energy modelling for south africa, latest approaches...

TRANSCRIPT

Dr Tobias Bischof-NiemzChief Engineer

Energy Modelling for South Africa, Latest Approaches & Results in a Rapidly Changing Energy EnvironmentKeynote Address at STERG Symposium 2017

Dr Tobias Bischof-Niemz, Head of the CSIR Energy Centre

Stellenbosch, 13 July 2017

Cell: +27 83 403 1108Email: [email protected]

4

Research Groups overview: Value-chain logic, driven by end-user demand and system view

Energy Efficiency

Technologies

Demand Shaping

Technologies

Technology-focussed Research GroupsEnd user-focussed

Research Groups

System-focussed

Research Group

Energy

Meteorology

Renewable

Energy

Technologies

Battery

Technologies

Hydrogen

Technologies

Heat Storage

Technologies

Energy System

Design

Energy System

Operation

Industry demand / pull

System view on

technologies user requirements

Technology

performance and cost

(today and future)

Products (hardware), solutions (software)

Energy

Demand

ED

Energy

Supply

ESu

Energy

Storage

ESt

Energy

Systems

ESy

E. Market Design

(DoE/NERSA)EM

Energy

Industry (DTI)

EI

Energy-Autonomous Campus

EACReal-world implementation of research programme

5

CSIR’s Energy Centre currently has ~40 highly qualified staff members

EC Leadership

Energy Demand

Demand Assessment in

End-use Sectors

Demand-side Technologies

(energy efficiency & demand shaping)

Demand Forecasting

(short-term, long-term, spatially)

Energy Supply

Resource Assessment

(solar & wind)

Renewable Energy Technologies(solar, wind, biogas, small hydro, HPs)

Supply Forecasting

(short-term, spatially)

Energy Storage

Batteries

(design and integration)

Hydrogen(production and

storage)

Heat Storage

Storage System Integration

(P2eMobility, P2pumping)

Energy Systems

Energy Planning

Grid Planning

(incl. smart grids)

Island Grids

Energy-System Operations

Energy Markets and Policy

Energy Economics

Energy Markets(local, regional,

global)

Energy Regulation

Energy Trading

Energy Statistics

Energy Industry

Local Content

Energy Industry Development

???

Energy-Autonomous

Campus

EAC Energy Demand

EAC Energy Supply

EAC Energy Storage

EAC Grid Design

EAC Operations(control and visualisation)

Administrative Support Functions

Research Support Functions

1) Technical (labs, GIS)2) Project Management3) Specialist

1) Head2) Technical Lead3) Commercial Lead4) Operational Lead5) HCD Lead

38 33 41 29 14 18 194

112

1

0

21

7

11

0

0

2

9

2

4

0

1

1

6

13

31

11

4

10

0

Interns Bursars

21

4

Emp

loye

es

Inte

rns/

Stu

de

nts

~20

2

5

Emp

loye

es

ED ESu ESt ESy EM EI EAC

RSFASF

ECL

In recruitment

process

Position

filled

Long-term

plan

6

HCD Highlights: Quick ramp up, very strong and diverse team

Very fast, yet very high-profile ramp-up achieved sofar (from 0 in July 2014 to 40 in July 2017)

Entire leadership team (Research Group Leaders and Programme Managers) is South African and black

4 black female engineers (South African)

Examples of internationally recognised experts

• Former head of systems operations at Eskom, was in charge to operate entire national grid

• Energy Commissioner in the National Planning Commission led by Minister in the Presidency

• Former CEO/MD of Swaziland Electricity Company, well connected in the region

• Chief Engineer transmission grid planning for Eskom and the region

7

Context

8

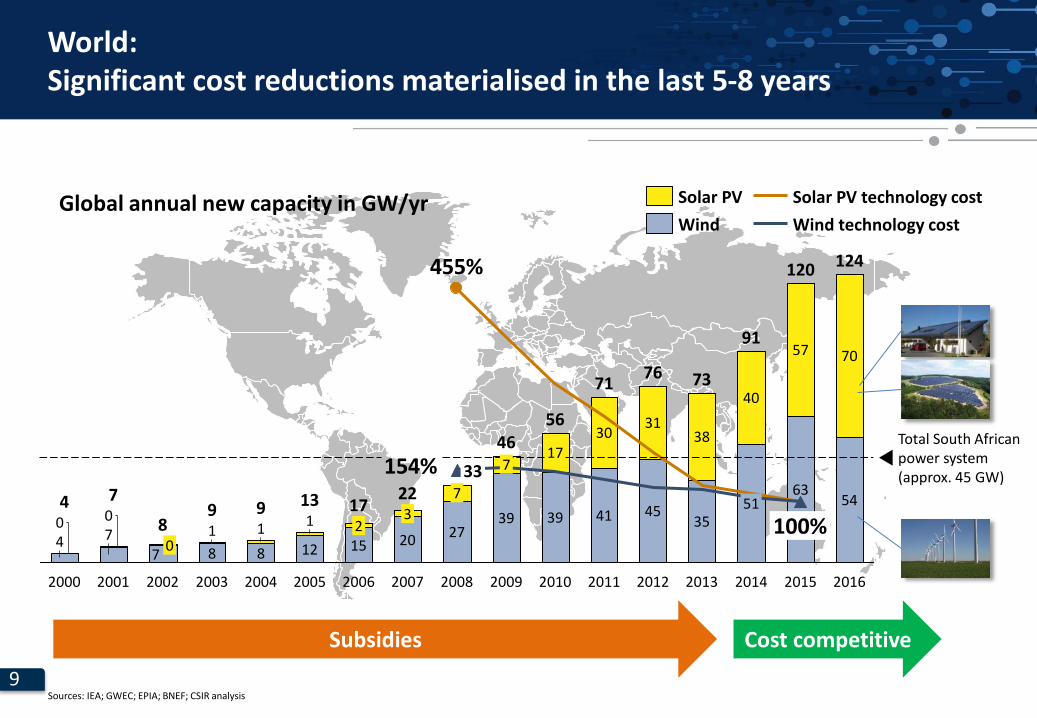

World:In 2016, 124 GW of new wind and solar PV capacity installed globally

124

54

70

2015

120

63

57

2014

91

51

40

2013

73

35

38

2012

76

45

31

2011

7

2008

33

27

7

2007

22

20

3

2006

17

152

2005

13

121

2004

9

81

2003

9

81

2002

71

70

2001

77 0

2000

44 0

841

30

2010

56

39

17

2009

46

39

2016

Total South Africanpower system(approx. 45 GW)

Wind

Solar PV

Sources: GWEC; EPIA; BNEF; CSIR analysis

Global annual new capacity in GW/yr

This is all very new: Roughly 80% of the globally existing solar PV capacity was installed during the last five years

9

World:Significant cost reductions materialised in the last 5-8 years

455%

154%7

70

2000

4

40

33

27

7

2007

22

20

3

2006

152

2005

13

12

1

2004

9

8

1

17100%

9

8

1

2002

8

70

2001 2003

124

54

70

2015

120

63

57

2014

91

51

40

2016

Total South Africanpower system(approx. 45 GW)

2013

73

35

38

2012

76

45

31

2011

71

41

30

2010

56

39

17

2009

46

39

7

2008

Wind technology cost

Solar PV

Wind

Solar PV technology cost

Sources: IEA; GWEC; EPIA; BNEF; CSIR analysis

Subsidies Cost competitive

Global annual new capacity in GW/yr

10

Renewables until today mainly driven by US, Europe, China and JapanGlobally installed capacities for three major renewables wind, solar PV and CSP end of 2015

