enestor dos santos – principal economist for latin america at bbva research macroeconomic outlook...

TRANSCRIPT

Enestor Dos Santos – Principal Economist for Latin America at BBVA Research

Macroeconomic outlook of the Pacific Alliance

MILADAY - October 2015

Pacific Alliance / MILADAY 2015

Página 2

Pacific Alliance: the real Latam giant

Pacific Alliance: macroeconomic prospects at the current juncture

Index

1

2

Pacific Alliance / MILADAY 2015

Página 3

Pacific Alliance (PA): the real Latam giant

Main contributions to world GDP growth in the next 10 years (PPP adjusted USD billions)Source: BBVA Research and FMI

Main economies in 2013(PPP adjusted USD millions) Source: BBVA Research y and FMI

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Ch

ina

Indi

a

EE

UU

AP

Indo

nes

ia

Bra

sil

Ru

sia

Co

rea

Japó

n

Tur

quía

Ale

man

ia

Re

ino

U.

MEX CHI COL PER13k 5k 4k

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

EE

UU

Ch

ina

Indi

a

Japó

n

Ale

man

ia

AP

Ru

sia

Bra

sil

Re

ino

U.

Fra

ncia

Italia

Co

rea

MEX CHI COL PER

16k 12k

Pacific Alliance / MILADAY 2015

Página 4

0

10

20

30

40

50

60

70

80

CH

I

ME

X

AP

PE

R

Lata

m7

CO

L

AR

G

BR

A

Pacific Alliance: a bloc committed to free trade

Trade openness * ( % GDP, 2008-201 average) Source: COMTRADE and BBVA Research

Latam: free-trade agreementsSourcee: OMC and BBVA Research

* Exports plus imports as a share of GDP.

ARGBRA

URUPAR VEN

MEX

COL

CHIPER

0

10

20

30

40

50

60

70

80

0 10 20 30 40 50 60

% d

el P

IB m

un

dia

l co

n e

l q

ue

se t

ien

e u

n T

LC

*

número de países con los que se tiene un TLC*

*TLC = Tratado de Libre Comercio

Alianza del Pacífico

Pacific Alliance / MILADAY 2015

Página 5

Pacific Alliance: growth based on demographic dynamism and middle classes expansion

Population growth rate(% annual, 2011-21)Source: BBVA Research

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

BRA MEX ANDINOS

Middle classes expansion(millions of people, 2011-21)Source: BBVA Research

Population growth, demographic bonusPopulation growth, demographic bonus

Inequality reductionInequality reduction

Increase of per capita income

Increase of per capita income

Middle classes expansion

0

2

4

6

8

10

12

14

16

18

20

BRA Alianza delPacifico

PER

COL

CHI

MEX

Pacific Alliance / MILADAY 2015

Página 6

Potential growth is high. Certainly higher than in other Latam countries.

Potential growth is high. Certainly higher than in other Latam countries.

