bankmuscatsaog e.pdf · cbo central bank of oman ccl commercial companies law of oman as contained...

TRANSCRIPT

Prospectus

W i t h y o u , a l w a y s .

www.bankmuscat.com

BankMuscatSAOG

Issue Price of RO 1.010 per Bond(comprising a face value of RO 1.000 and 10 Baizas towards Issue expenses)

Issueof8%SubordinatedBonds

Issue Opens : 8th April 2009 | Issue Closes : 7th May 2009

Issue Manager:

Regd Office: BankMuscat SAOG, P.O. Box 134, P.C 112, Ruwi, Sultanate of OmanTel: 24768888, Fax: 24798220

BankMuscat S.A.O.G.P.O. Box 134, Ruwi

Postal Code 112Sultanate of Oman

Tel: 2476 8888 Fax: 2479 8220

Issue of 60,000,000 Subordinated Bonds at an Issue Price of RO 1.010 per Bond(comprising a face value of RO 1.000 and 10 Baizas towards Issue expenses)

Issue opens on: April 8, 2009

Issue closes on: May 7, 2009

Issue Manager

P.O. Box: 134, Postal Code: 112,Ruwi, Sultanate of Oman

Tel: 24768888; Fax: 24798220URL: www.bankmuscat.com

Registrar & TrusteeMuscat Depositary and Securities Registration Company SAOC

P.O Box 952, Ruwi, PC 112, Sultanate of OmanTel: 24822222; Fax: 24817491

This is an unofficial English version of the original Prospectus prepared in Arabic and approved by the Capital Markets Authority pursuant to the Administrative Order no 04/2009 dated March 29, 2009. In the event of any conflict between the Arabic version and the English version, the Arabic version will prevail. Although every effort has been made in preparing this translation, neither the Issuer nor the Issue Manager shall be held responsible for any information interpreted differently from the approved Arabic Prospectus.

اأعــــــمــــــال بــــنـــوك الإ�ســــتـــــثـــــمـــــار

I n v e s t m e n t B a n k I n g

BankMuscat SAOG

�

IMPORTANT NOTICE

All Investors are requested to read the following notice carefully.

The principal aim of this Prospectus is to present material information that may assist investors to make an appropriate decision as to whether or not to invest in the securities offered.

This Prospectus includes all relevant material information and data that is deemed important and neither includes any misleading information nor excludes any material information the omission of which may materially influence any investor’s decision pertaining to the investment in the Subordinated Bonds through this Prospectus.

Directors of BankMuscat SAOG are responsible for the authenticity of the information contained in this Prospectus and the same has been prepared in good faith. All reasonable care has been taken to include material information and no such information has been omitted, the omission of which would render this Prospectus misleading.

All investors should examine and carefully review this Prospectus and make their own independent investigation and examination of the financial conditions and affairs of BankMuscat SAOG in order to decide whether or not it would be appropriate to invest in the securities offered taking into consideration all the information contained in the Prospectus in its context.

With respect to this issue of Subordinated Bonds under this Prospectus, no one has any authority to give any information or make any representation other than those contained in this Prospectus and if any information is given or representation is made, it should not be relied upon by anyone.

The Capital Market Authority assumes no responsibility for the accuracy and adequacy of the statements and information included in this Prospectus nor shall have any liability for any damage or loss resulting from the reliance upon or use of any part of the same by any person.

BankMuscat SAOG

�

TABlE Of CONTENTS

Section Particulars Page No.

I Definitions and Interpretation 4

II Credit Rating 7

III Risk Factors and Mitigants 13

IV Subordinated Bond Issue Summary 15

V Issuer’s Objectives & Licenses 17

VI Purpose of the Bond issue and issue expenses 19

VII Terms and conditions of the Bond Issue 20

VIII Rights and responsibilities 28

IX Related Party Transactions 31

X Historical financial performance 33

XI Corporate snapshot, Business plan and future strategy 104

XII Board of Directors, Corporate Governance and Management 108

XIII Subscription Conditions and Procedures 117

XIV Undertakings 123

BankMuscat SAOG

�

SECTION IDEfINITIONS AND INTERPRETATION

Definitions

Agency Agreement The agreement between the Issuer and the MDSRC for the

MDSRC to act as the Trustee

ALCO Asset Liability Committee

Articles Articles of Association of the Issuer, as may be amended from time to time in accordance with the provisions as contained therein

BankMuscat/Issuer Bank Muscat SAOG

Board / Board of Directors Issuer’s Board of Directors elected in accordance with the Articles

Bonds 60,000,000 Subordinated Bonds with a nominal value of RO 1.000 (Rial Omani One) per bond and issued at a price of RO 1.010 (Rial Omani One and Ten Baiza) aggregating to RO 60,600,000 (Rial Omani Sixty Millon Six Hundred Thousand) to be issued hereunder. The Issuer shall have the right to accept applications for an additional 15,000,000 (Fifteen Million) Bonds in case of an oversubscription as set out in Chapter XIII of this Prospectus.

Bond eligible for redemption The Bonds will be redeemed in full in the form of a single bullet at the end of the 7th year from the Issue Date

Bondholders A holder of a bond issued by the Issuer pursuant to this Issue

Bondholders’ Resolution A resolution passed at a meeting of Bondholders duly convened and held in accordance with the provisions of the Trust Deed and in accordance with the applicable provisions of the CCL

Business Day A day in which banks and the Registrar are open for business in Oman

CBO Central Bank of Oman

CCL Commercial Companies Law of Oman as contained in Royal Decree 4/74 and the amendments thereto.

CMA Capital Market Authority of Oman

CMA Law Capital Market Law of Oman as contained in Royal Decree 80/98

BankMuscat SAOG

�

Collecting Banks Means BankMuscat SAOG, National Bank of Oman SAOG, Bank Dhofar SAOG and Oman Arab Bank SAOC.

Conditions The terms and conditions of the issue of Bonds as set out in Section VII of this Prospectus

Directors Means a member of the Board of Directors

Event of Default Any of the events described in Condition 21 of Section VII of this Prospectus

Financial Year The financial year of the Issuer commencing from 1st January and ending on 31st December or as may be amended by the shareholders in accordance with the Issuer’s Articles of Association

Interest Due Dates The dates until which interest is payable for the respective periods for which interest accrues in accordance with the terms of the bond issue.

Interest Payment Date 15th May and 15th November. Interest will be paid to all Bondholders whose name appears on

the Bondholders’ Register as on the Interest Payment Date.

Issue Date means 8th May 2009

Issuer Rating Standard & Poors’ (S&P): BBB+ (January 2009) Moody’s: A2 (September 2008) Fitch: A- (November 2008) Capital Intelligence: A (June 2008)

Issue Price / Offer Price RO 1.010 per bond including Baizas 10 towards issue expenses

Laws of Oman The laws of Oman in the form of Royal Decrees, Ministerial Decisions, CMA and CBO Regulations as the same may have been, or may from time to time be enacted, amended or re-enacted or issued

MDSRC/Registrar Muscat Depository and Securities Registration Company SAOC, P.O. Box 952, Ruwi, Postal Code 112, Oman

MOCI Ministry of Commerce and Industry of Oman

MSM Muscat Securities Market

Oman The Sultanate of Oman

Prospectus Means this Prospectus

BankMuscat SAOG

�

Register The Register to be maintained by the Registrar in which information relating to the Bonds and the Bondholders shall be recorded

Rial Omani or RO Omani Rial, which is the lawful currency of Oman. Each Omani Rial is equivalent to 1000 baizas.

Section Section of this Prospectus

Shares Shares issued by the Issuer with a face value of RO 0.100 (Baizas one hundred each)

Shareholders The shareholders of the Issuer

Subscription Period The period from 8th April, 2009 and ending 7th May, 2009 (both days inclusive)

Trust Deed The trust deed being entered into between the Issuer and MDSRC

Trustee MDSRC or any successor body thereto and includes all persons who may be appointed trustee under the terms of the Trust Deed to act for and on behalf of the bondholders as their representative

INTERPRETATIONS

In this Prospectus:

• Headings and underlining are for convenience only and do not affect the interpretation of the Prospectus.

• Words importing the singular include the plural and vice versa.

• An expression importing a natural person includes any juristic person.

• In case a day in which a transaction is required to be entered in to pursuant to the terms and conditions in Section VII and such day is not a Business Day, then the transaction will take place immediately on the following Business Day.

BankMuscat SAOG

�

SECTION IICREDIT RATING

Issuer Rating

The Issuer has been assigned ratings by four leading rating agencies of international repute namely Moody’s Investor Service (“Moody’s”), Fitch Rating (“Fitch”) and Standard & Poor’s (“S&P”) and Capital Intelligence (“CI”). For any debt issuance in Oman the rating of the issuer is limited by Oman’s sovereign rating. The Issuer rating is one notch below the sovereign rating of Oman.

Summary of the Ratings

Moody’s fitch S&P CI

BankMuscat Entity Rating

Long Term A2 A- BBB+ A

Financial Strength / Outlook C-/Stable Stable Stable A-/Stable

Moody’s Investor Service

Moody’s is a leading global credit rating, research and risk analysis firm, publishes credit opinions, research and ratings on fixed income securities, issuers of securities and other credit obligations. The firm provides credit ratings and analysis on more than $30 trillion of debt covering approximately 67,000 US public finance obligations, and 136,000 corporate, government, and structured finance securities. Moody’s maintains relationships with 29,000 US public finance issuers, as well as 12,000 corporate and financial institutions and 96,000 structured finance issuers, and 100 sovereign nations. Moody’s is a subsidiary of Moody’s Corporation (NYSE:MCO), which employs approximately 3,600 employees in 29 countries and had reported revenue of $2.3 billion in 2007. Additional information is available at www.moodys.com.

• Moody’s Issuer Rating

The deposit ratings for the Issuer are set at A2.

Moody’s Rating – Definitions

Aaa Banks rated Aaa for deposits offer exceptional credit quality and have the smallest degree of risk. While the credit quality of these banks may change, such changes as can be visualized are most unlikely to materially impair the banks’ strong positions.

Aa Banks rated Aa for deposits offer excellent credit quality, but are rated lower than Aaa banks because their susceptibility to long-term risks appears somewhat greater. The margins of protection may not be as great as with Aaa-rated banks, or fluctuations of protective elements may be of greater amplitude.

BankMuscat SAOG

�

A Banks rated A for deposits offer good credit quality. However, elements may be present that suggest a susceptibility to impairment over the long term.

Baa Banks rated Baa for deposits offer adequate credit quality. However, certain protective elements may be lacking or may be characteristically unreliable over any great length of time.