40

82

1.9

USA

Sources: GWEC; EPIA; CSPToday; CSIR analysis

Europe

77

0.3

169

China

0.52.53.9

Middle Eastand Africa

7 04

Rest of Asia Pacific02

19

Americasw/o USA/Canada

Total RSA power

system (45 GW)

CSP

5.1

Solar PV

302

Wind

487

Total World

50

03

Japan9

29

0.2

India

064

Australia

Operational capacities in GW

end of 2016

2.3

111

161

2 012

Canada

South Africa has 1.5/1.5/0.2 GW installed capacity of wind, solar PV

and CSP end of 2016

16

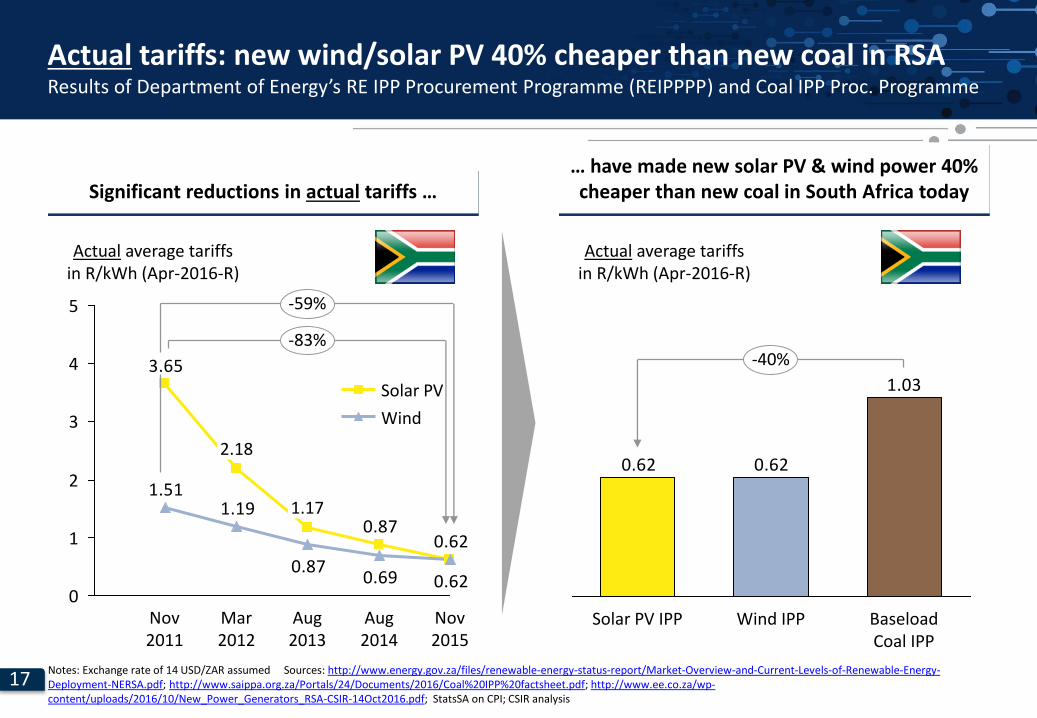

Significant reductions in actual tariffs …

REIPPPP results: new wind/solar PV 60-80% cheaper than first projectsResults of Department of Energy’s RE IPP Procurement Programme (REIPPPP) and Coal IPP Proc. Programme

0.620.87

3.65

0.620.690.87

1.191.51

0

1

2

3

4

5

-83%

-59%

Nov 2015

Aug 2014

Aug 2013

1.17

Mar 2012

2.18

Nov 2011

Wind

Solar PV

Notes: Exchange rate of 14 USD/ZAR assumed Sources: http://www.energy.gov.za/files/renewable-energy-status-report/Market-Overview-and-Current-Levels-of-Renewable-Energy-Deployment-NERSA.pdf; http://www.saippa.org.za/Portals/24/Documents/2016/Coal%20IPP%20factsheet.pdf; http://www.ee.co.za/wp-content/uploads/2016/10/New_Power_Generators_RSA-CSIR-14Oct2016.pdf; StatsSA on CPI; CSIR analysis

Actual average tariffsin R/kWh (Apr-2016-R)

17

Significant reductions in actual tariffs …

Actual tariffs: new wind/solar PV 40% cheaper than new coal in RSAResults of Department of Energy’s RE IPP Procurement Programme (REIPPPP) and Coal IPP Proc. Programme

0.620.87

3.65

0.620.690.87

1.191.51

0

1

2

3

4

5

-83%

-59%

Nov 2015

Aug 2014

Aug 2013

1.17

Mar 2012

2.18

Nov 2011

Wind

Solar PV

Notes: Exchange rate of 14 USD/ZAR assumed Sources: http://www.energy.gov.za/files/renewable-energy-status-report/Market-Overview-and-Current-Levels-of-Renewable-Energy-Deployment-NERSA.pdf; http://www.saippa.org.za/Portals/24/Documents/2016/Coal%20IPP%20factsheet.pdf; http://www.ee.co.za/wp-content/uploads/2016/10/New_Power_Generators_RSA-CSIR-14Oct2016.pdf; StatsSA on CPI; CSIR analysis

1.03

0.620.62

-40%

Baseload Coal IPP

Wind IPPSolar PV IPP

… have made new solar PV & wind power 40% cheaper than new coal in South Africa today

Actual average tariffsin R/kWh (Apr-2016-R)

Actual average tariffsin R/kWh (Apr-2016-R)

18

Approach to Power-System Planning

19

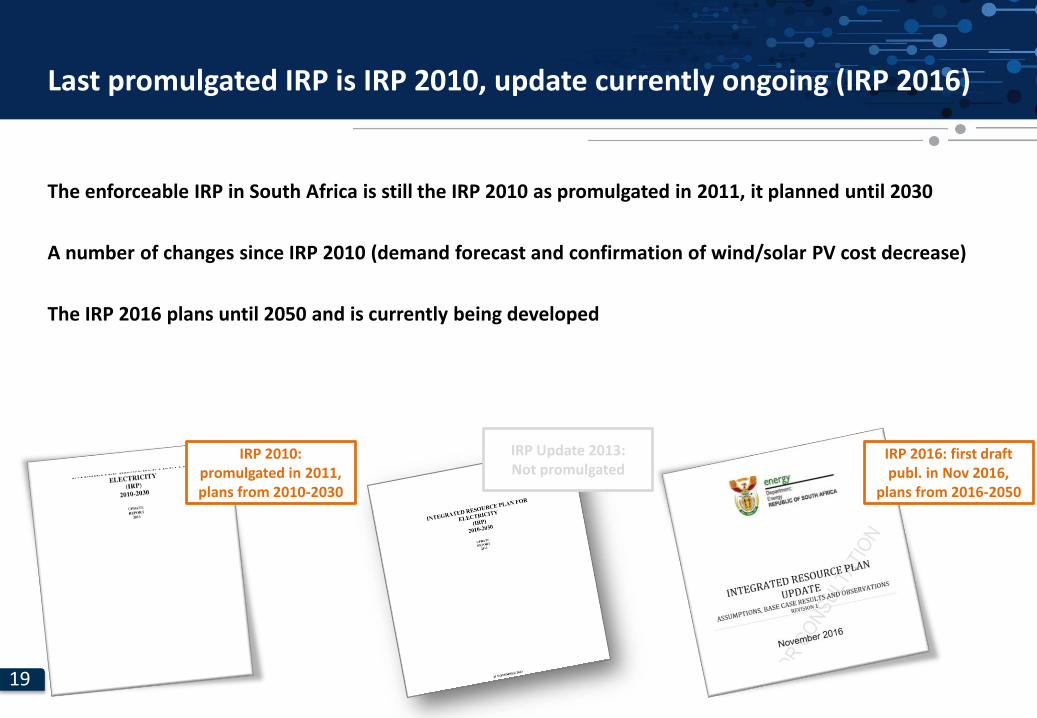

Last promulgated IRP is IRP 2010, update currently ongoing (IRP 2016)

