energy and public utility trends and issues what happens if customers “cut the wire”? 2015...

TRANSCRIPT

Energy and Public Utility Trends and Issues

What happens if customers “cut the wire”?

2015 CAMPUT Energy Regulation CourseBob Heggie, Chief Executive, Alberta Utilities Commission

Disclaimer

• The views and comments expressed in this presentation are my own and do not represent the views or positions of the Alberta Utilities Commission.

• Treatment of the issues discussed in this presentation will vary on a case-by-case basis; the outcome will be dependent on the facts of the case, applicable federal and provincial laws and previous tribunal and court decisions.

2

• Regulatory decisions must comply with applicable legislation and legal principles.

• Principles

1. Regulatory compact2. Prudence3. Used and useful (required to be used)4. Cost of capital / fair return

• Discussion – application of principles to a potential fact pattern.

3

4

What happens if customers “cut the wire”?

5

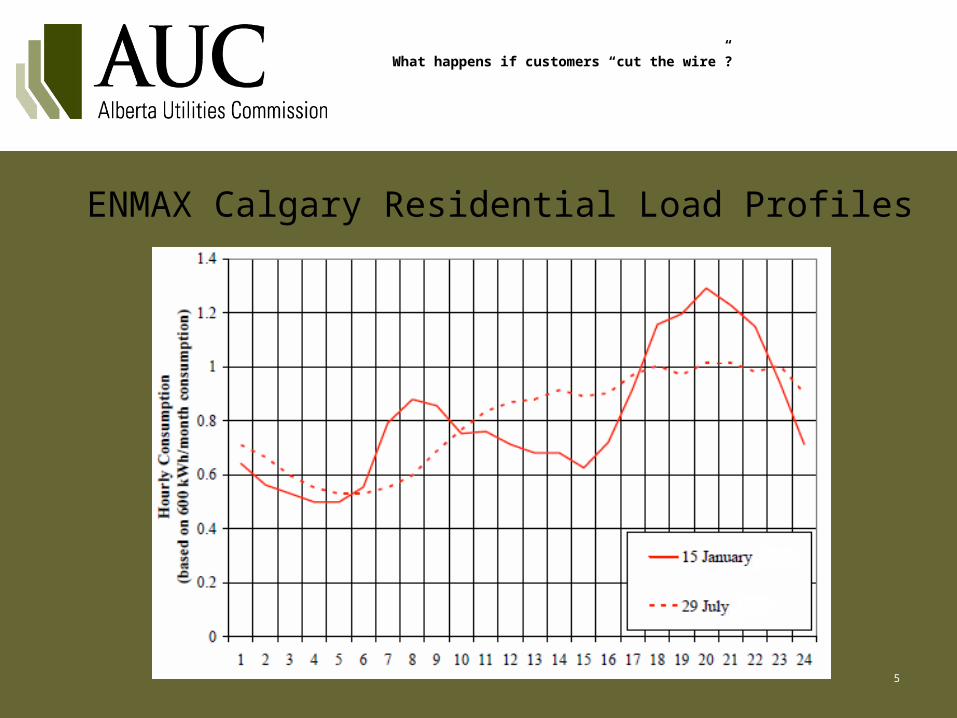

What happens if customers “cut the wire”?

ENMAX Calgary Residential Load Profiles

6

What happens if customers “cut the wire”?

7

Average delivered costs of electricity ($/month)Residential (600 kWh/month)

