engr 112 economic analysis. engineering economic analysis evaluates the monetary aspects of the...

TRANSCRIPT

ENGR 112

Economic Analysis

Engineering Economic Analysis Evaluates the monetary aspects of the

products, projects, and processes that engineers design

Aids in the decision making process when alternatives are compared

Especially useful when resources are limited Replace vs. keep Build vs. buy

Time Value of Money $1 today is more valuable than $1 a year

later

Engineering economy adjusts for the time value of money to balance current and future revenues and cost

0 5 10Years

Capital vs. Interest Capital

Invested money and resources Whoever owns it should expect a

return from whoever uses it Bank lends you money

Buy a car Go to college

Firm invests in a project Buy equipment Buy “knowledge”

Capital vs. Interest Interest

Return on capital Typically expressed as an interest

rate for a year

Interest rates are needed to evaluate engineering projects!!

Interest rate =Interest $ amount

Capital $ amount

“Interest”-ing Example

The engineering group of Baker Designs must decide whether to spend $90K (K for thousands) on a new project. This project will cost $5K per year for operations, and it will increase revenues by $20K annually. Both the costs and the revenues will continue for 10 years. Should the project be done? Eschenbach, T.G., Engineering Economy: Applying Theory to Practice, Irwin, 1995, p.22

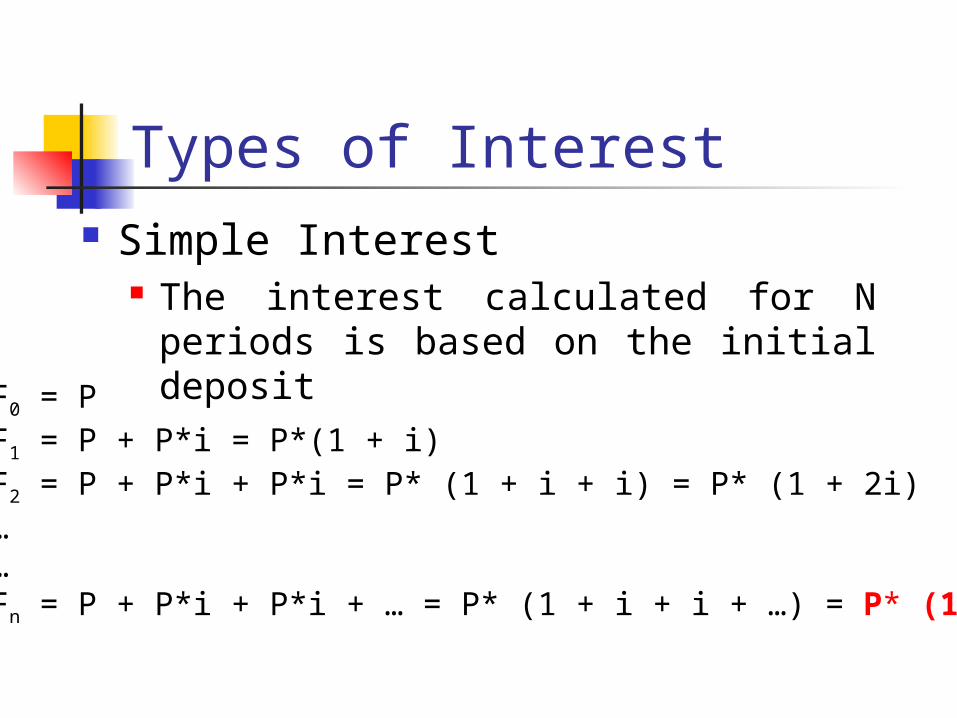

Types of Interest Nomenclature

P = Initial deposit (or principal) N = Number of years i = Interest rate per year F = Future value after N years

Types of Interest Simple Interest

The interest calculated for N periods is based on the initial depositF0 = PF1 = P + P*i = P*(1 + i)F2 = P + P*i + P*i = P* (1 + i + i) = P* (1 + 2i)……Fn = P + P*i + P*i + … = P* (1 + i + i + …) = P* (1 + Ni)

Types of Interest Compound Interest

Interest type used in engineering economic evaluations

Interest is computed on the current balance that has not yet been paid

Includes accrued interestF0 = PF1 = P + P*i = P *(1 + i)F2 = P1 + P1 * i = P1 *(1+i) = P *(1+i) *(1+i) = P *(1+i)2

……Fn = Pn-1 + Pn-1 * i = Pn-1 *(1+i) = P *(1+i)n-1 *(1+i) = P *(1+i)n

Simple vs. Compound Interest

If $100 is deposited in a savings account, how much is in the account at the end of each year for 20 years, if interest is deposited in the account and no withdrawals are made? Assume a 5% interest per year.

