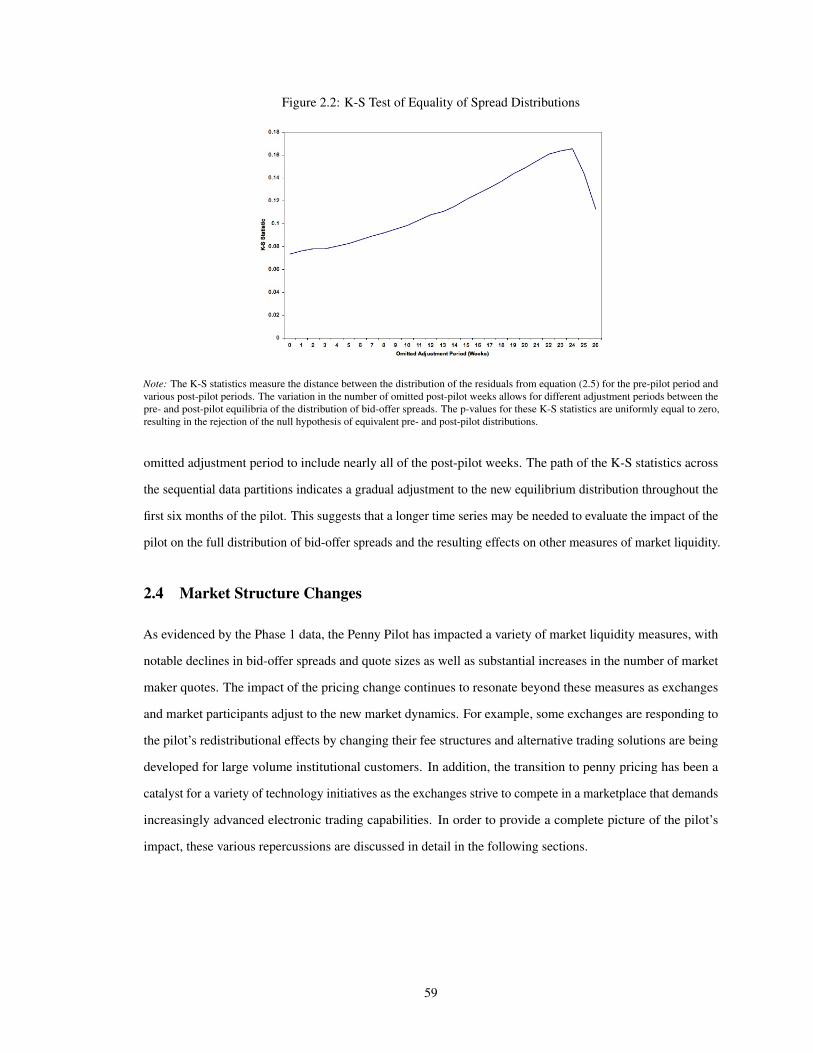

2.2 K-S Test of Equality of Spread Distributions . . . . . . . . . . . . . . . . . . . . . . . . . . 59

xi

Chapter 1

The Effect of Uncertainty on Investment: Evidence from Options

1.1 Introduction

The relationship between a firm’s investment decisions and the uncertainty it faces is a widely researched

topic in both academic and policy literatures. Underlying sources of uncertainty about the future may include

demand conditions, input prices, rates of return, and macroeconomic factors such as interest, exchange and

inflation rates. In the face of such uncertainty regarding market conditions, firms must decide whether to

invest in capital projects that will affect their future profitability differently depending on how uncertainty is

resolved. In this paper, we provide new empirical evidence on how uncertainty affects investment using data

disaggregated at the firm level.

Firms’ investment is a key factor for the business cycle and other aggregate economic phenomena. In order

to understand the effects of macroeconomic fluctuations in investment, however, it is valuable to examine the

microeconomic decisions that individual firms make to build factories, buy equipment, research new ideas, and

hire workers. For many years, theorists have argued that economic uncertainty can be an important determinant

of investment levels and dynamics. Understanding how uncertainty affects firms’ investment decisions is

important in macroeconomic analysis, but unfortunately, economic theory offers ambiguous predictions.

Given the possibility of hedging, why does uncertainty have an effect on investment at all? The answer

to this question lies in the fact that markets are incomplete and, therefore, instruments do not exist such

that firms can fully hedge against all risks. Further, when hedging instruments are available, they may be

prohibitively expensive; a firm may prefer to bear some risk rather than pay a large sum to eliminate it.1 Guay

and Kothari (2003) find that the hedging portfolios of non-financial firms are very modest relative to firm size

(and operating and investing cash flows), concluding that “corporate derivatives use appears to be a small piece

of non-financial firms’ overall risk profile.” As a result of this limited degree of hedging, firms must select

optimal investment levels in the face of significant residual uncertainty.

1In addition, if shareholders are able to diversify across a portfolio of assets, it may not be optimal for firms to hedge, even at modest cost.

1

This paper contributes to the investment under uncertainty literature in several important ways. Existing

empirical papers rely upon a variety of proxy measures of the degree of uncertainty faced by firms. These

measures include forecasted share return volatility derived from realized stock returns (Leahy and Whited,

1996), variance of analyst earnings forecasts (Bond et al., 2005), and volatility in real wages, material prices

and output prices (Huizinga, 1993; Ghosal and Loungani, 1996). This paper introduces a more appealing

measure: we proxy the level of uncertainty faced by a firm using the expected volatility of its stock price as

implied by equity options.

Options-implied volatility is an explicitly forward-looking measure of uncertainty. Rather than relying on

econometric methods to generate a forecast of future stock price volatility using information in past volatility,

the implied volatility from equity options represents the market’s own forecast. Implied volatility is arguably

less affected by movements unattributable to changes in fundamentals (“stock price bubbles”) than realized

stock returns. As discussed in Schwert (2002), realized volatility is often much higher or lower than the market

forecast, as evidenced by smoother series for implied volatility. Christensen and Prabhala (1998) find that

“implied volatility outperforms past volatility in forecasting future volatility and even subsumes the information

content of past volatility. . . .”

In addition, implied volatility allows us to capture uncertainty across multiple dimensions. Each equity

stock is associated with a variety of options that differ in their expiration dates and strike prices. By using

this broad menu of equity options, we can capture a rich depiction of uncertainty that traces out expected

stock price volatility over different time horizons and stock price levels. Leahy and Whited (1996) discuss

the advantage of implied volatilities over realized stock returns as a proxy measure of uncertainty; while the

necessary data were unavailable at that time, the enormous growth of the equity options markets over the past

decade means we now have access to an extensive archive of reliable options data.

Another important contribution of this paper is the introduction of a natural instrument strategy for our

estimation procedure. While we are interested in the effect of uncertainty on investment, a causal relationship

operating in the opposite direction is likely also present. For example, if a firm undertakes a risky investment

project, the observed implied volatility may increase to reflect the subsequently greater uncertainty regarding

future returns.2 One identification strategy relied upon throughout the literature uses “internal” instruments

to isolate the exogenous portion of uncertainty; these internal instruments are typically lagged values of the

dependent and explanatory variables (see Leahy and Whited, 1996; Bloom et al., 2007). In contrast, this

paper relies on a “natural” instrument strategy. We use a firm’s exposure to the volatility of energy prices

and currency exchange rates as a source of exogenous shocks to the uncertainty measured by options-implied

2Another potential source of endogeneity is the presence of a latent third factor that affects both investment and uncertainty. For example,Brunnermeier and Sannikov (2009) consider the mechanism by which shocks to credit conditions affect both asset price volatility andfirms’ capital stocks.

