engineering insurance statistics 2009 - 2011€¦ · engineering insurance premium and loss...

TRANSCRIPT

Engineering InsurancePremium and Loss

Statistics 2009 - 2011

The International Association of Engineering Insurers TM

Presented by Allianz Global Corporate & Specialty

22 – 26 September 2012Rio de Janeiro, Brazil

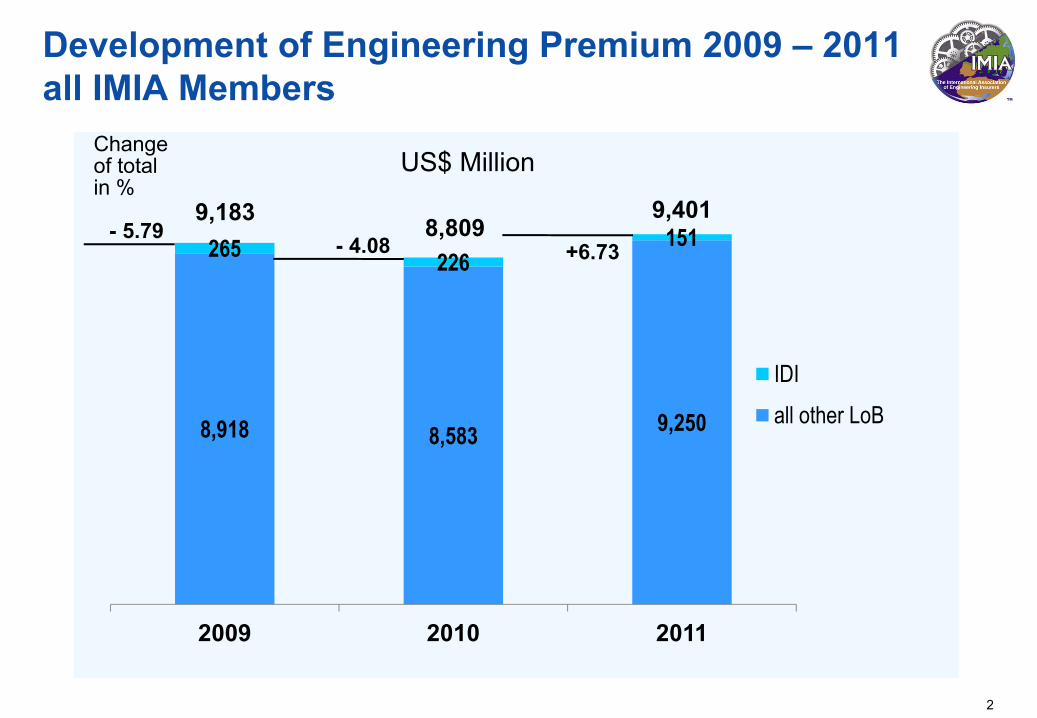

8,918 8,583 9,250

265 226151

2009 2010 2011

IDIall other LoB

Development of Engineering Premium 2009 – 2011all IMIA Members

2

US$ Million

- 4.08 +6.73- 5.79

Change of total in %

9,183 8,8099,401

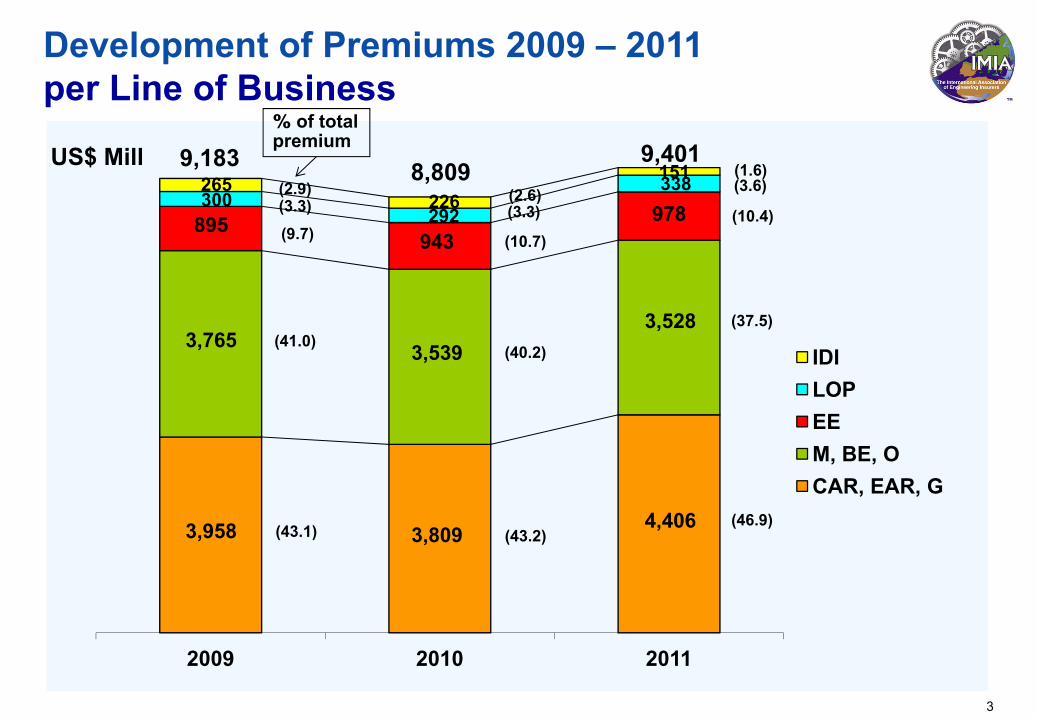

3,958 3,8094,406

3,765 3,5393,528

895943

978300

292

338265226

151

2009 2010 2011

IDILOPEEM, BE, OCAR, EAR, G

9,183 8,8099,401

Development of Premiums 2009 – 2011per Line of Business

% of total premium

(43.1)

(41.0)

(43.2)(46.9)

(40.2)

(37.5)

(9.7) (10.7)(10.4)(3.3)

(2.9)(3.3)(2.6) (3.6)

(1.6)

3

US$ Mill

0 500 1000 1500 2000

Finland

Sweden

Taiwan

Austria

Mexico

Netherlands

Spain

Switzerland

Australia

Turkey

Brazil

Canada

Italy

USA

Japan

Russia

Germany

Premiums and Claims 2011 per Country (excl. IDI)US$ Mill Loss Ratio (%)