However, contribution of productivity to GDP growth is relatively small (around

22%)…

However, contribution of productivity to GDP growth is relatively small (around

22%)…

Pacific Alliance: a high potential growth

Potential growth, next ten years (%)Fuente: BBVA Research

…which means that PA countries should continue focused on adopting reforms to

increase productivity

…which means that PA countries should continue focused on adopting reforms to

increase productivity

0

1

2

3

4

5

6

7

BRA MEX CHI COL PER EEUU UE China

Con reformas

Promedio APPA average

With reforms

Pacific Alliance / MILADAY 2015

Página 7

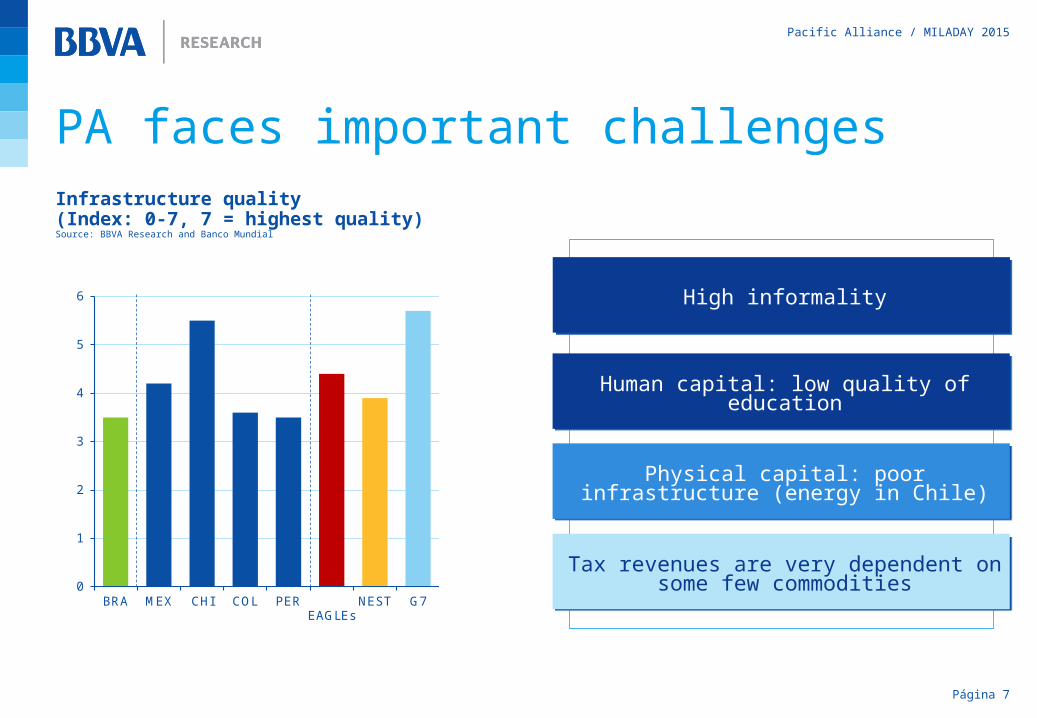

Human capital: low quality of educationHuman capital: low quality of education

Tax revenues are very dependent on some few commodities

Tax revenues are very dependent on some few commodities

Physical capital: poor infrastructure (energy in Chile)

Physical capital: poor infrastructure (energy in Chile)

PA faces important challengesInfrastructure quality(Index: 0-7, 7 = highest quality)Source: BBVA Research and Banco Mundial

0

1

2

3

4

5

6

BRA MEX CHI COL PEREAGLEs

NEST G7

High informalityHigh informality

Pacific Alliance / MILADAY 2015

Página 8

Pacific Alliance: the real Latam giant

Pacific Alliance: macroeconomic prospects at the current juncture

Index

1

2

Pacific Alliance / MILADAY 2015

Página 9

The external environment has not been as supportive as in the last years

Page 9

1. Commodity prices slumpBrent, USD/barrelSource: BBVA Research

405060708090

100110120130

mar

-08

dic-

08

sep-

09

jun-

10

mar

-11

dic-

11

sep-

12

jun-

13

mar

-14

dic-

14

sep-

15

jun-

16

Data Forecast, Oct-14

Forecast, Apr-15 Current Forecast, Sept-15

Mainly HigherSupply

LowerDemand

Economic Surprises …2. China’s bumpy slowdown and government reactionChina, Industrial Production, y/y, and PMI Source: BBVA Research

5

7

9

11

13

15

46

48

50

52

54

56

Aug

-10

Fe

b-1

1

Aug

-11

Fe

b-1

2

Aug

-12

Fe

b-1

3

Aug

-13

Fe

b-1

4

Aug

-14

Fe

b-1

5

Aug

-15

PMI IPI (rhs)

…as well as expected events

3. Incoming Fed’s tighteningSource: BBVA Research

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

mar

-08

mar

-09

mar

-10

mar

-11

mar

-12

mar

-13

mar

-14

mar

-15

mar

-16

mar

-17

Data Forecast, Oct-14 Current Forecast, Sept-15

Pacific Alliance / MILADAY 2015

Página 10

Growth has fallen, but less so in the PALatam: GDP growth forecastsSource: BBVA Research