The enforceable IRP in South Africa is still the IRP 2010 as promulgated in 2011, it planned until 2030

A number of changes since IRP 2010 (demand forecast and confirmation of wind/solar PV cost decrease)

The IRP 2016 plans until 2050 and is currently being developed

IRP 2010: promulgated in 2011, plans from 2010-2030

IRP 2016: first draft publ. in Nov 2016,

plans from 2016-2050

IRP Update 2013: Not promulgated

21

IRP process as described in the Department of Energy’s Draft IRP 2016 document: least-cost Base Case is derived from technical planning facts

Least CostBase Case

Scenario 2Scenario 1

Scenario 3

Case Cost

Base Case Base

Scenario 1 Base + Rxx bn/yr

Scenario 2 Base + Ryy bn/yr

Scenario 3 Base + Rzz bn/yr

… …

Constraint: RE limits

Constraint: e.g. forcing in of nuclear, CSP, biogas, hydro, others

Constraint: Advanced CO2

cap decline

1. Public consultationon costed scenarios

2. Policy adjustment of Base Case

3. Final IRP for approval and gazetting

PlanningFacts

Sources: based on Department of Energy’s Draft IRP 2016, page 7; http://www.energy.gov.za/IRP/2016/Draft-IRP-2016-Assumptions-Base-Case-and-Observations-Revision1.pdf

22

The CSIR conducted in-depth power-system analyses to determine the least-cost expansion path for the South African electricity system

The Integrated Resource Plan (IRP) is currently being updated by the Department of Energy / Eskom

Draft IRP 2016 Base Case entails a limitation: Amount of wind and solar PV capacity that the model is allowed to build per year is limited, which is neither technically nor economically justified/explained (no techno-economical reason provided)

The CSIR is therefore conducting a study to determine the Least Cost electricity mix in RSA until 2050

• Majority of assumptions kept exactly as per the Draft IRP 2016 Base Case

• First and most important deviation from IRP 2016: no new-build limits on renewables (wind/solar PV)

• Second (smaller) deviation: costing for solar PV and wind until 2030 aligned with latest IPP tariff results

• Scope of the CSIR study: purely techno-economical optimisation of the costs directly incurred in the power system

Two scenarios from the Draft IRP 2016 are compared with the Least Cost case

• “Draft IRP 2016 Base Case” – new coal, new nuclear

• “Draft IRP 2016 Carbon Budget” – significant new nuclear

• “Least Cost” – least-cost without constraints

An hourly capacity expansion and dispatch model (incl. unit commitment) using PLEXOS is run for all scenarios to test for technical adequacy same software platform as by Eskom/DoE for the IRP

Sources: CSIR analysis

23

[bR/yr]

Generation (Gx)

Total system

cost

Other(metering, billing, customer services,

overheads)

System services3

Distribution network

(Dx)

Transmission network

(Tx)

The IRP currently only optimises for the generation cost component of total system cost (this is the dominant component)

Optimised in PLEXOS model

Costs included in Gxoptimisation model:• CAPEX (plant level)• FOM1

• VOM2

• Fuel

Costs excluded in Gxoptimisation model:• Externalities e.g. CO2

emissions costs• Decommissioning

costs• Waste management

and/or rehabilitation• Major mid-life

overhaul• Shallow grid

connection costs

1 FOM = Fixed Operations and Maintenence costs; 2 VOM = Variable Operations and Maintenence costs; 3 Typically referred to as Ancillary Services includes services to ensure frequency stability, transient stability, provide reactive power/voltage control, ensure black start capability and system operator costs.

Not optimised in PLEXOS modelling framework(CSIR assumption for all scenarios = 0.30 R/kWh)

High-level costing applied to PLEXOS

outcomes

Not considered

Qualitatively discussed (quantified for system inertia)

Not considered

24

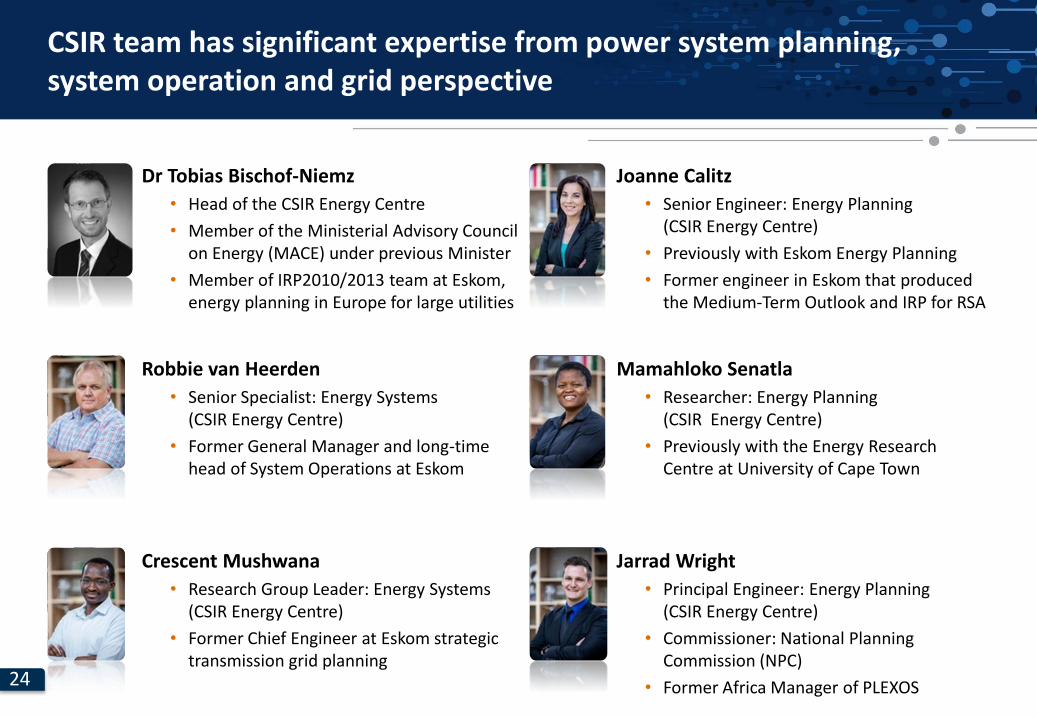

CSIR team has significant expertise from power system planning, system operation and grid perspective

Dr Tobias Bischof-Niemz

• Head of the CSIR Energy Centre

• Member of the Ministerial Advisory Council on Energy (MACE) under previous Minister

• Member of IRP2010/2013 team at Eskom, energy planning in Europe for large utilities

Jarrad Wright

• Principal Engineer: Energy Planning (CSIR Energy Centre)

• Commissioner: National Planning Commission (NPC)

• Former Africa Manager of PLEXOS

Robbie van Heerden

• Senior Specialist: Energy Systems (CSIR Energy Centre)

