entrepreneurship, access to capital & … · conseil de la fondation 16 octobre 2009 hicham y....

TRANSCRIPT

Strictly confidential – for internal use only

William C. Fellows

ENTREPRENEURSHIP, ACCESS TO

CAPITAL & SMES IN MENA:

SUPPLY? DEMAND?

THE ISSUES:

OECD – MENA

5th SME Working Group

22 February 2011, Casablanca, Morocco

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

2 2

The Key Question

• Problem: funds not flowing as desired to Entrepreneurs,

& Small & Medium Sized firms.

• Frequent observation in region:

– Banks are not taking risk

– Venture investors are not taking risk.

• First reactions: find ways to move more funds to SMEs.

– But are we asking the right questions and enough questions?

– Re Risk & Funding: To the extent true (and not always), we

need to ask WHY? What drivers, fundamentals?

2 March 2011 William C. Fellows 2

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

3 3

The Supply & Demand Question & Policy.

• Access to Capital:

– Demand: Entrepreneurs / Enterprises

– Supply: Financial Institutions (credit/debt, equity)

• Challenge: sustainable access to funding for

investment for SMEs, and particularly

entrepreneurial SMEs in early stages.

• Known:

– Relative to apparent demand, appears to be problem of

access.

• Assumptions? Where is the problem?

2 March 2011 William C. Fellows 3

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

4 4

SME Typology: Who are we talking about?

• Gazelles: High-Potential SMEs / SME Champions

– Outstanding SME focused on growht, with high prospects, usually highly innovative (e.g. IKEA

in early days)

• Entrepreneurial SME

– An SME that generates good profits, but may not seek growth (e.g. small traditional packaging

firm).

• Lifestyle SME

– An SME that is more focused on the owner‘s lifestyle (e.g. small boutique hotel with no desire

to grow).

• Ordinary SME / Traditional SME

– A small enterprise with minimal profits to its owner, usually very traditional. (e.g. Traditional

textile exporters, individual artisans)

• “Hobby” or Casual Business (Very small enterprise)

– A very small business operated on the side; not as main activity, no serious intention to make the

business grow.

• Craft, Traditional Very small enterprise

4

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

5 5

Looking at Demand Side via Risk Capital

• Reflect on Access to Finance on Demand side via

the lens of Equity Financing (VC, etc).

– Why VC as lens?:

• Equity Funding (Risk Capital) neglected component in

Policy Discussions.

• Equity cares more about internal quality of SME / quality of

Entrepreneur(s).

• Focused on high-impact Entrepreneurs seeking to build firms

that will drive competitiveness, the key need in region.

– In Maghreb decent level of Venture Capital available.

2 March 2011 William C. Fellows 5

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

6 6

Developing MENA Funds (2008)

2

86

1 9 1 6

48

12 18 9 1

36

534

46

627

453

290

12

266

7

733

54

181

0

100

200

300

400

500

600

700

800

Capital Raised Fund Stages (Select Countries, NA & Comp)

Millions US$, 2008

R&D

Seed

VC

Growth

LBO

101 138

10 21

1378

299

46

375 427

23

251

77

178 185

18

0

200

400

600

800

1,000

1,200

1,400

1,600

Funds in North Africa

(Select Countries) Millions US$, 2008

Consumer Goods

Energy

ICT &

Innovation

Multi-Sector

Other Industries

Construction & Public

Works

Services

2 March 2011 William C. Fellows 6

Source: ANIMA April 2008 “Med Funds: Overview of Private Equity in the MEDA Region”

Most

“Maghreb”

Funds go to

Morocco,

~50%, then

Tunisia

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

7 7

Supply vs Demand Reflection

• Assumption: Provide the capital and Entrepreneur

Access to Capital/Finance problem solved.

– Good evidence that this is not true.

• Moroccan regional risk capital funds experience

• Negative returns in venture funds

– Arguments to lower standards

• Do we have the capital to waste?

• If Quality of SMEs is low, there will be high levels of losses.

– For Example: High level of Bad Credit in Banks

• How ―eligible‖ (i.e. sustainable) is the SME demand?

• All Evidence says SMEs need serious upgrading, especially

in Human Resources (Management).