2009 2010 2011

107

474165

86

50

18452945

115

73526756

50

2223492646

101

533266

73

45 53 50

2529443150

43 47 4164 91 101

58

60 38 39

23

ClaimsPremiums

7472 741316 12

4

0 20 40 60 80 100

Finland

Sweden

Taiwan

Austria

Netherlands

Mexico

Spain

Switzerland

Australia

Turkey

Brazil

Canada

Italy

USA

Japan

Russia

Germany

14

15

6

32

29

63

IDI - Premiums and Claims 2011 per Country US$ Mill

Loss Ratio (%)2009 2010 2011

ClaimsPremiums

20 68

8252

5

Note:Only two countries reported IDI premium and losses

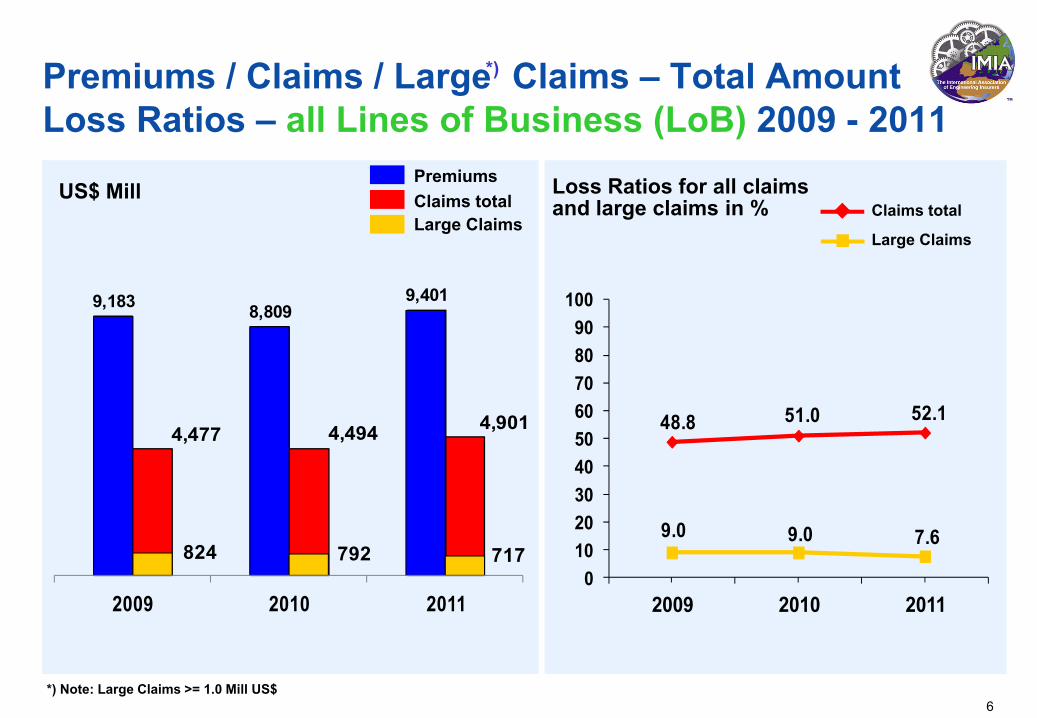

4,477 4,494 4,901

9,183 8,8099,401

824 792 717

2009 2010 2011

48.8 51.0 52.1

9.0 9.0 7.6

0102030405060708090

100

2009 2010 2011

6

Premiums / Claims / Large Claims – Total Amount Loss Ratios – all Lines of Business (LoB) 2009 - 2011

US$ MillClaims total

Large Claims

Claims totalPremiums

Large Claims

*)