2

volatility. We use a similar strategy to instrument Tobin’s q, a relevant explanatory variable in our econometric

specification that is widely considered throughout the literature on investment under uncertainty.

Our analysis is based on quarterly data for 2,230 U.S. manufacturing firms for the period from January

1996 though October 2009, covering a wide variety of market environments including the recent period of

economic turmoil. We begin by estimating an Ordinary Least Squares specification that (naïvely) fails to

account for the endogeneity of implied volatility. Here, we observe a strong negative covariance between

uncertainty (as proxied by implied volatility) and firm investment. We show that realized volatility is not

nearly as strong a predictor of investment as implied volatility. We then discuss the details of our instrumental

variables strategy and provide evidence that exposure to plausibly exogenous energy and currency volatility

shocks has strong explanatory power for firm-specific uncertainty. The Two-Stage Least Squares estimation

finds a negative and statistically significant effect of uncertainty on investment. The coefficient estimates are

larger in magnitude than those produced by OLS, suggesting the possibility that reverse causation is biasing

the OLS estimates towards zero.

Sections 1.2 and 1.3 discuss the theoretical foundations for our empirical work and briefly review the

relevant empirical literature. Section 1.4 describes our primary data sources and provides summary statistics

for our data sample. Ordinary Least Squares estimation results are presented in Section 1.5, and Section 1.6

develops the methodology and presents findings from our instrumental variables estimation. Section 1.7

concludes.

1.2 Theoretical Foundations

In a benchmark linear model of investment, uncertainty has no effect on firm decisions. In order for uncertainty

to be a relevant factor, there must be a non-linearity in some element of the firm’s problem. The theoretical

literature on investment under uncertainty falls into three general categories depending on the assumed source

of curvature. The first group of models assumes convexity stemming from adjustment costs. In real options

models such as that of Dixit and Pindyck (1994), the combination of uncertainty and irreversibility in capital

investment generates regions of inaction where firms prefer to “wait and see” rather than immediately invest.

Greater uncertainty expands this region of inaction, generating a negative relationship between uncertainty and

investment.3

The second group of models considers curvature in the production function. The effects of this assumption

are developed by Hartman (1972) and Abel (1983), who show that the marginal revenue product of capital

3Irreversible investment models do not always predict a negative relationship between uncertainty and investment. Ingersoll and Ross(1992) note that the effect of interest rate uncertainty on investment is ambiguous because present values are convex functions of interestrates. The nature of the shock process is also relevant; for example, firms are more responsive to a permanent or persistent shock than toa temporary shock.

3

is a convex function of output price if a firm can freely adjust its labor input after investment decisions have

been made. As a result, there is a positive relationship between uncertainty and investment. However, as

examined in a number of papers (such as Cabellero, 1991; Pindyck, 1993; Lee and Shin, 2000), this result

relies on particular modelling assumptions regarding the revenue function and the nature of demand shocks.

For example, the effect may be eliminated or reversed if demand shocks are modelled as quantity rather than

price shocks.

The third type of model assumes curvature in the utility function of an investor, and considers risk stemming

from the covariance of firm and market returns (e.g., CAPM) rather than risk faced by a firm in isolation.

An increase in the covariance of a firm’s returns with market returns represents undiversifiable portfolio risk,

increasing the required rate of return and thereby discouraging investment. Similar to real options models,

these models predict a negative relationship between investment and uncertainty.

Together, the array of theoretical models offer a variety of perspectives on the relationship between

investment and uncertainty, but ultimately their predictions are ambiguous. Rather than testing a particular

model, this paper attempts to identify the true relationship between investment and uncertainty in the data.

1.3 Empirical Evidence

A number of empirical papers investigate the relationship between aggregate investment and a variety of

measures of uncertainty. These measures include the variances of stock market returns (Pindyck, 1986)

and macroeconomic variables such as interest rates, inflation rates, exchange rates, real wages, and GDP

(Goldberg, 1993; Ferderer, 1993; Price, 1995,1996). The general consensus of these studies is a negative effect

of uncertainty on aggregate investment.

There is also an extensive literature examining the relationship between investment and uncertainty at a

more disaggregated level. These studies use measures similar to those of the aggregate studies, including

exchange rate volatility (Goldberg, 1993; Campa and Goldberg, 1993; Campa, 1993); volatility of real wages,

material prices and output prices (Huizinga, 1993; Ghosal and Loungani, 1996); forecasted volatility of stock

returns (Leahy and Whited, 1996; Baum et al., 2007); and the variance of analyst earnings forecasts (Bond

et al., 2005) and managers’ perceptions about future product demand (Guiso and Parigi, 1999). Unlike the

aggregate studies, these papers report less conclusive evidence on the relationship between investment and

uncertainty. While the relationship appears to be negative, it is often weak or not robust to the inclusion of

other variables relevant for investment such as Tobin’s q.

Differences among the findings of these papers is at least partially driven by the degree of disaggregation.

In particular, allowing for firm-level heterogeneity seems to be important. This is consistent with the prediction

4

by the investment irreversibility literature that investment will be more sensitive to changes in idiosyncratic

uncertainty than to changes in uncertainty that broadly affect all firms.4 Bloom et al. (2007) directly address

the issue of aggregation, showing both numerically (using simulated data) and empirically for a panel of

manufacturing firms that, under partial investment irreversibility, higher uncertainty (proxied by the standard

deviation of stock returns) reduces the responsiveness of investment to demand shocks. Their finding is robust

to a variety of investment cost specifications and aggregation over both time and plant investment decisions.

Baum et al. (2007) find that investment responds negatively to firm-specific and covariance-based uncertainty,

but positively to market-wide uncertainty.

While this extensive literature offers a variety of methods and findings, much of the empirical work to date

shares the common features of using realized variances to proxy for or forecast future uncertainty and relying

on internal instruments (i.e., lagged values of dependent and explanatory variables) in order to identify the

effect of uncertainty. In contrast, by using the expected volatility of stock prices as implied by equity options,

our paper makes use of the market’s own forecast of explicitly forward-looking uncertainty. In addition, our

paper introduces an identification strategy that relies on instruments which are intuitively and fundamentally

related to firm-level uncertainty.

1.4 Data Overview

Option Metrics provides daily implied volatility data for an unbalanced panel of 6,925 companies from January

1996 through October 2009. This data includes implied volatilities from options with ten different maturities,

ranging from 30 to 730 days. While data is available for a variety of strike prices, the present analysis is

restricted to at-the-money-forward call options. These are options for which the strike price is equal to the

stock’s forward price at the option’s expiration date, given current interest rates and the company’s dividend

payout schedule.5

Company financial data comes from Compustat. We rely on variables drawn from cash flow statements,

income statements, and balance sheets as well as stock prices and firm identifying information. The Compustat

data is available quarterly from January 1961 through December 2009 and covers 22,775 companies. We

merge the Option Metrics data with the Compustat data by 8-digit CUSIP. This merge gives us 5,470 company

matches for the period from January 1996 through October 2009 with an average of 20 quarters of data per

company.

4In addition, Davis and Haltiwanger (1992) argue that most shocks are not aggregate, but rather occur at the idiosyncratic firm or plantlevel.