Ba Banks rated Ba for deposits offer questionable credit quality. Often the ability of these banks to meet punctually deposit obligations may be uncertain and therefore not well safeguarded in the future.

B Banks rated B for deposits offer generally poor credit quality. Assurance of punctual payment of deposit obligations over any long period of time is small.

Caa Banks rated Caa for deposits offer extremely poor credit quality. Such banks may be in default, or there may be present elements of danger with regard to financial capacity.

Ca Banks rated Ca for deposits are usually in default on their deposit obligations.

C Banks rated C for deposits are usually in default on their deposit obligations, and potential recovery values are low.

Note: Moody’s applies numerical modifiers 1,2 and 3 in each generic rating classification from Aa through Caa. The modifier 1 indicates that the obligation ranks in the higher end of its generic rating category; the modifier 2 indicates a mid-range ranking; and the modifier 3 indicates a ranking in the lower end of that generic rating category.

fitch

Fitch is dual-headquartered in New York and London, operating offices and joint ventures in more than 49 locations and covering entities in more than 90 countries, including insurer financial strength ratings on over 2,000 insurance companies. Fitch is a majority-owned subsidiary of Fimalac, S.A., an international business support services group headquartered in Paris, France.

• fitch’s Issuer Rating:

The rating assigned to the Issuer is A-.

BankMuscat SAOG

�

fitch Ratings – Definitions

The following rating scale applies to foreign currency and local currency ratings:

Investment Grade

AAAHighest credit quality. ‘AAA’ ratings denote the lowest expectation of credit risk. They are assigned only in case of exceptionally strong capacity for payment of financial commitments. This capacity is highly unlikely to be adversely affected by foreseeable events.

AAVery high credit quality. ‘AA’ ratings denote expectations of very low credit risk. They indicate very strong capacity for payment of financial commitments. This capacity is not significantly vulnerable to foreseeable events.

AHigh credit quality. ‘A’ ratings denote expectations of low credit risk. The capacity for payment of financial commitments is considered strong. This capacity may, nevertheless, be more vulnerable to changes in circumstances or in economic conditions than is the case for higher ratings.

BBBGood credit quality. ‘BBB’ ratings indicate that there are currently expectations of low credit risk. The capacity for payment of financial commitments is considered adequate but adverse changes in circumstances and economic conditions are more likely to impair this capacity. This is the lowest investment grade category.

Speculative Grade

BBSpeculative. ‘BB’ ratings indicate that there is a possibility of credit risk developing, particularly as the result of adverse economic change over time; however, business or financial alternatives may be available to allow financial commitments to be met. Securities rated in this category are not investment grade.

BHighly speculative. ‘B’ ratings indicate that significant credit risk is present, but a limited margin of safety remains. Financial commitments are currently being met; however, capacity for continued payment is contingent upon a sustained, favorable business and economic environment.

CCC, CC, CHigh default risk. Default is a real possibility. Capacity for meeting financial commitments is solely reliant upon sustained, favorable business or economic conditions. A ‘CC’ rating indicates that default of some kind appears probable. ‘C’ ratings signal imminent default.

DIndicates an entity or sovereign that has defaulted on all of its financial obligations. Default generally is defined as one of the following:

BankMuscat SAOG

10

• Failure of an obligor to make timely payment of principal and/or interest under the contractual terms of any financial obligation;

• The bankruptcy filings, administration, receivership, liquidation or other winding-up or cessation of business of an obligor;

• The distressed or other coercive exchange of an obligation, where creditors were offered securities with diminished structural or economic terms compared with the existing obligation.

Issuers will be rated 'D' upon a default. Defaulted and distressed obligations typically are rated along the continuum of 'C' to 'B' ratings categories, depending upon their recovery prospects and other relevant characteristics.

Default is determined by reference to the terms of the obligations' documentation. Fitch will assign default ratings where it has reasonably determined that payment has not been made on a material obligation in accordance with the requirements of the obligation's documentation, or where it believes that default ratings consistent with Fitch's published definition of default are the most appropriate ratings to assign Notes: Gradations may be used among the five ratings: i.e. A/B, B/C, C/D, and D/E. (s) An Individual rating may be followed by the suffix (s), denoting that it is largely based on public information, though supplemented by data obtained from the rated entity.

S&P’s

S&P’s, a division of The McGraw-Hill companies, is the world’s foremost provider of independent credit ratings, indices, risk evaluation, investment research, data, and valuations. With 8,500 employees located in 23 countries, S & P’s is an essential part of the world’s financial infrastructure and has played a leading role for more than 145 years in providing investors with the independent benchmarks about their investment and financial decisions. Additional information about the company is available at www.standarrdandpoors.com

• S&P’s long-Term Issuer Credit Rating

The rating assigned to the issuer is BBB+

S&P’s Ratings – Definitions

AAAAn obligor rated ‘AAA’ has extremely strong capacity to meet its financial commitments. ‘AAA’ is the highest issuer credit rating assigned by Standard & Poor’s. AAAn obligor rated ‘AA’ has very strong capacity to meet its financial commitments. It differs from the highest-rated obligors only to a small degree.

BankMuscat SAOG

11

AAn obligor rated ‘A’ has strong capacity to meet its financial commitments but is somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories. BBBAn obligor rated ‘BBB’ has adequate capacity to meet its financial commitments. However, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity of the obligor to meet its financial commitments. BB, B, CCC, and CCObligors rated ‘BB’, ‘B’, ‘CCC’, and ‘CC’ are regarded as having significant speculative characteristics. ‘BB’ indicates the least degree of speculation and ‘CC’ the highest. While such obligors will likely have some quality and protective characteristics, these may be outweighed by large uncertainties or major exposures to adverse conditions.

BBAn obligor rated ‘BB’ is LESS VULNERABLE in the near term than other lower-rated obligors. However, it faces major ongoing uncertainties and exposure to adverse business, financial, or economic conditions which could lead to the obligor’s inadequate capacity to meet its financial commitments. BAn obligor rated ‘B’ is more vulnerable than the obligors rated ‘BB’, but the obligor currently has the capacity to meet its financial commitments. Adverse business, financial, or economic conditions will likely impair the obligor’s capacity or willingness to meet its financial commitments on the obligation. CCCAn obligor rated ‘CCC’ is CURRENTLY VULNERABLE, and is dependent upon favorable business, financial, and economic conditions to meet its financial commitments.

CCAn obligor rated ‘CC’ is CURRENTLY HIGHLY- VULNERABLE. Plus (+) or minus (-)The ratings from ‘AA’ to ‘CCC’ may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories.

CI

CI has been providing credit analysis and ratings since 1985, and now rates over 400 Banks, Corporates and Financial Instruments (Bonds & Sukuk) in 39 countries. A specialist in emerging markets, CI’s geographical coverage includes the Middle East, the wider Mediterranean region, Central and Eastern Europe, South Asia, South-East Asia, the Far East, and North and South Africa

• CI’s long-Term Issuer Credit Rating

The rating assigned to the Issuer is A.

BankMuscat SAOG

1�

Capital Intelligence Ratings – Definitions

Investment Grade

AAA The highest credit quality. Exceptional capacity for timely fulfilment of financial obligations and most unlikely to be affected by any foreseeable adversity. Extremely strong financial condition and very positive non-financial factors. AA Very high credit quality. Very strong capacity for timely fulfilment of financial obligations. Unlikely to have repayment problems over the long term and unquestioned over the short and medium terms. Adverse changes in business, economic and financial conditions unlikely to affect the institution significantly. A High credit quality. Strong capacity for timely fulfilment of financial obligations. Possesses many favourable credit characteristics but may be slightly vulnerable to adverse changes in business, economic and financial conditions. BBB Good credit quality. Satisfactory capacity for timely fulfilment of financial obligations. Acceptable credit characteristics but some vulnerability to adverse changes in business, economic and financial conditions. Medium grade credit characteristics and the lowest investment grade category.

Speculative GradeBB Speculative credit quality. Capacity for timely fulfilment of financial obligations is vulnerable to adverse changes in internal or external circumstances. Financial and/or non-financial factors do not provide significant safeguard and the possibility of investment risk may develop. B Significant credit risk. Capacity for timely fulfilment of financial obligations very vulnerable to adverse changes in internal or external circumstances. Financial and/or non-financial factors provide weak protection; high probability for investment risk exists. C Substantial credit risk is apparent and the likelihood of default is high. Considerable uncertainty as to the timely repayment of financial obligations. Credit is of poor standing with financial and/or non-financial factors providing little protection. RS Regulatory supervision (this rating is assigned to financial institutions only). The obligor is under the regulatory supervision of the authorities due to its weak financial condition. The likelihood of default is extremely high without continued external support. SD Selective default. The obligor has failed to service one or more financial obligations but CI believes that the default will be restricted in scope and that the obligor will continue honouring other financial commitments in a timely manner. D The obligor has defaulted on all, or nearly all, of its financial obligations.

BankMuscat SAOG

1�

SECTION IIIRISk fACTORS AND MITIGANTS

Investors should note that the risks and the corresponding mitigating factors described below are not exhaustive and represent the opinion and perception of the Bank only. The actual impact of the risks could be different from those mentioned.

General Risks

a) Economic Risk

The Bank’s performance is primarily dependent on the economic environment of Oman in which it operates. Any sustained change in the economic environment could have an impact on the Bank’s underlying performance.

The Bank has a well-experienced and stable management, and operates with prudent and

conservative policy of credit and credit control. The Bank is confident that in case of overall macro economic downturn, it will be in a position to minimize the negative effect if any, on the business performance.

b) Change in Regulations

The Bank is under the supervision of CBO, CMA and MOCI in Oman as well as the Saudi Arabia Monitory Authority in respect of its operations in Saudi Arabia. Any change in the prevailing regulatory climate in Oman and Saudi Arabia could have a consequent impact on the performance of the Bank.

As the largest bank in Oman by total assets, the Bank has the necessary organizational structure, highly skilled manpower and infrastructure to adapt to such changes in a short span of time with minimal cost and minimum impact to the business.

Specific Risks

a) Competition

The Bank faces competition from other commercial and specialized banks in Oman. This could result in increased pressure on business volumes as well as margins with a consequent impact on profitability.

The Bank follows a customer centric business approach by providing quality service and wide range of products. Being the market leader in Oman with a market share of 43.74% in terms of total assets as of November 2008, the Bank continuously prepares itself to face the competition in this dynamic financial market. It takes proactive steps to meet the challenges of competition.

b) Credit Risk

Perhaps the major risk faced by the Bank is the risk that loans given to customers are not repaid fully in a timely fashion. This could be attributable to a problem impacting the individual credit or to systematic portfolio weakness.