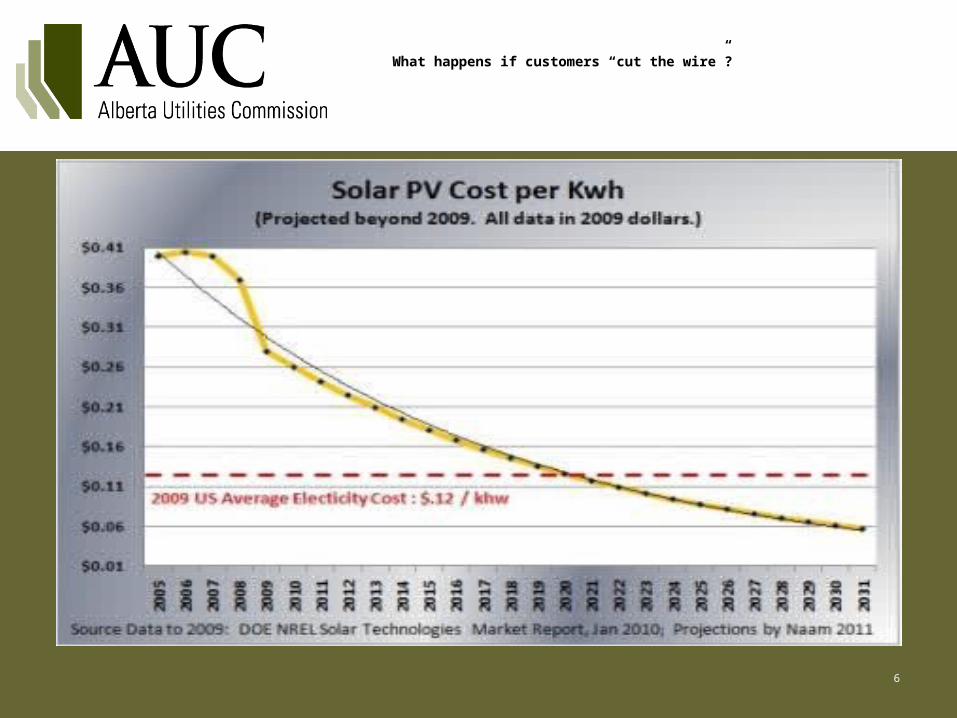

What happens if customers “cut the wire”?

Regulatory problemRegulatory problem: whether utility investors or customers should bear the risk of excess, and potentially stranded, capacity costs?

• Transmission system began operations decades ago as a natural monopoly.

• Transmission system is planned and built on an integrated basis.

• Applications to build facilities are determined based on need and the public interest.

• Prudently incurred costs are approved by the regulator in rate base, including a return on equity on a capital structure that reflects business and regulatory risk.

• Economy grows, system is built to a larger and larger territory, in anticipation of a larger load – rate base grows into the billions.

8

Regulatory problem

• Customers are responsible for paying for the transmission system through wire rates based on average cost of transmission build.

• Load disappears due to disruptive technology (distributed generation), potentially stranding costs that need to be absorbed.

• Wire company seeks a rate increase for it’s business of 30+ %, plus an increase in the return on equity and the equity component of the capital structure.

• Current environment will result in rate increases continuing.

• Applying regulatory principles – how would you argue this case?

9

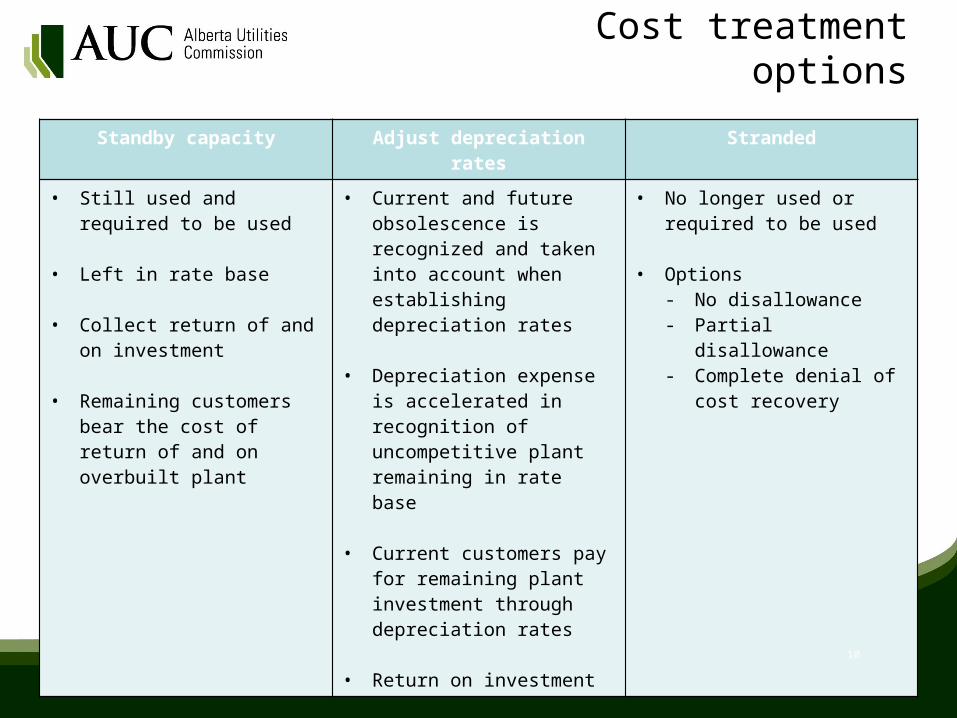

Cost treatment options

Standby capacity Adjust depreciation rates Stranded

• Still used and required to be used

• Left in rate base

• Collect return of and on investment

• Remaining customers bear the cost of return of and on overbuilt plant

• Current and future obsolescence is recognized and taken into account when establishing depreciation rates