*) Note: Large Claims >= 1.0 Mill US$

Loss Ratios for all claims and large claims in %

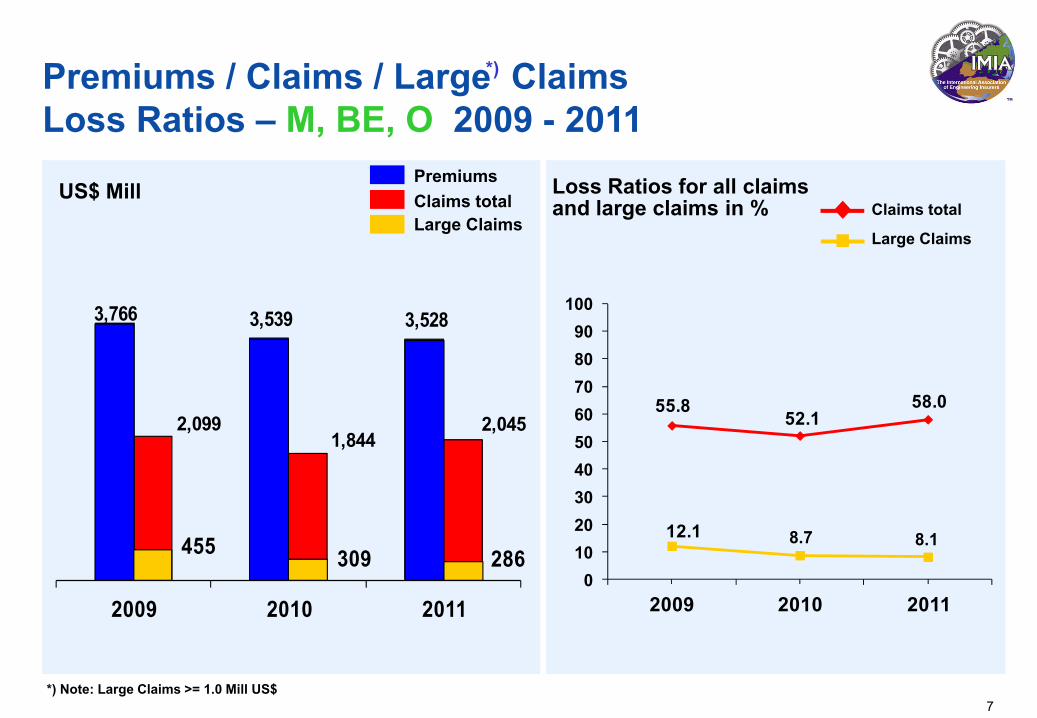

2,0991,844

2,045

3,766 3,539 3,528

455 309 286

2009 2010 2011

55.852.1

58.0

12.1 8.7 8.1

0102030405060708090

100

2009 2010 2011

7

US$ Mill

Premiums / Claims / Large Claims Loss Ratios – M, BE, O 2009 - 2011

Claims totalPremiums

Large ClaimsClaims total

Large Claims

Loss Ratios for all claims and large claims in %

*)

*) Note: Large Claims >= 1.0 Mill US$

191 209 230

299 292338

16 1235

2009 2010 2011

8

Premiums / Claims / Large Claims Loss Ratios – LoP 2009 - 2011