BankMuscat SAOG

1�

The Bank has set for itself clear and well defined limits to address different dimensions of credit risk including concentration risk. Procedures for day-to-day management of credit risk are determined by the business heads within the scope of the business policies and risk policy of the Bank. The Bank addresses credit risk through various processes such as; establishing an appropriate credit risk environment, operating under a sound credit granting process, maintaining an appropriate credit administration, measurement, monitoring and reporting process and ensuring adequate controls over credit risk. The Bank’s classified loans portfolio is adequately covered with specific provisions. In addition, the Bank creates general provision on standard loans and advances as per CBO regulations.

c) Liquidity Risk

Liquidity risk is the potential inability of the Bank to meet its maturing obligations to counter-party.

In order to ensure that the Bank can meet its financial obligations as and when they fall due, there is a close monitoring of the assets/liabilities position. Liquidity risk management ensures that the Bank has the ability under varying scenarios to fund increase in assets and meet maturing obligations, as they arise. The ALCO evaluates the balance sheet both from a structural as well as liquidity and interest rate sensitivity point of view.

d) Interest Rate Risk

Interest rate risk is the risk that the Bank’s profitability will be affected by changes in interest rates and mis-matches or gaps in the amount of assets and liabilities and off-balance sheet items that mature or are re-priced in a given period.

The responsibility for interest rate risk management rests with the ALCO. The interest rate maturity profile of assets and liabilities is carefully monitored by the ALCO in its meetings through the use of interest rate gap reports and sensitivity analysis facilitated by sophisticated asset-liability management system. In order to manage the Bank’s interest rate risks, the Bank uses limit structures, which inter-alia include limits relating to positions, portfolios and stop losses.

e) Foreign Exchange Risk

Foreign exchange risk is the risk that the foreign currency positions taken by the Bank may be adversely affected due to volatility in foreign exchange rates.

The responsibility for management of foreign exchange risk rests with the treasury of the Bank. The Bank’s foreign exchange exposures are governed by the treasury policy, and the risk policy approved by the Board of Directors. Foreign exchange risk management in the Bank is ensured through regular measurement and monitoring of open foreign exchange positions against approved limits. Most of the foreign exchange transactions carried out by the division is on behalf of corporate customers and all are on a back-to-back basis.

BankMuscat SAOG

1�

SECTION IVSuBORDINATED BOND ISSuE SuMMARy

Issuer BankMuscat SAOG Registered Office of Issuer P.O. Box 134, PC 112, Ruwi, Oman

Instrument offered Fixed Rate Subordinated Bonds

Maturity of the Bond The Bonds shall have a maturity of seven years from the Issue Date

Interest rate 8% per annum of the face value of the bond

Interest payments Semi-annually, payable in arrears on 15th May and 15th November each year. The first payment of interest will be on 15th November 2009.

Bond Issue Size RO 60,000,000 (Rial Omani Sixty Million). If the Issue is oversubscribed, the Issuer may increase the Issue size by a further 15,000,000 (Fifteen Million) Bonds up to a maximum of RO 75,000,000 (Rial Omani Seventy Five Million) subject to the approval of the concerned authorities

Number of Bonds 60,000,000 Bonds. In case of an oversubscription, the Issuer shall have the right to accept applications for an additional 15,000,000 (Fifteen Million) Bonds as set out in Chapter XIII of this Prospectus.

Allotment In case of any over-subscription or under-subscription of the

Issue, allotment will be done according to Article 65 of the CCL. The final allotment on the above basis will be decided by the Issue Manager and the Issuer in consultation with the CMA.

Face Value of the Bond RO 1.000 each payable in full on subscription

Issue price RO 1.010 per bond including Baizas 10 towards issue expenses

Security The Bonds will constitute direct, unconditional, subordinated and unsecured obligations of the Issuer, ranking pari passu without any preference among themselves and equally with all other existing and future unsecured and subordinated obligations of the Issuer save for such obligations that may be preferred by provisions of law that are mandatory and of general application.

Minimum and Maximum Applications must be for a minimum of 100 Bonds and Subscription in multiples of 100 thereafter

BankMuscat SAOG

1�

Use of Proceeds Proceeds of the issue will be utilised for general banking

purposes of the Bank.

Period of subscription 8th April 2009 to 7th May, 2009

Listing The Bank will apply for the Bonds to be listed on the MSM.

Date of Allotment Expected to occur within 15 days of the Closing Date.

Trustee and Registrar MDSRC

Collecting Banks BankMuscat SAOG, National Bank of Oman SAOG, Bank Dhofar SAOG and Oman Arab Bank SAOC

Issuer’s Auditor PriceWaterhouse Coopers LLP

Suites 204-210, Hatat House, Wadi Adai, P.O. Box 3075, PC 112 Muscat, Oman Tel: 968 24559110,

Fax: 968 24564408 http://www.pwc.com/me.

Financial Advisor & Issue BankMuscat SAOGManager Investment Banking Division P.O. Box 134, PC 112 Ruwi, Oman Tel: 24768888 Fax: 24798220

Legal Advisor to the Issue Al Busaidy, Mansoor Jamal & Co. P.O. Box 686, P.C. 112, Ruwi Oman Tel: 24706666/24787777

Rial Omani or RO Omani Rial, which is the lawful currency of Oman. Each Omani Rial is equivalent to 1,000 baizas

Value of the Bond issued Upto RO 60,000,000 (Rial Omani Sixty calculated by nominal million). If the issue is oversubscribed the Issuer may value increase the issue size upto a maximum amount of

RO 15,000,000 (Rial Omani Fifteen million) subject to the approval of the concerned authorities.

The issue of the Bonds was authorized by:

1. The resolution of the Board of Directors of the Issuer passed on October 26, 2008;2. The CBO vide their letter no. BDD/CBS/BM/2009/1370 dated March 3, 2009 and letter

no. BDD/CBS/BM/2009/1803 dated March 18, 2009 approving the Issue; and3. The Shareholders of the Issuer at an Extra-ordinary General Meeting held on March 24,

2007 approving the Issue of Rial Omani denominated Bonds .

BankMuscat SAOG

1�

SECTION VISSuER’S OBjECTIVES AND lICENCES

Objectives as set out in the Article of Association:

Pursuant to Article 4 of the Articles of Association, the Bank is empowered to carry on all commercial and investment banking activities in accordance with the license issued by the CBO and the Banking Law promulgated by the Royal Decree No. (114/2000) and its amendments, including the financing of trade and projects, the making of studies and the undertaking of research and matters connected therewith, for the Bank’s own account and for that of third parties, and of all activities including the acquiring or disposing of any rights, whether as owner or otherwise, in relation to real property, which are supplementary to such activities or connected therewith and which are requisite for the purpose of banking or investment business and subject to the provisions of Article (65) and (66) of the Banking Law. These objectives shall be subject to the laws applied in Oman from time to time, CBO circulars and subject to the approvals of the regulatory bodies as the case may be.

licenses issued by competent authorities authorizing the activities carried out by the Issuer:

BankMuscat carries out its activities pursuant to the following licenses granted to it:• Commercial registration from the MOCI No. 1/14573/8 dated 6th November 1982• CBO banking license dated 30 May 1999. • CBO Investment Banking license dated 30 May 1999.• CMA Annual license for carrying out capital market related lines of activity which is valid

till December 31, 2009 and due for renewal thereafter.

Statement of all issues of securities made in the last three years

Position as on December 31, 2005:

As on December 31, 2005, the Bank’s authorized share capital stood at RO 125,000,000 (Rial Omani One Hundred Twenty Five Million) consisting of 125,000,000 (One Hundred Twenty Five Million) shares of RO 1 (Rial Omani One) each. 75,666,424 (Seventy Five Million Six Hundred and Sixty Six Thousand Four Hundred and Twenty Four) shares of RO 1 (Rial Omani One) each had been issued and fully paid up as on that date

During the last three years, the share capital has changed as follows:

Changes during the year 2006:

During the year 2006, in the Annual General Meeting held on March 19, 2006, the shareholders approved the bonus issue proposed by the Board for the year ended December 31, 2005 and pursuant to that resolution 7,566,642 (Seven Million Five Hundred and Sixty Six Thousand Six Hundred and Forty Two) shares of RO 1 (Rial Omani One) each were issued as bonus shares.

In the same Annual General Meeting, the shareholders also resolved for a share split of the nominal value of the Bank’s shares from RO 1 (Rial Omani One) each to a nominal value of RO 0.100 (One Hundred Baizas) each.

BankMuscat SAOG

1�

As on December 31, 2006, the Bank’s authorized share capital stood at RO 125,000,000 (Rial Omani One Hundred Twenty Five Million) consisting of 1,250,000,000 (One Billion Two Hundred and Fifty Million) Shares. 832,330,650 (Eight Hundred and Thirty Two Million Three Hundred and Thirty Thousand Six Hundred and Fifty) Shares had been issued and fully paid up as on that date.

Changes during the year 2007:

During the year 2007, in the Annual General Meeting the shareholders approved the bonus issue proposed by the Board of Directors and pursuant to that resolution 83,233,065 (Eighty Three Million Two Hundred and Thirty Three Thousand Sixty Five) Shares were issued as bonus.

During November 2007, the Bank issued 161,570,000 (One Hundred and Sixty One Million Five Hundred and Seventy Thousand) Shares at RO 1.475 (Rials Omani One and Baizas Four Hundred and Seventy Five) per Share in the form of a private placement to Dubai Financial Group, a financial institution registered in Dubai, UAE. The transaction was closed and ordinary shares were allotted on 19 November 2007. The share premium on each Share sold to Dubai Financial Group was RO 1.375 (Rials Omani One and Baizas Three Hundred and Seventy Five).

As on December 31, 2007, the Bank’s authorized share capital stood at RO 125,000,000 (Rial Omani One Hundred Twenty Five Million) consisting of 1,250,000,000 (One Billion Two Hundred and Fifty Million) Shares. 1,077,133,715 (One Billion Seventy Seven Milion One Hundred and Thirty Three Thousand Seven Hundred and Fifteen) Shares each had been issued and fully paid up as on that date.