Year F (Simple) F (Compound) Year F (Simple) F (Compound)0 100 100.00 11 155 171.031 105 105.00 12 160 179.592 110 110.25 13 165 188.563 115 115.76 14 170 197.994 120 121.55 15 175 207.895 125 127.63 16 180 218.296 130 134.01 17 185 229.207 135 140.71 18 190 240.668 140 147.75 19 195 252.709 145 155.13 20 200 265.3310 150 162.89

100

150

200

250

300

0 5 10 15 20

End of year

To

tal i

n A

cco

un

t at

yea

r E

nd

Simple vs. Compound Interest

Compound

Simple

In Class Problem #1If $500 is deposited in a savings account, would a 5% simple interest rate be better than a 3% compound interest rate if you were planning to keep the money for 3 years? For 35 years? Assume that all earned interest is deposited in the account and no withdrawals are made.

Example #1

Sam Bostro borrows $4000 from his parents for his final year of college. He agrees to repay it 3 years later in one payment to which a 7% compound interest rate will be applied.

a) How much does he repay?

F = (4000)(1 + 0.07)3 = $4,900.17

b) How much of this is interest and how much is principal?

F = P + I P = $4,000; I = $900.17

Example #2

Susan Cardinal deposited $500 in her savings account and six years later the account has $600 in it. What compound rate of interest has Susan earned on her capital?

F = P(1+i)n i = [F/P]1/n – 1i = [600/500] 1/6 – 1 = .031i = 3.1%

In Class Problem #2Your friend is willing to loan you $1500 to buy a new computer, but you must agree to pay him back $2500 when you graduate in 4 years? What is the compound interest rate you will be paying your friend?

Cash Flow Diagrams Pictorial description of when and

how much money is spent or received

Summarizes the economic aspects of an engineering project

0 1 2 3 4 5

Cash Flow Categories First Cost

Expense to build or to buy and install Operation and maintenance (O&M)

Annual expenses (electricity, labor, minor repairs, etc.)

Salvage value Receipt at project termination for sale or

transfer of equipment There can also be a salvage COST

Cash Flow Categories Revenues

Annual receipts due to sale of products or services

Overhauls Major capital expenditures that occurs part

way through the life of the asset Prepaid expenses

Annual expenses that must be paid in advance (e.g., leases, insurance)

ExamplesErnie’s Earthmoving is considering the purchase of a piece of heavy equipment. What is the cash flow diagram if the following cash flows are anticipated?First cost $120KO&M cost $30k per yearOverhaul cost $35K in year 3Salvage value $40K after 5 yearsHow would the cash flow diagram change if Ernie decides to lease the equipment (at $25K per year) instead of purchasing it?

a)

b)

Solution

0 1 2 3 4 5

0 1 2 3 4 5

a)

b)

120K

30K 30K30K +35K

30K 30K

40K

25K25 +30K

25 +30K 25K +

30K +35K

25K +30K

30K

Frequency of Compounding Interest rates are typically

specified on an annual basis However, interest is often

compounded more often Semiannually Quarterly Monthly Daily

Frequency of Compounding How does that change our formula?

m = # of compounding periods per year n = # of compounding periods

n = m x N Quarterly?

Monthly?

m = 4n = 4N F = P(1+i/m)m*N = P(1+i/4)4N

m=12n = 12N F = P(1+i/12)12N

ExampleSuppose you borrow $3000 at the beginning of your senior year to meet college expenses. If you make no payments for 10 years and then repay the entire amount of the loan, including accumulated interest, how much money will you owe? Assume interest is 6% per year, compoundeda) Annually m=1 P=3,000b) Quarterly m=4 N=10 yearsc) Monthly m=12 i=6% per yeard) Daily m=365How significant is the frequency of compounding?

SolutionFA = P(1+i/1)1N = 3000(1+0.06/1)10 = $5,372.54

FQ = P(1+i/4)4N = 3000(1+0.06/4)40 = $5,442.05

FM = P(1+i/12)12N = 3000(1+0.06/12)120 = $5,458.19

FD = P(1+i/365)1N = 3000(1+0.06/365)3650 = $5,466.08

SolutionCollege Loan Payment Options

$3,000.00

$3,000.00

$3,000.00

$3,000.00

$2,372.54

$2,442.06

$2,458.19

$2,466.09

$0 $1,000 $2,000 $3,000 $4,000 $5,000 $6,000

Annually

Quarterly

Monthly

Daily

Freq

uenc

y of

Com

pund

ing

Amount owed

Principal

Interest

In Class Problem #3You need to borrow $500 to pay for the text books you will need for your sophomore level courses. Which is the better loan assuming that you will pay the entire loan amount plus interest when you graduate in 3 years?

3.0% compounded annually 2.5% compounded quarterly