US$ Mill

63.771.6 68.0

5.4 3.910.5

0102030405060708090

100110

2009 2010 2011

Claims totalPremiums

Large ClaimsClaims total

Large Claims

Loss Ratios for all claims and large claims in %

*)

*) Note: Large Claims >= 1.0 Mill US$

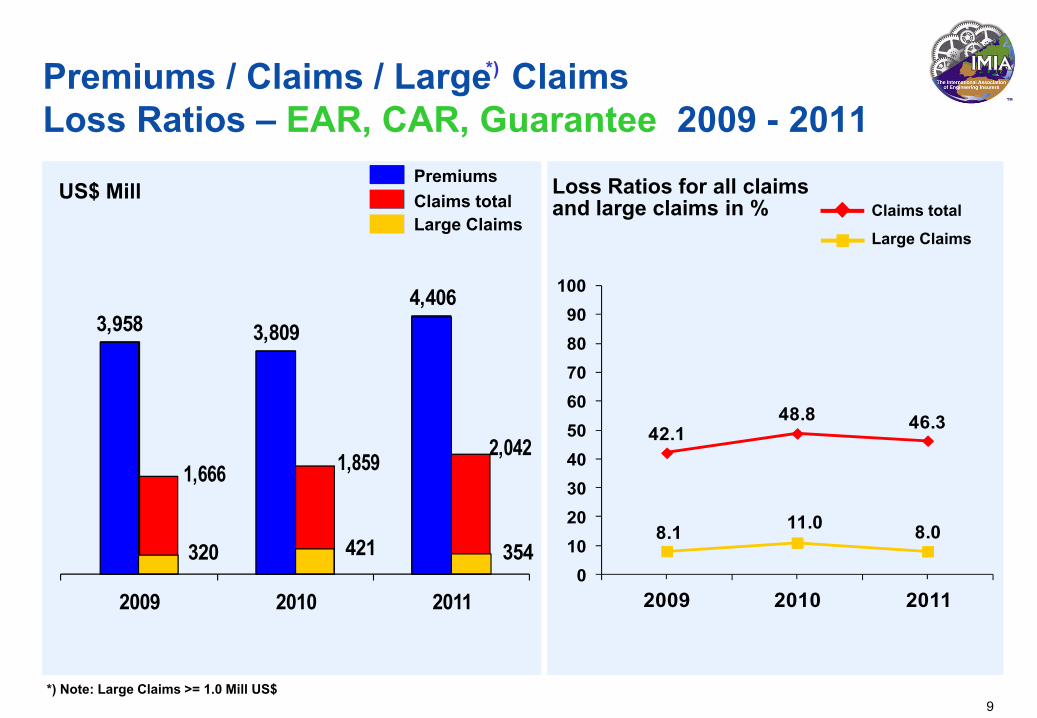

1,666 1,859 2,042

3,958 3,8094,406

320 421 354

2009 2010 2011

9

Premiums / Claims / Large Claims Loss Ratios – EAR, CAR, Guarantee 2009 - 2011

US$ Mill

42.148.8 46.3

8.1 11.0 8.0

0102030405060708090

100

2009 2010 2011

Claims totalPremiums

Large ClaimsClaims total

Large Claims

Loss Ratios for all claims and large claims in %

*)