• Depreciation expense is accelerated in recognition of uncompetitive plant remaining in rate base

• Current customers pay for remaining plant investment through depreciation rates

• Return on investment

• No longer used or required to be used

• Options- No disallowance- Partial disallowance- Complete denial of cost

recovery

- Various methods of accounting – facts will drive outcomes

10

Depreciation methodology

• Depreciation is designed to return full capital investment over the life of an asset. Mass property accounts group similar assets and estimate an expected service life for the assets based on actual experience and observed risks. Some assets may be retired early, some may remain in service longer. These differences are captured over time and trued up by amortizing the difference over the balance of the remaining assets. In this way ordinary ‘stranding’ of assets is contemplated and accounted for.

• Extraordinary ‘stranding’ occurs when assets are no longer required for utility service due to reasons not contemplated in the depreciation methodology.

11

Regulatory compact (1)

An economic and social arrangement that ensures customers access and receives service at a fair price.

“ Regulated utilities are given the exclusive right to sell their services within a specific area at rates that will provide companies with the opportunity to earn a fair return for their investors. In return for this right of exclusivity, utilities assume a duty to adequately and reliably serve all customers in their determined territories, and are required to have their rates and certain operations regulated.”

ATCO Gas & Pipelines Ltd. V. Alberta (Energy and Utilities Board), [2006] 1S.C.R. 140, 2006 SCC 4 at para. 63

12

Regulatory compact (2)

The regulatory compact balances the interests of investors and consumers.

Toronto Hydro-Electric System Limited v. Ontario Energy Board, 2010 ONCA 284 at para. 49; Great Lakes Power v. Ontario Energy Board, 2010 ONCA 399 at para. 24

BUT…

13

Regulatory compact (3)

• Regulatory compact is not absolute

• While the utility is obligated to serve all customers, due to it being granted an exclusive monopoly franchise area, there is no reciprocal obligation to buy on the part of the customers.

• Utility has no right to monopoly protection for competitive services.Ontario Energy Board Decision EB-2005-0441, p. 33

• The regulatory compact is not static, but may change over time due to evolving circumstances like the advent of competition.

14

Regulatory compact (4)

• “The expression regulatory compact is an expression the Board has not itself specifically articulated . We are not prepared to endorse the concept of the regulatory compact as a concept that compels the Board to set just and reasonable tolls in a particular manner. In our view, the concept is ill defined. TransCanada’s interpretation of the regulatory compact would have the effect of protecting the mainline from the impact of competition. Some interveners contended that the concept protects them from a pipeline’s market power. We are of the view that the differing characterizations of the regulatory compact evidences a fundamental flaw in using the concept to set just and reasonable tolls: the regulatory compact means different things to different people.”

National Energy Board decision RH-003-2011 at p. 38

15

Regulatory compact (5)Arguments

The regulatory compact means the regulator must allow the utility a reasonable opportunity to recover its costs. The opportunity to recovery of and return on investment must reflect the risks imposed by the regulatory compact on the utility. The traditional risks do not include the disruptive technology risk that a customer could leave the system entirely or only rely on the system for backup purposes after the utility had incurred a 30-40 year cost recovery investment to serve that customer.

OR

The regulatory compact is not absolute and the utility has no right to monopoly protection for competitive services. While in some circumstances remaining customers act as guarantors of recovery of costs to serve departing customers, generally the risk that customers will cease to use a utility’s services is generally assumed by the utility. This is a market risk for which the utility is compensated.

16

Prudence (1)

The prudent investment test establishes that investments are assumed to have been made based on reasonable judgment, unless the contrary is shown.

This test has been interpreted as establishing a rebuttable presumption of prudence.

This reverses the onus so that interveners are obliged to demonstrate mismanagement, inefficiency or bad faith to overcome the presumption.

See: State of Missouri ex rel. Southwestern Bell Telephone Co. v. Public Service Commission, 262 U.S. 276, 289 (1923) Brandeis J. concurring.

Re Chesapeake & Potomac Telephone Co., 57 PUR 3rd 1, 7 (D.C.P.S.C., 1864)

ATCO Gas and Pipelines Ltd. V. Alberta (Energy and Utilities Board) 2005 ABCA 122

17

Prudence (2)Arguments

The facilities were approved in the public interest when built. The regulator issued an approval to construct based on a demonstrated need. The costs arising from the investment were prudent when put into rate base and included in just and reasonable rates. Prudence determines the opportunity for cost recovery.