5Our decision to focus on at-the-money-forward options should not be surprising. These are the baseline options included in the OptionMetrics data archive, and strike prices of all other options are expressed as deviations from this baseline.

5

Throughout our analysis, we exclude companies principally operating in finance, insurance or real estate

(SIC Group 6). The relevant investment under uncertainty relationship for these firms is likely not captured

by an analysis of investment in physical capital. After removing these firms, the data sample includes 4,834

companies. As the instrumental variables estimates we present in Section 1.6 rely on data that is only available

for manufacturing firms (SIC Groups 2 and 3), we restrict our sample to these 2,230 firms to ensure the

Ordinary and Two-Stage Least Squares results are comparable. In addition, we require the firms in our sample

to have a prior year of non-missing data for both Tobin’s q and implied volatility. This further reduces the

sample to 1,807 firms and 35,835 observations.

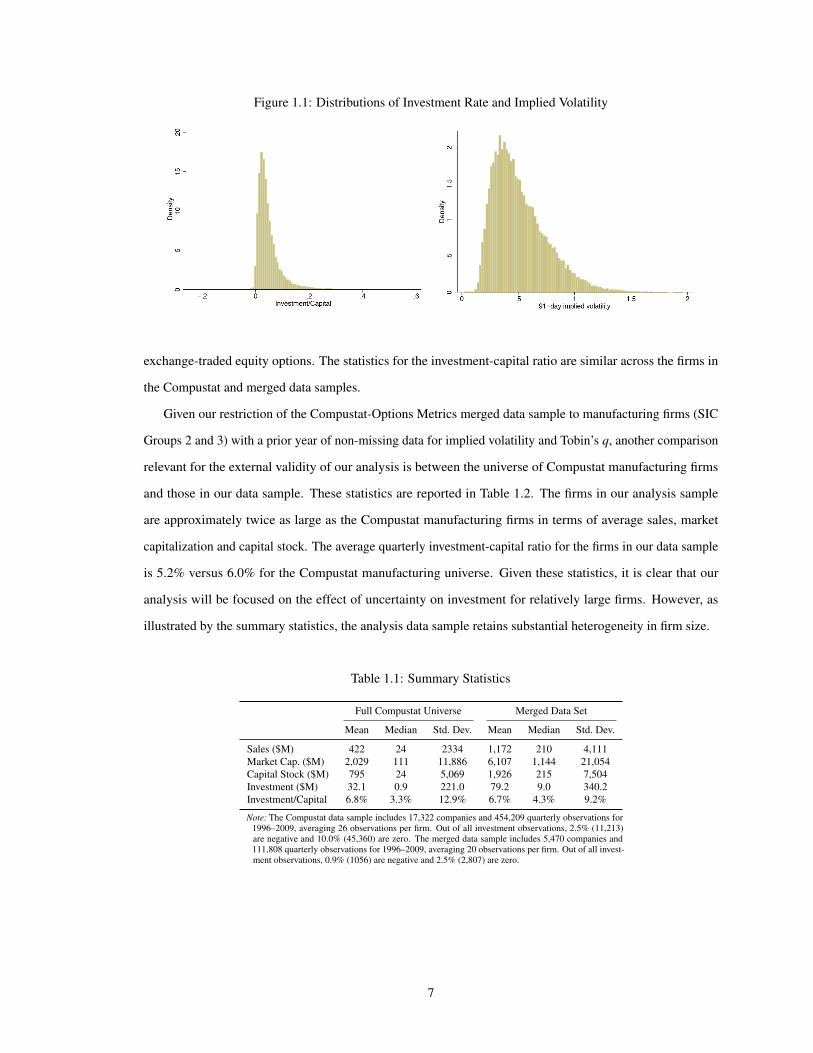

The mean investment-capital ratio in our data sample is 5.2%, with a standard deviation of 6.5%. As

illustrated in Figure 1.1, we observe very little disinvestment and the mass of firms with zero investment in a

given quarter is relatively small. The rarity of zero investment seems to be at odds with a story of irreversible

investment or fixed costs, but aggregation over time and across plants within a firm can help reconcile these

(see Bloom et al., 2007). Another possibility is that the costs incurred to replace depreciated capital may be

less than those incurred for the installation of new capital. As a result, we may observe small amounts of

investment each quarter as firms replace depreciated capital.

As illustrated in Figure 1.1, 91-day implied volatility varies significantly across firms and time, with an

average value of 0.52 and a standard deviation of 0.24.6 Implied volatility is a measure of the annualized

standard deviation of expected returns; the mean observation of 0.52 corresponds to a daily expected standard

deviation of 3.3%. Ideally, we would like to make use of the richness of the options data to evaluate the

importance of different uncertainty durations. For example, is 730-day implied volatility more relevant for

investment decisions than 91-day implied volatility? Unfortunately, the strong correlation between implied

volatilities of different durations makes it difficult to separately identify their roles. Given this high correlation

and the significant amount of new information relevant for investment decisions that is likely to be revealed

within a window of three months, we believe it is reasonable to rely upon 91-day implied volatility for the

majority of our analysis. An added benefit is the fact that implied volatilities of shorter duration options are

more consistently populated in the Option Metrics data. Additional information regarding our data sources is

provided in Appendix 1.8.1.

One potential concern is that firms with equity options may be unrepresentative of the average publicly-

traded firm in the United States. Table 1.1 reports summary statistics comparing firm characteristics for the full

universe of Compustat firms to those of the firms in the merged Compustat-Option Metrics data set. The firms

in the merged data set are approximately three times larger in terms of average sales, market capitalization,

and capital stock. This is consistent with the fact that larger, more established firms are more likely to have

6As illustrated in Appendix 1.8.1, there is substantial cross-sectional variation in implied volatility within each quarter.

6

Figure 1.1: Distributions of Investment Rate and Implied Volatility

exchange-traded equity options. The statistics for the investment-capital ratio are similar across the firms in

the Compustat and merged data samples.

Given our restriction of the Compustat-Options Metrics merged data sample to manufacturing firms (SIC

Groups 2 and 3) with a prior year of non-missing data for implied volatility and Tobin’s q, another comparison

relevant for the external validity of our analysis is between the universe of Compustat manufacturing firms

and those in our data sample. These statistics are reported in Table 1.2. The firms in our analysis sample

are approximately twice as large as the Compustat manufacturing firms in terms of average sales, market

capitalization and capital stock. The average quarterly investment-capital ratio for the firms in our data sample

is 5.2% versus 6.0% for the Compustat manufacturing universe. Given these statistics, it is clear that our

analysis will be focused on the effect of uncertainty on investment for relatively large firms. However, as

illustrated by the summary statistics, the analysis data sample retains substantial heterogeneity in firm size.

Table 1.1: Summary Statistics

Full Compustat Universe Merged Data Set

Mean Median Std. Dev. Mean Median Std. Dev.

Sales ($M) 422 24 2334 1,172 210 4,111Market Cap. ($M) 2,029 111 11,886 6,107 1,144 21,054Capital Stock ($M) 795 24 5,069 1,926 215 7,504Investment ($M) 32.1 0.9 221.0 79.2 9.0 340.2Investment/Capital 6.8% 3.3% 12.9% 6.7% 4.3% 9.2%

Note: The Compustat data sample includes 17,322 companies and 454,209 quarterly observations for1996–2009, averaging 26 observations per firm. Out of all investment observations, 2.5% (11,213)are negative and 10.0% (45,360) are zero. The merged data sample includes 5,470 companies and111,808 quarterly observations for 1996–2009, averaging 20 observations per firm. Out of all invest-ment observations, 0.9% (1056) are negative and 2.5% (2,807) are zero.