*) Note: Large Claims >= 1.0 Mill US$

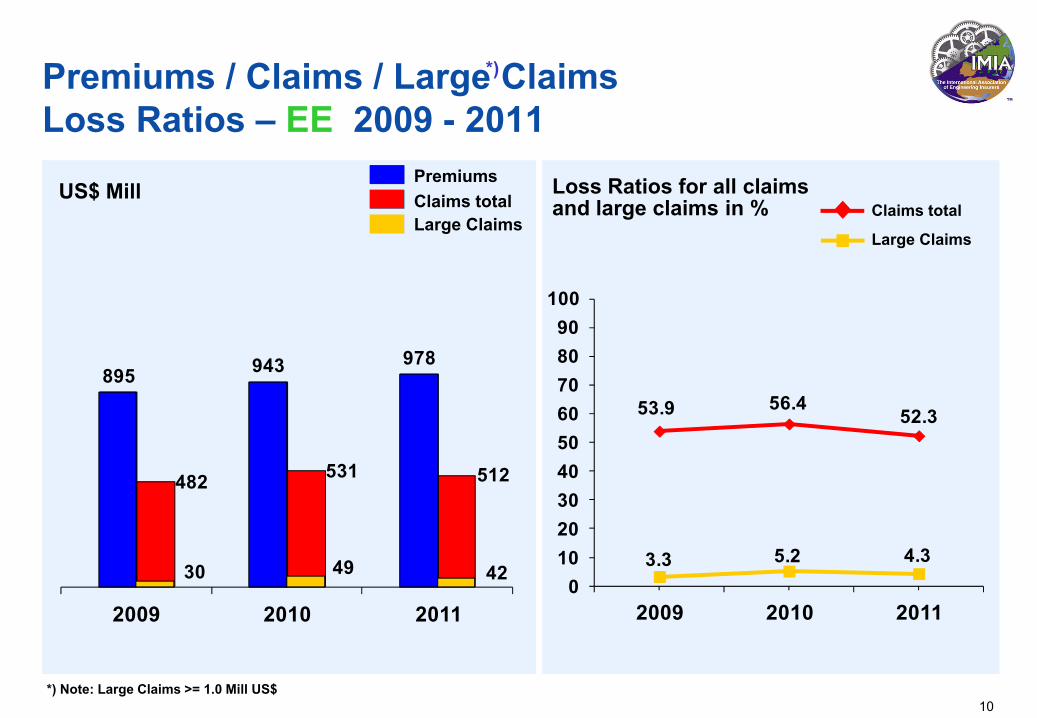

482 531 512

895 943 978

30 49 42

2009 2010 2011

10

Premiums / Claims / Large Claims Loss Ratios – EE 2009 - 2011

US$ Mill

53.9 56.452.3

3.3 5.2 4.30

102030405060708090

100

2009 2010 2011

Claims totalPremiums

Large ClaimsClaims total

Large Claims

Loss Ratios for all claims and large claims in %

*)