2 March 2011 William C. Fellows 7

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

8 8

Entrepreneur / SME issues

– Limited social capital (TRUST &UNDERSTANDING of

PRACTICE)

– Limited Entrepreneur networks & skill sets in Mgmt,

and limited connections with financing

– Limited and outdated legal forms for structuring

investments to meet both Venture Investors (Angels,

VCs, etc) & Entrepreneur expectations

– Lack of RETURNS on Capital.

• Early stage losing substantial money.

• Why?

– Weaknesses in firms, weakness in gmt w entrepreneurs

– Tough business climate, investment not enough.

2 March 2011 William C. Fellows 8

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

9 9

SME Quality, VC Impact, Morocco

91%

40%

58%

51%

56%

99%

80%

91% 91% 91%

0%

20%

40%

60%

80%

100%

120%

Audited by a CAC Exiistence of Oversight

Committees by Activity

Existence of Reporting Systems Existence of Performance

Indicators

Existence of Budgeting Policies

& Budget Oversight

At time of Investment To Date (mid 2010)

2 March 2011 William C. Fellows 9 Source: Adapted from Association Marocain des Investisseurs en Capital, pre release data July 2010

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

10 10

Key driver to lack of funding to Entrepreneurs

& SMEs

• ―A key reason that financing funds’ flows to emerging-market

SMEs are insufficient—especially for investments in the range

of $100,000 to $1.5 million—is that returns are not fully risk-

adjusted.‖

– Milken Institute, “Stimulating Investment in Emerging-Market SMEs,

Financial Innovations Lab Report” 2009

– Translated from Finance Speak:

Overall Profits / Returns to Investors in SMEs & Entrepreneurs from

venture investments are not covering the losses or are not attractive

enough to pull money away from “more certain bets” like Real Estate

(perception of RE as a safe & sure thing quite common, despite the 2008

crisis!).

WHY POOR PROFITS, POOR QUALITY.

– Without an ability to make good profits… capital simply will not be

sustainably invested in Entrepreneurs.

2 March 2011 William C. Fellows 10

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

11 11

Observation (Milken Inst. again)

― Entrepreneurs often need a great deal of

technical assistance in putting their companies’

financials in order, marketing, and other

initiatives that could make their businesses

successful.

This increases a fund‘s … expenses and lowers net

returns to investors.

Because they are not fully compensated for the risk,

investors have not embraced the opportunities.‖

2 March 2011 William C. Fellows 11

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

12 12

The Universal Story Capacity constraints &

Building SME Investment

The capacity constraints faced by risk funds in developing markets

across the globe are similar:

• Lack of good legal / investment structures to manage risk, find

common ground with Entrepreneurs

• Challenge to get good deal flow creation: eligible SMEs /

Entrepreneurs

– Too many 1 entrepreneur shows… not enough teams.

• Lack of good ―hands on‖ investor skills (VCs need to upgrade

too)

• Not enough resources in Funds to add value relative to needs of

SMEs

• Lack of profitable returns (exits) on SME investments .

2 March 2011 William C. Fellows 12

Adapted from : Capacity Constraints Facing Risk Fund Managers - Final report, Financing for Growth, 2008