Pacific Alliance: MEX, COL, PER, CHIMercosur: BRA, ARG, VEN, PAR, URU

-03

-02

-01

00

01

02

03

04

05

2012 2013 2014 2015 2016

LatAm Pacific Alliance Mercosur

The ugly: low productivity growthThe ugly: low productivity growth

The bad: still highly dependent on commodities and global growth

The bad: still highly dependent on commodities and global growth

The good: lower vulnerability than in the past (flexible exchange rate, inflation

targets, lower external and public debts, etc)

The good: lower vulnerability than in the past (flexible exchange rate, inflation

targets, lower external and public debts, etc)

Pacific Alliance / MILADAY 2015

Página 11

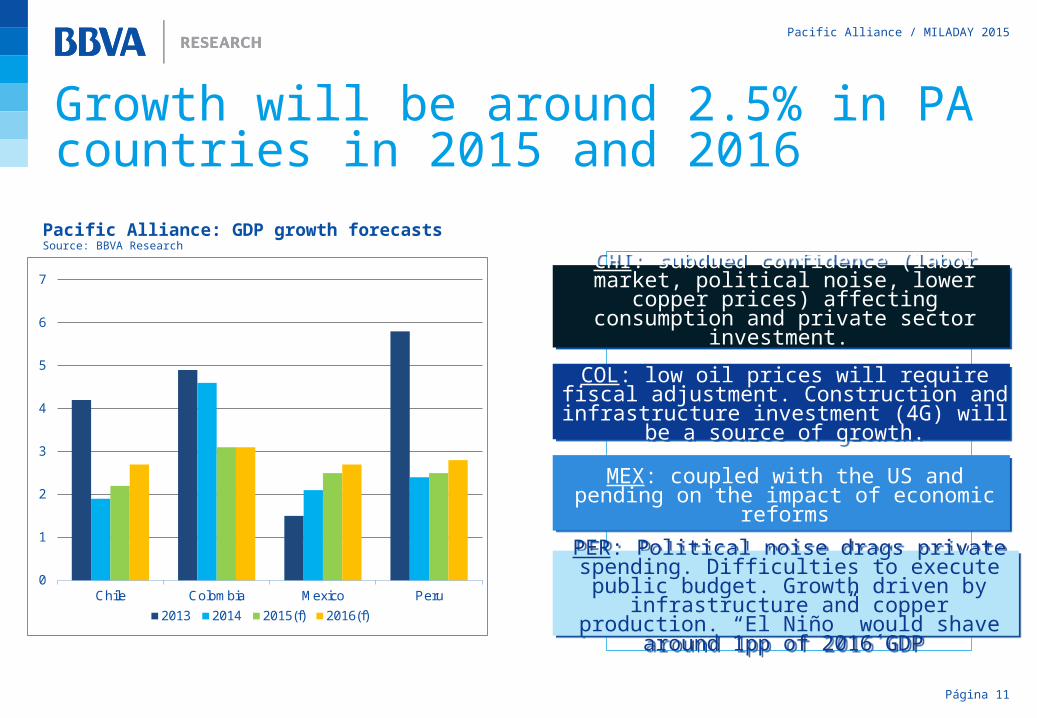

Growth will be around 2.5% in PA countries in 2015 and 2016

Pacific Alliance: GDP growth forecastsSource: BBVA Research

MEX: coupled with the US and pending on the impact of economic reforms

MEX: coupled with the US and pending on the impact of economic reforms

CHI: subdued confidence (labor market, political noise, lower copper prices)

affecting consumption and private sector investment.

CHI: subdued confidence (labor market, political noise, lower copper prices)

affecting consumption and private sector investment.

0

1

2

3

4

5

6

7

Chile Colombia Mexico Peru

2013 2014 2015(f) 2016(f)

PER: Political noise drags private spending. Difficulties to execute public budget. Growth driven by infrastructure and copper production. “El Niño” would

shave around 1pp of 2016´GDP

PER: Political noise drags private spending. Difficulties to execute public budget. Growth driven by infrastructure and copper production. “El Niño” would

shave around 1pp of 2016´GDP

COL: low oil prices will require fiscal adjustment. Construction and

infrastructure investment (4G) will be a source of growth.