7

Table 1.2: Summary Statistics – Manufacturing

Compustat Manufacturing Analysis Data Sample

Mean Median Std. Dev. Mean Median Std. Dev.

Sales ($M) 479 23 2,881 1,155 226 3,855Market Cap. ($M) 2,304 111 13,000 7,240 1,237 23,392Capital Stock ($M) 778 23 5,837 1,648 249 5,941Investment ($M) 30.2 0.8 258.5 62.0 9.0 280.2Investment/Capital 6.0% 3.0% 11.6% 5.2% 3.6% 6.5%

Note: The Compustat manufacturing data sample (SIC Groups 2 and 3) includes 6,045 companies and175,704 quarterly observations for 1996–2009, averaging 29 observations per firm. Out of all invest-ment observations, 2.3% (4,115) are negative and 6.4% (11,181) are zero. The analysis data sampleincludes 1,807 manufacturing companies with a prior year of non-missing data for implied volatilityand Tobin’s q. There are 35,835 quarterly observations for 1996–2009, averaging 20 observationsper firm. Out of all investment observations, 0.6% (227) are negative and 0.4% (131) are zero.

1.5 “Naïve” Estimation

For the purpose of exposition, we begin by describing our analysis process and reporting results for a reduced-

form regression of investment on uncertainty that captures covariances but does not allow causal interpretation,

since it fails to account for the likely endogeneity of our uncertainty measure. The dependent variable is the

ratio of a firm’s quarterly investment to its capital stock (Ii,t/Ki,t ). Financial statements report capital at book

value rather than replacement value. Therefore we derive Ki,t recursively using the perpetual inventory method

described in Salinger and Summers (1993), starting from the earliest observation available in Compustat for

each company:

Ki,0 = PPEi,0

Ki,t =πt

πt−1(1−δt)Ki,t−1 + Ii,t

where PPE is Property, Plant and Equipment, and π and δ are the price level and depreciation rate, respectively.7

The regression specification is as follows:

Ii,t

Ki,t= βσ ·σd

i,t−1 +βq ·qi,t−1 + ct + fi + εi,t (1.1)

where σdi,t−1 is the average implied volatility from options with a time horizon of d across all trading days in

the previous quarter (i.e., t−1). This is derived as described in Appendix 1.8.1 from listed equity options on

firm i’s stock that expire in d days. In using the lagged value of implied volatility, we are assuming that the

cash flow associated with a firm’s investment decision does not appear on the company’s financial statements

until the following quarter. This timing assumption allows for a variety of plausible factors including (1) a

7We use the Producer Price Index for Finished Capital Equipment Goods as a measure of the relevant price level and assume a quarterlydepreciation rate of 2.5 percent.

8

delay between a manager’s observation of uncertainty over expected profitability and her resulting investment

decision, (2) time to build, and (3) time to pay given typical invoice deadlines of 60–90 days. We perform a

variety of robustness checks that allow for adjustments to this timing assumption; the results are reported in

Appendix 1.8.2.

Much of the existing literature posits that uncertainty affects investment though marginal Tobin’s q, that

is, the ratio between the value and cost of an additional unit of capital.8 This relationship is highlighted by

Dixit and Pindyck (1994), who show that in the presence of investment irreversibility, uncertainty affects the

threshold value of q at which firms choose to invest. In particular, a higher degree of uncertainty increases the

threshold value of q above which investment occurs.9 A persistent challenge throughout the literature is the

lack of a suitable empirical measure of marginal q. We face the same problem and adopt the common measure

of average Tobin’s q, calculated as the ratio of the market value of the firm’s capital stock to the replacement

cost of the capital:10

q =Debt+Market Capitalization−Current Assets

K + Inventory+ Intangibles+ Investment & Advances

Including q as an explanatory variable serves two purposes. First, q is a natural control for the first moment

effect of the expected return on capital on firms’ investment decisions. Without such a control, our estimates

would suffer from omitted variable bias. Second, the inclusion of q allows us to compare our results with

those found by other researchers. For example, Leahy and Whited (1996) find a positive relationship between

Tobin’s q and investment and a negative relationship between uncertainty (proxied by stock price volatility

forecasts based on realized returns) and investment when each explanatory variable is considered separately;

however, when both q and uncertainty are included in the regression specification, they find that neither

coefficient estimate is statistically significant.11 With these prior findings in mind, we test whether uncertainty

and Tobin’s q have a role in driving investment patterns when we improve upon both the measurement of

uncertainty and the identification strategy.12

8Abel and Eberly (1994) note that marginal q is equivalent to the expected present value of the stream of marginal products of capital in amultiperiod model.

9In addition, Abel and Eberly (1994) develop a model that nests the model of Abel (1983) and an irreversible investment model. Theyshow that under general assumptions investment depends only on marginal q and the capital stock; that is, uncertainty affects investmentonly through marginal q.

10Perfect competition and constant returns to scale are necessary—though not sufficient—for average q and marginal q to be equal (seeHayashi, 1982).

11Leahy and Whited (1996) interpret this finding as evidence that uncertainty operates through the first moment of returns. However,it is important to emphasize that such a conclusion is not technically possible using this empirical test. Recall that in a world withconstant returns to scale and perfect competition, uncertainty has no effect on investment. As illustrated in Dixit and Pindyck (1994),without these conditions, uncertainty only affects investment through marginal q. In the absence of constant returns to scale or perfectcompetition, marginal q is not equal to average q. Therefore, an empirical specification using average q cannot conclusively test thetheory’s prediction that the effect of uncertainty on investment operates exclusively through marginal q.

12Kogan (2004) examines the direct relationship between Tobin’s q and stock price volatility. His general equilibrium model predicts anon-linear relationship between q and asset price volatility as prices absorb demand shocks in some states of the world. As suggestedby these predictions, we estimate the relationship between our implied volatility and Tobin’s q data series and find evidence of such

9

We estimate Equation 1.1 in first differences to eliminate the firm fixed effects ( fi) and to address the serial

correlation between consecutive error terms in the levels equation. All specifications include time controls to

capture the effect of the macroeconomic environment on firm investment. In some specifications, we include

the level of the S&P 500 Index, while in others we take a non-parametric approach and include quarterly time

fixed effects (ct ). As mentioned earlier, the instrumental variable estimates we present in the next section rely

on data that is only available for manufacturing firms (SIC Groups 2 and 3). As a result, we restrict our sample

to these 2,230 firms to ensure the Ordinary and Two-Stage Least Squares results are comparable. In addition,

we require the firms in our sample to have a prior year of non-missing data for both Tobin’s q and implied

volatility. This further reduces the sample to 1,807 firms and 35,835 observations. We report Ordinary Least

Squares results for the full Compustat-Option Metrics merged data set in Appendix 1.8.5.

As reported in Table 1.3, we find a negative and strongly statistically significant coefficient estimate of

−0.0282 for uncertainty as measured by the change in the one-quarter lag of 91-day implied volatility. Given

a standard deviation of implied volatility of 0.24 in our data sample, a one standard deviation increase in

uncertainty is associated with a 0.7% decline in the quarterly investment rate. The average firm in our sample

has an investment rate of 5.2%. Thus, this decrease is equivalent to an economically significant decrease in

investment of 13.0% for the average firm.