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

13 13

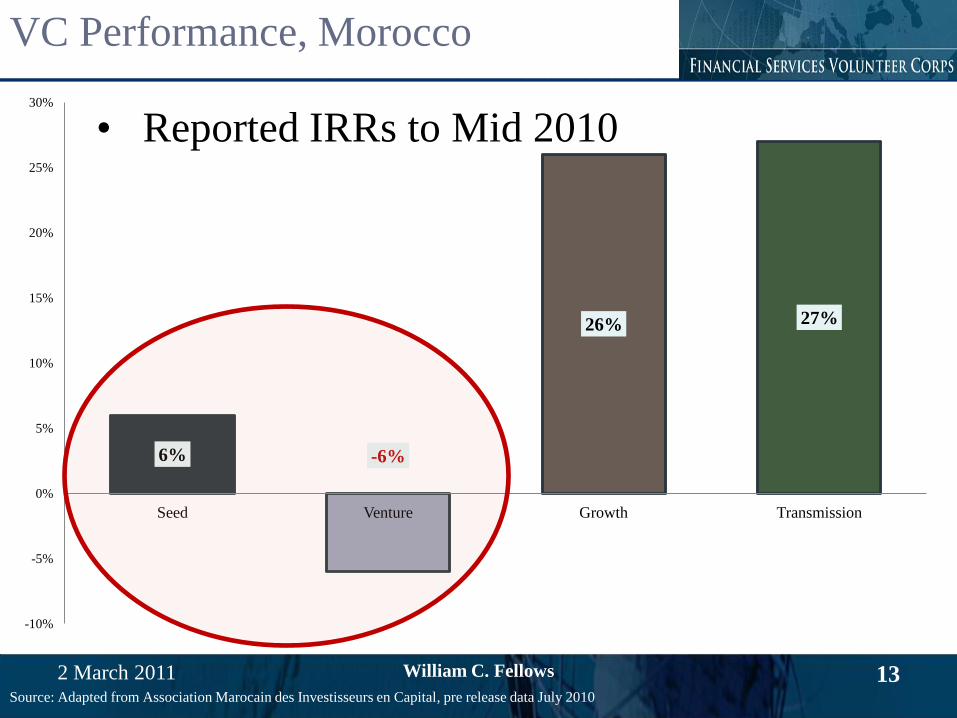

VC Performance, Morocco

6% -6%

26% 27%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Seed Venture Growth Transmission

2 March 2011 William C. Fellows 13

• Reported IRRs to Mid 2010

Source: Adapted from Association Marocain des Investisseurs en Capital, pre release data July 2010

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

14 14

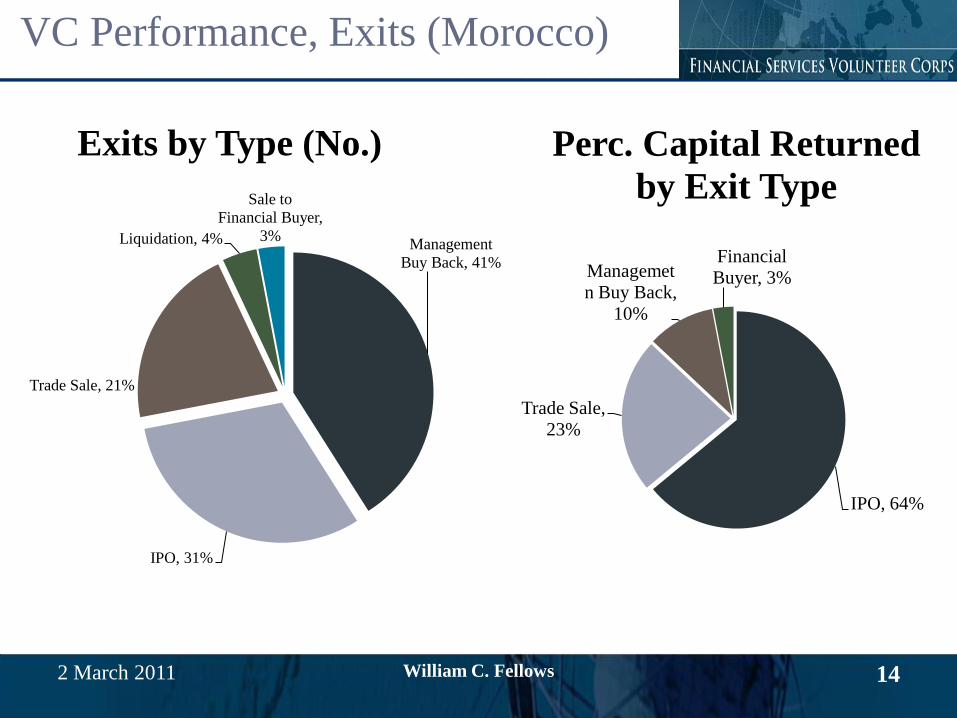

VC Performance, Exits (Morocco)

2 March 2011 William C. Fellows 14

Management

Buy Back, 41%

IPO, 31%

Trade Sale, 21%

Liquidation, 4%

Sale to

Financial Buyer,

3%

Exits by Type (No.)