OR

Including prudently incurred costs in rates provides a utility the opportunity to recover these costs. Whether costs that were prudent at the time they were first incurred continue to be prudent depends on the circumstances faced by the utility. Prudency is not the only standard that determines the opportunity for cost recovery. Failure to take timely action to mitigate cost impacts resulting from market changes could be imprudent.

18

Prudence (3)Pending cases

Two pending cases at the Supreme Court of Canada deal with the application of the prudent investment test to forecast costs.

• ATCO Gas and Pipelines Ltd. and ATCO Electric Ltd. v Alberta Utilities Commission, SCC File No. 35624, on appeal from ATCO Gas and Pipelines Ltd. v Alberta (Utilities Commission), 2013 ABCA 310.

• Ontario Energy Board v Ontario Power Generation Inc., et. al., SCC File No. 35506, on appeal from Power Workers’ Union (Canadian Union of Public Employees, Local 1000) v Ontario (Energy Board), 2013 ONCA 359.

19

Used and useful (1)

Facilities that are “used” (actually operating in the course of providing service to the customer) and “useful” (necessary to provide service in an economic fashion) remain in rate base. A utility receives return of and on capital employed related to those facility investments. (In Alberta the test is used or required to be used.)

“The words “used or required to be used” are intended to identify assets that are presently used, are reasonably used, and are likely to be used in the future to provide services. Specifically, the past or historical use of assets will not permit their inclusion in rate base unless they continue to be used in the system.”

See: ATCO Gas and Pipelines Ltd. v. Alberta (Energy and Utilities Board) 2008 ABCA 200, at paras. 23 and 25

ATCO Gas and Pipelines Ltd. v. Alberta (Utilities Commission), 2009 ABCA 246, para. 56

‘Prudence’ seeks to evaluate management’s performance, while ‘used and useful’ is largely an economic concept used to reflect market conditions or the continuing need for the facility to provide utility service.

20

Used and useful (2)Arguments

Utilities are allowed a reasonable opportunity to recover their prudently incurred costs regardless of whether the asset remains used and useful in the provision of service, provided that management imprudence does not contribute to underutilization. To disallow costs that were prudently incurred would be confiscatory. The cost of underutilization goes to the consumer, not the shareholder. Prudence trumps used and useful.

OR

A utility investment that is no longer used and useful in providing service because it is technologically or economically obsolete can be excluded from rate base. A utility is not guaranteed a recovery of its costs and a reasonable return on their investment, the compact requires a utility be afforded the opportunity to earn a fair return and has never meant that under all circumstances the utility will recover a return. Technological and competitive risks do not bar a utility from competing to maintain market share, it will have to adjust its price or it will result in a partial financial write-down. As the utility continues to own the asset and the opportunity to earn on the investment was afforded to the utility, it is not confiscation of utility property.

21

Used and useful (2)Arguments

See: National Energy Board RH-003-2011 TransCanada Pipelines Mainline decision, pp. 37-41

Alberta Utilities Commission decision 2013-417 (Utility Asset Disposition) pp. 32-34

[Not absolute – where it can be shown, for example, that government or a governmental agency required certain costs to be incurred, the utility’s claim for recovery may have merit.]

22

Fair return (1)

Utilities are funded by equity and debt.

Entitled to the opportunity to recover their cost of capital – a return on the equity and debt invested in the facilities providing service.

Overall the return must meet the ‘fair return standard’.

Three elements of fair return standard applied to ROE:

1. Comparable investment – return commensurate with returns available from investments of similar risk.

2. Financial integrity – maintains financial integrity of the utility.

3. Capital attraction – attract capital or reasonable terms and conditions.

23

Fair return (2)

Return on equity is a cost to be objectively determined.

Return on debt is actual (prudent) incurred cost of debt.

The return on equity must reflect the business risks facing the utility.

Whether the investor or customer should bear the risk of extraordinary stranding of assets depends on whether the investor has been compensated for bearing the risk that the utility service could be displaced by a generation technological advance – a competitor to wires.

24

Fair return (3)Arguments

Utilities are compensated

Rates of return reflect the potential that market conditions may change resulting in lost sales for a utility. This includes the risk that technology advancements may result in competitive pressures that will result in customers having viable alternate service offerings. Utilities knew or should have known that these risks would increase likelihood of lost revenues including the risk that facilities would no longer be required for service and did or should have sought adjustments in depreciation rates and rates of return.

Utilities are not compensated

Utilities have been historically compensated for traditional market risks of customers fuel switching or self-generating, not for extraordinary risks caused by disruptive technology which could not have been foreseen. This new risk and its sudden occurrence changes a utility’s business risk in a fundamental way for which the utility has not been compensated.

25

Thank You

26