• Former General Manager and long-time head of System Operations at Eskom

Crescent Mushwana

• Research Group Leader: Energy Systems (CSIR Energy Centre)

• Former Chief Engineer at Eskom strategic transmission grid planning

Mamahloko Senatla

• Researcher: Energy Planning (CSIR Energy Centre)

• Previously with the Energy Research Centre at University of Cape Town

Joanne Calitz

• Senior Engineer: Energy Planning (CSIR Energy Centre)

• Previously with Eskom Energy Planning

• Former engineer in Eskom that produced the Medium-Term Outlook and IRP for RSA

25

Key Input Assumptions

26

450

400

300

350

500

550

250

200

150

100

50

0

428

2040

268

356

454

2050

522

344

Electricity Demand

in TWh/yr

203020202016

Input as per IRP 2016: Demand is forecasted to double by 2050Forecasted demand for the South African electricity system from 2016 to 2050

Sources: DoE (IRP 2016); Eskom MTSAO 2016-2021; StatsSA; World Bank; CSIR analysis

Note: by 2050 the electricity demand per capita would still be less than that of Australia today

IRP 2016

IRP 2010

27

400

350

300

550

500

450

0

50

100

200

150

250

82

2040

260

20202016

174

20502030

Electricity

in TWh/yr

Input as per IRP 2016: Decommissioning schedule for existing plantsEnergy supplied to the South African electricity system from existing plants between 2016 and 2050

Wind

CSP

Solar PV

Other

Peaking

Hydro+PS

Gas (CCGT)

Nuclear

Coal

Decommissioning of Eskom’s coal fleet

All power plants considered for “existing fleet” that are either:1) Existing in 20162) Under construction3) Procured (preferred bidder)

Demand

Sources: DoE (IRP 2016); Eskom MTSAO 2016-2021; StatsSA; World Bank; CSIR analysis

Existing supply

28

0

50

100

150

200

300

400

500

250

350

550

450

Electricity

in TWh/yr

20302020 2040 20502016

42084 254 439

428

344

522

Demand grows, existing fleet phases out – gap needs to be filledForecasted supply and demand balance for the South African electricity system from 2016 to 2050

Supply gap

Other

Peaking

Gas (CCGT)

Hydro+PS

Nuclear

Coal

Solar PV

CSP

Wind

The IRP model fills the supply gap in the least-cost manner, subject to any constraints imposed on the model

Demand

Note: All power plants considered for “existing fleet” that are either Existing in 2016, Under construction, or Procured (preferred bidder)Sources: DoE (IRP 2016); Eskom MTSAO 2016-2021; StatsSA; World Bank; CSIR analysis

Decommissioning of Eskom’s coal fleet

29

PLEXOS actual inputs are individual cost items that together with the utilisation of the plant (a model output) allow to calculate LCOE

Overnight Cost (plant level)

Construction Cash Schedule

Discount Rate

Economic Lifetime

Fixed O&M (FOM)

Variable O&M (VOM)

Fuel Price

Heat Rate (1/efficiency)

FIXED COST

VARIABLE COST

LCOE

Utilisation (capacity factor)

R/kW

%/a

%

a

h/a

R/kW/a

R/kWh

R/GJ

kJ/kWh

CAPEX(plant level)

R/kW

Annualised CAPEX

R/kW/a

Fuel Cost

R/kWh

R/kW/a

R/kWh

f

f

+

x

+

./. +R/kWh

PLEXOS inputs

PLEXOS output

30

0.620.62

Variable(Fuel)

Fixed(Capital, O&M)

Diesel (OCGT)

3.69

Gas (OCGT)

2.89

Mid-merit Coal

1.41

Gas (CCGT)

1.41

Nuclear

1.09

Baseload Coal (PF)

1.00

Wind

2011

Solar PV

2011

Inputs as per IRP 2016:Key resulting LCOE from cost assumptions for new supply technologies

50%90% 50% 10%Assumed capacity factor2 10%

Today’s new-build lifetime cost per energy unit1

(LCOE) in R/kWh (April-2016-Rand)

1 Lifetime cost per energy unit is only presented for brevity. The model inherently includes the specific cost structures of each technology i.e. capex, Fixed O&M, variable O&M, fuel costs etc.2 Changing full-load hours for new-build options drastically changes the fixed cost components per kWh (lower full-load hours higher capital costs and fixed O&M costs per kWh); Assumptions: Average efficiency for CCGT = 55%, OCGT = 35%; nuclear = 33%; IRP costs from Jan-2012 escalated to May-2016 with CPI; assumed EPC CAPEX inflated by 10% to convert EPC/LCOE into tariff; Sources: IRP 2013 Update; Doe IPP Office; StatsSA for CPI; Eskom financial reports for coal/diesel fuel cost; EE Publishers for Medupi/Kusile; Rosatom for nuclear capex; CSIR analysis

82%

As per South African IRP 2016

0 0 1 000 0 1 000400 600 600

CO2 in kg/MWh

31

Supply technologies (technical characteristics)

Sources: CSIR Wind and solar Aggregation Study

Similar to the IRP 2016 - wind and solar PV profiles for 27 supply areas (with exclusion masks) were used

NOTE: These profiles were then aggregated into one profile that defines expected new wind and solar PV profiles

32

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

Hour of the year

Normalised power output

Wind: supply profile assumptions

UtilisationAnnual capacity factor = 36%

33

Solar PV: supply profile assumptions

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

Hour of the year

Normalised power output Utilisation

Annual capacity factor = 20.4%

34

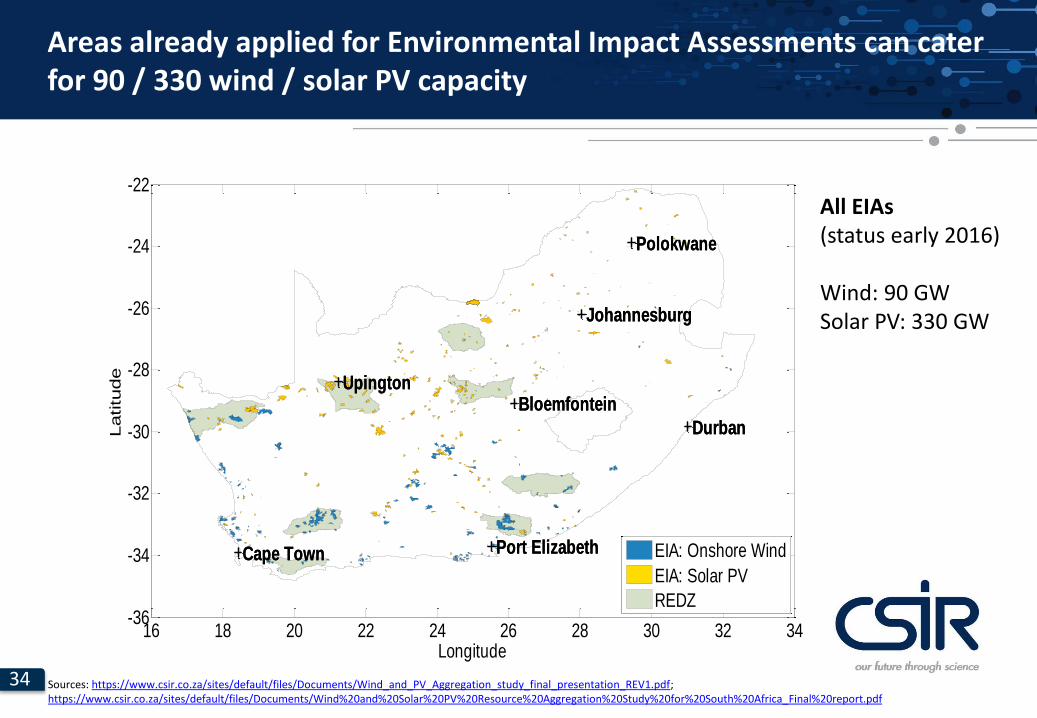

Areas already applied for Environmental Impact Assessments can cater for 90 / 330 wind / solar PV capacity