Table 1.3: OLS Regressions

(1) (2) (3) (4) (5) (6)D.I/K D.I/K D.I/K D.I/K D.I/K D.I/K

LD.91d vol -0.0282∗∗∗ -0.0242∗∗∗ -0.0235∗∗∗ -0.0176∗∗∗ -0.0189∗∗∗ -0.0120∗

(0.00496) (0.00500) (0.00607) (0.00621) (0.00640) (0.00658)

LD.Tobin’s q 0.00233∗∗∗ 0.00237∗∗∗ 0.00237∗∗∗

(0.000362) (0.000364) (0.000365)

LD.SPX level -0.0000117∗∗∗ -0.0000212∗∗∗ -0.0000157∗∗∗ -0.0000268∗∗∗

(0.00000369) (0.00000369) (0.00000402) (0.00000411)

LD.SPX 91d vol -0.0211∗∗ -0.0292∗∗∗

(0.0104) (0.0106)

Quarterly fixed effects X X

N 35835 35835 35835 35835 35835 35835∗ p < 0.10, ∗∗ p < 0.05, ∗∗∗ p < 0.01. Standard errors clustered by firm are reported in parentheses.

Note: Sample includes quarterly observations 1/1996–10/2009 for manufacturing (SIC Groups 2 and 3) firms with a prior year of data for impliedvolatility and Tobin’s q. The dependent variable is the quarterly change (“D”) in a firm’s investment rate (I/K). Explanatory variables includethe lagged differences (“LD”) of 91-day implied volatility from the firm’s equity options (“91d vol”), Tobin’s q, and the level and options-implied volatility of the S&P 500 Index (“SPX level” and “SPX 91d vol”). Quarterly time fixed effects are included in some specifications(denoted by a checkmark).

non-linearities. The results of this exercise are presented in Appendix 1.8.7.

10

When included as an additional explanatory variable, the coefficient estimate for Tobin’s q is positive and

statistically significant. Consistent with findings elsewhere in the literature, the coefficient estimate of 0.00233

implies an unreasonably large adjustment cost (equal to the reciprocal of the coefficient on q). This is likely

due to the susceptibility of the numerator in the calculation of Tobin’s q to market bubbles and noise. In strong

contrast to the findings of Leahy and Whited (1996), when both Tobin’s q and the uncertainty measure are

included in the specification, the negative coefficient estimate for uncertainty and positive coefficient estimate

for Tobin’s q remain statistically significant (with p-values of less than one percent). As we would expect

if a portion of the effect of uncertainty on investment operates through the first-moment effect of expected

returns, the coefficient estimate for implied volatility is smaller in magnitude when Tobin’s q is included in the

regression specification.

Specifications (3) and (4) include the implied volatility from S&P 500 Index options as a control for

market-wide, systematic uncertainty, allowing us to isolate the relationship between changes in firm-specific

idiosyncratic uncertainty and changes in investment. The coefficient estimate for S&P 500 implied volatility

indicates a negative relationship between market-wide uncertainty and firm-level investment. This is consistent

with the observation that market implied volatility tends to increase in periods of recession; periods when firm

investment typically declines.13

Controlling for systematic uncertainty, we find a negative and statistically significant coefficient estimate for

idiosyncratic uncertainty regardless of whether Tobin’s q is included. Given a standard deviation of 0.07 for the

91-day implied volatility of the S&P 500 Index, a one standard deviation increase in market-wide uncertainty

is associated with a 0.1% decline in a firm’s investment rate. The estimated relationship between systematic

uncertainty and investment is therefore smaller than the relationship between idiosyncratic uncertainty and

investment, according to which a one standard deviation increase in uncertainty is associated with a 0.6%

decrease in the investment rate.

To emphasize the pivotal role played by our use of implied volatility as a proxy measure of uncertainty,

we perform the same analysis using the realized volatility of stock returns. We calculate quarterly realized

volatility for each firm as the average of the rolling 90-day standard deviation of daily returns across all of the

trading days in each quarter. (The timing is thus consistent with our quarterly measure of implied volatility.)

Figure 1.2 presents the distributions of 91-day implied volatility and realized volatility in our data sample. The

implied and realized volatility measures have the same mean (0.52), but realized volatility has a slightly higher

standard deviation (0.28 versus 0.24 for implied volatility) and a higher kurtosis (10.4 versus 5.0 for implied

13Note that with time-varying volatility and risk-averse investors, option-implied volatility is the sum of expected volatility and a riskpremium. Risk premia vary over time and tend to be countercyclical. In a regression of investment on option-implied volatility, anegative coefficient may therefore reflect firms’ responses to high risk premia rather than to increases in uncertainty. Assuming the riskpremium is a primarily macroeconomic variable, the inclusion of time fixed effects or S&P 500 implied volatility controls for the effectof changing risk premia on firm investment patterns.

11

Figure 1.2: Distributions of Implied and Realized Volatility

volatility). As kurtosis is a measure of the peakedness of the distribution, the higher kurtosis for realized

volatility means that more of its variance is the result of infrequent extreme deviations, as opposed to frequent

modestly sized deviations. This is consistent with the observation that implied volatility is often a smoother

(and less noisy) series than realized volatility (Schwert, 2002).

Table 1.4 reports results for Ordinary Least Squares estimation of the first-differences of Equation 1.1,

where σdi,t−1 is now realized rather than implied volatility. In the regression specifications that include the

level of the S&P 500 Index as a time control, the coefficient estimates for realized volatility are negative and

statistically significant, although less than one-third the size of the estimated coefficients for implied volatility.

In the specifications including the volatility of the S&P 500 Index or quarterly time fixed effects, the coefficient

estimates on firm-specific realized volatility are neither economically nor statistically significant. Furthermore,

when both implied volatility and realized volatility are included in the regression specification, the coefficient

on implied volatility is negative and statistically significant while the coefficient on realized volatility is neither

economically nor statistically significant. These estimation results are reported in Appendix 1.8.6. Based on

these findings, realized volatility is not nearly as strong a predictor of investment as implied volatility.

12

Table 1.4: OLS Regressions – Realized Volatility

(1) (2) (3) (4) (5) (6)D.I/K D.I/K D.I/K D.I/K D.I/K D.I/K

LD.Realized vol -0.00823∗∗∗ -0.00815∗∗∗ 0.000737 0.00123 0.000699 0.00146(0.00296) (0.00292) (0.00335) (0.00332) (0.00338) (0.00336)

LD.Tobin’s q 0.00245∗∗∗ 0.00249∗∗∗ 0.00244∗∗∗

(0.000362) (0.000363) (0.000363)

LD.SPX level -0.00000661∗ -0.0000176∗∗∗ -0.0000167∗∗∗ -0.0000284∗∗∗

(0.00000359) (0.00000353) (0.00000394) (0.00000400)

LD.SPX realized vol -0.0448∗∗∗ -0.0468∗∗∗

(0.00620) (0.00623)

Quarterly fixed effects X X

N 35835 35835 35835 35835 35835 35835∗ p < 0.10, ∗∗ p < 0.05, ∗∗∗ p < 0.01. Standard errors clustered by firm are reported in parentheses.

Note: Sample includes quarterly observations 1/1996–10/2009 for manufacturing (SIC Groups 2 and 3) firms with a prior year of data forimplied volatility, realized volatility, and Tobin’s q. The dependent variable is the quarterly change (“D”) in a firm’s investment rate (I/K).Explanatory variables include the lagged differences (“LD”) of average realized volatility of the firm’s stock price (“Realized vol”), Tobin’sq, and the level and average realized volatility of the S&P 500 Index (“SPX level” and “SPX realized vol”). Quarterly time fixed effects areincluded in some specifications (denoted by a checkmark).