Changes during the year 2008:

During the year 2008, the share capital of the Bank remained at 31st Dec 2007 levels and no new shares were issued in the form of bonus shares or otherwise. As on 31st December 2008 the Bank’s authorized share capital stood at RO 125,000,000 (Rial Omani One Hundred Twenty Five Million) consisting of 1,250,000,000 (One Billion Two Hundred and Fifty Million)Shares. 1,077,133,715 (One Billion Seventy Seven Milion One Hundred and Thirty Three Thousand Seven Hundred and Fifteen) Shares had been issued and fully paid up as on that date.

BankMuscat SAOG

1�

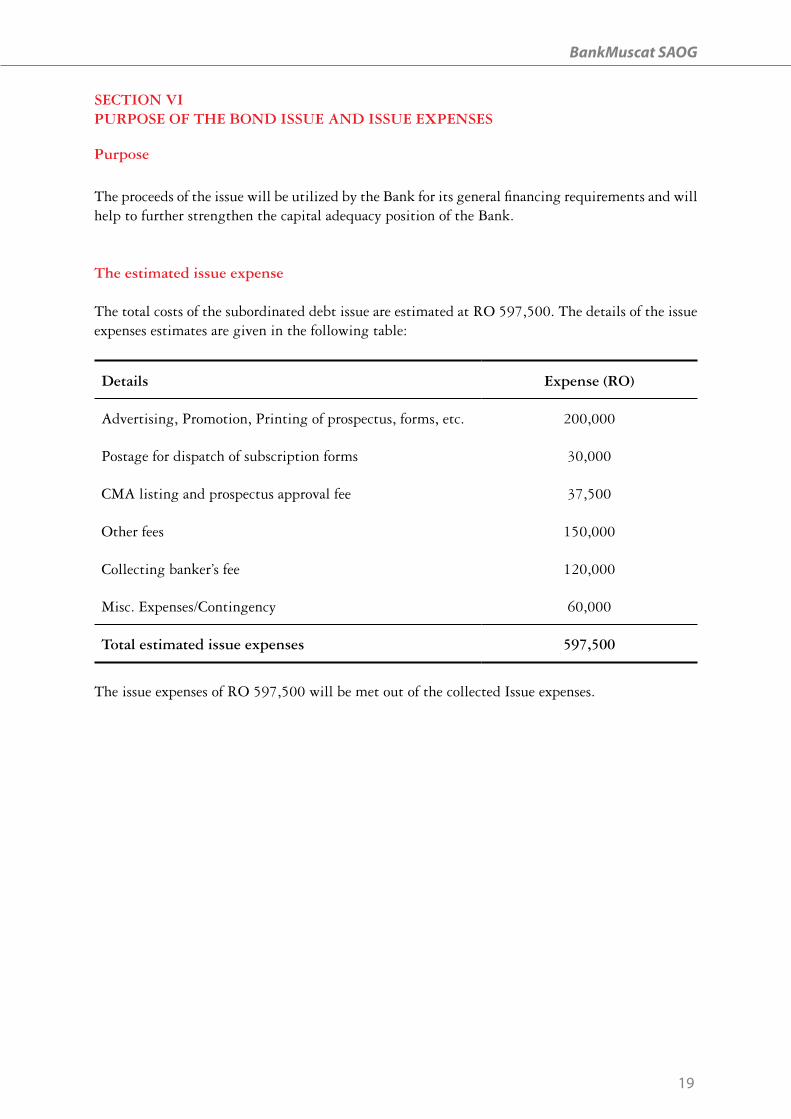

SECTION VIPuRPOSE Of THE BOND ISSuE AND ISSuE ExPENSES

Purpose

The proceeds of the issue will be utilized by the Bank for its general financing requirements and will help to further strengthen the capital adequacy position of the Bank.

The estimated issue expense

The total costs of the subordinated debt issue are estimated at RO 597,500. The details of the issue expenses estimates are given in the following table:

Details Expense (RO)

Advertising, Promotion, Printing of prospectus, forms, etc. 200,000

Postage for dispatch of subscription forms 30,000

CMA listing and prospectus approval fee 37,500

Other fees 150,000

Collecting banker’s fee 120,000

Misc. Expenses/Contingency 60,000

Total estimated issue expenses 597,500

The issue expenses of RO 597,500 will be met out of the collected Issue expenses.

BankMuscat SAOG

�0

SECTION VIITERMS AND CONDITIONS Of THE SuBORDINATED BOND ISSuE

1. The Issue

The Bonds will be created and issued by the Bank which is incorporated and registered as a Company in the Commercial Register maintained by the MOCI (C.R. No 1/14573/8) and as a Commercial Bank in Oman. The Issue is governed and has been made pursuant to the Articles and the Laws of Oman.

2. Nominal Value & Issue Price

Each Bond shall have a nominal value of RO 1.000 (Rial Omani One) and the Issue Price of RO 1.010 (Rial Omani One and Baizas Ten) and is inclusive of RO 0.010 (Baizas Ten) as Issue Expenses.

3. Allotment and issue of Bonds

The Issue Manager will make efforts to complete the allotment of Bonds within fifteen Business Days from the date on which the issue closes for subscription, subject to the approval of all relevant authorities.

4. Oversubscription

If the Issue is oversubscribed, the Issuer may increase the issue size by 15,000,000 (Fifteen Million) Bonds up to a maximum amount of RO 75,000,000 Rial Omani Seventy Five Million, subject to the approval of the concerned authorities.

5. Redemption

The Bonds shall be redeemed in full, by way of cheque, or electronic transfer at the Issuer’s discretion, to be made out in favour of the then registered holders thereof, on such date as will be seven years from the Issue date. The redemption date of the Bonds shall be 7 (Seven) years from the Issue Date. The Bonds are not redeemable at the initiative of the Bondholder or without the consent of the CBO.

6. Title

The MDSRC shall act as the Registrar and transfer agent with respect to the Bonds and shall also act as the Trustee in accordance with the terms of a Trust Deed which shall be entered into by and between the Bank and the Trustee. The title to the Bonds passes on the recordation of the transfer in the Bondholders Register maintained by the MDSRC. The registered owner of the Bonds save as otherwise required by the Laws of Oman will be treated as the absolute owner of the Bonds for all purposes.

7. Interest payments

Interest on the Bonds shall accrue with effect from the Issue Date. All further interest payments shall take place semi-annually in arrears, on the Interest Payment Dates shown below. Those payments will be made to the Bondholders’ on the designated record dates for each Interest Payment Date.

Interest Payment Date 15th May15th November

BankMuscat SAOG

�1

If the maturity date or an interest payment date for the Bonds fall on a date that is not a Business Day, that payment will be made on the next Business Day as if it were the date that payment was due and no interest will accrue from and after the original payment date. The first payment of interest will be on 15th November 2009. The final interest payment date shall be for the six month period ending 7th May 2016.

The interest payments shall be made to the Bondholders whose names appear on the Registrar as of the designated record date relative to the relevant Interest Payment Date. The record date for the same will be 3 Business Days prior to the Interest Payment Date. Interest payments shall be made by cheque or electronic transfer, at the discretion of the Issuer, payable to registered holders as at the time of commencement of trading on the respective interest payment dates. Interest cheques (or electronic payments) will be mailed by registered mail to respective Bondholders within one week of the respective Interest Payment Dates.

8. Interest rate

Interest shall be calculated on the nominal value of the Bond at an interest rate of 8% (Eight percent) per annum. The interest rate shall remain fixed at the aforesaid rate for the entire tenor of the Bond. Interest calculation shall be made on the basis of a 360 (Three Hundred and Sixty) day year consisting of 12 (Twelve) months of 30 (thirty) days each and in case of an incomplete month, the number of days elapsed.

9. Default interest

In the event that any interest payable by the Issuer under conditions 7, 8 and 21 of this terms and conditions is not paid on the due-date or otherwise in the manner provided by conditions 7, 8 and 21, the Issuer shall pay default interest at the rate of 1% p.a. (One percent per annum) over and above the applicable rate of interest on the overdue sum from the date of default up to the date of actual certification by the Issuer to the Trustee that payments have been made. So long as the default continues, the default interest shall continue to accrue on the same basis and shall be compounded annually.

10. listing on the MSM

The Bonds shall be listed on the MSM. The Issue Manager shall complete all the formalities relating to the trading of the Bonds on the MSM.

11. Registration of Transfers

The administration of registration of transfers of Bonds shall be maintained by MDSRC, the transfer agent which is normally responsible for maintaining the register of Shares, bonds and other listed securities of all companies listed on the MSM. MDSRC will act as the Registrar to the Bonds and maintain a register setting out the names and addresses, the number of Bonds held and the bank account details of the Bondholders.

12. Trading and transferability of Bonds and restrictions on transferability

The Registrar will maintain a separate register of Bondholders, in which the Registrar will record transfers of Bonds that take place through trading on the MSM. Transfers may be made for a minimum of one Bond and transfer of any fractional bond shall not be allowed. Bondholders may sell their Bonds, or acquire additional Bonds, through the MSM by placing either a sell order, or a buy order, through any MSM registered stockbroker. Trading through the MSM, as well as settlements and transfers through that market shall be governed under the rules applicable to trading of corporate bonds issued by MSM and

BankMuscat SAOG

��

the Laws of Oman.

The buyer shall provide his/her details to his/her broker who will in turn provide the buyer’s details to the register of the bond in the buyer’s name. Bonds may be pledged, donated or bequeathed by notifying the register to facilitate all necessary formalities.

The MDSRC will effect the registration of transfer of any Bonds. Any charges levied by the registrar shall be borne by the buyer and the seller of the Bonds in accordance with the regulations. All transfers of Bonds and entries on the register of the Bondholders as maintained by the Registrar will be made subject to the regulations concerning transfer of Bonds.

13. Variation of rights

The terms and conditions attaching to the Bonds shall be capable of amendment under the following circumstances:

13.1 In the event that any term or condition thereof needs to be amended in order to comply with the Laws of Oman, or change in the Laws of Oman, or any regulation of CBO, the CMA, the CBO, the MSM, or MOCI, the Issuer shall be entitled to enforce such change or amendment forthwith, on condition that each holder of the Bond shall be duly notified by registered mail of such amendment, within 14 days.

13.2 In the event that the Issuer intends proposing any other amendment or variation to the terms and conditions attaching to the Bonds, it shall call a meeting of Bondholders for such purpose, who shall be entitled to consider, and vote upon such variation or amendment by way of formal meeting to be held, other than as specifically provided for herein, in accordance with procedures similar to that applying to general meetings of shareholders of companies under the CCL and the Laws of Oman.