16 18 20 22 24 26 28 30 32 34-36

-34

-32

-30

-28

-26

-24

-22

Johannesburg

Cape Town

Durban

Upington

Port Elizabeth

Bloemfontein

Polokwane

Johannesburg

Cape Town

Durban

Upington

Port Elizabeth

Bloemfontein

Polokwane

Longitude

Latitu

de

EIA: Onshore Wind

EIA: Solar PV

REDZ

All EIAs(status early 2016)

Wind: 90 GWSolar PV: 330 GW

Sources: https://www.csir.co.za/sites/default/files/Documents/Wind_and_PV_Aggregation_study_final_presentation_REV1.pdf; https://www.csir.co.za/sites/default/files/Documents/Wind%20and%20Solar%20PV%20Resource%20Aggregation%20Study%20for%20South%20Africa_Final%20report.pdf

35

Results

36

Draft IRP 2016 Base Case is a mix of roughly 1/3 coal, nuclear, RE each

Draft IRP 2016 Base Case

100

550

400

450

500

350

300

250

200

150

50

0

13

2016

243

202

28(5%)

15

33(6%)

47(9%)

93(18%)

2040

15

434

Total electricity produced in TWh/yr

223

35

33

43

66

22

2030

350

238

2215

36

2050

528

173(33%)

148(28%)

Nuclear

Peaking Hydro+PS Coal

Gas (CCGT)Solar PV Wind

CSPSources: DoE Draft IRP 2016; CSIR analysis

As per Draft IRP 2016

More stringentcarbon limits

37

Draft IRP 2016 Carbon Budget case: 40% nuclear energy share by 2050

Draft IRP 2016 Base Case Draft IRP 2016 Carbon Budget

400

250

200

150

100

50

550

500

450

0

350

300

Total electricity produced in TWh/yr

15

2050

528

22 148(28%)

33(6%)

47(9%)

93(18%)

28(5%)

2040

434

223

35

33

4336

22

2030

350

238

15

173(33%)

13

2016

243

202

15

66

Coal

Nuclear

Hydro+PS

Gas (CCGT)

Peaking

Wind

CSP

Solar PV

0

550

450

500

400

350

300

250

200

150

100

50

54

25

63

23 74(14%)

243

202

1515

2050

Total electricity produced in TWh/yr

528

78(15%)

185(35%)

32(6%)

110(21%)

44(8%)

2040

435

103

121

26

2016

33

103

39

2030

350

170

As per Draft IRP 2016

More stringentcarbon limits

Sources: DoE Draft IRP 2016; CSIR analysis

No RE limits, reduced wind/solar PV costing, warm water demand flexibility

38

Least Cost case is largely based on wind and solar PV

Draft IRP 2016 Base Case Least CostDraft IRP 2016 Carbon Budget

300

550

500

450

400

350

150

100

50

250

200

0

Total electricity produced in TWh/yr

2050

529

60(11%)

33(6%)

55(10%)

257(49%)

109(21%)

2040

436

97

14

18

80

27

2016

250

27

1516

12(2%)

10

176

18

86

2030

351

190

15

207

As per Draft IRP 2016

More stringentcarbon limits

No RE limits, reduced wind/solar PV costing, warm water demand flexibility

Sources: DoE Draft IRP 2016; CSIR analysis

400

550

500

450

350

300

250

200

150

100

50

0

33(6%)

47(9%)

93(18%)

28(5%)

350

434

223

35

33

43

2040

66

22

2030

238

1522

3613

2016

243

202 173(33%)

1515

2050

528

148(28%)

Total electricity produced in TWh/yr

Coal

Nuclear

Hydro+PS

Gas (CCGT)

Peaking

Wind

CSP

Solar PV

500

550

350

450

400

300

250

200

150

100

50

0

Total electricity produced in TWh/yr

2050

528

78(15%)

185(35%)

32(6%)

74(14%)

110(21%)

44(8%)

2040

435

103

121

26

33

103

39

2030

350

170

54

25

63

23

2016

243

202

1515

39

Least Cost means no new coal and no new nuclear until 2050, instead 85 GW of wind and 74 GW of solar PV plus flexible capacities

Draft IRP 2016 Base Case Least CostDraft IRP 2016 Carbon Budget

150

0

300

250

200

100

50

Total installed net capacity in GW

2050

135

25

208

2213

30

16

2040

111

335 8

1712

2112

2030

85

39

2 68

117

2016

51

37

5 3

Coal

Nuclear

Hydro+PS

Gas (CCGT)

Peaking

Wind

CSP

Solar PV

0

300

250

200

150

100

50

10268

33

10

36

25

2040

129

1917

819

8

34

22

2030

98

34

7 8

Total installed net capacity in GW

2013

2016

51 105 3

2050

149

37

100

50

250

0

200

150

37

4 350

2050

234

108

19

37

85

74

2040

173

17 2510

27

58

Total installed net capacity in GW

2030

98

33

2

52

13

25

15

2016

5

As per Draft IRP 2016

More stringentcarbon limits

Plus 3 GW demand response from residential

warm water provision

Note: REDZ = Renewable Energy Development ZonesCurrent REDZ cover 7% of South Africa‘s land massSources: DoE Draft IRP 2016; CSIR analysis

No RE limits, reduced wind/solar PV costing, warm water demand flexibility

40

Conservative renewables and battery costing:Least Cost is R60-75 billion/yr cheaper than Draft IRP 2016 by 2050

IRP 2016 Base Case

688 627700

5%

18%

1%0%9%

6%28%

19%

14%

0%

Solar PV

CSP

Wind

Other storage

Biomass/-gas

Peaking

Gas

Hydro + PS

Nuclear (new)

Nuclear

Coal (new)

Coal

IRP 2016 Carbon Budget Least Cost

8%

21%

0%0%

16%

6%

35%

13%

0%

21%

49%

1% 2%

10%

6%11%

18

99 86

41

187

15

Energy Mix

in 2050

Costin 2050

Environ-mentin 2050

Jobs2

in 2050

Total system cost1 (R-billion/yr)

Average tariff (R/kWh) 1.34

CO2 emissions (Mt/yr)

Water usage (billion-litres/yr)

Direct & supplier(‘000)

1.32 1.20

310-325

Demand: 522 TWh

As per Draft IRP 2016

2050

235-253252-295

1 Only power generation (Gx) is optimised while cost of transmission (Tx), distribution (Dx) and customer services is assumed as ≈0.30 R/kWh (today‘s average cost for these items) 2 Lower value based on McKinsey study (appendix of IEP), higher value based on CSIR assumption with more jobs in the coal industry; Sources: Eskom on Tx, Dx cost; CSIR analysis; flaticon.com

Because of lack of data, zero jobs for

biomass/-gas assumed (affects Decarbonised)