1.6 Instrumental Variables Estimation

1.6.1 Endogeneity of Uncertainty

While we are interested in the effect of uncertainty on investment, the reverse relationship is likely also

relevant, with investment decisions driving the degree of uncertainty. For example, if a firm undertakes a risky

investment project, the observed implied volatility may increase to reflect the subsequently greater uncertainty

regarding future returns.14 Given the endogeneity of both investment and uncertainty, an instrumental variables

strategy is necessary. Much of the existing literature addresses this issue by using lagged values of the

dependent and explanatory variables as instruments (following the methodology of Arellano and Bond, 1991).

Instead, we suggest a natural instrument strategy and construct industry-specific exposures to energy and

currency volatility as proxies for exogenous uncertainty shocks.

In particular, following Rajan and Zingales (1998), the instruments are structured as the product of

predetermined cross-sectional intensity and time-varying volatility:

Exposurei,t ≡ Intensityi ·Volatilityt (1.2)

The instruments rely upon cross-sectional variation in predetermined measures of energy intensity-of-use and

country-specific trade volume. The role of trade volume can be thought of as follows: import trade volume in

a given industry captures foreign competition with the industry’s goods, and export trade volume captures

14Another potential source of endogeneity is the presence of a latent third factor that affects both investment and uncertainty.

13

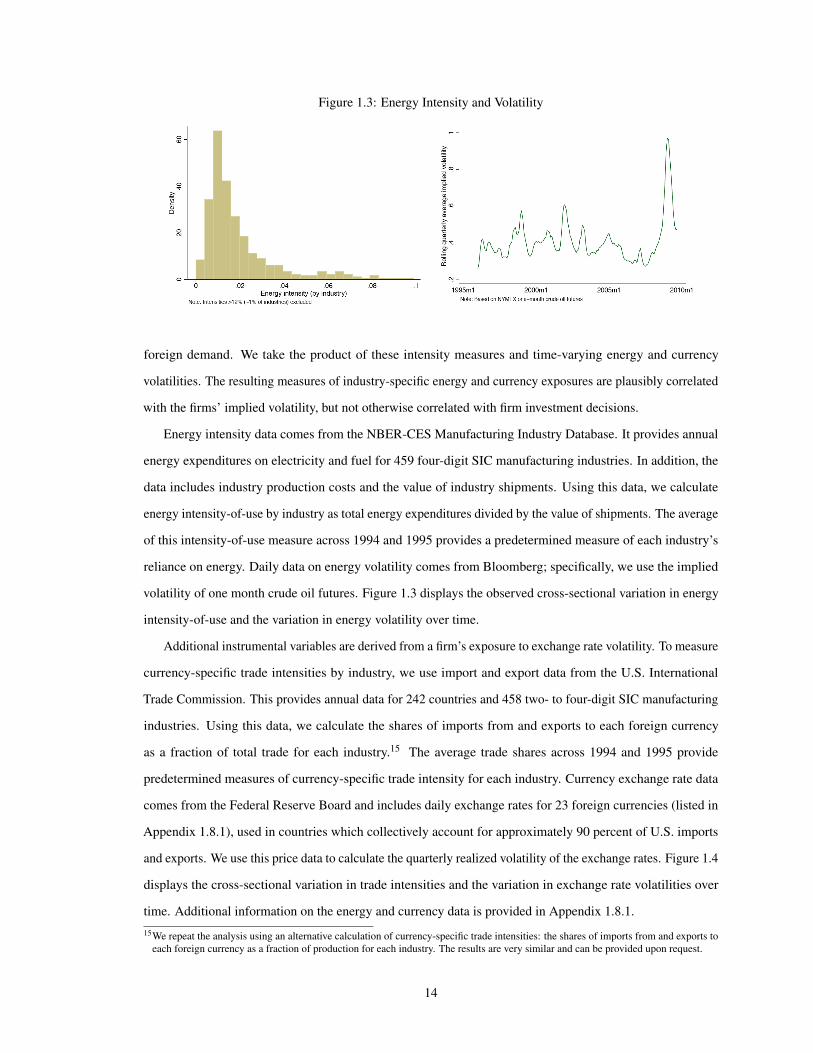

Figure 1.3: Energy Intensity and Volatility

foreign demand. We take the product of these intensity measures and time-varying energy and currency

volatilities. The resulting measures of industry-specific energy and currency exposures are plausibly correlated

with the firms’ implied volatility, but not otherwise correlated with firm investment decisions.

Energy intensity data comes from the NBER-CES Manufacturing Industry Database. It provides annual

energy expenditures on electricity and fuel for 459 four-digit SIC manufacturing industries. In addition, the

data includes industry production costs and the value of industry shipments. Using this data, we calculate

energy intensity-of-use by industry as total energy expenditures divided by the value of shipments. The average

of this intensity-of-use measure across 1994 and 1995 provides a predetermined measure of each industry’s

reliance on energy. Daily data on energy volatility comes from Bloomberg; specifically, we use the implied

volatility of one month crude oil futures. Figure 1.3 displays the observed cross-sectional variation in energy

intensity-of-use and the variation in energy volatility over time.

Additional instrumental variables are derived from a firm’s exposure to exchange rate volatility. To measure

currency-specific trade intensities by industry, we use import and export data from the U.S. International

Trade Commission. This provides annual data for 242 countries and 458 two- to four-digit SIC manufacturing

industries. Using this data, we calculate the shares of imports from and exports to each foreign currency

as a fraction of total trade for each industry.15 The average trade shares across 1994 and 1995 provide

predetermined measures of currency-specific trade intensity for each industry. Currency exchange rate data

comes from the Federal Reserve Board and includes daily exchange rates for 23 foreign currencies (listed in

Appendix 1.8.1), used in countries which collectively account for approximately 90 percent of U.S. imports

and exports. We use this price data to calculate the quarterly realized volatility of the exchange rates. Figure 1.4

displays the cross-sectional variation in trade intensities and the variation in exchange rate volatilities over

time. Additional information on the energy and currency data is provided in Appendix 1.8.1.

15We repeat the analysis using an alternative calculation of currency-specific trade intensities: the shares of imports from and exports toeach foreign currency as a fraction of production for each industry. The results are very similar and can be provided upon request.