COL: low oil prices will require fiscal adjustment. Construction and

infrastructure investment (4G) will be a source of growth.

Pacific Alliance / MILADAY 2015

Página 12

80

90

100

110

120

130

140

150

160

170

180

jun-1

4dic

-14

jun-1

5dic

-15

jun-1

6dic

-16

jun-1

4dic

-14

jun-1

5dic

-15

jun-1

6dic

-16

jun-1

4dic

-14

jun-1

5dic

-15

jun-1

6dic

-16

jun-1

4dic

-14

jun-1

5dic

-15

jun-1

6dic

-16

jun-1

4dic

-14

jun-1

5dic

-15

jun-1

6dic

-16

jun-1

4dic

-14

jun-1

5dic

-15

jun-1

6dic

-16

jun-1

4dic

-14

jun-1

5dic

-15

jun-1

6dic

-16

BRA CHI COL MEX PAR PER URU

Previsiones Observado

Exchange rate depreciation, driven to a great extent by Fed’s liftoff and commodity prices

Exchange rate vs USD in inflation targeting countries (index Dic 2014=100)Source: BBVA Research

Depreciation against USD

Pacific Alliance / MILADAY 2015

Página 13

Inflation is being pushed up by strong depreciation, despite weak activity. CBs to react.

Latam: Inflation (%yoy) and central bank target rangesSource: BBVA Research

0

2

4

6

8

10

Feb

-14

Au

g-14

Feb