14. Meetings of the Bondholders, modifications and waiver

The Trust Deed contains provision for convening meetings of Bondholders as per the CCL that considers matters affecting their interest as proposed by the Issuer, including the modification of any of these Conditions or any provisions of the Trust Deed. Any such modification may be made if sanctioned by a Bondholders’ Resolution as provided for in the Trust Deed. A Bondholders’ Resolution shall not be valid unless the meeting convened to consider the same is attended by personally or by proxy, a number of Bondholders representing at least two-thirds of the Bonds outstanding. The procedure for giving notice of a meeting of the Bondholders shall be as follows:

14.1 A meeting of the Bondholders may be called by the Issuer following a board resolution ordering such, by the statutory auditors of the Issuer, or by the Issuer at the request, in writing, of Bondholders representing at least two thirds of the then outstanding Bonds.

14.2 Within 14 days of receipt of such a request, or an authorizing board resolution, the Issuer shall, at its cost, issue a notice of meeting of the Bondholders which shall be published in two Arabic newspapers for two consecutive days and also sent by post to registered Bondholders, in each case, not less than 15 days prior to the appointed date of the meeting.

14.3 A notice of a meeting of the Bondholders shall contain details of the place, date and time of the meeting, accompanied by a description of the agenda of the meeting setting out the main purpose and businesses of the meeting. The venue of the meeting shall always be

BankMuscat SAOG

��

within a distance of 50 kilometers from the registered head office of the Issuer.

14.4 Any Director of the Issuer, the secretary of the Issuer, or in the absence of aforementioned, a registered Bondholder in person, duly appointed at the meeting, may preside as the Chairman of a meeting of the Bondholders.

14.5 A quorum for purposes of a meeting of the Bondholders shall be such persons representing at least two-thirds of the Bonds, the Bondholders may be present or represented at the meeting by way of written proxy, of the Bonds then outstanding as at the date of the notice of meeting. Failing such quorum a second meeting shall be convened to discuss the same agenda. Notice for the second meeting shall be issued in the same manner as set out in Condition 14.2 provided however, that the notice for the second meeting shall be published and dispatched to Bondholders not less than one week prior to the scheduled date of the second meeting. For the purposes of a quorum being present at the second meeting, the presence of Bondholders representing at least one-third of the Bonds shall be sufficient provided such second meeting is held within one month from the date of the first meeting. However, in the event that the meeting of Bondholders has been called in order to pass a resolution, which extends the redemption period of the Bonds, or reduces the interest rate on the Bonds or resolves to take any step, which is prejudicial to the rights of the Bondholders, such resolution shall not be passed unless the meeting is attended by Bondholders representing two-thirds of the Bonds.

14.6 In all circumstances, voting shall take place by way of a poll, in terms whereof each Bond shall represent 1 (One) vote. Resolutions shall be adopted by a two-thirds majority of the Bonds represented at the meeting through Bondholders present in person or through proxy

14.7 Notwithstanding any other matters on which a Bondholders’ Resolution would be required, Bondholders’ Resolution will be required in case of any proposal made by the Issuer to:

i) modify the maturity of the Bonds or the dates on which interest is payable in respect of the Bonds

ii) reduce or cancel the principal amount or interest on the Bonds or modify the date of payment in respect of the Bonds

iii) change the currency of payment of the Bondsiv) modify or cancel the conversion rights or alter the conversion periods in respect of the

Bondsv) sanction the exchange or substitution of the Bonds for, or the conversion of the Bonds into,

notes, debentures, debenture stock or other obligations or securities of the Issuer or any other body corporate formed or to be formed

14.8 Trustee may agree as per the powers vested in it by the Trust Deed without the consent of the Bondholders’, to (i) any modification of any of the provisions of the Trust Deed which is of a formal, minor or technical nature or is made to correct a manifest error, and (ii) any other modification (except as mentioned in the Trust Deed), and any waiver or authorization of any breach or proposed breach, of any of the provisions of the Trust Deed which does not, in the sole the opinion of the Trustee materially prejudice the interests of the Bondholders. Any such modification, authorization or waiver shall be binding on the Bondholders and, if the Trustee so requires, shall be notified by the Issuer to the Bondholders as soon as is reasonably practicable. In the event that the Issuer fails to notify the Bondholders within a reasonable period of time, the Trustee shall be at liberty to notify the Bondholders.

14.9 In connection with the exercise of its functions (including but not limited to those in relation to any proposed modification, authorization or waiver) the Trustee shall have regard to the

BankMuscat SAOG

��

interests of the Bondholders as a class and shall not have regard to the consequences of such exercise for individual Bondholders and the Trustee shall not be entitled to require, nor shall any Bondholder be entitled to claim from the Issuer any indemnification or payment in respect of any tax consequences of any such individual Bondholders.

15. further Issues

The Issuer shall be at liberty from time to time to make further issues of Bonds or any other debt instrument in accordance with the CCL and the Laws of Oman.

16. Security & Bondholder’s Claim over the Assets

The Bonds will be unsecured and subordinated to the senior debt. Articles 85, 86 and 87 of the Banking Law of 2000 set out the priority of payments on the liquidation of a bank. Assets held by the bank in a fiduciary capacity are excluded from the general pool of assets and must be distributed to the specified beneficiaries of those assets. Priority is also given to payment of all liquidation expenses (including fees of the administrator). The remaining assets of the bank in liquidation are distributed pursuant to Article 87 on a pro-rata basis in the following order of priority:

• unpaid monthly salaries within the limit of three months or R.O. 1,000, whichever is less, plus employees’ claims related to other entitlements

• claims by the Deposit Insurance Scheme, as a guarantor to the deposits

• claims of the CBO

• claims of “other creditors” of the bank in liquidation

In respect of repayment of principal and interest represented by the Bonds, the Bondholders will be unsecured and subordinated to Senior Liabilities of the Bank and form a part of the Issuer’s Subordinated Liabilities. The rights of the Bondholders in respect of repayment of principal and interest represented by the Bonds will, however, rank pari passu with all other Subordinated Liabilities of the Issuer and have priority over payment to Shareholders.

It is recorded that the subordinated Bonds are specifically intended to comply with the requirements of the regulations and laws applicable to banks registered and incorporated in Oman as they relate and refer to second tier (Tier II) capital.

In this Clause:“Senior Liabilities” mean liabilities of the Issuer, which are repayable ahead of Subordinated Liabilities and Share Capital; and“Subordinated Liabilities” mean liabilities of the Issuer, which are repayable after payment of Senior Liabilities and ahead of Share Capital.

17. Status

The Bonds constitute a direct obligation of the Issuer and shall, save for such exceptions as may be provided for by the Laws of Oman, at all times rank pari passu without any preference among themselves.

18. Covenants

As long as any Bond remains Outstanding (as defined in the Trust Deed), the Issuer shall duly obtain and maintain in full force and effect all governmental approvals (including any exchange control and transfer approvals) which, as a result of any change in, or amendment

BankMuscat SAOG

��

to, the Laws of Oman, such charge or amendment taking place as are necessary or advisable under the Laws of Oman for the execution, delivery and performance of the Bonds by the Issuer for the validity or enforceability for the Bonds and shall obtain all necessary governmental and administrative approvals in Oman in order to make all payments to be made under the Bonds as required by the terms of the Issue.

19. Corporate reorganization

In case of any consolidation, amalgamation or merger of the Issuer with any other corporate entity (other than a consolidation, amalgamation or merger in which the Issuer is the continuing entity), or in case of any sale or transfer of all, or substantially all, of the assets of the Issuer, the Issuer will forthwith notify the Bondholders of such event and (so far as legally possible) cause the corporate entity resulting from such consolidation, amalgamation or merger or the corporate entity which shall have acquired such assets, as the case may be, to execute a trust deed supplemental to the trust deed (in form and substance satisfactory to the trustee) whereby such entity assumes the obligations of the Issuer under the trust deed.

20. Ratings

The Issuer has been rated by four leading credit rating agencies in the World namely S&P, Moody’s, Fitch and CI. The long term ratings given by these agencies to the Issuer are shown in the table below:

Rating Agency RatingS&P BBB+Moody’s A2Fitch A-CI A

The Issuer shall give the Bondholder the right to surrender the Bonds after five years from the date of the Issue and every five years thereafter if the Issuers credit rating falls below the level indicating its ability to discharge its obligations.

The Issuer has entered into long term rating agreements with Moody’s & Fitch for rating its debt issuances. The Issuer undertakes to keep its rating under surveillance for the entire tenor of the Bond. The ratings are reviewed annually or earlier at the discretion of the rating agency

21. Events of Default

Following shall be treated as ‘Events of Default’ in connection with the Bonds being issued:

1. The Issuer fails to pay any interest in respect of the Bonds until a period of 45 days after the relevant interest payment date.

2. An order has been issued or legislation passed directing the liquidation of the Issuer.

3. The Issuer has stopped or intends to stop the payment of its debts generally or ceases to carry on business or substantially the whole of its business.

4. The Issuer sells, transfers or otherwise disposes of, directly or indirectly, the whole or a substantial part of its undertaking or assets except a disposal at market value or in the ordinary course of its business or a disposal the terms of which have previously been approved

BankMuscat SAOG

��

by the majority of not less than two-thirds in value of the bondholders. For this purpose, a certificate from the Auditors of the Issuer for the time being shall be obtained stating that, in its opinion, the business or assets disposed off is not substantial. Such a certificate shall be conclusive evidence.

5. The Issuer becomes insolvent or is unable to pay its debts as they mature or applies for the appointment of a liquidator or takes any proceedings under the prevailing laws for a deferment, readjustment, compromise or any such arrangement with and for the benefit of the creditors.

In each of such aforesaid events of default, the Trustee shall convene a meeting of the Bondholders and, if so directed by the bondholders’ resolution, shall give notice to the Issuer that the Bond will immediately start to accrue default interest as per Condition 9 mentioned above.

22. Prescription

Claims against the Issuer in respect of principal and interest shall become time-barred unless made within the limitation periods provided by the Laws of Oman.

23. General duties and obligations of the Issuer to Bondholders

23.1 The Issuer shall conduct its business of operating a bank and financial services network in accordance with the laws of Oman, as well as all bank and securities laws and regulations as may apply to it, or become applicable to it during the period of issue of the Bonds.

23.2 The Issuer shall prepare interim and annual financial statements in accordance with the laws applicable to banks in Oman. Any Bondholder shall be entitled to be furnished with a copy of any released financial results, or Annual Report, within 14 (Fourteen) days of a written request for such, which may be made to the Issuer.

23.3 The Issuer shall, in accordance with the regulatory requirements of Oman, publish its financial results timely in at least 1 (One) Arabic and 1 (One) English language newspaper, in each interim and annual financial reporting period.