IPO, 64%

Trade Sale,

23%

Managemet

n Buy Back,

10%

Financial

Buyer, 3%

Perc. Capital Returned

by Exit Type

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

15 15

Entrepreneur (Demand) Side Issues

• Less-than-ideal management practices prevalent in

region to overcome environment

• Acceptance of Role of Outside Investors:

– Sharing ownership, high level governance controls

• Acceptance of Applied Good Governance

– Old school family forms reality

– Modernized mgmt styles needed

2 March 2011 William C. Fellows 15

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

16 16

Resolving Investor & Entrepreneur Interests

VC/Equity Investor Objectives

Objectives of Equity Investors

• Maximum Return (IRR; X return)

• Large Equity participation

• Liquidity • IPO

• Merger or Trade Sale

• Put back to the Company

• Hedge Risk

Entrepreneur Objectives

• Keep as much equity as

possible

• Keep control of operations

• Incentives for founders (& key

employees)

– MENA very weak in providing

incentives, sharing control

internally with non-founders &

especially non-family

• Keep restrictions to a minimum

• Keep in the Family (MENA)

2 March 2011 William C. Fellows 16

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

17 17

SME Quality, VC Impact, Morocco

91%

40%

58%

51%

56%

99%

80%

91% 91% 91%

0%

20%

40%

60%

80%

100%

120%

Audited by a CAC Exiistence of Oversight

Committees by Activity

Existence of Reporting Systems Existence of Performance

Indicators

Existence of Budgeting Policies

& Budget Oversight

At time of Investment To Date (mid 2010)

2 March 2011 William C. Fellows 17 Source: Adapted from Association Marocain des Investisseurs en Capital, pre release data July 2010

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

18 18

Capital for Entrepreneurs, Sources

2 March 2011 William C. Fellows 18

Owner Capital

Family & Friends

Angels

Venture Capital/PE

Banks Buyout

IPO

Sale

Venture Financing Cycle

Breakeven

Angels,

Friends, Fools

& Family

Seed Capital

Early StageLater Stage

VC Acquisitions/Mergers &

Strategic Alliances

Exit (IPO,

Trade

Sale)

1st

2nd

3rd

Mezzanine

R

E

V

E

N

U

E

TIME

Valley of Death

Secondary

Offerings

Public

Market

The Enterprise & Funding Sources over Time

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

19 19

New Choices?

• Angel Capital?

– Good concept, however, requires (to be real sustainable

solution):

• Good Social Capital:

– Understanding of the

• Acceptance of outside investors on standard terms

– And outside investors who are also playing the game

– Legit worries by Entrepreneurs re ‗Faux Angels‘ taking over the

enterprise

– But what is the core motivation for promoting?:

• Increase funding to high-value start-ups, small-firms? (or

small firms generally?)

2 March 2011 William C. Fellows 19

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

20 20

Recall the Issues

• Positive role to play, but issues undermining

venture capital funds also hit Angels:

– Limited and outdated legal forms for structuring

investments to meet both Venture Investors (Angels,

VCs, etc) & Entrepreneur expectations

– Limited social capital (TRUST &UNDERSTANDING of

PRACTICE)

– Limited Entrepreneur networks & skill sets in Mgmt,

and limited connections w venture financing

– Lack of RETURNS on Capital.

2 March 2011 William C. Fellows 20

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

21 21

Returns, Why do we care?

• After all, investors are rich, right?

– Many funds are investing your retirement money.

• Investment in Entrepreneurs, SMEs competing

against other capital uses.

– EG: Real Estate (particular challenge in MENA)

• As one Angel told me, he hears all the time ―Why fund a risk

enterprise when you can get 50% in RE speculation.‖

– Without good returns, SMEs will be starved of capital

– Good returns also indicative of competitivenes and

MENA region needs more competitive enterprises,

more higher value, non-traditional enterprises.

2 March 2011 William C. Fellows 21

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

22 22

2 March 2011 William C. Fellows 22

The Risk, Profitability / Return Trade Off &

Financing Entrepreneurs / SMEs

Investment Returns Needed

Early Stage Growth Stage

• Investors seeking:

• Strong Management Teams

• Good Market Potential

• Revenue Traction

• High Upside Potential

• Large and Growing Markets

Late Stage Seed Stage

Ret

urn

Targ

et

20 x

1 x

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

23 23

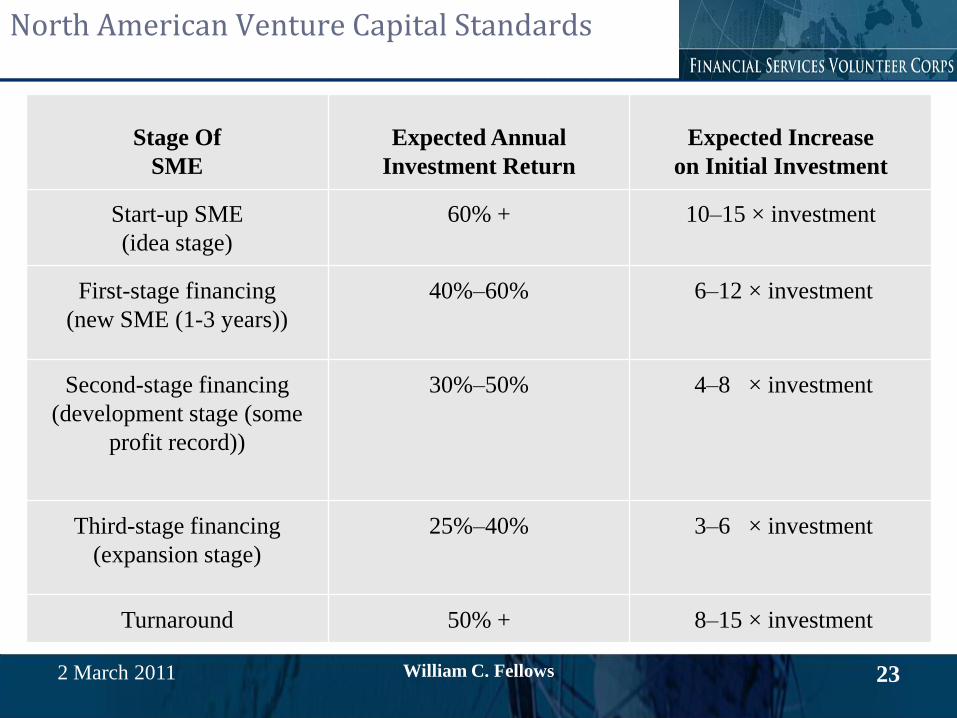

North American Venture Capital Standards

2 March 2011 William C. Fellows 23

Stage Of

SME

Expected Annual

Investment Return

Expected Increase

on Initial Investment

Start-up SME

(idea stage)

60% + 10–15 × investment

First-stage financing

(new SME (1-3 years))

40%–60% 6–12 × investment

Second-stage financing

(development stage (some

profit record))

30%–50% 4–8 × investment

Third-stage financing

(expansion stage)

25%–40% 3–6 × investment

Turnaround 50% + 8–15 × investment

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

24 24

Solutions, How to Address?

• We can‘t jump over these problems but how to

render them digestible:

• Enviro / Framework

– Need to look at breaking out into the key barriers to

Improve Returns to investing in SME from the Private

POV

• SME Quality

– How to help. Technical Assistance frequently wasted if

behind closed doors obs…

– And the volume of SMEs is huge!

2 March 2011 William C. Fellows 24

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

25 25

Environment: Where to go?

• Review Regulatory to remove barriers, follow best

practice:

– Enable investment & flexibility for CHANGE, do not

impose hard requirements

• Hard handcuff requirements are failures (See Lerner, Josh.

Boulevard of Broken Dreams (2010))

– Legal vehicles / Forms for Entrepreneurs & Investors:

• Reform and modernize to make EASY & Cost Effective to

use (e.g. Delaware LLC, France‘s reformed SAS);

– Restrictions on issues like Preferred Share structures, Quasi Equity

funding

2 March 2011 William C. Fellows 25

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

26 26

SME Quality & Returns

• Improve Returns to financing of Entrepreneurs /

SMEs? (That is make more attractive)

– Improve SME bottom-lines (profits) by improving

their competitiveness

• Targeted business development services to higher potential

SMEs (coming back to this)

• Improved overall business environment

• Improve investment tools

– Better corporate vehicles / forms for entrepreneurs & investors

– Improve liquidity tools (exits)

• Alt approaches

• Better public markets / alt markets

2 March 2011 William C. Fellows 26

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

27 27

Environment as Virtuous Cycles

• Bad Money drives out good

• Strong standards bring in better practice, money.