10% cheaper

Cleaner

10-20%more jobs

41

Operational Aspects

42

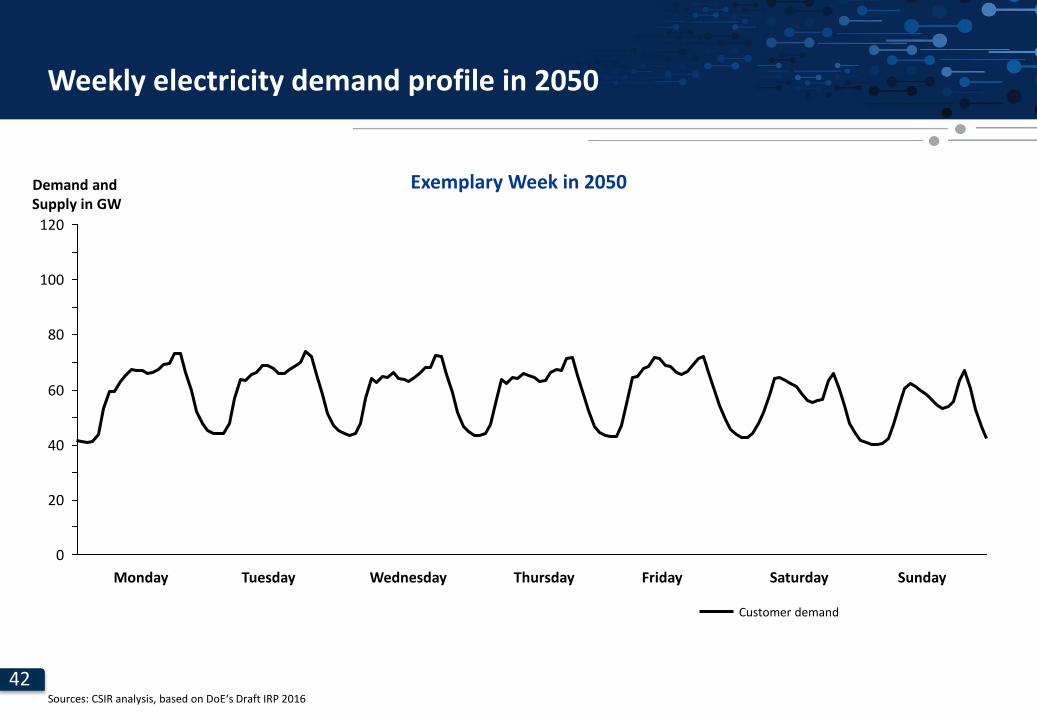

Demand and Supply in GW

120

0

20

80

40

60

100

Weekly electricity demand profile in 2050

Monday Tuesday Wednesday Thursday Friday Saturday Sunday

Sources: CSIR analysis, based on DoE‘s Draft IRP 2016

Customer demand

Exemplary Week in 2050

43

Demand and Supply in GW

120

0

20

80

40

60

100

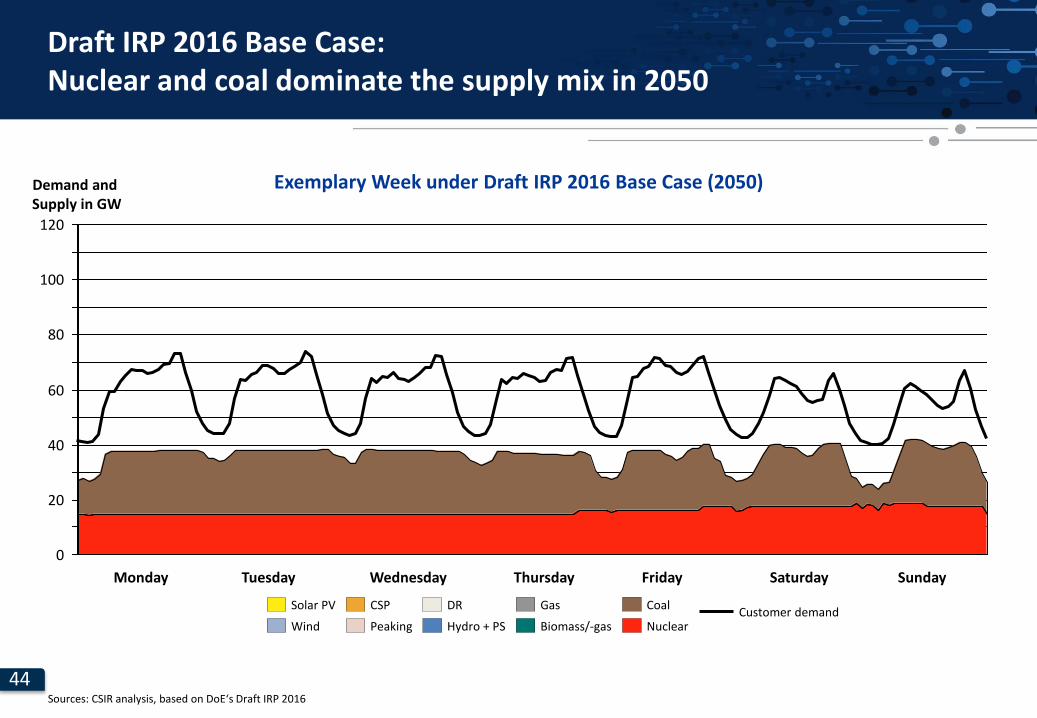

Draft IRP 2016 Base Case: Nuclear and coal dominate the supply mix in 2050

Monday Tuesday Wednesday Thursday Friday Saturday Sunday

Sources: CSIR analysis, based on DoE‘s Draft IRP 2016

Customer demand

Exemplary Week under Draft IRP 2016 Base Case (2050)

Coal

Hydro + PS Biomass/-gas

GasDRCSP

Wind

Solar PV

Peaking Nuclear

44

Demand and Supply in GW

120

0

20

80

40

60

100

Draft IRP 2016 Base Case: Nuclear and coal dominate the supply mix in 2050

Monday Tuesday Wednesday Thursday Friday Saturday Sunday

Sources: CSIR analysis, based on DoE‘s Draft IRP 2016

Customer demand

Exemplary Week under Draft IRP 2016 Base Case (2050)

Coal

Hydro + PS Biomass/-gas

GasDRCSP

Wind

Solar PV

Peaking Nuclear

45

Demand and Supply in GW

120

0

20

80

40

60

100

Draft IRP 2016 Base Case: Nuclear and coal dominate the supply mix in 2050

Monday Tuesday Wednesday Thursday Friday Saturday Sunday

Sources: CSIR analysis, based on DoE‘s Draft IRP 2016

Customer demand

Exemplary Week under Draft IRP 2016 Base Case (2050)