23.4 In the event that the Bonds for any reason whatsoever become delisted from the MSM while still in issue, or are at any time removed from the electronically recorded registration system, the Issuer shall be entitled to issue Bond certificates as valid documents of title in respect of any Bonds then outstanding, as substitute to the electronic recordal of ownership and title thereof.

24. Enforcement

At any time after the Bonds become due and payable, the Trustee may, at its discretion and without further notice, institute such proceedings against the Issuer as it may think fit to enforce the terms of the Trust Deed and the Bonds.

25. Other rights attaching to the Bonds

The Bonds, while being transferable, are not negotiable and cannot be dealt with as a bill of exchange or under the laws applicable to bills of exchange or similar commercial banking instrument. However, the Bonds shall be capable of being pledged, ceded, sold, bequeathed, donated or dealt with in any way as may be ordinarily allowed under the Laws of Oman in respect of listed and stock market tradable securities.

BankMuscat SAOG

��

26. Subscription period

The bond issue shall open for subscription by the shareholders on 8th April 2009 and shall close on 7th May 2009 (both days inclusive).

27. joint and fraction holdings

No joint holdings of a Bond shall be capable of registration. Each Bond shall be registered in the name of a single person, or a single legal entity. The Issuer shall not be held responsible for any misappropriation, loss or damage which any person may suffer due to a loss arising from a holding which is, directly, or indirectly jointly held. No person shall be capable of registering a fraction of a holding of a Bond.

28. Notices

Notices to the Bondholders will be sent by the Issuer by mail (airmail if overseas) at their respective addresses on the Register, and will be deemed to have been given on the date of mailing. Notices will also be published in one Arabic and one English newspaper having general circulation in Oman, and each such notice shall be deemed to have been given on the date of such publication, or if published more than once or on different dates, on the first date on which such publication is made. Copies of all notices shall also be given by the Issuer to CMA.

29. Documents for inspection

The Articles, the Trust Deed, the audited financial statements of the Issuer shall be available for inspection with the Trustee, at the specified offices of the Trustee and with the Issue Manager.

30. Applicability of the Commercial Companies law

The issue of the Bonds shall be governed by the CCL and the Laws of Oman. To the extent that any clause herein does not comply with, or contradicts any Article or Chapter of such Law, the Law shall override the provision contained in these terms and conditions. Nothing contained herein shall preclude any matter or dispute arising from the Bond issue from being adjudicated by a competent court of Oman.

31. Trusteeship

MDSRC will be appointed as Trustee to the Bond issue to oversee the compliance of the Issuer with the terms and conditions of the issue, and to oversee, co-ordinate and monitor the status and the rights of the Bondholders.

32. Governing law and jurisdiction

These Terms and Conditions shall be governed by and construed in accordance with the Laws of Oman and any disputes arising between the Trustee, on behalf of the Bondholders’ and the Issuer in respect of these Terms and Conditions or any interpretation thereof shall be subject to amicable negotiations between the Issuer and the Trustee on behalf of the Bondholders. Failing a satisfactory resolution of the dispute, the disputed matter may be referred to the exclusive jurisdiction of the Primary Commercial Court of Oman for its adjudication.

BankMuscat SAOG

��

SECTION VIIIRIGHTS AND RESPONSIBIlITIES

TRuSTEE

1. The responsibilities and duties of the Trustee

• Calling for periodical reports from the Issuer and inspect books of accounts, records, registers, the assets and the documents and reports relating to the credit rating of the Issuer.

• Monitoring material contracts, events, actions and announcements (including publications (including publication of annual financial statements) entered into or announced by the Issuer, from time to time. The Issuer shall inform the Trustee of any material transaction or contract that could be judged to affect the rights of Bondholders.

• Ensuring that interest due on the Bonds has been paid to the Bondholders on the relevant interest due dates.

• Monitoring the Issuer's adherence to the terms and conditions of the Issue and assessing whether or not the Issuer is able to discharge the claims of Bondholders as and when they become due.

• Ascertaining that the Bonds have been redeemed in accordance with the terms & conditions of the Issue.

• Act upon any reasonable request of a holder of the bonds, the auditors of the Issuer, the MOCI, CBO, the MSM, the CMA, or the Issuer itself, who may alert the MDSRC to a situation which may constitute an event or breach which has, or potentially may have a material effect on the rights of the Bondholders

• Calling or causing to be called the general meeting of bondholders or on a requisite by one or more bondholders who own at least 10% of the total issued Bonds. The call for the meeting shall be pursuant to Article 92 of the CCL.

• Ascertaining that the funds raised through this Issue are utilized in accordance with the Prospectus.

• Act as an intermediary in resolving any material dispute arising between the Issuer and any individual holder, or collective number of holders, of bonds on issues directly relevant the terms and conditions attaching to Bonds

• Carrying out such other acts as necessary for the protection of the interests of the Bondholders.

2. Rights and powers of the Trustee

The Trustee shall have the following specific powers, in addition to any other powers that may be conferred upon it by the Laws of Oman:

• The Trustee may act on the opinion or advice of, or information obtained from, any expert and will not be responsible to anyone for any loss suffered by so acting. Any such opinion, advice or information may be sent or obtained by letter, telex or fax and the Trustee will not be liable to anyone for acting in good faith on any opinion, advice or information purporting to be conveyed by such means even if it contains some error or is not authentic.

• The Trustee need not notify anyone of the execution of this Trust Deed or do anything to find out if an Event of Default has occurred. Until it has actual knowledge or express notice to the contrary, the Trustee may assume that no such event has occurred and that the Issuer is performing all its obligations under this Trust Deed and the Conditions.

BankMuscat SAOG

��

• The Trustee will not be responsible for having acted in good faith on a resolution purporting to have been passed at a meeting of Bondholders in respect of which minutes have been made and signed even if it is later found that no such event has occurred and that the Issuer is performing all its obligations under this Trust Deed and the Conditions.

• If the Trustee, in the exercise of its functions, requires to be satisfied or to have information as to any fact or the expediency of any act, it may call for and accept as sufficient evidence of that fact or the expediency of that act a certificate signed by an Authorised Signatory of the Issuer as to that fact or to the effect that, in their reasonable opinion, that act is expedient and the Trustee need not call for further evidence and will not be responsible for any loss occasioned by acting on such certificate.

• The Trustee may deposit the Trust Deed and any other documents with any bank or entity whose business includes the safe custody of documents or with any lawyer or firm of lawyers believed by it to be of good repute and may pay all sums due in respect thereof.

• The Trustee may, if it considers it expedient in the interests of the Bondholders, employ and pay any professionals selected by it, for the performance if any functions and exercise of any powers of the Trustee to transact or conduct, or assist in transacting or conducting, and business and to do or assist in doing all acts required to be done by the Trustee (including the receipt and payment of money) pursuant to the terms of this Trust Deed. If the Trustee exercises reasonable care in selecting an agent, the Trustee will not be responsible to anyone for any misconduct or omission by such agent so employed by it.

• The Trustee will not be liable to the Issuer or Bondholder by reason of having transferred any monies to a Bondholder based on the information recorded against the name of a registered Bondholder with the registrar.

• Unless ordered to do so by a court of competent jurisdiction, the Trustee shall not disclose or be required to disclose to any Bondholder or to any other person any confidential financial or other information made available to the Trustee by the Issuer unless the Trustee otherwise considers it necessary to so disclose for the proper discharge of its duties.

• As between itself and the Bondholders, the Trustee may determine all questions and doubts arising in relation to any of the provisions of this Trust Deed. Such determinations, whether made upon such a question actually raised or implied in the acts or proceedings of the trustee, will be conclusive and shall bind the Trustee and the Bondholders.

• The Trustee may determine whether or not an Event of Default is in its opinion capable of remedy. Any such determination will be conclusive and binding on the Issuer and the Bondholders. If the Trustee so decides that and Event of Default has occurred and/or is directed by the Bondholders pursuant to the passing of a Bondholders’ Resolution to commence proceedings against the Issuer, the Trustee shall commence enforcement of the payable default interest thereon.

• The Trustee will not be responsible for the receipt or application by the Issuer of the proceeds of the issue of the Bonds.

BankMuscat SAOG

�0

BONDHOlDERS

Bondholder’s Rights

The Bondholders shall enjoy equal rights inherent in the ownership of Bonds as follows:

• The right to receive interest payable on the Bonds in accordance with conditions 7, 8 and 9 of Section VII of this Prospectus.

• The right to dispose or transfer the Bonds in accordance with condition 12 of Section VII of this Prospectus and the Laws of Oman.

• In the event of the liquidation of the Bank, the right to claim any amounts outstanding under the Bonds as a debt owed by the Bank.

• The right to participate in Bondholders’ meeting and to vote at such meetings in accordance with the provisions of the Trust Deed and the CCL.