– Moroccan banking case as an example

2 March 2011 William C. Fellows 27

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

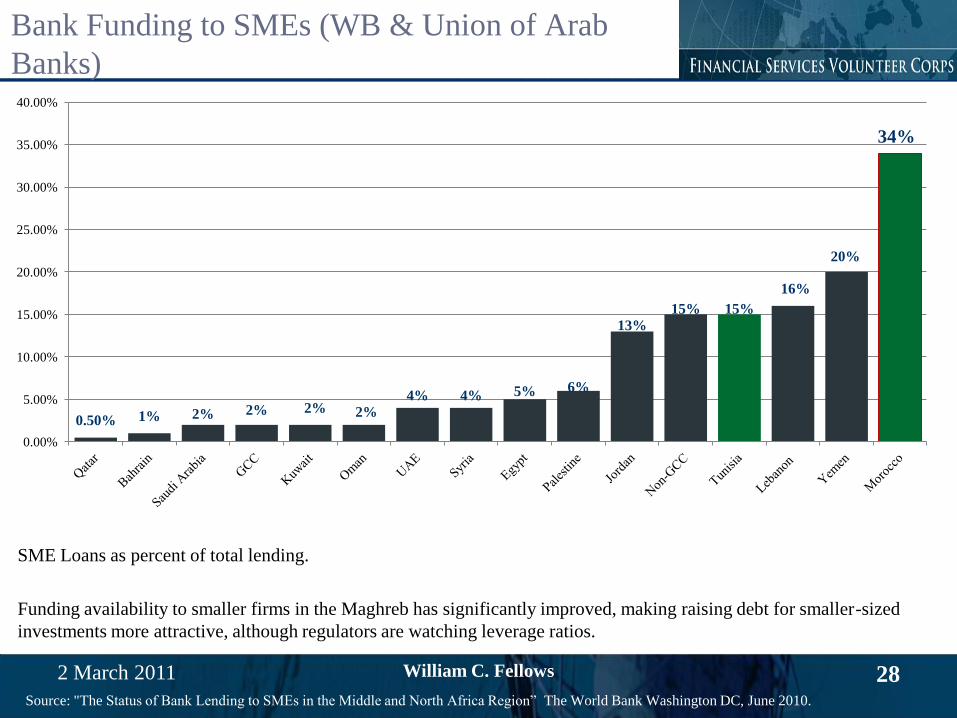

28 28

Bank Funding to SMEs (WB & Union of Arab

Banks)

SME Loans as percent of total lending.

Funding availability to smaller firms in the Maghreb has significantly improved, making raising debt for smaller-sized

investments more attractive, although regulators are watching leverage ratios.

2 March 2011 William C. Fellows 28

0.50% 1% 2% 2% 2% 2%

4% 4% 5% 6%

13%

15% 15%

16%

20%

34%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

Source: "The Status of Bank Lending to SMEs in the Middle and North Africa Region‖ The World Bank Washington DC, June 2010.