14

Figure 1.4: Currency Intensity and Volatility

05

100

510

05

100

510

0 .2 .4 .6 .8

Canadian Dollar

Euro

Japanese Yen

Mexican Peso

Den

sity

Export share (by industry)

These measures of exposure to energy and currency volatility are used as explanatory variables in the

following first-stage regression:

σi,t = αoil ·(

Eiσoilt

)+αimp ·

(∑

jw j,imp

i σj/USD

t

)+αexp ·

(∑

jw j,exp

i σj/USD

t

)+ ct + fi +ηi,t (1.3)

where Ei is the intensity of energy use for firm i’s industry and σoilt is the implied volatility of one-month

crude oil futures in quarter t. For the currency instruments, w ji σ

j/USDt is the trade-weighted realized volatility

of the exchange rate between the U.S. dollar and j’s currency in quarter t. For example, w j,impi is the fraction

of all imports in firm i’s industry that come from countries using currency j, and w j,expi is the fraction of all

exports from firm i’s industry that go to countries using currency j. The estimation includes time controls

(either the level of the S&P 500 Index or quarterly time fixed effects, ct ) and firm fixed effects ( fi), which are

especially important to capture heterogeneity in the relationship between implied volatility and exposure to

energy volatility.16

The results of the estimation of Equation 1.3 in first-differences are reported in Table 1.5 for an implied

volatility duration of 91 days. Each of the instruments is positively correlated with changes in implied volatility,

as expected, and the relationships are strongly statistically significant. For example, in specification (2), a

one percent increase in the oil exposure variable (intensity of energy use multiplied by oil price volatility)

is associated with a 6.1 percent increase in a firm’s implied volatility, holding all else constant. Further

confirming the strength of the instruments, the F-statistic for the joint test that the instruments’ coefficients are

equal to zero is well above the commonly referenced hurdle value of ten.17 In addition, as evidenced by the

16Without firm fixed effects, the overall relationship between implied volatility and the energy exposure instrument is negative. However,this is driven by extreme differences in implied volatilities and energy exposures across industries. For example, the computer gamingindustry has high implied volatility from equity options but very low exposure to energy volatility, while the concrete industry has lowimplied volatility from equity options but high exposure to energy volatility. While the relationship between implied volatility andenergy exposure may be positive within each industry, the relationship across industries is negative.

17Stock and Yogo (2005) provide critical values for a test of weak instruments in linear instrumental variables estimation. Given a single

15

reported R-squared values, the uncertainty instruments explain between 20 and 36 percent of the variation in

firm-specific implied volatility.

Table 1.5 also reports results for a specification that includes the implied volatility from S&P 500 Index

options as an additional control. Controlling for market-wide uncertainty drastically changes the estimated

coefficients on the currency instruments. The coefficient for import uncertainty shocks is economically and

statistically indistinguishable from zero and the coefficient for export uncertainty shocks is negative. These

changes are likely driven by the high correlation between market-wide uncertainty and the volatility of currency

prices.

Table 1.5: Volatility Partial First Stage

Hypothesis (1) (2) (3) (4)D.91d vol D.91d vol D.91d vol D.91d vol

D.Import curr vol shock + 0.416∗∗∗ 0.350∗∗∗ -0.0289 0.140∗∗∗

(0.0591) (0.0562) (0.0381) (0.0424)

D.Export curr vol shock + 1.008∗∗∗ 0.916∗∗∗ -0.208∗∗∗ 0.509∗∗∗

(0.0586) (0.0567) (0.0435) (0.0698)

D.Oil vol shock + 6.390∗∗∗ 6.124∗∗∗ 2.191∗∗∗ 2.516∗∗∗

(0.635) (0.619) (0.352) (0.449)

D.SPX level -0.000101∗∗∗ 0.0000456∗∗∗

(0.00000612) (0.00000593)

D.SPX 91d vol 1.321∗∗∗

(0.0223)

Quarterly fixed effects X

N 35835 35835 35835 35835F: All instruments = 0 1087.7 808.3 36.96 41.21R-squared 0.197 0.205 0.327 0.364∗ p < 0.10, ∗∗ p < 0.05, ∗∗∗ p < 0.01. Standard errors clustered by firm are reported in parentheses.

Note: Sample includes quarterly observations 1/1996–10/2009 for manufacturing (SIC Groups 2 and 3) firms with aprior year of data for implied volatility and Tobin’s q. The dependent variable is the quarterly change (“D”) in the91-day implied volatility from a firm’s equity options (“91d vol”). Explanatory variables include the changes inthe currency and energy volatility exposure instruments as well as in the level and options-implied volatility of theS&P 500 Index (“SPX level” and “SPX 91d vol”). Quarterly time fixed effects are included in some specifications(denoted by a checkmark).

1.6.2 Endogeneity of Tobin’s q

As with uncertainty, the exogeneity of Tobin’s q is unlikely. Again, much of the existing literature addresses

this issue by using lagged values of the dependent and explanatory variables as instruments. Instead, we pursue

a natural instrument strategy similar to what we use for uncertainty, but use industry-specific exposures to

energy and currency prices—rather than volatilities—as proxies for exogenous profitability shocks.

endogenous variable and three excluded instruments, a critical value of ten corresponds to a five to ten percent bias of the IV estimatorrelative to the OLS estimator and a Wald test size of fifteen to twenty percent.

16

The instruments for Tobin’s q are structured as:

Exposurei,t ≡ Intensityi ·Pricet (1.4)

The predetermined measures of cross-sectional energy intensity-of-use and currency-specific trade shares

are the same as those used for the volatility instruments. We take the product of the intensity measures and

time-varying energy and currency prices.18 The resulting measures of industry-specific energy and currency

exposures are plausibly correlated with the expected return on capital captured by a firm’s value of Tobin’s q,

but not otherwise correlated with the firm’s investment decisions.

Partial first stage results are reported in Table 1.6 (partial in the sense that the formal first-stage regression

will include the full set of both volatility and Tobin’s q instruments). We expect the coefficients for the import

and export instruments to be negative. An increase in the exchange rate is a depreciation of the foreign currency

relative to the U.S. dollar. This makes imports into the U.S. relatively cheap, hurting firms’ competitive position

relative to foreign firms. It also hurts the ability of domestic firms to sell their products abroad. Consistent

with these stories, we find negative and statistically significant coefficient estimates for the import and export

instrumental variables.

We also expect the coefficient on the energy instrument to be negative: a firm in an industry that uses

energy more intensively is expected to be less profitable when oil prices rise. Again, the results are consistent

with this prediction. The coefficient estimate on the energy instrument is negative and strongly statistically

significant after controlling for quarterly time effects. In all four first-stage specifications (with and without

quarterly time fixed effects, as well as with controls for the level and implied volatility of the S&P 500 Index),

the instrument variables for Tobin’s q are jointly significant with F-statistics well above ten. The reported

R-squared values range from 0.2 to 9 percent. The fact that we explain only a small fraction of the variation in

Tobin’s q is not surprising given the multitude of factors relevant for expected stock price returns. Exposures

to energy and currency prices are likely only a small subset of these potential factors.

The complete first-stage regression results are reported in Table 1.7. The full instrument set includes the

instruments for both implied volatility and Tobin’s q. Given the exogeneity of each group of instruments,

the combined set is jointly exogenous. All of the findings highlighted in the tables looking separately at the

validity of the instruments for implied volatility and Tobin’s q carry over to the full first-stage regression.19

18The crude oil price series used for the energy instrument is the deseasoned natural logarithm of the deflated price series provided byBloomberg.

19Stock and Yogo (2005) provide critical values for a test of weak instruments in linear instrumental variables estimation. Given twoendogenous variables and six excluded instruments, a critical value of ten corresponds to a five to ten percent bias of the IV estimatorrelative to the OLS estimator and a Wald test size of fifteen to twenty percent.