BankMuscat SAOG

�1

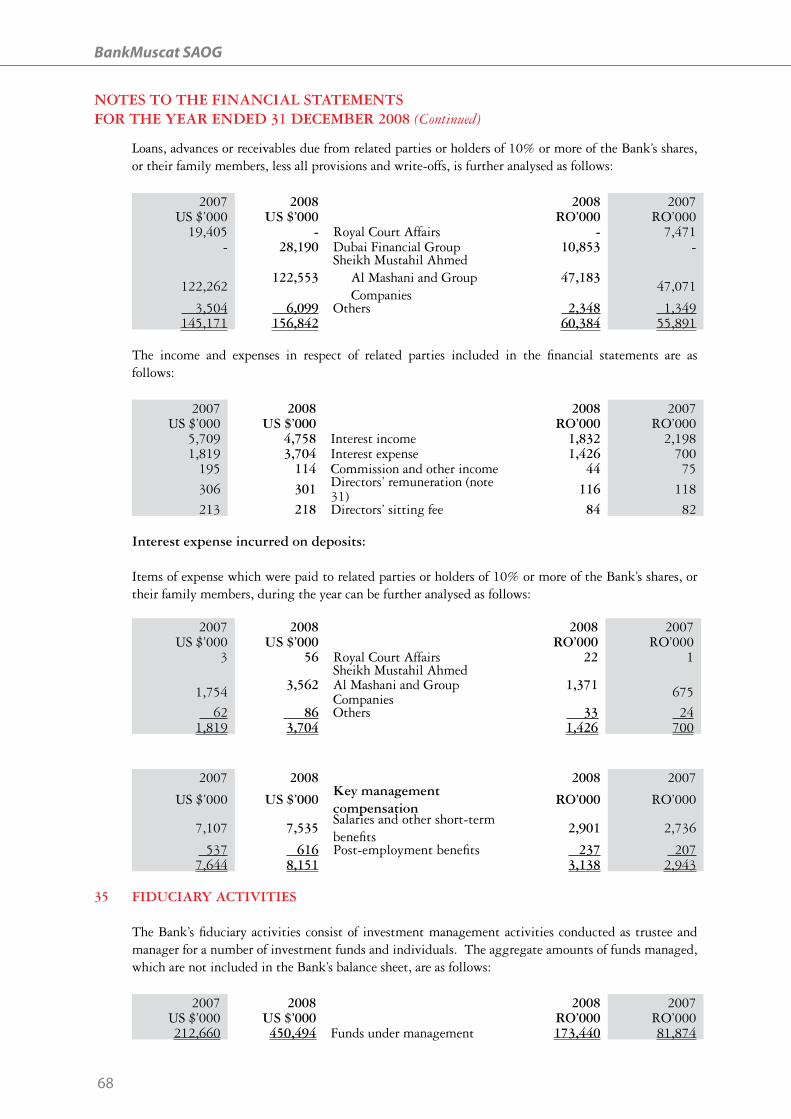

SECTION IxRElATED PARTy TRANSACTIONS

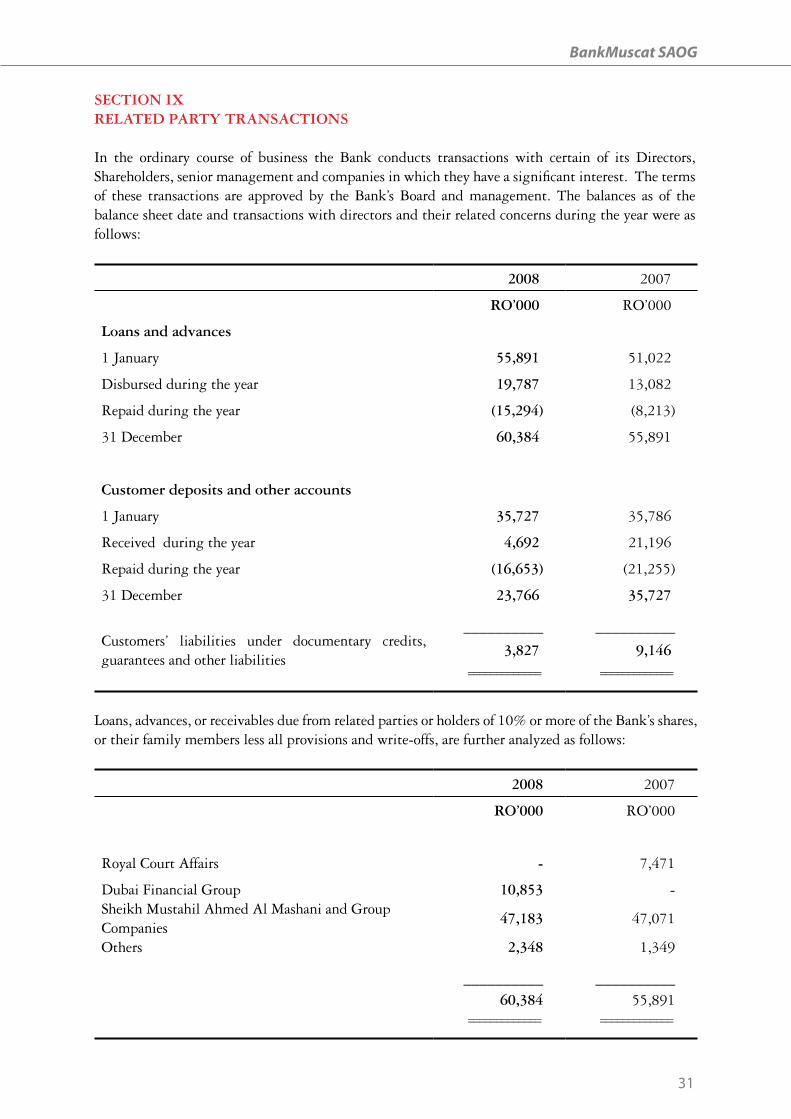

In the ordinary course of business the Bank conducts transactions with certain of its Directors, Shareholders, senior management and companies in which they have a significant interest. The terms of these transactions are approved by the Bank’s Board and management. The balances as of the balance sheet date and transactions with directors and their related concerns during the year were as follows:

2008 2007

RO’000 RO’000

loans and advances

1 January 55,891 51,022

Disbursed during the year 19,787 13,082

Repaid during the year (15,294) (8,213)

31 December 60,384 55,891

Customer deposits and other accounts

1 January 35,727 35,786

Received during the year 4,692 21,196

Repaid during the year (16,653) (21,255)

31 December 23,766 35,727

__________ __________Customers’ liabilities under documentary credits, guarantees and other liabilities

3,827 9,146============= =============

Loans, advances, or receivables due from related parties or holders of 10% or more of the Bank’s shares, or their family members less all provisions and write-offs, are further analyzed as follows:

2008 2007

RO’000 RO’000

Royal Court Affairs - 7,471

Dubai Financial Group 10,853 -Sheikh Mustahil Ahmed Al Mashani and Group Companies

47,183 47,071

Others 2,348 1,349

__________ __________60,384 55,891

============= =============

BankMuscat SAOG

��

The income and expenses in respect of related parties included in the financial statements are as follows:

2008 2007

RO,000 RO’000

Interest income 1,832 2,198

Interest expense 1,426 700

Commission and other income 44 75

Directors’ remuneration 116 118

Directors’ sitting fee 84 82

Interest expense incurred on deposits:

Items of expense which were paid to related parties or holders of 10% or more of the Bank’s shares, or their family members, during the year can be further analyzed as follows:

2008 2007

RO’000 RO’000

Royal Court Affairs 22 1Sheikh Mustahil Ahmed Al Mashani and Group Companies 1,371 675

Others 33 24

__________ __________1,426 700

============= =============

2008 2007

key management compensation RO’000 RO’000

Salaries and other short-term benefits 2,901 2,736

Post Employment benefits 237 207

__________ __________3,138 2,943

============= =============

BankMuscat SAOG

��

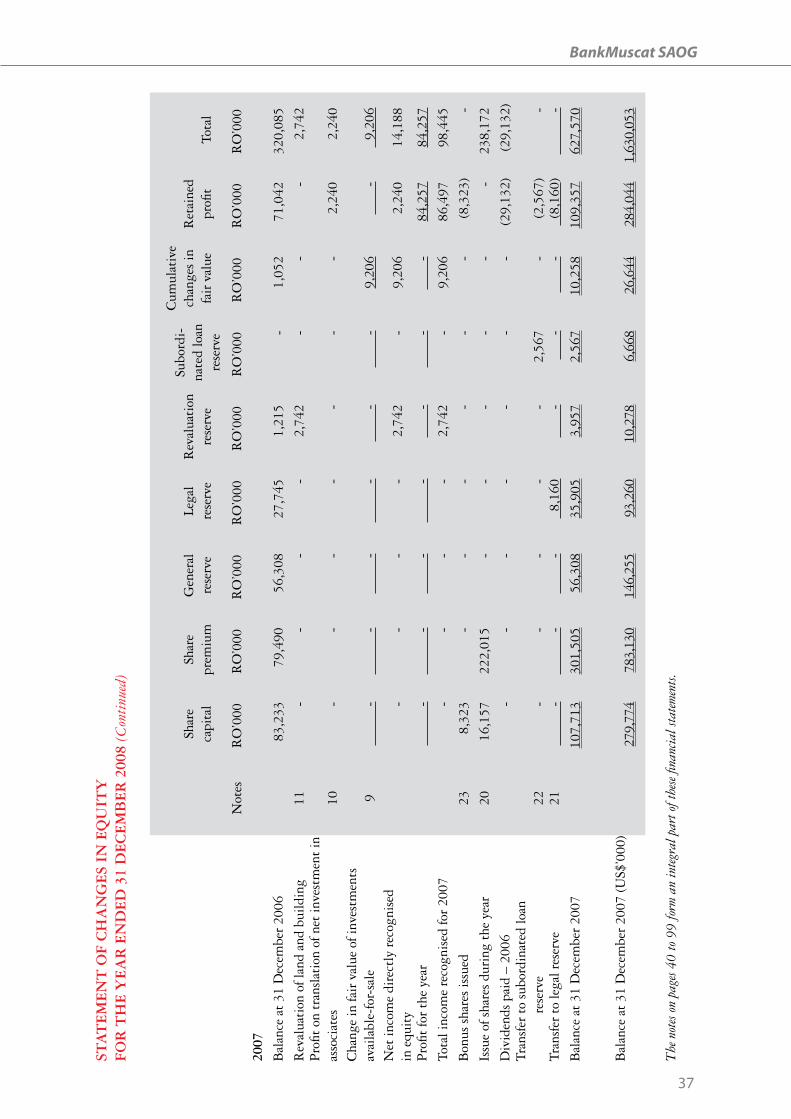

SECTION xHISTORICAl fINANCIAl PERfORMANCE

The following are the audited financial statements for the year 2008. Additional information on the financials of the Issuer can be obtained from the website www.msm.gov.om