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

29 29

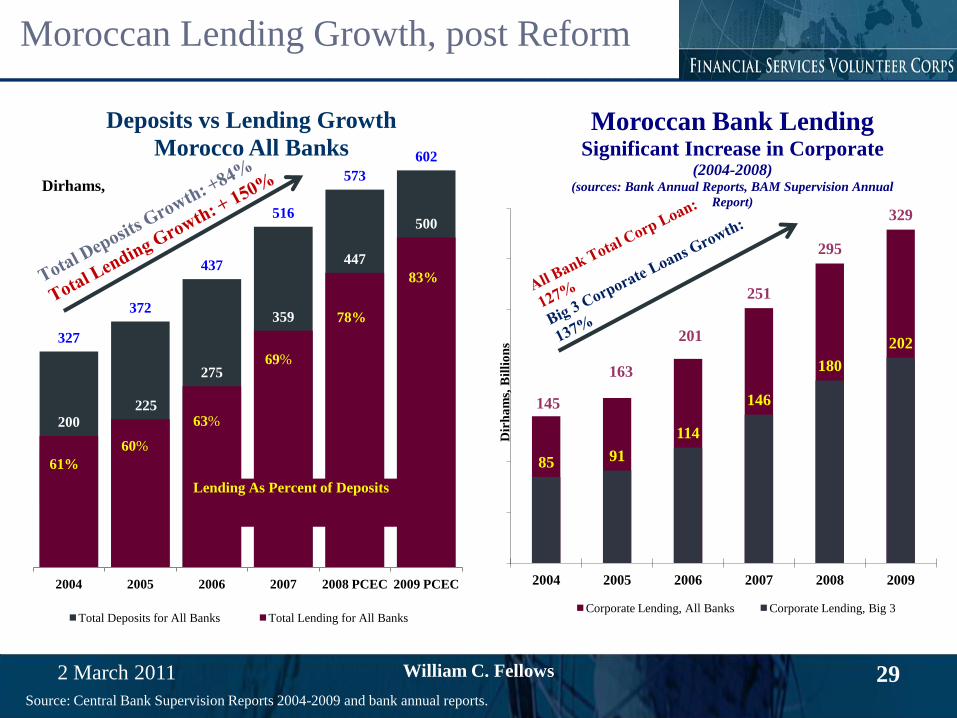

Moroccan Lending Growth, post Reform

327

372

437

516

573

602

200

225

275

359

447

500

2004 2005 2006 2007 2008 PCEC 2009 PCEC

Deposits vs Lending Growth

Morocco All Banks

Total Deposits for All Banks Total Lending for All Banks

61%

60%

63%

69%

78%

Dirhams,

Lending As Percent of Deposits

83%

145

163

201

251

295

329

85 91

114

146

180

202

2004 2005 2006 2007 2008 2009

Dir

ha

ms,

Bil

lio

ns

Moroccan Bank Lending Significant Increase in Corporate

(2004-2008) (sources: Bank Annual Reports, BAM Supervision Annual

Report)

Corporate Lending, All Banks Corporate Lending, Big 3

2 March 2011 William C. Fellows 29 Source: Central Bank Supervision Reports 2004-2009 and bank annual reports.

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

30 30

Moroccan Bank Lending Profile

2 March 2011 William C. Fellows 30

Households

28%

Financial

Activities

14%

Trade

7%

Trans. &

Comm.

4%

Hotels

3%

Construction

14%

Processing

Industry

18%

Primary Sector

3% Other Services

10%

Morocco Bank Lending

By Sector (2009)

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2003 2004 2005 2006 2007 2008 2009

12.3% 12.4%

9.6%

7.4%

5.3% 4.3%

4.2%

18.7% 19.4%

15.7%

10.9%

7.9%

6.0%

5.5%

Morocco Bank Non Performing

Loans

Improving Credit Management

%NPLs, Private Banks % NPLs, All Banks

All Bank

NPL% down

70.5% 03-09

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

31 31

Marry TA to SME w investment funds.

―Technical assistance—consulting an individual or group that has business or

finance experience on how to improve various aspects of a business—is critical to

emerging-market SMEs and can help enhance a company‘s value. Although the cost

of technical assistance can be substantial, it is one of the best ways to mitigate

investment risk. To prevent technical assistance from draining a commercial SME

fund of its revenue, investors can work with development institutions, governments,

foundations, and NGOs to create grant-based pools of funding to pay for technical

assistance to portfolio investees.

The net return on the investment in such a fund should be higher because of the

associated cost reductions for the fund itself and the improved performance of

portfolio businesses. As a result, more commercial investors would be attracted to

these funds while helping philanthropic organizations meet their objectives. Public

institutions can use their capabilities to leverage greater private capital for SME

investment funds.‖

2 March 2011 William C. Fellows 31

Source: Milken Institute: Stimulating Stimulating Investment in Emerging-Market SMEs Financial Innovations Lab Report, 2009

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

32 32

Focus in on Matching Mechanisms btw Investors &

Entrepreneurs (in their hands)

• ―Mechanisms are needed to match investors with projects that need

funding. …

• …such mechanisms would move beyond ad hoc, project-by-project

investments to create a more efficient marketplace. This need is

especially great given the information asymmetries in developing

countries.

• Investors find it difficult to identify appropriate investments, and

entrepreneurs have trouble locating sources of capital. Making

opportunities more visible would reduce investors‘ transaction costs

and increase the availability of capital for SMEs.‖

2 March 2011 William C. Fellows 32

Source: Stimulating Stimulating Investment in Emerging-Market SMEs, Financial Innovations Lab Report, 2009

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

33 33

TIME FOR DISCUSSION

End of Presentation.

2 March 2011 William C. Fellows 33

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

34 34

ENTREPRENEURS & RISK

FINANCING: VENTURE FINANCING

LANDSCAPE IN NORTH AFRICA, THE CONTEXT FOR ACCESS TO CAPITAL

Maghreb & North Africa VC & PE

(excluding Real Estate & Infrastructure) Reference Slides

2 March 2011 William C. Fellows 34

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

35 35

Morocco Funds Structure

2 March 2011 William C. Fellows 35 Source: FSVC research and adapted fromANIMA Study – April 2008 “Med Funds: Overview of Private Equity in the MEDA Region