*) Note: Large Claims >= 1.0 Mill US$

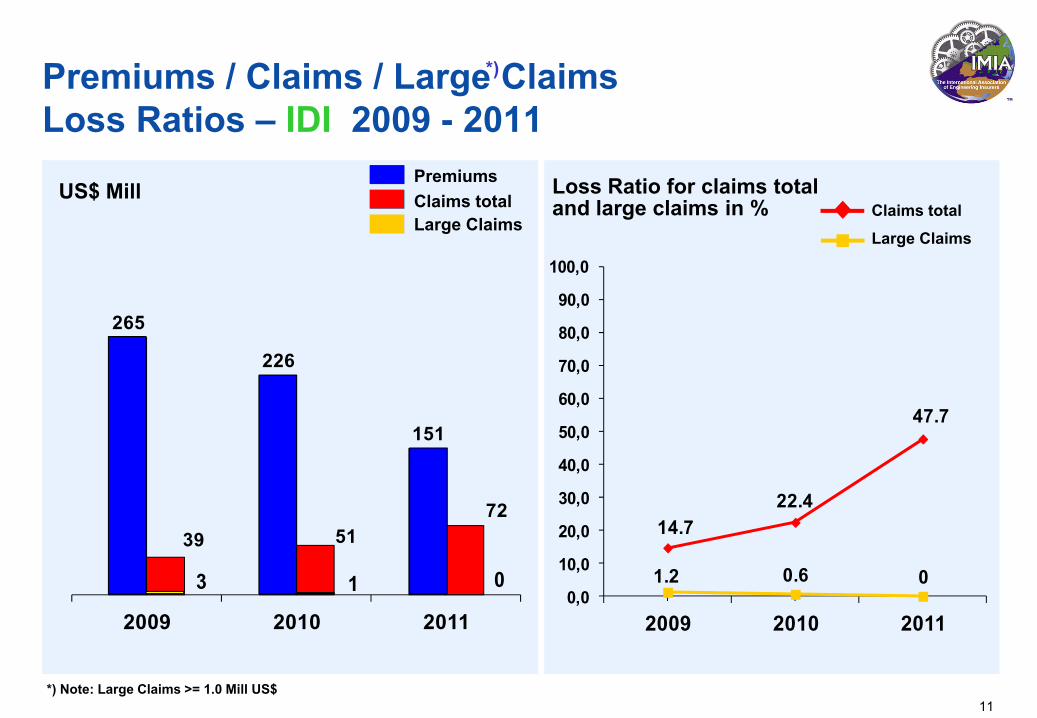

11

Premiums / Claims / Large Claims Loss Ratios – IDI 2009 - 2011

14.722.4

47.7

1.2 0.6 00,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

90,0

100,0

2009 2010 2011

US$ Mill Claims totalPremiums

Large ClaimsClaims total

Large Claims

Loss Ratio for claims total and large claims in %

*)