17

Table 1.6: Tobin’s q Partial First Stage

Hypothesis (1) (2) (3) (4)D.Tobin’s q D.Tobin’s q D.Tobin’s q D.Tobin’s q

D.Import curr price shock - -0.00971∗∗∗ -0.00592∗∗∗ -0.00596∗∗∗ -0.00833∗∗∗

(0.00174) (0.00168) (0.00168) (0.00180)

D.Export curr price shock - -0.00810∗∗∗ 0.000260 0.0000529 -0.00787∗∗∗

(0.00158) (0.00164) (0.00165) (0.00181)

D.Oil price shock - 6.592∗∗∗ -8.667∗∗∗ -7.999∗∗∗ -6.421∗∗∗

(1.292) (1.539) (1.483) (1.652)

D.SPX level 0.00443∗∗∗ 0.00449∗∗∗

(0.000152) (0.000173)

D.SPX 91d vol 0.259(0.241)

Quarterly fixed effects X

N 35835 35835 35835 35835F: All instruments = 0 49.74 14.62 14.30 20.07R-squared 0.00248 0.0590 0.0591 0.0868∗ p < 0.10, ∗∗ p < 0.05, ∗∗∗ p < 0.01. Standard errors clustered by firm are reported in parentheses.

Note: Sample includes quarterly observations 1/1996–10/2009 for manufacturing (SIC Groups 2 and 3) firms with a prioryear of data for implied volatility and Tobin’s q. The dependent variable is the quarterly change (“D”) in a firm’s Tobin’sq. Explanatory variables include the changes in the currency and energy price exposure instruments as well as in thelevel and options-implied volatility of the S&P 500 Index (“SPX level” and “SPX 91d vol”). Quarterly time fixed effectsare included in some specifications (denoted by a checkmark).

1.6.3 Two-Stage Least Squares Results

Using the fitted values from the first-stage regressions for volatility and Tobin’s q, we estimate the following

second-stage regression:Ii,t

Ki,t= βσ · σ̂d

i,t−1 +βq · q̂i,t−1 + ct + fi + εi,t

The results are reported in Table 1.8. In specifications (1) and (2), we control for time effects using the

level of the S&P 500 Index. Here, we find a negative and strongly statistically significant coefficient on

firm-specific implied volatility. Importantly, the coefficient estimates are larger in magnitude than the OLS

estimates presented in Section 1.5. This is evidence of potential reverse causation. Suppose a firm undertakes

an investment project and the market does not know whether this is a high or low quality investment. This

uncertainty regarding future returns will be reflected in a higher expected volatility of the firm’s stock price. In

this scenario, the OLS estimates will be biased towards zero since they fail to account for the endogeneity of

the uncertainty measure.

Specifications (3) and (4) include the implied volatility of the S&P 500 Index as a measure of market-

wide uncertainty. Recall that the inclusion of S&P 500 implied volatility generates surprising coefficient

estimates for the currency instruments in the first-stage regressions. As a result, we are hesitant to draw

strong conclusions from the results for these specifications. However, with this qualification in mind, it is

valuable to highlight the dramatically different effects of idiosyncratic versus systematic uncertainty. The

18

Table 1.7: Full First Stage Regression

(1) (2) (3) (4) (5) (6)D.Tobin’s q D.Tobin’s q D.Tobin’s q D.91d vol D.91d vol D.91d vol

D.Import curr vol shock 1.856∗∗∗ 2.004∗∗∗ -1.232∗ 0.350∗∗∗ -0.0408 0.126∗∗∗

(0.678) (0.698) (0.678) (0.0565) (0.0387) (0.0434)

D.Export curr vol shock -0.781 -0.346 -2.667∗∗∗ 0.915∗∗∗ -0.231∗∗∗ 0.486∗∗∗

(0.624) (0.669) (0.836) (0.0573) (0.0449) (0.0720)

D.Oil vol shock 8.268∗∗∗ 9.428∗∗∗ 10.20∗∗∗ 5.495∗∗∗ 2.442∗∗∗ 2.387∗∗∗

(2.443) (2.415) (2.823) (0.555) (0.341) (0.416)

D.Import curr price shock -0.00668∗∗∗ -0.00676∗∗∗ -0.00740∗∗∗ -0.0000128 0.000175∗ 0.000286∗∗

(0.00164) (0.00164) (0.00179) (0.000118) (0.0000990) (0.000112)

D.Export curr price shock -0.000319 -0.000469 -0.00658∗∗∗ 0.00000751 0.000404∗∗∗ 0.000343∗∗

(0.00159) (0.00159) (0.00181) (0.000140) (0.000127) (0.000161)

D.Oil price shock -4.655∗∗∗ -5.027∗∗∗ -3.121∗ -0.627∗∗∗ 0.352∗∗∗ -0.174(1.438) (1.472) (1.713) (0.149) (0.127) (0.145)

D.SPX level 0.00456∗∗∗ 0.00450∗∗∗ -0.000100∗∗∗ 0.0000469∗∗∗

(0.000163) (0.000173) (0.00000609) (0.00000590)

D.SPX 91d vol -0.505 1.330∗∗∗

(0.361) (0.0225)

Quarterly fixed effects X X

N 35835 35835 35835 35835 35835 35835F: All instruments = 0 10.79 11.36 12.86 406.5 25.52 23.35R-squared 0.0594 0.0595 0.0873 0.206 0.328 0.364∗ p < 0.10, ∗∗ p < 0.05, ∗∗∗ p < 0.01. Standard errors clustered by firm are reported in parentheses.

Note: Sample includes quarterly observations 1/1996–10/2009 for manufacturing (SIC Groups 2 and 3) firms with a prior year of data forimplied volatility and Tobin’s q. The dependent variable is the quarterly change (“D”) in a firm’s Tobin’s q in columns (1)–(3), and in the91-day implied volatility from its equity options (“91d vol”) in columns (4)–(6). Explanatory variables include the changes in the currencyand energy volatility and price exposure instruments as well as in the level and options-implied volatility of the S&P 500 Index (“SPX level”and “SPX 91d vol”). Quarterly time fixed effects are included in some specifications (denoted by a checkmark).

implied volatility of S&P 500 Index options has a positive and statistically significant coefficient, suggesting a

positive relationship between market-wide uncertainty and firm investment after controlling for idiosyncratic

uncertainty.

In specifications (5) and (6), we include quarterly time fixed effects rather than controls for the level and

implied volatility of the market. After removing all common time variation in the first-stage regression, the

instrumental variables estimation does not have sufficient power to generate precise estimates for the effect of

firm-specific uncertainty. In other words, there is not enough variation among the first-stage fitted values. This

is evidenced by the large standard errors for the 2SLS estimates. Given the magnitude of the standard errors,

we cannot reject that the coefficient estimate of 0.0223 in specification (5) is statistically different from the

estimate of −0.0483 in specification (1).

19

Table 1.8: Two-Stage Least Squares Estimation

(1) (2) (3) (4) (5) (6)D.I/K D.I/K D.I/K D.I/K D.I/K D.I/K

LD.91d vol -0.0483∗∗∗ -0.0608∗∗∗ -0.128∗∗∗ -0.158∗∗∗ 0.0223 0.0251(0.00751) (0.00890) (0.0421) (0.0452) (0.0352) (0.0302)

LD.Tobin’s q 0.0147∗∗∗ 0.00861∗∗ 0.00390(0.00475) (0.00420) (0.00350)

LD.SPX level -0.0000169∗∗∗ -0.0000862∗∗∗ -0.0000106∗∗∗ -0.0000485∗∗∗

(0.00000388) (0.0000226) (0.00000407) (0.0000187)

LD.SPX 91d vol 0.109∗∗ 0.144∗∗

(0.0528) (0.0565)

Quarterly fixed effects X X

N 35835 35835 35835 35835 35835 35835∗ p < 0.10, ∗∗ p < 0.05, ∗∗∗ p < 0.01. Standard errors clustered by firm are reported in parentheses.