Coal

Hydro + PS Biomass/-gas

GasDRCSP

Wind

Solar PV

Peaking Nuclear

46

Demand and Supply in GW

120

110

100

90

80

70

60

50

40

30

20

10

0

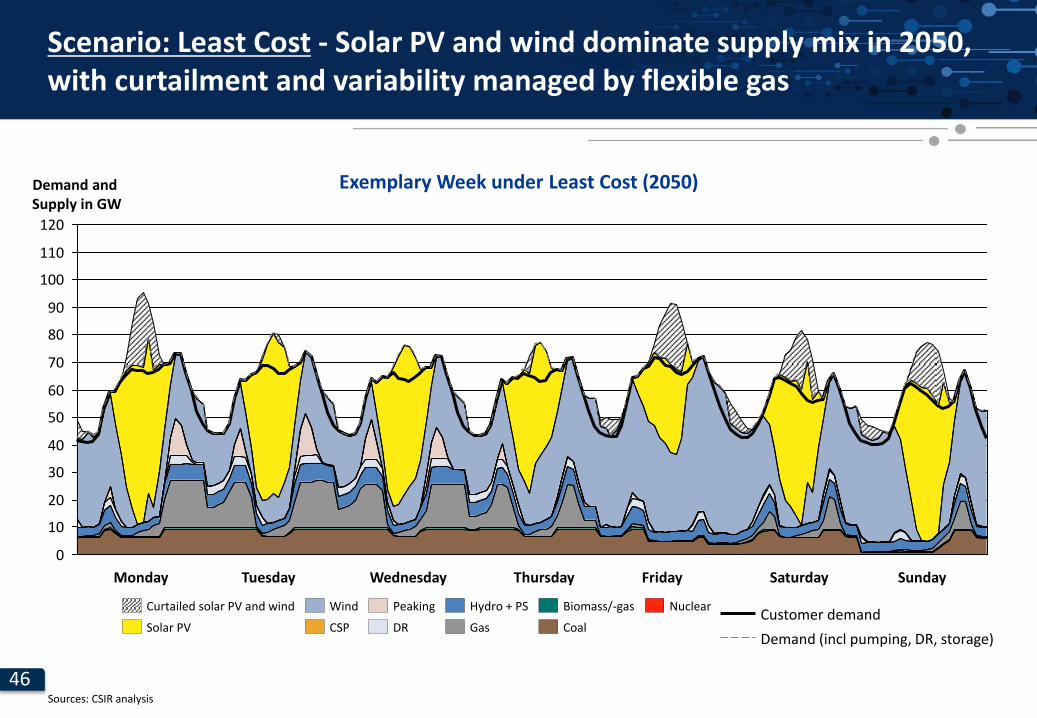

Scenario: Least Cost - Solar PV and wind dominate supply mix in 2050, with curtailment and variability managed by flexible gas

Monday Tuesday Wednesday Thursday Friday Saturday Sunday

Sources: CSIR analysis

Demand (incl pumping, DR, storage)

Customer demand

Exemplary Week under Least Cost (2050)

CoalGas

NuclearHydro + PS Biomass/-gas

DR

Peaking

CSP

Wind

Solar PV

Curtailed solar PV and wind

47

IRP PLEXOS model only optimises for cost of power generation (Gx) –two additional key aspects considered: system stability and grid cost

System Stability (inertia): worst case below 1% of Gx cost

• Connecting nuclear/coal via HVDC and/or solar PV/wind to the grid reduces the “system inertia”

• This reduces the inherent stabilising effect of synchronous inertia during contingency events

• Technical solutions to operate low-inertia system exist

• In this study the “worst case” was costed

‒ State-of-the-art technology (very high costs assumed, no further tech/cost advancements)

‒ Assumption: No further increase in engineering of how to deal with low-inertia systems by 2050

• In all scenarios, the worst-case-cost are well below 1% of the total cost of power generation (Gx) by 2050, cost differences between scenarios are much lower than 1%

Transmission grid cost: Gx Least Cost also cheapest for Tx

• High-level cost estimate for shallow and deep grid connection cost for all scenarios was developed

• Least Cost (Gx) case is additionally R20-30 billion/yrcheaper compared to Draft IRP 2016 Base Case and Carbon Budget case on transmission grid side

48

Next Steps and Summary

49

What has not been considered yet that makes Least Cost even cheaper?

Further cost reductions in solar PV, wind and battery technologies

• Solar PV cost were assumed to only decrease 20% by 2050

• Wind and battery cost were assumed to stay constant until 2050

• CSP cost were assumed to decrease to only 1.2 R/kWh until 2030 (for mid-merit operations)

With realistic cost reductions assumed, Least Cost is 25-30% cheaper than the IRP Base Case

Increasing penetration of Electric Vehicles (EV)

• No EV uptake assumed at all

With 5 million EVs by 2050, a large source of flexible demand is introduced into the system

Demand side flexibilisation only marginally considered

• Only source of flexibility considered: domestic electric warm water provision

With all heat/cool & pumping load made flexible, large source of flexible demand can be introduced

Transmission grid expansion for distributed power generators less costly

• Transmission grid costs assumed to be equal for all scenarios

Preliminary costing: transmission for Least Cost additionally R20-30 billion per year cheaper

50

Summary: A mix of solar PV, wind and flexible power generators is least cost

It is cost-optimal to aim for >70% renewable energy share by 2050

• Solar PV, wind and flexible power generators (e.g. gas, CSP, hydro, biogas, demand response) are the cheapest new-build mix for the South African power system

• There is no technical limitation to solar PV and wind penetration over the planning horizon until 2050

“Clean” and “least-cost” is not a trade-off anymore: South Africa can de-carbonise its electricity sector at negative carbon-avoidance cost

• The “Least Cost” mix is >R70 billion per year cheaper by 2050 than the current Draft IRP 2016 Base Case

• Additionally, Least Cost mix reduces CO2 emissions by 55% (-100 Mt/yr) over Draft IRP 2016 Base Case

Note: Wind and solar PV would have to be 50% more expensive than assumed before the IRP Base Case and the Least Cost case break evenSources: CSIR analysis

51

Outlook for Energy Planning beyond Electricity

52

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

GW

Monday Saturday SundayWednesdayTuesday FridayThursday

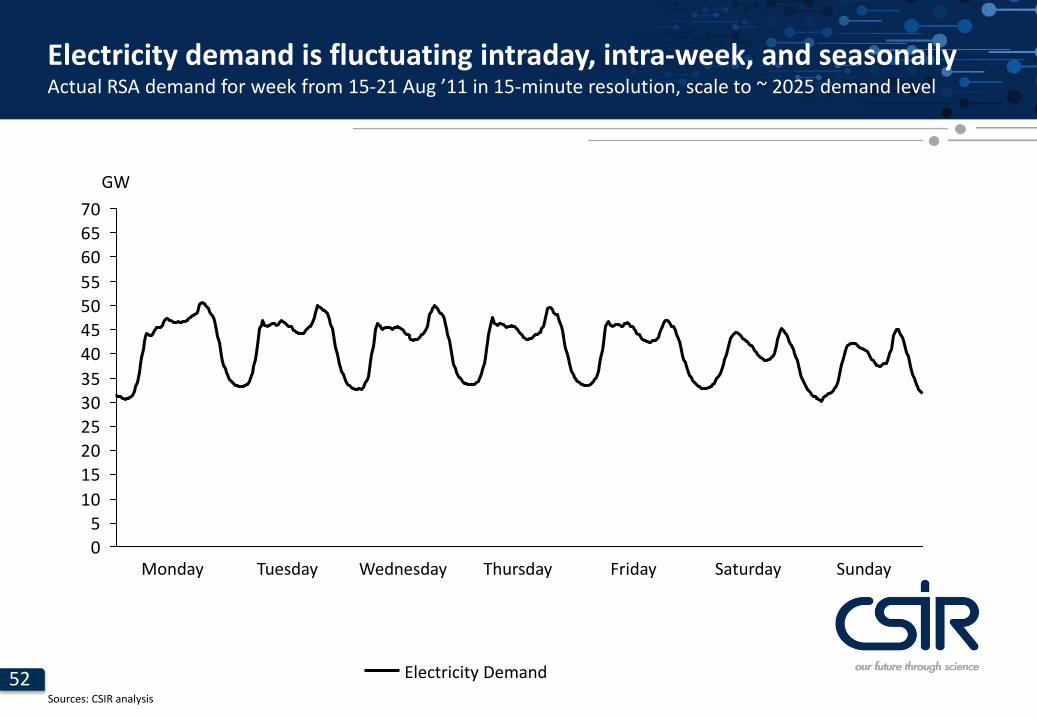

Electricity demand is fluctuating intraday, intra-week, and seasonallyActual RSA demand for week from 15-21 Aug ’11 in 15-minute resolution, scale to ~ 2025 demand level