-15

Au

g-15

Feb

-14

Au

g-14

Feb

-15

Au

g-15

Feb

-14

Au

g-14

Feb

-15

Au

g-15

Feb

-14

Au

g-14

Feb

-15

Au

g-15

Feb

-14

Au

g-14

Feb

-15

Au

g-15

Feb

-14

Au

g-14

Feb

-15

Au

g-15

Brasil Chile Colombia México Perú Uruguay

Inflation Inflation Target

Pacific Alliance / MILADAY 2015

Página 14

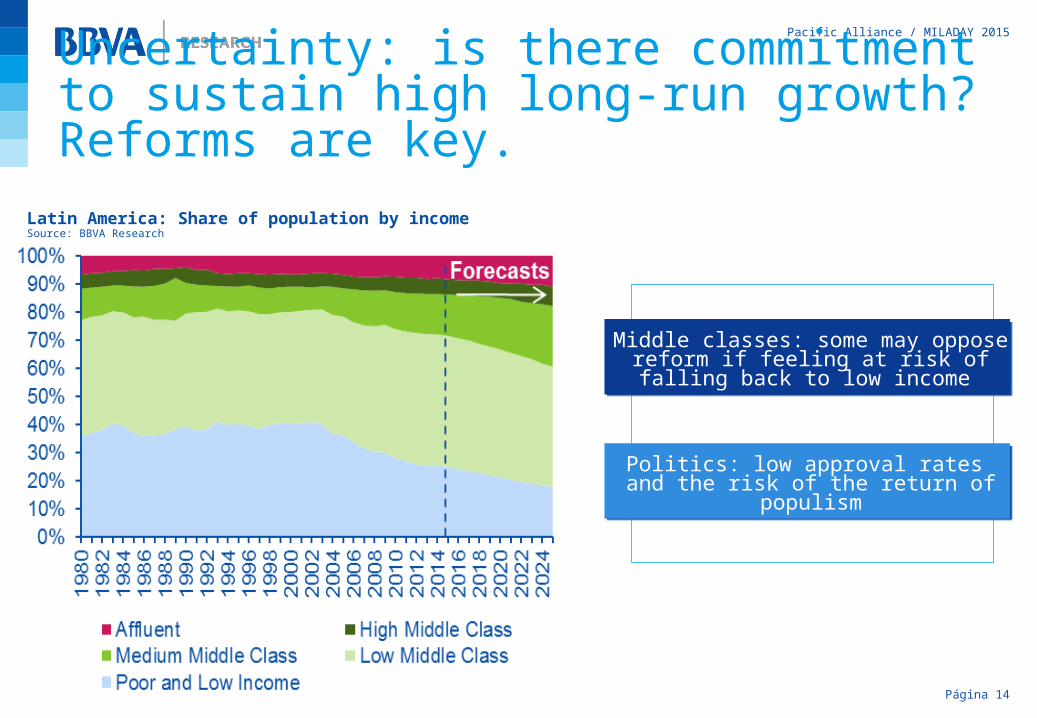

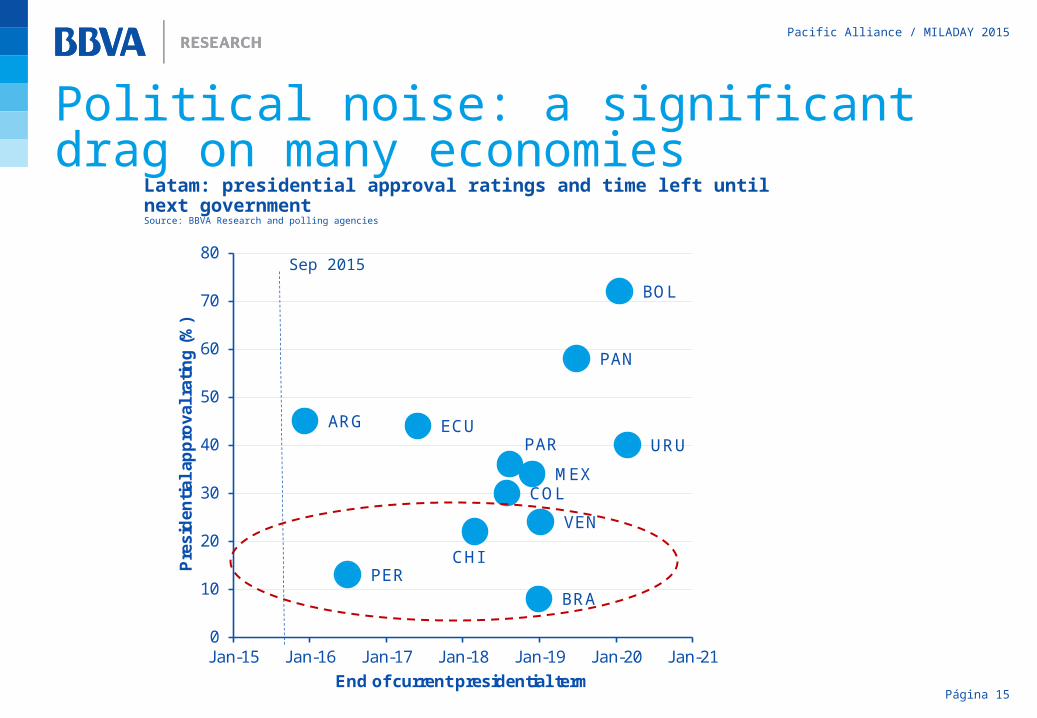

Uncertainty: is there commitment to sustain high long-run growth? Reforms are key.

Latin America: Share of population by incomeSource: BBVA Research

Politics: low approval rates and the risk of the return of populism

Politics: low approval rates and the risk of the return of populism

Middle classes: some may oppose reform if feeling at risk of falling

back to low income

Middle classes: some may oppose reform if feeling at risk of falling

back to low income

Pacific Alliance / MILADAY 2015

Página 15

ARG

BRA

COL

CHI

PAR

PER

URU

VEN

MEX

ECU

BOL

PAN

0

10

20

30

40

50

60

70

80

Jan-15 Jan-16 Jan-17 Jan-18 Jan-19 Jan-20 Jan-21

Pre

sid

enti

al a

pp

rov

al r

atin

g (

%)