BankMuscat SAOG

��

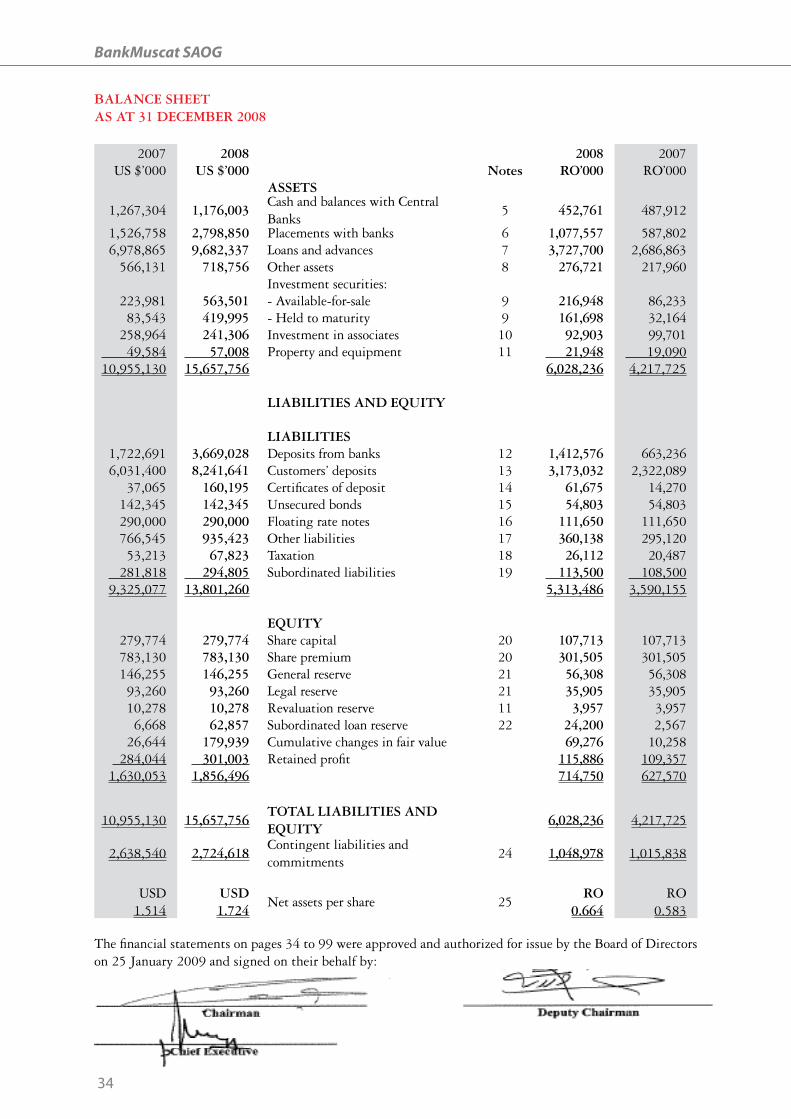

BAlANCE SHEETAS AT 31 DECEMBER 2008

2007 2008 2008 2007US $’000 uS $’000 Notes RO’000 RO’000

ASSETS

1,267,304 1,176,003Cash and balances with Central Banks

5 452,761 487,912

1,526,758 2,798,850 Placements with banks 6 1,077,557 587,8026,978,865 9,682,337 Loans and advances 7 3,727,700 2,686,863

566,131 718,756 Other assets 8 276,721 217,960Investment securities:

223,981 563,501 - Available-for-sale 9 216,948 86,23383,543 419,995 - Held to maturity 9 161,698 32,164

258,964 241,306 Investment in associates 10 92,903 99,701 49,584 57,008 Property and equipment 11 21,948 19,09010,955,130 15,657,756 6,028,236 4,217,725

lIABIlITIES AND EQuITy

lIABIlITIES1,722,691 3,669,028 Deposits from banks 12 1,412,576 663,2366,031,400 8,241,641 Customers’ deposits 13 3,173,032 2,322,089

37,065 160,195 Certificates of deposit 14 61,675 14,270142,345 142,345 Unsecured bonds 15 54,803 54,803290,000 290,000 Floating rate notes 16 111,650 111,650766,545 935,423 Other liabilities 17 360,138 295,12053,213 67,823 Taxation 18 26,112 20,487

281,818 294,805 Subordinated liabilities 19 113,500 108,5009,325,077 13,801,260 5,313,486 3,590,155

EQuITy279,774 279,774 Share capital 20 107,713 107,713783,130 783,130 Share premium 20 301,505 301,505146,255 146,255 General reserve 21 56,308 56,30893,260 93,260 Legal reserve 21 35,905 35,90510,278 10,278 Revaluation reserve 11 3,957 3,9576,668 62,857 Subordinated loan reserve 22 24,200 2,567

26,644 179,939 Cumulative changes in fair value 69,276 10,258 284,044 301,003 Retained profit 115,886 109,3571,630,053 1,856,496 714,750 627,570

10,955,130 15,657,756TOTAl lIABIlITIES AND EQuITy

6,028,236 4,217,725

2,638,540 2,724,618Contingent liabilities and commitments

24 1,048,978 1,015,838

USD 1.514

uSD 1.724

Net assets per share 25 RO 0.664

RO 0.583

The financial statements on pages 34 to 99 were approved and authorized for issue by the Board of Directors on 25 January 2009 and signed on their behalf by:

BankMuscat SAOG

��

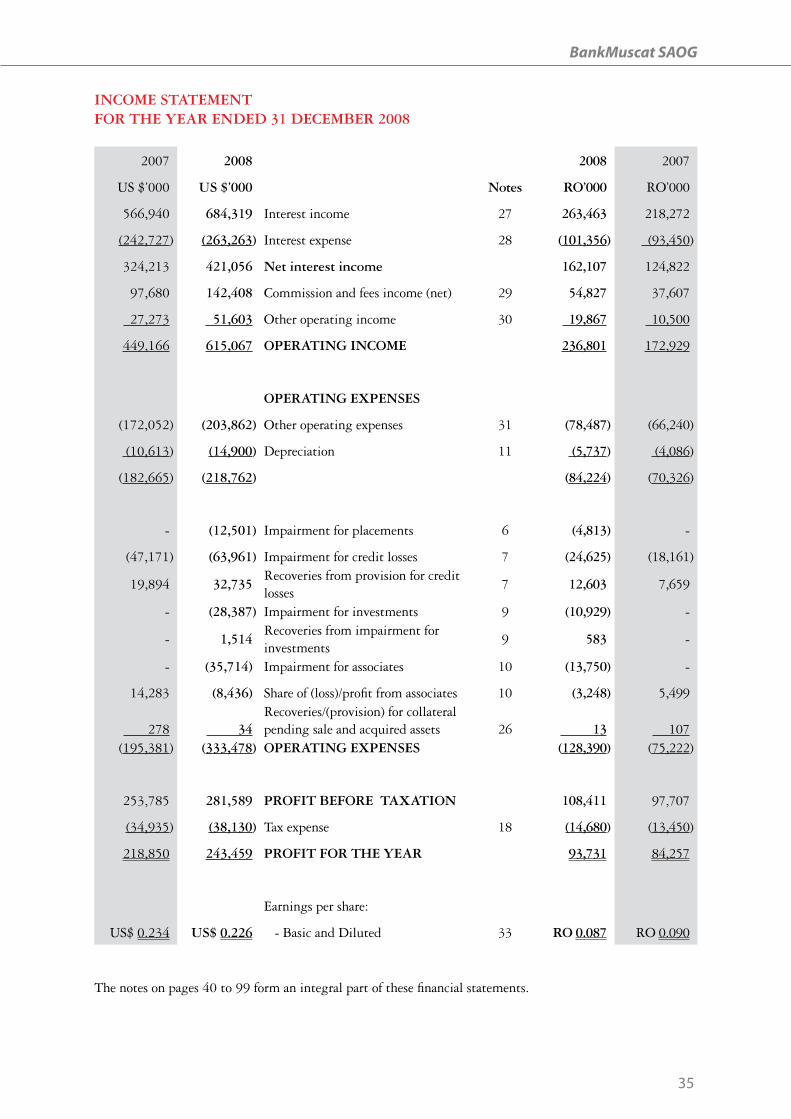

INCOME STATEMENT fOR THE yEAR ENDED 31 DECEMBER 2008

2007 2008 2008 2007

US $’000 uS $’000 Notes RO’000 RO’000

566,940 684,319 Interest income 27 263,463 218,272

(242,727) (263,263) Interest expense 28 (101,356) (93,450)

324,213 421,056 Net interest income 162,107 124,822

97,680 142,408 Commission and fees income (net) 29 54,827 37,607

27,273 51,603 Other operating income 30 19,867 10,500

449,166 615,067 OPERATING INCOME 236,801 172,929

OPERATING ExPENSES

(172,052) (203,862) Other operating expenses 31 (78,487) (66,240)

(10,613) (14,900) Depreciation 11 (5,737) (4,086)

(182,665) (218,762) (84,224) (70,326)

- (12,501) Impairment for placements 6 (4,813) -

(47,171) (63,961) Impairment for credit losses 7 (24,625) (18,161)

19,894 32,735Recoveries from provision for credit losses

7 12,603 7,659

- (28,387) Impairment for investments 9 (10,929) -

- 1,514Recoveries from impairment for investments

9 583 -

- (35,714) Impairment for associates 10 (13,750) -

14,283 (8,436) Share of (loss)/profit from associates 10 (3,248) 5,499

278 34Recoveries/(provision) for collateral pending sale and acquired assets 26 13 107

(195,381) (333,478) OPERATING ExPENSES (128,390) (75,222)

253,785 281,589 PROfIT BEfORE TAxATION 108,411 97,707

(34,935) (38,130) Tax expense 18 (14,680) (13,450)

218,850 243,459 PROfIT fOR THE yEAR 93,731 84,257

Earnings per share:

US$ 0.234 uS$ 0.226 - Basic and Diluted 33 RO 0.087 RO 0.090

The notes on pages 40 to 99 form an integral part of these financial statements.

BankMuscat SAOG

��

STA

TE

ME

NT

Of

CH

AN

GE

S IN

EQ

uIT

y

fO

R T

HE

yE

AR

EN

DE

D 3

1 D

EC

EM

BE

R 2

008 Sh

are

capi

tal

Shar

epr

emiu

mG

ener

alre

serv

ele

gal

Res

erve

Rev

alua

tion

rese

rve

Subo

rdi-

nate

d lo

an

rese

rve

Cum

ulat

ive

chan

ges

infa

ir v

alue

Ret

aine

dpr

ofit

Tot

al

Not

esR

O’0

00R

O’0

00R

O’0

00R

O’0

00R

O’0

00R

O’0

00R

O’0

00R

O’0

00R

O’0

00

2008

Bal

ance

at

31 D

ecem

ber

2007

107,

713

301,

505

56,3

0835

,905

3,95

72,

567

10,2

5810

9,35

762

7,57

0Lo

ss o

n tr

ansl

atio

n of

net

inve

stm

ent

in

asso

ciat

es10

--

--

--

-(1

1,71

2)(1

1,71

2)

Cha

nge

in fa

ir v

alue

of i

nves

tmen

ts

avai

labl

e-fo

r-sa

le9

-

-

-

-

-

-

59,0

18

-59

,018

Net

inco

me

dire

ctly

rec

ogni

sed

in e

quit

y

-

-

-

-

-

-59

,018

(11,

712)

47,3

06

Pro

fit fo

r th

e ye

ar

-

-

-

-

-

-

-93

,731

93,

731

Tota

l inc

ome

reco

gnis

ed fo

r 20

08-

--

--

-59

,018

82,0

1914

1,03

7

Div

iden

ds p

aid

- 20

0723

--

--

--

-(5

3,85

7)(5

3,85

7)Tr

ansf