Sources: CSIR analysis

Electricity Demand

53

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

Day of the week

SaturdayWednesday Thursday FridayMonday Tuesday Sunday

GW

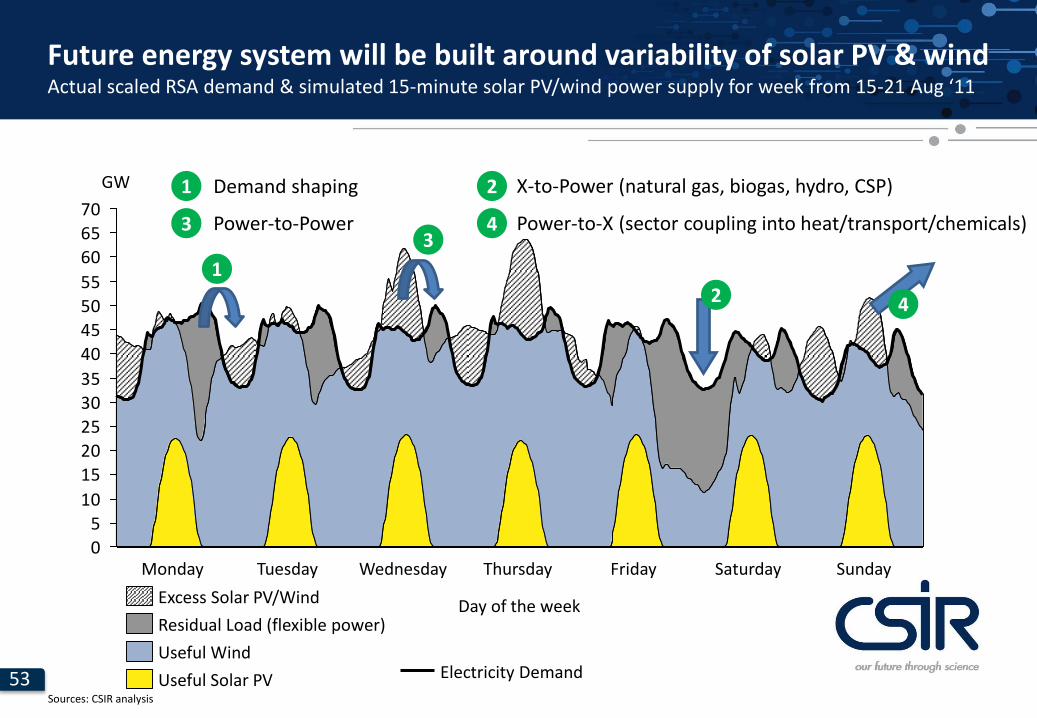

Future energy system will be built around variability of solar PV & windActual scaled RSA demand & simulated 15-minute solar PV/wind power supply for week from 15-21 Aug ‘11

Excess Solar PV/Wind

Residual Load (flexible power)

Useful Wind

Useful Solar PVSources: CSIR analysis

3

1

42

1

3

2

4

Demand shaping

Power-to-Power

X-to-Power (natural gas, biogas, hydro, CSP)

Power-to-X (sector coupling into heat/transport/chemicals)

Electricity Demand

54

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

GW

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

GW

SundaySaturdayFridayThursdayWednesdayTuesdayMonday

Nuclear can add carbon-free electricity: cost, not a technical questionActual scaled RSA demand & simulated 15-minute solar PV/wind power supply for week from 15-21 Aug ‘11

Useful Wind

Residual Load (flexible power)

Excess Solar PV/Wind Nuclear

Useful Solar PVSources: CSIR analysis

Electricity Demand

3

1

42

1

3

2

4

Demand shaping

Power-to-Power

X-to-Power (natural gas, biogas, hydro, CSP)

Power-to-X (sector coupling into heat/transport/chemicals)

55

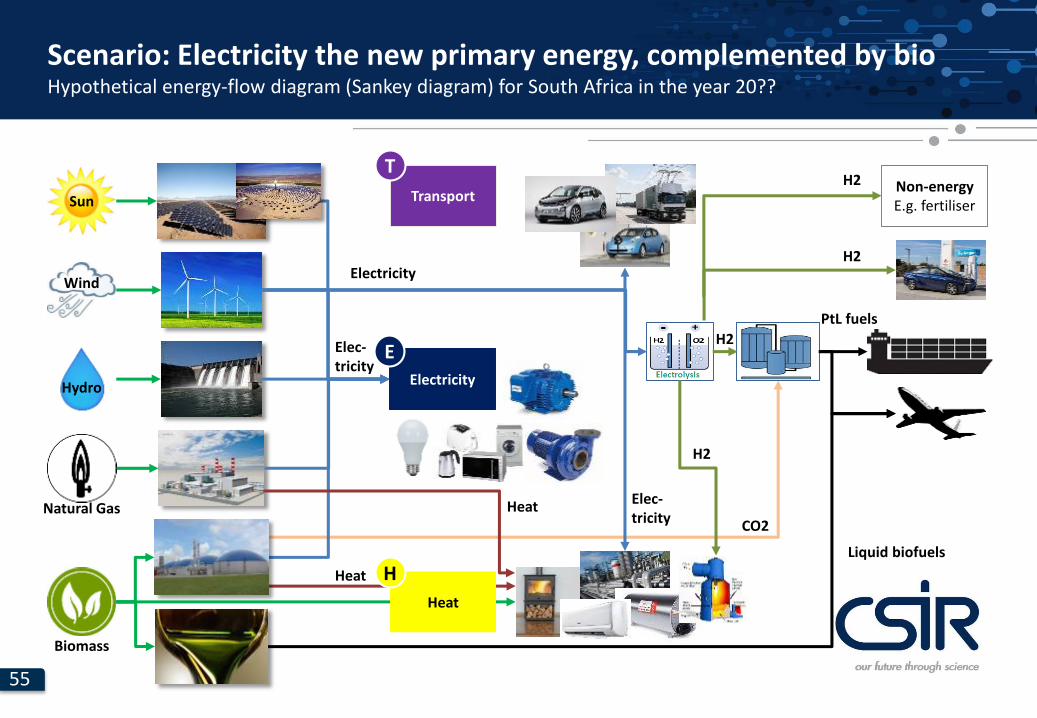

Scenario: Electricity the new primary energy, complemented by bioHypothetical energy-flow diagram (Sankey diagram) for South Africa in the year 20??

Transport

T

CO2

H2

PtL fuels

H2

Liquid biofuels

Electricity

E

Heat

H

Sun

Wind

Hydro

Biomass

Natural Gas

Heat

Heat

Electricity

Elec-tricity

Non-energyE.g. fertiliser

H2

H2

Elec-tricity

56

Thank you

Re a leboga

SiyathokozaEnkosi

Siyabonga

Re a leboha

Ro livhuha

Ha Khensa

Dankie

Note: „Thank you“ in all official languages of the Republic of South Africa