End of current presidential term

Political noise: a significant drag on many economies

Latam: presidential approval ratings and time left until next government Source: BBVA Research and polling agencies

Sep 2015

Pacific Alliance / MILADAY 2015

Página 16

All in all: PA still controls its future …

Medium run:Populism

Long run:Inequality

Short run: lower global liquidity

Medium run: Chinese slowdown

Reforms that enhance productivity:

Physical capital, human capital,

reduce informality

2%-3% growth may be ideal environment to push reforms

(not too high, not too low)

… key to deal with risksStill on time

to implement Reforms 2.0

Enestor Dos Santos – Principal Economist for Latin America at BBVA Research

Macroeconomic outlook of the Pacific Alliance

MILADAY - October 2015

Pacific Alliance / MILADAY 2015

Página 18

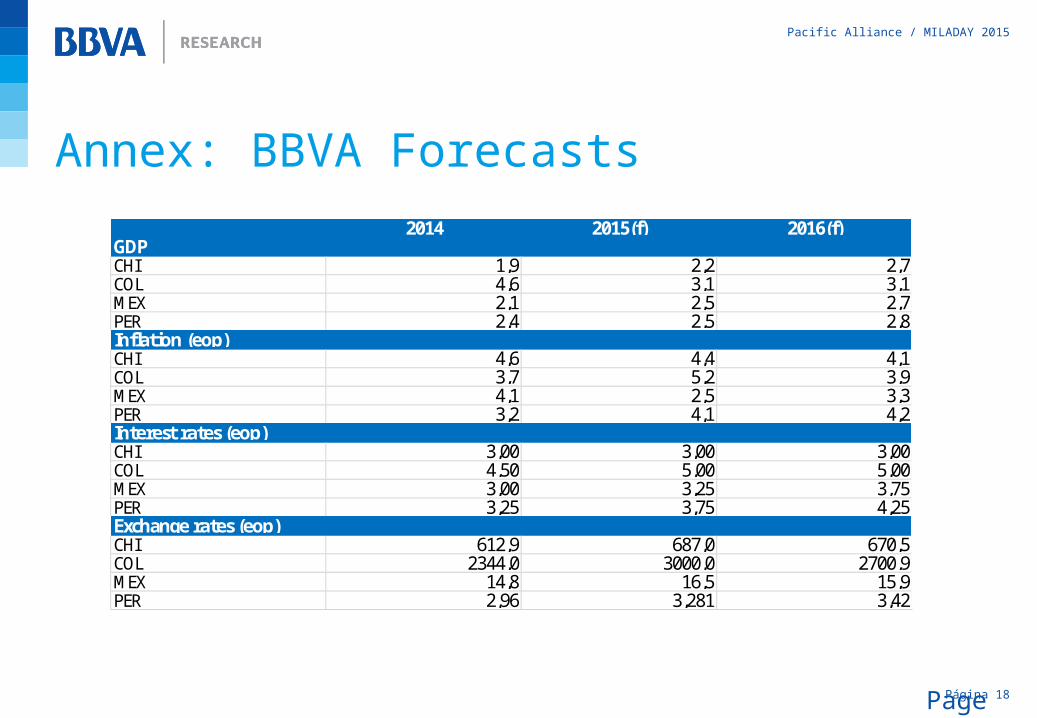

Annex: BBVA Forecasts

Page 18

2014 2015(f) 2016(f)GDPCHI 1,9 2,2 2,7COL 4,6 3,1 3,1MEX 2,1 2,5 2,7PER 2,4 2,5 2,8Inflation (eop)CHI 4,6 4,4 4,1COL 3,7 5,2 3,9MEX 4,1 2,5 3,3PER 3,2 4,1 4,2Interest rates (eop)CHI 3,00 3,00 3,00COL 4,50 5,00 5,00MEX 3,00 3,25 3,75PER 3,25 3,75 4,25Exchange rates (eop)CHI 612,9 687,0 670,5COL 2344,0 3000,0 2700,9MEX 14,8 16,5 15,9PER 2,96 3,281 3,42