*) Note: Large Claims >= 1.0 Mill US$

265

226

151

39 5172

2009 2010 2011

3 1 0

5888 91 79 75

52

12286 96 10216

14

6 5 15

1

17

17 17172 1

0

50

100

150

200

250

2007 2008 2009 2010 2011

12

Number of Large Claims per LoB 2007 - 2011

IDI EELoPCAR. EAR. GM.BE.O

Total Engineering209

127

241

198202

A) Faulty OperationB) Faulty Material and

Workmanship

C) Faulty DesignD) Fire

E) ExplosionF) Natural Hazards

US$ Mill

0

50

100

150

200

250

300

350

2007 2008 2009 2010 2011A B C D E F G A B C D E F G A B C D E F G A B C D E F G A B C D E F G

Large Claims - Cause of Loss: all LoB 2007 - 2011

13

G) Other Causes

14

US$ Mill

93

60

12 114

78

0 0

27

0 10 20 30 40 50 60 70 80 90

100

A B C D E F G H I

A) Faulty OperationB) Faulty Material and

Workmanship

C) Faulty DesignD) Fire

E) ExplosionF) Storm

G) Flood and InundationH) EarthquakeI) Others

Large Claims - Cause of Loss: M, BE, Others 2011

15

119

0 01

0

4

0

10

0

5

10

15

20

25

30

A B C D E F G H I

US$ Mill

B) Faulty Material andWorkmanship

Large Claims - Cause of Loss: LoP 2011

A) Faulty Operation C) Faulty DesignD) Fire

E) ExplosionF) Storm

G) Flood and InundationH) EarthquakeI) Others

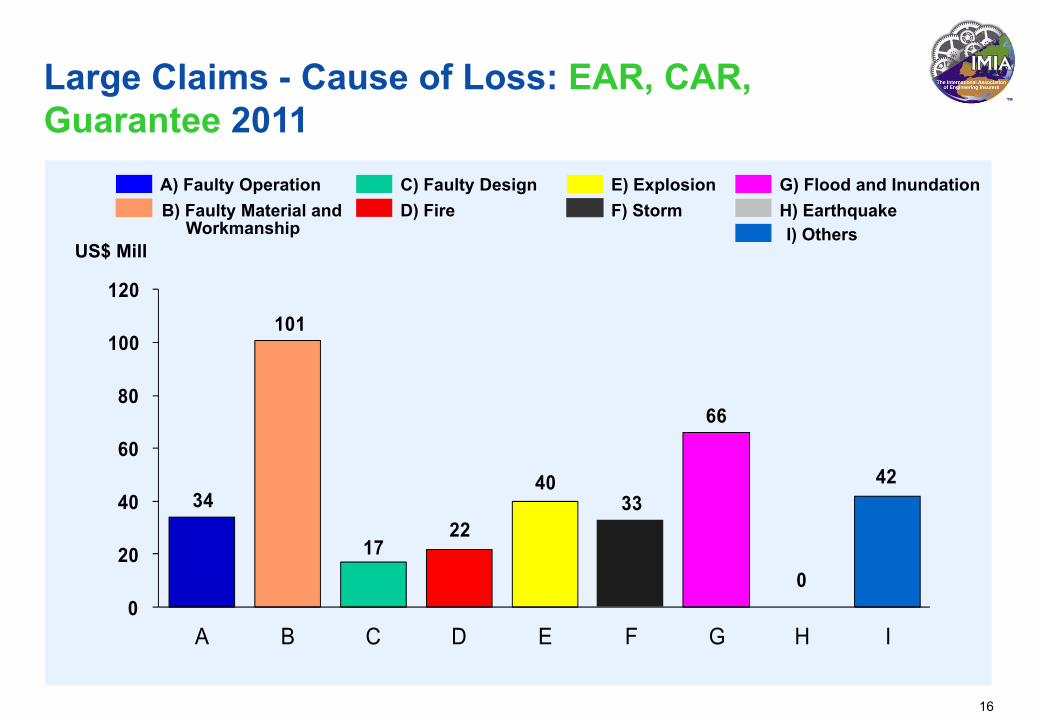

34

101

1722

4033

66

0

42

0

20

40

60

80

100

120

A B C D E F G H I

16

US$ Mill

Large Claims - Cause of Loss: EAR, CAR, Guarantee 2011

A) Faulty Operation C) Faulty DesignD) Fire

E) ExplosionF) Storm

G) Flood and InundationH) EarthquakeI) Others

B) Faulty Material andWorkmanship

17

32

30

7

0 0 0 0 00 5

10 15 20 25 30 35 40 45 50

A B C D E F G H I

US$ Mill

Large Claims - Cause of Loss: EE 2011

A) Faulty Operation C) Faulty DesignD) Fire

E) ExplosionF) Storm

G) Flood and InundationH) EarthquakeI) Others

B) Faulty Material andWorkmanship

18

0 0 0 0 0 0 0 0 00 5

10 15 20 25 30 35 40 45 50

US$ Mill

BA C D E F G H I

Large Claims - Cause of Loss: IDI 2011

A) Faulty Operation C) Faulty DesignD) Fire

E) ExplosionF) Storm

G) Flood and InundationH) EarthquakeI) Others

B) Faulty Material andWorkmanship

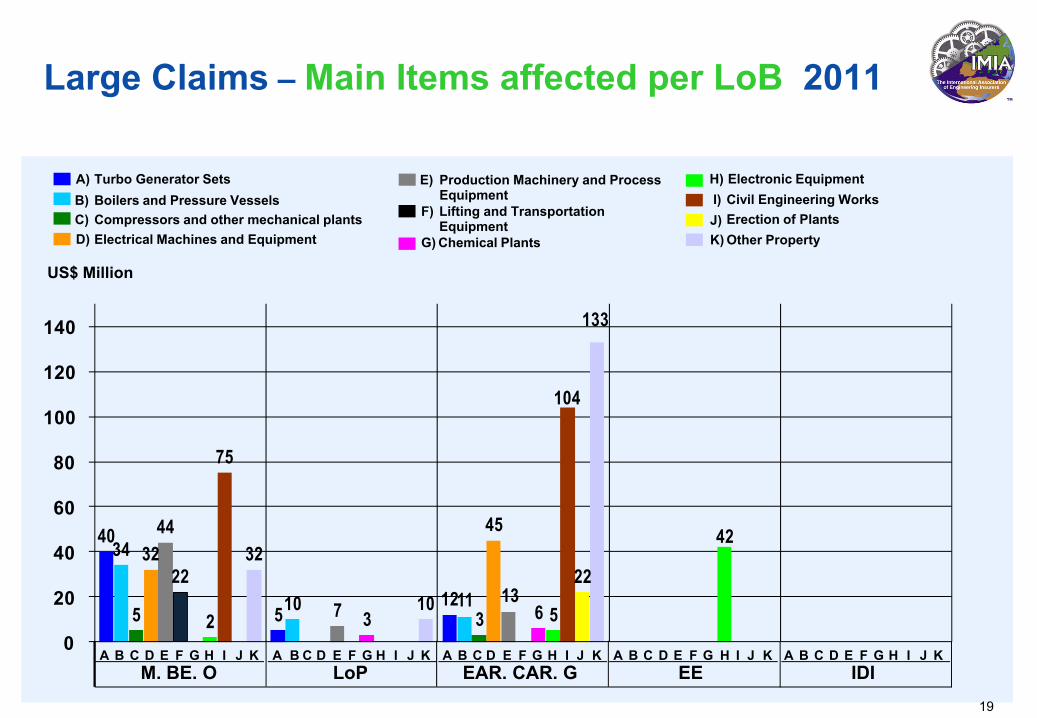

Large Claims – Main Items affected per LoB 2011

40

512

34

10 115 3

324544

713

22

3 62 5

42

75

104

2232

10

133

0

20

40

60

80

100

120

140