Moroccan PE/VC Funds by Size

62%

10%

23%

0% 5%

<$50m $50 to 100m $100 to 500m >$500m Announced funds

86 48

534

266

R&D Seed VC Growth LBO

86 48

534

266

Consumer

goods

Energy ICT &

Innovation

Multi-sector Other

industries

Funds announced by Investment Stage (in $USm)

86 48

534

266

R&D Seed VC Growth LBO

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

36 36

Maghreb Investment Style: Diversified & Small

2 March 2011 William C. Fellows 36

1

18 19

31

15

5

3

8

1 0

5

10

15

20

25

30

35

0 to

1

1 to

5

5 to

10

10

to 2

0

20

to 3

0

30

to 4

0

40

to 5

0

> 5

0

NC

Number of Deals by Capital Invested

(2010)

Millions Moroccan Dirhams

Small Investments

50%

18%

13%

12%

7%

Invested Companies by %

Capital Acquired (2010)

5 - 34% 34 - 50% > 67% < >50 - 67% < 5%

Source: Adapted from Moroccan VC Association (Association Marocain des Investisseurs en Capital,) July 2010 to mid year

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

37 37

VC Performance, Morocco

Revenue Growth, Invested

Cos, by Invest Stage

97%

21% 17% 19% 0%

20%

40%

60%

80%

100%

120%

Investment Stage Shares of total

portfolio.

Growth, 61% Venture, 15%

Transmission

13%

Turnaround,

6%

Seed,

5%

2 March 2011 William C. Fellows 37 Source: Adapted from Association Marocain des Investisseurs en Capital, pre release data July 2010

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

38 38

VC Performance, Morocco

6% -6%

26% 27%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Seed Venture Growth Transmission

2 March 2011 William C. Fellows 38

• Reported IRRs to Mid 2010

Source: Adapted from Association Marocain des Investisseurs en Capital, pre release data July 2010

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

39 39

SME Quality, VC Impact, Morocco

91%

40%

58%

51%

56%

99%

80%

91% 91% 91%

0%

20%

40%

60%

80%

100%

120%

Audited by a CAC Exiistence of Oversight

Committees by Activity

Existence of Reporting Systems Existence of Performance

Indicators

Existence of Budgeting Policies

& Budget Oversight

At time of Investment To Date (mid 2010)

2 March 2011 William C. Fellows 39 Source: Adapted from Association Marocain des Investisseurs en Capital, pre release data July 2010

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

40 40

VC Performance, Exits (Morocco)

2 March 2011 William C. Fellows 40

Management

Buy Back, 41%

IPO, 31%

Trade Sale, 21%

Liquidation, 4%

Sale to

Financial Buyer,

3%

Exits by Type (No.)

IPO, 64%

Trade Sale,

23%

Managemet

n Buy Back,

10%

Financial

Buyer, 3%

Perc. Capital Returned

by Exit Type

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

41 41

Guaranty for VC

• ―As downward protection acts against the investor‘s targeting the maximum

yield, it tends to promote the survival of venture capital investors instead of

enhancing the success of their investments. Hence the clearly observable

tendency that the more advanced the venture capital industry of a given country,

the more unlikely that downward protection play a major part in encouraging

venture capital. In the USA and in the United Kingdom, venture capital

programmes supported by the state tend to focus on raising the returns to private

sector investors. On the other hand, in Continental Europe, every one of the more

significant countries (France, Germany, Sweden, the Netherlands, Denmark) has

public programmes including the direct guarantee component.‖ Karsai, Judit.

―Can The State Replace Private Capital Investors? Public Financing of Venture

Capital In Hungary.‖ Discussion Papers MT–DP. 2004/9, Institute of Economics

Hungarian Academy of Sciences Budapest June 2004, p. 7

• Mason, Colin. ―Public Policy Support For The Informal Venture Capital Market In Europe: A

Critical Review‖ Working Paper 08-07 Hunter Centre for Entrepreneurship, University of Strathclyde

Business School, December 2008, p. 10

2 March 2011 William C. Fellows 41

Conseil de la Fondation

16 Octobre 2009

Hicham Y. Alaoui

Directeur Exécutif

42 42

FSVC MAGHREB

William C. Fellows

Directeur Régional (Regional Director, North Africa / Maghreb)

FSVC

26 Boul. Massira El Khadra, 3e étage

Casablanca, le Maroc 20100

www.fsvc.org

2 March 2011 William C. Fellows 42