A) Turbo Generator SetsB) Boilers and Pressure VesselsC) Compressors and other mechanical plantsD) Electrical Machines and Equipment

F) Lifting and TransportationEquipment

G) Chemical Plants

H) Electronic EquipmentI) Civil Engineering WorksJ) Erection of Plants

E) Production Machinery and Process Equipment

K) Other Property

US$ Million

A B C D E F G H I J KM. BE. O

A B C D E F G H I J KLoP

A B C D E F G H I J KEAR. CAR. G

A B C D E F G H I J KEE

A B C D E F G H I J KIDI

19

20

Key to the abbreviationsBE Boiler ExplosionCAR Contractor‘s All RisksEAR Erection All RisksEE Electronic EquipmentG GuaranteeIDI Inherent Defects (Decennial) InsuranceLoB Line of BusinessLoP Loss of Profits (MLoP & ALoP) M Machinery BreakdownO Others

Please noteAll figures are based on information supplied to IMIA by its Member countries. It should be borne in mind that these figures may not always contain IBNR provisions, and that premium patterns may vary between reporting member countries and companies.Inherent Defects Insurance (IDI), also called Decennial Insurance in French speaking countries, is written only in a few countries. It is a compulsory class of business in some of these. Due to the different legal situation and others specifics, the scope of cover varies greatly from country to country. Therefore any attempt to make comparisons is very difficult and may lead to wrong conclusions. Since IDI contracts grant cover for material damage caused by latent defects for a period of (usually) ten years as from completion of the contract works, special attention needs to be given to the issue of premium earning patterns during the policy duration. These patterns vary considerably from country to country and are even regulated in some of them by the insurance supervisory body. IMIA is not in a position to reflect the various regulations governing the administration of this line of business in the various countries nor can IMIA validate the method used by its members in establishing their figures.Therefore IMIA recommends to adopt particular care when drawing conclusions from premiums, claims figures and loss ratios reported herein especially in respect of IDI. For further details it is recommended to contact the IMIA-delegate from a particular member country to obtain more accurate information on the particulars of a specific line of business in his country.